Anheuser-Busch InBev: The Empire of Beer

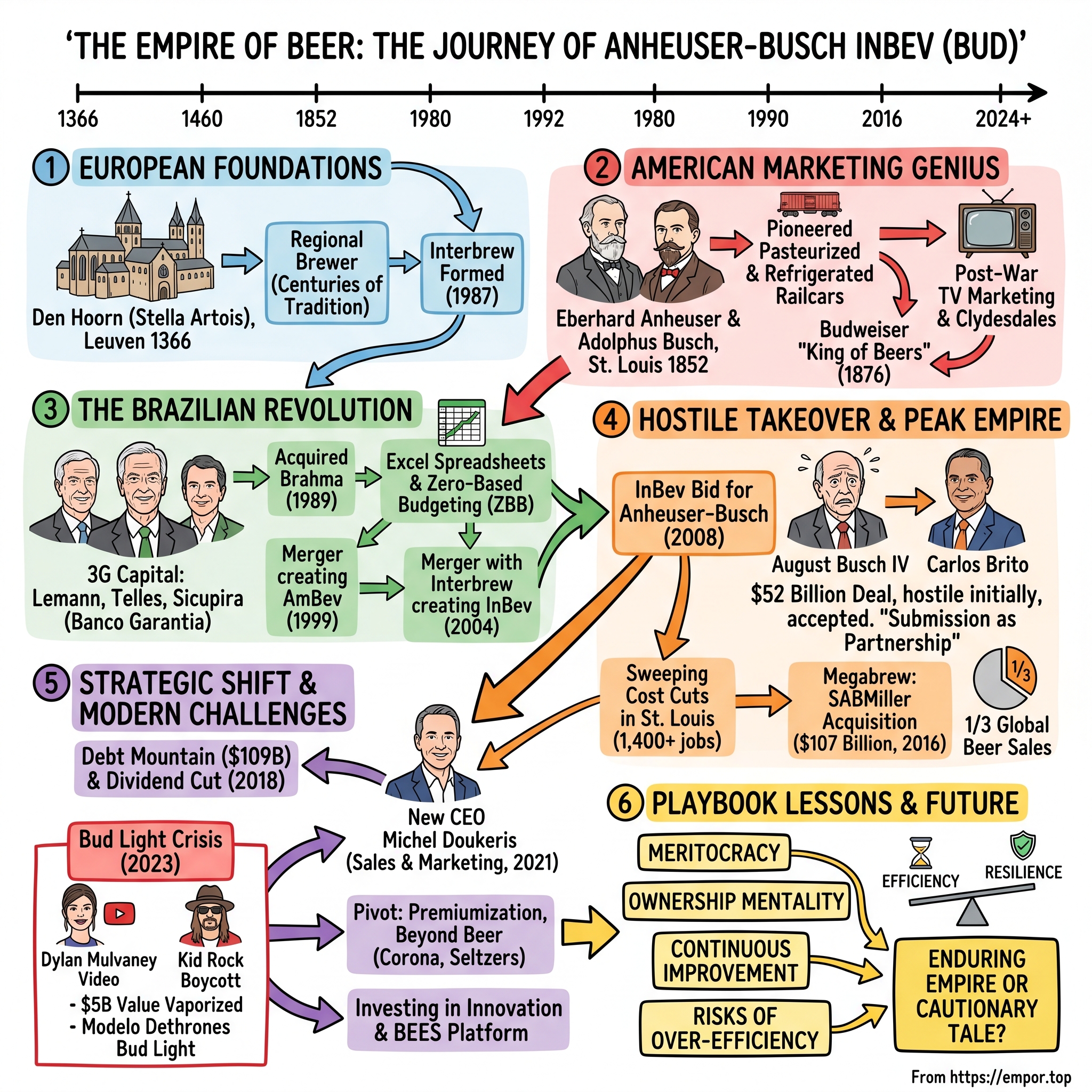

I. Introduction & Episode Roadmap

Picture this: Every third beer consumed on planet Earth passes through the corporate veins of a single company. From the neon-lit bars of Tokyo to the sun-drenched beaches of Rio, from Munich's ancient beer halls to American tailgate parties, one empire controls it all. Anheuser-Busch InBev—a $116 billion colossus that owns over 500 beer brands and commands nearly one-third of global beer sales.

How did we get here? How did a small brewery founded in 1366 in a Belgian university town transform into the undisputed emperor of beer? And perhaps more intriguingly—what happens when an empire built on aggressive acquisitions and ruthless efficiency collides with the cultural zeitgeist of modern America?

This is a story that spans continents and centuries, but at its heart, it's about three distinct business cultures colliding: European brewing tradition, American marketing genius, and Brazilian financial engineering. It's about how three investment bankers from Brazil revolutionized a 600-year-old industry using Excel spreadsheets and zero-based budgeting. It's about hostile takeovers that shook entire nations, cost-cutting so extreme that executives flew coach and shared desks, and a single Instagram post that vaporized $5 billion in market value.

The narrative arc follows a classic empire pattern: humble origins, aggressive expansion, peak dominance, and then the inevitable challenges of maintaining supremacy. We'll trace how medieval Belgian monks' brewing experiments evolved into Interbrew, how German immigrants built an American beer dynasty with Budweiser, and how Brazilian dealmakers orchestrated the most audacious series of mergers in consumer goods history.

But this isn't just a tale of financial engineering. It's about what happens when you apply private equity playbooks to beloved consumer brands, when you try to optimize the unoptimizable—human culture and tradition. The Bud Light crisis of 2023 wasn't just a marketing mishap; it was the culmination of decades of tension between efficiency and identity, between global scale and local relevance.

As we journey through this saga, we'll uncover the management philosophy that turned beer into a spreadsheet exercise, the hostile takeover that made grown men in St. Louis cry, and the moment when the world's most powerful beer company discovered that all the market share in the world can't protect you from a culture war.

The themes that emerge are timeless: Can you build lasting value through serial acquisitions? What's the true cost of operational excellence? And in an age of polarization, how do you manage brands that must appeal to everyone while offending no one?

Let's begin where all great beer stories should—in a medieval abbey where monks discovered that brewing beer was safer than drinking water.

II. The European Foundations: Building Blocks of an Empire (1366–1990s)

The year is 1366. The Black Death has just ravaged Europe, claiming nearly half the continent's population. In the small Flemish town of Leuven, thirty miles east of Brussels, monks at a local abbey make a discovery that will outlast empires: they can brew ale that's safer to drink than the contaminated water that's killing their neighbors. They call their brewery Den Hoorn—The Horn—after the symbol they hang outside to attract customers.

Six centuries later, that modest brewery would become Stella Artois, the crown jewel in what would eventually become the world's largest beer empire. But the path from medieval monastery to global monopoly was anything but straight.

The real acceleration began in 1717 when Sebastian Artois, a master brewer, purchased Den Hoorn and renamed it after himself. The Artois brewery would remain a regional player for another two centuries, perfecting its craft while Europe convulsed through wars, revolutions, and industrial transformation. It wasn't until 1926 that Artois created Stella—meaning "star" in Latin—as a Christmas beer. The name stuck, the seasonal limitation didn't, and Stella Artois was born.

Meanwhile, across the Atlantic, a different beer story was unfolding—one that would eventually collide with European brewing tradition in spectacular fashion. In 1852, German immigrant Eberhard Anheuser purchased a failing St. Louis brewery. His daughter Lilly had fallen in love with Adolphus Busch, another German immigrant with grand ambitions and a gift for salesmanship. Their marriage in 1861 wasn't just a romantic union—it was a business merger that would reshape American capitalism.

Adolphus Busch was no ordinary son-in-law. While other brewers focused on production, Busch obsessed over distribution and marketing. He pioneered the use of refrigerated railcars, allowing beer to travel across America without spoiling. He embraced pasteurization when other brewers called it heresy. Most audaciously, in 1876, he introduced a light, crisp pilsner that was unlike anything Americans had tasted—he called it Budweiser, after the Czech town of České Budějovice, known in German as Budweis.

The innovation wasn't just in the brewing; it was in the positioning. Busch marketed Budweiser as "The King of Beers"—not just another regional brew, but American royalty in a bottle. By 1901, Anheuser-Busch was producing over one million barrels annually. When Prohibition arrived in 1920, the company pivoted to producing everything from ice cream to truck bodies, keeping its workforce employed and its facilities maintained. When Prohibition ended in 1933, Anheuser-Busch was ready to reclaim its throne.

The post-war boom transformed American drinking culture. Returning GIs wanted light, refreshing beers, not the heavy ales of their ancestors. Television arrived, and with it, the power of mass marketing. August Busch Jr., great-grandson of Adolphus, understood this new world perfectly. Under his leadership, Anheuser-Busch became the first brewery to sponsor television sports broadcasts. The Budweiser Clydesdales became American icons. By 1957, Budweiser surpassed Schlitz to become America's best-selling beer.

Back in Belgium, consolidation was also underway, but with European sophistication rather than American swagger. In 1987, two of Belgium's largest breweries—Artois and Piedboeuf—merged to form Interbrew. This wasn't a hostile takeover or a private equity play; it was a strategic combination of complementary strengths. Artois brought Stella and international recognition; Piedboeuf brought Jupiler, Belgium's best-selling beer, and deep local distribution.

The newly formed Interbrew had ambitions beyond Belgium's borders. Throughout the 1990s, it acquired breweries across Europe—Labatt in Canada, Whitbread in the UK, Bass in England. Each acquisition was surgical, preserving local brands while leveraging combined distribution. The European approach was patient, methodical—building an empire one country at a time.

By the late 1990s, two beer empires had emerged on opposite sides of the Atlantic. Anheuser-Busch ruled America with 50% market share, built on marketing genius and the singular dominance of Budweiser. Interbrew controlled swaths of Europe through careful acquisition and brand portfolio management. Neither could have imagined that their fates would soon be determined by three Brazilian investment bankers who had never brewed a drop of beer in their lives.

The stage was set for a revolution—not in brewing techniques or marketing strategies, but in something far more fundamental: how beer companies create value. The old model of patient brand-building and territorial respect was about to collide with a new philosophy that treated breweries like any other cash-generating asset. The Europeans and Americans had built their empires on tradition and marketing. The Brazilians would build theirs on spreadsheets and ruthless efficiency.

III. The Brazilian Revolution: 3G Capital & The AmBev Story (1989–2004)

The Rio de Janeiro stock exchange floor hummed with activity on a sweltering summer day in 1989. Three men in their thirties—a former tennis champion, a underwater fishing enthusiast, and a head trader—huddled over financial statements of Brahma, Brazil's second-largest brewery. The numbers were mediocre, the brand was stagnant, but Jorge Paulo Lemann, Carlos Alberto "Beto" Sicupira, and Marcel Telles saw something others didn't: an entire industry waiting to be revolutionized by spreadsheets.

These three partners acquired a 20% economic and 51% voting stake in Brahma for $52 million, a move that would set in motion the most aggressive consolidation strategy in consumer goods history. But this wasn't their first rodeo. In 1971, Lemann, Sicupira and Telles founded the Brazilian investment banking firm Banco Garantia, which they built into Brazil's Goldman Sachs before selling it to Credit Suisse in 1998 for $675 million—a 50-fold return on their initial investment.

The Garantia culture was unique: meritocracy over seniority, transparency over hierarchy, ownership mentality over employee mindset. They recruited the hungriest graduates from Brazil's best universities, worked them mercilessly, and promoted the survivors rapidly. Those who couldn't handle the pressure were shown the door. Those who thrived became millionaires before thirty. This wasn't just investment banking—it was boot camp for capitalism.

When they took control of Brahma, the beer industry looked nothing like investment banking. It was sleepy, traditional, relationship-driven. Marketing budgets were set by adding 5% to last year's number. Executives had corner offices and company cars. Salespeople took three-hour lunches with distributors. The three partners saw inefficiency everywhere—and where others saw tradition, they saw opportunity.

After finishing business school, Brito went straight to work with 3G partner Marcel Telles at Brahma. Carlos Brito wasn't just any Stanford MBA. He first met Lemann in 1987 when he was working for Shell Oil and had been accepted to Stanford Business School. Lemann and his partners at Banco Garantia ran a scholarship program, and they backed Brito. This investment in talent would prove more valuable than any brewery acquisition.

At Brahma, Brito became the perfect vessel for the 3G philosophy. He introduced something revolutionary to the beer industry: zero-based budgeting. Instead of using the previous budget and adding a percentage increase, financial projections were built from the ground up. Every expense had to be justified anew. Every cost scrutinized. Every inefficiency eliminated.

The transformation was brutal and brilliant. Within five years, Brahma's market share in Brazil jumped from 35% to 45%. Operating margins doubled. In 1999, they orchestrated a merger with Antarctica, their largest rival, creating AmBev—instantly South America's largest beverage company. The combined entity controlled 70% of Brazil's beer market, a dominance that would have made American antitrust lawyers faint.

But the AmBev story wasn't just about cutting costs—it was about building a talent machine. Most of the people at the top of InBev came from the trainee system developed at AmBev. The company recruited 20-somethings straight from university, put them through grueling 18-month training programs, and gave the survivors real responsibility fast. A 27-year-old might run a brewery. A 30-year-old might manage a country. Performance was measured obsessively. Those who delivered were promoted. Those who didn't were gone.

In 2004, the partners merged Brazilian beer maker AmBev with Belgium's Interbrew, establishing the world's largest brewer InBev. This wasn't a merger of equals—it was a reverse takeover disguised as a combination. The Brazilians got 57% of the company and, more importantly, operational control. Soon after AmBev's tie-up with Interbrew, Brito was named as CEO of InBev at 45 years of age.

The European executives at Interbrew experienced culture shock. Gone were the leisurely Belgian lunches. In came hot-desking, where even senior executives shared workspace. Business class flights? Only for flights over eight hours. Five-star hotels? Three stars maximum. "Treat the company's money as your own," AB-InBev employees were constantly told.

The 3G Capital model had three core principles that seemed simple but were revolutionary in execution. First, meritocracy: The 3G way stood for extreme transparency, merit-based pay, promoting young talent quickly, and a spirit of competitiveness. Second, ownership mentality: executives received significant equity stakes, aligning their interests with shareholders. Third, continuous improvement: "We're constantly trying to train new people and we're constantly telling everybody that the newer people should be better than the old people," said Lemann.

Founded in 2004, 3G Capital evolved from the Brazilian investment office of Jorge Paulo Lemann, Carlos Alberto Sicupira, and Marcel Herrmann Telles. While technically a new entity, it was really the formalization of a partnership that had been building empires for three decades. The firm didn't just invest in companies—it transformed them using the playbook perfected at AmBev.

By 2004, the stage was set for their biggest play yet. InBev, armed with Brazilian efficiency and European brewing heritage, turned its sights on the crown jewel of global beer: Anheuser-Busch. The St. Louis brewery thought it was untouchable—American as apple pie, protected by political connections and cultural significance. They were about to learn that in the world of global capital, sentiment was just another inefficiency to be optimized away.

IV. The Hostile Takeover: InBev Conquers America (2008)

June 11, 2008. The boardroom at One Busch Place in St. Louis resembled a war room more than a corporate headquarters. August Busch IV, the 43-year-old scion who had waited his entire life to run the family business, stared at the fax that had just arrived from Brussels. InBev said on June 11 it wanted to buy Anheuser-Busch. The unsolicited offer: $65 per share, valuing America's most iconic brewery at $46 billion.

"They want to steal our company," Busch IV said to his assembled executives, his voice cracking with emotion. For 156 years, five generations of Busches had built Anheuser-Busch into an American institution. The Budweiser Clydesdales. The Super Bowl commercials. The baseball stadium naming rights. Few products are associated with America as much as Budweiser, which its owner calls the King of Beers. From college buildings to theme parks to offices to the stadium where the Cardinals play baseball, the Busch name is virtually everywhere in the Gateway City.

But InBev CEO Carlos Brito, sitting 4,000 miles away in Leuven, Belgium, saw none of that sentimentality. He saw inefficiency. He saw margins that could be expanded. He saw a bloated American company that "had never been a company to lay people off. I mean we needed to be doing that for a long time, but we just never had", as one HR executive would later admit.

InBev chief executive Carlos Brito, a tough 48-year-old Brazilian known for cutting costs, is to lead the new company. His playbook was simple: buy, cut, integrate, repeat. He had done it with Interbrew. He would do it with Anheuser-Busch. The fact that this was America's beer, that St. Louis would mourn, that thousands would lose their jobs—these were externalities, not obstacles.

The initial $65 offer was rejected as "financially inadequate and not in the best interests of Anheuser-Busch shareholders." InBev responded by threatening to seek the removal of all Anheuser's board members. Anheuser counterattacked, calling InBev's bid an "illegal scheme" because the company failed to mention that it owned a brewery in Cuba. The gloves were off.

The bid for Anheuser-Busch had stirred fierce opposition in the 150-year-old company's home state of Missouri where Governor Matt Blunt has called the prospect of a foreign takeover "deeply troubling." Politicians grandstanded. Unions protested. Local newspapers ran editorials defending their hometown champion. But many U.S. shareholders in Anheuser-Busch, including billionaire investor Warren Buffett, favored the deal.

The turning point came in early July. InBev raised its offer to $70 per share—a $52 billion takeover. At that price, even the Busch family's resolve began to crack. Board members who had initially resisted started asking uncomfortable questions about fiduciary duty. Investment bankers whispered about shareholder lawsuits if they rejected such a premium.

After having resisted offers from InBev for a month, the Anheuser-Busch board finally agreed on July 13 to accept a sweetened bid. Under the terms of the merger agreement, all shares of Anheuser-Busch will be acquired for US$70 per share in cash, for an aggregate of $52 billion. While capping Anheuser's roughly 150 years of independence as a premier American brewer, the deal creates not only the world's largest beer company but one of the top five consumer goods groups in the world.

The promises came fast and furious, designed to mollify opposition. Brito has sought to win over opponents to the merger by promising to make St. Louis the sprawling company's North American headquarters as well as by vowing not to close any U.S. breweries and lifting the international profile of Budweiser. "What consumers care is that their Bud will always be their Bud, and that's what we're committed to, not only the product, the quality, the beer ... but also the heritage, the breweries, who brews the beers, and everything that's connected to the breweries," InBev CEO Carlos Brito said in a media conference call.

During a Monday conference call with reporters, Anheuser chief executive August Busch IV stressed that the deal was "friendly," despite the fact that it came after a rough month of lawsuits and contentious press releases between the companies. The word "friendly" stuck in his throat. Nothing about this was friendly. It was submission dressed up as partnership.

The deal closed on November 18, 2008. Effective November 18, InBev has changed its name to Anheuser-Busch InBev to reflect the heritage and traditions of Anheuser-Busch. The name change was cosmetic. The real changes came three weeks later.

December 8, 2008. It didn't take long. Three weeks to the day after InBev, of Belgium, took over Anheuser-Busch, of St. Louis, the combined company announced sweeping cuts in its work force. A-B InBev is slashing 1,400 salaried jobs in the U.S., with an additional 415 contractor positions eliminated as well. Newly formed brewer says it will cut 1,400 U.S. jobs -- mostly from its North American headquarters in St. Louis. The Belgian brewer said 75% of the positions being cut are at corporate headquarters in St. Louis.

There were 21,000 AB employees in 2008; approximately 5,000 of them in St. Louis according to a spokesman for AB InBev corporate communications. This year, the company's official count in St. Louis is somewhat vague: "three to four thousand." The math was brutal: a 40% reduction in St. Louis headcount in less than a decade.

The mood inside was "somber," one woman said as she walked to the bank. No one knows just who will lose their jobs yet, she said, or whether there are more cuts to come. "Everybody who grew up here in St. Louis and sort of smelled the beer, aspired to work there," said Chambers who became a career coach after she got her pink slip from AB. "They didn't know what to do next if they were not going to be there [at AB]. They weren't prepared for that."

The ripple effects extended far beyond the brewery walls. The St. Louis ad agency community was not prepared either for InBev's next move: advertising and marketing budgets were severely cut. Stroube estimates more than half of the St. Louis ad community that depended on the beer business disappeared in the wake of combining Anheuser-Busch and InBev. "A lot of agencies have gone out of business as a result of it," he said. "A lot of people have lost their jobs, a lot of vendors to those agencies have had to either find other clients or have not survived."

At Ambev, Brito held various positions in finance, operations and sales, before being appointed CEO in January 2004. Headquartered in São Paulo, Ambev became Brazil's largest beer company. Now he was applying the same ruthless efficiency to an American icon. The 3G playbook had crossed the Atlantic, and St. Louis would never be the same.

The hostile takeover of Anheuser-Busch wasn't just a business transaction—it was a cultural collision that would reverberate for years. The promises to maintain jobs and respect tradition proved as ephemeral as foam on a freshly poured beer. What InBev had really purchased wasn't just a brewery or brands, but the right to impose Brazilian efficiency on American excess. And they would execute that right with surgical precision.

V. The Cost-Cutting Machine: Zero-Based Budgeting Era (2008–2015)

The St. Louis headquarters of Anheuser-Busch had always been a monument to American corporate excess. Executive suites with panoramic views. First-class flights to distributors' meetings. Elaborate landscaping with flowers changed seasonally. Company cars, generous expense accounts, and a culture where seniority meant security. All of that ended the moment Carlos Brito walked through the door in November 2008.

One of Brito's most distinctive skills is cost cutting. But this understates the revolution he brought to American beer. What Brito implemented wasn't just cost reduction—it was a complete philosophical overhaul of how a corporation should operate. There would be a relentless focus on costs, the establishment of an intense meritocracy, and a radical informality and openness symbolized by the smashing down of executives' office walls to have them work side-by-side at large tables, their metrics posted publicly for all to see.

The physical transformation of the offices was immediate and shocking. Corner offices were demolished. Executives who had spent decades earning their private sanctuaries suddenly found themselves at communal desks, their performance metrics displayed on boards for all to see. They wear jeans to work now. It no longer feels odd. They walk by flower beds that might not be tended as obsessively as in years past.

But the deeper changes went far beyond dress codes and desk arrangements. AB InBev relies on a concept called "zero-based budgeting", where financial projections are built from the ground up, instead of common practice of using the previous budget or actual results and then adding a certain percentage spend increase. Every expense, from paper clips to marketing campaigns, had to be justified from scratch each year. The goal wasn't just to spend less—it was to question why you were spending at all.

The economy flights and office hot-desking played well with investors who lapped up Brito's zeal for cost-cutting. At AB InBev, Brito has fuelled a culture of transparency, with executives sitting in central, open desks instead of in private offices. "For a while you had to book whatever flight or hotel was the cheapest, no matter if the flight had a six-hour layover or the hotel was 45 minutes away from your conference," the former employee says. "I will never forget [Craft Brewers Conference] in Portland [in 2015] when I stayed at a hotel 45 minutes away from the city center because it was the cheapest option.

The human cost was immediate and brutal. They did. And it hurt. Just as the U.S. economy fell into a steep recession, thousands of A-B workers nationwide lost their jobs. But in the city of St. Louis alone, the number of A-B workers fell 15 percent from 2007 to 2009, according to city government records. The company that "had never been a company to lay people off" was now cutting with surgical precision.

The company created an environment where every dollar spent must be justified. Management encourages employees to think of the company's money as their own. This wasn't just a slogan—it was enforced through constant evaluation and public accountability. Young managers who delivered results were promoted rapidly. Those who didn't were shown the door.

The management trainee program became legendary for its intensity. Most of the people who are at the top of InBev are people who came from our trainee system, which was developed and worked at Ambev. Recruits fresh from top universities were thrown into 18-month bootcamps where 60-hour weeks were the minimum expectation. They were rotated through different departments, given real responsibility, and evaluated constantly. The survivors became true believers in the 3G way.

Devotion to the brand is non-negotiable. Brito wants everyone in the company to be as dedicated as he is – he has admitted to having no hobbies outside of the business and his family, barring a daily 30-minute run on the treadmill. In a company press release around the time of the Megabrew deal, Brito said: "People thrive in a culture based on ownership, meritocracy and informality. It's not just a job – it has to be a passion. That is a crucial mindset. It's also one of our selection criteria. You could compare our employees with top athletes: the dream is big, talent is scarce, selection is strict [and] sacrifices are plentiful. But all of that ultimately makes the difference."

Brito emphasized lean operations, insisting on zero-based budgeting, in which departments build budgets from the bottom up every year to justify every expense. Another former ABI employee says the multinational cut all "unnecessary" expenses, including office snacks and cost-of-living raises. This—and layoffs—began in 2008 when InBev bought Anheuser-Busch, but it was "death by a thousand paper cuts" afterward, they say, and the nickel-and-diming of travel expenses got worse around 2015.

The high-pressure working environment sees young, ambitious staffers evaluated constantly; Brito makes it clear that anyone who does not meet his expectations will not remain in the company for long. AB InBev employees are not valued on seniority, but rather on the potential they offer the company and their inherent traits. This wasn't corporate Darwinism—it was corporate revolution.

The results, from a financial perspective, were undeniable. During Brito's tenure as CEO, from 2005 to 2020, AB InBev's market capitalization increased from $26 billion to $141 billion, annual revenue increased from $14.5 billion to $46.88 billion, normalized EBITDA increased from $4.14 billion to $17.32 billion, and normalized EBITDA margin increased from 28.6% to 36.9%.

But the human toll was equally undeniable. My sister currently works for Kraft Heinz, another 3G Capital company, and constantly talks about how the quality of life for junior employees is pretty terrible. She works private equity-like hours due to 3G's mandate, but isn't compensated in-kind due to the cost-cutting mentality of the owners. The same dynamic played out at AB InBev, where employees worked investment banking hours for consumer goods salaries.

The craft beer acquisition strategy during this period revealed another dimension of the 3G approach. Between 2011 and 2015, AB InBev acquired a dozen craft breweries—not primarily for their beer, but for their entrepreneurial talent and market intelligence. These acquisitions were talent acquisitions disguised as brand purchases, bringing in brewers and marketers who understood the changing consumer landscape that traditional AB InBev executives were missing.

But the corporate culture of the old A-B — tradition-bound, perfectionist, focused more on dominating the beer market than making money — has given way to an aggressive austerity. The extensive cost-cutting has squeezed more profits out of A-B, but questions remain over whether the company's new bosses can grow brands and sell more beer.

The zero-based budgeting era had transformed AB InBev into the most efficient beer company in history. Margins that were once thought impossible became standard. Costs that were once considered fixed became variable. Sacred cows became hamburger meat. But as the company prepared for its next major acquisition—SABMiller—a fundamental question emerged: How much efficiency is too much? At what point does cost-cutting become value destruction?

The answer would come sooner than anyone expected, and from a direction no spreadsheet could have predicted.

VI. The SABMiller Megabrew: Peak Empire (2015–2016)

October 13, 2015. Carlos Brito stood before a packed conference room in London's financial district, his usual uniform of jeans and a button-down shirt looking almost defiant among the sea of pinstripe suits. He had just made the boldest move in consumer goods history: a bid of £70 billion, (US$107 billion when the deal closed), or £44 per share, for its largest rival, the South African company SABMiller. If successful, AB InBev would control nearly one-third of the world's beer.

"This is not the end of our journey," Brito said, his Brazilian accent cutting through the British formality. "This is the beginning of creating the first truly global brewer." The room was silent. Everyone understood what wasn't being said: this was the final move in a fifteen-year chess game that had started in a São Paulo boardroom and would end with three Brazilian investment bankers controlling humanity's relationship with beer.

SABMiller wasn't just another brewery. Founded as South African Breweries in 1895 to serve miners in Johannesburg, it had grown through its own aggressive acquisition strategy to become the world's second-largest brewer. It was the world's second-largest brewer measured by revenues (after Anheuser-Busch InBev) and was also a major bottler of Coca-Cola. Its portfolio included Foster's, Miller, Pilsner Urquell, and dominant positions in Africa, Asia, and Latin America—precisely the growth markets where AB InBev was weakest.

But SABMiller was also everything AB InBev wasn't. Where Brito's company was centralized and standardized, SABMiller believed in local autonomy. The centralised nature of AB InBev versus the devolved strategy of SAB Miller will be one of the key cultural challenges to overcome. Ingrained in the culture of SAB Miller Executives is the ability to make decisions quickly and in greater isolation at a local level. Devolved structures give you the ability to react quickly to customer needs locally and stay close to your customers.

The timing of Brito's bid was no accident. Craft beer was eating into mainstream beer sales globally. Wine and spirits were gaining share. Beer consumption in developed markets was declining. SABMiller's stock had fallen 20% from its peak. The company was vulnerable, and Brito knew it.

What followed was corporate theater at its finest. The company had previously offered £38, £40, £42.15, £43.50 per share respectively, but each of these had been turned down. SABMiller's board, led by Chairman Jan du Plessis, rejected offer after offer, calling them "substantially undervalued." Behind the scenes, however, pressure was building. Altria, which owned 27% of SABMiller, wanted liquidity. The Colombian Santo Domingo family, with 14%, was wavering.

The drama intensified on June 23, 2016, when British voters chose to leave the European Union. The pound plummeted. SABMiller shareholders who would receive payment in sterling suddenly saw their windfall shrink by 15%. AB InBev raises its offer for SABMiller, after Brexit results in a fall in the pound. The fall in the pound had reduced the attractiveness of the November offer to SABMiller shareholders.

The regulatory hurdles were equally dramatic. Anheuser-Busch InBev won antitrust approval Wednesday for its $107 billion takeover of rival SABMiller after agreeing to give up ownership of the Miller brands in the U.S. and open the door to greater competition from craft brewers. This wasn't a minor concession—MillerCoors was SABMiller's crown jewel in America, generating billions in cash flow.

The U.S. Department of Justice had agreed to the deal only on the basis that SABMiller "spins off all its MillerCoors holdings in the U.S." Denver-based Molson Coors will buy SABMiller's 58 percent stake in MillerCoors, gaining the rights to all SABMiller beer brands currently imported or licensed for sale in the U.S. The $12 billion sale to Molson Coors meant AB InBev was essentially paying $107 billion for $95 billion worth of assets.

But Brito didn't care about the math—he cared about the map. SABMiller's brewing operations in Africa spanned 31 countries. In China, the group's national brand, Snow beer, was produced in partnership with China Resources Enterprise Limited, with SABMiller owning 49 per cent; this is the leading brand by volume in China. These were the growth markets that would define the next century of beer.

The integration planning was military in its precision. The Executive Board of Management (EBM) will be composed of 20 zone presidents and functional chiefs—19 from AB InBev and one from SABMiller—who will report to AB InBev's CEO Carlos Brito. The message was clear: this wasn't a merger of equals. This was an acquisition, and the conquering army would run the show.

The human cost was announced with typical AB InBev efficiency. As part of the cost-cutting drive at Inbev and SAB Miller 5,500 jobs will be lost which represents 3% of the combined workforce creating 30% of the estimated savings from the deal. Five thousand five hundred families learning their breadwinner was expendable, reduced to a line item in a synergy calculation.

The merger (AB InBev acquisition of SABMiller), closed on 10 October 2016. Anheuser-Busch InBev, the world's largest brewer, closed Monday on its more than $100 billion acquisition of rival SABMiller. The combined company has $55 billion in annual sales and an estimated global market share of 28 percent, according to market research firm Euromonitor International.

The numbers were staggering. It has approximately 630 beer brands in 150 countries. One company now controlled Budweiser, Stella Artois, Corona, Beck's, Leffe, Hoegaarden, Castle, Aguila, and hundreds more. From the townships of Soweto to the pubs of London, from the beaches of Brazil to the bars of Belgium, every third beer consumed passed through AB InBev's empire.

AB InBev cut $335m of costs in the second quarter, part of an initiative that includes eliminating more than 5,500 jobs to capture $2.8bn in savings from the acquisition in the next three to four years. "We're not changing the $2.8bn guidance but we are moving fast in that regard; we like first to deliver and then see what is next," chief financial officer Felipe Dutra said on a call with reporters.

Standing in the new company's headquarters in Leuven, Belgium, Brito looked at a world map covered in AB InBev's logos. Three investment bankers from Brazil had built the largest consumer goods empire in history. They controlled one-third of humanity's beer consumption. They had consolidated an industry that had been fragmented for centuries.

But empires, history teaches us, contain the seeds of their own destruction. The very efficiency that enabled AB InBev's rise would soon become its vulnerability. The ruthless standardization that created unmatched margins would clash with local cultures and preferences. The cost-cutting that impressed investors would alienate consumers.

The SABMiller acquisition marked peak empire—the moment when there was literally nothing left to buy. which if approved would give the company a third of the global market share for beer sales and a half of the global profit. After this, growth couldn't come from acquisition. It would have to come from innovation, from marketing, from understanding consumers—all the things the 3G model had systematically de-prioritized in favor of efficiency.

As 2016 ended, AB InBev stood atop the beer world like a colossus. But storm clouds were gathering. Craft beer continued to gain share. Cannabis legalization loomed. And in America, cultural forces were stirring that would soon teach the world's most powerful beer company that you can't manage culture the way you manage a spreadsheet.

VII. The Turning Point: Debt, Dividends, and Strategic Shift (2017–2021)

October 25, 2018. The morning started like any other at AB InBev's headquarters in Leuven. Carlos Brito reviewed quarterly numbers. The management team prepared for the earnings call. Then came the decision that would mark the beginning of the end of an era: Anheuser-Busch InBev slashed its dividend in half in a bid to deleverage the business to around a 2x net debt to EBITDA ratio after the company took over $100 billion to finance its acquisition of rival SABMiller. The board approved an annual dividend of €1.80 a share, which represents a 50% cut for shareholders but translates into a $4 billion saving that will help the business deleverage.

The market's reaction was swift and brutal. The stock dropped as much as 11% amid a global selloff, marking the steepest decline since 2008 and destroying 16 billion euros ($18 billion) of market value. In a single day, AB InBev lost more market value than most companies are worth in total.

The dividend cut wasn't just a financial decision—it was an admission of failure. The growth strategy that had built the empire had hit a wall. Management was a bit too optimistic in its forecasts of how the company would be paying it down. The SABMiller acquisition, which was supposed to be the crowning achievement, had become an albatross around the company's neck.

The world's largest brewer cut its dividend in half as it seeks to pay down a $109 billion debt mountain swelled by the acquisition of rival SABMiller Plc in 2016. The numbers were staggering. At the end of 2019, total liabilities amounted to US$95.5 billion. Net debt to normalized EBITDA decreased to 4.0×. Goodwill reached US$128.114 billion, which compares with revenues of US$52.329 billion in 2019.

Think about that for a moment: the company's goodwill—the premium paid for acquisitions above their tangible value—was more than twice its annual revenue. It was as if AB InBev had paid $2.50 for every $1 of sales it acquired. The financial engineering that had enabled the empire's growth had become its prison.

The company is choosing to be prudent, Chief Financial Officer Felipe Dutra said in a phone interview. "If the world proves we were too conservative, we can always accelerate the pace at which dividends are expected to grow," he said. But this was corporate speak for a harsh reality: the music had stopped, and AB InBev was left without a chair.

The parallels to another 3G Capital investment were impossible to ignore. In February 2019, just months after AB InBev's dividend cut, Kraft Heinz was forced to disclose a $15.4 billion write-down in the value of Kraft and Oscar Mayer and other intangible assets. Kraft Heinz took a record-breaking $15.4 billion write-down and its stock fell 27% the following day.

The Kraft Heinz debacle revealed the fatal flaw in the 3G model. In reality, there allegedly were fewer savings to be had, and Kraft Heinz had instead implemented extreme cost-cutting measures that decimated its supply chain and innovation. The undisclosed cost cuts ultimately led to a massive $15.4 billion impairment write-down of the value of Kraft and Oscar Mayer in February 2019 — the largest in the U.S.

Warren Buffett, 3G's partner in both Kraft Heinz and AB InBev, offered a rare admission of error. Several months later, Buffett told CNBC that Berkshire and 3G overpaid for Kraft Heinz, buoyed by optimism that its brands were more valuable than they actually were. If the Oracle of Omaha was admitting mistakes, what did that say about the 3G model?

The challenges weren't just financial—they were operational. AB InBev's debt paydown was slowed in part by continuing problems in the United States. "Their market share has been constantly eroding for the past 10 years in the United States," said Lombardi. Budweiser and Bud Light, once untouchable American icons, were losing relevance with each passing quarter.

Emerging markets, which were supposed to be the growth engine, became another source of pain. The Budweiser maker pointed to the plunge in emerging-market currencies, which is crimping profits after sales growth in the third quarter slowed to the weakest pace in more than a year. The most generous dividend-payer in the food-and-beverage industry has been battered by foreign-exchange moves, including the Argentine peso losing half its value this year.

In April 2020, the COVID-19 pandemic delivered another blow. The latest cut to the dividend was due to the coronavirus-induced slowdown of the global economy. The dividend was halved yet again from 1.00 EUR to 0.50 EUR. The dividend that had once been the pride of the company had been cut by 75% in less than two years.

The stock has declined (7.7%) over the past 10-years and even worse, it has declined (62.9%) over the past 5-years. For year-to-date, the stock is down about (-44%). An investment in a simple S&P 500 Index fund or a dividend index fund would have done better.

The leadership transition was inevitable. In July 2021, after 16 years at the helm, Carlos Brito stepped down. In July 2021, Brito left AB InBev and was succeeded as CEO by Michel Doukeris. Doukeris, another AmBev veteran but with a sales and marketing background rather than finance, represented a subtle but significant shift in philosophy.

The post-Brito era required a different approach. The company pivoted from its relentless focus on cost-cutting to investments in innovation and marketing. In December 2018, Anheuser-Busch InBev partnered with cannabis producer Tilray to begin researching cannabis infused non-alcoholic beverages with Tilray subsidiary, High Park Company. Zero-alcohol beers, hard seltzers, and ready-to-drink cocktails became priorities.

But the fundamental challenge remained: How do you grow when you already control one-third of the world's beer? When every acquisition faces regulatory scrutiny? When your core brands are in structural decline? When your balance sheet is stretched to its limits?

3G Capital and the other executives implemented an "across the board" cost-cutting program that "gutted" innovation and supply-chain capabilities. The drastic measures led the food and beverage company to internally cut its cost-saving and revenue targets, despite projecting more cost-savings and greater revenue to the market.

The comparison between AB InBev and Kraft Heinz was more than cautionary—it was prophetic. Both companies had followed the same playbook: aggressive M&A, extreme cost-cutting, financial engineering. Both had reached the same destination: overwhelming debt, declining market share, and brands that had lost their vitality.

As 2021 dawned, AB InBev faced an existential question that no amount of zero-based budgeting could answer: Can you cut your way to growth? The evidence from both AB InBev and Kraft Heinz suggested the answer was no. But with $100 billion in debt and declining beer consumption globally, the company had few alternatives.

The empire hadn't collapsed—not yet. But the cracks were showing. And in America, a cultural storm was brewing that would test whether the world's largest beer company could survive when efficiency collided with identity.

VIII. The Bud Light Crisis: When Culture Wars Meet Commerce (2023–2024)

April 1, 2023. Dylan Mulvaney, a 26-year-old TikTok personality with 10 million followers, posted a video to Instagram that would ignite the most devastating brand crisis in American corporate history. Dressed as Audrey Hepburn from Breakfast at Tiffany's, she held up a personalized Bud Light can featuring her face, part of March Madness promotions. On April 1, 2023, as part of a larger campaign to address Bud Light's decline in sales and attract younger audiences, Mulvaney promoted the company's Bud Light beer brand in a short video on her Instagram account during March Madness.

"So, I kept hearing about this thing called March Madness, and I thought we were all just having a hectic month!" Mulvaney joked in the video, sipping from the custom can. It was lighthearted, brief—less than a minute long. Within 48 hours, it would become a corporate nightmare.

The context mattered. In a March 23, 2023, interview for Make Yourself at Home, a show hosted by Kristin Twiford, Heinerscheid stated: ... this brand is in decline. It has been in decline for a really long time. And if we do not attract young drinkers to come and drink this brand, there will be no future for Bud Light. Alissa Heinerscheid, Bud Light's vice president of marketing, had been trying to solve a fundamental problem: the brand's core consumers were aging out, and younger drinkers saw Bud Light as their father's beer.

It's like, we need to evolve and elevate this incredibly iconic brand. And my ... what I brought to that was a belief in, okay, what does evolve and elevate mean? It means inclusivity. It means shifting the tone. It means having a campaign that's truly inclusive and feels lighter and brighter and different and appeals to women and to men.

But what Heinerscheid saw as brand evolution, others saw as betrayal. On April 3, two days after Mulvaney's post, the backlash exploded. On April 3, 2023, conservative country singer Kid Rock filmed himself shooting three cases of Bud Light with an MP5 submachine gun, while wearing a MAGA hat, exclaiming "Fuck Bud Light and fuck Anheuser-Busch." As of May 6, 2023, the video had been viewed more than 11 million times.

The boycott wasn't just social media theater—it had immediate, devastating financial consequences. In the week ending April 8, 2023, Bud Light had reportedly experienced an 11% drop in sales, and a 21% drop in the week ending April 15, 2023. As of May 1, 2023, Bud Light "off-premise sales" had dropped 26% since the start of the boycott.

Another country artist, Travis Tritt, joined Kid Rock in calling for the boycott. He pulled all Anheuser-Busch products from his upcoming concert tour, stating that Anheuser-Busch was "[a] great American company that later sold out to the Europeans and became unrecognizable to the American consumer. Such a shame."

The political dimension intensified the crisis. In April 2023, Florida Governor and Republican presidential candidate Ron DeSantis criticized Bud Light's association with Mulvaney as part of a trend of "woke companies" that were "trying to change our country", stating that "pushback is in order across the board".

AB InBev's response was a masterclass in how not to handle a crisis. The company's initial statement was tepid: Anheuser-Busch's immediate response to the boycott was the following statement: "From time to time, we produce unique commemorative cans for fans and for brand influencers, like Dylan Mulvaney. No defense of the partnership. No support for Mulvaney. Just bureaucratic distance.

CEO Brendan Whitworth's eventual statement made things worse: "We never intended to be part of a discussion that divides people. We are in the business of bringing people together over a beer," CEO Brendan Whitworth said in the statement. This attempt at neutrality satisfied no one. Conservatives saw it as insufficient contrition. LGBTQ+ advocates saw it as cowardice.

The human cost was real. Mulvaney said she has "been scared to leave my house, and I have been ridiculed in public, I have been followed," and she criticized Bud Light for not standing by her and the partnership. She said the company never reached out to her in the wake of the backlash.

"Supporting trans people, it shouldn't be political," Mulvaney said in a video posted June 29. Now, in a video posted to Instagram Thursday, Mulvaney is calling on Bud Light and other companies not only to work with trans and other queer influencers, but to support them through the process, even as trans rights are under fire across the country and corporations face anti-LGBTQ+ campaigns.

The sales collapse was historic. Bud Light sales volume dropped 29% in the four-week period ending in mid-June from a year earlier. By summer, the unthinkable had happened. America's top-selling beer is no longer American.

Modelo Especial is now officially America's best-selling beer, dethroning Bud Light, whose popularity faded following the Dylan Mulvaney controversy. Sales of Modelo at grocery and beer stores have surpassed Bud Light's over the course of 2023, according to newly released NIQ data, the first time Modelo has ever beaten Bud Light on a year-to-date basis. There's a tight race to the top, with Modelo landing in first place, gaining 8.34% share of dollars spent on beer vs. 8.28% for Bud Light through August 12. It's a significant move for Modelo since Bud Light has held the position of America's top-selling beer for the large part of the past two decades.

The irony was painful. "There's an irony here," Hough said. "This is an American beer icon, Bud Light, but it's been European-owned for 15 years.… An American beer icon that is technically European has been dethroned by a Mexican brand that is arguably American." Modelo is owned in the U.S. by Constellation Brands, based in New York.

The financial damage extended far beyond lost sales. In North America, organic revenue, seen as the best measure of operating performance, plunged $1.4 billion last year as beer sales by volume tumbled in the region. Small distributors, many family-owned businesses that had bet their livelihoods on Bud Light, were devastated. "It was really hurtful personally," an Anheuser-Busch wholesaler with a trans child in the Northeast, told ABC. "I'm trying to understand what my kid is going through and then this happens." The owner said he took a 30% pay cut and as a result is considering retirement.

The crisis revealed fundamental flaws in AB InBev's approach to brand management. The company had spent decades optimizing for efficiency, treating brands as financial assets to be leveraged. But brands aren't just assets—they're cultural symbols, emotional connections, identity markers. You can't manage culture with a spreadsheet.

Former Anheuser-Busch executive Anson Frericks wrote that Heinerscheid's campaign was a fueled by the intensive ESG and DEI initiatives begun by InBev's new CEO, Michel Doukeris. The new CEO, trying to modernize the company's image, had walked into a cultural minefield.

The company's attempts at recovery were tone-deaf. The apology was followed by an advertising campaign focusing on Bud Light's U.S. origins and "the American spirit." It showed a Clydesdale—a breed of horse associated with the brand and often used in Budweiser promotions—galloping across a range of American towns and landscapes. But as Jon Stewart mocked: "That Budweiser horse that wants to restore our American spirit is actually owned by a Belgian-Brazilian beverage conglomerate. "That all-American Clydesdale's name is probably Jean-Luc Bolsonaro."

By early 2024, the damage appeared permanent. Mulvaney's April 2023 Bud Light promotion, which lasted less than a minute, set off a boycott that pushed sales down 25% overall, with some distributors reporting as much as a 50% hit. In the first quarter of 2024, AB InBev reported U.S. sales off 9.1% compared to last year while sales to retailers were down 13.1%.

Former Anheuser-Busch President of Operations Anson Frericks remarked in February that the brand has yet to fully recover, though Bud Light has been making efforts to win back customers. "They are advertising Bud Light. And candidly, the commercials are actually pretty good," Frericks said on FOX Business' "Varney & Co." "They have Shane Gillis, who's about the opposite of Dylan Mulvaney.

But the deeper lesson wasn't about marketing tactics or spokesperson choices. It was about what happens when a company becomes so focused on financial engineering that it loses touch with its consumers' values and identities. AB InBev had spent fifteen years treating beer as a commodity to be optimized. They discovered, catastrophically, that to millions of Americans, beer was something more.

"Now that Modelo has overtaken Bud Light, the growth for Modelo likely will remain stronger," said Gerald Pascarelli, senior vice president of equity research at Wedbush Securities. "There's really no scenario at this point where you would see Bud Light regain its No. 1 position."

The Bud Light crisis wasn't just a marketing failure—it was the inevitable consequence of a business model that prioritized efficiency over empathy, global scale over local relevance, financial metrics over cultural understanding. In trying to appeal to everyone, Bud Light had connected with no one. In trying to evolve, it had alienated its base without attracting its target.

The empire hadn't fallen, but its crown jewel was irreparably tarnished. And in boardrooms across corporate America, executives were learning a painful lesson: in the age of social media and cultural polarization, a single Instagram post could destroy decades of brand equity. No amount of zero-based budgeting could calculate that risk.

IX. Modern Challenges & Strategic Evolution (2021–Present)

IX. Modern Challenges & Strategic Evolution (2021–Present)

Michel Doukeris took the helm of AB InBev in July 2021 with a mandate that would have been unthinkable during the Brito era: spend money. Not on acquisitions—the regulatory environment and balance sheet made those impossible—but on the very things the 3G model had systematically eliminated: innovation, marketing, and brand building.

The shift was subtle but significant. Where Brito came from finance, Doukeris came from sales. Where Brito spoke in EBITDA margins, Doukeris spoke about consumer occasions. Where Brito flew coach to prove a point, Doukeris invested $2 billion annually in marketing to prove a different one: you can't cost-cut your way to growth in a declining market.

The numbers told a sobering story. Global beer consumption peaked in 2019 at 191 billion liters and has declined every year since. In developed markets, the trend is even starker. U.S. beer consumption has fallen for five consecutive years. European beer volumes are down 8% since 2015. The only growth comes from Africa and Asia, where AB InBev faces entrenched local competitors and regulatory barriers.

Doukeris's strategy centers on premiumization—convincing consumers to pay more for better beer. The company's Beyond Beer portfolio now generates over $2 billion in revenue, growing at double-digit rates. Corona, acquired in the SABMiller deal, has become the company's fastest-growing global brand, commanding premium prices in markets from China to Chile. Stella Artois, repositioned as an affordable luxury, has gained share in the U.S. even as mainstream brands hemorrhage volume.

The digital transformation represents another departure from the Brito playbook. BEES, AB InBev's B2B e-commerce platform, now connects with 3.2 million retailers across 20 countries. In markets like Brazil and Mexico, small shop owners who once ordered beer via phone now use smartphones to manage inventory, access credit, and even sell airtime. The platform generates data on consumption patterns that no amount of cost-cutting could have revealed.

"Consumers continue to want the Bud Light brand to concentrate on the platforms that all consumers love, and we are doing just that through investing in partnerships with the NFL," Doukeris told investors in February 2024. The company signed a $250 million annual deal to remain the NFL's official beer sponsor through 2030, despite Bud Light's damaged brand equity.

But the structural headwinds are relentless. Cannabis legalization continues to expand, with 38 U.S. states now permitting medical or recreational use. Weight-loss drugs like Ozempic are changing consumption patterns—patients report losing their taste for alcohol entirely. Gen Z drinks 20% less than millennials did at the same age, preferring cannabis, hard seltzers, or nothing at all.

The geographic rebalancing reveals both opportunity and challenge. Asia-Pacific now represents 40% of global beer profit pools but only 15% of AB InBev's earnings. In China, the company has pivoted from volume to value, launching super-premium brands like Budweiser Supreme at five times the price of local beers. But competition from local champions like China Resources Beer remains fierce, and regulatory uncertainty under Xi Jinping's "common prosperity" agenda clouds the outlook.

Africa presents a different puzzle. The continent will add 800 million legal drinking age consumers by 2040—more than the current populations of the U.S. and Europe combined. AB InBev controls dominant positions in South Africa, Tanzania, and Mozambique. But infrastructure challenges, currency volatility, and informal markets that represent 80% of alcohol sales make profitable growth elusive. A bottle of beer that sells for $2 in Johannesburg might cost $5 to produce and distribute in rural Nigeria.

The sustainability imperative adds another layer of complexity. AB InBev has committed to net-zero emissions by 2040, requiring billions in capital expenditure for renewable energy, water recycling, and regenerative agriculture. The company's 2025 Sustainability Goals include having 100% of direct farmers skilled, connected, and financially empowered. These investments improve long-term resilience but pressure near-term margins—anathema to the old 3G model.

Technology investments reveal the extent of the strategic pivot. The company has deployed artificial intelligence across its supply chain, reducing out-of-stocks by 30% and improving demand forecasting accuracy by 50%. In Mexico, blockchain technology tracks beer from brewery to retailer, reducing theft and ensuring product quality. These aren't efficiency plays—they're growth enablers that require upfront investment with uncertain payback periods.

The talent strategy has also evolved. Where the Brito era celebrated 100-hour weeks and burnout-level intensity, Doukeris emphasizes work-life balance and mental health. The company introduced flexible work arrangements, expanded parental leave, and launched mental health support programs. The message to employees: we need you creative and engaged, not just efficient and exhausted.

Competitive dynamics have fundamentally shifted. Heineken, under CEO Dolf van den Brink, has pursued a "EverGreen" strategy focused on organic growth and brand investment. Carlsberg has consolidated its position in Europe and Asia through disciplined capital allocation. Constellation Brands, riding Modelo's success, now commands a higher valuation multiple than AB InBev despite being one-tenth the size.

The portfolio rationalization continues quietly. The company has divested non-core brands in markets from Australia to Eastern Europe, raising over $5 billion to reduce debt. But these are tactical retreats, not strategic pivots. The empire remains intact, even if its borders have contracted.

Partnership strategies reflect new realities. Rather than acquire craft breweries, AB InBev now takes minority stakes or distribution agreements, preserving entrepreneurial culture while accessing innovation. The company partners with Netflix on branded content, with music festivals on experiential marketing, with sports leagues on digital engagement. These collaborations would have been unthinkable in the cost-cutting era.

The most telling change might be the company's communication style. Earnings calls that once focused exclusively on cost synergies and EBITDA margins now discuss brand health scores, consumer sentiment, and digital engagement metrics. The language of efficiency has given way to the language of growth.

Yet fundamental questions remain unanswered. Can a company built through acquisition learn to grow organically? Can a culture shaped by financial engineering embrace creative risk-taking? Can brands managed for efficiency reconnect with consumers emotionally? The early returns under Doukeris are mixed—stability achieved, growth still elusive.

As 2024 draws to a close, AB InBev faces a paradox. It remains the undisputed emperor of beer, controlling more brands, markets, and distribution than any competitor. But empires built on conquest struggle when there's nothing left to conquer. The skills that built the empire—deal-making, cost-cutting, standardization—differ from those needed to sustain it: innovation, localization, cultural fluency.

X. Playbook: Business & Investing Lessons

The AB InBev saga offers a masterclass in both empire building and the limits of financial engineering. The lessons extend far beyond beer, speaking to fundamental questions about value creation, corporate culture, and the tension between efficiency and resilience.

The Power and Perils of Serial M&A

AB InBev's acquisition strategy redefined what's possible in consumer goods consolidation. From 2004 to 2016, the company executed over 20 major acquisitions worth more than $200 billion, creating unprecedented scale and market power. The playbook was consistent: identify underperforming assets, pay premium prices justified by cost synergies, integrate ruthlessly, repeat.

The power is obvious—global scale, distribution leverage, procurement savings, overhead elimination. But the perils are equally clear. Serial acquirers often overpay, betting on synergies that prove elusive. Integration complexity grows exponentially with each deal. Cultural clashes multiply. Debt accumulates. Eventually, you run out of targets or regulatory approval, and organic growth becomes imperative—a muscle that's atrophied from years of buying rather than building.

Zero-Based Budgeting: Revolutionary Tool or Value Destroyer?

ZBB transformed AB InBev from a sleepy beer company into a margin machine. By forcing every expense to be justified annually, the company eliminated decades of accumulated inefficiency. Marketing budgets that grew automatically each year suddenly faced scrutiny. Travel policies that entitled senior executives to first-class flights gave way to coach seats for everyone.

But ZBB's strength—relentless focus on efficiency—becomes its weakness when taken to extremes. Innovation requires experimentation and failure, both expensive. Brand building demands consistent investment over years, not annual justification. Employee morale suffers when every coffee machine and office plant becomes a battleground. The Kraft Heinz debacle shows what happens when you cut too deep: brands wither, talent flees, and revenue declines overwhelm cost savings.

Building a Global Talent Machine

The AmBev/AB InBev management trainee program produced an extraordinary generation of executives. By recruiting top university graduates, rotating them through functions, promoting rapidly based on merit, and providing significant equity upside, the company created a leadership pipeline that fueled decades of growth. Alumni now run companies across consumer goods, from Kraft Heinz to Restaurant Brands International.

Yet this talent machine had a dark side. The Darwinian culture that produced exceptional leaders also created burnout, turnover, and groupthink. The emphasis on analytical over creative skills produced managers who could optimize anything but struggled to innovate. The focus on internal promotion limited diverse perspectives. When markets shifted from efficiency to innovation, the talent model struggled to adapt.

Managing Stakeholder Relationships in Polarized Times

The Bud Light crisis revealed how dramatically stakeholder management has changed in the social media age. Traditional corporate strategy assumed you could segment stakeholders—keep investors happy with returns, employees with compensation, customers with products. Social media collapsed these boundaries. A marketing decision aimed at young consumers became a political statement that alienated core customers, destroyed distributor value, and triggered investor lawsuits.

The lesson isn't to avoid all controversial positions—that's impossible in polarized times. It's to understand that every decision now carries cultural weight, that brands exist in political contexts whether they acknowledge it or not, and that speed of response matters more than perfection of message. AB InBev's slow, equivocating response to the Bud Light boycott satisfied no one and prolonged the crisis.

Capital Allocation at Scale

AB InBev's capital allocation journey illustrates both mastery and mistakes. During the empire-building phase, the company expertly used debt to fund acquisitions, creating value through multiple arbitrage—buying at 10x EBITDA, achieving synergies, and trading at 15x. The dividend policy rewarded shareholders while maintaining acquisition capacity.

But capital allocation at peak scale presents different challenges. With limited acquisition opportunities, the company must choose between debt reduction, dividends, share buybacks, and organic investment. The 2018 dividend cut showed what happens when leverage limits flexibility. The current strategy—gradual deleveraging while investing in premiumization and technology—represents a middle path that may satisfy no one.

The Durability of Beer as an Investment Category

Despite all the challenges—craft beer, cannabis, health trends, demographic shifts—beer remains a remarkably durable category. It's affordable luxury in good times, accessible comfort in bad times. It's deeply embedded in social rituals across cultures. The production advantages of scale remain significant. Distribution barriers to entry stay high.

But durability doesn't mean growth. Global beer volumes have plateaued. Value growth comes from premiumization, which has limits. The investment case has shifted from growth story to value play—steady cash flows, high dividends, limited multiple expansion. For investors seeking excitement, beer has gone flat. For those seeking predictability, it still satisfies.

When to Pivot Strategic Models

The most difficult lesson from AB InBev is knowing when to abandon the strategy that brought success. The 3G model worked brilliantly for building an empire through acquisition and efficiency. But markets evolved, consumers changed, and growth opportunities shifted. The company's struggles since 2016 reflect the difficulty of pivoting from a model so deeply embedded in culture, incentives, and identity.

The Doukeris era represents an attempt at strategic evolution—maintaining cost discipline while investing in growth. But true transformation requires more than incremental change. It requires acknowledging that what got you here won't get you there, that core competencies can become core rigidities, and that sometimes the greatest risk is not taking enough risk.

XI. Analysis & Bear vs. Bull Case

The Bull Case: Unassailable Moat, Inevitable Recovery

Bulls see AB InBev as the ultimate value play in consumer goods—a company trading at historic discount multiples with irreplaceable assets and multiple paths to value creation.

The scale advantage remains overwhelming. With 500+ brands across 150 countries, AB InBev enjoys procurement savings, distribution leverage, and marketing efficiencies no competitor can match. The company buys 10% of the world's barley, giving it unmatched input cost advantages. Its distribution network reaches 6 million retail points, creating barriers to entry that technology can't disrupt.

Premium brands are gaining momentum. Corona, Stella Artois, and Michelob Ultra are growing double-digits globally, offsetting mainstream brand decline. Premiumization has room to run—premium beer represents 40% of profit pools but only 20% of volumes. As emerging market consumers trade up and developed market consumers seek quality over quantity, mix improvement drives margin expansion without volume growth.

Geographic diversification provides resilience. While North America struggles, Latin America and Africa are growing high single-digits. Asia-Pacific offers decades of growth as income levels rise and beer culture develops. No other beverage company has comparable emerging market exposure with established distribution and local brands.

The balance sheet is improving. Net debt to EBITDA has declined from 5.5x to 4.0x, heading toward the 2x target. As leverage decreases, capital allocation flexibility increases. The company could reinstate dividend growth, accelerate buybacks, or pursue tuck-in acquisitions. With $7 billion in annual free cash flow, shareholder returns could double without operational improvement.

Digital transformation is bearing fruit. BEES has created a direct relationship with millions of retailers, providing data advantages and cross-selling opportunities. D2C initiatives are improving margins and brand connection. AI-driven supply chain optimization is reducing costs and improving service levels. These investments, painful in the short term, create lasting competitive advantages.

The valuation discount is extreme. At 9x forward EBITDA, AB InBev trades at a 40% discount to consumer staples peers and a 50% discount to its own history. Even modest multiple re-rating would drive 50% upside. If the company simply returned to historical average multiples, the stock would double.

The Bear Case: Structural Decline, Permanent Impairment

Bears see AB InBev as a melting ice cube—a declining business model masked by financial engineering, facing existential threats without viable responses.

The core business is in terminal decline. Beer consumption has fallen for five consecutive years in developed markets. The trend is accelerating, not moderating. Bud Light's collapse from 20% to 12% U.S. market share is permanent. Budweiser is losing relevance globally. The company's two largest brands are dying, and no amount of marketing can resurrect them.

Debt constrains all options. Despite improvement, $85 billion in debt limits flexibility. Interest expense consumes $3 billion annually. Investment grade ratings require maintaining leverage ratios, preventing aggressive investments or acquisitions. The company is stuck in purgatory—too leveraged to grow, too large to sell.

Competition is intensifying everywhere. Heineken and Carlsberg are gaining share in Europe. Local champions dominate emerging markets. Spirits companies are entering beer categories. Hard seltzers, canned cocktails, and non-alcoholic alternatives are fragmenting occasions. The moat is wide but dry.

Cannabis will devastate beer economics. As legalization expands, cannabis becomes beer's direct substitute for relaxation and social occasions. Studies show legal cannabis reduces beer consumption by 15-20%. Federal U.S. legalization, increasingly likely, would accelerate substitution. AB InBev can't participate meaningfully given regulatory constraints and cultural conflicts.

Management lacks growth DNA. The entire leadership team was trained in the 3G model of cost-cutting and acquisition. They know how to optimize, not innovate. The cultural transformation required for organic growth will take a generation. By then, market position will have eroded beyond recovery.

ESG pressures are mounting. Alcohol faces increasing scrutiny from health advocates and regulators. Marketing restrictions are tightening globally. Sin taxes are rising. Climate change threatens barley supplies and increases production costs. Social acceptance of alcohol is declining among younger consumers. The industry faces tobacco-style headwinds without tobacco-style pricing power.

The Verdict: A Value Trap or Opportunity?

The truth likely lies between extremes. AB InBev isn't going bankrupt, but neither will it return to growth glory. It's a cash cow in a declining industry, capable of generating substantial returns for patient investors but unlikely to excite growth seekers.

The key variables to watch: Can premiumization offset volume declines? Will emerging markets compensate for developed market weakness? Can the culture evolve from efficiency to innovation? Will cannabis legalization accelerate or moderate? How will Gen Z's relationship with alcohol evolve?

For value investors, the risk-reward may be favorable at current valuations. The dividend yield exceeds 2%, with room for growth as leverage declines. The free cash flow yield approaches 10%. Downside appears limited given asset value and cash generation.

For growth investors, the story remains uninvestable. Secular headwinds overwhelm cyclical opportunities. Market share losses continue. Innovation efforts lag competitors. The empire may persist, but its best days have passed.

XII. Epilogue & "What Would We Do?"

Standing in the boardroom of AB InBev's headquarters in Leuven, looking at brewing equipment that dates back centuries alongside screens showing real-time sales data from six continents, the contrast captures the company's fundamental challenge: how to honor tradition while embracing transformation.

If we were running AB InBev today, the strategic priorities would be clear but execution would be complex.

Portfolio Rationalization: Fewer, Stronger, Better

The 500+ brand portfolio is a relic of the acquisition era—impossible to manage effectively, dilutive to marketing impact, and confusing to consumers. We would dramatically simplify, focusing on three tiers: global premiums (Corona, Stella Artois), regional champions (Brahma in Brazil, Castle in Africa), and local fighters (craft partnerships, cultural icons). Everything else would be divested or discontinued.

The savings from complexity reduction would fund innovation and marketing for core brands. Instead of spreading resources across hundreds of labels, concentrate firepower on the 20 brands that drive 80% of profit. Make big bets on fewer horses.

Cultural Renaissance: From Efficiency to Creativity

The 3G culture served its purpose but has become a liability. We would initiate a cultural transformation that preserves cost discipline while embracing creative risk-taking. Hire from outside industries—technology, entertainment, hospitality. Create innovation labs with venture-style funding and failure tolerance. Celebrate creative success as enthusiastically as cost savings.

Most critically, change the incentive structure. Today's compensation rewards efficiency metrics. Tomorrow's should balance efficiency with innovation metrics—new product revenue, brand health scores, talent retention. You get what you measure, and AB InBev has been measuring the wrong things.

Geographic Focus: Double Down on Growth Markets

The developed world strategy should be defensive—protect share, maximize cash, fund growth elsewhere. The real opportunity lies in Africa and Asia, where rising incomes, urbanization, and westernization drive consumption growth. We would dramatically increase investment in these markets, accepting lower near-term margins for long-term position.

This means local production, local brands, local partnerships. The colonial model of selling European brands to emerging markets has limits. Success requires becoming genuinely local while leveraging global scale for procurement and best practices.

Beyond Beer: Embrace the Inevitable

Fighting cannabis and alternative beverages is futile. We would aggressively expand beyond beer through partnerships, acquisitions, and innovation. Create a cannabis beverage division ready for legalization. Build a portfolio of functional beverages—energy, relaxation, cognitive enhancement. Develop non-alcoholic alternatives that satisfy the social occasion without the alcohol.

This isn't abandoning beer—it's recognizing that future consumers will have portfolios of substances and experiences. AB InBev should provide all of them, not just one.

Digital Transformation: From Wholesale to Direct

BEES is a start, but the real opportunity is direct-to-consumer. We would build a digital platform that connects directly with consumers—subscription services, personalized recommendations, exclusive releases, virtual experiences. Transform from a B2B wholesale model to a B2B2C hybrid that captures more value and builds direct relationships.

This requires different capabilities—data science, user experience, logistics. It means competing with Amazon, not just Heineken. But the companies that own customer relationships will own the future.

The Ultimate Question: Keep or Sell?

The most fundamental question facing AB InBev shareholders: Is this a business to own for the next decade, or an asset to monetize while value remains?

The answer depends on time horizon and risk tolerance. For 3G Capital, which has already extracted enormous value through financial engineering, selling might make sense. Find a sovereign wealth fund seeking stable cash flows, or break up the empire into regional pieces that strategic buyers would pay premiums to acquire.

But for long-term investors who believe in transformation potential, patience might pay. The assets are irreplaceable. The cash generation remains robust. The global footprint provides options. With the right leadership and strategy, AB InBev could evolve from beer company to beverage platform, from efficiency machine to innovation engine.

Final Reflections: The Price of Empire

The AB InBev story is ultimately a meditation on the price of empire. Three Brazilian financiers built the largest consumer goods empire in history through ambition, discipline, and ruthless efficiency. They consolidated a fragmented industry, created enormous shareholder value, and redefined what's possible in corporate transformation.

But empires extract costs. Communities lost employers. Workers lost jobs. Brands lost soul. The efficiency that enabled conquest became the rigidity that prevented evolution. The culture that built the empire couldn't sustain it.

As we contemplate AB InBev's future, broader lessons emerge. Financial engineering has limits. Efficiency without innovation leads to decline. Brands are cultural artifacts, not just commercial assets. Scale provides advantages but reduces agility. What works in one era fails in the next.

The beer industry's evolution mirrors broader economic trends—consolidation, financialization, globalization, and now fragmentation. AB InBev rode the first three waves masterfully but struggles with the fourth. The very scale that was its strength has become its weakness in an era demanding localization, personalization, and authenticity.