Granite Construction: America's Infrastructure Company

Building on Bedrock — A 125-Year Journey from Gold Rush Discovery to $4 Billion Construction Giant

I. Introduction: The Unexpected Treasure

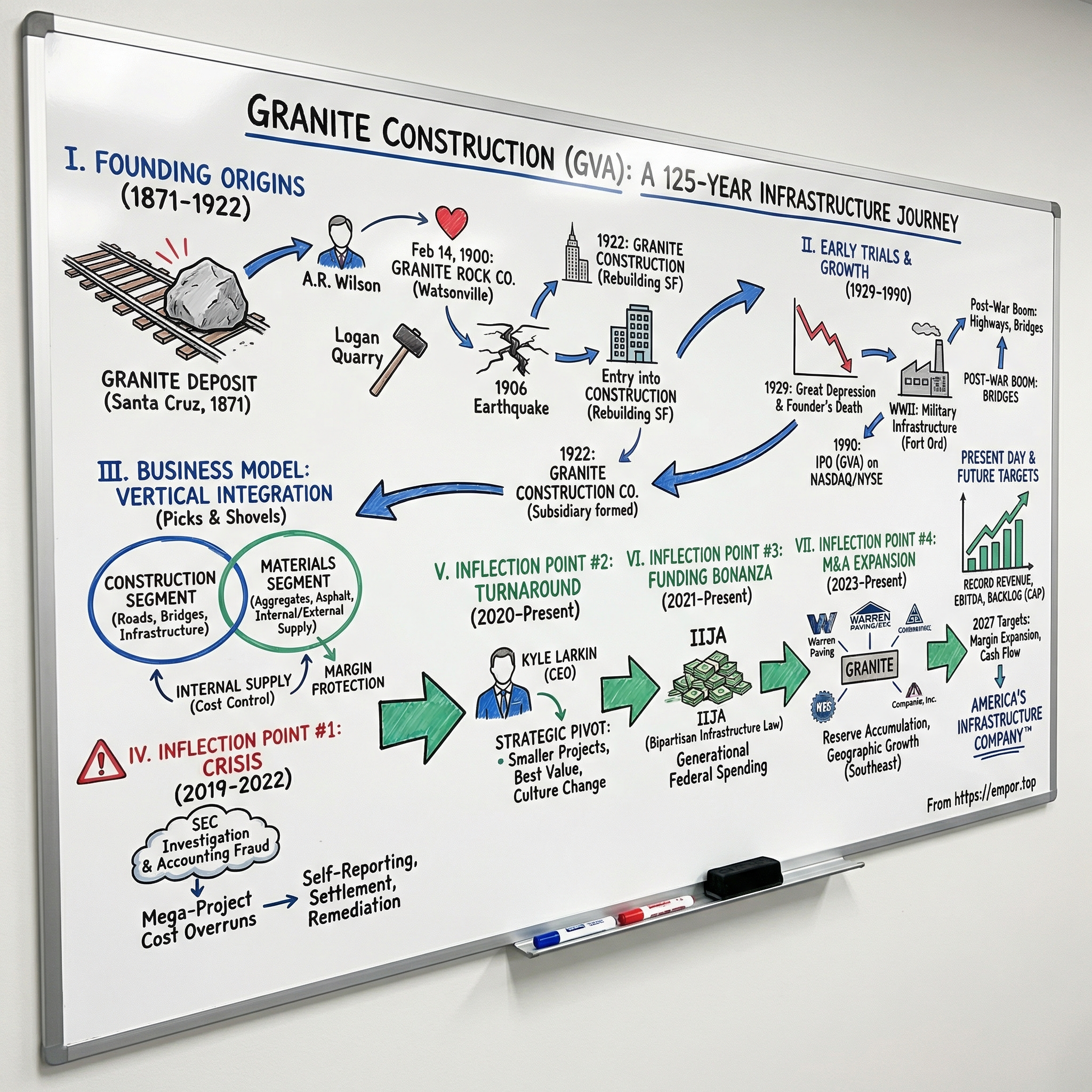

Picture this: California, 1871. Railroad engineers laying track for the Southern Pacific are moving through Santa Cruz County when their equipment strikes something unexpected. Not gold—which by then had driven California's frenzied growth for two decades—but something that would prove far more enduring: a massive deposit of granite, pushed to the earth's surface by the San Andreas Fault over 200 million years.

"Granite Construction Company's foundations lie in the lure and promise of the Wild West during the 1800s. Risking life and limb for fortune, tens of thousands of wildcatters flooded California bringing on the great Gold Rush during the mid-1800s. When the Transcontinental Railroad connected California with the rest of the nation in 1869, agricultural visionaries in Santa Cruz County began exploring ways to link into this vast rail system. While doing so, an unexpected discovery was found in the earth: granite."

Today, that accidental discovery has evolved into Granite Construction (NYSE: GVA), one of the largest vertically-integrated civil contractors and construction materials producers in the United States. The company's journey spans three centuries of American history—from the era of horse-drawn quarry carts to an age of federal infrastructure spending that CEO Kyle Larkin calls "the strongest market I've seen throughout my career."

But this isn't just a story of steady ascent. It's a tale of near-death experiences, an SEC fraud scandal that cratered the stock, a turnaround CEO who spent his entire career at the company, and a once-in-a-generation infrastructure funding bonanza. It's the story of how a "picks and shovels" strategy—selling materials to everyone building roads, including your competitors—can be more profitable than chasing the gold itself.

Granite is "America's Infrastructure Company™." Incorporated since 1922, Granite is one of the largest diversified vertically-integrated civil contractors and construction materials producers in the nation. The company operates through two segments: Construction and Materials segments.

"2024 was a record year for Granite," said Kyle Larkin, Granite President and Chief Executive Officer. "We set company records for revenue, adjusted net income, adjusted EBITDA, operating cash flow and safety." The numbers tell a remarkable story of reinvention: fiscal year revenue increased 14% to $4 billion, the culmination of a strategic transformation that emerged from the ashes of an accounting scandal.

This article explores the central questions of Granite's century-plus journey: How did a quarry operation become a diversified infrastructure giant? Why is owning aggregate reserves—essentially, rocks—such a powerful competitive advantage? What lessons can investors learn from a company that self-reported fraud to regulators, paid the price, and emerged stronger? And perhaps most importantly: Is Granite positioned to capture an outsized share of America's infrastructure renaissance, or is the company's turnaround story already priced in?

II. Founding Origins: Gold Rush to Granite (1871-1922)

The story of Granite Construction begins not with a company, but with a man whose middle name, according to a 1922 newspaper cartoon, "stands for 'Roads.'" Arthur Roberts Wilson, better known as A.R. Wilson, was born in San Francisco in 1866, the nephew of the only Hispanic to ever serve as governor of California, Romualdo Pachero. His uncle played an influential role in the young man's life after the early death of his father. Wilson was sent East for his education, earning a degree in engineering from the Massachusetts Institute of Technology in 1890. He then returned to the Bay area to become a construction engineer, serving a term as City Civil Engineer for Oakland and running the local quarry.

Wilson was searching for a reliable source of high-quality aggregate materials when opportunity knocked in an unusual way. Warren Porter, the son of a local banker named John T. Porter, counted himself as a lumberman, banker, and politician. When his father's bank, the Pajaro Valley Bank, foreclosed on a quarry in Aromas, Porter enlisted the help of Wilson and four other investors to purchase and manage the small granite quarry, convinced that the property could be turned into a profitable enterprise. Wilson's interest was piqued, so he borrowed $10,000 and moved his wife and three small children south to Watsonville.

To raise his share of the money, Wilson borrowed $10,000 from a cousin, backed by a life insurance policy. He then moved his family to Watsonville, and on February 14th, 1900—Valentine's Day—the partners incorporated Granite Rock Company. The symbolism of that date would prove apt: the Wilson family's love affair with the rock business would endure for generations.

In 1900, the men formed the Granite Rock Company. The Logan Quarry employed 15 men who were paid $1.75 per day for 10-hour, back-breaking shifts swinging sledgehammers and picks. The work was brutal, the pay modest, but the opportunity was immense. Prior to 1906, the quarry's output was used primarily for railroad ballast. In the months following the earthquake, as crews set to work replacing twisted stretches of rail, the need for railroad ballast increased dramatically.

Then came the earthquake that would reshape both San Francisco and Granite Rock's destiny.

"The Great 1906 Earthquake devastated San Francisco and neighboring towns—but it also created opportunity for Granite. In the earthquake's aftermath, more than 3,000 people were killed and 225,000 left homeless. Logan Quarry suffered damage, and its wreckage would take much time to untangle, but first things first: Wilson bought bread in Watsonville, and headed to San Francisco to help. Quarry workers turned into relief workers, helping to remove debris in order to get the area on its feet again. The need to reconstruct created a heavy demand back at the quarry. Returning workers found that the quake, despite its damage, had actually done them a favor. Huge rocks had dislodged and fell on the quarry floor, shattering into manageable fragments of granite, just the high-quality building material that was in urgent demand."

The signal development stemming from the earthquake, however, was Granite Rock's entry into the construction business. Wilson joined the massive effort to rebuild those areas flattened by the earthquake by acting as a general building contractor, marking Granite Rock's debut as both a mining and construction firm.

This dual identity—materials producer and construction contractor—would become the company's defining strategic advantage over the next century. By 1922, the construction business had grown substantial enough to warrant its own corporate structure. With business strong, Wilson and Porter wanted to move its construction arm into a wholly-owned subsidiary rather than a part of Granite Rock. Walter J. Wilkinson was tapped to head up the new venture called Granite Construction Company. Wilkinson had joined Granite Rock a year after the company's founding and had eventually become the superintendent of construction. Those who worked with him say that Wilkinson was a visionary. His cost estimates were detailed, including hay for the horses, and his time estimates were usually on the money.

Arthur Wilson bought all contracting equipment from Granite Rock for the sum of $29,180.39. The company set up shop in a tool shed at Logan Quarry and opened for business. Granite Rock, Granite Construction and a related material supplier, Central Supply Company, shared a symbiotic relationship in the early days.

This symbiosis—owning the materials you use in construction, and selling excess materials to other contractors—would become Granite's enduring competitive advantage. Wilson had inadvertently created one of America's first vertically-integrated civil construction businesses.

III. Early Trials: The Founder's Death and the Great Depression (1929-1945)

The late 1920s represented the peak of A.R. Wilson's empire. Wilson had purchased Warren Porter's interest in Granite Rock from Java Coconut Oil in 1928 and was the majority shareholder and president. The three interconnected companies—Granite Rock, Granite Construction, and Central Supply—formed a formidable regional operation.

Then, in a single October week in 1929, everything changed.

"Driving to a quarry on an October day in 1929, Wilson was overcome with dizziness and flagged down a passing vehicle to take him home. A doctor rushed to the house and diagnosed a heart attack. By the early morning hours of the next day, the founder of Granite Rock and Granite Construction was dead. His young wife Anna, whom he had married just seven years earlier, inherited the businesses. The day he died, the stock market began a downward slide, which culminated 10 days later in the Great Crash of 1929. That ushered in one of the greatest economic challenges in history: the Great Depression."

The timing couldn't have been worse. The Federal Reserve raised interest rates in hopes of cooling down the stock market; higher interest rates led to less construction, which was also reeling from an excess supply of housing thanks to a building boom in 1928.

Wilson ran these three companies until just ten days before the stock crash of 1929. Driving home from the quarry one day he suffered a heart attack and died. Wilson's wife Anna took over as president of the Granite companies and son Jeff Wilson served as general manager. The stock crash ushered in the Great Depression of the 1930s, and with the industries that it served suffering, the Granite companies struggled as well.

Anna Wilson, suddenly thrust into leadership, faced an impossible situation. With construction demand collapsing and capital scarce, maintaining three interlocking businesses became untenable.

Finding it too difficult to keep three businesses operating during this difficult period, the Wilson family decided in 1936 to sell Granite Construction Company to businessmen Walter Wilkinson, Sr., and Bert Scott. As a result, Granite Rock and Granite Construction now followed their own destinies.

This separation would prove permanent. Granite Rock (later known as Graniterock) remained a family business for generations, eventually earning the Malcolm Baldrige National Quality Award. Granite Construction, under new ownership, would chart its own course.

The Wilson family sold its interest in Granite Construction Company to Walter Wilkinson and Bert Scott in 1936. In the 1930s, the Company opened California's first asphaltic concrete plant in Aromas and also began California's first delivery of pre-mixed concrete in tiny dump trucks. This concrete was used in projects including the WPA's construction of the Santa Cruz Civic Auditorium.

The Depression years, despite their hardships, planted seeds of innovation. And when war came, Granite found its footing again.

World War II brought new activity, as materials were needed to build Fort Ord, Camp McQuaide and the Navy airstrip in Watsonville. Many men were away serving in the armed forces, so women and workers from Jamaica took over operations. A new plant was built at Asilomar in Pacific Grove, and excavation of the mining face at the Aromas quarry brought it down 100 feet, now level with the train tracks.

Granite managed to survive the 1930s. During World War II, with Bert Scott serving as president, the company did some work for military installations, including Watsonville Naval Air Station.

The war demonstrated a pattern that would define Granite's next eight decades: when government needs infrastructure built, Granite benefits. This cyclical exposure to public spending—both a vulnerability and an opportunity—would become central to understanding the company's investment thesis.

IV. Building America: Post-War Growth to IPO (1940s-1990)

The post-war era transformed Granite from a regional California contractor into a national force. "The company was responsible for much of the work on Fort Ord and the Watsonville Navy Air Station, and Highway 101, the first major artery connecting California. 'Our history is California's history, and even the U.S.'s history,' Larkin said. 'The impact that we have made in the communities where we have lived and worked is tremendous.'"

The company's evolution mirrored America's infrastructure boom. Granite remained very much a California contractor over the next 30 years. In 1955 it opened a Sacramento branch, and also during the 1950s acquired American Sand & Gravel Company. The company completed no significant acquisitions during the 1960s, then in 1971 bought E.H. Haskell Company to establish a branch in Santa Barbara. A Bakersville branch was established in 1976 through the acquisition of Owl-Folsom. In addition, Granite opened a branch in Stockton in 1978 when it acquired McGaw Company. It was also during the 1970s that Granite took on major projects outside of California. It completed a number of jobs related to the Washington Metropolitan Area Transit Authority, including several train stations in the District of Columbia and nearby Maryland. In Washington state, Granite worked on the Chief Joseph Powerhouse and the Rock Island Powerhouse, both on the Columbia River.

Wilkinson, widely considered the company's founder, authored in 1940 the "Founder's Guide for Future Generations," which to this day makes up the backbone of Granite's corporate philosophy. The 11-point list among other things encourages employees to follow the Golden Rule, respect the rights of others, exercise patience and good cheer, keep appointments and fulfill promises promptly.

By the late 1980s, Granite had grown into a substantial enterprise, but remained privately held. A decision to change that would prove transformative.

"In 1990, Granite Construction Incorporated entered the public market as GVA on the NASDAQ Exchange (later moved over to the NYSE) with an initial public offering (IPO). By the end of this decade, Granite would reach the $1 billion mark in annual revenues and expand into new markets."

Granite was then taken public in April 1990, and its shares began trading on the NASDAQ. A secondary offer was held a year later. The company solidified its California base of operations during the early 1990s. A Palm Springs branch was opened in 1992, as was a San Diego branch.

The IPO unlocked capital for aggressive expansion. Gibbons Co. was a holding company for several subsidiaries: Gibbons & Reed Co., a heavy civil contractor doing business in a number of Western states; Concrete Products Co., producers of concrete, asphalt, sand, and gravel; Garco Testing Laboratories; Inter-Mountain Slurry Seal; and Bear River Contractors. Tallied together, the Gibbons' companies generated annual revenues in the $90 million range. Granite completed another significant acquisition in 1997, bolstering its business in the Southeast by buying the highway and heavy civil construction divisions of Hardaway Co., a major construction company based in Columbus, Georgia.

Granite expanded into New York City in 2000, and would soon thereafter help rebuild the World Trade Center after the 9/11 terrorist attacks. Notable work also includes a $500 million superhighway in Maryland and a rebuild of the Tappan Zee Bridge in New York.

With Halmar in the fold, Granite saw its revenues rise to $1.55 billion in 2001 and $1.76 billion in 2002, along with net income of $50.5 million in 2001.

The transition from a regional California contractor to a national infrastructure player seemed complete. But growth through mega-projects would eventually expose Granite to risks that nearly destroyed the company.

V. The Business Model: Vertical Integration and Two Segments

Before diving into Granite's crisis and turnaround, it's essential to understand the business model that makes the company unique—and that ultimately saved it.

Granite Construction Incorporated operates as an infrastructure contractor in the United States. It operates through two segments: Construction and Materials segments. The Construction segment engages in the construction and rehabilitation of roads, pavement preservation, bridges, rail lines, airports, marine ports, dams, reservoirs, aqueducts, infrastructure, and site development for use by the public and water-related construction for municipal agencies, commercial water suppliers, industrial facilities, and energy companies.

The Materials segment is involved in the production of aggregates, asphalt concrete, liquid asphalt, and recycled materials production for internal use in construction projects and sale to third parties. It also offers site preparation, mining, and infrastructure services for railways, residential development, energy development, and commercial and industrial sites; and provides construction management professional services.

The power of this dual structure becomes clear when you understand the "picks and shovels" strategy that current CEO Kyle Larkin has emphasized.

"During the California gold rush of the 1850s, there were two broad paths to wealth: Go for the gold and strike it rich, or pursue the picks and shovels approach by selling tools and supplies to prospectors. More than a century and a half later, Granite Construction is pursuing a mix of the two approaches. The Watsonville, California-based civil contractor and road builder is searching for gold in infrastructure projects, which can provide steady revenue and backlog for years to come."

"On the picks and shovels side, Granite's materials business is selling the supplies needed to build infrastructure. It offers asphalt and aggregates to other horizontal contractors while supplying its own projects. The firm continues to amass ever more volume by snatching up smaller providers across different regions."

The Materials segment isn't just a support function—it's a strategic weapon. Aggregate reserves (crusite stone, gravel, sand) are finite, irreplaceable resources. Once a quarry is depleted, you can't create a new one. And permitting new quarries is extraordinarily difficult, often taking decades of regulatory approvals. This creates a natural moat around established materials businesses.

The vertical integration creates multiple advantages:

Internal Supply Security: Granite doesn't have to worry about materials shortages or price spikes when it's building roads—it supplies itself.

External Revenue Stream: Excess materials capacity is sold to competitors who bid against Granite on construction projects. In effect, Granite profits whether it wins or loses the construction contract.

Margin Protection: By controlling input costs through its materials business, Granite can bid more aggressively on construction contracts while protecting margins.

Asset Optionality: The aggregate reserves represent substantial embedded value that doesn't fully appear on the balance sheet.

"Under Larkin's leadership, Granite has sharpened its competitive edge through vertical integration—owning both the construction and materials sides of the business—and embracing 'best value' procurement models like progressive design-build."

For investors, understanding this dual nature is crucial: Granite isn't just a construction contractor (a notoriously challenging business with thin margins and project risk), nor just a materials company (a slower-growth but higher-margin business). It's the combination that creates value.

VI. Inflection Point #1: The Accounting Scandal & SEC Investigation (2019-2022)

Every great turnaround story requires a crisis. Granite's came in the form of an accounting fraud that nearly destroyed shareholder confidence and brought SEC investigators to Watsonville.

"The Securities and Exchange Commission today charged Granite Construction, Incorporated and its former Senior Vice President, Dale Swanberg, with fraud for inflating the financial performance of the major subdivision Swanberg managed. In 2021, Granite restated its financial statements from 2017 through 2019 to correct revenue and profit margin errors allegedly caused by Swanberg's misconduct. The company agreed to pay $12 million to settle the SEC's charges."

The scheme was rooted in the fundamental problem of large construction projects: estimating costs years into the future on complex, fixed-price contracts.

According to a complaint filed in federal court, in the face of pressure to turn around the flagging performance of his group, Swanberg "orchestrated a scheme to conceal the deteriorating performance of the Heavy Civil Group by improperly deferring the recording of additional costs that arose on significant projects." The scheme resulted in Granite overstating its financial results by about $62 million over several quarters in 2017 and 2018.

"The SEC's complaint against Swanberg alleges that, beginning in 2017, he faced demands within Granite to turn around the flagging performance of his group and to improve its financial metrics. Swanberg and his group, however, allegedly encountered significant increases in expected costs for their construction projects that, if recorded, would have decreased the group's earned revenues. The complaint alleges that Swanberg, when faced with these competing demands, orchestrated a scheme to manipulate profit margins and improperly defer the recording of expected costs to hide the group's flagging performance."

"The scheme allegedly unraveled in mid-2019 when several construction projects neared completion and Swanberg could no longer defer recognition of the cost increases."

The revelation hit shareholders like a freight train.

"Issues with the company's heavy civil construction unit continue to plague the stock, which has now lost nearly half of its value this year." Shares of Granite Construction lost more than 35% of their value in a single day after reporting quarterly results that fell well below expectations.

"Issues with the company's heavy civil construction unit continue to plague the stock, which has now lost nearly half of its value this year. Before markets opened on Friday, Granite reported third quarter adjusted earnings of $0.58 per share on revenue of $1.1 billion, falling well short of analyst expectations for $1.44 per share in earnings and missing revenue estimates by about $60 million."

"The company was under investigation from the SEC from 2019 to 2021 for misrepresenting revenue."

What happened next, however, distinguishes Granite from many corporate fraud cases.

"Granite agreed to pay $12 million to settle SEC charges, a number that may have been influenced by Granite's cooperation with the SEC and remediation efforts. According to the SEC's complaint against Granite, Granite self-reported potential revenue recognition issues to the SEC and initiated an internal investigation '[w]ithin weeks' of receiving internal complaints concerning the accuracy of certain project forecasts."

"The SEC's complaint against Granite is premised on Swanberg's alleged misconduct. The complaint credits Granite with self-reporting to the Commission and undertaking remediation by, among other things, redesigning its internal accounting controls and policies and procedures to increase the transparency and accuracy of expected costs for construction projects."

"In separate administrative proceedings, the company's former CEO, James H. Roberts, and former CFOs, Laurel Krzeminski and Jigisha Desai, while not charged with misconduct, agreed to return more than $1.4 million, $327,000, and $176,000, respectively, in bonuses and compensation to Granite. These clawbacks were made pursuant to Section 304 of the Sarbanes-Oxley Act, which requires executives to reimburse certain compensation when an issuer is required to restate its financials as a result of misconduct."

"Granite Vice President of Investor Relations Mike Barker told Construction Dive in an emailed statement that the company worked with the SEC to settle the charges against it. 'We fully cooperated with the SEC in its investigation into this matter, and we are pleased to put this matter behind us as we move forward under new leadership,' Barker said."

The self-reporting and genuine remediation—rather than denial and obstruction—proved critical to Granite's ability to move forward. But the company still needed new leadership to restore credibility and reimagine its strategy.

VII. Inflection Point #2: The Kyle Larkin Turnaround (2020-Present)

If Granite needed a leader who understood the business from the ground up, they found one in Kyle Larkin.

"Kyle Larkin was appointed Granite's president in September 2020, and as chief executive officer in June 2021. He is responsible for the development and implementation of both short- and long-term companywide strategies to ensure Granite's growth, effectiveness, sustainability, and overall stakeholder return. Kyle joined Granite in 1996 and has served in a variety of positions beginning as an estimator in the Reno, NV office, and most recently serving as executive vice president and chief operating officer responsible for overseeing the day-to-day operations of the company. Kyle's additional experience ranges from project engineer to manager of construction, as well as president of Granite's wholly-owned subsidiary, Intermountain Slurry Seal."

Larkin's journey from intern to CEO exemplifies the kind of deep institutional knowledge that turnaround situations often require.

"How did you choose the construction industry? Larkin: My dad inspired me. He worked in computers in Silicon Valley, and I knew I didn't want to do that. I wanted to be outside. When I was applying to college and trying to figure out what to do, he pulled out an old notebook of mine. I'd had all kinds of ideas for projects I wanted to do, and he got tired of hearing about them so he told me to write them down. I drew designs and listed materials for a skateboard ramp and PVC bicycle, for example. He reminded me of what I enjoyed doing, and my mom found a program. I got a degree in construction management at California Polytechnic State University."

"Kyle received a BS in construction management from Cal Poly, San Luis Obispo and an MBA from the University of Massachusetts, Amherst."

"What advice do you have for people looking to follow in your career footsteps? Larkin: When I look back on my career, beyond having great champions along the way, I've always taken on new things. Whether it's getting a graduate degree, signing on for stretch assignments, doing something different in the business, reading business books or getting involved in nonprofits, I made sure I was constantly learning. I've been working with a business coach for over a year and I plan to continue with him because he challenges me."

"What keeps you up at night as an executive? Larkin: There's a lot that comes with having the opportunity to lead a 100-year-old company. I feel inherent pressure to really deliver and perform at the highest level for our stakeholders, employees, shareholders and communities."

The strategic pivot under Larkin was immediate and decisive.

"Following the financial reporting missteps, Granite reorganized and appointed Kyle Larkin president in 2020 and CEO in 2021. Since Larkin took the lead, the firm has shifted its strategy away from mega projects worth more than $500 million to focus on smaller, less complex work that carries less risk and is easier to execute."

This wasn't just risk mitigation—it was a fundamental reimagining of how Granite would compete.

"Under Larkin's leadership, Granite has sharpened its competitive edge through vertical integration—owning both the construction and materials sides of the business—and embracing 'best value' procurement models like progressive design-build. These approaches allow the company to control cost, ensure consistent quality, and deliver on complex, high-value projects that demand innovation and collaboration."

"It's all about relationships, which is not necessarily specific to our industry. It's also about building high-performance teams, which comes back to people. If you can build high-performance teams, you can step out of the way and let them run."

"What do you think is the most pressing issue facing the construction industry right now? Larkin: Workforce development. It's always been our biggest issue. A second pressing issue is safety. We still are a somewhat dangerous industry, and if we can become safer, we can actually promote workforce development more. People would be more excited to work in an industry that is safer."

The results validated the strategy. "As discussed in previous quarters, we believe that we continue to experience the strongest market that I've seen throughout my career, excluding only the short-lived housing bubble. State transportation budgets are near record levels across our footprint. These state budgets are supported by the Federal Infrastructure Bill or IIJA."

VIII. Inflection Point #3: The IIJA Infrastructure Funding Bonanza (2021-Present)

The third major inflection point in Granite's recent history came from outside the company: a once-in-a-generation federal infrastructure bill.

"The Infrastructure Investment and Jobs Act (IIJA), also known as the Bipartisan Infrastructure Law (BIL), is a United States federal statute enacted by the 117th United States Congress and signed into law by President Joe Biden on November 15, 2021. It was introduced in the House as the INVEST in America Act and nicknamed the Bipartisan Infrastructure Bill. The act was initially a $547–715 billion infrastructure package that included provisions related to federal highway aid, transit, highway safety, motor carrier, research, hazardous materials and rail programs of the Department of Transportation. After congressional negotiations, it was amended and renamed the Infrastructure Investment and Jobs Act to add funding for broadband access, clean water and electric grid renewal in addition to the transportation and road proposals of the original House bill."

"The Infrastructure Investment and Jobs Act (IIJA), aka Bipartisan Infrastructure Law (BIL), was signed into law by President Biden on November 15, 2021. The law authorizes $1.2 trillion for transportation and infrastructure spending with $550 billion of that figure going toward 'new' investments and programs. Funding from the IIJA is expansive in its reach, addressing energy and power infrastructure, access to broadband internet, water infrastructure, and more."

For a company like Granite, positioned in highways, bridges, and civil infrastructure, the IIJA represented a structural shift in demand.

"By May 2024, the law's halfway mark, the numbers had increased to $454 billion (38 percent of the Act's funds) for more than 56,000 projects, and by the third anniversary in November 2024, they had increased to $568 billion (47 percent) to 68,000 projects, leaving 53 percent of IIJA funds unallocated but showing the administration had been accelerating funding approvals."

"He also said money from the Infrastructure Investment and Jobs Act, passed in 2021, hasn't reached its apex, which he expects to come in 2026 or 2027. 'IIJA funding continues to be strong,' Larkin said. 'I think that's pretty universal in all the markets that we're in.'"

"In recent earnings calls, heads of AECOM, WSP, Jacobs, Balfour Beatty and Granite Construction said the infrastructure act is giving their businesses a boost. 'Our [backlog] of $5.6 billion is a testament to the continued strong public and private market environment supported by the IIJA,' said Granite Construction CEO Kyle Larkin in the firm's second-quarter earnings call."

The funding environment has been particularly strong in Granite's home state. "California, our largest revenue state, the proposed 2025-2026 fiscal year transportation budget increased meaningfully in the key areas of local assistance and capital outlet projects from the 2024-2025 fiscal year forecast."

IX. Inflection Point #4: The M&A Expansion Strategy (2023-Present)

With strong cash flows, robust end markets, and a proven business model, Granite embarked on an aggressive acquisition campaign to expand its materials footprint.

"This marks the fifth and sixth companies Granite Construction has acquired in the last two years. Previous acquisitions include Mississippi material provider Dickerson & Bowen in August 2024, Tennessee-based aggregates producers and suppliers Lehman-Roberts Company and Memphis Stone & Gravel Company in December 2023, and Canadian construction aggregate producer Coast Mountain Resources in April 2023."

The crown jewel came in August 2025: "Granite today announced that it has completed two acquisitions that strengthen its vertically-integrated home markets for a combined purchase price of $710 million, subject to customary closing adjustments. Together, the acquisitions are expected to contribute approximately $425 million in revenue annually with an expected adjusted EBITDA margin of approximately 18%. This implies a blended multiple of approximately 9.2x expected adjusted EBITDA."

"These acquisitions mark another significant step forward as we continue to grow our industry–leading, vertically-integrated business. With our strong cash generation and robust acquisition pipeline, I expect to continue to grow our home markets through bolt-on transactions and expansion into new markets." Warren Paving is a leading aggregates producer with vertically-integrated operations in the Mississippi River and Gulf Coast regions, operating a network of strategically located assets, including one quarry, one sand and gravel operation, 11 aggregate yards, three asphalt plants and a fleet of 168 owned and leased barges.

"Papich Construction specializes in infrastructure projects, including road, rail and highway construction and supplies both internal projects and third-party customers with a full suite of asphalt and aggregates products, including sand, gravel and crushed rock. The acquisition includes a gravel mine, two quarries and two asphalt plants. Strengthens vertical integration with enhanced scale: The acquisitions strengthen Granite's vertical integration in both the California and Southeast markets. The barge network in the Southeast presents significant opportunities to supply additional locations as we continue to expand and work to increase volumes. Increases exposure to aggregates: These acquisitions increase Granite's aggregates reserves and resources by approximately 30 percent and annual aggregate production by approximately 5 million tons, or 27 percent."

"Then, in October, the firm bought Carson City, Nevada-based Cinderlite Trucking, which operates five aggregate yards, for an undisclosed amount. With this and other bolt-on acquisitions over the last several years, Granite has increased its aggregate production volume to 25 million tons, up from 16 million tons in 2021, Larkin said on the call."

The M&A strategy serves multiple purposes:

Geographic Expansion: The Southeast acquisitions give Granite exposure to high-growth markets outside California.

Reserve Accumulation: Each acquisition adds finite aggregate reserves that competitors can't replicate.

Margin Enhancement: Materials businesses carry higher margins than pure construction, improving the overall portfolio.

Customer Diversification: The data center boom in the Southeast creates private-sector demand to complement public infrastructure.

"Warren Paving's logistics expertise should allow us to supply materials to certain Lehman-Roberts and Dickerson & Bowen asphalt plants and positions us to expand the distribution network as we continue to grow our Southeast platform investment," Larkin said on the call. He also highlighted opportunities to supply data center jobsites in the region, which has been attractive to owners looking for cheap land, plentiful power and water and a robust labor pool. "We believe private investment will ramp up in the region, whether through data centers or other large commercial developments."

X. Current Performance & 2027 Targets

The fruits of Granite's turnaround are now visible in the financial results.

"In its third quarter of 2025, Granite Construction reported a significant increase in financial performance, with revenue rising by 12% year-over-year to $1.43 billion and net income increasing by 30% to $103 million."

"Granite Construction reported third-quarter 2025 revenue of $1.43 billion, representing a 12% year-over-year increase but missing analyst expectations of $1.51 billion by 5.3%. Despite the revenue shortfall, the company delivered strong profitability metrics with adjusted diluted EPS of $2.70, exceeding forecasts of $2.36 by 14.41%."

"Granite's adjusted EBITDA for Q3 2025 reached $216 million, a 45% increase from the prior year, while adjusted EBITDA margin expanded to 15.0%, representing a 330 basis point improvement year-over-year. More importantly, Granite achieved a construction gross profit margin of 16.5%, which the company attributed to 'improved project execution across our higher quality project portfolio.'"

"Committed and Awarded Projects (CAP) reached a record $6.3 billion, increasing by $718 million compared to the prior year. This growth in backlog provides visibility into future revenue streams and supports the company's optimistic outlook."

The materials segment has been a particular standout. "Revenue from its materials segment grew 39.1% to $270.99 million, up from $194.81 million a year earlier, according to its earnings release. Construction revenue was up to $1.16 billion, a 7.6% increase from $1.08 billion a year ago."

"Granite has secured the No. 1 ranking in Highways on Engineering News-Record (ENR) magazine's 2025 Top Contractors List for the fifth consecutive year. ENR, a leading trade publication in the construction industry, evaluates the largest public and private companies across major market sectors, highlighting the top performers in each category."

Looking forward, management has laid out clear targets:

"2025 outlook: revenue $4.35–$4.45B and adjusted EBITDA margin 11.5–12.5%."

"Granite's strong cash position, with $617 million in cash and marketable securities as of Q3 2025, provides flexibility for future acquisitions and investments."

"For 2025, our target operating cash flow margin is 9% of revenue, already at the low end of our 2027 target range of 9% to 11%."

"We expect to continue our organic revenue growth, execute on M&A, expand margins and generate consistent cash flow as we drive toward our 2027 targets. Our markets continue to be robust, as high levels of public funding and strong private investment are creating attractive opportunities for both our construction and materials segments. Against this backdrop, I believe we can meet our organic growth guidance while also growing CAP during 2025."

XI. Playbook: Business & Strategic Lessons

Granite's 125-year journey offers several enduring lessons for business operators and investors alike:

Vertical Integration as Competitive Advantage: Owning both materials production and construction services creates multiple profit points and reduces exposure to input cost volatility. Granite sells aggregates and asphalt to competitors bidding against it on construction projects—a remarkable strategic position.

The "Picks and Shovels" Strategy in Infrastructure: During gold rushes, those who sold tools often made more reliable money than those who dug for gold. Granite's materials business represents this approach—steady, recurring revenue from supplying the infrastructure boom regardless of which contractor wins specific projects.

Crisis Management Through Transparency: When the accounting fraud was discovered, Granite self-reported to the SEC within weeks. This proactive approach likely reduced penalties and accelerated the company's return to credibility.

Mega-Project Risk Management: The fraud scandal and project losses stemmed largely from large, complex fixed-price contracts with multi-year timelines. Under Larkin, Granite shifted to smaller, less complex work and "best value" contracts that reduce execution risk.

Capital Allocation in Infrastructure: With strong cash flow and an irreplaceable asset base (aggregate reserves), Granite has deployed capital into acquisitions that expand geographic reach and add to finite mineral reserves.

Riding Macro Tailwinds: The IIJA represents once-in-a-generation federal infrastructure spending. Companies positioned in highways, bridges, and public works—Granite's core competencies—are natural beneficiaries.

XII. Analysis: Competitive Position & Strategic Framework

Porter's Five Forces Analysis:

1. Threat of New Entrants: LOW Aggregate reserves are finite and irreplaceable—you cannot create new quarries. Permitting for new extraction sites is extremely difficult, often requiring decades of regulatory approvals. Heavy capital requirements for equipment and plants create additional barriers. Relationships with state DOTs and municipalities take decades to build.

2. Bargaining Power of Suppliers: MODERATE Granite's vertical integration reduces dependence on external material suppliers significantly. For non-integrated inputs like fuel and specialized equipment, the company has implemented hedging strategies to manage cost volatility.

3. Bargaining Power of Buyers: MODERATE TO HIGH Public sector clients (DOTs, municipalities) control significant project flow and often award contracts through competitive bidding. However, Granite's vertical integration and established relationships provide some pricing power, particularly in materials sales.

4. Threat of Substitutes: LOW There is no practical substitute for aggregates in road construction. While alternative materials research exists, crushed stone, gravel, and asphalt remain essential for modern infrastructure.

5. Competitive Rivalry: HIGH The construction industry is highly competitive with numerous regional and national players. "Granite Construction's competitors and similar companies include Saulsbury Industries, Duro Felguera, Skanska, Martin Marietta Materials and Tutor Perini." However, Granite's vertical integration and scale provide differentiation.

Hamilton Helmer's 7 Powers Framework:

Scale Economies: Granite benefits from scale in both materials production (spreading fixed costs over higher volumes) and construction operations (equipment utilization, overhead leverage).

Network Effects: Limited direct network effects, though geographic clustering of operations creates local market advantages.

Counter-Positioning: Granite's vertical integration model is difficult for pure-play contractors or pure-play materials companies to replicate without significant capital investment and strategic transformation.

Switching Costs: Moderate switching costs for materials customers who rely on Granite's delivery infrastructure and quality consistency.

Branding: Limited brand premium in commodity materials, though reputation matters significantly in construction contracting.

Cornered Resource: Aggregate reserves represent a genuine cornered resource—finite, irreplaceable, and increasingly difficult to permit.

Process Power: The company has developed expertise in progressive design-build and CM/GC delivery methods that allow more efficient project execution.

XIII. Key Metrics to Watch

For investors tracking Granite's ongoing performance, three KPIs deserve particular attention:

1. Committed and Awarded Projects (CAP) CAP represents Granite's project backlog—the revenue expected from executed contracts plus probable future work. This metric provides forward visibility into revenue and serves as the leading indicator of organic growth. As of Q3 2025, CAP reached a record $6.3 billion.

2. Adjusted EBITDA Margin The turnaround story hinges on margin expansion as Granite shifts its project mix toward smaller, less risky contracts and grows its higher-margin materials business. Management is targeting 11.5%-12.5% for 2025, with longer-term targets of 12%-14% by 2027.

3. Operating Cash Flow as Percentage of Revenue Cash generation validates the sustainability of reported earnings and funds the M&A strategy. The target of 9%-11% demonstrates the cash-generative nature of the business model.

XIV. Bull Case & Bear Case

The Bull Case:

Granite is positioned at the intersection of multiple favorable trends: generational infrastructure spending (IIJA), growing materials scarcity (aggregate reserves), and operational transformation (post-scandal culture change). The company has executed flawlessly on its turnaround under Larkin, expanding margins while growing the top line. The M&A strategy adds irreplaceable assets at reasonable multiples. If IIJA funding continues flowing and follow-on legislation materializes, Granite's backlog and margins could exceed current expectations.

The Bear Case:

Construction remains a cyclical, competitive, and execution-heavy business. A recession could reduce state DOT budgets and delay private construction. The incoming administration's policy priorities could affect IIJA implementation. "In January 2025, the incoming Trump administration froze selected IIJA grants." Integration risk from aggressive M&A could surface. Large project overruns—the same issue that caused the fraud scandal—could recur despite improved controls. Finally, the stock has appreciated significantly, potentially pricing in much of the turnaround.

XV. Conclusion: Building on Bedrock

When railroad engineers struck granite near Watsonville in 1871, they had no idea they'd discovered the foundation for a company that would spend the next 150 years building America's infrastructure. From A.R. Wilson's Valentine's Day incorporation to Kyle Larkin's post-scandal turnaround, Granite's story is one of adaptation, crisis, and renewal.

The company that emerged from its accounting scandal is stronger, more focused, and better positioned than the one that entered it. The shift away from mega-projects toward smaller, better-margined work represents genuine strategic learning. The aggressive M&A campaign is building an increasingly defensible materials business with irreplaceable aggregate reserves.

Yet questions remain for investors. Is the current valuation adequately discounting future growth, or has the market fully appreciated Granite's transformation? Will infrastructure spending remain robust through the current political transition? Can the company maintain execution discipline as it integrates multiple acquisitions?

What seems certain is that infrastructure remains essential—roads need repaving, bridges need replacing, and someone needs to supply the rock. For 125 years, Granite has been that someone. Under current leadership, with current market conditions, the company appears positioned to remain so for decades to come.

"Our history is California's history, and even the U.S.'s history. The impact that we have made in the communities where we have lived and worked is tremendous."

That impact continues to grow, one ton of granite at a time.

| Key Financial Metrics | FY 2024 | Q3 2025 | 2025 Guidance | 2027 Target |

|---|---|---|---|---|

| Revenue | $4.0B | $1.43B | $4.35-4.45B | Growth TBD |

| Adjusted EBITDA Margin | 10% | 15% | 11.5-12.5% | 12-14% |

| Operating Cash Flow % | 11.4% | 9%+ expected | 9% | 9-11% |

| CAP (Backlog) | $5.3B | $6.3B | Growing | -- |

| Aggregate Production | 20M tons | 25M tons | Expanding | -- |

Material Risks & Regulatory Considerations:

- SEC settlement ($12M) completed in 2022; no ongoing enforcement actions disclosed

- IIJA funding implementation subject to federal policy decisions

- Integration risk from six acquisitions in two years

- Construction project execution risk inherent in fixed-price contracts

- Cyclical exposure to public infrastructure spending

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube