Tutor Perini Corporation: Building America's Mega-Infrastructure

I. Introduction & Episode Roadmap

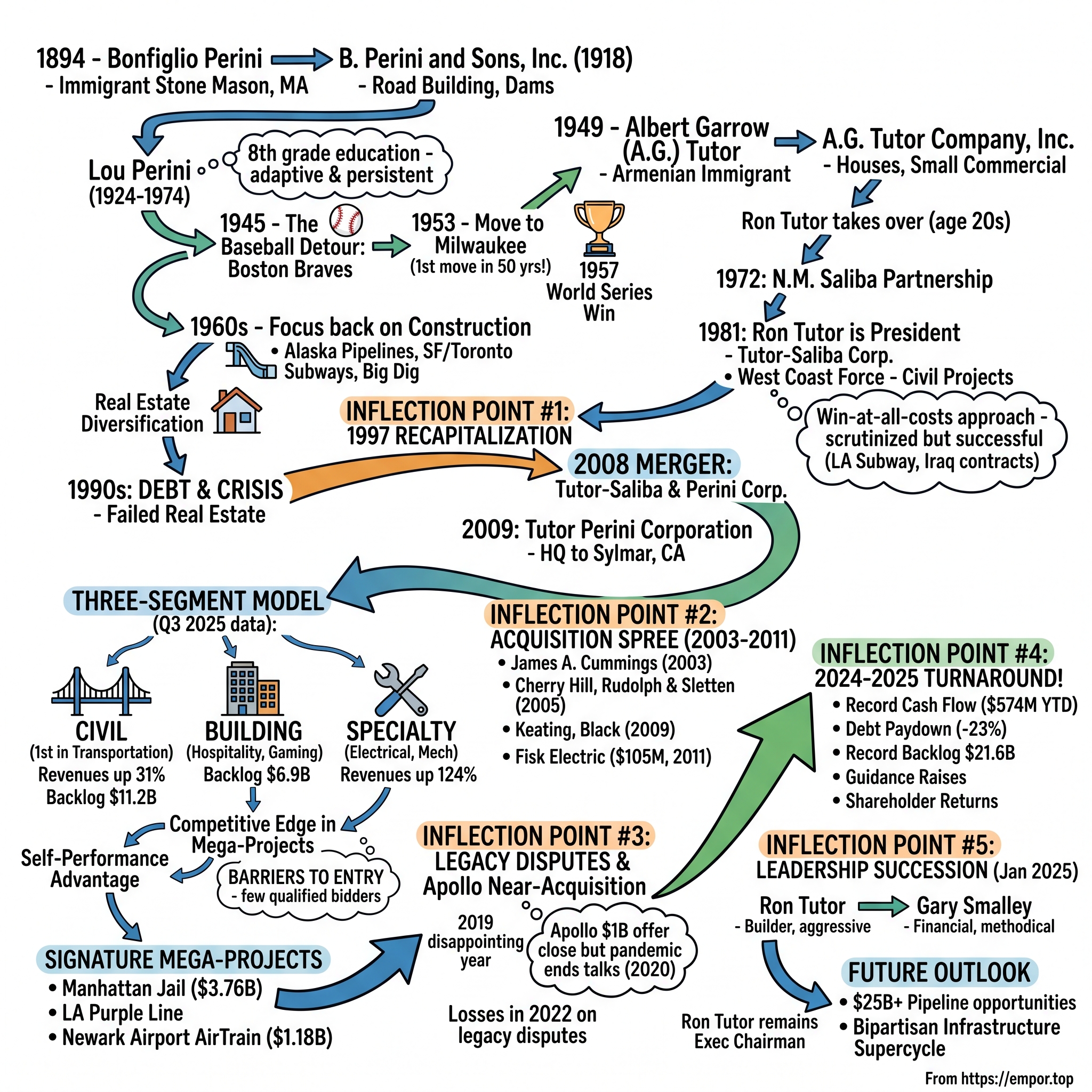

Picture a torrential monsoon evening in Mumbai, a family of four wedged precariously onto a single scooter—that's the kind of origin story you expect from a visionary founder. But the genesis of Tutor Perini Corporation unfolded across a different continent, in a different era, through the calloused hands of an Italian stonemason named Bonfiglio Perini. In 1894, in a modest storefront in Ashland, Massachusetts, Perini launched what would become one of America's most formidable construction empires—a company that has since built everything from the Los Angeles subway system to the Manhattan jail designed to replace Rikers Island.

Tutor Perini Corporation is one of the largest general contractors in the United States as a result of the merger of Perini Corporation and Tutor-Saliba Corporation in 2008. As of 2024, it reported annual revenue of approximately $4.33 billion. But that number barely hints at the transformation underway. The company now boasts a record backlog of $21.6 billion, up 54% from just a year ago—a staggering volume of contracted work that promises years of revenue visibility.

The question that drew us to this story: How does a 130-year-old company founded by an immigrant stonemason become the contractor behind America's most complex mega-projects? The company specializes in large, complex projects including highways, bridges, tunnels, mass-transit systems, military defense facilities, commercial buildings, and high-rise residential towers. Notable projects include the San Francisco Central Subway, California High-Speed Rail, and the Newark Airport Terminal One Redevelopment.

The themes that run through Tutor Perini's story are quintessentially American: immigrant entrepreneurship, strategic consolidation, the treacherous economics of mega-project construction, and the art of navigating bureaucratic labyrinths while building infrastructure that will outlast us all. It's a story of baseball ownership (yes, baseball), a near-takeover by Apollo Global Management during the pandemic, years of financial struggle, and a remarkable turnaround that has sent shares soaring in 2025.

This is not a simple tale of growth. It's a case study in how construction giants manage risk across multi-year, multi-billion-dollar projects—where a single change order can mean the difference between record profits and devastating losses. It's about the iron grip of a founding CEO who ran the company for six decades, and the leadership transition now underway. And it's about the macroeconomic tailwinds—historic infrastructure spending, bipartisan political support, crumbling bridges and roads—that make this perhaps the most favorable environment for American construction in a generation.

II. The Perini Corporation Origins: An Immigrant Story (1894-1945)

In the Lombardy region of northern Italy in 1863, a boy named Bonfiglio Perini was born into a world of stone. Bonfiglio Perini was a stone mason, born in 1863 in the Lombardy region of northern Italy. He immigrated to the United States around 1885, first arriving in New York City and relocating to Boston a few years later.

The name "Bonfiglio" translates to "good son" in Italian—an auspicious moniker for a man who would establish a construction dynasty spanning more than a century. After he married Clementina Marchesi in 1891, they briefly lived in Boston's Italian North End before departing for the rural countryside 20 miles west of Boston where there were masonry jobs in the building of dams for public-water-supply projects.

The early years were itinerant and harsh. The Perini family led an itinerant life, as Bonfiglio relocated his family periodically to new construction sites designated to provide drinking water for residents of the city of Boston. The workers' camps were "a predictably tough place, rife with tensions between Italian-Americans and African Americans and Eastern European immigrants," marked by frequent assaults and thefts.

Yet from these humble origins emerged something extraordinary. Around 1894, Bonfiglio established his own general contracting company in a storefront in Ashland. In the early years, the company built waterworks projects, such as dams and culverts, and sections of the Boston and Worcester Railway in Eastern Massachusetts.

One of his first large contracts was a 20-mile bluestone wall in the Catskill Mountains of New York, which historian Bob Steuding praised in Constructor as "a majestic project when you think about it, a giant piece of sculpture." This wasn't merely construction—it was craftsmanship at scale, the kind of work that establishes a reputation across generations.

In March 1915 Bonfiglio converted his sole-proprietor business into the Perini Construction Company, an incorporated business focused on road building. He was now a full-fledged contractor, responsible for the completion of an entire project. In 1917, they built one of the first hot-mix asphalt roads in Rhode Island.

The incorporation of B. Perini and Sons in 1918 marked a pivotal moment—the transformation from a family operation into an institution. After the First World War ended in November 1918, the family business was firmly established when Bonfiglio re-established his company as B. Perini and Sons, Inc. His three oldest sons joined him in the business.

Then, tragedy struck. When Bonfiglio died in 1924, four of his children took over running the company: Louis (age 21) became President, Joseph (age 24) became Treasurer, Ida (age 28) became Secretary, and Charlie (age 14) became Vice-President of Equipment. A twenty-one-year-old at the helm of a construction company during the Roaring Twenties—that took either remarkable courage or remarkable necessity.

The new head man proved quite adept at his job, and nobody was more dedicated; Possessing just an eighth-grade education, Lou took night classes to better understand the business world. Perini and Sons signed its first million-dollar contract around 1930 to build a stretch of the Boston-Worcester Turnpike.

During the 1920s, B. Perini & Sons worked mostly on highway projects, including relocating a section of the Boston Post Road (Route 20) in Sudbury paid for by Henry Ford and the Wayside Inn. The connection to Henry Ford wasn't coincidental—the automobile age was transforming America, and construction companies that could pave the way (literally) would prosper.

During World War II with the demand for coal great, they went into the coal strip-mining business while working in several coal belt states. The company was adapting, diversifying, following the money. A huge wartime defense contract to widen the Cape Cod Canal kept things humming.

But Lou Perini's ambitions extended beyond construction. By the mid-1940s, one of the most consequential—and unexpected—detours in American business history was about to begin.

III. Lou Perini & The Baseball Detour (1945-1974)

The Boston Braves baseball club was floundering with a losing record and a tired ballpark, handicapped by a struggling ownership group that could not afford to improve either. Lou Perini, whose own experience with the national pastime had peaked as a teenage catcher for the Ashland Dreadnaughts, saw in the situation a new landscape to conquer.

This wasn't merely a vanity acquisition. In 1945, he purchased the Boston Braves from Bob Quinn for $500,000 and the club won the National League pennant in 1948, but lost the World Series in six games.

Few men ever made a greater impact on the game without playing professionally than the construction giant who moved the Braves from Boston to Milwaukee. For a half-century from 1903 through 1952, the major leagues consisted of the same 16 teams playing in the same 11 cities.

But the economics in Boston were brutal. By 1952, the Braves had lost much fan support to the Red Sox, Boston's American League team. Boston fans were not responding to his moves to improve the lineup and Braves Field, and less than 500 season tickets had been sold for the coming 1953 season.

Perini made the move that would forever change professional sports. On March 18, 1953, Braves owner Lou Perini changed that when he took his team to Milwaukee. Baseball's future had arrived. When owner Lou Perini moved his National League baseball club from Boston to Milwaukee in March 1953, the Braves became the first major league ball club to change cities in half a century.

The gamble paid off spectacularly. In their first season the Braves drew 1,826,397 fans, a National League season record (the Braves led the National League in attendance from 1953 to 1958). The Braves shattered attendance records in their new home and won the 1957 World Series less than five years after relocating.

The move of the Braves from Boston to Milwaukee was so successful, in fact, that it paved the way for numerous other franchise shifts in the years to come. The Dodgers and Giants would follow suit, decamping from New York to California. Lou Perini, a construction executive, had revolutionized the business of American sports.

But the construction company itself had its own trajectory. The 1950s saw many changes. The company was renamed the Perini Corporation, they started a building division, and they took on projects worldwide. They worked on pipelines in Alaska and Saudi Arabia, built a hospital in Kuwait, and worked on subway systems in San Francisco and Toronto. In Massachusetts, they worked on the Callahan Tunnel, Copley Place, the Big Dig, Massachusetts Turnpike, Cape Cod Canal, and runways and buildings at Logan Airport.

By the early 1960s, however, the dual focus on baseball and construction was creating tension. At the completion of the 1962 season, he sold the franchise for $5.5 million to a Chicago group led by 34-year-old insurance executive William Bartholomay, who later moved the franchise to Atlanta for the 1966 season.

From $500,000 to $5.5 million in seventeen years—an 11x return. Lou Perini understood value creation, whether he was building highways or running a ball club.

Meanwhile, the construction company continued to evolve. As early as 1957, Perini had begun its investment in developmental property with 5,500 acres in West Palm Beach, Florida. Because of financial difficulties, all the partners withdrew except one: Louis R. Perini, Sr., president of Perini Corporation of Massachusetts. By 1988 Perini Land and Development Company had developed 35 percent of West Palm Beach with housing, commercial development, and entertainment facilities.

This real estate diversification would prove to be both blessing and curse—powering growth in the 1980s, then nearly destroying the company in the 1990s.

IV. The Tutor Family & Tutor-Saliba Rise (1949-1997)

Three thousand miles away, another immigrant construction dynasty was taking shape. His father was Albert Garrow Varjabedian, who Anglicized his name to "A.G. Tutor" in the early 1940s. Tutor is the son of Armenian immigrants. According to a profile in LA Weekly, his father's birth name was Albert G. Varjabedian. He decided to change it because Americans struggled to pronounce or spell it. The family decided on Tutor because their Armenian name meant "teacher" and the word "tutor" was close enough in meaning.

It began in 1949, when Albert G. Tutor launched a family construction business, A.G. Tutor Company, Inc. With a compelling combination of innovation and work ethic, the company found immediate success. Initially, the firm concentrated on building houses and small commercial structures, leveraging a combination of practical innovation and rigorous work standards to secure local contracts.

The trajectory changed when Albert's son joined the business. He graduated from the University of Southern California in 1963. Tutor said his career started in 1963 after he graduated from USC and went to work for his father at Tutor Perini's predecessor company. "Two years later he was diagnosed with prostate cancer and went into recovery for two years at home, which left me to take over the business, such as it was, doing less than $500,000 a year in a commercial sector."

Thrust into leadership in his mid-twenties by his father's illness, Ronald Tutor would spend the next six decades building an empire. The organization continued its dramatic growth in 1972 through a partnership with N.M. Saliba and, in 1981, when Ron Tutor took the reigns as president of the Tutor-Saliba Corporation.

He co-founded this firm with Naseeb Michael Saliba (born 11/03/1914 in Ozark, AL– d. 05/22/2008) in 1972. The partnership with Saliba brought complementary skills and the scale necessary to bid on increasingly larger projects.

The company continued to evolve into a major force, focusing on exceptional execution of massive, complicated projects. Tutor-Saliba established itself as the go-to contractor for complex civil projects on the West Coast—tunnels, transit systems, airport expansions.

Tutor's career accomplishments are staggering: "We built a significant part of the Ventura Freeway; the $200 million downtown Los Angeles Police Headquarters; over $5 billion of the L.A. subway system; the $200 million Los Angeles Central Library; numerous projects at USC, including the $150 million Ronald Tutor Academic Center and the $50 million Ronald Tutor Hall of Engineering."

The man himself defies easy characterization. He uses coarse language in interviews, angrily dismisses those who disagree with him and has seemed wholly unconcerned with a reputation for business practices that have drawn the ire and scrutiny of commentators, public officials and peers. That win-at-all-costs approach to dealmaking has helped Tutor Perini secure lucrative contracts for massive projects such as L.A.'s Red Line, military contract work in Iraq and the forthcoming 13 million-square-foot Hudson Yards development on New York's West Side.

By the mid-1990s, Tutor-Saliba was a formidable West Coast contractor. But Ron Tutor had his eye on something bigger—a struggling East Coast construction giant that might be available at a discount.

V. INFLECTION POINT #1: The 1997 Recapitalization & 2008 Merger

Perini's real estate success slowed in late 1988 as the real estate industry slumped, and by the early 1990s this portion of the company accounted for only 5 percent of corporate revenues. However, as the company incurred losses in its real estate investments, the company's construction divisions began to report record earnings.

The construction operations couldn't mask the growing real estate losses forever. By the mid-1990s, Perini Corporation was deeply in debt, weighed down by failed real estate ventures that had once seemed so promising. The company that built America's infrastructure was itself crumbling.

With an eye toward strategic growth, Ron identified a potential partner in the Perini Corporation. Established in 1894 by Bonfiglio Perini — a stonemason by trade who happened to have a remarkable instinct for construction — the company had earned significant recognition for infrastructure work over its decades in business.

Seeing an opportunity to bring together two likeminded industry powerhouses, Ron Tutor led a recapitalization of Perini Corporation in 1997. The 1997 recapitalization was the first major step—Tutor injected capital, acquired a board seat, and began steering Perini's strategic direction.

Tutor served as Director, Perini Corporation, Framingham, MA, 01/1997-05/2009, Chairman of the Board, Perini Corporation, Framingham, MA/Sylmar, CA, 07/1999-05/2009, and Chief Executive Officer, Perini Corporation, Framingham, MA/Sylmar, CA, 03/2000-05/2009.

For nearly a decade, Tutor-Saliba and Perini Corporation operated in parallel, with Ron Tutor at the helm of Perini while simultaneously running his family's company. Then came the merger that would create the modern Tutor Perini.

In 2008, the companies officially merged to create a powerful, client-focused firm — Tutor Perini Corporation. The transaction, valued at approximately $862 million, involved Perini issuing nearly 23 million shares of its common stock to Tutor-Saliba shareholders.

In May 2009, Perini shareholders voted to change the company's name to Tutor Perini Corporation. The company that had been founded in Massachusetts by an Italian stonemason would now carry the name of an Armenian-American construction magnate from California.

From 1931 to 2009, Perini was headquartered in Framingham, Massachusetts. It was headquartered in Framingham, Massachusetts until relocating to Sylmar, California in 2009. The headquarters migration signified the power shift—the West Coast had absorbed the East Coast legacy.

The strategic logic was compelling: combine Tutor-Saliba's civil construction expertise and West Coast relationships with Perini's building division and East Coast presence. The merged entity would have the scale to bid on America's largest infrastructure projects.

VI. INFLECTION POINT #2: The Acquisition Spree (2003-2011)

Ron Tutor's strategy wasn't limited to the Perini merger. Both before and after 2008, the company executed an aggressive acquisition campaign designed to build a comprehensive construction services powerhouse.

Pre-Merger Acquisitions (Perini-led):

In 2003, Perini acquired Florida-based James A. Cummings Inc. In 2005, the company acquired Cherry Hill Construction, a Maryland-based contractor, and California-based Rudolph & Sletten, Inc. In January 2008, Perini acquired Desert Heating and Cooling (later renamed Desert Mechanical), a southwestern U.S. mechanical contractor.

Post-Merger Acquisitions:

In 2009, Perini acquired Black Construction, based in Guam. In January 2009, the corporation acquired Philadelphia-based building contractor Keating Building Corporation. November 1, 2010 - Superior Gunite, a structural concrete firm headquartered in Lakeview Terrace, California. January 3, 2011 – Fisk Electric, a provider of electrical and technological services headquartered in Houston. April 4, 2011 – Anderson Companies, a general contractor headquartered in Gulfport, Mississippi.

The Fisk Electric acquisition was particularly significant—at $105 million, it was Tutor Perini's largest acquisition to date and gave the company a major presence in electrical contracting.

In January 2003, Perini acquired James A. Cummings, Inc., a Fort Lauderdale, Florida-based general contractor specializing in commercial and institutional construction, enhancing market presence in the Southeast. This move addressed limitations in organic growth amid competitive bidding environments by integrating established local expertise and backlogs.

The strategic logic behind this roll-up strategy was multi-faceted:

-

Geographic Diversification: The acquisitions gave Tutor Perini meaningful presence from Guam to Massachusetts, reducing dependence on any single regional market.

-

Vertical Integration: By acquiring specialty contractors (electrical, mechanical, HVAC), the company could self-perform critical trades rather than subcontracting them out—improving margin control and project execution.

-

Capability Expansion: Each acquisition brought specific expertise—Black Construction brought Indo-Pacific military contracts, Fisk Electric brought major electrical work, Superior Gunite brought specialized concrete capabilities.

Through strategic acquisitions of specialized construction firms, Tutor Perini has expanded its capabilities and geographic reach, positioning itself as a comprehensive construction services provider capable of executing diverse and technically challenging projects.

VII. The Three-Segment Business Model

Understanding Tutor Perini requires understanding how construction companies actually make money—and why it's more treacherous than it appears.

Tutor Perini operates through three primary segments: Civil, Building, and Specialty Contractors.

The Civil Segment: Where the Big Money Lives

The Civil segment, which generates the majority of the company's revenue, specializes in heavy civil infrastructure works such as tunnels, bridges, highways, rail systems, and mass transit facilities, employing design-build methodologies and self-performed construction to manage high-risk, technically demanding environments.

Tutor Perini Corporation (TPC), with its Civil East corporate office located in New Rochelle, NY, is ranked 1st in transportation in the United States by ENR. TPC is a leading civil and building construction company offering diversified general contracting, design-build (DB), and specialty subcontracting.

That ranking isn't merely a trophy—it represents hard-won expertise in the most technically demanding and highest-margin segment of construction. Civil infrastructure projects often span five to ten years, involve billions of dollars, and require capabilities that few competitors can match.

In Q3 2025, Civil segment revenues rallied 31% year over year to $770.2 million. Backlog for the segment increased 26% year over year to $11.2 billion, reflecting strong project wins and sustained demand.

The Building Segment: Volume and Variety

The Building Group is the recognized leader in the hospitality and gaming market, specializing in the construction of premier resorts and casinos, and has extensive experience in the government and military, education, sports, transportation and healthcare markets.

In Q3 2025, Building segment revenues were down 4% from the prior-year quarter's levels to $418.7 million. The segment's backlog decreased 2% year over year to $6.9 billion.

The Building segment has been somewhat flatter recently, but management expects it to accelerate as major projects move from preconstruction into active construction phases.

The Specialty Contractors Segment: The Integration Advantage

The specialty group offers electrical, mechanical, plumbing, HVAC, fire protection systems and pneumatically-placed concrete for jobs across all industries.

In Q3 2025, the Specialty Contractors segment's revenues increased 124% year over year to $226.5 million. Backlog for the segment increased 7% year over year to $3 billion.

That 124% revenue growth reflects both external market strength and the synergies of having specialty capabilities in-house. When Tutor Perini wins a major civil or building project, it can capture the electrical and mechanical work internally rather than paying subcontractor margins.

The company's self-performance of key trades across divisions reduces subcontractor dependencies, enhances quality control, and lowers costs by aligning incentives and minimizing interface errors—factors that provide a competitive edge in markets with limited rivals for mega-projects.

VIII. Signature Mega-Projects & The Art of Complexity

What separates Tutor Perini from dozens of other large contractors is its ability to execute the projects that others can't—or won't—touch.

The Manhattan Jail Project: Replacing Rikers Island

Tutor Perini Corporation announced that the Tutor Perini-OG Joint Venture is in the process of executing contract documents for the previously announced Manhattan Jail Project in New York. The City of New York recently held a public hearing regarding the proposed contract for this project between the New York City Department of Design and Construction and the Tutor Perini-OG JV. The anticipated contract amount is $3,764,251,168.

The contract term is expected to be 2,646 consecutive calendar days (seven years and three months) until final completion. That's over seven years of work—and seven years of revenue visibility.

The city Dept. of Design and Construction (DDC) is planning the project as part of the $15.6-billion Borough-Based Jail System program, with the aim of replacing Rikers Island Jail Complex with smaller jails in Brooklyn, the Bronx, Manhattan and Queens. DDC plans for the new 1,040-bed Manhattan jail to be built at the site of the former Manhattan Detention Complex on White Street in Chinatown.

The facility is one of four that New York City is building to replace its notorious Riker's Island prison, which is scheduled to close in 2027. In 2023, Tutor Perini also won the job to build the $2.95 billion Brooklyn jail.

The Manhattan and Brooklyn jail contracts alone represent over $6.7 billion in work for Tutor Perini—a testament to the company's ability to navigate complex urban environments and demanding public clients.

The LA Purple Line Extension

From the current terminus at Wilshire/Western, the Purple Line Extension will extend westward for about 9 miles with seven new stations. It will provide a high-capacity, high-speed, dependable alternative for those traveling to and from LA's "second downtown."

Tutor Perini is building on two sections and four stations on the Purple Line Extension: Wilshire/Rodeo, Century City/Constellation, Westwood/UCLA, and Westwood/VA Hospital. Tutor Perini is also the Design-Build Contractor for the Purple Line Extension Section 3 Tunnels contract which will add 2.56 miles of new rail to the Purple Line.

Newark Airport AirTrain Replacement

A $1.184-billion design-build contract was awarded to Tutor Perini/O&G to design and build the AirTrain at Newark Liberty International Airport in New Jersey.

Tutor Perini has completed both runway and terminal work at airports throughout the U.S., including JFK International Airport, LaGuardia Airport, Los Angeles International Airport, Harry Reid International Airport, Logan International Airport, Philadelphia International Airport, Miami International Airport, Fort Lauderdale-Hollywood International Airport, San Francisco International Airport, Oakland International Airport, Van Nuys Airport, and Pittsburgh International Airport.

The common thread across these projects: complexity that creates barriers to entry. When a transit authority or airport needs to build underground in dense urban environments, dig tunnels through geologically challenging terrain, or construct facilities that must remain operational during construction, the list of qualified bidders shrinks dramatically.

Tutor has often made the point on conference calls with investment analysts that while mega projects carry outsized risk, the firm also often encounters only two or three other bidders on major contracts that are able to provide the scale and resources called for.

IX. INFLECTION POINT #3: The Legacy Disputes & 2020 Near-Acquisition

For all its successes, Tutor Perini has faced periods of profound challenge. The years from 2019 through 2023 tested the company severely.

The Apollo Approach

Private equity firm Apollo Global Management Inc has approached Tutor Perini Corp, one of the largest U.S. general contractors, with a close to $1 billion acquisition offer, people familiar with the matter said on Friday.

Apollo's bid for Tutor Perini comes as the construction company is trying to recover from what its CEO Ronald Tutor this week called "an extremely disappointing year" in 2019.

Apollo Global Management Inc. had offered about $1 billion for the civil, building and specialty construction company. The private equity giant approached Tutor Perini with a cash bid of roughly $17 per share.

The timing was hardly coincidental. Tutor Perini recently reported a disappointing fourth quarter and FY 2019 with net losses of $86 million and $387.7 million, respectively, partially caused by a nearly $124 million charge related to the Alaskan Way Viaduct (SR99) Replacement project in Seattle and a pretax, noncash goodwill impairment charge of approximately $380 million.

Apollo saw opportunity in distress. But then came the pandemic.

The California-based company announced Wednesday night that talks to acquire it have ended "in light of continuing volatile market conditions." Tutor Perini didn't specify the other party in the negotiations, but Reuters reported earlier this year that private equity firm Apollo Global Management had offered to buy the construction company for nearly $1 billion.

The deal collapsed in May 2020, just as COVID-19 was devastating the global economy. In retrospect, Apollo's decision to walk away may have been a missed opportunity—Tutor Perini's share price has since multiplied many times over.

The Financial Struggles

The company's struggles weren't limited to one bad year. Large construction projects carry inherent risks: cost overruns, change orders, disputes with owners, weather delays, supply chain issues. When multiple projects go wrong simultaneously, the financial impact can be devastating.

The company reported losses on its 2022 revenue and earnings, a result of courtroom defeats and high-profile project cancellations, such as the $4 billion Capital Beltway project in the Washington, D.C., area.

Tutor said during the company's full-year 2022 earnings call that Tutor Perini had lost $11 billion in potential new work in the past two years, and added, "That's more low bids than we've lost in the history of the company over 50 years." Beyond those losses, the firm is also expecting to book an additional $84 million loss on its George Washington Bridge Bus Station project.

These were dark years. The company was bleeding money on legacy disputes while struggling to win new work at acceptable margins.

X. INFLECTION POINT #4: The 2024-2025 Turnaround

The turnaround that began in late 2023 and accelerated through 2024 has been nothing short of remarkable.

Record Cash Flow & Debt Paydown

Tutor Perini announced that the Company has prepaid an additional $75 million of its Term Loan B debt. With this latest paydown, Tutor Perini has now successfully deleveraged its balance sheet by a total of $430 million over the past twelve months, with $320 million of the debt reduction due to the early paydown of the Term Loan B.

Q3 2025 operating cash flow was $289 million, $574 million year-to-date. Total debt has been reduced by 23% to $413 million.

Our record operating cash flow for the first nine months of 2025 is already well in excess of last year's full-year record cash flow.

Legacy Dispute Resolutions

Look, what's really driving specialty performance is the work that we have, the non-claim resolution or dispute resolution work is just going extremely well. We're making a heck of a lot of money. The work that we're primarily doing is for Tutor Perini, but also the work that we're not doing for Tutor Perini is just doing extremely well. So we have a quarter that had very little noise from dispute resolutions, and that's what's really driving it.

The resolution of legacy disputes has been transformative. For years, the company was weighed down by claims and counterclaims on troubled projects. As those disputes settle, cash flows in and the distraction fades.

Record Backlog & New Awards

Record backlog of $21.6 billion, up 54%. In the second quarter of 2025, backlog reached $21.1 billion, up 102% year over year and nearly threefold since the end of 2022.

This backlog growth isn't just about volume—it's about quality. We continue to expect the long-duration and higher-margin nature of projects in backlog to translate into significantly higher revenue and earnings over the next several years.

Guidance Raises

Based on the Company's excellent year-to-date results in 2025 and management's increased confidence in its performance trajectory for the remainder of the year, the Company is raising its 2025 Adjusted EPS guidance, with Adjusted EPS now expected in the range of $4.00 to $4.20 (up from $3.65 to $3.95).

"Look, this is the first time we've ever raised guidance at Tutor Perini," said Smalley. "It's the first time ever, and we hope it's not the last time this year." That observation speaks volumes—a company with 130 years of history raising guidance for the first time ever.

Initiating Shareholder Returns

Tutor Perini Corporation announced Tuesday that its Board of Directors has declared a quarterly cash dividend of $0.06 per share and authorized a $200 million share repurchase program. This marks a significant shift for the construction company, which according to InvestingPro data, previously did not pay dividends to shareholders.

XI. INFLECTION POINT #5: The Leadership Succession (January 2025)

After sixty-one years in the construction industry—and seventeen years as CEO of the combined company—Ronald Tutor stepped aside in January 2025.

Tutor Perini Corporation announced today that Gary Smalley has become the Company's Chief Executive Officer and a member of its Board of Directors. Mr. Smalley, formerly President, succeeds Ronald N. Tutor who has transitioned to the role of Executive Chairman of Tutor Perini's Board of Directors after serving as Chairman and CEO since 2008.

Smalley served as Executive Vice President and Chief Financial Officer of the Company since September 2015. Before joining Tutor Perini, he held several financial management roles during nearly 24 years with Fluor Corporation (NYSE: FLR), a publicly traded multinational engineering and construction firm.

The transition was carefully orchestrated. Prior to today's announcement, Mr. Smalley served as President of Tutor Perini since November 2023, when the Company announced its formal succession plan under which he would succeed Mr. Tutor as CEO, effective January 1, 2025.

With Fluor, he served as Senior Vice President and Controller for seven years, as Group Chief Financial Officer for one of Fluor's business segments, as Vice President of Internal Audit and in several other financial operations roles in Australia, Chile, Mexico and the United States. Prior to joining Fluor, he held audit positions with Ernst & Young and J.P. Stevens and Company. Mr. Smalley holds a Bachelor of Science degree in Business Administration from the University of North Carolina at Chapel Hill and a Master of Business Administration degree from Northwestern University.

The contrast in backgrounds is notable. Ron Tutor was a builder—colorful, aggressive, deal-oriented. Gary Smalley is a financial professional—methodical, disciplined, process-focused. The transition from founder-led to professional management is a critical inflection point for any company.

Robert Lieber, the Company's Lead Independent Director, remarked, "Our Board reiterates its strong confidence in Gary's appointment to serve as Tutor Perini's new CEO and looks forward to working with him to help guide the Company into the future. We also wish to express our deep gratitude to Ron and congratulate him on his more than 61 years of outstanding career accomplishments that have greatly improved our nation's infrastructure while creating thousands of jobs with lasting economic benefits across the United States."

Ronald Tutor, who served as Chairman and CEO since 2008, will continue as Executive Chairman through 2026, concluding over 61 years of career achievements in the construction industry.

The continued involvement of Ron Tutor provides continuity during the transition—he remains available to review cost estimates and provide input on bidding strategy for major projects.

Ron Tutor's Colorful Legacy

At the Cannes Film Festival last May, Ron Tutor announced himself as Hollywood's newest movie mogul. Tutor, the construction magnate who only months earlier had led a group that acquired the storied independent film company Miramax from the Walt Disney Co. for $663 million, hosted a lavish party aboard his $65 million yacht Pegasus II, which has six suites, a gym and a screening room.

Tutor owns home in exclusive Beverly Park community he pegs at $48 million, Boeing 737 jet and $60 million yacht. He deepened involvement in Hollywood despite past troubles at Capitol Films and ThinkFilm, both pushed into involuntary bankruptcy by creditors. He led group of investors who purchased Miramax from Walt Disney Co. for $660 million.

The worst part of working into your 80s is "overcoming the aches and pains and the fact that you can't put in an 18-hour day anymore. I have only slowed down to the point where I put in a 10-hour day." The chair and chief executive said he simply loves his job and is never bored. "It is challenging and fascinating and never dull," Tutor said.

XII. Current Performance & 2025 Outlook

The financial results through Q3 2025 represent a company in the midst of transformation.

Revenue for the third quarter of 2025 was $1.42 billion, up 31% compared to $1.08 billion for the same period in 2024. Revenue: $1.42 billion, up 31% year-over-year. Earnings per share: $1.15, compared to -$1.61 in Q3 2024.

Tutor Perini Corporation reported impressive Q3 2025 earnings, significantly surpassing analyst expectations. The company posted an adjusted EPS of $1.15, far exceeding the forecast of $0.60, representing a 91.67% surprise.

Segment Performance

Civil segment revenue was $770 million, up 41%. Building segment revenue was $419 million, down slightly compared to last year, but expected to increase substantially over the coming quarters. Specialty contractor segment revenue was $226 million, up a very strong 124%.

Future Pipeline

The firm sees "well over $25 billion of upcoming bidding opportunities over the next 12 to 18 months." The largest of those include the $12 billion Sepulveda Transit Corridor in Los Angeles; the $5 billion Penn Station Transformation project in New York City; the $3.8 billion Southeast Gateway Line, also in Los Angeles; and a $2 billion replacement hospital in California.

The Company continues to have significant project bidding opportunities, particularly on the West Coast, in the Midwest, and in the Indo-Pacific region, and remains well positioned to continue winning its share of new projects over the next several years.

Multi-Year Outlook

This record backlog should enable us to produce strong double-digit revenue growth and significantly higher earnings in 2026 and 2027, while serving as a catalyst for continued strong annual cash flow as our newer projects progress through design and into construction. Our excellent performance to date combined with our confidence in the results we expect to deliver for the fourth quarter has enabled us to raise our 2025 EPS guidance for the third consecutive quarter.

Based on current projections, the Company continues to expect that Adjusted EPS for 2026 and 2027 will be significantly higher than the upper end of its increased 2025 guidance.

Macro Environment

We still do not anticipate that tariffs will have a significant impact on our business. We also do not currently foresee the risk of any of our major projects in backlog being canceled, delayed, defunded, or otherwise materially impacted by the administration's targeted funding cuts or by the recent federal government shutdown, including our work on the first phase of the California High-Speed Rail project or any of our projects in New York.

XIII. Competitive Landscape & Industry Positioning

The U.S. construction industry is highly fragmented, but at the mega-project level—where Tutor Perini competes—the field narrows considerably.

In the civil construction segment, TPC competes with major players such as Granite Construction (GVA), AECOM (ACM), Fluor Corporation (FLR), and Jacobs Solutions (J). These companies vie for large-scale infrastructure projects including highways, bridges, tunnels, and transit systems, particularly those funded by government agencies.

In the building construction segment, Tutor Perini faces competition from firms like Turner Construction (private), Skanska USA (subsidiary of Skanska AB), Clark Construction Group (private), and Suffolk Construction (private). The company also competes with Bechtel Corporation (private) and Kiewit Corporation (private) across multiple segments.

Competition in this sector is primarily based on price, technical capability, experience with similar projects, safety record, and financial strength.

Recent Comparative Performance

In the latest round of third-quarter earnings filings, large contractors Tutor Perini, Granite Construction, Fluor and Skanska reported growing revenue from their construction operations.

Fluor's total third-quarter revenue fell 18% year-over-year to $3.4 billion, driven by a $653 million recorded loss from a lawsuit ruling stemming from a Gladstone LNG project in Queensland, Australia. In that case, Fluor was ordered to pay energy company Santos the disputed project costs that Santos sued to reclaim.

The Fluor lawsuit loss illustrates the risks inherent in large-scale construction. A single project dispute can swing hundreds of millions of dollars.

Tutor Perini's Competitive Advantages

Tutor Perini's U.S.-focused, federally backed pipeline offers greater visibility and protection. Ultimately, while all three firms are navigating the same macro uncertainty, Tutor Perini's selective backlog strategy and funding stability set it apart as the most tariff-resilient of the group.

Other Civil competitors such as Fluor, KBR, Parsons, Granite, Skanska, Dragados, Kiewit Corporation etc. can earn mid-to-high single margins on larger projects if managed well. Tutor Perini is still a smaller competitor, ranked 12th in the US but 2nd overall in the transportation (roads, bridges, tunnels) segment.

XIV. Bull and Bear Case Analysis

The Bull Case

1. Unprecedented Backlog Visibility

With $21.6 billion in backlog—roughly 4x current annual revenue—Tutor Perini has multi-year visibility into its future earnings trajectory. This isn't just volume; management has emphasized that the newer projects carry higher margins than legacy work.

2. Infrastructure Supercycle

Tutor Perini has been benefiting from favorable macroeconomic tailwinds which are driving strong sustained market demand for construction services across all segments. We believe that these tailwinds will persist due to the tremendous amount of federal, state, and local level funding that are now in place and because our country has for decades and until recent years neglected to adequately fund and prioritize the types of substantial infrastructure investments being made today.

America's infrastructure has been chronically underfunded for decades. The bipartisan Infrastructure Investment and Jobs Act, combined with state and local spending initiatives, has created perhaps the most favorable environment for infrastructure construction in a generation.

3. Competitive Moat in Mega-Projects

The company's self-performance of key trades across divisions reduces subcontractor dependencies, enhances quality control, and lowers costs by aligning incentives and minimizing interface errors—factors that provide a competitive edge in markets with limited rivals for mega-projects.

When projects exceed $1 billion in scope, the competitive field shrinks dramatically. Few companies have the financial strength, bonding capacity, technical expertise, and track record to compete.

4. Deleveraged Balance Sheet

As of Sept. 30, 2025, Tutor Perini had cash and cash equivalents of $695.7 million compared with $455.1 million at 2024-end. Long-term debt, less current maturities, totaled $393 million, down from the $510 million at 2024-end.

The company has transformed from a leveraged balance sheet to a net cash position—providing flexibility for acquisitions, shareholder returns, or weathering any future downturns.

5. Leadership Transition to Professional Management

The transition from Ron Tutor to Gary Smalley brings financial discipline and process rigor that may further improve margins and reduce the volatility that has historically plagued the company.

The Bear Case

1. Project Execution Risk

Construction is inherently risky. A single troubled project can wipe out years of profits. The Alaskan Way Viaduct project, the George Washington Bridge Bus Station—these weren't anomalies, they're endemic to the industry.

2. Fixed-Price Contract Exposure

Many of Tutor Perini's contracts are fixed-price, meaning the company bears the risk of cost overruns. Inflation, labor shortages, supply chain disruptions, or unforeseen site conditions can transform profitable projects into money-losers.

3. Customer Concentration

A significant portion of revenue comes from government entities—federal, state, and local. Political changes, budget constraints, or project cancellations could impact the pipeline.

4. Cyclicality

Construction is cyclical. When economic downturns hit, infrastructure spending is often delayed or cancelled. The current infrastructure spending boom may eventually moderate.

5. Succession Risk

The company has been led by Ron Tutor for decades. While Gary Smalley has been groomed for succession, any leadership transition carries execution risk.

Porter's Five Forces Analysis

| Force | Assessment | Impact |

|---|---|---|

| Threat of New Entrants | Low | Mega-projects require bonding capacity, track record, and specialized expertise that create significant barriers to entry |

| Supplier Power | Moderate | Specialty labor and certain materials can be scarce; vertical integration mitigates this |

| Buyer Power | Moderate-High | Government clients have procurement power, but complexity limits alternatives |

| Threat of Substitutes | Low | Infrastructure must be built—tunnels can't be replaced by software |

| Competitive Rivalry | Moderate | Limited competitors at mega-project scale, but intense competition on major bids |

Hamilton Helmer's 7 Powers Assessment

Scale Economies: Moderate. Fixed costs are spread across projects, but each project is relatively bespoke.

Network Effects: Weak. Construction is not a network business.

Counter-Positioning: Present. Tutor Perini's willingness to tackle the most complex projects that others avoid creates differentiation.

Switching Costs: Moderate. Once engaged on a long-duration project, switching contractors is extremely costly and disruptive.

Branding: Present. The company's reputation for executing complex projects creates preference among sophisticated owners.

Cornered Resource: Weak. While the company has accumulated expertise, it doesn't control unique resources.

Process Power: Developing. The integration of specialty contractors and self-performance capabilities creates execution advantages.

XV. Key Metrics for Investors to Monitor

For investors tracking Tutor Perini, two metrics matter above all others:

1. Backlog and Book-to-Bill Ratio

Backlog represents contracted future work. The book-to-bill ratio (new awards divided by revenue recognized) indicates whether the company is winning enough work to sustain growth. A ratio above 1.0 means the backlog is growing; below 1.0 means it's shrinking.

Currently, Tutor Perini's book-to-bill ratio is extraordinarily strong. The backlog has grown from approximately $7 billion in late 2022 to $21.6 billion by Q3 2025—tripling in three years.

At the same time, he tried to temper Wall Street's expectations — the firm's stock is up more than 160% year to date — for ever-increasing backlog numbers. Asked by analysts if fourth quarter backlog would be higher, Smalley projected more level results. "It's probably a little bit more flattish in the fourth quarter," he said. "Lately, every quarter seems, you know, increased new record, new record, new record. We're not going to see that going forward in the short-term."

2. Operating Cash Flow Conversion

Construction companies often report earnings that differ significantly from cash flow due to the timing of billings, receivables, and project completions. Operating cash flow conversion—the percentage of reported earnings that convert to actual cash—reveals whether reported profits are real.

Tutor Perini reported record year-to-date operating cash flow of $574.4 million, with $289.1 million generated in the third quarter alone, alongside record backlog of $21.6 billion.

The company's recent cash flow performance has been exceptional, validating the earnings improvement and enabling the debt paydown and shareholder returns.

XVI. Key Risks & Regulatory Considerations

Legal and Dispute Risk

Construction disputes are endemic to the industry. The company has historically faced significant litigation costs and unexpected charges from project disputes. While management has made progress resolving legacy issues, new disputes on current projects remain possible.

Accounting Considerations

Construction accounting involves significant judgment in recognizing revenue over time on percentage-of-completion contracts. Changes in estimated costs to complete can swing reported earnings significantly. Investors should monitor "costs and estimated earnings in excess of billings" (CIE) as an indicator of potential future charges.

The Company's balance of costs and estimated earnings in excess of billings ("CIE") was $856 million as of June 30, 2025, down $91 million (or 10%) compared to the balance at the end of the first quarter of 2025 and at the lowest level it has been since the second quarter of 2017. This reduction in CIE was primarily driven by the resolution and billing of various previously disputed matters.

Federal Funding Risk

A significant portion of the pipeline depends on federal infrastructure funding. While current political support is bipartisan, future administrations could shift priorities.

Labor and Materials Inflation

Rising labor costs and materials prices can erode margins on fixed-price contracts, particularly for long-duration projects priced years before completion.

XVII. Conclusion

Tutor Perini Corporation represents a fascinating case study in American industrial capitalism: two immigrant families—one Italian, one Armenian—building construction dynasties over more than a century, eventually combining forces to create one of the nation's premier infrastructure contractors.

The company has navigated baseball ownership, real estate booms and busts, near-bankruptcy, a failed takeover, and multi-year financial struggles. Yet here it stands in late 2025 with a record backlog, pristine balance sheet, improving margins, and perhaps the most favorable infrastructure spending environment in decades.

The outlook for Tutor Perini is very bright over the next several years as we continue to benefit from favorable macroeconomic tailwinds and strong public and private customer funding that are fueling sustained market demand for our services. Finally, and just to reiterate, despite the dramatic growth we have seen this year in our stock price, I still believe we have tremendous opportunity ahead for further substantial shareholder value creation.

The leadership transition from Ron Tutor to Gary Smalley marks the end of an era—but also potentially the beginning of a new chapter of more disciplined, process-driven management.

For investors considering Tutor Perini, the core question is simple: Do you believe America will continue investing heavily in infrastructure, and can this company continue executing complex mega-projects profitably? The backlog says yes to the first question; the improving margins and cash flow suggest the answer to the second is increasingly affirmative.

The company that Bonfiglio Perini founded with his stonemason's hands in 1894 is now building tunnels under Manhattan, transit systems across Los Angeles, and jails to replace Rikers Island. The infrastructure of American civilization, built one mega-project at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube