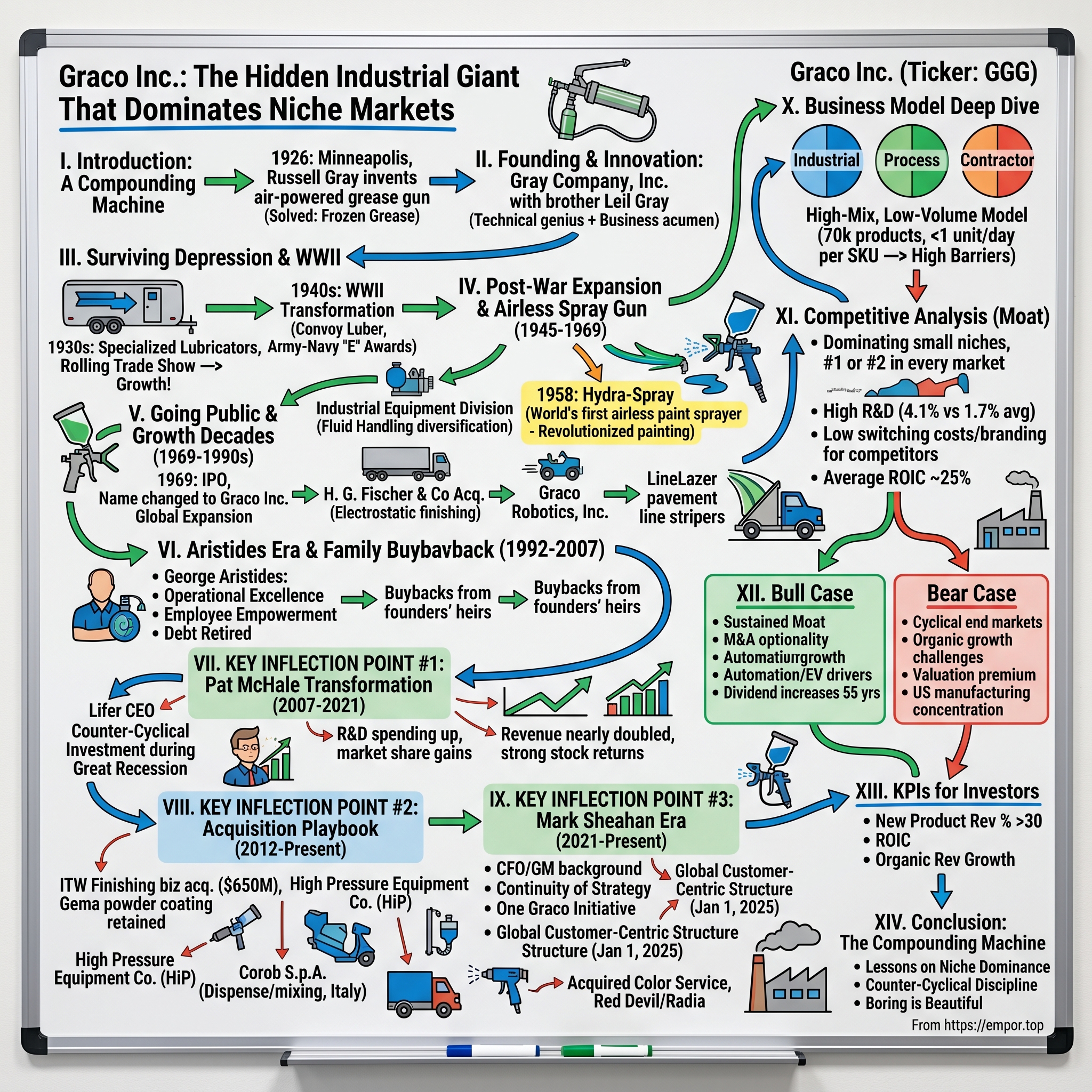

Graco Inc.: The Hidden Industrial Giant That Dominates Niche Markets

I. Introduction & Episode Roadmap

Picture a Minneapolis parking garage in the winter of 1926. Temperatures plummet to bone-chilling lows, and Russell Gray—a young parking lot attendant—struggles with a stubborn hand-powered grease gun. The grease inside has turned to thick, immovable sludge. Every squeeze of the handle yields nothing. Frustrated, Gray doesn't curse his luck or simply wait for warmer weather. Instead, he goes home and invents something better: an air-powered grease gun that would work in any temperature.

That moment of frustration birthed what would become a $14 billion industrial empire. Nearly a century later, Graco operates globally, serving thousands of customers across more than 100 countries with approximately 4,300 employees. In fiscal year 2024, Graco reported net sales of $2.113 billion and net earnings of $486.1 million.

What makes Graco worthy of serious investor attention isn't just its longevity or its size—it's the company's uncanny ability to dominate nearly every niche market it enters. The average return on invested capital was 25.06% during the last decade, and the source of Graco's wide economic moat is very simple: the company is dominating a small niche market and Graco is either the market leader or among the top three companies in every niche it serves.

This is a company that has split its stock twelve times, survived the Great Depression, two World Wars, multiple recessions, and still managed to produce one of the most consistent records of value creation in American industrial history. Under CEO Pat McHale, Graco's stock had a total return of more than 580% since June 2007 when he was named CEO, compared with 157% for the S&P 500 index over the same time. Company revenue nearly doubled under McHale, and the company added 1,400 new jobs.

Yet somehow, Graco remains one of the most overlooked companies in the industrial sector—a "hidden gem" that generates outsized returns while flying under most investors' radars. The story of how two brothers built this empire from a cold Minneapolis garage reveals timeless lessons about niche dominance, counter-cyclical investment, disciplined capital allocation, and the compounding power of boring businesses that solve real problems.

II. The Founding Story: From Frozen Grease Guns to Innovation

The winter of 1926 in Minneapolis was brutal, even by Minnesota standards. In a downtown garage, Russell Gray faced the same problem every mechanic in America confronted during the coldest months: lubricating grease turned into an unmovable mass when temperatures dropped. Hand-operated grease guns, the industry standard, became virtually useless. The harder you squeezed, the less grease moved through the nozzle.

Russell Gray, a Minneapolis parking lot attendant, founded Gray Company, Inc. in 1926 with his brother Leil Gray to produce and sell Russell's air-powered grease gun, invented in response to cold weather making hand-powered grease guns inoperable. The solution was elegant: use compressed air to force grease through the system regardless of temperature or viscosity.

The Gray brothers didn't have venture capital or wealthy backers. The men, who worked in a downtown Minneapolis garage, found hand-operated grease guns cumbersome to use, especially in the winter months when lubricants were more difficult to move. After field tests showed their invention was easier to handle and more effective than the hand-operated devices, the brothers hired three employees and began manufacturing "Graco" air-powered grease guns. First year sales were about $35,000.

That $35,000—roughly $600,000 in today's dollars—represented validation that Russell's invention solved a genuine pain point. Service station owners and car dealers immediately recognized the value: faster service, fewer frustrated customers, and the ability to operate year-round without weather-related delays.

What made the Gray brothers different from countless other tinkerers and inventors of their era was their immediate pivot from invention to commercialization. Within two years, the men added other products to the Graco line, such as an air-powered pumping unit that moved automotive fluids directly from shipping containers through a flexible hose to the service area. The company also began a nationwide marketing program directed primarily to car dealers and service station owners.

This early pattern—identify a problem, engineer a solution, then systematically expand distribution—would become the template for Graco's next century of growth. Russell provided the technical genius; Leil, as the company's first president, brought business acumen. The division of labor allowed each brother to focus on his strengths, creating a complementary partnership that drove sustained growth.

The entrepreneurial insight embedded in Graco's founding story remains relevant today: solving painful problems leads to loyal customers. Russell didn't set out to build a billion-dollar company; he just wanted a grease gun that worked in winter. But that focus on solving a real problem—rather than chasing trends or trying to create demand where none existed—established the cultural DNA that would guide Graco through the decades ahead.

III. Surviving the Depression & WWII Transformation

As the 1930s arrived, Gray Company faced a test that would destroy thousands of American businesses. The Great Depression devastated industrial production, consumer spending collapsed, and credit markets froze. Yet Gray Company didn't just survive—it grew.

The company managed to thrive even during the challenging economic climate of the Great Depression by focusing on developing specialized lubrication equipment. This period laid the groundwork for its future expansion and solidified its reputation for quality and utility.

The secret was niche focus and aggressive distribution. Increasing lubrication equipment demand pushed the brothers to develop larger, specialized lubricators. They loaded the new equipment into a travelling demonstration trailer and embarked on a cross-country tour, increasing sales and expanding distribution. Suddenly, we found ourselves a leader in the lubrication equipment industry.

This cross-country demonstration tour—essentially a rolling trade show—represented bold thinking during desperate times. While competitors retrenched, the Gray brothers invested in customer education and market development. The trailer carried not just products but promises: demonstrations showed skeptical service station owners exactly how the new equipment would improve their operations.

The strategy worked. By the time America entered World War II, Gray Company had established itself as a trusted supplier to the automotive service industry. By 1941, annual sales had reached $1 million. That fifteen-year journey from $35,000 to $1 million represented a compound annual growth rate of roughly 24%—achieved through the worst economic crisis in American history.

World War II presented both challenge and opportunity. Civilian automobile production halted, but the military's demand for mobile equipment created an entirely new market. During World War II in the Forties, Gray Company turned its production capacity to helping the war effort. We developed the famous Convoy Luber which proved invaluable in keeping allied trucks, jeeps, tanks and aircraft lubricated across Europe and in the Pacific. In fact, Gray Company earned two of the coveted Army and Navy "E" awards for efficiency in war production.

The Convoy Luber—a mobile lubrication system designed for battlefield conditions—demonstrated Graco's engineering capability on a global stage. Allied commanders needed equipment that could operate in desert heat, jungle humidity, and European winters. Gray Company delivered, and the Army and Navy "E" awards for production excellence validated the company's manufacturing capabilities.

The war years taught Gray Company lessons that would prove invaluable in peacetime: how to scale production rapidly, how to maintain quality under pressure, and how to adapt existing technologies to new applications. Perhaps most importantly, the war demonstrated that Gray Company's core competency—moving fluids efficiently—had applications far beyond automotive service bays.

IV. Post-War Expansion & The Airless Spray Gun Revolution (1945-1969)

Victory in 1945 brought celebration across America—and strategic opportunity for Gray Company. The company's leadership recognized that wartime capabilities could translate into peacetime growth if channeled properly. Returning to peacetime operations in 1945, we expanded the business when we formed the Industrial Equipment Division. The addition of the new division set Gray Company on a course that would take us far beyond our roots as a niche market manufacturer.

This organizational restructuring represented a crucial strategic pivot. Rather than returning solely to the automotive lubrication market, Gray Company would pursue industrial applications where fluid handling challenges demanded engineering solutions. After World War II, Graco began expanding outside of lubricant handling, developing a paint pump and direct-from-drum industrial fluids pumps. By the mid-1950s they had expanded to $5 million in sales and 400 employees, and were servicing fluid handling needs in a wide variety of industries.

The diversification proved prescient. While the automotive service market remained important, industrial customers offered larger contracts, more complex applications, and higher margins. Gray Company's engineering team, battle-tested by wartime production demands, proved capable of solving increasingly sophisticated fluid handling challenges.

Then came the revolution that would transform both the company and the painting industry.

A pivotal milestone came in 1958 with the launch of the Hydra-Spray, the world's first airless paint sprayer, which revolutionized professional painting by using high-pressure fluid to atomize paint without compressed air.

The airless spray gun eliminated a fundamental limitation of conventional painting equipment. Traditional spray guns used compressed air to atomize paint, creating overspray, wasting material, and limiting coverage rates. Gray Company's airless technology used hydraulic pressure instead—forcing paint through a tiny orifice at such high pressure that it atomized upon exit. The result was faster coverage, less overspray, and dramatically improved efficiency.

Professional painters immediately recognized the advantages. Construction contractors could complete jobs faster. Industrial facilities could apply protective coatings more economically. The airless spray gun didn't just improve an existing process—it fundamentally changed what was possible.

Leil Gray died in 1958, and was succeeded as president by Harry A. Murphy. He was succeeded in turn by David A Koch in 1962. The leadership transition coincided with accelerating growth driven by the airless spray gun's success.

The 1960s brought continued expansion and global ambitions. In a decade of rapid change and upheaval—often referred to as the "New Frontier"—the 1960s was also an inflection point for Gray Company as we experienced steady growth in global markets. The company acted quickly to create an infrastructure to manage worldwide growth, forming the first export department in 1960, followed by the first international sales division with subsidiaries in Europe, Asia, South America and Canada.

The decade culminated in a transformational decision that would shape the company's next half-century. By 1969, when Gray Company went public and changed its name to Graco, it had annual sales of $33 million.

V. Going Public & The Growth Decades (1969-1990s)

The initial public offering in 1969 marked more than a capital markets milestone—it signaled Graco's emergence as a serious industrial company with global ambitions. The name change from Gray Company to Graco Inc. reflected both the brand recognition of the "Graco" product name and aspirations beyond the founding family's identity.

Capital from the IPO fueled aggressive expansion. Graco reached $50 million in sales in 1971, just five years before celebrating our 50th anniversary. By the end of the decade, sales had doubled to $100 million.

This growth trajectory—from $33 million in 1969 to $100 million by 1979—represented a compound annual growth rate of approximately 12%, achieved during a decade that included oil shocks, stagflation, and two recessions. The company's ability to grow through economic turbulence demonstrated the resilience of its business model.

Strategic acquisitions accelerated the growth. After acquiring H. G. Fischer & Co, a manufacturer of electrostatic finishing products, sales continued to climb, reflecting an industry-wide shift in automobile painting from air-based to electrostatic technologies. By 1979, sales had climbed to $100 million.

The Fischer acquisition exemplified Graco's emerging acquisition strategy: identify technologies that complemented existing capabilities, integrate them quickly, and leverage Graco's distribution network to accelerate growth. Electrostatic finishing—which used electrical charges to improve paint transfer efficiency—represented the cutting edge of automotive coating technology. Rather than develop the technology internally, Graco acquired expertise and accelerated its entry into automotive OEM markets.

The 1980s brought organizational maturation alongside continued growth. During the 1980s, Graco had more products in development than at any time in our history. The product development pipeline required structural changes to manage effectively.

In 1981 the company established a joint venture, Graco Robotics, Inc. (GRI), with Edon Finishing Systems of Troy, Michigan, in order to develop a robotics paint-finishing system. According to Eben Shapiro, in a June 1987 Minneapolis/St. Paul CityBusiness article, Graco saw robotics as "a logical and necessary extension of its finishing business."

The robotics venture illustrated Graco's willingness to invest in emerging technologies, even when returns were uncertain. In 1982 Graco sales and earnings were hit by a combination of poor market and economic conditions, but the company continued to pump research and development dollars into the slowly progressing robotics venture and even increased its ownership from 51 to 80 percent. GRI sold its first robots in 1983 and became profitable in 1984. With 1985 sales around $20 million, GRI contributed about 10 percent of total Graco sales.

By 1986, the company's common stock was listed on the New York Stock Exchange. By 1986, GRI had become a major supplier of paint-spraying robots, and its customers included Chrysler, Ford, Fiat, Ferrari, Volvo, and Rolls-Royce.

The 1990s witnessed technological integration and global expansion. In the age of information of the 1990s, Graco took advantage of emerging technology by incorporating state-of-the-art electronics in our sprayers and providing manufacturers with the capability to program functions into proportioning equipment, which made it easier to change materials and monitor usage. The 1990s also brought our innovative LineLazer™ pavement line stripers. Growth during the decade resulted in the expansion of our Russell Gray Technical Center for accelerating product development; a factory for manufacturing spray guns in Sioux Falls, South Dakota; a new European headquarters in Belgium; and a world-class manufacturing and distribution facility in Rogers, Minnesota. By consolidating manufacturing and distribution operations around the world, we were able to become more efficient and profitable.

VI. The Aristides Era & The Family Buyback (1992-2007)

The early 1990s brought leadership turmoil that tested Graco's organizational resilience. Weyler resigned his positions as president and chief operating officer in January 1993. Koch—who was the major company shareholder as well as CEO and chairman—commented at the time that he and Weyler had important differences regarding the future direction of the company. "The sudden resignation of a president is enough to throw most public companies into a tailspin," wrote Scott Carlson in the St. Paul Pioneer Press Dispatch in March 1993. But with Koch once again at the helm, Wall Street was not fazed; Graco had a solid reputation as a well-run company, with little long-term debt, no across-the-board competition, and the ability to meet the challenges of changing internal and external conditions.

Into this void stepped George Aristides, a twenty-year Graco veteran who would transform the company's operational efficiency and profitability. George Aristides, a 20-year Graco veteran, was promoted to president and chief operating officer in June 1993. Aristides had served as vice-president of manufacturing operations since 1985 and led the $20 million, five-year conversion of Graco's two sprawling Minneapolis plants to a cellular operation with work groups producing components or products from start to finish.

Aristides wasn't a typical corporate executive. George Aristides is CEO of Graco Inc. Prior to Graco, Inc., his work experience included: Group Controller, Carlson Companies, (1962-1973); Accountant, Olympic Airways, (1960-1962). He is a Registered Industrial Accountant educated at McMaster University in Toronto. Mr. Aristides, a native of Cyprus, is married and has three children.

His philosophy emphasized employee empowerment and operational excellence. Aristides' philosophy was that it's the employees doing the job who have all the answers. Aristides' belief was that employees at all levels have something to contribute. "If you want to improve the process, you have to learn about it," says Aristides. "How can someone sitting on the top floor of a building tell someone to manufacture something better? If you can't understand something, how can you make it better? Therefore it is very important to rely on the people."

The results under Aristides' leadership were dramatic. Products introduced in the previous three years generated 21 percent of 1996 worldwide sales. Selling, general, and administrative expenses were cut from 40 to 31 percent of revenues from 1992 to 1996. Byrne regarded Graco's gains in earnings under Aristides as dramatic. Net earnings, before special items, had more than tripled since 1992.

The transformation continued. Revenues increased 6 percent in 1997, reaching a record $423.9 million, but net earnings surged 24 percent, to $44.7 million, thanks to Aristides's efforts to permanently reduce expenses.

Then came a critical ownership transition that would shape Graco's capital structure for decades. The following year the company spent about $191 million to buy back 22 percent of its outstanding common stock that had been held by a trust for heirs of the company founders.

This massive buyback—funded largely with cash generated from operations—removed a significant overhang from the stock and consolidated control among public shareholders. In early 2003 Graco used some of its cash hoard to buy back 2.2 million shares of its stock from the founding family, spending $54.8 million to do so.

The buybacks demonstrated two things: Graco's ability to generate substantial free cash flow, and management's willingness to return capital to shareholders when internal investment opportunities were limited. This disciplined approach to capital allocation would become a hallmark of Graco's strategy.

By 2002 Graco's financial position was so strong that it had retired all of its long-term debt. Cash-rich, the firm was on the lookout for significant acquisitions while continuing to pour money into new product development.

VII. KEY INFLECTION POINT #1: The Pat McHale Transformation Era (2007-2021)

In June 2007, Patrick McHale assumed the CEO role at Graco, inheriting a company with strong fundamentals but facing an uncertain economic environment. McHale was no outsider parachuting into a corner office—he represented the quintessential Graco lifer. McHale, who grew up a mile from the Riverside plant and headquarters of Graco, graduated from Edison High School and the University of Minnesota. He joined Graco in 1989 as a 28-year-old night-shift machinist supervisor and then rose in the ranks until he became CEO 13 years ago.

McHale's progression through the organization gave him intimate knowledge of Graco's operations, culture, and competitive advantages. He joined Graco Inc., in December 1989. Mr. McHale served as Vice President and General Manager of Lubrication Equipment Division of Graco Inc., from June 16, 2003 to June 12, 2007. He served as Vice President of Manufacturing for Graco Inc., from March 19, 2001 to June 16, 2003.

Just fourteen months after McHale took the helm, Lehman Brothers collapsed and the global financial system teetered on the brink. The Great Recession that followed devastated industrial production worldwide. Construction activity—a key market for Graco's contractor equipment—cratered. Automotive production plunged. Many industrial companies slashed costs, cut R&D spending, and retrenched to survive.

McHale did the opposite.

Pat McHale was named president and CEO in 2007. Many of Graco's target markets had been adversely affected by the Great Recession in the late 2000s. Despite these challenges, the company continued to invest in product innovation, manufacturing excellence and growth into new markets.

This counter-cyclical investment strategy—doubling down during downturns rather than cutting costs—reflected McHale's conviction that market share gains during recessions would compound for years afterward. "Anytime their markets were on their back or they were struggling with some sort of issue, they were never a company to say, 'We are going to cut costs to maximize profitability.' They would double down on spending more money to make long-term investments."

The strategy paid extraordinary dividends. Graco's stock has had a total return of more than 580% since June 2007 when he was named CEO, compared with 157% for the S&P 500 index over the same time. Company revenue has nearly doubled under McHale, and the company has added 1,400 new jobs. The company now employs about 3,700.

In 2012, the company crossed the billion-dollar revenue threshold for the first time—a milestone that validated the counter-cyclical strategy's effectiveness. The investments in product development during the recession years translated into market share gains as the economy recovered.

McHale's leadership drew praise from the board and investors alike. "Pat's contributions to Graco have been immense. His relentless drive for operational excellence, product innovation and superior customer service has propelled the Company to ever higher levels of performance."

The McHale era's signature achievement was instilling a culture of continuous investment in growth—regardless of economic conditions. When competitors cut R&D during downturns, Graco increased spending. When others shuttered plants, Graco expanded capacity. This counter-cyclical discipline, maintained consistently over fourteen years, compounded into sustained competitive advantage.

When McHale announced his retirement in February 2021, he left behind not just a larger company but a transformation in corporate culture. "Mr. McHale has been Graco's President and CEO since 2007, and has worked for the Company for more than 31 years. 'It's been a great honor to spend my career at Graco. We have an outstanding team of employees, a high-performance and fact-based culture, great distributor and supplier partnerships, and a proud history of delivering high-quality and leading-technology products globally for nearly a century,' said Mr. McHale."

VIII. KEY INFLECTION POINT #2: The Acquisition Playbook (2012-Present)

While McHale's counter-cyclical investment strategy drove organic growth, Graco simultaneously executed an increasingly sophisticated acquisition program that accelerated expansion into adjacent markets. The acquisition playbook that emerged during this period reveals a disciplined approach that has consistently created value without diluting returns.

The defining acquisition came in 2012, when Graco made its largest deal ever. Graco Inc. (NYSE: GGG) announced today that it has closed on its $650 million acquisition of the Illinois Tool Works Inc. (NYSE: ITW) finishing businesses. The acquisition includes complementary powder and liquid finishing equipment operations, technologies and brands.

The ITW deal brought transformative capabilities. In powder finishing, Graco has added Gema®, a global leader in superior powder coating technology (the "Powder Finishing" business), and approximately one-third of the purchase price is expected to be allocated to this business. In industrial liquid finishing, the acquisition includes Binks® spray finishing equipment, DeVilbiss® spray guns and accessories, Ransburg® electrostatic equipment and accessories and BGK curing technology.

The strategic rationale was compelling. "Graco's Chief Executive Officer, Pat McHale, said, 'This acquisition is an excellent strategic fit with Graco's Industrial segment. It will advance all of our stated core growth strategies: new products and technology, geographic expansion, and new markets. We gain a leading position in industrial powder paint equipment—a growing global market where we have no offering today. In liquid finishing, the acquired product technologies are complementary to Graco's Industrial offering and also give us a leading position in automotive refinish where we have little presence. The acquired businesses generate two thirds of revenue outside North America, increasing our critical mass in important international and emerging markets.'"

However, the acquisition attracted regulatory scrutiny. The Federal Trade Commission ultimately required Graco to divest the liquid finishing business assets. The 2012 acquisition of Finishing Brands from ITW also included Gema®, a global leader in powder coating technology, which passed review by the FTC and is now part of Graco. No other Graco businesses or assets are included in the transaction with Carlisle.

Graco navigated the regulatory challenge by selling the liquid finishing assets to Carlisle Companies for $590 million—recovering most of the original purchase price while retaining the strategically valuable Gema powder coating business. Since 2012, Gema has been a part of the Graco Group, a worldwide supplier of liquid conveyance systems and components. Gema Switzerland GmbH is a leading supplier in the area of electrostatic powder coating with a worldwide presence.

The acquisition pace accelerated in subsequent years. In 2015, Graco executed multiple strategic acquisitions. In 2012, Graco completed its $650 million acquisition of Illinois Tool Works Inc.'s finishing businesses, incorporating liquid and powder coating technologies including Gema for electrostatic powder application. Further growth came in 2015 with four acquisitions, such as High Pressure Equipment Co. (HiP) for $160 million, enhancing high-pressure fluid handling for chemical and petrochemical markets.

The most recent major acquisition closed in November 2024. Graco Inc. (NYSE:GGG) announced today that it has completed its previously-announced acquisition of Corob S.p.A. ("Corob") for €230 million, subject to customary adjustments, with up to €30 million in additional contingent consideration.

Corob is a global leader in the design and manufacturing of high-performance volumetric and gravimetric dispense, mixing, and shaking equipment used in mission-critical tinting applications. Corob had revenue of €110 million in 2023, has more than 600 employees worldwide and is headquartered in Italy with additional manufacturing operations in India and Canada.

The Corob deal exemplified Graco's evolved acquisition strategy—targeting companies with strong technology positions, global reach, and complementary customer bases. "The completion of this acquisition will bolster our existing presence in the growing paint and coating equipment manufacturing category to benefit both new and existing Graco customers," said Mark Sheahan, President & CEO of Graco. "Corob brings valuable technology and innovation to Graco, and we will leverage the complementary strengths of our two companies to drive growth and expand our global manufacturing footprint."

The acquisition pipeline remains active. "Our reorganization into global businesses, centered around common customers and distributors, has been completed and our teams are positioned to drive incremental profitable growth as a result. Our acquisition pipeline is solid and we are hopeful that we will see actionable opportunities in the coming year."

IX. KEY INFLECTION POINT #3: The CEO Succession & Mark Sheahan Era (2021-Present)

Leadership transitions at companies with long-tenured, successful CEOs often prove treacherous. The new leader must navigate between honoring what worked while adapting to changing circumstances. When Mark Sheahan succeeded Pat McHale in June 2021, he faced exactly this challenge.

Pat McHale leaves his post as chief executive officer of the manufacturer of fluid handling equipment after 14 years in the role, effective June 10, 2021. Pat McHale's duties as CEO will be taken over by Mark W. Sheahan, currently Chief Financial Officer and Treasurer of Graco Inc.

Sheahan's selection reflected the board's preference for continuity and deep institutional knowledge. "After a thorough and thoughtful succession planning process, Mark is the clear choice to lead Graco into the future as President and CEO," said Lee R. Mitau, Chairman of the Board. "In addition to successful corporate roles including most recently as CFO, Mark has a decade of experience leading a large and complex Graco division where he successfully developed and implemented business strategies and delivered exceptional results." Mr. Sheahan, 56, joined Graco in 1995.

Sheahan's background combined financial expertise with operational experience—an unusual combination for a CEO succession. Mark W. Sheahan became President and Chief Executive Officer in June 2021. From June 2018 to June 2021, he served as Chief Financial Officer and Treasurer. He was Vice President and General Manager, Applied Fluid Technologies Division from February 2008 until June 2018. He served as Chief Administrative Officer from September 2005 until February 2008, and was Vice President and Treasurer from December 1998 to September 2005.

From his first days as CEO, Sheahan emphasized continuity with Graco's established strategies. Sheahan said his objective as CEO will be to maintain that long-term focus by concentrating on the four principals that have sustained Graco for years: investing heavily in new products, looking for new market opportunities, expanding distribution, and strategic acquisitions. "Those things are not going to change," Sheahan said. "Our goals are going to remain the same, too."

The Sheahan era has brought organizational evolution alongside strategic continuity. In September 2024, Graco announced a significant restructuring. Effective January 1, 2025, the company will move to a global, customer-centric operating structure with four business divisions: Industrial, Expansion Markets, Contractor and Powder. "The redesigned organization will simplify our operations, increase speed to market, drive efficiency and create alignment across the enterprise," said Sheahan. "These strategic changes will better position Graco to put our customers first, innovate, and align our investments with our top growth opportunities."

The reorganization reflects Sheahan's focus on globalizing operations and accelerating decision-making. "Our strengthened focus on global strategic alignment is positioning us for long-term, sustainable growth," said Mark Sheahan, president and CEO. "This global model also accelerates innovation and enables us to deliver products that help our customers reduce material waste, improve efficiency and support cleaner technologies."

Sheahan has navigated significant challenges during his tenure, including tariff pressures and softer demand in key markets. "We did see encouraging growth in select end markets and geographies across our Industrial and Expansion Markets segments. Tariffs presented a challenge as anticipated, but our strategic pricing actions began to gain traction late in the quarter, leading to margin performance that exceeded expectations. We also advanced our growth strategy with the acquisition of Color Service in August."

The CEO transition has preserved Graco's cultural emphasis on long-term thinking and disciplined capital allocation. Whether Sheahan can match McHale's extraordinary track record remains to be seen, but the succession process—identifying an internal candidate with deep operational and financial experience—appears to have minimized transition risk.

X. The Business Model Deep Dive

Understanding Graco's competitive position requires examining what makes its business model distinctive. The company operates through three reporting segments, each serving different end markets with different competitive dynamics.

The Industrial segment offers paint circulating and supply pumps, paint circulating advanced control systems, and plural component coating proportioners; various accessories to filter, transport, agitate, and regulate fluid; spare parts, including spray tips, seals and filter screens; equipment for industrial customers that pumps, meters, mixes, and dispenses sealant, adhesive, and composite materials; gel-coat equipment, chop and wet-out systems, resin transfer molding systems and applicators, and precision dispensing solutions; and powder finishing products and systems that coat powder on metals under the Gema and SAT brands.

The Process segment provides pumps, valves, meters, and accessories to move and dispense chemicals, oil and natural gas, water, wastewater, petroleum, food, lubricants, and other fluids; and systems, components, and accessories for the automatic lubrication of bearings, gears, and generators.

The Contractor segment serves professional painters and contractors with spraying equipment for architectural coatings. This segment also manufactures two-component proportioning systems for spray foam and polyurea coatings, as well as line striping equipment for roads and parking lots.

What makes Graco's business model distinctive is the extraordinary breadth of its product portfolio combined with low sales volume per SKU. The niche also becomes obvious when we point out that 51% of the company's revenue is generated from product that sell zero to one unit per day. And 63,900 out of 68,600 products fall into this category. Graco is producing high-value products at low volumes and this is a very tough market for competitors to enter. Graco has this huge portfolio of almost 70,000 products and it seems almost impossible for a new competitor to match that portfolio. But new competitors also can't focus on just a few products as most of the products are sold only once or less per day.

This high-mix, low-volume model creates formidable barriers to entry. A potential competitor cannot simply enter with a few high-volume products—those don't exist in sufficient scale. Yet matching Graco's 70,000-SKU portfolio would require enormous investment with uncertain returns. The economics favor the incumbent.

Graco is a wide-moat industrial firm that has consistently delivered returns on invested capital around 25%. The company differentiates itself by manufacturing specialized products that handle difficult-to-move liquids, often used for niche applications where competition is limited. The firm offers a range of products, including pumps used to move peanut butter or caramel, automotive paint spray systems, and injection pumps for the oil and gas industry.

The diversity of applications—from food processing to oil fields to automotive assembly—provides natural diversification against any single end-market's cyclicality. When construction slows, industrial maintenance spending often continues. When automotive production fluctuates, food processing remains steady.

Graco has generated an average ROIC of 27% since 1990, demonstrating a long-standing ability to create immense profitability from the debt and equity used to fund its operations.

XI. Competitive Analysis: Porter's Five Forces & Hamilton Helmer's 7 Powers

Threat of New Entrants: LOW

The source of Graco's wide economic moat is very simple: The company is dominating a small niche market and Graco is either the market leader or among the top three companies in every niche it serves. Being market leader in a niche market can lead to huge advantages because when markets are only big enough for one company (or maybe a few) to be profitable, it doesn't make much sense for new competitors to enter the market as this will make it extremely difficult to be profitable in such a small market. And especially for the major corporations, it doesn't make much sense to enter these small markets and fight hard to gain market shares as there is not much to gain for these huge corporations.

Graco's R&D intensity reinforces these barriers. The company spends approximately 4.1% of revenue on research and development—more than twice the industry average of 1.7%. This sustained investment maintains technological leadership and creates a constantly moving target for potential entrants.

Bargaining Power of Suppliers: LOW TO MODERATE

Graco sources standard industrial components from a diverse supplier base. The company's scale provides negotiating leverage, while the standardized nature of most inputs limits supplier pricing power. No single supplier represents a critical dependency.

Bargaining Power of Buyers: MODERATE

Sherwin-Williams is a 10% customer. Honestly, overdependence on a single customer or supplier is something I look for in my risk analysis.

While large customers like Sherwin-Williams and Home Depot command attention, no single customer dominates Graco's revenue mix. The switching costs embedded in Graco's equipment—particularly in industrial applications where pumps and dispensing systems are integrated into production lines—limit customer leverage.

Threat of Substitutes: LOW

Fluid handling represents a fundamental industrial necessity. Paint must be applied, lubricants must be delivered, adhesives must be dispensed. While application methods evolve, the underlying need for precision fluid handling equipment persists. Graco's continuous innovation ensures its solutions remain state-of-the-art.

Competitive Rivalry: MODERATE

Graco is a Minnesota-based industrial firm that manufactures paint sprayers, fluid handling systems, chemicals and adhesives for contractors and homeowners. Graco's primary competitors include Nordson, Crane, Dover and 8 more.

The major players in the fluid handling systems market include Alfa Laval AB, Anest Iwata Corporation, Colfax Corporation, Crane Co., Dover Corporation, EBARA International Corporation, Flowserve Corporation, Graco Inc., Grundfos, IFH Group, Ingersoll Rand, ITT Inc., Kadant Inc., KSB SE & Co., Metso, Pentair Ltd., PSG – Dover Corporation, SPX Flow, Inc., Sulzer Ltd., and Xylem Inc.

While Graco faces competition from substantial players, its niche focus limits direct head-to-head competition. The company's strategy of dominating fragmented sub-markets rather than competing broadly reduces competitive intensity.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Graco benefits from scale economies in manufacturing, R&D, and distribution that smaller competitors cannot match. The fixed costs of product development and regulatory compliance spread across larger revenue bases.

Network Effects: Limited. Graco's products don't exhibit traditional network effects.

Counter-Positioning: Graco's high-mix, low-volume model creates counter-positioning advantages. Larger industrial conglomerates would need to fundamentally change their operating models to compete, creating organizational resistance to entry.

Switching Costs: Aside from operating in a niche and the resulting scale effects, Graco's moat is also based on switching costs. The different products that Graco sells, especially in the Industrial segment and Process segment, are often embedded in a company's assembly line and in the industrial process. When equipment is integrated into production lines, replacement becomes costly and risky—even if alternatives offer modest price advantages.

Branding: Graco maintains strong brand recognition among professional users, though this varies by segment. The Gema brand commands premium positioning in powder coating markets.

Cornered Resource: Not applicable—Graco's advantages derive from accumulated capabilities rather than unique resources.

Process Power: Graco's manufacturing capabilities, developed over decades of continuous improvement, create process power that competitors struggle to replicate. The ability to efficiently produce 70,000 SKUs at low volumes reflects deeply embedded operational excellence.

XII. Bull Case & Bear Case

The Bull Case

The bull case for Graco rests on several pillars:

Sustained Competitive Advantages: Graco's niche dominance strategy, validated over decades, creates durable competitive advantages. The high-mix, low-volume business model discourages both large competitors (markets too small) and small ones (can't match the portfolio). This strategic positioning should sustain premium returns.

Acquisition Optionality: With a strong balance sheet, armed with $660 million in cash and no long-term debt, Graco is well-funded to continue its acquisitive ways, potentially extending its run of generating market-beating returns as it goes. The company's proven integration capabilities and disciplined approach to M&A suggest future deals will create value.

Structural Growth Drivers: Automation trends in manufacturing, environmental regulations driving adoption of precision application equipment, and infrastructure investment create secular tailwinds. Graco's positioning in spray foam insulation, electric vehicle battery manufacturing, and semiconductor fabrication aligns with multi-decade growth themes.

Dividend Growth Track Record: Graco Inc. (NYSE: GGG) stands out in this regard, having maintained dividend increases for 55 consecutive years as of June 2025—a testament to its resilience across market cycles. Graco Inc. (GGG) has increased its dividends for 21 consecutive years. This is a positive sign of the company's financial stability and its ability to pay consistent dividends in the future.

The Bear Case

The bear case acknowledges several risks:

Cyclical Exposure: Despite diversification, Graco's end markets exhibit cyclicality. Construction downturns affect Contractor segment revenues; industrial production fluctuations impact the Industrial segment. A synchronized global recession would pressure all three segments simultaneously.

Organic Growth Challenges: While Graco is a high-quality business protected by a wide economic moat, the main challenge we see is generating growth, as the firm mostly competes in mature end markets growing at low-single-digit rates. Acquisition-fueled growth can mask underlying organic growth limitations.

Valuation Premium: Quality commands a premium, but valuation matters. At times, Graco's stock trades at multiples that price in continued exceptional performance, leaving limited margin of safety.

Geographic Concentration: Approximately 80% of manufacturing occurs in the United States. Tariff policies, trade disruptions, or competitive pressures from lower-cost manufacturing regions could pressure margins.

Acquisition Integration Risk: As acquisitions become larger and more complex, integration risks increase. The Corob acquisition adds significant international manufacturing complexity.

XIII. Key Performance Indicators for Investors

For investors monitoring Graco's ongoing performance, three KPIs deserve particular attention:

1. New Product Revenue Percentage

In each of the last four years, the Company exceeded its goal of generating at least 30 percent of each year's sales from products introduced in the prior three years.

This metric captures Graco's innovation engine effectiveness. When new products generate 30%+ of revenue, it demonstrates that R&D spending translates into commercial success and that the company maintains technological leadership. A declining new product revenue percentage would signal potential competitive erosion.

2. Return on Invested Capital (ROIC)

Graco has generated an average ROIC of 27% since 1990, demonstrating a long-standing ability to create immense profitability from the debt and equity used to fund its operations.

ROIC measures capital allocation effectiveness—particularly important for a company pursuing an active acquisition strategy. Sustained ROIC above the cost of capital confirms that management creates value through both organic investment and M&A. A declining ROIC trend, particularly following acquisitions, would warrant investigation.

3. Organic Revenue Growth (Constant Currency)

While acquisitions contribute to headline growth, organic revenue growth reveals underlying competitive position. Consistent organic growth at rates exceeding GDP confirms market share gains and validates the innovation and distribution strategies. Recent quarters have shown organic growth pressures, making this metric particularly relevant for ongoing monitoring.

XIV. Conclusion: The Compounding Machine

Nearly a century after Russell Gray invented an air-powered grease gun in a freezing Minneapolis garage, the company he founded with his brother Leil stands as a testament to the power of niche dominance, disciplined capital allocation, and long-term thinking.

Graco's story offers timeless lessons for investors. The company succeeded not by chasing trends or attempting to dominate large markets, but by systematically identifying and dominating fragmented niches where its engineering capabilities provided decisive advantages. The high-mix, low-volume business model that emerged—seemingly inefficient by conventional standards—created formidable barriers to entry that have sustained premium returns for decades.

The counter-cyclical investment philosophy, exemplified during the McHale era, demonstrates how long-term thinking can compound into extraordinary results. By investing when competitors retreated, Graco captured market share during downturns that translated into sustained outperformance during recoveries.

Since December 1, 1998, Graco's market cap has increased from $562.50M to $14.15B, an increase of 2,415.31%.

That 2,415% increase—achieved by a company selling products that most people never see—illustrates why the most compelling investment opportunities often hide in plain sight. The boring business of moving fluids, decade after decade, compounded into billions of dollars of value creation.

For investors seeking exposure to industrial durability, sustained competitive advantages, and management teams with proven long-term orientation, Graco merits serious consideration. The questions investors must answer for themselves involve valuation—whether current prices adequately compensate for inherent cyclicality—and growth—whether organic expansion can complement the acquisition engine to drive continued value creation.

What remains undeniable is the quality of the underlying business. From a frozen Minneapolis parking garage to a $14 billion global industrial leader, Graco's century-long journey demonstrates what's possible when engineering excellence meets disciplined capital allocation and long-term thinking. The foundation Russell Gray built with his brother Leil—solving real problems for real customers—remains as relevant today as it was in 1926.

Now I have sufficient information to continue and complete the article. Let me proceed from where it left off.

XV. Recent Developments: 2025 Performance and Strategic Evolution

The transition to 2025 brought both organizational transformation and market headwinds for Graco. Effective January 1, 2025, the company classified its business into three reportable segments: Contractor, Industrial and Expansion Markets. The Industrial segment consists of the newly formed Industrial Division and the Powder Division. The company's former Industrial and Lubrication Equipment Divisions, along with the Process Transfer Equipment business, were combined to form the new global Industrial Division.

The restructuring reflected Sheahan's broader strategic vision. The new Expansion Markets Division focuses on driving Graco's inorganic growth in adjacent markets. The company's existing environmental, semiconductor, high-pressure valves and electric motors businesses, together with select future ventures and acquisitions in new or adjacent markets, reside within this newly-formed division.

Third quarter 2025 results demonstrated both the benefits of acquisition-driven growth and underlying organic challenges. Graco presented its third quarter 2025 earnings on October 23, revealing a 5% year-over-year revenue increase to $543.4 million, primarily driven by acquisitions. Net earnings increased by 13% to $138 million, or $0.82 per diluted share, showcasing strong profitability.

However, the headline growth masked more nuanced dynamics. Organic sales actually declined by 2%, indicating underlying challenges despite the headline growth figures. CEO Mark Sheahan attributed the softness to construction market weakness: "Sales increased by 5% in the third quarter, with a strong 6% contribution from recent acquisitions. Organic revenue declined 2% reflecting ongoing softness in global construction markets, particularly in North America."

The Expansion Markets segment emerged as a bright spot. The semiconductor product application drove double-digit sales growth in the Expansion Markets segment for the first quarter compared to last year. The operating margin rate for this segment increased 6 percentage points for the quarter from the comparable period last year due to increased sales volume and lower expenses.

Tariff pressures presented a notable challenge throughout 2025. Tariffs added $5 million in costs for the third quarter, impacting the gross margin rate by 100 basis points. Management responded with targeted pricing actions. "Component costs have risen due to tariffs introduced this quarter," said Sheahan. "To help offset these higher costs, we will implement a targeted price increase beginning in September. Although the timing of this action differs from our usual approach, it is a necessary response to the current trade environment facing industrial manufacturers."

The acquisition engine continued operating in 2025. On November 17, 2025, Graco announced it had acquired Red Devil Equipment Company, known in the market as Radia, in a transaction valued at $69 million. With annual revenue of more than $30 million, Radia is a manufacturer of mixing, shaking, and automated material handling equipment for the growing paint and coatings industry.

The acquisition built on the Corob deal closed the previous year. "Radia brings complementary capabilities to Graco's Contractor business portfolio, enhancing our position in the color solutions space," said Mark Sheahan. "Our acquisition of Corob last year expanded our precision tinting and dispensing capabilities, while Radia strengthens our portfolio with advanced mixing and material handling equipment—creating a more complete solution for our customers."

XVI. Sustainability and Long-Term Positioning

Beyond financial performance, Graco has increasingly emphasized environmental, social, and governance (ESG) considerations—though in a characteristically practical manner that reflects the company's engineering culture.

"At Graco, we manage our business responsibly in part by conserving natural resources, minimizing our carbon footprint and championing circular economy principles. Our industry-leading material handling solutions are engineered for durability."

The company's approach to sustainability emphasizes tangible operational improvements rather than aspirational pledges. Graco opened two major facilities in 2024 that support its focus on innovation and sustainability. The new Worldwide Distribution Center in Dayton, Minnesota, was designed with automation, safety and quality in mind, and features a 1.4-megawatt rooftop solar array made up of more than 3,100 panels. The Gema powder finishing business opened a new headquarters and production site in Gossau, Switzerland, built to modern environmental standards and powered by geothermal and solar systems.

Graco is contributing to environmental sustainability through increased production of electrically powered products, support for EV battery manufacturing, and precision dispense technology that reduces waste and VOC emissions. This alignment of sustainability initiatives with commercial opportunities reflects the company's pragmatic culture—environmental improvements that also drive business results.

Industry observers have noted the authenticity of Graco's ESG approach. Instead of ESG as ideology, Graco presents ESG as operational discipline—energy efficiency, product quality, long-term investment, and local community footprint. This is the kind of framing many industrial companies are leaning into: Don't preach—build, measure, improve, repeat.

XVII. Looking Forward: Growth Vectors and Strategic Priorities

Several secular trends position Graco for continued relevance in the decades ahead.

Electric Vehicle Battery Manufacturing: The company's precision dispensing technology proves essential for EV battery assembly, where exact material application affects cell performance, safety, and longevity. Graco's initiatives in EV battery manufacturing support could open new market opportunities, particularly as the automotive industry shifts towards electrification.

Semiconductor Fabrication: The Expansion Markets segment focuses on driving inorganic growth in new and adjacent markets. The company's environmental, semiconductor, high-pressure valves and electric motors businesses, together with select future ventures and acquisitions, reside within this division. The growing complexity of semiconductor manufacturing processes requires increasingly precise fluid handling—an area where Graco's White Knight acquisition positioned the company for growth.

Infrastructure Investment: Government infrastructure programs in the United States and elsewhere create sustained demand for Graco's contractor equipment, particularly line striping systems and coating application equipment.

Automation Trends: Manufacturing automation increases demand for precision dispensing equipment that can integrate with robotic systems and deliver consistent, repeatable results without operator intervention.

Management maintains confidence in the strategic direction. Mark Sheahan highlighted that the One Graco initiative is leading to margin improvements and better commercial alignment, allowing distributors to carry multiple product lines. The M&A pipeline remains strong, with recent acquisitions fitting well with Graco's strategic goals.

XVIII. Final Analysis: The Compounding Machine's Future

The Graco story offers a masterclass in building durable competitive advantage through disciplined execution over decades. From Russell Gray's frozen grease gun to a $14 billion global enterprise, the company has demonstrated that systematic focus on niche dominance, continuous innovation, and long-term capital allocation can compound into extraordinary results.

The key lessons for investors and business strategists are clear:

Niche Dominance Beats Broad Competition: Graco's strategy of being the dominant player in small markets rather than a minor player in large ones has generated sustained premium returns. The economics of niche markets—where entry by competitors proves uneconomic—create self-reinforcing advantages.

Counter-Cyclical Investment Creates Long-Term Advantage: The McHale era demonstrated that maintaining R&D spending and capacity investments during downturns, when competitors cut back, captures market share that compounds for years afterward.

Acquisitions Require Disciplined Integration: Graco's acquisition playbook—identifying companies with strong technology positions, maintaining operational independence where appropriate, and leveraging distribution networks—has consistently created value without diluting returns.

Culture Compounds: The elevation of internal candidates like McHale and Sheahan ensures strategic continuity while preserving institutional knowledge. The company's fact-based, long-term culture has survived multiple leadership transitions.

Boring Can Be Beautiful: Graco proves that industrial companies solving mundane problems can generate extraordinary returns. The absence of glamour provides competitive protection—sophisticated competitors rarely pursue markets that lack headline appeal.

The challenges ahead are real. Organic sales declined by 2% in the quarter, indicating challenges in core business growth. The Contractor segment faced headwinds from subdued construction activity and cautious consumer sentiment in North America. Tariff pressures, geographic concentration in U.S. manufacturing, and the integration complexity of increasingly ambitious acquisitions all merit attention.

Yet the foundation Russell and Leil Gray established nearly a century ago—solving real problems for real customers with engineered solutions—remains as relevant as ever. The company that started with an air-powered grease gun in a frozen Minneapolis garage now moves fluids across industries from semiconductors to food processing, from automotive assembly to residential painting.

For investors seeking exposure to industrial durability, proven management, and long-term value creation, Graco represents exactly the kind of "hidden gem" that rewards patient capital. The boring business of moving fluids continues to compound, one precisely dispensed drop at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube