ESCO Technologies: The Phoenix from the Pentagon's Ashes

I. Introduction & Episode Roadmap

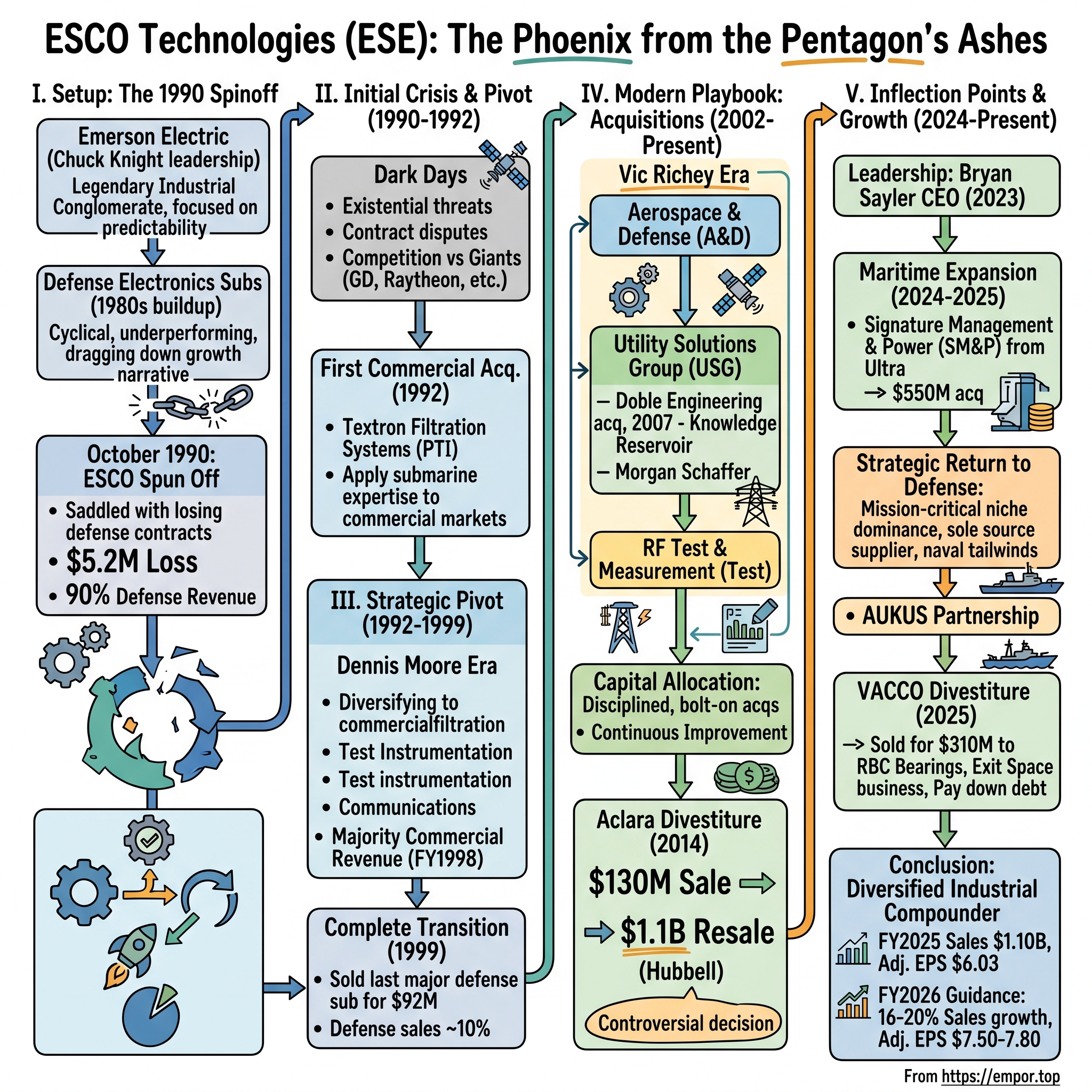

Picture a company left for dead. It's October 1990, and Emerson Electric—one of America's most respected industrial conglomerates—has just jettisoned a collection of defense subsidiaries into the cold, uncertain waters of post-Cold War America. The new entity, saddled with the clunky name ESCO Electronics Corporation, hits the public markets with a whimper rather than a bang. Profits had cratered from $36 million in 1985 to a $5.2 million loss by 1990. Two major contract disputes with the U.S. government hung over the company like executioner's blades. And the very reason for its existence—the Reagan-era defense buildup—had just ended with the fall of the Berlin Wall.

At the time of the spin-off, approximately 90% of ESCO's business was with military and defense customers—the remainder involved providing engineering services and load control products to the electric utility industry. ESCO was focused primarily on system-level defense projects, competing against large contractors such as General Dynamics, Raytheon, Northrop Grumman and Boeing.

Few observers gave ESCO much chance. Why would they? This was a company too small to compete with defense giants, too specialized to pivot easily, and too burdened by money-losing contracts to attract buyers. Emerson itself had tried to find a joint venture partner before giving up and opting for the spinoff.

Fast forward thirty-five years to December 2025, and ESCO Technologies has become something entirely different: a company with FY 2025 sales of $1.10 billion, entered orders of $1.6 billion (up 57%), record year-end backlog of $1.1 billion, and Adjusted EPS of $6.03 (up 26%). The company operates through three distinct segments: Aerospace & Defense (A&D), Utility Solutions Group (USG), and RF Test & Measurement (Test). Management guides FY 2026 to 16–20% sales growth and Adjusted EPS of $7.50–$7.80.

The big question that shapes this deep dive: How did a dying defense contractor spun off as unwanted baggage transform into a high-margin, diversified industrial compounder?

The answer involves one of the most disciplined corporate pivots in modern industrial history—a transformation executed across three CEOs over three decades. It's a story about recognizing when a market is dying, having the courage to sell crown-jewel assets at what seemed like terrible prices, and understanding that sustainable competitive advantage comes from owning mission-critical niches rather than chasing scale.

The major themes we'll explore: spinoffs as opportunity (why the cast-offs often outperform), defense-to-commercial pivots (the playbook for exiting a declining market), serial acquirers (the art of bolt-on dealmaking), and niche market dominance (why being the biggest fish in a small pond beats being a minnow in the ocean).

II. The Emerson Electric Origins & The Spinoff Setup

To understand ESCO, you first need to understand its parent. Emerson was established in 1890 in St. Louis, Missouri, as Emerson Electric Manufacturing Co. by Civil War Union veteran John Wesley Emerson to manufacture electric motors using a patent owned by the Scottish-born brothers Charles and Alexander Meston. The company's origin story is quintessentially American: immigrant entrepreneurs with technical expertise finding a financier with capital and credibility.

Two Scotland-born brothers, Charles and Alexander Meston, saw a tremendous business opportunity in developing a reliable electric motor. With the financial backing of John Wesley Emerson, a former Union army officer, judge and lawyer, they launched what would become one of America's most storied industrial companies. In 1892, it became the first to sell electric fans in the United States.

By the mid-20th century, Emerson had evolved into a diversified industrial conglomerate under the legendary leadership of Chuck Knight, who defined a strategy focused on new product and technology development, acquisitions and joint ventures, and international growth. The company became known for operational excellence and consistent earnings growth—the kind of boring, predictable performance that institutional investors loved.

But diversification has its costs. Emerson's portfolio included a collection of defense electronics businesses that had grown through the Reagan defense buildup of the 1980s. In 1983, VACCO was acquired by Emerson Electric and in 1990 six Emerson subsidiaries, including VACCO, formed ESCO.

The problem? Defense spending was cyclical, and the cycle had turned. With the Soviet Union collapsing and the Cold War ending, defense budgets faced unprecedented cuts. These subsidiaries were dragging down Emerson's consistent growth narrative.

After failing to find a joint venture partner, Emerson opted for the spinoff. ESCO Electronics Corporation (later renamed ESCO Technologies Inc.) was spun off from Emerson Electric Co. in October of 1990. On October 19, 1990, Emerson Electric Co. distributed a trust receipt for one share of ESCO Electronics Corporation for each 20 shares of Emerson Electric Co. common stock held by Emerson stockholders of record.

The message from Emerson was clear: these businesses no longer fit. They were too small, too volatile, and facing too many headwinds to warrant continued investment within a conglomerate focused on consistency. What Emerson's management couldn't know was that this unwanted baggage would eventually outperform expectations—not by succeeding in defense, but by having the wisdom to leave it behind.

For investors, the Emerson-ESCO spinoff provides an early lesson in what would become a well-documented phenomenon: spin-offs often outperform both their parents and the broader market. The key insight is that companies divested because they "don't fit" the parent's strategy often find themselves with more focused management, clearer incentives, and freedom to pursue opportunities that the parent would never have allowed.

III. The Dark Early Days: A Company in Crisis (1990-1992)

The years immediately following the spinoff were brutal. To understand just how close ESCO came to disaster, consider the numbers.

A major consideration leading to the spinoff was that Esco's after-tax profits had declined from $36.3 million in 1985 to $6.7 million in 1989 after $8.2 million of nonrecurring charges and to a loss of $5.2 million in 1990 after $13.8 million of nonrecurring charges. The company was spun off with a conservative capitalization, having only $45 million in debt compared with almost $500 million in equity. Tangible book value exceeded $25 per share.

On paper, the balance sheet looked reasonable. In reality, the company faced existential threats on multiple fronts.

Two questions regarding Esco's future worried investors. One was whether the sharp recent drop in profitability, related to money-losing defense contracts the company had taken on, would reverse. The second concerned the outcome of two pending contract disputes between Esco and the U.S. government; an adverse outcome could have cost Esco tens of millions of dollars.

The Persian Gulf War offered a momentary reprieve—or so management hoped. Surely conflict in the Middle East would boost defense spending? Instead, despite the war, military budgets continued to decline, leading to steady layoffs at ESCO throughout 1991. When the fiscal year closed in September 1991, the company posted a staggering net loss of $67.4 million, much of it related to charges for contract cancellations and cost overruns.

The competitive position was nearly impossible. At the time of the spin-off, ESCO was focused primarily on system-level defense projects, competing against large contractors such as General Dynamics, Raytheon, Northrop Grumman and Boeing. These projects required major capital investments, and had a significant amount of financial and execution risk associated with them.

Think about that competitive dynamic. ESCO was trying to compete for complex defense systems against companies with market capitalizations 50 to 100 times larger. The prime contractors had political connections, established relationships with the Pentagon, and enough financial firepower to absorb the inevitable cost overruns that plague defense programs. ESCO had none of these advantages.

Obviously there was some chance that the company would lose one or more of its contract disputes with the U.S. government. There was some possibility that a widely anticipated reduction in national defense spending would cause the company to lose profitable contracts or fail to receive new ones. There was a chance that the newly independent company, smaller than most of its competitors, would face difficulties in trying to operate apart from Emerson.

The smart money was betting on failure. Indeed Esco had been put up for sale prior to spinoff, and no buyers emerged at prices acceptable to Emerson.

Yet within this darkness were seeds of eventual success. The conservative capitalization meant the company had time. The contract disputes, which seemed like existential threats, were, in fact, tentatively settled within months of the spinoff on terms favorable to Esco. And the very desperation of the situation forced a clarity of thinking that might never have emerged under comfortable corporate parentage.

IV. The Dennis Moore Era: Strategic Pivot Begins (1992-2002)

The turning point came in October 1992 when the company's first post-spinoff CEO, Adorjan, resigned to return to Emerson.

In October 1992 Adorjan resigned to return to Emerson, where he took over as president. He was replaced as chairman and CEO at Esco by Dennis J. Moore, the company's president and chief operating officer. A 1961 graduate of the U.S. Naval Academy, Moore served as a U.S. Navy pilot in the Vietnam War. After his discharge in 1967 he went to work in the aerospace industry. Twenty years later he moved to St. Louis to become president of Electronics & Space Corp., and in 1989 became a group vice-president of Emerson's defense subsidiaries.

Moore's background was perfect for what ESCO needed: someone who understood defense, who had seen its cycles, and who recognized that the current downturn wasn't temporary but structural. He also brought something equally important—a willingness to completely reimagine the company's future.

Under Moore's guidance, Esco began to execute a diversification plan. While remaining a defense contractor, the company looked to pursue areas that fit in with its capabilities. Five areas were targeted: valves and filters; utility communications; test instrumentation; communications and antennas; and motion control.

This framework—identifying adjacent markets where defense-derived engineering capabilities could create competitive advantage—became ESCO's transformation blueprint. Moore understood something crucial: the company's competitive moat wasn't in assembling complex systems; it was in precision engineering and manufacturing of mission-critical components.

In the early 1990s ESCO's management team quickly determined that the defence marketplace was not going to be a successful place to do business long term, and began its plan of conversion. The transition from being primarily a defence contractor to a commercial and industrial supplier began in earnest in 1992 with the first commercial filtration acquisition, and was completed in 1999 with the divestiture of the last major defence subsidiary.

The first step taken in the diversification plan through external means was the $28 million September 1992 acquisition of Textron Filtration Systems, a California company that manufactured commercial and industrial filtration systems and parts used by chemical-processing, fluid-power, and aviation customers. The operation, renamed PTI Technologies Inc., was meant to complement Esco's Vacco Industries unit, which made submarine filters and valves.

The acquisition logic was elegant: take existing engineering capabilities in precision filtration (developed for submarine applications) and apply them to commercial markets where margins were more predictable and customers paid on time. Next, in March 1993, Esco bought Electro-Mechanics Company, Inc. (EMCO), in a $4.6 million deal that added to the Rantec test business. Esco then added more filter assets to PTI in December 1993 with the $7.6 million acquisition of Schumacher Filters, Ltd., a U.K. company that gave PTI a European presence. A year later Esco acquired Ray Proof North America, maker of RF shielding.

This addition helped to fuel further growth in commercial sales, which increased to 57 percent of Esco's total sales of $365.1 million in fiscal 1998.

The pace of transformation was remarkable. In just six years, ESCO had flipped from 90% defense/10% commercial to majority commercial revenues. But Moore wasn't done.

As the year came to a close the company hired J.P. Morgan to provide advice on whether to divest Systems & Electronics, Esco's largest remaining defense unit. Because business conditions were not favorable, Esco elected to hold onto the subsidiary until September 1999 when it was sold for $92 million in cash to Engineered Support Systems, Inc. By unloading Systems & Electronics, Esco completed its transformation from a company that derived 95 percent of revenues from defense contracts in 1990 to one that had defense sales in the 10 percent range.

The transformation process included the acquisition of over ten businesses and the divestiture of our major subsidiaries. ESCO believed that this change in strategic direction, via a systematic conversion of the business composition, was in the best interests of its shareholders.

The Moore era established several principles that would guide ESCO for the next three decades: acquire focused businesses in niche markets, avoid competing against giants for commodity products, and be willing to exit businesses that don't fit the strategy—even if it means taking short-term losses.

V. The Vic Richey Era & Building the Modern ESCO (2002-2022)

If Dennis Moore saved ESCO from extinction and pointed it toward commercial markets, Vic Richey built the operating model that would create decades of shareholder value.

Vic Richey is Executive Chairman of the Board of ESCO Technologies Inc., a St. Louis based company with subsidiaries operating throughout the United States and around the world. Mr. Richey began his career with the Company in 1985 prior to ESCO's spin-off from Emerson Electric in 1990. He has held a variety of positions with the Company both at the subsidiary and corporate levels, primarily in Marketing (Domestic and International) and general management. In 2001 he became President and Chief Operating Officer of ESCO. On October 1, 2002 he became Chairman, CEO and President.

He retired from his CEO and President roles effective December 31, 2022. Prior to joining the Company, Mr. Richey spent six years as a military intelligence officer in the U.S. Army. He received his undergraduate degree from Western Kentucky University and his Masters of Business Administration from Washington University.

Vic Richey is the third CEO since ESCO's spinoff from Emerson in 1990 and has served as CEO for 20 years. He has been instrumental in the portfolio transformation that created the ESCO of today — a global provider of highly engineered products and solutions focused on aerospace and defense, utility solutions and RF shielding and test.

Richey's twenty-year tenure can be understood through several strategic pillars.

Building the Three-Segment Structure

At the time of the spin-off, ESCO had a small Filtration/ Fluid Flow business which served the defence and aerospace market. In 1990, this business had approximately $15 million in sales. ESCO management targeted this segment as its first growth platform; through acquisitions and supported by solid organic growth, this business segment generated approximately $175 million in sales in 2005 and diversified out of the defence market by serving automotive, medical, aerospace and industrial markets.

A similar approach was taken in the RF Shielding & Test segment. What began as a $20 million business serving a small portion of the defence market is today a $130 million provider of sophisticated products and services to the electronic, wireless, automotive and aerospace markets. ESCO is the market share leader, and manufactures products and provides services around the world in support of its broad customer base.

Since 1993, ETS-Lindgren has been part of the ESCO Technologies' (NYSE ESE) portfolio. ETS-Lindgren is a multinational organization created over several decades through a combination of organic growth and strategic mergers of industry leaders in RF, EMC, MRI, Acoustic and Wireless test and measurement. The company was officially formed in 1995 by joining a number of leading companies including EMCO (The Electro-Mechanics Company), Rantec and Ray Proof, to create EMC Test Systems (ETS) in Austin, Texas.

The Doble Acquisition: Building Utility Solutions

A defining transaction came in December 2007 with the acquisition of Doble Engineering Company. ESCO Technologies Inc. today announced that it has completed its $319 million acquisition of Doble Engineering Company. Doble, headquartered in Watertown, Massachusetts, is a worldwide leader in providing high-end, diagnostic test solutions for the electric utility industry.

Doble's annual revenue and EBIT for the trailing 12 months ended September 30, 2007 was approximately $80 million and $24 million, respectively. The acquisition is expected to be accretive to ESCO's earnings per share in fiscal 2008, excluding amortization of intangible assets.

Founded in 1920, Doble pioneered the design and manufacture of the standard high voltage insulation diagnostic test. The company's crown jewel was its "Knowledge Reservoir" of over 25 million apparatus test results—a database that gave Doble irreplaceable institutional knowledge about how power equipment ages and fails.

Vic Richey commented, "We are very excited about completing this acquisition and the immediate financial impact it will have on our operations. Doble supplements our commitment to the utility industry and allows us to participate more meaningfully in support of the Intelligent Grid. As part of our Communications segment, Doble is expected to provide consistent sales revenue which will help offset the somewhat cyclical nature of AMI spending."

The Operating Philosophy

Under Richey's leadership, ESCO developed a distinctive approach to capital allocation: acquire businesses with defensible market positions, invest in engineering capabilities, and optimize operations through continuous improvement. The company avoided large, transformational deals in favor of disciplined bolt-on acquisitions.

Under Richey's leadership, ESCO has built a strong foundation with a well-tested operating model and three profitable business segments serving diverse end-markets.

"It's been a privilege leading ESCO Technologies for the past 20 years, and I couldn't be prouder of what we've accomplished in building a customer-centric market leader with some of the deepest and broadest engineering expertise and technology-driven products and services across our industries," said Richey.

VI. Inflection Point #1: The Aclara Divestiture (2014)

One of the most important—and controversial—decisions of the Richey era came in 2014 with the sale of Aclara.

ESCO Technologies Inc. today announced that it has signed an agreement to divest Aclara Technologies LLC to an affiliate of Sun Capital Partners, Inc. The gross cash proceeds from the transaction are expected to be approximately $150 million, comprised of a $130 million purchase price plus approximately $20 million in cash related to specific Aclara receivables retained by ESCO.

For the Quarter ending March 31, 2014, the Company expects to recognize in Discontinued Operations a net book loss of approximately $50 million on the sale of Aclara.

A $50 million loss on a sale? Aclara was ESCO's smart metering business—exactly the kind of "intelligent grid" technology that seemed poised for explosive growth. Why would management sell at what appeared to be a depressed price?

Vic Richey commented, "This agreement creates an exciting opportunity for ESCO. After closing, and essentially debt free, ESCO will be a more strategically focused, higher margin business with a much steadier and predictable growth profile. This divestiture presents an improved outlook of our future and further enhances our ability to increase shareholder value."

The strategic logic was subtle but important. Aclara's core business in smart metering has slowed in recent years as the North American market experienced a downturn. The smart meter market was becoming commoditized, with utilities increasingly focused on price rather than differentiated features. ESCO's competitive advantage lay in engineering excellence, not low-cost manufacturing.

ESCO Technologies Inc. today announced that it has completed the previously announced sale of Aclara Technologies LLC to an affiliate of Sun Capital Partners, Inc. The divestiture generated approximately $150 million of gross cash proceeds that will be applied to pay down a significant portion of the Company's outstanding debt under its revolving credit facility. The Company has over $600 million of available liquidity under its existing credit facility to support its strategy of profitable organic growth, accretive acquisitions around its existing core businesses, and opportunistic repurchases of outstanding shares. Vic Richey, ESCO's Chairman and Chief Executive Officer, commented, "Completing the sale of Aclara creates an exciting opportunity for ESCO and our shareholders both today and for the future."

The Aftermath: Did ESCO Leave Money on the Table?

In 2014, Sun Capital acquired the company from ESCO Technologies for an upfront purchase price of $130 million. The firm subsequently sponsored four add-ons to the Aclara platform and helped quadruple the company's EBITDA during the investment period.

Hubbell Incorporated today announced that it has entered into a definitive agreement to acquire Aclara Technologies LLC, an affiliate of Sun Capital Partners, Inc. for approximately $1.1 billion in an all-cash transaction.

Read that again: ESCO sold for $130 million, Sun Capital executed a rollup strategy with four acquisitions, and Hubbell bought the combined entity for $1.1 billion less than four years later.

Was this a mistake? The math certainly looks painful. But several considerations complicate the analysis:

First, the $1.1 billion Aclara that Hubbell acquired was a different company than what ESCO sold. Sun Capital's add-on acquisitions fundamentally changed the scale and scope of the business.

Second, the smart meter market's competitive dynamics remained challenging. ESCO would have needed to either execute the same rollup strategy or accept lower margins in an increasingly commoditized market.

Third, the proceeds from the Aclara sale gave ESCO the financial flexibility to pursue acquisitions in its core segments—businesses with better margin profiles and more defensible competitive positions.

Whether ESCO made the right call remains debatable. What's undeniable is that the decision reflected a consistent philosophy: focus on high-margin, defensible niches rather than chasing scale in commoditizing markets.

VII. The Modern Playbook: Acquisitions & Portfolio Optimization (2015-2024)

Following the Aclara divestiture, ESCO refined its acquisition strategy around bolt-on deals that enhanced existing segment capabilities.

The company's acquisition pace accelerated. The most active year was 2016, with four acquisitions. The approach was consistent: target businesses with strong engineering capabilities, defensible market positions, and opportunities for margin improvement under ESCO's operating model.

Q4 organic sales increased $23 million (8.5 percent) and the MPE acquisition contributed $3 million (1.0 percent) of revenue in the quarter. FY 2024 Sales increased $71 million (7.4 percent) to $1.03 billion compared to $956 million in FY 2023. Organic sales increased $61 million (6.4 percent) and the MPE acquisition added $10 million (1.0 percent) of revenue growth for the full year.

The MPE Acquisition (November 2023)

ESCO's most recent pre-SM&P acquisition was MPE, a UK-based manufacturer of high-performance EMC/EMP filters and capacitor products. Founded in 1925 and located in Liverpool, MPE brought additional capabilities to the Test segment while providing a stronger European manufacturing footprint.

Building Scale Through Discipline

Unlike many serial acquirers that pursue transformational deals, ESCO's approach resembled what investors call "programmatic M&A"—a steady cadence of smaller acquisitions that compound value over time. This discipline showed in several ways:

- Target companies were typically in adjacent markets where ESCO understood the competitive dynamics

- Deal sizes remained manageable relative to ESCO's balance sheet capacity

- Integration followed a consistent playbook focused on operational improvement rather than cost synergies

- Acquisitions enhanced segment leadership rather than diversifying into new categories

The results spoke for themselves. Over the last five years, ESCO grew its sales at a solid 9.7% compounded annual growth rate.

VIII. Inflection Point #2: The SM&P Acquisition & Naval Expansion (2024-2025)

The biggest deal in ESCO's history came in 2024-2025 with the acquisition of Signature Management & Power (SM&P) from Ultra Maritime.

ESCO Technologies Inc. today announced that it has agreed to acquire the Signature Management & Power business of Ultra Maritime for a purchase price of $550 million. The transaction will be funded through cash on hand and incremental debt, with committed financing in place.

Signature Management & Power is a well-established, long-standing provider of mission-critical signature and power management solutions for submarines and surface ships for the US and UK naval defense markets. The Business is well positioned to benefit from increasing global naval defense spending as the US and its allies upgrade aging naval defense programs. The Business' Signature Management and Power Management product lines and their deep engineering capabilities are highly complementary to ESCO's current naval programs.

Signature Management offers solutions for surface ships and submarines that provide magnetic and electric field countermeasures to prevent underwater mine and sensor detection. Power Management provides innovative and highly-engineered motors that drive critical ship propulsion systems with an ultra-quiet design ensuring low vibration levels to increase stealth capabilities.

The Business is headquartered in Long Island, New York, operates out of four facilities based in the US and the UK, and has approximately 410 employees. Signature Management & Power will become part of ESCO's Aerospace & Defense (A&D) segment and is expected to have approximately $175 million of revenue in calendar year 2024, with Adjusted EBITDA margins in excess of A&D segment margins.

Why This Acquisition Made Strategic Sense

The SM&P deal represented ESCO's strategic return to defense—but with important differences from the 1990 business mix:

SM&P is an established, long-standing provider of mission-critical signature and power management solutions for the US and UK naval defense markets. Their sole source product offerings will add significant scale to ESCO's Navy businesses, providing increased content on US Navy submarine and surface ship programs and expansion into vital UK and AUKUS navy platforms.

The key phrase is "sole source." Unlike the competitive, fixed-price defense contracts that nearly destroyed ESCO in 1990-1992, SM&P's products are mission-critical components where ESCO becomes the only qualified supplier. This dramatically changes the customer relationship and margin profile.

This acquisition supports ESCO's long-term objective of expanding our leadership positions in our high-growth end-markets. SM&P is well-positioned to benefit from increasing global naval defense spending as the US and its allies upgrade their aging naval defense programs.

On April 28, 2025, ESCO Technologies Inc. today announced that it has completed the acquisition of the Signature Management & Power (SM&P) business of Ultra Maritime for a purchase price of $550 million in cash.

The timing aligned with several secular tailwinds: the AUKUS defense partnership between Australia, UK, and US; increased global naval spending amid geopolitical tensions; and an aging U.S. submarine fleet requiring modernization.

IX. Inflection Point #3: The VACCO Divestiture (2025)

Within months of closing SM&P, ESCO executed another portfolio transformation move—selling VACCO Industries, one of the original subsidiaries from the 1990 spinoff.

ESCO Technologies Inc. today announced that it has entered into a definitive agreement to sell VACCO Industries (VACCO) to RBC Bearings Incorporated, an international manufacturer and marketer of highly engineered precision bearings and products, headquartered in Oxford, Connecticut. The Company expects to finalize the transaction upon receipt of certain customary regulatory approvals with expected gross cash proceeds of $310 million subject to typical post-closing adjustments. A sizable book gain is expected on the transaction, with a plan to use the net proceeds for paying down debt incurred in connection with the Maritime acquisition.

Last August, the Company announced a strategic review of the VACCO business and the resulting divestiture supports ESCO's long-term strategy to focus its portfolio on core high-growth end-markets.

In July 2025, RBC Bearings Incorporated (NYSE:RBC) has successfully completed its previously announced acquisition of VACCO Industries from ESCO. Today, VACCO is a part of RBC Bearings family!

The Company completed this divestiture on July 18, 2025. The Company received net proceeds from the sale of approximately $270 million and recorded a $172.6 million after-tax gain on the sale in the fourth quarter of 2025.

For the 12-month period ending March 31, 2025, VACCO generated revenue of approximately $118 million.

The Strategic Logic

The sale of VACCO represents a strategic shift for the Company to exit the Space business. In July 2025, we completed the sale of our former A&D subsidiary VACCO Industries (VACCO) for net sales proceeds of approximately $270 million. The sale was made as part of our strategic portfolio analysis, which is focused on positioning us to serve high-growth markets that have high margin potential.

The VACCO divestiture illustrated ESCO's disciplined approach to portfolio management. Despite VACCO's heritage as one of the original 1990 spinoff businesses, management recognized that the space segment faced different growth dynamics than ESCO's naval and commercial aerospace businesses. By selling VACCO and using proceeds to pay down SM&P acquisition debt, ESCO optimized its portfolio around the fastest-growing, highest-margin opportunities.

VACCO has been a part of ESCO since its formation in 1990 and is a key supplier of highly-technical mission-critical solutions. Bryan Sayler, Chief Executive Officer and President, commented, "We view this transaction as a great outcome for all and are confident that VACCO and its dedicated management team and employees are positioned for a positive future with RBC Bearings."

X. The Business Today: Three Segments Deep Dive

ESCO today operates as a global provider of highly-engineered products and solutions to diverse and growing end-markets that include the defense, aerospace, space, wireless, consumer electronics, healthcare, automotive, electric utility, and renewable energy industries. The company consists of three technology-driven business segments – Aerospace & Defense, Utility Solutions Group, and RF Test & Measurement.

Aerospace & Defense (A&D)

The A&D segment has become ESCO's largest and fastest-growing business following the SM&P acquisition. Visit the Crissair, ESCO Maritime, Globe, Mayday, PTI, and Westland websites.

The segment designs and manufactures specialty filtration products, including hydraulic filter elements and fluid control devices used in commercial aerospace applications; filter mechanisms used in micro-propulsion devices for satellites; and custom designed filters for manned aircraft and submarines. With the SM&P acquisition, it now also designs, develops, and manufactures elastomeric-based signature reduction solutions and power management systems for the U.S. and UK Navy.

The $137.7 million, or 40.4%, increase in net sales in 2025 as compared to 2024 was mainly due to a $94.1 million increase in navy revenues and a $39.8 million increase in commercial aerospace revenues, partially offset by a $5.2 million decrease in defense aerospace revenues. By subsidiary, the $137.7 million increase in net sales in 2025 as compared to 2024 was due to an $8.1 million increase in net sales at PTI, a $13.3 million increase in net sales at Globe, a $19.6 million increase in net sales at Crissair, a $1.5 million increase in net sales at Mayday and a $95.2 million net sales contribution from the current year acquisition of Maritime.

The $39.3 million, or 45.8%, increase in EBIT in 2025 as compared to 2024 was primarily due to leverage on higher sales volumes and price increases at Mayday, PTI, Crissair and Globe and the contribution from the current year acquisition of Maritime partially offset by a decrease in EBIT due to inflationary pressures. EBIT in 2025 was negatively impacted by $4.5 million primarily consisting of inventory step-up charges and UK stamp duty charges related to the Maritime acquisition.

Utility Solutions Group (USG)

Our Utility Solutions Group (USG) provides industry-leading diagnostic, protection testing, and condition monitoring equipment, consulting and laboratory testing services, and data analytics vital for maintaining electric grid reliability and renewable energy project development. Visit the Doble, Morgan Schaffer, NRG Systems, isa, Techimp, and Phenix websites.

Doble develops, manufactures and delivers diagnostic testing solutions that enable electric power grid operators to assess the integrity of high-voltage power delivery equipment. NRG designs and manufactures decision support tools for the renewable energy industry, primarily wind and solar.

The $10.9 million, or 3.0%, increase in net sales in 2025 as compared to 2024 was mainly due to a $17.8 million increase in net sales at Doble mainly due to higher shipments of offline and protection testing products and service revenue, partially offset by a $7.0 million decrease in net sales at NRG driven by lower shipments of solar and wind products due to renewables market weakness.

The $8.8 million, or 10.2%, increase in EBIT in 2025 as compared to 2024 was mainly due to leverage on higher sales volumes at Doble with a favorable product mix and price increases, partially offset by lower sales at NRG and inflationary pressures. EBIT in 2025 was negatively impacted by $0.4 million of restructuring charges (mainly severance).

The Utility Solutions Group achieved record orders of over $100 million and a 29% adjusted EBIT margin, indicating strong operational performance.

RF Test & Measurement (Test)

Our RF Test & Measurement (Test) business is an industry leader in designing and manufacturing products and systems to measure and control RF and acoustic energy for research and development, regulatory compliance, medical, and security applications. Test supplies a broad range of turnkey systems, including RF test facilities and measurement systems, acoustic test enclosures, RF and magnetically shielded rooms, and secure communications facilities. Visit ETS Lindgren, and MPE website.

ETS-Lindgren is an industry leader in providing its customers with the ability to identify, measure and control magnetic and electromagnetic energy.

The Test business experienced a 10% revenue growth in the fourth quarter, with a 25% increase in orders over the prior year, showing a rebound in activity across its markets.

The $5.5 million, or 19.2%, increase in EBIT in 2025 as compared to 2024 was primarily due to an increase in EBIT from the segment's U.S. operations.

XI. Leadership Transition: Bryan Sayler Takes the Helm (2023-Present)

On September 12, 2022, ESCO announced a carefully planned leadership transition.

ESCO Technologies Inc. announced today that Vic Richey, Chairman, Chief Executive Officer and President, will retire from his CEO and President roles effective December 31, 2022. Richey will continue as Executive Chairman of the ESCO Board of Directors. Bryan Sayler, currently President of ESCO's Utility Solutions Group, has been selected to serve as CEO and President beginning January 1, 2023, allowing for an orderly and smooth leadership transition.

Bryan Sayler is President and CEO of ESCO Technologies Inc., a St. Louis based company with subsidiaries operating throughout the United States and around the world. Mr. Sayler joined the company in 1995 via an ESCO acquisition. Over the next two decades, he gained a wide range of experience in ESCO's Test segment leading global operations, and strategic market development through active participation in global standards bodies including IEEE, CTIA, 3GPP and the Wi-Fi Alliance. Prior to his appointment as CEO, Mr. Sayler led ESCO's Utility Solutions Group where he played a key role strategically building out the utility group, including leading ESCO's entry into the renewables business and overseeing six successful acquisitions that have more than doubled the size of the utility segment.

He has a Bachelor of Arts degree from Southeastern University and a Master of Business Administration from Baylor University. Mr. Sayler began his role as CEO and President on January 1, 2023.

Sayler's background made him uniquely qualified for the role. He previously worked at ETS-Lindgren as a SVP Solutions Development. Bryan Sayler attended Baylor University - Hankamer School of Business.

"Bryan Sayler is an outstanding leader with a great track record of effectively integrating acquired companies, delivering growth, and building a strong, cohesive team. The rigorous CEO succession planning process undertaken by the Board, which engaged a leading executive search firm and considered both external and internal candidates, confirmed that Bryan is the best choice to drive the organization forward and lead ESCO into the future." "I'm honored to succeed Vic and excited to lead this outstanding organization as we build on a strong foundation and address the opportunities and challenges ahead," said Sayler.

Sayler's First Major Moves

Sayler's initial years as CEO demonstrated continuity with the Richey era's disciplined approach while accelerating capital deployment. His first major moves—the SM&P acquisition and VACCO divestiture—represented the largest portfolio transformation transactions since the Aclara sale. These deals showed willingness to make bold capital allocation decisions while maintaining the strategic focus that defined ESCO's turnaround.

Q: Can you provide an update on the integration of SM&P and whether it is tracking ahead or behind plan? A: Bryan Sayler, CEO: The integration is on plan, possibly slightly ahead, with cultural and financial integration going well. The Maritime business is performing above initial expectations, with positive new order activity in the fourth quarter and early 2026.

XII. Current Financial Performance & FY2025 Results

ESCO's fiscal 2025 results (fiscal year ending September 30, 2025) demonstrated the impact of its strategic initiatives.

ESCO (NYSE: ESE) reported Q4 2025 and FY 2025 results with broad improvement in sales, orders, margins and earnings. Key metrics: Q4 sales $353M (+29%), FY 2025 sales $1.10B (+19%), FY entered orders $1.6B (+57%), record year-end backlog $1.1B, Q4 adjusted EPS from continuing operations $2.32 (+30%), FY adjusted EPS $6.03 (+26%).

ESCO Technologies reported a sales increase of $79 million (28.9 percent) to $353 million in Q4 2025. The Maritime acquisition contributed $58 million (21.2 percent) of revenue growth in Q4 2025.

The company's backlog reached a record $1.1 billion, boosted by a 56.5% increase in entered orders for the year. The sale of VACCO Industries was completed, reflecting a gain of $173 million in Q4.

The company closed the VACCO divestiture and recognized an after-tax gain of $173M. Cash from continuing operations was $200M for FY 2025.

FY2026 Outlook

Management anticipates double-digit growth in net sales, Adjusted EBIT, and Adjusted EPS for FY 2026. Looking ahead, ESCO expects continued growth for FY 2026 across all segments, with projected sales growth of 16 to 20%.

Management guides FY 2026 to 16–20% sales growth and Adjusted EPS of $7.50–$7.80.

Adjusted EPS guidance for the upcoming financial year 2026 is $7.65 at the midpoint, beating analyst estimates by 5.4%.

Q: Could you expand on the $200 million in ESCO Maritime orders and the growth outlook for the acquired business? A: Bryan Sayler, CEO: The orders are related to UK submarine programs and will generate revenue over two years, starting in the second or third quarter of 2026. The Maritime business is expected to continue its strong performance, contributing significantly to our growth.

XIII. Bull Case, Bear Case & Competitive Analysis

The Bull Case

The optimists point to several factors:

ESCO's backlog reached $1.13 billion in the latest quarter and averaged 29% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future.

Bullish investors often emphasize the strong five year earnings trajectory of around 24.8 percent per year and the move toward higher quality, recurring revenues.

The SM&P acquisition positions ESCO for sustained naval spending growth. The AUKUS partnership and geopolitical tensions create durable tailwinds for submarine and surface ship programs. Unlike competitive defense markets, SM&P's sole-source positions protect margins.

The Maritime acquisition significantly contributed to the company's top and bottom-line results, with over $200 million in orders booked in the first month of the new fiscal year.

The record backlog provides excellent visibility and stability for future revenues, particularly in the A&D segment where backlog reached $832 million. This positions ESCO well for sustained growth through fiscal 2025 and beyond.

The Bear Case

On these numbers, skeptics wondering whether ESCO can grow fast enough to justify a 45x multiple may find fresh ammo in the modest margin slippage and gap to DCF fair value. In Q4 2025, earnings from discontinued operations were about 173.8 million versus a small loss of roughly 5.0 million in Q4 2024, a swing that is large relative to continuing net income excluding extra items of 44.9 million in the latest quarter.

At a share price of 204.02, ESCO is trading on a trailing P/E of 45.3 times, well above both the US Machinery industry average of 24.5 times and the peer average of 26.3 times, and also above a DCF fair value of about 168.50 per share. Bears focus on this rich multiple, arguing that even with forecast earnings growth of roughly 24.3 percent per year and revenue growth of about 11.3 percent, the current price already embeds strong execution.

The Utility Solutions Group faced policy headwinds in the renewables market, leading to lower sales growth in the quarter.

At the same time, the recent margin step down shows that integration costs, competitive pressures, or mix shifts can still weigh on profitability even when revenues rise. This is the kind of risk the consensus narrative highlights around execution and end market volatility.

Competitive Analysis: Porter's Five Forces

Threat of New Entrants: LOW ESCO operates in markets with significant barriers to entry. Defense programs require security clearances, years of qualification testing, and established relationships. The company's Test segment serves customers with highly specialized requirements that take decades of institutional knowledge to understand.

Bargaining Power of Suppliers: MODERATE ESCO sources specialized materials and components but has sufficient scale and multiple sourcing options to manage supplier relationships. The biggest risk is in sole-source situations where specific materials are required for defense applications.

Bargaining Power of Buyers: MIXED In defense and aerospace, customers are large (Navy, major airlines, OEMs) but face significant switching costs once ESCO's products are designed into platforms. The utility segment has more fragmented customers with higher price sensitivity. Test serves diverse end markets with varying dynamics.

Threat of Substitutes: LOW to MODERATE For mission-critical applications like submarine stealth systems or utility grid diagnostics, there are limited substitutes. Customers need the specific performance characteristics that ESCO's products provide. The Test segment faces somewhat higher substitution risk as measurement technologies evolve.

Competitive Rivalry: MODERATE ESCO has deliberately positioned itself in niche markets where it can achieve leadership positions. Competition exists but tends to be from other specialized players rather than diversified giants seeking to enter.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: MODERATE ESCO benefits from scale in R&D spending across its segments, spreading development costs over a larger revenue base. However, the company competes through specialization rather than cost leadership.

Network Effects: LOW ESCO's businesses don't exhibit classic network effects, though Doble's database of 25+ million apparatus test results creates a form of data network effect that improves with use.

Counter-Positioning: STRONG ESCO's strategy of focusing on niche, mission-critical components represents counter-positioning against larger competitors who rationally choose not to pursue smaller, specialized markets. This was the fundamental insight that enabled the 1990s transformation.

Switching Costs: STRONG Once ESCO's products are designed into aircraft, submarines, or utility systems, switching costs are substantial. Customers face requalification expenses, operational risks, and long lead times to change suppliers.

Branding: MODERATE Within their specialized markets, ESCO's subsidiaries (Doble, ETS-Lindgren, etc.) carry significant brand value. However, this is professional/industrial branding rather than consumer brand power.

Cornered Resource: MODERATE ESCO's engineering talent and institutional knowledge represent cornered resources that competitors cannot easily replicate. Doble's test database is a unique asset.

Process Power: MODERATE Over three decades, ESCO has developed distinctive processes for acquiring, integrating, and optimizing niche engineering businesses. This operational expertise is embedded in the organization but not easily codified or transferred.

XIV. Key Performance Indicators for Investors

For long-term fundamental investors tracking ESCO, three KPIs deserve primary attention:

1. Book-to-Bill Ratio

The ratio of new orders to revenues shipped measures whether demand is accelerating or decelerating. For fiscal 2025, ESCO's book-to-bill was 1.43 for the year, meaning orders substantially exceeded revenues—a strong indicator of future growth visibility. The A&D segment showed even stronger metrics, with the backlog reaching record levels.

A sustained book-to-bill above 1.0x indicates growing demand, while readings below 1.0x suggest potential future revenue declines. Given the long-cycle nature of ESCO's defense and utility businesses, this metric provides 12-24 months of forward visibility.

2. Adjusted EBIT Margin by Segment

ESCO's strategy depends on maintaining premium margins in its niche markets. The Utility Solutions Group achieved a 29.1% Adjusted EBIT margin, demonstrating the segment's pricing power and operational efficiency. The Test segment showed improvement with a 17.5% margin after restructuring.

Tracking margins by segment reveals whether ESCO is maintaining competitive positioning or facing pricing pressure. Material margin compression would indicate commoditization risks that could undermine the investment thesis.

3. Organic Revenue Growth

While acquisitions contribute to ESCO's growth story, organic revenue growth measures the underlying health of existing businesses. The Aerospace and Defense segment saw organic sales growth of 53% in the quarter and 24% year over year.

Separating organic from acquired growth helps investors assess whether ESCO is creating value through operational excellence or simply buying revenue.

XV. Risk Factors & Regulatory Considerations

Defense Spending Cyclicality: Despite ESCO's sole-source positions, the company remains exposed to government budget decisions. While bipartisan support for naval modernization currently provides tailwinds, future administrations could shift spending priorities.

Integration Risk: The SM&P acquisition represents ESCO's largest deal ever. While integration is on plan, possibly slightly ahead, history shows that large acquisitions frequently encounter unexpected challenges.

Valuation Risk: At a share price of 204.02, ESCO is trading on a trailing P/E of 45.3 times, well above both the US Machinery industry average of 24.5 times. The current valuation assumes continued strong execution. Any operational stumble could trigger meaningful multiple compression.

Renewables Market Volatility: NRG faced a $7.0 million decrease in net sales driven by lower shipments of solar and wind products due to renewables market weakness. Policy changes affecting renewable energy investment could impact USG segment growth.

Customer Concentration: Defense contracts involve significant customer concentration with the U.S. Navy and UK Ministry of Defence. While relationships are long-standing, any procurement delays or program cancellations would materially impact revenues.

XVI. Conclusion: What the ESCO Story Teaches

The ESCO Technologies story offers several lessons for business students and investors:

Spinoffs Can Create Value: What Emerson viewed as unwanted baggage became a multi-billion dollar success story. The independence forced strategic clarity that might never have emerged under comfortable corporate parentage.

Knowing When to Exit Is as Important as Knowing When to Buy: ESCO's transformation succeeded because management recognized that competing against defense giants was unwinnable. The courage to sell crown-jewel defense businesses—and later Aclara—freed capital for more attractive opportunities.

Niche Dominance Beats Commodity Scale: ESCO deliberately chose to be the biggest fish in small ponds rather than competing for commodity business in large markets. This strategic clarity enabled sustainable margins and defensible competitive positions.

Serial Acquirers Need Discipline: ESCO executed over 18 acquisitions without a major integration failure. The key was targeting businesses with clear strategic fit, maintaining reasonable deal sizes, and applying a consistent integration playbook.

Leadership Transitions Matter: The smooth handoffs from Moore to Richey to Sayler preserved strategic continuity while bringing fresh perspectives. Each CEO built on their predecessor's foundation rather than pursuing disruptive changes.

For investors considering ESCO today, the critical questions center on whether the company can sustain its margin profiles as defense revenues grow, whether the SM&P integration delivers expected synergies, and whether the current valuation fairly reflects execution risks alongside growth opportunities.

What's beyond debate is that ESCO Technologies represents one of the most successful corporate transformations in modern industrial history—a phoenix that truly rose from the Pentagon's ashes to become a diversified, high-margin industrial compounder serving markets its founders never imagined.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube