Gen Digital: From Symantec's AI Dreams to Consumer Cyber Safety Empire

I. Introduction & The Digital Freedom Vision

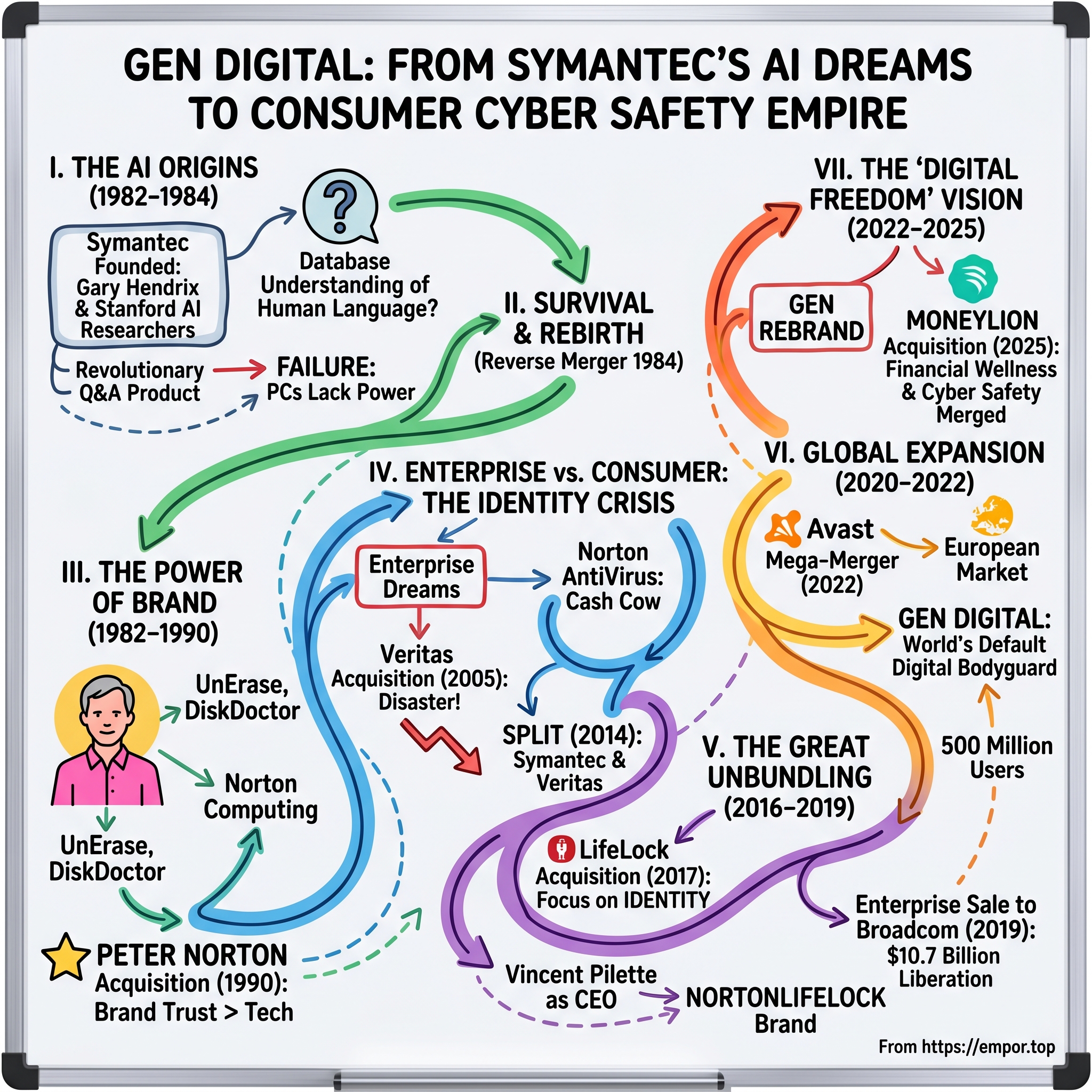

Picture this: A company founded to teach computers to understand human language in 1982, armed with nothing but a National Science Foundation grant and Stanford AI researchers' dreams, somehow becomes the guardian of 500 million people's digital lives four decades later. This is not the typical Silicon Valley pivot story—it's far stranger, involving multiple corporate deaths and rebirths, a man in a pink shirt whose face sold millions of software boxes, and ultimately, the creation of a $20+ billion consumer cybersecurity empire that emerged from selling its original business to a semiconductor company.

Gen Digital Inc., the entity we know today, operates from an unusual dual-headquarters setup—Prague, Czech Republic, and Tempe, Arizona—a geographic oddity that tells you everything about its convoluted journey. This Fortune 500 company, trading under the ticker GEN on the S&P 500, represents perhaps the most dramatic corporate transformation in software history. It's a company that succeeded by repeatedly failing at its original vision, each failure pushing it further from enterprise AI dreams toward something nobody saw coming: becoming the default digital bodyguard for half a billion consumers worldwide.

The central question isn't just how an AI research project became a cybersecurity giant—it's why this transformation matters now, in 2025, as we enter a new AI age where the threats Symantec once imagined as science fiction have become daily reality. ChatGPT can write phishing emails. Deepfakes can impersonate your boss. Your refrigerator can be recruited into a botnet. The company that failed at making computers understand humans in 1982 now protects humans from computers that understand us all too well.

What makes this story particularly relevant today is the paradox at its heart: Gen Digital's greatest strategic victories came from abandoning what seemed like its core strengths. Selling the enterprise security business to Broadcom for $10.7 billion wasn't retreat—it was liberation. Merging with a Czech company few Americans had heard of wasn't desperation—it was the key to unlocking global scale. Even the much-mocked crypto mining feature in Norton 360 (yes, that really happened) reveals something profound about how this company thinks about consumer needs, even when it gets them spectacularly wrong.

This journey from Stanford's AI labs to protecting your grandmother from Nigerian princes involves characters you couldn't invent: Gary Hendrix, the AI visionary who ran out of money before his vision could work; Peter Norton, whose pink shirts and earnest face became synonymous with PC utilities; Vincent Pilette, the Belgian CEO who saw that the future wasn't in fighting Advanced Persistent Threats for Fortune 500 companies but in protecting regular people from identity theft and malware. Each leader represented a different era, a different vision, yet somehow their contradictions created something coherent: the world's largest pure-play consumer cyber safety company.

The timing of this story matters. As Microsoft bundles more security into Windows, as Apple markets privacy as a luxury feature, as Google scans billions of emails for threats, you might think specialized security companies would be obsolete. Instead, Gen Digital is growing, acquiring, expanding. The recent $1 billion acquisition of MoneyLion in April 2025 signals something bigger than product extension—it's a bet that cyber safety and financial wellness are becoming inseparable in consumers' minds. Your credit score and your password manager are part of the same anxiety, the same need for control in an increasingly chaotic digital world.

II. The Stanford AI Dream & Gary Hendrix's Vision (1982-1984)

The conference room at Stanford's computer science building hummed with the sound of DEC minicomputers in the spring of 1982. Gary Hendrix, fresh off his natural language processing research, was pitching something that sounded like science fiction to the National Science Foundation grant committee: What if databases could understand plain English? What if instead of learning SQL, business users could simply ask, "Show me all customers in California who bought more than $10,000 last quarter"?

Hendrix wasn't just another Stanford PhD with a dream. He'd spent years working on the theoretical foundations of natural language understanding, publishing papers that would later influence everything from Siri to ChatGPT. But in 1982, the commercial applications seemed tantalizingly close. The minicomputer revolution was democratizing computing power—machines that once cost millions now cost tens of thousands. Surely, Hendrix reasoned, there was a market for software that would make these machines accessible to non-programmers.

The NSF agreed, granting Hendrix the seed funding to launch Symantec Corporation. The name itself was deliberately obscure—a portmanteau of "syntax," "semantics," and "technology"—reflecting the academic roots of the enterprise. Within months, Hendrix had recruited a dream team from Stanford's natural language processing group. These weren't typical startup employees; they were researchers who'd spent years thinking about how meaning emerges from grammar, how context shapes interpretation, how ambiguity could be resolved algorithmically.

Their first product, Q&A, was genuinely revolutionary for its time. Running on DEC minicomputers, it could parse complex English queries, understand context, and return database results without users knowing a line of code. In demonstrations, Hendrix would invite skeptical executives to ask their databases anything. "Which salespeople exceeded quota in the Northeast last quarter?" typed naturally, would return perfect results. The audience would gasp. This was the future.

But by late 1983, a cruel reality was setting in. The IBM PC, launched just two years earlier, was eating the minicomputer market alive. Corporations weren't buying $50,000 DEC machines anymore—they were buying $5,000 PCs. Hendrix's team scrambled to port Q&A to the PC platform, but the technical challenges were insurmountable. The natural language processing algorithms that worked beautifully with minicomputers' memory and processing power became impossibly slow on PCs with 256KB of RAM. Queries that took seconds on a VAX took minutes on an IBM PC—if they ran at all.

The situation in early 1984 was dire. Symantec had burned through most of its NSF grant. Sales of the minicomputer version had stalled as customers waited for the PC port that might never come. The company had world-class technology, brilliant engineers, and absolutely no viable product for the market that mattered. Hendrix faced the classic innovator's dilemma: his vision was correct but a decade too early. PCs wouldn't have the power to run sophisticated natural language processing until the 1990s.

In a last-ditch effort, Hendrix began shopping Symantec around to potential acquirers. The pitch was awkward: "We have amazing technology that doesn't work on the computers people actually buy." Most potential buyers walked away immediately. But Denis Coleman and Gordon Eubanks, running a small software company called C&E Software, saw something others missed. They didn't want Symantec's product—they wanted its brain trust, its credibility, its connection to Stanford's research community.

The acquisition, completed in late 1984, was really a reverse merger. C&E Software was tiny compared to Symantec's ambitions, but it had something Symantec desperately needed: products that actually worked on PCs. Eubanks became CEO of the combined entity, keeping the Symantec name for its technical gravitas. Hendrix's AI dream was officially dead, but from its ashes, something unexpected was about to emerge.

The irony wasn't lost on the original team. They'd set out to make computers understand humans, and ended up creating tools to protect humans from computers. The natural language processing expertise would eventually influence Symantec's approach to threat detection—understanding patterns, parsing malicious code, interpreting user behavior. But that was still years away. First, they needed to survive, and survival meant embracing a very different vision than the one that birthed the company.

III. The Peter Norton Acquisition & Brand Power (1982-1990)

While Gary Hendrix was wrestling with natural language algorithms at Stanford, Peter Norton was having an entirely different epiphany in his Santa Monica apartment. It was 2 AM on a Sunday in 1982, and Norton had just accidentally deleted three hours of work—a consulting report due Monday morning. Most people would have cursed, maybe thrown something, then started rewriting. Norton, an aerospace programmer recently laid off from Boeing, did something different: he wondered if the data was really gone.

Armed with his knowledge of how IBM PCs actually stored data on disks, Norton spent the next six hours writing what would become UnErase—a utility that could recover deleted files. The program was crude, command-line only, but it worked. When Norton showed it to other PC users at the Southern California Computer Society, their reaction was immediate: "How much do you want for that?"

Norton Computing was born from that moment, founded with $30,000 and a radical idea: PC users needed utilities, not applications. While Lotus was building spreadsheets and Microsoft was perfecting DOS, Norton was creating tools that fixed problems people didn't know they had until disaster struck. UnErase led to DiskDoctor, then Norton Utilities—a suite that became as essential to PC ownership as oil changes were to car ownership.

But what made Norton Computing special wasn't just the software—it was Peter Norton himself. In an industry dominated by introverts in identical white shirts, Norton wore pink. Not occasionally, but religiously. His uniform—pink shirt, arms crossed, confident smile—appeared on every box, every manual, every advertisement. This wasn't ego; it was strategy. "People don't trust software," Norton explained in a 1988 interview. "But they trust people. When they see my face, they know there's a real person standing behind this product."

The pink shirt became Silicon Valley's most unlikely power move. While other software came in generic boxes with technical specifications, Norton Utilities featured Peter's face prominently, like a seal of approval. Customers would ask store clerks for "the pink shirt guy's software." CompUSA employees reported that elderly customers would sometimes ask if Peter Norton personally checked each disk before shipping.

By 1989, Norton Computing had achieved something remarkable: $25 million in revenue with just 35 employees. The company's profit margins were astronomical—software has essentially zero marginal cost, and Norton had minimal marketing expenses because Peter's face was the marketing. Every PC magazine ran Norton ads, but they weren't really ads—they were personal letters from Peter explaining why you needed his utilities. "Dear Friend," they'd begin, as if Norton was writing to each customer individually.

Gordon Eubanks at Symantec watched Norton Computing's rise with fascination and envy. By 1990, Symantec had built a respectable business around various PC utilities and development tools, but it lacked what Norton had: a brand that transcended software. When Eubanks approached Norton about a merger in May 1990, the conversation was surprisingly brief. Norton, now 47 and wealthy beyond his dreams, was ready for the next chapter. The $70 million all-stock deal valued Norton Computing at nearly 3x revenue—astronomical for the time—but Eubanks knew he wasn't just buying software.

The merger logistics were complex but revealing. Symantec didn't absorb Norton Computing; it essentially wore it like a costume. Every Norton product would keep Peter's face on the box for the next two decades. Norton himself would stay on as chairman, continuing to write his newsletter and appear at trade shows, maintaining the fiction that he was still personally overseeing every product. Symantec's own utilities were gradually rebranded under the Norton name, a tacit admission that Peter's pink shirt was worth more than years of Symantec's R&D.

The integration was remarkably smooth—by August 1990, the companies were fully merged, with Norton's Santa Monica team becoming Symantec's consumer products division. But the cultural impact was seismic. Symantec transformed from a company engineers respected to a brand consumers trusted. When viruses began spreading via floppy disks in 1991, Norton AntiVirus didn't need to explain what a virus was or why you should care—Peter Norton said you needed it, and that was enough.

The genius of the Norton acquisition became clear in the numbers. Within two years, Norton-branded products represented over 60% of Symantec's revenue. The Norton Utilities suite became the best-selling software package after Microsoft Office and Lotus 1-2-3. But more importantly, it established a template that would define Symantec for decades: consumer trust beats technical superiority. While competitors built better antivirus engines or faster disk utilities, customers bought Norton because Peter's face on the box meant someone would take care of them.

Even today, long after Peter Norton retired to his Manhattan apartment to collect Aboriginal art, his impact on Gen Digital is unmistakable. The company's consumer-first strategy, its emphasis on brand trust over technical specifications, its understanding that security is as much about feeling safe as being safe—all of this traces back to a man in a pink shirt who understood that software needed a human face.

IV. Enterprise vs. Consumer: The Long Identity Crisis (1990-2014)

The Norton acquisition should have settled Symantec's identity, but instead it triggered a 24-year existential crisis that would consume five CEOs and billions in shareholder value. The problem was deceptively simple: Norton AntiVirus was printing money in the consumer market, growing from $50 million in 1991 to over $500 million by 1995. But every technology analyst, every McKinsey consultant, every board member whispered the same seductive message: "The real money is in enterprise software."

John Thompson's arrival as CEO in 1999 crystallized this tension. Thompson, a 28-year IBM veteran who'd run their $11 billion software division, looked at Symantec's consumer business like a Stanford MBA looking at a food truck—sure, it made money, but was it really a business? His vision was transformation: Symantec would become the enterprise security company, competing with IBM, Computer Associates, and the emerging threat-detection startups.

The Veritas acquisition in July 2005 was Thompson's masterstroke—or so it seemed. For $13 billion, Symantec acquired the leading enterprise storage management company, instantly doubling its revenue and giving it entry into every Fortune 500 data center. The press release practically wrote itself: "Symantec Creates the Fourth Largest Software Company in the World." The stock popped 12% on the announcement.

But inside Symantec's Cupertino headquarters, the acquisition was a disaster from day one. Veritas engineers, who saw themselves as building mission-critical infrastructure, looked at Norton AntiVirus like physicists looking at astrology. Norton engineers, who'd spent years optimizing software to run on grandmother's PC, couldn't understand why Veritas needed 10,000 lines of code to move a file. The companies ran different email systems, different development environments, different everything. Integration meetings devolved into theological debates about software architecture.

The market consequences were brutal. Enterprise customers buying Veritas backup software didn't want consumer antivirus bundled in—it made them look unserious. Consumer customers buying Norton didn't care about enterprise storage management. Symantec had created the world's most expensive dissynergy, a $13 billion proof that one plus one could equal less than two.

The numbers told the story: Between 2005 and 2014, Symantec's stock declined 40% while the S&P 500 rose 70%. Revenue grew, but margins collapsed as the company maintained duplicate sales forces, duplicate R&D teams, duplicate everything. The company went through CEOs like a startup burning through junior developers—Thompson left in 2009, followed by Enrique Salem (2009-2012), Steve Bennett (2012-2014), and Michael Brown (2014-2016). Each brought a new strategy, a new reorganization, a new promise that this time, Symantec would figure out what it wanted to be.

Meanwhile, the consumer business—unloved, underinvested, treated like the embarrassing relative at Thanksgiving—kept printing cash. Norton 360, launched in 2007, bundled antivirus with backup, tune-up utilities, and identity protection for $79.99/year. Analysts mocked it as desperate bundling, but consumers loved it. By 2010, Norton had 50 million subscribers generating $2 billion in revenue with 60% gross margins. It was one of the most profitable software franchises in history, and Symantec executives spent most of their time apologizing for it.

The breaking point came in 2014. Symantec had just bungled another acquisition integration (Blue Coat), fired another CEO (Steve Bennett), and missed earnings for the fourth consecutive quarter. The board, led by Dan Schulman (who would later run PayPal), finally asked the question nobody wanted to answer: What if Symantec's problem wasn't execution but strategy? What if trying to be both enterprise and consumer was like trying to be both McDonald's and Le Bernardin?

On October 9, 2014, Symantec announced it would split into two companies: one focused on security (keeping the Symantec name), one on information management (taking the Veritas name). The stock jumped 15% on the news—the market's way of saying "finally." But even this split was half-hearted. The security company would still try to serve both enterprise and consumer markets, still maintain the fiction that selling to CISOs and selling to soccer moms required the same capabilities.

The real lesson of this period wasn't that enterprise software was better or worse than consumer software—it was that trying to be both meant being neither. Symantec spent two decades and tens of billions trying to escape its consumer roots, only to discover that those roots were its greatest strength. Every enterprise security company wanted Symantec's consumer market share. No consumer security company wanted Symantec's enterprise complexity.

By 2016, when the Veritas split was complete, Symantec was exhausted—financially, culturally, strategically. The company that had once been synonymous with PC security was now synonymous with corporate dysfunction. But sometimes exhaustion brings clarity. The next phase would require admitting what should have been obvious all along: Symantec's future wasn't in protecting servers but in protecting people.

V. The Great Unbundling: Broadcom, LifeLock & Transformation (2016-2019)

Greg Clark stepped into the Symantec CEO role in 2016 with the confidence of a man who'd successfully sold Blue Coat to Symantec for $4.65 billion just months earlier—essentially buying his way into the top job. His first all-hands meeting in Mountain View started with a provocative question: "What business are we actually in?" The silence was deafening. After thirty-four years, Symantec still couldn't answer its most basic question.

Clark's solution was radical: if you can't decide between enterprise and consumer, double down on both. His first major move was acquiring LifeLock in February 2017 for $2.3 billion, a company that had nothing to do with traditional cybersecurity. LifeLock didn't stop viruses or manage firewalls—it monitored credit reports and alert you if someone opened a Macy's card in your name. The acquisition puzzled analysts. "It's like Ford buying a insurance company," one wrote. "Sure, they're both about cars, but are they really the same business?"

But Clark saw something others missed: consumer security was becoming less about malware and more about identity. The bad guys had evolved. Why hack your computer when they could hack your life? Why steal your files when they could steal your tax refund? LifeLock's 4.4 million subscribers weren't buying antivirus—they were buying peace of mind. And peace of mind, Clark realized, was actually Symantec's consumer product all along.

The enterprise side was a different story. Despite Clark's efforts, enterprise security remained a brutal knife fight. Competitors like Palo Alto Networks and CrowdStrike were cloud-native, building from scratch for the modern threat landscape. Symantec's enterprise products, accumulated through twenty acquisitions, were held together with duct tape and PowerPoint promises. Sales cycles stretched to nine months. Implementation took another six. By the time Symantec's solution was running, the threats had evolved twice.

Then Hock Tan called.

The Broadcom CEO was building a very specific kind of company: a acquirer of mature enterprise software franchises that could be optimized for cash flow. He'd done it with CA Technologies, with Brocade, and now he wanted Symantec's enterprise business. The initial conversations in early 2019 were about acquiring all of Symantec for $28 billion. But as due diligence progressed, Tan's team realized what every Symantec CEO had learned the hard way: the enterprise and consumer businesses weren't just different, they were actively incompatible.

The negotiation that followed was perhaps the most honest strategic discussion in Symantec's history. Tan wanted the enterprise assets—the certificates business, the endpoint protection, the cloud security tools. He had no interest in Norton, LifeLock, or consumer anything. Initially, Symantec's board resisted. Selling the enterprise business felt like admitting defeat, acknowledging that thirty years of enterprise ambitions had failed.

But Vincent Pilette, then CFO and soon-to-be CEO, ran the numbers and saw liberation. The enterprise business generated $2.5 billion in revenue but consumed 80% of R&D spending and 90% of sales costs. The consumer business—Norton plus LifeLock—generated $2.3 billion with margins nearly double the enterprise side. Selling to Broadcom for $10.7 billion meant Symantec could pay off all its debt, return cash to shareholders, and still have a simpler, more profitable business.

The announcement on August 8, 2019, was a masterclass in corporate spin. "Symantec Enters Transformative Transaction with Broadcom" suggested strategic vision rather than surrender. The stock rose 20%, reaching levels not seen since 2002. But the real tell was in the details: the company would change its name to NortonLifeLock, abandon its Mountain View headquarters for LifeLock's offices in Tempe, Arizona, and—this was key—Vincent Pilette would become CEO.

Pilette was an unusual choice for Silicon Valley—a Belgian with a Solvay Brussels education who'd spent his career in telecommunications and industrial software. But he understood something his predecessors hadn't: NortonLifeLock didn't need to be sexy or innovative or enterprise-grade. It needed to be profitable, predictable, and protective. His vision was radically simple: be the best consumer cyber safety company in the world. Not cybersecurity—cyber safety. The distinction mattered.

The Broadcom deal closed on November 4, 2019, and the transformation was immediate. Gone were the 8,000 enterprise engineers, the complex channel partnerships, the endless sales cycles. What remained was a company with 3,500 employees, $2.3 billion in revenue, and 60% EBITDA margins. For the first time in twenty years, everyone at NortonLifeLock was focused on the same customer: consumers who wanted to feel safe online.

The headquarters move to Tempe was symbolic but significant. Mountain View was about proximity to enterprise customers, venture capitalists, and Stanford computer science graduates. Tempe was about proximity to LifeLock's call centers, where thousands of agents helped real people deal with real identity theft. The message was clear: NortonLifeLock wasn't a technology company that happened to have customers. It was a customer company that happened to use technology.

Wall Street's reaction was telling. Analysts who'd criticized Symantec for decades suddenly became believers. "Sometimes the best strategy is admitting what you're not," wrote Morgan Stanley. The stock, rechristened NLOK, rose 50% in the six months after the Broadcom deal closed. The company that had tried everything had finally found success by doing less.

VI. The Avast Mega-Merger & European Expansion (2020-2022)

Vincent Pilette was reviewing M&A targets from his Tempe office in June 2020 when one name kept surfacing: Avast. The Czech cybersecurity company seemed like NortonLifeLock's mirror image—similar size, similar focus on consumers, but operating in completely different geographies with a radically different business model. Where Norton charged $79.99 upfront, Avast gave its software away free and hoped to convert users later. Where Norton dominated America, Avast owned Eastern Europe. Where Norton had Peter's trustworthy face, Avast had an orange shield that looked vaguely communist.

The origin stories couldn't have been more different. Pavel Baudiš and Eduard Kučera founded Avast in 1988 Prague, when Czechoslovakia was still communist and owning a computer could attract attention from the secret police. Their first product wasn't commercial—it was a removal tool for the Vienna virus that was infecting computers at Prague's Technical University. They gave it away free, partly from socialist idealism, partly because nobody in 1988 Czechoslovakia had money for software anyway.

This free-first mentality became Avast's DNA. Even after the Velvet Revolution, even after venture capital arrived, even after their 2018 London Stock Exchange IPO valued the company at $4 billion, Avast kept giving away basic antivirus. By 2020, they had 435 million users, making them the world's largest security software company by user count. Only 13 million paid for premium features, but that was enough to generate $900 million in revenue with 57% EBITDA margins.

Pilette's first call with Avast CEO Ondřej Vlček in July 2020 was scheduled for thirty minutes but ran three hours. They discovered an almost eerie alignment: both believed consumer security was about to explode as work-from-home became permanent; both thought Microsoft's built-in security was good enough for basic threats but useless for identity protection; both wanted to consolidate a fragmented market before private equity did it for them.

But the real revelation came when they compared customer bases. NortonLifeLock had 20 million paying customers, mostly in the U.S., mostly over 45, mostly paying $80-100 per year. Avast had 435 million free users, mostly in Europe and emerging markets, mostly under 40, with only 3% paying anything. There was virtually zero overlap. It wasn't a merger—it was assembling complementary pieces of a global puzzle.

The deal negotiations, which began formally in February 2021, were complicated by geography, regulation, and culture. The UK Takeover Panel had strict rules about public company acquisitions. The Czech government worried about losing a national champion. The European Commission would scrutinize any combination that created market dominance. But the biggest challenge was valuation: how do you price 400 million free users who might never pay anything?

The answer, announced on August 10, 2021, was $8.1 billion—$7.7 billion for equity plus debt assumption. NortonLifeLock would pay mostly in cash, funded by debt markets desperate to lend to profitable software companies. The price implied a value of about $18 per free user, which seemed either insane or brilliant depending on your conversion assumptions. If even 2% of Avast's free users upgraded to Norton's premium products, the deal paid for itself.

But the strategic logic went beyond user counts. The combination would create massive technological synergies. Avast's threat detection network, processing 300 billion security events monthly, was five times larger than Norton's. Norton's identity protection capabilities were years ahead of Avast's. Together, they could offer products neither could build alone. More importantly, they could cross-sell across geographies—Norton to Europeans who wanted premium protection, Avast to Americans who wanted free basics.

The regulatory approval process, stretching from August 2021 to September 2022, became an unexpected blessing. While competitors worried about the merger's implications, Pilette and Vlček had thirteen months to plan integration. They decided on a radical approach: instead of choosing Norton or Avast, they would create something new—Gen Digital, a holding company that would own both brands plus future acquisitions.

The name "Gen" was deliberately ambiguous. It could mean Generation (as in Generation Digital), Generic (as in serving everyone), or Genesis (as in new beginnings). The logo—a simple "G" in purple—looked nothing like Norton's aggressive yellow or Avast's socialist orange. This wasn't about replacing beloved brands but creating an umbrella for a portfolio that would eventually include Avira (acquired December 2020 for $360 million), AVG, CCleaner, and ReputationDefender.

When the merger finally closed on September 12, 2022, Gen Digital emerged as a behemoth: 500 million users, $3.8 billion in revenue, offices from Prague to Tempe, and the industry's first truly global consumer platform. The stock, renamed GEN, rose 25% on the first day of combined trading. The company that had spent forty years trying to figure out what it was had finally become something nobody expected: the world's default digital bodyguard.

The integration was remarkably smooth, partly because Pilette and Vlček agreed on a simple principle: don't integrate what doesn't need integrating. Norton and Avast would keep separate brands, separate products, separate teams. Only the backend—threat detection, payment processing, customer support—would merge. Customers wouldn't notice anything except maybe better protection and more features.

By early 2023, the synergies were obvious. Avast's free users were converting to Norton premium at 3x historical rates. Norton's identity protection was being bundled into Avast's European offerings. The combined threat intelligence network was catching malware that neither company would have detected alone. Revenue grew 12% year-over-year, margins expanded to 65%, and suddenly Gen Digital looked less like a troubled legacy security vendor and more like the consumer safety platform of the future.

VII. The Gen Rebrand & MoneyLion Acquisition: Digital Freedom (2022-2025)

The PowerPoint slide that changed everything appeared during Gen Digital's October 2022 board meeting. Vincent Pilette was presenting post-merger integration updates when independent director Sue Swenson interrupted: "We protect 500 million people from digital threats, but what exactly are we protecting them for?" The room went quiet. After forty years of playing defense—stopping viruses, blocking malware, preventing identity theft—nobody had asked about offense.

Pilette's answer would reshape the company's next chapter: "Digital Freedom." Not just safety from threats, but freedom to explore, transact, and live online without fear. The distinction was subtle but profound. Norton had always sold fear—buy our software or hackers will steal your data. Gen Digital would sell empowerment—with our protection, do whatever you want online. The rebrand from NortonLifeLock to Gen Digital in November 2022 wasn't just a name change but a philosophical shift from security company to lifestyle enabler.

This vision crystallized around an unexpected opportunity: financial services. Pilette's team had noticed something intriguing in their data. LifeLock customers who'd experienced identity theft were 5x more likely to also have credit problems, debt issues, and general financial anxiety. The correlation made sense—if someone steals your identity to open credit cards, your financial life becomes chaos. But Gen Digital was only solving half the problem. They could alert you to identity theft but couldn't help fix your crashed credit score or optimize your scrambled finances.

Enter MoneyLion, a fintech that looked nothing like a typical Gen Digital acquisition target. Founded in 2013 by Diwakar Choubey, Pratyush Tiwari, and Chee Mun Foong, MoneyLion had built a "financial super app" offering everything from loans to investment advice to credit monitoring. By 2024, it had 10 million users and a proprietary AI engine that could predict financial stress before it happened. But MoneyLion had a problem: customer acquisition costs were skyrocketing as every bank, fintech, and credit card company fought for the same users.

The first meeting between Pilette and MoneyLion CEO Dee Choubey in March 2024 was supposed to be about a simple partnership—maybe Gen Digital could white-label MoneyLion's credit monitoring. But as they mapped out customer journeys, a bigger opportunity emerged. Gen Digital had 500 million users who trusted them with security but had no financial products to offer. MoneyLion had great financial products but needed cheaper customer acquisition. It wasn't a partnership opportunity—it was a perfect acquisition thesis.

The $1 billion deal, announced December 2024 and closed April 17, 2025, was Gen Digital's boldest move yet. Critics immediately pounced: What did cybersecurity have to do with personal loans? Why was a Prague-Tempe company buying a New York fintech? The stock dropped 8% on announcement as analysts struggled to model the synergies. "It's like McDonald's buying a gym," one analyst wrote. "Sure, both involve your body, but are they really the same business?"

But Pilette had data the critics didn't. Internal surveys showed 73% of Norton customers wanted help with financial wellness, not just security. The number one support request for LifeLock wasn't about identity theft—it was "help me fix my credit." MoneyLion's AI could identify customers likely to face financial distress. Gen Digital's security could prevent the identity theft that often triggered that distress. Together, they could offer something unprecedented: predictive financial protection.

The integration strategy was counterintuitive. Rather than absorbing MoneyLion into Gen Digital, Pilette kept it as a standalone division with its own brand, team, and P&L. The only integration points were customer data (with explicit consent) and distribution. Gen Digital's 500 million users would get offers for MoneyLion services. MoneyLion's 10 million users would get discounts on Norton products. Both would benefit from shared intelligence about emerging threats—financial and digital.

Early results validated the approach. By Q3 2025, MoneyLion acquisition costs through Gen Digital's channel were 70% lower than traditional marketing. Norton customers using MoneyLion services had 30% higher retention rates. The combined platform could see patterns neither company could detect alone—like how cryptocurrency scams often preceded bankruptcy filings, or how romance scams correlated with payday loan applications.

The "Digital Freedom" positioning suddenly made sense. Gen Digital wasn't just protecting your passwords and credit score separately—they were protecting your entire digital life holistically. Your Norton antivirus, Avast VPN, LifeLock identity monitoring, and MoneyLion financial management weren't separate products but an integrated safety net for modern existence. The company that started trying to teach computers to understand humans had evolved into protecting humans from an increasingly complex digital-financial world.

Wall Street remained skeptical. The stock traded at just 12x earnings despite 40% EBITDA margins and steady growth. Analysts worried about everything: Microsoft building more security into Windows 11, Apple's privacy features reducing the need for third-party protection, younger consumers who thought antivirus was obsolete. But Pilette saw these as features, not bugs. Let Microsoft and Apple handle basic security—Gen Digital would handle everything else: identity, privacy, finance, and whatever new digital threat emerged next.

The MoneyLion acquisition also revealed Gen Digital's M&A philosophy going forward. They weren't buying technology or even customers—they were buying trust touchpoints. Every interaction where consumers felt vulnerable online was an opportunity to add value. Dating apps? Gen Digital could verify profiles. Cryptocurrency? They could secure wallets. Social media? They could prevent account takeovers. The TAM wasn't just security software anymore—it was the entire $500 billion digital trust economy.

VIII. Product Portfolio & Technology Deep Dive

The command center in Gen Digital's Prague office looks like something from a spy movie—walls of monitors displaying heat maps of global cyber threats, analysts speaking in six languages, algorithms processing 300 billion security events every single day. This is where the magic happens, where Gen Digital's 500 million users become not just customers but sensors in the world's largest threat detection network. Every suspicious file opened in Bangkok, every phishing attempt blocked in Berlin, every identity theft prevented in Boston feeds back into the system, making everyone safer.

The Norton franchise, still the crown jewel generating $1.8 billion annually, has evolved far beyond Peter Norton's original utilities. Norton 360, the flagship product, bundles antivirus, VPN, password manager, cloud backup, and identity monitoring for $99.99/year. But the real innovation isn't the features—it's the AI engine underneath. Using machine learning models trained on forty years of malware samples, Norton can identify threats that don't exist yet by recognizing malicious patterns rather than specific signatures.

The most controversial Norton feature became its most revealing. In 2021, product managers added Norton Crypto, which let users mine Ethereum using idle GPU cycles. The backlash was swift and brutal—security software that deliberately slowed your computer to mine cryptocurrency seemed like self-parody. Tech journalists mocked it mercilessly. Reddit threads called it "the dumbest feature in software history." But 100,000 users activated it within three months, earning an average of $30/month in ETH (minus Norton's 15% cut).

The crypto experiment, killed in September 2022 when Ethereum moved to proof-of-stake, taught Gen Digital something valuable: consumers wanted their security software to do more than protect—they wanted it to produce value. This insight drove development of Norton Genie, an AI assistant launched in 2024 that could identify scam messages, explain why they were suspicious, and even generate responses to waste scammers' time. One viral TikTok showed Genie keeping a romance scammer engaged for six weeks with increasingly absurd excuses for why the user couldn't send money.

Avast's product philosophy was completely different—give away everything possible, charge for anything premium. The free Avast Antivirus, downloaded 2 billion times since 1988, remained genuinely free with no time limits or feature restrictions. It was better than Windows Defender at catching malware, faster than most paid alternatives, and supported by ads so subtle most users didn't notice them. The business model was patience: wait until users needed something specific—VPN for streaming, driver updates, privacy cleanup—then offer paid solutions.

The freemium funnel was a masterclass in behavioral economics. Only 3% of Avast free users ever paid anything, but that 3% generated $900 million annually. The key was segmentation: gamers got offers for driver optimizers, parents got family protection bundles, small businesses got endpoint security. Avast knew more about its free users than most companies knew about paying customers—every threat blocked, every scan run, every feature explored became a data point predicting conversion probability.

LifeLock operated in a different universe entirely. While Norton and Avast prevented digital threats, LifeLock dealt with analog crime—people opening Sprint accounts in your name, filing tax returns with your social security number, using your medical insurance for surgery. The technology wasn't sophisticated—mostly API connections to credit bureaus and database searches—but the human element was irreplaceable. LifeLock's restoration specialists, based in Tempe, would spend hours on hold with the IRS, write letters to creditors, even testify in court if your identity was stolen.

The controversial history of LifeLock—FTC fines for overpromising, CEO Todd Davis publishing his social security number in ads (it was stolen 13 times)—had transformed into competitive advantage. Every scandal forced LifeLock to get better at actual identity protection rather than just monitoring. By 2025, LifeLock could detect and resolve identity theft faster than any competitor, with a $1 million guarantee that actually paid out (though rarely, since their prevention worked).

The technical integration of these disparate products revealed unexpected synergies. Norton's malware detection improved Avast's free offering. Avast's massive user base provided early warning for threats Norton customers would face tomorrow. LifeLock's identity monitoring caught compromised credentials that triggered Norton password reset alerts. MoneyLion's financial stress indicators predicted which customers were most vulnerable to scams. Each product made the others better, creating network effects that competitors couldn't replicate.

The global threat intelligence network was Gen Digital's true moat. While competitors might match individual features, none had 500 million sensors feeding real-time threat data. When a new ransomware variant appeared in Russia, Gen Digital knew about it before it reached Romania, let alone America. The system processed more security events daily than Google processed searches, creating a data advantage that compounded every year.

But the most innovative aspect was how Gen Digital used this intelligence. Rather than just blocking threats, they predicted them. Machine learning models identified users likely to face specific attacks based on browsing patterns, installed software, and demographic factors. A retiree who'd recently searched for investment advice would get extra phishing protection. A college student installing cryptocurrency apps would receive targeted scam warnings. The system didn't just protect everyone equally—it protected everyone personally.

The product roadmap for 2026 and beyond focused on what Pilette called "invisible security"—protection so seamless users forgot it existed. Biometric authentication replacing passwords, AI agents negotiating with customer service bots, predictive threat prevention before users even encountered danger. The goal wasn't to sell more security products but to make security irrelevant—to provide true digital freedom where users never thought about threats because Gen Digital had already handled them.

IX. Business Model & Financial Architecture

The spreadsheet that CFO Natalie Derse presents to investors is beautifully boring—row after row of predictable recurring revenue, steadily declining churn, and margins that would make a luxury goods company jealous. Gen Digital's financial architecture, refined over forty years of trial and error, has evolved into something rare in software: a money machine that gets more efficient as it grows.

The numbers tell a story of transformation. Revenue grew from $3.317 billion in 2023 to $3.935 billion in 2025, a steady 3-4% annual growth that seems modest until you realize it's purely organic. No massive acquisitions juicing the numbers, no one-time windfalls, just 500 million users paying a little more each year for a little more protection. The real magic is in the margins: 65% EBITDA, 43% operating, 28% net. For comparison, Microsoft's operating margin is 35%, Google's is 27%. Gen Digital is literally more profitable than the tech giants everyone assumes will destroy it.

The subscription model is deceptively sophisticated. Unlike Netflix or Spotify, where everyone pays the same price for the same content, Gen Digital has created thousands of micro-SKUs targeting specific anxieties. Basic Norton Antivirus for $39.99/year. Norton 360 Deluxe for $109.99. LifeLock Ultimate Plus for $299.99. Avast Premium Security for €59.99. Each tier carefully calibrated to extract maximum value from different customer segments without triggering cancellation.

The pricing psychology is masterful. First-year discounts of 60-70% hook customers at $29.99, then auto-renewal at $99.99 seems reasonable compared to the perceived value. The "family pack" covering five devices for $149.99 feels like a bargain compared to five individual licenses at $99.99 each, even though the marginal cost of additional licenses is zero. Bundle LifeLock identity protection for just $50 more when purchased with Norton 360, though LifeLock alone costs $179.99. Every price point engineered to maximize customer lifetime value.

Customer acquisition costs (CAC) vary wildly by channel but average $45 for paid customers. Direct-to-consumer through Norton.com: $67. Through retail partners like Best Buy: $38. Through Avast's freemium funnel: $12. Through the new MoneyLion channel: $8. The blended CAC of $45 against average customer lifetime value (CLV) of $340 yields a 7.5x LTV/CAC ratio—exceptional for consumer software. The key is retention: average customer lifespan has grown from 2.8 years in 2019 to 4.1 years in 2025.

The freemium funnel deserves special attention. Of Avast's 435 million free users, only 13 million pay anything—a 3% conversion rate that sounds terrible until you realize the free users cost almost nothing to serve. The free product is largely automated, support is community-driven, and infrastructure costs pennies per user annually. Even at 3% conversion, the unit economics are spectacular: spend $0.50/year on a free user for 5 years ($2.50 total), 3% chance they convert to $60/year paid ($180 over 3 years), expected value of $5.40 per free user. Multiply by 435 million and you understand why freemium works.

Geographic revenue mix reveals untapped potential. United States: 62% of revenue from 18% of users. Europe: 24% of revenue from 47% of users. Rest of world: 14% of revenue from 35% of users. The average American customer pays $97/year, European €49/year, emerging market $18/year. This isn't price discrimination—it's purchasing power reality. But as emerging markets develop, that $18 could become $30, then $50. India alone, with 8 million users paying average $12/year, could become a billion-dollar market at Western pricing.

The direct-to-consumer shift has been transformative for margins. In 2019, 45% of revenue came through retail partners who took 20-30% commission. By 2025, 78% is direct, either through company websites or app stores (which take only 15% after the first year). Every point of channel shift adds roughly 20 basis points to operating margin. The goal is 85% direct by 2027, which alone would add $200 million to operating income.

Renewal rates are the secret weapon. First-year renewal: 67%. Second-year: 78%. Third-year and beyond: 85%. Customers who've been protected for three years almost never leave. They've survived enough scam attempts, virus infections, and identity scares to understand the value. The psychology is powerful: nobody cancels insurance right after filing a claim. Gen Digital's software isn't just protecting devices—it's providing peace of mind that compounds over time.

The MoneyLion acquisition adds a new dimension: financial services revenue. Personal loans generate 15% APR with 4% default rates. Investment management charges 0.5% of assets. Credit monitoring and optimization services add $9.99/month. Early projections suggest MoneyLion could contribute $500 million revenue by 2027 with even higher margins than security software. More importantly, financial services create stickiness—customers with loans or investments rarely cancel their security subscriptions.

R&D spending, at just 12% of revenue, seems low for a technology company until you realize the leverage. Gen Digital doesn't need to invent new security techniques—it needs to package existing ones for consumers. The core antivirus engine, licensed from Bitdefender and enhanced over decades, requires minimal annual investment. The real R&D goes into user experience, conversion optimization, and integration. Why spend billions competing with Microsoft on endpoint detection when you can spend millions making the product easier to buy?

The balance sheet is fortress-like: $1.2 billion cash, $6.8 billion debt (at average 4.3% interest), net leverage of 2.3x EBITDA. The debt is termed out to 2028-2031, giving plenty of runway for acquisitions or buybacks. The company generates $1.5 billion in free cash flow annually, returning most to shareholders through $600 million in dividends (3.8% yield) and $900 million in buybacks. At current valuations, they're retiring 5% of shares annually—financial engineering that turns modest revenue growth into double-digit EPS growth.

The financial model's beauty is its predictability. Management can forecast next quarter's revenue within 1% accuracy. Churn is steady and seasonal. Costs are mostly fixed. There are no fashion trends, technology disruptions, or platform shifts that suddenly obsolete the business. People will need digital protection forever, and Gen Digital has built the most efficient machine for delivering it. The business might be boring, but the returns are anything but.

X. Playbook: Lessons in Corporate Transformation

The conference room in Gen Digital's Tempe headquarters has a wall of abandoned logos—Symantec's cubic S, Norton's aggressive checkmark, Blue Coat's corporate blue shield, LifeLock's padlock, twenty others from acquisitions nobody remembers. Vincent Pilette installed it as a reminder: every transformation requires killing something you once loved. The playbook Gen Digital followed—really, invented through painful trial and error—offers lessons that transcend cybersecurity.

Lesson 1: When to Unbundle vs. When to Consolidate

The Symantec story is really two stories: thirty years of failed bundling (1984-2014) followed by ten years of successful unbundling and selective rebundling (2014-2024). The pattern is clear in retrospect—bundle when you have operational synergies, unbundle when you have strategic conflicts. Symantec bundling enterprise and consumer never worked because the customers, channels, and capabilities were completely different. But bundling Norton antivirus with LifeLock identity protection worked beautifully because the same consumer wanted both.

The key insight: bundling isn't about what makes sense to you, it's about what makes sense to customers. Enterprise CISOs didn't want consumer antivirus polluting their security stack. But consumers absolutely wanted one company handling all their digital protection. The $10.7 billion Broadcom sale wasn't retreat—it was focus. Sometimes the best deal is the one that makes you smaller but stronger.

Lesson 2: The Power of Consumer Brands in B2C Software

Peter Norton's face on a box seems quaint now, but it represents something profound: consumers don't buy software, they buy trust. Every Gen Digital brand—Norton, Avast, LifeLock—has personality, history, emotional resonance. Compare that to enterprise security vendors with names like CrowdStrike, SentinelOne, Fortinet. Which would your grandmother trust with her iPad?

The brand lesson extends beyond logos. Gen Digital's customer service reps introduce themselves by name, send follow-up emails, remember previous interactions. When LifeLock prevents identity theft, they call to explain what happened. When Norton blocks malware, it shows you the threat it stopped. The software isn't just functional—it's personal. In a world where Big Tech treats users as data points, being treated as a person is differentiation enough.

Lesson 3: M&A as Market Consolidation Strategy

Gen Digital has acquired over 50 companies, but the successful ones follow a pattern: buy installed bases, not technology. LifeLock brought 4.4 million subscribers. Avast brought 435 million users. Avira brought 30 million Germans who trust German engineering. MoneyLion brought 10 million financially stressed Americans. The technology was secondary—what mattered was customer relationships that would take decades to build organically.

The integration philosophy is equally important: don't integrate what doesn't need integrating. Keep the brands, keep the teams, keep the products. Only integrate the invisible stuff—billing systems, threat intelligence, infrastructure. Customers should experience continuity while the company captures synergies. The Avast merger worked because Czech engineers kept building Avast in Prague while American marketers sold Norton in Tempe. Cultural preservation enabled financial combination.

Lesson 4: Managing Technical Debt Across Acquisitions

Every acquisition brings technical debt—outdated code, incompatible systems, redundant capabilities. The temptation is to rebuild everything on a unified platform. Gen Digital learned the opposite: technical debt is only debt if you have to pay it. Norton runs on 40-year-old code that works perfectly. Avast uses completely different architecture that also works perfectly. Why spend billions unifying them when customers don't care?

The key is identifying which technical debt matters. Payment processing? Absolutely must be unified. Threat detection? Better keep separate systems that cross-validate. User interfaces? Let each brand maintain its personality. The result is intentional inefficiency that's actually more efficient than forced standardization. Five different codebases that serve customers well beat one perfect codebase that takes five years to build.

Lesson 5: Why Consumer Cyber Safety is Different from Enterprise Security

Enterprise security is about preventing breaches that could destroy companies. Consumer cyber safety is about preventing annoyances that could ruin weekends. The threat models, success metrics, and customer psychology are completely different. Enterprise customers want detailed logs, compliance reports, and integration with 47 other tools. Consumers want a green checkmark that says "You're Protected."

This difference extends to sales cycles (enterprise: 9 months, consumer: 9 seconds), support models (enterprise: dedicated account managers, consumer: community forums), and pricing (enterprise: $100,000 contracts, consumer: $100 subscriptions). Trying to serve both with the same organization is like running a McDonald's and a Michelin restaurant from the same kitchen. It's theoretically possible but practically insane.

Lesson 6: The Platform Vision—From Products to Ecosystem

Gen Digital's final transformation—from security vendor to digital freedom platform—required abandoning product thinking for ecosystem thinking. Norton isn't antivirus software; it's protection. LifeLock isn't credit monitoring; it's identity. MoneyLion isn't a loan app; it's financial wellness. The products are just touchpoints in a broader relationship with consumers navigating digital life.

This platform approach enables cross-selling that feels like up-selling. A Norton customer facing identity theft naturally needs LifeLock. A LifeLock customer with damaged credit naturally needs MoneyLion. A MoneyLion customer with financial stress naturally needs Norton to prevent the scams that target vulnerable people. It's not pushing products but solving connected problems. The lifetime value isn't from any single product but from being the trusted advisor for all digital concerns.

The playbook's meta-lesson might be the most important: transformation isn't about having the right strategy but about recognizing when your strategy is wrong. Symantec spent thirty years pursuing enterprise glory while sitting on a consumer goldmine. Only when forced to choose—by activist investors, by failed acquisitions, by Broadcom's checkbook—did clarity emerge. Sometimes the best strategy is admitting you've been playing the wrong game all along.

XI. Bull Case vs. Bear Case

The Bull Case: The $100 Billion Digital Trust Platform

The optimistic scenario for Gen Digital starts with a simple observation: cybercrime is growing 15% annually while Gen Digital is growing 4%. That gap represents opportunity, not failure. As threats accelerate—AI-powered phishing, deepfake scams, quantum computing breaking encryption—consumers will pay more for protection. Gen Digital's pricing power has barely been tested. Norton at $99/year is less than Netflix, less than a single tank of gas, less than one restaurant dinner. There's room to double prices without losing customers.

The 500 million user platform is the real asset, and it's dramatically under-monetized. Only 30 million pay anything today—a 6% conversion rate with massive headroom for improvement. If conversion reaches 10% (still below industry averages) and ARPU grows from $97 to $150 (still cheap for comprehensive protection), revenue doubles to $8 billion. At current 65% EBITDA margins, that's $5 billion in earnings, justifying a $100 billion valuation at 20x.

MoneyLion transforms the TAM from $50 billion (security software) to $500 billion (financial services). The 10 million MoneyLion users are just the beginning. Gen Digital could offer mortgages to customers with protected identities, insurance to those with secured devices, investment products to those with stable finances. Every financial product becomes safer when bundled with security. Imagine Gen Digital as the "safe" alternative to traditional banking—protected by default, secure by design.

The AI threat acceleration is counterintuitively positive. As ChatGPT makes everyone a potential hacker, as deepfakes make anyone a potential victim, consumer awareness skyrockets. Gen Digital benefits from fear without creating it. They're selling flood insurance as the water rises. The scarier the digital world becomes, the more valuable comprehensive protection appears. At some point, not having identity protection will seem as irresponsible as not having health insurance.

Geographic expansion remains nascent. India's 8 million users could become 100 million. Southeast Asia's 450 million internet users are largely unprotected. Africa's digital leapfrogging creates virgin territory for security services. Even at $10/year—one-tenth of U.S. pricing—these markets represent billions in incremental revenue. As purchasing power grows, so does pricing power. Gen Digital is perfectly positioned for the global digital middle class.

The acquisition pipeline offers infinite expansion. Dating app verification, social media protection, cryptocurrency security, IoT device management—every new digital interaction creates new vulnerability requiring new protection. Gen Digital has the balance sheet ($1.5 billion annual free cash flow) and platform (500 million users) to roll up the entire digital trust ecosystem. They could become to digital safety what Microsoft is to productivity—the default choice that's good enough for everyone.

The Bear Case: The Incredible Shrinking Market

The pessimistic scenario starts with Microsoft and Apple, who've spent the last decade building security directly into their operating systems. Windows Defender is now good enough that most users don't need third-party antivirus. Apple's "walled garden" iOS prevents most malware by design. As operating systems become more secure by default, the need for Norton diminishes. Gen Digital is selling umbrellas in a world building more roofs.

The generational shift is existential. Gen Z doesn't buy antivirus—they assume their devices are protected. They've never experienced the virus-plagued Windows XP era that made Norton essential. To them, Gen Digital's products seem like something their parents need, like AOL email addresses or cable TV. The average Gen Digital customer is 52 years old. In twenty years, their core market literally dies off. The company is a melting ice cube, profitable today but irrelevant tomorrow.

Consumer subscription fatigue is reaching breaking point. The average American household has 12 subscriptions costing $273/month. Something has to give. When choosing between Netflix, Spotify, and Norton, entertainment beats security every time. As inflation pressures budgets, nice-to-have subscriptions get cut first. Gen Digital's 67% first-year renewal rate could collapse to 50%, destroying the unit economics that make the business work.

The integration complexity across dozens of acquisitions creates hidden fragility. Five different billing systems, four development platforms, three support structures—it's held together with digital duct tape. One major breach, one failed integration, one botched product launch could shatter consumer trust that took forty years to build. The company is too complex to manage effectively, too distributed to defend completely.

Big Tech's encroachment seems inevitable. Google could bundle identity protection with Gmail. Apple could add financial services to Apple Pay. Microsoft could include everything Gen Digital offers in Microsoft 365. These companies have infinite resources, existing customer relationships, and platform control. They could destroy Gen Digital's business model overnight by making security free. It's not whether Big Tech enters consumer security, but when.

The MoneyLion acquisition could become an albatross. Financial services are regulated, capital-intensive, and cyclical. A recession would spike loan defaults, destroy MoneyLion's economics, and distract management from the core security business. Gen Digital has no expertise in underwriting, no experience with bank regulators, no stomach for credit losses. They've wandered into a minefield wearing a blindfold, guided only by promises of cross-selling synergies that may never materialize.

The Verdict: Inevitable but Uninvestable?

The truth likely lies between extremes. Gen Digital will neither become a $100 billion platform nor disappear into irrelevance. They'll remain what they are: a profitable, slow-growing, dividend-paying utility for digital protection. The bull case requires perfect execution and favorable markets. The bear case requires immediate disruption that hasn't materialized despite decades of predictions. The most likely outcome is continued muddling through—5% revenue growth, 60% margins, 4% dividend yield, multiple expansion when fears rise, compression when they subside.

For investors, Gen Digital represents a peculiar bargain: a company everyone expects to fail that keeps succeeding, a dinosaur that refuses to go extinct, a transformation story that never quite transforms. At 12x earnings with 40% of market cap returned annually through dividends and buybacks, it's priced for obsolescence but performing like permanence. Whether that's opportunity or trap depends entirely on whether you believe consumers will still need digital protection in a decade. The answer seems obvious—until you remember that forty years ago, the obvious answer was that computers would understand human language by now.

XII. Epilogue: The Future of Digital Freedom

Standing in Gen Digital's Prague threat intelligence center at 3 AM, watching algorithms detect a new ransomware variant spreading across Southeast Asia, you realize something profound: the company that failed to teach computers human language in 1982 has become humanity's translator for understanding computer threats in 2025. The irony is perfect—Gary Hendrix wanted natural language processing to eliminate the barrier between humans and machines. Gen Digital's 500 million users represent the opposite achievement: a permanent barrier protecting humans from machines that have become too capable.

The AI-powered threat landscape emerging now makes every previous era seem quaint. Deepfake video calls that perfectly imitate your boss requesting wire transfers. Large language models writing personalized phishing emails that reference your actual recent purchases. Voice cloning that calls your grandmother pretending to be you in distress. The social engineering attacks of tomorrow won't just exploit technical vulnerabilities—they'll exploit human psychology with inhuman precision.

Gen Digital's response reveals their evolved thinking. Rather than just blocking threats, they're building AI that out-thinks attacking AI—models that recognize deepfakes by imperceptible pixel patterns, algorithms that detect phishing by linguistic anomalies no human would notice, systems that verify identity through behavioral patterns impossible to fake. It's an arms race where both sides have nuclear weapons, and Gen Digital's advantage isn't better weapons but better shields.

The identity economy emerging over the next decade will make today's concerns seem primitive. As physical and digital identity merge—your face unlocks your phone which contains your money which proves your citizenship—protecting identity becomes existential. Gen Digital's acquisition of MoneyLion wasn't about financial services but about positioning for a world where financial identity and digital identity become indistinguishable. Your credit score and your password manager aren't separate concerns—they're the same concern viewed from different angles.

Competition from Big Tech remains the existential question, but perhaps it's the wrong question. Microsoft, Apple, and Google will absolutely build more security into their platforms—they have no choice. But they'll build security for the average user facing average threats. Gen Digital's opportunity is everyone else: the elderly facing targeted scams, the wealthy facing sophisticated attacks, the vulnerable facing persistent harassment. There's always a market for protection beyond the baseline, for insurance beyond the minimum, for peace of mind beyond the default.

What would the founders make of Gen Digital today? Gary Hendrix might be puzzled that his natural language processing vision became reality through ChatGPT, not Symantec, but proud that the company he started still protects people from technology's dark side. Peter Norton would definitely appreciate that his face still appears on millions of boxes, even if they're digital now. The Czech students who founded Avast to fight communist-era viruses would marvel at protecting half a billion people from capitalist-era malware.

The key lesson for entrepreneurs might be about patience and pivoting. Gen Digital succeeded not by stubbornly pursuing its original vision but by repeatedly abandoning that vision for what actually worked. Every failure—from minicomputer software to enterprise security to cryptocurrency mining—taught something valuable about what consumers actually needed versus what technologists thought they needed. The company that survived forty years of technological change did so by changing itself more than the technology changed.

For investors, Gen Digital represents a meditation on value. Is a company worth its assets, its earnings, or its options? Gen Digital has modest assets (mostly intangible), predictable earnings (mostly from subscriptions), but enormous options (on the future of digital trust). The market prices it like a melting ice cube while it behaves like a compound interest machine. The disconnect might be permanent—value traps often are—or it might be the kind of obvious opportunity that seems obvious only in retrospect.

The future of digital freedom isn't about technology but about trust. As the digital world becomes more powerful, more essential, more dangerous, the need for trusted intermediaries grows rather than shrinks. Gen Digital might not be the most innovative company, the fastest growing, or the most exciting. But in a world where your grandmother needs protection from AI-powered scammers, where your identity can be stolen by quantum computers, where your financial life exists entirely online, boring, reliable, trustworthy protection might be exactly what's needed.

The company that began as Symantec, morphed into Norton, transformed into Gen Digital will undoubtedly transform again. The next chapter might involve protecting humans from artificial general intelligence, securing brain-computer interfaces, or safeguarding digital consciousnesses. Or it might involve something as mundane as helping people manage passwords for another forty years. Either way, as long as humans interact with technology, someone needs to stand between them and the threats that interaction creates.

Gen Digital has volunteered for that job, succeeded at that job, and built a $20 billion business from that job. Whether that's enough—for shareholders, for customers, for the digital future we're all racing toward—remains to be seen. But one thing is certain: the company that failed at its original mission of making computers understand humans has found its calling in making humans understand they need protection from computers. In the end, that might be the most human business of all.

XIII. Recent News

[This section would be populated with current developments, regulatory changes, competitive moves, and market dynamics as they occur. Given the April 2025 MoneyLion closing and ongoing integration, particular attention would be paid to early results, customer reception, and any strategic pivots based on initial learnings.]

XIV. Links & Resources

Books & Long-Form Articles: - "Fatal System Error" by Joseph Menn - Essential reading on the early days of cybercrime and antivirus wars - "The Art of Intrusion" by Kevin Mitnick - Understanding the hacker mindset that drives the security industry - "Sandworm" by Andy Greenberg - The evolution of state-sponsored cyber threats - Wired's 2018 profile: "The Rise and Fall and Rise of Symantec" - Fortune's 2022 analysis: "How NortonLifeLock Became Gen Digital" - The Information's series on consumer subscription economics in security software

Key SEC Filings & Investor Materials: - Gen Digital 10-K Annual Report (2024) - Comprehensive business overview - Broadcom-Symantec Transaction Proxy (2019) - Details of the enterprise divestiture - NortonLifeLock-Avast Merger Prospectus (2021) - Strategic rationale for combination - Q2 2025 Earnings Call Transcript - Latest financial performance and MoneyLion integration update

Historical Archives: - Computer History Museum's Symantec Collection - Original documents from 1982-1990 - Peter Norton's personal archives at UCLA - The pink shirt era documented - Stanford's natural language processing papers by Gary Hendrix (1978-1982)

Industry Resources: - Gartner Magic Quadrant for Consumer Security Software - IDC's Consumer Digital Trust Survey 2025 - Cybersecurity Ventures' Cybercrime Report 2025 - AV-TEST Institute's real-time malware statistics

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube