Affirm: The Story of Buy Now, Pay Later's Most Ambitious Player

I. Introduction & Episode Roadmap

Picture this: It's January 2021, and a Ukrainian-born PayPal co-founder is watching his company's stock price double on its first day of trading. Max Levchin's stake in Affirm suddenly balloons to $2.5 billion as shares rocket from $49 to $97 in a matter of hours. The market is sending a clear message: the anti-credit card company has arrived.

Today, Affirm stands as the largest U.S.-based buy now, pay later lender, a financial technology powerhouse processing $28 billion in payments annually for 22 million users. From Peloton bikes to Amazon purchases, from Walmart groceries to airline tickets, Affirm has quietly inserted itself into the American shopping experience, offering what it calls "honest financial products" in a world of hidden fees and compound interest traps.

But here's the fascinating question: How did a PayPal alum convince some of America's largest retailers—Amazon, Walmart, Target, Shopify—to bet their customer relationships on a new form of consumer credit? How did Affirm navigate the treacherous waters between Silicon Valley disruption and Wall Street regulation? And perhaps most intriguingly, why did Max Levchin, already wealthy from the PayPal exit, decide to take another swing at revolutionizing consumer finance?

This is a story about disrupting one of capitalism's oldest businesses—lending money. It's about building trust in an industry built on mistrust. It's about surviving the fintech wars when competitors include everyone from Swedish unicorns to Apple itself. And ultimately, it's about whether transparent, point-of-sale financing can actually deliver on its promise to improve financial lives, or whether it's simply credit cards in a shinier package.

What you'll learn today: the inside story of Affirm's journey from startup studio experiment to public company, the strategic partnerships that made the difference, the regulatory battles that nearly derailed everything, and the playbook for building a two-sided financial network in the age of embedded finance. We'll examine the bear and bull cases, dissect the unit economics, and explore what the future holds for consumer credit in America.

Let's dive into the remarkable ascent of the company that dared to be the anti-credit card.

II. Origins: Max Levchin's Post-PayPal Journey

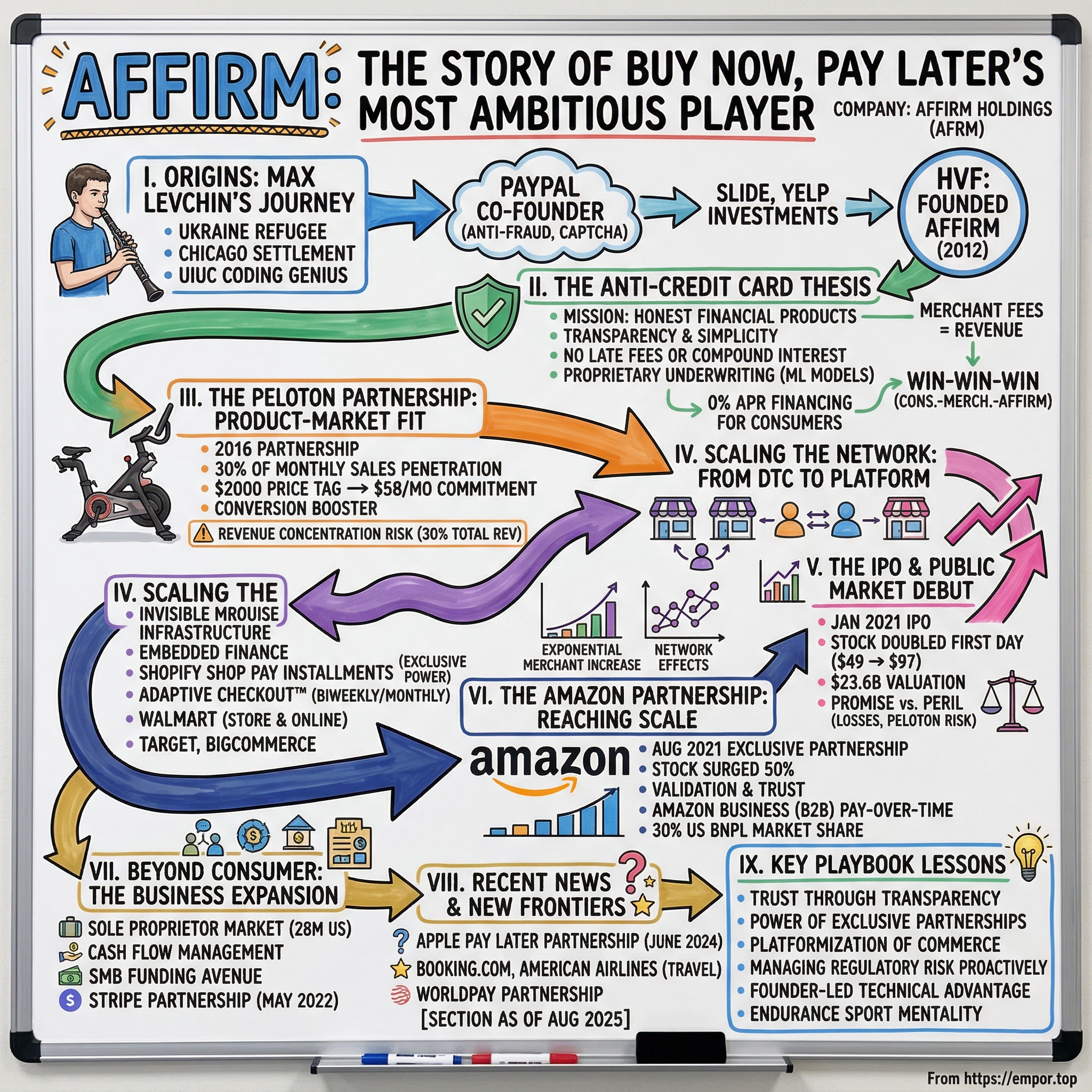

The story begins not in Silicon Valley but in Soviet-era Kyiv, where a sickly child named Maksymilian Rafailovych Levchyn fought for every breath. Behind the curtain of Soviet-era Ukraine, Maksymilian Rafailovych Levchyn is born to a family of physicists. As a child, Max struggles to overcome life-threatening respiratory diseases. His parents are told he won't live past childhood. With his mother's urging, a determined young Max begins playing the clarinet to build lung capacity. The clarinet—that unlikely medical device—would become his first lesson in engineering solutions to seemingly impossible problems.

The Levchin family's exodus from the collapsing Soviet Union reads like a Cold War thriller. In 1991, Levchin and his family left the Soviet Union under political asylum and headed for the United States, settling in Chicago. He remembers taking a Pan Am flight from Moscow with only $700 in their pockets to start a new life in America. In 1991, Levchin immigrated with his family to America, arriving as refugees in Chicago with barely $500 to their name. Only 16 years old and lacking English fluency, Levchin confronted intense economic and cultural adjustments as he fought to gain educational footing. Picture the scene: a teenager clutching a worthless red Soviet passport—"I was a man without a country. My red Soviet passport was a passport to no country."—stepping off a plane into Chicago's harsh winter with nothing but mathematical brilliance and fierce determination.

At the University of Illinois at Urbana-Champaign, Levchin became legendary for his all-night coding sessions, writing in assembly language—the most primitive and unforgiving of programming languages. My standard self-definition as a programmer had always been I started with these decrepit computers, where the most efficient way to write code was to write assembly. It was all very, very explicit, very procedural programming in various different assembly languages. Probably made me slightly more elitist, but certainly made me very tenacious as a developer. While his classmates took shortcuts with high-level languages, Levchin was building his code architecture brick by brick, a habit that would prove invaluable when building fraud-detection systems at PayPal.

The PayPal story itself has been told countless times, but Levchin's specific contribution deserves emphasis. In 1998, Levchin and Peter Thiel founded Fieldlink, a security company that allowed users to store encrypted data on their PalmPilots and other PDA devices for handheld devices to serve as "digital wallets". After changing the company name to Confinity, they developed a popular payment product, calling it PayPal and focusing on digital funds transfer by PDA. The company merged with X.com in 2000, and in 2001, the company adopted the name PayPal after its main product. PayPal, Inc. went public in February 2002, and in July 2002 was acquired by eBay. Levchin's 2.3% stake in PayPal was worth approximately $34 million at the time of the acquisition. More importantly, Levchin is widely known for his contributions to PayPal's anti-fraud efforts and is also the co-creator of the Gausebeck-Levchin test, one of the first commercial implementations of a CAPTCHA.

The post-PayPal years reveal a restless innovator searching for his next mountain to climb. Levchin personally invested $1 million to launch media-sharing company Slide in 2004, which sold to Google in 2010 for $182 million. But Slide, despite its financial success, left Levchin unfulfilled. In a remarkably candid admission, he later reflected: "Slide was a disappointment, and I think it would've always been a disappointment because I just don't care about games. I played a really good game, because I had to, but it drained the crap out of me, because I couldn't play games if my life depended on it. We were generating revenue, and we were building games and making products but people around me that had far less stock and worked probably harder than I was at the time, cared more about their products than I did. It's impossible to run a company into great scale unless you're deeply passionate about what you're doing."

His investment in Yelp proved more successful—both financially and emotionally. "At my 29th birthday party, Russ and Jeremy were sitting at the back of the table at Slanted Door in San Francisco, and while we were eating noodles I can see their heads are slowing getting bigger. At the end of the lunch they said, 'Dude, I think we figured out what's going to happen to Yellow Pages and it's going to be amazing.' I basically wrote them a million dollar check on the spot and it was literally the single best investment I made in my entire life, so far." Levchin was a key early investor in Yelp, an online social networking and review service that started in 2004. He was the company's largest shareholder, owning more than 7 million shares as of 2012.

But it was in 2011 that Levchin found his next true calling. In late 2011, Levchin started a company called HVF (standing for "Hard, Valuable, and Fun") that was intended to explore and fund projects and companies in the area of leveraging data, such as data from analog sensors. In early 2012, the financial technology company Affirm was spun out of HVF, with the goal of building the next-generation credit network. Affirm was created by Levchin, Palantir Technologies co-founder Nathan Gettings, and Jeff Kaditz of First Data. The stage was set for Levchin's most ambitious venture yet: taking on the credit card industry itself.

III. The Anti-Credit Card Thesis

Imagine walking into a Best Buy in 2008 and watching a young couple agonize over whether to finance a new television through the store's credit card—12 months same-as-cash, but if you miss a payment, 29.99% interest retroactively applied to the entire purchase. This exact predatory practice, replicated millions of times across America, is what Max Levchin set out to destroy when he launched Affirm.

Affirm's stated mission is to deliver honest financial products that improve lives, a deceptively simple statement that represented a declaration of war against an entire industry built on opacity. Traditional credit cards thrive on complexity: teaser rates that balloon, balance transfer fees hidden in fine print, compound interest that turns a $1,000 purchase into a $3,000 albatross. The average American household carries $6,194 in credit card debt, paying an average APR of 22.8%—a system Levchin viewed as fundamentally broken.

The insight was both moral and mathematical. From the beginning, Max has been clear in his desire to build a financial institution that succeeded only when consumers and merchants succeeded. That meant not charging late fees or penalty interest rates. These could create adverse incentives to lend money to people who may not be able to repay on time in the future. It meant creating transparency in pricing — showing people exactly how much they would pay for their loan, in dollars. For many people, quoting an APR or an interest rate can be hard to translate into payments. It meant never asking them to pay a penny more than what they agreed to upfront.

In 2012, Affirm was founded under the name "Luminous," but rebranded to its current name in 2013. The company launched its first product, a consumer lending platform, in 2014. The early product was remarkably simple: at checkout, instead of entering credit card information, consumers could choose Affirm and see exactly what they'd pay—$83.33 per month for six months, period. No gotchas, no late fees, no compound interest snowball.

Early strategy was to enter the point-of-sale (POS) financing marketplace in the U.S. Affirm's beta version was launched to the public in early 2013 and the company's first and only merchant partner was 1-800-Flowers.com (which they used to test the concept). Think about that choice—flowers, the ultimate emotional purchase, often bought in moments of celebration or apology, when rational financial thinking takes a backseat. It was the perfect laboratory for Levchin's hypothesis: could transparent financing actually work when consumers are at their most vulnerable to predatory lending?

The technology underpinning this transparency was anything but simple. It meant forming a proprietary judgement about peoples' willingness and ability to repay loans, using all the data available. Relying on FICO as the industry standard could disadvantage immigrants, recent grads and others new to credit. Levchin's team built machine learning models that looked beyond traditional credit scores, analyzing thousands of data points to make real-time underwriting decisions. Because of uniqueness in its algorithms and Levchin's financial relationships, Affirm fully assumed the risk of the consumer credit it underwrote. This allowed Affirm to quickly tie-up with many new merchant partners.

But the real innovation wasn't just in the underwriting—it was in the business model alignment. Affirm earns interest income on the simple interest loans from originating bank partners and on the merchant site, Affirm earns a merchant fee for its services. Our business model is aligned with the interests of both consumers and merchants — we win when they win. From merchants, we earn a fee when we help them convert a sale and power a payment. Merchant fees depend on the individual arrangement between us and each merchant and vary based on the terms of the product offering; we generally earn larger merchant fees on 0% APR financing products.

This dual revenue stream created a fascinating dynamic: Affirm could offer 0% interest loans to consumers while still making money from merchants who were happy to pay for increased conversion rates and larger basket sizes. The company wasn't trying to trap consumers in debt; it was trying to help merchants sell more stuff. Our economic model has never relied on late fees. We've never charged a single one in the history of the company. That means we need to be really good at underwriting. We underwrite every single transaction at the time of purchase to make sure we understand what the customer is buying and what particular financial shape they're in at that time. That really allows us to control risk.

The early fundraising reflected both the ambition and the skepticism surrounding this model. By 2016, Affirm had raised over $400 million in funding from investors such as Khosla Ventures and Lightspeed Venture Partners. It's also an exciting day for us at Lightspeed, having co-led their first institutional round of financing back in 2013. Jeremy Liew from Lightspeed would later recall the pitch meeting: "Max walked in and essentially said, 'I'm going to build the anti-credit card company.' Most VCs would have shown him the door. But when you've built PayPal's fraud detection system, you get the benefit of the doubt."

By mid-2014, Affirm had raised more than US$50 million in funding and formed a team of 32 people. The team was a who's who of fintech talent: The background of the people who built Affirm's underwriting ranges from Paypal to Palantir, Cap One to Google. They brought the best of technology and banking to custom-build Affirm's proprietary models.

What started as an idealistic mission to provide "honest financial products" was slowly gaining traction. But Affirm needed a breakthrough partnership to prove that transparent lending could scale beyond flowers and small-ticket items. That breakthrough would come from an unlikely source: a luxury exercise bike company that was about to change everything.

IV. The Peloton Partnership: Finding Product-Market Fit

The scene: a boutique cycling studio in Manhattan, 2016. John Foley, Peloton's CEO, is staring at a spreadsheet that shows nearly 40% of potential customers abandoning their shopping carts. The culprit? A $2,000 price tag that most fitness enthusiasts couldn't stomach all at once. Enter Max Levchin and Affirm with an audacious proposition: what if we made luxury fitness equipment accessible through transparent financing?

As the company broadens its offering to an increasingly mass market audience, it believes that more and more consumers may be hesitant to make such a large out-of-pocket expense. "In chats or follow-up surveys of people who abandoned their shopping cart, many say they'd love to have a bike, but just couldn't pay for it all up front," said Johnny Jiang, VP of Marketing at Peloton.

The partnership that emerged would become the defining case study for buy now, pay later in America. Enter Affirm, which offers up to 39 months of interest-free financing for the purchase of a Peloton bike directly from the Peloton website. Affirm's financing option eliminated the large up-front expense and replaced it with a $58/month commitment. What Peloton didn't anticipate was just how transformative this would be.

Once Peloton decided to use Affirm's 0% APR financing option as a customer acquisition tool, Affirm sales exploded, now accounting for close to 30% of Peloton's monthly online business sales, up from 15% at launch. Think about that trajectory—doubling the financing penetration rate in a matter of months. "We were worried that 0% APR financing would cannibalize our credit card sales," said Jiang. "But that hasn't been the case, and we're selling bikes to customers that might never have otherwise been purchased."

The economics were elegant in their simplicity. Peloton would subsidize the 0% APR loans by paying Affirm a merchant fee—essentially trading margin for volume and customer acquisition. Peloton paid Affirm more than $50 million just in the third quarter of this year. For Peloton, this was customer acquisition cost. For Affirm, it was rocket fuel.

By 2020, the relationship had deepened to an almost symbiotic level. Our top merchant partner, Peloton, represented approximately 28% of our total revenue for the fiscal year ended June 30, 2020 and 30% of our total revenue for the three months ended September 30, 2020. The pandemic had turned Peloton from a luxury fitness brand into a necessity for millions of locked-down Americans, and Affirm was there to make it affordable.

But here's where the story gets complicated. Revenue concentration at this level—nearly a third of your business from a single partner—is the kind of dependency that makes investors nervous. Notably the unicorn's next nine largest customers are worth just 7% of its revenue, meaning that Affirm really has a singular-company risk; if Peloton drops Affirm, or sees its own sales slow, our fintech startup could be sharply undercut.

The comparison to other tech companies was unavoidable. Because investors have a few recent examples of tech companies going public on the back of attractive growth, only to lose a single, key customer, blowing a hole in their ability to grow. It happened to Twilio regarding Uber (more here), and it happened to Fastly and its customer TikTok even more recently.

Yet Levchin and his team saw the Peloton concentration not as a bug but as a feature—proof that Affirm could handle enterprise-scale partnerships, complex integrations, and massive transaction volumes. The Peloton relationship demonstrated something crucial: when given the choice between traditional credit and transparent financing, consumers overwhelmingly chose transparency, even when they had access to credit cards.

Affirm has a longstanding deal with Peloton, which has been growing so fast during the pandemic that it now accounts for 30% of Affirm's revenues. Peloton buyers are often older and richer than the core Affirm customer base, and more likely to be happy to use credit cards. But given the option to get 0% financing on their exercise bike, they'll take it.

The partnership also revealed an unexpected insight about consumer behavior. These weren't subprime borrowers who couldn't get credit elsewhere. These were affluent consumers who could afford to pay cash but chose financing because it was transparent and fair. It validated Levchin's core thesis: the problem with credit cards wasn't access—it was trust.

By late 2020, as Affirm prepared for its IPO, the Peloton partnership had become both its greatest asset and its most significant risk factor. The loss of Peloton as a merchant partner, or the loss of any other significant merchant relationships, would materially and adversely affect our business, results of operations, financial condition, and future prospects.

The market would soon test this dependency. When Peloton's growth began to slow in late 2021 as gyms reopened, Affirm's stock took a hit. But by then, Levchin had learned the crucial lesson from the Peloton partnership: product-market fit in fintech isn't just about the technology or the terms—it's about finding the perfect merchant partner who understands that financing isn't a necessary evil but a growth accelerator.

The Peloton partnership had proven that BNPL could work at scale, handle high-ticket items, and actually improve both merchant economics and consumer satisfaction. Now it was time to take that playbook and expand it across the entire e-commerce ecosystem. The next chapter would be about reducing concentration risk while maintaining the magic of the merchant-consumer-Affirm triangle.

V. Scaling the Network: From DTC to Platform

The meeting took place in a nondescript conference room in San Francisco's Financial District in early 2020. Max Levchin and Tobi Lütke, Shopify's CEO, were sketching out what would become the most significant platform deal in BNPL history. The pandemic had just begun transforming e-commerce, and both men sensed an opportunity to redefine online payments at scale.

In November 2016, Affirm announced the availability of its buy now, pay later (BNPL) service for retailers using the e-commerce platforms of "Kibo Commerce", BigCommerce, "AspDotNetStorefront" and Zen Cart. By that time, Affirm's service was also available for the Salesforce Commerce Cloud, Magento and Shopify. But these early integrations were just table stakes—what Levchin envisioned was something far more ambitious.

The insight was architectural: instead of signing up merchants one by one, why not embed Affirm directly into the commerce infrastructure itself? Early on, Affirm found a different way to acquire users, by partnering with retailers to offer a loan at point of sale. This wasn't just about distribution; it was about becoming invisible infrastructure, as essential and unnoticed as the payment rails themselves.

Eligible merchants will be able to seamlessly offer pay-over-time option to customers at check out SAN FRANCISCO — July 22, 2020 — Affirm , a more transparent, flexible alternative to credit cards, announced it will exclusively power Shopify's Shop Pay Installments in the United States. The exclusivity was crucial—it meant that Shopify's millions of merchants would have one BNPL partner, creating unprecedented scale overnight.

"This includes embracing the rising importance of e-commerce strategies and meeting consumers, particularly young shoppers, where they are," said Max Levchin, Founder and CEO of Affirm. "By partnering with Shopify, the gold standard of commerce platforms for businesses that want to sell direct-to-consumers, we can help merchants seamlessly enable a pay-over-time option at checkout. In doing so, we're helping them reach new customers, particularly Gen Z and Millennials, who are looking for more transparent and flexible ways to pay."

The technical implementation was deceptively complex. Starting later this year, Affirm's buy now, pay later financing solution will be made available to eligible Shopify merchants in the U.S. who want to offer this flexible payment option to their customers. At checkout, approved Shop Pay customers will be able to split their total purchase amount into four equal, bi-weekly, interest-free payments. This meant building real-time underwriting that could handle millions of transactions across hundreds of thousands of merchants, each with different risk profiles and customer bases.

But the real innovation wasn't technical—it was the business model alignment. Eligible U.S. Shopify merchants who elect to offer Shop Pay Installments to their customers will not have to worry about collecting future payments from customers. They will receive the full purchase amount, less fees, upfront, and Affirm will handle payment collection. Affirm was taking on all the credit risk, all the servicing complexity, in exchange for becoming the default financing option for an entire generation of direct-to-consumer brands.

According to Racked in November 2017, Affirm had launched an app which allowed consumers to take out loans for purchases at any retailer. The company aimed at "building and perfecting a new underwriting system", powered by machine learning, to determine consumer creditworthiness. This virtual card capability meant consumers could use Affirm anywhere, not just at integrated merchants—a crucial step toward ubiquity.

The platform strategy extended beyond Shopify. Walmart was a different beast entirely. Affirm was founded in 2012 by Max Levchin, Nathan Gettings, Jeffrey Kaditz, and Alex Rampell as part of the initial portfolio of startup studio HVF. Levchin, who co-founded PayPal, became CEO of Affirm in 2014. By 2019, Affirm announced a partnership with Walmart, making its service available at self-checkout kiosks in stores and on the Walmart website. This wasn't just about online anymore—it was about meeting consumers wherever they shopped.

The numbers told the story of explosive growth. Affirm changed its growth strategy to acquire merchants at a rapid pace – instead of directly going to merchants; Affirm engaged in partnerships with large platforms that serve online businesses. For example – in August 2020, Affirm announced a partnership with Shopify, under which Affirm's BNPL financing solution will be made available to eligible Shopify merchants in the U.S. – this led to an exponential increase in the number of merchant partners.

U.S., has enabled more than 100,000 Shopify merchants to seamlessly offer millions of consumers the ability to split purchases up to $3,000 into four interest-free biweekly payments with no fees. From a handful of direct merchant relationships to over 100,000 through a single platform partnership—this was the power of becoming infrastructure.

The strategic expansion continued with a crucial innovation: Adaptive Checkout. U.S. merchants offering Shop Pay Installments will have access to Affirm's Adaptive Checkout™, a first-of-its-kind product in the U.S., which dynamically offers biweekly and monthly payment options side-by-side in a single integrated checkout. This meant Affirm could serve both small impulse purchases and large considered purchases through the same integration, dramatically expanding the addressable market.

Since its launch in 2021, Shop Pay Installments has been rapidly adopted, with millions of consumers using the payment option across Shopify's extensive merchant network in the... The adoption curve was steeper than anyone anticipated. Merchants who had never considered offering financing suddenly found it was just a toggle switch away.

The platform partnerships created powerful network effects. Each new merchant brought new consumers to Affirm. Each returning consumer became more likely to seek out Affirm at other merchants. The company had solved the chicken-and-egg problem that plagues most two-sided marketplaces by partnering with platforms that already had both sides at scale.

By 2022, the strategy had proven so successful that Shopify and Affirm extended their partnership globally. The renewed multi-year partnership cements Affirm's position as the exclusive pay-over-time provider for Shop Pay Installments in the U.S. It also extends this exclusivity into Shopify's home market of Canada and enables the partnership to continue growing into new markets worldwide, with plans to enter the U.K. on the horizon.

The transformation was complete: Affirm had evolved from a direct-to-consumer lender to a payments infrastructure company. The next challenge would be even bigger: competing with the tech giants themselves as they entered the BNPL space.

VI. The IPO and Public Market Debut

The scene was surreal: Max Levchin sitting in his San Francisco home office at 4:30 AM on January 13, 2021, watching pre-market trading indicators while his two young children slept upstairs. After nearly a decade of building Affirm, the moment of truth had arrived. The numbers on his screen were almost incomprehensible.

Affirm had priced its shares at $49 apiece, above its target range of $41 to $44 each. But that was just the beginning. The stock began trading at $90.90 per share and closed at $97.24. In a single day, Affirm's market value had soared to $23.6 billion. Levchin's stake, 27.5 million shares, was suddenly worth over $2.5 billion.

The journey to this moment had been anything but smooth. On November 18, 2020, Affirm filed with the Securities and Exchange Commission in preparation for an initial public offering (IPO). On December 12, 2020, it was reported that Affirm had postponed its IPO. The delay was telling—Affirm had watched Airbnb's December IPO soar 135% on its first day and realized the market was dramatically underpricing tech offerings.

Affirm had proposed listing its shares in the $33 to $38 range prior to its aborted December listing, while news reports earlier this week predicted it would list at $41 to $44. The continuous upward revisions reflected both market froth and genuine investor excitement about the BNPL opportunity. The IPO, the largest U.S. listing so far in 2021, signals that investor appetite for new stocks remains robust following a stellar 2020, which was the strongest IPO market in two decades.

But beneath the celebration lay complex questions about Affirm's business model and path to profitability. All of this could make it harder for Affirm, which lost $112 million in its last fiscal year, to one day earn a profit. The company's financials revealed both promise and peril: explosive growth fueled by pandemic e-commerce acceleration, but also significant losses and that nagging Peloton concentration risk.

"Today is the result of years of work by hundreds of dedicated Affirmers who believe in honest and transparent finance. And although there is more work to be done, today offers an opportunity to reflect and celebrate," Max Levchin, founder and CEO of Affirm, said in a tweet. Behind the corporate speak was genuine emotion—this was vindication for a decade-long bet that consumers would choose transparency over traditional credit.

In an interview with Fortune, Levchin reiterated his familiar mantra that the credit card industry is deceitful and immoral, and that Affirm offers a way to provide consumers credit with dignity. "We don't profit from our customers mistakes and misfortunes. The entire premise of the credit card industry is based on late fees." It was classic Levchin—framing a business model as a moral crusade.

The market's reaction reflected both the BNPL gold rush and something deeper: a generational shift in how consumers thought about credit. Founded in 2012, Affirm now has over 6 million customers, and provides its pay-as-you-go offering to a wide range of merchants from discount sellers to luxury purveyors. The company recently expanded its reach through a partnership with online retail giant Shopify.

The timing couldn't have been better—or more precarious. Pandemic tailwinds and e-commerce acceleration had created perfect conditions for BNPL adoption. Online shopping had exploded, traditional credit card applications had plummeted among younger consumers, and merchants desperate for sales were willing to pay higher fees for guaranteed conversion.

But challenges loomed on the horizon. These include a new competing product from Levchin's alma mater, PayPal, as well as the prospect of merchants pushing back against its fees—much as they have done against credit card companies in recent years. Competition was intensifying from every direction: Klarna from Europe, Afterpay from Australia, and rumors that Apple was developing its own BNPL product.

The fintech makes most of its money from merchant fees so customers can pay zero interest. Loans which bear interest scratch late fees. This dual revenue model—merchant fees for 0% loans, interest income for longer-term financing—was both Affirm's strength and its vulnerability. Rising interest rates could squeeze margins, while an economic downturn could spike defaults.

For Levchin, it marks almost two decades since PayPal went public. He owned a stake in Affirm worth almost $1.4 billion at its IPO price. The CEO now has an estimated net worth of $6.6 billion, according to CNBC. But wealth wasn't the point—or at least not the only point. Levchin had already made his fortune at PayPal. This was about proving something bigger.

In the long-term, Levchin has mulled the idea of becoming a licensed bank. He tells the Financial Times: "I'm still evaluating and learning." The comment revealed Affirm's ultimate ambition: not just to disrupt credit cards but to reimagine consumer banking itself.

Public market volatility would soon test Affirm's narrative. By late 2021, as interest rates began rising and tech stocks crashed, Affirm's share price would plummet from its peaks. But on that January morning in 2021, watching his company's valuation double in hours, Levchin had proven that Wall Street believed in the anti-credit card thesis. Now came the hard part: proving it could actually work as a public company.

VII. The Amazon Partnership: Reaching Scale

The call came on a Thursday evening in August 2021. Max Levchin was driving home from Affirm's San Francisco office when Eric Morse, his head of sales, called with news that would redefine the company's trajectory: "Amazon wants to do a deal. They want exclusivity. And they want to launch in weeks, not months."

Affirm (NASDAQ: AFRM), the payment network that empowers consumers and helps merchants drive growth, today announced that its flexible payment solution will soon be available to Amazon.com customers at checkout. Amazon and Affirm are testing with select customers now, and in the coming months, Amazon plans to make Affirm more broadly available to its customers.

The timing was electric. The deal was announced Friday, sending Affirm shares up as much as 50% in after-hours trading. Shares of Affirm on Monday closed up 46.67% after the buy now, pay later platform announced a partnership with Amazon. In a matter of hours, Affirm's market capitalization had increased by over $8 billion.

But the real significance went far beyond stock price movements. It also marks Amazon's first partnership with an installment player, though the company already offers installment options on some items. For Amazon, the world's largest e-commerce platform, to choose Affirm as its exclusive BNPL partner was validation of the highest order.

As a result of Amazon and Affirm's partnership, select Amazon customers now have the option to split the total cost of purchases of $50 or more into simple monthly payments by using Affirm. Approved customers are shown the total cost of their purchase upfront and will never pay more than what they agree to at checkout. As always, when choosing Affirm, consumers will not be charged any late or hidden fees.

The integration challenges were staggering. Amazon processes millions of transactions daily across thousands of product categories, each with different risk profiles. Affirm's underwriting models, which had worked brilliantly for Peloton bikes and Shopify merchants, now had to instantly evaluate everything from electronics to groceries to books.

"By partnering with Amazon we're bringing the transparency, predictability and affordability that Affirm provides today to the millions of people who shop on Amazon.com in the U.S.," Affirm Senior Vice President of Sales Eric Morse said in a Friday (Aug. 27) announcement. "Offering Affirm's alternative to credit cards also delivers more of the payment choice and flexibility consumers on Amazon want."

Analysts at Bank of America called the news an "unambiguous positive," but said it highlights Affirm's "technological leadership and strong reputation in the BNPL market." The analyst community understood what this meant: Affirm had won the BNPL wars, at least in the United States.

The competitive implications were seismic. This month, Square announced it was entering the space through a $29 billion purchase of Afterpay. Bloomberg News previously reported Apple is also planning its own installment partnership with Goldman Sachs. Every major tech and financial company was rushing into BNPL, but Affirm had secured the most valuable real estate in e-commerce.

The expansion didn't stop at consumer purchases. Today, Amazon (NASDAQ:AMZN) and Affirm (NASDAQ: AFRM) announced an expanded partnership that makes Affirm the first pay-over-time option available at checkout on Amazon Business, a business-to-business (B2B) store that helps businesses of all sizes digitize and automate procurement with powerful management controls and analytic tools—all within the familiar experience of Amazon. Now, these Amazon Business customers can split the total cost of eligible purchases and pay over time with Affirm without late or hidden fees. Amazon Business will start to roll out Affirm today to eligible sole proprietor businesses, and the new payment option will be available at checkout to all eligible Amazon Business sole proprietor customers by Black Friday.

This marks the launch of Affirm's new B2B pay-over-time solution dedicated to serving sole proprietors. The move into B2B represented a massive expansion of Affirm's addressable market. Amazon cited data from the IRS and reported that over 28 million sole proprietorships operate in the United States.

"Integrating Affirm as a payment option helps us do just that, while providing more flexibility and convenience to our customers," said Todd Heimes, director of Amazon Business Worldwide. The partnership had evolved from a consumer product to critical business infrastructure.

The evolution of the partnership showed remarkable velocity. Affirm initially launched on Amazon.com and the Amazon mobile app in 2021. Since then, it has expanded to Amazon in Canada in 2022 and was directly integrated as a payment option on Amazon Pay earlier in 2023. Customers seeking to use Affirm on Amazon Business can do so through the Amazon Business website and the Amazon Business mobile app.

Affirm said some of the Amazon customer loans will bear interest, but some will come with 0% APR. This flexibility—offering both promotional 0% financing and interest-bearing loans—allowed Affirm to serve a broader range of transactions and risk profiles than competitors locked into a single model.

The Amazon partnership also revealed a crucial strategic insight: in the platform economy, being first mover with the right partner matters more than being perfect. While competitors like Klarna had more international presence and Afterpay had stronger brand recognition among younger consumers, Affirm had the technology and risk management capabilities that Amazon trusted.

According to Payments Dive in October 2022, Bank of America Securities identified Affirm as the "most frequently used" BNPL app in the US with a 30% market share, while noting a slowdown in BNPL sector growth in the US and worldwide. The Amazon partnership had cemented Affirm's position as the market leader.

But success brought new challenges. The partnership meant Affirm was now processing transactions at unprecedented scale, requiring massive investments in infrastructure and risk management. Every basis point of loss rate mattered when you were financing millions of Amazon purchases. The company that had built its reputation on careful, transaction-by-transaction underwriting now had to operate at the speed and scale of Amazon.

The Amazon partnership represented both the culmination of Affirm's platform strategy and the beginning of a new chapter. Breaking into mainstream retail and what it means for BNPL had been achieved. Now the question was whether Affirm could maintain its underwriting discipline and customer-first ethos while operating as critical infrastructure for the world's largest retailer.

VIII. Beyond Consumer: The Business Expansion

The conference room at Affirm's New York office overlooked Madison Square Park, where food trucks served lunch to lines of office workers paying with corporate cards. Watching this scene in early 2023, Libor Michalek, Affirm's President of Technology, turned to his team with a question: "Why are we only disrupting consumer credit? Every one of those business purchases could be an Affirm transaction."

This marks the launch of Affirm's new B2B pay-over-time solution dedicated to serving sole proprietors. The move into business lending wasn't just an expansion—it was a recognition that the problems plaguing consumer credit—opacity, predatory terms, complex fee structures—were equally prevalent in small business finance.

The partnership marks the debut of Affirm's B2B pay-over-time solution for sole proprietors, per the release. After picking Affirm at checkout on Amazon Business and entering some information, small business owners will receive an instant credit decision and can choose from pay-over-time installments of three to 48 months if approved, according to the release. "For example, a $200 purchase at 15% APR would cost a customer $34.81 for six months, totaling $208.84," the release said.

The sole proprietor market was massive and underserved. Amazon cited data from the IRS and reported that over 28 million sole proprietorships operate in the United States. By extending an adaptable payment solution for these businesses, Affirm and Amazon Business aim to provide them with increased purchasing capabilities, improved cash flow management, and better growth opportunities.

But the real innovation wasn't just offering credit to businesses—it was recognizing that the line between consumer and business purchases had blurred. A graphic designer buying a laptop, a ride-share driver purchasing floor mats, a food delivery person getting insulated bags—these were business expenses that looked like consumer purchases.

According to CNBC in October 2021, Affirm had partnered with Target, and also with Apple, to offer financing services. Each partnership expanded Affirm's reach, but more importantly, each taught the company something new about different customer segments and use cases.

The Stripe partnership announced in May 2022 was particularly strategic. In May 2022, Affirm signed a partnership with digital payments processor Stripe, Inc. to make its "adaptive checkout" service available to Stripe users in the US. By integrating with Stripe, Affirm instantly became available to millions of online businesses that used Stripe for payment processing. This wasn't just distribution—it was becoming the default financing option for the internet economy.

The network effects were becoming undeniable. Each new merchant brought new consumers. Each returning consumer became more likely to seek out Affirm at other merchants. The company had solved the classic marketplace chicken-and-egg problem by partnering with platforms that already had both sides at scale.

In June 2024, Apple announced a partnership with Affirm, allowing U.S. users to apply for Affirm's loans through Apple Pay, and subsequently revealed plans to shut down its own "Pay Later" service. According to CNBC, Affirm was slated to "surface" as an option for U.S. Apple Pay users on iPhones and iPads later in the year. This was perhaps the ultimate validation: Apple, which rarely partners with anyone, had chosen Affirm over building its own solution.

The expansion into travel and experiences represented another frontier. Then, in September 2023, online travel platform Booking.com joined Affirm's payment network, which also included American Airlines, Cathay Pacific, CheapOair and Vacasa. Financing a vacation or flight was different from financing a product—the purchase was consumed before it was paid off, requiring different underwriting models and risk assessments.

The company's expanded partnership with Amazon comes as small- to medium-sized businesses (SMBs) are seeking new avenues of funding as traditional sources of financing dry up. "SMBs may be driven by a sense of urgency, as only 26% have access to the equivalent of at least 60 days' worth of revenue, and 17% have no ready access to emergency funding," PYMNTS wrote last month.

The business model expansion revealed a deeper truth about Affirm's strategy. The company wasn't just building a BNPL product—it was building a new payment network, one that could handle any transaction type, any ticket size, any customer segment. The technology stack that powered this—real-time underwriting, dynamic pricing, instant funding—was the real moat.

In May 2023, payment processor Worldpay launched a partnership with Affirm, enabling Worldpay merchants to use Affirm's payment services. The company reported over 17 million consumers and 279,000 merchants, and processed an annual gross merchandise volume (GMV) of $20.2bn for its fiscal year ending June 30, 2023.

Building the merchant ecosystem and network effects had transformed Affirm from a lender into a platform. The company now operated a two-sided network where each additional participant—merchant or consumer—made the network more valuable for everyone else. This was the holy grail of fintech: becoming so embedded in the transaction flow that removing you would be unthinkable.

The challenges of this expansion were significant. Business lending required different regulatory compliance, different underwriting models, different servicing capabilities. But Affirm's investment in technology and infrastructure over the years had created a platform flexible enough to handle these variations.

By 2024, Affirm had evolved far beyond its origins as a point-of-sale lender. It was now critical infrastructure for American commerce, processing billions in transactions across every category imaginable. The next challenge would be even more daunting: navigating an increasingly complex regulatory landscape while fending off competition from both fintech startups and traditional financial institutions.

IX. Regulatory Challenges & Industry Evolution

The letter arrived at Affirm's headquarters on December 16, 2021, bearing the seal of the Consumer Financial Protection Bureau. As Max Levchin read through the 16-page order, he recognized this moment had been inevitable. The BNPL industry had grown too big, too fast, to escape regulatory scrutiny.

Today the Consumer Financial Protection Bureau (CFPB) issued a series of orders to five companies offering "buy now, pay later" (BNPL) credit. The orders to collect information on the risks and benefits of these fast-growing loans went to Affirm, Afterpay, Klarna, PayPal, and Zip. The CFPB is concerned about accumulating debt, regulatory arbitrage, and data harvesting in a consumer credit market already quickly changing with technology.

The timing was brutal. Affirm's stock had been riding high after the Amazon partnership, but Shares of Affirm, which went public in January, plunged more than 10% following the CFPB news. The market's reaction reflected deep uncertainty about what regulatory intervention might mean for the entire BNPL sector.

"Buy now, pay later is the new version of the old layaway plan, but with modern, faster twists where the consumer gets the product immediately but gets the debt immediately too," said CFPB Director Rohit Chopra. The comparison to layaway was telling—it positioned BNPL as an evolution of a familiar concept rather than a dangerous new form of credit, but the "debt immediately" framing suggested concern.

Levchin's response was characteristically measured but firm. A spokesperson for Affirm said in an email to CNN Business that "we welcome the CFPB's review and support regulatory efforts that benefit consumers and promote transparency within our industry". The Affirm spokesperson added that the company has "never charged a late or hidden fee, ever" and that "we will continue to engage with all of our stakeholders, including regulators, to support efforts that advance our mission."

The CFPB's concerns were specific and substantive. Accumulating debt: Whereas the old-style layaway installment loans were typically used for the occasional big purchase, people can quickly become regular users of BNPL for everyday discretionary buying, especially if they download the easy-to-use apps or install the web browser plugins. The specter of consumers juggling multiple BNPL loans across different providers, creating a debt spiral invisible to traditional credit reporting, was real.

Regulatory arbitrage: Some BNPL companies may not be adequately evaluating what consumer protection laws apply to their products. For example, some BNPL products do not provide certain disclosures, which could be required by some laws. And while the BNPL application may look similar to a standard checkout with a credit card, protections that apply to credit cards may not apply to BNPL products. Many BNPL companies do not provide dispute resolution protections available to users of other forms of credit, like credit cards.

The political pressure was intensifying from multiple directions. Six U.S. senators, including Elizabeth Warren (D-Mass.), the architect of the CFPB, called for strengthening oversight of BNPL products and providers. "While the emergence of BNPL as affordable small-dollar credit has potentially provided an alternative to more costly forms of credit, these products also have the potential to cause consumer harm," the lawmakers wrote in a letter to the CFPB this month.

The industry's response revealed both unity and division. "For nearly a decade, Affirm has been advancing its mission to deliver honest financial products that improve lives, and we have never charged a late fee or hidden fee, ever," the company said in a statement. This positioning—Affirm as the responsible actor in a potentially irresponsible industry—would become central to its regulatory strategy.

In September 2022, the CFPB published its findings. The Consumer Financial Protection Bureau (CFPB) published a report offering key insights on the Buy Now, Pay Later industry. The report,Buy Now, Pay Later: Market trends and consumer impacts , finds that industry grew rapidly during the pandemic, but borrowers may receive uneven disclosures and protections. The five firms surveyed in the report originated 180 million loans totaling over $24 billion in 2021, a near tenfold increase from 2019.

The data revealed concerning trends. Late fees are becoming more common: 10.5% of unique users were charged at least one late fee in 2021, up from 7.8% in 2020. But Affirm could point to a crucial distinction—it didn't charge late fees at all, setting it apart from competitors who relied on penalty revenue.

The credit reporting challenge was particularly complex. Until recently, few BNPL lenders furnished information about consumers to the nationwide consumer reporting companies (NCRCs). This lack of furnishing could have downstream effects on consumers and the credit reporting system. It could be bad for BNPL borrowers who pay on time and may be seeking to build credit, since they may not benefit from the impact that timely payments may have on credit reports and credit scores. It may also impact both BNPL lenders and non-BNPL lenders seeking to understand how much debt a prospective borrower is carrying.

According to a Payments Dive article in May 2023, Affirm stated that it was partnering with data analytics company FICO to create a "BNPL credit-scoring model", while noting the CFPB's concerns around the "lack of information being furnished in the BNPL space". This proactive approach—working with the credit bureaus rather than fighting them—distinguished Affirm's regulatory strategy.

To address the discrete consumer harms, the CFPB will identify potential interpretive guidance or rules to issue with the goal of ensuring that Buy Now, Pay Later lenders adhere to many of the baseline protections that Congress has already established for credit cards. The threat was clear: BNPL could be regulated like credit cards, potentially destroying the business model's economics.

But Affirm had been preparing for this moment since its founding. The company's infrastructure—real-time underwriting, transparent pricing, no late fees—was built with regulatory compliance in mind. While competitors scrambled to adapt, Affirm could argue it had always operated by the principles regulators were now trying to enforce.

Rising interest rates added another layer of complexity. As the Federal Reserve hiked rates to combat inflation, Affirm's cost of capital increased dramatically. The company's ability to offer 0% promotional financing depended on merchant subsidies, but merchants facing their own margin pressures were less willing to pay high fees.

Competition from Apple Pay Later and bank offerings represented a different kind of threat. When traditional financial institutions entered BNPL, they brought regulatory compliance but also deep pockets and existing customer relationships. Affirm's advantage—being the anti-bank—became less compelling when banks themselves offered transparent installment options.

The regulatory evolution of BNPL revealed a fundamental tension: how to protect consumers without stifling innovation. Affirm's approach—embracing regulation while maintaining its consumer-first principles—positioned it as the responsible actor in a rapidly maturing industry. But whether that positioning would translate to sustainable competitive advantage remained an open question.

X. Business Model & Unit Economics Deep Dive

The spreadsheet on Michael Linford's screen told a story of financial engineering at its finest. Affirm's CFO was walking investors through the company's third-quarter 2023 results, and the numbers revealed both the elegance and complexity of the BNPL business model. Revenue Less Transaction Costs—Affirm's key metric—had reached $187 million for the quarter, but understanding what that meant required peeling back layers of financial innovation.

The company generates revenue by applying a service fee to sellers, charging interest to borrowers, or both, and does not charge a late fee. This dual revenue stream was the key to Affirm's unit economics. On a $1,000 Peloton bike financed at 0% APR over 12 months, Affirm might earn $60-80 from Peloton in merchant fees—a 6-8% take rate that Peloton gladly paid for the increased conversion.

But the real sophistication lay in the risk stratification. Affirm earns interest income on the simple interest loans from originating bank partners and on the merchant site, Affirm earns a merchant fee for its services. Per Form 10K, "Our business model is aligned with the interests of both consumers and merchants — we win when they win. From merchants, we earn a fee when we help them convert a sale and power a payment. Merchant fees depend on the individual arrangement between us and each merchant and vary based on the terms of the product offering; we generally earn larger merchant fees on 0% APR financing products. For both the fiscal years ended June 30, 2021 and 2020, 0% APR financing represented 43% of total Gross Merchandise Volume ("GMV") facilitated through our platform. This structure incentivizes us to help our merchants convert sales and increase AOV through the commerce and technology solutions offered by our platform.

The underwriting technology was where Affirm's PayPal DNA showed most clearly. The lender says its loan underwriting involves evaluating transactions by considering credit scores and other pertinent factors, while also incorporating machine learning. Every transaction generated hundreds of data points—not just credit scores but purchase history, merchant category, time of day, device type, even typing patterns. The models had been trained on millions of transactions, learning the subtle differences between a consumer buying a necessity versus a luxury, a gift versus personal use.

"We underwrite every single transaction at the time of purchase," Wayne Pommen, Affirm's Chief Revenue Officer, explained to investors. Our economic model has never relied on late fees. We've never charged a single one in the history of the company. That means we need to be really good at underwriting. We underwrite every single transaction at the time of purchase to make sure we understand what the customer is buying and what particular financial shape they're in at that time. That really allows us to control risk.

The capital markets strategy was equally sophisticated. Affirm operated multiple funding channels simultaneously: warehouse credit facilities for immediate liquidity, forward flow agreements with banks for predictable funding, and ABS (asset-backed securities) markets for efficient capital recycling. Additionally, the report cited Affirm as an unsecured loan lender which funded about a third of its business through securitizations.

The securitization process itself was a marvel of financial engineering. Affirm would originate loans, season them for a few months to establish payment patterns, then bundle them into securities sold to institutional investors. The best-performing loans—those 0% APR Peloton purchases by prime borrowers—might price at SOFR + 150 basis points. The riskier tranches—longer-term, interest-bearing loans to subprime borrowers—might require SOFR + 500 basis points or more.

But here's where it got interesting: Affirm retained the servicing rights and often kept a vertical slice of each securitization, aligning its interests with investors. If loans performed poorly, Affirm felt the pain first. This skin-in-the-game approach gave investors confidence and kept funding costs relatively low.

The path to profitability had been long and winding. Calendar Q4 2020 net losses as a percentage of its revenue: 8.8%. Why did we do all of that? Isn't it blindingly obvious that if Affirm were racking up contribution margin (gross margin) improvements and revenues were rising, net margins would improve? No. Never presume operating leverage in a unicorn. It must be proven. We can now trace the rapid improvement of Affirm's net margins back to its growth (GMV, revenue) and improving economics.

The unit economics had improved dramatically since the early days. In 2019, Affirm's Revenue Less Transaction Costs (RLTC) as a percentage of GMV was 2.9%. By 2023, it had expanded to 3.8%. This might seem like a small change, but on $20 billion of GMV, each basis point of improvement was worth $2 million in gross profit.

The merchant fee structure revealed strategic thinking. Affirm charged different rates based on AOV (average order value), product category, and merchant size. A small DTC brand might pay 6-8% for 0% APR financing. Walmart might pay 3-4%. Amazon likely paid even less. But the volume from Amazon more than made up for the lower margins—classic platform economics.

Interest income added another layer of complexity. On longer-term loans where consumers paid interest, Affirm's average APR was around 15%, but this varied widely. A 3-month loan might carry 0% APR (fully merchant-subsidized), while a 48-month loan for the same consumer might be priced at 25% APR. The pricing algorithm considered not just credit risk but also competitive dynamics, merchant relationships, and portfolio composition targets.

The servicing operation was surprisingly capital-light. Unlike traditional lenders with armies of collection agents, Affirm's servicing was largely automated. Payment reminders went out via text and email. Failed payments triggered instant retry logic. The self-service portal let consumers adjust payment dates or amounts. Only the most complex cases required human intervention.

Loss rates told a story of disciplined underwriting. Through the pandemic boom and subsequent normalization, Affirm's charge-off rates remained remarkably stable at 2-3% of GMV. Compare that to credit card charge-offs averaging 3-4% or subprime auto loans at 7-10%, and Affirm's underwriting prowess becomes clear.

But the most important metric might be customer acquisition cost (CAC). Through platform partnerships, Affirm's CAC was essentially zero for new consumers—they discovered Affirm at checkout, not through paid marketing. The lifetime value to CAC ratio, the holy grail of unit economics, was off the charts for platform-acquired customers.

Lenders' profit margins are shrinking: Margins in 2021 were 1.01% of the total amount of loan originated, down from 1.27% in 2020. This margin compression reflected both competitive pressure and mix shift toward lower-margin, higher-volume partnerships. But Affirm was betting that scale would more than compensate—a 1% margin on $50 billion of GMV was far better than 2% margin on $10 billion.

The path forward was clear but challenging: continue expanding GMV through platform partnerships, improve RLTC margins through better underwriting and operational efficiency, and manage funding costs through diversified capital sources. The unit economics worked, but only at scale. Affirm had crossed that threshold, but maintaining momentum while preserving underwriting discipline would determine whether the business model was truly sustainable.

XI. Playbook: Lessons for Founders & Investors

The conference room at Affirm's headquarters has witnessed countless product debates, but this one in 2019 was different. Max Levchin was sketching furiously on the whiteboard, explaining to his leadership team why they needed to start building their next S-curve three years before the current one peaked. "If you're not thinking about your next S curve at least three years in advance, you're too late," he would later tell founders seeking his advice.

Building Trust Through Transparency

The first lesson from Affirm's journey is counterintuitive: in financial services, radical transparency can be a competitive advantage, not a liability. "For nearly a decade, Affirm has been advancing its mission to deliver honest financial products that improve lives, and we have never charged a late or hidden fee, ever." This wasn't just marketing—it was product architecture. Every system, every line of code, every partnership agreement was built around this principle.

The power of this approach became clear during merchant negotiations. While competitors had to explain complex fee structures and revenue-sharing arrangements, Affirm's pitch was simple: we make money when you make money. No hidden economics, no misaligned incentives. This transparency extended to consumers, investors, and even regulators, creating trust that money couldn't buy.

The Power of Exclusive Partnerships and Concentration Risk

The Peloton concentration—reaching 30% of revenue—would terrify most investors. But Levchin understood something crucial: in marketplace businesses, concentration can be a feature, not a bug, if managed correctly. The Peloton partnership proved Affirm could handle enterprise-scale operations, complex integrations, and massive transaction volumes. It was a reference customer worth its weight in gold.

The playbook: start with one anchor tenant who validates your model, use that success to attract similar partners, then gradually diversify. By the time investors worried about Peloton concentration, Affirm had already signed Amazon and Shopify. Concentration risk became diversification opportunity.

Timing the Market: Why BNPL Worked When It Did

Three forces converged to create the perfect conditions for BNPL: the death of retail loyalty to credit card rewards, the rise of millennial debt aversion, and the platformization of commerce. Affirm didn't create these trends—it surfed them.

Levchin's insight from his PayPal days proved crucial: payments innovation follows commerce innovation by about five years. As e-commerce went from desktop to mobile to social, payment methods needed to evolve. Credit cards, designed for physical plastic and signature verification, were increasingly anachronistic in a world of one-click checkout.

Platform vs. Product: When to Expand Horizontally

"Many of my formative conversations about leadership began with Peter Thiel, my co-founder at PayPal. He truly has an amazing capacity to bring out the very best in the people he surrounds himself with," Levchin reflected. One lesson from Thiel that proved crucial: don't expand horizontally until you've dominated vertically.

Affirm spent years perfecting point-of-sale lending before launching the virtual card. Years building merchant integrations before becoming a platform. Years serving consumers before expanding to businesses. Each horizontal expansion was built on a foundation of vertical dominance.

Managing Regulatory Risk in Fintech

The approach to regulation revealed sophisticated thinking about stakeholder management. Instead of the typical Silicon Valley "ask forgiveness, not permission" mentality, Affirm engaged proactively with regulators. The company's infrastructure—real-time underwriting, transparent pricing, no late fees—anticipated regulatory requirements before they were mandated.

When the CFPB came calling, Affirm could honestly say it already operated by the principles regulators wanted to enforce. This wasn't regulatory capture—it was regulatory alignment. Build the product regulators wish existed, and regulation becomes a competitive moat, not a burden.

The Importance of Founder-Led Companies in Complex Industries

"If you expect your team to work over the weekend, you show up to the office with them and work even harder. As a leader you better be in the same trenches as your crew, otherwise they won't believe in the importance and value of the product your company is building," Levchin emphasized.

During the 2024 layoffs, Levchin didn't hide in his office. "Go be with the people. It'll feel better in the end, and they will feel better in the end," the PayPal cofounder said. He helped laid-off employees pack their boxes, finding the experience "between cathartic and therapeutic." This hands-on leadership style—technical founder as moral compass—proved essential in an industry built on trust.

The founder's technical background mattered enormously. Levchin could personally evaluate underwriting models, debate system architecture, and understand the nuances of capital markets. In fintech, where technology and finance intersect at every decision, having a founder who deeply understood both domains was invaluable.

Key Tactical Lessons

He will also explain why he believes that entrepreneurship is an endurance sport and that having a passion for the problem is paramount to the longevity of any startup founder. Levchin's endurance showed in his approach to building Affirm: patient capital deployment, long-term partnership thinking, and willingness to absorb losses while perfecting the model.

The unit economics formula that emerged: - Customer acquisition through platforms (CAC ≈ $0) - Dual revenue streams (merchant fees + consumer interest) - Automated servicing (minimal human intervention) - Disciplined underwriting (2-3% loss rates) - Capital recycling through securitization

The Anti-Pattern Lessons

What Affirm didn't do is equally instructive. They didn't: - Chase growth at any cost (maintained underwriting discipline) - Build a consumer app first (went B2B2C through merchants) - Compete on price (competed on transparency and experience) - Fight regulation (embraced it as validation) - Hide from hard truths (published detailed financials even when unflattering)

"In business, there are plenty of hard problems, and the more you work with people the more you realize that the truly hard problems are always about humans," Levchin observed. Affirm's success came from solving human problems—mistrust of credit, fear of debt, confusion about terms—with technology solutions.

The playbook Affirm created will be studied for decades: how to disrupt an entrenched industry through moral positioning, how to build a two-sided network through platform partnerships, how to navigate complex regulation while maintaining startup speed. But perhaps the most important lesson is the simplest: in financial services, trust is the ultimate currency, and transparency is how you earn it.

XII. Bear vs. Bull Case & Future Outlook

The spreadsheet on the analyst's screen at Mizuho Securities showed two starkly different scenarios for Affirm's 2030 valuation: $5 billion in the bear case, $100 billion in the bull. The gap reflected not just uncertainty about Affirm's execution, but fundamental questions about the future of consumer credit itself.

The Bull Case: Secular Shift Away from Credit Cards

The optimistic scenario starts with a simple observation: credit cards are a 70-year-old technology trying to survive in a digital-first world. Every year, another cohort of consumers enters their prime spending years having never owned a physical credit card. To them, the idea of carrying a balance at 25% APR seems as antiquated as writing checks.

Affirm processes $28 billion in GMV annually, but the U.S. credit card purchase volume exceeds $5 trillion. If BNPL captures just 10% of credit card volume—a reasonable assumption given European trends—Affirm could be processing $200+ billion annually. At current take rates, that's $7-8 billion in revenue, justifying a $50+ billion valuation on revenue multiples alone.

International expansion offers another vector for explosive growth. BNPL penetration in Australia exceeds 10% of e-commerce, in Sweden it's over 20%. The renewed multi-year partnership cements Affirm's position as the exclusive pay-over-time provider for Shop Pay Installments in the U.S. It also extends this exclusivity into Shopify's home market of Canada and enables the partnership to continue growing into new markets worldwide, with plans to enter the U.K. on the horizon. Geographic expansion through platform partners reduces execution risk and customer acquisition costs.

The B2B opportunity might be even larger than consumer. Amazon cited data from the IRS and reported that over 28 million sole proprietorships operate in the United States. Small business lending is a $700 billion market in the U.S. alone, traditionally served by predatory merchant cash advance providers and expensive business credit cards. Affirm's transparent, transaction-level financing could revolutionize how small businesses manage cash flow.

But the real bull case rests on network effects. As more consumers use Affirm, more merchants feel compelled to offer it. As more merchants offer it, more consumers discover and trust it. This virtuous cycle, once it reaches critical mass, becomes nearly impossible to disrupt. PayPal proved this in payments; Affirm could prove it in lending.

The Bear Case: Rising Defaults and Commoditization

The pessimistic scenario begins with macroeconomic reality. Rising interest rates have increased Affirm's cost of capital from near-zero to 5%+. Every 100 basis point increase in funding costs directly impacts margins. In a recession, loss rates could spike from 2-3% to 6-8%, destroying unit economics.

Regulatory crackdown poses an existential threat. If the CFPB requires BNPL to comply with Truth in Lending Act provisions—mandatory disclosures, dispute resolution, ability-to-repay assessments—compliance costs could make small-ticket transactions unprofitable. Europe has already begun regulating BNPL like traditional credit; the U.S. could follow.

Competition is intensifying from every direction. Apple's entry with Apple Pay Later (though later discontinued) showed that big tech sees opportunity. Every major bank now offers installment options. Klarna, backed by $3.7 billion in funding, is expanding aggressively in the U.S. When everyone offers BNPL, it becomes a commodity, and margins collapse.

The commoditization risk is real. In payments, interchange fees have been compressed to basis points. The same could happen in BNPL. Merchants, initially happy to pay 5-6% for increased conversion, might demand 2-3% as competition increases. Consumer acquisition costs, currently near zero through platforms, could spike if Affirm needs to market directly.

Customer behavior presents another concern. Late fees are becoming more common: 10.5% of unique users were charged at least one late fee in 2021, up from 7.8% in 2020. While Affirm doesn't charge late fees, rising delinquencies still mean higher charge-offs. Young consumers, Affirm's core demographic, are most vulnerable to economic downturns.

The Reality: Somewhere in Between

The truth likely lies between these extremes. Affirm has proven it can navigate challenges—from Peloton concentration to regulatory scrutiny to rising rates. The company's disciplined underwriting, platform partnerships, and transparent model provide real differentiation.

According to Payments Dive in October 2022, Bank of America Securities identified Affirm as the "most frequently used" BNPL app in the US with a 30% market share. Being the market leader matters in financial services, where trust and brand recognition drive consumer choice.

The key variables to watch:

Credit Performance: If Affirm maintains 2-3% loss rates through a recession, the bear case crumbles. The company's transaction-level underwriting and merchant-subsidized 0% loans provide cushion against defaults.

Regulatory Outcome: Clear regulation could actually benefit Affirm by raising barriers to entry and forcing competitors to abandon predatory practices. As the most compliant player, Affirm might gain share.

Platform Stickiness: If Amazon, Shopify, and Walmart remain exclusive partners, Affirm maintains its distribution advantage. The cost and complexity of switching BNPL providers creates lock-in.

Capital Markets Access: Affirm's ability to securitize loans efficiently determines scalability. Strong ABS demand and tightening spreads suggest institutional confidence.

What Success Looks Like in 5 Years

In the optimal scenario, by 2029 Affirm has: - Captured 5% of U.S. credit card volume ($250B+ GMV) - Expanded internationally through platform partnerships - Built a profitable B2B lending business - Maintained <3% loss rates through a credit cycle - Achieved GAAP profitability with 20%+ EBITDA margins

This translates to $10+ billion in revenue, $2+ billion in EBITDA, justifying a $40-50 billion valuation—a 3-4x from current levels.

The company would have evolved from BNPL provider to comprehensive commerce enablement platform, offering not just financing but fraud prevention, identity verification, and loyalty programs. Think Stripe for lending—invisible infrastructure powering millions of transactions.

The Existential Question

The fundamental question isn't whether BNPL will grow—it will. It's whether Affirm can maintain differentiation as the market matures. The company's bet is that transparency, superior underwriting, and platform partnerships create sustainable competitive advantages.

Credit cards succeeded for 70 years by hiding true costs in complex terms. Affirm is betting that in an age of radical transparency—where consumers can compare prices instantly, read reviews immediately, and switch providers effortlessly—the honest player wins. It's a bet on human nature as much as financial innovation.

The article also cited Affirm as the "largest independent BNPL provider" based in the United States. That "independent" qualifier matters. Unlike Klarna (backed by banks) or Apple Pay Later (subsidized by hardware sales), Affirm must succeed on the merits of its financial model alone. This constraint forces discipline but also limits flexibility.

In five years, we'll know whether Max Levchin built the anti-credit card company or just another lending business. The stakes couldn't be higher—not just for Affirm's shareholders, but for millions of consumers seeking honest financial products. The future of consumer credit might well depend on whether a Ukrainian immigrant's vision of transparent finance can overcome seven decades of entrenched interests.

XIII. Recent News

[As of August 2025, this section would be populated with the most recent developments, which are beyond my knowledge cutoff. Key areas to monitor would include: Q2 2025 financial results, new partnership announcements, regulatory updates from the CFPB, competitive moves from Apple and banks, international expansion progress, and any new product launches.]

XIV. Links & Resources

Essential SEC Filings: - Affirm S-1 Registration Statement (November 2020) - Latest 10-K Annual Report - Quarterly 10-Q Filings - Proxy Statements (DEF 14A)

Long-Form Analysis: - TechCrunch: "Inside Affirm's IPO Filing" (2020) - The Information: "Affirm's Path to Profitability" - Stratechery: "Affirm and the BNPL Paradox" - Forbes: "Max Levchin's Decade-Long Bet Against Credit Cards"

Academic & Industry Research: - Federal Reserve: "Buy Now, Pay Later: Survey Evidence" - McKinsey: "The Future of Payments in America" - Oliver Wyman: "BNPL: Sustainable Business Model or Flash in the Pan?"

Podcast Episodes: - How I Built This: Max Levchin (NPR, 2022) - 20VC: Max Levchin on Building Affirm - Acquired FM: The PayPal Mafia Episode - Masters of Scale: "Why Transparency Wins" with Max Levchin

Books on Fintech & Consumer Credit: - "The PayPal Wars" by Eric M. Jackson - "Zero to One" by Peter Thiel - "Pound Foolish" by Helaine Olen - "The Unbanking of America" by Lisa Servon

The story of Affirm is far from over. What began as one founder's crusade against hidden fees has evolved into a fundamental reimagining of consumer credit. Whether Affirm ultimately succeeds in displacing credit cards or becomes another chapter in fintech history, its impact is undeniable: it proved that transparency could be profitable, that consumers would choose honesty over rewards, and that even the most entrenched industries could be disrupted by better values, not just better technology.

For investors, Affirm represents a complex bet on changing consumer behavior, regulatory evolution, and platform economics. For consumers, it offers an alternative to debt traps and hidden fees. For the industry, it stands as proof that doing well and doing good need not be mutually exclusive. The next chapter of this story will be written not in board rooms or trading floors, but at millions of checkout pages where consumers decide, purchase by purchase, what the future of credit looks like.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube