TransUnion: The Data Dynasty That Built Modern Credit

I. Introduction & Cold Open

Picture this: It's June 25, 2015, and the opening bell rings at the New York Stock Exchange. A company that has operated in the shadows for nearly half a century—tracking, scoring, and cataloging the financial lives of hundreds of millions of Americans—steps into the public spotlight for the first time. TransUnion, trading under the symbol TRU, opens at $22.50 per share, instantly creating a public company worth $4 billion. The private equity firms behind the IPO, Goldman Sachs and Advent International, are sitting on paper gains of nearly 3x their initial investment in just three years.

But here's what makes this story remarkable: TransUnion didn't start as a financial services company. It didn't begin with a vision to revolutionize credit scoring or democratize financial access. No, TransUnion's origin story begins with railcars—literal steel boxes on wheels carrying freight across America. The journey from Union Tank Car Company subsidiary to one of the "Big Three" credit bureaus is a tale of accidental empire-building, private equity financial engineering, and the relentless digitization of human trust.

Today, TransUnion generates $4.18 billion in annual revenue, growing at 9.2% year-over-year as of 2024. The company maintains files on over a billion consumers globally, processes tens of billions of data points monthly, and has become the invisible infrastructure underlying trillions of dollars in lending decisions. Every mortgage application, every credit card approval, every auto loan—there's a good chance TransUnion's algorithms and databases played a role in that decision.

Yet for most of its existence, TransUnion operated as a private company, passed between industrial conglomerates and private equity firms like a prized asset in a game of financial hot potato. Each owner extracted value, added capabilities, and positioned the company for the next transaction. The result? A business that has been bought and sold for increasingly astronomical sums: $688 million in 1981, $3 billion in 2012, and a market capitalization approaching $18 billion today.

The central question isn't just how a railcar company became a credit bureau—it's how a business built on filing cabinets and index cards transformed into an AI-powered data oligopoly. It's about how three companies came to hold the financial destinies of nearly every American in their servers. And perhaps most intriguingly, it's about what happens when the fundamental infrastructure of trust in a modern economy becomes a tradeable asset, subject to the whims of private equity engineering and public market pressures.

This is the story of data as destiny, of information as empire, and of how TransUnion built one of the most powerful—and controversial—businesses in modern capitalism. It's a story that touches every person with a credit card, every immigrant trying to establish financial identity, and every entrepreneur seeking their first business loan. And as we'll discover, the company's evolution from physical file cabinets to cloud-based AI systems mirrors the broader transformation of the American economy itself.

II. The Unlikely Origins: From Railcars to Credit Files (1968-1980)

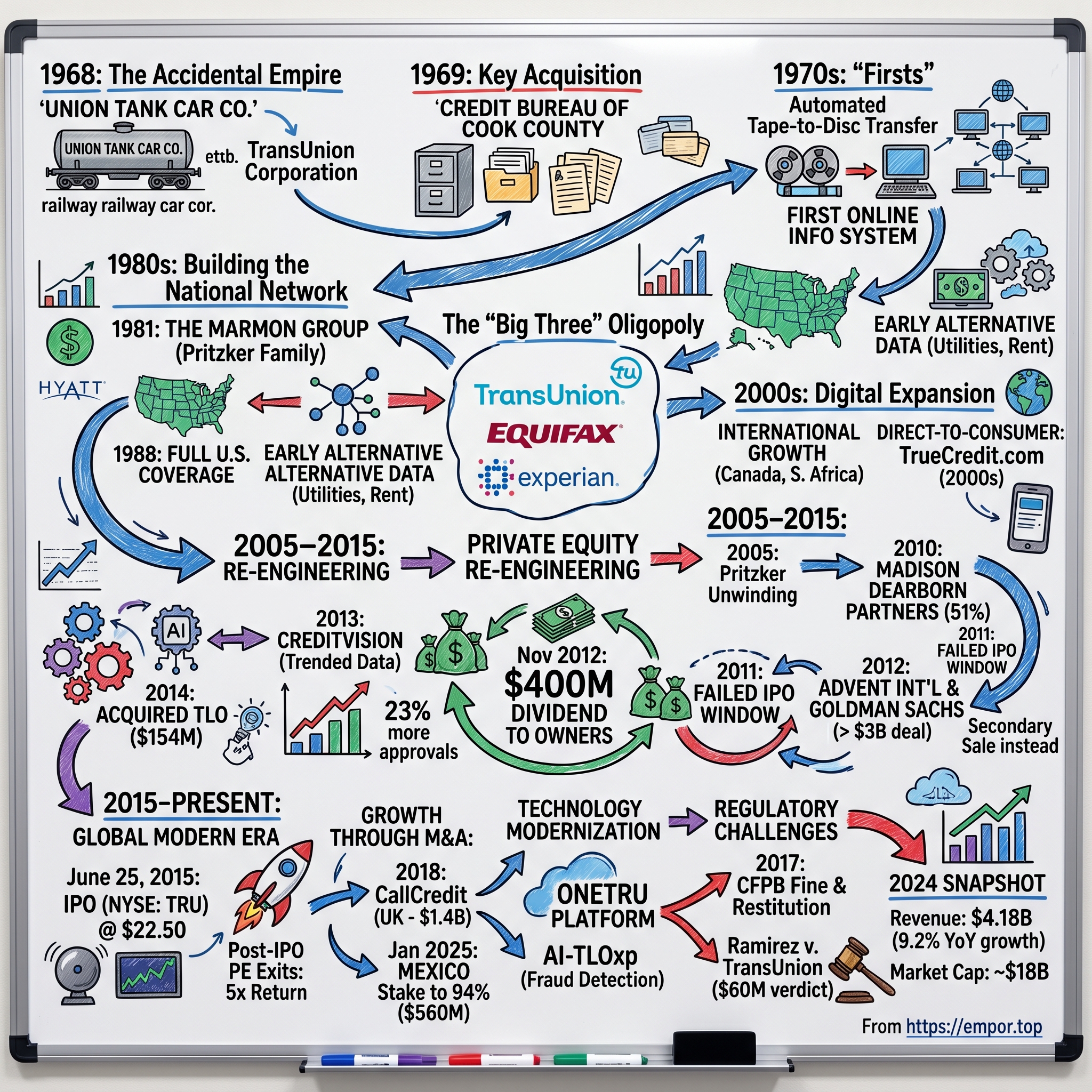

The year was 1968, and America was in upheaval. While protests raged over Vietnam and civil rights, a quieter revolution was beginning in the back offices of American finance. Union Tank Car Company, a railcar leasing business that had operated since 1891, decided it needed a holding company structure. They created TransUnion Corporation—a name that suggested transportation and unity, perfectly fitting for a railcar business. Nobody in that Chicago boardroom could have imagined they were naming what would become one of the three pillars of American consumer finance.

The pivotal moment came just one year later. In 1969, TransUnion's executives made what seemed like an odd acquisition: the Credit Bureau of Cook County. This wasn't some sophisticated financial services firm—it was essentially a warehouse of information, containing 3.6 million credit accounts stored on paper cards in 400 seven-drawer filing cabinets. Imagine it: row upon row of metal cabinets in a Chicago warehouse, each drawer containing thousands of index cards with handwritten notes about people's payment histories, employment records, and financial mishaps. This was the state of credit reporting in 1969—entirely manual, intensely local, and ripe for disruption. Why did a railcar company want to own a credit bureau? The answer reveals a stunning insight about American capitalism in the late 1960s. Union Tank Car wasn't just any railcar company—it was a descendant of Standard Oil, created in 1866 to serve the oil industry's transportation needs. By 1968, the company's executives recognized that the real value wasn't in moving physical goods but in information about who could pay for those goods. TransUnion was originally formed in 1968 as a holding company for Union Tank Car Company, making TransUnion a descendant of Standard Oil through Union Tank Car Company.

The acquisition of the Credit Bureau of Cook County, which possessed and maintained 3.6 million credit accounts stored in 400 seven-drawer cabinets, transformed TransUnion overnight from a transportation company into an information business. But here's what made this acquisition genius: TransUnion's engineers looked at those filing cabinets and saw not a warehouse of paper but a database waiting to be born.

Within months of the acquisition, TransUnion made a move that would revolutionize the entire credit industry. TransUnion became the first credit reporting agency to implement automated tape-to-disc transfer, drastically cutting the time and cost to update consumer files. Think about what this meant: while competitors were still manually pulling index cards and making phone calls to verify information, TransUnion was processing updates electronically. A task that once took days could now be completed in hours.

The company didn't stop there. TransUnion's engineers, many of whom came from the railcar business where logistics and routing were paramount, understood networks. They recognized that credit information, like rail networks, became exponentially more valuable when connected nationally. Throughout the 1970s, TransUnion embarked on an aggressive acquisition spree, buying up regional credit bureaus in major cities and signing service agreements with smaller bureaus they couldn't acquire outright. The real breakthrough came with TransUnion's vision for connectivity. Early in their history, they recognized the enormous benefit that a national, online information system would bring to clients and responded with the first online information storage and retrieval data processing system. This wasn't just digitization—it was networking before the internet existed. This system provided credit grantors across the country with one source for fast and valuable consumer credit information.

By the mid-1970s, TransUnion had built something unprecedented: a real-time, national credit information network. A bank in California could instantly access the credit history of someone who had just moved from New York. A car dealer in Texas could verify the creditworthiness of a customer in seconds rather than days. This speed and scale created a competitive moat that would prove nearly impossible for new entrants to overcome.

The expansion through the 1970s was relentless. Throughout the 1970s and 1980s, TransUnion continued to expand facilities and capabilities through investments in technology, strategic growth and acquisitions. The company wasn't just buying credit bureaus; it was assembling a national data infrastructure. Each acquisition brought not just customer files but also local relationships with banks, retailers, and other creditors who regularly reported payment information.

By 1980, TransUnion had transformed from a railcar company's side project into a technology-driven information powerhouse. The company processed millions of credit inquiries monthly, maintained files on tens of millions of Americans, and had become indispensable to the emerging world of instant credit decisions. Credit cards, which were exploding in popularity during the 1970s, relied heavily on TransUnion's ability to quickly verify creditworthiness.

The genius of TransUnion's early strategy was recognizing that credit information wasn't just data—it was a network effect business. The more lenders who reported to TransUnion, the more complete its files became. The more complete its files, the more valuable its reports were to lenders. And the more lenders who relied on TransUnion, the more essential it became for others to report their data to the system. This virtuous cycle, established in the 1970s, would define the credit bureau industry for decades to come.

III. The Marmon Years & Building Scale (1981-2005)

In 1981, TransUnion caught the attention of an unlikely buyer: The Marmon Group, a Chicago-based industrial conglomerate controlled by the Pritzker family. The Marmon Group acquired TransUnion for approximately $688 million. For context, this was an astronomical sum for a credit bureau in 1981—roughly $2.2 billion in today's dollars. The Pritzkers, already billionaires from their Hyatt Hotels empire, saw something in TransUnion that others missed: data as the ultimate scalable asset.

Jay Pritzker, the dealmaker behind the acquisition, had a philosophy about buying businesses with irreplaceable assets. Hotels could be built by competitors. Manufacturing plants could be replicated. But a comprehensive database of American consumers' financial histories, built over more than a decade with exclusive relationships and proprietary technology? That was a moat as wide as Lake Michigan.

Under Marmon's ownership, TransUnion underwent a dramatic transformation from a solid regional player to a true national powerhouse. The Pritzkers poured capital into the business, funding aggressive acquisitions and massive technology upgrades. They understood that TransUnion's value wasn't in its current revenue but in its potential to become the central nervous system of American consumer finance.

The 1980s saw TransUnion systematically fill in the gaps in its coverage map. The company acquired credit bureaus in secondary and tertiary markets, signed reciprocal data-sharing agreements with regional players, and most importantly, invested heavily in standardizing data formats across disparate systems. This unglamorous work of data standardization would prove crucial—while competitors struggled with incompatible systems from various acquisitions, TransUnion could seamlessly integrate new data sources into its unified platform.

In 1988, TransUnion achieved full coverage in the United States, maintaining and updating information on virtually every market-active consumer in the country. This was a watershed moment. For the first time in American history, a single company could provide comprehensive credit information on essentially any adult American within seconds. The implications were staggering: instant credit approvals became possible, risk-based pricing could be implemented at scale, and entirely new financial products could be created based on granular risk assessment.

The competition with Experian and Equifax intensified during this period, creating what would become known as the "Big Three" oligopoly. Each company raced to add new data sources, improve processing speeds, and expand their analytics capabilities. But TransUnion had a unique advantage under the Pritzkers: patient capital. While Equifax and Experian faced quarterly earnings pressure as public companies, TransUnion could make long-term investments without worrying about Wall Street's reaction.

One of the most significant innovations during the Marmon years was TransUnion's pioneering work in alternative data. While traditional credit reports focused on loans and credit cards, TransUnion began incorporating utility payment histories, rental payments, and even some employment data. This expanded view of consumer creditworthiness would later become crucial for serving "thin file" consumers—those with limited traditional credit history.

The technology investments during this period were massive. TransUnion migrated from mainframe computers to distributed systems, implemented early artificial intelligence algorithms for fraud detection, and built one of the first real-time data processing systems capable of handling millions of simultaneous queries. The company's Chicago data center became one of the largest commercial computing facilities in the Midwest, with redundant power systems, military-grade security, and enough processing power to rival some government installations.

TransUnion acquires one of the most powerful technologies for high-volume, individual-level decisions strengthening analytics and decisioning capabilities. This wasn't just about storing data anymore—it was about making that data actionable. TransUnion developed sophisticated scoring models that went beyond simple credit scores, offering predictive analytics for everything from bankruptcy risk to response rates for credit card offers.

By the late 1990s, TransUnion had also begun its international expansion, recognizing that credit bureaus in other countries were decades behind the U.S. market. The company established operations in Canada, then South Africa, and began exploring opportunities in Latin America and Asia. Each new market presented unique challenges—different regulatory frameworks, varying levels of financial system development, and cultural differences in attitudes toward credit and privacy.

The dot-com boom brought both opportunities and challenges. TransUnion partnered with early e-commerce companies to provide instant credit decisions for online purchases, developed APIs for real-time credit checks, and even experimented with direct-to-consumer services. But the company also faced new competitors—fintech startups claimed they could disrupt the credit bureau oligopoly with new technology and alternative data sources.

TransUnion enters the direct-to-consumer market with the acquisition of TrueCredit.com. This marked a significant strategic shift. For decades, TransUnion had sold data to businesses about consumers. Now, it would sell data directly to consumers about themselves. The move was partly defensive—legislative pressure was mounting for greater transparency in credit reporting—but it also opened an entirely new revenue stream that would eventually generate hundreds of millions in annual revenue.

Under the Pritzkers' ownership, TransUnion also developed a culture of strategic patience and operational excellence. The company became known for its "Midwest work ethic"—less flashy than Silicon Valley tech companies but relentlessly focused on reliability, accuracy, and gradual improvement. This culture would prove crucial as the company navigated the increasingly complex regulatory environment of the late 1990s and early 2000s.

By 2005, after nearly 25 years of Pritzker ownership, TransUnion had transformed from a $688 million acquisition into a business worth billions. The company processed over 30 billion data updates annually, maintained files on over 200 million Americans, and had become so essential to the financial system that regulators considered it "systemically important." The stage was set for the next chapter: the private equity era.

IV. The Private Equity Carousel Begins (2005-2012)

The year 2005 marked the beginning of TransUnion's journey through the private equity washing machine—a series of increasingly complex financial transactions that would extract billions in value while somehow, paradoxically, making the company more valuable with each flip. The Pritzker family, facing estate tax issues following Jay Pritzker's death in 1999, began the process of unwinding their empire. TransUnion, their crown jewel of data, would be one of the first major assets to go.

But the Pritzkers didn't immediately sell. Instead, they spun TransUnion out from Marmon Group while maintaining control, essentially creating a standalone entity that could be more easily marketed to buyers. This restructuring alone took years and involved untangling decades of shared services, inter-company agreements, and operational dependencies. It was financial engineering at its most complex—and most lucrative. In April 2010, Madison Dearborn Partners, a Chicago-based private equity firm with $18 billion under management, stepped forward as the buyer. Madison Dearborn acquired a 51 percent equity stake in TransUnion, with the Pritzker family business interests retaining an approximate 49 percent ownership interest in the Company. The terms weren't disclosed, but industry sources estimated the valuation at around $2.5-3 billion, representing a healthy return on the Pritzkers' decades-old investment.

Madison Dearborn brought the classic private equity playbook to TransUnion. Tim Hurd, a Managing Director at Madison Dearborn, noted that "TransUnion is a market-leading organization with an outstanding management team and a clear path to continued success". But behind this corporate speak lay a more aggressive strategy: leverage the business, cut costs, accelerate growth through acquisitions, and prepare for a quick flip. Just over a year later, in July 2011, Madison Dearborn attempted to cash out through an IPO. The company filed for an IPO in July 2011 but was then reported to be in talks with The Carlyle Group, Bain and Advent. The timing couldn't have been worse. European debt markets were in turmoil, U.S. economic growth was sputtering, and the aftermath of the 2008 financial crisis still cast a shadow over credit markets. The IPO window slammed shut.

What happened next was a masterclass in private equity opportunism. Rather than wait for markets to improve, Madison Dearborn pivoted to a secondary sale. Multiple private equity firms circled the asset, recognizing that TransUnion's steady cash flows and oligopolistic market position made it a perfect leveraged buyout candidate even in uncertain times. In February 2012, the winners emerged: Advent International and Goldman Sachs agreed to buy TransUnion from Madison Dearborn Partners and the Pritzker family for over $3 billion. The deal structure was classic private equity financial engineering. According to reports, the two buyers paid more than $900 million of cash and about $2.2 billion of new and existing debt. The deal valued TransUnion at $3 billion, giving Madison Dearborn and the Pritzkers a healthy return on their investment.

But here's where the story gets interesting. The 2008 financial crisis had created a new regulatory environment that would profoundly impact TransUnion. The Consumer Financial Protection Bureau (CFPB), created by the Dodd-Frank Act, had begun scrutinizing credit bureaus with unprecedented intensity. For the first time, federal regulators would examine the books of credit reporting agencies. This regulatory overhang made TransUnion simultaneously more valuable (as compliance requirements created barriers to entry) and more risky (as potential fines and restrictions loomed).

The period from 2005 to 2012 represented a fundamental shift in how TransUnion was viewed by the capital markets. No longer just a data company, it had become a financial asset to be optimized, leveraged, and flipped. Each owner extracted value while positioning the company for the next transaction. The Pritzkers had nurtured it for decades; Madison Dearborn had professionalized it; and now Goldman and Advent would prepare it for its ultimate transformation—becoming a public company.

V. The Goldman Sachs & Advent Transformation (2012-2015)

April 2012 marked the beginning of what private equity professionals would later study as a textbook case of value extraction and creation. Goldman Sachs and Advent International didn't just buy TransUnion—they architected a financial transformation that would generate returns that most hedge funds only dream about. They put $1.1 billion of equity into the deal, with the rest financed through debt that TransUnion itself would carry.

The first move came swiftly and shocked nobody who understood private equity playbook mechanics. In November 2012, just seven months after closing the acquisition, TransUnion borrowed $400 million to pay its new owners a dividend. Of that amount, $373.8 million went directly to Goldman and Advent. In less than a year, they had recouped more than a third of their equity investment while maintaining 100% ownership. This wasn't corporate raiding—it was financial optimization, they would argue. TransUnion's steady cash flows could support the debt, and the dividend simply reflected confidence in the business.

But Goldman and Advent weren't just financial engineers. They understood that TransUnion's real value lay not in its existing business but in its potential to expand beyond traditional credit reporting. Under CEO Bobby Mehta, who had been retained from the previous ownership, the company embarked on an aggressive product development and acquisition strategy.

The crown jewel of this transformation was CreditVision, launched in October 2013. This wasn't just another credit score—it represented a fundamental reimagining of credit assessment. Traditional credit scores were snapshots: your payment history, current balances, length of credit history. CreditVision introduced trended data, showing not just where a consumer's credit stood today but how it had evolved over time. A consumer whose debt was decreasing month over month looked very different from one whose debt was increasing, even if their current scores were identical.

The impact was immediate and profound. Lenders using CreditVision could approve 23% more applicants while maintaining the same risk levels, or reduce defaults by 15% while maintaining approval rates. For TransUnion, this meant premium pricing—lenders would pay significantly more for CreditVision reports than traditional credit reports. The product generated hundreds of millions in incremental revenue within its first two years. But the most audacious acquisition came in 2014: TransUnion acquired Hank Asher's data company TLO for $154 million. Asher, known as the "father of data fusion," had built a company that could aggregate and analyze billions of data points to uncover hidden relationships between people, businesses, and assets. TLO's technology wasn't just about credit—it could track down fraud rings, identify money laundering networks, and even help law enforcement find missing children.

The acquisition was controversial. Asher had died in 2013, leaving TLO in bankruptcy with $109 million in liabilities. But Goldman and Advent saw what others missed: TLO's TLOxp technology represented the future of data analytics. Its TLOxp technology aggregates data sets and uses a proprietary algorithm to uncover relationships between data. Within months of the acquisition, TransUnion had integrated TLO's capabilities into its platform, creating what would become its AI-TLOxp product—a deep learning system that could predict consumer behavior with unprecedented accuracy.

Goldman and Advent also pushed TransUnion aggressively into new verticals. Healthcare became a major focus, with the company developing products to verify insurance eligibility, predict patient payment behavior, and identify fraud in medical billing. The insurance industry became another growth driver, with TransUnion providing not just credit data but comprehensive risk profiles that included property records, criminal histories, and even social media analysis.

International expansion accelerated dramatically. TransUnion acquired or established operations in India, Brazil, South Africa, and a dozen other countries. Each market required customization—different regulatory frameworks, different data sources, different cultural attitudes toward credit—but the core technology platform scaled beautifully. By 2015, international operations were growing at twice the rate of the U.S. business.

The direct-to-consumer business, which had been a defensive afterthought under previous ownership, became a strategic priority. TransUnion launched mobile apps, partnered with fintech startups, and began offering subscription services that went far beyond simple credit monitoring. The company recognized that consumers increasingly wanted to understand and control their financial data, and that this represented not just a regulatory requirement but a massive business opportunity.

Throughout this transformation, Goldman and Advent maintained remarkable financial discipline. Despite the aggressive growth investments, TransUnion's EBITDA margins actually expanded during their ownership. The company generated enough cash to service its debt, fund acquisitions, and still return capital to its owners. This wasn't financial engineering—it was operational excellence combined with strategic vision.

By early 2015, the transformation was complete. TransUnion had evolved from a traditional credit bureau into a global information services powerhouse. Revenue had grown from $1.1 billion to $1.3 billion despite the challenging economic environment. The company had expanded from 25 countries to over 30. And most importantly, it had built technology capabilities that would define the next decade of growth.

The stage was set for the ultimate exit: taking TransUnion public. Goldman and Advent had transformed the company, extracted significant value through dividends, and positioned it for public market success. What happened next would validate their entire investment thesis—and generate returns that would become legendary in private equity circles.

VI. Going Public & The Modern Era (2015-Present)

The morning of June 25, 2015, marked a historic moment in American finance. TransUnion became a publicly traded company for the first time, opening at $22.50 per share on the New York Stock Exchange. The IPO raised $665 million, valuing the company at roughly $4 billion. For Goldman Sachs and Advent International, who had invested $1.1 billion just three years earlier, the paper gains were already extraordinary. After the IPO, Goldman and Advent held an 80 percent stake worth about $3.2 billion at $22 per share, about three times their equity investment.

But the real genius of Goldman and Advent's strategy became apparent in what happened next. Rather than dump their shares immediately, they orchestrated a masterful series of secondary offerings that would maximize their returns while maintaining market confidence. Between March 2016 and February 2017, Goldman and Advent sold 71.2 million shares for a total of $2.2 billion at prices ranging from $25 to $36.57. Each offering was timed perfectly—after strong earnings reports, during market rallies, when investor appetite was strongest.

The numbers were staggering. Including the $374 million dividend from 2012, Goldman and Advent extracted over $2.5 billion in cash while still retaining a 40% stake in TransUnion worth nearly $3 billion at 2017 prices. Their total return exceeded 5x their initial investment—one of the most successful private equity exits of the decade.

Under public ownership, TransUnion's transformation accelerated. CEO Jim Peck, who had been installed by Goldman and Advent in 2012, unveiled an ambitious strategy to position TransUnion as more than a credit bureau. The vision was to become "Information for Good"—a global information solutions company that happened to have credit reporting at its core. The acquisition strategy as a public company was markedly different from the private equity era. In 2015, TransUnion acquired Trustev for $21 million, minus debts—a digital verification company specializing in online fraud prevention. The deal structure revealed the new discipline: $21 million upfront with up to $23 million more contingent on performance targets. This wasn't about financial engineering; it was about strategic capability building. In 2017, TransUnion acquired FactorTrust, a consumer reporting agency specializing in alternative credit data. FactorTrust brought data on payday loans, rent-to-own agreements, and other non-traditional credit products—information that could help 60 million Americans with limited credit histories access mainstream financial services. The acquisition closed on November 14, and financial terms were not disclosed, but industry sources estimated the deal value at over $100 million. The biggest swing came in 2018: In mid-April 2018, TransUnion announced it intended to buy UK-based CallCredit Information Group for $1.4 billion, subject to regulatory approval. This wasn't just an acquisition—it was TransUnion's entry into the world's second-largest credit market. CallCredit, founded in 2000, had built itself into the UK's second-largest credit bureau with 2,500 customers including the top 10 banks.

The CallCredit deal revealed how dramatically TransUnion had evolved as a public company. This was a strategic bet on international expansion, funded through a combination of cash and debt markets that eagerly provided financing. The company could now access capital markets at rates that would have been unthinkable during the private equity era. Most recently, in January 2025, TransUnion has been observed in buying a majority stake in its Mexican arm in a deal worth around $560 million. TransUnion's stake in Trans Union de Mexico is said to be shot up around 94%, from a current 26%. This deal, announced just days ago, represents the company's continued commitment to international expansion, particularly in high-growth emerging markets.

The modern era has also seen TransUnion navigate significant regulatory challenges. In January 2017, TransUnion was fined $5.5 million and ordered to pay $17.6 million in restitution by the CFPB for deceiving consumers about credit scores and luring them into costly recurring payments. Later that year, in June 2017, a California jury ruled against TransUnion with a $60 million verdict for falsely reporting consumers on a government list of terrorists.

These setbacks, while costly, barely dented TransUnion's momentum. The company's stock price continued to climb, revenue grew double-digits annually, and new products launched regularly. By 2024, TransUnion had achieved annual revenue of $4.18 billion, a 9.2% increase from 2023. The market cap of $17.98 billion as of July 22, 2025, increased by 22.48% in one year.

The transformation from private to public ownership fundamentally changed TransUnion's trajectory. As a public company, it could access capital markets for growth, make strategic acquisitions without the debt burden of leveraged buyouts, and invest in long-term technology initiatives without the pressure of near-term exits. The company that Goldman and Advent had flipped for a 5x return has continued to compound value, creating billions more in market capitalization since the IPO.

VII. The Business Model & Product Evolution

TransUnion's business model represents one of the most elegant examples of a three-sided marketplace in modern capitalism. On one side sit consumers—over a billion globally—whose financial lives are tracked, scored, and packaged into data products. On another side are businesses—65,000 of them—who pay TransUnion for insights to make lending, hiring, and marketing decisions. And on the third side are data furnishers—banks, utilities, landlords—who provide the raw material that makes the entire system work.

The genius of this model is its self-reinforcing nature. The more data furnishers who report to TransUnion, the more complete its files become. The more complete the files, the more valuable they are to businesses making decisions. And the more businesses rely on TransUnion data, the more essential it becomes for furnishers to report their data to ensure their customers have complete credit profiles. It's a virtuous cycle that has proven nearly impossible for new entrants to break.

At the core of TransUnion's product portfolio remains the traditional credit report—that familiar document showing payment history, outstanding debts, and credit inquiries. But calling today's credit report "traditional" is like calling a Tesla a horseless carriage. Modern credit reports incorporate trended data showing payment patterns over 24 months, alternative data from utility and rental payments, and increasingly, behavioral analytics that predict future payment probability with startling accuracy.

The evolution from static snapshots to dynamic predictions represents TransUnion's most important product innovation. CreditVision, launched in 2013, doesn't just tell lenders what a consumer's credit score is today—it predicts where that score is heading. A consumer with a 650 score whose debt is decreasing monthly is a fundamentally different risk than one with the same score whose debt is increasing. This insight seems obvious in retrospect, but it took TransUnion's massive data infrastructure and advanced analytics to operationalize it at scale.

The direct-to-consumer business, once an afterthought, has become a profit engine generating hundreds of millions in high-margin recurring revenue. TransUnion enters the direct-to-consumer market with the acquisition of TrueCredit.com, but the real transformation came with mobile apps and subscription services. Today's consumers don't just check their credit when applying for a loan—they monitor it continuously, receive alerts about changes, and use TransUnion's tools to simulate how different actions might affect their scores.

The subscription model has proven particularly lucrative. Consumers pay $30-40 monthly for premium monitoring services that cost TransUnion pennies to deliver. With customer acquisition costs declining thanks to digital marketing and retention rates exceeding 80% annually, the lifetime value of a direct-to-consumer subscriber can exceed $1,000. Multiply that by millions of subscribers, and you have a business unit generating hundreds of millions in nearly pure profit.

But the real innovation has come in TransUnion's expansion beyond credit into what the company calls "Information for Good." Healthcare represents a massive opportunity. TransUnion's healthcare solutions help hospitals verify insurance eligibility, predict patient payment probability, and identify charity care candidates. In an industry where bad debt can exceed 5% of revenue, TransUnion's analytics can save hospitals tens of millions annually.

The insurance vertical leverages similar capabilities. TransUnion doesn't just provide credit scores to insurance companies—it offers comprehensive risk profiles that incorporate property records, criminal histories, professional licenses, and even social media indicators. An insurance company can instantly know not just whether someone pays their bills, but whether they've had multiple addresses recently (a fraud indicator), whether they've had professional licenses revoked, or whether public records suggest undisclosed risks.

The fraud prevention suite represents TransUnion's most technologically advanced offering. A growing segment of TransUnion's business is its business offerings that use advanced big data, particularly its deep AI-TLOxp product. This system processes billions of data points in real-time to identify synthetic identities, account takeover attempts, and organized fraud rings. The technology can detect patterns invisible to human analysts—like networks of fake identities created with similar naming patterns or suspicious velocity of credit applications across seemingly unrelated individuals.

TLOxp's capabilities extend far beyond traditional fraud detection. The system can identify human trafficking networks by analyzing payment patterns, uncover money laundering operations by tracking complex fund flows, and even assist law enforcement in locating missing persons by analyzing digital footprints. These capabilities command premium pricing—enterprises pay millions annually for access to TLOxp's insights.

The international expansion has required fundamental reimagining of TransUnion's products. Operations extend to 33 countries worldwide, but each market demands localization. In India, where formal credit history is limited, TransUnion developed products using mobile phone payment data and e-commerce transaction history. In Brazil, the company navigates a positive credit registry system fundamentally different from the U.S. model. In South Africa, TransUnion became the largest credit bureau by understanding local lending practices around stokvels (informal savings clubs) and mashonisas (informal lenders).

The OneTru platform, TransUnion's cloud-based technology infrastructure, represents the company's biggest technology investment to date. This isn't just a migration from on-premises servers to the cloud—it's a complete reimagining of how credit data is stored, processed, and delivered. OneTru enables real-time data updates, API-based integrations, and machine learning models that improve with every query. The platform processes over 100 billion transactions annually with 99.99% uptime—reliability that makes TransUnion mission-critical infrastructure for global finance.

VIII. Regulatory Battles & Consumer Trust

The regulatory landscape for TransUnion shifted seismically with the creation of the Consumer Financial Protection Bureau in 2011. For the first time, credit bureaus faced a federal regulator with examination authority, rule-making power, and the willingness to levy significant fines. The CFPB's oversight has fundamentally altered how TransUnion operates, forcing transparency in an industry that thrived in opacity for decades.

The first major confrontation came in January 2017, when TransUnion was fined $5.5 million and ordered to pay $17.6 million in restitution by the CFPB for deceiving consumers about credit scores and luring them into costly recurring payments. The bureau found that TransUnion and Equifax deceived consumers about the value of credit scores they sold, falsely representing that these scores were the same ones lenders typically use to make credit decisions. In reality, lenders rarely used these educational scores, preferring FICO scores or proprietary models.

The CFPB's order revealed troubling practices. TransUnion had enrolled consumers in subscription services without proper authorization, made it difficult to cancel subscriptions, and misrepresented the usefulness of their products. The company was forced to overhaul its marketing practices, simplify cancellation procedures, and provide clear disclosures about what scores lenders actually use.

Just five months later came an even more damaging verdict. In June 2017, a California jury ruled against TransUnion with a $60 million verdict for falsely reporting consumers on a government list of terrorists. The case, Ramirez v. TransUnion, involved 8,185 class members who had been incorrectly flagged as potential matches to the Treasury Department's Office of Foreign Assets Control (OFAC) list—essentially labeling them as potential terrorists or drug traffickers.

The implications were devastating for affected consumers. Imagine being denied a car loan, having a job offer rescinded, or being unable to rent an apartment because a credit bureau incorrectly suggested you might be a terrorist. The jury awarded $60 million in statutory and punitive damages, sending a clear message about the consequences of sloppy data practices.

These regulatory battles exposed a fundamental tension in TransUnion's business model. The company profits from collecting and selling data about consumers, but those same consumers have little choice in whether their data is collected and limited recourse when errors occur. The Fair Credit Reporting Act, passed in 1970, provides some protections, but it was written for an era of paper files and local credit bureaus, not global data conglomerates processing billions of records with artificial intelligence.

Data breaches have become another source of regulatory and reputational risk. While TransUnion hasn't suffered a breach as catastrophic as Equifax's 2017 incident that exposed 147 million Americans' data, the company faces constant cyber threats. Nation-state actors, criminal organizations, and hacktivists all target credit bureaus as treasure troves of valuable personal information. TransUnion spends tens of millions annually on cybersecurity, employing hundreds of security professionals and implementing military-grade encryption.

The company has also faced scrutiny over its data collection practices. TransUnion gathers information from thousands of sources—not just traditional lenders but also utility companies, cell phone providers, property records, court filings, and increasingly, alternative data providers. Critics argue this creates detailed surveillance profiles of Americans without their explicit consent. Privacy advocates have called for restrictions on what data can be collected and how it can be used.

The regulatory environment varies dramatically across TransUnion's international markets. The European Union's General Data Protection Regulation (GDPR) imposes strict requirements on data collection, storage, and usage. China has essentially blocked foreign credit bureaus from operating independently. India requires data localization. Brazil has implemented a positive credit registry that fundamentally changes the bureau model. Each jurisdiction requires different compliance frameworks, creating complexity and cost.

TransUnion has responded to regulatory pressure with a two-pronged strategy. First, it has invested heavily in compliance infrastructure—hiring former regulators, implementing robust quality controls, and creating consumer-friendly dispute resolution processes. Second, it has embraced the narrative of "Information for Good," positioning itself as enabling financial inclusion rather than simply profiting from consumer data.

The consumer trust challenge remains acute. Surveys consistently show that most Americans distrust credit bureaus, viewing them as secretive organizations that profit from their personal information while providing little value in return. TransUnion's direct-to-consumer products represent an attempt to change this perception, giving consumers tools to understand and improve their credit. But with subscription services generating hundreds of millions in revenue, critics argue the company profits from consumer anxiety about credit scores that it helps create.

IX. Playbook: Lessons in Data, Capital, and Trust

The TransUnion story offers a masterclass in building and scaling a data network effects business. The first lesson is the power of being early to digitization. TransUnion's 1969 decision to computerize credit files—when competitors were still using filing cabinets—created a compounding advantage that persists today. Every year of earlier digitization meant more historical data, better algorithms, and stronger relationships with data furnishers. In network effects businesses, small early advantages compound into insurmountable moats.

The second lesson involves the relationship between data businesses and private equity. TransUnion has been owned by private equity firms for much of its existence, and each owner extracted enormous value. But contrary to criticism of private equity strip-mining, each owner also invested heavily in capabilities that made TransUnion more valuable for the next buyer. The Pritzkers built national scale. Madison Dearborn professionalized operations. Goldman and Advent developed new products and international markets. The private equity playbook—leverage, operational improvement, strategic acquisitions, and exit optimization—works particularly well for businesses with predictable cash flows and high barriers to entry.

Building regulatory moats represents another crucial lesson. While TransUnion faces constant regulatory scrutiny, the compliance requirements create massive barriers for potential competitors. A startup trying to replicate TransUnion would need to navigate federal regulations, state laws, international requirements, and industry standards—requiring hundreds of millions in compliance investment before generating a dollar of revenue. Regulation that seems burdensome actually protects incumbents.

The international expansion playbook reveals important insights about globalizing data businesses. TransUnion didn't try to impose the U.S. credit bureau model on other countries. Instead, it adapted to local requirements while leveraging its core technology platform. In India, it emphasized alternative data. In Latin America, it focused on financial inclusion. In Europe, it stressed privacy protection. The lesson: globalize the platform, localize the product.

The subscription model transformation offers lessons for any business seeking recurring revenue. TransUnion converted a transactional business (selling credit reports) into a subscription business (credit monitoring) by creating ongoing value and manufactured anxiety. Consumers don't need to check their credit daily, but TransUnion created products that make them want to. The subscription revenue—highly predictable, low churn, minimal marginal cost—now represents one of TransUnion's most valuable business units.

Technology modernization while maintaining legacy systems presents a challenge every established company faces. TransUnion still processes some transactions on systems built in the 1980s, yet it also runs cutting-edge machine learning models in the cloud. The company's approach—gradual migration, API layers abstracting legacy complexity, parallel running of old and new systems—provides a template for digital transformation without disruption.

The trust paradox offers perhaps the most important lesson. TransUnion profits from consumer data while consumers generally distrust the company. This tension isn't sustainable long-term. TransUnion's investment in consumer-facing products, financial education, and "Information for Good" initiatives represents an attempt to align consumer and corporate interests. The lesson for other data businesses: you can't build a sustainable franchise on data exploitation. Eventually, you need consumer buy-in.

X. Power Analysis & Competitive Dynamics

TransUnion's competitive position rests on multiple interconnected power sources that create an almost impregnable moat. The most obvious is network effects—the more lenders who report to TransUnion, the more valuable its data becomes, attracting more lenders in a self-reinforcing cycle. But this is just the beginning of TransUnion's competitive advantages.

Switching costs represent an underappreciated source of power. Large financial institutions have integrated TransUnion data feeds into thousands of internal systems, decision models, and workflows. Switching to another bureau would require rewriting code, retraining models, and restructuring processes that have been refined over decades. A major bank estimated it would cost $50 million and take three years to fully switch credit bureau providers—and that's assuming the alternative could provide comparable data quality and coverage.

The oligopoly structure of credit bureaus creates unusual competitive dynamics. TransUnion, Equifax, and Experian don't really compete on price or even product features. Most large lenders use all three bureaus, pulling tri-merge reports for important decisions. This "coopetition" means the bureaus can maintain high margins without engaging in destructive price competition. It's similar to the dynamics between Visa and Mastercard—nominal competitors who actually benefit from each other's existence.

Scale economies become more powerful as data volumes grow. TransUnion processes over 100 billion transactions annually across its global platform. The marginal cost of processing an additional credit inquiry is essentially zero, while the fixed costs of maintaining data centers, security systems, and compliance infrastructure are enormous. A new entrant would need to match these fixed costs while starting with a fraction of TransUnion's volume—a recipe for massive losses.

Data advantages compound over time. TransUnion doesn't just have current data—it has decades of historical data showing how consumer behavior evolved through multiple economic cycles. This temporal depth enables predictive models that no amount of current data can replicate. When COVID-19 hit, TransUnion could model consumer behavior based on patterns from 2008, 2001, and even earlier recessions. New entrants, even with perfect current data, lack this historical perspective.

The regulatory barrier has become increasingly formidable. Following various scandals and breaches, credit bureaus face scrutiny from the CFPB, FTC, state attorneys general, and international regulators. Navigating this regulatory maze requires expertise, relationships, and resources that take years to develop. More importantly, regulators are unlikely to approve new national credit bureaus given concerns about data security and consumer protection.

Competition from fintech and alternative data providers represents the most significant threat to TransUnion's power. Companies like Plaid aggregate banking data directly from financial institutions. Fintech lenders use alternative data sources—from social media to mobile phone usage—to make credit decisions. Chinese tech giants have built credit scoring systems based on e-commerce and payment behavior. These alternatives don't directly compete with TransUnion today, but they could diminish the importance of traditional credit bureaus over time.

The China model presents a particular challenge. Ant Financial's Sesame Credit scores consumers based on Alibaba purchase history, Alipay payment behavior, and even social connections. With over a billion users, it has created an alternative credit system that bypasses traditional bureaus entirely. While regulatory and cultural differences make this model unlikely in the U.S., it demonstrates that TransUnion's moat isn't impregnable.

TransUnion has responded to these threats by becoming more than a credit bureau. The acquisition of alternative data providers, investment in AI capabilities, and expansion into new verticals represent attempts to maintain relevance as the financial system evolves. The company's power doesn't just come from its traditional credit data but from its ability to synthesize multiple data sources into actionable insights.

XI. Bull vs. Bear Case

The Bull Case:

TransUnion's bulls see a company perfectly positioned for the global digitization of finance. Start with the numbers: Market cap of $17.98 billion as of July 22, 2025, increased by 22.48% in one year, demonstrating sustained investor confidence. With 2024 revenue of $4.184B, a 9.2% increase from 2023, the company continues to deliver high single-digit to low double-digit growth despite its scale—a remarkable achievement for a 50-year-old business.

The international opportunity alone could double TransUnion's addressable market. The company operates in 33 countries, but most of the world's population lives in countries without comprehensive credit bureaus. As emerging markets develop consumer finance infrastructure, TransUnion's technology and expertise position it to capture disproportionate share. The recent Mexican acquisition, where TransUnion is taking its stake from 26% to 94%, exemplifies this opportunity. India, Brazil, Southeast Asia—each represents a multi-billion dollar opportunity as consumer credit expands.

Artificial intelligence and alternative data create new revenue streams that didn't exist five years ago. TransUnion's AI-TLOxp platform can identify fraud patterns, predict consumer behavior, and uncover insights that human analysts would never discover. As AI capabilities improve, TransUnion's vast data assets become more valuable. The company isn't just selling data anymore—it's selling predictions, insights, and decisions. These AI-driven products command premium pricing and higher margins than traditional credit reports.

The subscription economy transformation continues to gain momentum. Direct-to-consumer subscriptions provide predictable, high-margin revenue that grows even during economic downturns (when consumers become more concerned about credit). With customer acquisition costs declining through digital channels and lifetime values increasing through product expansion, this business could generate billions in value.

Financial inclusion initiatives open entirely new markets. Sixty million Americans have limited credit histories. Globally, over two billion adults lack access to formal financial services. TransUnion's alternative data capabilities—incorporating rental payments, utility bills, and mobile phone usage—can bring these populations into the financial mainstream. This isn't just socially beneficial; it's enormously profitable.

The embedded finance revolution multiplies TransUnion's touchpoints. As every company becomes a fintech—Uber offering driver loans, Amazon providing small business credit, Apple launching credit cards—demand for instant credit decisions explodes. TransUnion's APIs power these decisions, earning fees on transactions that didn't exist in the traditional banking model.

The Bear Case:

The bears see fundamental threats to TransUnion's business model. Regulatory risk looms largest. The CFPB has demonstrated willingness to levy large fines and impose operational restrictions. One major data breach could trigger existential regulatory response—forced breakups, data collection limitations, or price controls. The political climate increasingly favors consumer protection over corporate profits, and credit bureaus make easy targets for populist anger.

Data breach risk represents a constant threat. Equifax's 2017 breach cost over $1.7 billion and permanently damaged its reputation. TransUnion holds similarly sensitive data on over a billion consumers globally. A comparable breach wouldn't just trigger fines and lawsuits—it could catalyze regulatory changes that fundamentally restrict the credit bureau business model.

Fintech disruption accelerates every year. Open banking regulations in Europe and elsewhere force banks to share customer data with third parties, potentially eliminating the need for credit bureaus. Plaid, Yodlee, and other aggregators can provide real-time banking data that's more accurate and timely than credit reports. As lenders gain direct access to consumer financial data, traditional credit bureaus could become obsolete.

Economic cycle dependence remains acute despite diversification efforts. Credit inquiries drop during recessions as lending contracts. Marketing services decline as businesses cut spending. Even the direct-to-consumer business could suffer if unemployment spikes and consumers cancel subscriptions. TransUnion weathered COVID-19 well, but that crisis included massive government support that won't necessarily recur in future downturns.

The China threat isn't just competitive—it's existential. If alternative credit scoring models based on e-commerce and social data prove superior to traditional credit reports, TransUnion's entire business model becomes obsolete. Young consumers already share more data with tech companies than with banks. If Amazon, Apple, or Google decided to launch credit scoring services based on their vast data assets, they could potentially bypass traditional bureaus entirely.

Margin pressure seems inevitable. TransUnion has maintained exceptional margins through oligopoly pricing power. But regulators increasingly scrutinize these margins. Customers push back on price increases. New technologies reduce the cost of data processing. The 40%+ EBITDA margins that make TransUnion attractive to investors also make it a target for disruption and regulation.

Privacy legislation could fundamentally restrict TransUnion's business. Europe's GDPR already limits data collection and use. California's CCPA provides similar protections. If the U.S. passes comprehensive federal privacy legislation—increasingly likely given bipartisan concern about data protection—TransUnion might face restrictions on collecting alternative data, selling marketing services, or even maintaining credit files without explicit consumer consent.

XII. Epilogue: The Future of Identity & Trust

The OneTru platform represents TransUnion's bet on the future—a cloud-native, API-first, AI-powered system that can process any data type, deliver any insight, and integrate with any platform. This isn't just technology modernization; it's a fundamental reimagining of what a credit bureau can be. OneTru enables real-time everything: real-time data updates, real-time scoring, real-time decisions. In a world where consumers expect instant everything, batch processing credit reports seems as antiquated as mailing paper statements.

Alternative credit scoring will define the next decade of financial services. Traditional credit scores work well for people with traditional credit histories—credit cards, auto loans, mortgages. But they fail for immigrants, young adults, and anyone outside mainstream financial services. TransUnion's alternative data initiatives—incorporating rental payments, utility bills, mobile phone usage, and even social media behavior—could bring billions into the financial mainstream. The company that successfully scores the unscorable will capture enormous value.

The global opportunity dwarfs TransUnion's current business. Over two billion adults globally lack access to formal financial services. As smartphones proliferate and digital payments expand, these populations will need credit to participate in the modern economy. TransUnion's experience in emerging markets—from South African townships to Indian villages to Brazilian favelas—positions it to capture this opportunity. But success requires more than exporting U.S. credit models. It demands fundamental innovation in how creditworthiness is assessed in societies with different financial customs, limited formal employment, and varying attitudes toward debt.

What would founders do differently if starting TransUnion today? They certainly wouldn't begin with filing cabinets and mainframe computers. A modern TransUnion would likely start with mobile-first data collection, using smartphone usage patterns, app behavior, and digital payment history as primary inputs. It would leverage cloud computing from day one, enabling global scale without massive infrastructure investment. Machine learning would be core to the product, not an add-on. And critically, it would build consumer trust and engagement from the beginning, recognizing that sustainable data businesses require consumer participation, not just passive data collection.

The key tension facing TransUnion—and the broader data economy—is between utility and privacy, between enabling commerce and protecting consumers, between innovation and regulation. TransUnion enables trillions in lending by reducing information asymmetry between borrowers and lenders. But it also creates detailed surveillance profiles of citizens without their explicit consent. This tension isn't sustainable indefinitely. Either regulation will force fundamental changes to the business model, or TransUnion will need to evolve into something consumers actively choose rather than passively accept.

The bull case for TransUnion ultimately rests on information inequality. As long as lenders know less about borrowers than borrowers know about themselves, intermediaries like TransUnion create value by reducing that information gap. The bear case rests on technological disruption. If consumers can share their financial data directly with lenders—securely, selectively, and profitably—traditional credit bureaus become unnecessary middlemen.

XIII. Recent News

The most significant recent development is TransUnion's January 2025 announcement about buying a majority stake in its Mexican arm worth around $560 million, increasing stake to 94% from 26%. This move signals confidence in Latin American growth and TransUnion's commitment to controlling key international operations rather than maintaining minority positions.

The company's Q3 2024 results showed continued momentum with revenue growth of 9.2% year-over-year, beating analyst expectations. The strong performance was driven by double-digit growth in international markets and the direct-to-consumer segment, offsetting slower growth in U.S. financial services.

TransUnion's AI initiatives gained traction with several major financial institutions adopting TLOxp for fraud prevention. The company claims its AI models can now identify synthetic identity fraud with 90% accuracy, compared to 60% for traditional rule-based systems.

Regulatory scrutiny continues with the CFPB's ongoing examination of credit bureau practices. The bureau has indicated potential new rules around data accuracy, dispute resolution, and consumer access to credit information. TransUnion has set aside additional reserves for potential regulatory actions while maintaining that its practices comply with all current requirements.

The company also announced partnerships with several embedded finance providers, positioning itself as the credit infrastructure for the next generation of fintech companies. These partnerships could significantly expand TransUnion's transaction volumes as every company becomes a potential lender.

XIV. Links & Resources

For those seeking to dive deeper into TransUnion's history and the credit bureau industry, several resources prove invaluable:

"The Credit Bureau Report" by Evan Hendricks remains the definitive historical account of how credit bureaus evolved from local merchants' associations to global data conglomerates. Though published in 2005, its historical perspective provides essential context for understanding TransUnion's origins.

TransUnion's SEC filings, particularly the S-1 from its 2015 IPO, offer unparalleled insight into the company's operations, financials, and strategy. The annual 10-K reports since going public document the transformation from leveraged buyout target to public company.

For understanding the private equity transactions, "The Buyout of America" by Josh Kosman provides context on how PE firms like Goldman Sachs and Advent approach companies like TransUnion. The detailed financial engineering of the 2012-2015 period exemplifies broader private equity strategies.

Academic research on credit scoring and financial inclusion, particularly papers from the Consumer Financial Protection Bureau's research division, illuminate the societal impact of TransUnion's business model. Studies on alternative data and financial inclusion demonstrate both the potential and pitfalls of expanding credit assessment beyond traditional metrics.

Industry publications like American Banker and National Mortgage News provide ongoing coverage of TransUnion's strategic moves and regulatory challenges. Their archives contain detailed reporting on major acquisitions, product launches, and regulatory actions.

For international perspective, the World Bank's reports on credit infrastructure development offer insights into TransUnion's global expansion opportunities. Understanding credit bureau development in emerging markets helps evaluate TransUnion's growth potential beyond developed economies.

Final Thoughts

TransUnion's journey from a railcar company's filing cabinet acquisition to a global information services powerhouse worth $18 billion encapsulates the transformation of modern capitalism. It's a story of data becoming destiny, of information asymmetry creating enormous value, and of how essential infrastructure for economic activity can generate extraordinary returns for those who control it.

The company stands at an inflection point. It can continue extracting value from its oligopoly position, generating steady returns for shareholders while facing ongoing regulatory scrutiny and consumer distrust. Or it can reimagine itself as a consumer-empowering platform that aligns its interests with those whose data it monetizes. The path it chooses will determine whether TransUnion remains a powerful but controversial gatekeeper or evolves into something genuinely transformative for global financial inclusion.

For entrepreneurs and investors, TransUnion offers crucial lessons: the power of network effects in data businesses, the importance of regulatory moats, the value of patient capital in building enduring franchises, and the necessity of maintaining social license to operate in businesses built on personal data. As the world becomes increasingly digitized and financialized, these lessons only become more relevant.

The credit bureau that began with 3.6 million index cards in Chicago filing cabinets now influences billions of financial decisions globally. Whether TransUnion's next chapter involves continued dominance, disruption by new technologies, or transformation into something entirely different remains to be written. What's certain is that the business of trust—quantifying it, packaging it, and selling it—will remain central to the global economy. And TransUnion, for all its controversies and challenges, has proven remarkably adept at evolving with the times while maintaining its position at the center of that business.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube