Grayscale Bitcoin Trust (GBTC): The Bridge Between Wall Street and Bitcoin

I. Introduction & Cold Open

Picture this: It's January 10, 2024, and the trading floor at the New York Stock Exchange is buzzing with an electric energy not seen since the dotcom days. After a decade of regulatory battles, billions in investor losses, and a corporate crisis that nearly destroyed its parent company, the Grayscale Bitcoin Trust—GBTC—is finally converting to a spot Bitcoin ETF. The bell rings at 9:30 AM, and within minutes, nearly $2.2 billion flows out of the fund. Not in celebration, but in exodus.

This is the paradox of GBTC: the financial product that democratized Bitcoin access for American investors, that once traded at a 130% premium to its underlying assets, that controlled nearly 3% of all Bitcoin in existence, was hemorrhaging capital at the very moment of its greatest triumph. How did the pioneer of institutional Bitcoin exposure become the cautionary tale of crypto finance?

The story of GBTC is really three stories woven together. First, it's the tale of Barry Silbert, a distressed-debt specialist who saw Bitcoin not as internet money for libertarians but as the ultimate non-correlated asset for Wall Street portfolios. Second, it's a masterclass in regulatory arbitrage—how to give investors Bitcoin exposure when the SEC wouldn't approve a Bitcoin ETF. And third, it's a Greek tragedy of first-mover disadvantage, where being first meant being stuck with yesterday's structure in tomorrow's market.

What makes this story essential right now? Because GBTC wasn't just a fund—it was the prototype for every attempt to bridge traditional finance and crypto. Its successes showed how to navigate hostile regulators and skeptical institutions. Its failures revealed the hidden costs of innovation in regulated markets. And its transformation from premium to discount became the most reliable barometer of institutional crypto sentiment, predicting every major market turn from 2017 to 2024.

Today, GBTC still holds over 220,000 Bitcoin worth approximately $21 billion, making it one of the largest Bitcoin holders on Earth. But it's bleeding assets to competitors charging a fraction of its fees, its parent company Digital Currency Group is still recovering from a near-death experience, and the very success it fought for—ETF approval—may have sealed its long-term decline. This is that story.

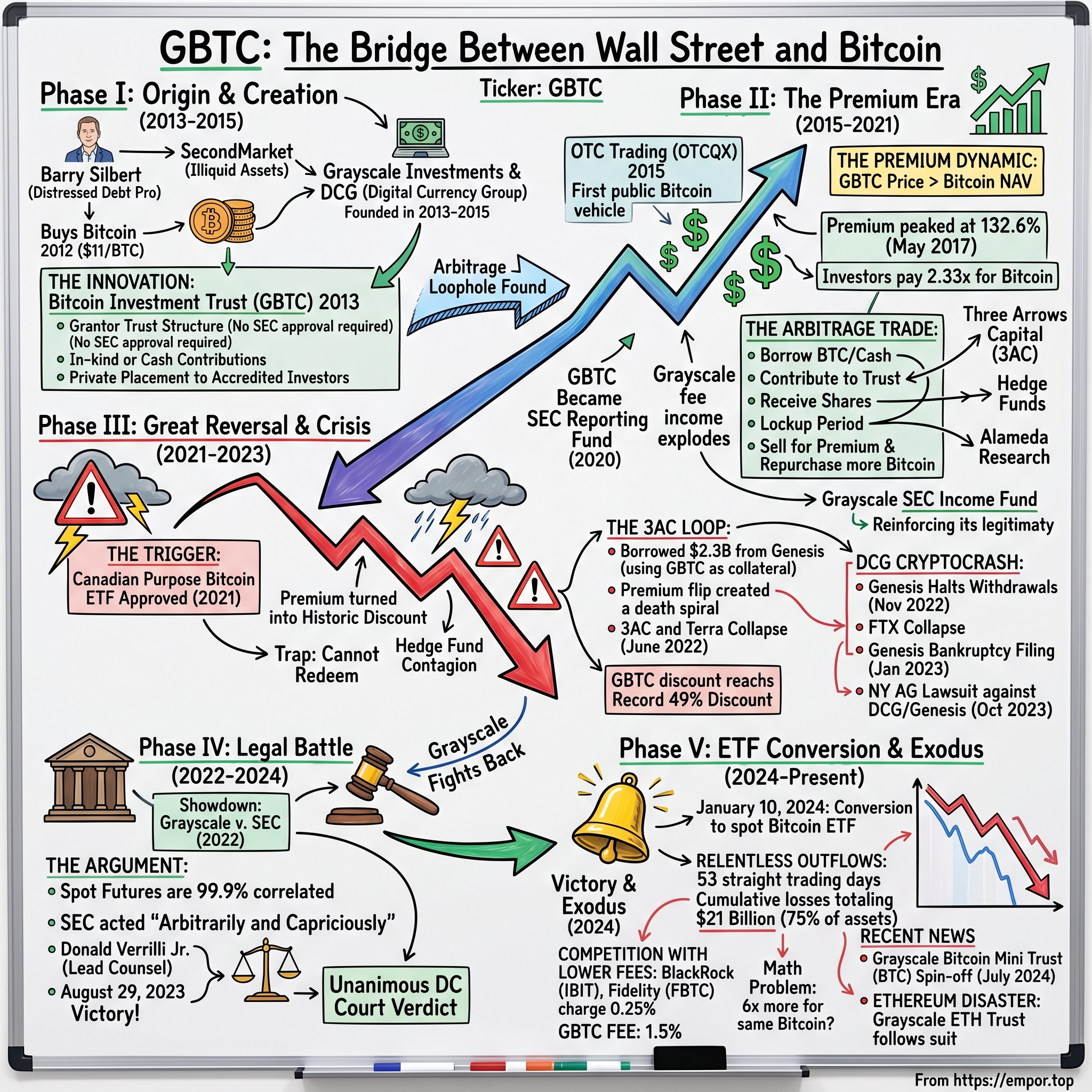

II. The Barry Silbert Origin Story & Digital Currency Group Formation

The story of Barry Silbert's rise from distressed-debt specialist to crypto mogul begins not in Silicon Valley or Wall Street's gleaming towers, but in the suburbs of Maryland, where a teenage prodigy was already displaying the financial instincts that would later reshape how institutions access Bitcoin.

At 13, Barry Silbert was making a business out of trading baseball cards. He spent his bar mitzvah money on stocks, and at 17 was the youngest person to pass the Series 7 stockbrokers' exam. Born in 1976 in Gaithersburg, Maryland, Silbert wasn't just another finance-obsessed teenager—he was systematically building expertise in illiquid markets before he could legally vote. Silbert was also the youngest person to pass the Series 7 stockbroker exam at 17 years old. He graduated from Emory University's Goizueta Business School with a Bachelor's degree in Finance.

After graduating from Emory in 1998, Silbert joined Houlihan Lokey as an investment banker, where fate placed him at the epicenter of corporate America's most spectacular failures. Silbert began his professional life in investment banking, working at Houlihan Lokey where he focused on distressed assets and restructuring—cases involving companies like Enron and WorldCom. For five years, he navigated the wreckage of companies that had promised to revolutionize their industries—Enron with energy trading, WorldCom with telecommunications. These weren't just failed companies; they were failed visions of the future. The experience would prove formative: Silbert learned that revolutionary ideas often arrive wrapped in regulatory complexity and corporate hubris.

In 2004, armed with insights from restructuring some of history's largest corporate collapses, Silbert founded Restricted Stock Partners, later renamed SecondMarket. The concept was elegantly simple yet revolutionary: create liquidity for assets that weren't supposed to be liquid. Private company stock, bankruptcy claims, auction-rate securities—if institutions needed to sell something that couldn't be sold, SecondMarket would find a way. SecondMarket was founded in 2004 by Barry Silbert to provide liquidity for restricted securities in public companies.

The platform's growth trajectory was extraordinary. By 2010, SecondMarket was facilitating $400 million in private company transactions annually. When Facebook and Twitter were still private companies, their shares were changing hands on SecondMarket, giving early employees and investors an exit before the IPO circus began. So promising was this back-channel way of selling start-up shares that SecondMarket itself raised money at a $200 million valuation. The World Economic Forum named it a Technology Pioneer in 2011, and Silbert landed on Fortune's "40 Under 40" list.

But then, in 2012, something shifted Silbert's entire worldview. Barry Silbert first bought Bitcoin in 2012, investing $175,000 when the price was still only around $11 per BTC. This wasn't pocket change—it was a serious bet from someone who had spent his career valuing distressed and illiquid assets. At $11 per Bitcoin, his $175,000 investment netted him approximately 15,900 BTC. If he held even a fraction of that position, it would be worth billions today.

What Silbert saw in Bitcoin wasn't just digital gold or internet money. He recognized the ultimate illiquid asset—something that major institutions wanted exposure to but couldn't access through traditional channels. No custody solutions, no regulatory framework, no way for a pension fund or family office to get Bitcoin on their balance sheet without looking reckless. It was SecondMarket's thesis taken to its logical extreme.

The pivot was swift and decisive. By 2013, while still running SecondMarket, Silbert had founded Grayscale Investments and launched the Bitcoin Investment Trust. Starting in 2012, Barry became one of the first and most active investors in the bitcoin space, providing seed funding for Coinbase, Ripple, BitPay, and a number of other companies who have gone on to define the industry. He wasn't just buying Bitcoin anymore—he was building the infrastructure for everyone else to buy it too.

The culmination came in 2015. The terms of the deal were not disclosed. Nasdaq acquired SecondMarket Solutions, though the price remained undisclosed. What mattered more was what Silbert did with the proceeds: he immediately founded Digital Currency Group (DCG), positioning himself at the center of a web that would eventually touch nearly every major crypto company in existence. After a couple of years, Barry Silbert established Digital Currency Group in 2015 with the funds he received from the sale of SecondMarket to NASDAQ.

DCG's structure was unique—part venture capital firm, part holding company, part crypto conglomerate. Rather than just investing in startups, Silbert would build and own entire verticals of the crypto economy. Grayscale for asset management. Genesis for trading and lending. CoinDesk for media. Foundry for mining. Each piece strategically positioned to capture value as crypto moved from fringe to mainstream.

"I have a vision of creating a new category of company that's not public and not private but has the benefits of both," said Mr. Silbert. This wasn't just corporate speak—it was the philosophy that would drive GBTC's creation. The same vision that made SecondMarket successful—finding liquidity in illiquid markets—would now be applied to the most controversial asset class of the 21st century.

By 2015, Silbert had transformed from a traditional finance player into crypto's most connected power broker. His journey from trading baseball cards to controlling billions in Bitcoin wasn't just a personal success story—it was a blueprint for how traditional finance could colonize the crypto frontier. But the vehicle that would make him both famous and infamous was just getting started.

III. The GBTC Innovation: Creating the First Public Bitcoin Vehicle (2013–2015)

On a crisp September morning in 2013, while Bitcoin traded at around $125 and most of Wall Street still dismissed it as "magic internet money," Barry Silbert quietly launched what would become the most controversial financial product in crypto history. Grayscale Bitcoin Trust was launched on 25 September 2013 under the name "The Bitcoin Investment Trust" as a private placement to accredited investors, marking the birth of institutional Bitcoin investing in America.

The genius of GBTC wasn't technological—it was regulatory. Silbert had identified a loophole so elegant it bordered on the obvious: if you couldn't get the SEC to approve a Bitcoin ETF, why not use a structure that had existed since the 1940s? A grantor trust, the same vehicle used for gold and silver funds, required no special approval. It just held assets and issued shares. The fact that the asset happened to be Bitcoin was, legally speaking, irrelevant.

The initial structure was deliberately exclusive. Only accredited investors—those with over $1 million in net worth or $200,000 in annual income—could participate in the private placement. Each GBTC share represented ownership of 0.1 bitcoins at the fund's inception in September 2013. But here's where Silbert's SecondMarket experience became crucial: he knew that after a one-year holding period, these restricted shares could potentially trade publicly under Rule 144 of the Securities Act.

The mechanics were byzantine but brilliant. Grayscale would accept either cash or "in-kind" Bitcoin contributions from accredited investors, issue them shares at net asset value (NAV), then make them wait. During that year-long lockup, investors couldn't sell, couldn't redeem, couldn't do anything but watch Bitcoin's price gyrate wildly. It was a test of conviction wrapped in regulatory compliance.

But the real innovation came in May 2015. Grayscale Bitcoin Trust (OTCQX: GBTC) began trading over-the-counter on the OTCQX market, becoming the first publicly traded bitcoin fund in the United States. This wasn't a triumphant IPO on the NYSE or Nasdaq—it was a quiet listing on the "pink sheets," the market typically associated with penny stocks and foreign companies. Yet for Bitcoin, it was revolutionary.

"We are proud to welcome the Bitcoin Investment Trust, the nation's first publicly-traded bitcoin investment vehicle, to our OTCQX Best Marketplace," said R. Cromwell Coulson, President and CEO of OTC Markets Group. The significance of this moment cannot be overstated. For the first time, any investor with a brokerage account could buy Bitcoin exposure alongside their stocks and bonds. No crypto exchange accounts, no private keys, no fear of being hacked.

The trust structure, however, came with peculiarities that would later prove both lucrative and destructive. Unlike an ETF, GBTC couldn't create or redeem shares on demand. The only entity able to create and remove shares from the market is Grayscale. It does so through private placements and redemptions, which are only available to accredited investors on a periodic basis at the firm's discretion. This meant supply and demand could become wildly misaligned.

The 2% annual management fee seemed steep even then—most gold ETFs charged 0.4%—but Silbert was betting on monopoly pricing power. Where else could a pension fund or family office get Bitcoin exposure in a regulated, audited, insured wrapper? The answer was nowhere, and both Silbert and his investors knew it.

From the beginning, GBTC attracted an unusual coalition of investors. There were the crypto-curious institutions who wanted Bitcoin exposure but couldn't hold actual Bitcoin due to custody concerns or investment mandates. There were retail investors willing to pay extra for the convenience of buying through their existing brokerage accounts. And then there were the arbitrageurs, who quickly realized that GBTC's structural inefficiencies created massive profit opportunities.

The trust's holdings grew steadily but not spectacularly in those early years. By late 2015, GBTC held roughly 170,000 Bitcoin, worth about $70 million at the time. Small by today's standards, but it represented something profound: Wall Street money was flowing into Bitcoin, even if through a side door.

What made GBTC particularly clever was how it solved the custody problem that terrified institutional investors. The Sponsor does not store, hold, or maintain custody or control of the Fund's digital assets but instead has entered into the Custodian Agreement with a third party to facilitate the security of its digital assets. The Custodian controls and secures the Fund's digital asset accounts, a segregated custody account to store private keys, which allow for the transfer of ownership or control of the digital asset, on the Fund's behalf. Investors didn't need to worry about losing private keys or getting hacked—that was Grayscale's problem.

The regulatory positioning was equally shrewd. By trading on OTCQX under the Alternative Reporting Standard, GBTC didn't need to register with the SEC initially. It could provide quarterly reports and audited financials without the full burden of being an SEC-reporting company. This lighter regulatory touch allowed Grayscale to move quickly while competitors remained stuck in SEC approval purgatory.

But perhaps the most prescient aspect of GBTC's creation was its timing. Launched when Bitcoin was still recovering from its first major crash, trading publicly just as institutional interest began to percolate, GBTC positioned itself perfectly for what was coming. The trust wasn't just a investment vehicle—it was a Trojan horse that would bring Bitcoin into the portfolios of some of the world's most conservative investors.

As 2015 drew to a close, GBTC was trading at a slight premium to its NAV—maybe 10-20%. Annoying for buyers, but not unreasonable given the convenience factor. Nobody could have predicted that within two years, that premium would explode to over 100%, creating one of the most lucrative arbitrage trades in financial history. The monopoly Silbert had carefully constructed was about to print money in ways that would make even crypto veterans gasp.

IV. The Premium Era: When GBTC Traded Above Bitcoin (2015–2021)

In December 2016, something extraordinary happened in the crypto markets that would reshape institutional Bitcoin investing forever. GBTC shares, which should have tracked Bitcoin's price closely, began trading at a premium that defied all logic. In other words, a person willing to subscribe one (1) spot bitcoin on December 31st, 2016, and receive GBTC units on May 31st, 2017, could have sold those units for dollars, and repurchased more than 130% more Bitcoin that was subscribed - or 2.3 BTC. The monopoly Silbert had created was about to become a money-printing machine.

Historically the GBTC's premium peaked at 132.6 percent in late May of 2017. Think about that for a moment: investors were willing to pay $2.33 for every dollar of Bitcoin held by the trust. It was as if someone was selling $100 bills for $233, and buyers were lining up around the block. The premium wasn't a bug—it was a feature of GBTC's unique position as the only game in town for institutional Bitcoin exposure.

The mechanics of why this happened were both simple and profound. Institutional investors—pension funds, endowments, family offices—desperately wanted Bitcoin exposure but couldn't hold actual Bitcoin due to regulatory restrictions, custody concerns, or investment mandates that prohibited direct cryptocurrency ownership. GBTC was their only option, and they were willing to pay whatever it cost.

But the real genius wasn't in the premium itself—it was in who could exploit it. Along with other Hedge Funds, they realized that GBTC could be used in arbitrage trading (selling two identical assets in two different markets for a profit) because GBTC was not priced based on the actual price of Bitcoin, but rather the NAV (Net Asset Value). The arbitrage worked like this: accredited investors could contribute Bitcoin to Grayscale at NAV, receive GBTC shares, wait six months (later extended to twelve), then sell those shares on the open market at the premium.

They were able to turn 1 spot btc into 2.3 spot BTC after 6 months through the GBTC trade. It was alchemy—turning one Bitcoin into two through regulatory arbitrage and patience. The trade became so lucrative that it attracted some of the biggest names in crypto trading.

Enter the arbitrageurs. One of these investors was Three Arrows Capital (3AC), a hedge fund founded by two MIT graduate traders, Su Zhu and Kyle Davies, that had made money trading Crypto in 2019 and 2020. 3AC saw this opportunity to make essentially a "risk-free" trade and submitted documentation to own 6.1% of the Grayscale Bitcoin Trust. 3AC took out a loan with Genesis Trading (Genesis) to buy enough Bitcoin that would satisfy the 6.1% ownership.

The scale of the arbitrage was staggering. Major hedge funds would borrow Bitcoin, contribute it to GBTC, hedge their Bitcoin price exposure with futures or swaps, wait out the lockup period, then sell the GBTC shares at a massive premium. The profits were essentially risk-free as long as the premium persisted.

He said the firm could see Alameda entering the market because FTX's sister trading firm used Interactive Brokers, the popular retail trading platform, to make trades. "You'd have these massive orders coming from Interactive Brokers. And it took us a long time to find out who is actually this trader. Because it's big, like really big," he said. "They would come in with a few hundred thousand share orders at clips, like every day."

Alameda Research, Sam Bankman-Fried's trading firm, was perhaps the most aggressive player in the GBTC arbitrage game. But wasn't Alameda also arbitrage trading GBTC in 2020 and had GTBC collateral with Genesis which was at a discount along with the other hedge funds? The firm would eventually hold hundreds of millions of dollars worth of GBTC, using it as collateral for loans while waiting for lockup periods to expire.

The premium created bizarre market dynamics. Said differently, to arbitrage the "premium" trade - you need to buy spot BTC and sell GBTC. This added buy pressure on spot bitcoin markets as the premium was positive. The arbitrage trade was actually driving Bitcoin's price higher, as hedge funds needed to buy spot Bitcoin to contribute to the trust, creating a self-reinforcing cycle of demand.

For Grayscale, the premium era was a goldmine. For instance, Grayscale sold more than 59 million shares at NAV between Dec. 15 and Dec. 28, 2020, collecting approximately $1.2 billion in new assets from institutional investors, which it used to purchase Bitcoin for the trust. The 2% management fee applied to an ever-growing pile of assets as arbitrageurs poured Bitcoin into the trust to capture the premium.

By early 2020, GBTC had become a behemoth, holding over 300,000 Bitcoin. The trust's influence on Bitcoin markets was undeniable—when GBTC had large inflows, Bitcoin's price often rallied. When the premium expanded, it signaled institutional bullishness. Traders began using the GBTC premium as a market sentiment indicator, with Increase In Premium: Bullish or becoming overbought. Decrease In Premium: Bullish or becoming oversold.

The success attracted imitators but no real competition. GBTC became an SEC-reporting bitcoin investment fund in 2020. This elevated status—becoming a full SEC-reporting company—only reinforced its dominance. It was now fully legitimate in the eyes of compliance departments and investment committees.

But cracks were beginning to show. Canadian regulators approved the Purpose Bitcoin ETF in February 2021, offering investors a true ETF structure with daily redemptions and a 1% management fee—half of GBTC's. Purpose Bitcoin ETF (a Canadian fund that invests directly in Bitcoin) began trading on Feb. 18 and quickly amassed more than $1 billion in assets in a month of trading.

The market's response was swift and brutal. Ten (10) days after the Canadian Bitcoin ETF was announced, the GBTC premium had been arbitraged away - it had gone to 0%. But it didn't stop there - within hours the premium turned into a discount. For the first time in its history, GBTC began trading below the value of its Bitcoin holdings.

The premium era officially ended in February 2021, but its impact rippled through the crypto ecosystem for years. Hedge funds that had borrowed Bitcoin to arbitrage the premium found themselves trapped when it flipped to a discount. They couldn't exit their positions without taking massive losses. The founders of the now-bankrupt Three Arrows Capital told Bloomberg last year that GBTC flipping, as well as Terra's implosion, was one of the key reasons the fund blew up.

What started as financial innovation had become a systemic risk. The very structure that had made GBTC so profitable—the inability to redeem shares for underlying Bitcoin—was about to become its greatest weakness. The trust that had introduced Wall Street to Bitcoin was about to teach it a painful lesson about the dangers of closed-end fund structures in volatile markets.

V. The Great Reversal: From Premium to Historic Discount (2021–2023)

The reversal began innocuously enough. On February 21, 2021, GBTC closed at a 3% discount to NAV—the first time it had ever traded meaningfully below the value of its Bitcoin holdings. Investors initially brushed it off as a temporary aberration. Within days, they would realize they were witnessing the beginning of one of the most spectacular value destructions in financial history.

The catalyst was competition—real competition—for the first time. Purpose Bitcoin ETF (a Canadian fund that invests directly in Bitcoin) began trading on Feb. 18 and quickly amassed more than $1 billion in assets in a month of trading. Its management fee of 1.00% is half that of Grayscale Bitcoin Trust, and its structure as an ETF allows it to track Bitcoin more closely, making it more appealing than Grayscale's offering.

The mathematics of what happened next were brutal and unforgiving. Ten (10) days after the Canadian Bitcoin ETF was announced, the GBTC premium had been arbitraged away - it had gone to 0%. But it didn't stop there - within hours the premium turned into a discount. Hedge funds that had borrowed Bitcoin at $30,000 to arbitrage a 40% premium suddenly found themselves trapped in positions worth less than what they owed.

For Three Arrows Capital, the GBTC discount was an existential threat. 3AC saw this opportunity to make essentially a "risk-free" trade and submitted documentation to own 6.1% of the Grayscale Bitcoin Trust. 3AC took out a loan with Genesis Trading (Genesis) to buy enough Bitcoin that would satisfy the 6.1% ownership. But when the premium flipped to a discount, their "risk-free" trade became a death spiral.

The contagion spread through the crypto ecosystem like wildfire. From 3AC's bankruptcy filings, we now know that Genesis loaned Three Arrows Capital a whopping $2.3 billion dollars. To make matters worse, the loan was undercollateralized with GBTC and other illiquid cryptocurrencies. When Three Arrows collapsed in June 2022, it left Genesis with a $1.2 billion hole in its balance sheet and illiquid GBTC shares as collateral.

By November 2022, following the FTX collapse, the situation had become apocalyptic. The uncertainty pushed the market price of GBTC to a record 49% discount compared to its net asset value in December. Investors who bought GBTC at a premium were now down as much as 70% even as Bitcoin itself had only fallen 50%. The trust had become a leveraged bet on Bitcoin in reverse—amplifying losses rather than gains.

GBTC currently trades at a massive 45% discount to the price of the underlying bitcoin (BTC), the note said, meaning investors are trapped in an investment vehicle they can exit only after a six-month lock-in period and with a significant discount. GBTC is the largest bitcoin investment vehicle and holds more than $10.5 billion of BTC.

The human toll was staggering. Retail investors who had bought GBTC in their retirement accounts, thinking it was a safe way to get Bitcoin exposure, watched their investments crater. Institutional investors faced redemption requests they couldn't meet. And the arbitrageurs—those masters of the universe who had printed money during the premium era—were now facing bankruptcy.

Genesis Global Capital's situation epitomized the crisis. Shortly after FTX collapsed into its own bankruptcy case in November, Genesis Global Capital was forced to suspend customer withdrawals, which hurt customers of a yield product offered by the Gemini crypto exchange. Genesis had been scrambling to raise fresh capital or reach a deal with creditors.

The interconnections within the Digital Currency Group empire made everything worse. On November 10th, 2022, DCG repaid the loan with nearly 26 million GBTC shares worth approximately $250 million. DCG then made Genesis extend the loan on the remaining 4,550 Bitcoin to, once again, May 2023. So this is how Genesis ended up with another large tranche of GBTC shares. DCG was essentially paying debts with discounted GBTC shares, creating a circular reference of value destruction.

Genesis was restricted from selling these GBTC shares, so by consistently forcing Genesis to extend its cash loans and choosing to partially repay its Bitcoin loan in GBTC shares instead of Bitcoin, DCG actually worsened Genesis's liquidity crunch. The very structure that had made GBTC successful—the inability to redeem—was now destroying its parent company.

Cameron Winklevoss, whose Gemini exchange had $900 million trapped in Genesis's Earn program, went public with his fury. In a series of blistering tweets, he accused Barry Silbert of fraud and demanded immediate repayment. The crypto community watched in horror as two of its most prominent figures engaged in a public knife fight over a billion dollars.

In its filing, Genesis Global Capital, the partner firm to Gemini's defunct Earn program, estimated more than 100,000 creditors and between $1 billion and $10 billion in liabilities. The January 19, 2023 bankruptcy filing marked the formal acknowledgment that the GBTC discount had destroyed not just portfolios but entire companies.

The discount created perverse incentives throughout the ecosystem. The odds of Grayscale winning its case vs SEC in light of related party transactions with Genesis Trading, Genesis Capital, and at least two bankrupt counterparties (BlockFi and 3AC) are now 0," Selkis said on Twitter. "Delays in pursuing a Reg M program hurt shareholders while enriching DCG/Grayscale." Critics argued that Grayscale was deliberately maintaining the discount to continue collecting its 2% fee on trapped capital.

Armour also does not expect the fund group to liquidate GBTC, as according to his estimates, Grayscale made about $900 million in management fees since the beginning of 2021. GBTC carries an annual management fee of 2%. "They may not be willing to kill the golden goose," Armour said.

The market began to price in catastrophic scenarios. What if DCG was forced to liquidate GBTC entirely? There are market fears that the repercussions of the Genesis bankruptcy could somehow lead to the liquidation of GBTC's holdings of 600,000+ bitcoin. Such a liquidation would crash Bitcoin's price globally, potentially triggering a crypto winter worse than anything seen before.

Meanwhile, investors who had bought GBTC during the discount, hoping to profit when it eventually converted to an ETF, found themselves in a prisoner's dilemma. Every day they held was another day of 2% annual fees eating into their potential profits. But selling meant locking in a 45% loss. It was financial purgatory with no clear exit.

The legal battles intensified. Alameda Research, despite being bankrupt itself, sued Grayscale to force redemptions. "If Grayscale reduced its fees and stopped improperly preventing redemptions, the FTX Debtors' shares would be worth at least $550 million, approximately 90% more than the current value of the FTX Debtors' shares today," FTX said in a statement at the time of filing.

By late 2023, GBTC had transformed from Bitcoin's gateway to institutional investment into its albatross. The trust still held over 600,000 Bitcoin, worth tens of billions, but its shares traded as if that Bitcoin might disappear entirely. The discount had become a barometer of existential fear in crypto markets—the wider it grew, the closer the industry felt to complete collapse.

The only hope for redemption lay in the courts, where Grayscale's lawsuit against the SEC was slowly grinding forward. If they could force approval of an ETF conversion, the discount would disappear instantly. If they lost, GBTC might remain trapped in its discount spiral forever, slowly bleeding value through fees while its investors watched helplessly.

The reversal was complete: the product that had promised to democratize Bitcoin access had become its most painful prison.

VI. The Legal Battle: Taking on the SEC

The showdown between Grayscale and the SEC was years in the making, but it began in earnest on June 29, 2022. That day, the SEC issued yet another denial—this time rejecting Grayscale's application to convert GBTC into a spot Bitcoin ETF. For Grayscale, watching its shares trade at a 30% discount while the SEC approved futures-based Bitcoin ETFs felt like regulatory persecution. Within days, they made a decision that would reshape crypto regulation forever: they would sue the most powerful financial regulator in America.

Grayscale sought to turn GBTC into an ETF in 2017, but voluntarily withdrew the application following negative remarks from the SEC. But by 2022, the landscape had changed dramatically. The SEC had approved multiple Bitcoin futures ETFs—products that didn't hold actual Bitcoin but rather derivatives contracts. Meanwhile, GBTC, which held actual Bitcoin worth billions, was denied the same regulatory treatment.

The hypocrisy was maddening. The SEC rejected Grayscale's initial application to convert the Grayscale Bitcoin Trust to a spot Bitcoin ETF on June 29, 2022. Grayscale argued that the SEC acted "arbitrarily and capriciously" in rejecting spot Bitcoin ETF applications, especially considering it had approved Bitcoin futures ETFs. The core argument was elegant: if the SEC trusted regulated futures markets enough to approve ETFs based on them, how could it claim spot markets were too manipulated when those futures prices were 99.9% correlated with spot prices?

Behind the scenes, Grayscale assembled a legal dream team. Donald Verrilli Jr., who had served as Solicitor General under President Obama and argued landmark cases before the Supreme Court, would lead the charge. The Davis Polk law firm, one of Wall Street's most prestigious, would handle the intricate securities law arguments. This wasn't going to be a typical crypto company throwing a tantrum—it would be a sophisticated legal assault on regulatory inconsistency.

The oral arguments, held in March 2023, were a masterclass in appellate advocacy. A three-judge panel was convened for the opinion, with Judges Neomi Rao, Sri Srinivasan, and Harry Edwards presiding. Judge Rao, in particular, seemed skeptical of the SEC's position from the start. Previously, Judge Rao said that the SEC did not "offer any explanation" as to why Grayscale was in the wrong.

Verrilli hammered home a simple point: Grayscale — specifically, Donald Verrilli Jr. — had provided the court with evidence that CME bitcoin futures prices are 99.9% correlated with spot market prices. The SEC did not dispute the data provided by Grayscale and did not suggest "that market inefficiencies or other factors would undermine the correlation." If futures and spot markets were essentially the same, how could the SEC approve one and deny the other?

The SEC's lawyers struggled to articulate a coherent distinction. They argued about surveillance-sharing agreements and market manipulation, but couldn't explain why these concerns applied to spot ETFs but not futures ETFs. The judges weren't buying it. "The Commission's unexplained discounting of the obvious financial and mathematical relationship between the spot and futures markets falls short of the standard for reasoned decisionmaking," the judges wrote.

Then came August 29, 2023—a date that would live in crypto history. On August 29, 2023, a unanimous panel of the U.S. Court of Appeals for the District of Columbia Circuit granted the petition of Davis Polk's client Grayscale Investments, LLC and vacated an order of the U.S. Securities and Exchange Commission denying approval to list and trade shares of Grayscale Bitcoin Trust as an exchange-traded product on NYSE Arca, Inc.

The victory was total and devastating for the SEC. It was ordered that "Grayscale's petition for review be granted and the Commission's order be vacated." The court explained that the denial of Grayscale's proposal was arbitrary and capricious because the Commission failed to explain its different treatment of similar products.

Michael Sonnenshein, CEO of Grayscale, could barely contain his excitement on Twitter: JUST IN The D.C. Circuit ruled in favor of @Grayscale in our lawsuit challenging the SEC's decision to deny $GBTC's conversion to an ETF! Thank you to everyone who has been on this journey with us, especially our investors. We are grateful for your support...

The market reaction was instant and dramatic. Bitcoin (BTC) experienced a 6% percent bump on the news before retracting slightly to around 5%. More importantly, the GBTC discount began to narrow immediately, as investors bet that ETF approval was now inevitable.

But the SEC still had cards to play. The Court's action does not necessarily mean that GBTC (or anyone else) will be able to list shares of a spot bitcoin ETP any time soon. Indeed, shortly after the Grayscale decision, the SEC announced that it will postpone decisions on a number of other outstanding spot bitcoin ETPs until at least October 19, 2023.

The agency faced a choice: appeal to the Supreme Court, or accept defeat and approve the ETFs. As a preliminary matter, the SEC could potentially appeal the ruling (up until October 30, 2023), and the appeals process can take time. But appealing would mean arguing that their own approved Bitcoin futures ETFs were somehow fundamentally different from spot ETFs—a position that would be difficult to maintain before the Supreme Court.

The decision marks the latest in a string of crypto losses for the SEC, following Ripple's victory over the SEC in July. Rather than setting clear rules of the road for crypto, Chairman Gensler has pursued one-off enforcement actions against digital asset companies and made up the law as he goes along," said Chamber of Progress CEO Adam Kovacevich. "That strategy hasn't held up in court."

Behind the scenes, the floodgates were opening. BlackRock, the world's largest asset manager with $10 trillion under management, had filed for a spot Bitcoin ETF in June 2023, timing their application perfectly with Grayscale's likely victory. Fidelity, Invesco, WisdomTree, and others rushed to file their own applications. The race was on.

The SEC chose not to appeal that ruling, making today's action a formality. The ball now returns to the SEC's court, where the agency could choose to approve Grayscale's application or perhaps reject it on other grounds. But everyone knew the game was over. The SEC couldn't approve BlackRock's ETF while denying Grayscale's—not after losing in court.

What Grayscale had won wasn't just the right to convert to an ETF. They had broken the SEC's decade-long blockade against spot Bitcoin ETFs. They had forced the most powerful financial regulator in the world to treat Bitcoin as a legitimate asset class. But in winning this battle, they may have sealed their own fate.

The victory had come at a terrible cost. During the long legal battle, GBTC's discount had devastated investors, competitors had prepared superior products with lower fees, and billions had already been earmarked to flow out the moment conversion happened. Grayscale had won the war but might lose the peace.

VII. The ETF Conversion: Victory and Exodus (2024)

January 10, 2024 should have been Barry Silbert's coronation. After a decade of building, years of legal battles, and billions in investor capital, GBTC was finally becoming a spot Bitcoin ETF. The bell rang at the New York Stock Exchange, confetti fell, and champagne corks popped. Within hours, the celebration turned into a wake.

The fund, which won US Securities and Exchange Commission approval to convert to an ETF from a trust last week, has seen outflows totaling about $579 million, according to data compiled by Bloomberg. The exodus had begun before the markets even closed on day one. By the end of the first week, nearly $2 billion had fled. It was a stampede, not a celebration.

The numbers were staggering in their relentlessness. That's 53 straight trading days of outflows totaling $14.7 billion. GBTC became the first ETF in history to experience outflows every single trading day for over two months. I can't think of another time anything like this has happened. Even notorious underperformers had occasional good days. GBTC had none.

The culprit was obvious: fees. At 1.5%, GBTC's expense ratio is far and away the highest in the category—nearly 60 basis points more than the next-costliest fund, Hashdex Bitcoin ETF (DEFI)— and several times as expensive at IBIT, FBTC, and other large spot bitcoin ETFs, most of which charge between 20 and 25 basis points. While GBTC charged 1.5%, BlackRock's IBIT and Fidelity's FBTC charged 0.25%. For a $1 million investment, that's the difference between paying $15,000 or $2,500 per year.

The competition wasn't just cheaper—it was better. BlackRock's fast-growing iShares Bitcoin Trust (IBIT) and the Fidelity Wise Origin Bitcoin Fund (FBTC), for example, each carry fees of 0.25%. While IBIT has notched $9.7 billion of net inflows after nearly two months of trading, assets flowing into FBTC hit $6 billion Thursday. BlackRock's ETF became the fastest ever to reach $10 billion in assets under management.

What made the situation particularly painful was who was selling. This shift from a closed-end format to an ETF allowed investors to end a widely-used arbitrage trade , leading to significant sell-offs, including those by the estate of the defunct FTX exchange. The arbitrageurs who had bought GBTC at massive discounts were now rushing for the exits, booking their profits at the expense of long-term holders.

Genesis's bankruptcy estate was perhaps the most dramatic seller. Some industry watchers in X posts last week speculated that the outflows uptick could be driven in part by bankrupt lender Genesis, which was granted approval earlier this month to offload roughly $1.6 billion worth of GBTC shares. The very GBTC shares that Genesis had accepted as collateral from Three Arrows Capital were now being dumped on the market.

The mathematics of the outflow were brutal. Grayscale Bitcoin Trust (GBTC) has faced significant challenges, experiencing average daily outflows of $89.5 Million over the past 11 months, Farside data shows. Since its conversion into a spot ETF in January 2024, GBTC has recorded cumulative losses totaling $21.027 Billion. That's roughly three-quarters of the fund's assets, gone.

For Grayscale executives, watching their triumph turn to disaster must have been agonizing. It's weird because GBTC has incredible name recognition inside and even outside the crypto world. The firm behind the ETF, Grayscale, is spending millions of dollars marketing it; they've placed ads in subway stations and put on drone shows at ETF conferences. All that marketing couldn't overcome a simple math problem: why pay six times more for the same Bitcoin?

The irony was crushing. On the one hand, GBTC remains a massive fund with $26.6 billion in AUM, making it the 63rd largest of all U.S.-listed ETFs. At current asset levels, and an expense ratio of 1.5%, the ETF is generating almost $400 million in annual revenue for the firm. To put that in perspective, IBIT would need to reach $160 billion in AUM to match those levels of revenues based on its 0.25% expense ratio. Even hemorrhaging assets, GBTC was still a cash cow.

Michael Sonnenshein, Grayscale's CEO, tried to remain optimistic. Earlier this month, chief executive officer Michael Sonnenshein told CNBC that the firm would trim the fee, although he didn't provide a timeframe. "Typically when products are earlier in their lifecycle, when they're new to be introduced, these [fees] tend to be higher," Sonnenshein said. But the market wasn't waiting for Grayscale to find religion on fees.

The human stories behind the numbers were heartbreaking. Retail investors who had held GBTC for years through the discount, believing in the ETF conversion thesis, watched their patience rewarded with... nothing. The discount disappeared, yes, but so did their capital as they fled to cheaper alternatives. The opportunity cost of loyalty was measured in tens of thousands of dollars for even modest portfolios.

JPMorgan's analysts had predicted outflows, but reality exceeded even their pessimistic forecasts. Since its transformation into an exchange-traded fund on January 11, the fund has experienced about $4.8 billion in withdrawals, exceeding JPMorgan's initial estimate of approximately $3 billion. The Wall Street consensus had underestimated just how violently capital would rotate to cheaper options.

The competitive dynamics were ruthless. But it's also unique in another way that structurally works against it. It converted into an ETF the same day on which a bunch of other competing funds launched— and many of those other funds had strong brands behind them, like iShares and Fidelity. That neutralized one of GBTC's key advantages. Additionally, because those rival funds increased their assets and liquidity so quickly, it neutralized another one of GBTC's selling points.

Seven months after conversion, the bleeding hadn't stopped. The pace of the bleeding may have slowed, but investors are still taking money out of the Grayscale Bitcoin Trust (GBTC), more than seven months after Grayscale converted the fund into an ETF. Over the past week, approximately $200 million has left the fund, while over the past month, outflows have totaled $935 million. The outflows combined with recent price declines have shrunk GBTC's total assets under management to $13.1 billion, its lowest AUM since March 2023, when bitcoin was trading a little above $20,000.

The great rotation was complete. GBTC has lost its ranking as the No.1 spot bitcoin ETF to the $20 billion iShares Bitcoin Trust (IBIT), and it's conceivable that it could eventually even fall behind the current No. 3 spot bitcoin ETF, the $10 billion Fidelity Wise Origin Bitcoin Fund (FBTC). The king was dead, and there would be no resurrection.

Grayscale's attempt at damage control—launching a "mini" Bitcoin ETF with lower fees—felt like too little, too late. GBTC's expense ratio is also 10 times that of the least least-costliest fund, the Grayscale Bitcoin Mini Trust (BTC), another spot bitcoin ETF backed by Grayscale that debuted at the end of July. In an investor-friendly move, investors in GBTC had 10% of their positions swapped into BTC, dramatically lowering the expense ratio for a portion of their holdings. On the other hand, that still left 90% of their positions in the much more expensive GBTC.

The victory GBTC had fought so hard for—ETF approval—had become its undoing. By forcing the SEC to approve spot Bitcoin ETFs, Grayscale had opened the door for every major asset manager in America to compete directly with them. And in that competition, GBTC's first-mover advantage meant nothing compared to BlackRock's scale, Fidelity's distribution, and everyone else's lower fees.

The trust that had introduced America to Bitcoin was being abandoned by America. The irony was complete: in winning the right to be an ETF, GBTC had signed its own death warrant.

VIII. The DCG Drama: Contagion, Lawsuits, and Survival

VIII. The DCG Drama: Contagion, Lawsuits, and Survival

The collapse began with a single bad bet. In May 2022, Three Arrows Capital had borrowed $2.3 billion from Genesis Trading, DCG's crypto lending arm, collateralized primarily with GBTC shares and the now-worthless LUNA tokens. When Terra's algorithmic stablecoin imploded that month, taking $60 billion in value with it, 3AC's portfolio vaporized. By June, the hedge fund was insolvent, leaving Genesis with a $1.2 billion hole and rapidly depreciating GBTC shares as collateral.

Barry Silbert's empire, built over a decade of careful positioning, was suddenly teetering on the edge of collapse. Digital Currency Group, the parent company of both Grayscale and Genesis, found itself in an impossible position: Genesis needed immediate capital to avoid bankruptcy, but DCG's primary asset was GBTC shares trading at a massive discount. It was like trying to bail out a sinking ship with buckets full of holes.

The interconnections within DCG made everything worse. When Genesis needed liquidity, DCG couldn't simply sell GBTC shares—that would crash the price further and potentially trigger a death spiral. Instead, Silbert orchestrated a complex series of intercompany loans and promissory notes that would later attract regulatory scrutiny. DCG issued a $1.1 billion promissory note to Genesis due in 2032, essentially kicking the can down the road while hoping crypto markets would recover.

But the respite was brief. On November 8, 2022, FTX collapsed in spectacular fashion, taking with it another major Genesis counterparty. Alameda Research, which had borrowed hundreds of millions from Genesis using GBTC as collateral, was suddenly bankrupt. Within days, Genesis was forced to halt withdrawals, freezing $900 million belonging to users of Gemini's Earn program.

Cameron Winklevoss went nuclear. In a blistering public letter on January 2, 2023, he accused Silbert of operating a fraud: "For the past six weeks, we have done everything we can to engage with you in a good faith and collaborative manner in order to reach a consensual resolution for you to pay back the $900 million that you owe... It is now becoming clear that you have been engaging in bad faith stall tactics."

The letter detailed alleged deceptions and accounting tricks, claiming DCG had hidden Genesis's insolvency while continuing to collect fees from trapped investors. Winklevoss's most damaging allegation: that DCG had known about the $1.2 billion 3AC hole since July 2022 but concealed it from Gemini and other creditors while continuing to accept new deposits into the Earn program.

Silbert fired back on Twitter, denying the allegations and claiming DCG had injected $2 billion into Genesis since the crisis began. But the damage was done. Trust in the DCG empire had evaporated, and creditors were circling like vultures.

On January 19, 2023, Genesis Global Capital filed for Chapter 11 bankruptcy protection in the Southern District of New York, listing between $1 billion and $10 billion in liabilities to more than 100,000 creditors. The filing revealed the true scope of the disaster: Genesis owed $3.6 billion to its top 50 creditors alone, with Gemini at the top of the list.

The bankruptcy documents painted a picture of a company that had been technically insolvent for months, surviving only through creative accounting and intercompany transfers. Genesis had been using customer funds to cover losses, borrowing from Peter to pay Paul while hoping for a market recovery that never came.

Then came the regulatory hammer. On October 19, 2023, New York Attorney General Letitia James filed a lawsuit against DCG, Silbert, Genesis, and former Genesis CEO Michael Moro, alleging a $1.1 billion fraud. The complaint was devastating in its specificity: "Through a campaign of lies and deceptive statements delivered to the marketplace and to investors over the course of nearly two years, the defendants misled investors and lenders... in an effort to artificially prop up the companies."

The AG's office alleged that DCG and Genesis had engaged in a circular scheme, with DCG borrowing Bitcoin from Genesis, then using GBTC shares to repay the loans when it couldn't deliver actual Bitcoin. This created an illusion of solvency while actually deepening both companies' financial holes. The scheme allegedly allowed them to continue collecting fees and attracting new investment even as they spiraled toward insolvency.

Internal documents subpoenaed by the AG revealed panic behind the scenes. In one email, a Genesis executive wrote about the need to "manage the narrative" around their solvency. Another showed DCG executives calculating how long they could maintain the facade before running out of cash entirely.

The settlement negotiations were brutal. Genesis's creditors, led by an ad hoc committee of major institutional lenders, initially demanded full repayment plus damages. DCG countered that liquidating its assets would destroy value for everyone. The negotiations dragged on for months, with both sides leaking damaging information to pressure the other.

In February 2024, a breakthrough: DCG agreed to a comprehensive settlement that would see it pay over $2 billion to Genesis creditors. The deal required DCG to sell assets, take on new debt, and importantly, maintain GBTC's operations to preserve fee income for repayment. Silbert would remain CEO but under strict oversight from a creditor committee.

The terms were harsh but survivable. DCG would pay $500 million immediately, funded by asset sales and a new credit facility. Another $700 million would come due over the next two years, secured by GBTC fee income. The remaining obligations would be satisfied through a combination of DCG equity and long-term payment plans.

For Genesis creditors, the recovery was better than expected—most would receive 70-80 cents on the dollar, far above typical crypto bankruptcy recoveries. Gemini Earn users would be made mostly whole, ending the Winklevoss brothers' crusade against Silbert.

But the cost to DCG's reputation was permanent. The company that had positioned itself as crypto's responsible adult, the bridge between Wall Street and Bitcoin, had been revealed as another overleveraged player in crypto's casino. Regulatory settlements continued to pile up, with DCG ultimately paying hundreds of millions in fines to various state and federal agencies.

The survival of GBTC through this crisis was perhaps the most remarkable aspect. Despite everything—the bankruptcy of its sister company, criminal investigations of its parent, the exodus of billions in assets—the trust continued operating. The Bitcoin remained secure, the NAV was published daily, and the 2% management fee kept flowing.

That fee income, ironically, may have been what saved DCG. Even as GBTC bled assets, it still generated hundreds of millions annually—a reliable cash flow that creditors could count on for repayment. The product Silbert created to democratize Bitcoin access had become the life raft keeping his empire afloat.

IX. Playbook: Financial Innovation Lessons

The GBTC saga offers a masterclass in financial innovation's double-edged sword—how regulatory arbitrage can create billion-dollar businesses and destroy them just as quickly. The playbook written by Barry Silbert's experiment contains lessons that extend far beyond crypto, speaking to fundamental truths about market structure, competitive dynamics, and the cost of being first.

The Monopoly Trap

GBTC's initial success stemmed from its monopoly position—it was the only SEC-compliant way for institutions to buy Bitcoin. This exclusivity justified the 2% management fee and created the premium that made early investors fortunes. But monopolies in financial products are inherently unstable. Unlike technology platforms with network effects or consumer brands with emotional loyalty, financial products are commodities. Once competitors arrive with identical offerings at lower prices, the monopoly premium evaporates instantly.

The lesson: Regulatory moats are temporary. What seems like an impregnable advantage—being the only approved product in a category—becomes a liability when the regulatory environment shifts. GBTC's structure, perfect for a monopoly, became an albatross in a competitive market. Companies building on regulatory arbitrage must plan for the day their exclusive position ends.

The Premium/Discount Paradox

The GBTC premium wasn't a bug—it was the feature that attracted billions in arbitrage capital. Hedge funds borrowing Bitcoin to capture the premium created a virtuous cycle: their buying drove Bitcoin prices higher, which attracted more retail interest, which expanded the premium further. But this same mechanism worked in reverse when the premium flipped to a discount, creating a doom loop of selling pressure and value destruction.

This dynamic appears throughout finance. Closed-end funds regularly trade at discounts to NAV. SPACs see their shares detach from trust value. Even ETFs can trade away from their underlying assets during market stress. The lesson: any structure that allows price to diverge from fundamental value creates systemic risk. The arbitrageurs who profit from closing these gaps in good times become forced sellers in bad times, amplifying volatility.

First-Mover Disadvantage

Being first in financial innovation often means bearing all the costs while competitors reap the benefits. GBTC spent millions in legal fees fighting the SEC, establishing precedents that BlackRock and Fidelity could exploit for free. Grayscale educated investors about Bitcoin exposure through traditional securities, creating demand that competitors would ultimately capture.

This pattern repeats across finance. The first high-yield bond ETF, the first inverse ETF, the first cryptocurrency exchange—pioneers rarely dominate their categories long-term. They establish the market, prove the concept, fight the regulatory battles, then watch nimbler competitors offer better versions of their innovation.

The Redemption Mechanism Matters

GBTC's fatal flaw was its inability to allow redemptions. This wasn't an oversight—it was a deliberate choice that made regulatory approval easier and protected the fee stream. But it created a roach motel: investors could check in but couldn't check out. When sentiment shifted, this one-way door turned GBTC into a value trap.

The broader lesson extends beyond crypto. Any financial product that restricts exit—whether through lockups, gates, or structural limitations—must offer compelling benefits to justify that illiquidity. When those benefits disappear, as GBTC's monopoly did, the restrictions become existential threats.

Network Effects in Finance Are Weak

Unlike technology platforms, financial products rarely benefit from true network effects. GBTC's millions of shareholders didn't make the product more valuable to new buyers. Its massive AUM didn't create switching costs. When cheaper alternatives appeared, investors fled without hesitation.

This reality challenges the Silicon Valley playbook of "grow first, monetize later." In financial products, sustainable competitive advantages come from only three sources: proprietary strategies that can't be replicated, distribution networks that provide exclusive access, or cost structures that enable permanent price leadership. GBTC had none of these.

The Cascade Effect of Interconnection

DCG's structure—with Grayscale, Genesis, and other entities under one umbrella—was supposed to create synergies. Instead, it created contagion. Genesis's bad loans threatened Grayscale's operations. GBTC's discount undermined Genesis's collateral. Each entity's problems amplified the others'.

This interconnection risk appears throughout finance, from the 2008 financial crisis to the recent regional banking turmoil. Diversification within a single corporate structure isn't true diversification if the entities share counterparties, collateral, or funding sources. True resilience requires genuine independence, not just separate legal entities.

Timing the Regulatory Window

GBTC succeeded by exploiting a regulatory gap—the SEC wouldn't approve a Bitcoin ETF but couldn't prevent a grantor trust from holding Bitcoin. This window lasted nearly a decade, generating billions in fees. But Grayscale failed to anticipate how quickly that window would close once real competition arrived.

The lesson for financial innovators: regulatory arbitrage has an expiration date. Products built on regulatory gaps must either evolve beyond their original advantage or extract maximum value before the gap closes. Grayscale did neither, maintaining high fees and restrictive terms even as competition loomed.

The Price of Complexity

GBTC's structure—a trust that traded like a stock but couldn't create or redeem shares like an ETF—confused investors and created unexpected risks. Many retail buyers didn't understand why GBTC could trade at such massive premiums or discounts. This complexity, initially a feature that enabled regulatory approval, became a bug that destroyed billions in value.

Simple products win in finance. Complexity might enable regulatory arbitrage or higher fees initially, but it creates fragility. When markets stress, complex products break in unexpected ways. The institutions that survive are those that resist the temptation to engineer clever structures and instead offer straightforward value propositions.

The Innovation Cycle

GBTC's lifecycle illustrates the natural progression of financial innovation: pioneering innovation, regulatory arbitrage, monopoly profits, competitive entry, commoditization, and eventual disruption. This cycle typically takes 5-10 years in traditional finance but compressed to just 3-4 years in crypto's accelerated timeline.

Understanding where a product sits in this cycle is crucial for investors and operators. The strategies that work during the monopoly phase—high fees, restrictive terms, focus on education—become liabilities during commoditization. Grayscale's failure to adapt its strategy as GBTC moved through this cycle cost investors billions.

X. Bear vs. Bull Case Analysis

The Bear Case: A Melting Ice Cube

The mathematics of GBTC's decline appear irreversible. At 1.5% annual fees versus competitors charging 0.2%, GBTC bleeds $300 million more in fees annually per $20 billion in AUM—dead money that compounds against investors year after year. Even if Grayscale cut fees to match competitors tomorrow, the damage to their reputation is permanent. Why would investors return to a manager that extracted excessive fees for over a decade?

The outflow data tells a brutal story. Fifty-three consecutive days of redemptions isn't just a trend—it's a verdict. Institutional investors have voted with their feet, and they're not coming back. The $21 billion that fled represents sophisticated money that did the math: every basis point matters when holding an asset as volatile as Bitcoin. GBTC's current AUM of roughly $21 billion might seem substantial, but at the current burn rate, it could halve within two years.

The structural disadvantages run deeper than fees. GBTC carries tax liabilities from years of trading that new ETFs don't have. Its massive size makes it less nimble in execution. Its association with the DCG crisis creates reputational overhang. Every advantage GBTC once held has inverted into a disadvantage.

The competitive landscape offers no relief. BlackRock and Fidelity aren't just offering lower fees—they're bundling Bitcoin ETFs with other products, providing superior customer service, and leveraging massive distribution networks. These aren't startups that might fail; they're the titans of asset management with unlimited resources to crush competition.

The DCG overhang remains toxic. Despite settlements, the parent company still needs cash to satisfy creditors. If forced to sell GBTC or dramatically cut fees to avoid further lawsuits, the revenue stream supporting DCG's recovery evaporates. It's a catch-22: maintain high fees and lose all assets, or cut fees and lose the revenue needed for survival.

Most damning is the lack of differentiation. GBTC holds the same Bitcoin as every other ETF. It provides the same exposure. It trades on the same exchanges. In a commoditized market, the high-cost provider doesn't survive—it just manages decline. GBTC could become finance's equivalent of a legacy airline: still operating but perpetually shrinking, sustained only by inertia and switching costs.

The Bull Case: Reputation and Resilience

Yet GBTC's obituary may be premature. The trust still manages $21 billion—more than most ETF providers dream of achieving. At 1.5% fees, that generates $315 million annually, enough to sustain operations indefinitely even with continued outflows. This isn't a startup burning cash; it's a profitable business with a decade-long track record.

The brand value remains substantial. "GBTC" has become synonymous with institutional Bitcoin investment. During the next crypto bull market, when retail investors flood back, many will default to the name they know. Grayscale's marketing spend—subway ads, conference sponsorships, media campaigns—has built awareness that competitors would need years and millions to replicate.

The institutional memory matters. GBTC survived the 2017 bubble, the 2018 crash, the COVID pandemic, the 2022 crypto winter, and its own parent company's near-bankruptcy. It never missed a NAV calculation, never lost Bitcoin to hacks, never failed to trade. That reliability through crisis has value that's hard to quantify but easy to appreciate during the next market stress.

The fee differential might compress. Grayscale has already signaled willingness to reduce fees, and a cut to 0.75% would dramatically slow outflows while maintaining profitability. Moreover, as Bitcoin ETFs mature, investors might accept higher fees for perceived safety and track record, just as they do with actively managed funds that outperform.

The regulatory environment could shift in GBTC's favor. If the SEC implements new restrictions on Bitcoin ETFs, GBTC's established structure and compliance history become advantages. If crypto faces another crisis requiring government intervention, regulators will likely preserve the oldest, most established players while letting newcomers fail.

The technical position has improved dramatically. The discount has vanished, removing the main source of selling pressure. Bankruptcy estates have largely liquidated their positions. The weak hands have been thoroughly shaken out. What remains are long-term holders who've already accepted the fee structure.

Most intriguingly, GBTC could pivot to differentiation. With its massive Bitcoin holdings, Grayscale could offer services competitors can't: securities lending, options strategies, or yield generation through DeFi integration. The trust structure that seemed like a disadvantage could enable innovations that ETF regulations prohibit.

The Verdict

The bear case relies on extrapolating current trends indefinitely—outflows continuing at the same pace, fees remaining static, competition intensifying. But markets rarely move linearly. The next Bitcoin bull run could change everything, bringing new investors who value brand recognition over basis points.

The bull case requires believing in mean reversion—that GBTC's discount to fair value in terms of market share will eventually correct, that fees will rationalize, that brand value will reassert itself. History suggests established financial products rarely disappear entirely; they find equilibrium at lower but sustainable levels.

The most likely outcome sits between extremes. GBTC probably stabilizes at $10-15 billion in AUM, cuts fees to 0.75-1%, and remains profitable but diminished. It becomes the Pan Am of crypto—a pioneer that survived its glory days to become a shadow of its former self, still flying but no longer defining the industry it helped create.

XI. Epilogue & What It All Means

The transformation of GBTC from crypto's gateway drug to its cautionary tale encapsulates the entire digital asset industry's journey from rebellious startup to regulated commodity. What began as Barry Silbert's hack to give institutions Bitcoin exposure became the test case for crypto's integration into traditional finance—a test that revealed both the promise and peril of building bridges between incompatible worlds.

The supreme irony of GBTC's story is that its greatest success enabled its greatest failure. By forcing the SEC to approve spot Bitcoin ETFs, Grayscale didn't just win a regulatory battle—it destroyed its own moat. The legal victory that should have been the culmination of a decade's work instead marked the beginning of the end. It's the corporate equivalent of a Greek tragedy: the hero's greatest strength becomes their fatal flaw.

This pattern—innovation creating its own obsolescence—runs throughout financial history. The junk bond pioneers of the 1980s were displaced by investment banks. The first index funds were overtaken by Vanguard's low-cost model. The original ETF creators watched BlackRock dominate their invention. GBTC joins this pantheon of financial innovations that succeeded so completely they eliminated their own competitive advantage.

But GBTC's legacy extends beyond its own decline. The trust proved that institutional demand for Bitcoin was real, not theoretical. It demonstrated that crypto could operate within existing regulatory frameworks, not just outside them. It showed that billions of dollars would flow into digital assets if given a compliant pathway. Every Bitcoin ETF that launches, every institutional allocation to crypto, every pension fund that buys digital assets traces back to GBTC proving the concept.

The human cost of this innovation can't be ignored. Retail investors who bought GBTC at 130% premiums lost fortunes. Institutions that held through the 45% discount watched billions evaporate. The Gemini Earn users who had funds frozen, the Genesis creditors who took haircuts, the employees who lost jobs—all paid the price for financial innovation's growing pains. Creative destruction sounds clinical in economics textbooks but feels devastating when it's your wealth being destroyed.

Barry Silbert's pivot to decentralized AI through his new venture Yuma represents more than just personal evolution—it's an acknowledgment that the financial bridge-building era has ended. The infrastructure for institutional crypto investment now exists; the pioneers' work is done. Silbert, like many first-generation crypto entrepreneurs, is moving on to the next frontier, leaving behind a transformed but troubled legacy.

The broader implications for crypto remain profound. GBTC proved that regulatory arbitrage can work but can't last. It showed that being first matters less than being best. It demonstrated that complex financial structures create hidden risks that only appear during stress. These lessons will shape the next generation of crypto products, from tokenized real-world assets to DeFi integration with traditional finance.

For traditional finance, GBTC serves as both template and warning. The template: how to package unconventional assets for conventional investors. The warning: that financial innovation without structural innovation creates unstable products. Every asset manager now rushing to tokenize stocks, bonds, and real estate should study GBTC's rise and fall carefully.

The regulatory implications reverberate globally. GBTC's successful lawsuit against the SEC didn't just enable Bitcoin ETFs—it established precedent that regulatory agencies must treat similar products similarly. This principle will constrain regulatory creativity going forward, forcing more consistent frameworks across asset classes. The age of regulatory arbitrage might be ending, replaced by regulatory standardization.

The market structure lessons are equally important. GBTC showed that closed-end funds are poorly suited for volatile assets, that redemption mechanisms matter more than management expertise, that fee compression in commoditized products is inevitable and brutal. These aren't just crypto lessons—they apply to any asset class undergoing institutionalization.

Looking forward, GBTC's story suggests the crypto industry is maturing from its wild west phase into something more resembling traditional finance—complete with all its benefits and limitations. The days of 100% premiums and regulatory arbitrage are ending. The future belongs to those who can compete on price, service, and scale—the boring virtues that dominate mature markets.

Yet something vital may be lost in this transition. GBTC, for all its flaws, represented crypto's hacker ethos applied to traditional finance—finding clever workarounds to seemingly impossible problems. As crypto becomes just another asset class, served by the same giant asset managers through the same standardized products, it risks losing the innovative spirit that made it revolutionary.

The final lesson of GBTC might be the most profound: that building bridges between old and new systems is necessary but painful work. The bridge builders—like Silbert and Grayscale—often don't survive to see the traffic flowing freely. They exhaust themselves in construction, make compromises that later seem inexcusable, and watch others traverse the paths they blazed.

GBTC will likely persist for years, perhaps decades, as a zombie fund—still operating, still collecting fees, but no longer growing or innovating. It will serve as a monument to crypto's adolescence, when the industry was mature enough to attract institutional capital but not mature enough to serve it efficiently. Future financial historians will study GBTC as we study the original joint-stock companies or the first mutual funds—as primitive but necessary steps toward modern market structure.

The trust that started as a hack became an institution, then became a relic. But in that journey, it changed finance forever. Every pension fund that now owns Bitcoin, every 401(k) that offers crypto exposure, every traditional broker that sells digital assets owes a debt to GBTC's painful pioneering. The bridge it built might be crumbling, but the path it opened will never close.

In the end, GBTC's story isn't really about Bitcoin or even crypto. It's about the cost of innovation in regulated markets, the price of being first, and the inevitable obsolescence of revolutionary products. It's about how financial systems evolve not through grand design but through messy experimentation, failed structures, and expensive lessons.

The Grayscale Bitcoin Trust won't be remembered as a success or a failure, but as something more complex: a necessary transition, a brilliant mistake, a bridge that had to be built even if it couldn't last. In finance, as in evolution, the transitional forms rarely survive, but without them, nothing would ever change.

XII. Recent News**

January 2024: The Conversion and Exodus**

On January 11, 2024, GBTC officially converted from a trust to a spot Bitcoin ETF and began trading on NYSE Arca, marking a historic victory after years of legal battles. However, the celebration was short-lived. Within days, nearly $579 million flowed out of the fund, beginning what would become the longest outflow streak in ETF history.

By March 29, 2024, GBTC had experienced 53 straight trading days of outflows totaling $14.7 billion—a record that may never be broken. Industry analysts couldn't recall another time anything like this had happened in the ETF market.

The Peak Outflow Crisis (March 2024)

March 2024 marked the darkest period for GBTC. On March 18, outflows hit a single-day record of $643 million, contributing to net outflows of $154 million for all Bitcoin ETFs combined. By March 22, GBTC saw another $359 million exit in a single day, pushing weekly outflows over $830 million.

The culprit remained the same: GBTC's 1.5% fee was significantly higher than competitors. BlackRock's IBIT and Fidelity's FBTC each charged only 0.25%, making GBTC six times more expensive.

The Mini Bitcoin Trust Solution (July 2024)

In response to the hemorrhaging assets, Grayscale launched a creative solution. On July 30, 2024, Grayscale set a record date for the initial creation and distribution of shares of Grayscale Bitcoin Mini Trust (BTC) to GBTC shareholders. Each GBTC shareholder received BTC shares on a 1:1 ratio, with GBTC contributing 10% of its Bitcoin holdings to the new fund.

The Mini Trust launched on July 31, 2024, with a dramatically lower expense ratio of 0.15%—one-tenth of GBTC's fee. This spin-off allowed existing investors to reduce their blended fee exposure while maintaining their Bitcoin allocation.

Current State and Cumulative Damage

As of late 2024, the damage to GBTC has been catastrophic. GBTC has seen significant outflows of $21 billion since its conversion in January 2024. Over the past 11 months, GBTC has experienced average daily outflows of $89.9 million, making it the only U.S. spot Bitcoin ETF to generate negative investor flows.

Meanwhile, competitors have thrived. BlackRock's IBIT has emerged as the dominant player, pulling in $35.883 billion since launch, including $153.3 million daily. The contrast couldn't be starker: while GBTC bleeds assets, newer ETFs capture the institutional flows that once belonged exclusively to Grayscale.

Management's Response

Grayscale's leadership has tried to remain optimistic. In March 2024, CEO Michael Sonnenshein confirmed that "over time, as this market matures, the fees on GBTC will come down", though he provided no specific timeline. By April, Sonnenshein claimed the fund had begun to reach an "equilibrium" with its outflows, suggesting the worst might be over.

The company has also pursued aggressive marketing, placing ads in subway stations and putting on drone shows at ETF conferences, but these efforts have failed to stem the tide against mathematical reality: investors won't pay six times more for identical Bitcoin exposure.

Beyond Bitcoin: The Ethereum Disaster

GBTC's problems extend beyond Bitcoin. Grayscale's Ethereum Trust ETF (ETHE) has faced $3.5 billion in losses since its launch in July 2024, mirroring GBTC's struggles. Meanwhile, BlackRock's iShares Ethereum Trust and Fidelity Ethereum Fund have taken in $3.2 billion and $1.4 billion respectively, showing that Grayscale's brand damage extends across asset classes.

The Ongoing Reality

Despite the massive outflows, GBTC still manages $21.19 billion in net assets as of August 2025, maintaining its position as one of the largest Bitcoin ETFs by AUM. However, this represents a decline of over 75% from its peak holdings, and the bleeding continues—albeit at a slower pace.

The fund that pioneered institutional Bitcoin access has become a cautionary tale of how quickly market leadership can evaporate when competitive advantages disappear. While GBTC survives, it does so as a shadow of its former self, generating substantial fee revenue from a shrinking base while watching competitors capture the market it created.

XIII. Links & Resources

Official Grayscale Resources: - Grayscale Bitcoin Trust official page: etfs.grayscale.com/gbtc - Grayscale Bitcoin Mini Trust: etfs.grayscale.com/btc - Regulatory filings: grayscale.com/documents#regulatoryfilings - Investor relations: [email protected]

Court Documents & Legal Filings: - Grayscale v. SEC Court Opinion (August 29, 2023): D.C. Circuit Court of Appeals - Genesis Bankruptcy Docket: Southern District of New York, Case No. 23-10063 - NY Attorney General DCG Lawsuit (October 2023): NY State Court

Market Data & Analytics: - GBTC Premium/Discount Tracker: ycharts.com - Daily ETF Flow Data: BitMEX Research, Farside Investors, SosoValue - Bitcoin ETF Comparison Tool: etf.com - Historical GBTC Data: Bloomberg Terminal (subscription required)

Key Research Reports: - "The GBTC Arbitrage Trade" - Three Arrows Capital (2021) - "Bitcoin ETF Market Analysis" - JPMorgan Research (2024) - "Digital Asset Fund Flows" - CoinShares Weekly Reports - "GBTC Discount Analysis" - Morningstar Research

Books & Long-Form Analysis: - "Digital Gold" by Nathaniel Popper (Bitcoin's early history) - "The Bitcoin Standard" by Saifedean Ammous - "Kings of Crypto" by Jeff John Roberts (Coinbase and crypto's rise)

Podcast Episodes & Interviews: - Barry Silbert on "Unchained" with Laura Shin (Multiple episodes) - Michael Sonnenshein CNBC interviews (2024) - "What Bitcoin Did" Peter McCormack's GBTC analysis episodes - Bloomberg Crypto Report coverage of GBTC conversion

Academic Papers: - "The Economics of Cryptocurrency Pump and Dump Schemes" - Journal of Monetary Economics - "Closed-End Fund Discounts and Financial Market Equilibrium" - Journal of Finance - "Bitcoin ETFs and Market Efficiency" - Various working papers

News Archives: - CoinDesk's comprehensive GBTC coverage - The Block's ETF flow tracking - Bloomberg's daily ETF analysis - Wall Street Journal's Digital Currency Group investigations

Regulatory Documents: - SEC Bitcoin ETF denial orders (2017-2022) - SEC approval order for spot Bitcoin ETFs (January 2024) - CFTC Bitcoin futures approval documentation - Congressional testimony on digital assets

Data Visualization Tools: - TradingView GBTC charts - Glassnode on-chain analytics - CoinGecko ETF tracker - Messari institutional research platform

This comprehensive resource list provides readers with the tools to conduct their own deep dive into the GBTC saga, from its pioneering early days through its current struggles as a high-fee legacy product in a competitive market.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube