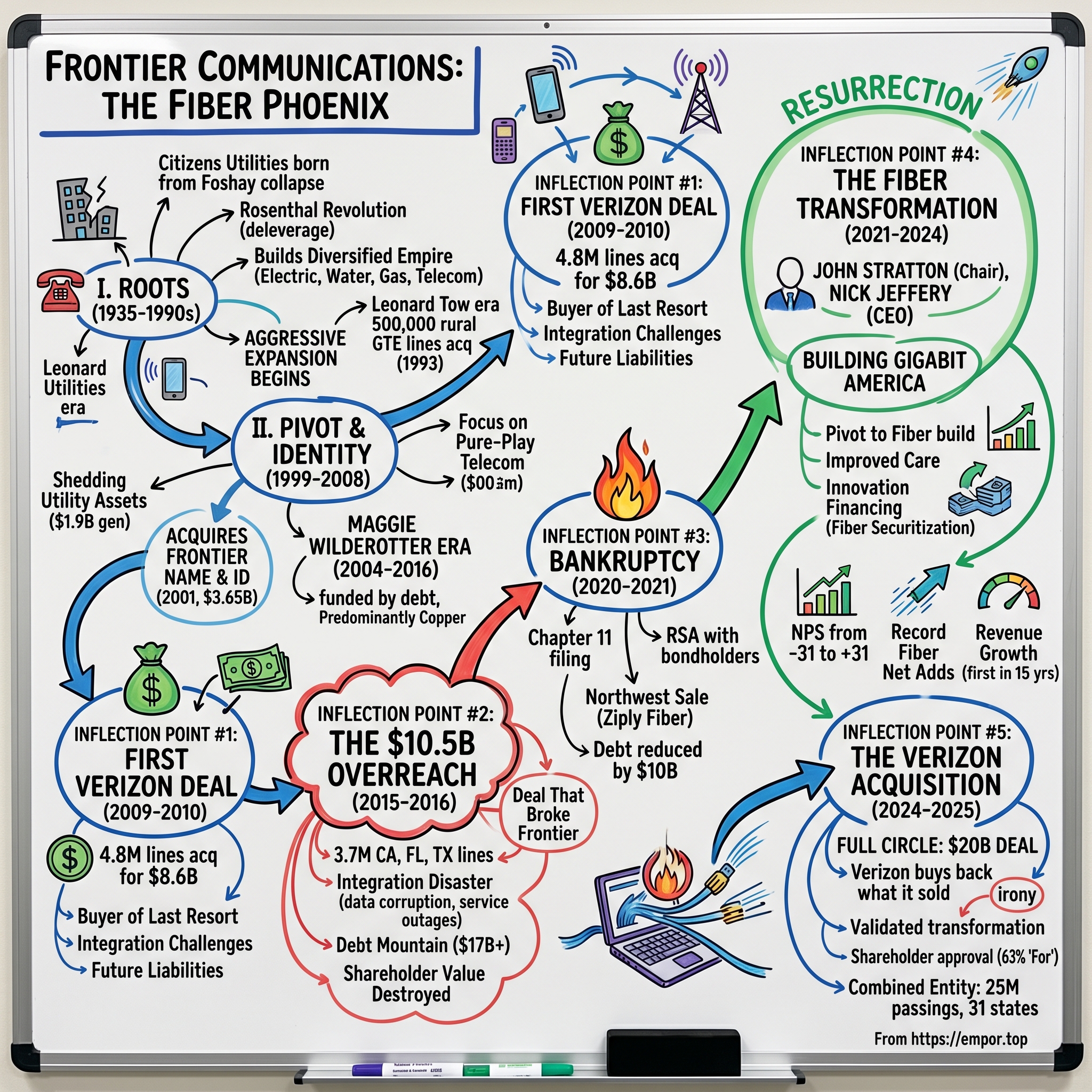

Frontier Communications: The Fiber Phoenix

I. Introduction & Episode Roadmap

Picture this: September 2024. Hans Vestberg, CEO of Verizon, stands before a bank of cameras announcing a $20 billion deal to acquire Frontier Communications. The irony is almost too perfect to ignore. Just fifteen years earlier, Verizon had handed over millions of wireline customers to Frontier in what amounted to a confession that rural and suburban copper networks were dead weight. Now, Verizon wants it all back—and they're paying a premium.

The story of Frontier Communications is one of the most instructive case studies in American business history: a ninety-year odyssey from Depression-era utility conglomerate to debt-fueled consolidator to bankruptcy casualty to fiber-first phoenix. Frontier stands today as the largest pure-play fiber provider in the U.S., driven by its purpose of "Building Gigabit America®."

How did a company that went bankrupt in 2020 with over $17 billion in debt become a $20 billion acquisition target just four years later? The answer involves a remarkable transformation story—one that offers profound lessons about the perils of debt-fueled empire building, the existential importance of technology transitions, and the surprising possibility of corporate redemption.

This is not just a telecom story. It's a story about American infrastructure, about the economics of rural connectivity, about what happens when a company mistakes acquisition for strategy—and what happens when fresh leadership finally gets the formula right. In just four years, the team worked together to transform Frontier "from a bankrupt and broken legacy telephone business into the largest pure-play fiber internet company in the country."

The central question we'll answer: How did a rural utility company from the 1930s survive bankruptcy, shed $10 billion in debt, and emerge as a fiber-first broadband champion—only to find itself acquired by the very company that had once cast it aside?

II. Origins: Citizens Utilities & The Diversified Utility Model (1935–1990s)

The Foshay Collapse and Corporate Rebirth

To understand Frontier, you must first understand its unlikely birth amid the wreckage of one of America's great financial frauds. Citizens Utilities was created in 1935 during a government reorganization of the utilities industries. The company was formed from several smaller utilities companies previously controlled by the Public Utilities Consolidated Corporation.

Public Utilities was assembled by W. B. Foshay. During the 1920s, Foshay had a relatively easy time acquiring utility assets and other properties with unsecured debt. The company owned telephone, electric power, and gas operations in several states and controlled additional businesses in Alaska and Nicaragua.

The Foshay story is a cautionary tale that would echo through Frontier's own history decades later. Unable to sustain his business, Foshay's company was forced to reorganize in 1928 to avoid bankruptcy. The financial crisis in 1929 that began the Great Depression was caused by thousands of investors whose holdings were financed with up to 90 percent debt. When confidence in this huge debt collapsed, capital markets dried up, forcing companies like Public Utilities to fail almost immediately.

Foshay was convicted of three counts of mail fraud and sent to federal prison, serving three years before his sentence was commuted by President Roosevelt. President Truman fully pardoned Foshay in 1947.

From this wreckage emerged Citizens Utilities, incorporated in 1935 in Delaware as the Citizens Utilities Company. The early years were modest—while Citizens Utilities managed to survive the 1930s, it was hardly a prosperous concern. After World War II came to a close it had revenues of $2.4 million and earnings of less than $180,000.

The Rosenthal Revolution

The company's fortunes changed dramatically in 1945 with the arrival of a young Wall Street analyst named Richard Rosenthal. It attracted the attention of a young Wall Street financier. Rosenthal was born in Canada in 1915 and came to the United States six years later. He earned an undergraduate degree at New York University, graduating summa cum laude in 1936. He then spent two years in postgraduate studies at NYU before taking a job with a Wall Street investment firm.

After securing interest from the existing board members, the financiers hired Richard Rosenthal to oversee their investment. Rosenthal, at that time a 29-year-old financial consultant who was born in Canada and raised in Brooklyn, had studied finance at New York University and, after stints as an analyst with several Wall Street firms, set up his own consulting firm specializing in utility acquisitions.

Rosenthal's approach was revolutionary for a utility executive. During his first year in Minneapolis, as a director for Citizens Utilities, Rosenthal doubled shareholders' dividends and proposed so many changes in the company that he and his backers successfully waged a proxy fight to have him installed as president. In 1946 Rosenthal, at age 30, became the youngest company president in the industry at the time.

During his first ten years as president, Rosenthal doubled revenues and net income and reduced long-term debt from 85 percent of capitalization to 60 percent. The contrast with what would come later—Frontier loading up with debt through massive acquisitions—makes this early focus on deleveraging particularly poignant.

Building the Diversified Empire

Rosenthal's strategic vision was deceptively simple: spread risk across multiple utility types and geographies. He faced the task of nurturing the business. "I had to decide either to liquidate much of what was there and have Citizens be a one-category, one-area utility company," he told Barron's, "or to extend what was in place and have it become more multi-state and more variegated. I chose the latter." As a result, Citizens became diversified by region, insulated from local economic cycles and not excessively impacted by the decision of regulators in a particular state. Under Rosenthal, Citizens acquired more than 40 small companies in the electric, water, gas, wastewater, and telephone industries.

By the mid-1970s, Citizens Utilities' electric power business grew to 40 percent of total earnings. The lucrative three-state telephone operation contributed 31 percent, while water constituted 15 percent, and gas and sewage each registered seven percent.

This diversification served Citizens well for decades. Through such operational and geographic diversity, Citizens managed to de-emphasize the effects of crisis and regulation in any one area of jurisdiction. For example, disastrous weather or heavy regulation impacting one region was largely offset by the performance of another operation.

The Aggressive Expansion Begins

By the early 1990s, under new leadership, Citizens began pivoting toward telecommunications. Under chairman and CEO Leonard Tow, Citizens Utilities agreed to acquire 500,000 rural access lines from GTE in 1993. The transfers of lines and subsidiaries occurred separately in different states as different regulatory approvals were received. 190,000 lines in Idaho, Tennessee, West Virginia and Utah were officially transferred in late 1993.

Some of the Alltel lines were officially transferred to Citizens Telecommunications Company of the Volunteer State in Tennessee in September 1995. Citizens acquired Alltel lines in Pennsylvania, California, and Nevada in 1996. With major subsidiaries such as Electric Lightwave, Citizens had expanded into 18 states by the start of 1995, with services including telecommunications, natural gas, electric, water, and wastewater treatment.

The company was building something genuinely unique: a multi-state, multi-utility conglomerate that operated outside the traditional Bell System monopoly structure. But change was coming—change that would transform Citizens from a diversified utility into a pure-play telecom consolidator, setting the stage for both its greatest triumphs and its near-fatal overreach.

III. The Strategic Pivot: From Utilities to Pure-Play Telecom (1999–2008)

Shedding the Utility Assets

The late 1990s brought a fundamental strategic shift. Citizens Utilities Company announced plans in 1999 to sell its utilities assets and become solely a telecommunications company.

The divestiture proceeded rapidly. Citizens' water and wastewater operations (serving Arizona, California, Illinois, Indiana, Ohio and Pennsylvania) were sold for $835 million to American Water in October 1999, electric utility operations for $535 million in February 2000, and Louisiana natural gas assets to Atmos Energy in April 2000 for $375 million. The company was known as Citizens Utilities Company until the summer of 2000, when it was renamed Citizens Communications Company. Citizens then sold its Colorado gas utilities to Kinder Morgan in 2001.

Citizens Communications Company sold its remaining water and wastewater operations to American Water Works in 2002. Also that year it sold its Kauai Electric Company for $215 million and its Gas Company of Hawaii for $115 million, at which point Citizens had generated a total of $1.9 billion from selling off its utilities.

In one sense, this was a smart capital allocation move—monetizing stable but low-growth utility assets to fund expansion in the faster-moving telecom sector. But it also eliminated the diversification hedge that had protected the company for decades. Citizens was betting everything on telecommunications.

Acquiring the Frontier Name & Identity

The pivot's most significant milestone came in 2001. In July 2001, Citizens Communications acquired assets and the Frontier name from Global Crossing for $3.65 billion. Global Crossing had previously acquired the Frontier name when it had purchased Frontier Corporation two years prior.

This wasn't just an acquisition of lines—it was an acquisition of identity. The "Frontier" name carried brand equity as a recognizable telecom provider, particularly in the Northeast. In 2000, Citizens Communications Company agreed to acquire the local telephone operations and the Frontier brand from Global Crossing Ltd. for $3.65 billion in cash, a transaction that expanded its rural incumbent local exchange carrier footprint across 13 states and included approximately 1.1 million access lines. The deal allowed Citizens to rebrand its telecommunications operations under the Frontier name, emphasizing its focus on wireline services in underserved markets.

The timing was fortuitous. Global Crossing, a company built on the dot-com bubble's fiber dreams, was racing toward bankruptcy. For the year 2000, the company lost $1.4 billion. In 2001, the company sold its local telephone operations and the Frontier name to Frontier Communications for $3.65 billion in cash. Citizens got a bargain on a distressed sale—a playbook they would repeat, not always successfully.

The Maggie Wilderotter Era

The Citizens board recognized that pure-play telecom required different leadership skills. In 2004, they found their answer. In the fall of 2004, Wilderotter joined Citizens Communication in Stamford, Conn., as President and CEO and in 2006, became Chairman and CEO.

Maggie Wilderotter (born Mary Agnes Sullivan; February 9, 1955) is an American businessperson who is the chairwoman of Docusign, and the former chief executive officer of Frontier Communications from November 2004 to April 2015, then executive chairman of the company until April 2016.

Wilderotter arrived with serious telecom credentials. Wilderotter was Senior Vice President of Global Business Strategy and ran the Worldwide Public Sector at Microsoft. Before this, she was president and CEO of Wink Communications Inc., Executive Vice President of National Operations for AT&T Wireless Services Inc., Chief Executive Officer of AT&T's Aviation Communications Division, and a Senior Vice President of McCaw Cellular Communications Inc.

She inherited a company in transition. There had been a falling out between the previous CEO and the board. They tried to sell the company, but no one would buy it. So I came in with high expectations on what we could do, but there were pretty low expectations of the outcome for the company at that point. So for the first couple of years, all I did was right-size the business, get people in the right seats on the bus, develop a new strategy for the company and build the board.

I replaced 10 of the 12 board members in the first 18 months. This board refresh would prove critical for the aggressive M&A strategy to come.

Citizens Communications stockholders approved changing the corporate name to Frontier Communications Corporation at the annual meeting on May 15, 2008. The name change became effective on July 31, 2008, and the company's stock symbol on the New York Stock Exchange changed from "CZN" to "FTR".

During her tenure with Frontier, the company grew from a regional telephone company with customer revenues of less than $1 billion to a national broadband, voice and video provider with operations in 29 states and annualized revenues in excess of $10 billion.

The transformation was real—but it was funded by debt, and the underlying assets remained predominantly copper. The stage was set for Frontier's most ambitious—and ultimately most destructive—chapter.

IV. INFLECTION POINT #1: The First Verizon Deal (2009–2010)

The $8.6 Billion Mega-Deal

In May 2009, Frontier announced what was then the most transformative deal in its history. In May 2009, Frontier announced that it would acquire Verizon Communications' landline assets in Arizona, Idaho, Illinois, Indiana, Michigan, Nevada, North Carolina, Ohio, Oregon, South Carolina, Washington, West Virginia, and Wisconsin for $8.6 billion. Verizon had been in the process of divesting its landlines in an effort to focus more on its broadband and wireless businesses. In all states other than West Virginia, this takeover primarily involved rural exchanges that were formerly a part of the GTE system.

Verizon in 2009 sold about 4.8 million access lines to Frontier for stock valued at $8.6 billion. Frontier said at the time that the transaction made it the largest rural service provider in the U.S. and the fifth largest incumbent local exchange provider (ILEC).

The logic appeared sound on paper. Verizon was pivoting to wireless and FiOS fiber in dense East Coast markets. Rural copper networks were dragging down their growth story and capital efficiency. Frontier, with its rural heritage and operational expertise in smaller markets, seemed like the natural buyer.

The asset transfer included 4.8 million access lines in a deal valued at $8.6 billion. The spin-off established Frontier as the nation's fifth largest local exchange carrier, with 16,000 employees across 27 states.

The Integration Challenge

The transition was finalized on July 1, 2010; in some states, Frontier was required not to raise rates, and in others, broadband access was to be expanded. Ninety-two percent of people in Frontier's existing service area had access to broadband, while just 65 percent did in the newly acquired areas, with a goal to reach 85 percent in three years.

This gap revealed a fundamental challenge: Frontier was acquiring networks that had been starved of investment. The regulatory conditions meant Frontier would need to invest significant capital just to bring these assets up to par—capital that might otherwise go toward paying down acquisition debt.

In West Virginia, the skepticism ran particularly deep. In West Virginia, Frontier acquired Verizon West Virginia, formerly The Chesapeake and Potomac Telephone Company of West Virginia, a former Bell System unit. When combined with its existing subsidiary Citizens Telecommunications Company of West Virginia, Frontier became the incumbent local exchange carrier telephone company for all but five exchanges in the entire state.

The 2010 deal established a pattern that would prove disastrous: Frontier as the buyer of last resort for networks that larger carriers no longer wanted to invest in. Each acquisition added scale, but the underlying technology—aging copper networks in an era of accelerating broadband demand—remained fundamentally challenged.

What looked like growth was actually the accumulation of future liabilities. The copper networks generated cash flow today but required massive investment to remain competitive against cable providers with their superior technology. Frontier was buying problems and calling them assets.

V. The AT&T Connecticut Acquisition (2014)

Between the two Verizon deals, Frontier continued building scale. On October 24, 2014, Frontier closed its acquisition of AT&T's wireline, DSL, U-verse video and satellite television businesses in Connecticut. The deal included the wireline subsidiaries Southern New England Telephone and SNET America and consumer, business and wholesale customer relationships.

The Connecticut acquisition represented a different strategic bet—a relatively dense, affluent market in the Northeast corridor. But it shared the same fundamental challenge: Frontier was acquiring legacy infrastructure in an era when cable competition was intensifying and consumer expectations for bandwidth were skyrocketing.

The pattern was clear by now. Frontier had become the telecom industry's consolidator of "non-core" wireline assets—the buyer that materialized whenever a larger carrier wanted to shed copper networks. Each deal expanded Frontier's footprint and revenue, but each deal also came with integration challenges, regulatory commitments, and the fundamental problem of competing with cable companies over aging infrastructure.

By 2015, Frontier was preparing for its most ambitious acquisition yet—one that would prove to be the deal that broke the company.

VI. INFLECTION POINT #2: The Second Verizon Deal—The $10.5B Overreach (2015–2016)

The Deal That Broke Frontier

In February 2015, Frontier announced what would become its undoing. In February 2015, Frontier Communications announced an agreement to acquire Verizon Communications' wireline operations in California, Florida, and Texas for $10.54 billion in cash, a transaction valued at 3.7 times the projected 2014 pro forma EBITDA of the acquired assets. The deal encompassed approximately 3.7 million access lines, including Verizon's FiOS fiber-to-the-premises networks serving over 2 million broadband customers. Completed on April 1, 2016, following regulatory approvals, the acquisition roughly doubled Frontier's size.

Frontier Communications Corporation today announced completion of its $10.54 billion acquisition of Verizon Communications, Inc. wireline operations providing services to residential, commercial and wholesale customers in California, Texas and Florida. The acquired businesses include approximately 3.3 million voice connections, 2.1 million broadband connections, and 1.2 million FiOS video subscribers.

On the surface, this deal looked more attractive than the 2010 transaction. California, Florida, and Texas were high-growth, high-density states. The properties included Verizon's FiOS fiber networks—modern infrastructure with genuine competitive advantages. Maggie Wilderotter, Frontier's chairman and chief executive officer, said: "These properties align with Frontier's disciplined strategic focus and enhance our footprint with rich fiber-based assets. We look forward to building on the strong results Verizon has delivered in these three states."

But the deal was financed almost entirely with debt, elevating the company's leverage and interest obligations. And the integration challenges would prove overwhelming.

The Integration Disaster

The deal was, as Frontier's CEO stated at the time, a "natural evolution for our company and leverages our proven skills and established track record from previous integrations." As it turns out, that "established track record" didn't mean all that much. Shortly after Frontier began attempting to integrate 3.7 million customers in the three states starting April 1, things began to unravel. Numerous customers complained they couldn't use phone, broadband or cable TV services—at all—for weeks.

Frontier Communications blamed corrupt data for widespread phone, internet and television service outages in California, Florida and Texas. During a legislative hearing in Sacramento, the company said it inherited the problem in its $10.5 billion acquisition of certain Verizon businesses. Frontier West Region President Melinda White told California lawmakers that the data issue caused outages that its technicians were not yet trained to handle.

On February 5, 2015, Frontier announced that it would acquire Verizon's wireline assets in California, Florida and Texas for $10.5 billion. The transition took effect April 1, 2016; technical issues with the integration resulted in a disruption of service for many FiOS users in the markets. In May 2016, California assemblyman Mike Gatto announced a hearing over the matter, stating that "there has been an alarming rate of telephone and Internet outages in Southern California."

Network management practices had diverged enough in ~7 years that the networks acquired in 2016 were markedly different animals than the 2009-2010 networks. Frontier's playbook from earlier integrations simply didn't apply.

A year after buying Verizon's landline business in Texas, California and Florida, Frontier Communications continues to lose customers in video and broadband. In April 2016, Frontier bought those Verizon operations, and the switch-over was a mess. Many people lost service and endured long delays for repairs. Frontier took a public relations beating on social media and in the news. Many customers voted with their feet, too. In the 12 months after taking over the Verizon business, Frontier suffered a net loss of half a million subscribers from the three states.

The Debt Mountain

The integration of these assets intensified financial strain, as Frontier's legacy copper-based networks continued to generate declining revenues from voice services. Frontier Communications accumulated substantial debt through leveraged acquisitions, including the $10.54 billion purchase of Verizon's wireline operations in 2016, which expanded its footprint but strained finances amid declining legacy revenues from voice and video services.

On Monday, it was worth less than $1.4 billion. Last month, Frontier cut its dividend by over 60 percent to free up money to pay down debt. It's now borrowing against other assets to pay down more. That still may not be enough. "Frontier faces a narrow path of recovery that leaves it little room for error, especially given its hefty debt load," Morningstar analyst Alex Zhao wrote. Frontier may have to eliminate the dividend entirely and cut back on capital spending next year.

By 2019, the company's debt exceeded $17 billion. The stock price, which had been around $125 adjusted for splits, plummeted to 37 cents per share. The 2016 acquisition, intended to transform Frontier into a fiber-equipped national competitor, instead became the weight that dragged it underwater.

VII. INFLECTION POINT #3: Bankruptcy & Restructuring (2020–2021)

The Filing

On April 14, 2020, with the COVID-19 pandemic raging, Frontier filed for Chapter 11 bankruptcy. Frontier Communications filed for bankruptcy Tuesday night to kick-start a prearranged $10 billion debt-cutting proposal backed by its bondholders. Frontier announced it has entered into a Restructuring Support Agreement (RSA) with bondholders representing more than 75% of its $11 billion outstanding unsecured bonds.

The company announced that it is filing for Chapter 11 and shared its plan for restructuring its $17.5 billion in debt. The plan for restructuring includes $460 million DIP financing to keep the company running.

The bankruptcy was not a surprise—the company had been in crisis for years. CEO Bernie Han, who replaced longtime CEO Dan McCarthy in December, had been meeting with creditors and advisors since January in order to find a path out of its $17.5 billion debt load.

The Northwest Sale: Ziply Fiber

As part of the restructuring, Frontier divested its Pacific Northwest operations. Frontier said it intends to follow through on its deal last year to sell wireline assets and operations in Washington, Oregon, Idaho and Montana for $1.35 billion. That deal was scheduled to close on or around April 30. WaveDivision Capital, in partnership with Searchlight Capital Partners, bought Frontier's assets in the four states and renamed them Ziply Fiber.

This divestiture made strategic sense—the Northwest assets were geographically disconnected from Frontier's core footprint. The proceeds helped fund the restructuring, and Ziply Fiber has since emerged as an aggressive fiber builder in its own right.

Emergence & New Leadership

On August 27, 2020, the Bankruptcy Court entered an order approving the Joint Plan of Reorganization. On April 30, 2021, the Effective Date of the Plan occurred, and the Plan was consummated.

Upon emergence, the Company reduced its total outstanding indebtedness by more than $10 billion and achieved significant financial flexibility to support continued investment in its long-term growth.

The company stated that it plans to re-enter the Nasdaq on May 4. Frontier has reportedly trimmed some $11 billion in debt and obtained a liquidity of about $1.3 billion.

But the most important element of the restructuring wasn't the balance sheet—it was the leadership. Frontier Communications announced that former Verizon executive John Stratton will be executive chairman of its board once the company emerges from Chapter 11. Frontier said it was targeting early next year for emerging from Chapter 11 bankruptcy.

Mr. Stratton retired from Verizon Communications in 2018. During his 25 years with the company, he held multiple executive and leadership positions and played a pivotal role in positioning Verizon as the leading U.S. wireless carrier. Most recently, he served as Executive Vice President and President of Global Operations, where he had full P&L responsibility for all of Verizon's telecom businesses.

During his stint at Verizon, he led a cost transformation of Verizon's operations, developing and overseeing a restructuring of processes across all business segments that yielded more than $8 billion of annual operating expense savings.

For CEO, the board recruited Nick Jeffery, who would become the architect of Frontier's transformation. Frontier announced that it intends to appoint Nick Jeffery as the Company's next President and Chief Executive Officer, effective March 1, 2021, following the expiration of his notice period with Vodafone UK. Mr. Jeffery will succeed Bernie Han.

Senior Leadership: President and Chief Executive Officer of Frontier Communications since 2021. Prior to this, served as Chief Executive Officer of Vodafone UK, where he led the turnaround of the business, returning it to revenue and market share growth, reducing operating expenses, and increasing customer satisfaction, while delivering double-digit EBITDA growth. During his time at Vodafone the company became Europe's fastest-growing broadband provider.

The combination of Stratton's operational expertise and Jeffery's turnaround experience would prove transformative.

VIII. INFLECTION POINT #4: The Fiber Transformation—"Building Gigabit America" (2021–2024)

The Strategic Pivot

When Nick Jeffery arrived at Frontier in March 2021, he found a company in existential crisis. Frontier was still months away from emerging from bankruptcy. Frontier was burdened with a tarnished brand, a net promoter score (NPS) that was in the dumps, and years of subscriber losses and financial woes. "Frontier was really broken," Jeffery recalls. "The team had lost faith in the company. And it didn't have a strategy."

When I joined Frontier in March 2021, we were a bankrupt company with a broken spirit and a tarnished reputation. At the same time, we knew we had a huge opportunity. We had fiber—the best technology for connecting homes and businesses, capable of transmitting data at the speed of light.

That only started to emerge after Jeffery had an opportunity to analyze and reflect on what Frontier had in terms of talent, assets and potential opportunities. He reckoned that Frontier's turnaround path forward centered on four relatively simple "pillars": building fiber, selling fiber, improving customer care and boosting efficiencies by becoming more automated and more digital.

The strategy crystallized in August 2021 when Frontier announced its "Building Gigabit America" initiative. Nick Jeffery, President and Chief Executive Officer of Frontier, said, "The acceleration of our fiber network expansion is clear evidence that Frontier's transformation is taking hold. Over the past several months, we've made real progress in executing our strategy—by adding world-class leadership, introducing a purpose-driven culture, improving the customer experience. Demand for high-speed broadband is growing rapidly, and fiber is the best product to meet the needs of consumers and businesses."

For 2021, the company increased its expectation for new passings from 495K to >600K, which will complete "wave one" of its fiber upgrade project and leave it with ~4M total FTTH passings. Between 2022 and 2025, the company plans to build to another 6M passings, bringing its total to 10M, or about two thirds of its broadband-enabled locations.

Execution & Results

The execution was remarkable. Frontier ended 2022 with 1.7 million fiber customers, a figure that represents the majority of its total base of 2.8 million broadband subs. Frontier also built out a record 381,000 new fiber locations in Q4, ending 2022 with 5.2 million fiber locations. That gets Frontier past the halfway point toward a goal of building fiber-to-the-premises to 10 million locations by 2025.

"We delivered another strong quarter and reached a critical milestone in our transformation. Thanks to our team's consistent operational performance, we achieved EBITDA growth for the first time in five years," said Nick Jeffery. "We are creating an internet company that people love. Over the last two years, we have rallied around our purpose of Building Gigabit America."

"We delivered another strong quarter of financial and operational results. We said that 2024 is the year that we would return to full year revenue growth," commented Nick Jeffery. "Q2 was our second consecutive quarter of revenue growth, and our fastest quarter of organic growth in more than a decade. This acceleration was driven by record fiber broadband net adds and strong ARPU growth."

Frontier crossed the halfway point of its 10 million goal in late 2022 and, after adding 1.3 million for full-year 2024, ended 2024 with 7.8 million. Frontier's fiber build has also aided other aspects of the business. In 2023, Frontier achieved full-year EBITDA growth for the first time in more than a decade, and in 2024 it achieved full-year revenue growth for the first time in more than 15 years.

In less than four years, we've scaled our fiber footprint and connected millions of homes and businesses to our high-speed fiber internet. We've set a new standard for service, taking our net promoter score from an industry-worst to the best in the business. We've also become a more efficient, digital-first tech company. In 2024, we hit a major milestone—returning our company to full-year organic revenue growth for the first time in 15 years. Many said it couldn't be done. Yet here we are—a great U.S. turnaround story.

Frontier's net promoter score went from -31 to +31 as it has prioritized making thousands of tiny improvements.

Innovative Financing: The Fiber Securitization

To fund the massive fiber buildout, Frontier pioneered a new financing approach. Frontier announced the closing of its previously announced fiber securitization notes offering as part of a $2.1 billion financing. The transaction unlocks access to new capital to fully fund its fiber build. "This landmark deal is a significant milestone in our transformation and confirms the attractiveness of fiber as critical digital infrastructure," said Scott Beasley, CFO of Frontier. Frontier is the largest pure-play fiber provider in the country and the first publicly traded company in the U.S. to secure funds backed by fiber-to-the-home assets.

According to CEO Nick Jeffery, Frontier only securitized "about 11%" of its already-built fiber network to reach $2.1 billion in financing. In August, Frontier closed its fiber securitization notes offering as part of a $2.1 billion financing, a significant jump from its initial goal of raising $1.05 billion. "We're very, very proud to be the first public company to do a fiber securitization," said Jeffery.

This innovative financing approach demonstrated the value inherent in Frontier's transformed asset base and provided a template for future capital raises.

IX. INFLECTION POINT #5: The Verizon Acquisition—Full Circle (2024–2025)

The $20 Billion Deal

Verizon Communications and Frontier Communications today announced they have entered into a definitive agreement for Verizon to acquire Frontier in an all-cash transaction valued at $20 billion. Under the terms of the agreement, Verizon will acquire Frontier for $38.50 per share in cash, representing a premium of 43.7% to Frontier's 90-Day volume-weighted average share price. The transaction is valued at approximately $20 billion of enterprise value.

The irony was not lost on industry observers. It's another chapter in a history of deals between the two. Now Verizon is getting those assets and more back for the price of $20 billion. "The gist of it is that Verizon is buying back networks and operations it sold to Frontier many years ago. Verizon is getting Frontier and all its other acquired properties in the bargain."

The deal would return to Verizon assets it had previously sold to Frontier. In 2016, Verizon completed a $10.5 billion deal to sell TV and internet landline businesses in California, Texas and Florida to Frontier. And in 2009, Verizon sold landline businesses in 14 states in "predominantly rural areas" to Frontier for $8.6 billion.

What changed? The transformation under Jeffery's leadership had converted Frontier from a distressed copper-network operator into a modern fiber-based provider. In acquiring Frontier, Verizon will take control of a fiber network into which much investment has been made. During about the past four years, Frontier invested $4.1 billion into fiber network expansion and now derives more than half of its revenue from fiber related products.

"The U.S. market's become very dynamic. It's always been dynamic, more so perhaps with the advent of convergence and fixed and mobile coming together, so now the wireless players need fiber assets, hence the Verizon acquisition of us," Jeffery says.

The Deal Approval

Frontier Communications today announced that its stockholders approved the acquisition by Verizon Communications at its special meeting held on November 13, 2024. Approximately 63% of stockholders voted "For" the merger agreement proposal, with ten of the company's top 12 stockholders voting to approve the transaction.

The FCC's Wireline Competition Bureau approved Verizon's $20 billion acquisition of Frontier by granting a series of applications that transfer FCC licenses and authorizations.

Today, the Federal Communications Commission (FCC) Wireline Competition Bureau approved the acquisition of Frontier by Verizon for $20 billion. "By approving this deal, the FCC ensures that Americans will benefit from a series of good and common-sense wins. The transaction will unleash billions of dollars in new infrastructure builds in communities across the country—including rural America," said FCC Chairman Brendan Carr.

Verizon and Frontier have said they expect to close the transaction in the first quarter of 2026, pending final approval from DOJ and state regulators.

X. Strategic Analysis: Why This Matters for Investors

The Transformation Mathematics

Consider what happened: Verizon sold approximately $19 billion in wireline assets to Frontier between 2010 and 2016 (the $8.6 billion 2010 deal plus the $10.5 billion 2016 deal). Frontier then went bankrupt, wiping out shareholders. The new Frontier, rebuilt around fiber, is now being acquired by Verizon for $20 billion.

From Verizon's perspective, they effectively outsourced the painful copper-to-fiber transition—and its associated capital requirements and operational risk—to Frontier and its bondholders. When the asset emerged as a fiber-focused provider, Verizon stepped back in.

From the old Frontier shareholders' perspective, they funded $19 billion in acquisition activity that ended in total loss. The equity went to zero.

From the new Frontier shareholders' perspective (the former bondholders who converted their debt to equity in the restructuring), they acquired a company for the value of their debt claims, watched it transform, and are now receiving $38.50 per share in cash—a substantial return.

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW-MEDIUM

Fiber deployment requires massive capital investment. Overall, Frontier expects fiber build costs in 2023 to be in the range of $1,000 to $1,100 per location. This creates genuine barriers to entry. However, government BEAD funding is enabling new entrants in underserved areas, and cable companies are upgrading their networks to compete.

2. Bargaining Power of Buyers: MEDIUM

Consumers have increasing choices—cable, fiber, fixed wireless access, and potentially satellite. However, in many markets, Frontier's fiber represents the only gigabit-capable option. Bundling with wireless (which Verizon will enable) further reduces churn.

3. Bargaining Power of Suppliers: LOW

Fiber equipment and construction services are relatively commoditized. Scale players like Frontier can negotiate favorable terms.

4. Threat of Substitutes: MEDIUM

Fixed wireless access (FWA) and satellite internet (Starlink) represent real alternatives, particularly in less dense areas. However, fiber's superior latency and symmetrical speeds maintain technological advantages.

5. Competitive Rivalry: HIGH

Cable companies (Charter, Comcast) remain formidable competitors with strong existing infrastructure and bundled offerings. The convergence of wireless and wireline is intensifying competition among AT&T, Verizon, and T-Mobile.

Hamilton Helmer's Seven Powers Framework

1. Scale Economies: Frontier benefits from scale in purchasing, network operations, and customer acquisition. However, scale advantages in telecom are moderate—each market still requires dedicated infrastructure.

2. Network Economies: Limited direct network effects, but dense fiber networks create options for commercial services, cell tower backhaul, and wholesale arrangements. This expanded collaboration with Frontier enables AT&T to utilize Frontier's fiber network to help reach enterprise customers and continue to ensure wireless services are powered by fiber optic networks.

3. Counter-Positioning: Frontier's fiber-first strategy represented counter-positioning against cable's DOCSIS technology—but cable is now upgrading, reducing this advantage.

4. Switching Costs: Moderate. Installation requirements and bundled services create some friction, but consumers can switch providers.

5. Branding: The "Building Gigabit America" positioning and NPS turnaround created brand value, but telecom branding is historically weak.

6. Cornered Resource: Incumbent Local Exchange Carrier (ILEC) status provides regulatory advantages and rights-of-way that are difficult to replicate.

7. Process Power: Jeffery's four-pillar approach—building fiber, selling fiber, improving customer care, boosting efficiencies—created operational excellence.

Key Metrics to Track

For investors evaluating telecom transformations like Frontier's, three KPIs matter most:

1. Fiber Subscriber Net Adds: The fundamental measure of whether the fiber investment is translating to market share gains. Frontier's consistent growth here—from 83,000 quarterly adds in Q1 2023 to over 100,000 more recently—demonstrated the strategy's success.

2. Consumer Fiber ARPU Growth: Consumer fiber ARPU increased by 3.5% YoY, in line with the company's long-term target range of 3-4 percent. Sustainable ARPU growth indicates pricing power and product strength.

3. Fiber Penetration Rate: The percentage of fiber passings that convert to subscribers. Higher penetration improves unit economics and cash flow. Frontier expects penetration to be in the mid-teens to 20% at the end of year one, rise to 25% to 30% at the end of year two, and then on up to 45%.

XI. Key Lessons for Investors

Myth vs. Reality

Myth: Debt-fueled M&A creates shareholder value Reality: Frontier's acquisition spree created scale but not sustainable competitive advantage. The debt burden ultimately destroyed equity value.

Myth: Rural telecom is a dying business Reality: The technology was dying (copper), but the market (rural broadband) was growing. The winners are those who invest in modern infrastructure.

Myth: Bankruptcy means failure Reality: Bankruptcy can be a strategic tool for recapitalization. Frontier emerged leaner, with clear strategy and new leadership—and created substantial value for post-emergence shareholders.

Material Risks and Regulatory Considerations

Integration Risk: The Verizon acquisition must still receive final DOJ and state regulatory approvals. At the state level, oversight proceedings are underway. In California, the Public Utilities Commission has scheduled eight public forums through mid-July to evaluate the merger's potential impact.

Labor Relations: With the acquisition of Frontier by Verizon, workers at Frontier have a more stable outlook for their jobs after years of inadequate investment and mismanagement. Verizon has committed to significant investment in fiber upgrades across the Frontier footprint.

Competitive Dynamics: The combined Verizon-Frontier will face intense competition from AT&T's fiber expansion and cable's network upgrades.

The Bottom Line

Frontier's story is ultimately one of redemption through focus. The company's collapse came from unfocused debt-fueled acquisition. Its resurrection came from disciplined execution of a clear strategy: build fiber, sell fiber, delight customers, operate efficiently.

In the years following Jeffery's arrival in 2021, Frontier executed a turnaround that was dramatic by the standards of telecom or any industry. Emerging from bankruptcy with a tainted brand and plummeting customer approval ratings, Frontier reinvented itself with a bold fiber-first vision. Today the company is the largest pure-play fiber internet provider in the country.

The Verizon acquisition represents the final chapter of Frontier's independent story—but it validates the transformation thesis. A company that went bankrupt in 2020 commanded a $20 billion enterprise value by 2024. The lesson: in infrastructure businesses, technology transitions create enormous opportunities for companies willing to make the capital investment and execute the operational transformation.

For investors, Frontier's journey offers several enduring insights:

-

Leverage is destiny: Frontier's collapse was ultimately about debt, not operations. The acquisitions created scale but the leverage created fragility.

-

Technology transitions reward the bold: The companies that emerge strongest from technology transitions are those that invest aggressively in the new technology, not those that squeeze the last cash flows from the old.

-

Turnarounds require fresh leadership: Stratton and Jeffery brought not just different strategies but different cultures and capabilities. The transformation would have been impossible with incumbent leadership.

-

Post-bankruptcy equity can create value: For sophisticated investors, the post-emergence equity represented an opportunity to participate in the transformation with a clean balance sheet.

The Frontier phoenix has risen. Its story offers lessons that extend far beyond telecom—about the dangers of empire building, the discipline required for transformation, and the possibility of corporate resurrection when strategy and execution align.

Now I have the information needed to complete the article. Let me continue from where it left off.

Remaining Regulatory Hurdles

Despite the FCC approval in May 2025 and shareholder approval in November 2024, the acquisition faces a final critical hurdle. Verizon and Frontier are making a final push for California regulators to clear their $20 billion merger by the end of the year. Justice Department approval expires in February, and the companies are eager to close the deal before that happens.

The Department of Justice cleared the deal on February 13, 2025, but that approval only lasts for one year. If the deal were still pending after that, the agency would have to conduct its review again and delay the process further.

The Frontier deal has gained approval from eight states, the Department of Justice, and the Federal Communications Commission, and remains on track for an early 2026 close. However, California's approval remains outstanding, and the California Public Utilities Commission continues its review process.

The CPUC is reviewing the request to determine whether it is in the public interest. This includes assessing the potential impacts on service quality, competition, financial stability, and long-term benefits to customers and communities. The CPUC will also evaluate whether Verizon can maintain or improve upon Frontier's current obligations and services, particularly in rural and underserved areas.

The approval process in California has been complicated by broader political dynamics. After Verizon agreed to demands from the Trump administration to eliminate diversity equity and inclusion programs to get approval for its acquisition of Frontier Communications, the state of California is pushing back. The California Public Utilities Commission held an initial hearing on the $20 billion Verizon-Frontier merger. The FCC approved the deal on May 16 after Verizon agreed to end multiple policies, programs and goals related to DE&I. That being said, Verizon must secure regulatory approval from various states, including California where Frontier is the second largest carrier of last resort.

"As part of the settlement, Verizon has committed to ensuring that income eligible customers, including those of Frontier, have access to essential telephone and internet services," noted Commissioner Kathryn L. Zerfuss at Pennsylvania's PUC public meeting. Pennsylvania approved the merger in September 2025 with extensive consumer protection conditions. Under the settlement terms, Verizon will complete a detailed audit of Frontier's copper and fiber networks within 10 months of closing, identify problem areas, and develop a multi-year plan to rehabilitate and modernize facilities. Verizon will establish a formal maintenance program to track and address infrastructure conditions, with commitments to resolve at least 75% of reported issues within 90 days.

Q3 2025: The Final Quarter as an Independent Company

Even as the acquisition looms, Frontier's operational momentum continued. Frontier Communications added more than 133,000 fiber Internet customers during its most recent financial quarter, a trend that helped boost the company's key revenue points. During the third quarter of the year, Frontier grew its fiber Internet customer base to 2.76 million, a 20 percent increase compared to the same time period last year. Fiber-based average revenue per user grew to $68.59, a 5 percent uptick. Overall revenue attributed to Frontier's operations climbed 4 percent to $1.55 billion.

"The team absolutely crushed it – once again delivering our best quarter ever," said Nick Jeffery. "We achieved outstanding results across our operational and financial metrics, delivered double-digit EBITDA growth, and reached an all-time high in customer growth. Our success is a credit to the relentless execution of our strategy and the belief that we play a critical role in building the digital infrastructure this country needs."

Frontier's Q3 2025 results show Adjusted EBITDA jumped 16% year-over-year to $637 million, significantly outpacing the 4.1% total revenue growth. This operating leverage drove the Adjusted EBITDA margin to expand meaningfully to 41.1% from 36.9% in the year-ago quarter, validating the long-term unit economics and scalability of the fiber model.

The company continued its fiber expansion strategy, adding 326,000 fiber passings during the quarter to reach 8.8 million total locations passed with fiber. Consumer fiber broadband customer churn improved to 1.41% compared to 1.49% in the third quarter of 2024.

These results demonstrate that Frontier's transformation continues to generate momentum even as the company prepares to become part of Verizon. The fiber strategy that emerged from bankruptcy has proven its viability.

X. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW-MEDIUM

Fiber deployment requires substantial capital investment and operational expertise. Permitting, rights-of-way, and construction timelines create genuine barriers to entry. Over the past decade, broadband carriers of all sizes have deployed fiber broadband to both rural and suburban areas. But as coverage becomes ubiquitous, the market will reward companies that find efficiencies of scale. The industry is likely to see an uptick in mergers and acquisitions as private equity players look for an exit. One survey from AlixPartners found that 93% of network provider executives expect increased consolidation to happen soon.

However, government funding programs are enabling new entrants. 2024 was about preparing for BEAD funding allocations and readying to make the best use of the funds. In 2025, BEAD funding started to be allocated, and states began implementing their program plans. The peak project work is expected around 2027-28. Just over half of U.S. households currently have access to fiber broadband, and approximately 90 percent of homes that receive network availability through BEAD funding will be passed by fiber.

2. Bargaining Power of Buyers: MEDIUM

Consumer choice continues to expand across technology platforms. Technological convergence has increased broadband competition. Fiber, fixed wireless access, cable, and low-earth-orbit satellites now offer substitutable performance for consumer applications.

Market data demonstrates robust competition. Consumers are switching services, industry profit margins indicate competitive rather than monopoly profits, and providers are offering extensive promotions.

However, fiber's superior latency and symmetrical speeds maintain technological advantages for demanding applications. The combined Verizon-Frontier entity will also be able to offer wireless-wireline bundles that increase switching costs.

3. Bargaining Power of Suppliers: LOW

Fiber equipment and construction services are relatively commoditized, with multiple global suppliers. Scale players can negotiate favorable terms, and the consolidation trend further strengthens buyer power.

4. Threat of Substitutes: MEDIUM-HIGH

The competitive landscape has fundamentally changed. Today, there are four broad categories of home broadband technology that deliver substitutable performance for most consumer applications: fiber optic networks, coaxial cable, fixed wireless access, and low-earth-orbit satellite constellations. This convergence increases the competitive dynamics that were already present but limited by the footprint of incumbent telephone and cable companies. These new avenues of competition benefit consumers.

Market competition is intensifying, driven by new entrants leveraging alternative delivery models such as wireless backhaul and satellite-assisted fixed wireless access. Collaborative public-private initiatives are streamlining infrastructure rollouts, particularly in underserved regions.

5. Competitive Rivalry: HIGH

The telecom industry remains intensely competitive. The telecommunications industry is experiencing a dynamic transformation, propelled by sweeping technological innovations, fierce competition, and changing consumer behavior. As one of the most integral components of the global economy, telecom connects nearly every aspect of modern life.

Telecom giants like Verizon and AT&T are responding with aggressive investments in fiber-to-the-home infrastructure, offering ultra-high-speed internet, TV, and phone services in bundled packages. These strategies aim to retain customers and tap into the growing demand for faster connectivity and streaming capabilities.

XI. Industry Context and Competitive Dynamics

The Fiber Imperative

The broader industry context validates Frontier's strategic pivot—and Verizon's decision to reacquire these assets. The Fiber-to-the-Home market is valued at USD 65.49 billion in 2025 and is forecast to touch USD 120 billion by 2030, advancing at a 19.24% CAGR. Growth rests on three pillars: accelerating data traffic, policy targets that define gigabit service as a basic right, and optical-access innovation that lifts network capacity while containing cost. Operators worldwide upgrade from GPON to XGS-PON and prepare for 50G PON to secure symmetrical multi-gigabit speeds that copper or hybrid coax cannot deliver.

The broadband industry is at a critical point, as federal funding drives rural buildouts and network upgrades, and rapid technological advancements like AI and automation drive the need for powerful, future-proofed networks. Carriers need to evolve and continue to focus on expanding access to all, as well as preparing for the demands of the future—and fiber will play a major role.

M&A Wave in Fiber

The fiber broadband market is poised for further consolidation in 2025, as providers pursue mergers and acquisitions to expand their networks and customer bases. This strategic shift is driven by increasing competition and the growing need for efficient infrastructure deployment.

Recent activity from Verizon-Frontier, Bell Canada-Ziply, and several T-Mobile announcements support this concept. The Verizon-Frontier deal represents the largest example of this consolidation wave, creating a fiber footprint that spans 31 states.

The Combined Entity

In its 20-page approval order, the FCC concluded the merger was "unlikely to result in competitive harms" and found it "likely to generate public interest benefits," particularly in expanding high-speed broadband access and completing Frontier's unfinished fiber buildouts. The merger will fold Frontier's 8 million fiber passings and 2.5 million fiber subscribers into Verizon's national footprint, which already includes 18 million fiber passings and 7.5 million FiOS customers.

If the deal closes, the new entity will have 25 million fiber passings in 31 states and the District of Columbia.

In a webcast announcing the deal, Verizon Chairman and CEO Hans Vestberg focused on the synergies of Verizon's mobile and Frontier's fiber assets. The goal is to incorporate various elements—wireless, fixed wireless access, fiber, and Verizon's edge network—into a highly integrated network serving residential and small businesses with service and delivery options. "Fiber and fixed wireless access are winning in the market," Vestberg said.

XII. Key Lessons for Business Leaders

The Perils of Debt-Fueled M&A

Frontier's journey offers a masterclass in the dangers of acquisition-driven growth. The company's collapse was not caused by operational incompetence or market decline—it was caused by leverage. Each acquisition expanded scale but added debt, creating a balance sheet that could not withstand integration challenges or competitive pressures.

The mathematics were unforgiving: Frontier acquired approximately $19 billion in assets from Verizon between 2010 and 2016, funded largely with debt. When integration problems emerged and legacy revenues declined faster than fiber revenues could grow, the debt became unsupportable. The lesson is clear: scale without sustainable capital structure is fragile empire-building.

Technology Transitions Reward the Bold

The most valuable insight from Frontier's transformation is the importance of embracing technology transitions rather than milking legacy assets. Under the pre-bankruptcy regime, Frontier's strategy amounted to extracting cash from copper networks while underinvesting in fiber. This approach accelerated decline.

Under Jeffery's leadership, the strategy reversed: invest aggressively in fiber, accept near-term cash consumption, and build toward long-term value creation. The results vindicated this approach—fiber subscriber growth, ARPU expansion, and improving churn metrics all demonstrated the viability of the fiber-first strategy.

Fresh Leadership Enables Transformation

Frontier's turnaround would have been impossible without the leadership change that accompanied bankruptcy. Stratton brought operational expertise from Verizon's transformation; Jeffery brought turnaround experience from Vodafone UK. Together, they implemented a clear four-pillar strategy—building fiber, selling fiber, improving customer care, and boosting efficiencies—that produced measurable results.

The cultural transformation was equally important. When Jeffery arrived, he found a company with "broken spirit and tarnished reputation." The NPS transformation from -31 to +31 reflects not just operational improvements but a fundamental shift in organizational culture.

Post-Bankruptcy Equity Can Create Value

For sophisticated investors, Frontier's emergence from bankruptcy represented an opportunity. The bondholders who converted their debt to equity acquired ownership of a company with a clean balance sheet and clear strategic direction. Their investment has now generated substantial returns through the Verizon acquisition.

This pattern—distressed debt conversion creating value through operational transformation—offers a template for infrastructure investments where underlying assets have value obscured by capital structure problems.

XIII. Conclusion: The Fiber Phoenix Completes Its Journey

Frontier Communications' ninety-year history encapsulates nearly every major theme in American telecommunications: the extension of connectivity to rural America, the consolidation of fragmented utility assets, the transition from regulated monopoly to competitive markets, the perils of debt-fueled empire building, and the redemptive power of focused operational execution.

The company's arc—from Depression-era utility conglomerate to telecom consolidator to bankruptcy casualty to fiber-first phoenix—offers lessons that extend far beyond the telecom sector. At its core, this is a story about the relationship between capital structure and strategy, about the importance of technology transitions, and about what becomes possible when fresh leadership aligns resources with market opportunity.

The irony of Verizon's acquisition cannot be overstated. The same company that sold these assets to Frontier—implicitly declaring them non-core and value-destructive—is now paying a premium to reacquire them. What changed was not the geography or the customer base but the technology: copper networks that were liabilities have been transformed into fiber networks that are strategic assets.

For investors, the Frontier story validates several enduring principles. First, balance sheet strength matters enormously in capital-intensive industries—Frontier's collapse was a leverage event, not an operational failure. Second, technology transitions create windows of opportunity for companies willing to invest when others retreat. Third, bankruptcy can be a strategic reset that enables value creation rather than simply destruction.

Verizon committed to completing Frontier's planned expansion to 10 million homes by 2026, a goal that Frontier had acknowledged it lacked the resources to fund independently. This commitment ensures that the fiber transformation will continue under Verizon's ownership.

As the combined entity prepares to operate across 31 states with 25 million fiber passings, it will face intensifying competition from cable operators, fixed wireless providers, and satellite entrants. The industry consolidation wave that Frontier's acquisition represents reflects the capital requirements of next-generation network deployment—requirements that favor scale and financial strength.

The Frontier phoenix has risen from bankruptcy, executed a remarkable transformation, and found its final home. Its story will be studied by business strategists, telecom executives, and investors for years to come—a cautionary tale about the limits of debt-fueled growth, and an inspiring example of what focused execution can achieve when strategy and capital structure align.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube