Acuity Brands: From Linen Supply to Lighting Giant — The Story of North America's Dominant Light

I. Introduction & Episode Roadmap

Picture this: a sprawling commercial office building in downtown Atlanta. The lights flicker on automatically as employees stream through the doors. The HVAC system anticipates occupancy patterns, the conference room AV equipment springs to life for a scheduled meeting, and sensors track foot traffic to optimize space utilization. Behind these seamlessly orchestrated systems sits a single company most people have never heard of—one with roots stretching back not to Silicon Valley garages or engineering labs, but to a linen supply business founded in 1919 by a towel salesman returning from World War I.

As of 2024, Acuity Inc. has approximately 12,000 employees and recorded net sales of $3.84 billion for the fiscal year. In terms of market share, Acuity Brands is the largest lighting manufacturer in North America.

The central question that animates this story is almost absurd in its improbability: How did a company that started by renting towels and linens to Atlanta restaurants transform itself into the dominant force in commercial lighting and an emerging leader in intelligent building technology?

The answer lies in three distinct transformations spanning over a century: from linens to conglomerate, from conglomerate spinoff to LED pioneer, and from LED lighting manufacturer to intelligent spaces orchestrator. Each transition required prescient leadership, disciplined capital allocation, and the courage to ride—rather than fight—industry disruption.

The company-wide commitment to shifting from traditional lighting to solid-state lighting (LED) was a massive undertaking. Yet this transformation, under CEO Vernon Nagel's 16-year tenure, was merely the second act. Today, under Neil Ashe's leadership, Acuity is attempting something equally ambitious: transforming itself from a hardware manufacturer into a technology company that controls not just the lights in a building, but how that entire space functions, feels, and performs.

Acuity revenue for the quarter ending August 31, 2025 was $1.209B, a 17.13% increase year-over-year. Acuity revenue for the twelve months ending August 31, 2025 was $4.346B, a 13.14% increase year-over-year.

The threads we'll trace include technology transitions that destroyed competitors but enriched Acuity, a remarkably consistent approach to acquisitions that builds platforms rather than just revenue, and the art of navigating from commodity manufacturing toward high-margin, software-enabled solutions. For investors watching the industrial technology space, Acuity offers a case study in how legacy companies can reinvent themselves—not once, but repeatedly.

II. Origins: The Unlikely Genesis (1919–1969)

The Linen Supply Roots

In 1919, Atlanta was a bustling Southern city emerging from the shadow of Reconstruction, its economy diversifying beyond cotton into railroads, manufacturing, and a growing service sector. It was here that Isadore M. Weinstein spotted an opportunity that would plant the seeds of a future lighting empire.

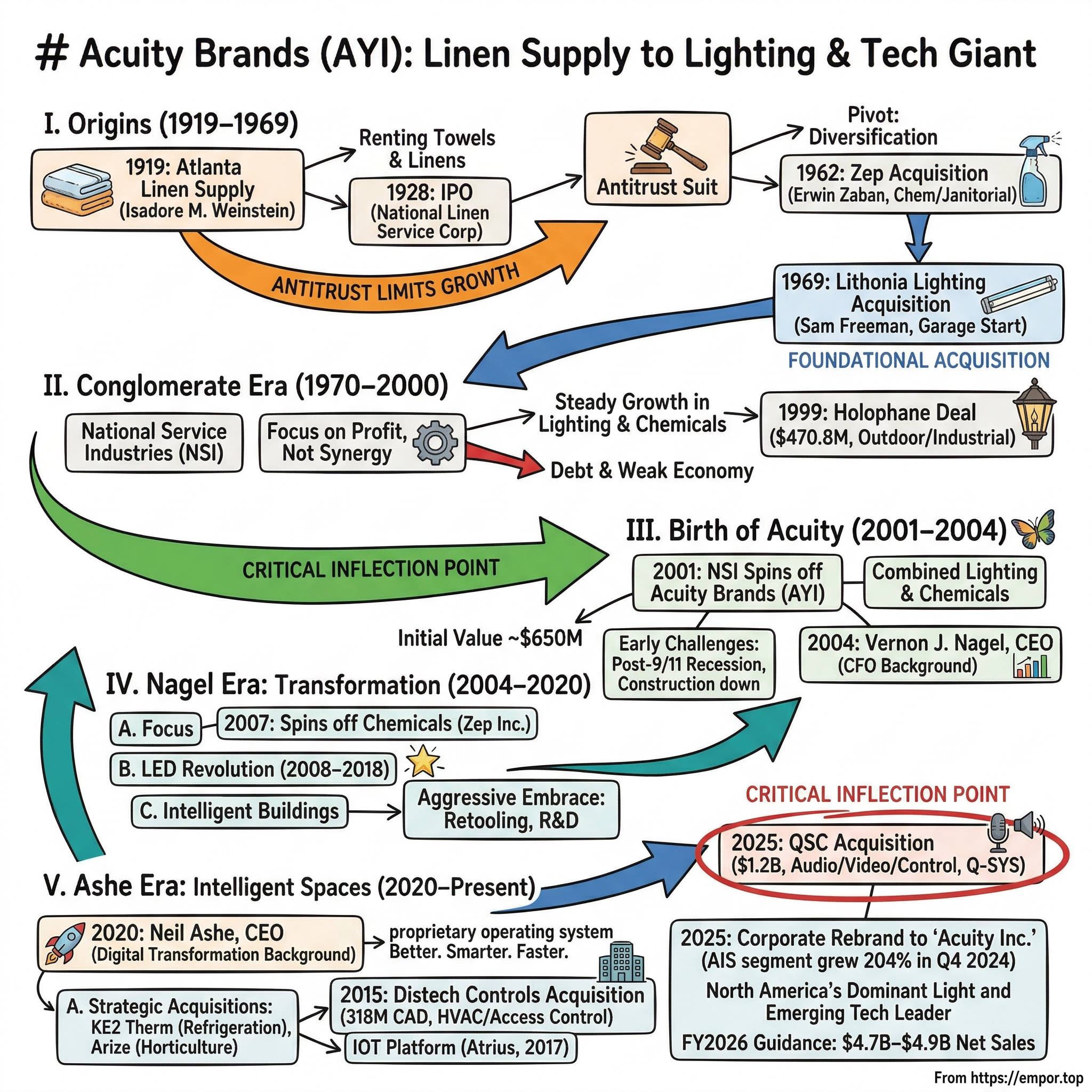

The roots of Acuity Brands date back to 1919 when Isadore M. Weinstein founded the Atlanta Linen Supply company. Weinstein had previously been employed in the towel supply business in Cleveland, and after serving in World War I, he started his own business renting towels, uniforms, and linens.

The business model was elegantly simple: rather than force restaurants, hotels, and businesses to purchase, launder, and maintain their own linens, Weinstein would rent them clean inventory on a weekly basis. It was a recurring revenue business model a century before software-as-a-service made that concept fashionable.

He opened several locations throughout the south, changing the name to the Southern Linen Service Corporation in 1920. The company went public in 1928 as National Linen Service Corporation and continued to grow, eventually expanding to markets in the southwest and west coast.

The 1928 IPO—just a year before the Great Crash—demonstrated both ambition and opportunistic timing. National Linen Service Corporation survived the Depression years and emerged stronger, expanding its geographic footprint across the rapidly industrializing Sun Belt.

The Antitrust Pivot

Following World War II, the idea of renting rather than buying durable goods exploded in popularity. Businesses wanted to focus on their core competencies, not manage ancillary functions like laundry. National Linen rode this wave to become dominant in its highly fragmented industry.

Under the leadership of Isadore's son, Milton N. Weinstein, National Linen became so dominant that regulators took notice. In the 1950s, the company faced an antitrust suit—a settlement with the U.S. Department of Justice in 1956 effectively capped its ability to grow through linen service acquisitions.

This legal constraint would prove to be the most consequential forcing function in the company's history. Unable to expand horizontally, National Linen's management began looking for profitable companies in entirely unrelated industries. The conglomerate era of American business was dawning, and National Linen would ride that wave too.

The Zep Acquisition and Erwin Zaban

National Linen's first acquisition outside of linens and uniforms was Zep Manufacturing Company, an Atlanta-based chemical and janitorial supply manufacturer, in 1962. Zep became synonymous with NSI's chemical division, acquiring Selig Chemical Industries in 1968 and several smaller acquisitions throughout the 1970s and 1980s.

The Zep deal was transformative not just for what it added to the portfolio, but for who it brought through the door. To better reflect its new variety of business units, National Linen became National Service Industries (NSI) in 1964. Zep co-founder Erwin Zaban, who had stayed on following the company's acquisition and was also Weinstein's neighbor, took over NSI's operation in 1966.

Zaban would prove to be a pivotal figure—a disciplined operator who understood that in the conglomerate model, the key wasn't operational synergy between divisions but rather excellent management and consistent cash generation in each unit. This philosophy would guide NSI's acquisition strategy for the next three decades.

Lithonia Lighting: The Foundational Acquisition

The acquisition that would ultimately define Acuity came in 1969, when NSI purchased a Georgia-based light fixture manufacturer with an unusual founding story of its own.

The Lithonia Lighting story began in 1946 when Sam Freeman founded the Lithonia Lighting Products Company. Operations began with just two employees working out of a 2,000-sq.-ft. garage in Lithonia, Georgia, which at the time was a small town east of Atlanta.

Another piece of what would become Acuity Brands was added in 1969 with the acquisition of Georgia lighting fixture manufacturer Lithonia Lighting, Inc., laying the foundation for a fifth division at National Service. Originally begun in 1946 Lithonia had been involved in both incandescent and fluorescent lighting fixtures, selling to residential, commercial, and industrial customers. It had since narrowed its focus to the commercial and industrial fluorescent market.

This focus on commercial and industrial fluorescent lighting—rather than the glamorous residential decorative market—would prove prescient. The commercial market offered steady demand tied to office and industrial construction, long replacement cycles, and relationships with electrical contractors and distributors that created barriers to entry.

In 1969, NSI acquired Lithonia Lighting Inc., a light fixture manufacturer founded in Georgia in 1946, and established a lighting division. Along with the chemical division that grew out of the Zep acquisition, the lighting division that grew out of the Lithonia Lighting acquisition formed the foundation for what would eventually become Acuity Brands.

Neither Milton Weinstein nor Erwin Zaban could have known that this lighting company, purchased as part of a diversification strategy forced by antitrust concerns, would eventually outgrow everything else and become the core of a $4+ billion industrial technology company. But that's exactly what happened.

III. The NSI Conglomerate Era (1970–2000)

The Conglomerate Model

The 1970s and 1980s represented the heyday of American conglomerates—sprawling corporate empires that owned everything from insurance companies to aerospace divisions to restaurant chains. NSI embraced this model wholeheartedly, though with a distinctive regional flavor rooted in Atlanta's business culture.

National Service continued to grow externally, unconcerned with achieving synergy between units, instead looking for profitable companies with strong management teams in place.

Zaban continued NSI's new expansion strategy of acquiring profitable companies without much consideration for synergy among the company's increasing number of business units throughout the 1970s and 1980s. Six business units remained at the core of NSI's operations: linens, chemicals, lighting, insulation, envelopes, and printing.

This might seem like a chaotic collection of businesses, but there was method to the apparent madness. Each unit served business-to-business customers, generated consistent cash flows, and required strong distribution relationships. The management philosophy was simple: buy good companies, keep good management, let them operate independently, and harvest the cash.

Building the Lighting Portfolio

Through the 1970s and 1980s, Lithonia Lighting grew steadily within the NSI portfolio. The fluorescent lighting market was expanding alongside the American office building boom, and Lithonia's focus on commercial applications positioned it well.

By the 1990s, NSI's lighting and chemical divisions made up more than half of the company's revenues and operating incomes combined, and both divisions were still rapidly growing. In 1992, NSI added Graham Group, Europe's second-largest specialty chemical manufacturer at the time, and Kleen Canada to its chemical division. NSI added outdoor lighting company Infranor Canada in 1995 and invested in a fluorescent lighting manufacturing facility in Monterrey, Mexico that would serve the entire North American market.

The lighting division's growth was propelled by a series of smaller acquisitions that expanded both product lines and geographic reach. But the biggest deal of the era would come at the decade's end.

The Holophane Deal

NSI acquired several other lighting manufacturers over the next 30 years, the largest of which occurred in 1999, when Ohio-based Holophane Corporation, a large outdoor and industrial lighting manufacturer, was purchased.

The largest acquisition for the group came in July 1999 when National Service paid $470.8 million for Columbus, Ohio-based Holophane Corporation, a leading outdoor and industrial lighting equipment manufacturer that brought with it a direct lighting fixture sales force. In addition, four small lighting companies were acquired in the late 1990s. Although National Service was able to grow revenues to a record $2.22 billion in fiscal 1999, the debt taken on for the acquisition of Holophane, as well as major investments in the envelope line, suppressed earnings.

Holophane was a storied name in the lighting industry, founded in 1898 and known for prismatic glass technology that directed light more efficiently than competitors. The acquisition gave NSI's lighting division a strong presence in outdoor and industrial applications—exactly the kind of portfolio expansion that would prove valuable in the LED transition that lay ahead.

As a result investors bid down the price of National Service stock. A weakening economy in 2001 only worsened the situation.

The debt burden and soft economy would force NSI's hand, leading to the most significant corporate restructuring in the company's history—and the birth of Acuity Brands as an independent company.

IV. The Spinoff: Birth of Acuity Brands (2001–2004)

Creating a Focused Entity

By 2001, NSI was a sprawling conglomerate struggling under the weight of its diverse operations and the debt accumulated from the Holophane acquisition. Management concluded that the whole was worth less than the sum of its parts—a classic setup for a spinoff.

In 2001, National Service Industries announced it would combine the lighting and chemical divisions and spin off that combined entity as a separate, publicly traded company. Initially incorporated as L&C Spinco in June 2001, it was renamed Acuity Brands in November of the same year.

The company officially began operations as an independent entity on November 30, 2001, following its spin-off from National Service Industries (NSI).

The name "Acuity"—derived from the Latin for sharpness of vision—was meant to signal clarity of purpose and focus. The irony, of course, was that the new company still housed two unrelated businesses: lighting and specialty chemicals. That lack of focus would eventually be addressed, but first came the challenge of survival.

Its initial public market valuation was approximately $650 million.

Early Challenges

The timing could hardly have been worse. The spinoff became effective on November 30, 2001—just weeks after the September 11 attacks had plunged the U.S. economy into recession.

James S. Balloun, who had taken over as CEO of NSI in the mid-1990s, moved with the spinoff to serve as the president, CEO, and chairman of the board.

The nonresidential construction market was hit especially hard, a situation that adversely impacted the lighting group, which experienced flat sales in 2002 and a drop in operating profit.

The post-9/11 economic malaise was particularly brutal for a company dependent on commercial construction. New office buildings and industrial facilities weren't being built, which meant minimal demand for new lighting installations. The young company posted revenues of $1.98 billion and net income of $40.5 million in 2002—respectable numbers, but hardly the growth story investors craved.

Leadership Transition

Balloun retired in September 2004 and was replaced by Vernon J. Nagel, who had joined the firm as executive vice president and chief financial officer in December 2001.

The appointment of Vernon Nagel would prove to be one of the most consequential leadership decisions in the company's history. Nagel wasn't a lighting industry veteran—He was formerly a principal with Jepson Associates, Inc.; Executive Vice President, Chief Financial Officer, and Treasurer of Kuhlman Corporation; and Vice President of Finance, Chief Financial Officer, Treasurer, and Secretary of Stericycle, Inc. He received a B.B.A. degree from the University of Michigan and is a Certified Public Accountant (inactive).

Nagel's background as a CFO and financial operator, rather than a product or sales executive, would shape his approach to leading Acuity through the massive technological transition ahead. He understood capital allocation, margin expansion, and the discipline required to invest through uncertainty.

V. The Nagel Era: Transformation & The LED Revolution (2004–2020)

A. The First Strategic Move: Spinning Off Chemicals

Nagel's first major strategic decision signaled his commitment to focus. The chemical division, while profitable, had no operational synergy with lighting. It consumed management attention and capital that could be deployed elsewhere.

Effective July 2007, the company's chemical division, Acuity Specialty Products, spun off as Zep, Inc. and included the Zep, Enforcer, and Selig brands. The remaining Acuity Brands, Inc. became the holding company for Acuity Brands Lighting, which included the Lithonia Lighting, Holophane, Peerless, and Mark Architectural brands, among others.

This spinoff was more than just a financial transaction—it was a statement of intent. Acuity Brands would be a pure-play lighting and controls company, able to invest fully in the technological transformation that Nagel saw coming.

Separating from the diversified NSI allowed Acuity to concentrate resources and strategic direction purely on the lighting and building technology markets. This focus was crucial for navigating subsequent industry disruptions.

B. The LED Transition (2008–2018) — CRITICAL INFLECTION POINT

The shift from incandescent to fluorescent to LED lighting represented one of the most complete technological transformations in industrial history. For legacy lighting manufacturers, it was an existential threat—the equivalent of film photography companies facing digital cameras, or typewriter makers confronting personal computers.

Most incumbents were destroyed or dramatically diminished. General Electric, once the dominant name in American lighting, essentially exited the business. Philips spun off its lighting division. Osram was acquired. The graveyard of lighting companies that failed to navigate the LED transition is extensive.

Nagel's tenure as CEO saw the transition of the lighting industry to LED lighting as well as the rise of smart lighting and the internet of things.

What made Acuity's navigation of this transition remarkable was its aggressive embrace of the new technology rather than defensive protection of legacy products. Under Nagel's leadership, Acuity invested heavily in LED R&D, supply chain transformation, and product development.

In 2010, Acuity made a strategic acquisition to accelerate its LED capabilities: Acuity Brands today announced that it has acquired for an undisclosed amount of cash the remaining outstanding capital stock of Renaissance Lighting, Inc., a privately-held, pioneering innovator of solid-state light-emitting diode ("LED") architectural lighting. Renaissance, based in Herndon, Virginia, offers a full range of LED-based specification-grade downlighting luminaires and has developed an extensive intellectual property portfolio related to advanced LED optical solutions and technologies.

"This acquisition will extend our innovation capabilities in solid-state lighting and controls, enabling Acuity Brands to continue to deliver leading-edge lighting solutions to the market."

The transformation required more than R&D investment—it demanded complete retooling of manufacturing processes, retraining of sales forces, and reconditioning of customer expectations. Legacy lighting fixtures were relatively simple electromechanical devices; LED luminaires incorporated sophisticated electronics, thermal management systems, and increasingly, embedded controls and sensors.

C. The Intelligent Buildings Strategy: Distech Controls Acquisition (2015) — CRITICAL INFLECTION POINT

While competitors focused exclusively on the lighting hardware transition, Nagel saw further ahead. If LED fixtures were going to incorporate electronics and connectivity, why stop at lighting? Why not control the entire building?

On September 1, 2015, Acuity Brands announced that its wholly-owned subsidiary, Acuity Brands Lighting, Inc., completed the previously announced acquisition of Distech Controls Inc., a leading provider of building automation and energy management solutions that allow for the seamless integration of lighting, HVAC, access control, closed circuit television, and related systems. Acuity Brands Lighting acquired all of the outstanding capital stock of Distech Controls for approximately 318 million Canadian dollars.

Distech Controls' building automation and energy management solutions combined with Acuity Brands' solid-state lighting portfolio, will offer solutions that can provide true end-to-end optimization of all aspects of the building for enhanced occupant experience, quality visual environment, seamless operation, energy efficiency, operational cost reductions, and increased digital functionality. Distech Controls will continue to employ its 190 team members worldwide, led by current executives, including Founder, President and CEO Etienne Veilleux.

This acquisition represented a fundamental strategic pivot. Acuity was no longer just a lighting company—it was becoming a building technology company. Nagel articulated this vision clearly: "The combination of Acuity Brands' broad-based industry-leading lighting portfolio, control technologies, and integrated digital solutions along with Distech Controls' wide-breadth of innovative products, services, and solutions that optimize comfort and energy efficiency in buildings will contribute to our tiered solutions strategy for making buildings smarter and more simple to operate. Distech Controls will enhance our ability to offer true end-to-end optimization of all aspects of the building, including improved occupant experience, quality visual environment, energy efficiency, operational cost reductions, and increased digital functionality, by leveraging the capability to collect vast amounts of data to better enable the Internet of Things for building owners."

D. Building the IoT Platform

Acuity grew with these changes in technology, launching the Atrius IoT brand in 2017 after the acquisitions of Sensor Switch and organic creation of brands such as nLight and ROAM.

The Atrius platform represented Acuity's attempt to create a software layer on top of its hardware products—enabling location services, asset tracking, space utilization analytics, and energy optimization. For a traditional manufacturing company, this was unfamiliar territory, but it reflected Nagel's recognition that hardware margins would compress while software and services could generate recurring revenue.

E. Revenue Growth Under Nagel

The financial results under Nagel's leadership were remarkable. When the Zep spinoff was completed in 2007, Acuity Brands had net sales of approximately $2.4 billion. By fiscal 2018, that figure had grown to over $3.7 billion.

CEO Vernon J. Nagel of Acuity Brands, Inc. received the EY Entrepreneur Of The Year® 2016 National Award in the distribution and manufacturing category. Now in its 30th year, the award recognizes outstanding entrepreneurs who demonstrate excellence and extraordinary success in such areas as innovation, financial performance, and personal commitment to their businesses and communities.

We successfully navigated one of the greatest technology transformations faced by any industry with the advent of digital lighting, and over that time period more than doubled our sales, tripled our operating margins, became the clear industry leader, and saw an eight-fold increase in shareholder value.

When Nagel announced his transition to Executive Chairman in January 2020, he could claim one of the most successful CEO tenures in industrial company history: guiding a traditional manufacturer through an existential technological disruption and emerging not just intact, but stronger.

VI. The Neil Ashe Era: Intelligent Spaces & QSC (2020–Present)

Leadership Transition

In January 2020, Acuity announced a leadership change that signaled the company's technological ambitions were accelerating rather than plateauing.

Acuity Brands, Inc. announced today that Neil M. Ashe will become its next President and Chief Executive Officer ("CEO") effective January 31, 2020.

Neil M. Ashe has served as President and CEO of Acuity since 2020 and as Chairman of Acuity since 2021. Neil has transformed Acuity from a traditional luminaires business into a leading industrial technology company comprised of electronics, data and controls. Under his leadership, Acuity's market capitalization has tripled, driven by strategic focus and improved financial performance.

Ashe's background was strikingly different from typical industrial company CEOs: He was CEO of the investment firm, Faster Horses LLC (2017-2019), advising companies on digital transformation and growth strategies. He served as President and CEO of Global eCommerce & Technology at Walmart, Inc (2012 to 2017), where he reimagined and rebuilt the eCommerce business including the technology and fulfillment operations. He also served as President of CBS Interactive (2008-2011) and CEO of CNET Networks, Inc. (2006-2008).

This was a leader who had spent his career in digital transformation—not lighting fixtures. His appointment signaled that Acuity's board saw the company's future as fundamentally technology-driven.

He established a values-driven culture and introduced the proprietary Better. Smarter. Faster. operating system that empowers associates to operate more productively with greater distribution of responsibility.

Neil reorganized the business into two segments—Acuity Brands Lighting and Acuity Intelligent Spaces—and oversaw strategic acquisitions that expanded capabilities and reach, including OSRAM's North American Digital Systems business in 2021 and the $1.2 billion acquisition of QSC, LLC in 2025.

Strategic Acquisitions: KE2 Therm and Arize

Ashe continued the disciplined acquisition strategy, adding capabilities that extended the intelligent buildings platform:

In May 2023, Acuity acquired KE2 Therm Inc., a U.S.-based provider of advanced refrigeration controls and solutions. This acquisition extended Distech Controls' building management capabilities into commercial refrigeration—think grocery stores, restaurants, and cold storage facilities where energy consumption is substantial.

Later that year, in November 2023, Acuity acquired the Arize family of horticulture lighting products from Current Lighting Solutions, LLC. This moved Acuity into the rapidly growing vertical farming and controlled environment agriculture market, where sophisticated LED lighting is essential for indoor crop production.

The QSC Acquisition (2025) — CRITICAL INFLECTION POINT

The most significant transaction of the Ashe era—and arguably in Acuity's history—was announced in October 2024 and closed January 1, 2025.

Acuity, a market-leading industrial technology company, has reached a definitive agreement to acquire QSC, LLC ("QSC") for a purchase price of $1.215 billion, or $1.1 billion net of approximately $100 million in present value of expected tax benefits. The net purchase price represents approximately 14 times QSC's estimated EBITDA for the last twelve months ending August 31, 2024.

Founded over five decades ago, QSC, LLC is a globally recognized leader in the design, engineering, and manufacturing of award-winning solutions and services. Leading the company's success is Q-SYS, a cloud-first platform for audio, video, and control, built on a modern, standards-based IT architecture. With established solutions across Corporate, Education, Hospitality, Venues, Events, Cinema, Government, Healthcare, and Transportation, Q-SYS is redefining possibilities for live, hybrid, and virtual experiences. QSC Audio complements these offerings with high-performance loudspeakers, digital mixers, power amplifiers, software, and accessories.

QSC, headquartered in Costa Mesa, California, is a well-established player in the AVC market, with annual sales of $535 million for the twelve months ending August 31, 2024.

"In our Intelligent Spaces business we are delivering meaningful outcomes for end users that are powered by disruptive technologies and that generate strong financial results," said Neil Ashe, Chairman, President and Chief Executive Officer of Acuity Brands, Inc. "QSC has built a differentiated cloud-manageable audio, video and control platform that controls what happens in a built space."

QSC's $535M now makes up two-thirds of Acuity's Intelligent Spaces Group revenues.

The strategic logic is compelling: through Distech, Acuity can manage the building's systems (HVAC, lighting, access). Through QSC, Acuity can now control what happens inside those spaces—the audio-visual experience in conference rooms, classrooms, and entertainment venues. This integration enables scenarios where a conference room booking automatically triggers climate adjustment, lighting configuration, and AV system preparation.

Corporate Rebrand

The transformation culminated in a symbolic change: Acuity Brands, Inc.'s corporate name is changing from Acuity Brands, Inc. to Acuity Inc. effective March 26, 2025. Acuity will continue to operate through two business segments, Acuity Brands Lighting (ABL) and Acuity Intelligent Spaces (AIS), formerly Intelligent Spaces Group (ISG).

For Acuity, this is about more than just branding—it's a statement of where the company is heading. The lighting giant is increasingly positioning itself as an industrial technology company, where lighting is just one part of the equation.

"For over 50 years we've been known for our innovative solutions and for transforming the status quo. We led the LED digital evolution to change how people experience light."

VII. Business Model Deep Dive

Two-Segment Structure

Acuity Inc. provides lighting, lighting controls, building management system, and an audio, video, and control platform in the United States and internationally. It operates in two segments, Acuity Brands Lighting (ABL); and the Acuity Intelligent Spaces (AIS).

In fiscal 2024, Acuity Brands Lighting and Lighting Controls (ABL) remained the company's largest segment, generating $3.6 billion in net sales, which accounted for approximately 93% of the company's total sales.

The Intelligent Spaces Group (ISG) contributed $291.9 million in net sales, representing about 7% of the company's overall revenue, and showed strong growth with a 15.5% increase in sales compared to the previous year.

The AIS segment is growing much faster and carries higher margins, but ABL remains the foundation—generating the cash that funds strategic investments and acquisitions.

Product Portfolio

The breadth of Acuity's product offering creates significant competitive advantages in specification and distribution:

The ABL segment provides lighting solutions and luminaires with advanced electronics under the Aculux, American Electric Lighting, Cyclone, Dark to Light, eldoLED, Eureka, Fresco, Gotham, Healthcare Lighting, Holophane, Hydrel, IOTA, Juno, Lithonia Lighting, Luminaire LED, Luminis, Mark Architectural Lighting, Nightingale, nLight, Peerless, RELOC Wiring Solutions, and SensorSwitch brand names.

The AIS segment offers Distech Controls intelligent Building Management Systems (BMS), such as products for controlling heating, ventilation, air conditioning, lighting, shades, refrigeration, and building access that prioritize end-user outcomes; Q-SYS, a full-stack audio, video, and control platform, and QSC Audio, an audio technology for live entertainers and sound reinforcement professionals. This segment serves retail stores, airports, universities, enterprise campuses, sports venues, themed entertainment, and hospitality sectors through system integrators. It offers its products and solutions under the Atrius, Distech Controls, QSC, and KE2 Therm Solutions brands.

Distribution Strategy

This segment serves electrical distributors, consumer retailers, large corporate accounts, and original equipment manufacturer customers.

Acuity's multi-channel distribution strategy is a key competitive moat. Products reach customers through independent sales agents who maintain deep relationships with architects and specifiers, electrical wholesalers who serve contractors, direct sales to major national accounts, digital platforms for smaller orders, and relationships with retailers and utilities for efficiency programs.

This distribution network took decades to build and would be nearly impossible for new entrants to replicate quickly. When an architect specifies lighting for a new building, they typically choose brands they know and trust, sold through distributors with whom they have longstanding relationships. Acuity's heritage brands—Lithonia, Holophane, Juno—carry specification advantage that converts to orders.

R&D and Innovation

Value creation stems from robust research and development focused on LED technology, controls, and IoT integration. R&D spending typically represents around 2-3% of net sales annually—modest by technology company standards, but substantial for an industrial manufacturer.

Manufacturing primarily occurs in North America, with major facilities in Georgia, Kentucky, Ohio, and Mexico. This regional concentration provides supply chain resilience and responsiveness to customer demand—a competitive advantage that became more apparent during COVID-era supply chain disruptions.

VIII. Financial Performance & Recent Results

Fiscal 2024 Performance

Acuity Brands, Inc. (NYSE: AYI), North America's largest lighting company, reported its full-year results for fiscal 2024, ending on August 31, 2024. Despite a 2.8% decline in net sales, totaling $3.84 billion, the company achieved notable profitability, with full-year diluted earnings per share (EPS) rising by 25% to $13.44 and adjusted diluted EPS up 11% at $15.56. Operating profit for the year reached $553.3 million, an increase of $79.9 million or 16.9% over the prior year.

The ability to grow profitability despite declining revenue reflects Acuity's successful margin expansion strategy—product mix shift toward higher-margin items, operational efficiency improvements, and disciplined pricing.

At the end of fiscal 2024, cash and cash equivalents totaled $845.8 million, more than doubling from $397.9 million in fiscal 2023.

This cash accumulation positioned Acuity to fund the QSC acquisition without excessive leverage.

Fiscal 2025 Trajectory

Acuity Brands, Inc., a market-leading industrial technology company, announced net sales of $951.6 million in the first quarter of fiscal 2025 ended November 30, 2024, an increase of $16.9 million, or 1.8 percent, compared to the prior year.

The QSC acquisition began contributing in the second quarter of fiscal 2025: The acquisition of QSC was successfully closed, with two months of its performance contributing to the consolidated results. Net Sales: Total Acuity net sales reached $1 billion, an 11% increase year-over-year ($100 million). This growth was primarily driven by the continued expansion of the Acuity Intelligent Spaces (AIS) segment and the inclusion of QSC's sales. Adjusted Operating Profit: Adjusted operating profit stood at $163 million, marking a 16% increase year-over-year ($23 million).

The Acuity Intelligent Spaces (AIS) segment delivered explosive growth: AIS net sales surged by 204% to $255 million from $84 million in Q4 2024, primarily driven by the acquisition of QSC. Adjusted operating profit for this segment increased by 154% to $55 million from $22 million.

Updated Guidance

Acuity provided an updated outlook for fiscal year 2025: Net Sales: $4.3 billion to $4.5 billion for the total company. Adjusted Diluted EPS: $16.50 to $18.00.

FY2026 guidance: Net sales $4.7B-$4.9B; Adjusted EPS $19-$20.50; Focus on organic growth in AIS segment, low single-digit ABL growth.

IX. Competitive Landscape & Industry Analysis

Market Position

Their largest market share is in the Building Lighting Control System Manufacturing industry, where they account for an estimated 30.7% of total industry revenue.

These companies collectively accounted for 50.96% of the total market share in 2024. Signify Holding and Acuity Brands Lighting Inc. hold a significant share of over 31.2% in the market.

Key Competitors

Some of the key competitors of Acuity Brands Inc include: Philips Lighting: As one of the largest lighting companies globally, Philips Lighting poses a significant competition to Acuity Brands Inc. The company offers a wide range of lighting solutions and has a strong presence in both residential and commercial markets. Eaton Corporation: Eaton Corporation is another major competitor of Acuity Brands Inc. The company specializes in power management solutions, including lighting systems, control devices, and advanced building management technologies. Hubbell Incorporated: Hubbell Incorporated is a well-established player in the lighting and electrical equipment industry. The company offers a diverse portfolio of lighting solutions, including indoor and outdoor lighting fixtures, controls, and sensors.

Acuity Brands operates as a major IoT-led lighting provider in North America by offering multiple systems that power commercial and industrial buildings.

Porter's Five Forces Analysis

Threat of New Entrants: LOW-MODERATE Barriers to entry include established distribution relationships, brand recognition among specifiers, manufacturing scale, and increasingly, software/IoT capabilities. However, commoditization of basic LED fixtures has enabled low-cost Asian manufacturers to capture portions of the market.

Bargaining Power of Suppliers: MODERATE LED chips are sourced from a limited number of suppliers (Cree, Nichia, Samsung, etc.), but these suppliers serve many manufacturers. The supply chain has matured to the point where Acuity has multiple sourcing options for most components.

Bargaining Power of Buyers: MODERATE-HIGH Large distributors and national accounts can negotiate pricing. However, specification by architects and engineers creates switching costs, and Acuity's breadth of product offering means customers often prefer working with a single supplier.

Threat of Substitutes: LOW Buildings need lighting—that's not changing. The relevant question is whether traditional lighting companies or technology companies will dominate the intelligent buildings space.

Competitive Rivalry: HIGH Intense competition: The lighting industry is highly competitive, with numerous players vying for market share. Acuity Brands faces strong competition from both established companies and new entrants, which could impact its market position and profitability.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Acuity's North American manufacturing footprint and volume provide meaningful cost advantages over smaller competitors.

Network Economies: Limited in traditional lighting, but Acuity's IoT platforms could develop network effects as more buildings adopt integrated systems.

Counter-Positioning: Acuity's aggressive move into building automation and AV controls represents counter-positioning against pure-play lighting companies that haven't made similar investments.

Switching Costs: Moderate in traditional lighting (products are specified but can be value-engineered). Much higher in building management systems where Distech and Q-SYS installations create meaningful lock-in.

Branding: Heritage brands like Lithonia, Holophane, and Juno carry specification advantage among architects and contractors.

Cornered Resource: The Distech and QSC platforms represent proprietary technology assets, though defensibility depends on continued innovation.

Process Power: Acuity's "Better. Smarter. Faster." operating system and disciplined capital allocation represent process advantages, though these are less defensible than structural competitive advantages.

X. Investment Considerations: Bull & Bear Cases

The Bull Case

1. Intelligent Spaces is an Emerging Growth Engine The explosive growth in the AIS segment, combined with margin expansion in the core lighting business, has driven substantial improvements in overall financial performance. With a clear strategic direction and positive outlook for fiscal 2026, Acuity appears well-positioned to continue its growth trajectory and deliver value to shareholders.

The QSC acquisition fundamentally changes Acuity's growth profile. AIS is growing at 15%+ organically, and the addition of QSC creates a platform for continued expansion into adjacent markets.

2. Recurring Revenue Potential Software platforms like Q-SYS and Distech's building management systems create opportunities for subscription-based pricing, maintenance contracts, and upgrade paths that generate recurring revenue—a dramatic improvement over one-time hardware sales.

3. Valuation Discount to Technology Peers Acuity trades at industrial company multiples (roughly 15-18x forward earnings) despite increasingly looking like a technology company. If the AIS segment continues growing and market perception shifts, there's potential for multiple expansion.

4. Secular Tailwinds Energy efficiency regulations, sustainability mandates, and the trend toward smart buildings create durable demand drivers. Connected lighting and building automation aren't optional in new commercial construction—they're increasingly table stakes.

The Bear Case

1. Core Lighting Remains Cyclical Intense competition: The lighting industry is highly competitive, with numerous players vying for market share.

The ABL segment still represents 93% of revenue and is tied to nonresidential construction, which is inherently cyclical. A recession that impacts commercial building activity would pressure results.

2. Acquisition Integration Risk The QSC acquisition is Acuity's largest ever. Integration of a California-based AV company into an Atlanta-based lighting manufacturer is complex. Talent retention, culture clash, and execution risk are real concerns.

3. Competition from Technology Giants Google, Amazon, Microsoft, and specialized building technology companies are all investing in smart building platforms. Acuity may find itself competing with better-funded technology companies as the intelligent buildings market matures.

4. LED Commoditization Pressure Intelligent luminaires can cost 40-60% more than basic LED fixtures, and many small enterprises lack access to performance contracting or on-bill financing. Decision makers often prioritize visible capex savings over lifetime operating benefits, lengthening sales cycles.

Asian manufacturers continue to pressure pricing on basic LED fixtures. Acuity's response—moving up the value chain toward specification-grade products and controls—works, but requires constant innovation to stay ahead of commoditization.

XI. Key Performance Indicators for Investors

For investors tracking Acuity's ongoing performance, three KPIs warrant particular attention:

1. AIS Segment Revenue Growth Rate

This is the single most important metric for tracking Acuity's transformation thesis. Organic growth in Acuity Intelligent Spaces (excluding acquisition contributions after the first year) will indicate whether the platform strategy is gaining traction with customers. Look for sustained double-digit organic growth to validate the bull case.

2. Adjusted Operating Margin

Acuity has expanded margins significantly over the past several years through product mix shift, operational efficiency, and disciplined pricing. Operating profit as a percent of net sales was 15.2 percent in the fourth quarter of fiscal 2024, an increase of approximately 430 basis points compared to the prior year. Continued margin expansion would demonstrate pricing power and operating leverage; margin compression would signal competitive pressure or integration challenges.

3. AIS Revenue as Percentage of Total Revenue

The mix shift from traditional lighting toward intelligent spaces tells the transformation story numerically. In fiscal 2024, AIS represented approximately 7% of total revenue. With QSC fully integrated, this should rise to 15-20% in fiscal 2025 and potentially higher thereafter. Tracking this mix shift reveals how quickly Acuity is diversifying away from cyclical, lower-margin lighting hardware.

XII. Risk Factors & Regulatory Considerations

Material Legal/Regulatory Overhangs

No material legal or regulatory issues appear in recent filings that would represent significant risk to the investment thesis. Standard risks related to product liability, intellectual property disputes, and employment matters exist but are typical for a company of Acuity's size and scope.

Tariff Exposure

July 2025: Acuity Brands announced its third 2025 price increase for luminaires and electronics, citing new global tariffs and market volatility.

Tariff policy remains a source of uncertainty. Acuity sources some components and finished goods from China and Mexico, creating exposure to trade policy changes. However, the company has demonstrated ability to pass through cost increases via pricing actions.

Accounting Judgments

Goodwill and intangible assets from acquisitions (particularly QSC) will be material balance sheet items requiring periodic impairment testing. Investors should monitor for any impairment charges that might signal acquisition value destruction.

XIII. Conclusion: The Next Chapter

The story of Acuity Brands—now Acuity Inc.—is a testament to corporate adaptability. From Isadore Weinstein's linen supply business to Erwin Zaban's conglomerate strategy to Vernon Nagel's LED transformation to Neil Ashe's intelligent spaces vision, the company has reinvented itself repeatedly while maintaining financial discipline and market leadership.

"Acuity is positioned for long term growth. We are innovators, disruptors and builders who are creating stakeholder value and compounding shareholder wealth," said Neil Ashe, Chief Executive Officer. "We are using technology to solve problems, redefine industries and create impactful experiences that shape how people live, work and connect."

The central question for investors now is whether Acuity can successfully execute its third major transformation—from lighting manufacturer to intelligent building platform. The QSC acquisition places a $1.2 billion bet on this thesis. Early results are encouraging, with AIS segment growth accelerating and the combined platform offering unique capabilities.

For long-term fundamental investors, Acuity presents a rare opportunity: a market-leading industrial company with durable competitive advantages, trading at reasonable multiples, with an emerging growth platform that could drive both revenue expansion and multiple re-rating.

The lights came on in that Atlanta garage in 1946. More than seven decades later, Acuity's lights illuminate hospitals, schools, stadiums, and office buildings across North America. The question now is whether those lights will also illuminate a new path—one where Acuity controls not just the light in a space, but the entire experience of being there.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube