Baker Hughes: The Energy Technology Transformation Story

I. Introduction & Episode Roadmap

In January 2026, some 2,500 energy executives from 80 countries gathered not in Houston or Abu Dhabi, but in a Renaissance opera house in Florence, Italy. The theme of Baker Hughes' 26th Annual Meeting was "The Energy Equation"—the idea that industrial outcomes and energy sources are now inseparable. The choice of venue was no accident. Baker Hughes CEO Lorenzo Simonelli grew up in Tuscany, where his family still tends a vineyard. But more than personal nostalgia, the Florence setting signaled something profound: this is a company that sees itself as fundamentally different from the oilfield services giants it grew up alongside.

Baker Hughes generated $27.7 billion in revenue in 2025 and sits at a market capitalization exceeding $60 billion. It operates in over 120 countries with roughly 57,000 employees, co-headquartered in Houston and London. On paper, it belongs in the same conversation as SLB and Halliburton—the traditional "Big Three" of oilfield services. But the company that showed up in Florence is not the same one that was cobbled together from the merger of two drilling pioneers in 1987, or the one GE used as a vehicle for its oil and gas ambitions in 2017.

The central question of this story is deceptively simple: How did a century-old oilfield services company transform itself into an energy technology leader straddling the divide between the hydrocarbon world and the energy transition? The answer involves two legendary inventors, a string of mega-mergers that would make any M&A lawyer's head spin, an FCPA scandal, a $34.6 billion deal that died on the DOJ's doorstep, a GE marriage that almost nobody wanted, and a quiet Italian executive who somehow stitched it all into a coherent strategy.

This is the story of Baker Hughes—told from the origin myths of its dual founders through to the data-center-powering, hydrogen-compressing, geothermal-drilling company it has become.

II. The Twin Origin Stories: Baker & Hughes

The Third-Grade Dropout Who Revolutionized Cable-Tool Drilling

In the dusty oil patches of central California at the turn of the twentieth century, a man who never made it past the third grade was about to change the petroleum industry forever. Reuben Carlton "Carl" Baker was born in 1872 on a farm, following his older brother Aaron into the oil business. By 1895, he was driving a horse team to haul oil for drillers in Coalinga, California—grueling, unglamorous work. A year later, he had talked his way into becoming a drilling contractor himself.

Baker was the kind of tinkerer who saw problems as personal affronts. Cable-tool drilling—the dominant method at the time—required lowering steel casing into the borehole to prevent it from collapsing. But getting the casing down smoothly was maddening. The bottom of the casing would catch on rock ledges, get stuck, or fail to seat properly. Drillers lost weeks and fortunes wrestling with the problem.

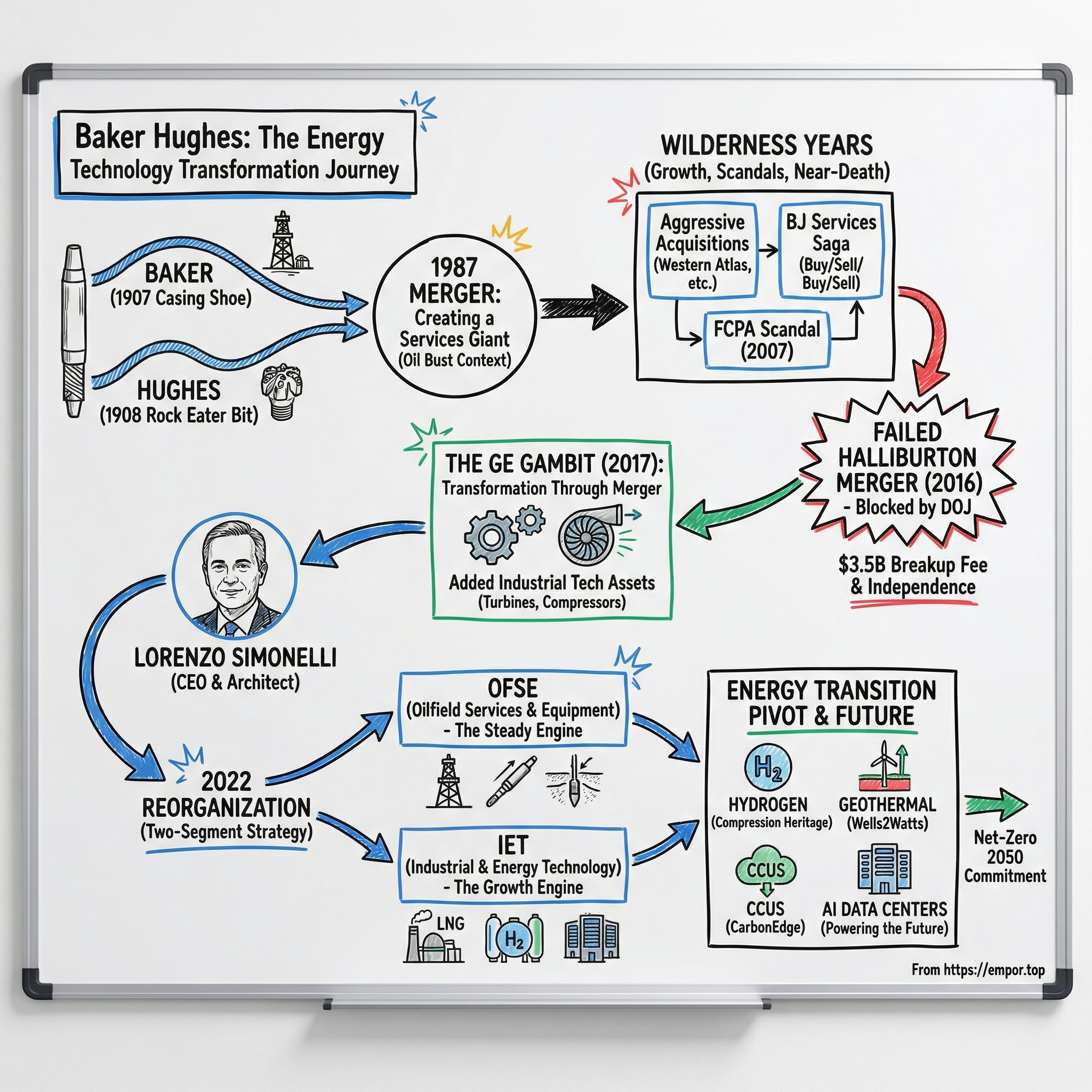

In July 1907, Baker received a U.S. patent for a casing shoe—a simple but elegant device that guided casing into the wellbore and allowed it to be cemented in place. It sounds mundane, but this was a breakthrough that made cable-tool drilling dramatically more reliable. Baker would go on to accumulate more than 150 patents on drilling tools over his career—an astonishing output for a self-taught inventor.

He was shrewd about monetization too. Rather than manufacturing immediately, Baker licensed his patents and lived off royalties for years. It was not until the 1920s that he began manufacturing his own tools in Huntington Park, California. In 1928, he renamed the operation Baker Oil Tools, Inc. The company grew steadily, and by 1976 it had become Baker International Corporation under the leadership of E. H. "Hubie" Clark Jr., a Caltech-trained mechanical engineer who joined in 1947 and eventually acquired roughly 20 companies, including Reed Tool Company, a major drill-bit manufacturer, in 1975.

Howard Hughes Sr. and the Bit That Ate Rock

Meanwhile, a parallel revolution was happening in rotary drilling—and its hero was Howard Robard Hughes Sr. If Baker was the quiet tinkerer, Hughes was the swashbuckling entrepreneur. Born in 1869 in Missouri, Hughes had bounced between mining ventures and law school before landing in the Texas oil boom.

The problem Hughes attacked was even more fundamental than Baker's. Rotary drilling—the newer, faster method that was displacing cable-tool rigs—relied on drill bits to chew through rock. The bits available in 1908 were essentially fishtail-shaped blades that worked fine in soft formations but shattered against anything hard. Drillers would watch helplessly as their bits dulled to uselessness against limestone or granite, burning through time and money.

In 1908, Hughes and his business partner Walter Benona Sharp built a wooden model of a two-cone drill bit—a design that used rotating conical cutters instead of fixed blades. The cones would roll against the rock face, crushing and chipping it away rather than trying to scrape through it. On November 20, 1908, Hughes filed the patents. When the bit was first tested at Goose Creek, Texas, it penetrated 14 feet of hard rock in 11 hours—rock that no previous equipment had been able to penetrate at all. Drillers nicknamed it the "rock eater."

The Sharp-Hughes Tool Company was founded in 1909. After Sharp died in 1912, Hughes gradually bought out his partner's estate, renaming the firm Hughes Tool Company by 1918. By 1914, the two-cone roller bit was in use across 11 U.S. states and 13 foreign countries. Hughes had not just invented a tool—he had unlocked geological formations that were previously considered undrillable.

Then came tragedy. On January 14, 1924, Howard Hughes Sr. died of a heart attack at age 54 in his company's offices in Houston. His only child, Howard Hughes Jr.—destined to become one of the most famous and enigmatic figures in American history—inherited 75 percent of the company at age 19. The younger Hughes had himself legally declared an adult, bought out his grandparents and uncle for full control, and promptly appointed Noah Dietrich as CEO so he could pursue filmmaking and aviation in California.

Hughes Tool Company thrived even without its founder. In 1933, two company engineers invented the Tricone three-cone drill bit, which quickly became the industry standard. During the Tricone's 17-year patent protection period from 1934 to 1951, Hughes Tool's market share in drill bits approached 100 percent—a monopoly that funded Howard Hughes Jr.'s increasingly eccentric lifestyle and business ventures. In 1972, the oil-tools business was floated on the NYSE, while the remaining Hughes enterprises were reorganized under the name Summa Corporation.

Baker and Hughes had been running on parallel tracks for decades—one perfecting the wellbore itself, the other perfecting the tools that cut through rock. Both companies embodied a particular kind of American industrial genius: practical inventors who saw problems in the field and engineered solutions that became industry standards. Baker's casing shoe made wells structurally sound. Hughes's roller bit made them possible in hard rock. Together, they covered the two most fundamental challenges of petroleum drilling.

By the 1980s, both had grown into significant international operations with thousands of employees and operations on multiple continents. Baker International had expanded aggressively under Hubie Clark into Peru, Nigeria, Libya, Iran, and Australia. Hughes Tool Company had become a global standard in drill bits, its Tricone design as ubiquitous as the derrick itself. Their eventual collision was almost inevitable—and the oil bust of 1986 would provide the catalyst.

III. The 1987 Merger: Creating a Services Giant

A Shotgun Wedding in an Oil Bust

By the mid-1980s, the global oil industry was in agony. OPEC's decision to flood the market had cratered crude prices from over $30 a barrel in 1985 to under $10 by early 1986. Oilfield services companies—whose fortunes rise and fall with drilling activity—were hemorrhaging cash. It was the perfect environment for consolidation, and in 1987, Baker International and Hughes Tool Company agreed to merge in a $728 million stock transaction.

The logic was straightforward: combine Baker's strength in completions, cementing, and downhole tools with Hughes's dominance in drill bits and drilling services. Together, they would create a company second in size only to Schlumberger in the oilfield services world.

But the wedding was anything but smooth. The U.S. Department of Justice required Baker to sign a consent decree divesting its Reed Tool Company domestic operations, Reed's Singapore facility, and its Baker Lift division—businesses that overlapped too heavily with Hughes's existing portfolio. This is where the drama really started. After Baker agreed to the consent decree, Hughes attempted to terminate the entire merger agreement, apparently deciding the divestitures made the deal less attractive. Baker responded with a $1 billion lawsuit.

The legal battle was fierce but brief. Hughes shareholders voted overwhelmingly to complete the transaction despite management's cold feet. On April 1, 1987, Baker Hughes Incorporated began trading on the NYSE at $18.63 per share. Two days later, Hughes formally agreed to the consent decree terms, and the merger was done.

Building Through Acquisitions

What followed was one of the most aggressive acquisition campaigns in the history of oilfield services. The newly combined company went on a buying spree that lasted more than a decade, filling gaps in its portfolio and building scale across every major service line.

The acquisitions read like a who's who of the oilfield services ecosystem. In drilling fluids: Milchem and Newpark. In completions: Brown Oil Tools, CTC, Elder Oil Tools. In mud logging: EXLOG. The 1990 acquisition of Eastman Christensen for $600 million brought world-class directional drilling systems and diamond bit technology—a transformative deal that was merged with Hughes Tool to form Hughes Christensen Company. In 1992, Baker Hughes paid $200 million for Teleco Oilfield Services, adding measurement-while-drilling capability. Teleco and four other drilling systems companies were eventually combined into Baker Hughes INTEQ.

The fishing tools business came through Tri-State and Wilson. Artificial lift capability arrived via Centrilift. Specialty chemicals were built through Aquaness, Chemlink (acquired in 1990 for $136 million), and the crown jewel—Petrolite, purchased in 1997 for $693 million in stock. Petrolite had its own fascinating origin story, having been formed in 1930 from the merger of William Barnickel's Tret-O-Lite with Petroleum Rectifying Company of California.

The biggest deal of the post-merger era was the $5.5 billion stock acquisition of Western Atlas on August 10, 1998, plus the assumption of $700 million in debt. Western Atlas's wireline division became Baker Atlas, while its seismic division (Western Geophysical) was later combined with Schlumberger's Geco-Prakla to form WesternGeco in 2000.

By the end of the 1990s, Baker Hughes had assembled a full-spectrum oilfield services portfolio spanning everything from drill bits to seismic surveys. It was firmly established as one of the Big Three alongside Schlumberger and Halliburton—the three companies that collectively controlled approximately 85 percent of the global oilfield services market. But the acquisition machine had also created organizational complexity that would haunt the company for years to come.

Integrating dozens of fiercely independent operations—each with its own culture, sales force, technology platform, and often its own views about how wells should be drilled—was a management challenge that Baker Hughes never fully solved during this era. The company was big enough to compete everywhere but often lacked the focus to dominate anywhere. Schlumberger, by contrast, had a more disciplined technology-first culture and a unified global brand. Halliburton had laser focus on execution and cost efficiency, particularly in North American pressure pumping. Baker Hughes was the broadest portfolio of the three, but breadth without strategic coherence can be as much a liability as an asset—a lesson the company would learn painfully in the decades ahead.

IV. Growth, Scandals, and Near-Death: The Wilderness Years

The BJ Services Saga

Perhaps no single story better illustrates Baker Hughes' strategic confusion during this period than the saga of BJ Services. In 1990, Baker Hughes sold a 71 percent stake in BJ Services—its pressure pumping and cementing business—through an IPO, creating a standalone publicly traded company. The rationale at the time was to unlock value and focus the parent company on its core drilling and completions operations.

Then the shale revolution happened. Hydraulic fracturing went from a niche technique to the technology that unlocked the greatest energy boom in American history. And Baker Hughes had sold off the very business that was perfectly positioned to profit from it. In April 2010, the company paid $5.5 billion to re-acquire BJ Services—issuing approximately 118 million shares and paying $800 million in cash. The deal massively expanded Baker Hughes' pressure pumping capabilities, but the timing was questionable. The company had sold BJ Services for a fraction of what it cost to buy it back.

The story gets stranger. In January 2017, Baker Hughes effectively divested BJ Services again, selling a 53.3 percent stake in its North American land cementing and hydraulic fracturing businesses to CSL Capital Management and Goldman Sachs' West Street Energy Partners for $325 million. The new entity operated under the BJ Services brand, headquartered in Tomball, Texas. Three years later, in July 2020, BJ Services filed for Chapter 11 bankruptcy. The business Baker Hughes had bought, sold, bought back, and sold again was now worthless.

The FCPA Scandal

The mid-2000s brought a different kind of crisis. On April 26, 2007, Baker Hughes pleaded guilty to violating the antibribery provisions of the Foreign Corrupt Practices Act, resulting in $44.1 million in fines—the largest combined monetary sanction ever imposed in an FCPA case at that time.

The facts were ugly. A Baker Hughes subsidiary had paid approximately $4.1 million in bribes over a two-year period from 2001 to 2003 to an intermediary in Kazakhstan who funneled money to an executive at KazakhOil, the state oil company. The bribes were connected to the Karachaganak oil project. Despite the intermediary performing no legitimate services, Baker Hughes had agreed to pay commissions of 2 percent of revenue on Karachaganak and 3 percent on future Kazakhstan projects. The settlement included an $11 million criminal penalty, a $10 million civil penalty, roughly $20 million in disgorgement of profits, and $3.1 million in prejudgment interest.

The scandal forced a comprehensive overhaul of the company's compliance culture. But it also reinforced a growing perception in the market that Baker Hughes was the least disciplined of the Big Three—a company that could win contracts and build technology but struggled with execution, governance, and strategic consistency.

The Shale Revolution and Its Discontents

The shale revolution transformed the oilfield services industry in ways that both helped and hurt Baker Hughes. On one hand, the explosion of drilling activity in the Permian Basin, Eagle Ford, Bakken, and other U.S. unconventional plays created enormous demand for drilling, completions, and production services. Baker Hughes invested in new capabilities, including introducing the largest fracturing proppants vessel for deepwater Gulf of Mexico operations in 2001—a technological milestone that demonstrated the company's engineering prowess.

On the other hand, shale drilling was increasingly dominated by Halliburton's massive North American pressure pumping fleet and by SLB's digital workflows. Baker Hughes found itself in an awkward middle ground—strong enough to compete but lacking the clear strategic identity of its rivals. Schlumberger was the technology and digital leader. Halliburton owned North American completions. Baker Hughes was a bit of everything, which in a competitive market often means not enough of anything.

By the mid-2010s, the company was at a crossroads. It had world-class technology in several product lines—drill bits, artificial lift, chemicals, directional drilling—but lacked a coherent strategy to tie them together. Market share in key product lines had eroded. The stock had underperformed both SLB and Halliburton over most of the preceding decade. Analysts regularly questioned whether Baker Hughes had a sustainable competitive position or was simply the weakest of the Big Three—the one most likely to be acquired.

The oil price collapse of 2014 would force a reckoning that nearly erased Baker Hughes from the map as an independent company. But as the old energy industry saying goes, the best deals get done when the industry is on its knees.

V. The Halliburton Merger That Wasn't

The Biggest Deal That Never Happened

In November 2014, with oil prices in freefall from over $100 a barrel to below $60, Halliburton announced its intention to acquire Baker Hughes in a deal valued at approximately $34.6 billion—roughly $78.62 per Baker Hughes share. Had it been completed, it would have been the largest merger in petroleum industry history.

The strategic rationale was classic downturn consolidation. With drilling activity collapsing worldwide, the oilfield services industry was drowning in overcapacity. Combining the number-two and number-three players would create a colossus to rival SLB, with massive cost synergies and pricing power. Halliburton CEO Dave Lesar pitched the deal as the kind of bold move that only makes sense when an industry is on its knees.

But regulators saw it differently. On April 6, 2016, the U.S. Department of Justice filed suit to block the merger, alleging it would "unlawfully eliminate significant head-to-head competition" in at least 23 markets crucial to oil and gas exploration and production. The DOJ's complaint painted a picture of a combined entity with too much pricing power—one that could raise prices, reduce output, and stifle innovation across a wide range of oilfield services.

Halliburton had offered to divest certain assets to address antitrust concerns, but the DOJ found the proposal wholly inadequate, noting it "did not include full business units, withheld many critical assets and personnel." International regulators in Europe and elsewhere echoed similar concerns.

On May 1, 2016, Halliburton and Baker Hughes terminated the merger agreement. Halliburton paid Baker Hughes a $3.5 billion breakup fee—one of the largest termination payments in M&A history. The fee was a lifeline for a company that had been in limbo for 18 months, unable to make strategic decisions or retain top talent while the deal hung in regulatory purgatory.

But the failed merger left Baker Hughes at a crossroads unlike any it had faced before. The company had spent a year and a half preparing to be absorbed. Key executives had left. The strategic planning process had been frozen. Baker Hughes was suddenly independent again, weakened and directionless, sitting on $3.5 billion in termination cash and no clear path forward. That vulnerability made it a target—and the next suitor would come from an entirely unexpected direction.

VI. The GE Gambit: Transformation Through Merger

An Industrial Giant Comes Calling

In October 2016—barely five months after the Halliburton deal collapsed—GE announced plans to merge its Oil & Gas division with Baker Hughes. If the Halliburton deal had been about consolidation within oilfield services, the GE transaction was something altogether different: a bet that the future of energy required combining oilfield expertise with industrial technology.

GE Oil & Gas was already a significant business in its own right, with a strong portfolio in gas turbines, compressors, pumps, and process technology. Jeff Immelt, GE's CEO at the time, saw the energy industry heading toward a convergence of oil and gas production, power generation, and digital technology. Merging with Baker Hughes would create what GE called a "fullstream company"—one that could serve customers from the wellhead to the power plant.

The transaction closed on July 3, 2017. GE took a 62.5 percent stake in the combined entity, which was named Baker Hughes, a GE company—or BHGE, as it became universally known. The new company had roughly 70,000 employees and was led by Lorenzo Simonelli, who had been running GE Oil & Gas, as president and CEO.

The Unlikely Partnership

The cultural challenges were immense. Baker Hughes was a 130-year-old oilfield services company rooted in the rough-and-tumble world of drilling rigs and oil patches. GE Oil & Gas was a division of America's most iconic industrial conglomerate, with a culture steeped in Six Sigma processes, corporate planning cycles, and the management philosophy of Jack Welch. Combining them was like merging a ranch with a factory.

The vision, as articulated by Baker Hughes' outgoing CEO Martin Craighead and incoming leader Simonelli, was compelling on paper. Baker Hughes had deep expertise in what happens below the ground—drilling wells, completing them, and extracting hydrocarbons. GE Oil & Gas had equally deep expertise in what happens above the ground—processing, compressing, and transporting gas; generating power from natural gas turbines; and monitoring industrial assets through sensors and digital platforms. Together, they could offer customers an integrated solution spanning the entire energy value chain.

But GE itself was falling apart. Under Immelt and then his successor John Flannery, the conglomerate was unraveling across multiple fronts—GE Capital's legacy liabilities, Power division write-downs, and a collapsing stock price. By June 2018, GE announced it would eventually divest its 62.5 percent stake in BHGE. The grand vision of a GE-powered energy technology platform was being abandoned before it had fully taken shape.

Simonelli Seizes the Moment

What happened next was remarkable. Rather than viewing GE's retreat as a crisis, Simonelli used it as an opportunity to reshape Baker Hughes on his own terms. In September 2019, GE reduced its ownership to approximately 38.4 percent through a secondary offering that generated about $2.7 billion in net proceeds—a transaction in which GE booked an estimated $7.4 billion loss on its original investment. GE no longer had a controlling interest.

On October 17, 2019, BHGE officially changed its name to Baker Hughes Company. The following day, it began trading under the new ticker "BKR" on the NYSE. The GE brand was gone, but the industrial assets GE had brought—the turbines, compressors, process technology, and digital platforms—stayed. Simonelli had kept the dowry while freeing the company from the marriage.

GE continued divesting its stake through a series of secondary offerings over the next few years, completing its full exit by 2023. Baker Hughes emerged from the GE era as something genuinely new: an oilfield services company with a world-class industrial technology business grafted onto its core. Whether that hybrid model would work was the question that would define the next chapter.

VII. Lorenzo Simonelli: The Transformation Architect

A Tuscan in GE's Machine

To understand Baker Hughes' transformation, you have to understand the man driving it. Lorenzo Simonelli was born on July 27, 1973, in Tuscany, Italy—the kind of place where families measure time in generations and harvest cycles. His family still owns a vineyard that produces wine and olive oil. At age nine, he moved to London with his father and was educated at Highgate School, one of the city's oldest independent schools. He earned his degree in business and economics from Cardiff University in Wales—a solid but unglamorous credential that belied the career that would follow.

Simonelli began in international and corporate finance at Mitsubishi Bank before joining GE's legendary Financial Management Program in 1994. The FMP was GE's training ground for future leaders—a rotational program that cycled ambitious young managers through multiple divisions at breakneck speed. Simonelli thrived in the system, moving through GE International, GE Shared Services, GE Oil & Gas, and Consolidated Financial Insurance.

The Youngest Division Chief

The moment that marked Simonelli as someone special came in July 2008, when he was named president and CEO of GE Transportation at age 34. This made him the youngest person ever to lead a GE division and the first non-American to run GE Transportation—a business headquartered in Erie, Pennsylvania, that made locomotives, mining equipment, and propulsion systems. The appointment signaled that GE's leadership saw in Simonelli a rare combination: a European sensibility about global markets paired with an American-style bias for action.

At GE Transportation, Simonelli spent five years expanding and diversifying the business, pushing into advanced technology manufacturing, intelligent control systems, and diverse propulsion solutions. The experience was formative. He learned to manage a complex industrial business through a global financial crisis, to think in terms of technology platforms rather than individual products, and to build leadership teams that could operate across cultures.

In October 2013, at age 40, Simonelli was appointed president and CEO of GE Oil & Gas. This was the role that would set the stage for everything that followed. At GE Oil & Gas, he oversaw a business that manufactured the turbines that powered LNG plants, the compressors that moved natural gas through pipelines, and the monitoring systems that kept industrial equipment running. When the opportunity came to merge GE Oil & Gas with Baker Hughes in 2017, Simonelli was the natural choice to lead the combined company.

Leadership Philosophy

Simonelli's leadership style is distinctive in the energy industry—quieter and more deliberate than the Texas-bred executives who have traditionally dominated the oilfield services world. He thinks in terms of long-term technology platforms rather than quarterly drilling metrics. His speeches and interviews consistently return to a single theme: the energy industry needs to solve three challenges simultaneously—energy security, affordability, and sustainability—and the companies that build technology to address all three will win.

The recognition has followed. Fortune named him to its Forty under Forty list. Petroleum Economist named him CEO of the Year. The University of Florence awarded him an honorary master's degree in chemical sciences. But Simonelli's most important accomplishment has been less visible: he took a company that GE was trying to dump, kept the best parts of what GE brought, stripped away the corporate overhead, and built a strategic narrative that the market has increasingly bought into.

VIII. The Energy Transition Pivot: Becoming an Energy Technology Company

The Reorganization That Changed Everything

On September 6, 2022, Baker Hughes announced the reorganization that crystallized Simonelli's vision. The company would restructure from four reporting segments into two: Oilfield Services & Equipment (OFSE) and Industrial & Energy Technology (IET). The change, effective October 1, 2022, was more than an org chart exercise. It was a declaration of identity.

The old four-segment structure—Oilfield Services, Oilfield Equipment, Turbomachinery & Process Solutions, and Digital Solutions—had been a legacy of the GE merger, an awkward blend of oilfield and industrial businesses that made it hard for investors to see what Baker Hughes actually was. The new two-segment structure drew a clean line. OFSE was the traditional oilfield services business—drilling wells, completing them, producing hydrocarbons. IET was everything else: gas turbines, compressors, climate technology solutions, condition monitoring, industrial sensors.

The strategic message was unmistakable. Baker Hughes was not just an oilfield services company that happened to make turbines. It was an energy technology company with two distinct engines—one serving the hydrocarbon present, the other building toward the energy future. The restructuring was expected to deliver at least $150 million in cost reductions, and it came with new leadership: Maria Claudia Borras as EVP of OFSE and Rod Christie as EVP of IET.

Building the New Energy Portfolio

Under the IET umbrella, Baker Hughes began aggressively building capabilities in four areas that Simonelli identified as the pillars of the energy transition: hydrogen, geothermal energy, carbon capture utilization and storage (CCUS), and emissions abatement.

In hydrogen, Baker Hughes brings a heritage that surprises many observers—the company built its first hydrogen reciprocating compressor in 1915, more than a century ago. Today, its hydrogen technology spans high-pressure ratio centrifugal compressors designed specifically for hydrogen gas (already in second-generation development), electrolyzer technology for producing green hydrogen, and compression and transport solutions for the entire hydrogen value chain. A partnership with ADNOC involves installing next-generation electrolyzers in Abu Dhabi.

In CCUS, Baker Hughes has been involved in more than 60 projects worldwide—a number that positions it as one of the most experienced companies in the nascent carbon capture industry. The company supplies compression equipment for CO2 transport and injection, and in September 2024 it launched CarbonEdge, described as the first end-to-end, risk-based digital solution for CCUS operations. CarbonEdge uses real-time data and alerts to monitor CO2 flows across capture, compression, pipeline transport, and subsurface storage infrastructure.

In geothermal, the company launched the Wells2Watts consortium in late 2022—a partnership with Continental Resources, INPEX, Chesapeake Energy, and California Resources Corporation to develop technology for converting abandoned oil and gas wells into geothermal energy producers. The logic is elegant: there are approximately 3 million abandoned wells in the United States alone, and drilling represents 40 to 60 percent of geothermal project costs. By repurposing existing wellbores, Wells2Watts aims to dramatically lower the capital threshold for geothermal development.

The consortium has also partnered with GreenFire Energy, whose GreenLoop closed-loop technology circulates working fluid to harvest heat without depleting the geothermal resource, and with ICE Thermal Harvesting, which provides heat-to-power systems using Organic Rankine Cycle technology. A first-of-its-kind closed-loop geothermal test facility was commissioned at Baker Hughes' Energy Innovation Center at the Hamm Institute in Oklahoma City in October 2023.

Net-Zero Commitments and Carbon Out

Baker Hughes was one of the first companies in its industry to commit to net-zero Scope 1 and Scope 2 emissions by 2050, with an interim target of a 50 percent reduction by 2030 from a 2019 baseline. The progress has been meaningful—by the latest reporting, the company had achieved a 40 percent reduction in Scope 1 facility emissions, a 42.4 percent reduction in Scope 2 facility emissions, and nearly one-third of its electricity sourced from zero-carbon sources.

The internal program driving these reductions is called Carbon Out—an employee-driven initiative where field personnel, scientists, and product line leaders actively identify and implement emissions reduction projects. The program is designed to create cultural change, not just hit top-down targets. It extends to developing a Scope 3 emissions reduction roadmap, which covers emissions from the company's products in use—by far the largest emissions category for any energy equipment provider.

For investors, the energy transition pivot raises a fundamental question: is Baker Hughes actually building a differentiated business in clean energy, or is it simply greenwashing a fossil fuel company? The evidence increasingly favors the former. Climate Technology Solutions revenue within IET grew 114 percent year-over-year in the first quarter of 2025. IET orders hit a record $14.9 billion for full-year 2025. The backlog reached $32.4 billion—a mountain of contractually committed future revenue that gives Baker Hughes multi-year visibility in a way that traditional oilfield services companies can only dream of.

IX. The Two-Segment Strategy Deep Dive

OFSE: The Steady Engine

Baker Hughes' Oilfield Services & Equipment segment provides technologies and services across the full lifecycle of a well—from exploration and appraisal through development, production, rejuvenation, and decommissioning. It operates through four product lines.

Well Construction covers drill bits, drilling fluids, and drilling services. This is the business descended directly from the Hughes rock eater and Baker's completions innovations—the technological DNA that has been refined over more than a century. In fiscal 2024, Well Construction generated $4.15 billion in revenue.

Completions, Intervention, and Measurements encompasses well completions equipment, wireline logging services, and pressure management. This product line generated another $4.15 billion in 2024—a business that sits at the critical junction between drilling a well and turning it into a producing asset.

Production Solutions provides artificial lift systems (descended from the Centrilift acquisition) and specialty chemicals (the legacy of Petrolite and Chemlink). At $3.47 billion in 2024 revenue, this is the product line that helps operators maximize recovery from existing wells—increasingly important as the industry focuses on extracting more from mature fields rather than drilling new ones.

The fourth product line, Subsea & Surface Pressure Systems, provides the hardware that controls and manages the flow of hydrocarbons from the wellhead to production facilities. In January 2026, Baker Hughes closed a joint venture with Cactus, Inc. for its surface pressure control business, selling a 65 percent stake for $344.5 million while retaining 35 percent. The JV, operating as Cactus International, reflects Simonelli's disciplined approach to portfolio management—keeping exposure to a business with strategic value while freeing up capital for higher-growth opportunities.

Three-fourths of OFSE revenue comes from outside North America—a geographic mix that insulates the segment somewhat from the volatility of U.S. shale drilling. But international exposure cuts both ways; OFSE's international revenue came under pressure in 2025, with Europe, CIS, and Sub-Saharan Africa declining 36 percent in the third quarter due to geopolitical headwinds and reduced spending by operators in those regions.

The critical thing to understand about OFSE is its evolving role within Baker Hughes. The segment represented approximately 45 percent of projected 2025 revenue and roughly 40 percent of projected EBITDA. Those percentages are trending downward—not because OFSE is shrinking dramatically, but because IET is growing faster. OFSE is the cash engine that funds Baker Hughes' transformation, generating reliable earnings even as the oilfield services market cycles. But it is no longer the growth story.

What keeps OFSE strategically interesting is its potential application beyond traditional hydrocarbons. The same drilling, completions, and production expertise that builds oil wells can also build geothermal wells and CO2 injection wells for carbon capture. Baker Hughes is already leveraging OFSE capabilities for geothermal projects with Fervo Energy and Controlled Thermal Resources—a cross-segment synergy that pure-play oilfield services companies cannot replicate.

IET: The Growth Engine

If OFSE is the company Baker Hughes was, IET is the company it wants to become. The Industrial & Energy Technology segment combines the legacy GE Oil & Gas assets—gas turbines, compressors, process technology—with newer capabilities in climate technology, digital solutions, and industrial monitoring.

Gas Technology Equipment, or GTE, is the heart of the segment. Baker Hughes designs, manufactures, tests, and installs solutions for the entire natural gas value chain: onshore and offshore production, pipeline compression, LNG liquefaction, gas storage, and distribution. The crown jewel is the LM9000 aeroderivative gas turbine, derived from GE Aviation jet engine technology—a cornered resource that very few companies in the world can replicate. These turbines power some of the largest LNG liquefaction facilities on the planet.

Gas Technology Services provides maintenance, upgrades, and lifecycle support for installed equipment. This is the recurring revenue stream that makes the IET business model so attractive—once a Baker Hughes turbine or compressor is installed in an LNG facility or pipeline compression station, the customer is locked into a multi-decade relationship for spare parts, field engineering, and performance upgrades. Service agreements of 90 months or longer are common.

Think of it like the razor-and-blade model, except the "razor" is a $100 million turbine installation and the "blades" are decades of service revenue with margins that expand as the installed base grows. This is what gives IET its strategic power: high switching costs and long-duration contracts that provide visibility years into the future.

Climate Technology Solutions spans carbon capture systems, hydrogen production and compression equipment, clean power generation, and emissions management solutions for hard-to-abate industrial sectors like cement, steel, and petrochemicals. This product line is still relatively small but growing rapidly—114 percent year-over-year revenue growth in the first quarter of 2025.

Industrial Technology rounds out the segment with condition monitoring systems, non-destructive inspection equipment, pumps, valves, and gears. Some of these businesses are being actively evaluated for strategic fit. In February 2026, reports emerged that Baker Hughes was exploring the sale of its Waygate Technologies unit—which makes industrial CT scanners, radiographic testing systems, and remote visual inspection equipment—for approximately $1.5 billion, part of Simonelli's ongoing portfolio optimization.

The numbers tell the story of IET's trajectory. In the third quarter of 2025, IET orders reached $4.14 billion—up 44 percent year-over-year—driven by a doubling of Gas Technology Equipment orders as major LNG projects including Rio Grande and Port Arthur moved forward. IET backlog reached a record $32.1 billion by quarter's end. For full-year 2025, IET orders hit a record $14.9 billion. Baker Hughes has set an ambitious target of $40 billion in cumulative IET orders over the three-year period from 2026 to 2028.

Perhaps most striking is the revenue mix shift. IET represented approximately 52 percent of company revenue in the fourth quarter of 2025, and Baker Hughes expects IET to exceed 55 percent of the total by 2028. For a company that was a pure oilfield services player just eight years ago, this represents a profound transformation.

X. Technology Leadership & Innovation

From CO2 Problem to CO2 Business

One of the most compelling aspects of Baker Hughes' technology strategy is how it turns environmental challenges into commercial opportunities. CarbonEdge, launched in September 2024, exemplifies this approach. Powered by the company's Cordant digital platform, CarbonEdge is designed as an end-to-end monitoring and optimization system for carbon capture operations.

To understand why this matters, consider the challenge facing any CCUS project. Carbon capture is not a single technology—it is a chain of processes: capturing CO2 from industrial exhaust, compressing it, transporting it via pipeline, and injecting it deep underground for permanent storage. Each link in the chain involves different equipment, different operators, and different risks. A leak in a CO2 pipeline, an underperforming capture unit, or unexpected behavior in a geological storage formation can all derail a project.

CarbonEdge provides real-time data and alerts across this entire chain—from capture facility to subsurface reservoir. Its launch customer, Wabash Valley Resources, uses it to monitor CO2 volumes at a facility in Indiana. For an industry that is still in its early stages and where regulatory confidence depends on demonstrable safety and reliability, having a single digital platform that spans the full CCUS value chain is a significant competitive advantage.

Hydrogen: A Century of Compression Experience

Baker Hughes' hydrogen strategy builds on what may be the company's most underappreciated asset: more than a century of experience in hydrogen compression. The company built its first hydrogen reciprocating compressor in 1915—a fact that tends to surprise people who think of hydrogen as a futuristic technology. Hydrogen has been used in oil refining and chemical manufacturing for over a hundred years; what is new is the ambition to use it as a clean energy carrier at scale.

The company's current hydrogen technology portfolio spans three generations of high-pressure ratio centrifugal compressors designed specifically for hydrogen, which behaves differently from natural gas in compression systems due to its low molecular weight and tendency to embrittle steel. Baker Hughes is also pursuing electrolyzer technology—the devices that use electricity to split water into hydrogen and oxygen—including solid oxide and alkaline exchange membrane designs.

The pending acquisition of Chart Industries, announced in July 2025 for $13.6 billion, adds another critical dimension. Chart is a leading manufacturer of cryogenic equipment—the ultra-cold storage tanks, heat exchangers, and liquefaction systems needed to handle hydrogen and LNG in their liquid states. The deal, which is expected to close in mid-2026, would give Baker Hughes end-to-end capability across the hydrogen and LNG value chains, from production through compression, liquefaction, storage, and transport.

Geothermal: Drilling for Heat Instead of Oil

Baker Hughes' geothermal ambitions represent perhaps the most elegant strategic pivot in the company's portfolio. The core insight is simple: the same drilling technology, completions expertise, and subsurface knowledge used to extract oil and gas can be applied to extract heat from the earth. Geothermal energy is baseload—meaning it produces power 24 hours a day regardless of weather—making it a natural complement to intermittent renewables like wind and solar.

The Wells2Watts consortium commissioned its first closed-loop test facility in October 2023 and has begun planning a field pilot with California Resources Corporation near Bakersfield—a site chosen because existing well infrastructure and accessible geothermal heat resources reduce the capital required for testing.

Beyond Wells2Watts, Baker Hughes signed agreements in 2025 with Fervo Energy for the Cape Station project in Utah—100 megawatts of baseload geothermal power in Phase I, coming online in 2026, with an additional 400 megawatts in Phase II by 2028. It also partnered with Controlled Thermal Resources for 500 megawatts of geothermal development in California. These are not pilot projects—they represent commercial-scale deployments that leverage Baker Hughes' OFSE drilling expertise and IET power generation equipment in combination.

Digital Transformation and AI

On the digital front, Baker Hughes has developed two primary platforms. Leucipa is a cloud-based automated field production system that uses data analytics and automation to optimize oil and gas production. Customer results include production increases of up to 14 percent, 75 percent efficiency gains in engineering time, and an annualized incremental margin of $6 million across 4,000 wells for one North American operator. Cordant is a broader industrial asset performance management platform that integrates data from Baker Hughes' sensors, valves, pumps, and inspection equipment to optimize industrial operations.

The company invested $643 million in R&D in 2024 and acquired more than 1,600 patents that year—a level of innovation investment that underscores the shift from services company to technology company.

XI. Market Position & Competitive Dynamics

The Competitive Landscape

Baker Hughes occupies a unique position in the energy industry. Among the Big Three oilfield services companies, SLB remains the largest with $35.7 billion in 2025 revenue, followed by Baker Hughes at $27.7 billion and Halliburton at $22.2 billion. Further out, TechnipFMC ($9.8 billion), NOV ($8.7 billion), and Weatherford ($4.9 billion) compete in specialized niches.

But revenue rankings only tell part of the story. Each of the Big Three has developed a distinct strategic identity. SLB has positioned itself as the digital and deepwater technology leader, with a New Energy division targeting $3 billion in revenue by decade's end and a JV with Aker Carbon Capture (SLB Capturi) for CCUS. Halliburton has doubled down on its dominance in North American completions and hydraulic fracturing—a strategy that has made it most sensitive to U.S. shale activity but also most efficient in that arena. Halliburton's net income fell 48.7 percent in 2025 as U.S. drilling softened, illustrating the risk concentration.

Baker Hughes has chosen a different path entirely: the two-engine model that combines oilfield services with industrial and energy technology. No other oilfield services peer has anything comparable to the IET segment. This is not a minor point—it fundamentally changes the company's earnings profile, customer base, and growth trajectory.

The Energy Services Trilemma

Baker Hughes is effectively playing a three-dimensional chess game. Dimension one is traditional oil and gas services, where it must compete effectively with SLB and Halliburton to maintain market share and generate cash. Dimension two is industrial energy technology—LNG equipment, gas turbines, compression—where its competitors are not oilfield services companies but industrial giants like Siemens Energy and Mitsubishi Heavy Industries. Dimension three is the energy transition—hydrogen, CCUS, geothermal—where the competitive landscape is still forming and the winners have not yet been decided.

The geographic footprint supports this multi-dimensional strategy. Baker Hughes operates in over 120 countries, with three-quarters of its OFSE revenue coming from international markets. Its IET business serves customers across the LNG, petrochemical, power generation, and industrial sectors globally—a customer base that extends well beyond the oil and gas operators that SLB and Halliburton primarily serve.

The AI Data Center Wild Card

An unexpected growth vector emerged in 2024 and accelerated through 2025: powering data centers for artificial intelligence. The explosion of AI training and inference has created insatiable demand for electricity, and Baker Hughes' NovaLT gas turbines have proven well-suited for providing reliable, dispatchable power to data center campuses. The company booked $2.5 billion in power systems orders in 2025, of which roughly $1 billion was specifically tied to data center applications.

This is a market that barely existed for Baker Hughes three years ago. In February 2026, the company received an order for 25 generators from BRUSH Power Generation to support 1.3 gigawatts of onsite power capacity for Boom Supersonic's AI data center operations, with deliveries running from mid-2026 through 2028. Baker Hughes has set a target of $3 billion in cumulative data center orders between 2025 and 2027.

The data center opportunity illustrates why the GE heritage matters so much. Without the gas turbine technology that came through the GE Oil & Gas merger, Baker Hughes would have no way to participate in this market. The turbines were designed for LNG plants and pipeline compression, but they turn out to be equally useful for generating the kind of reliable, high-density power that AI data centers require—power that must be available 24/7, cannot tolerate interruption, and needs to scale quickly in increments that match the modular buildout of data center campuses. Gas turbines fit these requirements better than almost any other power source: they can be ordered, manufactured, and installed in months rather than years; they produce predictable, dispatchable power without depending on weather; and they can eventually be paired with carbon capture to reduce their environmental footprint.

Sometimes the most valuable assets are the ones you did not know you needed. Jeff Immelt may have gotten the strategy wrong at GE, but the industrial assets he married to Baker Hughes are now generating revenue streams that nobody predicted when the deal closed in 2017.

XII. Playbook: Business & Investing Lessons

The Power of Crisis-Driven Transformation

Baker Hughes' history offers a masterclass in how crisis creates opportunity—if leadership is willing to seize it. The $3.5 billion Halliburton breakup fee, which could have been viewed as a consolation prize, instead became the financial foundation for a GE merger that fundamentally changed the company. The GE marriage itself, which was widely viewed as a distraction when GE began divesting, became the source of the industrial technology assets that now drive Baker Hughes' growth. At every inflection point, the company's trajectory was shaped more by what happened after the crisis than by the crisis itself.

Managing Complex Mergers

Few companies have experienced more mergers, acquisitions, divestitures, and restructurings than Baker Hughes. The lessons are instructive. First, the 1987 Baker-Hughes merger shows that even hostile combinations can create lasting value if the underlying strategic logic is sound. Second, the BJ Services saga—bought, sold, bought again, sold again, bankrupt—demonstrates the cost of strategic inconsistency. Third, the GE partnership illustrates that sometimes the most valuable mergers are the ones where you keep the assets and let the partner walk away.

Portfolio Management in Cyclical Industries

Simonelli's approach to portfolio management deserves particular attention. Rather than trying to be all things to all customers, he has systematically evaluated each business within Baker Hughes for its strategic fit, growth potential, and margin profile. Businesses that do not meet the bar—like the surface pressure control unit sold to Cactus, the Precision Sensors & Instrumentation line sold to Crane Company, and potentially the Waygate Technologies unit—are divested to fund investments in higher-growth areas. The pending $13.6 billion acquisition of Chart Industries is the boldest expression of this strategy: selling lower-growth assets while making a transformative bet on the LNG and hydrogen value chains.

The Role of Visionary Leadership

Baker Hughes' transformation would not have happened without a leader who understood both the oilfield services world and the industrial technology world. Simonelli's career trajectory—from GE's Financial Management Program through GE Transportation and GE Oil & Gas to Baker Hughes CEO—gave him a perspective that no traditional oilfield services executive could have had. He understood that the future of energy was not about choosing between hydrocarbons and clean energy, but about building technology that could serve both.

XIII. Analysis: Bear vs. Bull Case

Through the Lens of Porter's Five Forces

The oilfield services industry presents a mixed picture through the Porter framework. The threat of new entrants is low—the capital requirements, technological complexity, and decades of accumulated IP create formidable barriers. Baker Hughes alone acquired 1,600 patents in a single year. Buyer power is moderate to high and rising, as upstream M&A consolidation (approximately $206.6 billion in 2024 alone) concentrates the customer base into fewer, more powerful operators. Supplier power is moderate—the Big Three have sufficient scale to negotiate with input providers, but specialized materials and components can create bottlenecks.

Competitive rivalry is intense among the Big Three and second-tier players, particularly in traditional oilfield services where price competition can be fierce during downturns. The threat of substitutes is the most nuanced force—renewables threaten the long-term demand for the hydrocarbons that OFS companies help produce, but companies like Baker Hughes that pivot toward energy technology can ride the substitution wave rather than be overwhelmed by it.

Hamilton Helmer's Seven Powers

Applying Helmer's framework reveals where Baker Hughes' competitive advantages truly lie.

Counter-positioning is arguably Baker Hughes' most powerful strategic asset. The IET platform—LNG turbomachinery, compression, climate technology—has no direct parallel at SLB or Halliburton. Competitors would need to fundamentally restructure their businesses or make massive acquisitions to replicate it. But doing so would cannibalize their core OFS-centric identity and alienate their existing investor base. This "damned if you do, damned if you don't" dynamic is classic counter-positioning—Baker Hughes has made a strategic bet that incumbents cannot easily match without disrupting themselves.

Switching costs are formidable in the IET business. LNG turbines and compression systems are installed for 20-to-30-year project lifespans. Once Baker Hughes equipment is operating in a customer's facility, the relationship is locked in through long-term service agreements—typically running seven to ten years—that cover maintenance, spare parts, and field engineering. The $32.4 billion IET backlog at year-end 2025 represents contractually committed future revenue that competitors cannot easily displace.

Cornered resource is the third meaningful power. The GE-heritage turbomachinery technology, particularly the LM9000 aeroderivative turbine platform derived from jet engine technology, represents a technological base that cannot easily be replicated. The pending Chart Industries acquisition adds another cornered resource—cryogenic equipment technology for hydrogen and LNG that only a handful of companies in the world possess.

Scale economies are moderate—Baker Hughes has manufacturing scale in LNG turbomachinery but is the third-largest OFS company by revenue. Network economies are weak, as OFS is not a network-effects business. Branding and process power are present but not dominant competitive advantages.

Bull Case

The bull case rests on Baker Hughes' differentiated positioning in the energy transition. The IET segment provides exposure to structural growth in LNG infrastructure, data center power generation, hydrogen, and CCUS—markets that are driven by long-term trends rather than the short-cycle drilling activity that whipsaws traditional oilfield services companies. The record IET backlog of $32.4 billion provides multi-year revenue visibility. The Chart Industries acquisition, if successfully integrated, would create an end-to-end platform across the LNG and hydrogen value chains with $325 million in expected annual cost synergies. The company's first-mover advantages in several clean energy technologies—CarbonEdge for CCUS, Wells2Watts for geothermal, fuel-flexible turbines for hydrogen—could compound as these markets scale.

Baker Hughes has also demonstrated margin discipline. Adjusted EBITDA reached a record $4.825 billion in 2025, up 5 percent year-over-year despite flat revenue. Free cash flow hit a record $2.732 billion. The IET EBITDA margin reached 20 percent in the fourth quarter of 2025—and the trajectory is toward further expansion as the higher-margin services portion of IET grows relative to equipment sales.

Bear Case

The bear case starts with the cyclicality risk that haunts every energy company. Baker Hughes expects global upstream spending to decline at a low single-digit rate in 2026, with North America falling at a mid-single-digit pace. OFSE, which still generates roughly 40 percent of EBITDA, is directly exposed to this softness. International OFSE revenue fell 11 percent year-over-year in the third quarter of 2025, with particularly sharp declines in Europe and the CIS region.

There is meaningful execution risk around the $13.6 billion Chart Industries acquisition. Large industrial acquisitions are notoriously difficult to integrate, and Chart was the target of a contested bidding process (Baker Hughes outbid a previously announced merger-of-equals between Chart and Flowserve). The deal has not yet closed, and the integration will require careful management to achieve the promised synergies without disrupting either business.

Competition in Baker Hughes' growth markets is intensifying. SLB's Capturi joint venture with Aker Carbon Capture may have a head start in CCUS capture technology. Siemens Energy and Mitsubishi Heavy Industries are formidable competitors in large-frame gas turbines and hydrogen technology. Policy risk looms large—much of the economic case for hydrogen, CCUS, and other clean energy technologies depends on government incentives like the U.S. Inflation Reduction Act and the EU Green Deal, which face political uncertainty.

The company also faces tariff headwinds, having estimated a $100 million to $200 million impact on adjusted EBITDA at current tariff levels—a manageable but real drag on profitability that will require ongoing mitigation through supply chain diversification and domestic sourcing.

Finally, in November 2025, activist investor Ananym Capital took a position and began pushing for a spin-off of OFSE, arguing it would unlock 51 percent share price upside because the two segments have "different natural investors." This argument has some merit—OFSE is a cyclical services business that appeals to value and energy investors, while IET is a growth-oriented industrial technology business that might attract industrial and technology-focused funds. A conglomerate discount may be suppressing Baker Hughes' valuation if the market cannot properly price the two businesses as a unit.

But the counter-argument is equally compelling. The cross-segment synergies between OFSE and IET—using drilling expertise for geothermal and CCUS wells, combining subsurface knowledge with surface equipment for integrated energy solutions—are precisely what makes Baker Hughes different from every other company in the energy services space. Separating the businesses might unlock short-term value but could destroy the strategic differentiation that underpins the company's long-term growth thesis. Whether holding them together creates more value than separating them is a question that Baker Hughes' leadership will need to answer definitively over the coming years.

Key Metrics to Watch

For investors tracking Baker Hughes, two metrics stand above all others.

First, IET orders and the book-to-bill ratio. IET orders are the leading indicator of future revenue—every LNG project, data center contract, and hydrogen compression deal flows through this line item. A book-to-bill ratio above 1.0 means the backlog is growing, de-risking future revenue and providing the long-duration visibility that makes IET so valuable. Full-year 2025 IET orders of $14.9 billion against guidance of $13.5 billion to $15.5 billion for 2026 provide the benchmark.

Second, the IET revenue mix as a percentage of total company revenue. This is the single best measure of Baker Hughes' transformation from oilfield services company to energy technology company. IET represented 52 percent of revenue in the fourth quarter of 2025, trending toward 55 percent or higher by 2028. If this ratio continues climbing while IET margins expand—the 20 percent EBITDA margin achieved in Q4 2025 is the benchmark—it validates the strategic thesis that Baker Hughes is building a structurally higher-margin, less cyclical business.

XIV. Epilogue & Future Outlook

The Road Ahead

Baker Hughes enters 2026 in a stronger position than at any point in its history. The company guided for $27.25 billion in revenue and approximately $4.85 billion in adjusted EBITDA—essentially flat on the top line but continuing to expand margins through mix shift toward IET and operational efficiency. The Chart Industries acquisition, if it closes as expected in mid-2026, would be immediately accretive and marks the largest strategic bet in Simonelli's tenure.

The geopolitical landscape remains complex. Baker Hughes described itself as "vigilant but calm" regarding global tensions, maintaining operations across more than 120 countries while navigating trade barriers, sanctions regimes, and shifting alliance structures. The company's co-headquarters model—Houston and London—reflects an intentionally global posture that provides flexibility as the geopolitical winds shift.

The technology breakthroughs on the horizon are genuinely exciting. Enhanced geothermal systems—drilling deep into hot rock formations and circulating fluid to harvest energy—could unlock baseload clean power at massive scale. Hydrogen as an industrial fuel and energy carrier is moving from pilot projects to commercial deployment. Carbon capture is transitioning from a cost center to a revenue-generating business as carbon pricing mechanisms expand globally. And the entirely unexpected AI data center power opportunity is just beginning—Baker Hughes' target of $3 billion in data center orders through 2027 may prove conservative if AI infrastructure buildout continues at its current pace.

Baker Hughes' stock has reflected the market's growing confidence in this transformation. After returning 24 percent in 2024 and nearly 10 percent in 2025, shares surged more than 37 percent in the first two months of 2026 alone, hitting a 52-week high above $65 in late February—outperforming even the major technology companies that dominate market headlines. The analyst consensus stands at 27 Buy ratings against just 2 Holds and zero Sells, with an average price target of $62.62. The market is pricing in a company that is more than the sum of its parts.

The key question for the next five years is whether Baker Hughes can successfully manage three transitions simultaneously: shifting its revenue mix toward IET, integrating Chart Industries, and building commercial-scale businesses in hydrogen, CCUS, and geothermal—all while maintaining the profitability and cash generation of its traditional OFSE business. The track record suggests it can. The company has navigated more complex transformations than most—from the contentious 1987 merger through the BJ Services saga, the FCPA scandal, the failed Halliburton deal, and the GE partnership—and has emerged from each stronger.

What Reuben Baker and Howard Hughes Sr. started more than a century ago with a casing shoe and a rock-eating drill bit has evolved into something neither could have imagined: an energy technology company with $32 billion in committed future orders, turbines powering AI data centers, compression systems moving hydrogen across continents, and technology turning abandoned wells into geothermal power plants. The transformation is far from complete. But the direction of travel is clear.

XV. Recent News

Baker Hughes' most recent quarterly results, reported in late January 2026, showed fourth-quarter revenue of $7.4 billion and adjusted EBITDA of $1.337 billion. For the full year, the company generated record adjusted EBITDA of $4.825 billion and record free cash flow of $2.732 billion on revenue of $27.7 billion. Full-year IET orders reached a record $14.9 billion, with the IET backlog climbing to $32.4 billion.

In the first quarter of 2025, Climate Technology Solutions revenue had surged 114 percent year-over-year—a sign that the energy transition business is approaching meaningful scale. By the third quarter, IET orders of $4.14 billion represented a 44 percent year-over-year increase, driven by Gas Technology Equipment orders that doubled as major LNG projects advanced.

The Chart Industries acquisition, announced in July 2025 at $210 per share for a total enterprise value of $13.6 billion, received shareholder approval in October and remains on track to close in mid-2026. The deal is expected to be double-digit EPS accretive in its first full year and deliver $325 million in annual cost synergies by year three.

In January 2026, Baker Hughes closed its joint venture with Cactus for surface pressure control, receiving $344.5 million for a 65 percent stake while retaining 35 percent. That same month, it completed the sale of its Precision Sensors & Instrumentation product line to Crane Company.

In February 2026, the company signed a multi-year agreement with Marathon Petroleum—the largest U.S. refiner—to be its preferred provider of hydrocarbon treatment products across 12 refineries and 2 renewable fuel facilities. Also in February, it secured a contract to supply 25 generators supporting 1.3 gigawatts of data center power capacity for Boom Supersonic. Reports emerged that Baker Hughes was exploring the sale of its Waygate Technologies unit for approximately $1.5 billion.

CFO Ahmed Moghal, who joined in February 2025, guided for 2026 revenue of $27.25 billion, adjusted EBITDA of approximately $4.85 billion, and an effective tax rate of 22 to 26 percent. The company also announced a dividend increase from $0.21 to $0.23 per share and continued share repurchases.

Activist investor Ananym Capital, which took a position in November 2025, has publicly advocated for a spin-off of the OFSE segment, arguing it would unlock significant shareholder value by separating two businesses with fundamentally different growth profiles and investor bases. Management has not publicly responded to the proposal.

XVI. Links & Resources

Company Materials - Baker Hughes Investor Relations: investors.bakerhughes.com - Baker Hughes Annual Report and 10-K filings (SEC EDGAR) - Baker Hughes Corporate Sustainability Report (2023) - Baker Hughes Annual Meeting 2026 materials: bakerhughes.com/am-2026

Historical Archives - Texas State Historical Association: "Baker Hughes" entry (tshaonline.org) - American Oil & Gas Historical Society: "Carl Baker and Howard Hughes" (aoghs.org) - FundingUniverse: Baker Hughes Incorporated Company History - Encyclopedia.com: Baker Hughes Inc company profile

Industry Reports - The Business Research Company: Oilfield Services Global Market Report - IEA World Energy Outlook (latest edition) - Rystad Energy: Global Oilfield Services Market Analysis

Regulatory Filings - DOJ: Halliburton/Baker Hughes merger opposition (April 2016) - DOJ: Baker Hughes FCPA settlement (April 2007) - SEC: Baker Hughes proxy statements and 10-K filings

Leadership Profiles - Lorenzo Simonelli biography: bakerhughes.com/lorenzo-simonelli - Rice Business faculty page: Lorenzo Simonelli - Hart Energy: "GE Shake-up Puts Youngest Leader at Helm of Fast-Growing Oil & Gas Unit"

Technology Deep Dives - Baker Hughes: CarbonEdge digital CCUS solution - Baker Hughes: Wells2Watts geothermal consortium - Baker Hughes: Hydrogen Technologies portfolio - Baker Hughes: Cordant and Leucipa digital platforms

Analysis and Commentary - CNBC: Ananym Capital activist push for OFSE spin-off (November 2025) - Bloomberg: Waygate Technologies potential divestiture (February 2026) - Fortune: Chart Industries acquisition analysis (July 2025)

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube