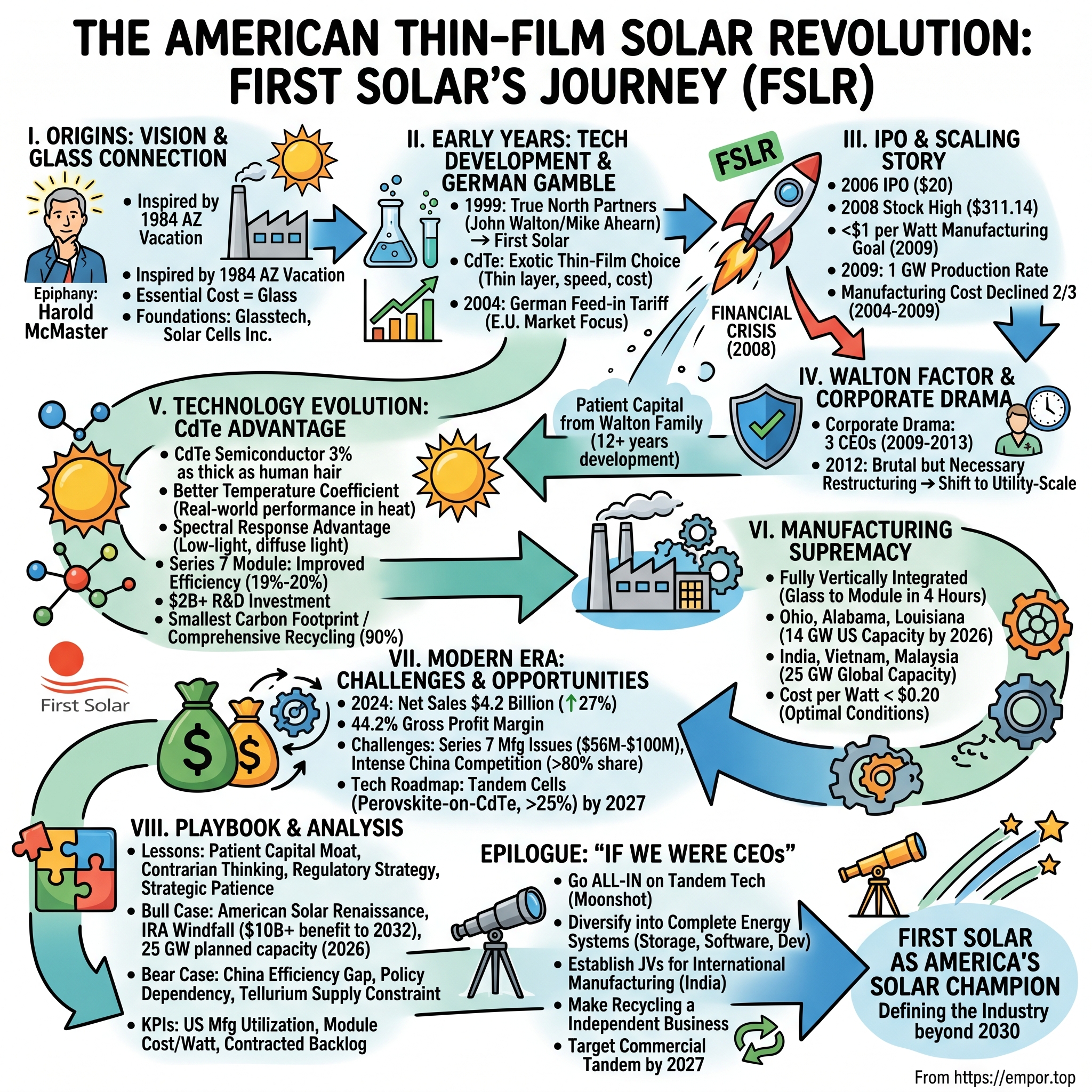

First Solar: The American Thin-Film Solar Revolution

I. Introduction & Episode Roadmap

Picture a gleaming factory floor in Perrysburg, Ohio, where sheets of ordinary glass enter one end of a production line and emerge four hours later as sophisticated solar panels. No imported silicon wafers. No Chinese supply chains. Just American manufacturing transforming sand into energy independence. This is First Solar's revolution—a company that zigged when the entire solar industry zagged, betting on an exotic cadmium telluride technology that everyone else had written off as impossible to scale.

Founded in 1984 by glass industry legend Harold McMaster, who began with Glasstech Solar before pivoting to cadmium telluride and founding Solar Cells, Inc. in 1990, First Solar represents one of the most audacious bets in American industrial history. While the rest of the solar world chased ever-cheaper crystalline silicon panels from Asia, this Toledo-born company pursued a radically different path—one that would take them from near bankruptcy to becoming a $4.21 billion revenue powerhouse in 2024, America's sole large-scale solar manufacturer independent of Chinese supply chains.

The journey from Harold McMaster's glass laboratory to dominating utility-scale solar in America is a masterclass in contrarian thinking. It's the story of how patient capital from the Walton family sustained losses for over a decade before the technology clicked. How a company survived the 2008 financial crisis that decimated the solar industry. How they navigated the European subsidy collapse that killed dozens of competitors. And ultimately, how they positioned themselves to become the biggest beneficiary of the Inflation Reduction Act's $1 trillion environmental spending in 2022.

Today, First Solar stands alone among Western solar manufacturers. They're not just surviving—they're thriving with $4.2 billion in 2024 revenue, up from $3.3 billion the prior year, driven primarily by higher module sales volumes. Their thin-film panels grace vast solar farms across America's deserts, their factories hum with expansion plans, and their technology roadmap promises efficiencies that seemed impossible just years ago. This is the story of how betting against conventional wisdom, paired with relentless innovation and strategic patience, built America's answer to solar dominance.

We'll explore three critical phases: the technology gamble that nearly failed, the strategic pivots that saved the company, and the current renaissance driven by American industrial policy. Along the way, we'll unpack the lessons for investors, entrepreneurs, and anyone interested in how deep technology companies navigate the valley of death to emerge as category definers.

II. Origins: Harold McMaster's Vision & The Glass Connection

The blazing Arizona sun in 1984 did more than just beat down on Harold McMaster during his vacation—it sparked an epiphany that would reshape American solar manufacturing. Inspired by that sunny Arizona vacation, McMaster founded Glasstech Solar in 1984, with the insight that the essential cost element of large area solar arrays was glass, and he could treat the actual solar cell as simply a different kind of coating on glass. This wasn't McMaster's first dance with revolutionary glass technology. Having sold his previous company, Glasstech, in 1987 for $100 million after essentially creating the market for tempered glass, McMaster understood glass at a molecular level that few others could match.

McMaster's journey to solar began decades earlier. Following his graduation from Ohio State with a combined master's degree in physics, mathematics, and astronomy in 1939, McMaster worked as the first research physicist ever employed by the Libbey Owens Ford Glass in Toledo, Ohio. His inventive mind had been evident since childhood—his father gave him a set of tools at age 6, and by 8, he had built a set of farm machinery, by 10, a threshing machine that husked corn, and by 12 he was making car motors. This hands-on engineering brilliance would prove crucial in tackling solar's manufacturing challenges.

The initial Glasstech Solar venture burned through investor money with little to show. After doing little except absorbing $12 million in cash over five years working with amorphous silicon to little effect, McMaster gave up on the amorphous silicon research and offered to pay back the 57 investors who followed him into solar cells. But McMaster wasn't finished. In a move that would define entrepreneurial persistence, Glasstech Solar was reincarnated as Solar Cells Inc. in 1990, and McMaster offered to pay back any investors who wanted out, then raised another $15 million—$2 million of which was his own—to start again with cadmium telluride.

The choice of cadmium telluride (CdTe) over silicon was revolutionary and risky. While the entire solar industry was perfecting crystalline silicon technology, McMaster saw an opportunity in thin-film technology that others had dismissed. His vision was audacious: coat ordinary glass with a semiconductor layer thinner than a human hair and produce solar panels at speeds and costs that silicon could never match. By fall 1997, SCI's scientists had a eureka moment when they perfected a technique that allowed them to coat one two-foot-by-four-foot panel every 30 seconds—while competitors like BP Solar required six hours to coat a similar sized panel.

The technology showed promise, but Solar Cells Inc. needed more than just technical breakthroughs—it needed patient capital and strategic vision. Enter John Walton, son of Walmart founder Sam Walton, whose investment philosophy would prove perfectly matched to the long development timeline of breakthrough technology. In 1999, John Walton and Mike Ahearn formed True North Partners with $43 million in capital, which purchased Solar Cells Inc. and spawned First Solar, developing the semiconductor technology that promised to drive down the cost of manufacturing solar panels.

The transformation from Solar Cells Inc. to First Solar marked more than just a name change—it represented a fundamental shift in ambition and scale. Mike Ahearn, a lawyer specializing in startups who became Walton's venture capital partner, brought disciplined business acumen to McMaster's technical genius. Together with Walton's patient capital, they created the conditions for one of the longest and most expensive technology development programs in solar history.

III. Early Years: Technology Development & The German Gamble

Mike Ahearn co-founded First Solar in 1999, led as CEO from 2000-2009, and had previously worked as an attorney specializing in start-ups before forming True North Partners with John Walton. Taking the helm of a company with revolutionary technology but no clear path to profitability, Ahearn faced a daunting challenge: transform McMaster's laboratory breakthrough into a commercially viable manufacturing process that could compete with established silicon solar panels.

The early 2000s were a crucible for First Solar. The company's Perrysburg, Ohio facility became a testing ground for scaling up the CdTe deposition process. Commercial operations started in January 2002 with a 25-megawatt base plant, which began high-volume production a couple of years later. The manufacturing process they developed was unlike anything in the solar industry—transforming glass into solar panels in just two and a half hours, about a tenth the time it took for silicon equivalents.

But technical success didn't guarantee commercial viability. The U.S. market showed little interest in solar energy in the early 2000s, with inconsistent government support and no clear economic case for adoption. Ahearn and his team faced a critical decision: continue burning cash hoping for U.S. policy changes, or look abroad for markets that valued solar energy. The answer came from an unexpected source—Germany's revolutionary feed-in tariff system.

Germany's system fixed solar energy rates for 20 years, turning solar from just 'green' technology into an attractive, income-producing investment, like an annuity. This policy transformation created the world's first truly commercial solar market, and First Solar seized the opportunity with both hands. In 2004 Germany began the first solar feed-in program, where utilities were required to purchase electricity from customers producing solar power at a rate set by national law for 20 years, creating a large and stable market that First Solar decided to enter.

The German gamble paid off spectacularly. Early sales were primarily in Germany because of strong incentives for solar enacted in the German Renewable Energy Sources Act of 2000, with 86% of First Solar's net sales in 2009 generated from customers headquartered in the European Union. The company wasn't just selling panels—they were building massive utility-scale installations across Europe. By focusing on large ground-mounted systems rather than rooftop installations, First Solar could leverage their panels' unique advantages: superior performance in hot climates, better low-light response, and most importantly, dramatically lower costs per watt.

The path to manufacturing excellence wasn't smooth. Engineers in Perrysburg worked around the clock to optimize the deposition process, improve module efficiency, and reduce defects. Every percentage point improvement in efficiency meant millions in additional revenue. Every second shaved off the production line meant lower costs. The company was engaged in a race against time—they needed to achieve cost parity with fossil fuels before European subsidies inevitably declined.

Meanwhile, Ahearn was building more than just manufacturing capacity—he was creating a vertically integrated powerhouse. First Solar didn't just make panels; they developed entire solar farms, managed installations, and even created recycling programs for end-of-life modules. This comprehensive approach set them apart from Chinese competitors who focused solely on manufacturing. First Solar was the first solar PV company to establish and run its own PV module recycling program, collecting used modules from owners and transporting them to facilities for recycling.

The efficiency improvements came steadily. According to the company, efficiency levels reached 10.8% in Q4 2008, further testament to First Solar's continuous productivity improvement programmes during a period of rapid capacity expansion. While these numbers might seem modest compared to silicon panels, First Solar's modules had a secret weapon: they maintained their efficiency in real-world conditions where silicon panels struggled.

IV. The IPO & Scaling Story

On November 17, 2006, First Solar went public on NASDAQ under ticker FSLR with an initial public offering of 20,000,000 shares at $20 per share, including 6,750,000 shares sold by certain stockholders. The timing seemed perfect—solar energy was gaining momentum globally, oil prices were climbing toward historic highs, and climate change was entering mainstream consciousness. But few could have predicted the rocket ship trajectory that followed.

Within eighteen months of the IPO, First Solar's stock price experienced one of the most spectacular rises in clean energy history. The stock reached an all-time high of $311.14 on May 16, 2008, a fifteen-fold increase from its IPO price. The market was valuing First Solar not just as a solar manufacturer, but as the potential winner of the entire renewable energy revolution. Investment banks initiated coverage with breathless reports about the coming solar age. Retail investors poured in, seeing First Solar as the "next big thing" in technology.

Behind the soaring stock price was genuine operational excellence. By the end of 2009, First Solar had surpassed an energy power production rate of 1 GW and became the largest producer of PV cells in the world, while also becoming the first solar panel manufacturing company to lower its manufacturing cost to $1 per watt. This $1-per-watt milestone was revolutionary—it meant solar energy was approaching cost competitiveness with traditional electricity generation in many markets.

The manufacturing expansion during this period was breathtaking. Since 2002, the company replicated its manufacturing line at the Ohio site, built four more lines in Germany, and began constructing a fourth plant in Malaysia with 16 production lines. Each new factory represented not just additional capacity but improved efficiency and lower costs through economies of scale and manufacturing innovation.

From 2004 through 2009, First Solar's manufacturing costs declined two-thirds from over $3 per watt to less than $1 per watt. This wasn't incremental improvement—it was a complete transformation of solar economics. The company's proprietary manufacturing process, which could transform a sheet of glass into a functioning solar module in under four hours, gave them a structural cost advantage that crystalline silicon manufacturers couldn't match.

Then came the financial crisis. FSLR stock fell 72.0% from its high of $311.14 on May 16, 2008 to $87.23 on November 20, 2008, versus a peak-to-trough decline of 56.8% for the S&P 500. The entire solar industry was thrown into chaos. Credit markets froze, making it nearly impossible to finance new solar projects. European governments, facing budget crises, began cutting the generous feed-in tariffs that had driven First Solar's growth.

Yet First Solar didn't just survive—they used the crisis to strengthen their competitive position. While competitors laid off workers and canceled expansion plans, First Solar continued investing in R&D and manufacturing efficiency. They had something others lacked: patient capital from the Walton family and a balance sheet strong enough to weather the storm. John Walton stuck with them for 12 years before the first manufacturing line even became operational, unlike Silicon Valley venture capitalists who generally expect a return on investment within 5 years.

The financial crisis also accelerated a crucial strategic shift. Recognizing that European subsidies were unsustainable, First Solar began pivoting toward utility-scale projects in the United States. They weren't just selling panels anymore—they were becoming full-service solar developers, designing, building, and sometimes operating massive solar farms. This vertical integration strategy would prove prescient as the industry evolved from subsidy-dependent to genuinely competitive with fossil fuels.

V. The Walton Factor & Corporate Drama

The death of John Walton in a plane crash on June 27, 2005, just a year before First Solar's IPO, could have derailed the entire enterprise. John Walton never was able to see First Solar fully shine—he died when the experimental aircraft he was piloting near his home in Wyoming crashed, and at his death was known mostly for his advocacy of the charter school movement. Yet his investment philosophy lived on through the Walton family's continued ownership, creating one of the most unusual dynamics in corporate America.

The Walton family continues to hold about 27% of First Solar's stock, a stake worth about $1.4 billion as of 2014, though the actual figure fluctuated dramatically with the company's volatile stock price. This wasn't passive ownership—the Waltons remained deeply engaged in First Solar's strategy, seeing it as more than just an investment but as part of their broader vision for American energy independence and environmental stewardship.

The 2011-2012 period brought corporate drama that tested the company's resilience. As European subsidies collapsed and Chinese manufacturers flooded the market with cheap panels, First Solar's business model came under severe pressure. Between 2009 and 2013, the company was led by three different CEOs: Robert Gillette (2009-2011), Michael Ahearn (Interim CEO, 2011-2012), and James Hughes (2012-2016). This leadership instability reflected deeper strategic uncertainties about First Solar's future direction.

Mike Ahearn's return as interim CEO in 2012 was particularly significant. As co-founder and the architect of First Solar's original strategy, his return signaled that dramatic changes were needed. On April 17, 2012, First Solar announced it would restructure operations worldwide, phasing out operations in Frankfurt, Germany and idling four production lines in Kulim, Malaysia, with approximately 30% of First Solar's workforce laid off as a result.

The restructuring was brutal but necessary. First Solar was transforming from a panel manufacturer dependent on European subsidies to a developer of utility-scale solar projects that could compete without subsidies. Beginning in December 2011, First Solar shifted away from existing markets heavily dependent on government subsidies toward providing utility-scale PV systems in sustainable markets with immediate need, beginning to compete against conventional power generators.

Throughout this turmoil, the Walton family's steady hand proved invaluable. During the lean times when many investors fled, the Waltons remained steadfast, and because First Solar has reliable cash flow, it becomes a takeover target every time its stock dips, but would-be raiders never get very far as the Waltons aren't interested in exiting. This patient capital allowed First Solar to make long-term strategic decisions that public market pressures might have otherwise prevented.

The appointment of James Hughes as CEO in 2012 marked a new phase. Hughes, an energy industry veteran, brought operational discipline and a focus on execution. Under his leadership, First Solar completed its transformation from a module manufacturer to a fully integrated solar solutions provider. The company began winning massive utility-scale projects in the American Southwest, leveraging its panels' superior performance in hot, desert conditions.

On July 1, 2016, Mark Widmar succeeded James Hughes as CEO, having previously served as chief financial officer, while former CEO Mike Ahearn remained chairman of the board. Widmar's appointment represented continuity with change—he understood First Solar's technology and financial position intimately but brought fresh perspective on growth opportunities in the evolving solar market.

VI. Technology Evolution: The CdTe Advantage

The cadmium telluride technology that Harold McMaster bet the company on in 1990 has evolved from a laboratory curiosity into one of the most sophisticated semiconductor manufacturing processes in the world. Unlike the crystalline silicon panels that dominate the global market, First Solar's thin-film approach deposits a layer of CdTe semiconductor just 3% as thick as a human hair onto a glass substrate. This fundamental difference drives everything from manufacturing economics to real-world performance.

The manufacturing process itself reads like science fiction. Utilizing uniquely American technology, First Solar transforms a sheet of glass into a fully functional PV module in about four hours. The process begins with ordinary soda-lime glass entering a sealed production line. Through a series of vapor deposition chambers, multiple semiconductor layers are applied with nanometer precision. Laser scribing creates the electrical circuits. Lamination seals the module. Quality control systems powered by artificial intelligence inspect every square centimeter. When the module emerges four hours later, it's ready to generate electricity for the next thirty years.

The efficiency journey has been remarkable. While First Solar's modules started with single-digit efficiencies in the early 2000s, relentless R&D investment has driven dramatic improvements. Series 7 offers improved module efficiency ranging from 19% to 20%, providing higher energy output per panel, making it ideal for large-scale solar farms demanding the highest possible energy production. These efficiency gains came through breakthrough materials science—replacing copper with arsenic as a dopant, optimizing the buffer layers, and perfecting the crystalline structure of the semiconductor.

But efficiency numbers only tell part of the story. First Solar's modules excel where silicon panels struggle. CdTe thin-film technology has a better temperature coefficient, typically around -0.28% per °C, meaning it loses less energy in hot conditions compared to silicon panels, making them ideal for large-scale solar farms in desert regions where heat would otherwise limit energy production. In the scorching deserts of Arizona or the Middle East, this advantage translates into millions of additional kilowatt-hours over a project's lifetime.

The spectral response advantage is equally important but less understood. First Solar's thin-film modules excel in low-light and diffuse light conditions, with performance superior to traditional crystalline silicon panels, generating more energy during overcast days or in morning and late afternoon when sunlight is less direct. This means First Solar panels start generating electricity earlier in the morning and continue later into the evening, squeezing more energy from each day.

The latest Series 7 modules represent a quantum leap in form factor and installation efficiency. The 1216mm x 2300mm module design optimizes form and function, with added strength and rigidity from galvanized steel back rails, without fear of power loss from cell cracking or other issues prevalent in crystalline silicon modules. These larger modules mean fewer pieces to install, reducing labor costs and installation time—crucial factors in utility-scale deployments where millions of panels must be installed.

Research and development has always been First Solar's lifeblood. The company has invested over $2 billion in R&D throughout its history, maintaining one of the industry's largest research teams. In 2024, First Solar commissioned a new R&D innovation center in Lake Township, Ohio—believed to be the largest facility of its kind in the Western Hemisphere, the 1.3 million square-foot Jim Nolan Center for Solar Innovation dedicated to the late James F. Nolan, architect of the company's CdTe semiconductor platform.

Looking forward, First Solar is pushing the boundaries of what's possible with thin-film technology. The acquisition of Evolar in 2023 for $38 million brought crucial perovskite technology in-house. Perovskite-on-CdTe tandem cells represent the next frontier, potentially pushing efficiencies above 25% while maintaining the cost and performance advantages of thin-film. The company's technology roadmap suggests commercial tandem products could emerge by 2027, potentially revolutionizing solar economics once again.

The environmental advantages of CdTe technology have become increasingly important as sustainability concerns drive purchasing decisions. First Solar's modules have the smallest carbon footprint in the industry, requiring less than one year for energy payback compared to 2-3 years for crystalline silicon. Water usage during manufacturing is 95% lower than silicon production. And unlike silicon panels that often end up in landfills, First Solar operates comprehensive recycling programs that recover 90% of semiconductor materials for reuse in new panels.

VII. Vertical Integration & Manufacturing Supremacy

The thunderous hum of automated machinery fills First Solar's newest facility in Lawrence County, Alabama, where a $1.1 billion investment has created one of the most advanced solar manufacturing plants on Earth. The Lawrence County facility adds 3.5 gigawatts of fully vertically integrated nameplate solar manufacturing capacity, creating over 800 new energy technology manufacturing jobs, bringing First Solar's domestic nameplate capacity to almost 11 GW and global capacity to over 21 GW once fully ramped.

This Alabama facility represents more than just additional capacity—it's a statement about American manufacturing capability. First Solar's cadmium telluride thin-film manufacturing process transforms a sheet of glass into a fully formed solar panel in approximately four hours all under one roof, with the Series 7 modules produced using Alabama-sourced steel fabricated within 25 miles of the facility. Every aspect of production, from semiconductor deposition to final testing, happens within these walls—a stark contrast to the fragmented supply chains that characterize most solar manufacturing.

The vertical integration extends far beyond the factory floor. First Solar controls its supply chain from raw materials to recycling, creating a closed-loop system unique in the solar industry. The company sources its cadmium and tellurium through long-term contracts with mining companies, maintains strategic stockpiles of critical materials, and operates recycling facilities that recover semiconductor materials from end-of-life panels. This comprehensive control insulates First Solar from the supply chain disruptions that regularly roil the solar industry.

The numbers behind the manufacturing expansion are staggering. First Solar is also constructing a $1.1 billion, 3.5 GW facility in Louisiana expected to be commissioned in the second half of 2025, with the company expecting to have over 14 GW of annual nameplate capacity in the United States and 25 GW globally by the end of 2026. This represents over $4 billion in U.S. manufacturing investments, making First Solar the largest solar manufacturer in the Western Hemisphere.

The manufacturing strategy goes beyond simple capacity addition. Each new facility incorporates lessons learned from previous generations, with improvements in automation, quality control, and efficiency. The latest production lines feature advanced robotics that handle glass sheets with microscopic precision, vapor deposition chambers that maintain tolerances measured in nanometers, and AI-powered inspection systems that detect defects invisible to the human eye. The result is a manufacturing process that produces consistent, high-quality modules at speeds that seemed impossible just a decade ago.

Geographic diversification has become increasingly important as geopolitical tensions rise. Beyond the U.S. facilities in Ohio and Alabama, First Solar operates major manufacturing sites in Vietnam and Malaysia, with a new facility in India. The company's manufacturing plant in India added 3.2GW of annual nameplate manufacturing capacity in 2023, all for Series 7 modules, while manufacturing plants from other countries boasted an annual nameplate manufacturing capacity for Series 6 modules of 7.4GW. This global footprint allows First Solar to serve regional markets while maintaining supply chain flexibility.

The operational excellence extends to logistics and delivery. First Solar has developed sophisticated systems for packaging, shipping, and deploying millions of panels annually. Special rail cars designed specifically for solar modules move products from factories to project sites. Advanced planning software optimizes delivery schedules to minimize transportation costs and ensure just-in-time delivery to construction sites. The company even operates mobile quality testing labs that can verify module performance at project sites.

Labor relations and workforce development have been crucial to manufacturing success. A study commissioned by First Solar projects that as the company grows to 14 GW in annual US nameplate capacity by 2026, it will support an estimated 30,060 direct, indirect, and induced jobs across the country, representing $2.8 billion in annual labor income, with every direct job supporting 7.3 jobs nationwide. First Solar has partnered with local community colleges to develop training programs, creating pipelines of skilled workers for advanced manufacturing roles.

The manufacturing supremacy translates directly into competitive advantage. While Chinese manufacturers rely on massive scale and government subsidies to achieve low costs, First Solar's integrated approach and advanced technology deliver superior economics. The company's cost per watt has fallen below $0.20 in optimal conditions, approaching parity with Chinese producers while maintaining higher margins through premium pricing for American-made, forced-labor-free products.

VIII. Policy Plays & The IRA Windfall

The August 16, 2022 signing of the Inflation Reduction Act marked a watershed moment for First Solar, transforming the company from a successful niche player into the crown jewel of American solar manufacturing. The Inflation Reduction Act of 2022 is the most significant climate legislation in U.S. history, offering funding, programs, and incentives to accelerate the transition to a clean energy economy. For First Solar, it was like winning the lottery—except they had spent decades buying the right tickets.

The Act's Section 45X Advanced Manufacturing Production Credit was essentially written with First Solar in mind. Fully integrated domestic solar manufacturers like First Solar can take advantage of tax credits of up to about 16 cents per watt for a solar module manufactured in a U.S. factory. With First Solar producing billions of watts annually, the math becomes staggering. First Solar sold $857 million in 45X tax credits to Visa for $819 million in cash in February 2025, generated from the sale of modules produced in 2024.

The political chess game behind the IRA reveals First Solar's sophisticated approach to policy influence. First Solar executives and lobbyists met at least four times in late 2022 and 2023 with administration officials who oversaw the measure's environmental provisions, while Democratic donors had invested heavily in the company prior to the act being signed into law. This wasn't luck—it was the culmination of years of relationship building and strategic positioning.

The IRA's impact extends far beyond direct manufacturing credits. The domestic content requirements for solar projects seeking maximum tax credits create enormous demand for First Solar's American-made panels. Projects using First Solar modules can qualify for an additional 10% tax credit, making them more economically attractive than projects using imported panels. This regulatory moat is worth billions in additional revenue over the coming decade.

First Solar's strategic response to the IRA has been masterful. Rather than simply pocketing the windfall, they've accelerated investments in new manufacturing capacity, betting that the policy environment will remain favorable. The company aimed to increase its nameplate capacity to over 21GW by the end of 2024, with CEO Mark Widmar adding that the new Louisiana facility is expected to commence commercial operations in late 2025, bringing expected total nameplate capacity to over 25GW by the end of 2026 with 14GW in the US.

The international trade dimension adds another layer of advantage. While the U.S. has imposed various tariffs on Chinese solar panels over the years, enforcement has been inconsistent and circumvention common. The IRA's positive incentives for domestic production prove more effective than punitive tariffs, creating genuine economic advantages for American manufacturing rather than simply raising prices on imports. First Solar benefits from both sides—protection from dumped Chinese panels and subsidies for domestic production.

Environmental and social governance considerations have become increasingly important in solar procurement, and here too First Solar holds aces. In 2024, First Solar communicated an audit had discovered use of forced labor in a Malaysian factory that produces parts for the company. Rather than hiding this discovery, First Solar proactively disclosed it and took corrective action, demonstrating the transparency that differentiates them from Chinese competitors who face ongoing scrutiny over forced labor in Xinjiang.

The state-level policy landscape provides additional tailwinds. California's aggressive renewable energy mandates, Texas's booming electricity demand from data centers, and supportive policies across the Sun Belt create massive domestic demand for solar panels. First Solar's utility-scale focus aligns perfectly with the large projects these policies encourage. State renewable portfolio standards requiring utilities to source specific percentages of power from clean sources ensure steady demand growth regardless of federal policy changes.

Looking beyond the IRA, First Solar has positioned itself to benefit from the broader industrial policy shift in America. The CHIPS Act's emphasis on semiconductor manufacturing, the Infrastructure Act's grid modernization funds, and growing concerns about energy security all reinforce First Solar's strategic position. The company represents exactly what policymakers want: advanced manufacturing jobs in America, reduced dependence on China, and leadership in a critical technology sector.

The durability of these policy advantages remains a key question for investors. While the IRA passed with only Democratic votes, the concentration of clean energy manufacturing investments in Republican states creates bipartisan constituencies for maintaining support. First Solar's new facilities in deep-red Alabama and Louisiana employ thousands of workers who will pressure their representatives to maintain policies supporting domestic solar manufacturing.

IX. Modern Era: Challenges & Opportunities

The year 2024 marked First Solar's emergence as an undisputed American industrial champion, yet success brought its own complex challenges. First Solar's 2024 results show a 27% increase in net sales reaching $4.2 billion, boosted by higher module volume and $115 million in termination payments, with gross profit margins expanding by 5 percentage points to 44.2%. Behind these headline numbers lies a more nuanced story of strategic choices, operational challenges, and calculated bets on the future of American energy.

The manufacturing ramp-up, while impressive, hasn't been without significant growing pains. Manufacturing issues with certain Series 7 modules could cost between $56 million and $100 million. These quality issues, while manageable given First Solar's strong financial position, underscore the challenges of rapidly scaling complex semiconductor manufacturing. Each new production line requires months of fine-tuning to achieve optimal yields, and even small variations in process parameters can impact module performance years down the line.

Global competition has intensified rather than abated despite American policy support. Chinese manufacturers, led by giants like LONGi and JA Solar, continue to push crystalline silicon technology forward with massive R&D investments and economies of scale that dwarf even First Solar's expanded capacity. China has invested tens of billions of dollars to command more than 80 percent of global solar manufacturing capacity, now more than 800 gigawatts and actually gaining share, while U.S. module production capacity is now at just about 11 gigawatts.

The strategic decision to reduce production in certain markets reveals the ongoing challenges of competing globally. Production output of Series 6 modules in Malaysia and Vietnam will decrease by 1 GW in 2025 amid intense competition and unfavorable market conditions. This pullback from international markets represents a focusing of resources on the more profitable and policy-supported American market, but it also potentially cedes ground to Chinese competitors in fast-growing Asian markets.

Customer concentration presents another risk that's often overlooked. Large utility companies and renewable energy developers comprise the bulk of First Solar's customer base. A handful of major customers can account for a significant portion of annual sales. The termination payments received in 2024—while boosting current profits—also highlight the risk of customer changes in strategy or financial distress impacting First Solar's carefully planned production schedules.

The technology roadmap, while promising, requires massive sustained investment. In May 2023, First Solar acquired Evolar, a European company providing perovskite technology, for $38 million. Perovskite tandem cells could revolutionize solar efficiency, but the technology remains unproven at commercial scale. Billions in R&D spending over the coming years will be necessary to maintain technological leadership, with no guarantee of success.

Supply chain vulnerabilities persist despite vertical integration. Tellurium, the critical element in CdTe panels, is primarily a byproduct of copper refining with limited global supply. While First Solar has secured long-term supply agreements and maintains strategic reserves, any disruption in tellurium availability could constrain production growth. The company has invested in research to reduce tellurium usage per watt, but fundamental geological constraints remain.

The data center boom presents both massive opportunity and strategic complexity. According to Bloomberg Intelligence, US-listed solar companies such as First Solar could see revenues approach $40bn by 2026, driven by growth of data centers and emerging technologies. However, serving this market requires not just panels but complete energy solutions, including storage and grid integration capabilities that First Solar currently lacks.

Financial management in this growth phase requires delicate balance. The company's 2025 projection calls for net revenues between $5.3 billion and $5.8 billion with earnings per diluted share between $17 to $20, while capital expenditures are forecast between $1.3 billion to $1.5 billion. This massive capital investment program must be funded while maintaining financial flexibility for opportunistic moves and weathering potential downturns.

The human capital challenge is equally pressing. Scaling from 11 GW to 25 GW of production capacity requires thousands of skilled workers in advanced manufacturing roles. Competition for talent with other high-tech manufacturers, particularly in the semiconductor industry, has intensified. First Solar must build training programs, create career pathways, and maintain competitive compensation while managing margin pressure.

X. Playbook: Business & Investing Lessons

The First Solar story offers a masterclass in building and sustaining competitive advantage in capital-intensive industries. Their journey from Harold McMaster's Toledo laboratory to becoming America's solar manufacturing champion reveals patterns that transcend the solar industry, offering lessons for entrepreneurs, investors, and strategists navigating technology transitions.

Patient Capital as Competitive Moat The Walton family's investment philosophy stands in stark contrast to typical venture capital approaches. The Walton family's willingness to invest for the long term is a significant factor in First Solar's success, first nurturing the company through years of money-losing R&D and then supporting a recent pivot into a whole new line of business building large-scale power projects. This patient capital created a temporal moat—competitors simply couldn't afford to spend a decade perfecting technology without revenue. The lesson extends beyond solar: breakthrough technology requires investors who measure returns in decades, not quarters.

Technology Differentiation in Commodity Markets First Solar's decision to pursue CdTe technology when the entire industry was standardizing on silicon exemplifies successful contrarian thinking. But the key insight wasn't just being different—it was identifying sustainable differentiation. CdTe's advantages (better temperature coefficient, superior low-light performance, lower manufacturing cost) created value in specific applications (utility-scale projects in hot climates) where these benefits commanded premium pricing. The broader lesson: in commodity markets, sustainable differentiation requires both technical superiority and market segments that value that superiority.

Regulatory Capture Through Alignment First Solar's relationship with policy makers represents sophisticated regulatory strategy without crossing into cronyism. By positioning themselves as the solution to policymakers' goals (domestic manufacturing, energy independence, job creation), they shaped policy to their advantage while genuinely delivering public benefits. The IRA didn't just happen to benefit First Solar—the company spent years building relationships and demonstrating why supporting domestic thin-film manufacturing served national interests.

Vertical Integration as Strategic Choice The decision to vertically integrate from raw materials through recycling wasn't driven by simple cost calculations but by strategic imperatives. Control over the entire value chain provided: supply chain security in volatile markets, quality control in precision manufacturing, speed of innovation when technology and process are tightly coupled, and differentiation through capabilities competitors couldn't easily replicate. The integration strategy worked because First Solar's technology was fundamentally different from standard silicon panels, making specialized capabilities valuable.

Managing Technology Risk vs Market Risk First Solar's journey illustrates the delicate balance between technology and market risk. Early on, they took massive technology risk (unproven CdTe technology) while minimizing market risk (selling into subsidized German market). As the technology matured, they shifted to taking market risk (competing without subsidies) while their technology risk diminished. This sequencing—prove technology in protected markets, then compete openly with proven technology—provides a template for deep tech companies.

Capital Intensity as Barrier to Entry First Solar's massive manufacturing investments create formidable barriers to entry. The company's operational manufacturing footprint in Ohio, Alabama and Louisiana represents over $4 billion in US manufacturing investments. New entrants face not just the capital requirement but also the learning curve of optimizing these complex facilities. The lesson: in industries where manufacturing excellence matters, capital intensity combined with accumulated know-how creates sustainable competitive advantage.

The Power of Strategic Pivots First Solar's history includes several major strategic pivots: from R&D company to manufacturer (2002), from European to U.S. focus (2011), from module supplier to project developer (2012), and from international to domestic concentration (2024). Each pivot was painful, involving layoffs and write-downs, but necessary for survival and growth. The ability to recognize when fundamental strategy must change—and execute that change decisively—separated First Solar from the dozens of failed solar companies.

Building Ecosystems, Not Just Products First Solar's success came not just from making panels but from building an entire ecosystem: developing project finance relationships, creating recycling programs, training installation crews, and lobbying for supportive policies. This ecosystem approach created switching costs and network effects that pure manufacturing couldn't achieve.

The Value of Strategic Patience Throughout its history, First Solar has shown remarkable strategic patience. They spent years perfecting manufacturing before scaling, accepted lower margins to build market share, and invested in R&D during downturns when competitors retreated. This patience, enabled by patient capital, allowed them to make decisions that looked suboptimal short-term but created long-term advantage.

XI. Analysis & Bear vs. Bull Case

The investment case for First Solar in late 2024 presents one of the most fascinating risk-reward profiles in industrial technology. Trading at a significant premium to book value but at reasonable multiples relative to growth, the stock embodies the tension between transformational opportunity and existential risk that defines breakthrough technology companies.

The Bull Case: American Solar Renaissance

The optimistic scenario for First Solar rests on multiple reinforcing trends that could drive explosive growth over the coming decade. The Inflation Reduction Act alone could generate over $10 billion in benefits through 2032 through manufacturing tax credits. The company's strong profitability was bolstered by its ability to leverage the U.S. 45X tax credit, which contributed to a year-end net cash position of $1.2 billion. These aren't one-time windfalls but recurring benefits that provide a structural cost advantage over international competitors.

The demand picture appears even more compelling. Data center electricity consumption is projected to triple by 2030, requiring massive new generation capacity. Tech giants have committed to renewable energy for these facilities, and First Solar's utility-scale focus positions them perfectly. With 25 GW of planned capacity by 2026 and a backlog stretching to 2030, revenue visibility exceeds almost any industrial company.

Technology leadership could extend First Solar's advantages. Their CdTe technology roadmap shows a path to 25% efficiency by 2025 and 28% by 2030. More importantly, perovskite tandem cells could deliver step-change improvements in efficiency while maintaining thin-film's cost advantages. If First Solar commercializes tandem technology first, they could dominate utility-scale solar globally.

The geopolitical environment increasingly favors First Solar. U.S.-China tensions make Chinese solar panels politically toxic for many American projects. European countries are reconsidering dependence on Chinese clean technology after experiencing the dangers of energy dependence on Russia. First Solar offers the only scaled alternative to Chinese dominance, positioning them as a strategic asset beyond mere commercial considerations.

Operational leverage should drive margin expansion. As new factories reach full utilization, fixed costs will be spread across more units. Manufacturing improvements continue to reduce variable costs. Premium pricing for American-made, forced-labor-free panels appears sustainable given regulatory requirements and ESG considerations. Operating margins could expand from current low-40s to above 50% by 2027.

The Bear Case: Structural Challenges

The pessimistic scenario focuses on fundamental challenges that policy support cannot permanently overcome. Chinese manufacturers continue to push crystalline silicon technology forward, with some achieving 26% efficiency in commercial modules. The efficiency gap between silicon and CdTe has widened, not narrowed, over the past five years. If this trend continues, First Solar's technology could become obsolete regardless of manufacturing cost advantages.

Policy dependency creates existential risk. The IRA passed with zero Republican votes, and while repeal seems unlikely given investments in red states, modifications that reduce benefits are probable. A 50% reduction in 45X credits would devastate First Solar's economics. International markets offer no refuge—without subsidies, First Solar cannot compete with Chinese manufacturers selling at marginal cost.

Supply constraints could cap growth regardless of demand. Tellurium supply cannot easily expand, potentially limiting First Solar's ability to scale beyond 30-40 GW globally. Attempts to reduce tellurium usage have shown limited success. If First Solar cannot solve the tellurium constraint, they'll hit a growth ceiling just as demand explodes.

Competition is intensifying from unexpected directions. Tesla's solar roof tiles target a different market but could evolve. Korean manufacturers are investing heavily in tandem cells. European governments are subsidizing domestic manufacturers. Most threateningly, Chinese companies are establishing U.S. manufacturing to qualify for IRA benefits, potentially eroding First Solar's policy advantages.

The customer concentration risk is underappreciated. A handful of large developers account for much of First Solar's backlog. If one major customer faces financial distress or strategic change, it could trigger massive order cancellations. The 2024 termination payments, while profitable, demonstrated this vulnerability.

Applying Strategic Frameworks

Through Porter's Five Forces lens, First Solar occupies an enviable but precarious position. Supplier power is moderate (tellurium constraint) but manageable. Buyer power is high (concentrated customers) but offset by limited alternatives for domestic content. New entrants face massive barriers (capital requirements, technology, policy relationships). Substitutes exist (crystalline silicon) but face their own limitations. Rivalry is intense globally but limited domestically.

Hamilton Helmer's 7 Powers framework reveals First Solar's strategic foundations. They possess Counter-Positioning (thin-film vs silicon), Scale Economies (massive factories), Switching Costs (integrated solutions), and Process Power (manufacturing expertise). However, they lack Network Effects, Brand (in commodity market), and Cornered Resource (beyond temporary policy advantages).

Key Performance Indicators

For fundamental investors tracking First Solar's trajectory, three KPIs matter most:

-

U.S. Manufacturing Utilization Rate: This measures actual output versus nameplate capacity at American facilities. High utilization (>90%) indicates strong demand and operational efficiency. Below 80% suggests demand weaknesses or operational issues.

-

All-in Module Cost per Watt: This comprehensive metric includes manufacturing, materials, overhead, and warranty provisions. Staying below $0.25/watt is crucial for competitiveness. Progress toward $0.20/watt would indicate sustainable advantage.

-

Contracted Backlog Coverage Ratio: Years of forward sales covered by firm contracts indicates demand visibility and pricing power. Above 2 years suggests strength; below 1 year signals vulnerability.

XII. Epilogue & "If We Were CEOs"

Standing at the intersection of technological possibility and market reality, First Solar faces defining choices that will determine whether they become the Intel of solar or merely another American manufacturing story that couldn't compete with Asian scale. The next five years will test every assumption about domestic manufacturing, clean energy economics, and American industrial policy.

If we were running First Solar, the strategic priorities would be clear but execution would be diabolical. First, we'd go all-in on tandem technology, treating the perovskite opportunity not as an R&D project but as a company-defining moonshot. This means not just funding research but creating entirely separate production lines for rapid iteration, partnering with universities globally, and potentially acquiring competing perovskite companies. The goal: commercial tandem modules by 2027, not 2030.

Second, we'd diversify beyond panels into complete energy systems. The acquisition strategy would focus on storage technology, grid management software, and project development capabilities. First Solar should become the Apple of solar—vertically integrated, premium positioned, and offering complete solutions rather than components. This transformation requires cultural change from manufacturing excellence to customer solution mindset.

Third, international expansion cannot be abandoned despite current retrenchment. We'd establish manufacturing in India through joint ventures, creating a base for serving Asian markets without Chinese supply chains. European production could follow if EU policies provide sufficient support. The goal isn't to compete with Chinese manufacturers on cost but to provide alternative supply chains for countries seeking energy security.

The recycling opportunity deserves massive investment. As first-generation solar panels reach end-of-life over the next decade, recycling could become a billion-dollar business. First Solar's existing recycling capabilities provide first-mover advantage. We'd create a separate division, sign long-term contracts for panel takeback, and position recycling as a differentiator for environmentally conscious customers.

Financial engineering could accelerate growth while managing risk. The massive tax credits should be monetized through sophisticated structures that provide upfront capital for expansion. Consider creating a separately traded subsidiary for manufacturing assets, allowing pure-play investment while maintaining control. Dividend policy should balance returning cash to shareholders with maintaining flexibility for opportunistic investments.

The talent war requires revolutionary approaches. Beyond competitive compensation, create an ownership culture through aggressive equity participation. Establish First Solar University for training programs that create career paths from factory floor to engineering leadership. Partner with historically black colleges and universities to develop diverse talent pipelines. Make First Solar the SpaceX of solar—a mission-driven company attracting the best minds.

Risk management must evolve with scale. Tellurium supply requires strategic stockpiles, long-term contracts with multiple suppliers, and aggressive R&D to reduce usage. Customer concentration needs active management through diversification and structured contracts that limit cancellation risk. Technology risk demands parallel development paths—advance CdTe while preparing for potential technology shifts.

The ultimate question isn't whether First Solar can succeed but what success means. Is the goal to maximize shareholder value over the next five years, potentially through sale to a larger industrial conglomerate? To build an enduring American champion that leads global solar manufacturing for decades? To catalyze the entire American solar industry through technology leadership and ecosystem development?

The answer shapes every strategic choice. Our view: First Solar should embrace its role as America's solar champion, accepting the responsibilities and opportunities that entails. This means sometimes sacrificing short-term profits for long-term positioning, investing in technologies that benefit the entire industry, and maintaining independence even if acquisition offers emerge.

The clean energy transition represents one of history's greatest economic opportunities. Solar will grow from 4% of global electricity today to potentially 40% by 2050. The companies that dominate this transition will shape the 21st century economy. First Solar has earned its seat at the table through four decades of innovation, persistence, and strategic courage.

The path forward demands continued courage. Competition will intensify. Technology will evolve. Policies will change. But First Solar's fundamental advantages—integrated manufacturing, proven technology, patient capital, and American industrial base—provide the foundation for continued leadership. The question isn't whether First Solar will survive but whether it will seize the moment to define an industry.

As we look toward 2030 and beyond, First Solar stands as proof that American manufacturing can compete in global technology markets. Not through protection or subsidy alone, but through innovation, strategic thinking, and relentless execution. The thin-film revolution that Harold McMaster imagined in his Toledo laboratory has become reality. The next revolution—whether tandem cells, recycling, or technologies yet unimagined—awaits.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube