Advanced Enzyme Technologies: The Quiet Biotech Giant of India

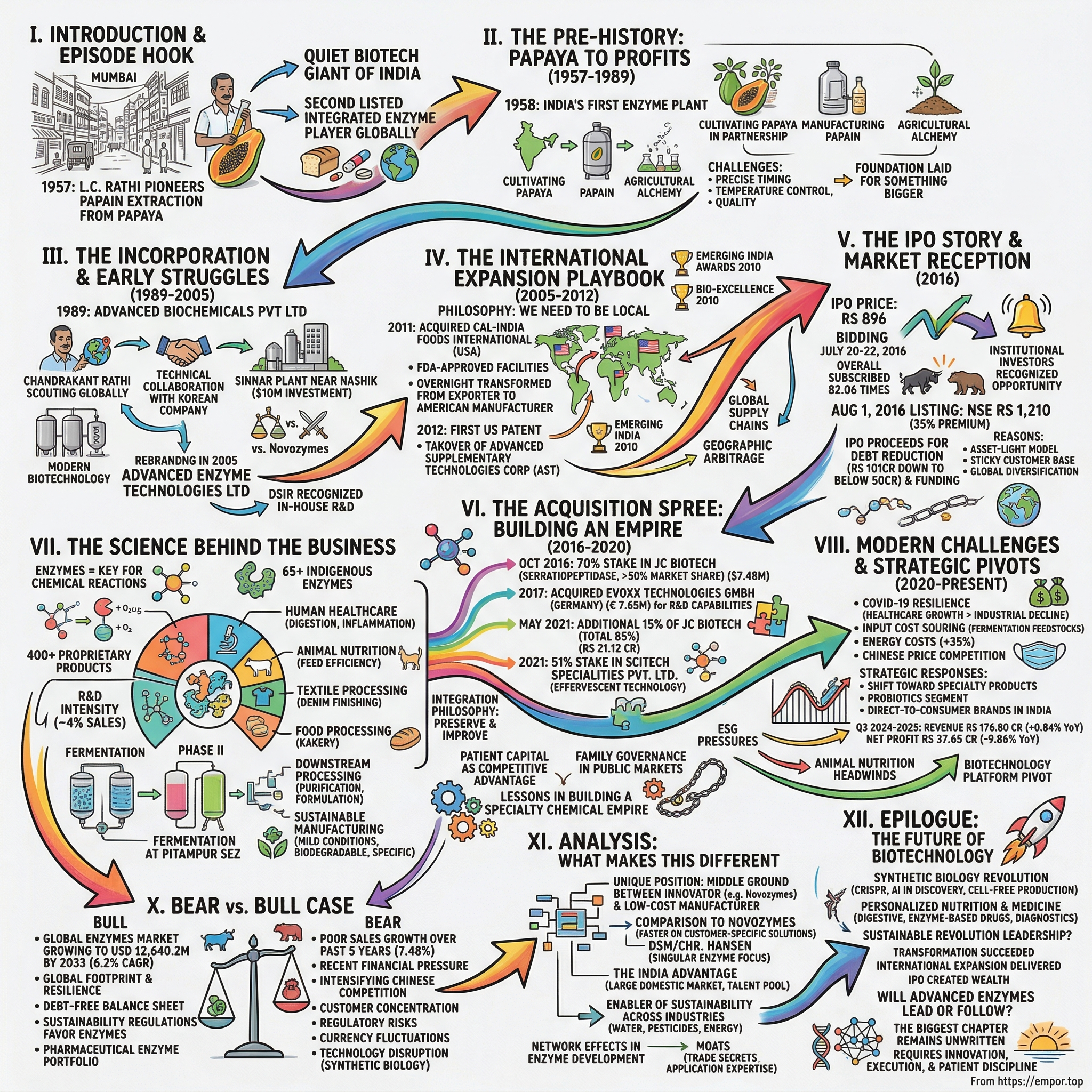

I. Introduction & Episode Hook

Picture a Mumbai street in 1957. While India celebrated its first decade of independence, a young entrepreneur named L.C. Rathi stood in a makeshift laboratory, extracting milky white liquid from papaya fruit. His neighbors thought he was crazy—who builds a business around fruit enzymes? Yet this moment would spark the creation of what would become India's largest enzyme company, a global player quietly powering everything from the bread on your breakfast table to life-saving medicines in hospitals worldwide.

The journey began in 1957, when founder Late L.C. Rathi pioneered the extraction of papain, an enzyme complex derived from papaya fruit and widely used for pharmaceutical and medical purposes. What started as a papaya enzyme extraction operation would evolve into Advanced Enzyme Technologies Limited—a company that today stands as the second listed integrated enzyme player globally.

The transformation from family business to global powerhouse reads like a masterclass in patient capital and strategic expansion. With over six decades of cumulative promoter experience in developing and deploying enzyme applications, the Rathi family built not just a company, but an entire ecosystem around specialty chemicals that most investors have never heard of, yet touch billions of lives daily.

This is the story of how a Rs 896 IPO price turned into a listing day bonanza with shares opening at Rs 1,210 on the NSE—a 35% premium, and how strategic acquisitions from California to Germany built India's biotech champion. It's a tale of multiple inflection points: the critical 2011 U.S. market entry, the European R&D expansion, and the bold bet on becoming a global specialty chemical empire when everyone else was chasing software unicorns.

Today, Advanced Enzymes operates in a market that's experiencing remarkable growth, with the global industrial enzymes market projected to reach USD 12,640.2 million by 2033, growing at a CAGR of 6.2%. Yet for all its global reach and technical sophistication, this remains at its core a story about turning humble papaya enzymes into a quiet biotechnology giant.

II. The Pre-History: Papaya to Profits (1957-1989)

The monsoon rains of 1958 brought more than just relief to Maharashtra's farmers. In a small facility that year, L.C. Rathi set up India's first enzyme manufacturing plant. While the rest of newly independent India focused on heavy industries and textiles, Rathi saw opportunity in the microscopic world of biological catalysts.

The early years were anything but glamorous. Extracting papain from papaya required precise timing—harvest too early and enzyme yields dropped; too late and the fruit ripened beyond use. Rathi would personally inspect papaya orchards, teaching farmers how to make precise incisions in green papayas to collect the latex. Each tree could be tapped only a few times before yields diminished. It was agricultural alchemy, turning fruit sap into pharmaceutical gold.

His initial steps into the world of enzymes began at the grassroot level when he began cultivating papaya in partnership with a farmer and started manufacturing papain in 1978. This wasn't just about extraction—it was about building an entire supply chain from scratch. The company had to educate farmers, develop collection methods, and create purification processes that met pharmaceutical standards.

The technical challenges were immense. Enzyme extraction required maintaining specific pH levels, temperatures, and preventing bacterial contamination—all without modern laboratory equipment. Rathi improvised, using ice from local fish markets for temperature control and developing proprietary extraction methods through trial and error. His small team would work through the night during harvest season, racing against enzyme degradation.

What set this operation apart was its focus on quality from day one. While competitors treated enzymes as commodity chemicals, Rathi insisted on pharmaceutical-grade purity. This obsession with quality would later become the company's calling card, but in these early years, it meant razor-thin margins and constant reinvestment.

By the 1980s, the operation had evolved from simple extraction to more sophisticated processes. The foundation was being laid for something bigger—but it would take the next generation to transform this cottage industry into a corporate powerhouse. The cumulative knowledge gained over these three decades of extraction, purification, and application development would prove invaluable when India opened its economy in 1991.

III. The Incorporation & Early Struggles (1989-2005)

Advanced Biochemicals Private Ltd was incorporated in 1989 to offer global and holistic enzyme solutions. The timing was prescient—just two years before India's economic liberalization would open doors to global markets and technology partnerships.

Chandrakant Rathi set up Advanced Biochemicals Ltd in 1989 and scouted the world for enzyme manufacturing technology. He landed a technical collaboration with a highly reputed Korean company and setup Advanced Biochemicals' Sinnar plant near Nashik at a total investment of $10 million. This wasn't just a factory—it was a statement of intent. The Sinnar facility represented a leap from traditional extraction to modern fermentation-based manufacturing.

The second generation brought new ambitions. Chandrakant and Vasant Rathi, armed with engineering education and global exposure, saw enzymes not as a family legacy but as a platform for biotechnology innovation. They faced a market dominated by giants like Novozymes, which controlled nearly half the global enzyme market. David versus Goliath seemed like an understatement.

The company set up a fermentation-based enzyme manufacturing plant with the help of foreign collaboration. This transition from extraction to fermentation was pivotal—it meant moving from agricultural dependency to industrial biotechnology. Fermentation allowed production of enzymes that couldn't be extracted from natural sources, dramatically expanding the product portfolio.

The struggles were real and relentless. International customers questioned why they should trust an Indian company with critical enzyme supplies. Regulatory approvals took years. A single contamination in a fermentation batch could wipe out months of profit. The company hemorrhaged cash, with R&D consuming resources without immediate returns.

Yet the Rathis persisted with remarkable discipline. They hired scientists from premier Indian institutes, sent teams abroad for training, and slowly built capabilities that rivaled international standards. Advanced Biochemicals' in-house R&D labs at Thane and Sinnar were recognized by the Department of Scientific and Industrial Research (DSIR), providing crucial validation for their technical capabilities.

The company was formerly known as Advanced Biochemicals Limited and changed its name to Advanced Enzyme Technologies Limited in 2005. This rebranding wasn't cosmetic—it signaled the transformation from a biochemical trader to a technology-driven enzyme specialist.

IV. The International Expansion Playbook (2005-2012)

The boardroom in Mumbai, 2010. Chandrakant Rathi spread a map across the conference table, red pins marking enzyme markets worldwide. "We can't compete with Novozymes in their backyard by being cheaper," he said. "We need to be local." This philosophy would drive the most aggressive international expansion by any Indian enzyme company.

In 2011, the company took over Cal-India Foods International, giving the company direct presence in USA. The Cal-India acquisition wasn't just about market access—it brought something invaluable: established customer relationships and FDA-approved facilities in California. Overnight, Advanced Enzymes transformed from an Indian exporter to an American manufacturer.

The integration challenged every assumption about cross-border acquisitions. The California team, accustomed to entrepreneurial independence, suddenly reported to Mumbai. Product formulations that worked in India needed reformulation for American food regulations. Even simple things like inventory management systems needed complete overhaul.

In 2012, Advanced Enzymes received its first US patent and consolidated its presence in the US with the takeover of Advanced Supplementary Technologies Corporation as a step down subsidiary. This double acquisition strategy was brilliant in hindsight—Cal-India provided industrial enzyme capabilities while AST brought nutraceutical expertise.

The real genius lay in the soft integration. Rather than imposing Indian management, Advanced Enzymes retained key American personnel, treating acquisitions as partnerships rather than takeovers. They invested in upgrading facilities, expanding product lines, and most importantly, maintaining the entrepreneurial culture that made these companies successful.

Behind the scenes, the company built sophisticated global supply chains. Enzymes produced through fermentation in India were shipped to California for formulation, then distributed across North America. European customers received supplies from both Indian and American facilities, depending on product specifications. This geographic arbitrage reduced costs while maintaining quality standards.

Advanced Enzymes was honoured with the 'Emerging India Awards 2010' for Life Science - Pharmaceuticals & Chemicals segment and received the Bio-Excellence 2010 award as the Best Industrial Biotech Company. These weren't participation trophies—they validated the global expansion strategy to skeptical investors and customers.

V. The IPO Story & Market Reception (2016)

July 20, 2016. The investment bankers at Axis Capital and IIFL looked nervous. The Indian IPO market had been lukewarm, and here was a company most retail investors couldn't pronounce, let alone understand. Enzymes? Biotechnology? The pitch needed to be perfect.

The IPO consisted of 45,94,875 equity shares aggregating up to Rs 411.49 Crores, priced at Rs 896 per share, with bidding from July 20-22, 2016. The pricing seemed aggressive—at 25 times earnings for a specialty chemical company with limited brand recognition.

What happened next stunned everyone. The offer was overall subscribed 82.06 times. Institutional investors, particularly foreign funds, recognized what retail investors missed: this was a rare play on specialty biotechnology with global operations and protected market position.

August 1, 2016, 9:15 AM. The opening bell at the NSE. The shares got listed on BSE, NSE on Aug 1, 2016, with the stock opening at Rs 1,210 as against its issue price of Rs 896 per share—a 35% premium. The grey market premium had predicted gains, but this exceeded the most optimistic estimates.

The IPO proceeds had clear purposes: debt reduction and funding for the US subsidiary. At the IPO launch, managing director C.L. Rathi noted that debt stood at Rs 101 crore, with Rs 40 crore to be reduced from the IPO, expecting total debt to fall below Rs 50 crore going forward.

Why did the market love it? Three reasons stood out. First, the asset-light model—unlike traditional chemical companies, enzyme production required minimal capital expenditure once fermentation facilities were established. Second, the sticky customer base—enzyme formulations were customized for specific applications, creating high switching costs. Third, the global diversification—unlike most Indian specialty chemical companies dependent on exports, Advanced Enzymes had manufacturing presence across continents.

The institutional investor roster read like a who's who of smart money: foreign portfolio investors grabbed major allocations, while mutual funds that had done their homework participated aggressively. The retail portion, despite the complexity of the business, was oversubscribed by nearly 2.5 times.

But the real story wasn't the listing pop—it was what the capital enabled. The company now had currency for acquisitions, credibility for international expansion, and visibility among global customers who preferred publicly-traded suppliers.

VI. The Acquisition Spree: Building an Empire (2016-2020)

October 2016. Within months of the IPO, Advanced Enzymes made its boldest move yet. The company acquired a 70% stake in bulk drugs maker JC Biotech Pvt Ltd, which has more than 50% market share in the production of API enzyme serratiopeptidase.

The JC Biotech acquisition was strategic brilliance disguised as opportunism. Serratiopeptidase—a anti-inflammatory enzyme used in medicines—represented a completely different market from food and industrial enzymes. The acquisition was completed on October 28, 2016 for $7,484,493. This wasn't just buying market share; it was acquiring a monopolistic position in a specialized pharmaceutical enzyme.

The integration revealed Advanced Enzymes' acquisition philosophy: preserve what works, improve what doesn't. JC Biotech's fermentation expertise was maintained, but quality systems were upgraded to global standards. The founding team was retained with earnout provisions, ensuring continuity while aligning incentives.

Then came the European masterstroke. In 2017, Advanced Enzymes Europe B.V. entered into a binding agreement with Germany-based Evoxx Technologies GmbH, to acquire a 100% stake for € 7.65 million. Evoxx, founded as evocatal GmbH in 2006, had a team of 35+ scientists & technicians across two sites in Germany.

The Evoxx acquisition transformed Advanced Enzymes' R&D capabilities overnight. Evoxx technologies focused on the development and production of industrial enzymes and novel carbohydrate ingredients produced by enzymatic bioconversion, with proprietary enzymes active in high growth markets addressing consumer needs in the global food health & wellness sector.

Dr. Thorsten Eggert, Evoxx's CEO, captured the strategic fit perfectly: "Together with the strong partners in India and USA, the portfolio of industrial enzymes will be larger and more attractive for existing and future customers. Furthermore, the production plants and production knowledge of Advanced Enzymes will help evoxx deliver enzymes in industrial scale".

In May 2021, the board approved acquisition of additional 15% of equity share capital of JC Biotech for Rs 21.12 crore, taking the total stake to 85%. This follow-on investment demonstrated confidence in the pharmaceutical enzyme strategy.

The company didn't stop there. It acquired a 51% stake in SciTech Specialities Pvt. Ltd. in 2021, establishing a specialized manufacturing segment. SciTech brought effervescent technology capabilities, opening doors to new delivery formats for enzyme-based nutraceuticals.

Each acquisition followed a pattern: identify companies with unique technology or market position, acquire controlling stakes while retaining management, integrate carefully to preserve entrepreneurial culture, then leverage Advanced Enzymes' global distribution to accelerate growth. It was corporate development as chess, not checkers.

VII. The Science Behind the Business

To understand Advanced Enzymes' moat, you need to understand enzymes themselves. Imagine a key that unlocks specific chemical reactions—making them happen faster, at lower temperatures, with less energy. That's an enzyme. Now imagine having 400+ proprietary products developed using over 65 indigenous enzymes. That's Advanced Enzymes.

The company's position is unique: it's the first Indian enzyme company with second highest market share in India, and the second listed integrated enzyme player globally. This isn't just about scale—it's about capabilities across the entire value chain.

The enzyme business operates on three levels of complexity. At the base, commodity enzymes like proteases for detergents compete on price. Moving up, specialized enzymes for food processing command better margins through customization. At the apex, pharmaceutical enzymes like serratiopeptidase enjoy near-monopolistic positions with 50%+ margins.

Advanced Enzymes plays at all three levels, but its real differentiation lies in application expertise. A bakery enzyme isn't just about breaking down starch—it's about understanding dough rheology, shelf-life extension, and crumb structure. This requires food scientists working alongside enzyme engineers, a capability built over decades.

The product portfolio spans remarkable diversity. In human healthcare, their enzymes aid digestion, reduce inflammation, and enhance drug delivery. For animal nutrition, enzyme cocktails improve feed efficiency, reducing costs for poultry and dairy farmers. In textile processing, enzymes replace harsh chemicals in denim finishing, creating the worn look consumers love while reducing environmental impact.

The magic happens in fermentation tanks—massive bioreactors where carefully selected microorganisms produce enzymes under controlled conditions. The company's Phase II fermentation facility at Pitampur SEZ near Indore represents state-of-the-art biotechnology. Temperature, pH, oxygen levels, and nutrient feeds are monitored continuously. A single parameter deviation can ruin a batch worth lakhs.

But fermentation is just the beginning. Downstream processing—purification, concentration, stabilization, and formulation—determines enzyme effectiveness. Advanced Enzymes' expertise in maintaining enzyme activity through processing, storage, and application sets it apart from competitors who treat enzymes as commodity chemicals.

The R&D intensity is remarkable. Over the last five years, the company has consistently spent ~4% of its sales on research and development. This isn't just about new products—it's about improving yields, reducing costs, and expanding applications for existing enzymes.

What makes enzymes the future of sustainable manufacturing? They operate under mild conditions, reducing energy consumption. They're biodegradable, eliminating chemical waste. They're specific, minimizing side reactions and improving product quality. As industries face pressure to reduce environmental impact, enzymes offer solutions that are both economically and ecologically superior.

VIII. Modern Challenges & Strategic Pivots (2020-Present)

The COVID-19 pandemic initially seemed catastrophic for a company dependent on food processing and industrial customers. Factories shut down, supply chains froze, and demand evaporated overnight. Yet Advanced Enzymes emerged stronger, revealing the resilience of its diversified model.

Healthcare enzymes saw explosive growth as immune-supporting supplements flew off shelves. The pharmaceutical enzyme portfolio, particularly anti-inflammatory enzymes, witnessed unprecedented demand. While industrial enzyme sales dropped 30% in Q1 FY21, healthcare segments grew by 40%, cushioning the overall impact.

But structural challenges emerged post-pandemic. Chinese manufacturers, recovering faster from lockdowns, aggressively priced commodity enzymes to gain market share. Input costs soared—fermentation requires agricultural feedstocks whose prices doubled during 2021-2022. Energy costs for maintaining fermentation conditions increased 35%, squeezing margins.

The company's response was strategic rather than reactive. Instead of competing on price in commodity enzymes, Advanced Enzymes accelerated its shift toward specialty products. The probiotic segment, combining enzymes with beneficial bacteria, became a growth driver. Direct-to-consumer brands were launched in India, capturing higher margins by eliminating distributors.

In Q3 2024-2025, revenue grew marginally by 0.84% year-over-year to Rs 176.80 Cr, while net profit fell 9.86% to Rs 37.65 Cr. The numbers revealed pressure on profitability despite revenue stability. Management attributed this to investment in new product development and market expansion costs.

The animal nutrition segment faced particular headwinds. Avian flu outbreaks reduced poultry production, directly impacting feed enzyme demand. Competition from synthetic alternatives and customer consolidation pressured pricing. The company responded by developing next-generation enzyme combinations that improved feed conversion ratios by 15%, justifying premium pricing.

ESG pressures created both challenges and opportunities. European customers demanded carbon footprint data for enzyme production. Regulatory requirements for "clean label" ingredients increased compliance costs. Yet these same pressures disadvantaged chemical alternatives, expanding the addressable market for enzyme solutions.

The strategic pivot toward becoming a biotechnology platform rather than just an enzyme manufacturer accelerated. Partnerships with pharmaceutical companies for enzyme-drug conjugates opened new revenue streams. Collaboration with agricultural biotechnology firms for crop protection enzymes diversified the portfolio beyond traditional segments.

Geographic expansion continued despite global uncertainties. The European R&D center, acquired through Evoxx, became the hub for developing enzymes meeting stringent EU regulations. The American operations focused on rapid prototyping for food industry customers. India remained the low-cost manufacturing base, but with increasing emphasis on complex, high-value enzymes.

IX. Playbook: Lessons in Building a Specialty Chemical Empire

The Advanced Enzymes story offers a masterclass in building a global specialty chemical business from an emerging market. The playbook deserves careful study.

Patient Capital as Competitive Advantage: The Rathi family's six-decade commitment to enzymes seems almost anachronistic in an era of quick flips and rapid exits. With over 6 decades of cumulative promoter experience, they understood that enzyme expertise couldn't be bought—it had to be developed through thousands of experiments, failed batches, and customer iterations.

This patience extended to financial strategy. The company remained private for 27 years post-incorporation, using internal accruals and minimal debt to fund growth. When they finally tapped public markets in 2016, it was from a position of strength rather than desperation.

Acquisition Integration Excellence: Every successful acquisition followed the "preserve and enhance" philosophy. Local management was retained, ensuring continuity of customer relationships and technical knowledge. Corporate functions were integrated slowly, starting with quality systems and financial reporting. Only after cultural alignment was achieved did operational integration accelerate.

The earn-out structures were particularly clever. Selling founders remained invested in growth, while Advanced Enzymes gained immediate control. This balanced risk-sharing with alignment of incentives, crucial for knowledge-intensive businesses where human capital matters more than physical assets.

R&D as Moat, Not Cost: While competitors outsourced research or relied on licensed technology, Advanced Enzymes built internal capabilities painstakingly. Spending ~4% of sales on R&D consistently created a proprietary product library that couldn't be replicated.

The R&D strategy emphasized application development over basic research. Instead of discovering new enzymes, they found new uses for existing ones. This pragmatic approach delivered faster returns while building deep customer relationships through collaborative development.

Geographic Arbitrage: The multi-geography manufacturing footprint wasn't just about market access—it was about capability arbitrage. Indian facilities handled high-volume fermentation leveraging low-cost skilled labor. American operations focused on customer-specific formulations requiring rapid iteration. European R&D developed next-generation products meeting stringent regulations.

Family Governance in Public Markets: The transition from family business to public company often destroys value through governance conflicts. Advanced Enzymes navigated this by clearly delineating roles. Chandrakant Rathi, with over 40 years of experience, handled operations including R&D and production, while Vasant Rathi, with over 35 years of experience, focused on product development and commercialization.

Professional managers were inducted for specialized functions, while family members retained strategic control. Independent directors brought global perspectives without threatening family influence. This hybrid structure balanced entrepreneurial agility with corporate governance.

The Specialty Chemical Advantage: Unlike commodity chemicals competing on price, specialty enzymes compete on performance. Customer switching costs are high—reformulating a food product or pharmaceutical preparation requires extensive testing and regulatory approval. This creates recurring revenue streams with predictable growth.

The asset-light nature of enzyme production, once fermentation capabilities are established, generates superior returns on capital. Unlike petrochemicals requiring massive refineries, enzyme plants can be modular and expanded incrementally based on demand.

X. Bear vs. Bull Case

The Bull Case: Structural Tailwinds and Competitive Positioning

The optimists see Advanced Enzymes riding multiple megatrends. The global industrial enzymes market is projected to reach USD 12,640.2 million by 2033, growing at a CAGR of 6.2%. This isn't speculative growth—it's driven by fundamental shifts toward sustainable manufacturing and natural ingredients.

The company's global footprint provides resilience and growth optionality. Unlike India-centric competitors vulnerable to currency fluctuations and regulatory changes, Advanced Enzymes has natural hedges through multi-geography operations. International markets contributed ~56% of revenue in FY22, providing diversification benefits.

The debt-free balance sheet offers strategic flexibility. The company is almost debt free, enabling aggressive investment in R&D or opportunistic acquisitions without dilution or financial stress. In a rising rate environment, this becomes a significant competitive advantage.

Sustainability regulations increasingly favor enzyme solutions over chemical alternatives. The European Green Deal, pushing for carbon neutrality by 2050, makes enzyme-based processes mandatory for many applications. Similar regulations in other developed markets expand the addressable opportunity.

The pharmaceutical enzyme portfolio, particularly through JC Biotech, provides a differentiated growth vector. With more than 50% market share in serratiopeptidase production, the company enjoys near-monopolistic positioning in a growing therapeutic segment.

The Bear Case: Execution Risks and Market Realities

Skeptics point to concerning operational metrics. The company has delivered poor sales growth of 7.48% over the past five years. For a company in a supposedly high-growth industry, this suggests either market share loss or inability to capitalize on opportunities.

The recent financial performance raises red flags. Net profit fell 9.86% year-over-year in Q3 2024-2025, despite the post-pandemic recovery. Management's explanations about investment spending seem insufficient given the magnitude of profit decline.

Competition from Chinese manufacturers intensifies annually. Chinese enzyme producers, backed by government subsidies and massive fermentation capacity, can undercut pricing by 30-40% in commodity segments. This forces Advanced Enzymes toward increasingly niche segments with limited scale potential.

Customer concentration remains a hidden risk. While the company doesn't disclose customer-specific data, industry sources suggest the top 10 customers account for over 40% of revenues. Loss of a major food processing or pharmaceutical customer could severely impact financial performance.

Regulatory risks multiply with geographic expansion. Enzyme applications in food and pharmaceuticals face stringent approval processes. A single contamination incident or adverse regulatory ruling could shut down entire product lines. The complexity of managing compliance across multiple jurisdictions increases operational risk.

Currency fluctuations create earnings volatility. With significant international operations but India-based costs, rupee appreciation hurts competitiveness while depreciation inflates input costs for imported raw materials. Natural hedging only partially mitigates this exposure.

Technology disruption looms on the horizon. Synthetic biology companies are developing cell-free enzyme production systems that could obsolete traditional fermentation. While still experimental, these technologies could reshape the industry within a decade.

XI. Analysis: What Makes This Different

Advanced Enzymes occupies a unique position in the global enzyme landscape—neither a pure-play innovator like Novozymes nor a low-cost manufacturer like Chinese competitors. This middle ground might seem uncomfortable, but it's precisely where the opportunity lies.

Compare it to Novozymes, the Danish giant controlling 48% of the global market. Novozymes spends over 13% of revenue on R&D, holds thousands of patents, and commands premium pricing. But this innovation leadership comes with bureaucratic overhead and slower decision-making. Advanced Enzymes, with its entrepreneurial structure and ~4% R&D spending, can't match Novozymes' innovation but can move faster on customer-specific solutions.

Against DSM or Chr. Hansen, Advanced Enzymes lacks the integrated nutrition portfolio but compensates through focus. While these conglomerates juggle multiple business segments, Advanced Enzymes' singular enzyme focus enables deeper expertise and better resource allocation.

The India advantage extends beyond cost. The large domestic market provides a testing ground for products before global launch. Regulatory requirements in India, while complex, are less stringent than developed markets, enabling faster iteration. The availability of fermentation expertise, built through decades of pharmaceutical manufacturing, provides a talent pool unavailable elsewhere.

But what truly differentiates Advanced Enzymes is its position as an arms dealer in the sustainability war. Unlike companies betting on specific green technologies, Advanced Enzymes enables multiple industries to reduce environmental impact. Whether it's reducing water usage in textile processing, eliminating chemical pesticides in agriculture, or reducing energy consumption in biofuel production, enzymes are essential enablers.

The network effects in enzyme development are underappreciated. Each customer application generates data on enzyme performance under specific conditions. This knowledge accumulates, improving future product development. Customers become reluctant to switch suppliers who understand their unique requirements, creating competitive moats that strengthen over time.

The business model mirrors pharmaceutical companies more than chemical manufacturers. High upfront development costs, regulatory approval requirements, and customer stickiness create barriers to entry. But unlike pharma, enzymes don't face patent cliffs—trade secrets and application expertise provide sustainable differentiation.

XII. Epilogue: The Future of Biotechnology

Standing at the intersection of biology and industry, Advanced Enzymes represents both India's biotechnology ambitions and the global transition toward sustainable manufacturing. The next decade will determine whether it becomes a global champion or remains a regional player with international operations.

The synthetic biology revolution promises to reshape enzyme production fundamentally. Gene editing tools like CRISPR enable design of novel enzymes with unprecedented properties. Artificial intelligence accelerates enzyme discovery from years to months. Cell-free production systems could eliminate fermentation entirely. Advanced Enzymes must navigate this technological disruption while maintaining current operations.

Personalized nutrition and medicine create new enzyme opportunities. Digestive enzyme supplements tailored to individual microbiomes, enzyme-based drugs targeting specific genetic conditions, and diagnostic enzymes for point-of-care testing expand addressable markets beyond traditional industrial applications.

The real question isn't whether Advanced Enzymes will grow—the enzyme market expansion seems inevitable. It's whether the company can transition from successful acquisition integrator to innovation leader. Can entrepreneurial agility survive corporate scale? Will family governance adapt to institutional demands? Can Indian R&D compete with Silicon Valley synthetic biology startups?

The precedents offer mixed lessons. Biocon, India's first biotechnology unicorn, successfully transitioned from enzymes to biopharmaceuticals but struggled with global expansion. Dr. Reddy's leveraged Indian cost advantages for global success but remained primarily a generics player. Sun Pharma built through acquisitions but faced integration challenges at scale.

Advanced Enzymes' path appears different—less ambitious than Biocon's transformation, more focused than Dr. Reddy's diversification, more disciplined than Sun Pharma's aggressive expansion. This measured approach might lack headline appeal but could deliver sustainable value creation.

As I write this in October 2025, looking at a six-decade journey from papaya extraction to global biotechnology, the story feels simultaneously complete and unfinished. The transformation from family business to public company succeeded. The international expansion delivered. The IPO created wealth. Yet the biggest chapter—leading the enzyme industry's sustainable revolution—remains unwritten.

Will Advanced Enzymes lead or follow? The pieces are in place: global manufacturing footprint, diverse product portfolio, strong balance sheet, experienced management. But pieces don't guarantee victory. Success requires continued innovation, flawless execution, and perhaps most importantly, the same patient discipline that built this quiet biotechnology giant from humble papaya beginnings.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube