Fidelity National Financial: The Empire Builder's Title Insurance Story

I. Introduction & The Puzzle

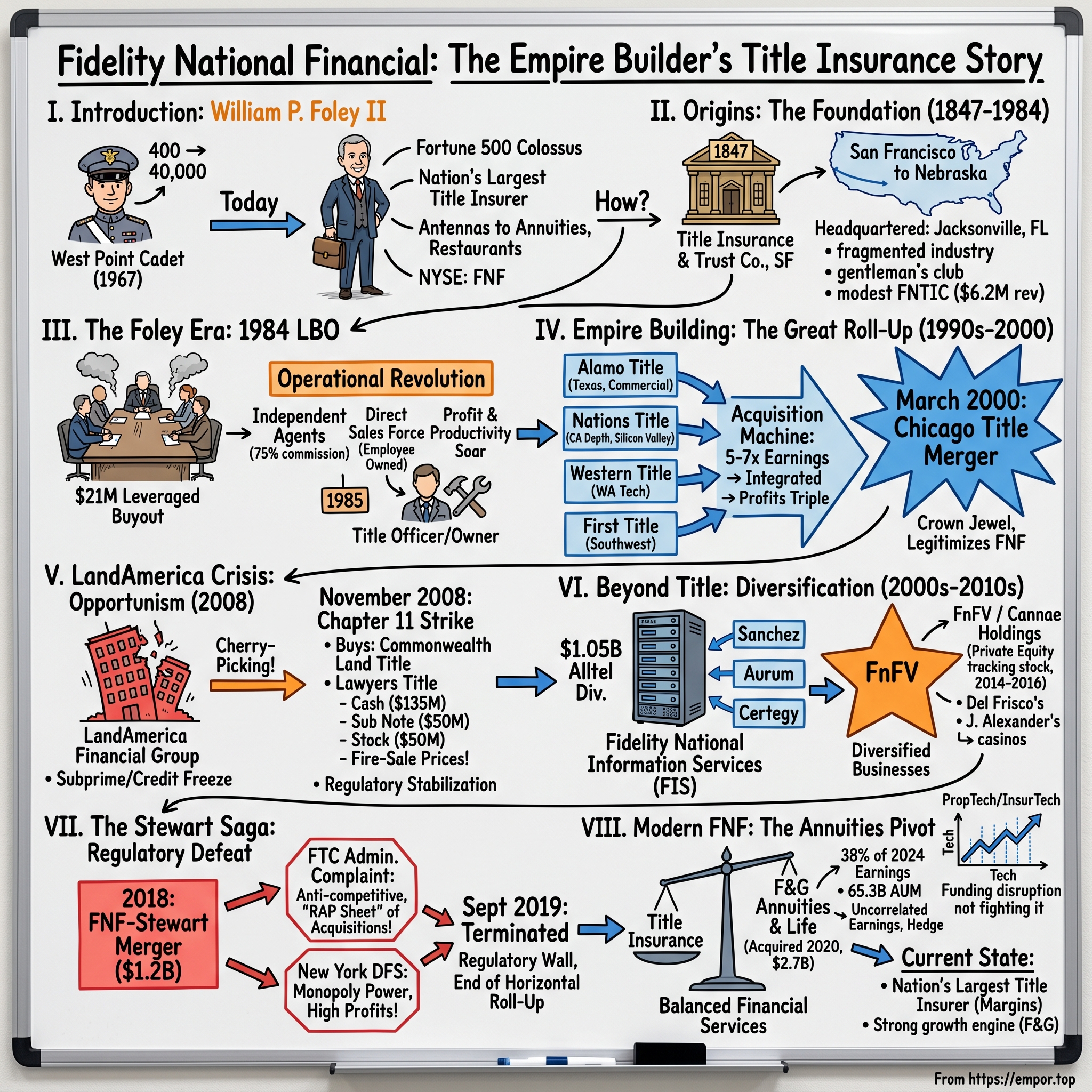

Picture this: A West Point cadet sits hunched over financial newspapers in his dorm room, having just turned $400 into $40,000 trading stocks between military drills. It's 1967, and while his classmates dream of commanding battalions, William P. Foley II is already plotting corporate conquests. Fast forward to today, and that same cadet has built Fidelity National Financial into a Fortune 500 colossus—the nation's largest title insurance empire with tentacles reaching into everything from annuities to restaurant chains.

How exactly does someone transform a sleepy Arizona title insurer doing $6.2 million in revenue into a financial services behemoth trading on the NYSE under symbol FNF? How does a company founded in 1847 as Title Insurance and Trust Company in San Francisco end up headquartered in Jacksonville, Florida, controlling legendary brands like Chicago Title, Commonwealth Land Title, and Alamo Title?

The answer lies in one of corporate America's most underappreciated empire-building stories—a tale of leveraged buyouts, crisis opportunism, and operational revolution that transformed an entire industry. While tech founders get magazine covers and hedge fund managers become household names, Bill Foley quietly assembled one of the most dominant positions in American finance, controlling the invisible infrastructure that makes nearly half of all U.S. real estate transactions possible.

This is the story of how a military-trained lawyer discovered that the boring business of title insurance could be the foundation for something far grander. It's about recognizing that in heavily regulated, fragmented industries, the spoils go not to the disruptor but to the consolidator. And it's about understanding that sometimes the best businesses are the ones nobody else wants to think about—until it's too late.

Our journey spans from that original 1984 leveraged buyout worth $21 million to today's diversified financial empire. Along the way, we'll explore how Foley's playbook—direct distribution over independent agents, employee ownership, aggressive M&A, and crisis exploitation—became the template for building scale in America's most overlooked financial services sector. Welcome to the Fidelity National Financial story: where title insurance meets empire building.

II. Origins: The Foundation Years (1847–1984)

The title insurance industry of 1984 was a gentleman's club—regional fiefdoms run by local attorneys, independent agents taking hefty commissions, and underwriters content with their slice of the American dream. Companies operated like utilities: steady, boring, profitable enough. Nobody was getting rich, but nobody was complaining either.

Into this sleepy world stepped Fidelity National Title Insurance Company (FNTIC), incorporated in Nebraska and ranking 48th among U.S. title insurers with its modest $6.2 million in annual revenues. The company traced its roots back to 1847, when California's gold rush created the first real need for clear property titles. Those San Francisco origins as Title Insurance and Trust Company gave it historical gravitas, but by the early 1980s, FNTIC was just another small player in a fragmented industry where the top ten companies controlled less than half the market.

The title insurance business itself was beautifully simple yet maddeningly inefficient. When someone buys property, title insurance protects against claims from previous owners, unpaid taxes, or fraudulent deeds. Unlike other insurance that guards against future events, title insurance covers past sins—making it essentially a one-time research fee disguised as an insurance premium. The loss ratio? Typically under 10%, compared to 60-80% for auto or health insurance. Pure profit margin, if you could control distribution.

But here's what made the industry ripe for disruption: almost nobody understood this. Title insurance operated through a byzantine network of independent agents who pocketed 70-80% of premiums as commissions. Underwriters like FNTIC essentially ran research operations while agents walked away with the profits. State regulations created local monopolies. Technology meant typewriters and filing cabinets. Customer service was whatever the local attorney felt like providing that day.

The regulatory environment added another layer of complexity. Each state had its own insurance commissioner, its own rules, its own rate structures. Some states like Florida and Texas regulated rates strictly; others like California allowed price competition. This patchwork system meant that building a national player required not just capital but intimate knowledge of fifty different regulatory regimes. It was precisely the kind of messy, complex, relationship-driven business that scared away Wall Street but attracted operators who understood that complexity creates opportunity.

By 1984, the industry was generating about $2 billion in annual premiums, growing steadily with real estate values but lacking any real innovation since the 1960s. The largest players—Chicago Title, First American, Stewart Title—operated regionally with minimal overlap. Nobody talked about market share or operational efficiency. Nobody thought about roll-ups or synergies. It was exactly the kind of industry where an ambitious operator with a different playbook could build an empire. The stage was set for transformation—it just needed someone with the vision to see it and the audacity to execute.

III. The Foley Era Begins: The 1984 LBO

The Boeing conference room in Seattle was thick with cigarette smoke and tension. It was 1969, and Second Lieutenant William P. Foley II sat across from executives three times his age, negotiating million-dollar defense contracts for the Air Force. Fresh out of West Point, where he'd turned his cadet allowance into $40,000 through shrewd stock picks, Foley was learning that business was war by other means. "They thought they could intimidate some kid in uniform," he'd later recall. "They learned different."

By 1984, Foley had traded his uniform for a law degree from the University of Washington and built a successful practice in Phoenix. But legal work bored him. What excited him were the distressed companies his clients brought him—broken businesses that could be fixed with better operations and aggressive management. When a client mentioned that small FNTIC was available, something clicked. Here was an industry with 5% loss ratios hiding behind 80% commission structures. Here was inefficiency at scale.

Foley assembled a group of investors and structured a leveraged buyout worth approximately $21 million—significant money for a company doing $6.2 million in revenue, but Foley saw what others missed. With partner Frank Willey, he incorporated a new Fidelity National Financial Inc. as the acquisition vehicle. The leverage was aggressive: they put down just $3 million in equity, borrowing the rest. Foley would serve as president and chairman, bringing military discipline to an industry that hadn't seen a new idea since Eisenhower.

The operational revolution began immediately. Where competitors relied on independent agents who controlled customer relationships and commanded princely commissions, Foley and Willey made a radical decision: build a direct sales force. "Why should we pay someone 75% commission to do what an employee could do for salary plus 10%?" Foley asked his team. The math was compelling—cutting distribution costs from 75% to 25% of premiums would transform the entire business model.

But the masterstroke came in 1985. Rather than pocket the savings from direct distribution, Foley sold stock to employees, making Fidelity the nation's first employee-owned title insurance underwriter. Suddenly, every title officer, every researcher, every sales rep had skin in the game. Employee-owners didn't just process titles; they hunted for business, controlled costs, and thought like owners because they were owners. Productivity soared. Turnover plummeted. Competitors watched in bewilderment as Fidelity's direct operations achieved loss ratios below 5% while maintaining premium growth above 30% annually.

The cultural transformation was equally dramatic. Foley instituted military-style accountability: daily reports, weekly reviews, monthly deep dives. Managers who missed targets were gone. Those who exceeded them became wealthy through stock options. "We're not running a country club," Foley told a gathering of employees in 1986. "We're building an empire."

By 1987, just three years after the buyout, Fidelity was ready for the public markets. The IPO on the American Stock Exchange under symbol FNF valued the company at over $100 million—a five-fold increase from the purchase price. Foley's $1 million personal investment was now worth $20 million. But this was just the beginning. With public currency and a proven playbook, Foley could now execute the real plan: rolling up the entire industry while competitors still debated whether this upstart from Phoenix was a serious threat. They would learn, just as those Boeing executives had learned two decades earlier, that underestimating Bill Foley was an expensive mistake.

IV. Empire Building: The Great Roll-Up (1990s–2000)

The fax machine in Foley's Jacksonville office—FNF had relocated to Florida for tax advantages—never stopped humming in the 1990s. Each transmission brought intelligence on another struggling title insurer, another opportunity to expand the empire. Foley had developed a simple formula: find regional players with good brands but poor operations, buy them for 5-7x earnings, integrate them into FNF's direct distribution model, and watch profits triple within eighteen months.

The acquisition machine started modestly. Alamo Title brought Texas exposure and a coveted position in Houston's booming commercial market. Nations Title Inc. provided California depth just as Silicon Valley was creating unprecedented wealth. Western Title Company of Washington captured Seattle's tech-fueled real estate boom. First Title Corp. solidified the Southwest. Each deal followed the same playbook: terminate independent agent contracts, hire the best agents as employees, install FNF's technology systems, and ruthlessly cut costs.

But Foley wasn't just buying companies—he was building a psychological advantage. "Every time we bought someone, five other CEOs would call asking if they were next," recalled a former FNF executive. The industry was gripped by a mixture of fear and greed. Stock prices of potential targets rose on acquisition rumors. Independent agents began defecting to FNF preemptively, knowing resistance was futile.

The integration strategies were surgical. Within 90 days of closing, FNF would consolidate back-office operations, standardize underwriting procedures, and implement its proprietary title plant technology. Local brands were maintained—customers still wrote checks to Alamo Title or Nations Title—but behind the facades, everything ran on FNF's platform. Competitors couldn't match this efficiency. Their patchwork of independent agents and legacy systems meant they were paying 70 cents to generate a dollar of premium while FNF spent 40 cents.

Then came March 2000—the deal that transformed FNF from ambitious consolidator to industry colossus. Chicago Title Insurance Company wasn't just another acquisition; it was the crown jewel of the title insurance world. Founded in 1847, Chicago Title had insured landmark properties from the Empire State Building to the Golden Gate Bridge. It had survived the Chicago Fire, the Great Depression, and countless real estate cycles. Now, in a historic merger, it would join the Fidelity National Financial family.

The complexity of the Chicago Title integration dwarfed anything FNF had previously attempted. Chicago Title brought 8,000 employees, operations in 40 states, and a book of business that included most of America's largest commercial real estate transactions. But it also brought something invaluable: legitimacy. No longer could competitors dismiss FNF as an upstart. The combination created the world's largest title insurer and provider of real estate-related products and services.

The numbers told the story of Foley's transformation: from $6.2 million in revenue in 1984 to over $4 billion by 2000. Market share had grown from less than 1% to nearly 30%. The company that had ranked 48th was now unquestionably number one. But Foley understood something his competitors still didn't grasp: in a scale business, being number one wasn't just about bragging rights. It meant dictating terms to regulators, setting industry standards, and having the balance sheet to weather any storm. The empire was built. Now it needed to be defended—and the greatest test would come sooner than anyone expected.

V. The LandAmerica Crisis Acquisition (2008)

The September 2008 FNF board meeting felt like a war room. Lehman Brothers had collapsed two weeks earlier. AIG was being nationalized. Real estate transactions—the lifeblood of title insurance—had dropped 40% year-over-year. Lesser companies would have been playing defense, but Foley saw blood in the water. "Gentlemen," he told his directors, "this crisis will deliver us our competitors on a silver platter."

LandAmerica Financial Group, the nation's third-largest title insurer, was drowning. The Richmond-based company had made an ill-timed push into subprime mortgage services just as that market imploded. Its stock had crashed from $80 to $5. Its commercial paper funding had evaporated overnight when the credit markets froze. CEO Ted Chandler was desperately seeking a buyer, and FNF initially signed a definitive merger agreement with LFG shareholders receiving 0.993 shares of FNF common stock for each share owned.

But Foley, the former military intelligence officer, knew that desperation creates leverage. As LandAmerica's position deteriorated through October and November, he began repositioning. Why buy the entire company with its toxic mortgage assets when he could cherry-pick the best pieces from bankruptcy? When LandAmerica finally filed for Chapter 11 protection on November 26, 2008, FNF was ready with a surgical strike.

The execution was masterful. Rather than acquiring LandAmerica wholesale, FNF signed a stock purchase agreement to acquire only its crown jewels: Commonwealth Land Title and Lawyers Title. Chicago Title would acquire Commonwealth for $158.6 million while Fidelity National Title would take Lawyers and United Capital for $139.4 million. The total purchase price of $298 million was less than one-third what FNF had initially agreed to pay for the entire company.

But here's where Foley's strategic genius shone: he structured the deal to minimize cash outlay during a credit crisis. The final terms included just $135 million in cash, with the balance in a $50 million subordinated note and $50 million in FNF stock. Total consideration of approximately $235 million for assets that had generated over $1 billion in revenue just two years earlier. The sellers had no leverage; it was FNF or liquidation.

The regulatory navigation required was extraordinary. The combined entity would control approximately 46% market share nationally, with FNF's investment portfolio swelling to $5.5 billion. State insurance commissioners from California to New York scrutinized every detail. The Department of Justice conducted a preliminary review. But Foley had learned from decades of acquisitions: in a crisis, regulators prioritize stability over competition concerns. Better to have one strong player than multiple failing ones.

By the time the acquisition closed in early 2009, the competitive landscape had been permanently altered. The "Big Four" of title insurance had become the "Big Three," with FNF controlling nearly half the market. First American and Stewart Information Services were left to fight over the scraps. The company that had started with $6.2 million in revenue now had pro forma 2007 market share that dwarfed its nearest competitor by twenty percentage points.

The LandAmerica acquisition became a Harvard Business School case study in crisis opportunism. While competitors were laying off thousands and closing offices, FNF was consolidating its dominance at fire-sale prices. The 2008 financial crisis, which should have been catastrophic for a real estate-dependent business, instead became the moment FNF achieved unassailable market leadership. As Foley would later tell investors with characteristic understatement: "We tend to do our best work when others are panicking."

VI. Beyond Title: The Diversification Years (2000s–2010s)

The Jacksonville conference room in 2003 looked more like a tech startup's war room than a title insurer's boardroom. Whiteboards covered with system architecture diagrams, flow charts mapping payment processing, and Post-it notes tracking potential acquisition targets. Foley had decided that title insurance, despite its beautiful margins, was too cyclical, too dependent on real estate transactions. The empire needed diversification. The answer? Financial technology.

The opportunity came through Alltel's financial services division—a hodgepodge of payment processing and banking software assets that the telecom company wanted to shed. Foley saw what others missed: the bones of a fintech giant. FNF bought the division for $1.05 billion, roughly 7x EBITDA, a price that made Wall Street skeptical. But Foley wasn't buying current earnings; he was buying a platform for transformation.

This became the foundation for Fidelity National Information Services (FIS). Over the next two years, Foley deployed another $1.2 billion acquiring about a dozen companies, methodically building FIS's software capabilities. Sanchez Computer Associates brought core banking systems. Aurum Technology added payment processing. Certegy provided check verification services. Each acquisition was integrated into an increasingly powerful technology stack that could serve everything from community banks to global financial institutions.

The structural engineering was elegant. Old FNF was merged with and into FIS, after which the surviving entity changed its name back to Fidelity National Financial, Inc. By spinning off FIS as a separate public company while retaining a significant stake, FNF created a $10 billion market cap fintech leader while maintaining its title insurance core. FIS would eventually become larger than its parent, processing over 75 billion transactions annually and serving thousands of financial institutions worldwide.

But Foley's diversification ambitions extended beyond fintech. The company expanded into mortgage services, real estate technology, and eventually annuities and life insurance. Each move followed the same pattern: find an industry with stable cash flows, fragmented competition, and operational inefficiencies. Buy at reasonable multiples. Apply the FNF playbook. Generate superior returns.

The most audacious structural innovation came in 2014 with the creation of FNFV, a tracking stock designed to hold FNF's portfolio of non-title investments. This was essentially Foley's personal private equity vehicle trading publicly—a structure that would make Carl Icahn jealous. The portfolio included everything from restaurant chains (Del Frisco's, J. Alexander's) to casinos (Cannae's stake in Dun & Bradstreet).

In 2016, FNFV was spun off and renamed Cannae Holdings, with Foley and his team earning a 1.5% management fee on invested capital plus 15-20% carry above an 8% hurdle rate. Critics called it aggressive financial engineering. Foley called it alignment. "I eat my own cooking," he told skeptics. "When Cannae wins, I win. When it loses, I lose more."

The real estate technology investments proved particularly prescient. FNF backed companies digitizing every aspect of real estate transactions—from online notarization to blockchain-based title verification. While pure-play insurtechs burned through venture capital trying to "disrupt" title insurance, FNF was quietly funding the tools that would enhance, not replace, its core business. Why fight disruption when you can own it?

By the end of the 2010s, FNF had transformed from a monoline title insurer into a diversified financial services conglomerate. The company operated through four distinct segments: Title Insurance, Mortgage & Real Estate Services, Real Estate Technology, and Annuities & Life Insurance. The title business that generated 100% of revenues in 2000 now contributed less than 60%. The empire had evolved from horizontal consolidation to vertical integration to conglomerate diversification—each phase building on the last, each expansion creating new opportunities for the next.

VII. The Stewart Saga: Regulatory Defeat (2018–2019)

The press release dropped at 7 AM Eastern on March 19, 2018, sending shockwaves through the title insurance industry: FNF would acquire Stewart Information Services for $50 per share—$25 in cash and 0.6425 shares of FNF common stock, valuing the fourth-largest title insurer at $1.2 billion. At a 23% premium to Stewart's closing price, it seemed like a done deal. Bill Foley was about to eliminate his last meaningful competitor.

Stewart shareholders were ecstatic. The Houston-based company had struggled for years, losing market share to the Big Three while burning cash on failed technology initiatives. The combination would create an entity with over 43% market share nationally. For Foley, it was the capstone acquisition—eliminating the last independent player of scale and creating an essentially unassailable market position.

But this time, Foley had overplayed his hand. The Federal Trade Commission, which had largely ignored title insurance consolidation for decades, suddenly woke up. The numbers were simply too stark: the Big Four already controlled more than 85% of all title insurance sales. Post-merger, FNF-Stewart would have more market share than its two largest competitors combined. In certain states, the combined entity would control over 60% of the market.

The FTC's administrative complaint, filed in September 2018, read like a greatest hits of Foley's empire building. "Fidelity gained its dominant position through a series of acquisitions," the complaint noted, listing the Chicago Title, Commonwealth, and Lawyers deals like a rap sheet. The Commission argued that further consolidation would reduce competition for large commercial transactions where only the Big Four had the financial strength and national footprint to compete.

But the real death blow came from an unexpected source: New York regulators. The state's Department of Financial Services conducted its own analysis and concluded that the combined market share of approximately 50% would create "increased market power leading to greater profits than price competition and consumer choice." Translation: New York believed FNF-Stewart would have effective monopoly power to raise prices.

The New York rejection was particularly damaging because of the state's outsized importance in commercial real estate. Manhattan alone generated more title insurance premiums than most entire states. Without New York approval, the deal economics collapsed. FNF could theoretically proceed in other states, but running a national title insurer without New York was like running an airline without landing rights at JFK.

Internal FNF documents later revealed the depth of frustration. Foley had spent $50 million on deal costs, including an army of antitrust lawyers and economists arguing that title insurance was really a local, not national, market. They pointed to new entrants like Doma (formerly States Title) as evidence of continued competition. They offered divestitures in concentrated markets. Nothing worked.

On September 9, 2019, FNF and Stewart mutually terminated the merger agreement. The official statement was diplomatic: "changing regulatory environment" and "extended timeline for approval." But industry insiders knew the truth—Foley had finally hit the regulatory wall. The same consolidation playbook that had worked for 35 years had reached its limits.

The Stewart saga taught the industry a crucial lesson: there was now a ceiling on title insurance consolidation. FNF's 32.7% market share in the first half of 2020, with Stewart holding 10.1%, represented the effective maximum for any single player. The empire could grow vertically into adjacent businesses or improve operations, but the great horizontal roll-up was over. For the first time in his career, Bill Foley had been told "no" and made to stick. The question now was: what would the empire builder do when he couldn't build through acquisition?

VIII. Modern FNF: The Annuities Pivot & Current State

The 2021 analyst day presentation opened with an unusual slide: a life insurance company's actuarial tables. The title insurance analysts in the audience exchanged confused glances. Had they walked into the wrong meeting? Then Foley appeared on stage with his characteristic grin. "Ladies and gentlemen, let me introduce you to FNF's next act: becoming a balanced financial services company where title insurance is just one pillar of a three-legged stool."

The vehicle for this transformation was F&G Annuities & Life, acquired from HRG Group in 2020 for $2.7 billion. Where others saw a sleepy annuity writer with $30 billion in assets under management, Foley saw an uncorrelated earnings stream that could smooth out title insurance's violent cyclicality. When mortgage rates rose and real estate transactions plummeted, annuity sales soared as retirees sought guaranteed income. It was portfolio theory applied to corporate strategy.

The execution was vintage Foley. F&G's investment portfolio was repositioned from low-yielding corporate bonds to higher-returning structured products and private credit. Distribution was revolutionized, moving from captive agents to independent marketing organizations that could scale rapidly. Product innovation accelerated, with new indexed annuities that captured market upside while protecting downside. By 2024, F&G had achieved record assets under management of $65.3 billion, driven by record gross sales of $15.3 billion.

The transformation was remarkable: F&G contributed 38% of FNF's consolidated adjusted net earnings in 2024, up from 30% in 2023. During a period when rising interest rates crushed title insurance volumes, F&G's contribution kept overall earnings stable. Wall Street, initially skeptical of an title insurer owning an annuity business, began to appreciate the genius of the hedge.

Meanwhile, the core title business wasn't standing still. FNF's 32.7% market share in the first half of 2020 remained industry-leading, but maintaining that position required constant innovation. The company poured resources into digital transformation: AI-powered title searches that reduced processing time from days to hours, blockchain experiments for instant title verification, and mobile apps that allowed real estate agents to order title insurance with three taps.

The technology investments were defensive as much as offensive. Venture-backed insurtechs like Doma and Qualia were raising hundreds of millions to "disrupt" title insurance. Rather than dismiss these threats, FNF partnered with or acquired the promising ones while letting others burn through capital trying to recreate what FNF already had. "Let them spend venture money educating the market about digital solutions," Foley told his team. "We'll be the ones to actually deliver them at scale."

The competitive landscape had crystallized into a stable oligopoly. First American held second place with roughly 20% market share, focused on technology innovation. Old Republic commanded about 15%, content with steady profits and dividend payments. Stewart, post-failed merger, maintained its 10% share while exploring strategic alternatives. The remaining 20% was fragmented among regional players and new entrants, none with more than 2% share.

But the most intriguing development was Foley's continued deal-making at age 79. Through Cannae Holdings, his publicly traded investment vehicle, he orchestrated acquisitions in everything from software companies to restaurant chains. Despite activist investor criticism that Cannae was merely "Bill Foley's co-investment vehicle" and had seen shares decline nearly 50% over five years, Foley remained undeterred. The empire builder was still building, just through different vehicles.

Today's FNF is a testament to strategic evolution. From a small title insurer to a Fortune 500 conglomerate with dominant positions in title insurance and growing strength in annuities. The company that started with $6.2 million in revenue now generates over $12 billion annually. The stock that IPO'd at $14 in 1987 has delivered total returns exceeding 3,000% including dividends. And Bill Foley, still chairman, still dealing, remains one of the most successful yet unknown empire builders in American business history.

IX. Playbook: The Foley Method

Study Bill Foley's career across four decades, and patterns emerge like a military campaign map. The same tactics appear again and again: identify inefficient industries, consolidate through acquisitions, revolutionize operations, exploit crises, diversify strategically. It's a playbook so consistent you could set your watch to it, yet flexible enough to work across title insurance, financial technology, and annuities. As one competitor ruefully observed: "Foley is John Malone on steroids, one of the most active deal junkies in American business."

The serial acquirer's toolkit starts with pattern recognition. Foley doesn't look for innovative industries; he hunts for inefficient ones. Title insurance in 1984: 5% loss ratios hidden behind 75% distribution costs. Financial technology in 2003: banks paying millions for systems that should cost thousands. Annuities in 2020: sleepy mutuals generating 5% returns when 10% was achievable. Each time, the pattern was identical—operational inefficiency masking fundamental profitability.

The operational excellence through direct distribution became FNF's signature move. While competitors clung to independent agents like security blankets, Foley understood that controlling distribution meant controlling destiny. The math was irrefutable: why pay 75% commission to an independent agent when an employee could do the same work for salary plus 10% bonus? But the real insight was psychological—employees think like owners when they are owners, while agents think like mercenaries because that's what they are.

This led to Foley's most underappreciated innovation: employee ownership as competitive advantage. The 1985 decision to make FNF the nation's first employee-owned title insurer wasn't about feel-good management theory. It was cold, calculated brilliance. Employee-owners don't just process more transactions; they find new business, eliminate waste, and police fraud with zealous intensity. They turned what competitors saw as back-office drudgery into front-line profit centers.

The crisis-as-opportunity philosophy reached its apotheosis in 2008. While competitors panicked as real estate transactions evaporated, Foley went shopping. The LandAmerica acquisition—cherry-picking prime assets from bankruptcy for 23 cents on the dollar—became a Harvard case study in opportunistic capitalism. But this wasn't luck; it was preparation meeting opportunity. FNF had deliberately maintained a fortress balance sheet, minimal leverage, and diverse funding sources specifically to exploit the next crisis.

"Foley and his top aides made Fidelity the envy of the industry by achieving what no other major title insurer has been able to do," noted a Federal Reserve study on financial services consolidation. They created a virtuous cycle: scale begets efficiency, efficiency begets profits, profits fund acquisitions, acquisitions increase scale. Competitors couldn't break in because each element reinforced the others.

The conglomerate advantage in regulated industries deserves special attention. While Silicon Valley preaches focus, Foley built a deliberately diversified empire. Why? Because insurance regulators move slowly, think locally, and prioritize stability. A focused player is vulnerable to regulatory whims; a conglomerate can shift resources, cross-subsidize, and present multiple faces to multiple regulators. When New York blocked the Stewart acquisition, FNF simply pivoted to annuities. When title insurance slowed, F&G accelerated.

The management philosophy was military in its clarity: clear objectives, defined metrics, swift consequences. Managers received daily reports, weekly reviews, monthly deep dives. Miss your numbers? You're gone. Exceed them? You're wealthy. No politics, no excuses, no second chances. This wasn't cruel; it was clear. Everyone knew the rules, the score, and the stakes.

But perhaps Foley's greatest insight was understanding that boring businesses make the best empires. Title insurance, annuities, payment processing—these aren't sexy industries that attract top talent or venture capital. They're grinding, detailed, relationship-driven businesses with regulatory moats and switching costs. Precisely because they're boring, they're stable. Precisely because they're complex, they're defensible. Precisely because nobody wants to think about them, nobody tries to disrupt them—until it's too late.

The Foley Method isn't replicable through imitation; it requires a rare combination of operational excellence, financial engineering, and strategic patience. It's Warren Buffett's capital allocation married to Jack Welch's operational discipline, executed with George Patton's aggressive tactics. And at 79, still serving as chairman, still orchestrating deals through Cannae Holdings, Bill Foley continues to demonstrate that sometimes the best entrepreneurs aren't the ones who create new industries—they're the ones who perfect old ones.

X. Bull vs. Bear Case

The Bull Case: Fortress at Fair Price

Start with market position. FNF's 32.7% market share isn't just a number—it's a moat filled with regulatory crocodiles. After the Stewart acquisition failure, it's clear no competitor can achieve similar scale through consolidation. New entrants face state-by-state licensing requirements, massive technology investments, and the need to build title plants that FNF has accumulated over 175 years. The installed base is essentially permanent; when was the last time you heard of a title insurer losing significant market share?

The annuities diversification transforms FNF from cyclical to balanced. F&G's 38% contribution to adjusted net earnings provides ballast when real estate markets soften. Rising interest rates, which crush title insurance volumes, actually benefit annuity sales as consumers seek guaranteed returns. This natural hedge is already proven—during the 2022-2023 rate hiking cycle, F&G's record $15.3 billion in gross sales offset title weakness. The portfolio effect is powerful: lower volatility, higher multiple.

The operational excellence gap remains vast. FNF's direct distribution model generates combined ratios below 90% while competitors struggle to break 95%. The company processes more transactions per employee, generates more premium per dollar of expense, and converts more of that premium to free cash flow. This isn't temporary advantage; it's structural. Competitors can't replicate FNF's employee ownership culture or operational intensity without destroying their own businesses in transition.

Valuation remains reasonable despite the quality. At current multiples, investors are paying roughly 12x normalized title earnings plus getting F&G at book value. Compare that to specialty insurers like Markel (1.5x book) or RLI Corp (3x book) and FNF looks cheap. The dividend yield above 4% provides downside protection while you wait for the market to recognize the transformation from title insurer to diversified financial services.

The Bear Case: Yesterday's Empire

But empires age, and FNF shows signs of sclerosis. Start with Cannae Holdings, Foley's shadow empire, which has destroyed nearly 50% of shareholder value over five years. Activist investors correctly label it "Bill Foley's co-investment vehicle"—a structure that enriches management through fees while shareholders suffer. The governance questions are obvious: how can Foley fairly allocate opportunities between FNF and Cannae? The conflicts of interest are baked in.

The title insurance moat might be shallower than it appears. Venture-backed insurtechs have raised over $1 billion to attack the industry. While none have gained significant share yet, technology eventually wins. When Doma or Qualia figure out how to instantly verify title through blockchain or AI, what happens to FNF's army of researchers? The industry's 5% loss ratio suggests massive overcapacity—in efficient markets, such margins attract disruption like honey attracts bears.

Real estate dependency remains despite diversification. Yes, F&G provides some offset, but 60% of earnings still come from title insurance. When mortgage rates hit 8% in 2023, existing home sales plummeted to decade lows. Commercial real estate faces an office apocalypse with remote work potentially permanent. A serious real estate recession—think 2008 without the ability to buy competitors cheap—would savage earnings regardless of annuity sales.

The succession question looms largest. Bill Foley is 79 years old. He is FNF—the strategist, the dealmaker, the culture carrier. Who replaces an empire builder? The company has operational executives but no obvious visionary successor. History shows what happens to founder-dependent companies after the founder exits: best case, they become boring dividend stocks; worst case, they disintegrate as professional managers lack the founder's risk appetite and operational edge.

Regulatory constraints create a ceiling on growth. The Stewart rejection proved FNF can't grow title insurance through major acquisition. Organic growth in a mature industry might be 2-3% annually. F&G can scale, but annuities are commodity products with thin margins. Without Foley's deal-making magic, where does growth come from? The empire might have reached its natural borders.

The Verdict

Both cases have merit, but the balance tilts bullish for patient investors. FNF is that rare creature: a dominant franchise in a boring but essential business, trading at reasonable multiples, with proven crisis resilience and emerging earnings diversification. The bear concerns are real but manageable—technology disruption moves slowly in regulated industries, real estate cycles but always recovers, and even post-Foley, the operational advantages should persist for years.

The key insight: FNF is transitioning from growth story to value stock, from empire building to empire harvesting. That's not exciting, but it's profitable. Sometimes the best investments aren't the ones conquering new territories—they're the ones collecting rent on territories already conquered.

XI. Epilogue: What Would Happen Next?

The December 2024 board meeting will be remembered as a passing of the torch—or perhaps more accurately, the beginning of the torch-passing discussion. Bill Foley, approaching 80, still commands the room with military bearing and deal-maker's intensity. But for the first time, succession planning tops the agenda. The empire builder must contemplate what happens to empires when builders exit.

The succession challenge isn't finding someone who can run title insurance operations—FNF has plenty of capable executives who've internalized the operational playbook. The challenge is replacing Foley's three irreplaceable qualities: the deal-making instinct that spots value where others see problems, the political capital to navigate regulatory approvals, and the force of personality that makes employees run through walls. You can't promote someone to visionary.

The digital transformation imperative offers both threat and opportunity. FNF has invested hundreds of millions in technology, but the question remains: is it enough? The next generation of homebuyers won't tolerate three-day title searches and paper-intensive closings. The winner in digital title insurance might not be who has the best technology, but who can change consumer behavior fastest. FNF's advantage—distribution relationships with every major real estate broker—could become liability if brokers themselves get disintermediated.

Potential acquisition targets reveal strategic priorities. With horizontal consolidation blocked, FNF must think adjacently. Property and casualty insurance offers obvious synergies—same customers, similar distribution, complementary risk. Mortgage origination remains tempting despite previous mixed results. The real prize might be wealth management, creating cradle-to-grave financial relationships: title insurance at home purchase, annuities at retirement, wealth transfer at estate planning.

But the elephant in the room is blockchain—the technology that could theoretically eliminate title insurance entirely. Imagine property records immutably recorded on distributed ledgers, ownership transfers executing automatically via smart contracts, title verification happening instantly and costlessly. It sounds like science fiction until you remember that Estonia already runs its entire land registry on blockchain. FNF's response has been clever: fund blockchain experiments while lobbying for regulatory frameworks that ensure traditional insurers remain necessary for consumer protection.

The future of title insurance might not be about insurance at all, but about becoming the trust layer in digital real estate transactions. FNF could evolve from insuring against past title defects to guaranteeing entire transaction flows—identity verification, fund transfers, document execution, regulatory compliance. The company that started by protecting against forged deeds could end by making forgery technically impossible.

Key lessons emerge for entrepreneurs and investors. First, boring industries with regulatory moats create more wealth than sexy startups—Foley's net worth exceeds most Silicon Valley founders despite never gracing a magazine cover. Second, operational excellence beats strategic brilliance—FNF won through better execution of simple ideas, not breakthrough innovation. Third, crisis creates opportunity for the prepared—having capital and courage when others have neither is the ultimate competitive advantage.

The next chapter might be titled "The Professional Era." Without Foley's deal-making prowess, FNF likely becomes a steady-state cash flow machine—generating reliable returns, paying growing dividends, making small tactical acquisitions, but never again transforming industries. That's not failure; it's maturation. Every empire eventually stops expanding and starts optimizing.

Yet betting against Bill Foley has always been expensive. At 79, he still runs Cannae Holdings, still evaluates deals, still thinks in decades not quarters. The title insurance roll-up might be complete, but the empire builder's ambitions rarely are. Whether through FNF, Cannae, or some yet-unimagined vehicle, Foley will likely orchestrate one more transformation—one final deal to cement the legacy.

The most probable scenario: FNF becomes the Berkshire Hathaway of financial services—a collection of dominant franchises generating prodigious cash flow, run by professional managers but guided by an founding philosophy that outlasts the founder. The empire stops expanding geographically but deepens economically, using its title insurance cash cow to fund whatever comes next in American finance. That's not just a business model; it's a blueprint for permanent capital in an impermanent world.

XII. Recent News### **

Latest Quarterly Earnings**

FNF reported full year 2024 adjusted net earnings of $1.3 billion, or $4.63 per share, compared to $962 million, or $3.55 per share, for the year ended December 31, 2023. The strong performance was driven by both the Title and F&G segments delivering above expectations.

The Title Segment contributed $263 million and $877 million for the fourth quarter and full year 2024, respectively, compared to $174 million and $760 million for the fourth quarter and full year 2023, respectively. This represents a 51% increase in fourth quarter earnings and 15% increase for the full year, despite challenging market conditions with elevated mortgage rates.

The F&G Segment contributed $123 million and $475 million for the fourth quarter and full year 2024, respectively, with F&G contributing 38% of FNF's consolidated adjusted net earnings for the full year 2024 as compared to 30% in 2023. The annuities business has become an increasingly important earnings driver for the company.

Recent Acquisitions and Market Position

In October 2024, FNF announced the acquisition of the commercial operations of First Nationwide Title Agency ("FNTA"), a division of AMT Commercial Title Services and a subsidiary of AmTrust Financial Services. The acquisition of this significant New York City based team continues FNF's strategy of acquiring the best companies and talent in the industry and bringing them into its portfolio to better service commercial real estate clients.

As part of the acquisition, FNTA's key commercial leadership team will join FNF, including Steven Napolitano, who serves as FNTA's President and CEO with over 35 years of industry experience and will continue to lead the company's day-to-day operations under FNF's ownership.

F&G Performance and Strategic Growth

F&G achieved record assets under management before flow reinsurance of $65.3 billion at year end driven by record gross sales of $15.3 billion for the full year 2024, a 16% increase over 2023, with gross sales having more than tripled since 2020. During 2024, the company achieved record full year retail channel and pension risk transfer sales due to favorable market conditions and secular demand for products that is poised to persist.

Cannae Holdings Activist Situation

Cannae Holdings Inc., the investment firm led by FNF founder and Chairman William Foley II, is facing accusations of poor governance and a lack of strategic focus from activist investor Carronade Capital Management, with the firm pointing to actions it claims have contributed to a loss of almost $1 billion in shareholder value.

Carronade holds 2.9 million shares in Cannae and criticizes the company's "vague and undifferentiated" investment approach, condemning board actions including an accelerated equity vesting plan for directors if they are not reelected and a requirement for Cannae to repurchase half of Foley's shares "at a significant premium to market prices."

There has been no clear investment narrative for shareholders, with Cannae consistently described as "the Bill Foley co-investment vehicle," and company shares have declined nearly 50% over the past five years. Carronade has notified Cannae of its intent to nominate four independent directors at the company's 2025 annual meeting, setting the stage for a heated proxy battle.

Market Position and Operational Performance

The company maintains its position as the nation's largest title insurance company with industry-leading margins. FNF has continued to invest in the business despite the challenging real estate market—actively recruiting talent to drive revenue, making strategic acquisitions and investing in technology, all while maintaining industry leading margins, firmly believing in the long-term value of the title insurance business regardless of the cyclical nature of the real estate market.

The Title segment has significantly outperformed prior cycle troughs and is well positioned for the eventual upturn in the residential housing market once mortgage interest rates begin to normalize, with F&G serving as a strong growth engine expected to continue as they execute against their medium-term financial goals.

XIII. Links & Resources

SEC Filings and Investor Materials

- FNF Investor Relations: investor.fnf.com

- Latest 10-K and 10-Q Reports: SEC EDGAR Database

- Q4 2024 Earnings Call (February 21, 2025): Available on FNF investor site

- F&G Annuities & Life investor information: FG investor relations

Historical Documents and Industry Analysis

- Title Insurance Industry Reports: American Land Title Association (ALTA)

- FTC administrative complaint on Stewart merger (2018-2019)

- New York Department of Financial Services regulatory filings

- Federal Reserve studies on financial services consolidation

Related Company Resources

- Cannae Holdings Inc.: cannaeholdings.com

- Carronade Capital activist campaign materials (March 2025)

- Fidelity National Information Services (FIS) historical documents

- Black Knight Inc. acquisition history

Books and Long-Form Analysis

- Harvard Business School case studies on crisis acquisitions

- "The Title Insurance Industry: Competition, Consolidation, and Consequences" - Federal Reserve Research

- William P. Foley II profiles and interviews in financial press

Market Data and Analytics

- Real estate transaction volumes: National Association of Realtors

- Title insurance market share data: ALTA and state insurance departments

- Mortgage origination statistics: Mortgage Bankers Association

- Commercial real estate trends: CBRE and JLL research

Technology and Innovation Resources

- Doma (formerly States Title) investor materials

- Qualia technology platform documentation

- Blockchain in real estate: Estonia e-Residency program

- PropTech investment trends: CB Insights

Regulatory Filings and Decisions

- State insurance department rate filings

- FTC merger review documents

- CFPB title insurance market studies

- State-by-state regulatory frameworks

Management Profiles and Interviews

- William P. Foley II speeches and presentations

- Michael Nolan (CEO, Title Group) industry commentary

- Chris Blunt (CEO, F&G) investor day presentations

- Executive compensation proxy statements

Competitor Analysis

- First American Financial Corporation (FAF)

- Old Republic International (ORI)

- Stewart Information Services (STC)

- Regional title insurers market analysis

Real Estate and Economic Data

- Federal Reserve Economic Data (FRED)

- Case-Shiller Home Price Indices

- Mortgage rate forecasts and historical data

- Commercial real estate default rates

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube