Lennar Corporation: Building the American Dream Machine

I. Introduction & Episode Roadmap

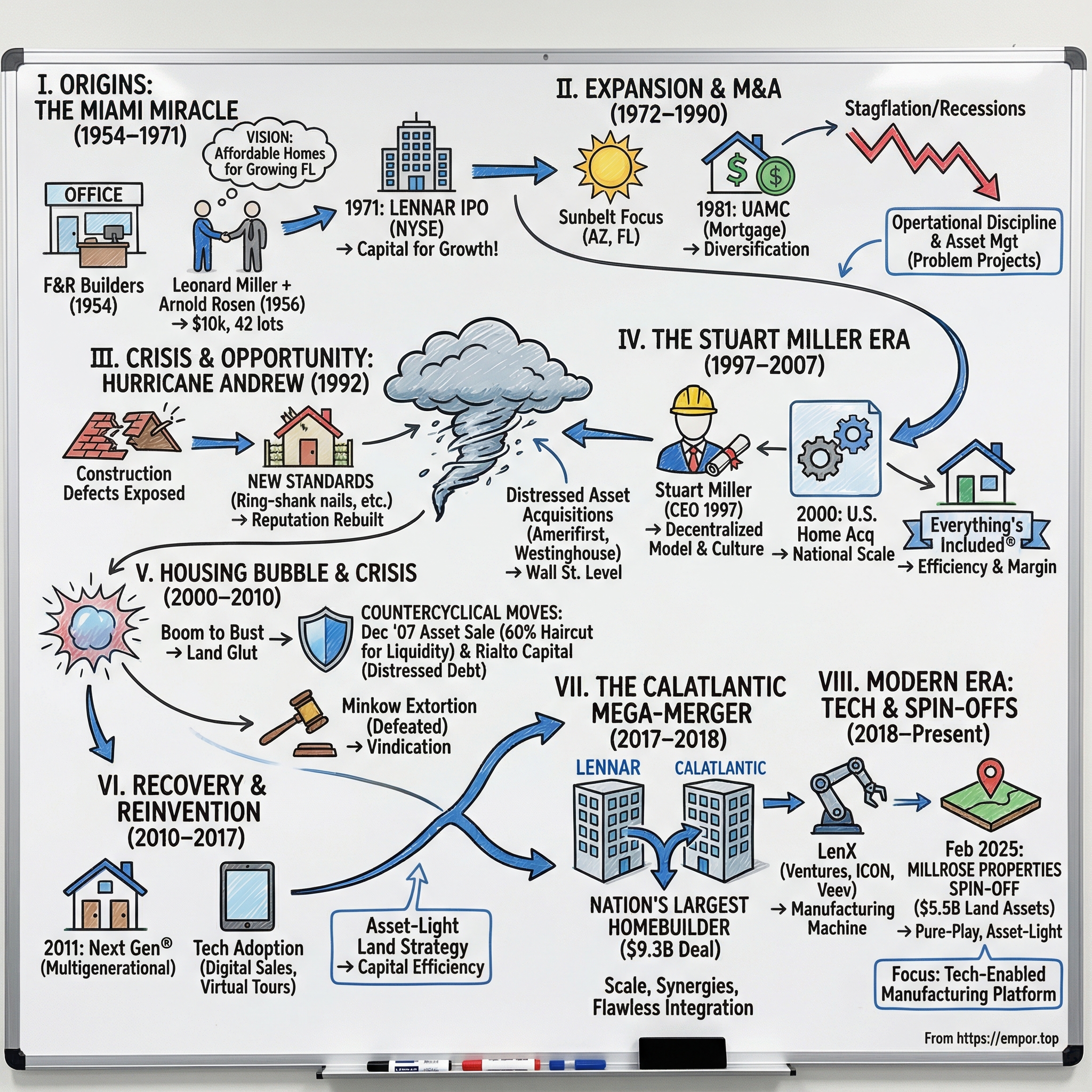

Picture this: It's 1956 in Miami. A 23-year-old entrepreneur named Leonard Miller walks into a small construction office with $10,000 in hand and a vision that seems almost quaint by today's standards—he wants to build homes for middle-class families moving to Florida. Fast forward to 2024, and that modest investment has morphed into Lennar Corporation, America's second-largest homebuilder with $34 billion in annual revenue, operating across 26 states and 75 markets.

The story of Lennar isn't just about building houses—it's about constructing an empire through the most brutal economic cycles imaginable. While competitors collapsed during the 2008 financial crisis, Lennar emerged stronger. When Hurricane Andrew devastated South Florida in 1992, threatening the company with extinction through lawsuits, they transformed disaster into competitive advantage. Today, as the company spins off its $8 billion land portfolio into a separate entity and doubles down on technology investments, we're witnessing yet another reinvention.

Here's the central question that should fascinate any student of business: How did two Miami builders create a Fortune 500 homebuilding machine that has not only survived but thrived through seven decades of boom-bust real estate cycles? The answer involves a rare combination of operational discipline, strategic M&A, and an almost mystical ability to time the market. This is a story about family dynasties (the Millers still run the company), Wall Street engineering, and the relentless pursuit of scale in America's most cyclical industry.

What makes Lennar particularly compelling for investors today? The company sits at Fortune 500 #119, commands a ~$47 billion market cap, and operates with a vertically integrated model that would make Andrew Carnegie jealous. They don't just build homes—they finance them, insure them, and increasingly, rent them out. As we'll explore, this isn't your grandfather's homebuilder; it's a sophisticated real estate platform disguised as a construction company.

II. Origins: The Miami Miracle (1954–1971)

The humid Miami air in 1954 carried the scent of opportunity. Post-war America was booming, and nowhere was the promise more palpable than in South Florida. Into this environment stepped Gene Fisher and Arnold P. Rosen, establishing F&R Builders with a straightforward mission: build homes for the families flooding into the Sunshine State. They founded F&R Builders in 1954, but the real magic wouldn't happen for another two years.

In 1956, Leonard Miller, a 23-year-old entrepreneur who owned 42 lots in Miami-Dade County, Florida, invested $10,000 and partnered with the company. Miller wasn't just another investor—he was a force of nature with an intuitive understanding of land development and marketing that would prove transformative. Miller participated in several joint ventures with Arnold Rosen, adding his land management and marketing skills to Rosen's proven technical ability to build low- and medium-priced single-family homes.

The partnership clicked immediately. While Rosen brought construction expertise honed over a decade of Miami homebuilding, Miller contributed something equally valuable: vision and hustle. The young entrepreneur understood that Florida wasn't just experiencing temporary growth—it was undergoing a permanent transformation. Air conditioning had made the state livable year-round, the interstate highway system was connecting it to the Northeast, and retirees were discovering they could trade snow for sunshine.

By the mid-1960s, the partnership of Miller and Rosen had proved to be a boon to F & R Builders' growth, enabling the company to become the largest home builder in the greater Miami area in roughly a decade. Their target market was brilliantly chosen: first-time homebuyers and the growing wave of retirees seeking affordable Florida homes. This wasn't luxury development—it was volume business, and they executed it with precision.

The transformation from local builder to public company reveals the ambition driving Miller and Rosen. In 1969, Lennar reached an equity base of $1 million, and by 1971, Miller and Rosen changed the name to Lennar Corporation. The name itself tells a story: Lennar is a portmanteau of the first names of two of the company's founders, Leonard Miller and Arnold Rosen. It was personal, memorable, and suggested partnership—qualities that would define the company's culture for decades.

That year the firm became a public company via an initial public offering, raising $8.7 million. For context, $8.7 million in 1971 dollars equals roughly $65 million today—substantial capital for a regional homebuilder, but modest compared to what Lennar would become. The IPO wasn't just about money; it was about legitimacy and creating a currency for acquisitions. Miller and Rosen understood that to build a national homebuilder, they needed Wall Street's backing.

The early Lennar story establishes patterns that would define the company for the next five decades: opportunistic partnerships, strategic use of capital markets, and an uncanny ability to ride demographic waves. As we'll see, the decision to go public in 1971 set the stage for an acquisition spree that would transform a Miami builder into a national powerhouse.

III. Geographic Expansion & Early M&A (1972–1990)

The moment Lennar stock began trading on the New York Stock Exchange in 1972, Miller and Rosen had a new weapon: acquisition currency. Wall Street legitimacy meant more than just prestige—it meant access to capital markets that would fuel two decades of aggressive expansion. It was listed on the New York Stock Exchange in 1972.

Their first major move came swiftly. In 1973, when Lennar entered the Phoenix, Arizona, market with the acquisition of Mastercraft Homes, Inc., for approximately $2 million, and Womack Development Company, both established home builders in the greater Phoenix area. This wasn't random geography—Phoenix represented the Sunbelt thesis in its purest form. The city was exploding with retirees and young families fleeing cold winters and high taxes. Shortly thereafter, the company established operations in the Midwestern United States, purchasing Bert L. Smokler & Company, based in Detroit, Michigan, and Dreyfus Interstate Development Corp., based in Minneapolis–Saint Paul.

But timing, as they say, is everything. The mid-1970s brought stagflation, oil shocks, and a brutal housing recession. Lennar was not immune to the negative conditions afflicting many home builders and incurred its share of losses; however, the downturn in housing construction starts did provide the company's management time to integrate the recent acquisitions into Lennar's operations and further develop the company's business philosophy.

This forced pause proved transformative. Miller and Rosen didn't just wait for recovery—they rethought their entire business model. An intrinsic objective of this philosophy, created in part during F & R Builders' rise during the 1950s and strikingly germane during the downswing now restraining the company's growth, was the need for Lennar to develop a core earnings base unrelated to the frequently volatile housing construction market. This insight—that pure homebuilding was too cyclical to sustain consistent growth—would drive Lennar's strategy for decades.

By 1977, as the housing market recovered, Lennar's geographic footprint told a clear story. Florida still represented Lennar's primary market, accounting for 66 percent of its total housing deliveries, whereas its Midwest and Arizona markets accounted for 15 percent and 19 percent, respectively. But the company was evolving beyond single-family homes. By this time, in the late 1970s, the company was responding to changing consumer housing needs by constructing townhouses and condominiums.

The real breakthrough came in 1981 when Lennar made a move that would fundamentally alter its DNA. Universal American Mortgage Company (UAMC) has been making homeownership possible since 1981. Lennar diversified further, entering the home mortgage business and originating what would later become Lennar Financial Services, Inc. In response to the S & L crisis, Lennar expands its mortgage financing business with UAMC Universal American Mortgage Company (UAMC); this is the beginning of Lennar Financial Services. This wasn't just about capturing more revenue per transaction—it was about controlling the entire customer experience and creating recession-resistant income streams.

The acquisitions continued through the 1980s with surgical precision. Lennar acquired H. Miller & Sons in 1984 for $24 million. Then came a particularly shrewd move: In January 1989, the company acquired Richmond American Homes of Florida for $18 million. Each acquisition expanded either geographic reach or operational capability, but never both simultaneously—a discipline that prevented the organizational chaos that plagued many roll-up strategies.

What's remarkable about this period is how Lennar earned trust from Florida's banking establishment. Initially, Lennar gained entry into these other business sectors as a reward for its financially conservative and prudent management policies, which earned the respect of several lending institutions in Florida. These lending institutions asked Lennar to assume management responsibility for problem projects in their portfolios, leading, in many cases, to the acquisition of such projects by Lennar and signaling the beginning of the company's involvement in asset management.

By 1990, Lennar had transformed from a Miami homebuilder into a diversified real estate platform operating across multiple states with integrated financial services. The company had survived its first major recession, established a presence in key growth markets, and built the operational infrastructure for much larger ambitions. As the 1990s dawned, however, Mother Nature had other plans—and Hurricane Andrew would test whether Lennar's carefully constructed empire could withstand a different kind of storm.

IV. Crisis & Opportunity: Hurricane Andrew & The 1990s

August 24, 1992, 5:05 AM. Hurricane Andrew makes landfall in Homestead, Florida, with sustained winds of 165 mph. Within hours, entire neighborhoods built by South Florida homebuilders are reduced to splinters. The damage is catastrophic—but the real disaster for Lennar is about to begin. In the hurricane's aftermath, homeowners discover that many houses, including some built by Lennar, failed catastrophically not because of the storm's unprecedented power, but due to construction defects: missing hurricane straps, inadequate roof attachments, substandard materials.

In 1992, following Hurricane Andrew, the company faced several lawsuits from homeowners alleging careless building quality. The lawsuits threatened more than financial damage—they challenged Lennar's reputation at its core. For a company that had spent four decades building trust in Florida, this was an existential crisis. Local news stations ran nightly segments showing Lennar homes with roofs peeled off like sardine cans. Class action attorneys circled like vultures.

Yet in February 1992—just months before Andrew struck—Lennar had made a move that would prove prescient. In February 1992, the company acquired Amerifirst's $1 billion real estate portfolio in a joint venture with Morgan Stanley. This wasn't homebuilding; it was distressed asset management, and the timing couldn't have been better. While competitors struggled with hurricane lawsuits, Lennar had a massive new revenue stream from managing troubled real estate.

The Amerifirst deal revealed Lennar's evolving sophistication. Working with Morgan Stanley signaled that Lennar could play at Wall Street's level, structuring complex transactions that went far beyond building houses. The portfolio included everything from failed condo projects to half-built subdivisions—the detritus of the late-1980s real estate bust. Lennar's team, hardened by years of Florida's boom-bust cycles, knew how to extract value from these disasters.

Then came an even bigger swing. In 1993, Lennar partnered again with institutional capital to acquire a $2 billion loan portfolio from Westinghouse—yes, the same Westinghouse that made refrigerators and nuclear reactors had gotten catastrophically over-extended in real estate lending. These two acquisitions, concluded in the two years prior to 1993, gave Lennar an interest in real estate management assets valued at more than $4 billion, complementing an already solid combination of business interests that provided an enviable foundation for the company's future.

But Lennar's response to Hurricane Andrew went beyond financial engineering. The company implemented new construction standards that exceeded Florida's building codes. They started using ring-shank nails instead of smooth nails, added more hurricane straps, and reinforced roof-to-wall connections. Marketing materials began emphasizing "Hurricane-Resistant Construction Features." What could have destroyed the company instead became a differentiator. Lennar homes built after 1992 became known as the safest in Florida—a reputation that translated directly into pricing power.

The mid-1990s brought a series of strategic acquisitions that expanded Lennar's footprint in California, the promised land of American homebuilding. In 1995, two major deals reshaped the company's geographic profile. First came Friendswood Development Company, acquired from Exxon—another oil giant retreating from real estate adventures. Friendswood brought massive land holdings in Texas, particularly around Houston. Then came the acquisition of Bramalea's California operations, giving Lennar serious scale in the nation's largest housing market.

The Bramalea deal deserves special attention. Bramalea was a Canadian company that had aggressively expanded into California during the 1980s boom, only to get crushed in the early 1990s recession. Lennar picked up their California operations at a fraction of replacement cost, acquiring not just land and partially completed projects, but also local teams who knew how to navigate California's byzantine approval processes. This pattern—buying quality assets from distressed sellers—would become a Lennar signature move.

By 1996, as the economy roared back to life, Lennar had quietly assembled one of the industry's strongest portfolios. The company operated in Florida, Texas, California, Arizona, and several other states. It had survived Hurricane Andrew and transformed disaster into competitive advantage. The balance sheet was clean, operations were humming, and the stage was set for the next generation of leadership. Leonard Miller's son Stuart was ready to take the helm, and he had very different ideas about what Lennar could become.

V. The Stuart Miller Era Begins (1997–2007)

Picture the scene: Harvard-educated lawyer returns to family business, starts mowing lawns. That's Stuart Miller in 1982, and if it sounds like a reverse Horatio Alger story, you're missing the point. At the age of 11 Miller began mowing the lawns of Lennar's model houses. By his teens Miller was working odd jobs around Lennar's construction sites to save money for a car. The boss's son wasn't proving he could rough it—he was learning the business from the ground up.

Miller left Florida for Harvard University. After receiving his undergraduate degree, Miller attended the University of Miami Law School, being graduated in 1982. Having achieved his educational goals, Miller returned to the company he had grown up with. Unlike many second-generation executives who coast on family legacy, Miller brought intellectual firepower and fresh perspective to a company that needed both.

From 1991 to October 1997, he was President of both these business segments and the primary force behind their growth and success during that time. He became CEO of Lennar in April 1997 The timing was perfect—or perfectly terrifying. The late 1990s housing market was heating up, technology was disrupting every industry, and Lennar needed someone who could think beyond just building boxes.

Miller's first major move as CEO revealed his strategic ambition. In October 1997, Lennar Corporation spun off its commercial real estate investment, financial, and management activities into LNR Property Corporation, and the company became separately listed on the NYSE. Miller served as Chairman of the Board of LNR until the sale of LNR in February 2005. This wasn't just financial engineering—it was philosophical clarity. By separating the volatile commercial real estate business from stable homebuilding, Miller created two pure-play companies that investors could value appropriately.

But what truly set Miller apart was his management philosophy, which seemed ripped from a Silicon Valley playbook rather than a traditional homebuilder. At the same time he made extensive efforts to foster an atmosphere of creativity and fun in and around the office. Miller believed that empowered and happy employees were vital to the success of the company. Early in his career with Lennar, Miller attended a seminar at the Disney Institute, a management training program run by Walt Disney Company.

The Disney influence manifested in unexpected ways. For many employees Miller's management style gave everyday business an unexpected twist at Lennar's Miami headquarters. On Fridays, before regularly scheduled meetings, Miller played music and danced with employees. He did not assign parking for executives and had no reserved space himself. Miller also instituted the production of lighthearted holiday videos that were distributed and shown to all Lennar employees to laud their accomplishments and encourage further success in the upcoming year.

If dancing before meetings sounds frivolous, consider the results. Under Miller's leadership, Lennar perfected a decentralized operating model that balanced autonomy with accountability. Each of Lennar's 50 divisions sent Miller a monthly, one-page report showing whether it was meeting its financial goals. One page. Fifty divisions. Monthly. This wasn't micromanagement—it was radical simplification that forced division presidents to focus on what mattered.

The operational discipline extended to capital allocation. Miller said that his process of determining whether an acquisition would work was to analyze whether the acquisition would make Lennar a better company. Miller conducted extensive financial, cultural, and marketing research. This sounds obvious, but in the go-go late 1990s and early 2000s, many homebuilders were acquiring for size alone. Miller was playing a different game.

In 2000, Lennar made its biggest bet yet: acquiring U.S. Home Corporation. U.S. Home had been the nation's largest homebuilder through much of the 1970s and 1980s but had struggled with profitability. The acquisition doubled Lennar's size overnight, but more importantly, it brought operational capabilities and geographic reach that would have taken a decade to build organically.

Then came the innovation that would define Lennar's consumer strategy: Everything's Included®. Introduced in the early 2000s, this wasn't just a marketing gimmick. Lennar began including thousands of dollars of upgrades—granite countertops, stainless steel appliances, premium flooring—as standard features. The genius wasn't generosity; it was operational efficiency. By standardizing options, Lennar could negotiate better prices with suppliers, reduce construction complexity, and eliminate the upgrade center profit leakage that plagued competitors.

The company's operations included house construction and sales, land development, mortgage financing, title insurance, closing services, insurance agency services, high-speed Internet access, cable television, and alarm installation and monitoring services. Miller understood that by diversifying Lennar's operations, he could tap into all the needs of house buyers and provide them with a complete service platform.

By 2006, as housing prices reached astronomical levels, Lennar was generating over $16 billion in revenue. The company had become a fully integrated real estate machine, capturing profit at every step of the homebuying journey. Miller had transformed his father's regional builder into a national powerhouse. But storm clouds were gathering, and what happened next would test whether Miller's cultural innovations and operational discipline could survive the ultimate stress test.

VI. The Housing Bubble & Financial Crisis (2000–2010)

The year 2000 began with triumph. Lennar acquired U.S. Home Corporation for about $1.2 billion, expanding the company's operations into New Jersey, Maryland, Virginia, Minnesota, Ohio and Colorado. By the end of that year, the acquisition gave Lennar housing revenues of almost $5 billion. This wasn't just growth—it was transformation. U.S. Home, once the nation's largest homebuilder, brought national scale and operational expertise that catapulted Lennar into the industry's top tier.

The early 2000s saw housing prices climb at rates that defied gravity. Phoenix homes doubled in value between 2002 and 2006. Miami condos sold for $1,000 per square foot. Las Vegas builders held lotteries for the right to buy new homes. Lennar, like every major builder, gorged on land, leveraged up, and built as fast as construction crews could pour foundations. By 2006, the company was generating over $16 billion in revenue—a tenfold increase from a decade earlier.

But Stuart Miller sensed something was wrong. While competitors bragged about land positions at investor conferences, Miller began quietly de-risking. In the years leading up to the crisis, Lennar was expanding aggressively, acquiring land and properties and building homes in some of the fastest-growing markets in the United States. When the crisis hit, the company was hit hard, with plummeting home prices and a credit crunch that made it difficult to secure financing for new projects. However, under the leadership of Stuart A. Miller, Lennar was able to weather the storm and emerge stronger than ever.

The key move came in December 2007, a decision that would save the company. In December 2007, during the subprime mortgage crisis, the company sold an 80% interest in 11,000 properties for 40% of their previously stated book value to Morgan Stanley. Think about that math: Lennar took a 60% haircut on book value to get liquid. Competitors called it panic selling. Miller called it survival.

In 2007, Lennar founded Rialto Capital Management, which was originated to acquire distressed real estate and mortgage debt. This was classic countercyclical thinking—while bleeding from their homebuilding operations, Lennar was positioning to profit from others' distress. Rialto would eventually manage billions in distressed assets, generating fees that helped offset homebuilding losses.

The numbers from 2008 tell the story of corporate carnage. Lennar reported losses of over $1.1 billion in net income in 2008, down from gains of $593.8 million in 2006. But unlike many competitors who filed for bankruptcy or were acquired at fire-sale prices, The company, long regarded a smart cycle timer, however, was able get by, in part by selling off assets at lower prices than they cost.

Then, in January 2009, came an attack from an unexpected quarter—one that would test whether Lennar could survive a different kind of crisis. In 2009, Minkow issued a report accusing major homebuilder Lennar of massive fraud, claiming that irregularities in the company's off-balance-sheet debt accounting were evidence of a massive Ponzi scheme. Minkow accused Lennar of not disclosing enough information about this to its shareholders, and also claimed a Lennar executive had taken out a fraudulent personal loan. In an accompanying YouTube video, he denounced Lennar as "a financial crime in progress" and "a corporate bully." Lennar's stock plummeted in the wake of Minkow's reports, tumbling from $11.57 a share to $6.55 in two weeks.

Barry Minkow wasn't just any critic. The convicted fraudster-turned-pastor had reinvented himself as a corporate fraud investigator, and his accusations carried weight with media and investors still shell-shocked from Enron and WorldCom. In 2008 and 2009, former businessman and convicted felon Barry Minkow engaged in an extortion scheme, spreading false information about the company that resulted in its stock price falling 26% in one day. Minkow was sentenced to 5 years in prison and was ordered to pay $584 million in restitution.

The truth was more sordid than anyone imagined. Minkow issued the report after being contacted by Nicholas Marsch, a San Diego developer who had filed two lawsuits against Lennar for fraud. The Los Angeles Times obtained a copy of the plea agreement, in which Minkow admitted to issuing his FDI report on Lennar at Marsch's behest. According to the agreement, Marsch offered to have Minkow retract his report if Lennar paid him in cash and stock. It also said that Minkow's report triggered a bear raid which temporarily reduced the market capitalization of Lennar by $583 million.

What made the scheme particularly insidious was its timing. In or around November 2008, the Minkow defendants entered into an agreement with the Marsch defendants to extort Lennar. The Minkow defendants and the Marsch defendants agreed to manipulate the public securities markets to harm the Lennar plaintiffs' business and reputation in an effort to force the Lennar plaintiffs to pay millions of dollars to the Marsch and Minkow defendants. They attacked when Lennar was most vulnerable, during the worst housing crisis since the Great Depression.

But Lennar fought back with characteristic aggression. The company didn't just defend itself—it went on offense, pursuing criminal charges and civil litigation. According to court records, Minkow had shorted Lennar stock, buying $20,000 worth of options in a bet that the stock would fall. Even more seriously, he also bought Lennar stock after his FDI report, believing the stock would rebound after its dramatic plunge. Minkow initially denied doing this, only to be forced to recant when confronted with trading records.

The vindication was complete. "The jury award represents a complete vindication of Lennar's reputation and good name," said Lennar CEO Stuart Miller. A Florida jury has awarded Miami homebuilder Lennar $1 billion in damages stemming from an alleged extortion scheme that resulted in phony accusations against an Orange County-based executive, the company announced Tuesday. Monday's civil court judgment is the second in two years stemming from Lennar's defamation lawsuit against La Jolla developer Nicolas Marsch III, his company, Briarwood Capital LLC, and ex-con Barry Minkow, whom Marsch allegedly hired to defame the builder. He was ordered in 2011 to pay Lennar $584 million in civil damages.

One of the key strategies that Lennar employed during the crisis was diversification. The company had traditionally focused on building single-family homes, but in the wake of the crisis, it began to explore other areas of the real estate market. While competitors retreated to their core markets, Lennar expanded into distressed debt, multifamily development, and asset management. By 2010, as the market bottomed, Lennar had not just survived—it had positioned itself to dominate the recovery.

VII. The Recovery & Reinvention (2010–2017)

The spring of 2011 marked a turning point. While competitors were still licking their wounds from the financial crisis, Lennar launched something revolutionary in Phoenix: The nation's largest homebuilder pioneered the Next Gen model in Phoenix, Arizona in 2011. Next Gen is best described as a home within a home, offering a private suite providing all the essentials multigenerational families need to work, learn, live and have a sense of independence.

The timing was perfect. An increasing number of homebuyers are caring for aging parents, or housing a daughter or son who's graduated from college and is seeking a full-time job while juggling student loan debt. Add in cultural influences and it's not surprising that approximately 76.4 million American households — a statistic cited by the U.S. Census Bureau for 2009-2011 — contain three or more generations under one roof. Lennar wasn't just building homes; they were solving a societal problem.

Next Gen debuted with one model, Evolution, in Gilbert's Layton Lakes that is still built today. In 2011, the Evolution was priced at $289,900 for 2800 sq ft. Today, Lennar sells 8 different versions of their best-selling model, ranging from 1,929 sq. ft in the low $400,000s to 3,520 sq ft starting in the high $600,000s. The concept evolved from a single prototype to a core product line that would drive billions in revenue.

Alan Jones, Arizona Division President of Lennar, introduced the Next Gen model to the Valley of the Sun. "Ten years ago, when we held the grand opening for our first Next Gen home, customers had never heard of it before and it required a lot of explanation," said Jones. "Today, Next Gen seems to be a household name. It doesn't need any explanation, customers come out specifically looking for it!"

The genius of Next Gen wasn't just the product—it was the insight. The Great Recession, in part, prompted the rise in multigenerational living and Lennar understands that. While other builders were trying to return to 2006's product mix, Lennar recognized that American family structures had permanently changed. Boomerang kids, aging parents, remote work—the traditional single-family home no longer fit how Americans actually lived.

Meanwhile, Lennar was building an entirely new business vertical. Founded in 2011, Quarterra, previously known as Lennar Multifamily Communities, offers rental apartment communities nationwide for those who are not yet ready to buy a home. This wasn't a side project—it was strategic positioning for demographic reality. Millennials weren't buying homes at the same rate as previous generations, but they still needed quality housing. Lennar would provide it and capture the economics either way.

The operational excellence that Stuart Miller had instilled was paying dividends. While competitors struggled with quality control and customer satisfaction coming out of the recession, Lennar refined its processes. The Everything's Included® approach, introduced years earlier, was perfected during this period. By standardizing features and eliminating the traditional options process, Lennar reduced cycle times, improved margins, and delivered a better customer experience.

Technology adoption accelerated. While the construction industry remained stubbornly analog, Lennar invested heavily in digital capabilities. Online sales centers, virtual tours, dynamic pricing models—capabilities that would prove invaluable during COVID-19 were being built in 2015. The company wasn't just recovering from the last crisis; it was preparing for the next one.

Land strategy during this period revealed Lennar's sophisticated approach to capital allocation. Instead of buying land outright, the company increasingly used options and joint ventures, reducing capital requirements and risk. This asset-light approach meant Lennar could control more lots with less capital, improving returns on equity that had been decimated during the downturn.

By 2016, the recovery was in full swing, and Lennar was firing on all cylinders. But Stuart Miller wasn't satisfied with organic growth. He saw an industry ripe for consolidation, with smaller builders lacking the scale to compete and larger builders hesitant to make bold moves. The stage was set for Lennar's most audacious acquisition yet.

VIII. The CalAtlantic Mega-Merger (2017–2018)

October 30, 2017. Stuart Miller picks up his phone to call CalAtlantic CEO Larry Nicholson. The conversation had been months in the making, but the moment of decision had arrived. "Larry," Miller says, "let's build something historic." Within hours, both boards would unanimously approve a definitive merger agreement pursuant to which each share of CalAtlantic stock will be exchanged for 0.885 shares of Lennar Class A common stock in a transaction valued at approximately $9.3 billion, including $3.6 billion of net debt assumed.

The scale of the deal was breathtaking. The business combination will create the nation's largest homebuilder with the last twelve months of revenues in excess of $17 billion and equity market capitalization, based on current market prices, of approximately $18 billion. The combined company will control approximately 240,000 homesites and will have approximately 1,300 active communities in 49 markets across 21 states, where approximately 50% of the U.S. population currently lives.

CalAtlantic itself was the product of consolidation. CalAtlantic, which is headquartered in Virginia and California, was formed in 2015 with the merger of Ryland Group and Standard Pacific Corp. This wasn't just acquiring a company—it was absorbing two storied homebuilding franchises with decades of operational expertise and market relationships.

The math made the strategic logic irrefutable. Based on the closing price of Lennar's Class A common stock on the NYSE on October 27, 2017, the implied value of the stock consideration is $51.34 per share, representing a 27% premium to CalAtlantic's closing price that same day. For CalAtlantic shareholders, it was a generous premium. For Lennar, it was a bargain for instant national dominance.

The synergy targets were aggressive but achievable. It is currently anticipated that the transaction will generate annual cost savings and synergies of approximately $250 million, with approximately $75 million achieved in fiscal year 2018. These synergies are expected to be achieved through direct cost savings, reduced overhead costs and the elimination of duplicate public company expenses. Additional savings are also expected through production efficiencies, technology initiatives, and the roll out of Lennar's digital marketing and dynamic pricing programs.

But the real genius was in the deal structure. Stockholders had the option to receive $48.26 per share in cash instead of Lennar stock with regard up to 24,083,091 shares, and a major CalAtlantic stockholder had agreed that to the extent stockholders did not elect to receive cash with regard to the maximum number of shares, the major stockholder would receive $48.26 per share in cash for the remainder of the 24,083,091 shares. This cash election mechanism gave stockholders flexibility while ensuring Lennar wouldn't be overwhelmed with cash requirements.

The voting agreements locked up the deal. Stuart Miller and the Miller Family Trusts have agreed to vote their 41.4% voting interest in Lennar in favor of the merger. MP CA Homes LLC, an affiliate of MatlinPatterson Global Opportunities Partners III L.P., has agreed to vote its 25.4% voting interest in CalAtlantic in favor of the merger. With controlling shareholders on both sides committed, the deal was essentially done before it was announced.

Execution was flawless. The transaction is subject to approval by Lennar and CalAtlantic stockholders. When the votes came in February 2018, the approval was overwhelming: The transaction, which is in the form of a merger of CalAtlantic into a wholly-owned subsidiary of Lennar, was overwhelmingly approved today by both companies' stockholders. Lennar saw 99.4% approval, while CalAtlantic hit 99.9%—as close to unanimous as public company votes get.

February 12, 2018, the merger closed. Therefore, the merger consideration will consist of approximately $1.16 billion in cash, 82,731,943 shares of Lennar Class A common stock and 1,654,639 shares of Lennar Class B common stock. Based on closing prices reported on the New York Stock exchange on Friday, February 9, 2018, the value of the Lennar Class A and Class B common stock that will be issued in the merger totaled $4.9 billion.

Stuart Miller's statement at closing captured the moment: "We are extremely pleased to announce the completion of this strategic combination with CalAtlantic, creating the nation's leading homebuilder. This combination benefits from overall economic strength, driven by low unemployment, rising wages, favorable tax reform, higher consumer confidence and strong housing demand."

The integration proceeded with military precision. CalAtlantic's operations were absorbed market by market, with best practices from both companies adopted across the platform. Digital marketing capabilities were rolled out nationally. Supply chain contracts were renegotiated with newfound scale. The promised synergies materialized ahead of schedule.

By year-end 2018, Lennar had transformed. The combined company sold 40,792 homes last year, according to the companies' separate SEC filings. D.R. Horton sold 40,309 homes. For the first time in decades, Lennar was America's largest homebuilder by units sold. The CalAtlantic merger wasn't just successful—it was transformative, creating a homebuilding colossus positioned to dominate the next decade.

IX. Modern Era: Technology, Innovation & Spin-offs (2018–Present)

April 2018. Stuart Miller steps into his new role as Executive Chairman, passing the CEO baton to Rick Beckwitt while remaining deeply involved in strategic direction. The transition signals not retirement but evolution—Miller wants to focus on transforming Lennar's business model for the next decade. His vision: turn America's largest homebuilder into an asset-light manufacturing machine.

The strategy was counterintuitive. While competitors hoarded land as a competitive moat, Miller saw land ownership as capital inefficiency. Why tie up billions in dirt when you could deploy that capital into technology, operations, and higher-return activities? The solution would take years to execute, but the destination was clear: separate the land business from the homebuilding business.

Meanwhile, Lennar was building something unprecedented in homebuilding: a venture capital arm. The same year, Lennar developed a venture capital arm, Lennar Ventures, dubbed LenX. This wasn't corporate innovation theater—it was serious capital deployment into technologies that could transform construction. In 2021, LenX announced strategic partnerships with companies ICON and Veev. ICON brought 3D printing technology for homes. Veev promised modular construction that could cut build times by 50%.

The Veev story illustrates both the promise and peril of construction technology. The company had raised hundreds of millions from top-tier VCs, promising to revolutionize homebuilding with prefabricated panels and integrated technology. Lennar committed to building hundreds of homes using Veev's system. But by 2023, Veev collapsed under the weight of its own ambition and operational challenges. With Veev's collapse in 2023, LenX acquired the company. Lennar didn't just write off the investment—they acquired the technology and talent, integrating what worked into their operations.

Digital transformation accelerated across every aspect of the business. Dynamic pricing algorithms adjusted home prices daily based on traffic, inventory, and competitive dynamics. Virtual reality tours became standard, allowing buyers to walk through homes from anywhere in the world. AI-powered chatbots handled initial customer inquiries, qualifying leads before human sales associates engaged. These weren't gimmicks—they drove measurable improvements in conversion rates and cycle times.

The November 2024 acquisition of Rausch Coleman Homes demonstrated that even as #1, Lennar wasn't done growing. In November 2024, Lennar acquired Arkansas based builder Rausch Coleman Homes. With this acquisition, Lennar entered the Birmingham, Kansas City, Little Rock, Northwest Arkansas, Tulsa and Tuscaloosa markets. In addition, it expanded its presence in Houston, Huntsville, Northwest Florida, Oklahoma City and San Antonio. Rausch Coleman brought expertise in entry-level homes, a segment where affordability challenges made operational excellence crucial.

But the biggest transformation came in February 2025. In February 2025, Lennar spun off Millrose Properties, Inc., a "first-of-its-kind" homesite option purchase platform. The numbers were staggering: In connection with the Spin-Off, Lennar has contributed $5.5 billion in land assets and cash of $1.0 billion. After giving effect to the Spin-Off (net of upfront option deposits from Lennar and third-party transaction costs), Millrose's book value of equity is approximately $5.8 billion as of December 31, 2024.

The structure was elegant. Prior to the open of trading on the New York Stock Exchange today, each holder of Lennar Class A or Class B common stock as of the close of business on January 21, 2025, the record date of the Spin-Off, received one share of Millrose Class A common stock, unless the holder elected to receive one share of Millrose Class B common stock, for each two shares of Lennar Class A or Class B common stock. Lennar shareholders got direct ownership in the land business while Lennar itself became asset-light.

Millrose wasn't just a repository for Lennar's land. Millrose engages in land purchases, horizontal development and homesite option purchase arrangements for Lennar and potentially other homebuilders and developers. The vision: create an industry utility that provides land banking services to multiple builders, generating steady returns while reducing capital requirements across the industry. Millrose intends to elect and qualify to be treated as a real estate investment trust ("REIT") for federal income tax purposes.

Stuart Miller's statement at the spin-off captured the strategic intent: "With today's successful launch of Millrose Properties, we are very excited to advance Lennar's strategy of becoming a pure-play land-light manufacturer of homes. The spin-off of Millrose Properties is a significant milestone for Lennar and the industry, and we look forward to the Millrose team building a Lennar solution, as well as an entire industry solution, and creating an exceptional, land banking platform that will drive accretive yield growth as it expands."

The Spin-Off transaction accelerates Lennar's longstanding strategy of becoming a pure-play, asset-light, new home manufacturing company. Post-spin-off, Lennar's balance sheet is transformed. Capital previously trapped in land can be deployed into technology, operations, and shareholder returns. Returns on equity should expand dramatically. The company can weather downturns without the burden of carrying billions in land through a recession.

As 2025 unfolds, Lennar stands transformed from its origins seven decades ago. It's no longer just America's largest homebuilder—it's becoming a technology-enabled manufacturing platform that happens to produce homes. The journey from Leonard Miller's 42 Miami lots to a separated $50+ billion enterprise represents one of American business's great evolution stories.

X. Business Model & Competitive Advantages

The modern Lennar operates less like a traditional homebuilder and more like a sophisticated manufacturing and financial services conglomerate. The integrated platform spans homebuilding, mortgage origination, title insurance, homeowners insurance, and until recently, land development. Each vertical reinforces the others, creating a flywheel effect that competitors struggle to replicate.

Start with the homebuilding operation itself. Lennar doesn't just build homes—it manufactures them using principles borrowed from Toyota and Dell. The Everything's Included® approach standardizes options packages, allowing bulk purchasing agreements that smaller builders can't match. When Lennar buys appliances, flooring, or fixtures, it's buying for 50,000+ homes annually. The purchasing power differential alone creates a 5-10% cost advantage over regional builders.

The financial services integration changes the customer experience fundamentally. Part of the Lennar family, UAMC is fully integrated into your home buying process and with Lennar to make closing on your new home easy. When a customer walks into a Lennar sales center, they can get pre-approved for a mortgage, select a home, and schedule closing—all within the Lennar ecosystem. The mortgage capture rate exceeds 70%, generating not just origination fees but also gain-on-sale revenue when loans are sold into the secondary market.

Geographic diversification provides natural hedging. With a total annual revenue of over $34 billion in 2023, Lennar operates in 26 states and 75 markets nationwide. When Phoenix slows, Orlando might accelerate. When California struggles with affordability, Texas and Florida pick up the slack. This portfolio effect smooths earnings volatility in ways single-market builders can't achieve.

The technology platform, built over the past decade, creates operational advantages that compound annually. Dynamic pricing algorithms have improved gross margins by 50-100 basis points. Digital marketing reduces customer acquisition costs by 20-30%. Virtual selling capabilities, refined during COVID, allow Lennar to maintain sales momentum even when physical traffic slows. These aren't one-time benefits—they create permanent structural advantages.

Scale economics manifest everywhere. Corporate overhead as a percentage of revenue runs 200-300 basis points below the industry average. Technology investments that would break a small builder's budget are rounding errors for Lennar. The company can afford to hire the best land acquisition teams, the smartest financial engineers, and the most sophisticated marketing professionals.

The multifamily and build-to-rent platforms provide optionality. When single-family demand softens, Lennar can pivot capital to apartments. When young buyers can't qualify for mortgages, Lennar can build rental communities. This flexibility to shift between products based on market conditions is unique among public builders.

Post-Millrose spin-off, the asset-light model fundamentally changes Lennar's risk profile. By using options rather than owning land outright, Lennar can control more lots with less capital. If the market turns, they can walk away from options, limiting losses. If the market strengthens, they exercise options and capture the upside. It's asymmetric risk-taking at its finest.

Cultural advantages, while harder to quantify, matter enormously. The Miller family's continued involvement provides continuity and long-term thinking rare in public companies. The decentralized operating model empowers local division presidents to make quick decisions while monthly reporting maintains accountability. The company promotes from within, creating institutional knowledge that new entrants can't replicate.

Supply chain relationships, built over decades, proved invaluable during recent disruptions. When lumber prices spiked 300% in 2021, Lennar's purchasing agreements and supplier relationships ensured continued access to materials. Smaller builders faced allocation shortages; Lennar kept building. These relationships aren't contracts—they're partnerships forged through cycles of mutual success.

The competitive moat widens each year. Every acquisition brings new capabilities and relationships. Every technology investment increases the cost for competitors to catch up. Every cycle survived adds institutional knowledge about risk management. The business model isn't just differentiated—it's increasingly difficult to replicate.

XI. Playbook: Lessons for Builders & Investors

The Lennar story offers a masterclass in building and investing in cyclical businesses. The lessons apply far beyond homebuilding—any capital-intensive, cyclical industry can learn from Lennar's seven-decade journey.

Lesson 1: Survive First, Thrive Second Leonard Miller and Arnold Rosen didn't try to time the 1970s recession—they used it to rethink their business model. Stuart Miller didn't predict the 2008 crisis perfectly, but he sold assets early enough to survive it. The pattern repeats: during every downturn, Lennar focused first on survival, then positioned for the recovery. This meant painful decisions—selling land at 40% of book value in 2007, laying off thousands of employees, walking away from deposits. But survival is binary. You either make it through the crisis or you don't.

Lesson 2: M&A as Capability Acquisition Lennar's acquisition strategy wasn't about getting bigger—it was about getting better. U.S. Home brought national scale. CalAtlantic brought West Coast expertise. Rausch Coleman brought entry-level product knowledge. Each deal added capabilities that would have taken years to build organically. The discipline: never acquire just for size, always acquire for strategic capability.

Lesson 3: Vertical Integration vs. Focus Conventional wisdom says focus on core competencies. Lennar went the opposite direction, vertically integrating into mortgage, title, and insurance. Why did this work? Because in homebuilding, the customer makes one purchase decision that triggers multiple transactions. Controlling the entire value chain meant capturing economics at each step while providing a superior customer experience. The lesson: vertical integration works when customer transactions are naturally bundled.

Lesson 4: Technology as Competitive Advantage Lennar didn't try to become a technology company—they applied technology to gain competitive advantage in their core business. Dynamic pricing, digital marketing, virtual reality—each technology served a specific business purpose. The discipline was remarkable: every technology investment had to show clear ROI within 18 months. No innovation theater, no chasing buzzwords—just practical application of technology to improve operations.

Lesson 5: Capital Allocation Through Cycles The Millrose spin-off represents sophisticated capital allocation. When land is scarce and expensive, own it. When capital is scarce and expensive, option it. When markets want pure-play exposure, separate the businesses. This isn't financial engineering—it's matching capital structure to market conditions. The playbook: be flexible on structure, rigid on returns.

Lesson 6: Culture + Systems Stuart Miller dancing on Fridays might seem trivial, but it represents something profound: culture matters in commodity businesses. When you're selling the same product as competitors, culture becomes the differentiator. But culture without systems is chaos. Lennar's monthly one-page reports from 50 divisions show the balance—autonomy with accountability, fun with discipline.

Lesson 7: Family Business, Professional Management The Miller family's multi-generational involvement could have been a liability. Instead, it became an asset by combining family commitment with professional management. Stuart Miller earned his position, working his way up despite being the founder's son. The lesson: family businesses work when merit matters more than bloodline.

Lesson 8: Crisis Creates Opportunity Hurricane Andrew's destruction led to Lennar's quality advantage. The 2008 crisis enabled the CalAtlantic acquisition. COVID accelerated digital transformation. Each crisis created opportunities for those with capital and courage to act. The playbook: maintain financial flexibility to be opportunistic when others are desperate.

Lesson 9: Operational Excellence Compounds Lennar's advantages compound over time. Better systems attract better people. Better people build better systems. Scale enables technology investments that improve operations, which increases scale. This virtuous cycle, once established, becomes self-reinforcing. Competitors can't catch up because Lennar keeps pulling further ahead.

Lesson 10: Think in Decades, Act in Quarters The Millrose spin-off was contemplated for years before execution. The CalAtlantic merger built on relationships developed over decades. Yet execution happens in quarters, with specific deadlines and deliverables. This temporal balance—long-term thinking with short-term accountability—drives sustainable outperformance.

For investors, Lennar offers additional lessons. First, in cyclical industries, buy the best operator, not the cheapest stock. Second, watch capital allocation decisions more than earnings reports—they reveal management quality. Third, understand that in commodity businesses, small advantages compound into large moats over time.

XII. Analysis & Investment Case

Lennar today trades at approximately $47 billion market capitalization, making it one of the most valuable homebuilders globally. The investment case rests on several pillars, each with supporting evidence and counterarguments.

The Bull Case: Start with industry fundamentals. America faces a structural housing shortage estimated at 3-5 million units. Household formation runs at 1.5 million annually while new construction barely keeps pace. Demographics favor continued demand: Millennials are entering prime homebuying years, while Baby Boomers are downsizing but not disappearing from the market. In 2023, the company was ranked 119th on the Fortune 500. This isn't a cyclical upturn—it's a secular growth story.

Lennar's competitive position keeps strengthening. Post-CalAtlantic integration, the company enjoys unmatched scale advantages. The Millrose spin-off transforms the balance sheet, reducing capital intensity while maintaining land control through options. Returns on equity should expand from mid-teens to mid-twenties as the asset-light model matures. Few companies successfully execute such fundamental business model transitions.

The financial services platform provides recession resistance. Even if home sales slow, the mortgage and title businesses generate fee income from refinancing and resale transactions. This diversification didn't exist in previous downturns. The company learned from 2008 and built structural hedges into the business model.

Technology investments are bearing fruit. Digital marketing reduces customer acquisition costs. Dynamic pricing optimizes margins. Virtual selling capabilities proved invaluable during COVID and remain valuable for remote buyers. These aren't theoretical benefits—they appear in improved gross margins and SG&A leverage.

Management execution deserves premium valuation. The same team that navigated 2008, executed the CalAtlantic integration, and engineered the Millrose spin-off remains in place. Stuart Miller as Executive Chairman provides continuity while allowing next-generation leadership to emerge. This combination of experience and energy is rare in corporate America.

The Bear Case: Interest rates pose the obvious threat. Every 100 basis point increase in mortgage rates prices out millions of potential buyers. The Fed's inflation fight could push mortgage rates above 8%, crushing affordability. Lennar can't build homes if customers can't afford mortgages, regardless of operational excellence.

The affordability crisis transcends interest rates. Home prices have outpaced income growth for two decades. In markets like California and New York, median homes cost 10x median income. Even with lower rates, structural affordability challenges limit the buyer pool. Lennar's average selling price exceeds $450,000, well above entry-level.

Economic recession remains possible. Unemployment at 4% won't last forever. When job losses mount, home purchases evaporate. Lennar survived 2008, but that doesn't guarantee survival through the next crisis. Leverage, while reduced, still exists. A severe recession could trigger covenant breaches and liquidity crises.

Competition intensifies from unexpected directions. Build-to-rent players like Invitation Homes compete for land. Technology companies explore construction disruption. International builders eye U.S. markets. Lennar's moat, while substantial, isn't impenetrable.

Execution risk multiplies with complexity. The Millrose spin-off could stumble. Technology investments might fail to generate returns. Cultural advantages could erode with generational transition. What worked for 70 years might not work for the next 10.

The Balanced View: Lennar represents a high-quality operator in a structurally attractive but cyclically volatile industry. The company's transformation from asset-heavy builder to asset-light manufacturer reduces risk while potentially expanding returns. The housing shortage provides multi-year demand visibility, while operational excellence ensures Lennar captures more than its fair share.

Valuation matters. At 10x earnings, Lennar offers compelling risk-reward. At 15x earnings, future returns likely match market averages. At 20x earnings, investors are paying for perfection. The stock's volatility creates opportunities for patient investors willing to endure cyclical swings.

The investment timeline matters more than timing. Lennar bought today and held for a decade likely generates attractive returns given housing fundamentals. Lennar bought today and sold next quarter could face any outcome depending on rates, sentiment, and headlines. This isn't a trading vehicle—it's an investment in America's housing future.

Risk management requires position sizing. Lennar's cyclicality makes it unsuitable for concentrated positions unless investors can withstand 50% drawdowns. As part of a diversified portfolio, it provides exposure to demographic trends and operational excellence. The key: size positions to survive the inevitable downturn while participating in the longer-term uptrend.

XIII. Looking Forward & Key Questions

As Lennar enters its eighth decade, several critical questions will determine whether the company maintains its industry leadership or faces disruption.

Can margins sustain in a normalizing rate environment? The past decade's ultra-low rates created abnormal conditions. As rates normalize higher, affordability pressures intensify. Lennar must balance volume and margin, potentially accepting lower margins to maintain production levels. The asset-light model helps—lower capital requirements mean acceptable returns at lower margins—but the trade-off remains challenging.

Will build-to-rent cannibalize or complement traditional sales? Lennar's expansion into build-to-rent addresses affordability challenges but potentially cannibalizes traditional sales. If young families rent instead of buy, does Lennar capture sufficient economics to offset lost sales? The answer depends on execution and capital allocation. Done right, build-to-rent provides countercyclical stability. Done wrong, it dilutes returns and confuses the investment thesis.

How does technology disruption play out? 3D printing, modular construction, and AI-designed homes promise construction revolution. Yet construction remains stubbornly physical, regulated, and local. Lennar's LenX investments position the company to adopt winning technologies, but predicting winners remains difficult. The risk isn't that Lennar misses disruption—it's that no disruption materializes and technology investments generate minimal returns.

What happens post-Stuart Miller? Generational transitions challenge family businesses. Stuart Miller transformed Lennar from regional builder to national powerhouse. Can the next generation maintain momentum? The bench appears strong, with Jon Jaffe and Rick Beckwitt proving capable. But losing the Miller family's involvement would remove a cultural cornerstone. Succession planning becomes critical over the next five years.

Does industry consolidation continue? Lennar and D.R. Horton dominate national homebuilding, but hundreds of regional builders remain. Further consolidation seems likely, but regulatory scrutiny intensifies with scale. Can Lennar continue acquiring without triggering antitrust concerns? The Rausch Coleman acquisition suggests room remains, but the easy deals are done.

How does climate change impact operations? Florida and Texas, Lennar's core markets, face increasing climate risks. Hurricanes, floods, and extreme heat challenge construction schedules and increase costs. Insurance availability diminishes in vulnerable areas. Lennar must balance market opportunity with climate risk, potentially shifting geographic mix over time.

Will Millrose succeed as an independent entity? The spin-off's success isn't guaranteed. Millrose must attract third-party builders, manage development risk, and generate REIT-qualifying income. If Millrose struggles, does Lennar have contingency plans? The separation might prove premature if markets don't value the businesses separately.

Can the culture survive institutionalization? Lennar's entrepreneurial culture drove historical success. As the company institutionalizes with processes and systems, does it lose the agility that enabled opportunistic pivots? The balance between scale and entrepreneurship becomes harder to maintain with size.

What's the next strategic transformation? From public listing to geographic expansion to vertical integration to asset-light operations, Lennar repeatedly transformed its business model. What's next? International expansion? Platform unbundling? Technology licensing? The company's history suggests another transformation awaits, but its form remains unclear.

These questions lack easy answers. Lennar's track record suggests the company will navigate challenges successfully, but past performance doesn't guarantee future results. Investors must weigh the company's proven resilience against unprecedented challenges.

The broader lesson transcends Lennar: in cyclical industries, competitive advantages matter more than cycle timing. Lennar's operational excellence, scale advantages, and cultural strengths position it to outperform through cycles, even if absolute performance varies with conditions.

As America faces a generational housing challenge, Lennar stands ready to build solutions. Whether those solutions generate attractive returns for investors depends on execution, capital allocation, and market conditions. The story continues, seven decades after Leonard Miller invested $10,000 in 42 Miami lots. The foundation he laid supports an enterprise worth 4.7 million times his initial investment—a testament to compound growth, operational excellence, and the enduring American dream of homeownership.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube