Wabtec: The Story of America's Rail Technology Giant

I. Introduction & Episode Roadmap

Picture this: It's February 25, 2019, and in a boardroom overlooking Pittsburgh's three rivers, executives from two industrial titans are signing papers that will create a $15 billion rail equipment behemoth. On one side sits Wabtec—itself born from a 1999 merger between the 150-year-old Westinghouse Air Brake Company and MotivePower. On the other, General Electric's legendary Transportation division, builder of locomotives that hauled America's freight for over a century. The deal structure? A byzantine Reverse Morris Trust transaction that would make investment bankers weep with joy.

But here's what makes this story remarkable: Wabtec wasn't some Silicon Valley unicorn or Wall Street darling. This was a company that traced its roots to George Westinghouse's 1869 invention of the automatic air brake—a technology that literally saved thousands of lives and enabled the modern railroad. How did a Pittsburgh-based brake manufacturer become sophisticated enough to swallow GE's crown jewel transportation business? How did they transform from a $1 billion revenue company in 1999 to a Fortune 500 giant generating over $8 billion today?

The answer lies in one of corporate America's most disciplined acquisition machines, led by a CEO who understood that in cyclical industries, the spoils go to those who consolidate intelligently. William Kassling, who ran Wabtec from its management buyout in 1990 until 2013, didn't just build a company—he created a playbook for industrial consolidation that would make Warren Buffett proud. Over 150 acquisitions later, Wabtec stands as the dominant force in global rail equipment, with products on virtually every freight train in North America and transit systems from New York to New Delhi.

This is a story about three intertwining themes that define modern industrial capitalism. First, the power of consolidation in fragmented markets—how rolling up mom-and-pop suppliers can create extraordinary value. Second, the art of managing cyclical businesses through diversification—balancing freight and transit, domestic and international, new equipment and aftermarket services. And third, the challenge of technological transformation in traditional industries—from air brakes to artificial intelligence, from diesel engines to battery-electric locomotives.

We'll journey from George Westinghouse's eureka moment watching a train wreck in 1866, through the dark days of American rail's decline in the 1960s, to the management buyout that saved WABCO from obscurity. We'll examine how Kassling and his team executed acquisition after acquisition with Swiss precision, building capabilities from rail signals to locomotive engines. We'll dive deep into the transformational deals—the $1.7 billion Faiveley acquisition that made Wabtec a global transit player, and the massive GE Transportation merger that redefined the industry landscape.

Along the way, we'll uncover lessons about capital allocation, operational excellence, and the importance of owning the installed base in industries with 30-year asset lives. We'll explore how a company selling 19th-century technology became a leader in 21st-century digital solutions. And we'll ask the critical question facing Wabtec today: In an era of autonomous vehicles, hyperloop dreams, and climate imperatives, what's the future of rail—and the companies that equip it?

The numbers tell one story: a stock that's delivered over 1,000% returns since going public in 1995, crushing the S&P 500. But the real story is richer—it's about industrial America's evolution, the entrepreneurs who saw opportunity where others saw decline, and the enduring importance of unsexy businesses that keep the economy moving. As we'll see, sometimes the best investments aren't in the latest tech disruption, but in companies that have been disrupting for 150 years and counting.

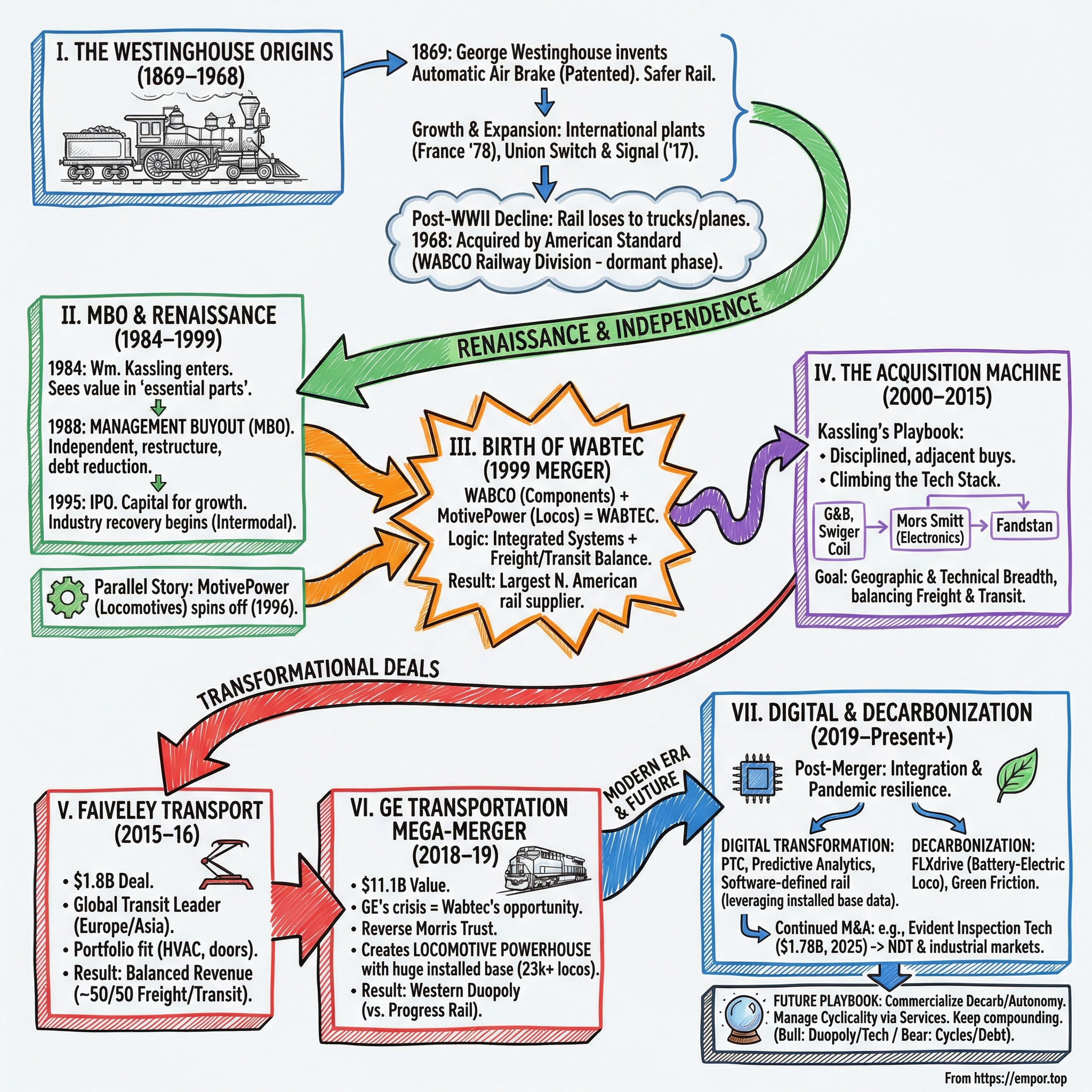

II. The Westinghouse Origins: Air Brakes Change Everything (1869–1968)

The scene was horrific even by 19th-century standards. On a cold January morning in 1866, twenty-two-year-old George Westinghouse Jr. stood amid the twisted metal and splintered wood of yet another train collision near Schenectady, New York. Bodies were being pulled from the wreckage—engineers who had seen the danger coming but couldn't stop their locomotives in time. The problem was maddeningly simple: stopping a train required brakemen to manually turn wheels on each car, a process that took precious minutes and perfect coordination. Westinghouse, already a prolific inventor with patents for rotary engines and railway frogs, became obsessed with solving this deadly puzzle.

His inspiration came from an unlikely source—a magazine article about compressed air drills being used to bore the Mont Cenis tunnel through the Alps. What if compressed air could simultaneously apply brakes across an entire train? Critics called it impossible; trains would need to carry heavy air compressors, and any leak in the system would spell disaster. But Westinghouse had a counterintuitive insight: make the system "fail-safe" by using air pressure to release the brakes, not apply them. A loss of pressure would automatically stop the train—the opposite of what everyone expected, but infinitely safer.

On April 13, 1869, Westinghouse convinced the Panhandle Railroad to let him test his contraption on a passenger train outside Pittsburgh. As the locomotive rounded a curve, the engineer spotted a farmer's wagon stuck on the tracks ahead. He yanked the brake valve. For the first time in railroad history, every car stopped simultaneously. The train screeched to a halt just feet from the terrified farmer. Word spread like wildfire through the railroad community—Westinghouse had done the impossible.

Within months, Westinghouse Air Brake Company was born in Pittsburgh with $500,000 in capital. But George Westinghouse wasn't content with dominating America. By 1878, he'd established a factory in France, making WABCO one of America's first truly multinational manufacturers. The company's growth paralleled the explosive expansion of global railroads—wherever steel rails were laid, Westinghouse brakes followed. By 1893, the U.S. government mandated automatic air brakes on all trains, essentially granting Westinghouse a license to print money.

The early 20th century brought both triumph and tragedy. In 1905, Westinghouse expanded beyond brakes, acquiring Union Switch & Signal Company to control more of the railroad safety ecosystem. Revenue soared past $10 million annually—astronomical for the era. But in March 1914, George Westinghouse died at age 67, his funeral attended by thousands of workers whose lives he'd improved through progressive labor policies decades ahead of their time. The company he left behind employed over 50,000 people across four continents.

World War I transformed WABCO into an arsenal of democracy, producing not just rail equipment but munitions and submarine parts. The interwar period saw continued innovation—automatic train control systems, improved brake designs, even early experiments with streamlined passenger trains. By 1940, virtually every American freight car and locomotive bore WABCO equipment. The company's Wilmerding, Pennsylvania plant alone covered 85 acres, a cathedral of American industrial might.

But the post-war era brought an existential crisis nobody saw coming. In 1956, President Eisenhower signed the Interstate Highway Act, launching 41,000 miles of highways that would devastate rail freight. Passenger rail collapsed even faster—why take a train when you could drive your new Chevrolet on smooth, fast interstates? Between 1950 and 1970, rail's share of intercity freight tonnage plummeted from 56% to 37%. Legendary railroads like Penn Central declared bankruptcy. WABCO's stock price reflected the carnage, falling over 60% from its 1950s peak.

Management's response was both desperate and prescient. If American railroads were dying, perhaps foreign markets and new technologies could fill the gap. In 1967, WABCO engineers unveiled the world's first electronically controlled pneumatic brakes for Washington's new Metroliner service—computer chips managing air pressure, a marriage of 19th and 20th-century technology. The company also pivoted toward rapid transit systems proliferating in cities worldwide, winning contracts for San Francisco's BART and Washington's Metro.

Yet innovation couldn't overcome industry headwinds. In 1968, with revenues stagnant and shareholders restless, WABCO's board accepted a $285 million acquisition offer from American Standard, the plumbing and HVAC conglomerate. The company that George Westinghouse built was folded into American Standard's Railway Products Group, renamed simply "WABCO Railway Products." It seemed like an ignominious end for one of America's great industrial pioneers.

But hidden in the bureaucracy of a bathroom fixtures conglomerate, something remarkable was happening. A young executive named William Kassling had been assigned to run the railway division. While American Standard's management focused on toilets and air conditioners, Kassling quietly studied every aspect of the rail equipment business—the players, the economics, the technology cycles. He noticed something others missed: while American railroads were struggling, the industry wasn't dying—it was consolidating. The survivors would need modern, efficient equipment. And globally, railways were thriving.

Kassling also observed that the rail equipment industry remained absurdly fragmented—hundreds of small suppliers, many family-owned, serving specific niches. Unlike aerospace or automotive, nobody had successfully rolled up rail suppliers into a dominant platform. The opportunity was hiding in plain sight, but executing would require patient capital, operational excellence, and deep industry knowledge. As the 1970s drew to a close, Kassling began formulating a plan that would eventually transform WABCO from an orphaned division into the foundation of a new rail equipment empire.

III. The Management Buyout & WABCO Renaissance (1984–1999)

William Kassling didn't look like a corporate revolutionary. With his accountant's demeanor and Pittsburgh accent, the 44-year-old executive who took over American Standard's Railway Products Group in 1984 seemed more suited for cost-cutting than empire-building. But Kassling possessed something rarer than charisma: he understood the DNA of industrial businesses—how they created value, where margins hid, and why Wall Street consistently undervalued them.

His first move was audacious in its simplicity. Kassling gathered his senior team in WABCO's Wilmerding headquarters and spread out financial statements from the past decade. "Look at this," he said, pointing to the aftermarket services revenue. "We sell a brake system once, but we service it for thirty years. The install base is an annuity, and nobody's paying attention to it." While American Standard's corporate headquarters fixated on new equipment sales—volatile and cyclical—Kassling saw that parts and services generated 60% gross margins with minimal capital requirements.

By 1987, Kassling had transformed WABCO's operations, improving operating margins from 6% to 14% through a combination of factory automation, supplier consolidation, and aggressive pricing on aftermarket parts. But he grew frustrated with American Standard's corporate bureaucracy. Every acquisition required months of approvals. Every strategic initiative got bogged down in committees. Meanwhile, private equity firms were circling, sensing opportunity in neglected industrial assets.

The breaking point came during a 1988 board meeting when American Standard's CEO announced plans to divest "non-core" assets to focus on building products. Kassling saw his opening. Within weeks, he'd assembled a management buyout proposal backed by Gibbons, Green & van Amerongen, a private equity firm specializing in industrial consolidation. The offer: $175 million for the entire Railway Products Group, financed with $25 million in equity and $150 million in debt—a leverage ratio that would make modern PE firms blush.

American Standard's board, eager to shed a cyclical business they never understood, accepted immediately. But Kassling's real coup came in the deal structure. He negotiated to keep the WABCO name and all international operations, while American Standard retained only a small royalty on certain products. Overnight, a division buried in a conglomerate became an independent company with a 120-year heritage and global reach.

The early days of independence were brutal. Interest payments consumed nearly 40% of cash flow. Kassling implemented draconian cost controls—travel bans, hiring freezes, even removing coffee machines from break rooms. But he also made strategic investments that seemed crazy for a leveraged company. He hired engineers from Boeing to modernize product development. He established a China office in 1989, years before most American industrials. Most critically, he began acquiring small suppliers at distressed prices, using seller financing to preserve cash.

The strategy crystallized during a 1990 visit to a struggling brake valve manufacturer in Illinois. The owner, nearing retirement with no succession plan, was asking $8 million. Kassling offered $3 million upfront plus earnouts based on performance. But here's where Kassling's genius emerged: he didn't just buy the assets. He retained the owner as a consultant, kept the experienced workforce, and integrated the operation into WABCO's supply chain. Within eighteen months, the acquisition was generating $2 million in annual EBITDA—a 66% return on investment.

This became the WABCO playbook: identify family-owned suppliers with strong products but weak business infrastructure. Acquire them cheaply using creative financing. Integrate operations while maintaining technical expertise. Cross-sell products through WABCO's global distribution. Rinse and repeat. Between 1990 and 1994, WABCO executed twelve such acquisitions, spending less than $50 million total while adding $150 million in revenue.

The results were staggering. Revenue grew from $275 million in 1990 to $425 million in 1994. Operating margins expanded to 18%. Net debt fell from 6x EBITDA to 2x. Kassling's team had achieved the impossible—a leveraged turnaround during a recession. Investment bankers started calling, sensing an IPO opportunity.

But Kassling faced a dilemma. Going public would provide capital for larger acquisitions, but it would also mean quarterly earnings pressure and Wall Street scrutiny. He'd watched other industrial companies get punished for missing quarters by pennies, their stock prices crushed despite strong fundamentals. The solution came from an unexpected source—Warren Buffett's 1992 Berkshire Hathaway letter, which Kassling read religiously.

Buffett wrote about the advantage of patient capital in cyclical industries—buying when others were selling, investing for decades not quarters. Kassling realized he needed shareholders who understood industrial cycles and valued long-term compounding over short-term gains. He began courting institutional investors with this pitch: "We're not a growth story or a turnaround play. We're a compound returns machine in an essential industry."

The March 1995 IPO was priced at $20 per share, valuing WABCO at $450 million. Demand was modest—no hot tech story here—but Kassling had attracted the shareholders he wanted: Wellington, Fidelity, and other long-term focused funds. In his first earnings call as a public company CEO, Kassling set the tone: "We will optimize for free cash flow generation and intelligent capital allocation. We will not chase revenue growth or make acquisitions to hit quarterly targets."

Meanwhile, a parallel story was unfolding in Boise, Idaho. Morrison Knudsen, the legendary construction firm that built the Hoover Dam, had diversified into locomotive manufacturing through its MK Rail subsidiary. By 1994, MK Rail was generating $400 million in revenue, primarily rebuilding aging diesel locomotives for cash-strapped railroads. But Morrison Knudsen was struggling, bleeding cash from failed international projects.

In 1996, MK Rail's management, led by CEO John Rimmasch, engineered their own buyout, creating MotivePower Industries. Like WABCO, MotivePower went public seeking capital for consolidation. The two companies were mirror images—WABCO dominated brakes and signaling, MotivePower controlled locomotive services. Both served the same customers. Both pursued similar acquisition strategies. Competition was inevitable, but Kassling saw something else: combination could create the first truly integrated rail equipment platform.

The late 1990s brought an unexpected catalyst—the railroad renaissance. Deregulation under the Staggers Act had finally allowed railroads to price competitively with trucks. Intermodal shipping—containers moving seamlessly between ships, trains, and trucks—exploded. Railroad profits soared, driving equipment investment. WABCO's stock price tripled between 1995 and 1998. The company that American Standard had practically given away was now worth $1.5 billion.

As 1999 began, Kassling made his move. In a series of secret meetings, he proposed a merger of equals with MotivePower. The combined entity would have $1.3 billion in revenue, serve every major railroad globally, and possess the scale to pursue transformational acquisitions. On June 30, 1999, the deal closed. Wabtec Corporation was born—the name a portmanteau of WABCO and MotivePower, though insiders knew where the real power lay.

IV. The Birth of Wabtec: WABCO + MotivePower Merger (1999)

The merger announcement hit the wire services at 6 AM Eastern on January 11, 1999. "WABCO and MotivePower to Combine in $690 Million Stock Swap." Wall Street's reaction was swift and brutal—both stocks fell over 15% within hours. Analysts questioned the logic: Why combine two companies with overlapping customers but minimal product overlap? How could brakes and locomotives create synergies? One particularly caustic research note called it "a marriage of convenience between two companies that couldn't find better partners."

But in WABCO's Pittsburgh headquarters, Kassling was playing three-dimensional chess while critics played checkers. He'd studied every major industrial merger of the past decade—the disasters (Daimler-Chrysler), the successes (AlliedSignal-Honeywell), and everything in between. His conclusion: most mergers failed not because of strategy but execution. Integration was where value lived or died.

Six months before the public announcement, Kassling had secretly assembled an integration team, code-named "Project Railway." Led by his lieutenant Greg Sbrocco, the team included fifteen executives split equally between WABCO and MotivePower. Their mandate was surgical: identify $50 million in annual synergies without destroying either company's culture or customer relationships. They worked nights and weekends, meeting in airport hotels to avoid detection.

The integration playbook they developed would become Wabtec's secret weapon for future acquisitions. First principle: protect revenue at all costs. Every customer was assigned two relationship managers—one from each heritage company—ensuring no balls dropped during transition. Second: combine back-office functions ruthlessly. Within ninety days, Wabtec eliminated duplicate positions in accounting, HR, and IT, saving $15 million annually. Third: preserve technical expertise. Engineers and product specialists were untouchable, regardless of redundancy.

But the real genius was in commercial strategy. Kassling recognized that WABCO and MotivePower had been competing for wallet share at the same railroads. Burlington Northern might buy brakes from WABCO while sending locomotives to MotivePower for overhaul. Now, Wabtec could offer integrated solutions—brake systems designed specifically for MotivePower's remanufactured locomotives, bundled service contracts covering entire train consists. The value proposition was compelling: one vendor, one contract, one throat to choke.

The first major win came in March 2000. Union Pacific, America's largest railroad, awarded Wabtec a $450 million multi-year contract covering locomotive services and brake components. The deal was worth more than either company had ever won independently. UP's purchasing chief explained the decision simply: "We're tired of managing hundreds of suppliers. Wabtec can handle everything from couplers to computers."

Cultural integration proved trickier. WABCO employees, steeped in 130 years of history, viewed themselves as technology aristocrats. MotivePower folks, many former railroad workers, prided themselves on practical knowledge and customer intimacy. Early integration meetings devolved into turf battles—who owned locomotive brakes? Who called on mechanical officers versus procurement?

Kassling's solution was elegant: organize by customer outcome, not product line. Instead of brake divisions and locomotive divisions, Wabtec created Freight Groups and Transit Groups, each responsible for total customer satisfaction. A freight customer didn't care if their solution involved brakes, locomotives, or pixie dust—they wanted reliable, cost-effective operations. This customer-centric structure forced collaboration and broke down silos.

The numbers validated the strategy. In 2000, Wabtec's first full year as a combined entity, revenue hit $1.1 billion while operating margins expanded to 12.5%. More importantly, the company generated $95 million in free cash flow, exceeding pre-merger combined totals by 40%. The synergy target of $50 million was achieved in eighteen months, not the projected three years.

But Kassling wasn't celebrating. He saw the merger as merely phase one of a larger strategy. The rail equipment industry remained fragmented—Wabtec controlled maybe 5% of the global market. Hundreds of suppliers, many family-owned or parts of struggling conglomerates, dotted the landscape. The 2001 recession, triggered by the dot-com crash, would create buying opportunities for those with strong balance sheets and acquisition expertise.

The company's acquisition machine shifted into higher gear. Between 2000 and 2005, Wabtec completed twenty-three acquisitions, spending $400 million to add $600 million in revenue. Each followed the proven playbook: identify underperforming assets, acquire at reasonable multiples (typically 4-6x EBITDA), integrate rapidly, achieve 20%+ returns on invested capital. The acquisitions ranged from tiny ($5 million for a coupler manufacturer) to substantial ($85 million for CostaFer, a European brake supplier).

One acquisition deserves special attention for what it revealed about Wabtec's evolving strategy. In 2003, the company paid $35 million for Schaefer Equipment, a Cincinnati-based manufacturer of railway electronics and event recorders—essentially black boxes for trains. The price seemed steep for a company with just $20 million in revenue. But Kassling saw what others missed: data was becoming critical to railroad operations. Schaefer's technology could monitor brake performance, predict failures, and optimize maintenance schedules. It was Wabtec's first serious foray into digital solutions.

The international expansion accelerated dramatically. By 2004, Wabtec operated facilities in fifteen countries, with international sales comprising 35% of revenue. The company wasn't just exporting American products—it was localizing solutions for distinct markets. Chinese railroads needed ultra-durable components for extreme conditions. European operators demanded sophisticated electronics for high-speed trains. Indian railways required low-cost, high-volume solutions. Wabtec developed distinct product lines for each market while leveraging global scale in procurement and R&D.

Competition was intensifying from unexpected quarters. Knorr-Bremse, the German giant, was aggressively expanding in North America. Chinese manufacturers, backed by state capital, offered products at 50% lower prices. Some analysts questioned whether Wabtec could maintain margins in this environment. The bear case was simple: commoditization was coming to rail equipment just as it had to automotive suppliers.

Kassling's response revealed his strategic depth. At a 2004 investor day, he presented a slide that would define Wabtec's strategy for the next decade. It showed two circles—one labeled "Products" and one labeled "Services"—with arrows flowing between them. "Our competitors think this is a product business," he explained. "But products are just the entry ticket. The real value is in the thirty-year service tail. Every product we sell creates an annuity stream. Every acquisition expands our installed base. We're not in the equipment business—we're in the lifecycle value business."

The numbers backed up the strategy. By 2005, aftermarket services comprised 55% of revenue but 70% of gross profit. Wabtec's return on invested capital exceeded 20%, extraordinary for an industrial company. The stock price reflected this performance, rising from $11 at the merger to $35 by year-end 2005. The company that Wall Street had dismissed as a "marriage of convenience" was generating returns that made tech investors jealous.

V. The Acquisition Machine: Building Through M&A (2000–2015)

Inside Wabtec's Pittsburgh headquarters, there was a room few outsiders ever saw. Dubbed the "War Room" by insiders, its walls were covered with magnetic boards displaying hundreds of potential acquisition targets. Each magnet contained key data: revenue, EBITDA, ownership structure, strategic fit. Green magnets meant active discussions. Yellow indicated preliminary interest. Red meant "passed for now but monitor." At the center sat a simple mantra, hand-written by Kassling himself: "Discipline Beats Brilliance."

This wasn't corporate art—it was the nerve center of one of industrial America's most successful acquisition machines. Between 2000 and 2015, Wabtec would complete over sixty acquisitions, deploying $2.5 billion in capital while generating average returns on invested capital exceeding 20%. But what made Wabtec different wasn't the volume of deals—plenty of companies could write checks. It was the systematic, almost scientific approach to identifying, executing, and integrating acquisitions.

The process started with what Wabtec called "heat mapping." Every quarter, strategy teams analyzed global rail spending patterns, identifying pockets of growth and technological change. When European railroads began mandating positive train control systems in 2008, Wabtec mapped every supplier in the signaling ecosystem. When Chinese high-speed rail exploded in 2010, they catalogued component manufacturers serving that market. The heat maps revealed not just what to buy, but when buying opportunities would emerge.

Consider the 2010 acquisition of Swiger Coil Systems, a $43 million deal that barely made headlines. Swiger manufactured specialized coils for railway signaling systems—about as unsexy as industrial products get. But Wabtec's analysis revealed that new federal regulations would require positive train control on 60,000 miles of U.S. track by 2015. Every PTC system needed Swiger's type of coils. The company was generating $8 million in EBITDA on $35 million in revenue. Within three years, Swiger's revenue tripled as PTC installations accelerated. Wabtec paid 5.4x EBITDA; by 2013, they were earning their entire purchase price annually.

But Wabtec's real edge was in approaching family-owned businesses. By 2010, Kassling's team had developed a psychological profile of the typical rail equipment entrepreneur: engineers who'd built solid businesses but lacked succession plans. Their children often had no interest in manufacturing. Private equity buyers were too aggressive, promising huge returns but likely to flip quickly. Strategic buyers might close facilities or eliminate jobs.

Wabtec offered something different—preservation of legacy with professional management. They'd keep facilities open, retain employees, and maintain the founder's name on products. The pitch was emotional as much as financial: "You built something special. We'll make sure it lasts another generation." This approach opened doors that remained closed to competitors.

The 2012 acquisition of Mors Smitt exemplified this strategy. The Dutch company, founded in 1915, manufactured electrical components for trains—connectors, switches, and control panels. The founding family's fourth generation was running the business but wanted liquidity while ensuring continuity. Wabtec paid $88 million, a fair but not aggressive price. But here's what happened next: Wabtec kept the Mors Smitt brand, retained all 400 employees, and invested $10 million in factory upgrades. Revenue grew 40% in two years as Wabtec's global sales force distributed Mors Smitt products worldwide.

The integration playbook had evolved into a precise 100-day plan. Day 1-30: Protect revenue, communicate with customers, address employee concerns. Day 31-60: Integrate financial systems, eliminate redundancies, identify quick wins. Day 61-100: Implement commercial synergies, begin cross-selling, optimize supply chain. Every acquisition followed this template, adjusted for size and complexity. The predictability reduced integration risk and accelerated value creation.

Not every deal worked perfectly. The 2008 acquisition of Standard Car Truck Company for $285 million—Wabtec's largest to date—proved challenging. Standard manufactured railcar components including side frames and bolsters, the fundamental structures supporting freight cars. The business was more commodity-like than Wabtec anticipated, with Chinese competitors offering similar products at 40% lower prices. Integration took twice as long as planned, and returns barely exceeded Wabtec's cost of capital.

But even failures taught valuable lessons. After Standard Car Truck, Wabtec developed new criteria: avoid commoditized products, focus on technically differentiated solutions, and never assume pricing power exists without switching costs. The discipline to walk away became as important as the ability to close deals. Between 2010 and 2015, Wabtec evaluated over 200 potential acquisitions but completed only fifteen, a 7.5% close rate that reflected their selectivity.

The international expansion through acquisition was particularly sophisticated. Rather than simply buying foreign companies, Wabtec pursued what they called "beachhead" acquisitions—small purchases that provided market entry and local knowledge. The 2014 acquisition of Fandstan Electric Group for $199 million gave Wabtec significant presence in China's rail market. Fandstan manufactured traction motors and related components for Chinese locomotives, with deep relationships at China Railway Corporation.

But Fandstan wasn't just about accessing Chinese markets—it was about understanding Chinese competition. By operating inside China, Wabtec learned how local manufacturers achieved such low costs: vertical integration, government subsidies, and acceptance of lower margins. This intelligence informed Wabtec's global strategy, helping them decide where to compete on price versus where to emphasize technology and service.

The cumulative impact of fifteen years of disciplined acquisition was staggering. By 2015, Wabtec had assembled a portfolio of over forty brands, manufactured 10,000+ products, and maintained facilities in twenty countries. Revenue had grown from $1.1 billion in 2000 to $3.0 billion in 2015, with roughly half coming from acquired businesses. Operating margins expanded from 10% to 14%, defying the typical dilution from M&A. Return on invested capital remained above 15%, exceptional for asset-intensive manufacturing.

The financial engineering behind this growth was equally impressive. Wabtec maintained a simple capital structure—minimal debt, no preferred stock, no complex derivatives. They funded acquisitions through a combination of free cash flow (averaging $200 million annually) and occasional debt issuance at attractive rates. The average acquisition multiple was 6x EBITDA, while Wabtec traded at 12-14x, creating immediate multiple arbitrage. Every dollar deployed in acquisitions generated $1.50-2.00 in market value.

But as 2015 progressed, Kassling's successor Albert Neupaver (who took over as CEO in 2013) faced a strategic inflection point. The easy acquisitions—subscale family businesses—were largely exhausted. Remaining targets were either too small to matter or too large for Wabtec's balance sheet. Chinese competitors were becoming more sophisticated, and European rivals were consolidating. Growth through traditional acquisition seemed to be plateauing.

The answer would come from an unexpected source: a French company founded in 1919 that most Americans had never heard of. Faiveley Transport was everything Wabtec's previous acquisitions weren't—large, international, and expensive. But it also offered something Wabtec desperately needed: a transformation from North American freight specialist to global transit leader. The pursuit of Faiveley would test every aspect of Wabtec's acquisition machine and set the stage for an even more audacious deal to come.

VI. The Faiveley Transport Acquisition: Going Global in Transit (2015–2016)

The email arrived at 3:47 AM Pittsburgh time on May 15, 2015. Albert Neupaver, barely eighteen months into his CEO role, read it twice to make sure he understood correctly. Faiveley Transport, the French rail equipment giant, might be for sale. The Faiveley family, which controlled 51% of the company through a complex web of holding companies, was considering strategic alternatives. The asking price? North of $1.5 billion. It would be Wabtec's largest acquisition by a factor of five.

Neupaver immediately called his CFO, Patrick Dugan, who was traveling in China. "Pat, forget whatever you're doing. We need to model something big." Within seventy-two hours, a tiger team assembled in Pittsburgh, code-named "Project Paris." The opportunity was tantalizing but the challenges were enormous. Faiveley was a French national champion with operations in twenty-four countries, 6,000 employees, and revenue exceeding €1 billion. They manufactured everything from pantographs (the devices that collect power from overhead lines) to air conditioning systems for high-speed trains.

The strategic logic was compelling. Wabtec generated 70% of revenue from freight rail, which was highly cyclical and North America-centric. Transit represented only 30% but offered stable, government-backed demand globally. Faiveley was the inverse—85% transit-focused with dominant positions in Europe and Asia. Combined, they'd create the world's only truly balanced rail equipment company. The revenue synergies alone could exceed $200 million annually.

But the cultural chasm seemed unbridgeable. Faiveley epitomized French industrial elegance—sophisticated engineering, complex governance, strong unions. Their headquarters in Gennevilliers featured a museum of historic rail equipment and a Michelin-starred executive dining room. Wabtec was pure Pittsburgh pragmatism—functional offices, brown-bag lunches, and a culture where executives fixed their own coffee. When Faiveley's CEO visited Pittsburgh for preliminary discussions, he was shocked to find Neupaver's office was a converted conference room with folding tables.

The first negotiation session in Paris nearly derailed everything. Faiveley's advisors from Rothschild presented a 200-page valuation analysis justifying a €1.8 billion enterprise value. Wabtec's team countered with ten slides showing why €1.2 billion was the maximum justifiable price. The cultural disconnect was painful—Faiveley executives gave philosophical speeches about "industrial patrimony" while Wabtec focused on EBITDA multiples and return thresholds. After six hours, they hadn't agreed on basic terms.

Neupaver made a pivotal decision. Instead of battling over valuation, he shifted focus to structure. What if this wasn't a traditional acquisition but a strategic combination? Wabtec would acquire 51% initially, allowing the Faiveley family to retain significant ownership and benefit from future upside. The remaining 49% would be acquired over time based on performance metrics. This structure addressed French concerns about foreign takeover while giving Wabtec control and integration flexibility.

The breakthrough came during a dinner at Tour d'Argent, the legendary Parisian restaurant overlooking Notre-Dame. Erwan Faiveley, the family patriarch, asked Neupaver directly: "Will you preserve what my grandfather built?" Neupaver's response was carefully prepared but genuinely delivered: "We're not buying Faiveley to americanize it. We're buying it because you've built capabilities we can't replicate. Your engineering excellence plus our commercial execution equals something neither could achieve alone."

By July 2015, they'd reached preliminary agreement: $1.8 billion total consideration, with $840 million in cash and the remainder in Wabtec stock. The Faiveley family would own approximately 13% of combined Wabtec, making them the largest shareholder after Vanguard and BlackRock. But announcing the deal was just the beginning of a sixteen-month regulatory marathon that would test Wabtec's resolve.

The European Commission launched an extensive review, concerned about concentration in brake systems and pantographs. The investigation revealed just how dominant the combined entity would be—over 50% market share in certain product categories. French unions protested potential job losses. German competitors lobbied for deal blockage. Even the French government expressed concerns about a strategic asset falling under American control.

Wabtec's regulatory strategy was methodical. They hired former European Commission officials as advisors, conducted hundreds of customer interviews demonstrating support, and made strategic concessions. The key compromise: divesting Faiveley's North American freight brake business to satisfy competitive concerns. It was painful—that business generated $40 million in EBITDA—but necessary for approval.

The financing structure revealed Wabtec's financial sophistication. Rather than diluting shareholders with massive equity issuance, they arranged a creative package: $750 million in term loans at 2.8% interest (exploiting low rates), $250 million from free cash flow, and $800 million in stock issued primarily to Faiveley shareholders. The math was elegant—Wabtec's stock traded at 18x EBITDA while Faiveley was acquired at 11x, creating immediate accretion.

Integration planning began six months before closing, unusual for a cross-border deal. Wabtec dispatched fifty executives to shadow Faiveley counterparts, learning their processes and building relationships. They discovered unexpected treasures—Faiveley's engineering center in Tours had developed predictive maintenance algorithms years ahead of Wabtec's capabilities. Their manufacturing plant in Czech Republic achieved quality levels that exceeded aerospace standards.

But they also found challenges. Faiveley's IT systems were a hodgepodge of acquisitions never fully integrated. Their supply chain was regionally fragmented, missing global sourcing opportunities. Most surprisingly, despite brilliant engineering, Faiveley's commercialization was weak—great products that customers didn't know existed. These insights shaped the integration priorities.

The deal finally closed on December 1, 2016, after 505 days of negotiation, regulation, and preparation. The final price of $1.74 billion reflected minor adjustments but remained within Wabtec's targets. The first symbolic decision: keeping the Faiveley name for all transit products globally. This wasn't just branding—it was a signal that Wabtec respected what they'd acquired.

The integration exceeded expectations. Within eighteen months, Wabtec achieved $85 million in cost synergies through procurement consolidation and facility optimization. Revenue synergies proved even more valuable—Wabtec's freight customers began buying Faiveley HVAC systems, while Faiveley's transit relationships opened doors for Wabtec brake products. Cross-selling generated $150 million in new annual revenue by 2018.

One story captures the cultural transformation. In 2017, engineers from Pittsburgh and Tours collaborated on a new brake system for European high-speed trains. The Americans brought cost discipline and manufacturing expertise. The French contributed sophisticated control algorithms and aesthetic design. The resulting product won a $400 million contract from SNCF, France's national railroad—validation that the combination could create something neither company could achieve independently.

The financial returns validated the strategy. Faiveley's EBITDA grew from €180 million in 2016 to €275 million in 2018, a 52% increase. The acquisition multiple fell from 11x at purchase to 7x based on current performance. Wabtec's stock price rose 45% in the two years post-closing, adding $3 billion in market value—nearly double the acquisition price.

But the Faiveley acquisition's greatest value might have been organizational learning. Wabtec discovered they could execute complex, international deals. They learned to navigate European regulations, manage foreign labor relations, and integrate sophisticated technologies. This expertise would prove invaluable when an even larger opportunity emerged—one that would have seemed impossible without the Faiveley experience.

As 2017 ended, Wabtec was a transformed company. Revenue exceeded $4 billion, with balanced exposure between freight and transit, Americas and international. They'd proven that American industrial companies could successfully acquire and integrate European champions. But nobody, not even Neupaver, anticipated what would come next. In a boardroom in Boston, General Electric's new CEO was contemplating radical portfolio changes that would create the opportunity of a lifetime.

VII. The GE Transportation Mega-Merger: Transformational Deal (2018–2019)

John Flannery's tenure as General Electric CEO was already unraveling when he made the call that would change Wabtec forever. It was March 2018, and GE's stock had collapsed from $30 to $13 in twelve months. Activist investors were circling, debt ratings were under threat, and the century-old conglomerate was fighting for survival. Flannery needed to raise cash fast, and GE Transportation—despite being profitable and growing—was deemed "non-core."

The irony was breathtaking. GE Transportation traced its heritage to 1907 when General Electric began manufacturing locomotives in Erie, Pennsylvania. For a century, GE locomotives had hauled America's freight, powered by increasingly sophisticated diesel-electric technology. By 2018, the division generated $4.5 billion in revenue with industry-leading 20% EBITDA margins. Their Evolution Series locomotive was the most fuel-efficient freight hauler ever built. This wasn't a struggling division—it was a crown jewel being sacrificed to save a dying conglomerate.

Neupaver got the call from Goldman Sachs on a Friday afternoon. "GE Transportation might be available. Are you interested?" The asking price was rumored to be $11 billion. Wabtec's entire market cap was $8 billion. It was like a python trying to swallow an elephant. Neupaver's first reaction was to laugh. His second was to call his board chair, Bill Kassling, who'd remained involved post-retirement.

"Albert, this is it," Kassling said without hesitation. "This is the deal that creates a forever company. Find a way to make it work."

The challenge wasn't just size—it was structure. GE couldn't afford a cash deal; they needed immediate liquidity. Traditional acquisition financing would be impossible given the multiples. But Wabtec's investment bankers at Morgan Stanley proposed something audacious: a Reverse Morris Trust transaction, a tax-efficient structure where GE would spin off Transportation to shareholders, then immediately merge it with Wabtec. GE shareholders would own roughly 50% of the combined company, Wabtec shareholders the other 50%.

The complexity was mind-bending. The deal required simultaneous approval from three sets of shareholders (GE, Wabtec, and GE Transportation bondholders), two regulatory jurisdictions (U.S. and EU), and navigating union contracts covering 7,000 employees. The documentation alone would exceed 10,000 pages. One tax lawyer called it "the most complex industrial transaction since RJR Nabisco."

But complexity created opportunity. While other bidders struggled with structure, Wabtec had an advantage—they'd just completed Faiveley, proving they could execute sophisticated deals. Their integration playbook was battle-tested. Most importantly, they understood rail equipment deeply while financial buyers would be operating blind.

The first negotiation session took place in neutral territory—a conference room at Newark Airport. Larry Culp had just replaced Flannery as GE CEO, and his mandate was clear: maximize value, minimize risk, close quickly. Wabtec's initial offer was $9.5 billion. GE wanted $11.5 billion. The gap seemed unbridgeable until someone proposed a creative solution: include a $2.9 billion cash payment to GE, satisfying their liquidity needs, while the remaining value came through stock ownership.

Due diligence revealed both treasures and landmines. GE Transportation's service business was extraordinary—23,000 locomotives in the installed base generating $1.8 billion in high-margin aftermarket revenue. Their digital division had developed Trip Optimizer software that reduced fuel consumption by 10%, saving railroads millions annually. The technology portfolio included 1,800 patents, some dating back to Thomas Edison.

But there were concerns. GE's locomotive order backlog had shrunk from $18 billion to $12 billion as railroads deferred purchases. The Erie manufacturing complex was sized for volumes that might never return. Most worryingly, Chinese competitor CRRC was offering locomotives at 50% of GE's price, targeting developing markets where GE had traditionally dominated.

The breakthrough came through scenario planning. Wabtec's team modeled fifty different market scenarios—oil prices from $30 to $150, GDP growth from -2% to +5%, various regulatory environments. In 45 of 50 scenarios, the deal generated returns exceeding 15%. The key insight: even in downside cases, the service business and cost synergies provided sufficient cushion. The deal was resilient, not just opportunistic.

May 21, 2018: The announcement shocked Wall Street. "Wabtec to Merge with GE Transportation in $11.1 Billion Deal." The structure was Byzantine but brilliant. GE would receive $2.9 billion cash. GE shareholders would get shares representing 50.1% of the combined company, distributed as a tax-free spinoff. Wabtec shareholders would be diluted but own 49.9% of a company triple the size. The implied valuation of GE Transportation was 10.3x EBITDA—reasonable given the quality.

Market reaction was mixed. Wabtec stock fell 10% on dilution concerns. GE stock rose 5% on better-than-expected terms. Skeptics questioned integration complexity—combining a 150-year-old brake company with GE's locomotive division seemed like mixing oil and water. One analyst called it "the industrial equivalent of a platypus—evolutionary oddity or breakthrough adaptation?"

The regulatory review was surprisingly smooth. Unlike Faiveley, there was minimal product overlap—Wabtec made components, GE made locomotives. The complementarity actually enhanced competition by creating a stronger alternative to foreign manufacturers. The Department of Justice approved without conditions. European regulators required minor divestitures but nothing material.

Integration planning was military in precision. Wabtec established twenty-five integration teams covering everything from IT systems to cafeteria menus. They discovered surprising synergies—GE's sophisticated supply chain software could optimize Wabtec's procurement. Wabtec's lean manufacturing expertise could improve GE's locomotive assembly. The combined engineering capabilities could accelerate next-generation product development.

The cultural challenge was real but manageable. GE Transportation employees were demoralized after years of uncertainty. Many assumed Wabtec would slash jobs and close facilities. Neupaver personally visited every major site, holding town halls where he committed to maintaining Erie as the locomotive headquarters. His message was consistent: "We didn't buy GE Transportation to dismantle it. We bought it to unleash it."

February 25, 2019: The deal closed after nine months of preparation. The final structure was remarkably close to the original proposal. GE received their $2.9 billion. Shareholders got their stock distributions. Wabtec became a $8 billion revenue company overnight, the undisputed leader in global rail equipment. The stock ticker remained WAB, but everything else had changed.

The first-year results exceeded expectations. Cost synergies hit $150 million, ahead of the $250 million three-year target. Revenue synergies emerged faster than anticipated—railroads loved buying complete solutions from locomotives to brakes. Operating margins expanded from 11% to 13% despite integration costs. Free cash flow exceeded $600 million, funding debt reduction and growth investments.

But the real transformation was strategic. Wabtec now controlled the entire value chain—from components to complete locomotives. They had relationships with every major railroad globally. The installed base exceeded 50,000 units generating predictable service revenue. Digital capabilities from GE's software division positioned them for the industry's technological future. Chinese competition seemed less threatening when customers could access Wabtec's integrated solutions and century of expertise.

One vignette captures the transformation. In late 2019, Indian Railways issued a tender for 1,000 locomotives—potentially the largest order in history. Pre-merger, neither Wabtec nor GE could have competed effectively. But combined, they offered a compelling proposal: GE's Evolution Series locomotive modified for Indian conditions, equipped with Wabtec brakes and controls, supported by local manufacturing and decades of service. They won against Chinese and European competitors, validating the merger thesis.

The financial markets eventually recognized the value creation. By December 2019, Wabtec stock reached $80, up 60% from pre-announcement levels. The company's market cap exceeded $15 billion, creating $7 billion in value from a deal many thought was too complex to succeed. GE's stake, initially worth $5.5 billion, had appreciated to $8 billion—better returns than most of their remaining portfolio.

VIII. Modern Era: Digital Solutions & Decarbonization (2019–Present)

The prototype sat on a test track outside Erie, Pennsylvania, looking deceptively ordinary. To casual observers, it appeared to be just another Evolution Series locomotive in BNSF Railway's distinctive orange livery. But hidden within its 4,400-horsepower frame was technology that would have seemed like science fiction just years earlier: a 2.4-megawatt-hour battery array capable of powering the 430,000-pound machine entirely on electricity. This was FLXdrive, Wabtec's answer to the existential question facing rail: How do you decarbonize an industry that moves 40% of American freight?

The journey to that test track began in an unlikely place—a 2019 customer advisory board meeting where the CEO of Canadian National Railway made a blunt statement: "We've committed to net-zero emissions by 2050. Either you help us get there, or we'll find partners who will." The room fell silent. Rail had always marketed itself as environmentally friendly compared to trucking, but diesel locomotives still burned 3.5 billion gallons of fuel annually in North America alone.

Rafael Santana, who'd joined Wabtec from Tesla to lead the newly formed Digital Intelligence division, saw opportunity where others saw threat. "The automotive industry is proving battery technology at scale," he argued in a strategy session. "We don't need to invent new chemistry—we need to adapt existing solutions to rail's unique demands." His team's analysis was compelling: a battery-electric locomotive could reduce fuel consumption by 30% when paired with conventional diesels, with payback periods under seven years at current fuel prices.

But Wabtec's digital transformation extended far beyond electrification. The GE Transportation acquisition had brought unexpected treasure—a software division with 400 engineers who'd spent a decade developing predictive analytics for rail operations. Their crown jewel was Trip Optimizer, an AI-powered system that analyzed terrain, weather, and train dynamics to optimize speed and fuel consumption. Think of it as autopilot for trains, but with 10% fuel savings worth millions annually to large railroads.

The integration of physical and digital capabilities created possibilities neither company could have achieved independently. Consider the Edge AI platform launched in 2020. By combining GE's locomotive computers with Wabtec's component sensors, they created a neural network spanning entire trains. The system could predict brake failures three weeks in advance, identify bearing problems before they caused derailments, and optimize maintenance schedules to minimize downtime. Union Pacific reported 25% reduction in unplanned maintenance after deploying the system.

The pandemic initially devastated rail traffic, with volumes dropping 20% in Q2 2020. But Wabtec's response demonstrated the resilience of their diversified model. While freight suffered, transit agencies received billions in federal stimulus, accelerating modernization projects. Wabtec pivoted resources, winning major contracts for contactless payment systems and air filtration upgrades. By year-end 2020, transit revenue had actually grown 5% despite the crisis.

Green Friction technology represented another breakthrough hiding in plain sight. Developed by Faiveley engineers but perfected in Wabtec labs, these brake pads reduced particulate emissions by 90% compared to traditional materials. The innovation seemed minor—slightly different composite materials and surface treatments—but the impact was enormous. London Underground adopted them system-wide, improving tunnel air quality dramatically. The European Union began mandating similar technology for all new rolling stock.

The institutional appetite for Wabtec's environmental solutions surprised even management. In 2021, the company issued its first green bond—$500 million at 2.9% interest, specifically earmarked for sustainable technology development. Demand exceeded supply by 4x, with ESG-focused funds competing for allocation. The capital markets were essentially paying Wabtec to develop products that would cannibalize their traditional offerings.

But the real validation came in January 2021 when BNSF ordered 100 FLXdrive locomotives after the successful pilot. The battery units would operate in consists with conventional diesels, capturing energy during braking and providing boost during acceleration. The economics were compelling—$400,000 annual fuel savings per unit, plus significant emissions reductions. It was the largest battery-electric locomotive order in history, worth over $1 billion including service contracts.

Recent acquisitions reflected this digital-first strategy. The 2022 purchase of Trimble's rail business for $85 million brought advanced computer vision capabilities for track inspection. The 2025 acquisition of Evident's Inspection Technologies for $1.78 billion—Wabtec's largest deal since GE—added ultrasonic and robotic inspection systems serving rail, aerospace, and industrial markets. These weren't traditional bolt-on acquisitions but capability accelerators for the digital age.

The organizational transformation was equally dramatic. By 2023, software engineers comprised 15% of Wabtec's workforce, up from 3% in 2018. The company established innovation centers in Austin, Bangalore, and Tel Aviv—locations chosen for tech talent, not manufacturing proximity. They launched Wabtec Ventures, a $100 million fund investing in startups developing autonomous systems, alternative fuels, and advanced materials.

One project exemplified this new Wabtec: the autonomous freight train pilot in Australia. Working with Rio Tinto, they deployed fully autonomous locomotives hauling iron ore across the Pilbara desert. No drivers, no conductors—just AI systems managing 2.5-kilometer-long trains carrying 30,000 tons of cargo. The technology reduced operating costs by 15% while improving safety and consistency. It was a glimpse of rail's future: fewer humans, more intelligence, dramatic efficiency gains.

The financial results validated the strategy. Digital solutions revenue grew from $200 million in 2019 to $800 million in 2023, with 30%+ margins. The installed base of connected assets exceeded 25,000 units, each generating recurring software revenue. Customer retention rates approached 95% as switching costs increased with system integration. The business model was evolving from selling products to selling outcomes—uptime, efficiency, emissions reduction.

Competition was evolving too. Chinese manufacturer CRRC remained a threat in developing markets, but their technology lag was evident. European competitors Knorr-Bremse and Alstom focused on high-speed passenger rail, ceding freight to Wabtec. The real competition came from adjacent industries—autonomous truck companies, hyperloop developers, even drone delivery services. But rail's fundamental physics—steel wheels on steel rails remain the most efficient means of moving heavy loads over land—provided a moat that technology couldn't easily breach.

Environmental regulations became a tailwind rather than headwind. California's Advanced Clean Trains Rule, requiring zero-emission locomotives by 2035, initially seemed catastrophic for diesel manufacturers. But Wabtec was ready with FLXdrive battery units, hydrogen fuel cell prototypes, and hybrid configurations. They weren't fighting regulation but enabling it. Each new environmental standard created replacement demand worth billions.

The supply chain challenges of 2021-2023 tested operational excellence. Semiconductor shortages delayed locomotive deliveries. Steel price volatility crushed margins. Labor shortages impacted manufacturing. But Wabtec's response demonstrated learned resilience: dual-sourcing critical components, passing through cost increases via escalation clauses, and accelerating automation to reduce labor dependence. They emerged stronger, with operating margins reaching 15% by late 2023.

As 2024 progressed, Wabtec faced strategic choices that would define its next decade. Should they double down on battery-electric or pivot to hydrogen? Should they acquire into adjacent markets or deepen rail specialization? Should they optimize for profitability or growth? The answers weren't obvious, but the company's track record suggested they'd find the right balance. After all, this was an organization that had successfully transformed from air brakes to artificial intelligence while maintaining the operational discipline that made them successful in the first place.

IX. Playbook: Business & Investing Lessons

The conference room at Wabtec's 2023 investor day was packed beyond capacity. Fund managers who'd never shown interest in industrial companies were suddenly fascinated by this Pittsburgh brake manufacturer turned rail technology giant. One portfolio manager's question captured the mood: "You've generated 20% annual returns for two decades in a 2% growth industry. What's the secret?" CEO Rafael Santana smiled and pulled up a slide that simply read: "The Wabtec Way."

What followed was a masterclass in industrial strategy that MBA programs should teach but don't. The first principle: consolidation in fragmented markets creates extraordinary value, but only with operational excellence. Wabtec didn't invent roll-up strategies—private equity firms had been trying this in industrials for decades. The difference was execution. While PE firms typically bought companies, cut costs, and flipped quickly, Wabtec integrated deeply, invested in capabilities, and held forever.

Consider the math: Wabtec acquired over 100 companies at an average multiple of 6x EBITDA. Through operational improvements, they expanded margins from 10% to 15-20%. Meanwhile, Wabtec itself traded at 12-15x EBITDA. This multiple arbitrage alone created billions in value. But the real magic was in revenue synergies—cross-selling products through combined channels, bundling solutions, and leveraging customer relationships. These synergies, often 2-3x larger than cost savings, were what separated Wabtec from failed roll-ups.

The second principle: own the installed base in industries with long asset lives. A locomotive operates for 30-40 years. A subway car runs for 25-30 years. Every unit sold creates an annuity stream of parts, service, and upgrades worth multiples of the original purchase price. Wabtec understood this better than competitors who focused on new equipment sales. By 2023, recurring aftermarket revenue comprised 60% of total sales with 25% EBITDA margins. The installed base was like a bond portfolio throwing off predictable cash flows regardless of new equipment cycles.

This led to the third principle: manage cyclicality through diversification across uncorrelated end markets. When North American freight collapsed in 2015-2016, European transit was booming. When Chinese infrastructure spending slowed in 2019, Indian Railways was modernizing. When pandemic crushed passenger rail in 2020, e-commerce drove freight volumes. The portfolio effect smoothed earnings in ways that single-product companies couldn't achieve. Wabtec's revenue never declined more than 10% even in severe recessions, while competitors saw 30-40% drops.

The fourth principle challenged conventional wisdom: technology adoption in traditional industries creates more value than pure-play tech companies. Why? Because incumbents have customer relationships, domain expertise, and switching costs that startups can't replicate. When Wabtec introduced AI-powered trip optimization, they didn't need to convince railroads to trust them—they'd been suppliers for a century. The technology enhanced existing products rather than replacing them. Margins on digital solutions exceeded 40%, but they were sold as part of integrated packages, not standalone software.

Capital allocation was the fifth discipline, and here Wabtec was borderline religious. They followed a strict hierarchy: first, invest in organic growth projects exceeding 20% IRR. Second, pursue acquisitions at reasonable multiples with clear synergies. Third, pay modest but growing dividends (raised for 15 consecutive years). Fourth, buy back stock but only when trading below intrinsic value. What they didn't do was equally important—no "transformational" pivots into unrelated industries, no expensive headquarters, no executive jets.

The acquisition integration playbook deserves special attention. Wabtec developed a 100-day template executed with military precision. Days 1-10: Communicate with customers and employees, ensuring no disruption. Days 11-30: Integrate financial systems and eliminate redundancies. Days 31-60: Identify and capture quick wins—procurement savings, facility consolidation. Days 61-100: Implement commercial synergies and cultural integration. This wasn't just process—it was muscle memory developed over hundreds of deals.

Management incentives aligned perfectly with shareholder interests. Executive compensation was 70% performance-based, tied to ROIC, free cash flow, and relative TSR. No adjusted metrics, no one-time exclusions, no gaming. Stock ownership requirements were substantial—5x salary for the CEO, 3x for senior executives. Many executives held stock worth 10-20x their annual compensation. They thought like owners because they were owners.

The role of activists was surprisingly constructive. When Mario Gabelli accumulated 10% of shares in 2010, demanding higher dividends and faster growth, management listened. When Larry Robbins of Glenview Capital pushed for the GE deal in 2018, they found willing partners. Unlike many industrial companies that fought activists, Wabtec engaged constructively, adopting good ideas while maintaining strategic discipline. The result: activists made money, management kept control, and long-term shareholders benefited.

International expansion strategy was sophisticated beyond typical industrial companies. Rather than simply exporting American products, Wabtec localized aggressively. Indian factories produced for Indian customers at Indian price points. Chinese operations developed products specifically for high-speed rail. European facilities maintained distinct engineering cultures. This "multi-local" approach was expensive but created competitive moats in each geography.

The approach to China was particularly nuanced. While competitors either avoided China (fearing IP theft) or went all-in (chasing growth), Wabtec pursued selective engagement. They manufactured commodity products locally but kept advanced technology in controlled facilities. They partnered with state-owned enterprises for market access but maintained majority control. They accepted lower margins in exchange for scale and learning. By 2023, China generated $600 million in revenue—meaningful but not dependent.

Risk management was boring but effective. Wabtec maintained conservative leverage (Net Debt/EBITDA never exceeding 3.5x), diversified customer exposure (no customer over 10% of revenue), and hedged commodity exposure (70% of steel costs passed through). They avoided fixed-price, long-term contracts that destroyed competitors. They maintained spare capacity for surge demand. They dual-sourced critical components. This belt-and-suspenders approach seemed excessive until disruptions hit—then it looked genius.

The cultural elements were harder to quantify but equally important. Wabtec maintained a blue-collar sensibility despite white-collar success. Executives regularly visited factories, understanding operations intimately. Engineers were celebrated more than financiers. Cost discipline bordered on obsession—travel policies that would make investment bankers weep, offices that resembled 1980s government buildings. This wasn't cheapness but focus—every dollar saved dropped to the bottom line.

Learning from failures was institutionalized. After the troubled Standard Car Truck acquisition in 2008, Wabtec created a "lessons learned" database documenting what went wrong and why. Every new acquisition team studied past mistakes. The 2014 decision to pass on Bombardier Transportation, which later sold to Alstom at a distressed price, was analyzed to understand why discipline trumped empire building. Failures weren't hidden but examined and absorbed.

The balance between standardization and entrepreneurialism was delicate but crucial. Wabtec standardized financial systems, procurement, and back-office functions across all operations. But they preserved local commercial relationships, technical expertise, and product development autonomy. This "tight-loose" structure captured scale economies while maintaining agility. It's why acquired companies often performed better under Wabtec than as independents.

For investors, the lessons were clear but counterintuitive. First, boring businesses with strong moats often generate exceptional returns. Second, serial acquirers can create value if they maintain discipline and operational excellence. Third, cyclical industries offer opportunities for patient capital that growth industries don't. Fourth, management quality matters more in traditional industries where strategy differences are subtle. Fifth, complexity can be a competitive advantage if managed properly.

The quantitative evidence was overwhelming. $10,000 invested in Wabtec at the 1995 IPO was worth over $200,000 by 2024, compared to $60,000 for the S&P 500. Risk-adjusted returns (Sharpe ratio of 0.85) exceeded most tech companies despite lower volatility. Return on invested capital averaged 18% through multiple cycles. Free cash flow conversion exceeded 100% consistently. These weren't lucky outcomes but systematic results of a refined strategy.

X. Analysis & Bear vs. Bull Case

The bear case against Wabtec writes itself with alarming clarity. Start with the obvious: railroads are a 19th-century technology facing 21st-century disruption. Autonomous trucks are no longer science fiction—TuSimple and Waymo are running daily routes on American highways. These robot trucks could operate 24/7, eliminate driver costs, and achieve door-to-door delivery that rail can't match. Why would shippers tolerate rail's inflexibility when autonomous trucking offers the same cost with superior service?

The China threat looms larger than management admits. CRRC, backed by unlimited state capital, offers locomotives at 50% of Wabtec's price. They've already captured markets in Africa, Southeast Asia, and Latin America. Their technology gap is closing rapidly—their latest CRH380 high-speed trains match anything from Europe or Japan. What happens when they seriously target North America? Wabtec's 50% market share could evaporate as customers choose adequate technology at half the price.

Debt levels flash warning signs that bulls ignore. Net debt of $4.5 billion against EBITDA of $1.6 billion puts leverage at 2.8x—manageable in good times but dangerous in downturns. The company has $12 billion in goodwill and intangibles on its balance sheet—accounting fiction that could require massive write-downs if acquisitions underperform. Remember, Wabtec paid 11x EBITDA for GE Transportation. If that business deteriorates, billions in shareholder value vanishes overnight.

The technological disruption extends beyond autonomous trucks. Hyperloop, while still experimental, could make conventional rail obsolete for high-value freight. Drone delivery might eliminate last-mile rail shipments. Even within rail, hydrogen fuel cells could leapfrog Wabtec's battery-electric technology. The company is investing billions in solutions that might be obsolete before they're fully deployed.

Environmental regulations cut both ways. Yes, they create replacement demand, but they also impose massive costs. Developing zero-emission locomotives requires billions in R&D with uncertain returns. California's mandates might be technically impossible to meet, forcing railroads to abandon routes rather than upgrade equipment. European emissions standards are already crushing margins on transit contracts.

The customer concentration risk is hidden but real. While no single customer exceeds 10% of revenue, the Class I railroads collectively represent 40%. These seven companies have oligopsony power—they can squeeze suppliers mercilessly. Union Pacific's recent decision to insource certain maintenance previously outsourced to Wabtec shows how quickly revenue can evaporate. If railroads consolidate further, Wabtec's negotiating position weakens dramatically.

Labor challenges are intensifying, not improving. The 2022 rail strike threat showed how vulnerable the industry remains to union power. Wabtec employs 27,000 people, many in high-cost, unionized facilities. Younger workers don't want manufacturing jobs, creating skill shortages and wage pressure. Automation can only go so far—complex assembly and field service still require human expertise that's increasingly scarce and expensive.

But the bull case remains compelling, grounded in structural advantages that bears underestimate.

Start with the physics that technology can't change: moving a ton of freight 480 miles on one gallon of fuel. Trucks, even autonomous ones, require 3-4x more energy. In an era of climate consciousness and carbon pricing, rail's efficiency advantage only grows. No amount of software can overcome steel wheels on steel rails being fundamentally more efficient than rubber on asphalt.

The installed base moat is practically insurmountable. Wabtec has equipment on 50,000+ rail vehicles globally, each generating service revenue for decades. Switching costs are enormous—not just equipment replacement but retraining, spare parts inventory, and system integration. Even if competitors offered free locomotives, railroads couldn't afford the switching costs. This is enterprise software stickiness applied to physical assets.

The acquisition pipeline remains robust despite past consolidation. Hundreds of family-owned suppliers across Europe and Asia need succession solutions. Distressed assets from COVID impacts are available at attractive prices. The recent Evident acquisition shows Wabtec can expand into adjacent inspection and testing markets worth $10+ billion. At current multiples, every $1 billion deployed in acquisitions creates $1.5-2 billion in market value.

Digital transformation is accelerating, not theoretical. Wabtec's software revenue is growing 30% annually with 40% margins. Their AI-powered trip optimization saves railroads millions in fuel costs—real, measurable ROI that ensures adoption. The company has 15,000 connected assets generating data that improves predictive maintenance algorithms daily. Network effects are emerging as more assets connect—each new installation makes the system smarter for all users.

The decarbonization opportunity is massive and Wabtec is winning. FLXdrive orders exceed $2 billion with deliveries through 2028. The hydrogen fuel cell prototype achieved 1,000-mile range in testing. Green Friction brake pads are becoming mandatory in Europe. The company isn't hoping for environmental regulations—they're banking on them. Every tightening standard creates replacement demand worth billions.

Geographic diversification provides multiple growth vectors. India is investing $500 billion in rail infrastructure through 2030. The European Green Deal allocates €550 billion for sustainable transport. Even China, despite local competition, needs Western technology for certain applications. Wabtec generates 40% of revenue internationally with higher growth rates than North America.

The financial algorithm is beautiful in its simplicity. Organic revenue growth of 3-5% plus bolt-on acquisitions adding 2-3% plus margin expansion of 50 bps annually equals high-single-digit EBITDA growth. Convert 100% to free cash flow. Deploy at 15-20% returns through acquisitions and buybacks. The result: low-teens EPS growth with minimal risk. It's the Berkshire Hathaway model applied to rail equipment.

Valuation remains reasonable despite the stock's performance. At 14x forward EBITDA, Wabtec trades at a discount to industrial peers like Parker Hannifin (16x) or Fortive (18x). On a PEG basis, paying 14x for 10% growth is attractive when software companies trade at 30x for similar growth rates. The free cash flow yield of 5% exceeds investment-grade bond yields with equity upside.

Management's track record deserves premium valuation. They've completed 100+ acquisitions without a major failure. They've navigated multiple cycles while growing margins. They've transformed from components to systems to software while maintaining operational discipline. This isn't a management team learning on the job—they've written the playbook others study.

The optionality is underappreciated. If autonomous trains become reality, Wabtec supplies the technology. If hydrogen dominates, they're developing fuel cells. If China closes markets, other geographies compensate. If regulations tighten, replacement demand accelerates. The company isn't betting on one future but positioning for multiple scenarios. This optionality has value that traditional models don't capture.

Risk mitigation is more sophisticated than bears acknowledge. Geographic diversification, product breadth, and aftermarket exposure create portfolio effects that smooth volatility. The company survived 2008-2009 with only a 10% revenue decline. They navigated COVID with minimal disruption. This resilience is worth paying for in an uncertain world.

The competitive position is strengthening, not weakening. Scale advantages in R&D, procurement, and service infrastructure grow with each acquisition. Digital capabilities require investments smaller competitors can't match. Regulatory compliance costs favor incumbents with resources. The industry is bifurcating between global champions and niche players—Wabtec is firmly in the former category.

The weight of evidence tilts bullish, but with important caveats.

This isn't a hyper-growth story that will double overnight. It's a compound returns machine that steadily creates value through cycles. Investors need patience, tolerance for complexity, and appreciation for industrial businesses. The stock will be volatile—rail is cyclical, and markets will periodically panic about disruption or recession. But for investors with 5+ year horizons, Wabtec offers a rare combination: defensive characteristics with offensive opportunities, proven execution with transformation potential, and reasonable valuation with multiple expansion possibilities.

The key metrics to monitor: aftermarket revenue growth (should exceed 5% annually), digital revenue expansion (targeting $1.5 billion by 2025), ROIC maintenance (above 15%), and successful integration of acquisitions (synergy achievement rates). If these metrics hold, the equity should compound at low-teens rates with lower volatility than the broader market.

XI. Epilogue & "If We Were CEOs"

Standing in Wabtec's Erie locomotive facility on a gray November morning in 2024, you can feel the tension between past and future. On one side of the massive complex, workers assemble Evolution Series diesels using techniques refined over decades—precision welding, careful cable routing, methodical testing. On the other side, engineers huddle around computer screens, monitoring battery performance data streaming from FLXdrive units operating across North America. This physical juxtaposition captures Wabtec's strategic challenge: honoring a 155-year heritage while building for a radically different future.