Reliance, Inc.: The Quiet Compounding Machine of American Industry

I. Introduction: The Steel Supermarket Nobody Talks About

In an era when technology stocks dominate investor conversations and software-as-a-service companies command eye-watering valuations, there exists a Fortune 500 giant that most Americans have never heard of—despite the fact that it helped build the very structures housing their offices, airports, and data centers.

Reliance, Inc., headquartered in Scottsdale, Arizona, is the largest metals service center operator in North America. The company provides metals processing services and distributes a line of approximately 100,000 metal products, including aluminum, brass, alloy, copper, carbon steel, stainless steel, titanium, and specialty metal products to 125,000 customers such as fabricators and manufacturers.

The company is ranked 247th on the Fortune 500. In 2024, the company made a revenue of $13.83 billion—a sum that would make it a household name were it selling smartphones or streaming subscriptions rather than precision-cut aluminum sheets and carbon steel bars.

The hook for today's deep dive: How did a rebar distributor from Depression-era Los Angeles become the largest metals service center in North America through 80+ years of patient compounding? And more importantly, what can long-term investors learn from this unsexy masterclass in serial acquisition, decentralized management, and counter-cyclical capital allocation?

The themes that emerge from Reliance's eight-decade journey are timeless: the art of buying family businesses and letting them flourish; the discipline to invest when others are panicking; and the compounding power of being the essential "middleman" in industrial America—a role that sophisticated observers might dismiss but that customers desperately need.

Since its 1994 IPO, Reliance has completed more than 65 acquisitions. That's roughly two acquisitions per year, every year, for three decades—a cadence that would make even the most aggressive private equity shop take notice. Yet Reliance has executed this strategy without the leverage-laden playbooks that define modern financial engineering. It has done so while paying regular quarterly cash dividends for 64 consecutive years without reduction or suspension.

This is the story of how a company built an empire by getting the boring things right, repeatedly, for longer than most investors' time horizons extend.

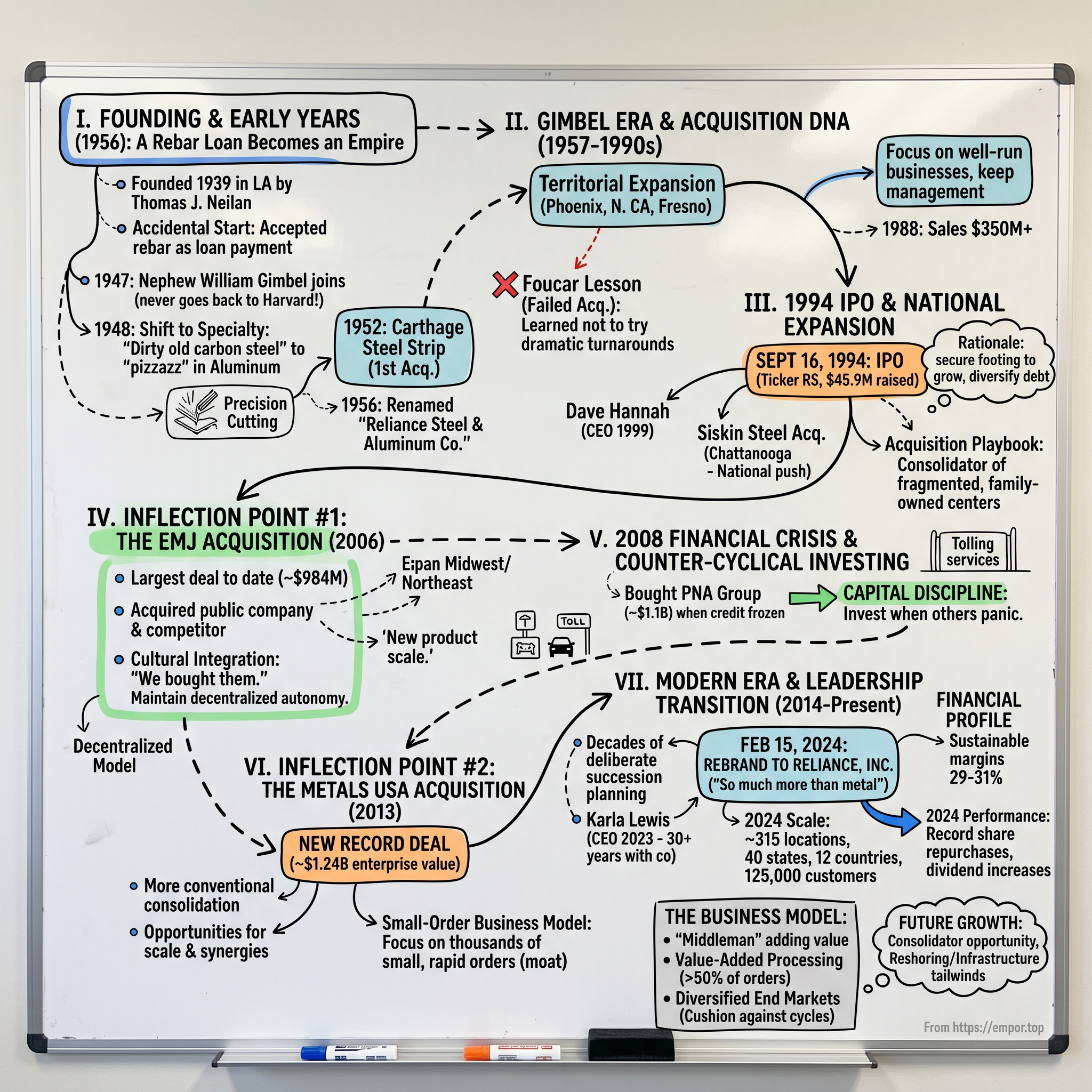

II. Founding & Early Years (1939–1956): A Rebar Loan Becomes an Empire

The Accidental Steel Man

The origin story of Reliance reads less like a founder's manifesto and more like a happy accident rooted in Depression-era pragmatism.

Reliance Steel & Aluminum Company was founded in Los Angeles on February 3, 1939 by Thomas J. Neilan. Originally named Reliance Steel Products Company, the business made and sold steel reinforcing bars (rebar) for the construction industry.

But the genesis was even more serendipitous. The story begins in 1939, when founder Thomas Neilan reluctantly accepted a few tons of rebar as payment for a loan. Neilan, who operated another company called N.J. Thomas and Co.—an oil well supply and real estate holding company—had lent money to a friend who worked for a steel company in northern California. When the friend couldn't repay, he sent steel rebar instead. Neilan, displaying the entrepreneurial instinct that would define the company's future, had the rebar fabricated, sold it, and made money. He kept buying more.

Thomas Neilan established Reliance Steel Products Company, a distributor of steel reinforcing bar, on February 3, 1939, in Los Angeles, California. Reliance subleased 6,600 square feet of warehouse space from Allied Supply Company on 37th Street in the city of Vernon, just outside Downtown Los Angeles.

The location was no accident. Los Angeles in 1939 stood at the precipice of extraordinary growth. The pre-war defense buildup, followed by the aerospace boom and California's post-war population explosion, would transform the region into one of America's great industrial centers. A small rebar distributor in Vernon—the industrial heart of Southern California—was perfectly positioned to ride that wave.

In 1944, the name was shortened to Reliance Steel Company.

The Nephew Who Never Went to Harvard

The next chapter in Reliance's story involves one of those pivotal moments that seems minor at the time but reshapes everything that follows.

In 1947, Thomas Neilan offered to fund his nephew's graduate studies at Harvard if he would work at Reliance for a year. William Gimbel accepted and joins Reliance as Warehouseman. Little does he know he will never go back to school.

This was more than a family favor—it was succession planning disguised as educational opportunity. Reliance recorded $1.2M in revenue that year, a modest sum but growing steadily as California construction boomed.

The Strategic Pivot to Specialty

In 1948, Reliance Steel also began manufacturing products of aluminum and magnesium. This pivot from pure rebar distribution to specialty metals would prove prescient. Reliance's product offering in 1948 expanded to include aluminum. The following year, Reliance becomes the nation's first distributor of magnesium.

William Gimbel later articulated the philosophy behind this evolution: "We started out (in 1939) with the dirty, old, down-in-the-gutter carbon steel, but that became a world commodity. So we decided that we wanted to upgrade into something that had a little bit more pizzazz, and we picked aluminum and magnesium."

That decision to seek "pizzazz"—to move up the value chain toward specialty materials that commanded higher margins and required more expertise—established a strategic template that Reliance would follow for decades: find products where expertise and service matter more than pure price competition.

First Acquisition and Growth

Reliance made its first acquisition in 1952: Carthage Steel Strip, in South Gate, California. The addition of precision cutting equipment, at the time a very new technology, greatly expanded business capabilities. By 1952, sales reached $4M and 7 acres were purchased on 26th Street in Vernon, CA, to accommodate the company's growth during the postwar manufacturing boom.

This first acquisition established another template: buy companies with capabilities you don't have, integrate the technology, expand the business. The precision cutting equipment from Carthage Steel Strip transformed Reliance from a simple distributor into a value-added processor—a distinction that would become central to its identity.

In 1956, the company was renamed for a second time to reflect its expanding product lines: Reliance Steel & Aluminum Co.

The company that would eventually distribute 100,000 products to 125,000 customers had found its foundation. But the real story was about to begin.

III. The Gimbel Era & Acquisition DNA (1957–1990s)

Succession, Near-Sale, and the Decision to Build

Gimbel, who started as a warehouse man, succeeded Neilan in 1957 as president of the company, a year after its name was changed to Reliance Steel & Aluminum Company.

The circumstances of this succession nearly led to a very different outcome. In the 1950s, the company was on the other side of the table. Before he passed away in 1957, Neilan was in discussions with another company to sell Reliance. Upon his death, the deal was put on hold and his nephew William Gimbel, who began his career in Reliance's warehouse, became president. "He, along with the other officers and board members of Reliance, decided they weren't going to pursue selling the company," Hannah says.

This decision—to build rather than sell—set the course for everything that followed. "Just like many of the companies that we have acquired and a lot of companies that still exist in the industry today, we had large family ownership," David Hannah continued. "We were fortunate that our founding family wanted to continue to grow the company as opposed to selling it and getting the cash or monetizing their investment."

The Gimbel-Crider Partnership

Under Gimbel, Reliance began its long-running territorial expansion, naming a resident sales agent in Phoenix in 1958. Two years later, Reliance acquired a small Phoenix-based competitor, the Effron Steel Co. With the purchase of another competitor, the Westates Steel Co., in Santa Clara, Reliance Steel expanded into Northern California in 1961. In 1963, Reliance continued its growth through acquisition by purchasing the Drake Steel Supply Co., which operated metals service centers in Fresno and San Diego, California.

The Drake Steel acquisition brought something perhaps more valuable than territory: With the purchase, Reliance also acquired the services of Joe D. Crider, who had joined Drake in 1949 as a billing clerk and worked his way up to Fresno sales manager.

Joe Crider was made Executive Vice President in 1975. During the next 12 years, Bill Gimbel and Joe Crider were called "perhaps the best known management team in the service center industry" by Metal Center News.

This partnership embodied what would become the Reliance approach to human capital: identify talent through acquisition, promote from within, and build leadership teams that span decades rather than quarters.

Learning from Failure: The Foucar Lesson

Every great acquirer eventually encounters a deal that doesn't work. What separates sustainable compounders from one-hit wonders is how they learn from failure.

In 1980, Reliance also acquired Foucar, Ray & Simon, a specialty tube distributor in Hayward, California, with a branch in Portland, Oregon. The Hayward center was eventually merged into the Reliance center in Santa Clara. The Portland operation foundered and then closed in 1984.

Gimbel's candid reflection on this failure reveals the intellectual honesty that characterized his leadership: "Foucar was probably the second oldest service center in California, with a good reputation. They'd done well over the years, but I guess they'd gotten rigor mortis. We thought that we could change all that. We tried and tried to change it, and it didn't work. So we had to admit defeat and close up the place."

The setback, however, did not slow the company's aggressive growth.

The lesson Reliance took from Foucar—that you cannot always transform a declining culture—would inform its future acquisition strategy. Going forward, the company would focus on buying well-run businesses with strong management and letting them continue operating as they had, rather than attempting dramatic turnarounds.

Specialty Metal Strategy

After more than three decades of operating full-service metals service centers, Reliance opened its first "specialty store" in 1976, forming the Tube Service Company, in Santa Fe Springs, California. The subsidiary specialized in tubular products.

To manage its aluminum, magnesium, and stainless steel products, Reliance created a nonferrous metals division, Reliance Metalcenter, in 1980.

By 1988, the company's 50th year, sales topped $350 million.

The company had grown from a rebar distributor in a 6,600-square-foot sublease to a diversified metals processor with operations across the Western United States. But the real acceleration was still to come—and it would require accessing public capital markets.

IV. The 1994 IPO & National Expansion

Going Public After 55 Years

In 1994, after 55 years as a closely held operation, Reliance issued its first public stock. At the time, the company had about 180 stockholders, most of them employees or relatives of founder Thomas J. Neilan. Reliance had previously considered, and rejected, going public several times.

The timing wasn't accidental. "We'd go and talk to the brokers, but, unfortunately, anything with the name steel in it didn't get them very excited," Gimbel had told Metal Service News in 1984. A decade later, the market was more receptive.

In 1995, Dave Hannah was promoted to President and Gregg Mollins to Chief Operating Officer. On September 16, 1994, Reliance issues 3.5 million new shares in its IPO, raising $45.9M and making Reliance a publicly-traded company on the New York Stock Exchange under the ticker symbol "RS."

The strategic rationale was clear. "The cyclical nature of the service center business makes it risky to finance growth with debt. If you get caught with too much debt in a downturn, it can cause some real problems for a company. It can put you out of business. So we felt [the IPO] was a good way to secure some financial footing in our strategy to grow the company."

"It also created an opportunity for family members to sell their stock [if] they wanted to," Hannah added. Without public shareholders, "the burden really falls on the company to buy those family members out."

William Gimbel retired later in 1994 but remained Chairman of the Board until 1997 (and Chair Emeritus until his passing in 1998).

The Acquisition Playbook Emerges

The IPO prospectus signaled what was to come: "Traditionally, metals service centers have been small, family-owned businesses that lack the diversity of experience and successful operating techniques of Reliance and thus have and may in the future become candidates for acquisition or consolidation."

This wasn't just corporate boilerplate—it was a declaration of intent. The metals service center industry was fragmented, with thousands of small, family-owned operations serving local markets. Reliance saw itself as the natural consolidator.

In 1996, Reliance acquired Siskin Steel & Supply Co., headquartered in Chattanooga, Tennessee. It was one of the oldest companies in the industry and an "integral part of our strategy to become a national company with operations extending beyond the Western half of the United States," according to David Hannah.

With the additions of AMI Metals, Inc. and Service Steel Aerospace Corp. in 1997, Reliance entered the aerospace industry. With sales at $654M, Reliance logged its 6th consecutive year of record sales.

The David Hannah Leadership Era

Mr. Hannah became Chief Executive Officer of Reliance in January 1999. He served as President from November 1995 to January 2002. Prior to that, he was appointed a Director in 1992 and had served as an Executive Vice President and as Chief Financial Officer since he joined Reliance in May 1981.

When Hannah came on board, Reliance was a regional player. Under his leadership, it would become a national and eventually international force. The transformation involved not just acquisitions but a conscious decision to maintain the decentralized culture that had characterized the company since Gimbel's era.

V. INFLECTION POINT #1: The EMJ Acquisition (2006)

The Transformational Deal

In April 2006, Reliance announced the largest deal in its history—one that would fundamentally reshape the company's position in the industry.

April 4, 2006 — Reliance Steel & Aluminum Co. completed its acquisition of Earle M. Jorgensen Co. The transaction was valued at approximately $984 million, including the assumption of EMJ's net debt, with a per-share consideration of $14.21.

Reliance acquired its longtime and well-respected competitor, Earle M. Jorgensen Company. The addition of EMJ's numerous facilities expanded Reliance's presence across the United States and Canada. The deal marked Reliance's first acquisition of a public company and was partially funded using Reliance stock.

The significance of this deal cannot be overstated. David H. Hannah, CEO of Reliance, said, "We are very excited about EMJ becoming a member of our Reliance family. This will be our largest acquisition to date and our first acquisition of a public company. This transaction will add a total of 39 facilities in the United States and Canada to our existing network. We will significantly increase our geographic, product and customer diversification by combining with an industry peer that complements our reputation for excellence and our corporate culture."

Why EMJ Mattered

EMJ was one of the largest distributors of metal products in North America with 40 service and processing centers. EMJ inventories more than 25,000 different bar, tubing, plate, and various other metal products, specializing in cold finished carbon and alloy bars, mechanical tubing, stainless bars and shapes, aluminum bars, shapes and tubes.

The combined companies had more than 150 locations in 35 states and Belgium, Canada, China and South Korea with total assets of approximately $3 billion and annual revenues of more than $5 billion.

The EMJ acquisition brought products Reliance hadn't previously carried at scale. It established the company's presence in the Midwest and Northeast. And it demonstrated that Reliance could successfully integrate a public company while preserving its culture.

The Cultural Integration Philosophy

Perhaps the most telling aspect of the EMJ deal was how Reliance approached integration. Karla Lewis, who would eventually become CEO, recalled an anecdote that captures the company's approach:

"I'm not the only one who's worked at Reliance over 30 years, so we had a lot of longtime employees who grew up working at Reliance in LA knowing Jorgensen. The day we put the press release out about the acquisition, I had a few of them come to me and say, 'Karla, they bought us, right?' We said, 'No, no, no. We bought them.'"

"These are employees, because of the way we stayed decentralized and gave the autonomy, they hadn't realized that Reliance had become larger than EMJ. But it was a transformational product. It got us into many more geographic locations. It got us into some products that we had not historically been in. Timing with the market was good. That was a great acquisition for us."

Hannah articulated the integration philosophy explicitly: "EMJ illustrated that there are a lot of different paths to success. We look at the culture of the companies we acquire and the way they have done business and we embrace it and help them refine it, but we don't change it. We've got a lot of different cultures within the company and as long as we can take that and live together and learn from each other, we don't need to change each other."

"[EMJ] transformed our business to a great extent," Hannah continued. "Their business is much more centralized, especially from a buying perspective. It needs to be because of the types of products they are in."

This willingness to accommodate different operating models within the same corporate umbrella—rather than forcing all acquisitions into a single template—would become a defining characteristic of Reliance's approach.

VI. The 2008 Financial Crisis & Counter-Cyclical Investing

Buying When Others Are Selling

As the global financial crisis unfolded in 2008, most companies retrenched. Reliance did the opposite.

In August 2008, Reliance acquired the PNA Group of 23 service centers and seven joint ventures. This acquisition added Delta Steel, LP, Feralloy Corporation, Infra-Metals Co., Metals Supply Company, Ltd., Precision Flamecutting and Steel, LP and Sugar Steel to Reliance's family of companies.

The 2008 PNA Group acquisition was for about $1.1 billion, incorporating 23 service centers and seven joint ventures, which expanded its footprint in the Midwest and Southeast while enhancing capabilities in steel processing and tolling services. The transaction emphasized acquiring regionally strong operators to achieve greater market density and reduce transportation costs through localized inventory management.

This $1.1 billion deal—executed as credit markets froze and competitors struggled to survive—exemplified the counter-cyclical discipline that had characterized Reliance since its founding. The company's conservative balance sheet management during good times provided the firepower to act opportunistically when others couldn't.

The PNA Group acquisition brought capabilities in tolling services—where Reliance processes customer-owned metal rather than selling its own inventory—expanding the company's service offering and reducing its exposure to commodity price fluctuations.

VII. INFLECTION POINT #2: The Metals USA Acquisition (2013)

The Largest Deal in Company History

April 15, 2013 - Reliance Steel & Aluminum Co. completed the previously announced acquisition of Metals USA Holdings Corp. for US$20.65 per share in cash, pursuant to which Metals USA has become a wholly-owned subsidiary of Reliance.

This acquisition added a total of 48 service centers strategically located throughout the U.S. to Reliance's existing operations and complemented its existing customer base, product mix and geographic footprint. The purchase price for Metals USA was US$786 million paid in cash at closing for the holders of Metals USA stock, options and restricted stock, and the assumption of US$454 million of net debt, representing a Metals USA enterprise value of approximately US$1.24 billion.

The April 2013 acquisition of Metals USA Holding Corp. was the largest purchase in company history. The deal added 48 service centers throughout the United States to Reliance's portfolio.

Unlike the EMJ acquisition, which brought new products and geographic expansion, Metals USA was a more conventional consolidation play. The company bought, sold, and processed many of the same products as Reliance. This created opportunities for operational synergies and procurement scale that hadn't existed with EMJ's differentiated product mix.

The Small-Order Business Model

The Metals USA integration also reinforced Reliance's commitment to a business model that distinguished it from larger competitors: focus on small orders with rapid turnaround.

Hannah explained the model: "We tend to focus on smaller orders. In 2013, about 40 percent of our orders were customers calling us today and wanting their metal tomorrow. Our average order size was $1,660. That's a lot of orders to get up to $9.2 billion in revenue."

This focus on small orders creates a moat that's difficult for competitors to replicate. Large mills don't want to handle thousands of small orders with next-day delivery requirements. Customers who need flexibility and speed are willing to pay a premium for service. And the fragmented customer base reduces concentration risk.

"We congratulate Reliance on its acquisition of Metals USA. It has been Apollo's pleasure to work with Metals USA and the management team and we are very proud of what we have been able to collectively accomplish. The sale of Metals USA concludes a successful investment for Apollo," said M. Ali Rashid, senior partner at Apollo Global Management, which was the majority stockholder of Metals USA.

VIII. The Modern Era: Leadership Transition and Continued Compounding (2014–Present)

The Succession Pipeline

Reliance's leadership transitions have been notably smooth—a reflection of deliberate succession planning that spans decades rather than quarters.

In March 2015, Reliance announced an executive leadership succession plan. David H. Hannah, who served as Reliance's Chief Executive Officer since 1999 and Chairman of the Board and CEO since 2007, announced his intention to transition from his role as CEO. Gregg J. Mollins, who served as President and Chief Operating Officer of Reliance, succeeded Mr. Hannah as President and CEO. Mr. Hannah remained on the Company's Board of Directors as Executive Chairman until July 2016.

When Mollins stepped down, the transition to Karla Lewis was equally methodical.

Mark Kaminski, Reliance's Chairman of the Board, stated: "The Board is also pleased to announce Karla Lewis' promotion to Chief Executive Officer, which is the result of a strategic, deliberate and well-executed long-term succession planning process. Karla has been an integral part of Reliance's executive management team for 30 years and brings unique, first-hand knowledge of Reliance's operations, financial position and strategic vision."

Karla Lewis: From Controller to CEO

Karla R. Lewis started her career as a public accountant with Ernst & Young (Ernst & Whinney). In 1992, Mrs. Lewis left Ernst & Young to join Reliance as the company's first controller. When Reliance became a public company in 1994, Mrs. Lewis designed and implemented the financial controls and reporting to meet SEC and other requirements. She was promoted to Vice President in 1995, to Chief Financial Officer in 1999, to Executive Vice President in 2002, and to Senior Executive Vice President & Chief Financial Officer in 2015.

In 2017, Mrs. Lewis further undertook operational responsibility on a number of Reliance subsidiaries and in January 2021, she was promoted to President and appointed a director of Reliance. Mrs. Lewis was named President and Chief Executive Officer of Reliance effective January 1, 2023.

Lewis's journey from controller to CEO—spanning more than three decades—embodies the Reliance culture of promotion from within. Her deep knowledge of both the financial and operational sides of the business provides a foundation for continued disciplined execution.

The 2024 Rebranding

Reliance Steel & Aluminum Co. changed the company name to Reliance, Inc. on February 15, 2024.

"I'm excited to introduce our new company identity as Reliance, Inc. Over the years, retaining 'Steel & Aluminum' in our corporate name has limited the perception of our company because Reliance is so much more than metal."

The rebranding reflects the company's evolution from a regional steel and aluminum distributor to a diversified metals solutions provider serving multiple end markets with an expanding range of value-added services.

Current Scale and Performance

Reliance's Family of Companies is a network of approximately 315 locations in 40 states and 12 countries outside of the United States. Today, Reliance is a leading diversified metal solutions provider, offering value-added metals processing services and distributing over 100,000 metal products to more than 125,000 customers in a broad range of industries.

In its 2024 financial report, Reliance announced substantial achievements including their third highest annual cash flow from operations at $1.43 billion and a record stock repurchase of $1.09 billion, reducing outstanding shares by 6%.

The company also completed four acquisitions and increased its quarterly dividend by 9.1% to $1.20 per share.

IX. The Business Model Deep Dive: How a Metals Service Center Works

The Essential Middleman

Understanding why Reliance exists requires understanding why steel mills don't sell directly to small customers.

A steel mill is a capital-intensive operation optimized for large production runs. The company buys steel and nonferrous metals in bulk from primary producers and cuts it to size for smaller buyers. Mills want to produce thousands of tons of standardized product and ship it in railcar quantities to a handful of large buyers. They have neither the infrastructure nor the incentive to handle thousands of small orders requiring custom cutting and next-day delivery.

Reliance focuses on small orders with quick turnaround and value-added processing services. In 2024, Reliance's average order size was $2,980, approximately 50% of orders included value-added processing, and approximately 40% of orders were delivered within 24 hours.

This is the service center's value proposition: aggregate demand from thousands of small customers, hold inventory across hundreds of locations, and provide the cutting, forming, and processing services that transform raw metal into components ready for manufacturing.

Value-Added Processing

The shift toward value-added processing represents a strategic evolution that has accelerated under recent management.

Reliance focuses on small orders with quick turnaround and increasing levels of value-added processing. In 2019, Reliance's average order size was $2,090, approximately 51% of orders included value-added processing and approximately 40% of orders were delivered within 24 hours.

The percentage of orders including value-added processing has grown from roughly 40% to 50% over recent years. This isn't just about higher prices per ton—it's about stickier customer relationships. A customer who relies on Reliance for precision cutting to exacting specifications is far less likely to switch to a competitor offering marginally lower prices on commodity products.

The Decentralized Model

Unlike some of its competitors, Reliance Steel & Aluminum operates through a decentralized structure, which enables it to respond quickly to market changes and maintain profitability.

Lewis has articulated the philosophy clearly: "We've strategically grown in a decentralized way by product, by end market, by geography. We think that's important because in our world, we can't control underlying metal prices coming from the mills. We pass those through, we pass the price on with a markup to our customers. If we're all in aluminum, we're all in carbon flat rolled, our earnings results we believe would be much more volatile. That's why we try to have this diversification across our products."

The company network includes over 75 brands, including Phoenix Metals, United Pipe & Steel, Allegheny Steel Distributors, Best Manufacturing, CCC Steel, Delta Steel, EMJ, Feralloy, Infra-Metals Co., KMS Fab LLC and KMS South, Liebovich, Metals USA, National Specialty Alloys, Pacific Metal, Reliance Metalcenter, Siskin Steel, Tube Service, Valex, and Yarde Metals.

Each of these brands maintains its own identity, customer relationships, and operational autonomy. Corporate headquarters provides capital allocation, financial controls, and strategic direction—but the people closest to customers make day-to-day decisions.

Financial Profile

The company maintains a long-term sustainable gross profit margin range of 29% to 31%.

This consistent margin range—maintained across commodity cycles, through acquisitions, and during economic volatility—reflects both the value Reliance provides to customers and the discipline with which it manages pricing and costs.

Reliance maintains total debt of $1.4 billion with a net debt to EBITDA ratio of less than 1.

The conservative leverage profile provides flexibility for opportunistic acquisitions while ensuring the company can weather cyclical downturns without financial distress.

X. Competitive Dynamics and Industry Analysis

The Fragmented Landscape

In 2024, over 9,000 metal service centers are estimated to be operational globally, providing a range of processed metal products including flat, long, and tubular forms. These centers act as vital intermediaries between metal producers and end users, offering value-added services such as cutting, slitting, and warehousing.

In the United States alone, more than 3,000 service centers handle over 42 million metric tons of metal annually, including stainless steel, aluminum, and carbon steel.

Despite this fragmentation, consolidation has accelerated. The metal service center landscape is more consolidated than ever. The Nos. 1 and 2 players—Reliance Inc. and now a combined Ryerson and Olympic—will serve a sizable portion of the metal market.

The Ryerson-Olympic Merger

The October 2025 announcement that Ryerson and Olympic Steel would merge represents the most significant competitive development in the industry in years.

Ryerson President and CEO Eddie Lehner described the combination as "a compelling and attractive merger" that will create the second-largest metals service center in North America, with more than $6.5 billion in annual revenue and a network of 160 facilities.

The executives emphasized synergies totaling $120 million over two years. They cited complementary product portfolios and geographic footprints.

Even combined, Ryerson-Olympic will have less than half of Reliance's revenue. The merger actually highlights Reliance's scale advantages—the combined competitor will still be significantly smaller, and the integration process will consume management attention and create potential disruption that Reliance can exploit.

Porter's Five Forces Analysis

Threat of New Entrants: LOW The metals service center business requires substantial capital investment in inventory, facilities, and processing equipment. More importantly, it requires deep customer relationships built over decades and specialized expertise in sourcing, inventory management, and value-added processing. Reliance's 86-year operating history and network of 315 locations create barriers that new entrants cannot easily overcome.

Bargaining Power of Suppliers: MODERATE Mills represent concentrated suppliers, but the service center industry's fragmentation creates competition for mill products. Reliance's scale—as the largest buyer in the industry—provides meaningful procurement leverage. The company's diversification across multiple metal types and multiple suppliers reduces dependence on any single source.

Bargaining Power of Buyers: MODERATE Reliance serves 125,000 customers, with no single customer representing a material percentage of revenue. The average order size of roughly $3,000 reflects a customer base of small and mid-sized manufacturers who value service and reliability over pure price competition. For these customers, the cost of switching to an alternative supplier—particularly one that might not be able to provide next-day delivery—often exceeds any potential savings.

Threat of Substitutes: LOW Metal remains essential for construction, manufacturing, aerospace, and industrial applications. While alternative materials exist for specific applications, there is no substitute for the broad range of metal products and processing services that Reliance provides.

Industry Rivalry: MODERATE TO HIGH The metals service center industry is competitive, with thousands of participants ranging from small regional players to national chains. However, Reliance's scale, diversification, and focus on value-added services provide differentiation that reduces direct price competition.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Reliance benefits from procurement leverage with mills, shared corporate functions across 315 locations, and the ability to spread fixed costs (IT systems, compliance, management overhead) across a much larger revenue base than competitors.

Network Effects: Limited direct network effects, but Reliance's breadth of locations creates density advantages—more locations mean shorter delivery distances and faster service to customers.

Counter-Positioning: Reliance's decentralized model and focus on small orders represents a counter-position that large mills cannot replicate. Mills are optimized for large production runs and bulk shipments; attempting to serve small customers would cannibalize their core economics.

Switching Costs: Customers who rely on Reliance for specialized processing, custom specifications, and rapid delivery face meaningful switching costs. The time to qualify an alternative supplier, test their capabilities, and establish inventory positions creates friction that protects incumbent relationships.

Branding: Limited brand premium in the traditional sense, but Reliance's reputation for reliability and service creates preference among sophisticated buyers who understand the cost of supply chain disruption.

Cornered Resource: Access to 86 years of institutional knowledge about metals sourcing, processing, and customer service. This expertise is embedded in the company's people and processes in ways that cannot easily be replicated.

Process Power: Reliance's acquisition integration methodology—buying well-run family businesses, keeping management, maintaining autonomy—represents a differentiated process that has been refined over 65+ acquisitions. This process enables continued consolidation at a pace competitors cannot match.

XI. Key Performance Indicators for Long-Term Investors

For investors tracking Reliance's ongoing performance, two metrics warrant particular attention:

1. Gross Profit Margin (Target: 29-31%)

This is the KPI that management emphasizes most frequently in earnings calls and investor communications. The company maintains a long-term sustainable gross profit margin range of 29% to 31%.

Why it matters: Gross profit margin reflects both pricing discipline and the value customers place on Reliance's services. In a commodity-driven business, maintaining margins through cycles demonstrates competitive advantage. Sustained margins above 29% indicate the company is not sacrificing profitability to chase volume; margins consistently above 31% might suggest pricing power that could attract competitive response.

2. Tons Sold vs. Industry Shipments

Reliance's tons sold increased 6.2% compared to the third quarter of 2024, significantly outperforming the service center industry, which reported a decrease of 2.9% in the same comparative period. Our outperformance of the industry demonstrates our ability to gain share in a demand environment constrained by market uncertainty.

Why it matters: Consistent outperformance versus industry shipment trends indicates market share gains driven by service quality, product availability, and processing capabilities. This metric distinguishes genuine competitive performance from broad industry tailwinds.

XII. Bull Case, Bear Case, and Investor Considerations

Bull Case

The Consolidator's Advantage: With 9,000+ metal service centers globally and thousands in the U.S. alone, the acquisition opportunity set remains vast. Reliance's proven integration playbook, conservative balance sheet, and management expertise position it to continue acquiring well-run family businesses at reasonable valuations for decades to come.

Value-Added Processing Tailwind: As manufacturers increasingly outsource first-stage processing to focus on their core competencies, Reliance's investment in processing capabilities positions it to capture additional revenue per ton shipped. The shift from 40% to 50% of orders including value-added processing demonstrates this trend in action.

Reshoring and Infrastructure: The CHIPS Act, Inflation Reduction Act, and broader reshoring trends create structural demand tailwinds for domestic metal consumption. Improved demand for Reliance's products was driven by Reliance's scale and geographic diversity that allowed the company to benefit from heightened data center construction and related infrastructure, as well as publicly funded infrastructure projects such as schools, hospitals and airports.

Capital Return Discipline: Reliance, Inc. (RS) has increased its dividends for 15 consecutive years. The combination of dividend growth and share repurchases provides compounding returns to patient shareholders while the business continues to grow through acquisitions.

Bear Case

Cyclical Exposure: Metals demand correlates with industrial production and construction activity. The merger comes as the steel industry weathers what the executives described as a downturn that's now stretching into its third year. Service center shipments have fallen both sequentially and year over year, with carbon steel margins under pressure and OEM demand running well below forecast. While tariffs and trade policies have provided some price support, demand has not recovered.

Tariff and Trade Policy Uncertainty: Trade policy uncertainty and readily available inventory have created a competitive market, making it difficult to increase selling prices to offset mill price increases. Changes in trade policy can create both opportunities and headwinds that are difficult to forecast.

Integration Risk: While Reliance's track record is strong, the continued pace of acquisitions creates ongoing integration risk. A significant failed acquisition could damage the company's reputation as an "acquirer of choice" and impair future deal flow.

Succession Uncertainty: While the transition to Lewis was smooth, the company's long-term success depends on continuing to develop leadership talent internally. Any disruption to this pipeline could impact performance.

Accounting and Regulatory Considerations

LIFO Inventory Accounting: Reliance uses LIFO (last-in, first-out) inventory accounting, which in periods of rising prices understates inventory values and overstates cost of goods sold on the balance sheet. This results in lower reported earnings during inflationary periods but provides tax benefits. Non-GAAP earnings that exclude LIFO adjustments provide better comparability across periods.

Trade Policy: Changes in tariffs on imported steel and aluminum directly impact pricing and demand patterns. The company has historically navigated trade policy changes successfully but cannot control this external variable.

XIII. The Quiet Compounder's Lessons

Reliance, Inc. doesn't command CNBC segments or generate viral Twitter threads. Its products don't inspire consumer devotion or TikTok unboxings. The company has never pivoted to blockchain, launched a streaming service, or announced a metaverse strategy.

What Reliance has done is compound value for shareholders over multiple decades through relentless execution of a straightforward strategy: buy well-run family businesses, let them operate autonomously, invest in processing capabilities, maintain balance sheet discipline, return capital to shareholders, and repeat.

Based on daily data since September 1994, the average daily return is 0.09%, while the average monthly return is 1.75%. The lowest end of day price was $1.61 USD on 1994-12-12. From that 1994 low to the all-time high of $342.24 on July 23, 2025, patient shareholders have seen their investment multiply more than 200-fold.

The lessons are simple but difficult to execute: stay disciplined through cycles, buy rather than build when you can, preserve cultures that work, and remember that compounding requires both returns and time.

In an investment landscape increasingly dominated by narratives of disruption and transformation, Reliance offers a different story—one of patient accumulation, operational excellence, and the remarkable power of doing the boring things right, repeatedly, for a very long time.

For investors seeking exposure to American industrial activity through a conservative, well-managed, dividend-growing vehicle with a proven acquisition playbook and disciplined capital allocation, Reliance merits serious consideration. As with any cyclical industrial business, position sizing should account for the inevitable volatility of economic cycles—but the company's 86-year track record suggests it will emerge from future downturns stronger than it entered, as it has from every previous one.

The quiet compounding machine rolls on.

XIV. End Market Diversification: The Hidden Moat

Understanding Reliance's Customer Base

One of the most underappreciated aspects of Reliance's business model is its extraordinary diversification across end markets. While many industrial companies tie their fortunes to a single sector—automotive, construction, or energy—Reliance has deliberately constructed a portfolio that cushions the blow when any single market weakens.

The Diversification Strategy in Practice

Demand in non-residential construction (including infrastructure), Reliance's largest end market, improved compared to the third quarter of 2023. Reliance continues to service new construction projects in diverse sectors, including public infrastructure, manufacturing, data centers and energy infrastructure.

This diversification extends beyond just end markets to encompass product types and geographies. As CEO Karla Lewis noted, "Our resilient business model, most notably the diversity of our products, end markets and geography, once again delivered strong performance in a more challenging pricing environment than we anticipated."

The end market dynamics reveal both opportunities and challenges: non-residential construction shows improvement, particularly in data centers and infrastructure projects, while manufacturing demand is mixed—strong in military, shipbuilding and rail sectors but weaker in consumer products.

The tolling business, which represents 4% of total sales, improved demand in the third quarter of 2024 compared to the prior year due to healthy demand in both the U.S. and Mexican automotive markets and ongoing investments to increase capacity.

Demand in the semiconductor market declined compared to both the fourth quarter and full year of 2023. However, while semiconductor industry demand remains subdued with continued excess inventories in the supply chain, it shows signs of stabilization in certain areas, and Reliance's long-term outlook for the semiconductor market remains positive.

The Data Center OpportunityThe data center construction boom has emerged as a particularly significant tailwind for Reliance's business. The company expects non-residential construction demand to remain at healthy levels, supported by new construction projects in diverse sectors including data centers, energy infrastructure, manufacturing and public infrastructure.

Non-residential construction—its largest segment—is buoyed by infrastructure projects in data centers and energy. As artificial intelligence drives unprecedented demand for computing infrastructure, the structural metal requirements for these massive facilities flow directly through service centers like Reliance.

2025 Performance: Market Share Gains Continue

The company's recent performance demonstrates the power of its diversified model. Reliance's tons sold in the third quarter of 2025 increased 6.2% compared to the prior-year quarter and remained flat compared to the second quarter of 2025, above management's expectations of down 1.0% to 3.0%. The company's growth in tons sold from the third quarter of 2024 far exceeded the industry-wide decline of 2.9% reported by the Metals Service Center Institute for the same comparative period, outperforming industry shipments by more than nine percentage points.

Non-GAAP earnings per diluted share of $4.43 in the second quarter of 2025 were slightly below management's expectations but, nonetheless up 17.5% from the first quarter 2025 as Reliance continues to gain market share, end market demand remains healthy, and policy conditions remain favorable for domestically sourced metals companies.

Record second-quarter tons sold once again significantly outperformed the industry due to the company's unparalleled scale, access to domestic metal, and breadth of processing capabilities. Demand across the broader manufacturing sectors Reliance serves increased compared to the second quarter of 2024. These diverse sectors include industrial machinery, military, consumer products, heavy equipment for agriculture and construction, shipbuilding and rail, among others.

The Domestic Sourcing Advantage

In an era of trade policy uncertainty and tariff volatility, Reliance's predominantly domestic supply chain provides a meaningful competitive advantage. Though the service center giant has operations in Mexico and Canada, as well as other countries, Reliance noted that it is about 95% domestically sourced, which will help insulate it from tariffs. In addition, those North American locations are typically buying domestically. "We're typically shipping within about a 150-mile radius, so we don't anticipate a significant impact, but we could see some disruptions in that part of our business that flows across the borders," Lewis explained.

As Lewis noted, "Our model of both buying and selling metal primarily in the U.S. market are positive for Reliance, and our employees, customers and suppliers."

XV. The Acquisition Machine: Past, Present, and Future

The Disciplined Approach to M&ASince its 1994 IPO, Reliance has completed 76 acquisitions that support its growth strategy, expanding product diversification and value-added processing capabilities. Since their 1994 IPO, they have completed 76 acquisitions that support their growth strategy, expanding product diversification and value-added processing capabilities.

The company's strong cash generation continues to support investments in value-added processing equipment, organic growth and accretive acquisitions, positioning Reliance for growth in all market environments.

The company's market share gains are directly attributable to this strategy. "Our third quarter results demonstrate how Reliance's scale, diversification, and high-performing management teams deliver strong financial performance and capture market share in a uniquely challenging market environment," said Karla Lewis. "Our tons sold were a third quarter record and outperformed the industry by approximately nine percentage points, increasing our U.S. market share to 17.1%, up from 14.5% in 2023, due to our smart, profitable growth strategy."

Lewis continued, "Trade policy uncertainty and readily available inventory are causing buyers to be hesitant, creating an extremely competitive market." Yet the company has succeeded by offsetting declining industry shipment trends by winning new business opportunities that also better leveraged operating expenses and meaningfully contributed to overall profitability.

What Makes Reliance an "Acquirer of Choice"

The metals service center industry remains fragmented, with thousands of family-owned businesses across North America representing potential acquisition targets. Reliance has built a reputation as the preferred buyer for these businesses, and the reasons are clear.

First, Reliance allows acquired companies to maintain their identities and operational autonomy. Family owners who spent decades building their businesses don't want to see their company names erased and their employees absorbed into a faceless corporate structure. Second, Reliance retains management. The entrepreneurs who built these businesses typically stay on to run them, now with the backing of Reliance's capital and resources. Third, Reliance has demonstrated patience. It doesn't force rapid integration or demand immediate synergies. This approach has created a virtuous cycle: successful acquisitions enhance Reliance's reputation, which generates more deal flow, which enables more successful acquisitions.

XVI. Capital Allocation Philosophy: The Shareholder Returns Engine### The Four Pillars of Capital Deployment

Reliance's capital allocation framework rests on four pillars, executed with remarkable consistency: capital expenditures, acquisitions, dividends, and share repurchases.

Reliance, Inc. (RS) has increased its dividends for 15 consecutive years—a positive sign of the company's financial stability and its ability to pay consistent dividends in the future.

Reliance, Inc.'s quarterly dividend per share was $1.20 as of December 5, 2025. Reliance has an annual dividend of $4.80 per share, with a yield of 1.71%.

Reliance, Inc. (RS) has a moderate payout ratio of 34.66%, which may indicate a balance between reinvesting earnings and rewarding shareholders with dividends, seen as sustainable for future growth and reasonable dividend yield.

The Shareholder Return Framework in Action

In 2025, Reliance has continued its balanced approach to shareholder returns. On July 22, 2025, the Board of Directors declared a quarterly cash dividend of $1.20 per share of common stock, payable on August 29, 2025 to stockholders of record as of August 15, 2025. Reliance repurchased 301,279 shares of its common stock in the second quarter of 2025 at an average price of $265.17 per share, for a total of $79.9 million.

As of June 30, 2025, $1.02 billion remained available under the Company's share repurchase program that was replenished to $1.5 billion on October 22, 2024.

Balance Sheet Strength

As of September 30, 2025, Reliance's cash and cash equivalents totaled $261.2 million with total debt outstanding of $1.39 billion, including $238.0 million of outstanding borrowings under the Company's $1.5 billion revolving credit facility. Reliance generated cash flow from operations of $261.8 million in the third quarter of 2025.

Inherent in the Company's business model, Reliance generates strong cash flow from operations throughout market cycles that it redeploys to execute opportunistic capital allocation strategies. As previously announced, on August 14, 2025, Reliance borrowed $400.0 million under an unsecured term loan agreement maturing in August 2028 and used the proceeds to repay $400.0 million of unsecured senior notes due August 15, 2025.

XVII. Risks and Challenges: What Could Go Wrong

Cyclicality: The Inescapable Reality

No analysis of Reliance would be complete without acknowledging the cyclical nature of its business. Metals demand rises and falls with economic activity, construction spending, and manufacturing output. The company cannot escape these cycles—but it has demonstrated an ability to manage through them.

"Trade policy uncertainty and readily available inventory are causing buyers to be hesitant, creating an extremely competitive market."

Pricing Pressure

The metals industry has faced significant pricing headwinds in recent years. While Reliance has maintained its gross profit margins within the target range through disciplined execution, sustained pricing weakness could eventually compress profitability.

Integration Risk

Each acquisition carries execution risk. While Reliance's track record is strong, a significant failed integration could damage its reputation as an acquirer of choice and impair future deal flow. The company's decentralized model reduces this risk but doesn't eliminate it.

Competition

The Ryerson-Olympic merger creates a more formidable competitor. While Reliance retains significant scale advantages, increased competition could pressure margins in certain markets or product categories.

Macroeconomic Sensitivity

As an industrial company, Reliance's performance correlates with broader economic conditions. A significant recession would likely impact demand across most of its end markets simultaneously, testing even the most diversified business model.

XVIII. Investment Thesis Summary

The Case for Reliance

Reliance represents a compelling opportunity for investors seeking exposure to American industrial activity through a disciplined, well-managed company with a proven track record of compounding shareholder value.

Durable Competitive Advantages: The company's scale, decentralized model, value-added processing capabilities, and reputation as an acquirer of choice create sustainable competitive moats that would be difficult for competitors to replicate.

Proven Capital Allocation: Management has demonstrated disciplined capital allocation across decades and economic cycles, consistently deploying cash toward high-return opportunities while returning excess capital to shareholders.

Counter-Cyclical Capability: The conservative balance sheet provides firepower for opportunistic acquisitions during industry downturns—precisely when the best deals become available.

Structural Tailwinds: Data center construction, infrastructure spending, and reshoring trends provide multi-year demand tailwinds that should benefit domestically-focused metals distributors.

Shareholder-Friendly Practices: Fifteen consecutive years of dividend increases, combined with aggressive share repurchases, demonstrate commitment to returning value to shareholders.

Key Monitoring Metrics

For investors who establish positions in Reliance, the following metrics warrant ongoing attention:

- Gross Profit Margin – Should remain within the 29-31% target range through cycles

- Tons Sold vs. Industry – Continued market share gains validate competitive positioning

- Acquisition Cadence – Sustained deal flow indicates robust M&A pipeline

- Value-Added Processing Mix – Increasing percentage indicates margin expansion potential

- Balance Sheet Leverage – Low net debt/EBITDA preserves financial flexibility

XIX. Conclusion: The Unsexy Art of Compounding

Reliance, Inc. will never grace the cover of a technology magazine or generate breathless coverage on financial television. Its products are not aspirational. Its business model cannot be pitched in a single catchy phrase. Its competitive advantages require paragraphs, not soundbites, to explain.

And yet, for 86 years, this company has done something remarkable: it has compounded value for shareholders through Depression, war, inflation, recession, and technological revolution. It has done so by mastering the unglamorous fundamentals of industrial distribution: holding the right inventory in the right locations, processing metal to customer specifications, delivering orders on time, integrating acquisitions successfully, and maintaining balance sheet discipline through cycles.

The company that Thomas Neilan founded with a few tons of rebar accepted as debt payment now operates 320 locations across 41 states and 10 countries, serving 125,000 customers with 100,000 products. From that Depression-era warehouse in Vernon, California, Reliance has become the largest metals service center in North America—and it achieved this position not through a single transformational moment but through eight decades of patient, disciplined execution.

For investors willing to look beyond the hype of high-growth technology stocks and meme-driven speculation, Reliance offers a different proposition: the power of compounding returns in a business that serves essential industrial needs, managed by operators who have demonstrated disciplined stewardship across decades. The company has survived every economic cycle since 1939 and emerged stronger each time.

The quiet compounding machine continues its work—one small order, one acquisition, one satisfied customer at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube