Extreme Networks: The Scrappy Underdog of Enterprise Networking

I. Introduction & Episode Roadmap

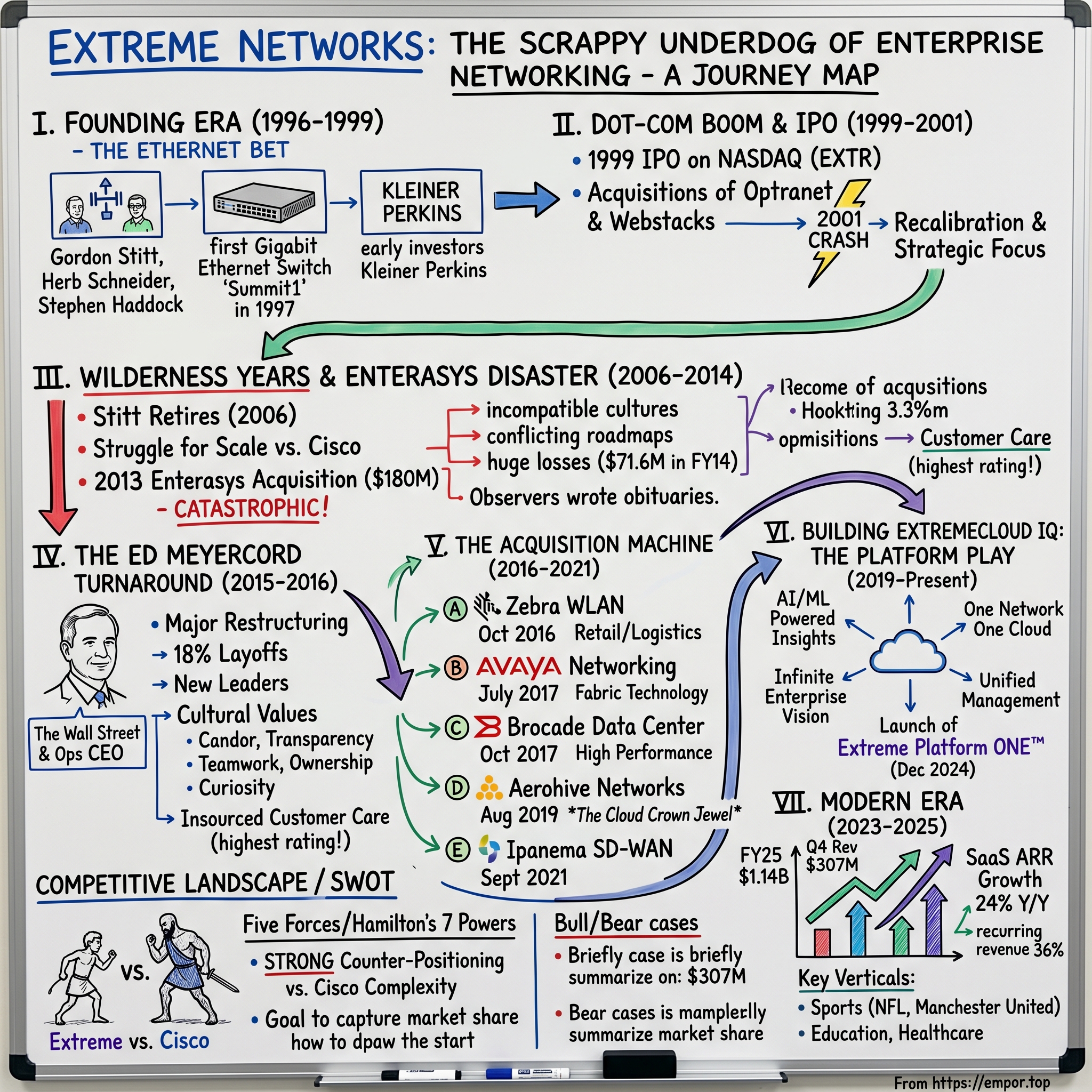

The year was 2014, and Extreme Networks was bleeding out. Just twelve months after completing what was supposed to be a transformative acquisition of Enterasys Networks, the combined company had hemorrhaged $71.6 million. The combined companies went on to lose $57.3 million in fiscal 2015, which ended June 30, and $71.6 million in fiscal 2014. The integration was a disaster—two incompatible corporate cultures, conflicting technology roadmaps, and a sales force that couldn't seem to get on the same page. Industry observers began writing the company's obituary.

Today, Extreme Networks (NASDAQ: EXTR) is an American technology company headquartered in Morrisville, North Carolina, with over 2,800 employees worldwide and annual revenue of $1.14 billion for its fiscal year 2025 ending June 30. The company that nearly died now powers the Wi-Fi networks at the Super Bowl, Manchester United's Old Trafford Stadium, and Taylor Swift concerts. It has been named a Gartner Magic Quadrant Leader for six consecutive years and positions itself as the third-largest enterprise networking vendor in the world.

How did this happen? The answer involves one of the most aggressive acquisition sprees in tech history, a turnaround CEO who understood that corporate culture eats strategy for breakfast, and a bet on cloud-managed networking that caught giants like Cisco flat-footed.

Through a series of historical and contemporary merger and acquisition activity, Extreme Networks claims an industry lineage that includes, at a minimum, the networking-focused elements of the following companies: Digital, Chantry, Siemens, Cabletron, Enterasys, AirDefense, Symbol, Motorola, Zebra, Wellfleet, SynOptics, Bay Networks, Nortel Networks, Avaya, Vistapointe, StackStorm, Foundry Networks, Brocade, and Aerohive Networks.

This is a story about strategic patience, execution under fire, and the art of turning a collection of discarded corporate networking assets into a coherent challenger brand. It's the story of a company that asked a fundamental question: What if enterprise networking could actually be simple?

For long-term investors, Extreme Networks presents a fascinating case study in several dimensions: the economics of serial M&A in enterprise technology, the transition from hardware to cloud-based subscription revenue, and the competitive dynamics of attacking an entrenched market leader. The key metrics to watch going forward are SaaS ARR (Annual Recurring Revenue), which reflects the company's transition to recurring software revenue, and market share gains versus Cisco, which determine whether Extreme can translate product innovation into durable competitive position.

II. Founding Era: The Ethernet Bet (1996–1999)

Picture Silicon Valley in 1996: Netscape had just gone public a year earlier, signaling the commercial dawn of the internet age. The World Wide Web was transitioning from curiosity to necessity, and every enterprise in America was scrambling to connect its computers to something faster than dial-up.

Extreme Networks was established by co-founders Gordon Stitt, Herb Schneider, and Stephen Haddock in 1996 in California, United States, with its first offices located in Cupertino, which later moved to Santa Clara, and later to San Jose.

The founding team brought deep networking expertise. Extreme Networks was founded in 1996 in Silicon Valley, California, by Gordon Stitt, Herb Schneider, and Stephen Haddock, who brought extensive experience in networking from prior ventures at companies like Xylan and Cisco Systems. These weren't starry-eyed first-time entrepreneurs—they were battle-tested engineers who had watched the networking industry evolve from its earliest days and saw an opportunity that others were missing.

Their bet was on Ethernet. While incumbents were still pushing proprietary protocols and expensive Token Ring solutions, the Extreme founders believed that Ethernet—cheap, standardized, and surprisingly scalable—would become the universal language of enterprise networking. It was a contrarian view at the time. Many enterprise IT managers considered Ethernet suitable only for connecting desktop PCs in small offices, not for mission-critical backbone infrastructure.

Early investors included Norwest Venture Partners, AVI Capital Management, Trinity Ventures, and Kleiner Perkins Caufield & Byers. The presence of Kleiner Perkins on the cap table was notable—John Doerr's firm was then at the height of its influence, backing companies that would define the internet era. Their investment in Extreme Networks signaled that sophisticated investors believed the networking infrastructure opportunity was far from saturated, despite Cisco's growing dominance.

In 1997, the company introduced the Summit1, recognized as one of the industry's first Gigabit Ethernet switches, equipped with a 17.5 Gbps backplane and eight full-duplex Gigabit Ethernet ports for wire-speed switching and routing at a price of $25,000. This was a genuine innovation. This product marked a significant breakthrough by enabling scalable, high-performance campus networking, addressing the growing demand for faster data transfer in enterprise environments. The Summit1's design supported modular expansion, laying the foundation for distributed network architectures.

Complementing the hardware, Extreme Networks developed ExtremeWare, a standards-based operating system tailored for modular switch management across its product line. The combination of cutting-edge hardware and purpose-built software established a pattern that would define the company's approach for decades: differentiation through integration.

The journey began in 1996, a pivotal year for the burgeoning internet era. It was founded by Gordon Stitt, Herb Schneider, and Stephen Haddock, who saw a significant opportunity within the rapidly expanding networking hardware sector. Gordon Stitt took the helm as CEO, a role he would hold for a full decade. Gordon Stitt was a co-founder and served as chief executive officer until August 2006, when he retired and became chairman of the board of directors.

The timing couldn't have been better. Enterprises were pouring capital into networking infrastructure, and the dot-com boom was about to provide rocket fuel for any company selling picks and shovels to the internet gold rush.

For investors, the founding era established Extreme's core DNA: engineering-led innovation, a willingness to bet against incumbents, and a focus on high-performance solutions for demanding enterprise environments. These traits would prove both a blessing and a curse in the years to come.

III. The Dot-Com Boom & IPO (1999–2001)

By 1999, the conditions for a networking IPO couldn't have been more favorable. Cisco had just become one of the most valuable companies on Earth. Investors were throwing money at anything with "network" in its name. And Extreme Networks had real products, real revenue, and real customers.

The initial public offering in April 1999 was listed on the NASDAQ stock exchange as ticker "EXTR."

The decision to become a publicly traded company was a pivotal moment in Extreme Networks' history. By choosing to list its common stock on Nasdaq under the ticker EXTR, the company sought access to capital markets to fuel its ambitious growth plans. The IPO was met with considerable attention from investors—a reflection of the tech sector's high expectations during the era.

Extreme Networks was co-founded in 1996 by Gordon Stitt, who served as its first president and CEO from inception through 2006, overseeing the company's initial product development, market entry in Ethernet switching, and its initial public offering on April 9, 1999, which fueled early expansion amid the dot-com boom.

The capital raised enabled aggressive expansion. Under Stitt's leadership, Extreme Networks established itself as a key player in high-performance networking solutions, navigating the challenges of rapid technological evolution and competitive pressures in the late 1990s and early 2000s.

With cash in the bank and stock as currency, Extreme made its first acquisitions. The company acquired Optranet in February 2001 and Webstacks in March 2001 for approximately $73 million and $74 million respectively. These deals were designed to expand the company's product portfolio and technological capabilities during what seemed like an era of limitless growth.

Then came the crash.

The dot-com bust of 2000-2001 was particularly brutal for networking equipment vendors. Enterprise customers who had been buying frantically suddenly stopped ordering entirely. IT budgets were slashed. Companies that had seemed like sure things filed for bankruptcy.

During the initial years on the public market, Extreme Networks was regarded as a potential powerhouse in the networking segment. Its early stock performance was influenced by several factors: Market Sentiment: The excitement around networking technologies and the overall buoyancy of tech market.

Extreme survived the crash, but the post-bubble period required painful recalibration. The company implemented measures to stabilize operations, streamline product offerings, and focus on core technological innovations. This period of recalibration was vital, leading to a more sustainable business model—but at significant cost in terms of growth and momentum.

The IPO era taught Extreme a lesson that would become central to its later strategy: capital markets can be fickle, and sustainable competitive advantage comes from solving real customer problems, not from financial engineering or market timing. It was a lesson the company would need to remember during its darkest hours.

IV. The Wilderness Years & Enterasys Disaster (2006–2014)

Gordon Stitt's retirement in August 2006 marked the beginning of Extreme's most challenging era. Following his retirement announcement in 2006, Stitt transitioned to chairman before later pursuing entrepreneurial ventures in networking and optics technologies. The company struggled with leadership turnover and strategic drift as the networking industry entered a period of intense consolidation.

The fundamental problem was scale. By the early 2010s, the enterprise networking market had evolved into a brutal arena where Cisco controlled approximately 60% market share. Smaller players were getting squeezed, unable to match Cisco's R&D spending, sales force reach, or brand recognition. Extreme needed to get bigger—fast.

On September 12, 2013, Extreme Networks announced it would acquire Enterasys Networks for about $180 million.

Enterasys had its own storied history. Enterasys Networks, Inc. was an American networking company. Enterasys products included networking equipment ranging from routers, switches, and IEEE 802.11 wireless access points and controllers. The company formed in March 2000 as a spin-off of Cabletron Systems. In addition to networking hardware such as switches, routers and wireless products, the company sold software for managing and securing networks such as intrusion prevention systems, network access control and security information management.

For Extreme, the deal makes all the sense in the world. First, for a price of $180 million, I'm not sure why someone else didn't swoop in and buy Enterasys. The company does somewhere in the range of $300 million per year, so the purchase price doesn't even equal its annual revenue.

The acquisition doubles Extreme's share in a customer base with almost no overlap. In fact, I'm not sure I know of any joint Enterasys/Extreme customers, so it's not likely to cause much churn if managed properly. Enterasys has long been known as a vendor with great security products, whereas Extreme had none, so that product line becomes available to its customer base.

The rationale seemed sound. But execution was catastrophic.

The company was struggling to stay afloat a few years ago after the poorly executed integration of fellow networking vendor Enterasys in 2013.

But it's not expecting a repeat of what happened when Extreme acquired Enterasys Networks in 2013, which Meyercord described as more of a merger and one where the companies' cultures were very different. That acquisition came with a lot of integration issues and technology debates about the R&D roadmap when that occurred, according to Meyercord.

It took eight months to effectively merge Enterasys into the company and the transaction and integration costs thus far are about $25.7 million. That doesn't count some $16.7 million in intangibles and a restructuring charge of $500,000.

A pro forma analysis, which combines the companies fiscal results from last year as if they were one company for comparison purposes, shows a decline in sales from $634 million to $619 million and a net loss of $71 million for all of fiscal 2014 (74 cents a share). That's lower than the $38 million loss both companies would have experienced together in fiscal 2013.

The combined company was losing money at an accelerating rate. The workforce reduction was in response to increasing losses since Extreme acquired Enterasys for $180 million in November 2013. The combined companies went on to lose $57.3 million in fiscal 2015, which ended June 30, and $71.6 million in fiscal 2014.

By early 2015, Extreme Networks was a company in crisis. Two incompatible product lines. Two different operating systems. Two competing roadmaps. And a management team that seemed unable to make the hard decisions required to rationalize the combined entity. The board faced a stark choice: find someone who could fix this mess, or watch the company die.

For investors contemplating any "rollup" strategy in technology markets, the Enterasys disaster offers a sobering lesson: integration risk in enterprise technology is profound. Customers make multi-year commitments to specific platforms, and their willingness to accept disruption is limited. Product rationalization decisions are politically charged internally and strategically consequential externally. Getting M&A wrong can destroy more value than staying subscale.

V. The Ed Meyercord Turnaround (2015–2016)

In moments of corporate crisis, boards often reach for the safe choice—a polished executive from a larger competitor, someone with impeccable credentials and a proven playbook. The Extreme Networks board took a different path.

Mr. Meyercord has served as President and Chief Executive Officer of Extreme since April 2015. He joined our Board of Directors as an independent director in October 2009 and served as Chairman from March 2011 through August 2015.

Meyercord, who was with a telecom services provider and had been on Extreme Networks' board since 2009, was asked by the company's board to become CEO. What followed was a major revamping of operations as Extreme Networks laid off 300 of its 1,500 employees.

Ed Meyercord's background was unconventional for a tech CEO. Ed Meyercord grew up in New York City with a fascination for Wall Street – but beneath the finance-driven ambition was a deeper instinct: the desire to lead. Today, as CEO of Extreme Networks, Ed has spent over 15 years transforming the company into a global powerhouse, delivering the networks behind everything from the Burj Khalifa to Old Trafford, Taylor Swift concerts to Samsung's operations.

Previously, Meyercord served as CEO, President and Director of both Cavalier Telephone & TV, a privately held voice, video and data services company with an extensive fiber network; and Talk America, Inc., a publicly traded company that provided phone and internet services to consumers and small businesses throughout the U.S. Meyercord was also a Vice President in the investment banking division of Salomon Brothers (now Citigroup).

Prior to assuming an operating role at Extreme, Mr. Meyercord was Chief Executive Officer and Director at Critical Alert Systems, LLC, a software-driven, healthcare information technology company that he co-founded in July of 2010.

His Wall Street background meant he understood the language of capital markets, but his operating experience at telecom companies gave him insight into enterprise customer psychology. And his years on the Extreme board meant he already understood the company's strengths, weaknesses, and cultural dynamics.

Ed Meyercord, Extreme Networks' new CEO, got down to business Thursday morning, giving investors and analysts details about a restructuring plan that will involve layoffs of 285, about 18 percent of the company.

The layoffs are expected to cost Extreme between $13 million and $15 million in employee-related termination benefits, but save the firm some $40 million in operating costs. Extreme posted a net loss of $15.7 million in the fourth quarter of fiscal 2015, slightly lower than the same quarter last year, even with revenue ($116.3 million) down 5 percent.

In announcing the layoffs, the company estimated that the 60 percent of the savings would come from a sales force reduction, 20 percent out of research and development, 10 percent out of manufacturing operations and 10 percent out of administration.

The company also named a new chief marketing officer and chief revenue officer, among other executive spots, in an effort to restructure and align for future success.

But cost-cutting was only half the strategy. Meyercord understood that Extreme couldn't shrink its way to greatness. The real challenge was defining a forward strategy that could differentiate the company against Cisco while building on the assets acquired from Enterasys.

"We hired from within" and "set a very forward strategy," Meyercord said. The product and leadership teams worked together to focus on what best served the needs of customers and then executed by developing these solutions.

The cultural transformation proved equally challenging. "When there's change, there's going to be conflict, because people have to change, and inherently as humans, people don't want to change."

Meyercord's approach to culture was deliberate. At Extreme, five core values define employees and drive culture: candor, transparency, teamwork, ownership, and curiosity. These weren't just slogans; they became filters for hiring decisions and performance evaluations.

Our customer care programs are the highest rated in the industry. Every team member is responsible for customer success. We have 100% insourced support with the industry's highest first call resolution rate of 94%.

The insourced support model was a key differentiator. While competitors outsourced their customer service to reduce costs, Extreme bet that enterprise customers would pay a premium for responsive, knowledgeable support. The bet paid off in customer retention and Net Promoter Scores.

Regarding hiring, Meyercord said he looks for team players who are candid, honest, curious, take ownership and are accountable. So far, he said, the turnaround "has absolutely been a success."

By mid-2016, the restructuring was complete. Extreme was profitable at the operating level, had stabilized its customer base, and had established a clear strategic direction. But Meyercord understood that the real opportunity lay not in organic growth—which would be slow and grinding against well-funded competitors—but in strategic acquisitions that could rapidly scale the business. The Enterasys experience had taught him what not to do. Now he was ready to show what disciplined M&A could achieve.

VI. The Acquisition Machine (2016–2021)

The eighteen months between October 2016 and March 2018 represent one of the most aggressive acquisition sprees in enterprise technology history. Extreme Networks, a company with approximately $500 million in annual revenue, would consume four separate businesses and emerge with the scale to credibly compete against Cisco.

A. Zebra Technologies WLAN (October 2016)

On October 31, 2016, Extreme Networks announced that it completed the acquisition of Zebra Technologies' wireless LAN business for about $55 million.

Walmart, TJ Max, Marriott, Hilton, Coca Cola, FedEx and UPS are just some of the brands that Extreme Networks will pick up as part of its acquisition of Zebra Technologies' WLAN business. The $55 million acquisition will create new growth opportunities in two vertical markets – retail and transportation/logistics – and expands its reach further into the hospitality and manufacturing verticals.

The Zebra deal was deliberately designed to be low-risk while Extreme developed its integration capabilities. That's not expected this time around.—a direct reference to learning from the Enterasys debacle.

In October 2016, the company closed its acquisition of the wireless LAN business from Zebra Technology Corporation, which is expected to generate over $115 million in annualized revenue.

B. Avaya Networking (March–July 2017)

On March 7, 2017, Extreme Networks announced its intention to acquire Avaya's networking business in a transaction valued at $100 million. The acquisition officially closed on July 17, 2017. As part of this transaction, Extreme acquired customers, personnel, and technology assets from Avaya.

Extreme has publicly stated that it expects to "generate over $200 million in additional annualized revenue" from the acquired networking assets from Avaya.

"This strategic acquisition will be another milestone in the execution of Extreme's growth strategy and clearly establishes Extreme as the third largest competitor in our enterprise markets and the only company in the world exclusively focused on delivering the highest quality end-to-end, wired and wireless enterprise IP networking."

The Avaya deal brought unique fabric technology—a software-defined networking architecture that provided automation, simplicity, and security to enterprise infrastructure. Over the last several years, Avaya has been working on a fabric technology that is truly the heart and soul of its broad hardware portfolio and we're looking forward to expanding that under the Extreme name. This technology is unique to the industry and provides important differentiators that a variety of enterprise organizations need.

C. Brocade Data Center Business (October 2017)

Just weeks after announcing the Avaya deal, Extreme revealed an even more ambitious acquisition.

SAN JOSE, Calif. and SINGAPORE, March 29, 2017 /PRNewswire/ -- Extreme Networks, Inc. (NASDAQ: EXTR) and Broadcom Limited (NASDAQ: AVGO) today jointly announced that they have entered into an agreement for Extreme to acquire Brocade Communications Systems, Inc.'s data center switching, routing, and analytics business from Broadcom following Broadcom's acquisition of Brocade. Brocade's data center networking business will be sold to Extreme for $55 million in cash, consisting of $35 million at closing and $20 million in deferred payments, as well as additional potential performance based payments to Broadcom, to be paid over a five-year term.

Extreme expects the acquisition to be accretive to cash flow and earnings for its fiscal year 2018 and expects to generate over $230 million in annualized revenue from the acquired assets.

Oct. 30, 2017 /PRNewswire/ -- Extreme Networks, Inc. (NASDAQ: EXTR) today announced that it has completed its acquisition of Brocade Communications Systems, Inc.'s (NASDAQ: BRCD) data center switching, routing and analytics business. Brocade's portfolio provides Extreme with an industry leading data center solution used by enterprises and service providers, supports the company's growth strategy to lead the networking industry from the data center to the wireless edge, and secures Extreme's position as a top player in the enterprise networking market.

"Through a series of synergistic acquisitions, Extreme is now a top player in the enterprise networking industry and expects to generate over $1 billion in annual revenues. Today's announcement is not only a significant milestone for our growth strategy, but it also allows us to assist more customers around the globe with end-to-end software-driven solutions to drive their digital transformation initiatives."

With the close of this acquisition, Extreme acquires customer relationships, personnel and technology assets from Brocade including the SLX, VDX, MLX, CES, CER, Workflow Composer, Automation Suites, and certain other data center related products. The acquisition enhances Extreme's data center solutions used by enterprises and service providers across industries such as education, hospitality, healthcare, retail, transportation and logistics, manufacturing and government.

The execution wasn't perfect. Meyercord acknowledged there were challenges in integrating the Avaya and Brocade businesses simultaneously. The company also began an acquisition strategy by taking out a large line of credit. Over the course of one year, it bought Brocade's data center business, Avaya's networking unit and Zebra's WLAN business.

D. Aerohive Networks (August 2019) – The Cloud Transformation

The crown jewel of Extreme's acquisition strategy came two years later, with a deal that would fundamentally transform the company's competitive positioning.

Extreme Networks, Inc. (Nasdaq: EXTR), a software-driven networking company, and Aerohive Networks (NYSE: HIVE), a pioneer in cloud-managed networking, today announced they have entered into a definitive agreement under which Extreme will acquire all of the outstanding shares of common stock of Aerohive at a price of $4.45 per share in cash, representing an aggregate purchase price of approximately $272 million.

Aerohive Networks, Inc. was an American multinational computer networking equipment company headquartered in Milpitas, California, with 17 additional offices worldwide. The company was founded in 2006 and provided wireless networking to medium-sized and larger businesses. In 2012, Aerohive was listed on The Wall Street Journal's list of "Top 50 Start-Ups." The company raised around $105 million in venture capital funding before undergoing an IPO in March 2014.

On June 26, 2019, Extreme Networks announced its intent to acquire Aerohive for a purchase price of approximately $272 million. The acquisition closed on August 9, 2019.

The strategic rationale was compelling. Extreme's lack of a cloud option made it a weaker competitor against Cisco and Aruba. Extreme had on-premises edge-to-core infrastructure but didn't have the cloud technology needed to compete with Meraki and Aruba's cloud offerings.

The acquisition of Aerohive adds critical cloud management and edge capabilities to Extreme's portfolio of end-to-end, edge to cloud software-driven networking solutions. It expands Extreme's technology leadership in Wi-Fi and NAC, adding cloud-managed Wi-Fi and NAC solutions to complement its on-premises Wi-Fi and NAC technology, driving Extreme deeper into key verticals and presenting numerous opportunities for cross-sell and up-sell within the combined portfolios. It also brings new SD-WAN capabilities to Extreme's solutions mix. Now, customers and partners of Extreme and Aerohive will be able to mix and match a broader array of software, hardware, and services Elements to create networks that support their unique needs and that may be managed and automated from end-to-end – from the enterprise edge to the cloud – to advance their digital transformation efforts.

"Closing our acquisition of Aerohive in just 45 days from initial announcement eliminates many execution risks and better positions us to transition customers smoothly." Chris DePuy, Founder and Technology Analyst, 650 Group said "The acquisition of Aerohive and its technology complements Extreme's portfolio of edge to cloud solutions, enhancing its enterprise WLAN offerings with leading cloud management capabilities as the industry continues making the transition to cloud-based networking products and solutions. Extreme also acquires other products and services in exciting new growth markets, such as Enhanced Network Access Control (ENAC), which includes solutions that allow customers to better manage IoT and BYOD scenarios. By combing Aerohive into Extreme, Extreme will be one of only a handful of vendors that can offer a full campus solution."

At a time when many of Extreme's customers and partners are turning toward as-a-service/subscription models to reduce costs and gain efficiencies, Aerohive will expand Extreme's mix of revenues to approximately 30% from subscription recurring revenue. With Aerohive, Extreme will offer customers and partners more choices for cloud and on-premises wired and wireless technology, and an industry-leading solution for cloud-based network management – all from a single vendor and backed by its award-winning, insourced services and support team. Post-acquisition, customers and partners of Extreme and Aerohive will be able to mix and match a broader array of software, hardware, and services Elements to create networks that support their unique needs and that may be managed and automated from end-to-end – from the enterprise edge to the cloud – to advance their digital transformation efforts.

E. Ipanema SD-WAN (September 2021)

On September 15, 2021, Extreme Networks acquired Infovista's Ipanema SD-WAN business. This completed Extreme's five major acquisitions in six years, giving the company capabilities across wireless, wired, data center, cloud management, and software-defined WAN.

The Integration Challenge

The scale of integration was daunting. Because Extreme had been on a buying spree, even end-to-end Extreme customers might have very different legacy hardware from Zebra, Avaya, Brocade, Aerohive, and Ipanema.

The rollout of Extreme Platform ONE is the culmination of many acquisitions and years of work. Today's Extreme is a rollup of many network vendors, including Enterasys, Brocade, Avaya Networking and Motorola/Zebra. The purchase of Aerohive brought the company the cloud back end that is being leveraged in the current platform launch. Along the way, the company rationalized its product set and implemented "Universal Hardware," which lets customers choose between different operating systems.

The strategy, as one analyst put it, was "Extreme-ifying"—taking disparate acquired assets and creating a unified customer experience with increased interoperability. This was the opposite of what many criticized acquirers (including Cisco) for doing: buying companies and leaving them as separate silos.

For investors, the acquisition spree demonstrates both the opportunity and risk of serial M&A in enterprise technology. The opportunity: rapid scale creation in a market where scale matters for R&D leverage, brand recognition, and sales force reach. The risk: integration complexity, customer confusion, and the possibility that the combined entity never achieves the synergies promised. Extreme's experience suggests that integration discipline—learning from each deal and applying those lessons to the next—is the critical success factor.

VII. Building ExtremeCloud IQ: The Platform Play (2019–Present)

If the acquisitions gave Extreme scale, the platform strategy gave it differentiation. The Aerohive acquisition provided the technological foundation, but the vision of what to build on that foundation was uniquely Extreme's.

ExtremeCloud IQ uses innovative ML technologies to analyze and interpret millions of network and user data points, from the edge to the data center, to power actionable business and IT insights. This innovative platform streamlines operations by delivering new levels of network automation and intelligence.

ExtremeCloud IQ, a key enabler of Extreme's cloud networking architecture, provides unified management and insights for an end-to-end view of the Extreme device and SD-WAN portfolio. Extreme's One Network One Cloud approach simplifies secure connectivity across branch, campus, and data center environments by leveraging artificial intelligence for IT operations (AIOps) and Universal ZTNA for network and application access control.

The platform's capabilities extend across the entire network lifecycle:

ExtremeCloud IQ provides unified management driven by Machine Learning (ML). It features intuitive configuration workflows, realtime and historical monitoring, comprehensive troubleshooting, and integrated network applications. ExtremeCloud IQ is an industry-leading approach to cloud-driven networking, designed to take full advantage of Extreme's end-to- end networking solutions. It delivers unified, full-stack management of access points, switches, and SD-WAN.

The tiered licensing model reflects Extreme's understanding that different customers have different needs:

The ExtremeCloud IQ CoPilot license tier is an add-on to the Pilot license tier. It includes all the capabilities of the ExtremeCloud Pilot and Navigator license tiers. CoPilot serves as more than a centralized point of management. It is a trusted digital advisor for your Extreme cloud-managed Wi-Fi networks that proactively reduces risk and provides the fastest time to the best experience. This includes advanced anomaly detection and capabilities to ensure the user experience of wireless and wired devices.

The transformation from hardware company to cloud platform company was substantial. As Meyercord noted: "Today, we've developed the capability to manage networks – from the wireless and IoT edge to the data center core – via the cloud, simplifying the complexity of managing and deploying distributed networks. The enterprise was already becoming more distributed, but the pandemic forced us to embrace huge changes overnight."

Extreme Networks is driving towards its 'Infinite Enterprise' vision, focusing on delivering connectivity that is distributed, high-quality, secure, and easily manageable. This strategy aims to create a seamless networking experience across all environments.

In December 2024, Extreme unveiled the next evolution of its platform strategy: Extreme Networks, Inc. (NASDAQ: EXTR) today unveiled Extreme Platform ONE™, a groundbreaking technology platform that reduces the complexity for enterprises by seamlessly integrating networking, security and AI solutions. The platform's AI-powered automation includes conversational, interactive and autonomous AI agents—to assist, advise and accelerate the productivity of networking, security and business teams—effectively reducing the time to complete complex tasks from hours to minutes.

Aiming to address the needs of a world in which the vast majority of business leaders see networks as more complicated than just two years ago, Extreme Networks has launched new capabilities in its Platform One offering, becoming, it claims, the first provider of its kind to integrate conversational, multimodal and agentic artificial intelligence (AI) into one enterprise networking platform. First announced in December 2024, Platform One is now in limited availability globally, and at its Extreme Connect 2025 conference in Paris, the company revealed the platform is now in use, with over 130 companies around the world developing use cases showing how companies can unlock new levels of visibility, control and efficiency across networks, streamlining operations and delivering insights that allow teams to act faster.

Extreme is now the first and only networking vendor to deliver conversational, multimodal, and agentic AI fully integrated into the networking experience with Extreme Platform ONE™, which was made generally available last month.

"For example, in our internal benchmarking, we've reduced troubleshooting and remediation times by up to 95 percent."

For investors, the platform strategy is critical because it drives the transition from one-time hardware sales to recurring subscription revenue. SaaS businesses typically trade at higher multiples than hardware businesses due to revenue predictability and customer lock-in. Extreme's success in this transition—measured by SaaS ARR growth—will be a key determinant of long-term shareholder returns.

VIII. Modern Era: Market Position & Financial Performance (2023–2025)

The fruits of a decade of strategic transformation are now visible in Extreme's financial results.

Q4 revenue grew 20 percent year-over-year and SaaS ARR by 24 percent, year-over-year. "We closed the fourth quarter with significant momentum, driven by sharp execution and growing demand for our solutions and services," said Ed Meyercord, President and CEO of Extreme.

The networking solutions provider reported its fifth consecutive quarter of revenue growth, with Q4 revenue reaching $307 million and full-year revenue totaling $1.14 billion.

The company reported Non-GAAP earnings per share of $0.25, up from $0.21 in the previous quarter. Recurring revenue reached $109 million, increasing 8% both sequentially and year-over-year. Free cash flow showed remarkable improvement, reaching $75.3 million in Q4, a significant increase from $24.2 million in Q3.

Recurring revenue represented 36% of total revenue in FY25, highlighting the company's progress in building a stable revenue foundation. Extreme Networks significantly strengthened its financial position during FY25.

The company ended the year with $231.7 million in cash and cash equivalents, up from $156.7 million at the end of FY24. More importantly, Extreme Networks shifted from a net debt position of $33.3 million in Q4 2024 to a net cash position of $51.7 million in Q4 2025. For the full year, Extreme Networks generated $152 million in operating cash flow and $127.3 million in free cash flow, compared to $55.5 million and $37.4 million respectively in FY24.

The post-pandemic recovery has been notable: "We're pleased to see strengthening global demand and to have moved past the historic challenges of the multi-year supply chain constraints. We successfully completed our initiatives to eliminate channel and inventory headwinds."

"As the second largest cloud networking services provider, and a continued strong leadership position in the Gartner MQ, Extreme is poised to benefit from the industry disruption from larger players in the enterprise market. Key competitors are either distracted by portfolio rationalization and integration, or shifting business focus away from networking, just as we are gaining share."

Revenue Growth in-line With Previous Outlook With 29% Year-over-Year Growth in SaaS ARR—this FY24 result demonstrates the transition to cloud-managed networking is accelerating.

Geographically, the Americas region contributed 52% of FY25 revenue ($597 million), while EMEA accounted for 40% ($452 million) and APAC represented 8% ($92 million). This distribution shows Extreme Networks' global reach and potential for further expansion in the Asia-Pacific region. From an industry perspective, Government and Education sectors represented approximately 40% of the company's bookings, followed by Manufacturing, Healthcare, Hospitality & Venues, and Retail & Transportation at approximately 10% each.

Looking ahead, for the full fiscal year 2026, Extreme Networks forecasts revenue between $1,228 million and $1,238 million, representing year-over-year growth of approximately 7.7% to 8.6%.

Kevin Rhodes, Executive Vice President and Chief Financial Officer stated, "Fourth quarter results were driven by continuous sequential growth in revenue and prudent expense management leading to a strong cash flow quarter. Heading into the new fiscal year, our outlook is for a re-acceleration of overall revenue growth on a full-year basis, which we expect to translate to higher earnings and cash flow."

For investors, the key metrics to track are SaaS ARR growth (indicating success in the cloud transition) and gross margin trends (indicating pricing power and competitive positioning). Both metrics showed improvement in FY25, suggesting the strategic investments of the past decade are beginning to generate returns.

IX. Vertical Focus: Sports, Education & Healthcare

Extreme Networks' most visible deployments are in venues where network performance is mission-critical and public—a strategic choice that serves both practical and marketing purposes.

Networking vendor Extreme Networks announced today a multi-year deal making it "an official Wi-Fi partner" of the National Hockey League, as well as a deal to deploy a new Wi-Fi 6 network at Old Trafford, the home stadium for the Manchester United team.

"Our collaboration with Extreme Networks is an important step in our drive to enhance the fan experience at Old Trafford and modernize the stadium, opening-up exciting opportunities for the Club to deliver next-generation digital services to fans on matchdays and to visitors throughout the year."

Extreme is transforming match day as the Official Wi-Fi Network Solutions and Wi-Fi Analytics Provider of Manchester United Football Club. Wi-Fi 6E technology is helping to connect fans, increase revenue, and streamline stadium operations.

Manchester United joins several other iconic venues and leagues leveraging Extreme's solutions to improve operational efficiency and the fan experience. Extreme's roster of customers includes the Los Angeles Coliseum, MLB, NFL, NHL and Olympiastadion Berlin.

Extreme's longtime NFL deal, which was renewed this past fall through 2024, has resulted in Extreme Wi-Fi gear being used in 12 of the 30 league stadiums. The newest NFL stadiums, SoFi Stadium in Los Angeles and Allegiant Stadium in Las Vegas, both used Cisco Wi-Fi 6 gear for their Wi-Fi network deployments.

Extreme Networks is the Official Wi-Fi and Wi-Fi Analytics Provider of the NFL.

The sports vertical demonstrates technical capability in dense, demanding environments—exactly the kind of reference that enterprise IT decision-makers find compelling.

Dell'Oro Group Research Director Siân Morgan told Fierce Telecom that even small share gains for a company in Extreme's position can have a big impact on revenue. "The combined campus switch and WLAN market is expected to be $32 Billion in 2023. A 1% gain in market share would boost Extreme's FY revenues by over 20%," she explained. She added Extreme has traditionally "outperformed" in the education sector as well as in the sports and entertainment realm. Its recent Kroger win "especially given that it's a huge retail customer signing on to a cloud-based solution, has shone a new light on Extreme's potential in other verticals."

Extreme Networks' software-driven solutions are easily adaptable to vertical solutions in healthcare, education, manufacturing, government, and hospitality. To that point, Extreme Networks' solutions are well-suited for vertical-specific partners.

With this digital transformation and the massive shift to smart schools in K-12 education, Extreme Networks builds open, software-driven educational networking solutions with the elements necessary for K-12 schools to remain agile, adaptive and secure while improving learning outcomes.

Extreme Networks has carved out a position with cloud-managed networking and fabric simplicity. Education, healthcare, and venues value its ease of deployment and flexible licensing. The strategy of winning in underserved segments before attacking core enterprise directly mirrors the playbook of successful challenger brands across technology markets.

X. Competitive Landscape Deep Dive

The enterprise networking market presents a classic David vs. Goliath scenario, with Extreme positioned as an aggressive challenger against much larger incumbents.

According to Meyercord, third party metrics show that Cisco currently owns about 60% of the enterprise networking market, with HPE at 15% and Juniper at 6-7%. Extreme Networks is currently on par with Juniper in terms of market share.

Extreme Networks is angling for a coup in the enterprise networking sector, waging war against entrenched incumbents Cisco, HPE and Juniper. CEO Ed Meyercord said Extreme's biggest challenge right now is building brand recognition and upleveling its presence in sales channels. Inertia is another major obstacle.

Extreme Networks, Inc. (Nasdaq: EXTR), a leader in cloud networking, today announced it has been named as a Leader by Gartner, Inc. for the sixth consecutive time in the 2024 Gartner Magic Quadrant for Enterprise Wired and Wireless LAN Infrastructure, published on March 6, 2024, authored by Tim Zimmerman, Christian Canales, Nauman Raja and Mike Leibovitz. Of the 12 companies in the Magic Quadrant, Extreme Networks was named a Leader for both vision and execution.

The competitive differentiation centers on integration and simplicity: Using Extreme's cloud platform, customers can manage not only Extreme's networking hardware (think core network switches and fixed and Wi-Fi access points) but also that of its competitors. Meyercord said Extreme's model stands in stark contrast to that of its rivals. He specifically called out Cisco, noting customers have become frustrated by a lack of interoperability between some of its product sets, such as Meraki and the Cisco's Catalyst DNA software. "People are really fed up with what's going on," Meyercord said.

"The big challenge Cisco has is they are the most complicated to deal with," he said. "They've never integrated an acquisition, so all this is playing out with the customer." HPE, meanwhile, found its success with its Aruba division but has increasingly focused on its GreenLake cloud platform after losing key executives in 2020 and 2021.

The talent acquisition strategy reflects confidence in Extreme's competitive position: CEO Ed Meyercord told Fierce Telecom that over the past 12 months Extreme has hired some 650 people to support its growth. About a third of those came from the company's major competitors. "We are able to hire the best of the best," he said "They kind of know where bodies are buried and they see a lot of opportunity. So, I would say the human talent that we're attracting at Extreme is going to help us with this flywheel [of growth]."

Morgan also noted that Extreme's subscription revenue in the public-cloud managed WLAN market "has outpaced the market, in terms of Y/Y growth, every quarter for the past two years. This success makes their strategy to expand their subscription model to their entire portfolio all the more compelling."

XI. Playbook: Business & Strategic Lessons

Extreme's journey offers several lessons for technology investors and operators:

The "Rollup" Strategy: Extreme executed serial acquisitions to build scale when organic growth alone couldn't compete with Cisco. But unlike failed rollups, Extreme invested heavily in post-merger integration and product rationalization. The Enterasys disaster taught the company what not to do; subsequent acquisitions benefited from that painful education.

Platform Over Products: The Aerohive acquisition represented the strategic pivot from hardware vendor to cloud platform company. This wasn't just an acquisition of customers or products—it was an acquisition of a fundamentally different business model that enabled recurring subscription revenue.

Counter-Positioning: Extreme's strongest strategic power is offering a unified, cloud-managed platform while incumbents struggle with fragmented acquisitions. Cisco's inability to integrate Meraki with Catalyst DNA creates customer frustration that Extreme can exploit.

Vertical Specialization: Winning in underserved segments (stadiums, education, healthcare) before attacking core enterprise provides proof points and reference customers without directly confronting Cisco's strongest competitive positions.

Board-to-CEO Pipeline: Meyercord's progression from independent director to chairman to CEO gave him deep institutional knowledge that enabled faster decision-making during the turnaround. Companies considering leadership transitions might benefit from developing board members as potential executive candidates.

XII. Porter's Five Forces Analysis

| Force | Assessment | Analysis |

|---|---|---|

| Threat of New Entrants | LOW-MEDIUM | High capital requirements, established relationships, and complex sales cycles create significant barriers. However, cloud-native startups could potentially disrupt from below. |

| Bargaining Power of Suppliers | MEDIUM | Semiconductor dependency is real, particularly for custom ASICs. Post-pandemic supply chain improvements have reduced leverage, and Extreme has diversified its supplier base. |

| Bargaining Power of Buyers | HIGH | Enterprise customers have significant leverage through long sales cycles and competitive bidding. However, switching costs are high once deployed, creating customer stickiness. |

| Threat of Substitutes | MEDIUM | SD-WAN, cloud-native networking, and 5G private networks are emerging as alternatives to traditional enterprise networking. Extreme has addressed this through Ipanema acquisition. |

| Competitive Rivalry | VERY HIGH | Cisco's dominance (~60% market share), HPE's Aruba division, and Juniper's enterprise push create intense competitive pressure. However, competitor distractions (HPE-Juniper merger) create opportunities. |

XIII. Hamilton's 7 Powers Analysis

| Power | Assessment | Analysis |

|---|---|---|

| Scale Economies | WEAK | Cisco owns ~60% market share; Extreme lacks scale advantages in R&D spending, manufacturing, or sales force reach versus the leader. |

| Network Effects | MODERATE | ExtremeCloud IQ ecosystem creates some lock-in; partner integrations grow value. However, networking hardware generally has weaker network effects than software platforms. |

| Counter-Positioning | STRONG | Cloud-native, unified platform vs. Cisco's fragmented acquisitions creates structural advantage. Cisco can't easily respond without cannibalizing existing businesses. |

| Switching Costs | MODERATE-HIGH | Network infrastructure is deeply embedded in enterprise operations; migration is costly, risky, and disruptive. Multi-year contracts and integrated management create lock-in. |

| Branding | WEAK | As Meyercord noted, Extreme's biggest challenge is building brand recognition. The company remains largely unknown outside IT departments. |

| Cornered Resource | WEAK | No unique patents or talent that competitors cannot replicate. The Aerohive cloud platform is valuable but not irreplaceable. |

| Process Power | EMERGING | Consistent execution over multiple quarters suggests operational discipline. Customer support ratings and integration expertise represent potential process advantages. |

Key Strategic Insight: Extreme's strongest power is Counter-Positioning—offering a unified, cloud-managed platform while incumbents struggle with integration. This is a durable advantage because Cisco cannot easily adopt Extreme's approach without disrupting its existing business model and channel relationships.

XIV. Bull and Bear Cases

Bull Case:

The enterprise networking market represents a $32+ billion annual opportunity, and Extreme needs only modest market share gains to generate substantial revenue growth. The company's cloud-managed platform positions it well for the ongoing shift from hardware capex to software opex. "The combined campus switch and WLAN market is expected to be $32 Billion in 2023. A 1% gain in market share would boost Extreme's FY revenues by over 20%."

Competitor distractions—including HPE's acquisition of Juniper Networks—could create customer churn opportunities. Wi-Fi 7 refresh cycles will drive replacement demand over the next several years. And the transition to AI-powered network management (Platform ONE) could create meaningful differentiation if execution continues.

Bear Case:

Cisco remains dominant with 60% market share and vastly superior resources. Extreme's brand recognition challenges make competing for greenfield enterprise accounts difficult. The company's serial acquisition strategy has created integration complexity that may constrain future M&A. Macroeconomic sensitivity in discretionary IT spending could pressure near-term results. And employee reviews suggest cultural challenges that could affect retention and innovation.

XV. Key Performance Indicators to Watch

1. SaaS ARR (Annual Recurring Revenue): This metric captures Extreme's transition from hardware vendor to cloud platform company. Growth in SaaS ARR indicates successful adoption of ExtremeCloud IQ and supports higher valuation multiples. The 24% year-over-year growth in FY25 is encouraging but must be sustained.

2. Win Rate vs. Cisco in Competitive Deals: Market share gains against the dominant incumbent are the ultimate test of Extreme's competitive positioning. Management commentary on "rip and replace" wins from Cisco customers provides qualitative evidence of success.

Material Considerations

Regulatory/Legal: No material regulatory overhangs identified. The company operates in a competitive market without significant antitrust concerns at current scale.

Accounting Judgments: Revenue recognition for subscription bundles and hardware/software combinations requires management judgment. The treatment of acquired intangible assets from serial acquisitions affects GAAP profitability but not cash flow.

Key Person Risk: Ed Meyercord has been CEO for over 10 years and is closely identified with the turnaround strategy. Succession planning and management depth are considerations for long-term investors.

Myth vs. Reality

| Consensus Narrative | Reality Check |

|---|---|

| "Extreme is too small to compete with Cisco" | While scale disadvantages are real, Extreme's cloud-native platform creates structural advantages in simplicity and integration that Cisco struggles to match. Market share gains are occurring. |

| "Serial M&A always destroys value" | The Enterasys disaster supports this narrative, but subsequent acquisitions (Zebra, Avaya, Brocade, Aerohive) have been more successful. Disciplined integration is the key variable. |

| "Enterprise networking is a commodity" | Gartner leadership positioning and customer testimonials suggest meaningful differentiation exists. Cloud management, AI capabilities, and customer support create switching costs. |

Extreme Networks' transformation from near-death experience to industry challenger represents one of the more compelling turnaround stories in enterprise technology. The company has successfully executed a multi-year strategy of acquisition-driven scale creation, cloud platform development, and focused vertical market penetration. Whether it can sustain momentum against well-funded competitors while maintaining profitability remains the key question for long-term investors.

The networking market's structural shift toward cloud-managed, subscription-based solutions plays to Extreme's strengths. But the company's path to meaningful market share gains requires continued execution excellence, sustained investment in AI-powered differentiation, and the patience to build brand recognition in a market where customer relationships are measured in years, not quarters.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube