QIAGEN: The Picks and Shovels of the Genomics Gold Rush

I. Introduction: The Hidden Giant of the Genomics Revolution

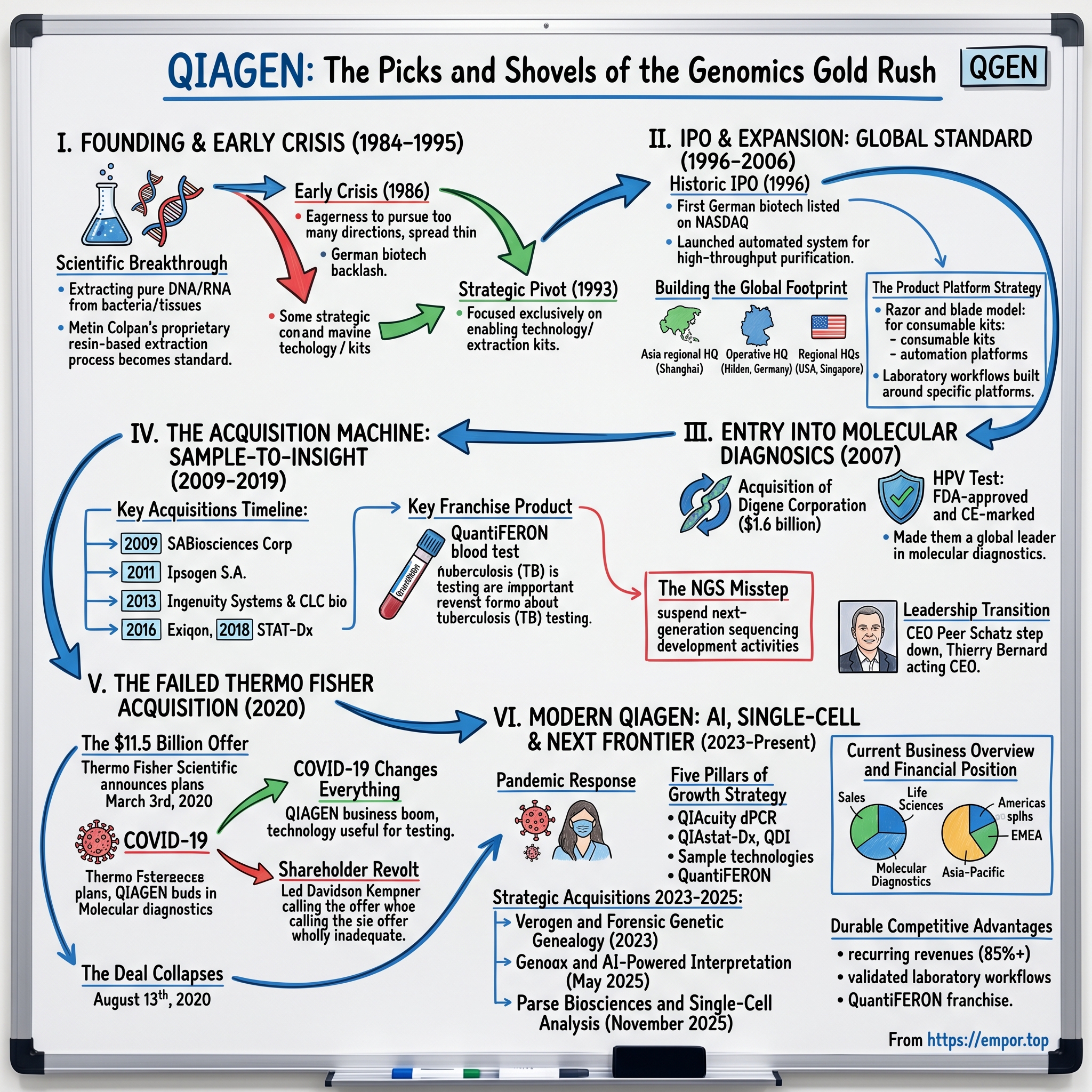

Picture a laboratory anywhere in the world—Shanghai, Boston, Munich, Sydney. Inside, a researcher prepares to analyze a tissue sample, seeking the genetic mutations that might explain a patient's cancer or tracking a viral pathogen threatening public health. Before any sequencing machine whirs to life, before any PCR test amplifies a single strand of DNA, one fundamental step must occur: the genetic material must be extracted, purified, and prepared. And more likely than not, the kit enabling that critical first step bears a name most investors have never heard: QIAGEN.

This is the story of a company that chose the unglamorous but indispensable path in biotechnology's gold rush. While headlines celebrated companies racing to cure diseases or sequence human genomes, QIAGEN quietly built an empire selling the equivalent of pickaxes and shovels to the genetic prospectors. Biotech pioneer QIAGEN N.V.—the holding company is based in the Netherlands but the company's main operations and headquarters are in Hilden, Germany—is providing the picks and shovels for the 21st century's genetics gold rush. The world leader in such fields as ultrapure DNA and RNA extraction and single nucleotide polymorphism (SNP) screening, QIAGEN dwarfs its nearest competitors, and is said to be seven times larger than all of its primary competitors combined.

QIAGEN's trailing twelve-month revenue as of June 2025 was $2.04 billion, representing a 5.15% year-over-year increase. The company's 2024 annual revenue reached $1.978 billion, a modest 0.66% increase from 2023, a stabilization after the wild swings of the COVID era. The company trades at roughly $42 per share with a market capitalization of approximately $9.5 billion—making it a mid-cap in an industry dominated by giants like Thermo Fisher Scientific ($200+ billion) and Illumina ($25+ billion).

But here's what makes QIAGEN's story compelling: it has survived and thrived for four decades in one of the most competitive, rapidly evolving industries on earth. It survived near-bankruptcy in the late 1980s, navigated Germany's hostile biotech climate, pioneered the first venture capital-backed company in German history, and built an acquisition machine that has completed 26 deals with an average acquisition value of $220 million. "These results underscore the resilience of our portfolio, with over 85% of sales coming from highly recurring revenues, and our focus on delivering solid profitable growth in an ongoing challenging environment," said Thierry Bernard, CEO of QIAGEN.

In 2020, QIAGEN walked away from an $11.5 billion acquisition offer that would have made it part of Thermo Fisher Scientific—a case where, uniquely in deal history, the COVID-19 pandemic improved the fortunes of the company being acquired, rather than weakened them. The failed deal proved to be a pivotal moment that set the stage for QIAGEN's current strategic direction.

This deep dive will explore how a PhD thesis from a German university became the foundation of a global leader in molecular diagnostics, why the company's "razor and blade" business model creates powerful customer lock-in, what the failed Thermo Fisher acquisition reveals about the company's intrinsic value, and whether QIAGEN can maintain its position as genomics enters the AI age.

II. Founding Story: From PhD Thesis to Biotech Pioneer (1984-1995)

The Scientific Breakthrough

The story begins in 1984 in Düsseldorf, Germany, where a 43-year-old biophysics professor named Detlev Riesner was working with three doctoral students on a problem that had bedeviled molecular biology for years. Extracting pure DNA from bacteria or from cells of human or animal tissues was a tedious and even dangerous process in the early 1980s, requiring the handling of toxic and extremely harsh chemicals and involving several days to complete. Yet the availability of large and reliable quantities of pure DNA and RNA was a requirement for the building of the nascent biotechnology field, then just gathering steam with the launch of the human genome project.

In 1984, three doctoral students—Metin Colpan, Karsten Henco and Jürgen Schumacher—founded a company in Düsseldorf with support from their supervisor, the 43-year-old biophysicist Detlev Riesner. The company was initially called Diagen (later renamed QIAGEN, a combination of 'QIA'—quality, innovation, automation—and 'gen' for genetics).

"In 1984 academia and industry seemed separated by a wall," Riesner later explained. "Big Industry had disappointed us. We had succeeded in purifying large amounts of viroid RNA and anticipated a rising need for such methods. Yet our partners in industry filed away our plans in their drawers. Fortunately, we had no exclusive deals with them."

The scientific breakthrough came from Metin Colpan, a Turkish-born chemist whose doctoral work focused on nucleic acid purification. QIAGEN holds the patent for a revolutionary and proprietary resin-based DNA extraction process developed by Colpan in the early 1980s that has since become a standard throughout the world. QIAGEN successfully leveraged and extended that technology to offer a wide array of more than 250 products, primarily in the form of consumable 'kits' to more than 150,000 customers worldwide.

Colpan joined with three other partners to launch QIAGEN N.V., a Netherlands-listed company with operational headquarters based in Hilden, Germany in 1984. The company claimed the distinction of being the first venture capital-backed German company.

The Early Crisis

The founding team's diverse talents—Riesner described them as "the far-sighted scientist Henco, the meticulous merchant Colpan and the solid decision-maker Schumacher"—proved to be both a strength and a weakness.

The tripartite nature of the enterprise favored by its founders soon proved to be a serious problem. "Effectively," writes Inken Rebentrost, author of an academic study on the origins of QIAGEN, "the constellation was three firms operating under one roof." Schumacher was out to develop tests identifying plant pests, while Henco was responsible for testing systems indicating human infectious diseases. The common denominator was the method underlying their approaches: the detection of pathogenic agents at the molecular level via their nucleic acids. Colpan's job was to develop novel separation techniques with which sufficient nucleic acids could be derived.

In 1986, QIAGEN introduced its first ready-to-use plasmid kit, which offered customers all the materials and equipment needed for the company's breakthrough nucleic acid cleansing process. But the company's eagerness to pursue too many directions nearly proved fatal.

Part of the company's troubles came from its eagerness to adapt its product to a broad variety of applications, targeting a range of industries from agricultural products to veterinary research laboratories, spreading the company too thin.

The situation was made worse by external factors unique to Germany at the time. In the mid-1980s, the country's biotechnology sector was reeling from public backlash against genetic research. The forced shutdown of another company's insulin production facility had created a hostile climate, and QIAGEN found itself shunned by potential German customers. By 1989, the company faced potential bankruptcy.

The Strategic Pivot

When QIAGEN diversified too much, it led to a liquidity crisis and the company split in 1993. Henco and Schumacher left to found their own companies. Colpan took over sole leadership of QIAGEN and, with newly recruited economist Peer Schatz, drew up a business plan that focused exclusively on separation technologies, expanded their areas of application and automated the process.

The arrival of Peer Schatz as CFO in 1993 helped the company put an end to its shaky financial condition. The Austrian-born and U.S.-educated Schatz helped Colpan redefine the company's strategy, narrowing its sights—and its resources—on the market for genetics research.

Peer M. Schatz (born August 3, 1965) is a Swiss and Austrian entrepreneur and executive in the life sciences. He was the chief executive officer of QIAGEN N.V. from 2004 to 2019. Schatz grew up in the United States and Switzerland. He studied business and social sciences at the University of St. Gallen, Switzerland, graduating with a master's degree in finance in 1989 and obtaining a Master of Business Administration (MBA) from the University of Chicago Graduate School in Business in 1990. Schatz worked in different positions for Sandoz AG and Computerland and participated in the foundation of startup companies.

The pivot was strategic brilliance. Rather than compete in drug development or gene therapies—which required years of costly research with no guarantee of success—QIAGEN focused exclusively on the enabling technology. If the genomics revolution was a gold rush, QIAGEN would sell the picks and shovels. QIAGEN also sells complete robotics systems enabling automated DNA extraction using its kits, freeing up valuable laboratory time and manpower. The company's technology, which has been used in such infamous circumstances as the O.J. Simpson murder trial and the testing of Monica Lewinsky's dress stains, has helped reduce DNA extraction times from several days to just two hours.

By the end of 1991, QIAGEN was profitable while still posting less than $10 million in total sales. The foundation for explosive growth had been laid.

III. IPO & Expansion: Becoming the Global Standard (1996-2006)

Historic IPO

In 1996, QIAGEN became the first German biotechnology company listed on the American NASDAQ stock exchange, and one year later it figured on the Neuer Markt in Frankfurt.

This wasn't just a financing event—it was a statement of ambition. By listing in the United States first, QIAGEN signaled that it viewed itself as a global player competing for American venture capital and institutional investors. Schatz joined QIAGEN and paved the way for both the company's initial public offering at the Nasdaq in 1996 as the first German company ever and the subsequent listing at the Frankfurt Stock Exchange.

In the same year, QIAGEN launched the first automated system for high-throughput purification of nucleic acids, revolutionizing the process of sample preparation for molecular assays. This was the critical second leg of the strategy: not just selling consumable kits, but developing the automation platforms that would make those kits essential.

Building the Global Footprint

The post-IPO years were defined by geographic expansion and product proliferation. QIAGEN established its Asia regional headquarters in Shanghai and built out operations across more than 35 offices in over 25 countries. The company's global corporate headquarters sits in Venlo, the Netherlands, while the main operative headquarters remains in Hilden, Germany. Regional headquarters span four continents—Germantown, Maryland for the Americas; Shanghai for China; and Singapore for Asia-Pacific.

The Product Platform Strategy

The genius of QIAGEN's business model emerged during this period. QIAGEN holds the patent for a revolutionary and proprietary resin-based DNA extraction process that has since become a standard throughout the world. QIAGEN successfully leveraged and extended that technology to offer a wide array of more than 250 products, primarily in the form of consumable 'kits.'

This is the classic "razor and blade" model, but with an important twist. Unlike razors, where switching costs are minimal, laboratory workflows are built around specific platforms. Once a lab validates its processes with QIAGEN kits and instruments, switching to a competitor means re-validating all protocols—a costly and time-consuming process that most laboratories avoid unless absolutely necessary.

The company generates approximately 90% of its revenue from consumables—the ongoing kits that laboratories must continue purchasing—with the balance coming from instrumentation and related services. This creates predictable, recurring revenue streams that provide remarkable stability even during economic downturns.

Under Peer Schatz's leadership, QIAGEN grew from $2 million of sales in 1993 to the current level of about $1.6 billion, while the market capitalization has increased by over 300 times and its employee base has grown from 25 employees to more than 5,200 today with a presence in over 35 countries.

By the mid-2000s, QIAGEN had become the poster child of Germany's biotechnology sector. But it still wasn't playing in the premier league internationally. That was about to change with the company's most transformative acquisition.

IV. The Digene Acquisition: Entry into Molecular Diagnostics (2007)

The Strategic Bet

In 2007, QIAGEN made a move that would fundamentally reshape the company. It acquired Digene Corporation, a Maryland-based molecular diagnostics company, for $1.6 billion—the largest acquisition in QIAGEN's history at the time and one of the largest in the molecular diagnostics industry.

That all changed in 2007 with the multibillion-dollar takeover of Digene, a company based in Maryland, USA, with what at the time was the only approved test for detecting human papillomavirus (HPV), which causes cervical cancer. QIAGEN's acquisition of Digene made it a global leader in molecular diagnostics.

Why Digene Mattered

Digene held a unique and defensible market position. Its primary product, the Digene HPV Test, screened for the presence of high-risk types of human papillomavirus—the causative agent in approximately 70% of cervical cancer cases. Crucially, the Digene HPV Test was the only test for HPV that was both FDA-approved and CE-marked, giving it a regulatory moat that competitors would take years to breach.

The market opportunity was enormous. Cervical cancer is the second most common cancer among women (after breast cancer) and is responsible for approximately 250,000 deaths annually worldwide. HPV testing represented one of the largest and most rapidly expanding market segments in women's health and molecular diagnostics.

The acquisition built on a successful relationship of more than a decade between the two companies, as QIAGEN had supplied sample preparation technologies for Digene's testing platforms.

Creating a Molecular Diagnostics Leader

The strategic logic was compelling: combining QIAGEN's leading portfolio of sample and assay technologies with Digene's leadership in HPV-targeted molecular diagnostic testing would create a global leader in molecular diagnostics outside blood screening and viral load monitoring. The combined company was projected to have over $350 million of molecular diagnostics revenues.

In 2007, QIAGEN's sales reached US$649.8 million and the number of employees surpassed 2,600. The Digene acquisition furthered QIAGEN in molecular diagnostics by revenue and diagnostics for disease prevention.

The Digene deal represented more than just revenue diversification—it shifted QIAGEN's strategic identity. The company was no longer solely a "picks and shovels" supplier to researchers; it was now directly in the business of diagnosing disease. This transition from pure research tools to clinical diagnostics would prove critical to the company's resilience through subsequent market cycles.

V. The Acquisition Machine: Building Sample-to-Insight (2009-2019)

The M&A Strategy

Following the Digene acquisition, QIAGEN embarked on a decade-long buying spree that would transform it from a sample preparation specialist into a full-spectrum molecular diagnostics powerhouse. QIAGEN has made acquisitions in 10 countries with the most activity in United States and Denmark. Most of QIAGEN's acquisitions are in Genomics (20) and Life Sciences Platforms and Tools (14).

The strategy was clear: build a "Sample to Insight" platform that could take a biological sample through the entire workflow—from collection and preparation through amplification, detection, and data interpretation. Each acquisition filled a gap in this end-to-end capability.

Key Acquisitions Timeline

2009: Personalized Healthcare Push In 2009, QIAGEN began building its Personalized Healthcare business through the acquisition of DxS Ltd, in a deal valued at US$95 million, and it acquired SABiosciences Corp. in a deal valued at US$90 million. At the end of 2009, QIAGEN surpassed the US$1 billion revenue mark and had over 3,500 employees. The billion-dollar revenue milestone, coming just two years after Digene, validated the acquisition strategy.

QIAGEN also became one of the first companies to release a clinically verified diagnostic test for the detection of H1N1 (Swine Flu), demonstrating its ability to respond rapidly to emerging public health threats—a capability that would prove essential a decade later.

2011: TB Testing and Blood Cancer QIAGEN acquired Ipsogen S.A. for US$101 million, adding to the company's product and IP portfolio in the blood cancer space. More significantly, QIAGEN acquired Cellestis Limited for US$374 million, gaining access to QuantiFERON technology for disease detection and prevention.

The Cellestis deal brought QIAGEN one of its most enduring franchise products. QIAGEN recently reached a major landmark in the field of tuberculosis (TB) testing. The company announced that since the time of its launch, its QuantiFERON blood test has been used more than 100 million times to detect TB infection. QuantiFERON is an Interferon-gamma release assay (IGRA) blood test that is claimed to be a superior alternative to the tuberculin skin test. The fourth-generation QuantiFERON-TB Gold Plus assay currently has a patient base in more than 130 countries worldwide.

QIAGEN leverages its QuantiFERON-TB Gold Plus and QuantiFERON-TB Access lines, which grew 24% in 2023, to defend share in hospitals and reference laboratories. Tuberculosis remains the world's most deadly infectious disease, and QuantiFERON delivered 11% CER growth for 2024, with significant opportunities for further expansion since only 40% of the global latent TB testing market has so far been converted from the outdated skin test.

2013: Bioinformatics Capability QIAGEN acquired Ingenuity Systems and CLC bio, which offers bioinformatics analysis software. These deals moved QIAGEN into the critical "Insight" portion of its Sample-to-Insight vision—enabling customers not just to generate genetic data but to interpret it.

2016-2018: Syndromic Testing Platform QIAGEN acquired the Danish molecular diagnostics company Exiqon in 2016. In April 2018, QIAGEN acquired the Spanish firm STAT-Dx and launched the QIAstat-Dx molecular diagnostics platform, a syndromic testing system that would become one of the company's key growth pillars.

In 2018, QIAGEN transferred its U.S. listing from NASDAQ to the New York Stock Exchange, signaling its evolution into a major healthcare company.

The NGS Misstep and Leadership Transition

Qiagen announced Monday CEO Peer Schatz is stepping down after 27 years at the company. Thierry Bernard, the head of the company's molecular diagnostics business, will serve as an interim CEO while Qiagen's supervisory board searches for a permanent replacement. The company also said it is undertaking a new restructuring strategy after unexpectedly tepid growth in China led to weak preliminary third quarter results. Qiagen is also suspending next-generation sequencing-related instrument development activities as it pivots to a 15-year partnership with Illumina.

Qiagen's stock dropped more than 20% on the news of Schatz's departure and the weak third quarter sales numbers. The company took a pre-tax restructuring charge of $260-265 million "predominately" in the third quarter related to its decision to suspend its NGS instrument development. Cowen analysts called the decision to suspend new placements of GeneReader "likely... the correct decision." "The product has had minimal adoption to date (no more than $10-15MM in 2018 revenue), and there were no catalysts in sight to improve results."

Peer M. Schatz stepped down as CEO to pursue new opportunities. He would remain with QIAGEN as Special Advisor to the Supervisory Board. Thierry Bernard, Senior Vice President, Head of Molecular Diagnostics Business Area, would act as interim CEO and work in tandem with Roland Sackers, Chief Financial Officer. "It has been a tremendous privilege to serve as the CEO of QIAGEN for such a long time. I am incredibly proud of the market and technology leadership that we have created and what our teams and partners have accomplished together," said Schatz.

The GeneReader episode illustrates the challenges of platform competition in genomics. QIAGEN had attempted to compete directly with Illumina in next-generation sequencing—a market where Illumina held dominant share and unmatched scale advantages. The pivot to partnership with Illumina rather than competition was a strategic acknowledgment of where QIAGEN's true strengths lay.

VI. The Failed Thermo Fisher Acquisition: A Pivotal Moment (2020)

The $11.5 Billion Offer

Thermo Fisher and Qiagen announced the $11.5 billion deal in March after an on-again, off-again courtship starting in November 2019. The companies portrayed the combination as complementary, with Thermo Fisher expanding its specialty diagnostics portfolio by adding Qiagen's capabilities in molecular diagnostics.

On March 3, 2020, Thermo Fisher Scientific announced plans for the acquisition of QIAGEN at €39 per share in cash, which valued the transaction at $11.5 billion at the time.

The timing was fateful. The deal was announced just days before the World Health Organization declared COVID-19 a global pandemic.

COVID-19 Changes Everything

What happened next was unprecedented in M&A history. While the COVID-19 pandemic continued to wreak havoc on the world, Qiagen's business saw a boom. The company's technology was found useful for COVID-19 testing, which led to a significant increase in sales for its equipment and services. In a Q2 earnings update, Qiagen noted that its sales grew 16% and its earnings grew by 70% compared with Q2 2019.

As the leading supplier of sample prep kits to extract nucleic acids—including viral RNA—QIAGEN found itself at the center of the global testing response. The company's products were essential for the initial rapid testing responses worldwide. Increased demand pushed QIAGEN's Q1 and Q2 revenues up 7% and 19% respectively compared to 2019.

QIAGEN's net income more than doubled, jumping 101% to $89.8 million year-over-year in Q2 2020. Net sales grew 16% during the quarter to $443.3 million.

The Shareholder Revolt

The opposition to the acquisition among Qiagen's shareholders was spearheaded by investment firm Davidson Kempner, which in early July owned 3% of Qiagen. The firm published an open letter voicing its objection to the sale and said it would not tender its shares under the initial proposed deal. When Thermo Fisher upped its takeover price, Davidson Kempner proceeded to increase its stake in Qiagen to 8% and said it would still not tender its shares. Davidson Kempner put the standalone share value at Qiagen at €48 to €52 a share, around 18% above Thermo Fisher's second offer.

Thermo Fisher had recently increased its offer to 43 euros per Qiagen share, up from an earlier proposal of 38 euros. For the deal to go through, two-thirds of Qiagen shareholders had to tender their shares by Aug. 10. However, Thermo Fisher disclosed only 47% shares were tendered.

The sweetened deal was not enough to attract one vocal critic, the hedge fund Davidson Kempner, which raised its stake in QIAGEN from 3.6% to 8%. "Davidson Kempner sees Qiagen's standalone fair value as €48-52/share [$57-$61], and therefore considers the current offer wholly inadequate."

The Deal Collapses

The acquisition offer was terminated on August 13, 2020, having only reached the threshold of 47% of shareholder approval, below the minimum 66.6% required as per agreement. Davidson Kempner was notable as having continued to reject the bid. Because of the lapsed offer, QIAGEN was required to reimburse $95 million to Thermo Fisher in expenses. Within a week of the collapse of the merger, QIAGEN's stock rose over 10%.

It's not especially common for a deal of this magnitude to fall apart because the COVID-19 pandemic improved the fortunes of the companies involved, instead of weakened them. However, despite Qiagen's significant growth, some analysts have argued that the company's good fortunes might not last.

The failed deal forced QIAGEN to chart an independent course. Going forward, CEO Thierry Bernard said Qiagen will proceed with plans for the full acquisition of COVID-19 and flu test developer NeuMoDx.

The Thermo Fisher episode remains a defining moment for QIAGEN. It validated the company's intrinsic value, demonstrated the shareholder base's confidence in standalone prospects, and set the stage for the company's post-COVID transformation.

VII. COVID-19 Era & Strategic Transformation (2020-2022)

Pandemic Response

With the Thermo Fisher deal dead, QIAGEN pivoted to aggressive pandemic response. The company reacted with agility and urgency, developing new tests in record time and producing them in mass quantities.

QIAGEN developed the QIAseq SARS-CoV-2 Primer Panel in June 2020, providing an optimized next-generation sequencing solution for targeted enrichment of the complete viral genome. The company also collaborated with BioNTech—the German biotech that would develop one of the leading COVID-19 vaccines—to develop rapid COVID-19 tests.

During the coronavirus pandemic, 750 million COVID-19 tests contained QIAGEN products.

The NeuMoDx Acquisition and Platform Expansion

In September 2020, QIAGEN announced the acquisition of Michigan-based NeuMoDx Inc., paying approximately $234 million for the outstanding 80.1% of shares it did not already own. The deal gave QIAGEN two fully integrated systems for automated PCR—critical infrastructure for high-volume COVID testing.

However, the NeuMoDx story would not have a happy ending. In July 2024, QIAGEN announced plans to cut 175 employees and close its Michigan PCR test plant. The platform was ultimately discontinued as COVID testing volumes normalized.

The "Five Pillars of Growth" Strategy

QIAGEN continues to prioritize and accelerate investments for growth in QIAcuity digital PCR (dPCR), QIAstat-Dx syndromic testing, and its QDI (QIAGEN Digital Insights) portfolio. At the same time, the company is building on its strong and proven leadership in Sample technologies and QuantiFERON, capitalizing on consistent demand and trusted market positions. Together, these strategic pillars form the foundation for sustainable, profitable growth and long-term value creation.

QIAGEN's digital PCR platform, QIAcuity, launched in late 2020 using nanoplate technology to disperse a sample over thousands of partitions. The platform found particular traction in wastewater testing for SARS-CoV-2 surveillance—an application that demonstrated how COVID accelerated adoption of molecular testing in entirely new contexts.

Converting COVID Growth to Sustainable Business

The critical challenge became converting pandemic-driven demand into sustainable growth. Though Qiagen's COVID-related revenues fell 9 percent year over year in the fourth quarter of 2021, its non-COVID-related business increased 8 percent in the quarter and 24 percent for the full year, with growth across all product groups.

In September 2021, QIAGEN entered the DAX—Germany's leading stock market index. This milestone reflected both the company's increased scale from pandemic revenues and its elevated profile in European capital markets.

Management consistently emphasized that while QIAGEN became COVID-relevant, it was not COVID-dependent. The company's diversified portfolio—spanning sample preparation, molecular diagnostics, bioinformatics, and automation—provided resilience that pure-play COVID testing companies lacked.

VIII. Modern QIAGEN: AI, Single-Cell & The Next Frontier (2023-Present)

Strategic Acquisitions in 2023-2025

QIAGEN has continued its acquisition-led strategy, but with a clear focus on two themes: forensics and AI-powered genomics.

Verogen and Forensic Genetic Genealogy (2023) QIAGEN completed the full acquisition of Verogen for $150 million in cash paid from existing reserves. QIAGEN currently expects about $20 million of sales from the Verogen portfolio in 2023, building on about $5 million of sales for QIAGEN in 2022 from the distribution agreement.

QIAGEN gains full access to Verogen's pioneering GEDmatch database and GEDmatch PRO portal. GEDmatch allows users to upload genetic profiles created by other genealogy sites in order to expand the search for familial links; it currently contains more than 1.8 million genealogical profiles and continues to grow.

Among the successes of this technology is work by public safety officials who used GEDmatch to apprehend accused Golden State Killer Joseph DeAngelo, a notorious serial killer who terrorized California and evaded police for decades until his arrest in 2018.

Genoox and AI-Powered Interpretation (May 2025) QIAGEN announced that it has acquired Tel Aviv, Israel-based genomics software firm Genoox for $70 million in cash and potential additional milestone payments of up to $10 million. The Genoox portfolio includes Franklin, a clinical decision support platform for genetic diseases. Genoox's AI-powered, cloud-based software enables small and mid-sized clinical labs to scale and accelerate the processing of complex genetic tests through next-generation sequencing data interpretation. The platform can be used to analyze targeted gene panels and whole-exome and -genome sequencing data, and is currently used by more than 4,000 healthcare organizations in 50 countries.

Parse Biosciences and Single-Cell Analysis (November 2025) QIAGEN will fully acquire Parse Biosciences for an upfront payment of approximately $225 million in cash, with Parse equityholders eligible for additional milestone payments of up to $55 million based on the achievement of targets over a multi-year period. The transaction is expected to be completed in December 2025. For full-year 2026, Parse is expected to contribute approximately $40 million in sales to QIAGEN (approximately two percentage points of growth), with sales expected to increase at a strong double-digit rate in subsequent years. The transaction is expected to be dilutive to adjusted earnings per share by approximately $0.04 in 2026 and accretive beginning in 2028.

Parse was co-founded in 2018 by Alex Rosenberg, who was a University of Washington postdoctoral fellow at the time, and Charles Roco, who was a UW graduate student. The company was an early entrant in the nascent field of single-cell RNA sequencing. Rosenberg and his colleagues discovered a new way to profile RNAs while working in the lab of UW synthetic biology professor Georg Seelig. The business initially launched as Split Biosciences, later changing its name and growing to 110 employees.

The acquisition strengthens QIAGEN's position in the rapidly growing single-cell analysis market, projected to grow from US$1.2 billion in 2024 to US$2.1 billion by 2029, a roughly 10% annual growth rate.

CEO Transition and Shareholder Returns

Venlo, the Netherlands, November 4, 2025—QIAGEN N.V. announces that Thierry Bernard will step down as Chief Executive Officer and Managing Director once a successor is appointed. The Supervisory Board, supported by an executive search firm, has initiated a process to identify, evaluate and appoint a successor from both internal and external candidates. Thierry Bernard, 61, joined QIAGEN in 2015 and has served as CEO since 2019.

Upon becoming interim CEO in 2019, Bernard inherited a company that was restructuring in response to slow growth in China and the suspension of next-generation sequencing development activities. Starting on what analysts called "clearly a bad day" for Qiagen, Bernard was soon confronted with a takeover bid from Thermo Fisher Scientific and the COVID-19 pandemic. Having guided Qiagen through the collapse of the Thermo Fisher deal, Bernard oversaw pandemic-fueled revenue peaks and troughs and initiated a restructuring to adapt to the post-COVID-19 environment. The changes have resulted in a business that is on course to grow 4% to 5% this year.

QIAGEN announced plans to complete a $500 million synthetic share repurchase in early January 2026 to further increase shareholder returns, bringing total returns to more than $1 billion since 2024 and well ahead of its 2028 goal. "Our strong profitability and cash generation are allowing QIAGEN to step up shareholder returns," said Roland Sackers, CFO of QIAGEN. "With the execution of the $500 million repurchase in January 2026 that shareholders approved at our last Annual General Meeting, we are returning more than $1 billion to shareholders well ahead of our 2028 goal."

Current Business Overview and Financial Position

QIAGEN serves more than 500,000 customers worldwide in the Life Sciences (academia, pharmaceutical R&D and industrial applications such as forensics) and Molecular Diagnostics (clinical healthcare). As of September 30, 2025, QIAGEN employed approximately 5,700 people across more than 35 locations.

The company's sales are split almost evenly between applications in life sciences and molecular diagnostics. Geographically, the Americas account for the largest portion of revenue (52% of 2024 sales), followed by EMEA (33%), and Asia-Pacific (15%).

QIAGEN reaffirmed its FY 2025 outlook for net sales growth of about 4-5% CER (about 5-6% CER core sales excluding divestments) and raised its adjusted diluted EPS target to about $2.38 CER. QIAGEN also expects an adjusted operating income margin of about 29.5% (about 30% CER) in 2025 while absorbing headwinds from currency movements and tariffs.

IX. Competitive Landscape, Bull & Bear Case

Competitive Position

QIAGEN operates in a competitive landscape dominated by larger players while defending against nimble specialists.

The global genomics market is competitive including key players such as Illumina, Inc. (US), Thermo Fisher Scientific Inc. (US), Danaher Corporation (US), F. Hoffmann-LA Roche Ltd. (Switzerland), QIAGEN (Germany), Agilent Technologies, Inc. (US), Revvity (US), and others including 10X Genomics (US).

The Giants: - Thermo Fisher Scientific ($200B+ market cap): The company that tried to acquire QIAGEN remains the elephant in the room. With vast resources and a comprehensive product portfolio, Thermo Fisher competes across virtually every segment. - Illumina ($25B market cap): The dominant force in sequencing instruments, Illumina represents both a competitor and a partner through QIAGEN's IVD kit development agreement. - Danaher ($180B market cap): Through subsidiaries including Cepheid and Integrated DNA Technologies, Danaher competes in molecular diagnostics and genomics.

The Specialists: - 10x Genomics ($2B market cap): 10x's Chromium uses microfluidics to isolate cells. Parse's Evercode adds combinations of DNA barcodes to trace cells, eliminating the need for specialized instruments and supporting the analysis of more cells in a single run. 10x filed a lawsuit against Parse in 2022. Parse invalidated a 10x patent last month. QIAGEN's Parse acquisition positions it directly against 10x Genomics in single-cell analysis. - bioMérieux: A major competitor in TB diagnostics and infectious disease testing.

Porter's Five Forces Analysis

Threat of New Entrants: LOW-MODERATE - Regulatory barriers (FDA, CE marking) create significant hurdles - Established customer relationships and validated workflows create switching costs - However, AI-driven software tools require less capital than traditional instruments

Bargaining Power of Suppliers: LOW - QIAGEN sources relatively commoditized raw materials - Vertical integration in manufacturing reduces dependency - Multiple sourcing options available for most components

Bargaining Power of Buyers: MODERATE - Large hospital systems and reference laboratories have negotiating leverage - However, switching costs from validated workflows are high - Fragmented customer base (500,000+ customers) dilutes individual bargaining power

Threat of Substitutes: MODERATE-HIGH - Competing technologies (sequencing vs. PCR, different sample prep methods) exist - AI interpretation tools could commoditize some bioinformatics offerings - Point-of-care testing could shift volumes away from centralized labs

Competitive Rivalry: HIGH - Multiple well-funded competitors across each product category - Price pressure in commoditized segments - Technology evolution requires continuous R&D investment

Hamilton Helmer's 7 Powers Framework

Scale Economies: MODERATE QIAGEN benefits from manufacturing scale in consumables but lacks the dominant scale position of larger competitors like Thermo Fisher.

Network Effects: EMERGING The GEDmatch database (1.8 million genealogical profiles) demonstrates network effects in forensics—each additional profile increases the database's value for investigative use. The Franklin platform's 4,000+ healthcare organizations creates a community network for genetic interpretation.

Counter-Positioning: LIMITED QIAGEN's "Sample to Insight" approach is not fundamentally different from larger competitors' strategies.

Switching Costs: HIGH This is QIAGEN's strongest competitive advantage. Once laboratories validate workflows with QIAGEN kits and instruments, switching requires re-validation of all protocols—a costly, time-consuming process. Over 85% of sales come from highly recurring revenues.

Cornered Resource: MODERATE Key patents (QuantiFERON technology, sample preparation methods) provide protection. In February 2025, QIAGEN received a favorable court ruling reaffirming a key QuantiFERON-TB patent. The decision upheld the validity of one of QIAGEN's core patents related to its QuantiFERON-TB diagnostic technology.

Process Power: MODERATE Deep expertise in sample preparation accumulated over 40 years provides operational advantages, though this is replicable over time.

Branding: MODERATE QIAGEN is a respected brand among laboratory professionals, though brand equity is limited in consumer awareness compared to diagnostic brands like Roche or Abbott.

The Bull Case

-

Structural Growth in Molecular Testing: The genomics market continues to grow at 5-10% annually, driven by precision medicine adoption, expanded screening programs, and AI-driven drug discovery.

-

Recurring Revenue Model: With 85%+ of revenue from consumables, QIAGEN enjoys predictable cash flows and customer lock-in through validated workflows.

-

QuantiFERON Runway: Only 40% of the global latent TB testing market has so far been converted from the outdated skin test, providing substantial untapped growth potential in one of QIAGEN's highest-margin franchises.

-

AI Integration Positioning: Recent acquisitions (Genoox, Parse) position QIAGEN at the intersection of sample preparation and AI-powered interpretation—increasingly important as labs generate massive data volumes.

-

Capital Return Program: Returning more than $1 billion to shareholders well ahead of the 2028 goal demonstrates confidence in cash generation and commitment to shareholder value.

The Bear Case

-

CEO Transition Risk: In an unexpected move, Bernard will step down from his role and the company "after a successor is appointed." He's helmed Qiagen for six years and was in charge during its 2020 roller coaster that saw it almost bought out by Thermo Fisher. Leadership transitions create execution risk.

-

Competitive Pressure from Giants: Thermo Fisher, Danaher, and Roche have vastly greater resources and can compete across QIAGEN's portfolio while absorbing losses in specific segments.

-

Post-COVID Revenue Hangover: QIAGEN annual revenue for 2023 was $1.965 billion, an 8.23% decline from 2022. QIAGEN annual revenue for 2022 was $2.142 billion, a 4.89% decline from 2021. COVID-era revenues created difficult comparisons that are only now normalizing.

-

Single-Cell Competition: The Parse acquisition puts QIAGEN directly against 10x Genomics, which has first-mover advantage and ongoing patent litigation creates uncertainty.

-

NeuMoDx Write-Off Caution: The discontinuation of the NeuMoDx platform after a $234 million acquisition raises questions about M&A execution risk.

X. Key Metrics and Investment Considerations

Critical KPIs to Track

For investors evaluating QIAGEN, two metrics deserve particular attention:

1. Core Sales Growth at Constant Exchange Rates (CER) This metric strips out discontinued products and currency fluctuations to reveal underlying business momentum. QIAGEN targets about 5-6% CER core sales growth for 2025. Sustained growth in this range would indicate successful transition from COVID-era volatility to durable expansion.

2. QuantiFERON Growth Rate As QIAGEN's highest-margin, most defensible franchise, QuantiFERON serves as a bellwether for the company's competitive position. QuantiFERON delivered 11% CER growth for 2024—continued double-digit growth would validate the secular tailwind from skin test conversion. Deceleration below market growth (~6% for TB diagnostics) would signal competitive encroachment.

Financial Considerations

-

Adjusted Operating Margin: The adjusted operating income margin improved by 2.6 percentage points to 30.6% in Q4 2024, driven by efficiency gains and NeuMoDx discontinuation. Targeting above 30% for 2025.

-

Balance Sheet: Strong cash generation supports both acquisitions and shareholder returns. The company maintains investment-grade credit profile.

-

Valuation Context: At roughly $42/share and ~$9.5B market cap, QIAGEN trades at approximately 4.8x trailing revenue and 18x adjusted EPS—a premium to diversified life sciences peers but a discount to growth stories like 10x Genomics.

Regulatory and Legal Considerations

-

In March 2025, QIAGEN filed a patent-infringement suit against bioMérieux to defend QuantiFERON proprietary technology in latent tuberculosis testing. The outcome could impact competitive dynamics in TB diagnostics.

-

The Parse acquisition faces standard regulatory review under Hart-Scott-Rodino, though closure in December 2025 is expected.

-

As a Netherlands-domiciled company trading on both NYSE and Frankfurt, QIAGEN navigates dual regulatory frameworks and currency exposure.

Conclusion: The Enduring Value of Essential Infrastructure

QIAGEN's four-decade journey from a PhD thesis in Düsseldorf to a global leader in molecular diagnostics illuminates a timeless business principle: there is enduring value in providing essential infrastructure for transformative industries.

While the headlines celebrate the companies racing to cure cancer or decode the human genome, QIAGEN has built a multi-billion dollar enterprise selling the picks and shovels. Providing the picks and shovels for the 21st century's genetics gold rush, the world leader in ultrapure DNA and RNA extraction and SNP screening, QIAGEN dwarfs its nearest competitors.

The company faces genuine challenges: a CEO transition, competition from giants with deeper pockets, and the need to prove that recent acquisitions in single-cell and AI will deliver returns. The NeuMoDx discontinuation serves as a reminder that not every bet pays off.

Yet QIAGEN possesses durable competitive advantages. Switching costs from validated laboratory workflows create sticky customer relationships. The QuantiFERON franchise continues to gain share against the outdated tuberculin skin test. And the fundamental demand driver—the relentless expansion of molecular testing across research, clinical, and applied markets—shows no signs of abating.

Perhaps most telling is what happened when the largest company in the industry, Thermo Fisher Scientific, tried to acquire QIAGEN for $12.5 billion. Shareholders rejected the offer, believing the company was worth more on its own. Within a week of the deal's collapse, QIAGEN's stock rose over 10%. Five years later, the company remains independent, profitable, and strategically positioned at the intersection of sample preparation, molecular diagnostics, and AI-powered interpretation.

For the genomics gold rush, the picks and shovels remain indispensable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube