Edwards Lifesciences: The Heart Valve Innovation Story

I. Introduction & Episode Roadmap

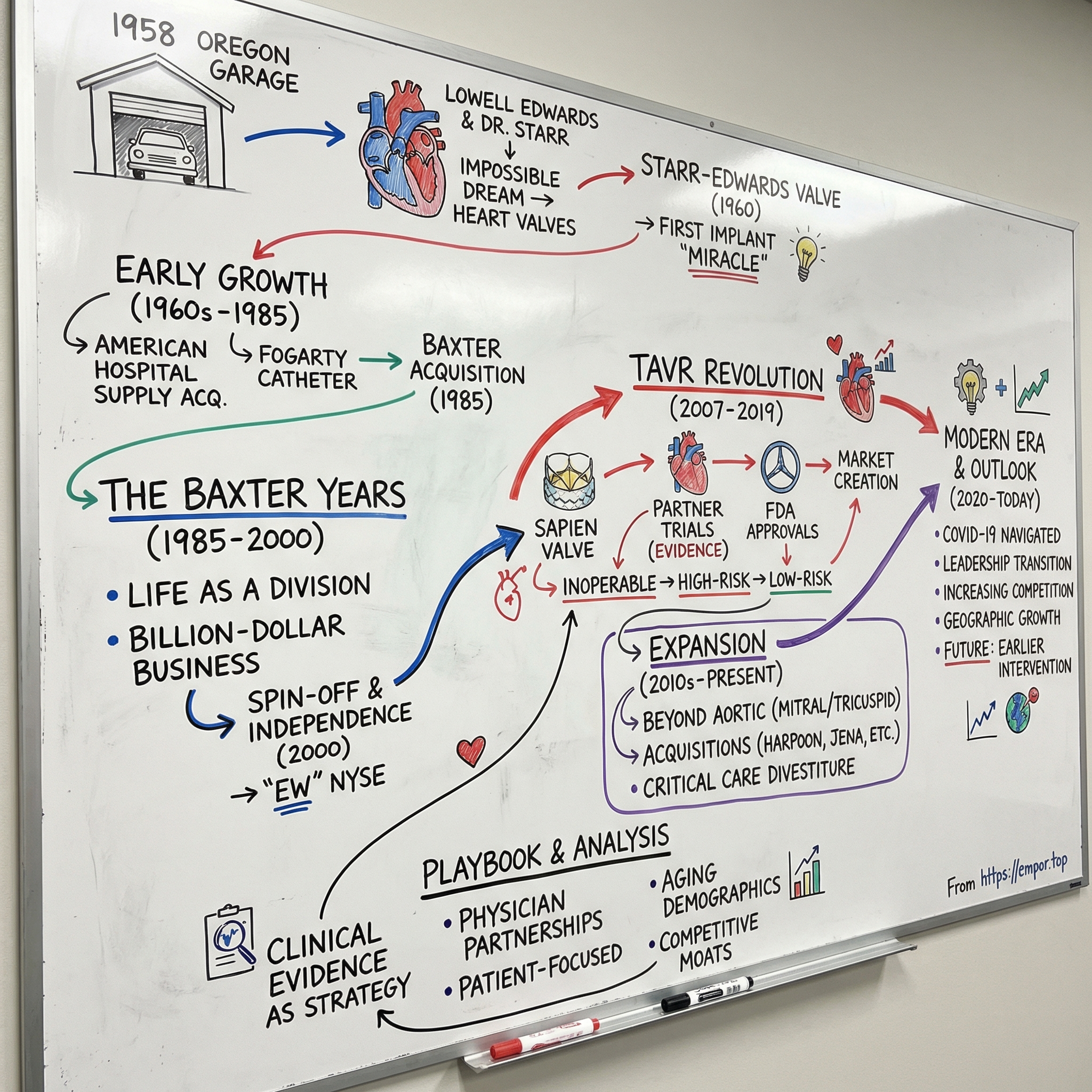

Picture this: A 61-year-old retired engineer sits in his garage in Portland, Oregon, tinkering with plastic tubes and ball bearings, convinced he can build a mechanical heart. The year is 1958. Open-heart surgery has only been possible for five years. Most cardiac surgeons consider replacing heart valves a fantasy. Yet within two years, this engineer—Miles "Lowell" Edwards—and a young surgeon named Albert Starr will implant the world's first successful artificial heart valve, fundamentally altering the trajectory of cardiac medicine.

Today, Edwards Lifesciences commands a $40.7 billion market capitalization, generating $5.44 billion in revenue from a portfolio of heart valves and hemodynamic monitoring devices that trace their lineage directly back to that Portland garage. The company has transformed from a scrappy startup challenging the medical establishment to the undisputed leader in transcatheter heart valve replacement—a market it essentially created. The story of Edwards Lifesciences is fundamentally the story of how cardiac medicine evolved from desperate, high-mortality surgery to routine outpatient procedures. It's a narrative of engineer-physician partnerships, calculated spin-offs, and perhaps most importantly, the creation of an entirely new medical device category that has treated over one million patients worldwide.

What makes Edwards particularly fascinating from a business perspective is how it transformed from a division buried inside two different conglomerates—first American Hospital Supply, then Baxter International—into an independent powerhouse with gross margins that increased from 47% in 2000 to 79% in 2024. The company's 2024 revenue of $5.44 billion and current market capitalization of approximately $43.99 billion represent one of the most successful medical device spin-offs in history.

But here's what really matters: Edwards didn't just iterate on existing technology. They fundamentally reimagined how heart valves could be replaced, turning open-heart surgery requiring a week in the hospital into a procedure that can be done through a catheter in your leg with patients going home the next day. This is the TAVR (Transcatheter Aortic Valve Replacement) revolution, and Edwards owns it.

Our journey through Edwards Lifesciences will take us from that Portland garage through the corporate labyrinths of the 1970s and 80s, into the high-stakes spin-off of 2000, and ultimately to the TAVR breakthrough that redefined an entire medical specialty. We'll examine how a company with such a narrow focus—essentially just heart valves—built one of the most defensible moats in medical devices. And we'll explore what the future holds as Edwards attempts to replicate its TAVR success in mitral and tricuspid valves while fending off increasingly aggressive competition.

This is not just a story about medical innovation. It's about market creation, clinical evidence as competitive advantage, and how sometimes the best business strategy is to solve a problem so completely that you define the entire category. Let's dive in.

II. The Founding Story: Lowell Edwards & Dr. Starr (1958–1960s)

The scene opens in 1958 Portland, Oregon. Lowell Edwards, a 61-year-old retired engineer who had spent his career designing hydraulic systems and fuel pumps for aircraft, sits across from Dr. Albert Starr, a 32-year-old cardiac surgeon at the University of Oregon Medical School. Edwards has been working alone in his garage for months, convinced he can build an artificial heart. Starr, who has been losing patient after patient to mitral valve disease, listens with a mixture of skepticism and desperate hope.

"I don't think the artificial heart is feasible," Starr reportedly told Edwards during that first meeting. "But what about artificial valves?"

This pivotal conversation would redirect the entire trajectory of cardiac medicine. Edwards had approached multiple surgeons with his artificial heart concept, but Starr was the first to engage seriously—and more importantly, to redirect the engineering brilliance toward a more achievable goal. Within days, they formed a partnership that would revolutionize cardiac surgery. The engineering approach was revolutionary in its simplicity. Edwards, working from his home workshop along the Sandy River, approached the problem with a hydraulic engineer's mindset: the heart was simply a pump with four check valves. Edwards recognized that the human heart is also a pump. His initial prototypes resembled industrial valve designs—rigid, mechanical, built to last. But the human body had different requirements than an oil pipeline.

Starr was an instructor in surgery when he met Lowell Edwards in September 1958. The generational divide should have been insurmountable—Edwards at 60, wealthy from his industrial pump patents, Starr at 32, just starting his career. Yet they clicked immediately. Starr has said of this meeting, "He was in his 60s and I was in my 30s, but there was no generation gap between us."

Their working relationship was intense and iterative. For the next two years, Starr and Edwards maintained constant communication. Edwards continued designing and making valve prototypes in his home workshop. Starr implanted the prototypes during experimental animal surgeries. Edwards would craft a new design, Starr would implant it in a dog, they'd observe the failure mode—thrombosis, hemolysis, mechanical failure—and Edwards would return to his workshop.

The breakthrough design was almost comically simple: a rather odd-looking contraption: a free-floating silicone rubber ball enclosed in an acrylic cage. When blood pressure pushed the ball forward, blood flowed through. When pressure reversed, the ball sealed against the valve ring. It looked nothing like nature's elegant tricuspid design, but it worked. On September 21, 1960, everything changed. The patient, a 52-year-old farmer named Philip Amundson, had a scarred and deformed heart valve as a result of childhood rheumatic fever. Dr. Starr successfully implanted the Starr-Edwards "caged ball" valve at the University of Oregon Medical School. The patient, who was near death, would survive and enjoy an active life for another 10 years. Newspapers nationwide reported on the 'Miracle' Heart Surgery Success.

The initial capital investment for Edwards Laboratories was remarkably modest—just $5,000 of Edwards' own money. But the impact was immediate and global. Within a year, Edwards and Starr had developed an aortic valve prosthesis. By 1961, Edwards had established Edwards Laboratories in Santa Ana, California, becoming one of the earliest pioneers in the biomedical high-tech field.

The early results were transformative. Until the development of the Starr-Edwards valve, there were no published reports of patients who had lived longer than 3 months with a prosthetic valve in the mitral position. Suddenly, patients who had been given death sentences were living productive lives. One early patient lived a record 48 years with the implant before requiring a replacement—a testament to the durability of that original design.

This wasn't just a medical breakthrough; it was the birth of an industry. The Starr-Edwards valve proved that mechanical devices could successfully replace human organs, opening the door to hip replacements, pacemakers, and eventually, the entire field of implantable medical devices. As Starr would later write, "In retrospect we had produced a 'black swan'—an occurrence of low predictability and large impact."

The partnership between Edwards and Starr exemplified what would become a recurring theme in medical device innovation: the critical collaboration between engineering and medicine. Neither could have succeeded alone. Edwards brought the mechanical expertise and manufacturing capability; Starr brought the clinical understanding and surgical skill. Together, they didn't just solve a medical problem—they created an entirely new therapeutic category that would eventually grow into a multi-billion dollar industry.

III. Early Growth & Acquisitions Era (1960s–1985)

The transition from garage startup to industrial-scale manufacturer happened with remarkable speed. By 1964, thousands of patients were traveling to Oregon seeking life-saving heart valve surgery. Edwards Laboratories, operating from its Santa Ana facility, was struggling to keep up with global demand. The company that had started with a $5,000 investment and two men's determination was suddenly confronting questions of scale, quality control, and international distribution. In 1966, Edwards Laboratories was purchased by American Hospital Supply Corporation and became American Edwards Laboratories. The acquisition price was not disclosed, but for Lowell Edwards, who retained a consulting role, it represented validation of his vision. American Hospital Supply, a major medical products distributor, provided the capital and infrastructure to scale production globally.

Under American Hospital Supply's ownership, Edwards expanded far beyond heart valves. The company became a magnet for cardiovascular innovation, developing and acquiring technologies that would define cardiac care for decades. The Swan-Ganz catheter, introduced in the early 1970s, revolutionized hemodynamic monitoring in intensive care units. The Fogarty embolectomy catheter became the standard for removing blood clots from peripheral vessels. The Carpentier-Edwards tissue valves, developed in collaboration with French surgeon Alain Carpentier, offered an alternative to mechanical valves that didn't require lifelong anticoagulation.

By the late 1970s, American Edwards had become the undisputed leader in heart valve replacement, commanding over 50% of the global market. The company's products were being implanted in over 100,000 patients annually. Revenue grew from approximately $10 million in 1970 to over $200 million by 1984.

Then, in 1985, American Edwards was acquired by Baxter International Inc. This second acquisition, valued at approximately $400 million, represented another strategic shift. Baxter, one of the world's largest medical products companies, saw Edwards as a crown jewel in its cardiovascular portfolio. The integration into Baxter would provide even greater resources for R&D and global expansion, but it would also begin a 15-year period where Edwards' entrepreneurial culture would increasingly clash with the bureaucracy of a massive conglomerate.

The product innovations during this era established patterns that would define Edwards for decades: physician-inventor partnerships, clinical evidence as competitive advantage, and premium pricing justified by superior outcomes. The company wasn't just selling devices; it was building an ecosystem of surgical training, clinical support, and continuous innovation that made switching costs prohibitively high for hospitals.

IV. The Baxter Years: Building Under a Conglomerate (1985–2000)

Life inside Baxter International was both a blessing and a curse for Edwards. On one hand, Baxter's vast resources enabled aggressive R&D investment and global expansion. On the other, Edwards found itself competing for attention and resources with dozens of other Baxter divisions, from IV solutions to renal care products. The numbers tell a story of both growth and frustration. Through its leading brands including Bentley, Carpentier-Edwards, Cosgrove-Edwards, Fogarty, Research Medical, Starr-Edwards and Swan-Ganz, the Edwards division had sales of nearly one billion dollars annually by the late 1990s. This represented spectacular growth from the $200 million level of the mid-1980s, but within Baxter's sprawling $5.7 billion empire, Edwards remained a relatively small piece.

Baxter alumni groomed by CEO Vernon Loucks included Mike Mussallem of Edwards Lifesciences Corp, who would later become Edwards' founding CEO after the spin-off. Mussallem joined Edwards in 1979 and quickly rose through the ranks, developing a reputation as someone who understood both the technical and commercial aspects of the heart valve business.

The Baxter years saw critical technological developments that would position Edwards for future success. The company invested heavily in tissue valve technology, recognizing that many patients—particularly elderly ones—preferred valves that didn't require lifelong anticoagulation therapy, even if they might need replacement after 10-15 years. The Carpentier-Edwards PERIMOUNT valve, introduced in the early 1990s, became the gold standard for surgical tissue valves, a position it maintains today.

But perhaps the most significant development during the Baxter era was happening quietly in R&D labs: the early work on transcatheter valve technology. Engineers and physicians within Edwards began asking a radical question: What if we could replace a heart valve without opening the chest? The technology didn't exist yet, but the vision was taking shape.

By the late 1990s, tensions were mounting. Edwards executives felt constrained by Baxter's corporate structure and capital allocation priorities. Baxter management, facing pressure from Wall Street to focus on higher-margin businesses, began questioning whether a heart valve business belonged in their portfolio. The stage was set for one of the most successful spin-offs in medical device history.

V. The Spin-Off & Independence (2000)

The boardroom at Baxter's Deerfield headquarters was tense in late 1999. Mike Mussallem, who had been running Edwards as Group Vice President since 1994, was making his final pitch. "We either need to invest a lot in this business or exit," he told the board. The Edwards division was Baxter's poorest-performing business in the 1990s, while cardiovascular competitors like Medtronic, Guidant, Boston Scientific and St. Jude were excelling.

But success wasn't a sure thing for Edwards Lifesciences when it spun out of Baxter in 2000. "The securities analysts didn't love us, let's put it that way," Mussallem would later recall. The spin-off, finalized on March 31, 2000, took the form of a tax-free dividend of Edwards Lifesciences common stock to Baxter shareholders. Baxter shareholders received one share of Edwards Lifesciences stock for each five shares of Baxter stock they owned on March 29.

In early 2000, the company began trading on the New York Stock Exchange under the symbol "EW." Edwards started with $804 million in sales in 2000, a far cry from the multi-billion dollar business it would become. For the first few years as an independent company, Edwards divested products and got smaller as it searched for the best path forward.

The early independence years were marked by strategic soul-searching. They considered peripheral vascular diseases, atrial fibrillation, transmyocardial revascularization and even becoming a biotech focused on angiogenesis to grow new coronary arteries. But ultimately, they realized they should stay close to home with structural heart.

Post-spin arbitration and disputes with Baxter created additional headaches. The companies fought over pension obligations, intellectual property rights, and transition service agreements. Edwards had to quickly build capabilities that had previously been provided by Baxter—everything from IT systems to regulatory affairs to international distribution networks.

"When you analyze it — and it didn't take a lot of analyzing — what [we were] missing was innovation," Mussallem said. Well before the spinoff, Mussallem started studying what separated the best innovators from the worst. What he learned from Stanford Biodesign's focused approach to innovation and others would influence the course he and his team set for Edwards.

The transformation began immediately. Edwards established a clear strategic focus: become the global leader in heart valve disease and critical care technologies. They would compete not on breadth but on depth, not on being a diversified medical device company but on owning specific disease states. This clarity of purpose would prove crucial when, just four years later, Edwards would make the acquisition that would define its future.

VI. The TAVR Revolution: Sapien Changes Everything (2007–2019)

The acquisition that would change everything happened quietly in 2004. Edwards paid $125 million for Percutaneous Valve Technologies (PVT), a small Israeli startup developing a radical concept: a heart valve that could be delivered through a catheter. The technology seemed impossibly ambitious—how could you compress a functional heart valve into a catheter, snake it through blood vessels, and have it work perfectly once deployed?

But Mike Mussallem and his team recognized something the market didn't: this wasn't just another product; it was a platform that could transform an entire medical specialty. The bet was enormous—Edwards would ultimately invest over $1 billion in clinical trials and development before seeing meaningful revenue.

The SAPIEN family of transcatheter heart valves have treated hundreds of thousands of patients worldwide since 2007, when the SAPIEN valve was first commercially approved in Europe. The European launch provided crucial real-world data and allowed Edwards to refine the technology before attempting the more rigorous U.S. regulatory process.

The PARTNER Trial would become one of the most significant clinical studies in cardiovascular medicine history. The first of the TAVR randomized clinical trials, the Edwards sponsored multi-center PARTNER trial tested TAVR for the treatment of severe symptomatic aortic valve stenosis and included a prohibitive surgical risk cohort (STS score >15% or not surgical candidates; cohort B) and a high risk (STS score >10%; cohort A) cohort. Cohort B was published first and randomized 358 patients to TAVR with the Sapien balloon expandable device vs. medical therapy (including balloon angioplasty). The results were striking. The treatment group had an all-cause death rate at 1-year of 30.7% vs. 50.7% in the control arm.

The numbers were so dramatic they seemed almost unbelievable: a 20% absolute reduction in mortality, a number-needed-to-treat of just 5 to save one life. For context, most breakthrough cardiovascular therapies are celebrated for single-digit improvements in mortality.

On November 2, 2011, Edwards received approval from the United States Food and Drug Administration (FDA) for the transfemoral delivery of the Edwards SAPIEN transcatheter aortic heart valve for the treatment of inoperable patients with severe symptomatic aortic stenosis. This is the first U.S. commercial approval for a transcatheter device enabling aortic valve replacement without the need for open-heart surgery.

The initial FDA approval was deliberately narrow—only for inoperable patients via transfemoral access. But Edwards had a methodical expansion strategy. High-risk patients were approved in 2012. Intermediate-risk patients followed. Then came the coup de grâce: The SAPIEN 3 TAVR's low-risk approval was based on data from the landmark PARTNER 3 Trial, an independently evaluated, randomized clinical trial comparing outcomes between TAVR and open-heart surgery. TAVR with the SAPIEN 3 system achieved superiority, with a 46 percent reduction in the event rate for the primary endpoint of the trial, which was a composite of all-cause mortality, all stroke and rehospitalization at one year.

On August 16, 2019, Edwards announced U.S. Food and Drug Administration (FDA) approval to expand use of the Edwards SAPIEN 3 and SAPIEN 3 Ultra transcatheter heart valve systems to the treatment of severe, symptomatic aortic stenosis (AS) patients who are determined to be at low risk of open-heart surgery.

This wasn't just regulatory creep—it was a complete paradigm shift. TAVR had gone from a last-ditch option for dying patients to the preferred treatment for the majority of aortic stenosis patients. The market expanded from perhaps 5,000 patients annually to over 100,000 in the U.S. alone.

The business model was as elegant as the technology. TAVR procedures commanded premium pricing—approximately $30,000 per valve—justified by dramatic clinical benefits and healthcare system savings from shorter hospital stays. Edwards built an ecosystem of physician training, proctoring, and clinical support that created enormous switching costs. Once a hospital invested in building a TAVR program, they rarely switched vendors.

By 2019, TAVR had become a multi-billion dollar business for Edwards, growing at 15-20% annually even as it reached massive scale. The company that had struggled as Baxter's worst-performing division had created one of the most successful medical device franchises in history.

VII. Innovation Portfolio Expansion (2010s–Present)

While TAVR dominated headlines and earnings calls, Edwards quietly pursued a broader strategy: replicate the TAVR playbook across other structural heart diseases. The mitral and tricuspid valves presented even greater technical challenges than the aortic valve—complex anatomies, delicate structures, and heterogeneous disease patterns. But the potential market was equally massive. In 2017, Edwards acquired Harpoon Medical of Baltimore, Maryland for $100 million. Harpoon, founded in 2013, developed a minimally invasive heart surgery product for mitral valve repair to treat degenerative mitral regurgitation. Under the terms of the merger agreement, Edwards paid $100 million in cash for Harpoon at closing on Dec. 1. In addition, there is the potential for up to $150 million in pre-specified milestone-driven payments over the next 10 years.

The Harpoon acquisition exemplified Edwards' disciplined approach to portfolio expansion. Rather than attempting to build everything internally, they would scout promising technologies, make structured investments with acquisition options, and bring them in-house once clinical feasibility was proven. In 2024, Edwards announced it would acquire Innovalve Bio Medical for approximately $300 million, and JenaValve Technology and Endotronix for $1.2 billion. The aggregate upfront purchase price for these strategic investments is approximately $1.2 billion. JenaValve is focused on transcatheter treatment for aortic regurgitation, with Edwards anticipating FDA approval of the JenaValve Trilogy THV system in late 2025. Meanwhile, Endotronix, maker of an implantable pulmonary artery pressure sensor for heart failure, received FDA approval for its Cordella sensor in June 2024.

The strategic acquisitions weren't just about adding products—they were about building platforms. Each acquisition brought unique technology that could be leveraged across Edwards' entire portfolio. The PASCAL system for mitral and tricuspid repair, developed through internal R&D and clinical partnerships, became another billion-dollar franchise.

But perhaps the most strategic move was Edwards' decision to divest its Critical Care business. In June 2024, Edwards sold its critical care portfolio to BD (Becton, Dickinson and Company) for $4.2 billion in cash, highlighting its plan to double down on its commitment to new structural heart technologies. The divestiture represented a fundamental strategic shift: Edwards would be purely a structural heart company, abandoning the diversification that had characterized its Baxter years.

The innovation portfolio expansion strategy reflects a sophisticated understanding of medical device economics. By focusing exclusively on structural heart, Edwards can maintain R&D intensity of 15-17% of sales—nearly double the industry average. This concentrated investment creates a virtuous cycle: superior clinical outcomes justify premium pricing, which funds more R&D, which produces better outcomes.

VIII. Modern Era & Market Position (2020–Today)

The COVID-19 pandemic initially devastated Edwards' business. TAVR procedures, considered elective in many cases, plummeted 70% in April 2020. Hospitals postponed all non-emergency cardiac procedures. The stock fell from $240 to $156 in a matter of weeks.

But Edwards demonstrated remarkable resilience. By focusing on medically necessary procedures, maintaining supply chain continuity, and preparing for recovery, the company emerged stronger. The healthcare environment gradually improved, and Edwards grew 8 percent in 2022, even while continuing to aggressively invest during this transient COVID environment, positioning the company for strong growth and leadership in a new era of structural heart and critical care innovation.

The recovery validated Edwards' strategic focus. Looking ahead to 2022, the company planned for a gradual COVID recovery with growth across all major regions and no significant impact from new variants. The pandemic accelerated certain trends—telemedicine adoption, focus on structural heart procedures, emphasis on healthcare efficiency—that ultimately benefited Edwards' business model.

Bernard J. Zovighian became CEO and joined the Board of Directors of Edwards Lifesciences in May 2023, after serving as the company's president. The transition from Mike Mussallem, who had led Edwards since its 2000 spin-off, was carefully orchestrated over several years. Zovighian joined Edwards Lifesciences in January 2015 as vice president and general manager of the Surgical Structural Heart business, and later became corporate vice president responsible for the company's Transcatheter Mitral and Tricuspid Therapies (TMTT) business in January 2018, establishing a global organization focused on developing a portfolio of therapies designed to change the standard of care for mitral and tricuspid patients.

"One of Mike Mussallem's greatest strengths is his ability to foster innovation," Edwards CEO Bernard Zovighian said, noting how his predecessor's vision was to pioneer big innovations and breakthrough technologies, underpinned by high-quality science. Zovighian inherited not just a company but a philosophy: patient-focused innovation, clinical evidence as competitive advantage, and the courage to create entirely new markets.

The competitive landscape has intensified dramatically. Led by the Sapien 3 Ultra Resilia balloon-expandable TAVR system, Edwards dominates the TAVR market, controlling about 60% worldwide and more than 70% in the US, while Medtronic is the number two TAVR competitor with about 28% worldwide and 24% in the US. But new challengers are emerging. Abbott rolled out Navitor, the successor to its Portico TAVR device, in Europe in 2022 and launched it in the US in 2023. Abbott only controls about 2% of the US TAVR market and 4% of the market worldwide, but that represents rapid progress since the company first launched the self-expanding Portico TAVR system in the US in 2021.

"In our 2028 assumptions, we already assume some minor share loss, which is going to be automatic with more competitors coming. But we have been dealing with competitors for many years in Europe, and we are the global leader and by far the preferred TAVR technology," Zovighian said at the J.P. Morgan Healthcare Conference in 2024.

The competition isn't just about market share—it's about expanding the entire market. According to Jefferies Equity Research, the worldwide transcatheter aortic valve replacement (TAVR) market will be worth nearly $7 billion annually by the end of 2024, up from $4.6 billion in 2019, and Jefferies expects the market to grow around 11% annually over the next three years. This growth creates room for multiple winners, even as Edwards faces share erosion.

Manufacturing excellence has become a critical differentiator. Edwards operates facilities in California, Utah, Puerto Rico, Ireland, and Singapore, with each location specializing in specific product lines. The company's ability to maintain quality while scaling production—particularly for the complex tissue valves that require biological materials—represents a significant competitive moat.

Geographic expansion continues to drive growth. While the U.S. remains Edwards' largest market, representing approximately 60% of revenue, international expansion offers substantial opportunity. Japan's approval of TAVR for low-risk patients, China's growing healthcare infrastructure, and emerging markets adoption all represent multi-year growth drivers.

But perhaps the most significant development in Edwards' modern era came in 2024. The U.S. Food and Drug Administration approved Edwards' transcatheter aortic valve replacement (TAVR) therapy, the SAPIEN 3 platform, for severe aortic stenosis (AS) patients without symptoms, marking the first FDA approval for transcatheter aortic valve replacement (TAVR) in asymptomatic AS patients.

This approval fundamentally changes the addressable market for TAVR. "These results shatter 60 years of ingrained belief on the treatment for severe aortic stenosis, with guidelines that currently recommend 'watchful waiting' for intervention until symptoms develop," said Philippe Genereux, MD. On the company's first-quarter earnings call, CEO Bernard Zovighian said that expanding Edwards' TAVR portfolio into asymptomatic patients represented a "multi-year growth opportunity," which would balloon as treatment guidelines and physician perspectives begin to evolve in the U.S. and globally.

The asymptomatic indication isn't just about volume—it's about transforming the entire treatment paradigm. Instead of waiting for patients to deteriorate, physicians can now intervene earlier, potentially preventing hospitalizations and improving long-term outcomes. This shift from reactive to proactive treatment represents the kind of market-creating innovation that has defined Edwards since the Starr-Edwards valve.

IX. Playbook: Business & Innovation Lessons

The Edwards Lifesciences story offers a masterclass in medical device innovation and market creation. Several key lessons emerge from their journey from garage startup to $44 billion market leader:

The Power of Clinical Evidence

Edwards doesn't just develop products; they invest billions in proving their superiority through rigorous clinical trials. The PARTNER Trial for TAVR involved over 3,000 patients and cost hundreds of millions of dollars. This commitment to evidence creates an almost unassailable competitive moat—competitors must not only match the technology but also the depth and breadth of clinical data.

The company's approach to clinical evidence goes beyond regulatory requirements. They conduct post-market surveillance studies, real-world evidence collection, and long-term durability assessments that continuously reinforce their market position. When a physician chooses Edwards, they're not just selecting a device—they're buying into decades of validated outcomes.

Building Category-Creating Products

TAVR wasn't an iteration; it was a revolution. Edwards recognized that true value creation comes not from incremental improvements but from fundamentally reimagining treatment paradigms. They transformed a week-long hospital stay with open-heart surgery into an outpatient procedure. This wasn't just a new product—it was a new market worth billions.

The lesson extends beyond TAVR. Edwards' approach to mitral and tricuspid therapies follows the same playbook: identify massive unmet needs, develop transformative solutions, and create entirely new treatment categories. They don't compete in existing markets; they create new ones.

Physician Partnerships as Competitive Advantage

From Lowell Edwards and Albert Starr to today's clinical investigators, Edwards has consistently recognized that medical device innovation requires deep physician collaboration. The company doesn't just consult with physicians; they make them partners in innovation.

Edwards' physician training programs, proctoring systems, and ongoing clinical support create switching costs that go beyond economics. Once a hospital builds a TAVR program with Edwards, the institutional knowledge, relationships, and trust become nearly impossible to replicate. This ecosystem approach turns customers into partners.

Capital Allocation Discipline

Edwards' decision to divest its Critical Care business for $4.2 billion in 2024 exemplifies their capital allocation discipline. Rather than pursuing diversification, they chose focus. The proceeds fund R&D in structural heart, where they have clear competitive advantages and market leadership.

Their acquisition strategy shows similar discipline. They don't buy revenue; they buy technology that fits their platform. The Harpoon, JenaValve, and Endotronix acquisitions each brought specific capabilities that enhance Edwards' structural heart franchise. They walk away from deals that don't meet their strategic criteria, regardless of market pressure.

R&D Intensity as a Moat

Maintaining R&D spending at 15-17% of sales—nearly double the industry average—requires conviction and discipline. This investment intensity creates a virtuous cycle: superior products justify premium pricing, which funds more R&D, which produces better outcomes. Competitors face a difficult choice: match Edwards' R&D spending and sacrifice profitability, or accept technological inferiority.

Regulatory Excellence

Edwards has mastered the complex dance of global regulatory approval. They design clinical trials that satisfy multiple regulatory bodies simultaneously, enabling faster global rollout. Their regulatory affairs team doesn't just ensure compliance; they shape regulatory pathways for entirely new device categories.

The FDA approval for asymptomatic patients exemplifies this capability. Edwards didn't just meet existing regulatory requirements; they worked with FDA to establish new ones for an indication that had never been approved before.

Premium Pricing Through Value Demonstration

Edwards commands premium prices—TAVR valves cost approximately $30,000—by demonstrating clear economic value. Shorter hospital stays, fewer complications, and better outcomes justify the price premium. They sell to the entire healthcare system, not just to purchasing departments.

This value-based pricing strategy requires sophisticated health economics modeling, extensive outcome tracking, and continuous communication with payers. Edwards doesn't compete on price; they compete on total system value.

X. Analysis & Investment Case

TAM Expansion: The Structural Heart Opportunity

The total addressable market for structural heart devices continues to expand dramatically. The shift from surgical to transcatheter procedures alone doubles the treatable population—elderly patients who couldn't survive surgery can now be treated. The asymptomatic indication adds another layer of growth, potentially tripling the addressable patient population over the next decade.

Demographics provide a powerful tailwind. The global population over 65 will double by 2050. Aortic stenosis prevalence increases exponentially with age—affecting 2% of people over 65 but 10% over 85. This demographic tsunami ensures decades of market growth regardless of competitive dynamics.

Geographic expansion multiplies these opportunities. Current TAVR penetration in the U.S. approaches 70% of eligible patients, but Europe remains under 50%, and Asia-Pacific under 20%. As healthcare systems develop and reimbursement expands, Edwards has multiple decade-long growth runways.

Competitive Moats

Edwards' competitive advantages compound over time:

- Clinical Evidence Moat: Thousands of patients in dozens of trials create an evidence base competitors can't quickly replicate

- Physician Loyalty: Decades of partnership create relationships that transcend commercial transactions

- Manufacturing Complexity: Tissue valve production requires biological expertise, quality systems, and scale that take years to develop

- Regulatory Expertise: First-mover advantage in new indications creates multi-year leads

- Innovation Pipeline: 15-17% R&D spending ensures continuous technology leadership

These moats reinforce each other. Clinical evidence drives physician adoption, which funds R&D, which produces innovation, which generates more evidence.

Bear Case Considerations

Several risks merit consideration:

Competitive Intensification: Abbott, Boston Scientific, and others are investing aggressively in TAVR. While Edwards maintains technology leadership, margin pressure seems inevitable as competition increases.

Reimbursement Pressure: Healthcare systems globally face budget constraints. While TAVR's value proposition remains strong, pricing pressure could accelerate, particularly in Europe and emerging markets.

Technology Disruption: New technologies—bioresorbable valves, regenerative approaches, pharmaceutical interventions—could eventually disrupt the mechanical/tissue valve paradigm.

Execution Risk: The transition to new leadership, while smooth so far, introduces uncertainty. Maintaining Edwards' innovation culture while scaling globally presents ongoing challenges.

Market Saturation: In developed markets, TAVR penetration approaches natural limits. While indication expansion provides growth, the easy gains from procedure conversion are largely complete.

Bull Case Drivers

The bull case for Edwards rests on multiple expansion opportunities:

Indication Expansion: Asymptomatic and moderate aortic stenosis indications could triple the addressable population. Early intervention becomes standard of care, transforming a late-stage intervention into preventive therapy.

Mitral/Tricuspid Opportunity: These markets remain largely untapped, potentially larger than aortic. Edwards' PASCAL platform and pipeline position them to capture significant share as these markets develop.

International Growth: China, India, and other emerging markets represent decades of growth as healthcare infrastructure develops and middle classes expand.

Innovation Pipeline: Next-generation platforms (SAPIEN X4 and beyond) could extend Edwards' technology leadership and support premium pricing.

Margin Expansion: The divestiture of Critical Care and focus on higher-margin structural heart should drive operating leverage. Gross margins could expand from 77% toward 80%+ over time.

Financial Performance Trajectory

Edwards' financial model demonstrates remarkable consistency:

- Revenue growth: 8-12% annually, sustainable for the next decade

- Gross margins: 77-79%, among the highest in medical devices

- Operating margins: 25-30%, with room for expansion

- Return on invested capital: 15-20%, well above cost of capital

- Free cash flow conversion: 20%+ of revenue

The company's capital-light model—no significant manufacturing capacity additions needed—ensures strong cash generation. The $4.2 billion from the Critical Care divestiture provides flexibility for acquisitions, R&D investment, or shareholder returns.

Valuation considerations suggest Edwards trades at a premium multiple—typically 30-35x forward earnings—reflecting its growth profile, competitive position, and execution track record. While not cheap, the multiple seems justified given the company's positioning in secularly growing markets with high barriers to entry.

XI. Epilogue & Future Outlook

Looking ahead, Edwards Lifesciences stands at an inflection point. The approval for asymptomatic patients represents not an end but a beginning—the start of a transformation in how cardiovascular disease is treated globally. Instead of waiting for patients to deteriorate, medicine moves toward prevention and early intervention.

The next frontier involves several parallel developments. Artificial intelligence and machine learning will increasingly guide patient selection and procedure planning. Imaging advances will enable better pre-procedure modeling and post-procedure monitoring. Robot-assisted procedures could further reduce invasiveness and improve outcomes.

But perhaps the most profound shift will be in treatment philosophy. As Edwards' CEO Bernard Zovighian noted, the company is "leading Edwards into a new era of groundbreaking structural heart innovation." This isn't just about new products—it's about reimagining the entire patient journey from diagnosis through long-term management.

The competitive landscape will undoubtedly intensify. Abbott, Medtronic, Boston Scientific, and others will continue to invest aggressively. New entrants from China and other markets will emerge. Price competition will increase, particularly in mature markets. But Edwards' response remains consistent: innovate, generate evidence, and create new markets rather than fighting over existing ones.

Success in 10 years would mean several things: TAVR becomes the default treatment for all aortic stenosis, regardless of symptoms or risk level. Mitral and tricuspid interventions achieve similar adoption curves. Structural heart procedures move from specialized centers to community hospitals. Most importantly, millions of patients who would have died from or lived diminished lives due to valve disease instead live full, active lives.

The key lessons from Edwards' journey transcend medical devices. True value creation comes not from incremental improvement but from reimagining entire categories. Competitive advantages compound when built on clinical evidence, physician partnerships, and patient outcomes. Focus beats diversification when you're creating new markets. And sometimes, the best business strategy is simply to solve a problem so completely that you define the solution.

From Lowell Edwards' Portland garage to a $44 billion global leader, Edwards Lifesciences exemplifies how vision, persistence, and patient focus can transform not just a company but an entire field of medicine. The artificial heart that Edwards originally envisioned may never have materialized, but the impact on cardiac care has been far more profound—not replacing the heart but restoring it, one valve at a time.

As we look to the future, Edwards Lifesciences remains what it has always been: an innovation company disguised as a medical device manufacturer, a clinical evidence organization that happens to make products, and ultimately, a company whose true product isn't valves or catheters but extended and improved human life. In an industry often criticized for incremental innovation and excessive focus on financial returns, Edwards stands as proof that doing well and doing good need not be mutually exclusive.

The story that began with two men believing they could build a better valve continues today with 15,000 employees worldwide united by a simple credo: helping patients is our life's work. For investors, physicians, and most importantly patients, the next chapter of the Edwards Lifesciences story promises to be even more transformative than the remarkable journey so far.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube