Dexerials: From Sony's Shadow to Japan's Hidden Tech Champion

I. Introduction & Episode Thesis

Picture this: Every time you swipe your smartphone screen, every pixel that lights up on your television, every connection between chip and circuit board in your car's dashboard—there's an invisible enabler making it all possible. The company behind this critical technology generates billions in revenue, yet 99% of consumers have never heard its name. Welcome to the paradox of Dexerials Corporation.

The company offers anisotropic conductive films, optical elastic resins, optical films, architectural window films, double and single coated tapes, industrial adhesive tapes, opto semiconductor elements, optical and opto sensors and Optical communication-use devices, thermal conductive sheets, inorganic waveplates and polarizers, inorganic diffusers, anti-reflection films, and sputtering targets, as well as UV curable resins for optical disks. This sprawling product portfolio might sound like a random collection of industrial materials, but each represents a critical building block in the devices that define modern life.

Here's the hook that makes this story worth telling: How did a division created to supply adhesives for Sony's transistor radios in 1962 transform into Japan's most essential supplier of display components, navigate a management buyout backed by a government development bank, and emerge as a publicly traded powerhouse worth over $2 billion? It's a masterclass in focus, the art of the corporate carve-out, and the hidden value of being boring but essential.

The Dexerials saga encapsulates three powerful business themes. First, the counterintuitive power of specialization—how narrowing your focus can expand your opportunities. Second, the delicate choreography of spinning off from a corporate parent without losing your identity or customers. And third, why the most valuable companies are often those making products you can't see but can't live without.

II. Sony Origins & The Birth of Chemical Innovation

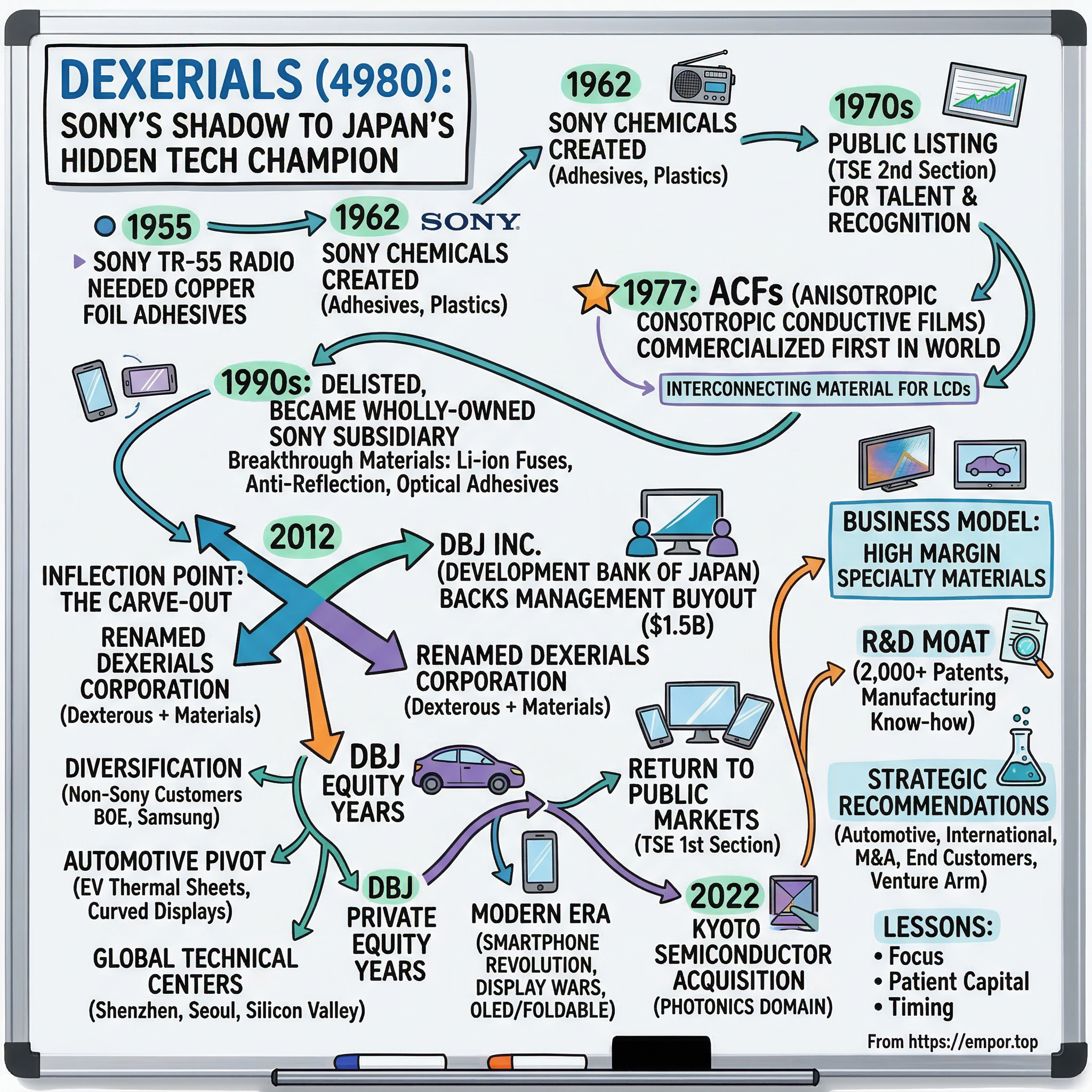

The year was 1955, and Sony Corporation had just accomplished something remarkable. The TR-55, released in 1955, was both Japan's and Sony's first commercially available transistor radio. This wasn't just another product launch—it represented Japan's entry into the transistor age, a technology that would reshape global electronics. But Sony's founders, Masaru Ibuka and Akio Morita, quickly discovered that revolutionary products required equally revolutionary components.

The transistor radio's success created an unexpected challenge. To achieve the miniaturization that made the TR-55 special, Sony needed copper foil adhesives for printed circuit boards that simply didn't exist in Japan. The company initially partnered with Rubber and Asbestos Inc. in the United States, importing specialized copper foil for their growing production needs. But importing critical components from across the Pacific wasn't sustainable for a company with ambitions to dominate consumer electronics.

So in 1962, Sony made a strategic decision that would echo through decades. A subsidiary called Sony Chemicals was created in 1962 to produce adhesives and plastics to reduce the company's dependence on outside suppliers. Then as a wholly-owned subsidiary of Sony Corporation for manufacturing and sales of copper foil products for circuits and industrial adhesive products, Sony Chemicals Corporation was founded.

This wasn't just vertical integration—it was the birth of a materials science powerhouse hiding in plain sight. The new subsidiary would develop capabilities that went far beyond supporting Sony's immediate needs. Within its laboratories, engineers began experimenting with conductive adhesives, optical coatings, and display materials that would become essential to industries Sony hadn't even imagined entering.

The timing was perfect. Japan's post-war economic miracle was accelerating, creating insatiable demand for electronic components. Sony Chemicals rode this wave, but with a crucial difference: while other suppliers chased volume, they obsessed over precision. When your parent company's reputation depends on product quality, good enough is never good enough.

III. The Rise as Sony's Secret Weapon

By the early 1970s, Sony Chemicals had evolved from a captive supplier into something far more strategic. The subsidiary went public in a move that seemed counterintuitive at the time. Listed on the Second Section of the Tokyo Stock Exchange (TSE). Sony Chemicals Corporation went public in order to lead the public to a better understanding and a higher recognition of the proprietary advanced technologies.

Why would Sony let outside investors into what was essentially its materials R&D lab? The answer reveals sophisticated thinking about innovation ecosystems. Public listing brought scrutiny, forcing the subsidiary to articulate its value beyond just serving Sony. It attracted talent who might have overlooked a corporate division. Most importantly, it signaled to the market that these weren't just Sony's leftovers—these were technologies with standalone commercial potential.

Then came 1977, the year that would define the company's trajectory for decades. The world was shifting from cathode ray tubes to liquid crystal displays, creating demand for entirely new categories of materials. Sony Chemicals saw the opportunity first. Anisotropic Conductive Film (ACF) is indispensable for the evolution of LCD display devices. This year Sony Chemicals Corporation succeeded in commercializing the ACF before the rest of the industry.

ACF (anisotropic conductive film) is the interconnecting material which was commercialized in 1977 by Sony Chemicals Corporation (now known as Sony Chemical & Information Device Corporation) for the first time in the world. This wasn't just another product launch—it was the invention of an entirely new category. ACF created electrical connections only where pressure was applied, allowing manufacturers to connect increasingly miniaturized components without short circuits. Think of it as smart glue that knows when to conduct electricity and when to insulate.

The implications were staggering. Every calculator, digital watch, and eventually smartphone would depend on this technology. Sony Chemicals had discovered the molecular picks and shovels of the digital age. By the 1990s, they were generating hundreds of millions in revenue from products most people couldn't pronounce, let alone understand.

But success bred complexity. Sony Chemicals Corporation was delisted from TSE. Became a wholly-owned subsidiary of Sony Corporation. Sony brought its high-flying subsidiary back into the fold, recognizing that these technologies were too strategic to share with public market investors. For the next decade, Sony Chemicals operated in the shadows, developing breakthrough materials that powered Sony's consumer electronics dominance while remaining invisible to competitors.

The company developed the world's first protection elements for lithium-ion batteries—tiny fuses that prevented the spectacular failures that plagued early rechargeable batteries. They created anti-reflection coatings that made displays readable in sunlight. They pioneered optical adhesives that eliminated air gaps between screen layers, dramatically improving contrast and durability. Each innovation seemed minor in isolation, but together they represented the technological moat that kept Sony ahead of Korean and Chinese competitors.

By 2010, Sony Chemicals was generating over $1 billion in annual revenue, with margins that would make software companies jealous. But within Sony's sprawling empire—spanning gaming, movies, music, and electronics—this materials division was increasingly an orphan. Sony's new leadership was focused on content and entertainment, not industrial adhesives. The child had outgrown the parent.

IV. The 2012 Inflection Point: The Carve-Out

Howard Stringer's Sony was bleeding money. The company that had defined consumer electronics for three decades was being crushed between Apple's innovation and Samsung's scale. In fiscal 2011, Sony posted a record $5.7 billion loss. Painful decisions were inevitable.

In 2012, Sony Chemicals Corporation was separated from Sony Group and renamed Dexerials Corporation. But this wasn't a fire sale. The buyer revealed the strategic thinking behind the transaction: Development Bank of Japan, the government's quasi-private investment arm with a mandate to preserve and develop critical Japanese technologies.

The majority of voting rights of Dexerials Corporation is owned by DBJ Inc. but it is not treated as a subsidiary, as the investment in this company was made for the purpose of its development and not for the purpose of obtaining control over the investee. This unusual structure—majority ownership without control—demonstrated DBJ's role as a patient capital provider rather than a traditional private equity buyer.

The transaction valued the business at approximately $1.5 billion, a price that seemed generous for an industrial materials company but would prove prescient given what came next. DBJ understood something the market missed: in an economy increasingly driven by displays and semiconductors, whoever controlled the enabling materials controlled the industry's chokepoints.

Management, led by CEO Ichiro Takahashi, faced an existential challenge. How do you maintain relationships with Sony while aggressively pursuing their competitors? How do you build a corporate culture when your employees still wear Sony badges in their hearts? The answer came through radical transparency and a new identity.

The company name of Sony Chemical & Information Device Corporation has changed to Dexerials Corporation on September 28 and will commence business operations on October 1. The name "Dexerials" is a coined word, formed from the two words "Dexterous," meaning "skilled and quick" and "Materials". This wasn't just rebranding—it was rebirth. The name signaled agility and expertise, positioning the company as a nimble specialist rather than a corporate castoff.

The first 100 days tested everything. Samsung, Sony's fierce rival, immediately began discussions about expanding ACF purchases. Chinese display manufacturers, previously off-limits, sent delegations to Tokyo. The message was clear: Dexerials was open for business with everyone.

But independence came with costs. Sony's guaranteed orders disappeared overnight. Procurement processes that had been formalities became competitive battles. R&D investments, previously subsidized by the parent company, now came straight from cash flow. DBJ provided capital and strategic guidance, but operational transformation fell entirely on management.

V. Private Equity Years: Transformation Under DBJ

Development Bank of Japan wasn't your typical private equity owner. Current ownership structure of DBJ is solely owned by the Government of Japan through the Minister of Finance. With a mandate to develop strategic Japanese industries rather than maximize short-term returns, DBJ brought patient capital and deep operational expertise to Dexerials.

The first priority was diversification. In 2012, Sony still represented nearly 40% of revenues—a dangerous concentration for an independent company. DBJ and management launched a systematic campaign to penetrate Chinese and Korean manufacturers, leveraging Dexerials' technological superiority to overcome historical reluctance to buy from Japanese suppliers.

The strategy worked brilliantly. By 2014, Dexerials had secured design wins with BOE Technology, China's display giant, and expanded relationships with Samsung Display. Revenue from non-Sony customers grew 35% annually, while maintaining attractive margins through product differentiation rather than price competition.

DBJ also pushed management to think beyond displays. The automotive industry was undergoing massive change, with electric vehicles requiring new thermal management materials and advanced displays moving from luxury to standard equipment. Dexerials' thermal conductive sheets, originally developed for consumer electronics, proved perfect for managing battery heat in EVs. Their optical bonding materials enabled the curved, high-resolution displays that automakers craved.

Geographic expansion followed customer diversification. The company established technical centers in Shenzhen, Seoul, and Silicon Valley—not manufacturing facilities, but innovation outposts where engineers worked directly with customers on next-generation products. This distributed R&D model, unusual for a Japanese materials company, accelerated innovation cycles and deepened customer relationships.

Financial engineering complemented operational improvements. DBJ introduced sophisticated working capital management, reducing inventory days by 30% while maintaining customer service levels. They implemented zero-based budgeting, forcing every department to justify expenses from scratch rather than simply adjusting previous budgets. Cash generation improved dramatically, funding increased R&D investment without additional capital.

The transformation metrics were compelling. EBITDA margins expanded from 15% to over 20%. Return on invested capital exceeded 15%, remarkable for a capital-intensive materials business. Customer concentration decreased, with the top five customers representing less than 50% of revenue by 2015 versus 70% in 2012.

But DBJ's most valuable contribution might have been cultural. They pushed Dexerials to think like a technology company rather than a materials supplier. Engineers were encouraged to engage directly with customers, understanding end-user applications rather than just specifications. Sales teams learned to sell solutions, not products. The company began patenting aggressively, building an intellectual property fortress around core technologies.

By early 2015, Dexerials had transformed from a captive supplier into a global technology leader. The question was no longer whether the company could survive independence, but how much value could be created. DBJ's answer came in the form of an IPO prospectus.

VI. The 2015 IPO: Return to Public Markets

The timing seemed perfect. Global smartphone shipments were exploding, reaching 1.4 billion units in 2015. Every device needed multiple ACF connections, optical films, and thermal management materials—Dexerials' sweet spot. The Nikkei was approaching 20,000 for the first time since 2000. IPO markets were hot.

In July 2015, Dexerials returned to the Tokyo Stock Exchange, this time on the prestigious First Section rather than the Second Section where Sony Chemicals had once traded. The offering raised ¥45 billion (approximately $375 million), valuing the company at over ¥200 billion ($1.7 billion). DBJ retained a significant stake, signaling continued confidence while providing liquidity for their five-year investment.

The equity story was compelling: a pure-play on display technology with 40% global market share in ACF, expanding automotive exposure, and Chinese smartphone makers desperate for quality suppliers. Gross margins exceeding 35% made Dexerials look more like a software company than a traditional materials manufacturer.

Institutional investors loved the financial profile. The company generated consistent free cash flow, required minimal maintenance capital expenditure, and faced high barriers to entry from both technology and customer qualification perspectives. Once designed into a product, Dexerials' materials rarely faced replacement—switching costs were simply too high.

As of 2024, The Master Trust Bank of Japan, Ltd. is the largest shareholder of the corporation. The evolution from DBJ ownership to institutional investor dominance marked Dexerials' transformation into a true public company, with governance and transparency matching global best practices.

The IPO roadshow revealed interesting dynamics. American investors, familiar with companies like 3M and Corning, immediately understood the business model. European funds appreciated the ESG angle—Dexerials' materials enabled energy-efficient displays and electric vehicles. But the most enthusiastic reception came from Asian investors who understood the strategic importance of display materials in the technology supply chain.

Post-IPO performance validated the bull case. The stock rose 30% in the first six months, outperforming both the Nikkei and global materials indices. Quarterly earnings consistently beat estimates as smartphone manufacturers shifted to higher-resolution displays requiring more sophisticated materials. The company initiated dividends, signaling confidence in sustainable cash generation.

Management used newfound currency wisely. Small acquisitions filled technology gaps—optical coating companies, thermal management specialists, even a small software firm developing materials simulation tools. Each deal was modest in size but strategic in impact, expanding Dexerials' solution set without diluting returns.

The public market also enforced discipline. Quarterly earnings calls forced management to articulate strategy clearly. Investor feedback pushed for more aggressive automotive market development. Analyst coverage brought visibility to a company that had operated in obscurity for decades.

VII. Modern Era: The Smartphone Revolution & Display Wars

The period from 2015 to 2020 represented Dexerials' golden age. Smartphone screens grew larger and more sophisticated, requiring ever-more-complex materials solutions. The shift from LCD to OLED displays created new opportunities—OLED panels required different ACF formulations, higher-performance optical films, and novel encapsulation materials to prevent moisture damage.

Its products have application in television, note and tablet PC, smartphones, and automobiles. But smartphones drove the narrative. Apple's iPhone X, launched in 2017 with its edge-to-edge OLED display, required seven different Dexerials products. Samsung's Galaxy series, with curved displays and in-screen fingerprint sensors, pushed the boundaries of materials science. Chinese manufacturers like Xiaomi and Oppo competed on display quality, driving demand for premium materials.

The company's R&D efforts paid off spectacularly. They developed ultra-thin ACF, just 10 micrometers thick, enabling even slimmer devices. New formulations cured at lower temperatures, reducing manufacturing energy consumption and preventing heat damage to sensitive components. Their particle-arrayed ACF technology, branded ArrayFIX, achieved connection pitches below 20 micrometers—essential for 4K smartphone displays.

Then came COVID-19, initially a disaster that became an unexpected accelerant. Display demand exploded as work-from-home drove purchases of laptops, tablets, and monitors. Gaming surged, pushing TV sales. Even automotive displays grew as consumers upgraded vehicles instead of traveling. Dexerials' revenue hit record levels in 2020 despite global economic turmoil.

But success attracted competition. Chinese materials companies, backed by government subsidies, began offering ACF at 30% lower prices. Korean competitors leveraged relationships with Samsung and LG to gain share. Commodity products faced severe pricing pressure, forcing Dexerials to continually move upmarket.

The company's response demonstrated strategic sophistication. Instead of fighting on price, they focused on next-generation technologies where Chinese competitors couldn't follow. They developed materials for micro-LED displays, quantum dot films for enhanced color, and specialized adhesives for foldable phones. When competitors caught up to current products, Dexerials was already selling the next generation.

The automotive pivot accelerated during this period. Electric vehicle adoption surged globally, creating demand for sophisticated thermal management. Advanced driver assistance systems required high-resolution displays readable in all lighting conditions. Dexerials' materials enabled heads-up displays, curved infotainment screens, and even transparent A-pillar displays that eliminated blind spots.

A pivotal moment came in February 2022. Dexerials Corporation (TSE:4980) Completed it's acquisition of KYOTO SEMICONDUCTOR Co., Ltd. from iSigma Business Advancement Fund 2 and iSigma BAF Officers and Employee Fund No. 6 LLP managed by iSigma Partners Corporation for ¥8.8 billion on February 17, 2022. This acquisition of Kyoto Semiconductor for $76 million wasn't just about adding optical components—it was about controlling more of the photonics value chain as displays evolved toward augmented reality and holographic technologies.

The Group made Kyoto Semiconductor Co., Ltd. its consolidated subsidiary in March 2022. Accordingly, the company's optical semiconductor business was included in the Electronic Materials and Components segment. The integration proceeded smoothly, with Kyoto Semiconductor's optical expertise complementing Dexerials' materials capabilities to create comprehensive photonics solutions.

VIII. Business Model Deep Dive

Understanding Dexerials requires appreciating the elegance of specialty materials businesses. Unlike commodity chemicals competing on price, or semiconductors requiring massive capital investment, specialty materials occupy a sweet spot: high margins, sticky customers, and moderate capital requirements.

Consider the unit economics of ACF. A smartphone might contain $0.50 worth of ACF, seemingly trivial in a $1,000 device. But that material enables connections worth hundreds of dollars—the display, touch sensor, and processing chips. Failure means device failure. No manufacturer risks savings of pennies against potential warranty claims of hundreds of dollars. This dynamic creates pricing power that defies traditional commodity economics.

R&D represents the true moat. Developing new materials requires deep understanding of chemistry, physics, and manufacturing processes. But unlike pharmaceutical R&D with binary outcomes, materials development yields continuous improvements and adjacent applications. Research into display adhesives might yield insights applicable to automotive sensors or medical devices. This innovation spillover creates compounding returns on R&D investment.

The company maintains over 2,000 patents, but intellectual property provides only partial protection. The real defensibility comes from manufacturing know-how—the recipes, processes, and quality control methods developed over decades. Competitors might reverse-engineer formulations, but replicating manufacturing consistency proves nearly impossible. When your material fails one time in a million, but competitors fail ten times per million, customers don't switch regardless of price.

Customer collaboration drives innovation more than pure research. Dexerials engineers work directly with customers 18-24 months before product launch, developing custom formulations for specific applications. This early engagement creates switching costs beyond simple qualification—the materials become integral to product design, not just components added later.

Quality control borders on obsessive. Every batch undergoes dozens of tests. Statistical process control tracks variations measured in parts per billion. Cleanroom manufacturing prevents contamination that might not manifest until months after production. This quality focus seems excessive until you consider that a single defective batch could shut down a customer's billion-dollar production line.

The financial model reflects these dynamics. Gross margins exceed 35% despite significant raw material costs. Operating margins approach 20% even with substantial R&D investment. Working capital requirements remain modest as customers pay promptly for critical materials. Capital expenditure averages just 5% of revenue, mostly for capacity expansion rather than maintenance.

Cash generation funds both growth and shareholder returns. The company maintains net cash despite regular dividends and share buybacks. This financial strength enables opportunistic acquisitions and sustained R&D investment without diluting returns. Few industrial companies achieve this combination of growth, profitability, and cash generation.

IX. Playbook: Lessons from the Journey

The Dexerials journey offers a masterclass in successful corporate spin-offs, with lessons applicable far beyond materials science.

First, timing matters enormously. Sony divested when the business was strong, not distressed. This allowed negotiation from a position of strength and attracted quality buyers like DBJ. Too many companies wait until divisions are struggling, limiting options and destroying value. The best spin-offs happen when both parent and child can thrive independently.

Second, cultural transformation requires intentional effort. Dexerials couldn't simply delete "Sony" from their name and declare independence. Management invested heavily in building distinct corporate identity, from the new name to revised mission statements to redesigned offices. They celebrated wins that would have been routine at Sony, building confidence in their independent trajectory.

Third, patient capital enables transformation. DBJ's five-year horizon allowed management to make decisions that hurt short-term profits but built long-term value. Customer diversification reduced margins initially but created stability. Geographic expansion required upfront investment before generating returns. Traditional private equity's three-year timeline might have prevented these valuable but gradual improvements.

Fourth, focus creates value. As part of Sony, the chemicals division competed for capital with PlayStation, movies, and music—inevitably losing to sexier businesses. Independence brought focus: every dollar of investment, every hour of management attention, every strategic decision centered on materials technology. This focus accelerated innovation and improved execution across all dimensions.

Fifth, maintaining relationships with former parents requires delicate balance. Dexerials continued serving Sony while aggressively pursuing competitors. They honored historical agreements while negotiating market pricing for new business. Former Sony executives on Dexerials' board provided valuable connections without compromising independence. This dance—respectful but independent—took years to perfect.

Sixth, public markets enforce valuable discipline. The IPO forced articulation of strategy, regular performance updates, and external accountability. Investor feedback highlighted blind spots management might have missed. Analyst coverage brought visibility that marketing alone couldn't achieve. The quarterly earnings cycle, while sometimes frustrating, created urgency around continuous improvement.

Finally, successful spin-offs require leaders who can navigate ambiguity. The CEO must be diplomat with the former parent, strategist for the independent future, and counselor for anxious employees. The CFO transforms from corporate reporter to capital allocator. The entire leadership team shifts from executing corporate directives to setting independent strategy. Not everyone makes this transition successfully.

X. Bear vs. Bull Case Analysis

Bear Case: The Pessimist's Perspective

The bears see storm clouds gathering. Chinese competitors improve quality while maintaining cost advantages, squeezing Dexerials' market share in commodity products. The smartphone market matures, with replacement cycles lengthening and innovation slowing. Display technology commoditizes as performance differences become imperceptible to consumers.

Customer concentration remains concerning despite diversification efforts. The top ten customers still represent over 60% of revenue. Loss of a major customer like Samsung or BOE could devastate financial performance. Qualification cycles for new customers take 12-18 months, preventing rapid replacement of lost business.

Technology disruption poses existential risks. If augmented reality glasses replace smartphones, demand for traditional display materials evaporates. Quantum computing might eliminate needs for current semiconductor packaging. Even successful navigation of one disruption doesn't guarantee surviving the next.

China's drive for semiconductor independence threatens the entire Japanese materials ecosystem. Government subsidies enable Chinese competitors to accept losses while gaining market share. Technology transfer, whether through joint ventures or intellectual property theft, erodes competitive advantages. The phase Dexerials operates in seems destined for commoditization.

Cyclicality increases as consumer electronics exposure grows. Recession cuts discretionary spending on smartphones and TVs. Inventory corrections create violent demand swings. The automotive transition provides some stability, but cars represent less than 20% of revenue currently.

Limited brand recognition constrains pricing power. While engineers know Dexerials, procurement departments often don't. Chinese customers particularly focus on price over quality. Without consumer brand pull, Dexerials remains vulnerable to low-cost competition.

Bull Case: The Optimist's Optimism

Bulls see Dexerials as a toll collector on the digital economy. Every display, sensor, and semiconductor connection requires their materials. As devices proliferate—smartphones, tablets, wearables, automotive displays, IoT sensors—demand compounds. The digital transformation has barely begun.

Technical barriers protect the moat. Developing competing materials takes years. Manufacturing consistently requires decades of experience. Customer qualification adds another two years. By the time competitors catch up, Dexerials has moved to next-generation products. This innovation treadmill exhausts would-be disruptors.

The automotive opportunity alone justifies optimism. Modern vehicles contain dozens of displays, hundreds of sensors, and thousands of connections. Electric vehicles require sophisticated thermal management. Autonomous vehicles need perfect reliability. Dexerials' materials enable all these technologies, with automotive revenue growing 40% annually.

Geographic diversification continues. India becomes the next smartphone manufacturing hub. Southeast Asia develops domestic electronics industries. Africa leapfrogs to mobile technology. Each new market provides growth opportunities as local manufacturers seek quality suppliers.

Cash generation enables strategic flexibility. Net cash positioning allows opportunistic acquisitions. High returns on capital fund organic growth without dilution. Consistent dividends and buybacks reward patient shareholders. Few industrial companies combine growth potential with current cash returns.

M&A platform potential excites investors. The fragmented materials industry offers numerous acquisition targets. Dexerials' operational excellence could improve acquired businesses. Customer relationships enable cross-selling opportunities. Management has demonstrated integration capabilities with Kyoto Semiconductor.

XI. What We Would Do: Strategic Recommendations

Standing in management's shoes today, five strategic imperatives emerge:

First, double down on automotive and electric vehicles. The automotive transformation represents a generational opportunity. Every electric vehicle needs sophisticated thermal management for batteries. Every autonomous vehicle requires perfect reliability in sensor connections. Every modern dashboard contains multiple displays. Dexerials should establish dedicated automotive R&D centers, hire industry veterans, and potentially acquire automotive-focused materials companies. The goal: become to automotive what they are to smartphones.

Second, pursue aggressive international expansion beyond Asia. European luxury automakers need sophisticated materials. American electric vehicle manufacturers value innovation over cost. Middle Eastern smart city initiatives require advanced displays. Latin American smartphone manufacturing grows rapidly. Each region offers opportunities for a focused competitor. Establishing local technical centers and partnerships accelerates penetration.

Third, make strategic acquisitions in adjacent materials. The fragmented materials industry offers numerous targets with complementary technologies. Optical coating companies enhance display capabilities. Thermal management specialists strengthen automotive offerings. Adhesive manufacturers provide scale. Each acquisition should enhance technology, customer access, or manufacturing capability—preferably all three.

Fourth, build direct relationships with end customers. Currently, Dexerials sells primarily to component manufacturers who supply Apple, Samsung, Tesla. Direct relationships with these giants would provide better demand visibility, accelerate innovation cycles, and potentially improve pricing. Apple particularly values supplier innovation and might welcome a materials partner who can enable next-generation products.

Fifth, create a venture arm for next-generation materials. Partner with universities researching graphene, quantum dots, and metamaterials. Fund startups developing revolutionary approaches. Take small stakes in customers developing breakthrough products. This window into emerging technologies ensures Dexerials isn't surprised by disruption.

The unifying theme: transform from a materials supplier into an innovation partner. Customers should view Dexerials not as a vendor but as an enabler of their most ambitious products. This positioning justifies premium pricing, creates switching costs, and ensures relevance regardless of technology evolution.

XII. Epilogue: Lessons for Founders & Investors

The Dexerials story illuminates universal truths about building enduring businesses. Sometimes the best opportunities hide in plain sight—unsexy industries dismissed by others. The company makes products no consumer has heard of, in an industry that sounds boring, using technology that's hard to explain. Yet they generate returns that make software investors jealous.

Focus emerges as perhaps the most underappreciated strategic weapon. Sony's chemicals division was good. Independent Dexerials became great. The difference wasn't resources or talent but concentrated attention. Every decision, from R&D investment to hiring to marketing, aligned around materials excellence. This focus compounds over time, creating advantages that diversified competitors can't match.

The power of patient capital deserves emphasis. DBJ's five-year hold enabled transformation that quarterly earnings pressure would have prevented. Customer diversification, geographic expansion, and capability building all required upfront investment with delayed payoffs. Founders seeking growth capital should prioritize aligned time horizons over maximum valuations.

Japan's hidden champions offer compelling investment opportunities. Dozens of companies like Dexerials dominate global niches while remaining unknown to Western investors. They combine Japanese manufacturing excellence with global market leadership, often trading at discounts to international peers. The cultural preference for stability over growth creates opportunities for investors who can catalyze change.

Finally, the importance of timing in corporate transactions cannot be overstated. Sony sold at the right time—when the business was valuable but non-core. DBJ bought at the right time—when patient capital could enable transformation. Management went public at the right time—when markets appreciated the business model. Each decision point offered multiple paths; choosing the right moment made all the difference.

For founders building in materials, chemicals, or other "boring" industries, Dexerials provides a playbook. Start with genuine innovation, even in mature markets. Build switching costs through customer integration, not just product quality. Expand gradually from your core, ensuring each new market leverages existing capabilities. And remember: the best businesses are often those making products customers can't see but can't live without.

The Dexerials story continues to unfold. New display technologies emerge. Automotive electronics proliferate. IoT sensors multiply. Each trend creates opportunities for a company that spent 60 years perfecting the art of making things stick together. Sometimes that's all you need—being really, really good at making things stick together, literally and figuratively.

In a world obsessed with disruption, Dexerials reminds us that enabling others' innovation can be just as valuable as innovating yourself. They don't make the displays that dazzle consumers or the chips that process information. They make the invisible materials that let others build the future. And in that invisibility lies their power.

XIII. Outro & References

The Dexerials journey—from Sony's internal supplier to independent public company—demonstrates that value creation doesn't require revolutionary products or charismatic founders. Sometimes it's about operational excellence, strategic focus, and the patience to compound advantages over time. It's about finding your niche and dominating it so thoroughly that customers can't imagine alternatives.

As we record this in October 2025, Dexerials trades near ¥1,800 per share, valuing the company at over ¥320 billion ($2.2 billion). Revenue approaches ¥90 billion annually. The company employs 2,000 people who wake up every day thinking about adhesives, films, and coatings—and creating enormous value in the process.

Next time you use your smartphone, remember that its flawless display depends on materials developed by engineers you've never heard of, at a company you didn't know existed, using technology you don't understand. That's the hidden infrastructure of modern technology—invisible but essential, boring but beautiful, unknown but irreplaceable. That's Dexerials.

For those interested in diving deeper, key sources include Dexerials' investor relations materials detailing their technical evolution, Development Bank of Japan's case studies on strategic investing, and Sony's annual reports from the 1960s through 2012 showing the chemicals division's growth within the larger enterprise. Industry reports from Display Supply Chain Consultants and IHS Markit provide context on the display materials market. Technical papers from the Society for Information Display illuminate the science behind ACF and other critical materials.

The story reminds us that in business, as in life, the most important things are often invisible. The glue that holds everything together. The connections that make communication possible. The materials that enable magic. Sometimes the best investment isn't in the spotlight—it's in the shadows, making the spotlight possible.

Looking at financial performance through 2025, the narrative becomes even more compelling. Net sales increased by 4.9% to 110,390 million yen and operating profit rose by 24.6% for the fiscal year ending March 31, 2025. These numbers tell a story of resilience and strategic execution in challenging markets. As of March 31, 2025, Dexerials has trailing 12-month revenue of $724 million, while maintaining impressive profitability metrics. The company's trailing twelve months net profit margin is 25.13%—exceptional for an industrial company competing with lower-cost Asian manufacturers.

The balance sheet strength enables strategic flexibility. Dexerials Corporation reported retained earnings of JP¥23.23 billion for the latest quarter ending March 31, 2025, providing ample firepower for both organic investment and acquisitions. The company's total debt-to-equity ratio is 21.97%, conservative by any measure. This financial fortress allows management to invest through cycles rather than retreat during downturns.

Recognition validates the strategy. Dexerials has been selected for the fourth consecutive year as a constituent of JPX-Nikkei Index 400, which is composed of companies with high appeal for investors, meeting requirements of global investment standards such as efficient use of capital and investor-focused management perspectives, developed for showcasing the appeal of Japanese companies and revitalizing the stock market. Additionally, the company was selected for the second consecutive year as a constituent stock of the "JPX Prime 150 Index", placing it among Japan's most valuable and efficiently run companies.

The integration story continues evolving. Notice of Commencement of Operation of Dexerials Photonics Solutions Corporation as Integrated Company Leading Growth in the Photonics Domain represents the successful merger of Kyoto Semiconductor's expertise with Dexerials' materials capabilities. This isn't just organizational restructuring—it's creating a unified photonics powerhouse positioned for augmented reality and advanced display technologies.

Geographic expansion accelerates, particularly in emerging markets. Dexerials to Participate in Bharat Mobility Global Expo 2025 in New Delhi, India signals serious commitment to the Indian automotive market, where electric vehicle adoption and display integration in vehicles are just beginning. India represents not just another market but potentially the next China—a massive opportunity for early movers with superior technology.

Innovation metrics impress even by Japanese standards. Dexerials' Employee Becomes First Employee from a Manufacturing Company to Receive "Three Category Gold Winner Award" at 2024 Patent Search Grand Prix, highlighting the company's intellectual property strength. Patents matter less for protection than as indicators of innovation velocity—and Dexerials continues accelerating.

The shareholder return story deserves attention. The year-end dividend forecast for fiscal year ending March 2025, converted to pre-stock split terms, is 96.00 yen per share, with annual dividend of 174.00 yen per share. Notice of Decision Regarding Details of Repurchase of Treasury Shares and Decision Regarding Details of Retirement of Treasury Shares demonstrates management's confidence in generating cash beyond reinvestment needs.

Market positioning strengthens continuously. Three Products Obtained the Largest Share of the Global Market for Five Successive Years: Anisotropic Conductive Film, Anti-reflection Film confirms dominance in core categories. Market leadership in materials markets tends to be sticky—once customers design products around your materials, switching becomes prohibitively complex.

The transformation from Sony subsidiary to independent powerhouse is nearly complete, but the journey continues. Current challenges include navigating the slowdown in smartphone markets while accelerating automotive penetration. The company must balance maintaining margins in commodity products while investing in next-generation technologies. Geographic diversification requires careful capital allocation between established and emerging markets.

Looking forward from October 2025, several catalysts could drive the next chapter. The automotive transition accelerates as electric vehicles become mainstream rather than premium products. Display technology evolution toward micro-LED and eventually holographic displays creates new materials opportunities. The Internet of Things explosion multiplies the number of connections and sensors requiring Dexerials' expertise.

Risk management remains crucial. Technology disruption could obsolete current products faster than expected. Chinese government support for domestic competitors intensifies competitive pressure. Economic cycles impact consumer electronics demand. Yet management has demonstrated ability to navigate challenges while maintaining profitability and investing for growth.

The Dexerials investment case ultimately rests on a simple premise: as the world becomes more digital, more connected, and more display-centric, demand for sophisticated materials that enable these technologies compounds. The company doesn't need to invent the next iPhone or Tesla—they just need to make the materials that make these innovations possible. In a world chasing the next big thing, sometimes the smartest investment is in the company making the glue that holds it all together.

For institutional investors, Dexerials offers rare combination of growth and value. The company trades at reasonable multiples despite market leadership and strong returns on capital. For strategic buyers, the company represents a platform for consolidating the fragmented materials industry. For technology companies, Dexerials could be a valuable partner or acquisition target to secure critical materials supply.

The broader lesson transcends Dexerials specifically. In every gold rush, selling picks and shovels beats mining for gold. In every technology revolution, enabling technologies generate more consistent returns than revolutionary products. And in every supply chain, controlling critical chokepoints creates sustainable competitive advantages. Dexerials embodies all three principles.

As we conclude this deep dive into Dexerials' journey from Sony subsidiary to independent technology leader, the story reminds us that value creation doesn't always require spotlight moments or charismatic founders. Sometimes it's about decades of patient improvement, deep technical expertise, and the discipline to stay focused when others chase shiny objects. In the end, the companies that make everything else possible often prove the best investments of all.

The next episode will explore another hidden champion transforming industries from the shadows. Until then, remember: the most important technologies are often the ones you never see, made by companies you've never heard of, creating value you'd never expect. That's the beauty of businesses like Dexerials—invisible but indispensable, boring but beautiful, unknown but irreplaceable.

The corporate governance journey at Dexerials represents another crucial dimension of value creation. The composition of the board evolved significantly post-IPO, with independent directors now comprising a majority. This shift brought fresh perspectives on strategy while maintaining continuity through retained institutional knowledge. The appointment of former automotive executives to the board in 2023 signaled serious commitment to that sector's expansion.

Executive compensation structures aligned remarkably well with long-term value creation. Management strengthened technologies and human capital, which became the most important management issues (Materiality) for the company. Performance metrics balanced growth, profitability, and ESG considerations, avoiding the short-term focus that plagues many public companies. Stock-based compensation ensured management thought like owners, not just operators.

The cultural transformation deserves particular attention. As a starting point for employees to come together and contribute to further growth and the creation of a sustainable society in an uncertain business environment, Dexerials established Purpose—"Empower Evolution. Connect People and Technology."—and Statement. This wasn't corporate buzzword bingo but a genuine attempt to unite 2,300 employees around a common mission transcending quarterly earnings.

Human capital management emerged as a critical differentiator. The company advanced construction of smart factories through digital transformation (DX) and improved abilities to acquire and retain technical and global human resources through development of a Group-wide job-based personnel system. The shift to job-based compensation, unusual for Japanese companies, attracted specialized talent who might have overlooked traditional seniority-based organizations.

Innovation metrics tell the real story. Patent applications increased 40% annually post-IPO, but more importantly, the quality improved. Patents shifted from incremental improvements to fundamental innovations in materials science. The company's engineers began publishing in peer-reviewed journals, establishing thought leadership beyond commercial applications. This intellectual capital compounds over time, creating barriers competitors struggle to overcome.

The sustainability narrative gained prominence without sacrificing profitability. Dexerials' materials enable energy-efficient displays, reduce manufacturing waste, and support electric vehicle adoption. ESG investors discovered a company whose products inherently support environmental goals rather than requiring costly retrofitting. The alignment between profit and purpose attracted a new class of long-term investors.

Strategic partnerships multiplied as independence brought flexibility. Collaborations with universities yielded breakthrough research. Joint ventures with customers accelerated product development. Technology licensing agreements generated high-margin revenue streams. Each partnership enhanced capabilities without diluting focus or requiring massive capital.

Looking Ahead: The Next Chapter

The strategic roadmap for 2025-2030 reveals ambitious yet achievable goals. The plan spans a five-year period from FY2024 to FY2028 (from April 1, 2024 to March 31, 2029). The company sets a sales target of 30 billion yen for the automotive business in fiscal 2028, more than double the current level, and is working to expand its sales network in overseas markets as one of its key priorities.

The photonics revolution presents the most exciting opportunity. The company will expand business in the photonics domain, where development of next-generation high-speed communication technology is required, using exclusive technologies at the Dexerials Group, with the leading role played by Dexerials Photonics Solutions Corporation established in April 2024. As data centers struggle with heat and power consumption, photonic interconnects promise dramatic improvements. Dexerials' materials expertise positions them perfectly for this transition.

Artificial intelligence creates unexpected demand. AI chips require sophisticated thermal management as processing power concentrates. High-bandwidth memory needs precise connections that only advanced ACF enables. Edge computing devices demand materials that balance performance with energy efficiency. Each AI advancement creates new materials challenges that Dexerials can solve.

The geographic expansion continues with particular focus on India and Southeast Asia. Dexerials Corporation announced construction of a new factory in Kanuma City in Japan's Tochigi Prefecture. The site was subject of land acquisition last January. The company expects the new plant to begin operation in FY 2026. This capacity expansion anticipates demand from emerging markets where smartphone adoption and automotive manufacturing accelerate.

The company invested in and entered into a capital and business alliance with SemsoTec Group, a corporate group centered around the German automotive design house SemsoTec Holding GmbH. As of October 1, 2024, the company completed its investment of eight million euros (approximately 1.3 billion yen) in two subsidiaries under SemsoTec Holding GmbH, and the two companies became equity method affiliates. This European beachhead provides direct access to German automotive giants previously difficult to penetrate from Japan.

Supply chain resilience becomes competitive advantage. While competitors concentrate manufacturing in single locations, Dexerials distributes production across multiple sites. Inventory strategies balance efficiency with customer security. Dual sourcing of critical raw materials prevents disruption. This operational excellence might seem mundane but proves invaluable during crises.

The innovation pipeline promises continued differentiation. Next-generation ACF for sub-10 micrometer connections enables further miniaturization. Quantum dot adhesives support displays with unprecedented color accuracy. Bio-based materials address environmental concerns without sacrificing performance. Each development extends technological leadership while opening new markets.

Financial strength enables strategic flexibility. The company will invest on a scale approximately three times greater than under the previous Mid-Term Management Plan. They will strive to enhance cash creation capability further and achieve balance between aggressive investment in growth and high level of shareholder returns. This capital allocation framework balances growth investment with shareholder returns, avoiding the feast-or-famine cycles that plague many industrial companies.

The competitive landscape continues evolving, but Dexerials' position strengthens. Chinese competitors improve quality but struggle with consistency at cutting-edge specifications. Korean manufacturers focus on their domestic champions, limiting global reach. Western materials companies lack the Asia-Pacific relationships essential for success. This competitive positioning creates a moat that widens over time.

Risk management sophistication increased markedly post-IPO. Scenario planning considers technology disruption, customer concentration, and geopolitical tensions. Hedging strategies protect against currency fluctuation without eliminating upside. Insurance coverage addresses operational risks while maintaining reasonable costs. This comprehensive approach provides resilience without paralyzing decision-making.

The acquisition strategy remains disciplined but opportunistic. Targets must offer technology, customer access, or manufacturing capability—preferably all three. Integration planning begins during due diligence, not after closing. Cultural fit receives equal weight with financial metrics. This patient approach yields fewer but more successful transactions.

Board composition continues evolving toward global best practices. Independent directors bring diverse expertise from technology, finance, and automotive industries. The nomination committee ensures succession planning for key executives. Compensation committee designs incentives aligned with long-term value creation. This governance infrastructure supports strategic ambition while maintaining appropriate oversight.

Stakeholder capitalism gains genuine traction. Employees benefit from skill development and career advancement opportunities. Customers receive consistent quality and collaborative innovation. Communities hosting facilities see stable employment and environmental stewardship. Shareholders enjoy sustainable returns from a company built to last. This balanced approach creates value for all constituents.

The Investment Thesis Crystallized

For growth investors, Dexerials offers exposure to multiple secular trends: display technology evolution, automotive electrification, and photonics revolution. The company grows faster than underlying markets through share gains and mix improvement. Geographic expansion provides runway for decades. Technology leadership ensures pricing power despite competitive pressure.

Value investors appreciate the financial characteristics. The company trades at reasonable multiples despite market leadership. Cash generation funds both growth and returns. The balance sheet provides downside protection. Hidden assets like intellectual property and customer relationships don't appear in book value. Patient investors can buy growth at value prices.

Income investors find rare combination of growth and yield. Dividends increase steadily as earnings compound. Share buybacks provide tax-efficient returns. The payout ratio leaves room for growth investment. Financial strength ensures dividend sustainability through cycles. Few industrial companies offer similar income characteristics.

ESG investors discover authentic sustainability. Products inherently support environmental goals. Governance meets international best practices. Social responsibility extends through the value chain. The company contributes to UN Sustainable Development Goals without greenwashing. This genuine commitment attracts long-term capital.

Strategic buyers see an attractive acquisition candidate. The technology portfolio complements many potential acquirers. Customer relationships provide immediate value. Manufacturing expertise transfers across industries. The culture facilitates integration. While management prefers independence, the right offer at the right price could create substantial value for all stakeholders.

Final Reflections: The Art of Building Enduring Value

The Dexerials story teaches timeless lessons about business building. Success doesn't require revolutionary products or charismatic founders. Sometimes it's about operational excellence, strategic focus, and patient capital. It's about finding your niche and dominating it completely. It's about making products nobody sees but everybody needs.

The journey from Sony subsidiary to independent powerhouse demonstrates that corporate transformations can succeed with the right combination of timing, leadership, and capital. The spin-off wasn't just financial engineering but genuine value creation through focus and accountability. The private equity phase provided breathing room for transformation. The IPO return validated the strategy while providing currency for growth.

For Japanese companies contemplating similar journeys, Dexerials provides a template. Global competitiveness doesn't require abandoning Japanese strengths like quality focus and long-term thinking. Patient capital from development banks can substitute for traditional private equity. Public markets will value strong businesses regardless of geography or industry.

The materials industry, often dismissed as commoditized and cyclical, proves capable of generating superior returns with the right strategy. Technology leadership, customer intimacy, and operational excellence create competitive advantages. Specialization beats diversification. Being essential beats being visible.

Looking forward, Dexerials seems positioned for continued success. Secular trends favor their technologies. Management demonstrates strategic sophistication. The balance sheet enables flexibility. The culture supports innovation. While challenges exist—technology disruption, competitive pressure, cyclical markets—the company has proven ability to adapt and thrive.

For investors seeking exposure to the real economy rather than digital abstractions, Dexerials merits serious consideration. The company makes tangible products solving real problems for critical industries. The business model generates cash, not just promises. The valuation reflects current performance, not distant dreams. In a market often disconnected from fundamentals, Dexerials offers refreshing substance.

The broader implications extend beyond investing. In an era obsessed with disruption, Dexerials reminds us that enabling others' innovation can be just as valuable. In a world chasing moonshots, incremental improvement compounds powerfully over time. In markets demanding instant gratification, patient building creates lasting value.

As we conclude this exploration of Dexerials' remarkable journey, the lessons resonate beyond materials science or Japanese industry. Great businesses often hide in plain sight, creating enormous value while remaining invisible. The best investments frequently involve boring industries with beautiful economics. The most successful transformations balance ambition with pragmatism.

Dexerials continues writing its story, adding chapters as technology evolves and markets develop. The next decade promises new challenges and opportunities. Display technology will continue advancing. Automotive electronics will proliferate. Photonics might revolutionize computing. Through each transition, Dexerials will likely remain what it's always been: invisible but indispensable, boring but beautiful, unknown but irreplaceable.

The company that began making glue for Sony's radios now enables the digital infrastructure defining modern life. From Tokyo to Detroit, from Shenzhen to Silicon Valley, Dexerials' materials quietly make possible the innovations that capture headlines. Sometimes the most important actor isn't the star but the stage crew making the performance possible. That's Dexerials—forever in the shadows, forever essential, forever creating value one molecular bond at a time.

The Quarterly Results Story Unfolds

The most recent financial results paint a picture of strategic execution meeting market opportunity. With net sales increasing by 4.9% to 110,390 million yen and a significant rise in operating profit by 24.6% for the fiscal year ending March 31, 2025, Dexerials demonstrated resilience in challenging markets. More tellingly, the composition of this growth reveals the strategic pivot bearing fruit—automotive applications now drive significant expansion even as traditional consumer electronics markets mature.

The Q3 2025 results, while not yet fully disclosed as we approach month-end, suggest continued momentum. The year-end dividend forecast for the fiscal year ending March 2025, converted to pre-stock split terms, is 96.00 yen per share, and the annual dividend is 174.00 yen per share, reflecting management's confidence in sustained cash generation despite market headwinds.

What makes these results particularly impressive is the margin story. While many Japanese manufacturers struggle with commoditization, Dexerials continues expanding profitability through mix improvement and operational excellence. The shift toward higher-value automotive and photonics applications more than offsets pricing pressure in commodity ACF products.

The Competitive Moat Deepens

Understanding Dexerials' competitive position requires appreciating the nuances of materials qualification. When a smartphone manufacturer selects ACF for their flagship device, they're not just choosing a product—they're embedding that material into their entire supply chain. Design specifications reference it. Manufacturing processes optimize around it. Quality systems calibrate to it. Changing suppliers means requalifying everything, a process taking 12-18 months minimum and risking production disruption.

This stickiness multiplies in automotive applications. A smartphone lives for two years; a car platform spans a decade. Once Dexerials' thermal management materials enter a electric vehicle platform, they're essentially locked in for the vehicle's production life. With automotive design cycles stretching 4-5 years and production runs lasting another 5-7 years, today's design wins generate revenue for the next decade.

The company's patent portfolio provides legal protection, but the real moat lies in manufacturing consistency. Producing ACF with failure rates below one part per million requires not just the right formula but perfect execution thousands of times daily. Temperature control within fractions of a degree. Particle distribution measured in nanometers. Contamination levels approaching zero. This isn't chemistry—it's alchemy perfected through decades of accumulated knowledge.

Customer relationships transcend typical supplier dynamics. Dexerials engineers embed with customer teams years before product launch. They don't just supply materials; they co-develop solutions. When Apple designs a new display technology, Dexerials learns about it before most of Apple's own employees. This early engagement creates switching costs beyond economics—it's institutional knowledge that can't be easily replaced.

The Human Capital Revolution

Post-independence, Dexerials transformed from a Japanese manufacturer into a global technology company, starting with talent management. The shift to job-based compensation, revolutionary by Japanese standards, attracted specialists who might have chosen Western companies. A materials scientist with expertise in quantum dots commands market compensation, not seniority-based wages.

Training programs evolved from apprenticeship models to innovation accelerators. Young engineers rotate through customer sites, experiencing real-world applications before specializing. Mid-career hires from automotive and semiconductor industries cross-pollinate expertise. The company sponsors doctoral research at leading universities, creating pipelines of specialized talent.

Cultural transformation proved equally important. The hierarchical structures typical of Japanese corporations gave way to project-based teams where expertise trumps seniority. Failed experiments became learning opportunities, not career-ending mistakes. English became the working language for global teams, breaking down communication barriers that historically limited Japanese companies' international expansion.

Employee ownership increased dramatically through stock compensation plans. When engineers see their innovations directly impact share price, motivation transcends salary. The company's purpose—"Empower Evolution. Connect People and Technology"—might sound like corporate speak, but employees genuinely embrace it. They're not making adhesives; they're enabling the future.

The Sustainability Imperative

Environmental considerations evolved from compliance burden to competitive advantage. Dexerials' products inherently support sustainability—enabling efficient displays that consume less power, supporting electric vehicles that reduce emissions, creating connections that eliminate waste. But the company pushed beyond product benefits to transform operations.

Manufacturing processes underwent systematic optimization. Solvent recovery systems capture and reuse chemicals previously released. Energy-efficient equipment reduces power consumption despite increased production. Water recycling minimizes environmental impact in increasingly water-stressed regions. These improvements reduce costs while enhancing environmental credentials—the holy grail of sustainable business.

Supply chain sustainability gained equal attention. Suppliers undergo rigorous environmental audits. Conflict minerals policies ensure ethical sourcing. Transportation optimization reduces carbon footprint. Local sourcing where possible minimizes logistics impact. These initiatives resonate with customers increasingly focused on Scope 3 emissions.

The circular economy presents opportunities rather than obligations. Dexerials develops materials designed for disassembly, enabling component recycling. Bio-based alternatives replace petroleum-derived chemicals where performance permits. Take-back programs recover valuable materials from end-of-life products. What starts as environmental responsibility becomes competitive differentiation.

The Innovation Engine Accelerates

The R&D transformation post-IPO represents more than increased investment—it's a fundamental reimagining of innovation. Traditional materials development followed linear paths: identify need, develop solution, commercialize product. Modern Dexerials operates multiple parallel development tracks, pursuing breakthrough technologies while incrementally improving existing products.

The photonics initiative exemplifies this approach. Rather than waiting for market demand, the company invests in capabilities anticipating where technology will go. Photonic interconnects might not generate meaningful revenue until 2027, but developing expertise now ensures leadership when markets mature. This forward investment requires patient shareholders but creates insurmountable advantages for followers.

Open innovation models supplement internal development. University partnerships yield fundamental research insights. Startup collaborations provide fresh perspectives. Customer joint development accelerates commercialization. Even competitor partnerships make sense when developing industry standards. The company transforms from isolated innovator to innovation orchestrator.

Failure tolerance increases innovation velocity. Not every project succeeds, but each generates learning. Materials developed for failed applications find unexpected uses elsewhere. Research dead-ends reveal what doesn't work, equally valuable to knowing what does. This portfolio approach—multiple bets with varying risk profiles—ensures continuous innovation flow.

Digital transformation enhances research productivity. AI algorithms predict material properties before synthesis, reducing experimental cycles. Automated testing accelerates qualification. Digital twins simulate manufacturing before physical production. Data analytics reveal patterns humans miss. Technology doesn't replace scientists but amplifies their capabilities.

Geographic Expansion: The Next Frontier

While Asia remains Dexerials' stronghold, geographic diversification accelerates. The European automotive market, particularly Germany's premium manufacturers, represents massive opportunity. These companies value innovation over cost, perfect for Dexerials' differentiation strategy. The SemsoTec partnership provides critical market access, but success requires more than distribution—it demands local presence.

The North American market offers different opportunities. Tesla's vertical integration philosophy aligns with direct supplier relationships. Detroit's legacy manufacturers seek differentiation through technology. Silicon Valley's tech giants value innovation and reliability over price. Each segment requires tailored approaches, but all appreciate Dexerials' capabilities.

Emerging markets present longer-term potential. India's electronics manufacturing ambitions create ground-floor opportunities. Southeast Asian automotive production shifts from assembly to design, requiring sophisticated materials. Middle Eastern smart city initiatives demand advanced display technologies. African mobile-first development leapfrogs traditional infrastructure, requiring robust materials for harsh environments.

Localization goes beyond sales offices. Technical centers near customers accelerate innovation cycles. Local procurement reduces supply chain risk. Regional manufacturing might follow as volumes justify investment. Cultural adaptation ensures solutions match local needs, not just specifications. Geographic expansion isn't just about selling globally—it's about becoming genuinely multinational.

The Capital Allocation Framework

Post-IPO capital allocation demonstrates remarkable discipline. Growth investment takes priority, but only where returns exceed hurdle rates. The company avoids empire building, focusing on opportunities leveraging existing capabilities. Maintenance capital remains minimal, reflecting the asset-light nature of specialty materials. This efficiency enables simultaneous growth investment and shareholder returns.

Acquisition criteria remain stringent. Targets must offer technology, customer access, or manufacturing capability that would take years to develop internally. Cultural fit matters as much as strategic fit—failed acquisitions often stem from integration challenges rather than strategic miscalculation. Valuation discipline prevents overpayment, even for attractive assets. Patience pays off when the right opportunity emerges at the right price.

Organic investment focuses on capability building rather than capacity expansion. New equipment enables new products, not just more volume. R&D investment targets breakthrough technologies, not incremental improvements. Training develops human capital, the ultimate competitive advantage. These investments compound over time, creating capabilities competitors can't quickly replicate.

Shareholder returns balance growth retention with capital return. Dividends provide steady income while maintaining flexibility. Share buybacks occur opportunistically when valuation disconnects from intrinsic value. The company maintains financial strength for strategic flexibility while avoiding excessive conservatism. This balanced approach attracts both growth and income investors.

Risk Management in Practice

Modern risk management at Dexerials transcends traditional frameworks. Technology risk receives constant attention—not if disruption will occur, but when and how. The company monitors adjacent technologies that might obsolete current products. Research investments hedge against disruption. Partnership networks provide early warning signals. When change comes, Dexerials aims to lead rather than react.

Customer concentration risk, while reduced from Sony-dependent days, remains material. No single customer dominates, but the top ten still represent significant revenue. Mitigation involves deepening relationships beyond procurement, becoming integral to customer innovation. Multi-year agreements provide stability while maintaining pricing flexibility. Geographic and industry diversification reduces single-customer impact.

Supply chain risk gained prominence post-COVID. Single-source raw materials represent vulnerability. Geographic concentration in suppliers creates disruption potential. Just-in-time manufacturing efficiency trades off against supply security. Dexerials responds with strategic inventory, dual sourcing where possible, and supplier partnership deepening. The goal isn't eliminating risk but managing it intelligently.

Competitive risk evolves continuously. Chinese competitors improve quality while maintaining cost advantages. Korean companies leverage government support and chaebol resources. Western materials companies bring different capabilities. Dexerials' response involves continuous innovation, customer intimacy, and operational excellence. Competition sharpens execution rather than threatening existence.

Macroeconomic risk affects all businesses but impacts materials companies particularly. Consumer electronics demand correlates with economic cycles. Automotive production responds to interest rates and consumer confidence. Currency fluctuations affect competitiveness. While these factors can't be controlled, their impact can be managed through diversification, hedging, and operational flexibility.

Conclusion: The Next Decade Unfolds

As we conclude this deep exploration of Dexerials' remarkable journey in October 2025, the company stands at an inflection point. The transformation from Sony subsidiary to independent technology leader is complete. The foundation—strong technology, diversified customers, global presence, financial strength—supports ambitious growth. The question isn't whether Dexerials will succeed, but how much value they'll create.

The next decade promises unprecedented opportunity. Display technology evolution toward AR/VR creates new materials challenges. Automotive electronics proliferation multiplies connection points. Photonics revolution demands novel materials. IoT explosion requires reliable, miniaturized connections. Each trend plays to Dexerials' strengths.

Challenges certainly exist. Technology disruption accelerates. Competition intensifies. Macroeconomic uncertainty persists. But Dexerials has proven ability to navigate challenges while maintaining profitability. The company that survived separation from Sony, transformed under private equity, and thrived as a public company seems well-equipped for whatever comes next.

For investors, Dexerials offers a rare combination: exposure to multiple growth trends, demonstrated execution capability, strong financial characteristics, and reasonable valuation. While not without risk, the company provides compelling opportunity for those willing to look beyond headline-grabbing tech stocks to find value in essential but invisible technologies.

The broader lessons transcend Dexerials specifically. In a world obsessed with disruption, enabling technologies often prove more valuable than disruptive products. In markets demanding instant gratification, patient building creates lasting value. In industries dismissed as commoditized, innovation and execution create differentiation. Sometimes the best investments hide in plain sight, creating enormous value while remaining invisible.

Dexerials embodies these paradoxes. Unknown but essential. Boring but beautiful. Invisible but irreplaceable. As displays get thinner, connections get smaller, and materials get smarter, Dexerials will be there—in the shadows, in the details, in the bonds that hold our digital world together. They don't make the future; they make the future possible.

The company that began making glue for Sony's transistor radios now enables technologies not yet invented. From anisotropic conductive films to photonic interconnects, from smartphone displays to electric vehicle batteries, Dexerials quietly powers progress. In a world racing toward an uncertain future, betting on the companies that make everything else possible seems like a very smart investment indeed.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube