Boston Scientific: The Engineering of Less-Invasive Medicine

I. Introduction & Episode Roadmap

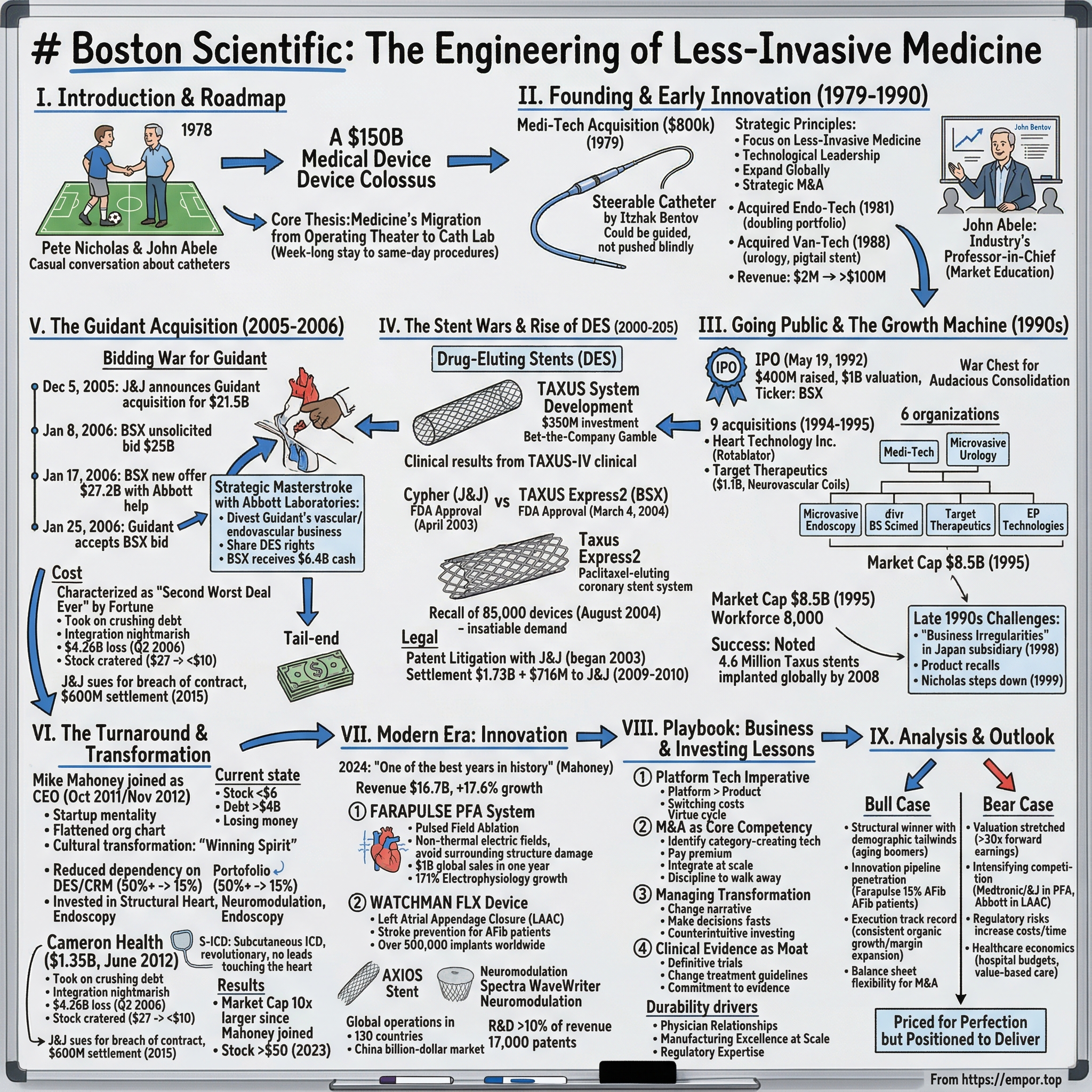

Picture this: It's a crisp Saturday morning in 1978 at a youth soccer field in Natick, Massachusetts. Two fathers stand on the sidelines, watching their kids chase a ball across dewy grass. One is Pete Nicholas, a polished Wharton MBA who'd cut his teeth at Eli Lilly's pharmaceutical empire. The other is John Abele, a philosophy and physics major from Amherst who'd been peddling medical devices to skeptical surgeons for years. Their casual conversation that morning—about catheters, of all things—would spawn a company that today commands a $150 billion market capitalization and fundamentally transformed how medicine is practiced worldwide.

How exactly did these two soccer dads build a medical device colossus that would eventually outbid Johnson & Johnson—yes, that Johnson & Johnson—in a $27 billion acquisition battle that Wall Street called "the deal of the century"? How did they convince surgeons to abandon their scalpels for thin, snake-like tubes? And perhaps most remarkably, how did they recover from taking on crushing debt that nearly destroyed everything they'd built?

Boston Scientific's story isn't just another corporate chronicle—it's the narrative of medicine's great migration from the operating theater to the catheterization lab, from week-long hospital stays to same-day procedures, from massive surgical scars to tiny puncture wounds. It's about betting billions on the radical notion that you could fix a heart without cracking open a chest, clear a blocked artery without major surgery, or treat an irregular heartbeat with a device smaller than a matchbox.

What we're about to explore is a masterclass in category creation, the art of scientific acquisition, and the high-stakes poker game of medical device innovation. We'll witness boardroom battles where billions changed hands in minutes, laboratories where engineers solved problems surgeons thought impossible, and hospital corridors where new technologies literally saved lives while generating extraordinary returns. From the company's scrappy $800,000 beginning to its current status as interventional cardiology's 800-pound gorilla, this is how Boston Scientific engineered the future of less-invasive medicine—and created one of the most compelling turnaround stories in modern business.

II. The Founding Story & Early Innovation (1979–1990)

The pivotal moment came not on that soccer field, but months later in a cramped conference room where Pete Nicholas and John Abele huddled over engineering drawings of something called a "steerable catheter." The inventor, Itzhak Bentov, was the kind of character Silicon Valley would later mythologize—a Czech-born meditation enthusiast who split his time between biomedical engineering and writing books about consciousness. His company, Medi-Tech, had developed a catheter that could actually be guided through the body's twisted highways of blood vessels, rather than pushed blindly like a garden hose through a maze.

Bentov's invention was revolutionary, but Medi-Tech was hemorrhaging cash. Nicholas saw opportunity where others saw a dying company. With his pharmaceutical industry connections and Abele's deep understanding of what interventional radiologists actually needed, they orchestrated what would become the founding transaction of Boston Scientific: acquiring Medi-Tech for $800,000—$500,000 from bank financing that Nicholas charmed out of skeptical lenders, plus $300,000 scraped together from friends, family, and their own savings accounts.

The first year's results vindicated their gamble: $2 million in revenue from catheters used primarily for gallbladder procedures. But revenue wasn't the real victory. What Nicholas and Abele had acquired was a beachhead in what they believed would become medicine's next frontier. Their thesis was elegant in its simplicity: as medical imaging improved—and they were certain it would—doctors would be able to see inside the body with unprecedented clarity. Once you could see clearly, why would you cut patients open when you could thread a catheter through a blood vessel and fix the problem from the inside? They built the company methodically, almost academically. Nicholas established four strategic principles that would guide Boston Scientific for decades: focus on less-invasive medicine, maintain technological leadership, expand globally from day one, and grow through strategic acquisitions. By 1981, they'd acquired Endo-Tech, their largest competitor in gastrointestinal and pulmonary endoscopic accessories, instantly doubling their product portfolio. In 1981, the company acquired Endo-Tech, its largest competitor in gastrointestinal and pulmonary endoscopic accessories.

The 1980s became a masterclass in market education. Abele understood that selling catheters wasn't about pushing product—it was about converting skeptics. In the early 1980s, Abele became a regular contributor to televised tutorials and in-person seminars on percutaneous transluminal angioplasty. He became the industry's professor-in-chief, hosting weekend workshops where interventional radiologists could practice threading catheters through plastic models of human vasculature. Boston Scientific's sales force became known as an "educational powerhouse"—they weren't salespeople, they were technical consultants who could scrub into procedures and guide physicians through complex cases.

The strategy worked brilliantly. By 1988, when they acquired Van-Tech and its game-changing pigtail ureteral stent, Boston Scientific bought Van-Tech, which boosted the urology business with products like its pigtail ureteral stent. Boston Scientific had transformed from a single-product company into a diversified medical device platform. They'd proven that less-invasive wasn't just possible—it was profitable. Revenue grew from that initial $2 million to over $100 million by decade's end, setting the stage for what would become one of the most aggressive expansion campaigns in medical device history.

III. Going Public & The Growth Machine (1990s)

The morning of May 19, 1992, Pete Nicholas stood on the floor of the New York Stock Exchange, watching as Boston Scientific's ticker symbol—BSX—flickered to life for the first time. The IPO raised $400 million at $17 per share, instantly valuing the company at nearly $1 billion. Nicholas and Abele, who retained two-thirds ownership post-IPO, had just become extraordinarily wealthy. But more importantly, they now had the war chest to execute their most audacious vision: consolidating the fragmented medical device industry through strategic acquisition.

What followed was a buying spree that would make private equity firms blush. Between 1994 and 1995 alone, Boston Scientific acquired nine companies in just 16 months, deploying $2.5 billion in a relentless pursuit of category leadership. Each acquisition followed a precise playbook: identify a company with breakthrough technology, acquire it at a premium that competitors couldn't match, then integrate its products into Boston Scientific's educational selling machine. The crown jewel acquisitions came in rapid succession. Heart Technology Inc., with its Rotablator—a catheter with a spinning diamond bit that cleaned out clogged arteries—saw sales explode from zero to $80 million between 1993 and 1995. Target Therapeutics, acquired for $1.1 billion in stock in 1997, brought revolutionary neurovascular products including a new coil that received FDA approval in 1995, offering a relatively safe and cost-effective treatment for patients with brain aneurysms.

The organization that emerged from this acquisition frenzy was formidable. Following its five-year string of acquisitions, Boston Scientific was organized into six divisions: EP Technologies specialized in cardiac electrophysiology; Medi-Tech was a leading developer of minimally invasive devices for peripheral vascular disease management; Microvasive Urology manufactured diagnostic and therapeutic products for stone management, incontinence, and prostate disease; Microvasive Endoscopy focused on gastrointestinal endoscopic procedures; Boston Scientific Scimed Inc. was the company's primary cardiology unit; and Target Therapeutics was a leader in neuro endovascular intervention.

The transformation was staggering: At the end of 1995 Boston Scientific's market capitalization had grown to $8.5 billion, compared to $1.5 billion at the end of 1994. Its workforce had grown from 2,000 to 8,000 employees. Its product line increased from 3,000 to 8,000 items.

But this explosive growth came with consequences. In November 1998, the company was forced to restate its financial results after discovering "business irregularities" at its Japanese subsidiary—a scandal that would cost executives their credibility and the stock its momentum. Product recalls mounted. The organization, bloated from acquisitions, struggled to integrate diverse cultures and systems. When Nicholas stepped down as CEO in March 1999, passing the torch to James Tobin, the company was at an inflection point: it had built an empire, but now needed to prove it could manage one.

IV. The Stent Wars & Rise of Drug-Eluting Stents (2000–2005)

The catheterization lab at Cleveland Clinic buzzed with anticipation on April 24, 2003. Dr. Stephen Ellis was about to implant one of the first Taxus drug-eluting stents in the United States—a device that Boston Scientific executives believed would revolutionize interventional cardiology. The tiny mesh tube, coated with the cancer drug paclitaxel, promised to solve cardiology's most vexing problem: restenosis, the re-narrowing of arteries that plagued 30% of patients receiving bare-metal stents. Boston Scientific's entry into the drug-eluting stent market was a bet-the-company gamble. They'd spent $350 million developing the Taxus system—an astronomical sum that required closing three plants and laying off thousands of workers to fund. Boston Scientific closed three plants and laid-off thousands of workers to come up with part of the $350 million it needed to develop the device. The stakes couldn't have been higher: Johnson & Johnson's Cypher stent had already captured the U.S. market after FDA approval in April 2003, giving them a crucial first-mover advantage.

But Boston Scientific had an ace up its sleeve. On March 4, 2004, Boston Scientific received FDA approval to market its TAXUS Express2 paclitaxel-eluting coronary stent system. The Company plans to launch the product in the United States immediately, and it has ample inventory in all sizes. The Company launched the TAXUS system in Europe and other international markets in February of 2003 and is the leader in those markets today. While J&J had been first in America, Boston Scientific had quietly dominated Europe for over a year, refining their manufacturing and building physician confidence.

The clinical data was compelling. The TAXUS-IV trial, which evaluated 1,326 patients, showed dramatic reductions in restenosis rates. CEO James Tobin declared it "a breakthrough event for the treatment of cardiovascular disease in the United States," noting that "Broad, consistent clinical data and extensive real-world experience have clearly demonstrated that polymer-based delivery of paclitaxel is a safe and effective therapy that dramatically reduces restenosis."

The launch was a masterpiece of operational execution—until it wasn't. Within weeks of the U.S. rollout, reports started flooding in about balloons that wouldn't deflate after deploying the stent. By August 2004, Boston Scientific was forced to recall 85,000 devices. But its roll out was marred by a partial recall of 85,000 of the devices. Wall Street panicked, but the market didn't care—physicians had seen the clinical results, and demand remained insatiable. Despite the recall, the device was a huge success for the company and helped drive Boston Scientific's profits more than five-fold in 2004.

The real cost of the stent wars, however, came in the form of patent litigation. Beginning in 2003, Boston Scientific and Johnson & Johnson were involved in a series of litigations involving patents covering heart stent medical devices. Both parties claimed that the other had infringed upon their patents. The litigation was settled once Boston Scientific agreed to pay $716 million to Johnson & Johnson in September 2009 and an additional $1.73 billion in February 2010. That $1.725 billion payout—one of the largest patent settlements in medical device history—was the price of admission to a market that would generate tens of billions in revenue.

By 2008, Boston Scientific had implanted approximately 4.6 million Taxus stents globally, making them the world's most frequently used drug-eluting stents. They'd proven that being first didn't guarantee victory—superior execution, global strategy, and deep physician relationships could overcome a late start. But as the decade closed, an even bigger opportunity was emerging: the chance to acquire their way to absolute market dominance.

V. The Guidant Acquisition: The Deal of the Century (2005–2006)

The phone call came at 6:47 AM on December 5, 2005. Jim Tobin was in his home office, reviewing European sales figures, when his head of corporate development burst through the door: "Johnson & Johnson just announced they're buying Guidant for $21.5 billion." Tobin set down his coffee. Guidant—the Indianapolis-based cardiac rhythm management powerhouse—had been struggling with product recalls, but their technology portfolio was irreplaceable. If J&J succeeded, they'd control both the stent and pacemaker markets. Boston Scientific would be boxed out of cardiology's highest-margin segments forever. What followed was the most dramatic bidding war in medical device history. On January 8, 2006, Boston Scientific stunned the market with an unsolicited $25 billion offer for Guidant—$3.5 billion more than J&J's agreed price. In December, Boston Scientific presented an unsolicited, $25 billion bid for Guidant, triggering the bidding war. The boardrooms of three medical device giants became war rooms. Bankers worked through the night calculating debt ratios and synergy models. Lawyers pored over merger agreements looking for loopholes.

The key to Boston Scientific's strategy was Abbott Laboratories. To preempt antitrust concerns, Boston Scientific had entered into an agreement with Abbott under which Boston Scientific has agreed to divest Guidant's vascular intervention and endovascular businesses, while agreeing to share rights to Guidant's drug-eluting stent program. Under its agreement with Abbott, Boston Scientific will receive $6.4 billion in cash from Abbott on or around the closing date of the Guidant transaction. This masterstroke solved two problems: it provided immediate cash to reduce debt burden and eliminated regulatory obstacles that could have killed the deal.

J&J fought back, raising their bid multiple times. But on January 17, 2006, Boston Scientific delivered the knockout punch: It was not until January 17 that Boston Scientific produced a new offer of $27.2 billion ($80 per share), with the help of Abbott Laboratories. The next week was agonizing. J&J had five days to respond. At Boston Scientific headquarters, executives barely slept, constantly refreshing their screens for news. Finally, at midnight on January 25, the deadline passed without action from J&J. On January 25, 2006, after Johnson & Johnson refused to raise their bid higher than $24.2 billion, Guidant declared Boston Scientific's offer "clearly superior" and accepted their bid.

The victory came at an enormous cost. Fortune magazine characterized the deal as the second worst deal ever, stating that the company paid too much for Guidant. Boston Scientific had taken on crushing debt to finance the acquisition. The integration proved nightmarish—Guidant's quality problems were worse than expected, requiring massive investments to fix. On July 27, 2006, Boston Scientific posted a loss of $4.26 billion for the quarter. The stock cratered, falling from $27 to under $10 by 2008.

But there was one more bill to pay. J&J, furious about losing Guidant, sued Boston Scientific for breach of contract, claiming Abbott had improperly accessed confidential information during the bidding process. In the lawsuit filed in 2006, Johnson & Johnson alleged that Guidant breached the merger agreement it had with Johnson & Johnson, and sought more than $7 billion in damages. The lawsuit dragged on for nearly a decade before Boston Scientific finally settled in 2015, paying J&J $600 million—a bitter epilogue to their Pyrrhic victory.

VI. The Turnaround & Transformation (2012–2020)

Mike Mahoney walked into Boston Scientific's boardroom on his first day as CEO in November 2012 and found a company on life support. The stock was trading at $5.42—down 80% from its pre-Guidant levels. Debt still exceeded $4 billion. Market share was hemorrhaging to competitors. The cardiac rhythm management business acquired from Guidant was losing money. Wall Street had written Boston Scientific's obituary. Mahoney wasn't a turnaround specialist—he was a builder. His career arc told the story: twelve years at GE Medical Systems, then founding CEO of Global Healthcare Exchange, then running J&J's massive medical device division. BSX shares were selling for under $6 apiece when Mahoney joined the company as CEO in October 2011. But what made him perfect for Boston Scientific was his startup mentality. "We actually thought of it as a startup: 'Let's create Boston Scientific,'" Mahoney said.

His first moves were surgical. He sold the bloated Natick headquarters and moved to smaller offices in Marlborough—a symbolic break from the imperial past. He flattened the organization chart, expanding his direct reports to get closer to the front lines. "We did some structural things, we enabled the organization to move a little bit faster by expanding the number of reports and the speed of the company."

But the real transformation was portfolio surgery. When he joined, drug-eluting stents and cardiac rhythm management made up more than half of the company's portfolio mix. Today, it's 15%. "We really modified the portfolio quarter after quarter through M&A, through alliances, through organic R&D consistently over 10 years to put ourselves in faster growth markets along the way," Mahoney said. He divested low-growth businesses and poured resources into emerging categories: structural heart, neuromodulation, endoscopy. The acquisition strategy was surgical. In June 2012, just months into his tenure, Mahoney closed the Cameron Health acquisition for up to $1.35 billion. Under the terms of the agreement, Boston Scientific paid $150 million at closing. The agreement calls for an additional potential payment of $150 million to be made upon FDA approval of the S-ICD System and up to an additional $1.050 billion of potential payments. The S-ICD (subcutaneous implantable cardioverter-defibrillator) was revolutionary—it sat entirely under the skin without leads touching the heart, eliminating the complications that plagued traditional ICDs. "This is a game-changer," physicians proclaimed at the Heart Rhythm Society meeting.

But the real genius was cultural transformation. Mahoney instilled what he called a "winning spirit"—a startup mentality in a 33-year-old company. "Most employees want to feel great about the company they work for, proud of the company, pride when they are talking about it at barbecues with their neighbors," he explained. By 2018, Glassdoor ranked him as the second-most-liked CEO in America, just behind Zoom's Eric Yuan.

The financial turnaround was staggering. Boston Scientific's market capitalization has grown nearly 10 times larger since Mike Mahoney joined as CEO in 2011. The stock climbed from $5.42 to over $50 by 2023. Revenue grew from stagnant single digits to consistent high single-digit organic growth. Operating margins expanded. The debt burden, once crushing, became manageable.

Most importantly, Boston Scientific had reclaimed its innovation mojo. The company wasn't just surviving—it was hunting again, identifying the next waves of medical innovation and positioning itself to lead them. The turnaround wasn't complete—turnarounds never really are—but Boston Scientific had transformed from a cautionary tale into a case study in corporate resurrection.

VII. Modern Era: Innovation & Category Leadership (2020–Today)

The conference call on February 1, 2024, was unlike any in Boston Scientific's recent history. Mike Mahoney, now in his twelfth year as CEO, couldn't contain his enthusiasm: "2024 was one of the best years in the history of Boston Scientific." The numbers backed him up—revenue had hit $16.747 billion, up 17.6% year-over-year, with organic growth approaching double digits. But the real story wasn't the financials; it was the technology revolution Boston Scientific was leading across multiple fronts. The crown jewel was FARAPULSE, Boston Scientific's pulsed field ablation system that was rewriting the rules of cardiac electrophysiology. MARLBOROUGH, Mass., Jan. 31, 2024 /PRNewswire/ -- Boston Scientific Corporation (NYSE: BSX) announced it has received U.S. Food and Drug Administration (FDA) approval for the FARAPULSE™ Pulsed Field Ablation (PFA) System. The technology used non-thermal electric fields to ablate heart tissue causing atrial fibrillation, avoiding damage to surrounding structures that plagued traditional thermal ablation. In a study of 17,000+ patients, FARAPULSE had zero reports of the serious adverse events seen in traditional thermal-based cardiac ablation—and an overall serious adverse event rate of less than 1%.

The market response was explosive. The company collected more than $1 billion of global sales for Farapulse in one year. Electrophysiology revenue grew 171% year-over-year, transforming what had been a sleepy division into Boston Scientific's fastest-growing business. Over 200,000 patients have found their rhythm again with the FARAPULSE procedure. Physicians weren't just adopting the technology—they were evangelizing it. But FARAPULSE was just one jewel in an increasingly impressive crown. The WATCHMAN FLX left atrial appendage closure device had become the gold standard for stroke prevention in atrial fibrillation patients. The trial met the primary safety endpoint of non-procedural major bleeding or clinically relevant non-major bleeding at 36 months, with the WATCHMAN FLX device demonstrating superiority to OAC (8.5% vs.18.1%; P<0.0001). It also met the primary efficacy endpoint of all-cause death, stroke or systemic embolism at 36 months, with the data showing non-inferiority of the device to OAC (5.4% vs. 5.8%; P<0.0001). With over 500,000 implants worldwide, WATCHMAN had created an entirely new treatment paradigm.

The portfolio breadth was staggering. The AXIOS Stent revolutionized treatment of pancreatic pseudocysts. The Spectra WaveWriter neuromodulation system provided relief for chronic pain patients who'd failed other therapies. Each product represented not just incremental improvement but category leadership—Boston Scientific wasn't competing in markets, it was creating them. The acquisition machine continued to hum. Apollo Endosurgery, acquired for $615 million in 2023, brought endoscopic weight management technologies just as obesity emerged as a global health crisis. The Apollo Endosurgery product portfolio includes devices used during endoluminal surgery (ELS) procedures to close gastrointestinal defects, manage gastrointestinal complications and aid in weight loss for patients suffering from obesity. Preventice Solutions, acquired in 2021, added remote cardiac monitoring capabilities that proved prescient as telehealth exploded post-pandemic.

The geographic expansion was equally impressive. With 53,000 employees operating in 130 countries, Boston Scientific had become truly global. China, once an afterthought, was now a billion-dollar market growing at 20% annually. The company wasn't just selling American innovation abroad—it was developing products specifically for emerging markets, understanding that the future of medical technology would be written as much in Shanghai and Mumbai as in Boston.

Most importantly, Boston Scientific had reclaimed its identity as an innovation powerhouse. R&D spending exceeded 10% of revenue, among the highest in the industry. The company held over 17,000 patents and patent applications. Clinical trials numbered in the hundreds. This wasn't the debt-laden, struggling company of 2012—it was a technology leader defining the future of medicine.

VIII. Playbook: Business & Investing Lessons

The transformation of Boston Scientific from near-bankruptcy to $150 billion juggernaut offers a masterclass in corporate strategy, capital allocation, and competitive positioning. The lessons aren't just academic—they're battle-tested principles forged in the crucible of one of business history's most dramatic turnarounds.

The Platform Technology Imperative

Boston Scientific's greatest strategic insight was recognizing that in medical devices, platforms beat products every time. FARAPULSE isn't just a single ablation catheter—it's an entire ecosystem of catheters, generators, sheaths, and software that work together seamlessly. Once a hospital invests in the platform, switching costs become prohibitive. Training staff on new systems, changing workflows, managing inventory—the friction is enormous.

This platform approach creates compounding advantages. Each new product that plugs into the platform increases its value. Each physician trained becomes an advocate. Each successful procedure builds evidence. The network effects are powerful: the more procedures performed, the more data collected, the better the outcomes, the more physicians adopt, creating a virtuous cycle competitors struggle to break.

M&A as Core Competency

Boston Scientific has executed over 50 acquisitions since going public, but the real skill isn't in dealmaking—it's in integration. The company developed a playbook: identify category-creating technologies, pay premium prices that competitors can't match, then leverage Boston Scientific's global commercial infrastructure to achieve scale impossible for standalone companies.

The Cameron Health acquisition exemplifies this approach. Boston Scientific had been an investor since 2004, watching the technology mature, understanding the market dynamics. When they struck in 2012, paying up to $1.35 billion for a company with minimal revenue, Wall Street scoffed. But Boston Scientific saw what others missed: S-ICD would create an entirely new category, and category creators capture disproportionate value.

The discipline to walk away is equally important. When valuations don't make sense or strategic fit isn't perfect, Boston Scientific passes. They've watched competitors overpay for assets, burden themselves with integration challenges, and destroy shareholder value. Knowing when not to deal is as important as knowing when to strike.

Managing Through Transformation

Mike Mahoney's turnaround playbook should be required reading for any executive facing a crisis. First, he changed the narrative from "turnaround" to "transformation"—subtle but powerful reframing that energized employees rather than demoralized them. Second, he made tough decisions fast: divesting non-core assets, flattening the organization, moving headquarters. Speed matters in transformations; momentum builds confidence.

Third, and most importantly, he invested through the crisis. While cutting costs, Mahoney increased R&D spending. While managing debt, he made strategic acquisitions. This counterintuitive approach—simultaneously playing defense and offense—separated Boston Scientific from peers who retreated into pure cost-cutting mode and emerged from crisis weakened.

Clinical Evidence as Competitive Moat

In medical devices, clinical evidence is everything. Boston Scientific doesn't just run trials—it runs the definitive trials that become standard references for years. The OPTION trial for WATCHMAN FLX, with 1,600 patients across 114 sites, wasn't just large—it was designed to answer the exact questions physicians ask. When results showed superiority to anticoagulation for bleeding reduction, it didn't just support sales—it changed treatment guidelines.

This commitment to evidence requires patience and capital that many competitors lack. Trials take years and cost hundreds of millions. But the payoff is enormous: once established in guidelines, backed by Level 1 evidence, products become nearly impossible to dislodge. Competitors must not only match the technology but overcome the weight of accumulated evidence—a bar that rises with each published study.

Building Durability in Medical Devices

Sustainable competitive advantages in medical devices come from three sources, and Boston Scientific has mastered all three. First, physician relationships—not just selling to doctors but partnering in product development, clinical trials, and education. These relationships, built over decades, create switching costs beyond economics.

Second, manufacturing excellence at scale. Producing medical devices isn't like making widgets—it requires specialized facilities, quality systems, regulatory expertise. Boston Scientific's ability to manufacture FARAPULSE catheters at scale while maintaining quality is a barrier competitors can't quickly replicate.

Third, regulatory expertise as competitive advantage. Boston Scientific has mastered the art of regulatory strategy—knowing which pathways to pursue, how to design trials that regulators accept, how to manage post-market surveillance. In an industry where regulatory approval can take years and cost hundreds of millions, this expertise translates directly to speed-to-market advantages.

Capital Allocation in R&D-Intensive Businesses

Boston Scientific's capital allocation framework balances three competing demands: funding organic R&D, pursuing acquisitions, and returning capital to shareholders. The company maintains R&D spending above 10% of sales—non-negotiable even during crisis periods. This ensures the innovation pipeline never runs dry.

For acquisitions, the framework is disciplined: only category-creating or category-leading assets, only where Boston Scientific's commercial infrastructure creates clear synergies, only at prices that allow acceptable returns even in downside scenarios. Everything else gets passed over, regardless of banker pressure or competitor moves.

The beauty of this framework is its consistency. Employees know innovation is sacred. Investors know capital won't be wasted on empire building. Competitors know Boston Scientific will show up for the assets that matter and compete aggressively. Predictability in capital allocation is itself a strategic advantage.

The Guidant Lesson: When Betting the Company Makes Sense

The Guidant acquisition nearly destroyed Boston Scientific, yet Mahoney calls it one of the company's best decisions. This paradox contains a crucial lesson: sometimes the highest-risk path is doing nothing. Without Guidant's cardiac rhythm management business, Boston Scientific would have remained subscale in cardiology's highest-margin segments. The debt was crushing, the integration brutal, but the strategic logic was sound.

The key is execution after the deal. Boston Scientific spent five years fixing Guidant's quality problems, another five optimizing the portfolio, and is only now fully realizing the synergies. This decade-plus timeline is why most companies avoid transformational deals—quarterly earnings pressures make such patience impossible. But for those with conviction and staying power, betting the company on the right asset can create generational value.

The playbook's final lesson might be the most important: culture eats strategy. Boston Scientific's transformation worked not because of brilliant strategy—many companies have strategies—but because 53,000 employees believed in it. When Mahoney talks about "winning spirit," it sounds like corporate speak. But visit a Boston Scientific facility, watch engineers obsess over catheter design, see sales reps educating physicians, and you understand: culture isn't soft stuff. In medical devices, where innovation and execution determine success, culture is the ultimate competitive advantage.

IX. Analysis & Bear vs. Bull Case

The Bull Case: Structural Winner in Structurally Growing Markets

The bulls see Boston Scientific as the best-positioned player in medical technology's highest-growth categories. Start with demographics: 10,000 Americans turn 65 every day, a trend continuing through 2030. These aging baby boomers need exactly what Boston Scientific sells—devices for age-related cardiovascular disease, solutions for chronic pain, technologies for urological conditions. This isn't cyclical demand subject to economic fluctuations; it's structural, inevitable, and accelerating.

The innovation pipeline validates the growth trajectory. FARAPULSE has barely scratched the surface—only 15% of eligible atrial fibrillation patients receive ablation today. As the technology improves and expands to persistent AFib, that penetration could triple. WATCHMAN faces similar dynamics: millions of patients remain on blood thinners who could benefit from the device. Each product category shows similar penetration upside.

Execution track record matters. Under Mahoney's leadership, Boston Scientific has delivered consistent mid-single-digit organic growth while expanding margins—the holy grail of medical devices. The company has proven it can integrate acquisitions, launch new products globally, and navigate regulatory complexities. This execution muscle memory reduces risk; Boston Scientific has shown it can deliver in various environments.

The balance sheet provides flexibility for opportunistic moves. With debt manageable and cash flow strong, Boston Scientific can pursue transformational acquisitions while maintaining investment-grade ratings. In an industry where consolidation continues, this financial flexibility is a strategic weapon.

International expansion offers another growth vector. While U.S. healthcare faces reimbursement pressures, emerging markets desperately need medical technology. Boston Scientific's established presence in China, India, and Latin America positions it to capture this growth. These aren't far-off opportunities—international revenue already exceeds 40% of total sales and grows faster than U.S. business.

The Bear Case: Valuation Stretched, Competition Intensifying

Bears point to valuation as the primary concern. At over 30 times forward earnings, Boston Scientific trades at a premium to both historical averages and peers. This valuation implies perfect execution and continued market share gains—a dangerous assumption in the competitive medical device industry. Any stumble—a product recall, integration challenge, or competitive loss—could trigger multiple compression and significant downside.

Competitive dynamics are intensifying across every category. In pulsed field ablation, Medtronic and Johnson & Johnson have launched competing systems. In left atrial appendage closure, Abbott's Amulet is gaining share. In drug-eluting stents, the market has commoditized with pricing pressure mounting. Boston Scientific must defend existing positions while investing in new categories—an expensive proposition that could pressure margins.

Regulatory risks loom larger as scrutiny increases. The FDA has become more conservative, demanding larger trials and longer follow-up. European regulators have tightened medical device regulations. China has become increasingly protectionist. Each regulatory change adds cost, complexity, and time to market—headwinds that affect all players but particularly pressure companies with broad portfolios like Boston Scientific.

Healthcare economics pose structural challenges. Hospitals face staffing shortages and budget constraints. Insurers push for value-based care models that scrutinize high-cost procedures. Government reimbursement rates face continuous pressure. While demographics drive demand, the ability to pay for that demand isn't guaranteed. Procedure volumes could disappoint if economic conditions deteriorate or healthcare systems reach capacity constraints.

Integration execution remains a question mark. Boston Scientific has acquired aggressively, but truly integrating these technologies takes years. Sales force training, system integration, manufacturing scaling—each presents execution risk. The company must simultaneously integrate recent acquisitions while pursuing new ones, a juggling act that has tripped up many serial acquirers.

Competitive Positioning: The Decisive Factors

Against Medtronic, Boston Scientific holds advantages in innovation speed and focus. Medtronic's sprawling portfolio across multiple medical specialties creates complexity that slows decision-making. Boston Scientific's concentrated bet on interventional procedures allows faster pivots and clearer strategic focus. However, Medtronic's scale—nearly twice Boston Scientific's revenue—provides R&D resources and global reach that remain formidable.

Abbott presents a different challenge. Like Boston Scientific, Abbott has executed a successful transformation, particularly in structural heart and diabetes care. The companies compete head-to-head in several categories, often trading market share quarter by quarter. The competitive dynamic here isn't about clear superiority but incremental advantages—who launches next-generation products faster, who builds better physician relationships, who executes commercialization more effectively.

Johnson & Johnson's relationship remains complex—part competitor, part IP adversary, part potential acquirer. J&J's decision to spin off its consumer business to focus on pharmaceuticals and medical devices signals increased commitment to spaces where Boston Scientific operates. With enormous resources and the bitter memory of losing Guidant, J&J competes aggressively, particularly in electrophysiology.

The Verdict: Priced for Perfection but Positioned to Deliver

The weight of evidence tilts bullish, but with careful caveats. Boston Scientific has engineered remarkable transformation, built category-leading positions, and demonstrated execution excellence. The growth drivers—aging demographics, procedure adoption, international expansion—remain intact. Management has earned credibility through consistent delivery.

Yet the valuation leaves little room for error. At current prices, investors are paying for continued excellence, successful integration, and market share gains. Any disappointment could trigger significant multiple compression. The stock is a conviction buy for those who believe in medical technology's secular growth and Boston Scientific's execution ability, but it requires stomach for volatility and patience for multi-year value creation.

The most probable scenario: continued fundamental strength with periodic volatility as competitive dynamics shift and quarterly results fluctuate. Long-term investors who can withstand near-term turbulence should be rewarded as demographic tailwinds and innovation pipelines drive sustained growth. But this isn't a "safe" defensive healthcare holding—it's a growth stock that happens to make medical devices, with all the opportunities and risks that implies.

X. Epilogue & "If We Were CEOs"

Standing in Boston Scientific's Marlborough headquarters, looking out at the New England woods where the company's journey began, it's tempting to think the transformation is complete. From near-death to industry leader, from financial engineering disaster to innovation powerhouse—surely this is the happy ending. But Mike Mahoney knows better. In medical technology, standing still means falling behind. The next chapter isn't about recovery; it's about defining what's possible.

If we were running Boston Scientific, three frontiers would dominate our strategic thinking. First, the convergence of artificial intelligence and procedural medicine. Imagine FARAPULSE catheters that use machine learning to map cardiac tissue in real-time, identifying optimal ablation points with superhuman precision. Or WATCHMAN devices that predict stroke risk months before symptoms appear. The company that successfully integrates AI into medical devices won't just improve outcomes—it will render previous generations obsolete.

Second, the shift from treatment to prevention. Today's devices fix problems after they occur. Tomorrow's will prevent them entirely. Boston Scientific's acquisition of preventive monitoring companies hints at this direction, but the real opportunity is bigger: closed-loop systems that monitor, predict, and intervene automatically. A pacemaker that adjusts therapy based on activity patterns. A neurostimulator that prevents pain before it starts. The business model implications are profound—subscription-based healthcare that generates recurring revenue while improving outcomes.

Third, and most challenging: emerging market innovation. Not just selling Western products in developing countries, but creating entirely new categories for resource-constrained healthcare systems. Imagine ablation systems that work without expensive mapping equipment, or stroke prevention devices at one-tenth current costs. This isn't corporate social responsibility—it's accessing the next billion patients profitably.

The organizational challenges are equally complex. Boston Scientific must maintain entrepreneurial speed at $17 billion in revenue—a paradox that defeats most large companies. Our approach would be radical: split the company into autonomous units, each with its own P&L, development budget, and acquisition authority. Let the FARAPULSE team compete with the WATCHMAN team for resources. Create internal markets where the best ideas win funding. Accept that some units will fail—creative destruction inside the company is better than disruption from outside.

On capital allocation, we'd make a contrarian bet: while competitors chase artificial intelligence startups at astronomical valuations, we'd go deep on manufacturing innovation. The ability to produce complex medical devices at scale, with perfect quality, at declining costs—this unsexy capability becomes decisive as markets commoditize. Invest in automation, materials science, and supply chain resilience. Own the manufacturing moat while others chase software dreams.

The biggest decision facing Boston Scientific isn't strategic—it's existential. At $150 billion market cap, the company has entered the acquisition consideration set of big tech. Apple, Google, Amazon—each has healthcare ambitions and acquisition capacity that dwarfs medical device players. Does Boston Scientific remain independent, potentially becoming subscale as tech giants enter healthcare? Or does it seek a transformational combination—perhaps with a pharmaceutical giant creating integrated drug-device therapies?

Mahoney's assessment that "2024 was one of the best years in the history of Boston Scientific" isn't hyperbole—by every financial metric, the company has never been stronger. But the best leaders are paranoid in victory, knowing that success creates complacency. The competitive environment has never been more intense. Technological change has never been faster. Healthcare economics have never been more challenging.

Yet stepping back, what Boston Scientific has accomplished transcends financial metrics. Millions of patients live normal lives because WATCHMAN prevents strokes. Thousands avoid open-heart surgery thanks to transcatheter technologies. Chronic pain sufferers find relief through neuromodulation. The company's products don't just treat disease—they restore human dignity, letting people return to work, play with grandchildren, pursue dreams interrupted by illness.

This impact compounds over time. A stroke prevented saves not just immediate healthcare costs but decades of productivity. A successful ablation prevents progression to heart failure. A pain device eliminates opioid dependence. The full value Boston Scientific creates—medical, economic, social—is nearly impossible to calculate but undeniably enormous.

The final reflection brings us full circle to that soccer field in Natick. Pete Nicholas and John Abele didn't set out to build a $150 billion company. They saw physicians struggling with limited tools, patients suffering from invasive procedures, and imagined something better. That engineering mindset—seeing problems as opportunities, constraints as catalysts for innovation—remains Boston Scientific's true competitive advantage.

In an industry obsessed with disruption, Boston Scientific proves that sometimes the biggest value comes from persistent, incremental improvement. Each generation of products works a little better, treats a few more patients, causes fewer complications. Compounded over decades, these improvements transform medicine. It's not as exciting as breakthrough cures or revolutionary technologies. But for millions of patients whose lives depend on medical devices working perfectly every single time, this relentless pursuit of better is everything.

The next decade will test whether Boston Scientific can maintain this engineering excellence while adapting to technological upheaval. Can it integrate artificial intelligence without losing human judgment? Expand globally without sacrificing quality? Grow through acquisition without destroying culture? These aren't just business challenges—they're the questions that will determine whether Boston Scientific's best days remain ahead or behind.

What's certain is that the company's journey from struggling catheter manufacturer to medical technology leader offers lessons beyond business. It's a reminder that transformation is possible even from the deepest crisis. That betting everything on conviction sometimes pays off. That culture and execution matter more than strategy. And that in the end, the companies that succeed aren't necessarily the smartest or best-funded, but those that remain obsessed with solving real problems for real people.

As we look toward Boston Scientific's future, one thing is clear: the engineering of less-invasive medicine is far from complete. The opportunity to transform healthcare through innovation remains enormous. And for investors willing to embrace both the risks and rewards of medical technology leadership, Boston Scientific's story is far from over. It's just entering its most interesting chapter.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube