Penumbra Inc.: The Vacuum Cleaner for Your Brain

I. Introduction: When Minutes Mean Brain Cells

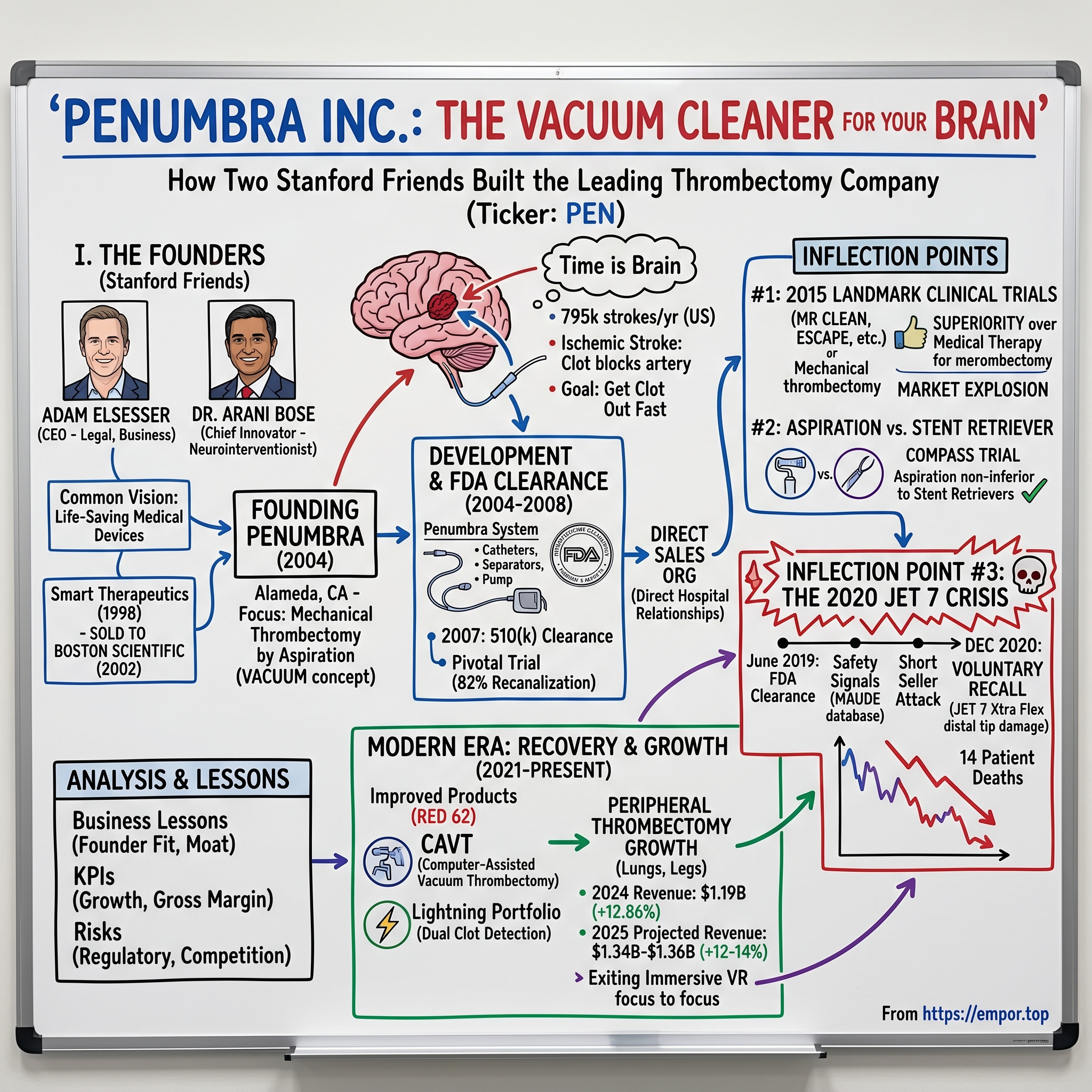

Picture a family gathered in a hospital waiting room at 2 a.m., hands clasped, faces etched with fear. Somewhere beyond those swinging doors, their grandmother lies motionless on a gurney, a blood clot the size of a pencil eraser lodged in an artery feeding her brain. Every minute that passes—every sixty seconds ticking away on the fluorescent clock—another 1.9 million neurons die. In stroke treatment, clinicians have a saying: "Time is brain."

Penumbra, Inc. (NYSE: PEN), the world's leading thrombectomy company, exists to compress those minutes into seconds. A vacuum cleaner for your brain? That's the innovation at Penumbra, a medical-device company that makes equipment to treat strokes and brain aneurysms.

The numbers tell a story of extraordinary growth. In 2024, Penumbra's revenue was $1.19 billion, an increase of 12.86% compared to the previous year's $1.06 billion. The Company projects total revenue for 2025 to be in the range of $1,340.0 million to $1,360.0 million, representing year over year growth of 12% to 14%. But beneath these figures lies a story of medical innovation, regulatory navigation, near-catastrophic crisis, and the relentless pursuit of better patient outcomes.

This is the story of how two best friends from Stanford University—a lawyer and a doctor—invented a technology that many believed was impossible, built a billion-dollar company from scratch, weathered a devastating product recall that threatened their life's work, and emerged stronger on the other side.

II. The Founders & Origin Story: When a Lawyer Met a Neurointerventionist

In the late 1990s, Adam Elsesser was practicing law at Shartsis Friese LLP in San Francisco. Before his work in the medical device industry, Adam was a partner in the law firm of Shartsis Friese LLP. He received a BA from Stanford University and a JD from Hastings College of the Law. But Elsesser harbored an entrepreneurial itch that legal briefs couldn't scratch.

His best friend from college, Arani Bose, had taken a different path entirely. Prior to founding Penumbra, Dr. Bose was an Assistant Professor of Radiology and Neurology at New York University (NYU) School of Medicine from 1997 to 2004, where he also had a clinical practice. While at NYU, Dr. Bose co-founded SMART Therapeutics. Dr. Bose received a B.A. from Stanford University and an M.D. from the University of Colorado School of Medicine with residency and fellowships at Yale University School of Medicine and NYU Medical Center.

This wasn't their first venture together. "I used to practice law, and my best friend from college, Dr. Arani Bose, was a practicing neuro-interventionist. In 1998 we formed our first business, Smart Therapeutics, which we sold in 2002 to Boston Scientific." At Smart Therapeutics, Dr. Bose developed the Neuroform Stent for the treatment of intracranial aneurysms and the Wingspan Stent for the treatment of intracranial atherosclerosis as well as led their respective international clinical trials that resulted in approval of both devices by the US FDA.

The successful exit to Boston Scientific proved something crucial: these two friends—one with business and legal acumen, the other with deep clinical expertise—could actually build, validate, and commercialize life-saving medical devices. They had found their playbook.

Two years later, they were ready for something bigger. CEO Adam Elsesser co-founded the Alameda, California-based business in 2004 with his best friend from college, Arani Bose, a doctor and Penumbra's chief innovator and director. We subsequently founded Penumbra in 2004 with a focus on developing a method to remove blood clots from the brain with aspiration, a concept many considered impossible at the time.

The company's name itself revealed their scientific focus. "Penumbra" refers to the salvageable brain tissue surrounding the core infarct during a stroke—the tissue that can still be rescued if blood flow is restored quickly enough. It was aspirational nomenclature: this company existed to save what could still be saved.

"We wanted to start a business that created products that would have a huge impact on patients and their families. Initially, we focused Penumbra on ischemic stroke. That's when there's a blood clot that gets lodged in an artery in your brain. The goal is to get the clot out as fast as possible. We developed a device to do that, with a treatment known as mechanical thrombectomy."

The founder-market fit here was exceptional. Bose wasn't just an academic researcher—he was a practicing neurointerventionist who performed these procedures, who knew intimately the limitations of existing tools, and who understood what physicians actually needed in their hands during the most critical moments of patient care. Elsesser brought the commercial discipline, regulatory savvy, and operational rigor to transform clinical insight into a scalable business.

Adam co-founded Penumbra and has served as Chief Executive Officer and a member of our board of directors since our inception in 2004, as Chairman of our board of directors since January 2015. Twenty years later, he remains at the helm—a rarity in Silicon Valley's age of founder departures and professional CEO transitions.

III. The Science of Stroke: Understanding the Battlefield

To appreciate what Penumbra built, one must first understand the enemy.

Ischemic stroke occurs when a blood clot blocks an artery supplying the brain, depriving neurons of oxygen and glucose. Despite recent advances in medical and mechanical therapies, ischemic stroke remains a debilitating and often intractable disease with few treatment options for effective acute intervention.

The statistics are staggering. According to the Centers for Disease Control and Prevention, approximately 795,000 individuals in the U.S. suffer from stroke annually, and about 87 percent of those are ischemic strokes—the type Penumbra's devices address. Stroke is the fifth leading cause of death in America and a leading cause of long-term disability. The economic burden, including healthcare costs and lost productivity, exceeds $50 billion annually.

The purpose of this clinical evaluation was to assess the safety and effectiveness of the Penumbra System in the revascularization of patients presenting with acute ischemic stroke secondary to intracranial large vessel occlusive disease. In this prospective, multicenter, single-arm study, 125 patients with neurological deficits as defined by a National Institutes of Health Stroke Scale score ≥8, presented within 8 hours of symptom onset, and an angiographic occlusion of a treatable large intracranial vessel were enrolled. Patients who presented within 3 hours from symptom onset had to be ineligible or refractory to recombinant tissue plasminogen activator therapy. All patients were followed clinically for 90 days postprocedure.

Before Penumbra, the treatment landscape was limited. Intravenous tissue plasminogen activator (IV tPA)—essentially a clot-dissolving drug—was the gold standard, but it worked best within a narrow time window and had significant limitations. Early mechanical devices like the MERCI retriever attempted to physically remove clots, but success rates were inconsistent.

Current treatment options in the United States are limited to thrombolytics such as recombinant tissue plasminogen activator, administered either intravenously or intra-arterially, or mechanical thrombectomy devices such as the MERCI clot retriever.

Penumbra's insight was deceptively simple but technically challenging: instead of grabbing the clot and pulling it out (like the MERCI retriever), why not vacuum it out? Aspiration—the medical term for suction—could potentially remove clots more completely and with less trauma to the delicate vessel walls.

It was an elegant concept. Making it work in the tiny, tortuous blood vessels of the human brain was another matter entirely.

IV. Early Product Development & FDA Breakthrough (2004-2008)

The first years were a grind of iterative engineering, animal studies, and regulatory strategizing. Penumbra, Inc. is an American medical device company headquartered in Alameda, California. The company was founded by Arani Bose and Adam Elsesser in 2004. It manufactures devices for interventional therapies to treat vascular conditions such as stroke and aneurysm.

The technical challenge was formidable. The blood vessels feeding the brain are small, fragile, and take serpentine paths through the skull. Any device entering this anatomy must be flexible enough to navigate curves, strong enough to withstand manipulation, and precise enough to apply suction without damaging vessel walls. And it must work quickly—because every minute of delay means more dead neurons.

Penumbra developed what would become known as the Penumbra System: an integrated platform of aspiration catheters, separators (to break up clots), and tubing connected to a vacuum pump. The FDA has granted 510(k) clearance for the Penumbra System, which is indicated for use in the revascularization of patients with acute ischemic stroke secondary to intracranial large vessel occlusive disease within eight hours of symptom onset. The Penumbra System is a package of tools used by neuro interventional specialists to remove occlusions from the large vessels of the brain that are causing an acute ischemic stroke. The Penumbra System is comprised of an aspiration platform containing multiple devices that are size-matched to the specific neurovascular anatomy allowing clots to be gently aspirated out of intracranial vessels.

The regulatory strategy was crucial. Rather than pursuing the more rigorous Premarket Approval (PMA) pathway—which requires extensive clinical trials demonstrating safety and effectiveness—Penumbra used the 510(k) process, which allows clearance based on "substantial equivalence" to existing devices.

"In the case of Penumbra, the original 2007 device was cleared under 510(k) using the Merci catheter as its predicate device, which itself was authorized based on evidence generated from nonrandomized, single-arm trials. The Merci device itself was cleared using the percutaneous catheter from Concentric (the Modified Concentric Retriever) as its predicate device, even though the latter device had a different indication."

The Penumbra System is a fully integrated system designed specifically for mechanical thrombectomy by aspiration that first received 510(k) clearance by the U.S. Food & Drug Administration in December 2007. This was a watershed moment—three years of development had yielded regulatory blessing to commercialize.

San Leandro, CA - Penumbra, Inc. recently announced the 510(k) clearance by the US Food and Drug Administration of the Penumbra System, which is indicated for use in the revascularization of patients with acute ischemic stroke secondary to intracranial large vessel occlusive disease within 8 hours of symptom onset. Penumbra will commence the immediate commercialization of the device in the United States.

The pivotal trial supporting this clearance demonstrated compelling results. The first results, presented in 2009 in The Penumbra Pivotal Stroke Trial, showed successful revascularization, with high thrombolysis in myocardial infarction – TIMI score (2–3), in 82% of patients.

An 82% recanalization rate was remarkable for the era—proof that aspiration thrombectomy could restore blood flow in the vast majority of cases. The scientific foundation was laid. Now came the hard work of commercialization.

V. The Long Road to Profitability (2008-2015)

Having a breakthrough product is only half the battle. Convincing thousands of physicians to adopt an entirely new technique—and training them to use it effectively—is another challenge entirely.

Our sales strategy focuses directly on hospitals and the physicians who perform the procedures, with specific approaches tailored to each medical specialty involved. Over the years, Penumbra's products, especially our newer launches, have gained significant recognition, easing the introduction process compared to the early days of the company.

Penumbra made a strategic decision early on to build a direct sales organization rather than relying on distributors. This was more expensive and operationally complex, but it gave the company direct relationships with physicians, real-time feedback on product performance, and control over the training process. For a device category that required significant physician education, this control proved invaluable.

Penumbra sells its products to hospitals and healthcare providers primarily through its direct sales organization in the U.S., most of Europe, Canada and Australia, and through distributors in select international markets.

The company expanded methodically, both geographically and across product categories. While stroke thrombectomy remained the flagship, Penumbra began developing products for treating aneurysms (via embolization coils) and eventually expanded into peripheral vascular—blood clots outside the brain, in the arms, legs, and lungs.

"Then we started looking at other areas within the neurovascular world, searching for ways to treat brain aneurysms and what's called the peripheral vasculature, which is the arteries and veins outside of the heart and the brain. We have a product that uses aspiration, or suction, to remove blood clots there. These clots can be limb- and life-threatening, and traditional treatment typically involves administering drugs to slowly dissolve them. That can take days, and may result in costly ICU stays."

Penumbra was profitable from 2012-2014—a notable achievement for a medical device company with significant R&D investments and a direct sales model. But the founders exercised remarkable discipline, resisting the temptation to go public at the first opportunity.

"Most healthcare technology companies go public long before they have nine-digit revenue. Why not do this earlier?"

The answer reveals much about Elsesser and Bose's philosophy: they wanted to be certain they had built something durable before facing the pressures of public markets.

"I've always run this business with the thought that we should be profitable, and I think we've done a credible job over the years of being disciplined. But, as I said, we're in a particular moment of time with so many different product families that have great opportunities to expand, so we're obviously going to invest in those product lines. The IPO really gives us the freedom to do that in a very controlled way."

VI. The 2015 IPO: Ringing the Bell

In September 2015, Penumbra finally went public. In September, the co-founders took Penumbra public, demonstrating that even in choppy markets, entrepreneurs who find scientific innovations can reap big rewards.

The timing was strategic. "Last year we brought in Fidelity in anticipation of entering this next phase. We had just expanded from our initial focus on neurovascular to peripheral vascular, and hired an entire dedicated salesforce pretty quickly to take advantage of that opportunity. We had gotten to know the folks over at Fidelity and clearly felt comfortable that we shared a similar vision for the next phase of Penumbra."

"Tomorrow morning you'll be ringing the New York Stock Exchange's opening bell. Who will be with you? We have invited a patient who was treated with our flagship stroke product to ring the bell, in order to remind us and investors that what we're really doing is for patients like her."

This gesture—inviting a stroke survivor rather than investment bankers or celebrity executives—encapsulated the company's culture. Penumbra positioned itself not primarily as a stock to trade, but as a mission to pursue. The patients came first; the financial outcomes would follow.

The IPO raised capital to accelerate expansion and R&D, but it also marked a transition. From this point forward, the company would face quarterly earnings scrutiny, short seller attention, and all the pressures that come with public ownership.

VII. INFLECTION POINT #1: The 2015 Landmark Clinical Trials

The year of Penumbra's IPO also happened to be the most important year in the history of stroke treatment. Five pivotal randomized controlled trials—MR CLEAN, ESCAPE, SWIFT PRIME, EXTEND-IA, and REVASCAT—fundamentally transformed the standard of care.

In 2015, The New England Journal of Medicine released the results of five separate multicenter, prospective, randomized trials between January and September 2015. Each trial supports the efficacy and safety of mechanical thrombectomy in the treatment of acute ischemic stroke. The results of these trials—MR CLEAN, EXTEND-IA, ESCAPE, SWIFT PRIME, and REVASCAT—demonstrated conclusively that mechanical thrombectomy improved patient outcomes compared to medical therapy alone.

The pivotal MR CLEAN trial was first presented at WSC on 25 October 2014, marking a turning point in the treatment of ischaemic stroke. This groundbreaking study highlighted the benefits of EVT for large vessel occlusion (LVO) strokes, and it paved the way for global changes in stroke management.

In 2015, multiple landmark trials (MR CLEAN, ESCAPE, SWIFT PRIME, REVASCAT, and EXTEND IA) established the superiority of endovascular thrombectomy over medical management for the treatment of anterior circulation large vessel occlusion strokes.

New evidence from MR CLEAN, ESCAPE, EXTEND-IA, SWIFT PRIME, REVASCAT, THERAPY, and THRACE has demonstrated an overwhelming benefit from endovascular intervention, preferably with stentriever-mediated mechanical thrombectomy, for the treatment of AIS secondary to LAO. Thus, a new standard of care for AIS management has been established.

For Penumbra, this was a rising tide that lifted all boats. While the trials primarily used stent retriever devices (from Medtronic and Stryker), they validated the entire concept of mechanical thrombectomy. Suddenly, every hospital system needed to offer this life-saving intervention. The addressable market exploded virtually overnight.

Mechanical thrombectomy (MT) is the current standard of care for large vessel occlusion–acute ischemic stroke (LVO-AIS) treatment. Results from multiple randomized controlled trials support the safety and efficacy of MT.

In 2016, roughly 30,000–40,000 thrombectomies were performed across the globe. By 2020, this number grew substantially to more than 100,000 annual procedures, driven by better access, expanded treatment windows, and the broadening criteria for patient eligibility.

VIII. INFLECTION POINT #2: Aspiration vs. Stent Retriever

The 2015 trials had validated mechanical thrombectomy, but they hadn't settled a fierce debate within the neurointerventional community: Which technique was better—aspiration (Penumbra's approach) or stent retrievers (Medtronic and Stryker's approach)?

Stent retrievers, most notably the Solitaire (ev3/Covidien, Irvine, CA, USA) and the Trevo (Stryker), were shown to be superior to first-generation devices in terms of achieving higher rates of favorable clinical outcomes.

Penumbra needed to prove that aspiration-first was at least as good as stent retrievers—and potentially better in some respects. The company invested heavily in clinical trials to generate this evidence.

Penumbra announced the presentation of the results of the COMPASS Trial, an independent, prospective, multi-center randomized trial that showed the use of Penumbra's aspiration system was non-inferior to stent retrievers for patients with acute ischemic stroke. The COMPASS Trial results were featured in the main event plenary session at the International Stroke Conference and add to the growing body of evidence demonstrating Penumbra's aspiration system is an effective frontline thrombectomy approach.

"The COMPASS Trial met its primary objective, demonstrating that acute ischemic stroke patients treated with the ADAPT approach do not have inferior outcomes to those treated with a first-line stent retriever." The data showed that the ADAPT technique was non-inferior to stent retrievers for treatment of large vessel occlusions: 52 percent of patients treated with Penumbra's aspiration system achieved the primary endpoint of modified Rankin Score (mRS) 0-2 at 90 days compared with 49 percent of patients treated with stent retrievers.

Citing results of COMPASS, ASTER, and the 3D Randomized Trial, the American Heart/American Stroke Association guidelines endorse frontline aspiration thrombectomy as noninferior to stent retrievers.

This endorsement from the most authoritative stroke guidelines was crucial. Penumbra could now legitimately claim its approach was a scientifically validated first-line option. "Both aspiration-first (including the subsequent use of stent retriever) and primary stent retriever thrombectomy approaches are equally effective in achieving good clinical outcomes. Our study suggests that direct aspiration with or without subsequent use of stent retriever is a safe and effective" approach.

The market increasingly adopted a combined approach—using aspiration as the first-line technique and adding stent retrievers when needed—which played to Penumbra's strengths while creating cross-selling opportunities.

IX. INFLECTION POINT #3: The 2020 JET 7 Crisis

Every company faces moments that define its character. For Penumbra, that moment arrived in 2020, when its latest and most advanced stroke catheter became the subject of a devastating recall.

The Product and the Promise

Penumbra announced U.S. commercial availability of the Penumbra System's most advanced technology – the Penumbra JET 7 Reperfusion Catheter with XTRA FLEX technology – at the Society of NeuroInterventional Surgery (SNIS) 16th Annual Meeting in Miami. Penumbra JET 7 with XTRA FLEX technology is used with the Penumbra ENGINE in the fully integrated Penumbra System – an aspiration-based mechanical thrombectomy system that enables physicians to extract thrombus in acute ischemic stroke patients.

The JET 7 with Xtra Flex was supposed to be Penumbra's crowning achievement—a catheter with enhanced flexibility to navigate the most challenging brain anatomy while maintaining powerful aspiration. It cleared the FDA via 510(k) in June 2019 and quickly became a commercial success.

The Emerging Safety Signals

The first known death linked to JET 7 with Xtra Flex was reported to the FDA Manufacturer and User Facility Device Experience (MAUDE) database in October 2019, 4 months after 510(k) clearance, and other complications followed. By July 2020, Penumbra had alerted clinicians to issues with the device's distal tip. Thereafter, the researchers say, the company reported record-high sales in its October 2020 earnings call.

The timeline became controversial. Critics alleged that Penumbra knew about problems but continued aggressive sales. The company maintained it was working with the FDA and clinicians to address the issues through labeling updates and warnings.

The Short Seller Attack

Into this situation stepped Gabriel Grego, managing partner at Quintessential Capital Management, a short-selling hedge fund. When Gabriel Grego, the founder of short-selling hedge fund Quintessential Capital Management, launched his first volley at medical device maker Penumbra by claiming the catheters it produces were not safe, the stock didn't just yawn. It ended the day up almost 8 percent. But on Tuesday, less than a month later, Grego came back with a second short report with even more shocking accusations.

Shares of Penumbra were sliding after short-seller Quintessential Capital Management released another critical report on the California-based medical devices maker. The firm first began targeting Penumbra in November. The California-based medical devices maker denied Quintessential Capital's "baseless" allegations.

The attack intensified with allegations about fake researchers and scientific misconduct. Penumbra pushed back forcefully, saying that since its founding in 2004 its "innovative medical devices have helped saved the lives of hundreds of thousands of patients facing life-threatening medical conditions." "This attack by sleazy short sellers QCM reads like an internet conspiracy written by teenagers. It is impossible to dispute the facts, because there are no facts," the company said in an email. "Penumbra feels very comfortable stating that none of the allegations in this short sellers' diatribe are accurate."

The Recall

Regardless of the short seller drama, the safety concerns were real. On December 17, 2020, Penumbra recalled the Penumbra JET 7 Xtra Flex because the catheter may become susceptible to distal tip damage during use. The FDA has received over 200 medical device reports (MDRs) associated with the JET 7 Xtra Flex catheter, including deaths, serious injuries, and malfunctions. Twenty of these MDRs describe 14 unique patient deaths, which include reports from different reporting sources for a single adverse event. Other MDRs describe serious patient injury, such as vessel damage, hemorrhage, and cerebral infarction.

Its manufacturer, Penumbra, voluntarily recalled the device in December 2020 due to the potential for distal tip damage during use, a move that the US Food and Drug Administration categorized as Class I, its most serious type.

The recall, which Penumbra originally announced on Dec. 15, 2020, involved more than 30,000 distributed units of its Jet 7 Reperfusion Catheters with Xtra Flex Technology after the company received 14 reports of death related to the device.

The saga caught his group's attention in part because of how widely JET 7 with Xtra Flex is used—the recall covered over 22,000 devices across the United States.

The Broader Questions

The JET 7 crisis raised profound questions about the FDA's 510(k) approval pathway and post-market surveillance. JET 7 is just one of thousands of devices the FDA clears annually under the 510(k) program. Within the past 9 years, approximately 13% have been subject to any recall and 1% subject to a Class I recall.

Critics argued that the system allowed potentially dangerous devices to reach patients without adequate pre-market testing. Defenders countered that the pathway enables faster innovation and that post-market surveillance, while imperfect, generally catches problems before they become widespread.

For Penumbra, the crisis was a crucible. The stock plunged. The company's reputation, carefully built over sixteen years, was under assault. Everything they had built was suddenly at risk.

X. Modern Era: Recovery and Growth (2021-Present)

The mark of a great company is not whether it faces adversity, but how it responds. Penumbra's post-recall trajectory suggests the organization is more resilient than its critics believed.

The company moved quickly to develop improved products. Penumbra announced U.S. Food and Drug Administration (FDA) 510(k) clearance and commercial availability of the RED 62 Reperfusion Catheter, the latest addition to the company's comprehensive Penumbra System. RED 62 is designed to navigate complex distal vessel anatomy and deliver powerful aspiration for the removal of blood clots in acute ischemic stroke patients with large vessel occlusions.

"With the continued success of aspiration thrombectomy, physicians asked us to address navigation in more challenging distal vessels. RED 62 builds on our previous design generations, continuing our efforts to maximize both trackability and aspiration power," said Adam Elsesser. "This is the first catheter in the RED series, which will provide physicians with the broadest portfolio of aspiration thrombectomy solutions for stroke management."

The company also expanded aggressively into peripheral vascular thrombectomy—blood clots in the lungs (pulmonary embolism) and legs (deep vein thrombosis). Penumbra announced U.S. Food & Drug Administration (FDA) clearance and launch of Lightning Flash, which the company reports is the most advanced mechanical thrombectomy system on the market to address venous and pulmonary thrombus. Next generation technology combines superior catheter design with the latest dual clot detection innovation.

In 2020, Penumbra became the first company to offer computer-aided technology with Lightning 12. Lightning 12's clot detection capabilities are made possible by Penumbra's patented clot detection algorithm, which enables the Lightning system to aspirate under nearly pure vacuum when the catheter is actively interacting with thrombus.

Now in 2023, the next generation of Lightning is here. Lightning Flash, launched in January 2023, is advancing the field of mechanical thrombectomy forward once again. Lightning Flash features dual clot detection algorithms, improving upon the singular algorithm featured in Lightning 12 and 7. One algorithm detects clot based on pressure differentiation, while the other algorithm detects the interaction of flow through the system.

The innovation continued with Lightning Bolt 7 for arterial thrombectomy. Lightning Bolt 7 received FDA clearance and became available in March 2023. It is part of Penumbra's Indigo System with Lightning portfolio, which are the only computer-aided thrombectomy systems currently available in the United States.

Recent Financial Performance

The numbers tell the story of a company that has not just recovered but accelerated:

Adjusted revenue of $1,200.4 million, excluding the $5.8 million impact of the Italian government's payback provision pertaining to prior years, an increase of 13.4% in adjusted and adjusted constant currency compared to the full year 2023. Revenue of $315.5 million for the fourth quarter of 2024, an increase of 10.8% in reported and constant currency compared to the fourth quarter of 2023.

The Company projects the U.S. thrombectomy franchise will grow 19% to 20% year-over-year, driven primarily by its computer assisted vacuum thrombectomy (CAVT) products.

The Company expects gross margin expansion of at least 100 basis points in 2025, to more than 67% for the full year, and operating margin expansion to a range of 13% to 14% of revenue for full year 2025.

Revenue of $324.1 million in the first quarter of 2025, an increase of 16.3% or 16.9% in constant currency, compared to the first quarter of 2024. U.S. Thrombectomy revenue of $187.9 million in the first quarter of 2025, an increase of 25.0% compared to the prior year.

The clinical evidence continues to accumulate. Penumbra today announced positive results from its landmark STORM-PE randomized controlled trial. "For the first time, we have prospective, level 1 evidence demonstrating that CAVT with anticoagulation is superior to anticoagulation alone," said James F. Benenati, MD, FSIR, chief medical officer at Penumbra.

Penumbra has appointed Shruthi Narayan as its new President, effective September 1, 2025. Narayan, who brings 20 years of medical device industry experience, will report to Adam Elsesser, who continues as chairman and CEO. Previously serving as president of Penumbra's interventional business, Narayan joined the company in 2013 and has led significant growth in both neuro and vascular franchises. Her experience includes roles at Medtronic and extensive work in engineering, regulatory affairs, and cardiovascular sales.

XI. Product Portfolio Deep Dive

Penumbra's strength lies in its comprehensive, integrated approach to thrombectomy. Rather than selling individual devices, the company offers complete systems designed to work together.

Neuro Thrombectomy: The Core Franchise

The Reperfusion Catheters and Separators are indicated for use in the revascularization of patients with acute ischemic stroke secondary to intracranial large vessel occlusive disease within 8 hours of symptom onset. Patients who are ineligible for intravenous tissue plasminogen activator (IV t-PA) or who fail IV t-PA therapy are candidates for treatment.

The Penumbra System includes the RED catheter family, the ENGINE aspiration pump, and various accessories. It also provides access products, including guide catheters and the Penumbra distal delivery catheters under the Neuron, Neuron MAX, BENCHMARK, BMX, DDC, MIDWAY, and PX SLIM brands; Penumbra System, an integrated mechanical thrombectomy system comprising reperfusion catheters and separators, the 3D Revascularization device, aspiration tubing, and aspiration pump.

Peripheral Thrombectomy: The Growth Engine

The company offers peripheral thrombectomy products, including the Indigo System for power aspiration of thrombus in the body; Lightning Flash, a mechanical thrombectomy system; Lightning Bolt 7, an arterial thrombectomy system.

In 2014, Penumbra broke into the peripheral thrombectomy space with the release of the first Indigo System catheters, the 5-F CAT5 catheter and the 3-F CAT3 catheter. These were quickly followed by the release of the 8-F CAT8 and 6-F CAT6 in 2015. These first-generation catheters were groundbreaking, as they offered continuous aspiration, differentiating them from manual syringe-based devices and lytic-based approaches. These catheters were the first step in the mechanical thrombectomy journey that Penumbra continues to this day.

Penumbra's Lightning devices are the only computer-aided mechanical thrombectomy devices on the United States market. The combination of dual clot detection algorithms and MaxID technology enable Lightning Flash to be minimally invasive and maximally effective.

Embolization Products

For treating aneurysms and other vascular malformations, Penumbra offers detachable coils that physicians deploy to fill and seal dangerous blood vessel defects. These complement the thrombectomy portfolio by addressing different aspects of neurovascular disease.

The Immersive Healthcare Exit

Not every diversification succeeds. Penumbra will discontinue its Immersive Healthcare business, which made virtual reality-based exercises for rehabilitation and mindfulness. CEO Adam Elsesser told investors the company's focus needs to be on its core thrombectomy business as it cut its sales forecast for 2024.

The Immersive Healthcare business includes a suite of virtual reality products that Penumbra acquired in 2021, including VR-based rehabilitation and mindfulness exercises. Penumbra said in the Aug. 20 WARN letter that it will "permanently discontinue" the segment due to "changing business needs."

Loss from operations of $81.0 million, which includes $110.3 million of one-time non-cash impairment and inventory write-down charges related to its Immersive Healthcare assets, and non-GAAP income from operations of $31.7 million in the second quarter of 2024.

The VR write-down was a painful reminder that even well-intentioned diversification can fail. Management's decision to exit decisively and return focus to core thrombectomy demonstrated discipline, even if the write-down was expensive.

XII. Competitive Landscape & Market Position

The mechanical thrombectomy market is intensely competitive, dominated by a handful of large players. Market players such as Stryker, Medtronic, Terumo Corporation, and Penumbra Inc. accounted for a major portion of the market share in 2024.

Medtronic, Stryker, and Penumbra, Inc. are the top players in the market.

The global mechanical thrombectomy devices market features intense competition among key players vying for market share. Established companies like Medtronic, Stryker, and Penumbra continue to dominate, leveraging their extensive R&D capabilities and broad product portfolios.

Competitive Positioning

- Medtronic leads in stent retrievers with its Solitaire line, leveraging massive scale and hospital relationships.

- Stryker competes aggressively in both stent retrievers (Trevo) and has expanded through acquisitions—in February 2025, Stryker Corporation completed its USD 4.9 billion acquisition of Inari Medical, expanding its thrombectomy portfolio to include peripheral vascular applications.

- Penumbra differentiates through its aspiration-first approach and computer-aided technology.

The Solumbra technique utilizes a stent and an aspiration retriever simultaneously, with the original combination being Medtronic's Solitaire FR and Penumbra's reperfusion catheter. This ensures the removal of thrombus fragments during stent retrieval.

Market Size and Growth

The Global Neurovascular Thrombectomy Devices Market is expected to reach USD 0.82 billion in 2025 and grow at a CAGR of 6.30% to reach USD 1.14 billion by 2030.

By product type, stent retrievers led with 54.45% mechanical thrombectomy devices market share in 2024, whereas large-bore aspiration catheters are forecast to expand at 7.23% CAGR to 2030. By end user, tertiary-care hospitals held 62.34% share of the mechanical thrombectomy devices market size in 2024.

North America held the largest share of the thrombectomy devices market in 2024, with a share of 34%, because of significant investments in healthcare infrastructure, technological innovation, rising demand for minimally invasive procedures, a growing elderly population, and a rise in cardiovascular disorders. In the United States, 3 classes of mechanical thrombectomy devices were cleared by the Food and Drug Administration: stent retrievers in 2012, coil retrievers in 2004, and aspiration devices in 2008.

XIII. Porter's Five Forces Analysis

| Force | Assessment | Analysis |

|---|---|---|

| Threat of New Entrants | Low-Medium | High regulatory barriers (FDA 510(k) clearance still requires substantial evidence), significant R&D investment ($192M in 2024), and critical physician training/relationships. However, the 510(k) pathway is more accessible than PMA, and emerging players like Rapid Medical are entering. |

| Bargaining Power of Suppliers | Low | Penumbra manufactures in-house, reducing dependency. Standard medical-grade materials with multiple sources. |

| Bargaining Power of Buyers | Medium | Hospital systems and GPOs have negotiating leverage, but stroke is emergent—physicians choose devices based on clinical preference, not price. Brand loyalty among trained operators creates stickiness. |

| Threat of Substitutes | Low-Medium | IV tPA remains first-line for eligible patients, but mechanical thrombectomy is now standard of care for large vessel occlusions. No true substitute for mechanical clot removal in appropriate patients. Future innovation in clot-dissolving drugs possible but not imminent. |

| Competitive Rivalry | High | Intense competition with Medtronic, Stryker, and J&J/Cerenovus. Continuous product innovation required. Stryker's acquisition of Inari signals consolidation. |

Overall Assessment: Moderately attractive industry with high barriers to entry but intense competition among established players. Penumbra's counter-positioning through aspiration technology provides meaningful differentiation.

XIV. Hamilton's 7 Powers Analysis

| Power | Present? | Analysis |

|---|---|---|

| Scale Economies | Developing | Revenue of $1.2B provides manufacturing scale, but competitors like Medtronic have superior scale. Penumbra is the clear leader in aspiration but not the overall market leader. |

| Network Effects | Weak | Limited direct network effects in medical devices. Physician training creates some community effects, but not true platform dynamics. |

| Counter-Positioning | Strong | Penumbra's aspiration-first approach vs. Medtronic/Stryker's stent retriever dominance creates meaningful differentiation. Incumbents would need to cannibalize existing product lines to compete fully in aspiration. |

| Switching Costs | Medium-Strong | Physician training on specific devices, hospital capital equipment (aspiration pumps), procedural familiarity, and integrated system design all create meaningful switching friction. |

| Branding | Medium | Strong reputation in the neurointerventional community. Adam Elsesser remains a visible founder-CEO. However, the 2020 recall damaged trust and required rebuilding. |

| Cornered Resource | Strong | Dr. Arani Bose as co-founder and chief innovator represents unique clinical expertise. Patent portfolio provides protection. Deep physician relationships built over 20 years. |

| Process Power | Developing | In-house manufacturing with quality systems, though the 2020 recall raised questions. Continuous product iteration culture is strong, with multiple new products annually. |

Primary Power: Counter-positioning through aspiration technology differentiation

Secondary Power: Cornered resource through founder expertise and patent portfolio

XV. Business & Investing Lessons

1. Founder-Market Fit Matters Enormously

The Elsesser-Bose partnership—combining business/legal acumen with physician-innovator clinical expertise—represents the ideal template for medical device entrepreneurship. Bose wasn't just advising; he was performing procedures and understanding the limitations of existing tools in real-time.

2. Platform Strategy Creates Switching Costs

By building integrated systems (catheters + pumps + accessories) rather than individual devices, Penumbra created meaningful switching friction. Once a hospital invests in Penumbra pumps and physicians are trained on Penumbra workflows, switching to competitors becomes genuinely difficult.

3. Clinical Evidence is the Ultimate Moat

Penumbra's investment in trials like COMPASS, COMPLETE, and STORM-PE generated the evidence base that convinced guideline committees and hospitals. In medical devices, published data in peer-reviewed journals is the currency of adoption.

4. Crisis Management Defines Character

The JET 7 recall was Penumbra's crucible. The company's response—voluntary recall, transparent communication, rapid development of improved products—demonstrated organizational resilience. The stock recovered, physicians continued using Penumbra products, and the company emerged stronger.

5. Patience with Profitability

Penumbra was profitable from 2012-2014, but the founders waited until 2015 to go public. This patience allowed them to build a durable product portfolio and organizational capability before facing public market pressures.

6. Know When to Exit Non-Core Businesses

The Immersive Healthcare write-down was painful, but management's willingness to acknowledge the failure and return focus to core thrombectomy demonstrated discipline. Diversification without clear strategic fit can destroy value.

XVI. Key Performance Indicators for Ongoing Monitoring

For investors tracking Penumbra's ongoing performance, three KPIs matter most:

1. U.S. Thrombectomy Growth Rate

U.S. Thrombectomy revenue of $187.9 million in the first quarter of 2025, an increase of 25.0% represents the core growth engine. This metric captures both market share gains and overall procedure growth. The company has guided for 20-21% growth in 2025—any sustained deceleration would signal competitive pressure or market saturation.

2. Gross Margin Trajectory

Gross profit for the first quarter of 2025 was $215.9 million, or 66.6% of total revenue. The improvement in gross margin was primarily driven by favorable product mix across our regions and productivity improvements. Gross margin expansion toward 67%+ demonstrates both pricing power and operational efficiency. Medical device gross margins typically exceed 60%, so Penumbra's trajectory here is important for long-term profitability.

3. Operating Margin Expansion

The company targets 13-14% operating margin for 2025. As revenue scales and the Immersive Healthcare drag disappears, operating leverage should accelerate. This metric captures the company's ability to translate topline growth into bottom-line profitability.

XVII. Risks & Considerations

Regulatory Risk

The FDA's 510(k) pathway remains a source of both opportunity and vulnerability. JET 7 is just one of thousands of devices the FDA clears annually under the 510(k) program. Within the past 9 years, approximately 13% have been subject to any recall and 1% subject to a Class I recall. Any future product recall would damage trust and potentially slow growth.

Competitive Intensity

Stryker's $4.9 billion acquisition of Inari Medical signals aggressive competitive positioning. Partnerships, acquisitions, and product launches are frequent strategies employed to expand market presence. Factors such as clinical efficacy, safety, and ease of use remain crucial in shaping competitive dynamics.

Geographic Concentration

The United States represented 77.2% of adjusted total revenue. Heavy reliance on the U.S. market creates vulnerability to domestic regulatory changes and reimbursement pressure.

China Exposure

It attributed the decrease to a reduction in business in China—reflecting broader geopolitical and market access challenges in the world's second-largest healthcare market.

Key Person Risk

Adam Elsesser has led the company since its 2004 founding. While Penumbra has appointed Shruthi Narayan as its new President, effective September 1, 2025, the eventual CEO transition will be a critical moment.

XVIII. Bull and Bear Cases

Bull Case: The CAVT Revolution

Penumbra's computer-assisted vacuum thrombectomy represents a genuine technological leap. "Lightning Flash will fundamentally change how blood clots are removed from the body," said Adam Elsesser. If CAVT becomes the standard of care—and STORM-PE provides Level 1 evidence supporting this—Penumbra's first-mover advantage in AI-assisted thrombectomy could drive sustained share gains.

The peripheral vascular opportunity is enormous. Pulmonary embolism alone causes 100,000+ U.S. deaths annually. "In the U.S., there are more than 1 million cases of blood clots in the body, resulting in more than 100,000 deaths. Furthermore, blood clots in the arms and legs are often associated with high amputation rates. Quick diagnosis and treatment can often result in a positive outcome. However, currently, only about 10% of these patients are treated with interventional approaches." If interventional penetration increases—as it almost certainly will—Penumbra is positioned to capture significant share.

Bear Case: Competitive Encirclement

Medtronic and Stryker have vastly greater resources. Stryker's Inari acquisition gives it a powerful peripheral vascular platform to compete with Penumbra's Indigo/Lightning portfolio. Medtronic's scale and hospital relationships could eventually erode Penumbra's neuro position.

The 2020 recall demonstrated that product quality issues can emerge unexpectedly. Any future safety problems would compound the reputational damage and potentially invite regulatory scrutiny of the entire product line.

Operating margin expansion requires continued gross margin improvement and operating leverage. If competitive pricing pressure intensifies or new product launches underperform, the path to 15%+ operating margins may prove elusive.

XIX. Conclusion: The Penumbra Playbook

Twenty years after two Stanford friends decided to build a vacuum cleaner for the brain, Penumbra stands as a testament to the power of founder-led innovation in medical devices.

The company's trajectory offers lessons that transcend the specifics of thrombectomy: build integrated systems rather than standalone products; invest relentlessly in clinical evidence; maintain founder discipline through booms and crises; know when to double down and when to exit.

Our broad portfolio, which includes computer assisted vacuum thrombectomy (CAVT), centers on removing blood clots from head-to-toe with speed, safety and simplicity. By pioneering these innovations, we support healthcare providers, hospitals and clinics in more than 100 countries, working to improve patient outcomes and quality of life.

The story is far from over. The peripheral vascular opportunity remains largely untapped. CAVT technology continues to evolve. New indications and geographies beckon.

But perhaps the most important metric isn't found in any financial statement. It's the grandmother who walked out of the hospital, the father who made it to his daughter's wedding, the colleague who returned to work—all because a blood clot was vacuumed from an artery within that critical window when salvageable tissue remained.

That's the penumbra they're saving. And that's why the story matters.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube