Eversource Energy: The New England Power Play

I. Introduction & Episode Roadmap

Picture this: It's February 2024, and across Connecticut, electric bills are landing in mailboxes like financial grenades. Standard service rates have just doubled to 24.2 cents per kilowatt-hour. Town halls are packed with furious customers. State legislators are calling emergency hearings. The villain in everyone's crosshairs? Eversource Energy—New England's largest energy delivery company, serving 4.4 million customers across Connecticut, Massachusetts, and New Hampshire with $12 billion in annual revenue.

Yet here's the paradox that defines Eversource: Everyone needs them, nobody loves them, and they're essentially guaranteed to make money regardless. It's the ultimate monopoly business model—regulated, essential, and perpetually controversial. How did a collection of 19th-century local utilities, some dating back to gas lamp era, evolve into this dominant force that controls the energy lifelines of New England?

This is a story about power—literal and figurative. It's about how small-town electric companies built by local entrepreneurs merged, acquired, and maneuvered their way into becoming a regional behemoth. It's about the delicate dance between public service and private profit, between infrastructure investment and rate affordability, between climate ambitions and economic reality.

The journey from gas lamps to grid dominance reveals fundamental truths about American capitalism, regulatory capture, and the impossibility of pleasing everyone when you control something everyone needs. We'll explore how Eversource navigated deregulation, doubled down through mega-mergers, gambled billions on offshore wind only to retreat, and now faces an existential question: Can a 150-year-old utility model survive the energy transition?

What makes this particularly fascinating is that Eversource operates in three of America's most politically engaged, climate-conscious states. They're trying to modernize century-old infrastructure while keeping rates affordable, transition to clean energy while maintaining reliability, and satisfy Wall Street while serving Main Street. It's an impossible balancing act that they perform daily, with mixed results.

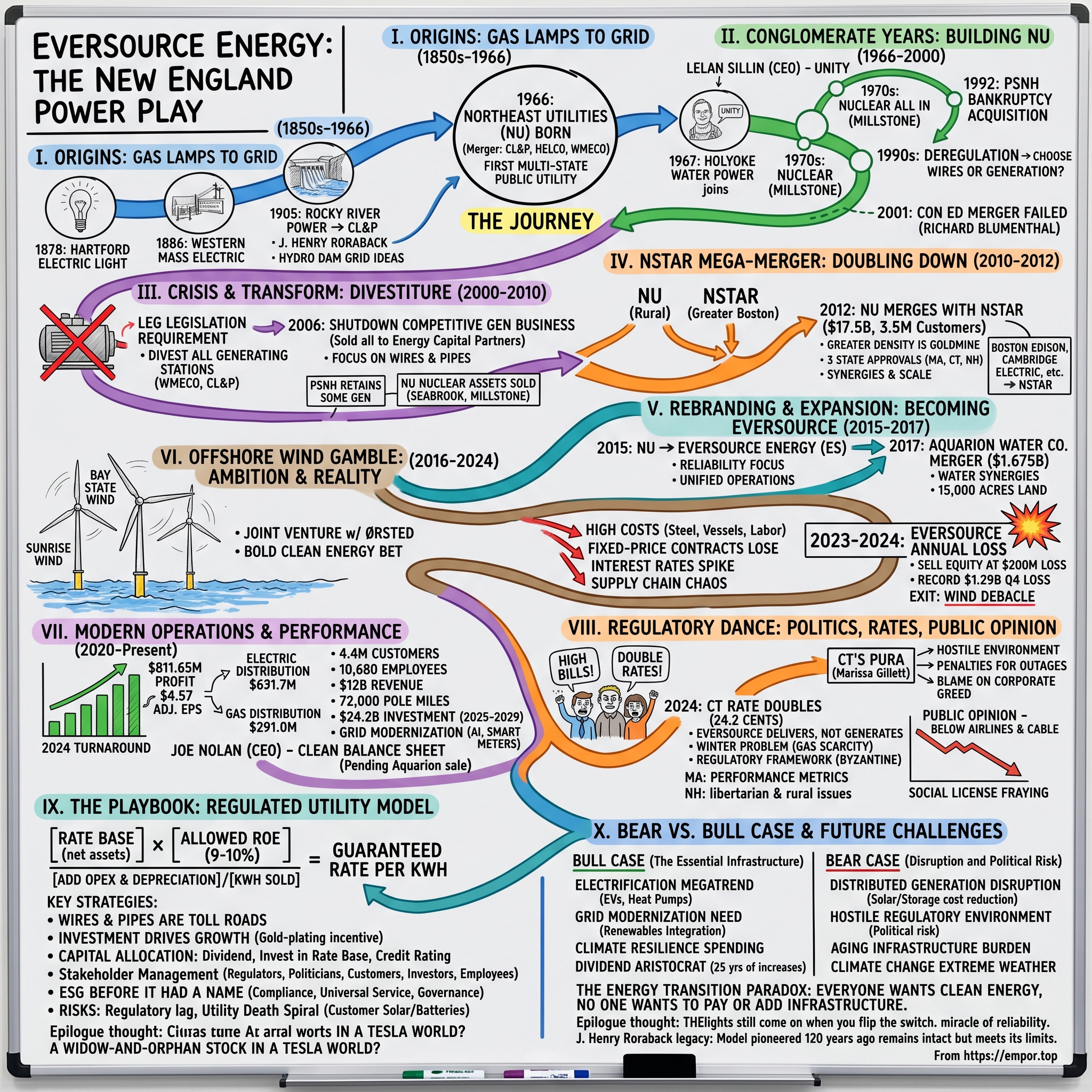

II. Origins: From Gas Lamps to Grid Formation (1850s–1966)

The story begins not with grand vision but with gaslight. In 1878, a group of Hartford businessmen gathered in a downtown office, watching as Thomas Edison's incandescent bulbs were demonstrated for the first time in Connecticut. Within months, they formed the Hartford Electric Light Company, convinced that electricity would replace gas lamps on every street corner. They were right about the technology but wrong about the timeline—it would take decades.

Meanwhile, in western Massachusetts, the Holyoke dam was generating more mechanical power than local mills could use. In 1886, entrepreneurs formed the Western Massachusetts Electric Company to sell this excess power, pioneering the concept of regional electricity distribution. They strung copper wires through forests and over mountains, bringing electric light to Springfield, Chicopee, and dozens of small towns that had never seen anything brighter than kerosene.

But the real power player emerged in Connecticut. J. Henry Roraback wasn't an engineer or an inventor—he was a lawyer and Republican political boss who understood that controlling electricity meant controlling development. In 1905, he formed the Rocky River Power Company, strategically located to serve Connecticut's growing industrial corridor. By 1917, through aggressive acquisitions and political maneuvering, Rocky River had transformed into Connecticut Light and Power (CL&P), serving most of the state. Roraback was more than just a lawyer—he was a political kingpin who became chairman of Connecticut's Republican Party in 1912, a position he held until his death in 1937. Between 1915 and 1931, his party controlled both the legislature and governorship, and virtually every Republican candidacy had to be cleared with "J. Henry." A big, forceful, mustachioed man who resembled the popular depiction of a political boss, Roraback actually denied the renomination of two Connecticut governors.

The genius of Roraback's strategy was using political power to build business empires and vice versa. He envisioned a string of hydroelectric plants along tributaries of the Housatonic River in a grid, harnessing the power of rushing water to bring electricity to homes and businesses throughout western Connecticut. CL&P's first development project was to build the Stevenson dam and hydroelectric plant on the Housatonic. Completed in 1919, it impounded what came to be called Lake Zoar. But the real masterpiece was Candlewood Lake—Connecticut legislature gave CL&P the right to divert water from the Housatonic back into the Rocky River, where it could be dammed and stored for release in periods of low water flow. The subsequent reservoir was named Lake Candlewood and became the state's largest body of water.

These weren't isolated companies building local grids—they were pieces of a larger puzzle that would take decades to assemble. Each utility served its territory like a feudal lord, responsible for everything from generating power to stringing lines to reading meters. The Hartford Electric Light Company illuminated Connecticut's capital. Western Massachusetts Electric powered the Springfield industrial corridor. Holyoke Water Power Company, formed in 1859, controlled valuable dam sites.

The post-World War II era brought explosive growth but also fragmentation. Returning veterans moved to suburbs that didn't exist five years earlier. Manufacturing boomed. Air conditioning transformed summer from a season of suffering to one of productivity. Every utility scrambled to build capacity, but coordination was minimal. Connecticut had dozens of separate electric companies, each with its own generation plants, transmission lines, and service territories.

By the early 1960s, forward-thinking executives recognized that this Balkanized system couldn't meet the region's growing needs. Nuclear power was on the horizon, requiring massive capital investments no single utility could afford. The Federal Power Commission was pushing for regional planning. Most importantly, the economies of scale in generation and transmission were becoming impossible to ignore. The stage was set. On July 1, 1966, Northeast Utilities (NU) was formed under CEO Lelan Sillin, with the merger of the Connecticut Light and Power Company (CL&P, formed in 1917), Western Massachusetts Electric Company (WMECO, formed in 1886), and the Hartford Electric Light Company (HELCO, formed in 1878), creating the first new multi-state public utility holding company since the enactment of the Public Utility Holding Company Act of 1935. This wasn't just a merger—it was the birth of modern utility scale in New England.

III. Building Northeast Utilities: The Conglomerate Years (1966–2000)

The conference room at Northeast Utilities' Berlin, Connecticut headquarters in April 1968 was thick with pipe smoke. Lelan F. Sillin, Jr., became president of NU in April 1968, inheriting a company that existed more on paper than in practice. The three merged utilities still operated like separate fiefdoms, with duplicate departments, incompatible systems, and cultures that viewed each other with suspicion.

Sillin, trained as an attorney who had risen from general counsel to CEO at Central Hudson Gas and Electric, understood that building Northeast Utilities meant more than just filing merger paperwork. His job was to unify the new Northeast Utilities and avoid fractionalism and duplication of service. "He consolidated several companies that came to make up NU. That was very difficult, but he brought them into one unified unit," said William B. Ellis, Sillin's successor.

The first major test came almost immediately. In 1967, Holyoke Water Power Company (HWP) (formed in 1859) joined the NU System, adding another layer of complexity. But the real strategic move was nuclear. At the time he took charge of Northeast, the New England region's electricity prices were higher than the national average, and Sillin viewed nuclear power as the least expensive, most efficient, and cleanest energy option. Skyrocketing petroleum prices due to 1970s energy crises just reinforced this view.

Northeast Utilities didn't just dabble in nuclear—they went all in. The company inherited four "Yankee" nuclear plants from its constituent companies and added the massive Millstone complex in Waterford, Connecticut. By the late 1970s, NU was generating more nuclear power per customer than any utility in America. The bet seemed brilliant when oil prices spiked during the Arab embargo. But nuclear came with hidden costs: endless regulatory battles, construction delays, and public opposition that would haunt the company for decades. The real drama came in 1992 with the acquisition of Public Service Company of New Hampshire (PSNH). On January 28, PSNH filed for protection under Chapter 11 of the U.S. Bankruptcy Code and became the first investor-owned utility since the Great Depression to declare bankruptcy. The culprit was Seabrook Nuclear Power Plant, which had ballooned from a $1.3 billion project to $6.6 billion and PSNH's share of the debt was $2.9 billion.

Northeast Utilities saw opportunity where others saw disaster. Connecticut-based Northeast Utilities (NU), one of the six major bidders, announced its plan in January 1989 and PSNH endorsed it in December of the same year. The deal was audacious: The state entered into an agreement on November 22, 1989 with Northeast Utilities in which it acquired PSNH for $2.3 billion. NU didn't just buy a troubled utility—they negotiated guaranteed rate increases of 5.5% per year for seven years, starting January 1, 1990. Step two was completed June 5, 1992 and PSNH became a fully owned subsidiary of Northeast Utilities.

This wasn't just financial engineering—it was regulatory arbitrage at its finest. NU understood that in the regulated utility model, what matters isn't the price you pay but the rate base you can build. Every dollar of investment, if approved by regulators, earns a guaranteed return. The PSNH acquisition doubled NU's size and gave them dominant positions in three states—crucial leverage in future rate negotiations.

The 1980s brought a new philosophy under William B. Ellis, who arrived from McKinsey in 1976. At Sillin's behest, Ellis left the consulting firm of McKinsey & Co. in 1976 to become NU's chief financial officer. In that year, total income was $85 million on revenues of $830 million. Two years later he was named president, and in 1983 he became chief executive officer. Ellis understood that utilities weren't really in the electricity business—they were in the capital allocation business. By 1982 revenues were up to $1.8 billion, but income had risen only to $151 million; by 1986, however, margins had improved, with sales of $2 billion and income of $300.9 million.

The 1990s brought deregulation, the great unbundling of the utility model. Generation would be competitive; transmission and distribution would remain regulated monopolies. For Northeast Utilities, this meant a fundamental strategic choice: try to compete in generation or retreat to the safety of regulated returns? They chose a hybrid approach that would later prove problematic. The Energy Policy Act of 1992 allowed utilities to compete for wholesale customers, opening markets but also creating new risks.

By the late 1990s, NU was pursuing what seemed like the deal of the century. In 1999, Con Edison and Northeast Utilities entered negotiations that would have created one of the largest utilities in the United States. The merger would have created a $19 billion behemoth controlling power from New York City to northern Maine. But Connecticut's Attorney General Richard Blumenthal saw it differently—this was too much concentration of power. However, Con Edison backed out of the merger in 2001 after Connecticut's Attorney General Richard Blumenthal threatened lawsuits to block it.

IV. Crisis and Transformation: Competitive Markets & Divestiture (2000–2010)

The millennium opened with Northeast Utilities facing an existential question: What business were they actually in? The California energy crisis of 2000-2001 sent shockwaves through the industry. Enron's spectacular collapse in December 2001 proved that energy trading and financial engineering had limits. For NU's board, watching from Connecticut, the message was clear: complexity kills utilities.

The strategic retreat began almost immediately. Legislation passed in the late 1990s deregulated the electricity market in New England and required regulated utilities to divest generating stations to competitive suppliers. In 1999 the company divested all of the generating assets of WMECO and CL&P per requirements of the Massachusetts and Connecticut legislation. This wasn't just selling assets—it was fundamentally reimagining what a utility should be. The pivotal year was 2006. In 2006, NU decided to sell the generating units it had earlier retained in the 1999 divestiture as competitive suppliers and shut down its competitive generation business units. The Northeast Generation assets, including Mount Tom Station and Northfield Mountain, were all sold to Energy Capital Partners. This wasn't a fire sale—it was strategic focus. NU recognized that competing in deregulated generation markets meant volatile earnings, massive capital requirements, and merchant risk. The regulated transmission and distribution business, while boring, offered predictable returns and political protection.

The divestiture strategy reflected a deeper truth about utilities: in a deregulated world, owning generation assets meant taking commodity price risk. Owning wires meant collecting tolls. Which would you rather be—a toll road or a trucking company? For NU's management, the answer was obvious.

PSNH continued to operate regulated hydroelectric and fossil fuel generation assets to serve its default/basic service customers who did not choose an alternative competitive supplier. This was the hybrid model—mostly wires, some generation where regulators required it. The company was positioning itself as the essential infrastructure provider, not an energy merchant.

Between 2000 and 2002, the nuclear exodus continued. Between 2000 and 2002 due to state laws, NU divested WMECO, CL&P, and PSNH's nuclear generating assets which consisted of their stakes in the Seabrook, Millstone, and Vermont Yankee stations. These sales marked the end of NU's nuclear era—plants that had nearly bankrupted them, then defined them, were now someone else's problem.

The financial engineering during this period was sophisticated. NU negotiated stranded cost recovery—essentially getting paid for bad investments made under the old regulated model. Regulators allowed utilities to recover these costs through special charges on customer bills, smoothing the transition to competitive markets while protecting utility shareholders. It was a masterclass in regulatory negotiation: heads we win, tails customers lose.

By 2010, Northeast Utilities had transformed from an integrated utility that generated, transmitted, and distributed power into primarily a "wires and pipes" company. Revenue came from regulated rates, not market prices. Growth came from infrastructure investment, not competitive wins. Risk was regulatory, not commercial. The transformation was complete, setting the stage for the next phase: consolidation through mega-mergers.

V. The NSTAR Mega-Merger: Doubling Down on New England (2010–2012)

The boardroom at Northeast Utilities' Berlin headquarters in October 2010 was electric with possibility. CEO Charles Shivery had just hung up from a call with Tom May, his counterpart at NSTAR. After months of secret negotiations, they were ready to announce something unprecedented: the merger of New England's two largest utilities, creating a $17.5 billion giant serving 3.5 million customers.

In October 2010, Northeast Utilities announced that it would merge with NSTAR, the major electric and gas provider in Greater Boston, with the resulting company retaining the Northeast Utilities name for the next several years. The strategic logic was compelling. NSTAR brought Boston—New England's economic engine—into the NU fold. NSTAR was formed in 1999 by the merger of BEC Energy and Commonwealth Energy System and had the following operating units: Boston Edison Company, Cambridge Electric Light Company, Commonwealth Electric Company, and NSTAR Gas Company (formerly Commonwealth Gas and Cambridge Gas Company).

This wasn't just about size—it was about density. Urban utilities are goldmines in the regulated model. More customers per mile of wire means better returns on infrastructure investment. Boston's maze of underground cables and gas pipes might be expensive to maintain, but the customer density made every dollar of investment more valuable. Where NU had rural expanses of Connecticut and western Massachusetts, NSTAR had the concentrated wealth of Greater Boston.

The regulatory gauntlet was formidable. Three state utility commissions—Massachusetts, Connecticut, and New Hampshire—each had to approve. Each state wanted different things. Massachusetts wanted reliability improvements. Connecticut wanted rate stability. New Hampshire wanted economic development commitments. The companies spent $50 million on lawyers, consultants, and experts to navigate the approval process.

The Massachusetts Department of Public Utilities proved the toughest negotiator. They demanded $21 million in merger-related savings be returned to customers, specific reliability targets, and maintenance of local employment. Connecticut extracted promises about transmission investment. New Hampshire wanted assurances about service quality in rural areas. Each concession reduced the merger's financial benefits but was necessary for approval.

After government approvals, the deal closed in April 2012. Under the terms of the transaction, NSTAR shareholders received 1.312 Northeast Utilities common shares for each NSTAR share that they own. The premium paid to NSTAR shareholders reflected the value of their Boston franchise—some of the most valuable utility territory in America.

Integration was a three-year marathon. Two companies with different cultures, systems, and processes had to become one. NSTAR's union relationships were different from NU's. Their IT systems were incompatible. Even something as simple as truck specifications varied. The companies had to standardize everything from safety procedures to accounting policies.

Following its 2012 merger with Boston-based NSTAR, Northeast Utilities had more than 4,270 circuit miles of electric transmission lines, 72,000 pole miles of distribution lines, and 6,459 miles of natural gas pipeline in New England. The combined company now served every major city in New England except Providence. It was a formidable market position.

The financial impact was immediate. Combined rate base grew to over $13 billion. The larger balance sheet enabled cheaper financing. Operating synergies, while modest, improved margins. Most importantly, the company now had the scale to invest in major transmission projects that smaller utilities couldn't finance. Size mattered in the capital-intensive utility business.

But the real genius of the NSTAR merger was timing. Interest rates were at historic lows, making the deal financing attractive. Regulators were concerned about reliability after several high-profile outages, making them receptive to utility investment. Natural gas prices were plummeting due to fracking, reducing customer bills and political pressure. The window for such a transformative deal was narrow, and NU jumped through it.

Tom May, who became CEO of the combined company, understood that this was more than a merger—it was a bet on New England's energy future. The region was shutting coal plants, fighting natural gas pipelines, and mandating renewable energy. Someone would need to rebuild the entire energy infrastructure. With the NSTAR merger, Northeast Utilities positioned itself as that someone.

VI. Rebranding & Expansion: Becoming Eversource (2015–2017)

The focus groups were brutal. In late 2014, Northeast Utilities' marketing team sat behind one-way glass watching customers discuss their utility. "Northeast Utilities? Never heard of them," said a Boston resident who had been an NSTAR customer for twenty years. "I pay my bill to Connecticut Light & Power," said a Hartford customer. After the massive merger, the company realized it had a brand problem: nobody knew who they were.

On February 2, 2015, the company and all its subsidiaries rebranded themselves as "Eversource Energy". The stock symbol changed on February 19, 2015, from "NU" to "ES". The name was meant to evoke reliability—your "ever-present source" of energy. Critics mocked it as corporate speak, but the strategy was sound: one company, one brand, one interface with 3.6 million customers.

"Energy is what brings us all together, and Eversource reflects the one-company focus we have been driving for the last few years," said Tom May, chairman, president and CEO. All of the company's subsidiaries, including Connecticut Light and Power Co., NSTAR Electric, NSTAR Gas, Public Service Co. of New Hampshire, Western Massachusetts Electric Co. and Yankee Gas Services adopted and operated under the Eversource name.

The rebranding cost $25 million—new signs, trucks, uniforms, websites, and marketing materials. Observers said the timing of the change was strange, and they were wary of the potential costs. But May saw it differently. A unified brand meant unified operations. Customer service representatives could handle calls from any state. Crews could be deployed across borders during storms. Procurement could be centralized. The soft benefits of cultural integration were as important as the hard savings.

Just as the paint was drying on the new Eversource signs, May made his next move. In June 2017 Eversource announced its merger with Aquarion Water Company for $1.675 billion. Aquarion would become a fully owned subsidiary and retain its own name, adding 300 employees and 230,000 customers in Connecticut, Massachusetts, and New Hampshire.

Water? The announcement puzzled analysts. Why would an electric and gas utility buy a water company? May's logic was infrastructure synergy. Water utilities faced the same challenges as electric utilities: aging infrastructure, rising environmental standards, and the need for massive capital investment. The same crews that fixed gas leaks could fix water leaks. The same customer service systems could handle water bills. Most importantly, water utilities earned regulated returns just like electric utilities.

Aquarion brought something else: pristine Connecticut watershed lands that could host solar farms and battery storage. As renewable energy became mandatory, controlling land became strategic. Aquarion's 15,000 acres of watershed property represented option value for future clean energy development.

In December 2017, the merger was completed after government approval. The integration was smoother than NSTAR—Eversource had learned from experience. They kept the Aquarion brand, maintained local management, and focused on operational improvements rather than dramatic changes.

During this period, Eversource also revolutionized its grid operations. The company invested $3 billion annually in infrastructure, much of it in "smart grid" technology. Sensors on power lines could detect problems before they caused outages. Smart meters gave customers real-time usage data. Automated switches could reroute power around damaged lines. It was the unsexy work of modernization that rarely made headlines but fundamentally improved reliability.

The financial results validated the strategy. Rate base grew from $13 billion in 2012 to $20 billion by 2017. Earnings per share increased 7% annually. The dividend grew reliably. The stock price doubled. For investors, Eversource had become exactly what May promised: a stable, growing utility with predictable returns.

But beneath the surface, tensions were building. Climate activists increasingly targeted Eversource for enabling natural gas expansion. Customers complained about rising rates despite falling energy costs. Regulators questioned whether all this infrastructure investment was necessary or just financial engineering. The social license that utilities had long taken for granted was starting to fray. The company would soon make a bold bet to address these concerns: offshore wind.

VII. The Offshore Wind Gamble: Ambition Meets Reality (2016–2024)

The renderings were gorgeous. Massive wind turbines rising from the Atlantic, their blades turning lazily in the ocean breeze, generating enough clean power for millions of homes. In 2016, when Eversource executives presented their offshore wind vision to investors, it seemed like the perfect evolution: from poles and wires to pioneering the clean energy future.

In 2016, Eversource started joint ventures for wind farm developments with Ørsted. The Danish company was the world's offshore wind leader, having built wind farms in the North Sea for decades. For Eversource, partnering with Ørsted meant buying expertise they didn't have. The joint ventures would develop multiple projects: Bay State Wind, South Fork Wind, Revolution Wind, and Sunrise Wind—names that evoked a clean energy dawn.

The strategic rationale seemed bulletproof. Northeastern states were mandating massive amounts of offshore wind. Massachusetts alone wanted 3,200 megawatts by 2035. Connecticut and Rhode Island had their own targets. Someone would build these wind farms and earn guaranteed long-term power contracts. Why shouldn't Eversource, with its regional relationships and regulatory expertise, capture this growth?

CEO Jim Judge, who succeeded Tom May in 2016, was particularly bullish. He saw offshore wind as Eversource's transformation from old-economy utility to new-energy leader. The company committed $1.5 billion to the ventures, money that could have gone to traditional infrastructure or dividends. Judge promised investors that offshore wind would drive earnings growth for decades.

The engineering challenges were staggering. These weren't land-based wind turbines but massive structures anchored to the seafloor 20 miles from shore. Each turbine stood 850 feet tall—higher than Boston's Prudential Tower. The blades swept an area larger than a football field. Installation required specialized ships that barely existed in American waters. Undersea cables had to connect the turbines to onshore substations. Every component had to withstand hurricane-force winds and corrosive salt water.

Then reality hit. Steel prices doubled. Specialized installation vessels that cost $500,000 per day were booked for years. The Jones Act required American-flagged vessels for certain work, but America had almost no offshore wind vessels. Labor costs exploded as unions demanded premium wages for dangerous offshore work. Environmental reviews took years longer than expected. Fishing interests filed lawsuits. Coastal communities that claimed to support clean energy fought actual projects in their viewfronts.

By 2022, the economics had inverted. Projects bid at $70 per megawatt-hour now needed $140 to break even. Power purchase agreements signed with states were now money-losers. Revolution Wind, originally budgeted at $2 billion, ballooned toward $3 billion. South Fork Wind faced similar overruns. The fixed-price contracts that seemed conservative when signed were now financial albatrosses.

The macroeconomic environment made everything worse. The Federal Reserve's inflation fight pushed interest rates from 0% to 5%, devastating project finance models built on cheap debt. Supply chain chaos from COVID and the Ukraine war made equipment procurement a nightmare. A turbine blade factory promised for Massachusetts never materialized. The entire American offshore wind industry was melting down, with projects canceled from Massachusetts to Virginia.

Inside Eversource, tensions erupted. Traditional utility executives who had opposed the offshore wind gamble felt vindicated. The board questioned why a regulated utility was taking development risk. Investors who bought Eversource for stable dividends were furious about billion-dollar write-offs. In analyst calls, Judge defended the strategy even as skepticism mounted.

In 2023, Eversource announced it would sell off its equity in these projects (Bay State Wind, South Fork Wind, Revolution Wind, and Sunrise Wind) at an expected loss of $200 million. The real damage was worse. In Q4 2023, Eversource recorded a $1.29 billion loss driven mainly by offshore wind investments. The company's first annual loss in decades shocked investors who viewed utilities as safe havens.

The exit was messy. Ørsted, facing its own financial crisis, wasn't eager to buy out Eversource's stakes. Other potential buyers smelled blood and offered pennies on the dollar. Some projects were so far along that exit costs exceeded staying in. Revolution Wind and South Fork Wind would be completed, but Eversource would never recoup its investment. Bay State Wind and Sunrise Wind faced uncertain futures.

The offshore wind debacle revealed uncomfortable truths about energy transition. Politicians mandated clean energy but wouldn't approve the transmission lines to carry it. Environmentalists demanded renewable power but fought actual projects. Customers supported climate action until they saw the bill. The gap between energy policy aspirations and implementation reality was vast.

For Eversource, the lesson was expensive but clear: stick to the regulated utility model. Let others take development risk. The company would connect offshore wind to the grid—earning regulated returns on transmission investment—but never again would it bet shareholders' money on building the turbines. The clean energy transition would happen, but Eversource would facilitate rather than lead it.

VIII. Modern Operations & Financial Performance (2020–Present)

The numbers tell a story of resilience and recovery. After the offshore wind disaster of 2023, Eversource's 2024 results showed a dramatic turnaround: $811.65 million profit after a $442.24 million loss in 2023, with adjusted earnings of $4.57 per share. Revenue held steady at $11.92 billion, essentially flat from 2023. The company had returned to what it did best: the steady, predictable business of delivering energy through regulated infrastructure.

The segment breakdown revealed where the real value lay. Electric distribution generated $631.7 million in earnings in 2024, while natural gas distribution contributed $291.0 million. These weren't exciting businesses—they were the equivalent of toll roads for electrons and molecules. But they generated cash like clockwork, quarter after quarter, year after year.

CEO Joe Nolan, who took over in 2021 after Jim Judge's retirement, brought a back-to-basics approach. A career utility executive who had run transmission operations, Nolan understood that Eversource's competitive advantage wasn't in developing new energy sources but in owning the irreplaceable infrastructure that delivered energy, regardless of its source. His mantra was simple: "We're not an energy company; we're an energy delivery company."

The company's footprint remained formidable: 10,680 employees serving over 4 million customers across three states. The physical infrastructure was staggering—72,000 pole miles of distribution lines, 4,270 circuit miles of transmission lines, 6,459 miles of gas pipeline. Replacing this infrastructure would cost hundreds of billions and take decades. It was the ultimate moat.

But owning infrastructure meant maintaining it, and maintenance meant capital investment, and capital investment meant rate base growth. Eversource announced a $24.2 billion investment plan for 2025-2029, roughly $5 billion per year. Every dollar invested earned a regulated return around 9.5%. It was the utility money machine: spend capital, grow rate base, increase earnings, repeat.

The investment priorities reflected new realities. Electric vehicle adoption required grid upgrades—every Tesla in a garage meant more demand on local transformers. Distributed solar meant two-way power flows that traditional grids weren't designed for. Climate change brought more severe storms, requiring hardening of infrastructure. Cybersecurity threats mandated new digital defenses. The boring old grid needed expensive modernization.

To fund this investment, Eversource needed to clean up its balance sheet. The pending Aquarion sale would raise $1.9 billion, money that would pay down debt from the offshore wind debacle. The water utility that had seemed strategic in 2017 was now expendable. Nolan was ruthlessly focused: electric and gas distribution in New England, nothing else.

The regulatory environment remained challenging. Connecticut's Public Utilities Regulatory Authority (PURA) had become increasingly hostile, challenging rate increases and imposing penalties for service issues. Massachusetts regulators demanded more renewable energy investment while capping customer rate increases. New Hampshire wanted economic development but resisted infrastructure spending. Threading this regulatory needle required constant political management.

Labor relations added complexity. Eversource's unionized workforce—lineworkers, gas fitters, customer service representatives—commanded high wages and generous benefits. A journeyman lineworker could earn $150,000 with overtime. During storms, when crews worked around the clock to restore power, overtime costs exploded. But these workers were also Eversource's greatest asset, the people who actually kept the lights on.

Technology was transforming operations in ways customers never saw. Artificial intelligence predicted equipment failures before they happened. Drones inspected transmission lines that once required helicopter flights. Smart meters eliminated manual meter reading. Grid sensors provided real-time visibility into system conditions. The utility of 2024 was far more digital than the utility of even 2014.

The financial metrics remained solid if unspectacular. Return on equity hovered around 9%, exactly where regulators set it. The dividend yielded 3.5%, attractive in a low-rate environment. Earnings grew at 5-7% annually, driven by rate base expansion. The stock traded at 18 times earnings, a premium to historical utility valuations but justified by Eversource's quality franchise.

Yet challenges loomed. Customer bills kept rising even as wholesale energy costs fell. The standard service rate that had doubled to 24.2 cents per kilowatt-hour in early 2024 created political backlash. Every rate case became a public battle. Social media amplified customer complaints. Politicians seized on utility bashing as a populist issue. The social contract between utility and society was fraying.

IX. The Regulatory Dance: Politics, Rates, and Public Opinion

The hearing room in Hartford was packed and hostile. It was January 2024, and Connecticut's Public Utilities Regulatory Authority (PURA) had summoned Eversource executives to explain why standard service rates had doubled to 24.2 cents per kilowatt-hour. Angry customers filled every seat, holding signs demanding lower rates. TV cameras rolled. Politicians grandstanded. CEO Joe Nolan sat at the witness table, knowing that nothing he said would satisfy the crowd.

"You're literally stealing from hardworking families," shouted one customer during public comment. "My electric bill is higher than my mortgage," said another. The frustration was real, the pain genuine, but the explanation was complex in ways that didn't fit on protest signs or in sound bites.

The root issue was a massive misunderstanding about how electricity pricing works. Eversource doesn't generate power—it delivers it. The company buys electricity through competitive procurement processes mandated by state law, then passes the cost directly to customers with no markup. When natural gas prices spike, electricity prices follow, because gas plants set the marginal price in New England's energy market. Eversource makes the same profit whether electricity costs 5 cents or 50 cents per kilowatt-hour.

"It's a winter problem, not a summer problem," Nolan tried to explain. New England's constrained natural gas pipeline capacity meant that during cold snaps, gas prices could increase tenfold as heating demand competed with electricity generation. The region had systematically blocked new pipeline projects for environmental reasons, creating scarcity that drove prices skyward. Customers wanted clean energy, cheap prices, and no new infrastructure—an impossible trinity.

The regulatory framework itself was Byzantine. In Connecticut, PURA regulated distribution rates but had no control over generation costs. The legislature mandated renewable energy purchases but didn't fund them. Federal regulators controlled interstate transmission pricing. ISO New England operated the wholesale market. Each entity pointed fingers at others when customers complained about bills.

PURA Chair Marissa Gillett had become Eversource's chief antagonist. A political appointee with ambitions beyond utility regulation, she turned rate hearings into theatrical productions. She accused Eversource of "corporate greed" and "putting profits over people," claims that resonated with voters but ignored the mathematical reality of regulated returns. When storms caused outages, she imposed millions in penalties. When bills rose, she demanded investigations.

The political theater masked serious policy failures. Connecticut's energy strategy was incoherent—shutting down nuclear plants while mandating carbon neutrality, blocking gas pipelines while depending on gas generation, demanding reliability while opposing infrastructure investment. Politicians who voted for these contradictory policies then blamed utilities for the inevitable consequences.

Massachusetts played a different game. Regulators there focused on performance metrics—reliability statistics, customer satisfaction scores, safety records. They approved rate increases but demanded specific improvements in return. It was technocratic rather than theatrical, but still challenging. The Massachusetts Department of Public Utilities required 500-page rate case filings, thousands of data requests, and months of hearings for even routine decisions.

New Hampshire brought its own complications. The state's libertarian streak meant skepticism of any rate increase, but its rural geography meant expensive infrastructure serving few customers. Maintaining power lines through the White Mountains cost far more per customer than serving dense Boston suburbs. The Public Utilities Commission tried to balance affordability with reliability, usually pleasing no one.

Consumer advocates added another layer of complexity. Groups like AARP and low-income advocates intervened in every rate case, hiring expert witnesses and lawyers to challenge utility proposals. They performed a valuable service—someone needed to push back on utility requests—but they also extended proceedings and increased costs that ultimately got passed to customers.

The procurement process for standard service revealed the market's dysfunction. Eversource issued requests for proposals to dozens of suppliers, but only a handful bid. Suppliers knew about New England's winter price spikes and built risk premiums into their offers. The winning bids reflected not just expected energy costs but also the cost of uncertainty. Customers paid for market volatility they didn't understand.

Climate mandates created new tensions. States required Eversource to buy increasing amounts of renewable energy, often at above-market prices. Offshore wind contracts signed at $120 per megawatt-hour looked expensive when wholesale power traded at $40. Solar net metering shifted costs from wealthy homeowners with rooftop panels to renters who couldn't afford them. Every green mandate came with a bill that someone had to pay.

The utility death spiral loomed as a long-term threat. As customers installed solar panels and batteries, they bought less electricity from the grid but still relied on it for backup. Fixed infrastructure costs got spread across fewer kilowatt-hours, raising rates and encouraging more customers to go solar. It was a vicious cycle that threatened the entire utility model.

Public opinion had turned decidedly negative. Surveys showed utilities ranking below airlines and cable companies in customer satisfaction. Social media amplified every outage, every rate increase, every corporate misstep. Eversource spent millions on advertising trying to rebuild trust, but slick commercials couldn't overcome angry customers opening high bills.

The regulatory compact—the century-old deal where utilities got monopolies in exchange for serving everyone at regulated rates—was breaking down. Politicians wanted to have their cake and eat it too: low rates, perfect reliability, clean energy, and no new infrastructure. Utilities were caught in the middle, blamed for problems they didn't create and couldn't solve. The question wasn't whether the model would change, but how dramatically and how soon.

X. Playbook: The Regulated Utility Model

The math is beautiful in its simplicity. Take your rate base—the net book value of all your poles, wires, transformers, and substations. Multiply by your allowed return on equity, typically 9-10%. Add your operating expenses and depreciation. Divide by kilowatt-hours sold. That's your rate. Every dollar invested in infrastructure earns a regulated return forever, or at least until it's fully depreciated. It's the closest thing to a perpetual money machine capitalism has created.

Rate base growth is the only growth that matters. Eversource can't increase prices at will—regulators set rates. It can't expand geographically—service territories are fixed. It can't develop new products—it sells a commodity. The only lever for earnings growth is investing more capital in infrastructure. Build a new substation? Rate base grows. Upgrade transmission lines? Rate base grows. Install smart meters? Rate base grows.

This creates perverse incentives. Utilities earn returns on capital investment but not operating efficiency. Spending $100 million on new equipment earns $9.5 million annually. Saving $100 million through efficiency earns nothing. The system rewards gold-plating—building the most expensive solution that regulators will approve. It's not corruption; it's the logical response to regulatory incentives.

Capital allocation in this model is straightforward. First, maintain the dividend—utilities are bond substitutes for many investors. Second, invest every dollar regulators will allow into rate base. Third, maintain investment-grade credit ratings to minimize financing costs. Fourth, return excess cash to shareholders. Growth acquisitions make sense only if they're immediately accretive and regulatorily approved.

The infrastructure investment treadmill never stops. Poles rot, wires corrode, transformers fail. Beyond maintenance, there's modernization—smart grid, storm hardening, cybersecurity. Then there's growth—new customers, electric vehicles, data centers. A utility that invests $5 billion annually just to maintain current service levels can show 6% rate base growth indefinitely. It's genuine growth, but it's also running to stand still.

Managing stakeholders requires political sophistication. Regulators control your returns—alienate them and suffer. Politicians control regulators—ignore them at your peril. Customer advocates influence politicians—dismiss them and face backlash. Investors provide capital—disappoint them and your cost of capital rises. Employees run the system—mistreat them and service deteriorates. Each stakeholder has leverage; managing all simultaneously is the CEO's primary job.

The utility-as-bond dynamic drives valuations. When interest rates fall, utility stocks rise as investors chase yield. When rates rise, utilities fall as bonds become competitive. The correlation is negative 0.7, almost perfectly inverse. This makes utilities a portfolio hedge but also means their valuations depend more on Federal Reserve policy than operational performance.

ESG before ESG was called ESG has always defined utilities. Environmental compliance isn't optional—it's existential. Social responsibility isn't marketing—serving everyone, including unprofitable rural customers, is the regulatory compact. Governance isn't just best practice—regulatory scrutiny ensures it. Utilities were doing stakeholder capitalism before it had a name.

The dividend aristocrat dynamic creates its own momentum. Eversource has raised its dividend for 25 consecutive years. Cutting it would signal distress, crushing the stock price. So the dividend must grow, which requires earnings growth, which requires rate base growth, which requires regulatory approval, which requires political capital. The dividend commitment drives the entire strategic cycle.

Regulatory lag is the hidden killer. Utilities invest capital today based on yesterday's rate case for tomorrow's returns. If inflation accelerates or storms increase, costs rise immediately but rates adjust slowly. The two-to-three-year lag between investment and recovery means utilities are always fighting the last war. Smart utilities under-promise and over-deliver, building cushions for unexpected costs.

The death spiral threat is existential. As distributed generation proliferates, grid defection becomes possible. Wealthy customers install solar and batteries, reducing grid purchases. Fixed costs get spread across fewer customers, raising rates. Higher rates encourage more defection. Eventually, only those who can't afford alternatives remain, creating an unsustainable dynamic. The solution—restructuring rates to recover fixed costs through fixed charges—is politically toxic.

Technological disruption looms but moves slowly. Utilities have survived every prior technology transition—from manufactured gas to natural gas, from local generation to regional grids, from analog to digital meters. The key is controlling the essential infrastructure. Electricity can be generated many ways, but it still needs delivery. Until wireless power transmission becomes reality, poles and wires remain valuable.

The playbook ultimately reduces to this: Own irreplaceable infrastructure in good regulatory jurisdictions. Invest capital at regulated returns. Maintain the political and social license to operate. Distribute reliable dividends. Avoid competitive markets, technology bets, and regulatory overreach. It's a boring business model that's created enormous wealth for patient investors. The question is whether it survives the energy transition intact.

XI. Bear vs. Bull Case & Future Challenges

Bull Case: The Essential Infrastructure Thesis

The bulls see Eversource as the toll road of the electron highway. No matter how electricity is generated—solar, wind, nuclear, or natural gas—it needs transmission and distribution. Eversource owns the irreplaceable infrastructure connecting 4 million customers across New England. Duplicating this network would cost $200 billion and require permissions that would never be granted. It's the ultimate moat.

The electrification megatrend supercharges the bull case. Every electric vehicle adds 3,000-4,000 kilowatt-hours of annual demand—equivalent to adding a third of a household. Heat pump adoption doubles home electricity consumption. Data centers are proliferating, each consuming as much power as thousands of homes. McKinsey projects electricity demand growing 40% by 2040 after decades of stagnation. More electrons flowing through Eversource's wires means more rate base investment, more earnings, more dividends.

The infrastructure investment opportunity is massive. Eversource's grid was built for one-way power flow from central plants to customers. The future grid must handle two-way flows from millions of solar panels, coordinate thousands of battery systems, and maintain reliability despite intermittent renewable generation. The company's $24.2 billion five-year investment plan might be conservative. Grid modernization could require $50 billion over the next decade—all earning regulated returns.

Climate resilience spending is non-negotiable. Every major storm demonstrates grid vulnerability. Customers and regulators demand storm hardening—undergrounding lines, reinforcing poles, adding redundancy. This isn't optional spending; it's existential. Eversource can invest billions in resilience and pass costs to customers because the alternative—persistent outages—is politically unacceptable.

The dividend aristocrat status provides downside protection. Twenty-five consecutive years of dividend increases attract income-focused investors who provide price support. The 3.5% yield looks attractive versus 10-year Treasuries at 4.5%, especially considering dividend growth. Utility dividends also get favorable tax treatment. For retirees and pension funds, Eversource is a bond substitute with upside.

Bear Case: The Disruption and Political Risk Thesis

The bears see existential threats everywhere. Distributed generation is the most obvious. Solar-plus-storage costs have declined 90% in a decade. Grid parity—where self-generation costs less than utility power—has arrived in high-cost states. Tesla's Powerwall and similar products make grid defection technically feasible. If 20% of customers significantly reduce grid purchases, the utility death spiral begins.

Regulatory risk has materialized into regulatory reality. Connecticut's PURA has turned hostile, challenging every rate request and imposing penalties for routine operations. Politicians campaign against "utility greed," making rate increases politically toxic. The regulatory compact assumes fair returns for prudent investment, but "fair" and "prudent" are increasingly political judgments. A few adverse decisions could slash returns below capital costs.

The aging infrastructure burden is staggering. Much of Eversource's system dates to the 1960s and 1970s. Replacing it all would cost more than the company's market capitalization. But not replacing it means increasing failures, outages, and safety risks. It's a no-win situation: spend massively and face rate shock, or defer investment and face reliability crises.

Climate change multiplies every challenge. Severe storms are more frequent and destructive. Summer heat waves stress equipment. Winter cold snaps spike demand. Flooding threatens substations. Each event costs millions in emergency response and repairs that may not be fully recoverable. Insurance costs are soaring when available at all. The utility model assumes normal weather patterns that no longer exist.

Customer dissatisfaction is reaching dangerous levels. Every rate increase generates headlines and hearings. Social media amplifies outrage. Politicians exploit anger for votes. The social license utilities enjoyed for a century is evaporating. When utilities become political punching bags, rational regulation becomes impossible. Populist policies that sound good but destroy economics become irresistible.

Technological disruption accelerates beyond utility adaptation speed. Blockchain-based peer-to-peer energy trading could bypass utilities entirely. Wireless power transmission, while nascent, could obsolete power lines. Artificial intelligence could optimize distributed resources better than centralized control. Utilities move in regulatory time—years for approvals—while technology moves in venture capital time—months for deployment.

The Realistic Middle Ground

The truth incorporates both narratives. Eversource will survive but struggle. The core business—delivering electricity and gas through regulated infrastructure—remains essential and profitable. But growth will slow, returns will compress, and political challenges will intensify. The company will generate steady cash flows but face constant battles over how to distribute them.

The energy transition creates opportunities and threats simultaneously. Transmission investment for renewable integration offers growth, but distributed generation threatens the traditional model. Electric vehicle adoption increases demand but requires expensive upgrades. Climate mandates drive investment but also rate increases that trigger political backlash.

The most likely scenario is evolution, not revolution. Utilities will remain essential but less central. They'll shift from energy providers to platform operators, managing complex systems of distributed resources. Regulations will evolve to maintain utility viability while accommodating new technologies. Rates will restructure to recover fixed costs through fixed charges. It will be messy, contentious, and slow.

For investors, Eversource represents a classical value versus growth dilemma. The dividend is safe, the business is essential, and the assets are irreplaceable. But growth is constrained, politics are hostile, and disruption looms. It's a widow-and-orphan stock in a Tesla world. Whether that's comforting stability or frustrating stagnation depends on your investment horizon and risk tolerance.

XII. Epilogue: The Energy Transition Paradox

The great irony of our time is this: Everyone wants clean energy, but nobody wants to pay for it. Everyone demands perfect reliability, but nobody wants new infrastructure in their neighborhood. Everyone supports fighting climate change, but nobody accepts the trade-offs required. Eversource sits at the intersection of these contradictions, trying to deliver an impossible mandate.

The numbers are sobering. Rebuilding New England's energy infrastructure for a carbon-neutral future will cost at least $100 billion over the next two decades. That's $25,000 per household, or $100 per month for twenty years. Add the cost of renewable generation, and it doubles. Add resilience for climate change, and it triples. The energy transition isn't free—it's the most expensive infrastructure project in human history.

Can regulated utilities lead this transition? They have advantages: access to capital, technical expertise, regulatory relationships, and operational scale. But they also have disadvantages: bureaucratic cultures, regulatory constraints, political vulnerabilities, and legacy systems. Asking century-old utilities to lead a technological revolution is like asking railroads to build airlines. They might manage it, but it won't be pretty.

The grid modernization challenge alone is staggering. Today's grid is essentially 1950s technology with digital controls bolted on. Tomorrow's grid must coordinate millions of solar panels, thousands of wind turbines, hundreds of thousands of batteries, and millions of electric vehicles. It must balance supply and demand microsecond by microsecond across resources that didn't exist a decade ago. It's not just an upgrade; it's a rebuild.

Electrification changes everything. If New England actually electrifies transportation and heating as planned, electricity demand could double. That means doubling generation, transmission, and distribution capacity. Every parking lot needs charging stations. Every home needs upgraded electrical service. Every substation needs expansion. The scope is almost incomprehensible.

Yet the alternative to utility-led transition might be worse. Silicon Valley disruption sounds exciting until you realize electricity isn't software. You can't beta test the power grid. You can't "move fast and break things" when those things keep hospitals running. You can't have different electric systems for rich and poor neighborhoods. The boring competence of utilities might be exactly what's needed.

The next decade will determine whether the utility model survives or transforms beyond recognition. If Eversource navigates the political storms, manages the infrastructure investment, and adapts to new technology, it could emerge stronger. If it fails to evolve, gets trapped by politics, or mismanages the transition, it could become the Kodak of energy—a former giant obsoleted by change it saw coming but couldn't navigate.

The final paradox is that utilities like Eversource are simultaneously the problem and the solution. Their infrastructure enables fossil fuel consumption, but also renewable integration. Their rates burden customers, but fund clean energy investment. Their monopoly power stifles innovation, but ensures universal service. They're the incumbent being disrupted and the platform enabling disruption.

For all the challenges, the lights still come on when you flip the switch. Gas still flows when you turn the furnace. That daily miracle of reliability, delivered through wars, recessions, pandemics, and storms, deserves respect. The engineers, lineworkers, and operators who maintain this invisible infrastructure are heroes whose heroism is noticed only in its absence.

The story of Eversource—from gas lamps to smart grids, from local utilities to regional giant, from nuclear ambitions to offshore wind retreats—is really the story of American infrastructure. It's a story of engineering triumphs and financial engineering, public service and private profit, essential services and political lightning rods. It's messy, complicated, and unfinished.

As New England contemplates its energy future, Eversource remains central to any realistic plan. Love them or hate them, you need them. They own the wires, pipes, and poles that make modern life possible. The question isn't whether Eversource survives but what it becomes. The answer will shape not just the company's future but the region's ability to achieve its climate goals while keeping the lights on and bills payable.

The utility model that J. Henry Roraback pioneered in 1905—using political power to build business empires that provide essential services—remains remarkably intact 120 years later. But every model eventually meets its limits. Whether Eversource transcends those limits or becomes trapped by them will be the next chapter in this long story of power, politics, and the paradoxes of progress.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube