Danaher Corporation: The Compounding Machine Built on Continuous Improvement

I. Introduction & Episode Thesis

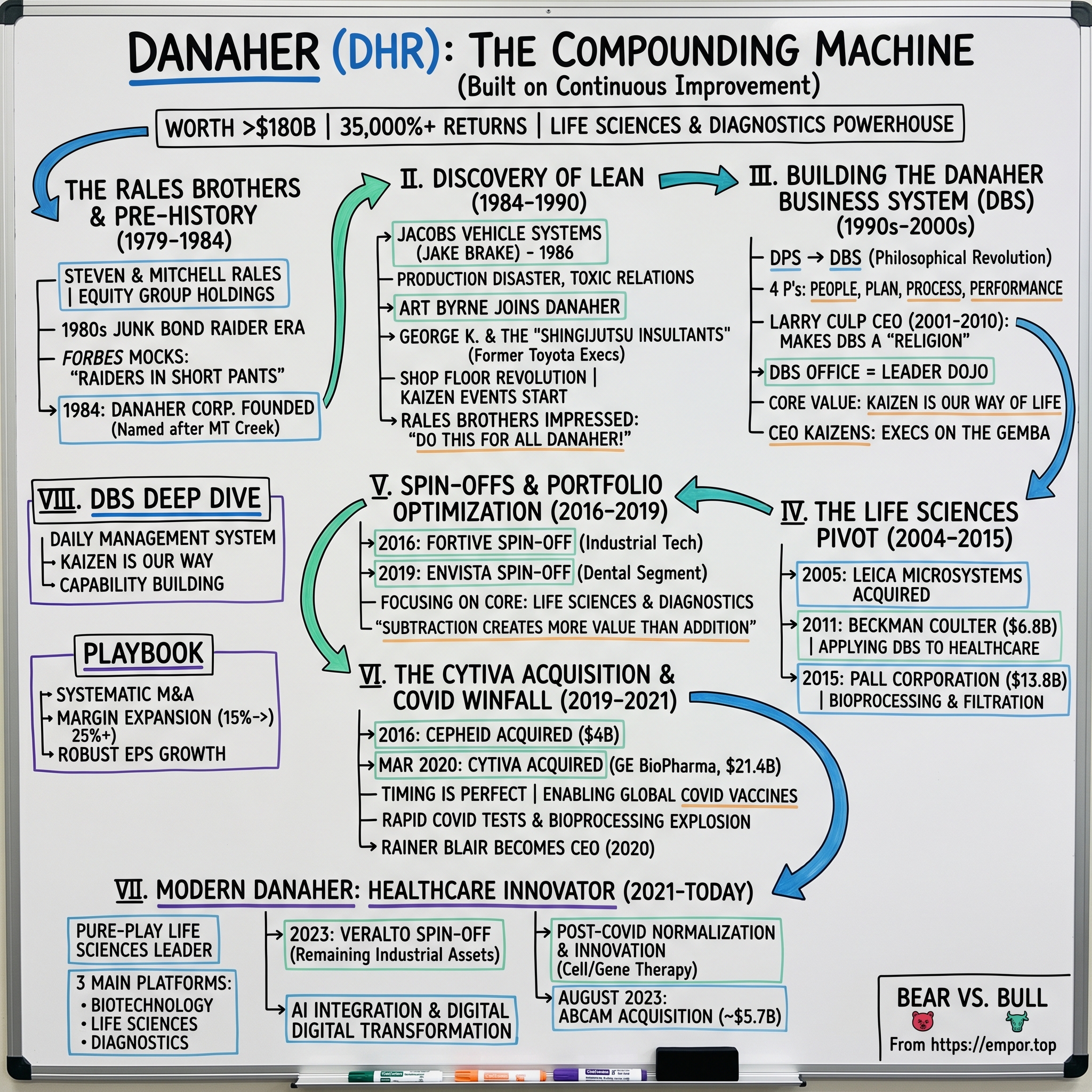

Picture this: A company worth over $180 billion that most people have never heard of. A conglomerate that touches nearly every COVID-19 vaccine produced, every cancer diagnosis made, and countless life-saving medical breakthroughs—yet operates almost invisibly behind the scenes. This is Danaher Corporation today, a life sciences and diagnostics powerhouse that has delivered returns exceeding 35,000% since its founding, crushing the S&P 500's performance by orders of magnitude.

But here's the paradox that makes this story irresistible: How did two brothers who started their careers being mocked by Forbes as "corporate raiders in short pants" build one of history's greatest compounding machines? How did hostile takeover artists transform themselves into operational excellence zealots who would make Toyota's production engineers proud?

The answer lies in one of corporate America's most unlikely transformations. Steven and Mitchell Rales didn't just build a company—they built a system. Not just any system, but the Danaher Business System (DBS), arguably the most successful operational framework ever deployed by a Western corporation. It's a system so powerful that former executives who leave Danaher are recruited like star athletes, commanding premium salaries to replicate its magic elsewhere.

Today, Danaher Corporation stands as an American global conglomerate designing, manufacturing, and marketing medical, industrial, and commercial products and services across the world. Headquartered in Washington, D.C., the company holds $78.5 billion in assets as of 2024. But those numbers only hint at the real story—a four-decade journey from leveraged buyouts to lean manufacturing, from industrial tools to biotechnology, from financial engineering to operational artistry.

What we're about to explore isn't just a corporate success story. It's a masterclass in evolution, discipline, and the compounding power of continuous improvement. It's about how two brothers fishing in Montana conceived a corporate philosophy that would ultimately help produce the world's COVID vaccines, enable breakthrough cancer treatments, and create more shareholder value than almost any company in history. This is the story of how raiders became builders, how a production system became a religion, and how Danaher became the compounding machine that every conglomerate wishes it could be.

II. The Rales Brothers & Pre-History (1969–1984)

The Danaher story doesn't begin in a garage or a dorm room, but in the decidedly unglamorous world of 1970s real estate investment trusts. The company's DNA actually traces back to 1969, when a Massachusetts REIT called DMG, Inc. was quietly organizing deals that no one would remember. By 1978, this entity had morphed into Diversified Mortgage Investors, Inc., a Florida corporation that was about as exciting as its name suggests. But this corporate shell would soon become the vessel for something extraordinary.

Enter Steven and Mitchell Rales in 1979. The brothers had just walked away from their father Norman's real estate firm—itself a fascinating operation that pioneered employee stock ownership plans (ESOPs) in America. Norman Rales wasn't just any real estate developer; he was a visionary who believed employees should own stakes in their companies, a philosophy that would echo through his sons' future empire in unexpected ways. When Steven and Mitchell left to found Equity Group Holdings, they carried with them not just capital but a distinct philosophy about ownership, incentives, and value creation.

The early 1980s were the Wild West of American finance. Michael Milken's junk bonds were revolutionizing corporate takeovers, and hostile acquisitions were the path to quick riches. The Rales brothers, both still in their thirties, dove headfirst into this world. They weren't building anything yet—they were hunting. Their strategy was simple but aggressive: identify undervalued industrial companies, leverage up with high-yield debt, take control, and then figure out what to do with them.

Forbes magazine wasn't impressed. In a scathing piece, they dismissed the brothers as "raiders in short pants," suggesting these Washington prep school kids were playing with fire in a game meant for grown-ups. The mockery stung, but it also lit a fire. Mitchell Rales would later say that article was "motivating in ways Forbes never intended." The brothers weren't just going to prove the magazine wrong—they were going to build something that would make the raiders label obsolete. In 1984, everything crystallized. The brothers reincorporated their holdings under Delaware law and gave their company a new name: Danaher. It was named after Danaher Creek in Western Montana, where the brothers had conceptualized it while fishing. The choice wasn't random. The origin of the name "Danaher" goes back to the root "Dana," a Celtic word dating from before 700 BC and meaning "swift flowing". Standing by that Montana stream, the Rales brothers weren't just naming a company—they were articulating a philosophy. Like the creek that constantly flows and adapts to its terrain while maintaining its essential force, their company would be about continuous movement, adaptation, and relentless forward momentum.

But what exactly would Danaher be? At this point, even the brothers weren't entirely sure. They had capital, they had ambition, and they had something to prove. What they didn't have was an operating philosophy beyond "buy cheap and figure it out." That would soon change in ways that would shock even them. Within two years of Danaher's founding in 1984, Danaher acquired 12 companies as part of a strategy to enter the manufacturing business. They were building a portfolio, but they hadn't yet discovered the secret that would transform their collection of industrial assets into something extraordinary.

III. The Early Industrial Years & Discovery of Lean (1984–1990)

The transformation of Danaher from financial engineering outfit to operational excellence powerhouse began, improbably, with truck brakes. Jacobs Manufacturing Company, maker of the Jake Brake engine retarder system beloved by truckers and feared by suburban residents for its distinctive roar, would become ground zero for one of the most successful implementations of lean manufacturing in American corporate history.

When the Rales brothers acquired Jacobs Vehicle Systems (Jake Brake) in 1986, they inherited a classic American manufacturing disaster. The factory floor was chaos—inventory piled to the ceiling, workers standing idle while waiting for parts, quality problems that seemed intractable. Union relations were toxic. The company was profitable on paper but bleeding potential. It was exactly the kind of operational mess that most financial engineers would either ignore or try to fix with layoffs and cost-cutting. Enter Art Byrne. Arriving at Danaher at the end of 1985 as Group Executive, Byrne had already experimented with Just-in-Time production at General Electric. At that time only two people in Danaher had any exposure to what we called Just-in-Time: myself, from my first general manager's job at General Electric, and the guy I had appointed as President of Jake Brake, George Koenigsaecker (George K.) from his prior experience at John Deere and Rockwell. Together with George Koenigsaecker, they would orchestrate one of the most dramatic operational transformations in American industrial history.

We knew we had to make drastic changes at Jake Brake or we would lose it, and we both wanted to use Just-in-Time as the approach. Our auditor at the time, Arthur Anderson, had a consulting arm that was selling Just-in-Time knowledge so we started with them in 1986. But Arthur Anderson's PowerPoint-heavy approach wasn't cutting it. The breakthrough came when Koenigsaecker discovered a seminar being taught by Shingijutsu consultants—three former Toyota executives who had worked directly for Taiichi Ohno himself, the father of the Toyota Production System.

The seminar was taught by the Shingijutsu consultants – three former Toyota executives who had worked directly for Taiichi Ohno, the father of the Toyota Production System, teaching TPS to Toyota's first-tier suppliers. George and I thought, "wow, these are the guys who could really help us," and George badgered them all week. He bought them dinner one night and took them to the plant afterwards. They came again later in the week when I could be there, and we had another meeting on Saturday morning before they left. Basically, we begged them to come help us. They said, "We are too old, we don't speak English, and it is too far away." We said, "But we have great steaks and lobster and lots of golf." I think golf won the argument.

What happened next was corporate theater at its finest. The Shingijutsu men told us, "Everything here is no good, what do you want to do about it?" They weren't normal consultants. No PowerPoint presentations. In fact, no presentations at all. We just worked on the shop floor finding and eliminating waste. They called themselves "insultants," not consultants, and their brutal honesty was exactly what Danaher needed.

The real magic happened when the Rales brothers came to inspect the chaos at Jake Brake. Inventory was dropping so fast that under standard cost accounting, the numbers looked terrible. As Jake Brake improved we were dropping inventory like a stone, and with Danaher's standard cost accounting our numbers weren't looking too good. In fact the Rales brothers called a "special emergency meeting" to see what was going on.

Koenigsaecker had a brilliant idea: instead of presenting financials in a conference room, they would start the visit on the shop floor. George K. then came up with the brilliant idea to have the workers in each area (all UAW members) conduct the tour. This took about three hours as our union guys were really into it. When we finally got to the conference room there was no review of the numbers. The Rales brothers, to their credit, just said, "Wow, how fast can you do this in the rest of Danaher?"

This moment marked the true birth of Danaher as we know it today. Well in my prior role as Group Executive of The Danaher Company, one of my group companies, Jake Brake, achieved a 29% productivity gain each year for the first five years with a workforce that belonged to the U.A.W. The union workers who had been ready to strike were now evangelists for continuous improvement. The lean revolution had begun.

When George Sherman was hired as CEO in 1990, he brought professional management to what had been essentially a family-run operation. When George Sherman became CEO in 1990, he asked me to "do for Danaher what you guys did to Jake Brake." The stage was set for transforming lean from a single factory experiment into a comprehensive business system that would become Danaher's defining characteristic.

IV. Building the Danaher Business System (1990s–2000s)

The evolution from the Danaher Production System to the Danaher Business System wasn't just a name change—it was a philosophical revolution. Originally, Danaher's process was called the Danaher Production System (DPS) and was shamelessly modeled after TPS. But the Rales brothers and their team quickly realized that manufacturing excellence alone wouldn't be enough. They needed something more comprehensive, more scalable, and uniquely Danaher.

The transformation began with a simple but profound insight: lean principles could be applied everywhere, not just on factory floors. Finance, sales, R&D, even corporate strategy—all could benefit from the relentless pursuit of waste elimination and continuous improvement. The company formally adopted the four P's framework: People, Plan, Process, and Performance. This wasn't corporate buzzword bingo; it was a systematic approach to making every aspect of the business better, every single day. The real power of DBS emerged when Larry Culp took the helm as CEO in 2001. The journey of Larry Culp with Kaizen began long before he assumed the role of the first outsider CEO of GE in 2018. His deep dive into continuous improvement methodologies left a permanent mark on his tenure at Danaher Corporation, propelling it to the forefront of operational efficiency and innovation. Under Culp's guidance, Danaher embraced the Kaizen philosophy, weaving it into its operations. Culp didn't just implement lean tools—he made them a religion. According to former CEO Larry Culp, "The DBS process system is the soul of Danaher; the system guides planning and execution."

The creation of the DBS Office was perhaps the most brilliant organizational innovation in Danaher's history. This wasn't just another corporate department—it was a dojo for operational excellence. He created the leadership development program where future leaders rotate through the DBS office for development purposes. He created the M&A integration process as well as the due diligence process as it related to DBS. And along with Larry Culp, Danaher CEO (and now the CEO of GE), developed the strategic planning process for all of Danaher.

But what made DBS truly special wasn't the tools—it was the cultural transformation. A Japanese philosophy centered on continuous improvement, kaizen serves as the cornerstone of the Danaher Business System (DBS), which is a key differentiator that sets Danaher's work and associate experience apart. A core value for the company is Kaizen is Our Way of Life. CEO Kaizens became legendary events. Picture this: the CEO of a multi-billion dollar company spending five days on a factory floor, sleeves rolled up, working alongside line operators to solve problems. In 2023, CEO Kaizens across Danaher operating companies focused on operational performance, inventory reduction, past-due backlog and on-time delivery – all complex challenges that directly impact customers. At the 2023 CEO Kaizen event with Cepheid in Solna, Sweden, the team focused on improving their material flow between factories, as well as within the production line, to ultimately reduce inventory. "This is what we do," said Weidemanis, who participated in the 5-day event. "We get together and we attack an important problem for our customers or for our associates in a week – and we get it done in a week."

The financial results were staggering. Due to the DBS Culture and the Strat to Action Process, Danaher has grown profitably by almost 30% every year. This is also reflected in market valuation: 80.000% growth since the 1980s.The generation of extremely high Free Cash Flows allowed the company to implement a very successful M&A Strategy with a strong effect in TSR Total Shareholder Returns. The evolution of KAIZEN™ from the manufacturing floor and the back office to innovation, marketing, R&D and sales allowed for a cumulative return on Danaher's stock from 2001–2010 over 150%, in comparison with S&P 500 returns of about 25%.

The system became self-reinforcing. Every acquisition wasn't just buying a company—it was acquiring raw material for the DBS machine to transform. "That's why, for me, the DBS Office is the secret sauce of Danaher. It's a culture that's difficult to copy, almost impossible." Companies would come in bloated and inefficient; within months, they'd be running like Swiss watches, with employees wondering how they ever operated any other way.

As the 2000s progressed, DBS evolved from a manufacturing system to a complete business philosophy. Sales teams used kaizen to improve customer relationships. R&D departments applied lean principles to accelerate product development. Even the corporate finance function embraced continuous improvement, dramatically reducing close times and improving accuracy. The transformation was so complete that when executives left Danaher, they were recruited like star athletes, commanding premium salaries to bring the DBS magic to other companies.

V. The Life Sciences Pivot & Major Acquisitions (2004–2015)

The boardroom at Danaher headquarters must have felt electric in 2004. After two decades of perfecting their operational excellence machine in the industrial sector, the Rales brothers and their team saw an opportunity that would fundamentally reshape their company: life sciences and diagnostics. It wasn't just about finding a new market—it was about recognizing where their unique capabilities could create the most value in the 21st century. Danaher established the life sciences business in 2005 through the acquisition of Leica Microsystems and has expanded the business through numerous subsequent acquisitions. But the real statement of intent came in 2011. Danaher announced it has entered into a definitive merger agreement with Beckman Coulter, Inc. pursuant to which Danaher will acquire Beckman Coulter by making a cash tender offer to acquire all of the outstanding shares of common stock of Beckman Coulter at a purchase price of $83.50 per share, for a total enterprise value of approximately $6.8 billion, including debt assumed and net of cash acquired.

Beckman Coulter wasn't just any acquisition—it was a transformational bet on the future of healthcare. With annual revenues of approximately $3.7 billion, Beckman Coulter develops, manufactures and markets products that simplify, automate and innovate complex biomedical testing. Its diagnostic systems are found in hospitals and other clinical settings around the world and produce information used by physicians to diagnose disease, make treatment decisions and monitor patients. Scientists use its life science research instruments to study complex biological problems including causes of disease and potential new therapies or drugs.

The acquisition price represented a 45% premium to Beckman Coulter's stock price, causing skeptics to question whether Danaher was overpaying. But the Rales brothers and Larry Culp saw what others didn't: an underperforming asset that would thrive under DBS. Within months of closing the deal, Danaher teams descended on Beckman Coulter facilities with the precision of a military operation. Kaizen events were scheduled, value stream maps were drawn, and the transformation began.

The results were nothing short of spectacular. Beckman Coulter's operating margins expanded by hundreds of basis points. Product development cycles shortened. Customer satisfaction scores soared. What had been a good but stagnant company became a growth engine, validating Danaher's thesis that operational excellence could unlock value in life sciences just as it had in industrial markets. In May 2015, Danaher announced the acquisition of Pall Corporation for $13.8 billion. Danaher Corporation announced today that it has entered into a definitive merger agreement with Pall Corporation pursuant to which Danaher will acquire all of the outstanding shares of Pall for $127.20 per share in cash, or a total enterprise value of approximately $13.8 billion, including assumed debt and net of acquired cash. This wasn't just another acquisition—it was Danaher's biggest bet yet, nearly doubling the Beckman Coulter price tag.

Pall is a leading global provider of filtration, separation and purification solutions that remove contaminants or separate substances from a variety of solids, liquids and gases. Decades of work by Pall's filtration engineers and scientists have built a highly-respected brand on which customers rely to solve their most difficult purification problems across the broad spectrum of life sciences and industry. The strategic logic was compelling: Pall's filtration technologies were essential to bioprocessing—the very processes used to manufacture biologics, vaccines, and cell therapies.

The integration of Pall showcased DBS at its most powerful. Within months, Pall's operating margins began expanding as waste was eliminated and processes streamlined. As Pall is integrated into the Company, the Company also expects to realize significant cost synergies through the application of the Danaher Business System and the combined purchasing power of the Company and Pall. Customer satisfaction improved as delivery times shortened and quality metrics soared. The transformation was so successful that competitors began studying the "Danaher playbook" for acquisitions.

But the genius of Danaher's life sciences pivot wasn't just about individual acquisitions—it was about building an ecosystem. Each acquisition strengthened the others. Beckman Coulter's diagnostic instruments worked alongside Pall's filtration systems in hospital labs. Leica's microscopes enabled research that drove demand for other Danaher products. The company was creating a virtuous cycle where each business unit made the others more valuable.

By 2015, more than 50% of Danaher's revenue came from life sciences and diagnostics, a remarkable transformation for a company that had started as an industrial conglomerate. The financial performance validated the strategy: margins expanded, organic growth accelerated, and returns on invested capital soared. The market rewarded this transformation with premium valuations that reflected Danaher's new identity as a critical enabler of global healthcare innovation.

VI. Spin-offs & Portfolio Optimization (2016–2019)

The conference room at Danaher headquarters in June 2016 witnessed a decision that would have seemed heretical to most conglomerates: voluntarily giving up billions in profitable revenue. In June 2016, Danaher spun off several subsidiaries, including Matco and AMMCO-COATS, to create Fortive Corporation. This spin-off included businesses in fields such as instrumentation, transportation, and industrial technologies—solid, profitable businesses that most companies would fight to keep.

But Danaher's leadership understood something profound about value creation: sometimes subtraction creates more value than addition. The industrial businesses being spun into Fortive were good businesses, generating strong cash flows and solid returns. But they were increasingly distant from Danaher's emerging identity as a life sciences and diagnostics leader. The management attention, capital allocation, and strategic focus these businesses required diluted Danaher's ability to maximize value in its higher-growth, higher-margin life sciences portfolio.

The Fortive spin-off was executed with surgical precision. The new company launched with approximately $6.2 billion in annual revenue and a portfolio of market-leading brands in instrumentation and industrial technologies. Danaher shareholders received one share of Fortive for every two shares of Danaher they owned, creating immediate value while maintaining their exposure to both business models. The market's reaction was telling: both companies' combined market value quickly exceeded Danaher's pre-spin value, validating the portfolio optimization strategy.

The corporate spin-off was completed in December 2019, with the new company called Envista Holdings Corporation. Danaher spun off its dental segment into a separate publicly traded company, Envista Holdings Corporation in 2019. This move allowed Danaher to focus more on its core areas in life sciences and diagnostics. The dental business, while profitable and well-run, required different capabilities and served different end markets than Danaher's core life sciences franchise.

The logic behind these spin-offs revealed Danaher's sophisticated understanding of capital allocation. Each business had different growth rates, margin profiles, and capital requirements. By separating them, each could optimize its capital structure, pursue appropriate acquisition strategies, and attract investors who understood their specific value propositions. It was financial engineering at its finest, but backed by operational excellence that ensured each entity could thrive independently.

What made these spin-offs particularly impressive was the care taken to ensure each new company launched with the capabilities to succeed. Fortive and Envista didn't just inherit assets—they inherited trained teams steeped in DBS principles, strong balance sheets, and clear strategic roadmaps. Each company launched with its own version of the business system, ensuring the operational excellence DNA would continue even after separation.

The market's response validated Danaher's portfolio optimization strategy. By focusing on higher-growth, higher-margin businesses with stronger competitive moats, Danaher commanded premium valuations. The spin-offs allowed investors to make pure-play bets on different sectors while unlocking value that had been hidden in the conglomerate structure. It was a masterclass in how to evolve a portfolio without destroying value—indeed, while creating substantial new value for shareholders.

VII. The Cytiva Acquisition & COVID Windfall (2019–2021)

In September 2016, the company announced it would acquire Cepheid for $4 billion, adding molecular diagnostics capabilities that would prove prescient. But nothing could have prepared Danaher—or the world—for what was coming in 2020.

In March 2020, Danaher acquired the biopharma business of the General Electric Life Sciences division for $21.4 billion and was named Cytiva. The timing seemed risky—a massive acquisition just as COVID-19 was shutting down the global economy. Wall Street questioned whether Danaher was overextending itself at precisely the wrong moment. But the Rales brothers and CEO Tom Joyce saw opportunity where others saw chaos.

Cytiva is a global provider of technologies and services related to the development, manufacture, and delivery of vaccines, diagnostics, and therapeutics to customers in organizations including academia, biotechnology, and drug manufacturing. Within weeks of closing the acquisition, it became clear that Danaher had accidentally timed the deal of the century. Every COVID vaccine in development needed Cytiva's bioprocessing technologies. Every scaling effort required their bioreactors, chromatography systems, and filtration products.

The operational excellence of DBS proved its worth during the supply chain chaos of 2020-2021. While competitors struggled with component shortages and logistics nightmares, Danaher's systematic approach to inventory management, supplier relationships, and operational flexibility allowed them to meet exploding demand. Cytiva's revenues surged as vaccine manufacturers placed massive orders, sometimes years in advance, to secure production capacity.

But Danaher didn't just ride the COVID wave—they enabled it. Their Cepheid molecular diagnostics business developed one of the first rapid COVID tests. Their life sciences tools accelerated vaccine development timelines from years to months. Their bioprocessing technologies scaled vaccine production to billions of doses. Danaher wasn't just a beneficiary of the pandemic response; they were an architect of it.

The financial windfall was staggering. Danaher's stock price nearly doubled during the pandemic as revenues and margins expanded dramatically. But leadership understood this was a temporary phenomenon. Unlike companies that assumed the COVID boom would continue indefinitely, Danaher began preparing for normalization even as they capitalized on near-term opportunities. They used the cash windfall to strengthen their balance sheet, invest in R&D, and position for post-pandemic growth.

In May 2020, it was announced that Tom Joyce would retire as CEO of the company. He was replaced by Executive Vice President Rainer Blair on September 1, 2020. The leadership transition during this period of extreme growth and uncertainty demonstrated the depth of Danaher's bench strength. Blair, a long-time Danaher executive steeped in DBS principles, seamlessly took the helm, maintaining strategic continuity while navigating unprecedented market dynamics.

VIII. Modern Danaher: Life Sciences & Diagnostics Leader (2021–Today)

Today's Danaher would be nearly unrecognizable to someone who knew the company in its industrial conglomerate days. With a market capitalization exceeding $180 billion and annual revenues approaching $30 billion, it stands as one of the world's premier life sciences and diagnostics companies. More than 50% of Danaher's total revenue today has been acquired in the past decade, but you'd never know it from the seamless integration and operational excellence across the portfolio.

The company's current structure reflects decades of strategic evolution. Three main platforms dominate: Biotechnology (including Cytiva and Pall), Life Sciences (including Beckman Coulter Life Sciences and Leica Microsystems), and Diagnostics (including Beckman Coulter Diagnostics, Cepheid, and Radiometer). Each platform operates with significant autonomy while benefiting from shared DBS expertise, purchasing power, and best practices.

On February 8, 2023, Danaher announced that the new company is named Veralto Corporation and will be headed by Danaher Executive Vice President Jennifer Honeycutt as Veralto's President and CEO. On September 30, Danaher announced the separation completion of Veralto and that Veralto will begin trading on the New York Stock Exchange on October 2 under the symbol "VLTO." The Veralto spin-off in 2023 represented the final step in Danaher's transformation to a pure-play life sciences company, divesting the remaining industrial assets to focus entirely on healthcare and life sciences.

But the post-COVID normalization has brought challenges. Bioprocessing demand has moderated from pandemic peaks, causing some investors to question whether Danaher can maintain its growth trajectory. The company has responded by accelerating innovation, with particular focus on cell and gene therapy manufacturing, continuous bioprocessing, and automation. These next-generation technologies represent the future of biopharmaceutical manufacturing, and Danaher is positioning itself to be as essential to these emerging modalities as it was to COVID vaccine production.

Competition has intensified, with Thermo Fisher Scientific, Agilent, and others aggressively pursuing similar strategies. But Danaher's competitive moat remains formidable. The company's installed base creates powerful switching costs—when a drug is approved using Danaher equipment, manufacturers are reluctant to change suppliers and risk regulatory complications. The breadth of Danaher's portfolio creates unique cross-selling opportunities that standalone competitors can't match.

On August 28, 2023, Danaher announced that it had entered into a definitive agreement to acquire Abcam for approximately $5.7 billion at $24 per share in cash. The Abcam acquisition demonstrates Danaher's continued commitment to strategic growth, adding critical antibody and reagent capabilities that strengthen its life sciences research offerings.

The integration of artificial intelligence and automation across Danaher's portfolio represents the next frontier. From AI-powered diagnostic algorithms in Cepheid's systems to automated bioprocessing in Cytiva's facilities, the company is systematically digitizing and automating workflows. This isn't just about efficiency—it's about enabling entirely new capabilities that weren't possible with manual processes.

Under Rainer Blair's leadership, Danaher has maintained its cultural commitment to continuous improvement while adapting to new realities. The company has embraced remote work flexibility while preserving the hands-on, gemba-walking culture that defines DBS. Virtual kaizen events have proven surprisingly effective, though nothing quite replaces the energy of in-person problem-solving sessions on the factory floor.

IX. The DBS Deep Dive: Why It Works

The Danaher Business System (DBS) is our system of continuous improvement and the culture that makes it work. This simple statement understates what might be the most successful operational framework ever deployed by a Western corporation. DBS isn't just a set of tools or processes—it's a complete philosophy that permeates every aspect of how Danaher operates.

At its core, DBS represents the marriage of Japanese lean principles with American entrepreneurial capitalism. When it started at Jake Brake in 1987, it was simply an attempt to copy Toyota's Production System. But over four decades, it has evolved into something uniquely Danaher. The system maintains the relentless focus on waste elimination and continuous improvement from its Toyota inspiration while adding layers of strategic thinking, acquisition integration, and innovation management that Toyota never needed.

A core value for the company is Kaizen is Our Way of Life. This isn't corporate speak—it's lived reality. Every Danaher employee, from factory workers to the CEO, participates in kaizen events. The CEO Kaizens are legendary: five-day intensive problem-solving sessions where senior executives work alongside front-line employees to solve critical business challenges. Picture the CEO of a $180 billion company spending a week on a factory floor in Sweden, sleeves rolled up, mapping material flows and calculating takt times. That's not photo-op leadership—that's DBS in action.

The daily management system forms the backbone of DBS execution. Every morning, in every Danaher facility worldwide, teams gather for brief stand-up meetings around visual management boards. Problems are identified, solutions are proposed, and progress is tracked. It's deliberately low-tech—whiteboards and markers rather than digital dashboards—because the physical act of writing and discussing creates engagement that screens can't replicate.

But what truly distinguishes DBS is its approach to capability building. He created the leadership development program where future leaders rotate through the DBS office for development purposes. The DBS Office isn't just a training center—it's a dojo where future leaders learn by doing. High-potential employees spend two years rotating through different businesses, leading kaizen events, solving problems, and absorbing the DBS philosophy through intensive practice.

The post-acquisition integration playbook represents DBS at its most powerful. When Danaher acquires a company, the integration follows a precise choreography. Week one: assessment and prioritization. Week two: first kaizen events targeting quick wins. Month one: value stream mapping and organizational design. Month three: full DBS deployment with trained internal champions. Month six: measurable improvements in quality, delivery, cost, and innovation metrics. The speed and predictability of these transformations astound newcomers who assume such changes must take years.

That's why, for me, the DBS Office is the secret sauce of Danaher. It's a culture that's difficult to copy, almost impossible. Why can't competitors replicate DBS despite decades of trying? The answer lies in the depth of cultural embedding. DBS isn't something Danaher does—it's what Danaher is. Every promotion decision, every capital allocation, every strategic choice is filtered through DBS principles. Employees who don't embrace continuous improvement don't last. Leaders who can't teach kaizen don't advance.

The measurement systems within DBS create unambiguous accountability. Every process has a metric. Every metric has an owner. Every owner has a improvement target. But unlike the suffocating bureaucracy this might suggest, the system creates clarity and empowerment. When everyone knows exactly what success looks like and has the tools to achieve it, extraordinary performance becomes routine.

The cultural elements of DBS prove equally important as the technical tools. Respect for people isn't just a slogan—it's embedded in every practice. When efficiency improvements eliminate work, employees aren't laid off; they're redeployed to higher-value activities. When mistakes happen, the focus is on process improvement, not blame. This psychological safety enables the rapid experimentation and honest problem-solving that drives continuous improvement.

X. Playbook: Capital Allocation & Operating Lessons

Since our founding in 1984, we've acquired hundreds of businesses. This understates one of the greatest capital allocation track records in corporate history. Danaher's approach to M&A isn't about empire building—it's about systematic value creation through operational transformation.

The acquisition criteria are remarkably consistent: market-leading positions, recurring revenue models, mission-critical products, and significant improvement potential under DBS. Danaher walks away from auctions where financial engineering is the only value creation lever. They want businesses where operational excellence can unlock transformative value. This discipline means they often lose bidding wars to private equity firms willing to use more leverage, but it also means their acquisitions consistently exceed synergy targets.

The math of operational improvement is compelling. A typical Danaher acquisition might have 15% EBITDA margins. Through DBS implementation, margins expand to 25% or higher within three years. Revenue growth accelerates from low single digits to mid-single digits or better through improved innovation and customer satisfaction. Working capital turns improve dramatically as inventory is reduced and cash collection accelerates. The cumulative effect: businesses worth 50-100% more than their purchase price within 3-5 years, before considering any revenue synergies.

Danaher's remarkable increase in earnings per share — an impressive ~10,000% since 1990 — underscores this immense success. But this isn't financial engineering—it's operational transformation that creates lasting value. Unlike leveraged buyouts that strip assets and cut costs, Danaher acquisitions typically see increased investment in R&D, improved employee engagement, and stronger market positions.

The decision framework for spin-offs reveals sophisticated portfolio theory in practice. Danaher divests businesses when: (1) they no longer fit the strategic focus, (2) they require different operating models or investment profiles, (3) they can achieve better valuations as standalone entities, or (4) the management attention they require exceeds their contribution to enterprise value. The Fortive and Envista spin-offs weren't failures—they were successful graduations of businesses ready to pursue independent strategies.

Building durable competitive advantages through operational excellence seems almost quaint in an era obsessed with software moats and network effects. But Danaher proves that exceptional execution can be just as powerful as technological disruption. When every process runs better, when every product launches faster, when every customer interaction satisfies more completely, the cumulative advantage becomes insurmountable.

The Rales brothers' ownership structure deserves special mention. Despite decades of acquisitions and equity issuance, they maintain significant ownership stakes that align their interests with long-term value creation. They don't take excessive compensation, don't pursue vanity projects, and don't prioritize quarterly earnings over long-term value. This owner-operator mentality permeates the organization, from capital allocation decisions to daily operating choices.

For other companies trying to replicate Danaher's success, the lessons are clear but difficult to implement: commit completely to operational excellence, invest heavily in capability building, maintain discipline in capital allocation, and cultivate a culture that values continuous improvement over continuous reorganization. The tools of DBS can be copied, but the decades of cultural development, the depth of expertise, and the systemic nature of the transformation cannot be easily replicated.

XI. Bear & Bull Cases

Bull Case: The Compounding Machine Continues

The bull case for Danaher rests on four powerful pillars that suggest the compounding machine has decades of growth ahead.

First, the operational excellence moat grows wider every year. While competitors chase the latest management fads, Danaher has spent four decades perfecting a single system. The accumulated expertise in DBS creates a competitive advantage that money can't buy and time can't shortcut. When Danaher acquires a company, they bring 40 years of pattern recognition about what works and what doesn't. This institutional knowledge compounds with each acquisition, making the next transformation faster and more certain.

Second, Danaher occupies critical positions in structurally growing markets. The biologics market is expected to grow at double-digit rates for the foreseeable future, driven by aging populations, emerging market healthcare expansion, and continuous therapeutic innovation. Cell and gene therapies, which require Danaher's tools at every step from development to manufacturing, are just beginning their growth trajectory. The company's installed base creates powerful recurring revenue streams—when a drug is manufactured using Danaher equipment, switching costs ensure decades of consumable sales and service contracts.

Third, the capital allocation track record suggests the Rales brothers and their team have developed a repeatable formula for value creation. Through multiple economic cycles, changing interest rate environments, and technological disruptions, Danaher has consistently identified, acquired, and improved businesses. The pipeline of potential acquisitions in fragmented life sciences markets remains robust, providing decades of deployment opportunities for Danaher's proven playbook.

Fourth, DBS provides a sustainable competitive advantage in an era where operational excellence matters more than ever. As supply chains grow more complex, regulations more stringent, and customer expectations higher, the ability to consistently execute becomes increasingly valuable. Danaher's systematic approach to problem-solving, standardized processes, and continuous improvement culture create resilience that pure-play competitors lack.

Bear Case: The Excellence Premium Faces Pressure

The bear case warns that Danaher's extraordinary run faces meaningful headwinds that could compress multiples and slow growth.

Premium valuations require perfect execution, and the law of large numbers suggests this becomes increasingly difficult. At nearly $30 billion in revenue, finding acquisitions large enough to move the needle becomes challenging. The company trades at significant premiums to both historical averages and peers, suggesting the market has already priced in flawless execution. Any stumble—a failed acquisition, integration problems, or competitive losses—could trigger multiple compression that overwhelms operational improvements.

The bioprocessing normalization post-COVID represents more than a temporary headwind. The pandemic pulled forward years of demand as pharmaceutical companies over-ordered to ensure supply. This inventory digestion could last years, creating a sustained headwind to growth in Danaher's largest and most profitable segment. Meanwhile, competitors have used pandemic windfalls to invest aggressively in competing technologies, potentially eroding Danaher's competitive advantages.

Integration risks multiply with mega-acquisitions. The Cytiva acquisition was Danaher's largest ever, and successfully integrating a $21 billion acquisition during a pandemic stretched even Danaher's proven capabilities. Future large acquisitions may prove harder to transform, especially as target companies become more sophisticated and Danaher's playbook becomes widely understood. The pool of underperforming assets that can be transformed through operational excellence may be shrinking.

Competition from well-capitalized peers intensifies every year. Thermo Fisher Scientific, with revenues exceeding $40 billion, has similar M&A firepower and operational capabilities. Private equity firms have hired former Danaher executives and explicitly copied DBS principles. Chinese competitors are emerging with government backing and cost advantages. The competitive landscape looks fundamentally different than when Danaher could acquire neglected divisions from unfocused conglomerates.

The Balanced View

The truth likely lies between these extremes. Danaher's operational excellence culture and proven acquisition model provide durable advantages, but premium valuations and increasing competition limit upside potential. The company will likely continue compounding value, but at rates closer to market averages than the extraordinary outperformance of the past four decades. For investors, the question isn't whether Danaher is a quality company—that's indisputable—but whether quality justifies the premium price in an environment where operational excellence is increasingly table stakes rather than differentiation.

XII. Epilogue: Lessons & Legacy

From "raiders in short pants" to builders of one of history's great compounding machines—the transformation of Steven and Mitchell Rales mirrors the transformation of American capitalism itself. When Forbes mocked them in the 1980s, corporate raiders were destroying value through financial engineering. The Rales brothers chose a different path, proving that operational excellence could create more value than financial leverage ever could.

Since the start of this chart, Danaher's stock has returned over 35,000% for its shareholders – excluding dividends. This staggering number represents more than financial success—it validates a philosophy. In an era obsessed with disruption, Danaher proved that continuous improvement beats discontinuous innovation. While Silicon Valley preached "move fast and break things," Danaher whispered "move deliberately and fix things."

The lesson that culture and systems beat strategy resonates far beyond Danaher's walls. Strategy provides direction, but culture determines whether you'll reach the destination. DBS isn't Danaher's strategy—strategies change with market conditions. DBS is Danaher's culture, and culture endures. When every employee from janitor to CEO shares a common language of continuous improvement, believes in data-driven decision making, and takes ownership of problems, the organization develops a resilience that transcends any individual leader or strategic plan.

The compounding power of continuous improvement offers perhaps the most profound lesson. Improving by 1% doesn't sound impressive, but 1% improvement every week compounds to 67% annual improvement. This mathematical reality, lived out over four decades at Danaher, demonstrates that consistency beats intensity. While competitors pursue dramatic transformations and bet-the-company pivots, Danaher simply gets better every single day.

What founders and operators can learn from Danaher extends beyond operational excellence. The company demonstrates that patient capital, aligned incentives, and long-term thinking create extraordinary value. The Rales brothers didn't optimize for quarterly earnings or exit multiples—they optimized for building something lasting. They didn't chase hot sectors or trendy technologies—they pursued boring, essential businesses where operational excellence could shine.

Looking ahead to the next 40 years, can the machine keep compounding? The challenges are real: size, competition, and valuation all create headwinds. But betting against Danaher means betting against the power of systematic improvement, the value of operational excellence, and the durability of strong culture. History suggests that's a dangerous bet.

The ultimate legacy of Danaher isn't the wealth created or the companies transformed—it's the proof that American manufacturing can compete with anyone when armed with the right system and culture. In an economy increasingly dominated by software and services, Danaher reminds us that making physical things still matters, that manufacturing excellence still creates value, and that the principles of continuous improvement apply universally.

For investors, operators, and students of business, Danaher offers a masterclass in value creation through operational excellence. The company proves that sustainable competitive advantages don't require proprietary technology or network effects—they can be built through superior execution, systematic improvement, and cultural excellence. In a business world obsessed with disruption, Danaher's steady compounding offers a powerful counternarrative: sometimes the best strategy is simply to be better than everyone else at the basics, and then get better still, every single day, forever.

The machine that Steven and Mitchell Rales built beside Danaher Creek continues its swift flow, adapting to new terrain while maintaining its essential force. Like the creek that inspired its name, Danaher demonstrates that persistent, directed flow can carve through any obstacle, creating value that compounds across generations. The raiders in short pants became builders of something permanent, proving that the greatest transformations come not from financial engineering but from the patient work of making things better, one improvement at a time, forever.

XIII. Recent News

For the first quarter 2025, the Company anticipates that non-GAAP core revenue will decline low-single digits year-over-year. For full year 2025, the Company expects that non-GAAP core revenue will increase approximately 3% year-over-year. This guidance reflects the ongoing normalization of bioprocessing demand post-COVID, but also demonstrates confidence in the company's long-term growth trajectory.

Danaher has appointed Martin Stumpe as Chief Technology and AI Officer, effective October 1, 2025. Reporting directly to CEO Rainer Blair, Dr. Stumpe will lead the company's digital transformation initiatives and AI integration across its global businesses. Dr. Stumpe, who joined Danaher in 2024 as Chief Data and AI Officer, brings significant expertise from his previous roles at Tempus, where he led AI initiatives in precision medicine, and Google, where he founded the Cancer Pathology project. His appointment aims to accelerate scientific discovery, operational efficiency, and clinical impact in life sciences and diagnostics.

Danaher Corporation announced that Jonathan Leiken has been appointed Senior Vice President and General Counsel, and Matthew Gugino, currently Group Chief Financial Officer of the Company's Life Sciences. These leadership appointments demonstrate Danaher's commitment to strengthening its executive team for the next phase of growth.

Blair continued, "Looking ahead, we believe Danaher is better positioned than at any point in our 40-year history. The transformation in our portfolio over the last several years has created a focused life sciences and diagnostics innovator, poised for higher long-term growth, expanded margins and stronger cash flow." This confident outlook from CEO Rainer Blair underscores the company's strategic positioning despite near-term headwinds.

Partnership seeks to improve patient outcomes and experience through novel digital and diagnostic solutions. Investment aligns with Danaher's mission to accelerate the transition to precision. The company's investment partnership with Innovaccer Inc. represents its continued push into digital health and precision medicine.

XIV. Links & Resources

Company Resources: - Danaher Corporation Official Website: www.danaher.com - Investor Relations: investors.danaher.com - Danaher Business System Overview: www.danaher.com/how-we-work/danaher-business-system - Annual Reports & SEC Filings: www.sec.gov/edgar/browse/?CIK=313616

Key Operating Companies: - Cytiva: www.cytiva.com - Beckman Coulter: www.beckmancoulter.com - Pall Corporation: www.pall.com - Cepheid: www.cepheid.com - Leica Microsystems: www.leica-microsystems.com

Spin-off Companies: - Fortive Corporation (FTV): www.fortive.com - Envista Holdings (NVST): www.envistaco.com - Veralto Corporation (VLTO): www.veralto.com

Industry Analysis & Research: - Harvard Business School Case Studies on Danaher - Lean Enterprise Institute Resources on DBS - Industry Reports from Healthcare & Life Sciences Analysts

Books & Articles on Danaher & Lean: - "The Lean Turnaround" by Art Byrne - "The Toyota Way" by Jeffrey Liker - Various Harvard Business Review articles on operational excellence

Financial Data Providers: - Bloomberg Terminal: DHR US Equity - S&P Capital IQ - Morningstar Direct

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube