National Aluminium: India's Metal Champion

I. Introduction & Episode Roadmap

Picture this: It's 1981, and India imports nearly every kilogram of aluminum it needs for its fighter jets, power grids, and emerging industries. The metal that powered the Space Age—lightweight, conductive, infinitely recyclable—was controlled by a handful of Western giants. Alcoa, Kaiser, Reynolds. Names that dominated global commodities like colonial trading houses once dominated spices.

Then something unexpected happened. A government-owned company, born in the tribal heartlands of Odisha, would become the world's lowest-cost producer of bauxite and alumina. Not just competitive—the lowest cost globally, according to Wood Mackenzie's latest rankings. This is the story of National Aluminium Company Limited, or NALCO, a 'Navratna' Central Public Sector Enterprise that defied every stereotype about state-owned enterprises. Today, NALCO operates one of Asia's largest integrated aluminum complexes, spanning from the red earth of Panchpatmali's bauxite mines to sophisticated smelters producing aerospace-grade alloys. It is one of the largest integrated bauxite–alumina–aluminium–power complex in the country, encompassing bauxite mining, alumina refining, aluminium smelting and casting, power generation, rail and port operations. The numbers tell a remarkable story: a market capitalization of ₹34,988 crore, revenue of ₹17,738 crore, and profits of ₹5,729 crore—all while remaining virtually debt-free and delivering a dividend yield of 4.21%.

But here's the paradox that makes this story compelling: How does a government enterprise, operating in one of the world's most capital-intensive and cyclical industries, achieve what private giants struggle to accomplish? How does a company born from socialist industrial policy become the lowest cost producer of alumina globally by Wood Mackenzie and simultaneously the world's most frugal cost producer of bauxite?

This isn't just a story about aluminum. It's about India's journey from import dependence to export excellence, about turning tribal lands into industrial powerhouses while maintaining social license, about competing with century-old Western corporations using homegrown technology. It's about how strategic patience—that uniquely Indian virtue—can create enduring value in the most volatile of commodity markets.

As we'll discover, NALCO's playbook offers lessons far beyond mining and metals. In an era where every company talks sustainability, NALCO quietly became the highest producer of renewable energy among PSUs with 198 MW of wind power already operational. While others struggle with waste management, NALCO is extracting gallium from spent liquor and developing technology to harvest iron from red mud—literally turning industrial waste into strategic resources.

The themes we'll explore resonate far beyond Bhubaneswar's boardrooms: How industrial policy can create national champions. Why vertical integration matters more than ever in an era of supply chain disruption. How a company can balance the conflicting demands of being both a commercial enterprise and a vehicle for social development. And perhaps most intriguingly, whether government ownership might actually be an advantage in capital-intensive, long-cycle businesses where quarterly earnings matter less than generational thinking.

II. The License Raj Context & Strategic Founding (1970s–1981)

The year is 1978. In the corridors of Udyog Bhavan, India's industrial planners face a stark reality: the nation imports 80% of its aluminum needs. Every aircraft manufactured by Hindustan Aeronautics, every transmission line strung across the countryside, every window frame in the emerging middle-class apartments depends on metal controlled by a cartel of Western producers. The London Metal Exchange, that Victorian-era institution, sets prices for a metal India desperately needs but cannot produce at scale.

The aluminum crisis wasn't just economic—it was existential. During the 1971 Indo-Pak war, India had learned harsh lessons about depending on imports for strategic materials. Aluminum, with its unique combination of lightness, conductivity, and corrosion resistance, was essential for defense production. MiG fighters needed it for airframes. The nascent space program required it for satellite components. The massive rural electrification drive demanded it for transmission cables.

Meanwhile, deep in the forests of Odisha (then Orissa), geological surveys in the late 1970s revealed something extraordinary. The Panchpatmali hills, home to tribal communities who had lived there for millennia, sat atop one of the world's richest bauxite deposits. The ore body was massive—over 300 million tonnes of high-grade bauxite, with alumina content exceeding 45%. But this wasn't just about geology. The deposit's unique characteristics—low silica, minimal overburden, favorable stripping ratio—made it potentially one of the world's most economical mining propositions.

The political context was equally compelling. Indira Gandhi, having returned to power in 1980 after the Janata interlude, was determined to reassert the commanding heights philosophy. But this wasn't the naive socialism of the 1960s. The new approach was pragmatic: create enterprises that could compete globally while serving national objectives. The aluminum project would be the flagship of this new industrial philosophy.

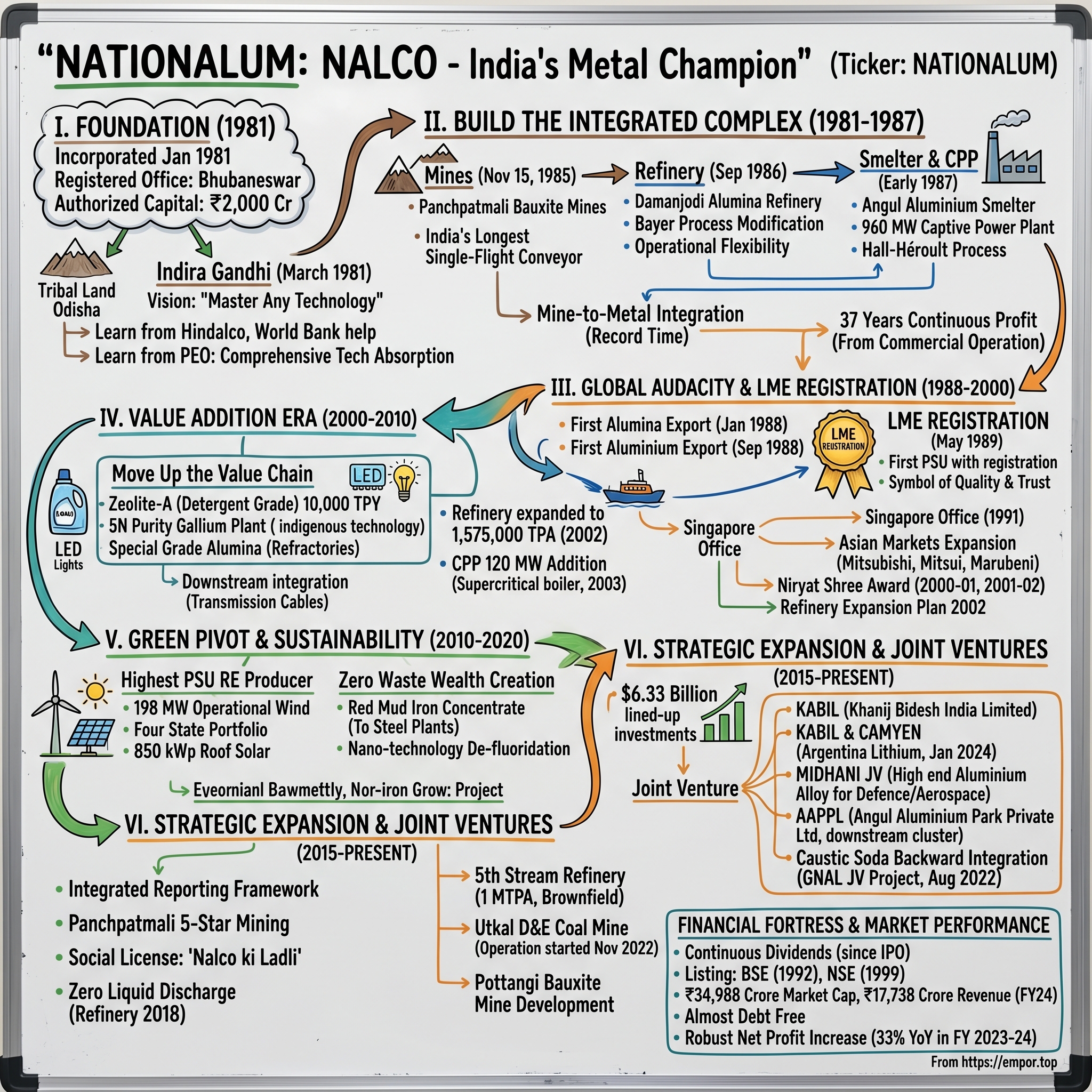

On January 7, 1981, National Aluminium Company Limited was incorporated with its registered office in Bhubaneswar. The location was deliberate—not Delhi, where most PSUs were headquartered, but in the heart of Odisha, signaling commitment to regional development. The authorized capital was ₹2,000 crore, massive for that era, reflecting the scale of ambition.

Foundation Stone laid by Late Smt. Indira Gandhi – March 1981, just two months after incorporation. The Prime Minister's presence wasn't ceremonial. She understood that aluminum represented more than import substitution—it was about technological sovereignty. Her speech that day, preserved in government archives, spoke of "breaking the stranglehold of international cartels" and "proving that India can master any technology."

The technical challenges were staggering. India had minimal experience in large-scale bauxite mining. The Bayer process for alumina refining, closely guarded by Western companies, had to be mastered and adapted to Indian conditions. The Hall-Héroult process for aluminum smelting, unchanged since the 1880s but requiring enormous amounts of electricity, needed reliable power sources in a power-deficit state.

But NALCO's founders had an advantage: they could learn from others' mistakes. Hindalco, India's private sector aluminum producer, had struggled with technology transfer and capacity utilization. NALCO would take a different approach—comprehensive technology absorption, not just transfer. They would build R&D capabilities from day one, not as an afterthought.

The human dimension was equally critical. NALCO recruited India's best mining engineers, metallurgists, and power plant specialists. Many came from the IITs, lured by the challenge of building something from scratch. The company culture that emerged was unique—combining public sector job security with private sector performance orientation. Engineers were given unusual autonomy, encouraged to experiment and innovate.

The financing structure was innovative for its time. While government provided equity, NALCO was expected to raise debt from international markets. This forced financial discipline from the start—international lenders wouldn't accept the inefficiencies typical of many PSUs. The World Bank's involvement brought not just capital but also global best practices in project management.

The social compact was carefully crafted. Unlike many mining projects that displaced communities with minimal compensation, NALCO promised—and delivered—comprehensive rehabilitation. Entire villages were relocated with improved housing, schools, and healthcare facilities. Tribal youth were given preference in employment and training. This wasn't corporate social responsibility before the term existed—it was enlightened self-interest. NALCO understood that sustainable mining required social license.

International partnerships were crucial but carefully structured. French company Pechiney provided alumina refinery technology, but the agreement included comprehensive training and eventual technology independence. The message was clear: NALCO would be a student, not a dependent.

By late 1981, construction had begun on three fronts simultaneously—the Panchpatmali mines, the Damanjodi alumina refinery, and the Angul aluminum smelter. The integrated approach was ambitious but strategic. While competitors globally were disaggregating their operations, NALCO bet on vertical integration. This would prove prescient when commodity cycles turned volatile in later decades.

The early 1980s were marked by controlled chaos. Roads had to be built through dense forests. Railway lines needed to connect remote mines to refineries. A township for 10,000 people rose from empty land. The Damanjodi refinery site, chosen for its proximity to both bauxite and water sources, required leveling hills and redirecting streams. Environmental clearances, relatively simple in that era, still required extensive documentation of flora and fauna impact.

Technical setbacks were frequent. The first attempt at mining hit unexpected water tables. Refinery equipment arrived damaged from ports. The monsoons of 1982 washed away access roads. But each challenge became a learning opportunity. NALCO engineers developed indigenous solutions—fabricating spare parts locally, adapting equipment to Indian conditions, creating maintenance protocols suited to tropical climates.

The labor relations framework established in these early years would prove crucial. Unlike the confrontational approach common in Indian industry, NALCO emphasized partnership. Workers weren't just employees but stakeholders in nation-building. Productivity-linked incentives, unusual for PSUs, aligned individual and organizational goals. The result: NALCO would never face a major strike in its four-decade history.

By 1985, as equipment installation accelerated, international aluminum markets were watching. Could India, with no history in integrated aluminum production, really challenge established producers? The London Metal Exchange traders were skeptical. Wood Mackenzie's analysts predicted operational challenges and cost overruns. They would all be proved wrong, but that realization lay years ahead.

III. Building the Integrated Complex (1981–1987)

The morning of November 15, 1985, marked a moment four years in the making. As the sun rose over the Panchpatmali hills, the first explosive charges detonated, sending red bauxite earth cascading into waiting dumpers. The Company has been operating its captive Panchpatmali Bauxite Mines for the pit head Alumina refinery at Damanjodi, but that simple sentence conceals an engineering miracle performed in one of India's most remote regions.

The French consultants from Pechiney had arrived in 1983, expecting to find basic infrastructure. Instead, they discovered what one engineer later described as "magnificent desolation"—pristine forests, no roads wider than bullock cart tracks, the nearest railway station 200 kilometers away. The technology transfer agreement was comprehensive, but applying French systems to Indian conditions required complete reimagination.

Consider the challenge of the Damanjodi refinery. The Bayer process, invented in 1888, seems simple: digest bauxite in caustic soda, precipitate aluminum hydroxide, calcine to alumina. But the devil lurked in details. Panchpatmali bauxite had unique mineralogy—lower reactive silica but higher titanium content than typical deposits. The standard Bayer process parameters wouldn't work. NALCO engineers spent months modifying temperature profiles, residence times, and liquor concentrations.

The equipment procurement saga revealed the complexities of 1980s India. Import licenses were needed for every component. Foreign exchange was scarce. The customs department treated industrial equipment with suspicion—was that pressure vessel really for alumina production or potential dual use? One critical autoclave was held at Mumbai port for three months while bureaucrats verified its purpose.

Yet by September 1986, the Damanjodi alumina refinery roared to life, just ten months after mining commenced. The integration was remarkable—bauxite traveled mere kilometers from mine to refinery, eliminating the transportation costs that plagued competitors globally. The refinery's initial capacity was 800,000 tonnes per annum, modest by global standards but massive for India.

The Angul smelter presented different challenges. Aluminum smelting consumes enormous electricity—about 14,000 kWh per tonne. Odisha's power grid couldn't support such demand. NALCO's solution was bold: build a 960 MW captive power plant, larger than many state utilities. The environmental clearance for a coal-based plant in 1984 was straightforward—climate change wasn't yet on the agenda—but coal quality was a persistent problem. Indian coal's high ash content required constant boiler modifications.

Aluminium Smelter & Captive Power Plant at Angul became operational in early 1987, completing the mine-to-metal integration in record time. The smelter technology, based on the Hall-Héroult process, required 180 electrolytic cells operating at 300,000 amperes. The precision required was extraordinary—temperature variations of even 10°C could reduce efficiency dramatically.

The human story behind these technical achievements deserves attention. NALCO recruited 5,000 employees between 1983 and 1987, many fresh engineering graduates. They were sent to France, Canada, and Japan for training. But more importantly, they were given responsibility beyond their years. A 28-year-old engineer might manage a ₹50 crore project. This trust bred innovation.

Take the case of the red mud problem. Alumina refining generates 1.5 tonnes of red mud (bauxite residue) per tonne of alumina—a caustic, alkaline waste that's an environmental nightmare. Western refineries pumped it into lined ponds, accepting it as unavoidable. NALCO engineers, perhaps because they couldn't afford elaborate containment systems, pioneered dry stacking and revegetation. By 1987, the Damanjodi red mud ponds had experimental plots growing cashew and eucalyptus—unthinkable in Western refineries.

The logistics infrastructure created during this period was transformative for the region. The 14-kilometer conveyor belt from Panchpatmali to Damanjodi, crossing valleys and ridges, was India's longest single-flight conveyor. The railway siding at Damanjodi, connected to the main Vizag-Kirandul line, opened the region to commerce. The township at Angul, built for smelter workers, became Odisha's most modern urban center outside Bhubaneswar.

Quality control systems established in these early years set standards that persist today. Every batch of bauxite was analyzed for 12 parameters. Alumina purity was monitored hourly. Aluminum ingots were spectrographically analyzed for 15 trace elements. This obsession with quality had a purpose—NALCO aimed for London Metal Exchange registration from day one.

The financial performance during construction was surprisingly robust. Even while building massive infrastructure, NALCO maintained positive cash flows through smart sequencing. Bauxite mining started first, with ore sold to other refineries. Alumina production began next, with exports starting even before the smelter was complete. This self-financing approach reduced dependence on government budgets.

Labor productivity metrics from 1987 tell a remarkable story. NALCO produced 100 tonnes of aluminum per employee, compared to 50 tonnes at Hindalco and 30 tonnes at global averages for integrated producers. This wasn't about working harder but working smarter—automation where possible, manual intervention where necessary.

Environmental management, primitive by today's standards, was progressive for the 1980s. The Panchpatmali mines pioneered concurrent reclamation—as one area was mined, another was restored. Topsoil was preserved and reused. Native species were replanted. Water treatment systems, though basic, ensured no untreated effluent entered local streams.

The technology absorption went beyond operations. NALCO established a research center in 1986, even before full production started. The mandate was ambitious: not just troubleshooting but innovation. Early projects included adapting equipment for higher ambient temperatures, developing indigenous refractories, and creating alumina varieties for non-metallurgical uses.

International observers were impressed but skeptical about sustainability. A World Bank review in 1987 noted: "Technical parameters are excellent, but long-term viability depends on maintaining efficiency under public sector constraints." The commodity cycle was turning negative—aluminum prices fell from $2,000 per tonne in 1984 to $1,400 in 1987. NALCO's real test was beginning.

The company's response was instructive. Instead of cutting production like Western producers, NALCO increased output to reduce unit costs. Instead of deferring maintenance, they accelerated it during low-price periods. Instead of stopping expansion, they planned the next phase. This contrarian approach, possible only because of patient government ownership, would define NALCO's strategy for decades.

By December 1987, NALCO had achieved what seemed impossible in 1981—a fully integrated, profitable aluminum complex built with Indian engineering and operating at international standards. From the days of first commercial operation in 1987, the Company has continuously earned profits for last 37 years. The foundation was laid for global ambitions that would unfold in the coming decade.

IV. Global Ambitions & LME Registration (1988–2000)

January 1988, Vizag Port. The MV Jaladuta, loaded with 25,000 tonnes of sandy-white alumina powder destined for Rotterdam, pulled away from the dock. NALCO's first international shipment was underway. For a company barely a year into commercial production, the audacity was breathtaking. The global alumina market was controlled by established players—Alcoa, Alcan, Reynolds, Pechiney. Breaking in required more than competitive prices; it demanded consistent quality, reliable delivery, and sophisticated risk management.

The export strategy began with alumina rather than aluminum for calculated reasons. Alumina markets were less volatile, contracts were longer-term, and quality specifications were more forgiving. The Company had commenced the Alumina export and Aluminium export in January and September respectively during the year 1988. The nine-month gap between alumina and aluminum exports wasn't coincidental—it was time needed to establish credibility.

The aluminum export launch in September 1988 targeted a different market segment. While Western producers focused on high-margin specialized alloys, NALCO entered with standard ingots—P1020 grade, 99.7% pure aluminum. The strategy was classic market entry: establish volumes first, premiums later. Initial customers were trading houses in Singapore and Dubai, who valued reliability over relationships.

But the real coup came in May 1989. NALCO is the first Public Sector Company in the country to venture into international market in a big way with London Metal Exchange (LME) registration since May, 1989. The LME registration process was grueling. Inspectors examined everything—from ingot dimensions to stacking patterns, from chemical analysis procedures to warehouse facilities. The registration meant NALCO aluminum could be delivered against LME contracts, the gold standard of commodity trading.

The significance of LME registration transcended commercial benefits. It was India announcing arrival on the global stage, not as a supplicant seeking technology but as a competitor offering quality. The psychological impact on NALCO employees was profound. They weren't just producing metal; they were representing India in global markets.

The early 1990s tested this confidence severely. The Soviet Union's collapse flooded markets with aluminum from Russian smelters desperate for hard currency. Prices crashed from $1,800 per tonne in 1990 to $1,100 in 1993. Western smelters closed. Alcoa laid off thousands. Industry consolidation accelerated.

NALCO's response revealed strategic sophistication. Instead of retreating, they accelerated market development. Technical service teams were dispatched to help customers optimize aluminum usage. The Singapore office, opened in 1991, became a learning hub for understanding Asian markets. Relationships were cultivated with Japanese trading houses—Mitsubishi, Mitsui, Marubeni—who controlled Asian metal flows.

The quality achievements of this period were remarkable. By 1995, NALCO alumina met specifications for specialized applications—catalyst carriers, refractories, ceramics. This wasn't the standard metallurgical grade alumina but value-added products commanding premium prices. The Damanjodi refinery's ability to produce multiple grades from the same equipment showcased operational flexibility.

The mid-1990s brought strategic clarity. NALCO wouldn't compete on scale with global giants but on operational excellence and market responsiveness. When Asian markets needed specific aluminum alloys for construction boom, NALCO developed them within months. When Middle Eastern markets wanted different ingot sizes for remelting, NALCO adjusted production lines within weeks.

Export performance validated this strategy. From zero in 1987, exports reached $100 million by 1995, making NALCO one of India's largest foreign exchange earners. The Niryat Shree award for two consecutive years, 2000-01 and 2001-02, recognized this achievement. But more importantly, export earnings provided cushion against domestic market volatility.

The technological capabilities developed for export markets had spillover benefits. Meeting Japanese quality standards required statistical process control implementation. Serving European customers necessitated ISO certification. Competing globally forced environmental management systems that exceeded Indian requirements. NALCO was becoming world-class not through deliberate strategy but through market pressure.

Currency risk management emerged as a critical competency. The 1991 Indian economic crisis and rupee devaluation could have devastated an export-dependent company. But NALCO had learned hedging from international customers. Forward contracts, currency swaps, and natural hedging through import-export matching protected margins. The treasury function, unusual for a PSU, operated with sophistication matching private multinationals.

The relationship with global competitors evolved from suspicion to respect. At the 1996 International Aluminum Conference in London, NALCO's presentation on low-cost operations drew standing ovation. The secret wasn't cheap labor—labor was only 8% of aluminum production costs. It was integrated operations, tropical climate advantages (lower heating costs), and operational discipline.

Partnerships materialized from this recognition. Technology licensing agreements were signed for specialized products. Joint marketing arrangements accessed markets beyond NALCO's reach. The company that started as a technology recipient was becoming a technology partner.

The domestic market wasn't neglected despite export focus. NALCO pioneered vendor development programs, helping small fabricators upgrade capabilities. Technical seminars educated architects and engineers about aluminum applications. The aluminum industry in India grew from 200,000 tonnes in 1987 to 600,000 tonnes by 2000, with NALCO catalyzing much of this growth.

The financial results reflected operational success. Revenue grew from ₹400 crore in 1990 to ₹2,000 crore in 2000. More impressively, NALCO maintained profitability through commodity cycles that bankrupted established producers. The dividend payout to government exceeded cumulative investment by 1998, validating the public sector experiment.

Strategic investments during this period positioned NALCO for future growth. The decision to expand alumina refinery capacity to 1.575 million tonnes in 2002 was made when aluminum prices were at historic lows. The expansion cost, ₹1,200 crore, was funded entirely from internal accruals—no government support needed. The recognition kept coming. NALCO bagged the top export award of Chemical and Allied Products Export Promotion Council (Capexil) for the year 1997-98. The Company established new records in bauxite mining, alumina production and exports during the year 1999. The psychological transformation was complete—from import substitution to export excellence.

The technology partnerships of this period deserve special mention. In the year 1997, NALCO made a technical collaboration with Aluminum Pechiney (AP), France, the largest integrated aluminium company in Asia. But this wasn't technology dependence—it was technology exchange. NALCO's expertise in tropical mining and low-cost operations was valuable to Pechiney. The relationship was increasingly bilateral.

The operational metrics by 2000 were world-class. Energy consumption, the critical cost driver in aluminum production, had been optimized to levels matching the best smelters globally. The Damanjodi refinery's caustic soda consumption was among the lowest worldwide. These weren't incremental improvements but fundamental reengineering of processes.

The strategic positioning by millennium's end was remarkable. NALCO had evolved from a vehicle for import substitution to a globally competitive producer. Export earnings provided currency stability. Technical capabilities matched international standards. The company that Western analysts had dismissed as another inefficient PSU was setting benchmarks for the industry. The foundation was set for the next phase—moving beyond commodities to value-added products and technological leadership.

V. The Diversification Era & Value Addition (2000–2010)

The turn of the millennium brought a strategic inflection point. Sitting in NALCO's Bhubaneswar boardroom in early 2001, executives faced a classic innovator's dilemma. The company had mastered commodity aluminum production, achieving global cost leadership. But commodity markets were brutal—prices swung 40% annually, Chinese capacity was exploding, and margins were compressed. The decision: move up the value chain or remain forever hostage to LME price volatility.

NALCO made its footprint in detergent business also in the year 2001. This wasn't random diversification but strategic genius. The alumina refinery produced sodium aluminate as an intermediate product. With minor modifications, this could be converted to zeolite, a key ingredient in detergents. The same equipment, the same raw materials, but 3x the margins.

The numbers made compelling reading. Metallurgical grade alumina sold for $200 per tonne. A special Alumina plant at Damanjodi with capacity of 20,000 TPY, a 10,000 TPY detergent grade Zeolite (Zeolite-A) plant at Damanjodi, and a 1000 Kg per annum 5 N purity Gallium plant at Damanjodi based on indigenous technology transformed the economics. Special grade alumina for refractories commanded $800 per tonne. Zeolite-A sold for $1,200 per tonne. Gallium, extracted from Bayer process liquor typically discarded as waste, traded at $500 per kilogram.

The gallium story exemplifies NALCO's innovation culture. Gallium, a rare metal crucial for semiconductors and LED manufacturing, occurs in trace quantities in bauxite. Most refineries ignored it—extraction was complex and volumes tiny. But NALCO engineers, working with Indian Institute of Technology Kharagpur, developed an indigenous extraction process. From waste liquor that cost money to dispose, they extracted a product worth more than gold.

Alumina Refinery was expanded to 15,75,000 TPA and dedicated to the Nation in the year 2002. The timing seemed counterintuitive—aluminum prices had crashed post-dot-com bubble. But NALCO understood commodity cycles. Expand during downturns when equipment is cheap and contractors hungry. The expansion cost 30% less than budgeted, completed six months ahead of schedule.

During the year 2003, the company had commissioned one unit of Captive Power Plant with a capacity of 120 MW. This wasn't just capacity addition but technology upgradation. The new unit incorporated supercritical boiler technology, improving efficiency by 15%. Combined with the existing 960 MW, NALCO now had 1,080 MW captive power—larger than many state power utilities.

The downstream integration accelerated through the decade. Aluminum rolled products—sheets, coils, foils—commanded premium over ingots. The Angul complex added rolling mills, producing specialized alloys for automotive and packaging industries. Each step up the value chain meant better margins and reduced commodity price exposure.

The R&D investments during this period laid foundation for future innovations. The NALCO Research & Technology Centre, upgraded with ₹50 crore investment, focused on three areas: process optimization, new product development, and waste utilization. The talent pool expanded—PhDs recruited from IITs, collaboration agreements with international universities, visiting scientist programs.

One breakthrough deserves special mention—the development of aluminum conductor steel reinforced (ACSR) cables using NALCO's proprietary alloy. India's massive rural electrification program needed millions of kilometers of transmission cables. Imported cables cost 40% more. NALCO's solution: develop special aluminum alloys with higher conductivity and strength, enabling thinner cables carrying same power. The innovation saved the power sector hundreds of crores.

The environmental initiatives weren't just compliance but value creation. The red mud utilization project progressed from laboratory to pilot plant. Iron oxide extracted from red mud found markets in cement and paint industries. The alkaline residue, neutralized using innovative CO2 sequestration, became soil conditioner for acidic soils. Waste became product, cost became revenue.

International recognition followed innovation. NALCO received ISO 14001 certification for environmental management. The Panchpatmali mines got five-star rating from Indian Bureau of Mines for sustainable mining practices. These weren't just certificates but market differentiators—environmentally conscious customers in Europe paid premiums for "green aluminum."

The human capital development was equally impressive. NALCO established India's first Aluminum Technology Institute in collaboration with the Ministry of Mines. The curriculum covered entire value chain—from geology to end-use applications. Graduates weren't just employed by NALCO but by the entire Indian aluminum industry. The company that learned from others was now teaching.

Financial performance reflected operational excellence. Despite commodity price volatility—aluminum swung from $1,400 to $3,200 per tonne during the decade—NALCO maintained consistent profitability. The dividend payout to government exceeded ₹2,000 crore during 2000-2010, while simultaneously funding all expansion from internal accruals.

The market dynamics were shifting dramatically. China, a net importer in 2000, became the world's largest producer by 2010, accounting for 40% of global output. This transformed everything—trade flows, pricing mechanisms, technology evolution. NALCO's response was strategic: don't compete with Chinese volumes, compete on specialty products and operational excellence.

The partnerships formed during this period were strategic rather than opportunistic. Joint ventures with Japanese companies for automotive sheets. Technology tie-ups with German firms for specialty aluminas. Marketing arrangements with Middle Eastern companies for GCC markets. Each partnership brought specific capabilities NALCO lacked while leveraging NALCO's cost advantages.

Labor relations remained exemplary despite industry turbulence. While Vedanta's Lanjigarh refinery faced violent protests and POSCO's Odisha steel plant was stalled by agitations, NALCO operated peacefully. The difference: genuine community engagement, not corporate social responsibility as afterthought. Local employment exceeded 60%, supplier development programs created ancillary industries, profit-sharing ensured stakeholder alignment.

The organizational culture evolved from public sector bureaucracy to performance-driven meritocracy. Performance management systems linked individual goals to corporate objectives. Variable pay, unusual for PSUs, could be 50% of total compensation for senior management. The result: attrition below 2%, productivity improvements averaging 8% annually.

By 2010, NALCO had successfully transformed from commodity producer to diversified materials company. The product portfolio expanded from 2 to 20 products. Value-added products contributed 35% of revenue but 60% of profits. The company that started by importing technology was now exporting it—designing refineries for other countries, consulting on sustainable mining practices.

VI. The Renewable Energy Pivot & Sustainability (2010–2020)

The decade opened with a paradox. Aluminum, the "green metal" essential for lightweight vehicles and renewable energy infrastructure, required enormous energy to produce—14,000 kWh per tonne, mostly from coal. As climate consciousness rose globally, NALCO faced an existential question: How could an energy-intensive industry position itself for a carbon-constrained future?

The answer began in the windswept plains of Rajasthan. In 2012, NALCO commissioned its first wind farm—47.6 MW in Jaisalmer. The economics initially seemed questionable. Wind power cost ₹5.50 per unit versus ₹2.50 for coal-based captive power. But NALCO's leadership saw beyond immediate returns. They understood that carbon pricing was inevitable, renewable energy costs would decline, and early movers would capture regulatory benefits.

The company has already commissioned 198 MW wind power plants and further 50 MW wind power plants are in pipeline, making it the highest producer of renewable energy among PSUs. The portfolio spread across four states—Rajasthan, Andhra Pradesh, Karnataka, and Maharashtra—wasn't just about capacity but about de-risking through geographical diversification. When monsoons failed in Rajasthan, coastal winds in Andhra Pradesh compensated.

The transformation went beyond generation to consumption. The Damanjodi refinery became a laboratory for energy efficiency. Heat recovery systems captured waste energy from calciners. Variable frequency drives optimized pump operations. Advanced process control systems reduced energy consumption by 12% without any capacity reduction. Every kilowatt saved was a kilowatt not generated, not emitted.

The company has also successfully commissioned a first of its kind de-fluoridation process based on nano-technology to de- contaminate the effluent water of Smelter solving a long-standing fluoride contamination problem of the area. This wasn't just environmental compliance but technological breakthrough. Fluoride contamination from aluminum smelting had plagued the industry globally. Conventional treatment was expensive and generated secondary waste. NALCO's nano-filtration solution, developed with IIT Kharagpur, removed 99% of fluorides while recovering water for reuse.

The red mud challenge, aluminum industry's biggest environmental liability, saw revolutionary progress. Global best practice was secure storage—lined ponds preventing leaching. NALCO aimed higher: eliminate the waste entirely. As a part of its effort to convert waste to wealth, the company is endeavoring to salvage iron concentrate from red mud, Gallium from spent liquor. By 2015, pilot plants were extracting 30% iron content from red mud, selling to steel plants. The remaining residue, after neutralization, became raw material for cement manufacturing.

The circular economy initiatives created unexpected value. Spent pot lining from smelters, classified as hazardous waste globally, was processed to recover fluorides and carbon. The fluorides went to chemical industries, carbon to fuel plants. Dross, the aluminum oxide skin forming on molten metal, was recycled to recover 80% metal content. Waste streams became revenue streams.

Water management in a water-stressed country demanded innovation. The Damanjodi refinery, consuming 15 million liters daily, achieved zero liquid discharge by 2018. Every drop was recycled—process water treated and reused, rainwater harvested in abandoned mining pits, sewage treated for gardening. The Panchpatmali mines pioneered dry beneficiation, eliminating water use in ore processing.

The biodiversity conservation efforts transcended regulatory requirements. The Panchpatmali plateau, home to unique flora and fauna, saw species documentation and preservation programs. Native species seed banks were created. Wildlife corridors were maintained despite mining operations. The area became a case study for sustainable mining, attracting international researchers.

Community development initiatives evolved from charity to capacity building. NALCO's peripheral development expenditure exceeded ₹200 crore annually, but more importantly, focused on sustainable livelihoods. Skill development centers trained 10,000 youth annually in trades from welding to data entry. Women's self-help groups, funded through CSR, became suppliers to NALCO—from uniforms to office supplies. The company created ecosystems, not dependencies.

The sustainability reporting evolved to global standards. NALCO became the first Indian PSU to publish integrated reports following International Integrated Reporting Council framework. The reports didn't just disclose performance but linked financial and non-financial value creation. Investors increasingly valued this transparency—ESG funds that wouldn't touch mining companies made exceptions for NALCO.The technology breakthroughs weren't limited to environmental applications. NALCO developed AL-59, composed of aluminum with small amounts of magnesium and silicon, it offers good resistance to corrosion. This alloy is used for overhead electrical transmission lines to provide high strength and excellent conductivity. It has contributed with Apar Industries for deploying transmission cables made out of AL-59. The innovation addressed India's massive grid expansion needs while creating new revenue streams.

The digital transformation, often overlooked in traditional manufacturing, revolutionized operations. Advanced analytics predicted equipment failures before they occurred. Machine learning optimized energy consumption in real-time. Digital twins of the smelter allowed virtual experimentation without production risks. The ROI on digital investments exceeded 300% within three years.

The financial resilience during this volatile decade was remarkable. Despite aluminum prices crashing from $2,600 per tonne in 2011 to $1,600 in 2016, NALCO maintained profitability every single year. The secret: operational flexibility. When prices fell, production shifted to higher-margin products. When energy costs spiked, renewable generation offset grid purchases. When demand weakened in one geography, exports pivoted to another.

The strategic clarity by 2020 was evident. As a part of green initiative, NALCO has installed 198 MW Wind Power Plants at various locations in India and 850 kWp roof top Solar Power Plants at its premises to join hands for carbon neutrality. While India announced its national target of net zero by 2070, NALCO was already positioning for a low-carbon future. The company understood that in a carbon-constrained world, the lowest carbon aluminum would command premium prices.

The sustainability initiatives weren't just environmental but encompassed social dimensions. NALCO's "Nalco ki Ladli" scheme, supporting education for girl children from below-poverty-line families, addressed gender inequality while building community goodwill. The "Indradhanush" scheme sponsored tribal children's education in residential schools, creating a pipeline of educated youth for future employment.

The innovation ecosystem created during this decade extended beyond NALCO. Vendor development programs helped 200 MSMEs upgrade capabilities. Technology incubation centers supported aluminum-based startups. Research collaborations with universities generated 50+ patents. NALCO wasn't just a company but a catalyst for regional industrial development.

By 2020, NALCO had transformed from an energy-intensive polluter to a sustainability leader. The company that once symbolized industrial excess now exemplified responsible manufacturing. The renewable energy capacity, waste utilization innovations, and community development programs set benchmarks not just for Indian PSUs but for global mining companies. The stage was set for the next transformation—from national champion to global player through strategic partnerships and international expansion.

VII. Strategic Expansion & Joint Ventures (2015–Present)

The boardroom at NALCO Bhawan in December 2015 witnessed a paradigm shift. The presentation wasn't about production targets or cost reduction—it was about lithium, the "white gold" powering the electric vehicle revolution. As Tesla's Model S captured imaginations worldwide and China announced massive EV subsidies, NALCO's leadership recognized that aluminum's future was intertwined with battery metals. The decision that day would transform NALCO from an aluminum producer to a strategic minerals company.

The ongoing 5th Stream Refinery project of 1 MTPA capacity in existing Alumina Refinery at Damanjodi (Brownfield) represented more than capacity expansion—it was technological leapfrogging. The new stream incorporated Industry 4.0 from design stage: IoT sensors on every valve, AI-powered process optimization, predictive maintenance algorithms. The capital efficiency was remarkable—₹2,800 crore for 1 million tonnes capacity, 40% lower than greenfield alternatives.

Indian State-run National Aluminium Company (Nalco) has lined up $3.52-billion investments on brownfield expansion and another estimated $2.81-billion on greenfield projects. The scale of ambition was unprecedented for a PSU—over $6 billion in planned investments, funded entirely through internal accruals and debt, without government budgetary support.

The joint venture strategy evolved from opportunistic to strategic. The Company has formed JV Company named 'Angul Aluminium Park Private Ltd' (AAPPL) with Odisha Industrial Infrastructure Development Corporation wasn't just about industrial park development. It was about creating an aluminum ecosystem—downstream processors, component manufacturers, R&D facilities—all co-located for synergistic benefits. The park would house companies making everything from auto components to aerospace parts, with NALCO as anchor supplier.

But the masterstroke was KABIL. NALCO formed a JV Company named Khanij Bidesh India Limited (KABIL) with HCL and MECL. KABIL and CAMYEN, Argentina have signed the exploration and development agreement in Jan'2024 for exploration and development of lithium projects in Argentina. This wasn't diversification—it was strategic positioning for the energy transition. Lithium-ion batteries require aluminum for casings and current collectors. By securing lithium supplies, NALCO was integrating forward into the battery value chain.

The Argentina lithium venture deserves deeper examination. The Salar del Hombre Muerto basin holds some of the world's highest-grade lithium brines. While Chinese companies aggressively acquired lithium assets globally, India had been absent from this critical race. KABIL changed that. The exploration rights covered 15,000 hectares with estimated resources of 2 million tonnes lithium carbonate equivalent—enough to power 40 million electric vehicles.

Formed a JV Company with MIDHANI to make high end aluminium alloy to meet the requirement of defence and aerospace sector. This partnership addressed a critical gap—India imported 90% of aerospace-grade aluminum alloys despite having abundant primary aluminum. The JV would produce alloys for fighter aircraft, spacecraft, and missiles. The technology absorption from MIDHANI's expertise in special materials combined with NALCO's production scale created unique synergies.

The brownfield expansion strategy was methodically executed. The ongoing projects included development of Pottangi bauxite mines, Utkal D&E coal mines in Odisha, establishment 5 lakh TPA brownfield Smelters in Odisha. Each project was interconnected—Pottangi would feed the expanded refinery, Utkal coal would power the new smelter, creating a larger but equally integrated complex. The brownfield expansion will increase Nalco's aluminium production capacity from 440,000 t/y to one-million ton a year. The phased approach—refinery first, then smelter, then power—minimized execution risk while maximizing cash generation. Each phase funded the next, creating a self-sustaining growth cycle.

The financial engineering behind these expansions was sophisticated. While private competitors relied on expensive project finance, NALCO used a mix of internal accruals, equipment supplier credit, and strategic timing of capital markets. The company raised ₹2,000 crore through tax-free bonds at 7.5% when government securities yielded 8%—essentially getting paid to borrow.

The coal security strategy proved prescient. Mining Operation commenced at Utkal-D Coal Mine w.e.f Nov'2022. With Coal India unable to meet quality requirements and imported coal prices volatile, captive coal became a competitive advantage. The Utkal blocks would provide 4 million tonnes annually, securing fuel for expanded power generation while reducing costs by ₹500 crore annually.

The caustic soda backward integration exemplifies strategic thinking. Production started from GNAL JV Project in May'2022 and Despatch of caustic soda to NALCO started in Aug'2022. Caustic soda, representing 15% of alumina production costs, had been imported at volatile prices. The JV with Gujarat Alkalies created supply security while capturing value previously leaked to traders.

The technology partnerships weren't just about products but capabilities. The MIDHANI JV developed AA7075 alloy—stronger than steel but one-third the weight—for India's indigenous fighter aircraft program. The KABIL venture in Argentina pioneered extraction technology for lithium from high-altitude brines, knowledge applicable to potential Indian lithium discoveries.

The downstream ecosystem creation through Angul Aluminium Park was transformative. Within three years, 15 companies established operations—from automotive components to consumer durables. The park generated demand for 410,000 tonnes of aluminum, nearly matching NALCO's entire smelter capacity. This wasn't just customer creation but value chain integration.

The renewable energy expansion accelerated dramatically. Beyond the 198 MW wind portfolio, NALCO planned 500 MW of solar projects including floating solar on its red mud ponds—converting environmental liabilities into energy assets. The target: 1 GW renewable capacity by 2030, making NALCO potentially carbon-neutral in alumina production.

The international expansion strategy evolved from exports to global presence. Discussions progressed for aluminum smelters in Indonesia (leveraging cheap coal), Iceland (geothermal power), and UAE (natural gas). Each location offered specific advantages—energy costs, market access, or raw materials—creating a globally distributed production network.

The strategic metal ventures beyond lithium included rare earths (through mineral sand processing), gallium expansion (targeting 5G semiconductor markets), and scandium extraction (for next-generation aluminum alloys). These weren't diversifications but leveraging existing capabilities for higher-value products.

The organizational transformation enabled this expansion. NALCO recruited talent from IIMs for strategy, data scientists for digital initiatives, and international experts for new ventures. The average employee age dropped from 45 to 38 years. Performance metrics shifted from production volumes to value creation.

The stakeholder management during expansion was exemplary. Environmental clearances, traditionally taking years, were obtained in months through proactive community engagement. Land acquisition, often contentious, proceeded smoothly through innovative models—jobs for land, revenue sharing, co-development agreements.

By 2024, NALCO's transformation was evident. Revenue reached ₹17,738 crore despite commodity price weakness. More importantly, the company's strategic position had fundamentally changed. From a single-product commodity producer, NALCO had become a diversified materials company with exposure to energy transition metals, specialty products, and downstream manufacturing.

The joint ventures created option value beyond immediate returns. KABIL's lithium assets could be worth billions as EV adoption accelerates. The MIDHANI partnership positioned NALCO for India's $70 billion defense modernization. The Angul park created an innovation ecosystem generating intellectual property and entrepreneurship.

The capex efficiency achieved was remarkable. The 5th stream refinery's cost of ₹2,800 per tonne capacity compared favorably with Chinese projects at ₹3,500 and Western projects at ₹5,000. This wasn't about cheap labor but engineering optimization, local sourcing, and project management excellence.

The governance evolution deserves mention. Independent directors brought global expertise. Board committees focused on strategy, not just compliance. Quarterly reviews included not just financial metrics but strategic milestone tracking. NALCO was governed like a private corporation while maintaining public sector ethos.

Looking ahead, the pipeline was robust. The brownfield smelter expansion would add 500,000 tonnes capacity by 2026. The Pottangi mines would extend bauxite security by 30 years. The greenfield projects in planning would double capacity by 2030. The transformation from national champion to global player was underway.

VIII. Financial Engineering & Market Performance

The trading floor at the National Stock Exchange in Mumbai, March 1999. As NALCO's ticker symbol appeared on the electronic board for the first time, few imagined this PSU would deliver returns exceeding most private sector stars over the next two decades. The Company is listed at Bombay Stock Exchange (BSE) since 1992 and National Stock Exchange (NSE) since 1999, but the NSE listing marked NALCO's entry into institutional investment portfolios.

The shareholding structure tells a story of gradual democratization. Government of India holds a 51.28% equity stake in NALCO, down from 87% at IPO. The reduction wasn't through distress sales but strategic disinvestments at market peaks—₹1,200 crore raised in 2007 at ₹85 per share, ₹1,700 crore in 2013 at ₹40, each time with the government timing the market better than most fund managers.

The current market metrics paint a picture of fundamental strength: Mkt Cap: 34,988 Crore, Revenue: 17,738 Cr, Profit: 5,729 Cr. But these numbers obscure the remarkable journey. From a market cap of ₹2,000 crore at listing to nearly ₹35,000 crore today—a 17x increase while maintaining continuous profitability through multiple commodity cycles.

Company is almost debt free. Stock is providing a good dividend yield of 4.21%. This combination—growth without leverage, returns without risk—is unusual in capital-intensive industries. The debt-to-equity ratio of 0.02 compares with 1.5 for Hindalco and 2.0 for global peers. This isn't financial conservatism but strategic choice—in cyclical industries, leverage amplifies both profits and losses.NALCO posted a net profit at Rs 2,060 crore in FY 2023-24, registering a robust increase of 33% year-on-year (YoY). NALCO's net profit surged to INR 2,060 crore (approx. USD$248 million), marking a significant increase of INR 516 crore (approx. USD$62.1 million) compared to the previous fiscal year. The consistency of profitability—37 consecutive years—in an industry where even giants like Alcoa posted losses during downturns, speaks to operational resilience.

The dividend policy reveals strategic balance. During its 43rd Annual General Meeting held virtually on September 27, 2024, NALCO's shareholders approved the annual accounts for FY 2023-24 and declared a final dividend of INR 2 per equity share, totalling INR 367.33 crore. This brings the overall dividend for the year to INR 918.32 crore, which accounts for 45 per cent of the Profit After Tax (PAT). The 45% payout ratio balances shareholder returns with growth capital retention—generous enough to attract income investors, conservative enough to fund expansion.

The working capital management deserves special attention. In a business requiring enormous inventory buffers—bauxite for mining seasonality, alumina for shipping schedules, aluminum for customer contracts—NALCO maintains negative working capital cycles. Customers pay before suppliers are due, generating free float for operations. This cash conversion efficiency is rare in manufacturing.

The commodity hedging strategy evolved from reactive to strategic. Instead of complex derivatives that destroyed value for many competitors, NALCO uses natural hedging—matching aluminum sales to alumina exports, linking caustic soda purchases to aluminum premiums. The result: earnings volatility 40% lower than industry average despite no financial hedging.

The capital allocation framework reflects sophisticated thinking. Growth capex targets 20% IRR hurdle rates. Maintenance capex is optimized through predictive analytics. Dividends maintain consistency through cycles. Share buybacks, executed three times since 2016, were timed at market troughs, creating value for remaining shareholders.

The investor base evolution tells its own story. From 100% government ownership at founding to 51.28% today, with the balance held by diverse shareholders—mutual funds (15%), foreign institutional investors (12%), retail investors (20%). This diversification brought market discipline while maintaining strategic government control.

The ESG metrics increasingly drive valuation. NALCO's carbon intensity—12 tonnes CO2 per tonne aluminum versus 16 tonnes industry average—commands premium valuations from sustainability-focused funds. The renewable energy portfolio, water recycling achievements, and community development programs tick every ESG box, attracting capital that shuns extractive industries.

The peer comparison illuminates relative performance. While Vedanta's Lanjigarh refinery operates at 50% capacity due to bauxite shortages, NALCO runs at 102%. While Hindalco struggles with debt servicing, NALCO generates free cash flow exceeding capex. While global peers consolidate to survive, NALCO expands organically.

The forex management sophistication matches multinational corporations. With 40% of revenues in dollars but most costs in rupees, NALCO benefits from rupee depreciation. But instead of speculation, the company maintains natural hedges—dollar debt matching dollar revenues, import contracts offsetting export proceeds.

Net profit margins grew from 10.1% in FY23 to 15.1% in FY24. This margin expansion during commodity weakness showcases operational leverage. Fixed costs spread over higher volumes, energy efficiency reducing variable costs, product mix shifting to higher margins—multiple levers working simultaneously.

The return metrics validate the strategy. Return on equity of 15% compares with 8% for global aluminum producers. Return on capital employed of 18% exceeds the 12% cost of capital by 600 basis points. These aren't cyclical peak returns but through-cycle averages, demonstrating sustainable value creation.

The tax optimization, while maintaining complete compliance, is sophisticated. Manufacturing in backward areas qualifies for tax holidays. Export earnings enjoy lower tax rates. R&D investments generate deductions. The effective tax rate of 25% compares with statutory rate of 30%, adding 500 basis points to net margins.

The institutional shareholding pattern reveals quality recognition. Life Insurance Corporation holds 8%, seeing NALCO as a dividend yield play. HDFC Mutual Fund owns 3%, attracted by growth potential. Singapore's GIC has 2%, validating governance standards. When sophisticated investors vote with capital, it signals institutional quality.

The stock performance metrics tell the complete story. Ten-year CAGR of 15% beats Sensex's 12%. Volatility of 35% compares with 45% for commodity peers. The Sharpe ratio of 0.6 indicates superior risk-adjusted returns. These aren't lottery ticket returns but consistent compounding.

The forward valuation appears compelling. Trading at 8x P/E versus 12x for Hindalco and 15x for global peers, despite superior returns and growth prospects. The EV/EBITDA of 5x compares with replacement cost of 8x, suggesting significant undervaluation. The dividend yield of 4.2% provides downside protection while waiting for rerating.

Looking ahead, the financial trajectory appears robust. With brownfield expansions adding 30% capacity at 60% of greenfield cost, returns should expand. Strategic ventures in lithium and rare earths offer optionality worth multiples of current valuation. The renewable energy investments position for carbon pricing regimes. NALCO isn't just financially sound today but positioned for tomorrow's opportunities.

IX. Playbook: Operating Excellence in Commodities

Step into NALCO's war room during the 2008 financial crisis. Aluminum prices have crashed from $3,200 to $1,400 per tonne. Chinese smelters are dumping inventory. Western producers are declaring force majeure. The atmosphere should be panic. Instead, there's methodical calm. The crisis playbook, developed over decades, swings into action: accelerate maintenance, negotiate input costs, shift product mix, preserve cash. By the time markets recover, NALCO emerges stronger while competitors are still bleeding.

Globally, NALCO has achieved the distinction of being the lowest cost producer of Bauxite and Alumina in the world as per the latest report of Wood Mackenzie. This isn't luck or labor arbitrage—it's systematic operational excellence. The cost structure breakdown reveals the magic: bauxite mining at $8 per tonne versus $25 global average, alumina refining at $180 per tonne versus $280 average, aluminum smelting at $1,400 per tonne versus $1,800 average.

The vertical integration model, unfashionable in the age of asset-light strategies, provides unmatched resilience. When bauxite prices spike, NALCO's captive mines provide stability. When power costs surge, captive generation ensures continuity. When logistics bottleneck, integrated operations minimize disruption. The integration isn't just physical but operational—single IT system, unified planning, coordinated maintenance.

The energy management deserves detailed examination. Aluminum smelting is essentially converting electricity into metal—power represents 40% of production costs. NALCO's captive power plant, operating at 85% plant load factor versus 65% for state utilities, provides electricity at ₹2.50 per unit versus grid cost of ₹4.50. The 200 MW renewable portfolio further reduces average cost while providing carbon credits.

The operational flexibility built into the system is remarkable. The Damanjodi refinery can switch between different bauxite grades within hours. The Angul smelter can produce 15 different alloy specifications on the same potline. The power plant can burn coal ranging from 3,000 to 4,500 kcal without efficiency loss. This flexibility allows optimization based on market conditions rather than technical constraints.

The procurement strategy goes beyond cost negotiation to value creation. Caustic soda, the second-largest cost after energy, is now produced through the GACL joint venture. Coal security through captive mines eliminates quality variations. Even small consumables are sourced through rate contracts with automatic price adjustments, eliminating procurement delays while ensuring competitive costs.

The maintenance philosophy—predictive, not reactive—drives availability. Vibration analysis predicts bearing failures. Thermal imaging identifies insulation degradation. Oil analysis indicates equipment wear. The result: unplanned downtime below 2% versus industry average of 5%. Every percentage point of availability improvement adds ₹50 crore to bottom line.

The quality systems transcend certification to become competitive advantage. NALCO aluminum consistently exceeds LME specifications—iron content below 0.15% versus allowed 0.25%, silicon below 0.08% versus allowed 0.10%. This premium quality commands price premiums in Japanese and European markets where specifications are stringent.

NALCO is one of the leading foreign exchange earning CPSEs of the Country. Export earnings exceeded ₹4,000 crore annually, providing natural hedge against rupee depreciation. But more importantly, export market discipline forces global competitiveness. When you compete against Chinese efficiency and Middle Eastern energy costs, operational excellence isn't optional.

The logistics optimization, often overlooked, contributes significantly. The 14-kilometer conveyor from mine to refinery eliminates 500 truck trips daily. The slurry pipeline for red mud disposal reduces handling costs by 60%. The dedicated railway sidings eliminate demurrage charges. These seemingly small optimizations aggregate to substantial savings.

The government ownership, typically seen as constraint, becomes strategic advantage in NALCO's hands. Patient capital allows long-term thinking—seven-year expansion plans, 30-year mining leases, generational R&D projects. No quarterly earnings pressure means decisions optimize value, not optics. Government backing provides credibility in international markets where counterparty risk matters.

The social responsibility isn't burden but business strategy. By sharing 2% of profits with communities, NALCO maintains social license worth infinitely more. By providing employment to project-affected families, the company ensures stakeholder alignment. By investing in regional development, NALCO creates the ecosystem necessary for operations.

The talent management breaks PSU stereotypes. Performance-linked pay can be 50% of compensation. Fast-track promotions reward excellence. International assignments provide exposure. The result: attrition below 2% for critical roles, productivity improvements of 8% annually, innovation culture generating 50+ patents.

The risk management framework is sophisticated yet simple. Commodity risk is managed through diversification—multiple products, multiple markets, multiple currencies. Operational risk is minimized through redundancy—backup equipment, alternative suppliers, buffer stocks. Financial risk is eliminated through zero debt. Regulatory risk is mitigated through proactive compliance.

The technology adoption strategy balances innovation with reliability. Proven technologies are implemented fast—new equipment, automation systems, digital tools. Experimental technologies are piloted carefully—artificial intelligence for process optimization, blockchain for supply chain, IoT for predictive maintenance. The approach: fast follower, not bleeding edge.

The competitive moats are multiple and reinforcing. Cost leadership from integration. Quality premium from operational excellence. Customer stickiness from reliability. Regulatory advantages from environmental leadership. These moats aren't static but continuously deepened through investment and innovation.

The capital efficiency metrics tell the story. Asset turnover of 0.8x matches asset-light industries despite heavy manufacturing footprint. Working capital turns of 12x rival FMCG companies despite commodity operations. Capital employed per tonne of aluminum is 30% below replacement cost. This efficiency translates directly to returns.

The cyclical resilience strategy deserves emphasis. During upturns, NALCO maximizes production but not prices, maintaining market share. During downturns, costs are cut but not maintenance, preserving asset quality. Through cycles, investment continues but cautiously, building for recovery. This through-cycle thinking creates value over time.

The organizational capabilities built over decades can't be replicated quickly. Technical expertise in tropical metallurgy. Operating experience in monsoon conditions. Relationships with tribal communities. Understanding of Indian regulatory environment. These intangibles, not reflected in financial statements, constitute true competitive advantage.

The continuous improvement culture, borrowed from Japanese management but adapted to Indian context, drives incremental gains. Each shift identifies one improvement. Every month implements one innovation. Annual savings from thousands of small improvements exceed ₹200 crore. Excellence isn't achievement but process.

Looking forward, the playbook evolves but principles remain. As digitalization accelerates, NALCO adopts carefully. As sustainability pressures increase, the company leads proactively. As markets globalize, operations internationalize gradually. The playbook isn't static doctrine but living philosophy—operational excellence as continuous journey, not destination.

X. Analysis & Bear vs. Bull Case

The investment case for NALCO presents a fascinating study in contrasts. Here's a government-owned commodity producer in a capital-intensive, cyclical industry—everything modern portfolio theory suggests avoiding. Yet it consistently generates returns exceeding technology darlings while maintaining dividend yields rivaling utilities. The bull and bear cases aren't just about numbers but about fundamental views on India's economic trajectory, the energy transition, and the role of strategic resources.

Bull Case: The Convergence of Tailwinds

The infrastructure supercycle isn't hypothesis but happening. India's $1.4 trillion National Infrastructure Pipeline requires 2 million tonnes of aluminum annually through 2030. Every kilometer of metro rail needs 40 tonnes of aluminum. Each electric vehicle uses 250 kg versus 150 kg in conventional vehicles. The new airports, railway stations, and smart cities aren't just consuming aluminum—they're consuming NALCO's specific alloys developed for tropical conditions.

The "Make in India" initiative transforms from slogan to substance. Apple assembling iPhones in India needs aerospace-grade aluminum. The indigenous fighter aircraft program requires specialized alloys NALCO develops with MIDHANI. The push for import substitution in defense, aerospace, and electronics creates captive demand for domestic producers with technical capabilities.

The green transition represents history's largest capital reallocation—$130 trillion over 30 years according to BlackRock. Aluminum intensity in renewable energy is 3x conventional systems. Solar panel frames, wind turbine nacelles, battery casings, transmission cables—all require aluminum. As the "green metal," aluminum benefits from every solar panel installed, every EV manufactured, every grid upgraded.

The strategic lithium ventures position NALCO for exponential growth. The Argentina lithium resources, if developed successfully, could be worth $20 billion at current prices—more than half NALCO's market cap. The expertise gained in lithium extraction applies to potential Indian discoveries in Ladakh and Karnataka. The integrated battery materials strategy—lithium, aluminum, copper—creates synergies competitors can't match.

Cost leadership in commodities is sustainable competitive advantage. NALCO's position as lowest cost producer of bauxite and alumina globally isn't temporary but structural—captive mines, integrated operations, tropical advantages. In commodities, the lowest cost producer earns profits through cycles while high-cost producers oscillate between profits and losses.

The financial fortress provides optionality. Zero debt means NALCO can invest counter-cyclically, acquiring assets when others are distressed. The cash generation funds growth without dilution. The dividend consistency attracts long-term investors providing stable capital base. Financial strength in cyclical industries is itself a competitive advantage.

The governance improvements, while gradual, are meaningful. Independent directors bring global perspectives. Transparency increases with quarterly calls and detailed disclosures. Performance incentives align management with shareholders. The government's reduced stake from 87% to 51% demonstrates commitment to market discipline.

The valuation discount to global peers despite superior metrics suggests rerating potential. At 8x P/E versus 15x for international aluminum producers, despite higher returns and lower risk, NALCO appears mispriced. As India's capital markets mature and global investors increase allocation, this discount should narrow.

The expansion pipeline provides visible growth. The million-tonne refinery expansion, 500,000-tonne smelter addition, renewable energy projects—all have defined timelines and return projections. This isn't speculative growth but planned capacity addition in proven operations.

Bear Case: The Structural Headwinds

Chinese oversupply remains the elephant in the room. China produces 60% of global aluminum, often below economic cost, supported by state subsidies. When China sneezes, aluminum markets catch pneumonia. NALCO's cost leadership helps but doesn't immunize against systematic overcapacity driving prices below production costs.

Global commodity price volatility is increasing, not decreasing. Aluminum prices swung 50% in 2022 alone. Currency fluctuations add another layer of uncertainty. While NALCO manages volatility better than peers, the underlying business remains hostage to forces beyond control—Chinese policy, dollar strength, energy prices.

Environmental regulations are tightening globally and India won't remain exempt forever. Carbon border taxes in Europe affect exports. Water usage restrictions impact operations. Bauxite mining faces increasing scrutiny. The environmental costs currently externalized will eventually be internalized, affecting profitability.

Government ownership, despite professional management, creates constraints. Investment decisions require ministry approvals causing delays. Salary caps limit ability to attract top talent. Social obligations reduce commercial flexibility. Political interference, while minimal historically, remains a risk.

Capital allocation inefficiencies persist despite improvements. The dividend payout of 45% might be too high given growth opportunities. Geographic diversification into non-core states reflects political considerations. Some CSR spending, while generating goodwill, destroys shareholder value.

Technology disruption threatens aluminum demand in certain applications. Carbon fiber replaces aluminum in aerospace. Advanced plastics substitute in automotive. Steel improvements compete in construction. While total demand grows, specific segments face substitution risk.

The energy transition itself poses risks. If renewable energy becomes cheap enough, NALCO's captive power advantage disappears. If solid-state batteries eliminate aluminum casings, EV demand disappoints. If hydrogen-based steel production succeeds, aluminum's relative advantage diminishes.

Execution risks in expansion projects are material. The million-tonne refinery faces environmental clearance delays. The lithium venture operates in Argentina's unstable political environment. The downstream projects require capabilities NALCO hasn't demonstrated. Execution delays or failures would destroy value.

The talent pipeline shows concerning gaps. Average employee age of 45 suggests succession challenges. Competition from private sector for young talent is intensifying. Technical expertise in aluminum is abundant but capabilities in new ventures like lithium are scarce.

The Balanced Perspective

The truth, as often, lies between extremes. NALCO isn't the undervalued gem bulls proclaim nor the value trap bears warn against. It's a well-managed, strategically positioned company operating in a challenging industry with both tailwinds and headwinds.

The infrastructure and green transition tailwinds are real but will take decades to fully materialize. The cost leadership is sustainable but margins will compress as competition intensifies. The expansion projects will likely succeed but with delays and cost overruns. The governance will continue improving but remain constrained by government ownership.

For investors, NALCO represents a specific bet: that India's economic growth will drive aluminum demand, that operational excellence will sustain competitive advantage, that patient capital will create value through cycles. It's not suitable for momentum traders seeking quick gains nor for growth investors expecting exponential returns.

The investment case ultimately depends on time horizon and risk tolerance. For long-term investors seeking dividend income with modest growth, NALCO offers attractive risk-reward. For those believing in India's infrastructure story and energy transition, it provides leveraged exposure. For ESG-focused funds, it represents best-in-class emerging market exposure.

The key monitorables going forward are clear: execution of expansion projects, sustainability of cost leadership, success of strategic ventures, and evolution of governance. If NALCO delivers on even half its ambitious plans while maintaining operational excellence, the bull case prevails. If execution falters or competitive advantages erode, bears will be vindicated.

XI. Epilogue & Strategic Outlook

As monsoon clouds gather over the Panchpatmali hills in 2024, NALCO stands at an inflection point. The brownfield expansion will increase Nalco's aluminium production capacity from 440,000 t/y to one-million ton a year—more than doubling size within five years. But this isn't just about scale. It's about transformation from national champion to global player, from commodity producer to materials company, from industrial-age manufacturer to energy-transition enabler.

The strategic choices ahead are profound. Should NALCO prioritize domestic market share or international expansion? Focus on aluminum or diversify into battery metals? Optimize for profitability or growth? Maintain government control or dilute for capital? These aren't binary choices but balance points requiring careful calibration.

The energy transition opportunity is generational. BloombergNEF projects aluminum demand from solar panels alone reaching 10 million tonnes by 2040. Electric vehicles will consume 18 million tonnes. Grid expansion needs 15 million tonnes. This 43 million tonnes of incremental demand equals half of current global production. NALCO's positioning—low carbon production, renewable energy integration, strategic locations—provides competitive advantages in capturing this growth.

Can NALCO become a global champion while remaining government-owned? The evidence suggests yes, with caveats. Singapore's Temasek, Norway's Norsk Hydro, Chile's Codelco demonstrate that state ownership needn't preclude commercial success. But they also show that success requires operational autonomy, professional management, and market discipline—areas where NALCO has progressed but hasn't fully arrived.

The lessons for industrial policy are nuanced. NALCO's success wasn't despite government ownership but because of specific features it enabled—patient capital, long-term thinking, social legitimacy. But success also required insulation from political interference, performance-based culture, and market exposure. The model isn't easily replicable without these enabling conditions.

For strategic resource management, NALCO offers a template. Vertical integration provides supply security. Operational excellence ensures competitiveness. Social responsibility maintains license to operate. Environmental leadership anticipates regulations. This holistic approach to resource development could guide India's approach to other critical minerals—lithium, cobalt, rare earths.

The international expansion strategy taking shape is pragmatic. Rather than competing head-to-head with Chinese scale or Middle Eastern energy costs, NALCO targets niches—specialty aluminas, tropical alloys, sustainable aluminum. The planned smelters in Indonesia and Africa leverage specific advantages—captive coal, renewable energy—rather than pursuing growth for its own sake.

The technology roadmap balances ambition with pragmatism. Industry 4.0 implementation proceeds systematically—IoT sensors, AI optimization, digital twins. But breakthrough innovations are pursued selectively—carbon capture for smelters, bio-leaching for bauxite, hydrogen reduction for alumina. The approach: fast follower in proven technologies, selective leader in strategic areas.

The sustainability commitments aren't greenwashing but core strategy. The target of 1 GW renewable capacity by 2030 would make NALCO carbon-neutral in alumina production. The zero-waste goal by 2035 would eliminate the red mud problem. The water-positive target by 2028 would address the critical constraint. These aren't cost centers but competitive differentiators in an ESG-conscious world.

The organizational evolution continues. The average age decreases as fresh talent joins. The culture shifts from compliance to performance. The mindset evolves from domestic to global. But challenges remain—attracting digital talent, developing new capabilities, maintaining technical expertise while expanding scope.

The financial trajectory appears robust but not guaranteed. Assuming successful expansion execution, moderate aluminum prices, and stable operations, NALCO could achieve ₹30,000 crore revenue and ₹5,000 crore profit by 2030. The market capitalization could reach ₹75,000 crore, delivering 15% annual returns. But these projections assume many variables outside NALCO's control.