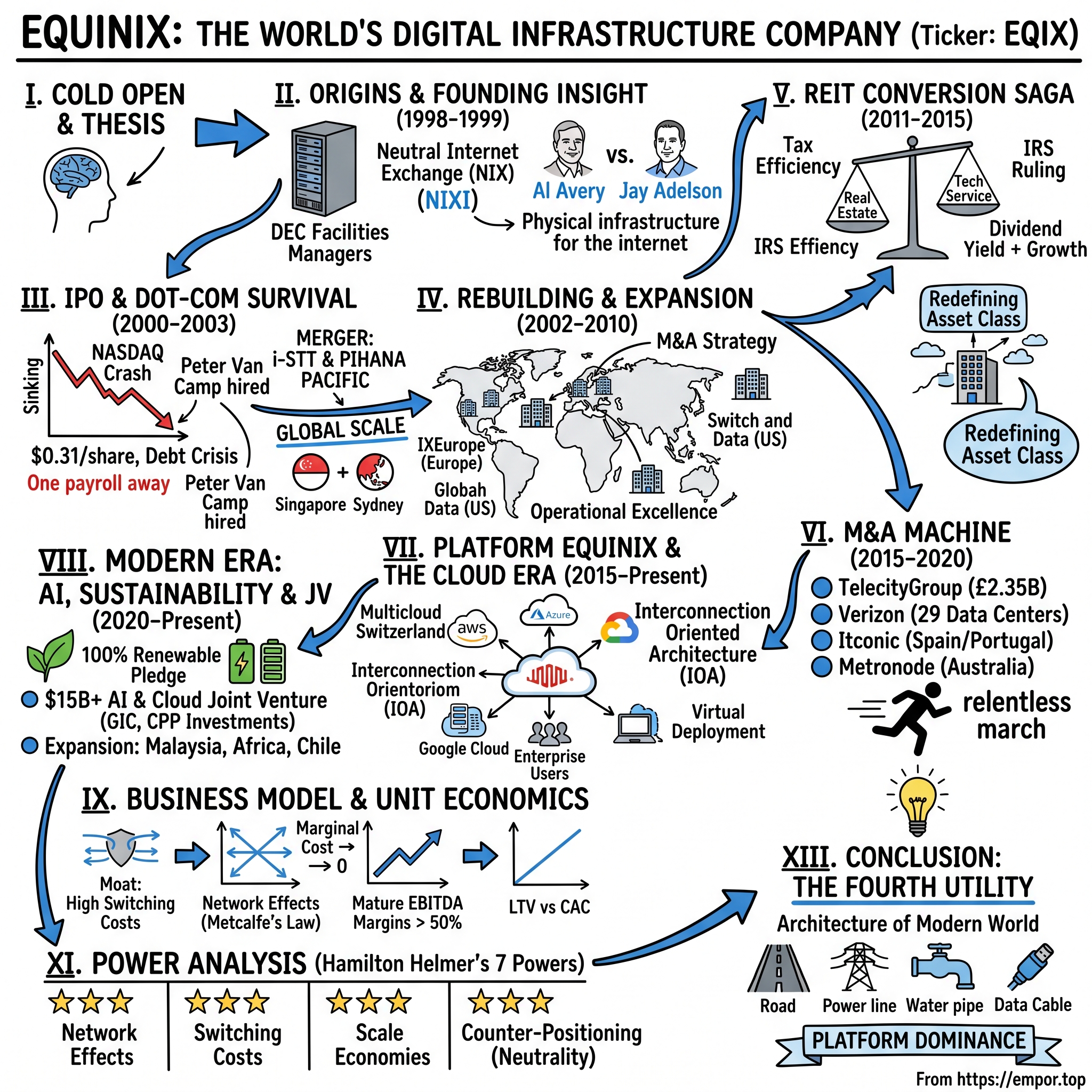

Equinix: The World's Digital Infrastructure Company

I. Cold Open & Thesis

Picture this: It's 3 AM on a Tuesday in Ashburn, Virginia, and while most of America sleeps, billions of data packets are racing through a nondescript warehouse at speeds approaching light itself. This isn't science fiction—it's the beating heart of the modern internet, and it happens inside one of Equinix's 260+ data centers scattered across the globe like digital embassies in the information age. How did a company operating over 260 data centers globally and generating quarterly revenues exceeding $2.2 billion as of Q3 2024 become the beating heart of the internet? The answer lies not in Silicon Valley boardrooms or Wall Street trading floors, but in the unglamorous server rooms where the digital economy actually lives.

Walk into any Equinix facility today and you'll find something remarkable: fierce competitors—Amazon Web Services, Microsoft Azure, Google Cloud—all housing their infrastructure mere feet apart, their data flowing through shared interconnection points. This would be like Ford, GM, and Toyota sharing the same assembly line. Yet in the digital infrastructure world, this seemingly impossible arrangement has become the foundation of a $75 billion market cap colossus. The story begins in 1998 with two facilities managers at Digital Equipment Corporation (DEC), Al Avery and Jay Adelson, who worked together as facilities managers at Digital Equipment Corporation. While the rest of Silicon Valley was chasing eyeballs and clicks, Avery and Adelson were focused on something far less glamorous but infinitely more essential: the physical infrastructure where the internet actually happened.

They developed the idea for a Neutral Internet Exchange (NIX) to create a physical place for networks to exchange critical information—a radical concept at the time. Imagine telling competing telecommunications companies they should house their most precious equipment in the same facility, operated by a third party. It was like asking Coke and Pepsi to share a bottling plant.

Yet that was precisely the genius of it. The firm promoted its data center platform as a neutral place where competing networks could connect and share data traffic. The firm capitalized on the "network effect," through which each new customer would broaden the appeal of its platform. Every new tenant made the facility more valuable to everyone else. It was a physical manifestation of Metcalfe's Law—the value of a network increases exponentially with each additional node. Microsoft and Cisco Systems emerged as some of the company's original investors, recognizing early that control of internet interconnection points would become as strategically important as control of railroad junctions had been a century earlier. Michelangelo Volpi, at the time Cisco's Senior Vice President and General Manager, joined the board alongside Scott Kriens from Juniper Networks, lending instant credibility to what many still saw as a quixotic venture. In July 1999, Equinix opened its first International Business Exchange (IBX) data center in Ashburn, Virginia—a location that would become the epicenter of the internet's physical infrastructure. The timing was exquisite: just as the dot-com boom was reaching its crescendo, Equinix was laying the foundation for what would become the internet's most important crossroads.

The naming of the company itself was telling. 'Equinix' reflected its core principle of equitable access to internet infrastructure—a democratic vision in what had been a feudal digital landscape dominated by incumbent telcos. This wasn't just marketing speak; it was a fundamental reimagining of how the internet's physical layer should work.

II. Origins & The Founding Insight (1998-1999)

The origins of Equinix trace back to 1996, when Jay Adelson was recruited by Digital Equipment Corporation (DEC) to work on an ambitious project: the Palo Alto Internet Exchange (PAIX). In late 1996, Adelson worked for Digital Equipment Corporation's Network System Laboratory, specifically with Albert M. Avery IV, to build and operate the Palo Alto Internet Exchange (PAIX). Adelson worked alongside Stephen Stuart and Paul Vixie to build a datacenter and services suited for scaling the core of Internet traffic. Adelson's efforts led to the facility's success as an Internet Exchange Point. This was the first major carrier-neutral internet exchange point—a radical departure from the telecom-controlled model that dominated the era.

The PAIX experiment proved transformative. Digital didn't know how to capitalize on the success of PAIX. "We started selling real estate really fast, and we were profitable." Adelson and Avery had been given US$3m by Digital to establish what is now known as the Palo Alto Exchange (PAIX) in an old basement—then the largest internet infrastructure in the world. The company sold to telecommunications company Metrofiber (now Abovenet) for $70m in 1999. But while PAIX was a technical success, Digital Equipment—struggling with its own identity crisis as the computing world shifted beneath its feet—couldn't figure out how to capitalize on this new model.

It was in this confusion that opportunity emerged. When Compaq acquired Digital Equipment in 1998, Adelson and Avery saw their chance. In June 1998, Adelson and Avery left Digital Equipment Corp and founded Equinix, Inc. (briefly Quark Communications). They struck a deal with Compaq's CEO before leaving, ensuring they wouldn't compete directly with PAIX. Their vision was far grander: to build numerous internet exchange points in data centers around the world, all interlinked—an International Business Exchange.

The founding insight was deceptively simple yet revolutionary: The firm promoted its data center platform as a neutral place where competing networks could connect and share data traffic. The firm capitalized on the "network effect," through which each new customer would broaden the appeal of its platform. In an industry where carriers jealously guarded their networks, Equinix would be Switzerland—a neutral territory where everyone could interconnect without fear of competitive disadvantage.

But neutrality alone wasn't enough. Adelson and Avery realized that to make their vision work, they needed to solve a fundamental infrastructure problem. "We knew for our idea to work everyone would have to use dark fiber coming into the facility – not three or four networks but 100 different networks – and we knew that inside our facility we would have to have infinite numbers of cross connections."

This meant reimagining the data center itself. As Adelson later recalled, "But we realized that if you wanted to offer this, then what most people would want to do is place a switch next to the other guy's routers and switches. We had to build a data center but we weren't quite sure how that worked. We weren't data center guys." This admission—that they weren't data center experts—proved to be their secret weapon. It forced them to approach the problem from first principles.

The fundraising journey illuminated the audacity of their vision. "We went to the CTO of Cisco at the time and Bill Gates – anyone with a vested interest in the internet growing. They agreed to put money in at a really high evaluation, which led to Venturemark Capital (which Equinix had earlier knocked back with an offer of $4m for 75% of the company) changing its offer and joining the group of C funding investors. This gave Equinix a total of $12m to kick off the first half of a data center in Ashburn, Virginia," Adelson says. "We founded the company on June 22, 1998, and were venture funded by September."

Several Silicon Valley tech companies embraced the business model, and the company could count on big names like Microsoft (MSFT) and Cisco System (CSCO) as some of its original investors. Michelangelo Volpi, at the time Cisco's Senior Vice President and General Manager of the Routing and Service Provider Group, joined the board, bringing instant credibility. Scott Kriens from Juniper Networks also came aboard, creating a who's who of networking royalty backing this upstart venture.

The location choice for their first data center was strategic genius. Adelson and Avery went just north of Fairfax, to Loudoun County, and visited officials there. "We went in like cowboys and said 'Hey, we have this idea to build the largest exchange point in the world in your county, and all we ask is for you to make it really easy and attractive financially for our customers to get their networks up'. We told them if this happens then companies like AOL and Broadcom will move in. Loudoun County had never had this before, so they said 'let's do it'. And it totally worked, just as we advertised." Equinix started building out in 10,000 sq ft increments in Ashburn, with the first instalment opening in June 1999.

The first IBX Data Center was opened in Ashburn, Virginia, on July 27, 1999. In order to attract networks, Equinix management used "match making" with content companies. AT & T and UUNet were the first two major networks interconnected using IBX Data Center, seven major companies followed and established a Point of Presence (PoP) in the company's data centers between 1999-2000.

The network effect began immediately. Once AT&T and UUNet—two of the internet's largest backbone providers—signed on, it became almost impossible for other networks to stay away. Each new customer made the platform exponentially more valuable to everyone else. It was Metcalfe's Law playing out in physical space, with routers and fiber optic cables instead of software and protocols.

By late 1999, Equinix had raised nearly $100 million in venture funding, valuing the company at levels that seemed astronomical for a startup with a single data center. As Adelson would later reflect with characteristic understatement: "You can be blown away by what you can accomplish if you decide not to listen. I mean, we raised US$1bn in three years because we decided to ignore common wisdom."

The stage was set for what should have been a triumphant IPO and rapid expansion. Instead, Equinix was about to walk straight into one of the most devastating market crashes in history.

III. The IPO & Dot-Com Survival Story (2000-2003)

August 10, 2000. The NASDAQ had already begun its sickening slide from its March peak, but there was still enough froth in the market for one more internet IPO. Equinix went public at $12 per share (or today's equivalent of $384 after the 2002 reverse split), raising more than $270 million in what would prove to be one of the last successful tech offerings before the music stopped entirely.

The man who pulled off this minor miracle was Peter Van Camp, a telecom industry veteran recruited from UUNET in May 2000 specifically to take the company public. Van Camp had the kind of resume that could calm jittery investment bankers—president of Internet markets at UUNET, the backbone that carried much of the internet's traffic, and before that, various roles at CompuServe dating back to 1982. He was the adult supervision the VCs demanded.

Peter Van Camp was brought on in 2000 to take the company public, and he pulled it off, even after our lead investment bank backed out on us. The IPO happened in August 2000, just months before everything really went south in Silicon Valley, and the cash we raised gave us resources at a critical time.

The drama behind that IPO reveals just how close Equinix came to missing its window entirely. Their lead investment bank—sources suggest it was one of the bulge bracket firms—got cold feet and backed out at the eleventh hour. In normal times, this would have killed the deal. But Van Camp, drawing on decades of relationships in the industry, managed to find new underwriters and push the offering through. The timing couldn't have been more fortuitous—or more terrifying.

Within weeks of the IPO, the bottom fell out completely. The NASDAQ, which had peaked at 5,048 in March 2000, would eventually crater to 1,114 by October 2002—a 78% decline. Equinix's customers—the dot-coms burning through venture capital to "get big fast"—began disappearing overnight. Companies that had signed multi-year contracts for cabinet space simply vanished. The phones stopped ringing. The sales pipeline evaporated. By mid-2002, the situation had become dire. Shares in the 4-year-old firm, down 89 percent this year, slid to 31 cents Thursday -- well below Nasdaq's $1 minimum. Equinix, which has 272 employees, said it is scrambling to renegotiate deals with lenders to avoid defaulting on $263 million in debt. "We are substantially leveraged," Equinix warned investors in a filing with the Securities and Exchange Commission. "The company does not currently have sufficient cash reserves or alternate financing available to repay the amount outstanding."

The company was literally one payroll away from extinction. As one employee would later recall: Two years later, our management team was able to renegotiate our debt at a time when we were one payroll away from closing our doors. This 2002 article from the San Francisco Chronicle lays it out: stock price down to 31 cents a share, $263 million in debt with insufficient cash reserves and financing to cover it.

The company's competitors were falling like dominoes. Exodus Communications, once valued at $50 billion, filed for bankruptcy. Metromedia Fiber Network, PSINet—all gone. The data center graveyard was filling up fast, and everyone expected Equinix to be next. Several of Equinix's largest investors recently liquidated their holdings. Times Square Capital Management dumped 1.2 million shares. The vultures were circling.

But then something remarkable happened. Van Camp and his team engineered one of the most impressive corporate turnarounds in Silicon Valley history—though it would come at a steep price for existing shareholders. The lifeline came from an unexpected source: Singapore. In December 2002, Equinix announced a complex three-way merger that would fundamentally restructure the company and give it a global footprint. Singapore Technologies Telemedia Pte Ltd (ST Telemedia), through its subsidiary STT Communications Ltd, made a strategic investment in Equinix in the amount of $30 million. Equinix also announced today that it has merged the assets of i-STT, a wholly-owned Internet infrastructure services subsidiary of ST Telemedia into its business, and has completed the acquisition of Pihana Pacific, which included the contribution of more than $26 million of cash from Pihana's balance sheet. Pihana Pacific is a leading provider of neutral Internet exchange data center services and managed e-infrastructure services in Asia-Pacific. By integrating i-STT and Pihana Pacific into its business, Equinix becomes the largest global network-neutral Internet exchange services company.

The deal was financially complex but strategically brilliant. Equinix also announced the retirement of more than $116 million of its 13% Senior Notes, which leaves approximately $30 million Notes outstanding. The existing shareholders got massively diluted—a 1-for-32 reverse stock split was implemented on December 31, 2002, to bring the company's stock price back into compliance with NASDAQ listing requirements. As part of the transactions approved at the stockholders meeting held December 30, Equinix announced a one for 32 reverse stock split effective December 31, 2002. This action is directed at bringing the company's stock price in compliance with Nasdaq initial listing requirements.

For those who held through the reverse split, it was brutal. Every 32 shares became 1 share. The stock that had IPO'd at $12 (and had briefly traded above $20) was now effectively worth less than 40 cents on a pre-split basis. Early investors were virtually wiped out. But the company survived.

More importantly, the merger gave Equinix something invaluable: instant global scale. In 2002, Equinix merged with I-STT, the Internet infrastructure service subsidiary of Singapore Technologies Telemedia, and Pihana Pacific. This established the company's presence in China, Singapore, Australia and Japan. Suddenly, Equinix wasn't just an American data center company struggling to fill empty cabinets in a post-bubble wasteland. It was the world's largest network-neutral internet exchange services company, with facilities spanning from Silicon Valley to Singapore.

Peter Van Camp would later reflect on this period with characteristic understatement: The $30 million strategic investment from ST Telemedia, $26 million of cash from Pihana's balance sheet, and the significant reduction of debt result in a strengthened balance sheet that provides Equinix with a solid financial base to build a profitable company for long-term growth and value.

But perhaps the most important outcome of the crisis wasn't financial—it was cultural. As one longtime employee would later observe: Equinix's culture was formed in those first years, as we went through a near-death experience, and it created a resiliency, determination and unity that still exists. I can honestly say the people at Equinix are like my second family, and as we've grown together, the bonds have only strengthened.

The company that emerged from the dot-com crash was leaner, globally diversified, and—most importantly—had proven that its fundamental thesis was correct. Even as hundreds of dot-coms disappeared, the need for neutral interconnection points only grew stronger. The networks still needed to connect. The data still needed to flow. And increasingly, there was only one global platform where everyone could meet: Equinix.

The survival story would become part of Silicon Valley lore—not because it was unique (many companies restructured during the crash), but because of what came next. While competitors continued to struggle or disappear entirely, Equinix began a relentless march toward global domination that would span two decades and counting.

IV. The Rebuilding Years & Geographic Expansion (2002-2010)

The merger with i-STT and Pihana Pacific in 2002 wasn't just a financial lifeline—it was a blueprint for everything that would follow. For the first time, Equinix management could see what a truly global interconnection platform might look like. The data centers in Singapore, Tokyo, and Sydney weren't just new revenue sources; they were nodes in an emerging network that would fundamentally reshape how global enterprises thought about their infrastructure.

The immediate challenge was integration. Three companies with different cultures, systems, and approaches to the market suddenly had to operate as one. The Tokyo facility inherited from Pihana Pacific, for instance, operated on completely different technical standards than the Ashburn data centers. Singapore's i-STT brought relationships with Asian telcos that operated nothing like their American counterparts.

But Van Camp and his team recognized that these differences were features, not bugs. Each market had its own interconnection dynamics, its own critical mass of networks, its own unique value proposition. The key was to maintain local relevance while building global consistency. This would become the Equinix playbook: acquire, integrate, standardize the platform, but preserve local ecosystem relationships. The year 2007 marked a critical transition. Peter Van Camp, who had shepherded the company through its near-death experience and painful restructuring, stepped aside as CEO while remaining as Executive Chairman. His replacement was Stephen M. Smith, a former Hewlett-Packard executive who had run HP's massive services business. Van Camp served as CEO of Equinix for seven years (2000 to 2007). Since 2007, he has served as executive chairman of the Equinix Board of Directors.

Smith brought something different to the table—operational excellence at scale. As Van Camp noted at the time, "Steve possesses exactly the broad leadership skills and experience needed to continue to expand our strong market leadership position: broad knowledge of the global technology industry; a total commitment to customer success; and a deep appreciation for the importance of team and culture."

Under Smith's leadership, the company would embark on one of the most aggressive expansion campaigns in technology history. From 2007 to 2018, he served as Chief Executive Officer and President of Equinix, the largest data center company globally. Under his leadership, Equinix grew from $2 billion to $34 billion in market value, while revenue increased from $400 million to $4.4 billion.

The expansion strategy was methodical. Rather than building new data centers from scratch—which required massive capital and took years—Equinix focused on strategic acquisitions. Each target was evaluated not just for its physical assets but for its ecosystem value: which networks were already there, which customers could be cross-sold, which local relationships could be leveraged. The 2007 acquisition of IXEurope for approximately $550 million (after a bidding war pushed up the price from the initial $482 million) exemplified this approach. IXEurope is a leader in the European network-neutral colocation market. It operates 14 data centers comprising approximately 325,000 square feet of net sellable space throughout Europe, including centers in Dusseldorf, Frankfurt, Geneva, London, Munich, Paris and Zurich. The company's more than 450 enterprise and Internet customers include Capgemini, Citigroup and Deutsche Boerse Systems.

As Smith explained at the time: "The strategic acquisition of IXEurope by Equinix will solidify Equinix's position as the world's market leading colocation provider with high-quality data centers across the United States, Asia-Pacific and Europe. Customers are increasingly demanding global solutions as the colocation industry continues to grow at double digit rates."

But the genius wasn't just in buying facilities—it was in preserving what made them valuable. The current management team, including Guy Willner, IXEurope CEO, and Christophe de Buchet, IXEurope COO, will join Equinix and continue to operate the European business. This wasn't American imperialism; it was federation building. Each region maintained its local expertise while gaining access to a global platform.

The 2010s would be remembered as Equinix's imperial decade, and no acquisition better exemplified this than the 2010 purchase of Switch and Data. The combined company would operate more than six million gross square feet of global data center space with more than 575 network service providers, adding more than one million gross square feet of data center capacity to Equinix's portfolio.

Under the terms of the agreement, Switch and Data stockholders would receive either 0.19409 shares of Equinix stock or $19.06 in cash for each share of Switch and Data stock, with the overall consideration being 80% Equinix stock and 20% cash. The $683.4 million acquisition closed on May 4, 2010, creating what TeleGeography called "a colocation services giant that dwarfs its competitors, both in the US and globally".

The strategic value went far beyond size. The transaction allowed Equinix to immediately expand into new strategic metropolitan areas, including Atlanta, Denver, Miami, Seattle and Toronto. These weren't just new pins on the map—they were critical nodes in an emerging digital nervous system. As Smith explained at the time, "Our collective customers will clearly benefit from our commitment to extraordinary customer satisfaction as we broaden our portfolio of services together".

What made the Switch and Data acquisition particularly brilliant was its history. Switch and Data had acquired PAIX in March 2003—the world's first commercial Internet peering exchange, which gave them a strong presence in global Internet peering and added some of the world's leading Internet content and service providers as customers. This was the same PAIX that Jay Adelson had helped build at Digital Equipment—the DNA of internet interconnection coming full circle.

By the end of 2010, Equinix had become something unprecedented in the data center industry. With the Switch and Data acquisition, Equinix almost doubled the inventory of cabinet equivalents available in the North American market, adding about 8,920 cabinet equivalents billing and an inventory of about 5,080 cabinets to Equinix's existing 23,600 cabinet equivalents billing in the U.S.

The transformation under Steve Smith's leadership was nothing short of remarkable. Under his leadership from 2007 to 2018, Equinix grew from $2 billion to $34 billion in market value, while revenue increased from $400 million to $4.4 billion, successfully integrating 21 acquisitions over 10 years representing over $25 billion in organic and inorganic investments.

V. The REIT Conversion Saga (2011-2015)

The idea first surfaced during a routine quarterly earnings call in 2011. CFO Keith Taylor, almost as an afterthought, mentioned that Equinix was exploring the possibility of converting to a Real Estate Investment Trust (REIT) structure. For most listeners, it seemed like financial engineering—a tax optimization play. They couldn't have been more wrong. This would become one of the most consequential strategic decisions in Equinix's history, a multi-year odyssey that would fundamentally reshape how investors valued digital infrastructure.

The logic was compelling on paper. REITs, which distribute at least 90% of their taxable income to shareholders as dividends, pay no corporate income tax on that distributed income. For a capital-intensive business like data centers, with predictable recurring revenues and substantial depreciation shields, the structure seemed tailor-made. Digital Realty, Equinix's closest competitor, had operated as a REIT since its 2004 IPO. DuPont Fabros, CoreSite—they were all REITs. Equinix was leaving money on the table.

But the path to REIT conversion would prove far more treacherous than anyone anticipated. In September 2012, after more than a year of analysis, Equinix's board unanimously approved a plan to pursue REIT conversion, announcing they would seek a private letter ruling from the IRS to confirm their qualification. This wasn't just about checking boxes—it was about convincing the IRS that a company running what were essentially server hotels qualified for a tax structure originally designed for shopping malls and office buildings.

The first blow came in 2013. The IRS, overwhelmed by a wave of unconventional REIT conversion applications, essentially pressed pause on the entire process. Data centers existed in a gray area—were they real estate assets generating rental income, or technology services companies? The interconnection revenues that made Equinix special also made it complicated. When you charge customers not just for space but for connecting to other customers, is that rent or is that a service?

Inside Equinix, the uncertainty was agonizing. The company had already begun restructuring operations to comply with REIT requirements, creating taxable REIT subsidiaries (TRS) to house non-qualifying activities. They were running two races simultaneously—continuing to execute on aggressive growth plans while preparing for a fundamental restructuring that might never happen.

The breakthrough came in late 2014. After nearly two years of negotiations, clarifications, and restructuring, the board felt confident enough to move forward even without the IRS ruling. In December 2014, they unanimously approved REIT conversion effective January 1, 2015. It was a calculated risk—if the IRS later ruled against them, the consequences would be severe.

To qualify for REIT status, Equinix needed to distribute its accumulated earnings and profits. This meant a special distribution totaling $1.0 to $1.1 billion to shareholders—a massive one-time windfall that would drain the company's cash reserves but reset its tax basis going forward. For shareholders, it was Christmas in January.

The vindication came in May 2015, when the IRS finally issued its private letter ruling. The ruling was more than just a green light—it was a blueprint for how data center REITs could operate. The IRS agreed that data center assets qualified as real estate and, crucially, that interconnection revenues could be considered qualifying REIT income. This wasn't just a win for Equinix; it legitimized an entire asset class.

The impact was immediate and profound. As a REIT, Equinix could offer investors something unique: growth plus yield. While traditional REITs in retail or office space offered stable dividends but modest growth, Equinix combined a dividend yield with double-digit revenue growth. It was having your cake and eating it too.

The REIT conversion also fundamentally changed how Equinix thought about capital allocation. With the requirement to distribute 90% of taxable income, the company needed to be more strategic about funding growth. This would lead to innovative joint venture structures with pension funds and sovereign wealth funds in later years—a preview of the capital markets innovation that would define the next era.

But perhaps the most important outcome was how it positioned Equinix in investors' minds. No longer was it just a technology company subject to the whims of Silicon Valley boom-bust cycles. It was now digital infrastructure—as essential and investable as toll roads or power plants. The REIT structure didn't just optimize taxes; it redefined the entire category.

VI. The M&A Machine & Global Domination (2015-2020)

May 29, 2015. While the ink was barely dry on the IRS's favorable REIT ruling, Equinix dropped a bombshell that would reshape the global data center landscape. The company announced it would acquire TelecityGroup, Europe's leading data center operator, for £2.35 billion ($3.8 billion)—the largest acquisition in Equinix's history and a deal that would more than double its European footprint overnight.

The TelecityGroup acquisition was transformative beyond its size. With 40 data centers across 11 European cities, including prime locations in London's Docklands, Amsterdam, Frankfurt, and Paris, TelecityGroup didn't just bring capacity—it brought ecosystems. These weren't empty shells waiting for tenants; they were thriving interconnection hubs where Europe's digital economy converged.

The deal almost didn't happen. Interxion, another European data center giant, had been circling TelecityGroup for months. A bidding war erupted, with Equinix ultimately prevailing by offering a 36% premium to TelecityGroup's pre-bid share price. Some analysts called it expensive. Equinix called it strategic.

The European Commission's antitrust review added another layer of complexity. To secure approval, Equinix agreed to divest eight data centers to Digital Realty—a painful concession that nonetheless preserved the deal's strategic value. Critically, Equinix retained TelecityGroup's crown jewel: the Telecity Harbour Exchange in London's Docklands, one of Europe's most important interconnection points.

But TelecityGroup was just the opening salvo in a five-year acquisition spree that would cement Equinix's global dominance. In December 2015, while still digesting the European mega-deal, Equinix pivoted to Asia, acquiring Japanese data center provider Bit-isle for $280 million. The six data centers added weren't just about capacity in Tokyo and Osaka—they were about depth in a market where relationships and local presence mattered more than anywhere else.

The year 2016 brought perhaps the most symbolically important deal: the $3.6 billion acquisition of 29 data centers from Verizon. Here was one of America's telecom giants essentially admitting that the data center business required a different model, a different focus. The portfolio spanned 15 markets across the Americas, including key sites in São Paulo, Miami, and Silicon Valley. For Equinix, it was like acquiring beachfront property in every major digital market.

The integration challenges were immense. Each acquisition brought different systems, different cultures, different customer expectations. The Verizon facilities, for instance, had been run as cost centers supporting the telco's network operations—Equinix needed to transform them into profit centers serving multiple customers. The TelecityGroup integration required harmonizing operations across different European regulatory regimes while maintaining the local relationships that made each facility valuable.

Equinix's integration playbook, refined over dozens of acquisitions, became a competitive advantage in itself. Within 90 days of closing, acquired facilities would be rebranded and connected to Equinix's global platform. Sales teams would begin cross-selling immediately—a TelecityGroup customer in London could now seamlessly expand to Singapore or Silicon Valley. Back-office systems would be standardized, but local teams who knew the customers, who understood the market dynamics, were retained and empowered.

The company also showed remarkable discipline in walking away from deals that didn't fit. When Digital Realty acquired DuPont Fabros in 2017, some expected Equinix to counter. They didn't. When CyrusOne went on the block, Equinix passed. The discipline to say no was as important as the ability to say yes.

By 2017, the acquisition engine was running at full throttle. The purchase of Itconic brought Equinix into Spain and Portugal. The Metronode acquisition in Australia added 10 data centers down under. Each deal followed the same pattern: identify markets where interconnection demand was accelerating, acquire the leading neutral provider, integrate rapidly, and watch the network effects compound.

The capital markets innovations keeping this M&A machine funded were equally impressive. Traditional debt and equity would have been prohibitively expensive or dilutive. Instead, Equinix pioneered joint venture structures that brought in patient capital from pension funds and sovereign wealth funds as partners, not just lenders. These partners would fund the development of new facilities, sharing in the returns while Equinix maintained operational control.

The transformation was staggering in its scope. The company that entered 2015 with 100 data centers in 33 metros emerged from this period with over 200 facilities spanning 52 metros. Revenue grew from $2.4 billion to over $5 billion. But the most important metric wasn't size—it was interconnection density. By 2020, Equinix customers were creating over 400,000 interconnections, each one making the platform more valuable to everyone else.

VII. Platform Equinix & The Cloud Era (2015-Present)

The transformation began with a simple observation: customers didn't want data centers—they wanted interconnection. They didn't care about square footage or power density; they cared about connecting to partners, accessing clouds, and reaching customers with minimal latency. This insight would drive Equinix's evolution from a real estate company that happened to house technology to a platform company that happened to own real estate.

In 2017, firms on the leading edge of digital transformation knew that leveraging Interconnection – direct, private data exchange between businesses – was a key ingredient in their success. This wasn't just marketing rhetoric. The company published the Global Interconnection Index that year, providing the industry's first annual global baseline to track, measure and forecast the growth of Interconnection, measuring Interconnection Bandwidth—the total capacity provisioned to privately and directly exchange traffic with a diverse set of counterparties and providers at distributed IT exchange points.

The numbers were staggering. Latin America was forecasted to be the fastest-growing region at 62% annually by 2020. Banking and Insurance was estimated to be the most interconnected industry with 61% annual growth by 2020. Every metric pointed to the same conclusion: the future of IT infrastructure wasn't about centralization or decentralization—it was about interconnection.

The Equinix Cloud Exchange, launched earlier in the decade, evolved into something far more ambitious. In 2017, Equinix rolled out new capabilities for its platform, renaming it Equinix Cloud Exchange Fabric, or ECX Fabric, intended to reflect the ability to use Equinix's SDN platform – built in-house with proprietary technology – to remotely connect between customers and partners in any ECX-enabled locations within North America and Europe, and eventually around the globe.

This wasn't just connecting to AWS or Azure anymore. Equinix created a rich, global ecosystem of nearly 10,000 companies including 1,800+ networks and 2,900+ cloud and IT service providers. Every major cloud provider, every significant SaaS platform, every critical network—they were all accessible through a single port, a single contract, often with a single API call.

The platform strategy went beyond technology. As both ecosystem suppliers and consumers on Platform Equinix, customers gained a network effect that continuously compounded their value. A financial services firm could connect to market data providers, cloud platforms for compute, security services for protection, and network providers for global reach—all from a single interconnection point. Each new service that joined the platform made it more valuable for everyone else.

By 2017, 85% of enterprises were employing a multicloud strategy – 58% being hybrid clouds – according to the "RightScale 2017 State of the Cloud Report." Equinix positioned itself as the Switzerland of this multicloud world. While AWS, Azure, and Google Cloud competed fiercely for workloads, Equinix provided the neutral ground where they could all coexist, where customers could use the best tool for each job without being locked into a single ecosystem.

The company introduced the concept of Interconnection Oriented Architecture (IOA), a proven and repeatable strategy to digitally transform enterprises, developed for network architects and informed by experts who had reinvented for the digital edge. This wasn't just about moving to the cloud—it was about fundamentally rethinking how distributed infrastructure should work.

Real-world implementations proved the model's power. A Fortune 100 pharmaceutical company conducting a clinical drug trial used a genome sequencing application that utilized computing cores from AWS for compute requirements while using Microsoft Azure for storage. The company deployed the Equinix Cloud Exchange to support a service aggregation edge node leveraging a multi-hybrid cloud architecture. Cloud Exchange, deployed within a digital edge node close to users, significantly reduced latency. The firm could select best-of-breed IaaS resources at scale and provision virtualized, high-speed connections for predictable application performance.

The shift from physical to virtual was equally transformative. Customers could deploy compute, networking and storage solutions virtually, in minutes, through an ecosystem of providers on the global platform, accelerating global delivery and consumption of digital services at scale with on-demand infrastructures. What once required months of procurement and installation could now happen with a few clicks.

But perhaps the most profound change was in how Equinix thought about competition and partnership. The hyperscalers—AWS, Microsoft, Google—weren't just customers anymore; they were partners in a complex dance. Equinix housed their edge nodes, their direct connect points, their regional presences. Yet it also competed with them as they built their own data centers and offered their own interconnection services.

The resolution of this tension came through specialization. The hyperscalers excelled at massive scale, commodity compute, and global reach. Equinix excelled at interconnection density, neutrality, and ecosystem richness. By 2024, 55% of enterprise IT workloads were hosted off-premises—up from 42% in 2020. Organizations needed to improve agility and facilitate better connectivity to partners and service providers—all in the interest of driving better business outcomes.

Platform Equinix became the answer to a question enterprises were just beginning to ask: in a world where applications span multiple clouds, data lives everywhere, and latency is measured in microseconds, how do you build infrastructure that's both globally distributed and tightly integrated? The answer wasn't choosing between centralized or decentralized, cloud or on-premises, public or private. It was "all of the above, connected intelligently."

VIII. Modern Era: AI, Sustainability & Joint Ventures (2020-Present)

The announcement came on October 1, 2024, and it sent shockwaves through the data center industry. Equinix signed a joint venture agreement with GIC and Canada Pension Plan Investment Board (CPP Investments), with the intent to raise over US$15 billion in capital together with its partners. Driven by increasing artificial intelligence (AI) and cloud growth, the JV is intended to accelerate the Equinix xScale data center portfolio. At full buildout, this new JV will nearly triple the investment capital of the Equinix xScale program.

This wasn't just another infrastructure deal—it was a bet on the future of computing itself. As CEO Adaire Fox-Martin explained: "As the world's leading companies build out their infrastructure to support key workloads such as artificial intelligence, they require the combination of large-scale data center footprints optimized for AI training and interconnection nodes for the most efficient inferencing. Our xScale and IBX offerings are uniquely positioned to address this business need, enabling companies to realize the powerful potential of AI."

The structure of the deal revealed how sophisticated data center financing had become. CPP Investments and GIC would each control a 37.5% equity interest in the joint venture, and Equinix would own a 25% equity interest. Each party made equity commitments, and the joint venture also expected to take on debt to raise the total pool of investable capital to more than US$15 billion over time.

This joint venture model wasn't new for Equinix—they had pioneered it over the previous decade. Equinix's existing hyperscale joint venture portfolio in Europe, Asia-Pacific and the Americas had a committed investment of over US$8 billion, which was expected to result in greater than 725 MW of power capacity across more than 35 facilities at full buildout. But the scale of this new venture dwarfed everything that came before.

The AI boom was reshaping everything about data center design and economics. Traditional data centers might consume 5-10 megawatts of power. AI training clusters needed 100+ megawatts—the equivalent of a small city. The heat densities were unprecedented, the cooling requirements extreme, the interconnection bandwidth measured in terabits. This wasn't evolution; it was revolution.

Meanwhile, Equinix's geographic expansion continued at breakneck pace, pushing into emerging markets that would define the next decade of digital growth. In November 2022, Equinix announced its market entry into Malaysia with plans to build a new International Business Exchange data center in Johor, called JH1. With an initial investment of approximately $40 million, JH1 was scheduled to begin operations in Q1 2024, providing 500 cabinets and 1,960 square meters of colocation space.

The Malaysia expansion exemplified Equinix's sophisticated market entry strategy. One of Equinix's main pitches to JH1's potential customers was the data centre's proximity to Singapore. The Managing Director of Equinix Malaysia, Cheam Tat Inn, noted that Malaysia, especially Johor, had started to become the next hub of choice due to the limited data centre capacity in Singapore. JH1 was just 15km away from the border in Tuas and connected directly to the Equinix data centres in Singapore. Equinix was confident that JH1 was in the prime location to take advantage of the excess demand from the city-state.

But perhaps the most profound shift was in sustainability. What had once been a nice-to-have became existential. In 2015, the company made a long-term pledge to power its entire platform with clean and renewable energy. JH1 and KL1 data centres ran on 100% renewable energy right from day one. All xScale data centers would be LEED certified (or certified in the regional equivalent).

The sustainability challenge was particularly acute with AI workloads. Training a single large language model could consume as much electricity as thousands of homes use in a year. Equinix VP Christopher Wellise cited artificial intelligence energy use as one of the "many growing strains on electric grids" and stated that AI needs to be viewed "through the lens of sustainability, no question."

The company's response went beyond renewable energy purchases. Heat recycling programs began repurposing waste heat from data centers to warm nearby buildings. Innovative cooling technologies reduced water consumption. Machine learning optimized power usage effectiveness (PUE) in real-time. The data center was becoming not just carbon-neutral but actively beneficial to its surrounding environment.

The joint venture strategy also evolved to address different market needs. In April 2024, Equinix entered a $600 million JV with PGIM Real Estate for its first xScale data center in the U.S. Earlier ventures with GIC had funded expansion in Korea ($525 million in 2022) and Japan ($1 billion in 2020). Each partnership brought not just capital but local expertise and relationships.

Africa emerged as the next frontier. In 2024, Equinix announced a $390 million expansion plan for Africa over five years, recognizing that the continent's digital transformation was accelerating and infrastructure investment couldn't wait. The December 2021 acquisition of Main One, a West African data center and connectivity solutions provider for $320 million, had established the beachhead.

The geographic expansion continued: Chile and Peru via a $758 million acquisition from Entel in March 2022. India through the acquisition of GPX India's Mumbai campus in 2020. Each new market added complexity but also opportunity—new ecosystems, new interconnection points, new paths for data to flow.

By 2024, Equinix operated 260 data centers in 33 countries, employing about 13,000 people worldwide. But the numbers only told part of the story. Each facility was becoming smarter, more autonomous, more integrated into the fabric of digital life. AI wasn't just something that happened inside the data centers—it was increasingly running the data centers themselves.

The convergence of AI, sustainability, and global expansion created unprecedented challenges. How do you provide the massive power AI requires while meeting carbon neutrality goals? How do you maintain security and sovereignty while enabling global data flows? How do you standardize operations across 33 countries while respecting local requirements and customs?

The answer, increasingly, was through partnerships—not just financial but strategic. The pension funds and sovereign wealth funds weren't just passive investors; they were long-term partners aligned with Equinix's vision of digital infrastructure as the fourth utility, as essential as electricity, water, or transportation.

As the world rushed headlong into the AI era, Equinix found itself at the center of a fundamental question: who would own and operate the physical infrastructure of artificial intelligence? The hyperscalers had the capital and the demand. The governments had the regulatory power and the sovereignty concerns. But Equinix had something perhaps more valuable: neutrality, global reach, and two decades of experience in making competitors comfortable as neighbors.

IX. Business Model & Unit Economics Deep Dive

At its core, Equinix operates one of the most elegant business models in technology: it's a landlord that makes its tenants more valuable to each other. Every new customer that joins an Equinix data center increases the value proposition for every existing customer. It's network effects in physical form, Metcalfe's Law made tangible in concrete, steel, and fiber optic cables.

The revenue model appears deceptively simple. Approximately 52% of revenues come from interconnection and colocation services. Customers pay monthly recurring charges for cabinet space (colocation) and for connections to other customers (interconnection). A typical enterprise might pay $2,000-$5,000 per month for a cabinet, plus $300-$500 per month for each cross-connect to another customer. For a financial services firm with 20 cabinets and 100 cross-connects, that's a $150,000 monthly bill—$1.8 million annually.

But the genius is in the unit economics. Once a data center is built, the marginal cost of adding a customer approaches zero. The power is already flowing, the cooling is already running, the security guards are already on duty. Incremental revenue drops almost entirely to the bottom line. This operating leverage is why mature Equinix facilities can generate EBITDA margins north of 50%.

The interconnection revenue is even more attractive. A cross-connect is literally just a cable running from one customer's cage to another's—perhaps 50 feet of fiber that costs $100 to install but generates $500 per month forever. The margins approach 95%. More importantly, each cross-connect makes it harder for either customer to leave. It's switching costs as a service.

The capital intensity is significant but front-loaded. In 2023, capital expenditures reached $3.8 billion, with $2.2 billion for data center construction. A typical 3MW data center might cost $30-40 million to build and take 18-24 months to reach break-even occupancy. But once stabilized, that facility could generate $15-20 million in annual revenue with 50%+ EBITDA margins—a cash-on-cash return exceeding 20%.

The REIT structure adds another layer of financial engineering. By distributing 90% of taxable income as dividends, Equinix pays no corporate tax on that distributed income. This tax efficiency allows them to offer investors both growth and yield—a combination that's rare in public markets. The dividend yield might only be 2%, but when combined with 10-15% annual revenue growth, the total return proposition becomes compelling.

Customer acquisition costs are surprisingly low for an enterprise business. Equinix doesn't need armies of salespeople or massive marketing budgets. The ecosystems sell themselves. If you're a financial services firm and all the major exchanges are in Equinix, you have to be there too. If you're a content delivery network and all the major ISPs interconnect at Equinix, you have no choice. The customer acquisition cost (CAC) might be $10,000-$20,000, but the lifetime value (LTV) of that customer could exceed $1 million.

The recurring revenue model provides extraordinary visibility. Customer contracts typically run 3-5 years with annual price escalators. Churn rates in mature markets run below 2% per quarter—implying average customer lifespans exceeding 12 years. This predictability allows Equinix to make massive capital commitments with confidence. They know with near certainty what revenues will look like three years hence.

The joint venture model has revolutionized the capital equation. Instead of funding all growth through debt and equity, Equinix brings in partners who provide 75% of the capital for new builds in exchange for 75% of the economics. Equinix maintains operational control and collects management fees, turning a capital-intensive business into something approaching capital-light. The return on invested capital (ROIC) math becomes extraordinary when you're generating returns on other people's capital.

Pricing power comes from the network effects. As interconnection density increases, customers will pay more to be in the building. An Equinix cabinet in Ashburn might cost 3x what a similar cabinet costs in a wholesale data center down the street. But that wholesale facility doesn't have 500+ networks, 100+ cloud on-ramps, and thousands of potential partners. The premium isn't for the real estate—it's for the ecosystem.

The scalability of the model is perhaps its most remarkable feature. Managing 260 data centers globally isn't 260 times harder than managing one. The same systems, processes, and platforms work everywhere. A customer onboarded in Singapore can deploy in Silicon Valley with a single phone call. This operational leverage means that Equinix can grow revenues faster than operating expenses, driving margin expansion even as the business scales.

But the real moat isn't financial—it's the impossibility of replication. A competitor could raise $15 billion and build 260 data centers, but they couldn't recreate the ecosystems. They couldn't convince 10,000 customers to relocate. They couldn't replicate two decades of trust and relationships. The business model isn't just defensible; it's essentially unassailable.

The unit economics tell a story of compound advantages. Higher interconnection density drives higher prices which drives higher margins which funds more expansion which attracts more customers which increases interconnection density. It's a virtuous cycle that's been spinning faster for more than two decades, and the AI boom is only accelerating the rotation.

X. Playbook: Lessons from Building Digital Infrastructure

The Equinix story offers a masterclass in building and scaling network effects in physical infrastructure. While software companies talk about network effects, Equinix literally built them—in concrete and steel, measured in kilowatts and cross-connects. The lessons from their journey read like a playbook for platform dominance.

Lesson 1: Neutrality as a Competitive Weapon

From day one, Equinix understood that neutrality wasn't weakness—it was strength. By refusing to compete with customers, they became indispensable to all of them. AWS, Azure, and Google Cloud Platform might fight viciously for workloads, but they all peacefully coexist in Equinix facilities. This Switzerland strategy required discipline. There were countless opportunities to move up the stack, to offer managed services, to compete with customers. Equinix resisted them all, maintaining its position as the neutral ground where the digital economy interconnects.

Lesson 2: Make Your Own Luck Through Persistence

The company's motto—"Luck is not chance. It's toil. Fortune's expensive smile is earned"—captured a fundamental truth. Equinix was "lucky" to survive the dot-com crash, "lucky" to get REIT approval, "lucky" to be positioned for the cloud boom. But that luck was manufactured through relentless execution, careful preparation, and the willingness to endure when others quit.

Lesson 3: Build Through Cycles, Not Despite Them

Equinix's greatest expansions came during downturns. The dot-com crash brought global scale through the i-STT merger. The 2008 financial crisis enabled the Switch and Data acquisition. The COVID pandemic accelerated digital transformation and cloud adoption. By building counter-cyclically, Equinix acquired assets cheaply and emerged from each downturn with increased market share.

Lesson 4: M&A as Core Competency

Between 2015 and 2020 alone, Equinix successfully integrated over 20 acquisitions worth more than $25 billion. This wasn't financial engineering—it was operational excellence. They developed a repeatable playbook: preserve local relationships, standardize the platform, cross-sell immediately, integrate within 90 days. Each acquisition made the next one easier. The integration muscle became as important as the balance sheet.

Lesson 5: Innovate the Capital Structure

The REIT conversion wasn't just tax optimization—it was category creation. By becoming a REIT, Equinix redefined how investors thought about digital infrastructure. The joint venture model took this further, turning a capital-intensive business into a capital-efficient platform. Financial innovation became as important as technical innovation.

Lesson 6: Switching Costs Through Interconnection

Every cross-connect a customer adds makes them less likely to leave. A financial services firm with 100 cross-connects would need to coordinate with 100 different partners to relocate—virtually impossible. These switching costs compound over time. The longer a customer stays, the more embedded they become, the higher the switching costs rise. It's lock-in through value creation, not vendor contracts.

Lesson 7: Global Platform, Local Execution

Equinix managed to be both global and local simultaneously. The platform was standardized worldwide—same systems, same processes, same service levels. But execution was intensely local. Each market had its own team that understood local regulations, relationships, and requirements. This "glocal" approach allowed rapid scaling without sacrificing local relevance.

Lesson 8: Infrastructure as a Moat

Physical infrastructure in the right locations with the right ecosystems is almost impossible to replicate. You can't download a data center. You can't copy-paste an ecosystem. You can't GitHub-fork interconnection density. In an increasingly digital world, physical presence became the ultimate differentiator.

Lesson 9: Compound Network Effects

Most businesses have linear growth—double the inputs, double the outputs. Equinix built exponential growth into its model. Each new customer made the platform more valuable to all existing customers. Each new interconnection increased the value of all existing interconnections. Value didn't add; it multiplied.

Lesson 10: Patient Capital for Long-Term Value

Data centers are 20-30 year assets. Customer relationships span decades. The investments made today might not pay off for years. By aligning with patient capital—pension funds, sovereign wealth funds, REITs structure—Equinix could make long-term bets that public market quarterly capitalism would never tolerate. Time horizon became a competitive advantage.

The playbook wasn't without its challenges. The capital intensity was enormous. The operational complexity of running facilities 24/7/365 across 33 countries was staggering. The technological changes—from client-server to cloud to AI—required constant adaptation. But by following these principles consistently over two decades, Equinix built something remarkable: a physical platform for the digital age.

XI. Power Analysis & Competitive Position

In the framework of Hamilton Helmer's "7 Powers," Equinix exhibits multiple forms of persistent differential returns—but three stand supreme: Network Effects, Switching Costs, and Scale Economies.

The network effects are obvious but worth quantifying. With over 10,000 customers creating more than 400,000 interconnections, each marginal customer adds value to all existing customers. This isn't theoretical—it's measurable. Locations with higher interconnection density command price premiums of 50-100% over less connected facilities. The Financial Times Stock Exchange (FTSE) is in Equinix Slough. If you want to trade on the FTSE with minimal latency, you must be in Equinix Slough. This creates a gravitational pull that only strengthens over time.

Switching costs manifest in multiple dimensions. The obvious one is physical—moving servers is expensive, risky, and disruptive. But the hidden switching costs are more powerful. Those 400,000 interconnections represent 400,000 reasons not to leave. Each cross-connect is a relationship, a partnership, a revenue stream that would be disrupted by relocation. For a large financial services firm, the switching costs could run into tens of millions of dollars and months of coordination.

Scale economies operate at both the facility and platform level. At the facility level, fixed costs (security, power infrastructure, cooling) are spread across more customers as utilization increases. A data center at 90% utilization has dramatically better unit economics than one at 60%. At the platform level, Equinix can spread R&D, sales, and overhead across 260 facilities. A competitor with 10 facilities faces 26x the relative burden.

The competitive landscape reveals Equinix's dominance. Digital Realty, the closest competitor, focuses primarily on wholesale data center space rather than interconnection. They're landlords; Equinix is a platform. CoreSite, now owned by American Tower, operates in just 10 U.S. markets. CyrusOne, taken private by KKR and Global Infrastructure Partners, lacks global reach. None match Equinix's combination of scale, interconnection density, and geographic scope.

The hyperscaler threat is more nuanced. AWS, Azure, and Google Cloud operate massive data center footprints, but they serve different purposes. Hyperscaler facilities are optimized for compute at scale—massive halls filled with identical servers running homogeneous workloads. Equinix facilities are optimized for interconnection—diverse customers with diverse needs connecting in diverse ways. The hyperscalers are Equinix's largest customers, not its competitors.

Regulatory and zoning advantages create additional moats. Many Equinix facilities sit in zones where new data center construction is now prohibited due to power constraints or environmental concerns. Northern Virginia has imposed data center moratoriums. Singapore stopped accepting new data center applications for years. These restrictions transform existing facilities into scarce assets whose value only appreciates.

The interconnection differentiator deserves special attention. While competitors can build data centers, they can't build ecosystems. The value isn't in the building—it's in who's inside the building. It's the "hotel bar" effect: the drinks aren't better, but the conversations are. This ecosystem value is path-dependent and essentially unreplicable.

Customer captivity runs deeper than switching costs. For many customers, Equinix has become embedded in their technical architecture. Their IP addresses are announced from Equinix facilities. Their cloud on-ramps terminate in Equinix meet-me rooms. Their disaster recovery plans assume Equinix availability. They're not just customers; they're dependents.

The platform power extends beyond individual facilities. A customer can deploy globally through a single relationship, single contract, single portal. This platform value creates winner-take-all dynamics in multinational enterprise segments. If you're a global company needing presence in 20 countries, would you rather manage 20 vendor relationships or one?

Competitive responses have been telling. Rather than competing head-on, most competitors have specialized. Digital Realty focuses on hyperscale wholesale. CoreSite targets specific U.S. metros. Local providers focus on single markets. The market has essentially conceded that competing with Equinix globally is economically irrational.

The durability of Equinix's advantages is perhaps most remarkable. Network effects typically weaken as networks grow large—Facebook doesn't become twice as valuable with twice the users. But Equinix's network effects strengthen with scale because business interconnection is fundamentally different from social networking. Every new bank makes the platform more valuable to every fintech. Every new cloud provider makes it more valuable to every enterprise. The network effects are heterogeneous and complementary, not homogeneous and redundant.

XII. Bear vs. Bull Case

Bull Case: The Infinite Escalator

The bull case for Equinix rests on multiple expanding trends that all point upward. Start with the macro: global data creation is doubling every two years. By 2025, humanity will create 463 exabytes daily—that's 463 billion gigabytes. Every byte needs to live somewhere, move somewhere, process somewhere. Equinix sits at the crossroads where all this data converges.

The AI revolution is just beginning. As AMD CEO Lisa Su told Time magazine when asked about a potential AI bubble: "Completely wrong… I think we'll be surprised, five years from now, how much AI has come into every aspect of our lives, and what we're seeing today is just the very, very tip of the iceberg." Every AI model needs training (massive compute), inference (edge deployment), and data (interconnection to sources). Equinix serves all three needs.

The secular shift to hybrid multicloud is irreversible. Enterprises aren't choosing one cloud—they're using 3-5 clouds plus on-premises infrastructure. Someone needs to connect all these pieces. That someone is increasingly Equinix. The company's platform becomes more valuable as infrastructure becomes more distributed and heterogeneous.

The REIT structure provides downside protection with upside potential. Even in a recession, the 2% dividend yield provides returns. The contractual revenue (typically 3-5 year terms) provides stability. The mission-critical nature of the service (you can't turn off your data center) ensures continuity. This isn't discretionary spending—it's the cost of existing in the digital economy.

The joint venture model has solved the capital intensity problem. With partners providing 75% of growth capital, Equinix can expand without dilution or dangerous leverage. The $15 billion commitment from GIC and CPP Investments funds years of growth. Return on invested capital skyrockets when it's mostly other people's capital.

Geographic expansion opens decade-long runways. Africa's internet economy will grow 10x by 2030. Southeast Asia adds 100,000 new internet users daily. Latin America's digital transformation is just beginning. Each new market represents not just revenue opportunity but ecosystem creation opportunity—the chance to become the foundational platform for a region's digital economy.

The impossibility of replication grows stronger over time. Every year, the ecosystems become denser, the switching costs higher, the network effects more powerful. A competitor starting today would need tens of billions of dollars and decades of execution to match Equinix's position—and by then, Equinix would be decades further ahead.

Bear Case: The Looming Threats

The bear case begins with the hyperscalers' growing appetite for vertical integration. AWS, Azure, and Google Cloud aren't just customers—they're potential existential threats. As they build their own facilities and offer their own interconnection services, they could gradually disintermediate Equinix. AWS's Direct Connect, Azure's ExpressRoute, Google's Partner Interconnect—these services compete directly with Equinix's core value proposition.

Capital intensity remains daunting despite financial engineering. xScale datacenters significantly increase the amount of megawatts of power required per facility. AI facilities need 100+ MW of power—10x traditional data centers. The infrastructure requirements are staggering: power, cooling, connectivity, security. Even with joint ventures, the capital needs could outstrip available funding.

Interest rate sensitivity is structural for REITs. As rates rise, REIT valuations typically fall as investors can get yield from safer bonds. Equinix trades at premium multiples (25x+ AFFO) that could compress violently if rates stay higher for longer. A reversion to historical REIT multiples (15x AFFO) would imply a 40% stock price decline.

Execution risk multiplies with complexity. Operating 260 facilities across 33 countries means 260 opportunities for something to go wrong every day. Power outages, cooling failures, security breaches, natural disasters—any incident could damage the reputation built over decades. As infrastructure becomes more critical, the consequences of failure become more severe.

Technology disruption could obsolesce the model. Edge computing could distribute workloads away from centralized facilities. Quantum computing could revolutionize processing requirements. New cooling technologies could enable data center construction in previously impossible locations. The physical infrastructure Equinix has spent decades building could become stranded assets.

Regulatory risks are rising globally. Data sovereignty laws could balkanize the internet, reducing the value of global interconnection. Energy regulations could limit data center expansion. Tax changes could eliminate REIT advantages. Privacy regulations could restrict data movement. The regulatory landscape is becoming more complex, not less.

Competition from sovereign wealth funds and infrastructure funds is intensifying. These deep-pocketed investors are building their own data center platforms, often accepting lower returns than public markets demand. The competitive landscape is getting more crowded just as the capital requirements are exploding.

Customer concentration risk is understated. The top 10 customers represent significant revenue concentration. If a major cloud provider decided to leave—or demanded significant price concessions—the impact would cascade through the ecosystem. The network effects that create value also create systemic risk.

The Verdict

The bull and bear cases aren't mutually exclusive—both could be right. Equinix could face hyperscaler competition while benefiting from AI growth. It could suffer from rate sensitivity while generating superior returns. It could face execution challenges while successfully expanding globally.

The key question isn't whether challenges exist—they clearly do. It's whether Equinix's advantages (network effects, switching costs, scale economies) are strong enough to overcome them. History suggests they are. Equinix has survived the dot-com crash, the financial crisis, the pandemic. Each challenge has made it stronger.

The ultimate bull case might be the simplest: in an increasingly digital world, physical interconnection points become more valuable, not less. As long as data needs to move between companies, clouds, and countries, someone needs to provide the neutral ground where that exchange happens. For now, and likely for decades to come, that someone is Equinix.

XIII. Conclusion: The Fourth Utility

Twenty-six years after Jay Adelson and Al Avery left Digital Equipment Corporation with a radical idea, their vision has become reality. Data centers are no longer just real estate—they're the physical manifestation of the digital economy. Equinix isn't just a company—it's infrastructure as essential as roads, power grids, or water systems. It has become the fourth utility.

The transformation from facilities management to platform orchestration represents one of the great business model evolutions of the digital age. What started as neutral colocation became interconnection, which became ecosystems, which became the indispensable substrate upon which the cloud economy operates. Every evolution added a layer of value, a degree of lock-in, a reason why customers could never leave.

The numbers tell one story: $75 billion market cap, 260 data centers, 10,000+ customers, 400,000+ interconnections. But the real story is about network effects in physical form, about turning competitors into neighbors, about making switching costs so high that customers become permanent residents of the platform.

Looking forward, Equinix sits at the intersection of every major technology trend. AI needs massive compute and interconnection. Edge computing needs distributed presence. Hybrid cloud needs neutral interconnection. Digital sovereignty needs local data residence with global connectivity. Every trend points toward a world where Equinix becomes more essential, not less.

The challenges are real—capital intensity, execution complexity, competitive threats. But the moats are equally real—ecosystem density, switching costs, geographic coverage, operational excellence. After 26 years, the barriers to replication haven't weakened; they've become insurmountable.

Perhaps the most remarkable aspect of the Equinix story is how unglamorous it is. No breakthrough technology. No charismatic founder cult. No viral consumer product. Just the patient accumulation of strategic assets, the careful cultivation of ecosystems, the relentless execution of a simple idea: in a connected world, the connections matter more than the nodes.

The future belongs to companies that own the choke points of the digital economy. Equinix owns the ultimate choke point—the physical locations where the world's data must converge to create value. In an economy increasingly mediated by artificial intelligence, processed at the edge, and distributed across clouds, these convergence points don't become less valuable—they become priceless.

As we stand on the brink of the AI revolution, with compute requirements growing exponentially and data sovereignty becoming paramount, Equinix's patient building of global, neutral, interconnected infrastructure looks less like a business strategy and more like prophecy. They built for a future that's only now arriving.

The lesson for investors isn't just about Equinix—it's about recognizing that in the digital age, the most valuable companies might not be the ones creating the technology, but the ones creating the conditions for technology to flourish. The platforms, not the products. The infrastructure, not the applications. The foundations, not the facades.

Equinix's journey from a single data center in Ashburn to the world's digital infrastructure company offers a masterclass in compound advantage, strategic patience, and the power of network effects. It's a reminder that in technology, as in life, fortune favors not just the bold, but the persistent—those willing to build for decades what others measure in quarters.

The digital economy needs a physical foundation. That foundation is Equinix. And as the economy becomes increasingly digital, that foundation becomes increasingly valuable. It's not just a investment thesis—it's an architectural necessity of the modern world.

In the end, Equinix achieved what Adelson and Avery envisioned but could scarcely have imagined: they built the place where the internet happens. Not the cables or the servers or the software, but the space where it all comes together. They built the world's digital town square, and in doing so, became indispensable to the digital age.

The story is far from over. The AI revolution, the edge transformation, the sovereignty challenges—these are chapters yet to be written. But if history is any guide, Equinix will not just adapt to these changes; it will profit from them. Because in a world of accelerating change, the one constant is the need for connection. And connection, ultimately, is what Equinix sells.

Note: This analysis is based on publicly available information and does not constitute investment advice. The author has no position in Equinix stock at the time of writing. Please conduct your own due diligence before making any investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube