Edison International: Power, Politics, and the California Dream

I. Introduction & Episode Roadmap

The lights flickered across Los Angeles on September 8, 2020. Not from a power shortage this time, but from smoke so thick it turned noon into twilight. As ash fell like snow across Southern California, Edison International's crews worked through apocalyptic orange skies, keeping electricity flowing to hospitals, homes, and the digital infrastructure that had become civilization's nervous system during the pandemic. This wasn't their first dance with disaster—far from it.

Edison International, through its crown jewel subsidiary Southern California Edison, delivers electricity to 15 million people across a 50,000-square-mile service territory. With a market capitalization hovering near $28.7 billion in late 2024, it stands as one of America's largest investor-owned utilities. But those numbers barely hint at the company's extraordinary journey—a story of survival, reinvention, and repeated brushes with corporate death.

Here's the question that should fascinate any student of business: How does a company that started lighting gas lamps on dusty California streets in 1886 transform into the backbone of the world's fifth-largest economy? And perhaps more remarkably, how does it survive not one but two existential crises that should have killed it—the 2000-2001 California energy crisis that nearly bankrupted the entire state's power system, and the ongoing wildfire liability apocalypse that has already claimed one major utility?

This is a story about the intersection of essential infrastructure and capitalism, where guaranteed returns meet catastrophic risks. It's about the delicate dance between public service and private profit, played out against California's unique backdrop of innovation, regulation, and environmental extremes. Most critically, it's about what happens when 19th-century business models collide with 21st-century climate reality.

Over the next several hours, we'll trace Edison's arc from its origins in the California frontier through its golden age as a regulated monopoly, into the deregulation disaster that nearly destroyed it, and finally to its current predicament—caught between wildfire liability that could wipe out shareholders and the massive infrastructure investments needed for California's clean energy transition. We'll examine how regulatory capture works in practice, why utilities are fundamentally different from other businesses, and what Edison's story tells us about America's infrastructure crisis.

This isn't just corporate history—it's a window into how essential services get delivered in a democracy, how political and business interests intertwine, and what happens when the assumptions underlying an entire industry prove catastrophically wrong. For investors, it's a masterclass in regulatory risk. For policymakers, it's a cautionary tale about unintended consequences. For everyone else, it's the hidden story behind every flip of a light switch in Southern California.

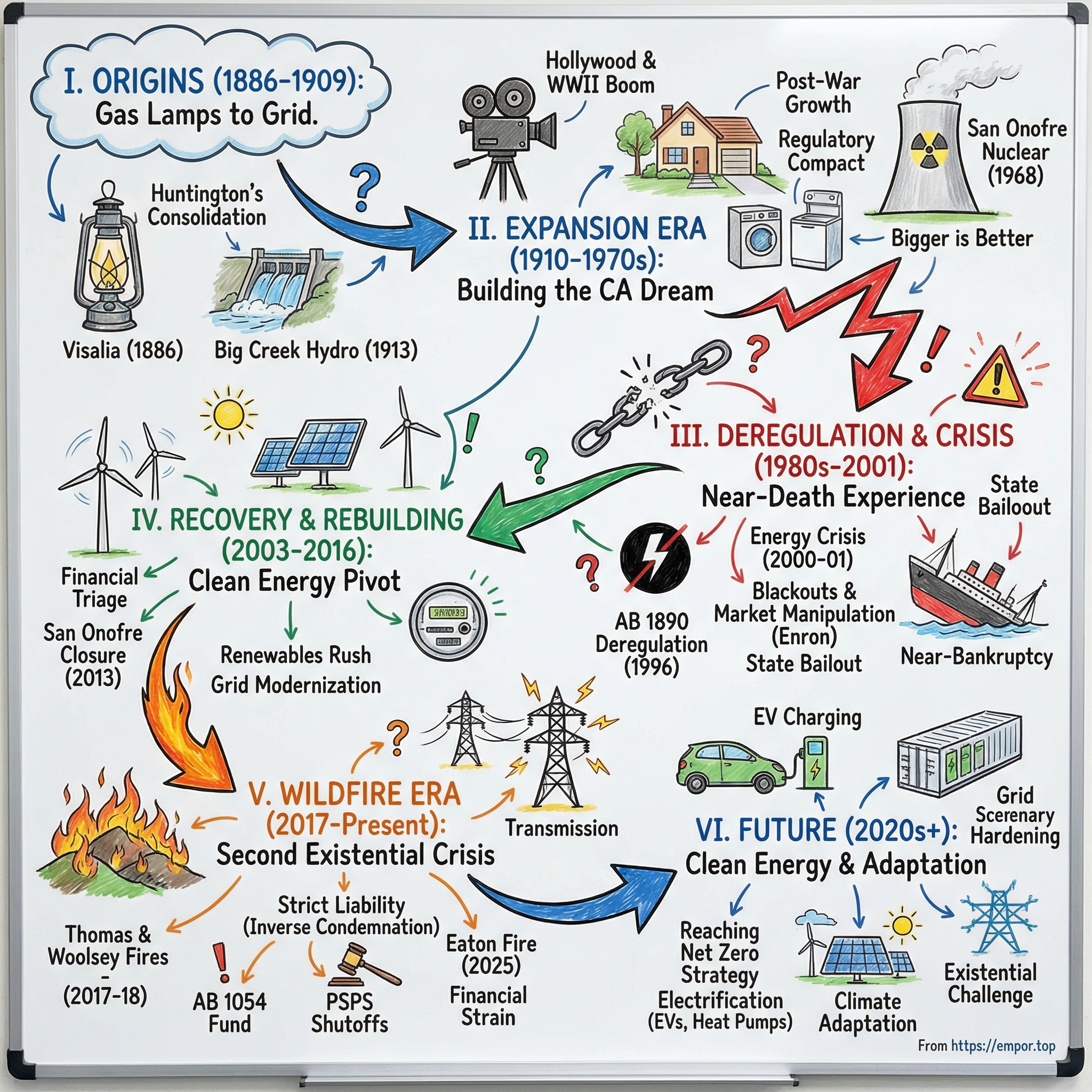

II. Origins: From Gas Lamps to Grid Power (1886-1909)

The year was 1886, and Visalia, California, was a dusty agricultural town in the Central Valley, population barely 2,000. But on Main Street, something revolutionary was happening. George Holt and William Knupps had just installed the town's first electric streetlights—arc lamps that hissed and sparked but lit the darkness with an intensity that made gas lamps look like candles. Their company, Holt & Knupps, would become the unlikely seed of what is now Edison International.

This wasn't Thomas Edison's operation—not yet. While the Wizard of Menlo Park was building his electrical empire on the East Coast, California was experiencing its own electricity gold rush. Dozens of small companies sprouted across the state, each serving a handful of blocks or a single town. The technology was so new that companies often ran different voltages and frequencies. Connecting systems was impossible; standardization was a dream.

The real action was 400 miles south in Los Angeles. In 1896, a group of local businessmen incorporated the Edison Electric Company of Los Angeles—one of many companies nationwide licensing the Edison name. They built a small generating plant on Alameda Street, powering streetlights and a handful of adventurous businesses. But Los Angeles was exploding—its population doubling every decade—and the hunger for electricity was insatiable.

Enter Henry Huntington, nephew of railroad baron Collis Huntington. Where others saw a patchwork of competing electric companies, Henry saw an empire waiting to be consolidated. Through his Pacific Light & Power Corporation, he began acquiring small utilities across Southern California. His masterstroke wasn't just consolidation—it was vision. While competitors focused on urban centers, Huntington saw that electricity's real value lay in connecting the sprawling communities spreading across the Southern California basin.

The corporate maneuvering of this era was byzantine. The Edison Electric Company of Los Angeles merged with the Los Angeles Electric Company in 1902. That entity was then acquired by Huntington's Pacific Light & Power in 1905. Meanwhile, other players were making similar moves. The San Gabriel Electric Company, the Riverside Light & Power Company, the Santa Ana Gas & Electric Company—each had carved out territorial fiefdoms, zealously guarding their service areas.

But the real transformation came with water—or more precisely, with falling water. In the Sierra Nevada mountains, 240 miles northeast of Los Angeles, lay Big Creek, a tributary of the San Joaquin River. The elevation drop was perfect for hydroelectric generation. The technology to transmit electricity over such distances was bleeding-edge, requiring voltages that many engineers thought impossible. But the economics were irresistible: hydroelectric power cost a fraction of steam generation.

In 1909, the consolidation reached its climax. A new entity, Southern California Edison Company, was incorporated, combining the assets of Edison Electric Company with several other utilities. The name was strategic—"Edison" carried technological prestige, while "Southern California" telegraphed regional ambitions. The company immediately embarked on what would become one of the most ambitious infrastructure projects of the early 20th century: the Big Creek hydroelectric system.

The engineering challenges were staggering. Building dams and powerhouses in remote mountain terrain required creating entire towns for workers. The transmission lines—running at what was then an unprecedented 150,000 volts—had to cross deserts, mountains, and active fault lines. Critics called it "Huntington's Folly." The first power from Big Creek reached Los Angeles in November 1913, traveling 241 miles in less than a second. It was the longest high-voltage transmission line in the world.

This early period established patterns that would define Edison for the next century. First, the company's growth came through aggressive consolidation—absorbing competitors to eliminate redundancy and achieve economies of scale. Second, it bet big on technology, pushing the boundaries of what was possible in generation and transmission. Third, and perhaps most importantly, it recognized that in the utility business, political relationships were as important as engineering excellence.

The company's executives became fixtures in Los Angeles society, joining the same clubs as bankers, real estate developers, and newspaper publishers. They understood that electricity wasn't just a product—it was the foundation upon which Southern California's entire economy would be built. Every new subdivision needed power lines. Every new factory needed reliable electricity. Every booster's dream of Los Angeles as a great metropolis depended on abundant, cheap power.

By 1909, as Southern California Edison formally began operations, it served about 15,000 customers across a handful of counties. The company's founders couldn't have imagined that this regional utility would one day power the entertainment capital of the world, the aerospace industry that would put men on the moon, and the technology companies that would reshape human civilization. But the seeds were planted: the infrastructure, the political connections, and most importantly, the regulatory framework that would guarantee profits while ostensibly protecting consumers.

The age of electricity had arrived in Southern California, and with it, the beginning of one of American business's most enduring—and troubled—corporate stories.

III. Building the California Dream: Expansion Era (1910-1970s)

The cameras rolled at Universal Studios in 1915, capturing Mary Pickford in silent melodrama. But behind the scenes, a different drama was unfolding. The massive arc lights that made moviemaking possible—each consuming as much power as dozens of homes—were pushing Southern California Edison's grid to its limits. Studio executives were furious about power interruptions ruining takes. Edison's response would define its next six decades: build bigger, build faster, and never stop building.

The Big Creek hydroelectric project had started modestly, generating 63,700 kilowatts when its first units came online. But by the 1920s, Edison's engineers had transformed the Sierra Nevada watershed into an industrial marvel—three reservoirs, eight concrete dams, 41 miles of tunnels, all feeding turbines that generated over 373,000 kilowatts. The project's chief engineer, A.C. Balch, became something of a legend, known for solving "impossible" problems through sheer determination and innovative engineering.

Hollywood wasn't just a customer—it was a co-conspirator in selling the California Dream. Every movie that showed palm-tree-lined streets and sun-drenched suburbs was essentially an advertisement for the electrically-powered lifestyle that Edison made possible. The company leaned into this symbiosis, running ads in variety trades and hosting studio executives at Big Creek to show off the engineering marvels powering their dream factories.

Then came World War II, and everything changed overnight. Douglas Aircraft's Santa Monica plant went from producing one plane per day to one per hour. Lockheed's Burbank facility expanded tenfold. The Kaiser shipyards in Los Angeles Harbor ran three shifts, seven days a week. Edison's load doubled in eighteen months. The company's engineers performed miracles of improvisation—stringing temporary lines, overloading transformers, praying nothing catastrophic failed before they could build permanent capacity.

The post-war boom made wartime look quaint. In 1946, Los Angeles County added 15,000 new homes. By 1950, it was 50,000 annually. Each tract house in Lakewood or Downey came with an all-electric kitchen—range, refrigerator, garbage disposal. Air conditioning, once a luxury, became standard in new construction by the 1960s. Edison's system load grew 7-8% annually, doubling every decade. The company's mantra, repeated in every annual report, was simple: "No customer will ever be denied service due to lack of capacity."

This growth machine ran on regulatory magic. California's Public Utilities Commission had created what economists called a "regulatory compact." Edison received exclusive franchise rights—monopoly protection—in exchange for serving all customers at regulated rates. The key innovation was rate-base regulation: Edison could earn a guaranteed return (typically 10-12%) on every dollar of infrastructure investment. The more Edison built, the more profit it earned. It was capitalism without risk, as long as you played by the rules.

The nuclear age arrived with fanfare in 1968 when San Onofre Nuclear Generating Station's Unit 1 achieved criticality. Edison executives spoke breathlessly about electricity "too cheap to meter." The plant, built on Camp Pendleton Marine Corps Base property (avoiding most local opposition), represented the ultimate expression of bigger-is-better thinking. Unit 1 alone could power 400,000 homes. Units 2 and 3, planned for the 1980s, would each be twice as large.

But the real genius of Edison's expansion era wasn't technical—it was political. The company's executives understood that in a regulated monopoly, the regulator is your most important stakeholder. Edison perfected what critics called "regulatory capture." Commissioners often came from utility backgrounds; after their terms, they frequently returned to industry. The company's rate cases—dense, technical documents running thousands of pages—overwhelmed public advocates. Edison could afford armies of lawyers and consultants; consumer groups had bake sales.

The financial performance during these "boring utility" decades was anything but boring for shareholders. From 1950 to 1970, Edison's stock price increased fifteenfold, not including dividends that yielded 4-6% annually. The dividend hadn't been cut since 1909—through two world wars, the Great Depression, everything. Widows and orphans—the archetypal conservative investors—loaded up on utility stocks. Edison was the definition of a blue chip: steady, predictable, essential.

By 1975, Edison served 3.5 million customer accounts across 50,000 square miles. The company operated one nuclear plant with two more units under construction, dozens of gas and oil-fired plants, and the Big Creek hydro complex. Its transmission system—23,000 miles of high-voltage lines—formed the spine of Southern California's economy. The company employed 17,000 people, making it one of the region's largest employers.

The formula seemed unbreakable: population growth plus electrification of everything equals perpetual expansion. Regulatory protection ensured profits. Political influence prevented disruption. Edison executives spoke confidently about serving 10 million customers by 2000, about nuclear plants dotting the California coast, about an all-electric future where clean, abundant power would solve every problem from air pollution to poverty.

Looking back, the 1970s marked peak hubris for the traditional utility model. The assumption that demand would grow forever, that bigger plants were always better, that regulatory protection was permanent—all of these would soon be shattered. But in the moment, Edison seemed invincible, the corporate embodiment of California's limitless ambition. The company had powered the state's transformation from agricultural backwater to economic colossus. What could possibly go wrong?

IV. The Deregulation Experiment (1980s-1996)

Steve Peace was furious. The Democratic assemblyman from San Diego stood at the podium in Sacramento in 1994, waving his electricity bill like a revolutionary's flag. "Californians pay 50% more for electricity than the rest of America!" he thundered. "While states like Pennsylvania enjoy competition and choice, we're held hostage by monopolist utilities!" Peace would become the architect of California's electricity deregulation—a reform that would nearly destroy Edison International and plunge the state into crisis.

The anger was real. California's electricity rates in the early 1990s averaged 9.5 cents per kilowatt-hour, compared to a national average of 6.5 cents. Industrial customers were fleeing to Nevada and Arizona. The California Manufacturers Association claimed high electricity costs had eliminated 44,000 manufacturing jobs. Even Hollywood was threatening to shoot elsewhere. The political pressure for action was overwhelming.

Edison saw the writing on the wall and decided to play offense. In 1988, the company restructured, creating SCEcorp as a holding company with Southern California Edison as its main subsidiary. The move seemed technical, but it was strategic—creating a corporate structure that could expand beyond the regulated utility business. CEO John Bryson, a co-founder of the Natural Resources Defense Council turned utility executive, understood that the old monopoly model was under attack.

The failed merger attempt with San Diego Gas & Electric in 1990 revealed just how much the ground was shifting. What should have been a straightforward consolidation—creating economies of scale, eliminating redundancies—became a political lightning rod. Consumer advocates screamed about creating a "mega-monopoly." Competitors lobbied furiously against it. After eighteen months of regulatory hearings, the companies withdrew the merger application. The message was clear: the era of utility empire-building was over.

In 1996, SCEcorp rebranded itself as Edison International, signaling ambitions beyond California. The company launched Edison Mission Energy, an unregulated subsidiary that would develop power plants worldwide. Executives spoke excitedly about opportunities in Thailand, Turkey, and the United Kingdom. The logic seemed impeccable: use expertise gained from a century of power generation to compete globally, earning unregulated returns that could dwarf the steady but modest profits from the California utility.

But the main event was Assembly Bill 1890, signed by Governor Pete Wilson on September 23, 1996. The legislation, crafted by Steve Peace and supported by an unusual coalition of consumer groups, industrial customers, and free-market advocates, would restructure California's entire electricity system. The key provisions seemed reasonable, even ingenious: utilities would sell their generating plants to create a competitive market, customers could choose their electricity supplier like they chose long-distance carriers, and rates would be frozen during a transition period to protect consumers.

Edison executives publicly supported deregulation, but privately they were terrified. The company agreed to sell most of its fossil fuel generating plants—4,000 megawatts of capacity—to independent power producers. The nuclear plant at San Onofre and the Big Creek hydro complex were retained, but everything else went on the block. AES Corporation bought the Alamitos and Huntington Beach plants. Dynegy acquired others. In eighteen months, Edison transformed from a vertically integrated utility that generated, transmitted, and distributed power into primarily a "wires company" that would buy electricity from others and deliver it to customers.

The numbers looked good on paper. Edison received $1.2 billion from asset sales, above book value. The company would earn regulated returns on its transmission and distribution system—the poles and wires—without the risk of operating power plants. In the new competitive market, innovative companies would build efficient plants, driving down wholesale prices. Consumers would benefit from choice and competition. It was the era of Enron, of dot-coms, of "markets solve everything."

Edison Mission Energy, meanwhile, was on a building spree. The subsidiary developed or acquired power plants from Illinois to Turkey, borrowing heavily to fund expansion. By 1999, it owned or had interests in forty plants worldwide with 15,000 megawatts of capacity. Analysts loved the story: regulated utility cash flows funding unregulated growth opportunities. Edison International's stock hit all-time highs.

But there were warning signs for those who looked closely. California's new electricity market was bizarrely complex—a day-ahead market, an hour-ahead market, a real-time balancing market, all operated by a new Independent System Operator. The rules ran to thousands of pages. Even worse, while wholesale prices were deregulated, retail rates remained frozen. If wholesale prices rose above retail rates, utilities would lose money on every kilowatt-hour sold.

The international expansions were proving trickier than expected. The Asian Financial Crisis of 1997 crushed electricity demand in Thailand and Indonesia. Turkey's currency collapsed. The UK's electricity market was more competitive than anticipated. Edison Mission Energy's profits were a fraction of projections. Debt was piling up.

As 1999 ended, Edison International looked successful—revenues of $9.8 billion, a market cap over $10 billion, ambitious international operations. CEO John Bryson was featured on magazine covers as a utility executive for the new millennium. The company's transformation from stodgy monopoly to dynamic competitor seemed complete.

In reality, Edison had traded a boring but stable business model for enormous complexity and hidden risks. It had sold the generating assets that gave it control over its costs. It had borrowed heavily to fund speculative international projects. Most dangerously, it was now dependent on California's newly deregulated wholesale market to buy the power its customers needed—a market that was about to spiral completely out of control.

V. California Energy Crisis: Near-Death Experience (2000-2001)

The lights went out at 1:47 PM on January 17, 2001. Not from a storm or equipment failure, but because California's electricity market had collapsed so completely that the state's grid operator ordered emergency blackouts across Northern California. In conference rooms at Edison International's Rosemead headquarters, executives watched news helicopters circle darkened Silicon Valley office parks. Traffic signals went dead. Elevators trapped passengers. Assembly lines stopped. For the first time since World War II, California was rationing electricity—not because there wasn't enough power, but because the market had been manipulated into dysfunction.

From December 1999 into 2001, Edison experienced a 900 percent rise in its power purchasing costs as California's deregulated electricity market spiraled into chaos. The numbers were staggering: For a product that Edison used to produce for about three cents per kilowatt hour, they were paying eleven to fifty cents, occasionally even more, but were capped at 6.7 cents when charging retail customers. Simple mathematics meant Edison was hemorrhaging cash on every electron it delivered.

The roots of the crisis traced back to the deregulation Edison had supported just four years earlier. The 2000-2001 California electricity crisis was caused by market manipulations and capped retail electricity prices. The market design was fatally flawed—wholesale prices were deregulated while retail rates remained frozen. When wholesale prices exploded, utilities became ATMs for power generators, forced to buy high and sell low until they ran out of money.

The manipulation was brazen. Enron traders, captured on recordings that would later become evidence, joked about "stealing money from California grandmothers." Manipulation strategies were known to energy traders under names such as "Fat Boy", "Death Star", "Forney Perpetual Loop", "Wheel Out", and "Ricochet". These weren't just colorful nicknames—they were sophisticated schemes to create artificial scarcity and drive prices through the roof. Generators would schedule phantom congestion on transmission lines, then offer to relieve it for astronomical fees. Plants would mysteriously go offline for "maintenance" during heat waves when demand peaked.

The financial hemorrhaging was immediate and catastrophic. In 1999, California's wholesale electricity expenditures totaled $7.4 billion. Just one year later, costs rose 277 percent to $27.1 billion, remaining at $26.7 billion in 2001. Edison was buying power at emergency prices—sometimes over $1,000 per megawatt-hour for electricity that normally cost $30—while legally prohibited from passing costs to customers.

By January 2001, Edison International had accumulated $3.9 billion in undercollections—money spent buying power that it couldn't recover from ratepayers. The company's commercial paper rating was cut to junk. Banks refused to extend credit. Generators, fearing they wouldn't be paid, refused to sell power to Edison unless the state guaranteed payment. California's entire electricity system was days from complete collapse.

Governor Gray Davis faced an impossible choice: let the utilities fail and watch California's economy implode, or orchestrate one of the largest corporate bailouts in American history. On January 17, 2001, the state began buying power on behalf of Edison and PG&E, essentially nationalizing California's electricity procurement. The state would ultimately sign $43 billion in long-term power contracts at inflated prices—deals that would haunt California ratepayers for decades.

PG&E went bankrupt, and Southern California Edison came close. On April 6, 2001, PG&E filed for Chapter 11 bankruptcy protection, listing $9 billion in losses from the crisis. Edison's board met that same day, bankruptcy papers drafted and ready. But CEO John Bryson had one card left to play—a political solution that would trade Edison's transmission grid for state support.

The negotiations were brutal. Consumer advocates screamed about bailouts. Industrial customers threatened to leave California. Politicians faced recall threats—Governor Davis would indeed be recalled in 2003, with the energy crisis as a primary cause. But Edison's lobbyists worked every angle, arguing that bankruptcy would make the crisis worse, not better. The company suspended its dividend for the first time since 1909, a symbolic gesture that it was sharing the pain.

The Memorandum of Understanding signed between Edison and the state in early 2001 was a masterpiece of financial engineering and political compromise. Edison would sell its transmission assets to the state for $2.76 billion—enough to pay down debt and avoid bankruptcy. The company would be allowed to recover $3.6 billion in crisis costs through a dedicated rate component that couldn't be challenged. In exchange, Edison agreed to not seek recovery of another $3 billion in costs and to maintain retail rate freezes for residential customers.

Edison worked diligently on a workout plan with the State of California to save their company from bankruptcy. The deal was controversial—consumer groups called it corporate welfare, while Edison shareholders complained about the massive write-offs. But it worked. Edison avoided bankruptcy, maintained its investment-grade credit rating (barely), and lived to fight another day.

The aftermath revealed the true scope of the market manipulation. Experts put the total damage to California's economy at more than $40 billion. Federal investigations uncovered systematic fraud by Enron and other traders. Tapes emerged of Enron employees laughing about shutting down plants to drive up prices. Criminal prosecutions followed. Civil settlements recovered billions, though nowhere near the total losses.

For Edison International, the crisis was transformative. The company wrote off $2.5 billion in stranded assets in December 2000. Edison Mission Energy, the unregulated subsidiary that was supposed to be the growth engine, became an albatross—its merchant power plants were suddenly worth a fraction of their construction cost. International adventures were abandoned. The company retrenched to its core California utility business, wounded but alive.

The California energy crisis shattered the deregulation consensus. Markets could be manipulated. Essential services couldn't be treated like commodities. The invisible hand sometimes formed a fist. Edison had survived its first near-death experience, but the scars would last. The company that emerged from the crisis was more cautious, more political, and more aware that in the utility business, financial engineering could never substitute for political protection.

VI. Recovery and Rebuilding (2003-2018)

Ted Craver took the CEO chair at Edison International in 2008, just as Lehman Brothers collapsed and the global economy cratered. His first all-hands meeting featured a stark message: "We survived the California energy crisis. We'll survive this too. But survival isn't enough anymore—we need to transform." Coming from the soft-spoken engineer who'd guided Edison through its post-crisis recovery as CFO, the words carried weight. Over the next decade, Craver would oversee Edison's painstaking rehabilitation from crisis-scarred survivor to clean energy advocate, though not without costly stumbles.

The immediate post-crisis years were about financial triage. Edison methodically paid down the $4.1 billion in debt accumulated during the energy crisis. The company reinstated its dividend in December 2003—a critical signal to investors that normalcy was returning. Credit ratings crept back to investment grade. By 2005, Edison was generating free cash flow again, though the balance sheet remained stretched.

Edison Mission Energy, the unregulated power subsidiary that was supposed to conquer global markets, had become a millstone. Its coal plants in the Midwest, purchased at peak valuations in the late 1990s, faced plummeting power prices and rising environmental compliance costs. The international projects were bleeding cash. In 2012, EME filed for bankruptcy, taking $2.4 billion in debt off Edison International's books but destroying any remaining dreams of unregulated growth.

Then came San Onofre—a disaster that would define Edison's next decade. The nuclear plant's two massive reactors had operated since the 1980s, providing carbon-free baseload power to Southern California. In 2009, Edison completed a $670 million project to replace the plant's steam generators, massive components that transfer heat from the nuclear reactor to generate electricity. The new generators, built by Mitsubishi Heavy Industries, were supposed to extend the plant's life by decades.

On January 31, 2012, operators detected a small radiation leak in Unit 3's new steam generator. The plant was immediately shut down for inspection. What they found was shocking: unprecedented tube wear in the brand-new generators, with some tubes degraded by 90% after just two years of operation. The cause was a phenomenon called fluid elastic instability—essentially, the tubes were vibrating themselves to death. Mitsubishi's design had failed catastrophically.

The political firestorm was immediate. Senator Barbara Boxer called for permanent closure, citing safety concerns. Anti-nuclear activists, energized by Japan's Fukushima disaster a year earlier, organized massive protests. The Nuclear Regulatory Commission launched extensive investigations. Edison found itself trapped between billions in sunk costs and political reality.

On June 7, 2013, Edison announced San Onofre's permanent closure. The financial hit was staggering: $2.2 billion in stranded investments, replacement power costs of $1.3 billion annually, and thousands of lost jobs. But the real cost was strategic—San Onofre had provided 20% of Southern California's power, all carbon-free. Its closure meant burning more natural gas, importing more out-of-state power, and scrambling to build renewable replacements.

The San Onofre debacle forced a strategic pivot. If nuclear was dead, Edison would bet everything on renewables and grid modernization. The company launched one of the largest infrastructure investment programs in its history, spending $4-5 billion annually on capital projects. Smart meters were deployed to all 5 million customers. Distribution circuits were automated. Substations were upgraded for two-way power flow to accommodate rooftop solar.

The renewable energy transformation was remarkable in its speed and scale. In 2003, Edison's power mix was 18% renewable. By 2018, it reached 36%, one of the highest percentages among major U.S. utilities. The company signed power purchase agreements for thousands of megawatts of solar and wind projects in the Mojave Desert and Tehachapi Mountains. Battery storage projects, uneconomical just years earlier, became routine.

California's renewable portfolio standard, requiring utilities to procure increasing percentages of clean energy, provided the regulatory cover for massive investments. Every solar farm and wind project added to Edison's rate base, earning guaranteed returns. The company had learned from the deregulation disaster—working with regulation, not against it, was the path to prosperity.

But this transformation came at a price: customer rates. Edison's average residential rate rose from 13 cents per kilowatt-hour in 2003 to 19 cents by 2018—among the highest in the nation. Industrial customers complained about competitiveness. Consumer advocates accused Edison of "gold-plating" the grid to maximize profits. The California Public Utilities Commission, caught between climate goals and affordability concerns, approved most investments while occasionally trimming Edison's return on equity.

The operational improvements were undeniable. System reliability improved dramatically—customer outage minutes fell by 40% despite aging infrastructure and extreme weather. Edison's workforce productivity increased 30% through technology and process improvements. The company's safety metrics reached record levels, though this achievement would soon ring hollow.

Financially, the recovery was complete by 2015. Edison International's market capitalization exceeded $20 billion, surpassing pre-crisis levels. The dividend grew steadily at 7-10% annually. Earnings per share doubled from post-crisis lows. Wall Street analysts praised Edison's "regulatory constructive" relationship with the CPUC and clear investment runway.

Pedro Pizarro, who succeeded Craver as CEO in 2016, inherited a company that seemed to have everything figured out. A career Edison employee who'd started as a nuclear engineer, Pizarro embodied the company's technocratic culture. His strategic plan, "Clean Energy, Reliable Future," called for investing $4 billion annually through 2020, earning steady returns while advancing California's climate goals. What could possibly disrupt this virtuous cycle?

The answer was already visible in the scorched hills above Santa Barbara, where the Thomas Fire had begun to burn.

VII. The Wildfire Era: Second Existential Crisis (2017-Present)

The camera towers stood like sentinels above Altadena on December 4, 2017, their infrared sensors scanning for smoke plumes. At 6:26 PM, one captured what would become evidence in a corporate nightmare: a flash of light near Edison power lines, then fire racing through drought-stressed chaparral. The Thomas Fire had begun. Over the next 38 days, it would burn 281,893 acres, destroy 1,063 structures, and kill two people. Six weeks later, rain fell on the denuded slopes above Montecito. The resulting debris flows killed 23 more people, including children swept from their beds. In 2017 and 2018, Edison's equipment was blamed for igniting wildfires in the Los Angeles area, resulting in estimated losses of $9.9 billion.

This wasn't supposed to happen anymore. After the 2007 wildfires that devastated San Diego, California utilities had spent billions on vegetation management, weather stations, and system hardening. Edison had its own fire department, meteorologists, and satellite monitoring. Yet here they were again, watching their equipment spark catastrophe in extreme weather conditions that were becoming less extreme and more normal.

The Woolsey Fire followed in November 2018, burning 96,949 acres across Los Angeles and Ventura counties, destroying 1,643 structures, and killing three people. Malibu mansions burned to their foundations. The entire city of Calabasas evacuated. Lady Gaga fled her estate. Gerard Butler posted Instagram photos of his charred home. The images were apocalyptic—but the financial implications for Edison were existential.

California law made this crisis inevitable through a doctrine called inverse condemnation. If utility equipment causes a fire—regardless of negligence, regardless of compliance with every safety regulation—the utility is strictly liable for all damages. It's a legal framework from the 19th century, when utilities were granted monopoly franchises in exchange for absolute responsibility. In an era of climate change and megafires, it had become a corporate death sentence.

The bills started arriving in 2019. Insurance companies, having paid out billions to fire victims, sued Edison for reimbursement. Thousands of individual lawsuits poured in—homeowners, renters, businesses, public agencies. The plaintiff's bar, sensing opportunity, assembled armies of lawyers. Edison's initial estimate of $4.7 billion in liabilities proved optimistic. With this current subrogation claims settlement, increased settlement activity with individual plaintiffs and currently available information, SCE is now establishing a best estimate of total expected losses for the 2017/2018 Wildfire/Mudslide Events litigation of $6.2 billion, the company announced in September 2020. By 2024, that number had climbed again. Edison International raised its estimated losses from 2017 and 2018 wildfires by another $490 million, saying victims were seeking more and higher claims than previously anticipated.

Meanwhile, PG&E's bankruptcy from the Camp Fire sent shockwaves through California's political establishment. The state's largest utility, unable to handle $30 billion in wildfire liabilities, had essentially collapsed. If Edison followed—and San Diego Gas & Electric after that—California's entire electricity system could unravel. Governor Gavin Newsom faced a crisis that threatened both the state's economy and his political future.

The solution emerged from frantic negotiations in Sacramento: Assembly Bill 1054, signed into law on July 12, 2019. On July 12, 2019, Governor Gavin Newsom signed AB 1054 and AB 111 (collectively, the "2019 Wildfire Legislation"). The 2019 Wildfire Legislation enacts a broad set of reforms and programs related to utility-caused wildfires in California, including establishing the California Wildfire Fund ("Fund"). The purpose of the Fund is to provide a source of money to reimburse eligible claims arising from a covered wildfire caused by a utility company that participates in the Fund by assisting in capitalizing the Fund, and undertaking certain other obligations specified in the law.

The mechanics were complex but the concept was simple: create a $21 billion insurance fund that utilities could tap for wildfire damages, funded half by shareholders and half by ratepayers. The new law establishes a Wildfire Fund of up to $21 billion to provide liquidity for utilities to cover eligible, uninsured third-party damage claims resulting from future catastrophic wildfires. The Wildfire Fund created by AB 1054 essentially acts as a supplemental line of credit for private utilities beyond what is covered by their insurance to pay for adjudicated, covered third party-claims arising from catastrophic wildfires ignited by utility equipment. The Wildfire Fund will create a state-backed pool of capital of at least $10.5 billion, which could be increased by contributions from participating utilities to a total of at least $21 billion.

But there was a catch—several catches. Managed by the California Public Utilities Commission (CPUC), the fund shields four of the state's investor-owned utilities, PG&E, SCE, SDG&E, and Bear Valley Electric Service (who joined the fund in 2020) from bankruptcy by reimbursing wildfire costs and expenses exceeding $1 billion. PG&E, SCE, and SDG&E were each required to contribute an initial amount to the fund based on their liabilities and histories of safety, totaling $7.5 billion. The bill anticipated PG&E would be responsible for 64.2%, SCE for 31.5%, and SDG&E for 4.3%.

The political genius of AB 1054 was how it balanced competing interests. In such proceedings, the electric utility bears the burden to demonstrate that its conduct was reasonable in order to pass wildfire costs onto ratepayers, unless it has a valid safety certification for the time period in which the covered wildfire that is the subject of the application ignited. If the utility has that valid safety certification, AB 1054 creates a presumption that the electric utility's conduct was reasonable and shifts the burden to other parties to demonstrate a serious doubt as to the reasonableness of the utility's conduct. Utilities got protection; victims got guaranteed funding; ratepayers got safety improvements.

Edison immediately began its wildfire mitigation transformation. The company spent billions on "system hardening"—replacing bare wires with insulated cables, installing stronger poles, creating fuel breaks around equipment. By 2021, Edison had covered roughly 2,500 miles of transmission lines with insulation, about 25% of overhead distribution lines in high fire risk areas. The company claimed these measures, combined with public safety power shutoffs during extreme weather, reduced catastrophic wildfire probability by 55-65% relative to pre-2018 levels.

The public safety power shutoffs (PSPS) became their own controversy. When Santa Ana winds howled and humidity dropped, Edison would preemptively cut power to hundreds of thousands of customers. The blackouts prevented fires but infuriated residents. Hospitals ran on generators. Food spoiled. Businesses lost millions. The cure sometimes seemed worse than the disease.

The financial recovery from the 2017-2018 fires was slow and painful. Edison International issued approximately $1 billion in equity in 2020 to maintain investment-grade credit ratings while paying settlements. Insurance covered some costs, but shareholders absorbed billions in losses. The company's stock price remained depressed for years as investors grappled with the new reality of wildfire risk.

Then came 2025. On January 7, the Eaton Fire erupted near Altadena during another extreme wind event. The January blaze, which killed 17 people and destroyed 9,414 structures, remains under investigation, but residents already have filed several lawsuits blaming Edison for sparking the conflagration. The devastation was immediate and overwhelming. Historic neighborhoods reduced to ash. The death toll mounting. And once again, attention turned to Edison's equipment.

The wildfire fund that was supposed to solve everything suddenly looked inadequate. "The fund, as of January, had more than $12 billion under management, a spokesperson said, and has so far only reimbursed PG&E for the 2021 Dixie Fire, making it the only utility to date to tap the fund. Michael Wara, an attorney and expert focused on climate policy at Stanford University, said the fund could conceivably be on the hook for $8 to $9 billion if Edison is found responsible for the Eaton Fire — and perhaps more if plaintiffs attorneys prove the power company was negligent, potentially leading to noneconomic pain and suffering damages."

CEO Pedro Pizarro defended the company vigorously, stating that telemetry data showed no electrical anomalies before the fire. But lawsuits poured in anyway. A judge ordered Edison to preserve all evidence. The investigations would take months, maybe years, but the market had already rendered judgment—Edison's stock plummeted 25% in the days after the fire.

The wildfire era had created an impossible equation for Edison. Climate change was making extreme weather more frequent and intense. Urban development pushed deeper into fire-prone wildlands. Drought stressed vegetation into kindling. The company could spend every dollar of profit on system hardening and still not eliminate risk in a landscape primed to burn. Yet under California law, any spark from their equipment meant potentially unlimited liability.

This second existential crisis was different from the energy crisis of 2000-2001. That was about market manipulation and regulatory failure—solvable through political negotiation. Wildfire risk was about physics and climate—forces beyond any boardroom's control. Edison had become a company whose survival depended on wind patterns, rainfall, and the random interaction of power lines with flying debris. It was a business model as fragile as the California ecosystem itself.

VIII. Clean Energy Transformation & Future Strategy (2020s)

The boardroom at Edison International's Rosemead headquarters features floor-to-ceiling windows overlooking the San Gabriel Mountains—the same mountains where power lines snake through chaparral, where wildfire risk haunts every hot, windy day. In 2024, as CEO Pedro Pizarro presented the company's "Reaching Net Zero" strategy to investors, he could see both Edison's past and future in that view: the century-old transmission corridors that built Southern California, and the climate-changed landscape that threatened to destroy it all.

The numbers were staggering. SCE Capital Investment in Safe, Reliable Clean Energy Grid (2024) ~$6 billion—roughly equivalent to building a new Fortune 500 company from scratch every year. This wasn't just maintenance or incremental improvement. This was wholesale transformation of infrastructure built for a different century, different climate, different economy.

The clean energy transition had become Edison's north star, partly by choice, mostly by necessity. California's Senate Bill 100, passed in 2018, mandated that 60% of electricity come from renewable sources by 2030 and 100% from carbon-free sources by 2045. For Edison, this meant fundamentally reimagining what a utility does. No longer would they generate power—that business was largely gone anyway. Instead, they would become the platform enabling everyone else's clean energy ambitions.

Today at Climate Week NYC, Edison International released Reaching Net Zero, a forward-looking analysis that reinforces the urgent need for multisector collaboration, enhanced efficiencies and significant investment in clean firm generation to meet California's goal of net-zero greenhouse gas emissions by 2045. The report wasn't just corporate greenwashing—it was a $100 billion infrastructure blueprint. Electricity demand in SCE's service area is projected to grow 35% faster over the next decade than estimated just two years ago, underscoring the need for accelerated grid readiness.

The challenge was mind-bending. California wanted to electrify everything—cars, trucks, buildings, industrial processes—while simultaneously making electricity 100% carbon-free. It was like rebuilding a plane while flying it, during a thunderstorm, with passengers demanding lower fares. Every electric vehicle added to the grid increased demand. Every rooftop solar panel added complexity. Every battery storage system required new software, new interconnection protocols, new rate structures.

Edison's strategy centered on three pillars: grid hardening for wildfire resilience, massive capacity expansion for electrification, and sophisticated orchestration of distributed resources. The company was essentially building three grids simultaneously—the physical grid of wires and transformers, the digital grid of sensors and software, and the market grid of prices and incentives.

The transportation electrification opportunity was particularly massive. Southern California had 12 million vehicles that would eventually need to go electric. Each EV was essentially a rolling battery that could either stress the grid (if everyone charged at 6 PM) or support it (through managed charging and vehicle-to-grid technology). Edison launched programs to install thousands of charging stations, offered time-of-use rates to incentivize off-peak charging, and partnered with automakers on grid integration.

Building electrification presented different challenges. Natural gas had heated Southern California homes for a century—cheap, reliable, with infrastructure already in place. Convincing customers to switch to electric heat pumps required not just rate design but cultural change. Edison launched demonstration projects, offered rebates, and worked with contractors to build expertise in heat pump installation. The economics were improving—heat pumps were three times more efficient than gas furnaces—but the transition would take decades.

The distributed energy revolution was perhaps most disruptive. SCE enabled ~1,000 MW of demand response program peak load reduction to help prevent rotating outages during times of grid stress and/or high energy prices. Virtual power plants—aggregations of home batteries, smart thermostats, and EV chargers—could provide the same services as traditional power plants. Edison had to evolve from controlling a few dozen large generators to orchestrating millions of small ones.

Battery storage was the game-changer everyone had waited for. Lithium-ion battery costs had fallen 90% in a decade, making grid-scale storage economically viable. Edison contracted for thousands of megawatts of battery capacity, turning the intermittent renewable grid into something that could provide power after sunset. The largest projects were stunning in scale—hundreds of shipping containers filled with batteries, capable of powering small cities.

But the clean energy transition wasn't just about technology—it was about equity. California's environmental justice movement had long pointed out that poor communities bore the brunt of pollution while wealthy communities installed solar panels. Edison created programs specifically for disadvantaged communities—community solar projects, subsidized electrification retrofits, workforce development for clean energy jobs. The company understood that the transition would fail politically if it wasn't inclusive.

The regulatory framework evolved to support these investments. The California Public Utilities Commission approved most of Edison's capital spending requests, understanding that grid investment was essential for meeting state climate goals. But they also pressed on affordability. Residential electricity rates had reached 32 cents per kilowatt-hour by 2024, among the highest in the nation. Every dollar spent on grid modernization showed up on customer bills.

The financial model was shifting too. Traditional utility investing was about steady, predictable returns from long-lived assets. The clean energy grid required more frequent technology refreshes, more software investment, more uncertainty about asset utilization. Edison had to convince investors that spending billions on infrastructure for an uncertain future would generate adequate returns.

By 2045, even accounting for the infrastructure investment necessary for a safe, clean and reliable grid, SCE customers will see their total energy costs reduced by 40%, due to reduced or eliminated fossil-fuel expenses. This was the grand bargain—higher electricity rates now for lower total energy costs later, as gasoline and natural gas were eliminated from the economy.

The wildfire overlay complicated everything. Every infrastructure investment had to be evaluated through the wildfire lens. Undergrounding power lines in high-risk areas cost $3-5 million per mile but eliminated ignition risk. Covered conductors were cheaper but less effective. Microgrids could island communities during public safety power shutoffs but added complexity. The company spent billions on wildfire mitigation that produced no revenue, only reduced liability.

Climate adaptation became as important as emissions reduction. In 2022, Edison International published Adapting for Tomorrow, which shares key findings from SCEs Climate Adaptation Vulnerability Assessment and calls for increased collaboration between public and private stakeholders to successfully adapt while transitioning to a clean energy future that can be equitable for all. Rising temperatures stressed equipment. Extreme weather events were more frequent and severe. Sea level rise threatened coastal substations. The infrastructure built for 20th-century weather patterns was increasingly inadequate.

By 2024, Edison's clean energy transformation was well underway but far from complete. SCE delivered 49% carbon-free power in terms of retail sales to customers, 67% cleaner than the national average GHG intensity among utilities. The company had become California's largest purchaser of renewable energy, its grid the platform for the state's climate ambitions. But the hardest work lay ahead—the last 50% of decarbonization would be far more difficult than the first 50%.

The existential question remained: Could a 138-year-old utility transform fast enough to meet the moment? Climate change wasn't waiting for regulatory proceedings or rate cases. The energy transition wasn't slowing for wildfire seasons or bankruptcy fears. Edison was racing against physics, politics, and its own institutional inertia. The clean energy future California envisioned depended on Edison succeeding. The alternative—grid failure, economic disruption, climate catastrophe—was unthinkable.

IX. Playbook: Lessons in Regulated Monopoly Management

The conference room in Sacramento was packed with utility executives from across the country, all trying to understand how Edison International had survived crises that should have killed it. Pedro Pizarro stood at the podium, looking tired but determined. "Everyone wants to know our secret," he began. "The truth is, there is no secret. There's only the playbook we've developed through pain, mistakes, and occasional luck. Today, I'll share what actually works in this business."

Lesson One: The Regulator Is Your Real Board of Directors

In theory, Edison answers to its shareholders. In practice, the California Public Utilities Commission controls essentially every major decision. Rate cases determine revenue. Safety certifications determine liability. Infrastructure approvals determine strategy. The CPUC's five commissioners, appointed by the governor, wield more power over Edison's future than its actual board.

The key insight: treat regulatory management as the core business function, not a support activity. Edison employs hundreds of regulatory professionals—lawyers, economists, engineers, policy experts. They produce rate cases that run tens of thousands of pages, supported by elaborate models and testimony from dozens of expert witnesses. A single paragraph in a regulatory decision can mean hundreds of millions in revenue or costs.

But the real work happens outside formal proceedings. Edison executives maintain constant dialogue with commissioners and staff. They preview major initiatives, socialize new concepts, build consensus before filing formal applications. When wildfire liability threatened to destroy the company, Edison's regulatory team essentially lived in Sacramento, crafting the legislative solution that became AB 1054.

The company learned to speak regulator—framing every proposal in terms of public benefit, safety improvement, and alignment with state policy goals. Return on equity was never the lead argument; it was the necessary consequence of serving the public good. This wasn't cynicism—it was survival.

Lesson Two: Political Capital Is Real Capital

Edison spends approximately $3 million annually on lobbying in California—a rounding error compared to its $17 billion in revenue, but arguably its highest-return investment. The company's political action committee contributes to candidates across the spectrum. Edison executives serve on civic boards, sponsor community events, and maintain relationships with mayors, assemblymembers, and members of Congress.

When crisis hit—whether the 2001 energy crisis or 2018 wildfire liability—these relationships mattered more than any financial metric. Politicians who knew Edison's local management, who'd seen the company's community involvement, were more likely to support solutions that kept Edison viable. The company wasn't just a corporation; it was a constituent, employer, and civic institution.

The sophistication of Edison's political operation would surprise those who think of utilities as stodgy. The company polls public opinion, tests messages, coordinates with allied organizations. When opposing rooftop solar subsidies that shifted costs to non-solar customers, Edison partnered with consumer advocates and framed the issue as equity, not profits. When supporting wildfire legislation, they mobilized labor unions, business groups, and local governments.

Lesson Three: Infrastructure Investment Is the Only Real Moat

In the age of disruption, Edison's protection isn't technology or talent—it's $30 billion of poles, wires, transformers, and substations. Distributed energy, rooftop solar, and microgrids might nibble at the edges, but nobody's going to replicate Edison's infrastructure. The grid is the ultimate network effect, more valuable as more connects to it.

The company learned to weaponize infrastructure investment. Every dollar of capital spending earned a regulated return, typically 7-8%. Operating expenses, by contrast, were pass-throughs with no profit. This created an institutional bias toward capital solutions. Why maintain old equipment when you could replace it and earn returns? Why hire employees when you could buy technology and add it to the rate base?

This dynamic drove Edison's massive capital program—$6 billion annually by 2024. Smart meters, distribution automation, grid hardening—all expanded the rate base while ostensibly serving public purposes. Critics called it gold-plating. Edison called it modernization. The CPUC mostly approved it, understanding that California's clean energy goals required massive infrastructure investment.

Lesson Four: Crisis Management Through Financial Engineering

Edison developed a core competency in structuring complex financial solutions to existential threats. The 2001 energy crisis produced the transmission asset sale and dedicated rate component. The wildfire crisis produced AB 1054's insurance fund and cost recovery mechanisms. Each solution involved elaborate financial engineering that balanced stakeholder interests while keeping Edison viable.

The key was creating structures that separated past liabilities from future operations. Securitization—issuing bonds backed by dedicated customer charges—could transform uncertain liabilities into manageable debt service. Trust structures could isolate toxic assets. Regulatory balancing accounts could smooth earnings volatility.

Edison's CFO team became experts in crisis finance. They maintained relationships with every major bank, rating agency, and institutional investor. They could raise billions in capital markets even during crisis, because investors understood the regulatory framework ultimately protected debt holders, if not equity.

Lesson Five: Safety Theater and Actual Safety

After the San Bruno pipeline explosion killed eight people in 2010, California utilities entered the age of safety theater. Every utility now had a "safety-first" culture, a board safety committee, and elaborate safety metrics. Most of it was performative—necessary to maintain regulatory and political support but loosely connected to actual risk reduction.

Edison learned to excel at both safety theater and actual safety. The company's wildfire mitigation plans were masterpieces of bureaucratic comprehensiveness—detailed protocols, sophisticated modeling, extensive documentation. But they also included real risk reduction: vegetation management, system hardening, operational changes that actually reduced ignition probability.

The distinction mattered during investigations. When fires occurred, Edison could demonstrate systematic safety efforts, even if those efforts failed in specific instances. The company had learned from PG&E's mistakes—inadequate documentation, deferred maintenance, and dismissive attitudes toward safety created liability beyond the actual incidents.

Lesson Six: The Dividend Is Sacred Until It Isn't

For 91 years, from 1909 to 2000, Edison paid uninterrupted dividends. Through world wars, depression, and disasters, shareholders received their quarterly payments. This created a virtuous cycle—conservative investors bought utility stocks for income, providing stable capital at low cost, enabling infrastructure investment that generated returns to pay dividends.

The energy crisis shattered this compact. Edison suspended its dividend in 2001, devastating retirees and institutions that depended on utility income. The stock price collapsed. Trust, once broken, took years to rebuild. Edison resumed dividends in 2003 but at lower levels, with conservative payout ratios that preserved financial flexibility.

The lesson: the dividend is a powerful signal but also a dangerous commitment. In regulated utilities, where government ultimately controls revenues, promising specific returns to shareholders creates political risk. Better to under-promise and over-deliver than to cut again.

Lesson Seven: Monopoly Preservation Through Controlled Competition

Edison faced constant threats to its monopoly—municipal takeovers, community choice aggregation, distributed energy resources. The company learned that fighting competition directly was usually futile and politically damaging. Instead, Edison embraced controlled competition that preserved its essential monopoly.

When cities wanted community choice—buying power independently while Edison still delivered it—the company shifted from opposition to accommodation. They'd lost the generation business anyway; better to keep the wires monopoly and avoid hostile takeovers. When rooftop solar threatened load, Edison became a solar developer itself, offering utility-scale solar at lower costs than distributed generation.

The key was defining the irreducible monopoly core—the distribution system—and being flexible about everything else. Let others generate power, provide customer services, or develop new technologies. As long as electricity flowed through Edison's wires, the company collected its returns.

Lesson Eight: Institutional Knowledge as Competitive Advantage

Edison's real asset wasn't technology or even infrastructure—it was institutional knowledge accumulated over 138 years. How to navigate CPUC proceedings. Which legislators mattered for which issues. How to mobilize during emergencies. Where every critical asset was located. This knowledge, embedded in processes and relationships, couldn't be replicated by new entrants.

The company cultivated this advantage through deliberate practices. Extensive documentation of decisions and rationales. Rotation programs that exposed high-potential employees to different functions. Regular engagement between senior executives and junior staff. Hiring from government and hiring to government, creating a revolving door of expertise.

When consultants proposed transformational changes, Edison's institutional antibodies usually rejected them—not from conservatism but from experience. The company had tried most innovations before, understood why they failed, and knew the regulatory and political constraints outsiders missed.

The Meta-Lesson: Utilities Are Political Entities That Happen to Deliver Electricity

The fundamental insight from Edison's playbook is that investor-owned utilities aren't really businesses in the conventional sense. They're quasi-governmental entities with private ownership, political creations that exist at the pleasure of the state. Every important decision—rates, investments, operations—is ultimately political.

This reality shapes everything. Strategy isn't about competitive advantage but regulatory positioning. Success isn't measured by growth or margins but by political sustainability. Leadership isn't about vision but stakeholder management. The executives who thrive understand they're playing a political game with business rules, not a business game with political constraints.

For investors, this means traditional financial analysis has limited value. The key variables aren't market dynamics or competitive position but regulatory philosophy, political climate, and stakeholder alignment. Edison's survival through multiple existential crises proves that in the utility business, political skill matters more than operational excellence.

The playbook, ultimately, is about recognizing what game you're actually playing. Edison survived because it understood earlier than competitors that the regulated monopoly model is fundamentally about political economy, not business strategy. In California's unique environment—aggressive climate goals, powerful regulators, extreme weather, wealthy but demanding customers—this understanding was the difference between survival and bankruptcy.

X. Bear vs. Bull Case Analysis

The investment committee at a major pension fund was in its eighth hour of debate. Edison International was trading at $65, down from recent highs but up from the post-Eaton Fire lows. The wildfire liability questions were unresolved. The clean energy transformation required massive capital. The regulatory environment was shifting. Should they buy, sell, or hold?

The Bull Case: Essential Infrastructure in the Energy Transition

The portfolio manager leading the bull case pulled up a map of Southern California at night—millions of lights from Los Angeles to San Diego, each one dependent on Edison's grid. "This is the ultimate infrastructure monopoly," she began. "Fifteen million people who have no choice but to buy electricity from Edison. California's economy—the world's fifth largest—literally cannot function without this company."

The regulatory framework, she argued, was actually Edison's greatest protection. Yes, the CPUC controlled rates, but they also guaranteed returns. Edison's authorized return on equity of 10.05% was locked in through 2028. With a rate base approaching $40 billion and growing at 6-8% annually, the earnings growth was mechanical, predictable, almost inevitable.

The wildfire liability issue, while serious, had been largely solved through AB 1054. The $21 billion insurance fund provided a buffer against catastrophic losses. More importantly, the presumption of prudency for utilities with safety certifications shifted the burden of proof. Edison had valid safety certifications and had invested billions in system hardening. The probability of bankruptcy-level liability was now remote.

California's clean energy mandate created an investment supercycle that would last decades. The state needed to build essentially an entire new grid to support electrification. Every electric vehicle sold, every heat pump installed, every battery deployed increased electricity demand and justified more infrastructure investment. Edison's rate base could double by 2035, driving earnings growth regardless of economic cycles.

The technology transition actually strengthened Edison's position. Distributed energy resources needed sophisticated grid management—exactly what Edison was building. Rooftop solar customers still needed grid connection for reliability. Battery storage required grid services to monetize. The utility wasn't being disrupted; it was becoming the platform enabling everyone else's innovation.

Climate change, paradoxically, made Edison more valuable. As weather became more extreme, reliable electricity became more critical. Air conditioning during heat waves was life-saving. Electric vehicle charging was essential mobility. The political will to let Edison fail had evaporated—California would do whatever necessary to keep the lights on.

The valuation was compelling. Edison traded at 14 times forward earnings, below historical averages and peer utilities. The dividend yield of 4.5% was well-covered by earnings. With interest rates likely peaking, utility valuations should recover. Patient investors could collect dividends while waiting for multiple expansion.

The Bear Case: Existential Risks in a Burning State

The short seller presenting the bear case had a different map—California's high fire risk areas, overlaid with Edison's service territory. Over 30% of Edison's infrastructure was in zones rated extreme or high fire risk. "This company is one bad wind event from insolvency," he stated flatly.

The Eaton Fire had exposed the wildfire fund's inadequacy. If Edison was found liable—and historically, utilities were almost always found liable when their equipment was involved—the damages could approach $10 billion. The fund had only $12 billion remaining. One more major fire and it would be depleted, leaving Edison naked against unlimited strict liability.

The insurance situation was deteriorating rapidly. Edison's wildfire insurance had already dropped from over $1 billion to under $400 million as insurers fled California. Premiums for remaining coverage had tripled. Soon, Edison would be completely self-insured for wildfire risk—essentially running an insurance company without insurance expertise or adequate reserves.

The political environment was turning hostile. Public power advocates were gaining ground, arguing that for-profit utilities couldn't safely operate in the climate era. San Francisco had already taken over PG&E's local distribution. Other cities were considering similar moves. Municipal takeover of Edison's most profitable service areas would destroy the investment thesis.

Rates were reaching political limits. At 32 cents per kilowatt-hour, Edison's residential rates were double the national average. Every rate increase triggered more rooftop solar adoption, reducing sales to remaining customers and forcing rates even higher—the utility death spiral. Political pressure for rate relief was building, threatening authorized returns.

The clean energy transition was a capital black hole. Edison needed to spend $6 billion annually just to maintain current reliability and safety. Electrification would require billions more. But every dollar of investment increased rates, accelerating customer defection and political opposition. The company was trapped in an investment treadmill it couldn't exit.

Technology disruption was accelerating. Battery costs were falling 20% annually. Solar panels were approaching grid parity even without subsidies. Microgrids could provide reliability without utility connection. Within a decade, large commercial customers could defect entirely, stranding Edison's infrastructure investments.

The regulatory compact was breaking down. The CPUC, under political pressure, was getting tougher on cost recovery. Wildfire costs were increasingly disallowed. The presumption of prudency was being challenged. Future rate cases would be contentious, with authorized returns likely declining.

Climate change was accelerating beyond adaptation capacity. The heat dome that killed hundreds in the Pacific Northwest could hit Southern California. Atmospheric rivers could cause massive flooding. Drought could eliminate hydroelectric generation. Edison was making linear improvements to infrastructure while climate change was creating exponential risks.

The financial flexibility was evaporating. Debt-to-capital ratios were rising. Credit ratings were one notch above junk. The dividend consumed most free cash flow. Any major shock—wildfire liability, regulatory disallowance, economic recession—could force another dividend cut or dilutive equity issuance.

The Synthesis: A Leveraged Bet on California's Future

The committee chair, a veteran of multiple market cycles, offered a synthesis. "Edison International is essentially a leveraged bet on three propositions: First, that California's political system will continue to support investor-owned utilities despite their problems. Second, that climate change proceeds gradually enough for adaptation. Third, that technological disruption enhances rather than replaces grid value."

The bull case assumed California needed Edison too much to let it fail. The bear case assumed the risks had become too large for any corporate structure to bear. Both were partially right. Edison would likely survive but in a fundamentally different form—more regulated, less profitable, essentially a government-sponsored enterprise with traded equity.

For investors, the question wasn't whether Edison was a good company—it was what kind of investment it represented. For conservative income investors, the dividend yield was attractive but the risk of cut was real. For growth investors, the rate base expansion was compelling but regulatory constraints limited upside. For ESG investors, the clean energy story was powerful but wildfire liability was problematic.

The committee ultimately decided to maintain but not increase their position. Edison International represented a complex bet on regulatory politics, climate adaptation, and technological change—forces beyond any investor's ability to fully analyze or predict. In a world of uncertainty, the only certainty was that Edison's next century would look nothing like its last.

XI. Epilogue: What Would We Do?

If you gave us control of Edison International tomorrow—handed us the keys to this $28.7 billion market cap utility with its 138-year history and existential challenges—what would we actually do? Not the consultant's PowerPoint version, but the real, messy, politically feasible actions that might actually work?

First, we'd acknowledge a hard truth: the investor-owned utility model as currently structured is probably broken beyond repair in the climate change era. The combination of strict liability for wildfire damages, obligation to serve all customers, and requirement to earn returns for shareholders creates an impossible trinity. Something has to give.

The most elegant solution would be converting Edison into a customer-owned cooperative or public power entity, eliminating the profit motive while maintaining operational expertise. But that's politically impossible—California can't afford to buy out Edison's shareholders at fair value, and confiscation would destroy the state's ability to access capital markets. So we need to work within the existing framework while fundamentally restructuring incentives.

We'd propose "California Utility 3.0"—a new regulatory compact for the climate era. The state would provide true wildfire liability protection, not just the inadequate insurance fund. In exchange, Edison would accept lower but guaranteed returns, essentially becoming a regulated infrastructure fund. Think of it as the utility equivalent of a toll road—boring, stable, predictable returns for boring, stable, predictable service.

The wildfire problem requires radical surgery. We'd separate Edison into two entities: GridCo, which owns and operates the distribution system in low-fire-risk urban areas, and FireCo, which operates in high-risk zones. FireCo would be jointly owned by Edison and the state, with explicit liability sharing. The state has better access to emergency funding and disaster relief; Edison has operational expertise. Share the risk, share the responsibility.

On technology, we'd stop fighting the future and start building for it. Every customer would become a potential generator, storage provider, and grid service supplier. We'd create an open platform—like iOS for electricity—where third parties could build applications on top of Edison's infrastructure. Let Tesla manage vehicle-to-grid programs. Let Google optimize home energy management. Let Amazon aggregate distributed resources. Edison would charge platform fees, not fight innovation.

The rate structure needs complete overhaul. The current system where volumetric charges cover fixed costs creates perverse incentives and inequity. We'd move to a subscription model—customers pay for grid connection based on their peak demand, then pay market prices for energy. Like Netflix for electricity. This would stabilize Edison's revenue while giving customers price signals to shift consumption.

For clean energy, we'd get out of the procurement business entirely. California has sophisticated energy markets; let them work. Edison should focus on what only it can do—build and operate the distribution grid. Let competitive markets handle generation, storage, and customer services. This would eliminate conflicts of interest and reduce regulatory complexity.

The workforce transformation would be massive and politically sensitive. Edison has 13,000 employees, many in unions with strong political connections. We'd negotiate a grand bargain: guaranteed employment for current workers who retrain for new roles, generous early retirement for those who won't, and aggressive hiring from communities hosting Edison infrastructure. The utility jobs of the future—grid operators, data analysts, customer experience designers—would look nothing like traditional utility roles.

On wildfire mitigation, we'd stop pretending we can engineer away all risk. Some areas are simply too dangerous for overhead power lines. We'd propose systematic undergrounding in highest-risk zones, funded by a combination of state climate resilience funds, federal infrastructure money, and long-term utility bonds. Yes, it would cost $50 billion over 20 years. That's still cheaper than burning down Paradise or Malibu every few years.

We'd radically increase transparency. Every wildfire risk model, every rate case assumption, every infrastructure investment decision would be public. Create a real-time dashboard showing system conditions, spending, and performance. Sunlight is the best disinfectant, and utilities have operated in darkness too long. This would build public trust and reduce regulatory friction.

The political strategy would shift from defense to offense. Instead of fighting municipal takeovers, we'd offer partnership agreements—cities could have more control over local energy decisions while Edison maintained economies of scale. Instead of opposing distributed energy, we'd become its biggest advocate, but on terms that fairly compensate grid services.

Most radically, we'd propose making Edison's equity returns contingent on meeting California's climate goals. If the state achieves its 2030 renewable targets, shareholders get bonus returns. If wildfire damages exceed thresholds, returns get cut. Align incentives with public policy objectives. Make Edison's success literally dependent on California's success.

None of this would be easy. The regulatory proceedings would take years. The political battles would be fierce. The implementation challenges would be enormous. But the alternative—stumbling from crisis to crisis, patching a broken model, hoping climate change slows down—is worse.

The meta-lesson from Edison's history is that utilities reflect their societies. The Edison that electrified Los Angeles's movie studios embodied 20th-century industrial ambition. Today's Edison, caught between climate catastrophe and clean energy transformation, embodies 21st-century contradictions. Tomorrow's Edison—whatever form it takes—will embody society's response to existential challenges.