Duke Energy: From Southern Power to America's Energy Giant

I. Introduction & Episode Roadmap

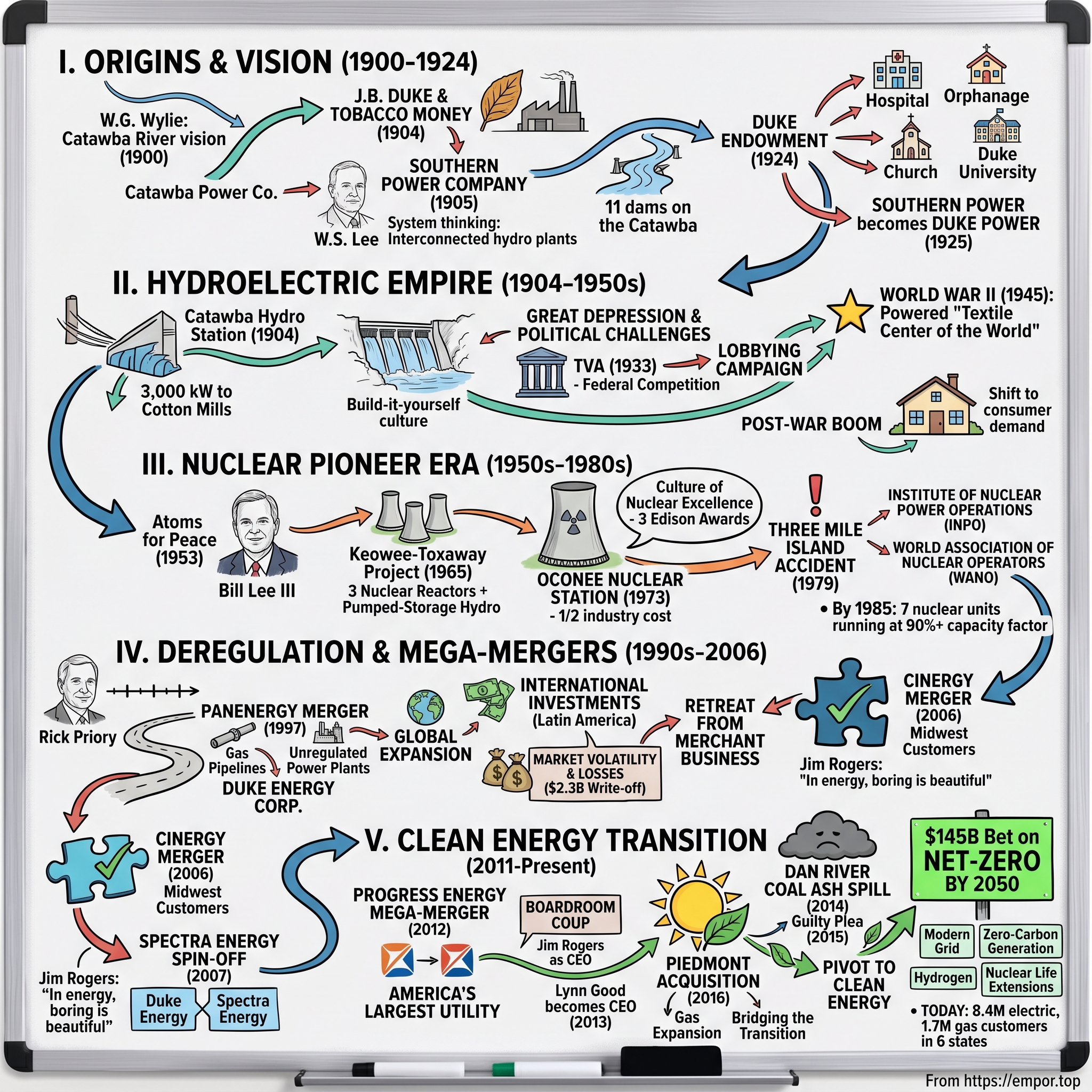

Picture Charlotte, North Carolina, on a humid August morning in 2024. From the 48th floor of Duke Energy Plaza, you can see the Catawba River snaking through the Piedmont—the same river that, 120 years ago, sparked an industrial revolution in the American South. Today, that view belongs to the executives of Duke Energy, a Fortune 150 behemoth with $30 billion in annual revenues, serving 8.4 million electric customers across six states and 1.7 million natural gas customers. It's America's second-largest investor-owned utility by market capitalization, worth roughly $97 billion.

But here's the remarkable part: this empire began with a simple observation by a textile mill owner named Walker Gill Wylie. He noticed that the Catawba River's rushing waters could power more than just a single mill wheel. What if, he wondered, you could harness an entire river system to electrify the South? That question would catch the attention of James Buchanan "Buck" Duke—yes, that Duke, the cigarette magnate whose tobacco fortune would transform into something far more enduring than smoke.

How does a regional hydroelectric startup, funded by tobacco money and born from the post-Reconstruction South's industrial ambitions, evolve into one of America's energy giants? How does a company navigate from water wheels to nuclear reactors, from regulated monopoly to deregulation and back again, from coal-fired baseload to a $145 billion bet on clean energy transition?

This is a story of patient capital meeting infrastructure ambition, of family fortunes reshaping regions, of nuclear pioneers and merger dramas, of environmental disasters and regulatory chess matches. It's about a company that has powered the Southeast's transformation from agrarian backwater to economic powerhouse, while simultaneously grappling with its role in climate change—both as contributor and, potentially, as solution.

We'll trace Duke Energy's journey through five distinct eras: the hydroelectric pioneering days under the Duke brothers' patronage, the post-war nuclear ambitions that made it an industry leader, the deregulation adventures that nearly destroyed it, the mega-mergers that created today's footprint, and the current $145 billion gamble on clean energy transformation. Along the way, we'll unpack the business model of a regulated utility—how it makes money, why Warren Buffett loves these assets, and what makes Duke both boring and fascinating to investors.

The themes we'll explore resonate far beyond utilities: the power of vertical integration, the challenge of managing regulated monopolies, the art of multi-decade capital allocation, and the delicate dance between public service and shareholder returns. We'll see how Duke Energy became both the villain in coal ash spills and the hero in hurricane recoveries, how it's simultaneously betting on natural gas as a "bridge fuel" while promising net-zero emissions by 2050.

II. The Tobacco Duke Origins & Founding Vision (1900–1924)

The story begins not in a boardroom but in a cotton mill along North Carolina's Catawba River in 1900. Walker Gill Wylie, a physician-turned-industrialist, stood watching the river's relentless current and saw something revolutionary: untapped power that could transform the agrarian South into an industrial competitor. Together with his brother, Dr. Robert Wylie, he financed the region's first hydroelectric station through their newly formed Catawba Power Company. But they needed something the South desperately lacked—capital, and lots of it.

Enter James Buchanan "Buck" Duke, a man who had literally mechanized addiction. By 1900, Duke had conquered the cigarette industry through a simple innovation: the Bonsack cigarette-rolling machine, which could produce 120,000 cigarettes per day compared to the 3,000 a skilled worker could hand-roll. His American Tobacco Company controlled 90% of the U.S. cigarette market, generating profits that needed reinvestment. When the Wylie brothers approached him in 1904 with their vision of an electrified South, Duke saw more than a business opportunity—he saw regional transformation.

"I've been all over the South," Duke reportedly told his associates, "and I know of no other place where water power can be so cheaply and extensively developed." He wasn't just talking about building power plants; he envisioned an integrated system that would fundamentally alter the South's economic trajectory. The region's heavy dependence on agriculture, Duke believed, was a prison that only industrialization could unlock. And industrialization required power—reliable, abundant, cheap power.

In 1905, Duke invested $1 million (roughly $34 million in today's dollars) to create the Southern Power Company, with W.S. Lee as chief engineer. Lee wasn't just any engineer—he was a visionary who understood that hydroelectric development wasn't about individual dams but about river systems. His plan for the Catawba was audacious: eleven interconnected plants along a 225-mile stretch, each dam creating a reservoir that would regulate flow for the next downstream. It was systems thinking applied to geography, decades before that became a management buzzword.

The early customers weren't households—they were textile mills. Duke deliberately favored industrial uses, offering power at rates that undercut steam engines. By 1910, Southern Power was serving 66 cotton mills across the Carolinas. The company didn't just sell electricity; it sold industrial transformation. Mill owners could now locate factories near labor rather than near coal deposits or river falls. Towns sprang up around these electrified mills: Gastonia, Kannapolis, Concord—the landscape of the New South literally powered into existence.

But Duke's vision extended beyond business. When he established the Duke Endowment in 1924 with $40 million (his entire fortune would eventually fund it with $100 million), he specified that annual income should support hospitals, orphanages, rural Methodist churches, and universities—including a small Methodist school called Trinity College that would become Duke University. The endowment owned significant Duke Power stock, creating a perpetual funding mechanism where the region's electrification would finance its education and healthcare.

The tobacco fortune had found its redemption in kilowatts. When Buck Duke died in 1925, the company he'd funded had 18 hydro plants generating 300,000 kilowatts, serving 278 communities. More importantly, it had established a model: patient capital building regional infrastructure, creating demand while supplying it, and viewing profit not as an end but as means to regional development. That same year, Southern Power became Duke Power Company, cementing the family name not on cigarette packs but on the utility bills of millions of Southerners.

III. Building the Hydroelectric Empire (1904–1950s)

On a foggy morning in April 1904, the turbines at Catawba Hydro Station began their first rotation, sending 3,000 kilowatts of power to Victoria Cotton Mills in Rock Hill, South Carolina. The workers who flipped that inaugural switch couldn't have imagined they were launching what would become the most sophisticated hydroelectric system in America. But W.S. Lee, Duke Power's chief engineer, knew exactly what he was building: not just a power plant, but an industrial revolution delivered by wire.

Lee's engineering philosophy was radical for its time—"do-it-yourself" construction that rejected the industry's reliance on outside contractors. Duke Power's crews built their own dams, poured their own concrete, and even manufactured their own equipment when necessary. This wasn't just cost-saving; it was knowledge accumulation. Every project taught lessons that improved the next. When the Great Falls development came in at half the projected cost in 1907, it wasn't luck—it was institutional learning made concrete.

The Catawba River development represented something unprecedented in American infrastructure: a single company controlling an entire river system. By 1928, Duke Power operated 10 major dams creating a 220-mile chain of lakes from Bridgewater to Wateree. Each reservoir became the regulating pool for the station below, turning the river's seasonal floods and droughts into steady, predictable power. The system could generate 700,000 kilowatts—enough to power every textile spindle from Virginia to Georgia.

Then came the Great Depression, and Duke Power discovered that being a monopoly during economic collapse made you everyone's favorite villain. Politicians who had celebrated electrification now campaigned against "the power trust." When Franklin Roosevelt created the Tennessee Valley Authority in 1933, offering government-generated electricity at subsidized rates, Duke Power faced its first existential threat. The company fought back through what internal documents called "an educational campaign"—funding local newspapers, organizing community groups, and lobbying intensively against federal power projects.

The battle over Mountain Island Shoals became Duke's Stalingrad. When the Public Works Administration proposed building a competing federal dam on the Catawba in 1934, Duke Power mobilized every political connection. Company president E.C. Marshall personally lobbied Interior Secretary Harold Ickes, arguing that government competition would destroy private investment in the South. The strategy worked—barely. The PWA abandoned the project in 1935, but the message was clear: Duke Power's monopoly existed at the pleasure of politics.

During World War II, Duke Power's industrial focus paid strategic dividends. The company's reliable power supply enabled the Carolinas to become the "Textile Center of the World," producing millions of uniforms, parachutes, and tents. The Aluminum Company of America located its massive smelters in the Duke Power territory specifically for the cheap, abundant electricity. By 1945, Duke was supplying 1.2 million kilowatts to the war effort—power that helped win battles from Normandy to Iwo Jima.

The post-war boom brought a different challenge: residential demand. Suddenly, every returning GI wanted electric appliances—refrigerators, washing machines, television sets. Duke Power, which had built its empire serving cotton mills, had to transform into a consumer company. The shift required not just new generating capacity but new thinking. The company launched "Live Better Electrically" campaigns, offered financing for home appliances, and even operated demonstration kitchens where housewives could learn to cook on electric ranges.

By 1950, Duke Power faced a crossroads. The best hydroelectric sites were developed. Coal plants were the obvious next step, but company leadership saw further ahead. In 1953, President Eisenhower's "Atoms for Peace" speech sparked imaginations in Charlotte. Nuclear power promised something hydroelectric delivered—massive baseload generation without fuel costs. It was a technology that required patient capital, engineering excellence, and regulatory navigation. In other words, it was perfect for Duke Power's DNA.

IV. The Nuclear Pioneer Era (1950s–1980s)

In March 1965, Bill Lee III—grandson of Duke Power's founding chief engineer—stood before a scale model of what would become America's most ambitious nuclear project. At 36, Lee was already the company's vice president of engineering, handpicked to lead Duke Power into the atomic age. His vision: the Keowee-Toxaway Project, a marvel of integrated engineering that would combine three nuclear reactors with the world's largest pumped-storage hydroelectric facility. "We're not just building a power plant," Lee told his team. "We're proving nuclear can be done right—on time, on budget, and safer than anyone imagines possible."

The first nuclear project, the Keowee-Toxaway Project, was launched in 1965. The project added the company's first nuclear plant and a pumped-storage hydro plant. The nuclear plant was completed in seven years – at a cost less than half the industry average. This wasn't hyperbole—it was prophecy. While the rest of the industry averaged 10-12 years and massive cost overruns for nuclear construction, Duke Power brought Oconee Nuclear Station online in 1973 for $500 million, roughly half what competitors spent on similar projects.

The secret lay in Duke's DNA—that same "do-it-yourself" engineering culture that had built the Catawba dams. Duke Power didn't hire contractors to build its nuclear plants; it built them itself, accumulating knowledge with every weld, every concrete pour, every cable pull. The project earned Duke Power its first of three Edison Awards, the power industry's highest honor. The company would earn two more Edison Awards—an unprecedented achievement that established Duke as the gold standard in nuclear operations.

But Lee's greatest moment came not from success but from crisis. On March 28, 1979, at 4:00 AM, a stuck valve at Pennsylvania's Three Mile Island triggered America's worst nuclear accident. As panic spread and the industry reeled, Duke Power President Bill Lee led the creation of the Institute of Nuclear Power Operations, which strengthened and standardized the industry's nuclear safety and training programs. Lee didn't just respond to Three Mile Island—he transformed it into a catalyst for industry-wide reform.

When the Three Mile Island Nuclear accident occurred in 1979, Lee led the recovery efforts, shutting down and stabilizing the reactor. He also worked long and hard to ease public concerns and make sure that a similar accident would not occur again. Within months, Lee had convinced every nuclear operator in America to join the Institute of Nuclear Power Operations (INPO), creating unprecedented information sharing and standardized safety protocols. When Chernobyl melted down in 1986, Lee was also an initiator of the World Association of Nuclear Operators, in the wake of the Chernobyl disaster, becoming its first president.

Duke's nuclear excellence wasn't limited to crisis management. By 1985, the company operated seven nuclear units across the Carolinas—Oconee's three units, McGuire's two units near Charlotte, and Catawba's two units on the South Carolina border. These plants ran at capacity factors exceeding 90%, meaning they generated power more than 90% of the time—remarkable reliability in an industry where 75% was considered good. Duke Energy's nuclear plants generate about half of the electricity for our customers in the Carolinas, with production costs among the lowest in the nation.

The financial model was elegant: massive upfront capital investment (each plant cost $1-2 billion in 1970s dollars) but minimal fuel costs once operational. A single uranium pellet the size of a fingertip contained as much energy as a ton of coal. Duke's nuclear fleet could run for 18-24 months between refuelings, providing the baseload power that enabled the Carolinas' economic transformation. Between 1970 and 1990, the region's GDP tripled, powered quite literally by Duke's atoms.

Yet nuclear's promise came with unique challenges. The Nuclear Regulatory Commission's oversight was unprecedented—Duke Power employed more lawyers and compliance officers for its nuclear operations than for all its other generation combined. Every modification, no matter how minor, required months of regulatory review. After Three Mile Island, new safety requirements added billions in retrofit costs. Plants designed for 40-year licenses now needed to prove they could safely operate for 60 or even 80 years.

Bill Lee understood these challenges intimately. Being named the Utility CEO of the Year four times by Financial World, he navigated Duke Power through nuclear's golden age and its darkest moments. When he retired as CEO in 1994, Duke's nuclear fleet was among the nation's best-performing, setting capacity and safety records that stand today. His legacy wasn't just the plants themselves but the culture of nuclear excellence—a DNA strand that would prove crucial as Duke Energy faced the 21st century's energy transition.

V. Deregulation, Expansion & Transformation (1990s–2006)

The boardroom at Duke Power's Charlotte headquarters crackled with tension in early 1997. CEO Rick Priory faced a decision that would either transform Duke into a national energy powerhouse or destroy a century of careful cultivation. Deregulation was sweeping through the energy industry like wildfire—California had just opened its electricity markets, and Wall Street was demanding utilities become "energy merchants" or face obsolescence. "Gentlemen," Priory announced, "we're merging with PanEnergy."

PanEnergy wasn't a utility—it was a Houston-based natural gas pipeline company that had surfed deregulation's first wave when gas markets opened in the 1980s. The $7.7 billion stock swap created Duke Energy Corporation, a name change that signaled ambitions far beyond the Carolinas. Duke Power merged with PanEnergy, a natural gas company, in 1997 to form Duke Energy. Suddenly, Duke owned 17,000 miles of natural gas pipelines stretching from the Gulf Coast to the Great Lakes, plus a portfolio of unregulated power plants from California to Maine.

The late 1990s became Duke Energy's gold rush era. The company built merchant power plants—unregulated facilities that sold electricity at market prices rather than regulated rates. Duke Energy North America, the new trading and generation subsidiary, constructed 4,000 megawatts of natural gas plants in two years, betting that deregulated markets would reward efficient generators. Trading floors sprouted in Charlotte and Houston, where Duke's energy traders bought and sold electricity and gas like stocks and bonds.

International expansion followed the same aggressive playbook. Duke Energy International acquired power plants in Latin America, launching operations in Brazil, Argentina, Peru, Ecuador, and Guatemala. The company paid $1.5 billion for Brazil's Paranapanema generating complex, betting that Latin America's growing economies needed American expertise to modernize their grids. By 2000, Duke Energy operated on four continents, managing $29 billion in assets and generating $49 billion in revenues.

But deregulation's promise concealed brutal realities. When California's electricity crisis exploded in 2000-2001, Duke Energy found itself accused of market manipulation, allegedly withholding power to drive up prices. Though Duke maintained its innocence, it eventually paid $2.5 million to settle charges. The Enron collapse in December 2001 cast a shadow over all energy trading—suddenly, complex financial engineering looked less like innovation and more like fraud.

Duke's international adventures proved equally challenging. Latin American currencies collapsed, governments reneged on contracts, and populist politicians demonized foreign utilities. In 2003, Duke Energy wrote off $2.3 billion in international assets and announced its retreat from overseas markets. The merchant generation business hemorrhaged money as power prices collapsed from oversupply. Duke Energy North America lost $1.2 billion in 2003 alone.

The solution came through consolidation. With the purchase of Cinergy Corporation announced in 2005 and completed on April 3, 2006, Duke Energy Corporation's customer base grew to include the Midwestern United States as well. The $9 billion acquisition of Cincinnati-based Cinergy brought 1.5 million electric customers in Ohio, Indiana, and Kentucky, plus 500,000 gas customers in Ohio. More importantly, it brought 8,000 megawatts of coal-fired generation in the Midwest—reliable, regulated assets that generated steady returns.

The Cinergy merger marked Duke's return to its roots: regulated utilities with predictable earnings. CEO Jim Rogers, who came from Cinergy, articulated the new philosophy: "The best business model in energy isn't the highest return—it's the most sustainable return." Duke sold its merchant plants, exited trading, and spun off its natural gas pipelines as Spectra Energy in 2007. On January 3, 2007, Duke Energy spun off its gas business to form Spectra Energy. Duke Energy shareholders received 1 share of Spectra Energy for each 2 shares of Duke Energy.

The transformation from swashbuckling energy merchant back to boring utility destroyed billions in shareholder value—Duke's stock fell from $45 in 2000 to $15 in 2003. But it also taught invaluable lessons about the limits of deregulation and the enduring value of regulated monopolies. As Rogers would say, "In energy, boring is beautiful."

VI. The Progress Energy Mega-Merger (2011–2012)

The PowerPoint slide on the conference room screen showed two companies becoming one: Duke Energy's service territory in blue, Progress Energy's in green, creating an unbroken swath from Ohio to Florida. It was January 10, 2011, and Duke CEO Jim Rogers was selling his board on the biggest utility merger in American history. "This isn't just about scale," Rogers argued. "It's about having the balance sheet to fund the energy transition. Separately, we're regional players. Together, we're a national platform."

The numbers were staggering: Duke would acquire Progress Energy for $13.7 billion in stock, with Progress shareholders receiving 2.6125 Duke shares for each Progress share. Duke would also assume $12.2 billion of Progress debt, creating a combined entity worth $65 billion. The new Duke Energy would serve 7.1 million customers across six states, operate 57,000 megawatts of generation, and become America's largest utility by customers served.

Progress Energy brought assets Duke desperately wanted: four nuclear plants in the Carolinas and Florida, a younger coal fleet with better emissions controls, and most crucially, regulatory relationships in Florida, where electricity demand was growing faster than anywhere in Duke's territory. Progress CEO Bill Johnson would become CEO of the combined company, with Rogers serving as executive chairman before retirement.

Or so everyone thought.

July 2, 2012—merger closing day—turned into one of the most dramatic boardroom coups in corporate history. The combined board met, as planned, to formally elect Bill Johnson as CEO. But within hours, Johnson was out, and Jim Rogers was CEO of the combined company. The official explanation: the board had lost confidence in Johnson's ability to lead the integration. The reality was more complex—a power struggle that had been brewing since merger talks began.

Johnson walked away with a $44 million severance package, but the damage to Duke's reputation was severe. North Carolina regulators launched investigations, shareholders filed lawsuits, and corporate governance experts called it one of the worst-handled successions in corporate America. The Wall Street Journal dubbed it the "shortest CEO tenure in history"—Johnson had technically been CEO for about 20 minutes.

Yet beneath the drama, the strategic logic remained sound. The merger created massive synergies: $650 million in annual fuel savings from optimizing the combined generation fleet, $300 million from eliminating duplicate corporate functions, and $250 million from joint procurement. The combined company could dispatch power from 31 coal plants, 11 nuclear units, and dozens of gas plants across six states, moving electricity to where it was needed most efficiently.

Regulatory approval came with strings attached. North Carolina required $16.48 million annually in community support programs, $10 million for low-income energy assistance, and $5 million for workforce development. Florida extracted promises to accelerate solar development. Environmental groups, initially opposed, won commitments to retire 6,000 megawatts of old coal plants by 2020.

The real revelation came from combining Duke's and Progress's nuclear fleets. Together, they operated 11 reactors in the Carolinas—the densest concentration of nuclear power in America. These plants, all built in the 1970s and 1980s, could run for decades more with proper maintenance. In an era when new nuclear construction was virtually impossible, this fleet became Duke's secret weapon—carbon-free baseload that competitors couldn't replicate.

Rogers, despite the succession controversy, pressed forward with his vision: Duke Energy as the utility of the future, big enough to fund massive infrastructure investments, sophisticated enough to manage complex regulations, and committed enough to navigate the energy transition. "Scale matters in utilities," he'd tell investors. "You need size to spread the costs of environmental compliance, grid modernization, and new technology development."

By 2013, the integration was largely complete. The combined Duke Energy generated $24 billion in revenues, employed 28,000 people, and had a market capitalization approaching $50 billion. The boardroom drama faded as financial results improved. Rogers retired in 2013, succeeded by Lynn Good, Duke's CFO who had navigated the company through the merger chaos. Her appointment signaled stability after turbulence—exactly what Duke needed as it faced the next challenge: the accelerating transition from coal to cleaner energy sources.

VII. The Piedmont Acquisition & Gas Expansion (2016)

Lynn Good stood before a map of the Southeast in Duke Energy's war room in Charlotte, October 2015. Red dots marked Duke's electric operations, but vast white spaces showed where the company had no presence—particularly in natural gas distribution. "We're fighting the energy transition with one hand tied behind our back," she told her strategy team. "Our competitors have both electric and gas. We need both to manage the transition efficiently."

In October 2016, Duke Energy acquired Piedmont Natural Gas for $4.9 billion in cash, adding 1 million natural gas customers in North Carolina, South Carolina, and Tennessee. But this wasn't just about adding customers—it was about positioning for a fundamental shift in energy economics. Natural gas prices had collapsed from $13 per million BTU in 2008 to under $3 in 2016, thanks to the fracking revolution. Gas was displacing coal for electricity generation, and Duke needed to own both sides of that transition.

Piedmont Natural Gas was a 115-year-old company with an enviable franchise: monopoly gas distribution rights in some of the Southeast's fastest-growing cities—Charlotte, Nashville, Raleigh. Its 22,000 miles of distribution pipes and 1,400 miles of transmission pipelines formed critical infrastructure that would take decades and billions to replicate. More intriguingly, Piedmont had been quietly investing in compressed natural gas (CNG) fueling stations for vehicle fleets, anticipating a shift from diesel to gas in trucking.

The strategic logic went deeper than diversification. Duke was retiring coal plants and building gas-fired replacements—but it had to buy that gas from third parties at volatile prices. Owning gas infrastructure meant Duke could better manage fuel costs, hedge price risks, and capture more of the value chain. In regulatory proceedings, Duke could now argue for integrated resource planning—optimizing electric and gas systems together for customer benefit.

The integration revealed unexpected synergies. Duke and Piedmont shared overlapping service territories but had maintained separate call centers, billing systems, and field crews. Combining operations saved $100 million annually. More importantly, Duke could now offer dual-fuel options to industrial customers—critical for factories that needed both electricity and gas for process heat. The company won several large manufacturing projects by guaranteeing both energy sources.

Gas also provided a bridge to Duke's renewable ambitions. Natural gas plants could ramp up and down in minutes, compensating for solar and wind's intermittency. Duke's new combined-cycle gas plants achieved 60% efficiency—far better than coal's 35%—while producing half the carbon emissions. The company marketed this as "cleaner energy," though environmental groups scorned gas as a "bridge to nowhere."

The Piedmont acquisition proved prescient when the Atlantic Coast Pipeline—a $8 billion project to bring Appalachian gas to the Southeast—collapsed in 2020. Duke had been a major partner in that pipeline, planning to use it for fuel supply. With the pipeline dead, owning Piedmont's existing infrastructure became even more valuable. Duke could access multiple gas supply sources through Piedmont's system, avoiding dependence on any single pipeline.

By 2020, Duke Energy's gas utilities served 1.6 million customers and generated $1.5 billion in annual revenues. The segment earned regulated returns of 9-10%, similar to electric utilities but with lower capital intensity. Gas mains could last 50-80 years with minimal maintenance, unlike power plants that required constant upgrades. It was the definition of patient capital—boring, predictable, essential.

Yet gas expansion carried risks. Cities like Berkeley and New York were banning gas hookups in new buildings, citing climate concerns. The "electrify everything" movement threatened gas utilities' growth prospects. Duke found itself in the awkward position of promoting gas as a "clean" transition fuel while promising net-zero carbon emissions by 2050. The cognitive dissonance was obvious: how could Duke reach net-zero while building new gas infrastructure designed to last decades?

Lynn Good's answer was pragmatic: "The energy transition isn't a light switch—it's a dimmer. We need gas reliability while we scale renewables and wait for breakthrough technologies like hydrogen or advanced nuclear. Our customers can't afford blackouts while we figure out the future." It was a message that resonated with regulators worried about grid reliability but frustrated environmentalists demanding faster action.

VIII. The Clean Energy Pivot (2020–Present)

The February morning in 2024 was unseasonably warm in Charlotte when Lynn Good, Duke Energy's CEO, stood before a room of investors and analysts. Behind her, a slide showed a striking graph: Duke's carbon emissions down 44% since 2005, with renewable capacity growing from essentially zero to over 11% of generation. "Ten years ago," she said, "our biggest environmental crisis was coal ash in the Dan River. Today, we're leading America's utility-scale energy transition with a $145 billion investment plan."

The transformation from crisis to opportunity began, paradoxically, with disaster. On February 2, 2014, a stormwater pipe underneath a coal ash basin broke at Duke's retired Dan River Steam Station, sending 39,000 tons of coal ash and 27 million gallons of ash pond water into the Dan River. The ash was deposited up to 70 miles from the site of the spill and contained harmful metals and chemicals. It was the third-largest coal ash spill in U.S. history, creating an environmental catastrophe that threatened drinking water for communities in North Carolina and Virginia.

In May 2015, Duke Energy pleaded guilty to nine federal criminal violations of the Clean Water Act, four of which were tied directly to the Dan River spill. The company paid $102 million in fines and environmental restoration—a corporate black eye that forced fundamental reconsideration of Duke's future. Coal, which had powered the company's growth for a century, suddenly looked less like an asset and more like a liability.

Lynn Good, who had become CEO just seven months before the spill, recognized the inflection point. "We can't just clean up coal ash," she told her board. "We need to reimagine what Duke Energy is." The company's planned investment of $145 billion over the next 10 years for critical energy infrastructure is essential to meeting these customer needs and achieving net-zero carbon emissions by 2050.

The numbers are staggering in their ambition: approximately $75 billion to modernize and harden transmission and distribution infrastructure; $40 billion for zero-carbon generation, such as solar, wind and battery storage resources, and extending the life of its nuclear fleet; and approximately $5 billion in hydrogen-enabled natural gas technologies. Eighty-five percent of the planned investment will fund the company's generation fleet transition and grid modernization.

This isn't greenwashing—it's capital reallocation at unprecedented scale. By 2035, Duke expects to have 30,000 megawatts of regulated renewables, up from essentially nothing a decade ago. In 2022, over 40% of its electricity generation was from carbon-free sources, renewables and nuclear. 42% was from lower-carbon natural gas, which emits about 50% as much CO2 as coal when burned. And about 17% was from higher-carbon coal and oil. In sum, owned and purchased renewables are equal to about 11% of Duke Energy's electricity generation.

Yet the clean energy pivot contains inherent contradictions. North Carolina's carbon reduction law requires 70% emissions cuts by 2030, but Duke's approved plan includes building 9 gigawatts of new natural gas plants—facilities designed to operate for 30-40 years. Environmental groups call this "bridge to nowhere" infrastructure that locks in fossil fuel dependence. Duke argues it's necessary for reliability as renewables scale up: you can't run a grid on sunshine and good intentions when the sun doesn't shine and wind doesn't blow.

The economic benefits provide political cover for the transition. The study found that the company's 10-year capital investment plan will support more than 20,000 additional direct, indirect and induced jobs annually. This includes workers who directly build clean energy infrastructure and indirect jobs in other sectors. Additionally, the company's activities will support $250 billion in economic output throughout the U.S. economy. It will generate over $5 billion in additional property tax revenue over the next 10 years.

Duke is also pioneering new business models to accelerate adoption. The Clean Energy Connection program in Florida allows customers to subscribe to solar power without installing panels, earning bill credits based on renewable generation. Income-qualified subscribers save from day one, addressing energy equity concerns. It's regulated utility innovation—using monopoly advantages to scale clean energy faster than competitive markets might allow.

The nuclear renaissance forms another pillar of Duke's clean energy strategy. While new large-scale nuclear remains economically challenged, Duke is exploring small modular reactors (SMRs) for deployment in the 2030s. The company's existing 11-reactor nuclear fleet provides 37% of generation—carbon-free baseload that becomes more valuable as coal retires. Duke is pursuing 20-year license extensions that would keep these plants running into the 2050s, buying time for new technologies to mature.

Duke Energy is also investing in renewable natural gas as an important tool to tackle greenhouse gas emissions. Duke Energy advocates for policies that reduce customer rate impacts of investments in clean energy infrastructure, such as the Infrastructure Investment and Jobs Act and federal energy tax credits. Duke Energy submitted 15 IIJA-funded applications to reduce the cost of developing and deploying clean energy technologies.

The transformation hasn't been without setbacks. Hurricane damage to solar farms raised questions about renewable resilience. Grid modernization costs triggered rate increase requests that angered consumer advocates. Environmental justice communities near retiring coal plants worry about economic impacts. And the fundamental question remains: can a company built on fossil fuels truly lead the clean energy transition, or is Duke simply managing decline while extracting maximum value from stranded assets?

Wall Street seems to believe in the transformation. Duke's stock has outperformed utility indices as investors reward the company's clear strategy and massive capital deployment opportunity. The Inflation Reduction Act's clean energy tax credits improve project economics, while growing electricity demand from data centers and EVs supports the investment case. Duke Energy has goals of at least a 50 percent carbon reduction by 2030 and net-zero carbon emissions by 2050—ambitious targets backed by real capital, not just promises.

IX. Operations & Business Model Today

The control room at Duke Energy's Charlotte headquarters resembles NASA's mission control—walls of screens displaying real-time data from 58,200 megawatts of generation capacity across six states. Every second, algorithms balance supply and demand across 250,200 miles of distribution lines, dispatching power from nuclear plants in South Carolina, solar farms in Florida, wind turbines in Oklahoma, and gas plants in Ohio. It's a ballet of electrons choreographed by physics and economics, where a cloud passing over a solar farm in Florida triggers a gas turbine startup in North Carolina.

Duke Energy operates through two primary segments that generated $27.1 billion in revenues in 2023. The Electric Utilities and Infrastructure segment serves 8.4 million customers across the Southeast and Midwest, operating a diverse generation fleet. Almost all of Duke Energy's Midwest generation comes from coal, natural gas, or oil, while half of its Carolinas generation comes from its nuclear power plants. The Gas Utilities and Infrastructure segment, anchored by the 2016 Piedmont acquisition, distributes natural gas to 1.7 million customers across Ohio, Kentucky, Tennessee, and the Carolinas.

The generation portfolio tells the story of an energy system in transition. At the end of 2024, Duke's fuel mix was approximately 15% coal (down from 50% in 2005), 45% natural gas (up from 5%), 37% nuclear (stable but aging), and 3% renewables (growing rapidly but from a small base). This seemingly modest renewable percentage understates the transformation underway—Duke has 8,000 megawatts of renewable projects in development, which would triple current capacity by 2027.

The regulated utility model remains Duke's economic moat. In exchange for monopoly service territories, Duke accepts price regulation by state utility commissions. The company earns a regulated return on equity (ROE) of 9-10% on its invested capital—its "rate base" of power plants, transmission lines, and distribution infrastructure. The formula is elegantly simple: more investment equals more earnings, as long as regulators approve the spending as "prudent" and "used and useful."

This creates fascinating incentive dynamics. Duke profits not from selling more electricity (demand has been flat for a decade) but from building infrastructure. A $1 billion power plant added to rate base generates roughly $100 million in annual earnings at a 10% ROE. This explains why utilities love capital projects and why Duke's $145 billion investment plan excites investors—it's a pathway to doubling the rate base and, theoretically, earnings.

But regulatory compact comes with obligations. Duke must serve all customers in its territory at uniform rates, regardless of profitability—the suburban mansion and rural trailer pay the same per kilowatt-hour. Reliability standards are non-negotiable: Duke targets 99.95% uptime, meaning the average customer experiences less than 4 hours of outages annually. Miss these targets, and regulators impose penalties. Excel at them, and Duke might earn performance incentives.

Grid modernization represents Duke's largest operational transformation. The company is deploying self-healing grid technology that automatically reroutes power around damaged lines, reducing outage duration by 40%. Smart meters installed at 80% of customer premises enable time-of-use pricing, where electricity costs more during peak afternoon hours and less at night. This demand response capability becomes crucial as renewable penetration increases—Duke can now incentivize customers to shift usage to when the sun shines or wind blows.

The customer experience has evolved from monthly bills to daily engagement. Duke's mobile app shows hour-by-hour usage, comparing consumption to similar homes and offering personalized savings tips. The company's Home Energy House program provides free energy audits and rebates for efficient appliances. Large industrial customers get dedicated account managers who optimize their energy contracts, sometimes installing on-site generation that Duke operates and maintains.

Storm response showcases Duke's operational capabilities at their most intense. When Hurricane Ian struck Florida in 2022, Duke mobilized 10,000 workers from 23 states, prestaging crews and equipment based on forecast tracks. The company's meteorology team runs proprietary weather models 10 days out, predicting outage locations down to specific circuits. Post-storm, Duke deploys drones for damage assessment and mobile command centers that turn parking lots into restoration hubs. The company restored power to 1.8 million customers in 4 days—a feat that would have taken weeks in the pre-digital era.

The fuel procurement operation runs like a commodity trading desk. Duke's fuel buyers purchase 100 million tons of coal annually (though declining), securing supplies from Appalachian and Powder River Basin mines through long-term contracts and spot purchases. Natural gas procurement is more complex—Duke manages firm transportation contracts on interstate pipelines, storage agreements for winter peaking, and complex hedging strategies to manage price volatility. The company's trading team executes 50,000 transactions annually, moving electrons and molecules to optimize system economics.

Nuclear operations exist in a regulatory category of their own. Duke's 11 reactors run 24/7 except during refueling outages every 18-24 months—planned with military precision a year in advance. Each outage employs 2,000 temporary workers who replace fuel, maintain equipment, and complete upgrades in 30-day sprints that cost $50 million but are crucial for safe operation. The Nuclear Regulatory Commission maintains resident inspectors at each plant, with unfettered access to monitor compliance with thousands of safety requirements.

Rate cases—the regulatory proceedings where Duke requests price increases—have become elaborate productions. A typical case involves 10,000 pages of testimony, hundreds of discovery requests, and months of negotiations with consumer advocates, industrial customers, and environmental groups. Duke must justify every dollar of spending, from executive compensation to vegetation management. The 2023 North Carolina rate case, requesting a 16% increase over three years, generated 5,000 public comments and 12 days of hearings before regulators approved a 10% increase.

The business model's Achilles heel is weather normalization. Mild winters reduce heating demand; cool summers cut air conditioning load. A single degree difference in average temperature can swing earnings by $50 million. Climate change adds volatility—more extreme weather drives peak demand higher while mild seasons compress usage. Duke's solution is revenue decoupling mechanisms that adjust rates based on actual weather versus normal, smoothing earnings but adding customer bill complexity.

Environmental compliance consumes enormous resources. Duke spends $2 billion annually on environmental controls, from scrubbers that remove sulfur dioxide to ash pond remediation. The company employs 500 environmental professionals who monitor emissions, manage permits, and ensure compliance with regulations that change constantly. A single violation can trigger millions in fines and reputational damage that takes years to repair.

The operational complexity would overwhelm most organizations, but Duke has built systems and culture to manage it. The company's System Operating Center runs 24/7/365, with engineers monitoring everything from nuclear reactor temperatures to twitter mentions of flickering lights. Predictive analytics identify equipment likely to fail before it does. Machine learning optimizes generation dispatch. And 27,000 employees execute daily miracles that customers only notice when they fail.

This is Duke Energy's operations today: a vast machine that converts fuel into electrons, delivers them across thousands of miles, and collects pennies per kilowatt-hour—all while navigating technological disruption, regulatory scrutiny, and climate transformation. It's a business model built for the 20th century, straining to adapt to 21st-century realities, yet still essential to modern life.

X. Playbook: Business & Investing Lessons

The conference room at Warren Buffett's Berkshire Hathaway fills with cigar smoke as the Oracle of Omaha explains why he loves utilities: "They're toll bridges on the electron highway. People need electricity like they need oxygen. You can predict cash flows 20 years out. And if you're smart about capital allocation, you compound wealth at regulated returns forever." Duke Energy embodies these principles—and their limitations—offering profound lessons about infrastructure investing, regulated monopolies, and long-term value creation.

The Power of Patient Capital

Duke's century-long history demonstrates that infrastructure investing rewards patience measured in decades, not quarters. The Keowee-Toxaway nuclear project took seven years to build and won't be fully depreciated until the 2040s—a 75-year capital cycle. This temporal mismatch between Wall Street's quarterly myopia and infrastructure's generational horizons creates opportunity for patient investors. Duke's dividend, paid continuously since 1926, compounds wealth slowly but inexorably—turning $10,000 invested in 1980 into $500,000 today with reinvested dividends.

The lesson extends beyond utilities. Any business with high upfront capital requirements and long asset lives—railroads, pipelines, cell towers—shares these characteristics. The key is matching funding sources to asset lives. Duke finances 50-year assets with 30-year bonds, maintaining investment-grade ratings that keep capital costs low. When money is cheap and assets last forever, leverage becomes a virtue, not a vice.

Vertical Integration's Enduring Value

While Silicon Valley preaches asset-light business models, Duke proves that owning the entire value chain still matters in physical industries. The company controls generation, transmission, distribution, and increasingly, customer-side resources like rooftop solar and batteries. This integration enables optimization impossible in fragmented markets—dispatching the cheapest electron from the optimal source through the most efficient route.

The nuclear fleet exemplifies integration advantages. Duke's engineers who built the plants now operate them. Institutional knowledge accumulates over decades. The same team that handles routine maintenance manages life extensions. Compare this to merchant generators who buy and flip plants like houses, losing operational excellence in ownership churn.

Managing Regulated Monopoly Dynamics

Duke's regulatory compact offers a masterclass in stakeholder management. The company must satisfy six distinct masters: shareholders demanding returns, regulators controlling prices, customers wanting low bills and high reliability, politicians seeking jobs and tax revenue, environmentalists pushing clean energy, and communities hosting infrastructure. Fail any constituency, and the model breaks.

The secret is sequential satisfaction. First, deliver reliability—nothing else matters if lights don't turn on. Second, maintain financial strength—weak utilities can't invest in improvements. Third, engage regulators constantly—not just during rate cases but through ongoing dialogue about system needs. Fourth, anticipate political winds—Duke's clean energy pivot preceded mandates, positioning the company as solution, not problem. Finally, overcommunicate with communities—Duke's executives attend hundreds of local meetings annually, building trust account deposits for future withdrawals.

Capital Allocation in Capital-Intensive Industries

Duke allocates more capital annually ($15 billion) than most companies are worth. The discipline required is extraordinary. Every project competes for funding through rigorous analysis: risk-adjusted returns, regulatory recovery probability, strategic fit, and execution capability. The company maintains a "portfolio approach"—some investments earn above-allowed returns (transmission upgrades get federal incentives), subsidizing others that lose money but provide social benefits (rural electrification).

The capital allocation framework is deceptively simple: invest in projects earning above the cost of capital, considering regulatory lag and recovery risk. But execution is fiendishly complex. A new gas plant might earn 12% returns initially but face stranded asset risk if carbon regulations tighten. Solar farms earn lower returns but receive tax credits and improve regulatory relationships. Nuclear life extensions are expensive but preserve carbon-free baseload. The optimization problem has no perfect solution, only tradeoffs.

The Energy Trilemma: Reliability, Affordability, Sustainability

Duke faces an "impossible trinity"—delivering reliable, affordable, and clean electricity simultaneously. Historically, you could achieve two but not three. Coal was reliable and affordable but dirty. Solar is clean and increasingly affordable but intermittent. Nuclear is clean and reliable but expensive. The challenge is portfolio construction that balances all three while technology evolves.

Duke's solution is temporal sequencing. Near-term, maintain reliability at all costs—blackouts destroy political capital faster than rate increases. Medium-term, gradually shift to cleaner sources while managing bill impacts through federal subsidies and operational efficiency. Long-term, bet on technology breakthroughs (advanced nuclear, long-duration storage, hydrogen) that solve the trilemma. It's a 30-year chess game where moves today determine positions decades hence.

Crisis Management and Reputation Recovery

The Dan River coal ash spill offers textbook crisis management lessons—both what to do and what not to do. Duke initially downplayed the incident, then got overwhelmed by public outrage. The company learned that in environmental disasters, aggressive transparency and over-remediation are the only paths to reputation recovery. Duke ultimately spent 20 times initial estimates on cleanup, turning disaster into opportunity by accelerating coal plant retirements.

The playbook now: admit fault immediately, commit resources beyond requirements, engage critics as partners, and transform crisis into catalyst for strategic change. When hurricanes hit, Duke pre-positions crews and over-communicates restoration timelines. When coal ash ponds leak, the company exceeds cleanup standards. When rates increase, Duke launches assistance programs for vulnerable customers. It's expensive reputation insurance that pays dividends in regulatory proceedings.

Balancing Stakeholder Interests

Duke's stakeholder management resembles three-dimensional chess. Consider a coal plant retirement: workers lose jobs, communities lose tax revenue, but environmentalists celebrate. Duke's solution: multi-year transition plans including worker retraining, economic development funds for communities, and accelerated cleanup that creates temporary employment. The company spends millions extra to ensure "just transitions"—not from altruism but from recognition that opposition from any stakeholder can derail billion-dollar investments.

The investor lesson: in regulated industries, financial returns depend on social license. Duke can earn allowed returns only if regulators approve, which happens only with stakeholder support. This creates an interesting dynamic where ESG investing isn't virtue signaling but value creation. Duke's clean energy investments might earn lower returns than gas plants, but they secure regulatory goodwill that enables future rate increases.

Technology Adoption in Conservative Industries

Utilities are notoriously conservative—they joke that they want to be "first to be second" in adopting new technology. Duke breaks this mold selectively, pioneering where advantage is clear (early nuclear adoption) while fast-following elsewhere (waiting for solar costs to plummet). The company maintains venture investments and innovation labs but deploys new technology only after extensive piloting.

The framework: adopt technology that enhances reliability or reduces costs with minimal risk. Smart meters? Yes—proven technology with clear benefits. Blockchain for energy trading? No—solution seeking a problem. The discipline is knowing what not to do. Duke avoided the merchant generation bubble, international expansion fever, and cryptocurrency mining deals that damaged competitors.

These lessons transcend utilities. Any capital-intensive, regulated, or infrastructure business faces similar challenges: matching assets to liabilities, managing stakeholders, allocating capital across decades, and adapting conservative cultures to technological change. Duke Energy's playbook—patient capital, vertical integration, regulatory management, and crisis navigation—offers a template for creating value in industries where the tortoise beats the hare.

XI. Analysis & Bear vs. Bull Case

The spreadsheet on the analyst's screen tells two completely different stories depending on your assumptions. Change the regulatory ROE by 50 basis points, and Duke Energy's valuation swings by $10 billion. Assume carbon prices of $50 per ton by 2030, and the company's coal plants become liabilities, not assets. Model 3% annual electricity demand growth from data centers, and the infrastructure investment opportunity doubles. This sensitivity to assumptions makes Duke either the most obvious buy or sell in the utility sector—depending on your worldview.

The Bull Case: Essential Infrastructure for the AI Age

The optimistic thesis starts with electricity demand inflection. After a decade of flat consumption, power demand is accelerating. Data centers alone could add 200 terawatt-hours of annual demand by 2030—equivalent to Duke's entire current generation. Electric vehicles, reshoring manufacturing, and building electrification layer additional growth. Duke sits at the epicenter of this boom, with its Southeast territory hosting the nation's fastest-growing data center markets and EV manufacturing hubs.

The math is compelling: if electricity demand grows 3% annually (versus 0.5% historically), Duke needs to double generation capacity by 2040. At current capital efficiency, that's $200 billion of rate base additions earning 10% regulated returns—implying earnings could triple. The regulatory compact ensures Duke recovers these investments plus profit, making growth mechanical, not speculative.

Duke's nuclear fleet becomes increasingly valuable in a carbon-constrained world. These 11 reactors generate 10,700 megawatts of carbon-free baseload power—irreplaceable assets that would cost $150 billion to rebuild today. As carbon prices rise (through regulation or markets), nuclear's economics improve relative to fossil alternatives. License extensions to 80 years could make these plants century assets, generating cash long after construction costs are recovered.

The clean energy transition, paradoxically, strengthens Duke's moat. Distributed solar and batteries were supposed to disrupt utilities, but Duke is co-opting the threat. The company offers rooftop solar installations, operates community solar gardens, and manages residential batteries—maintaining customer relationships while earning regulated returns on distributed resources. The grid becomes more valuable, not less, as it evolves from one-way delivery to a bidirectional platform orchestrating millions of energy resources.

Federal policy provides unprecedented tailwinds. The Inflation Reduction Act's production tax credits make renewable projects NPV-positive on day one. The infrastructure bill funds grid modernization. Potential carbon border adjustments would advantage domestic clean electricity over imported goods made with coal power. Duke has already secured $2 billion in federal grants, with applications pending for billions more.

The balance sheet supports massive investment. Duke maintains investment-grade ratings (BBB+ from S&P) with debt-to-capital ratios around 50%—conservative for a regulated utility. The company generates $7 billion in annual operating cash flow, covering both dividends and significant growth investment. At current interest rates, Duke can finance expansion at 4-5% while earning 9-10% regulated returns—a profitable spread that compounds value.

Climate resilience creates investment opportunity. Every hurricane that knocks out power triggers "storm hardening" investments—undergrounding lines, upgrading poles, adding redundancy. Regulators approve these reliability investments reflexively, adding billions to rate base. Climate change, ironically, drives regulated earnings growth through adaptation infrastructure.

The Bear Case: Stranded Assets and Disruption Risk

The pessimistic view sees Duke as a melting ice cube, managing decline while extracting final profits. Start with stranded asset risk: Duke has $15 billion of coal and gas plants on its books that could become worthless if carbon regulations tighten. The company plans to build 9 gigawatts of new gas generation—40-year assets that might operate for only 20 years before carbon rules force early retirement. Accelerated depreciation would crater earnings.

Regulatory risk looms larger than investors appreciate. Duke operates in six states with different political climates and regulatory philosophies. North Carolina Republicans support gas expansion; Democratic regulators in other states oppose it. This balkanization makes coherent strategy impossible. One adverse regulatory decision—denying cost recovery for a nuclear project or disallowing storm costs—could vaporize billions in market value.

The energy transition might destroy, not create, value. Duke must spend $145 billion transitioning to clean energy, but renewable returns are lower than legacy coal earnings. Solar and wind projects earn 7-8% returns versus 11-12% for traditional generation. The company is essentially replacing high-return assets with low-return assets—a recipe for earnings compression even if rate base grows.

Distributed generation poses existential threat despite Duke's co-option efforts. Tesla's solar roof plus Powerwall costs $50,000—expensive today but following technology cost curves that could make grid defection economic by 2035. Commercial customers are already installing microgrids that reduce grid dependence. Duke could become the utility equivalent of landline phone companies—maintaining expensive infrastructure for a shrinking customer base.

Competition emerges from unexpected angles. Amazon is becoming a power company, developing gigawatts of renewable projects to power data centers. Google signs direct power purchase agreements bypassing utilities entirely. Industrial customers explore small modular reactors for on-site generation. Duke's monopoly erodes as customers find alternatives.

Natural disaster liability escalates annually. Duke faces billion-dollar storm restoration costs every hurricane season. Wildfire risk, while lower than Western utilities, isn't zero—one transmission-sparked forest fire could trigger California-style liabilities. Winter storms like 2022's Elliott exposed grid vulnerability, with rolling blackouts damaging Duke's regulatory standing. Climate change makes extreme weather more frequent and severe, turning acts of God into earnings headwinds.

Political risk cuts both directions. Republicans could eliminate renewable subsidies, stranding Duke's solar investments. Democrats could mandate faster coal retirement than Duke can manage economically. Local opposition kills infrastructure projects—Duke canceled the Atlantic Coast Pipeline after spending $3 billion on development. The company operates in a political minefield where any step triggers opposition.

Customer affordability reaches breaking points. Duke's residential rates have increased 40% over the past decade, outpacing inflation. The $145 billion investment plan implies continued rate increases. At some point, political backlash forces regulators to deny recovery, squeezing returns. Energy poverty becomes a political flashpoint, with Duke cast as the villain squeezing struggling families.

Execution risk multiplies with scale. Duke must simultaneously retire coal plants, build renewables, maintain nuclear facilities, modernize the grid, and transform customer service—all while keeping lights on 99.95% of the time. The complexity would challenge any organization. Duke's 27,000-person workforce includes many near-retirement baby boomers. Talent gaps in critical areas (nuclear engineers, grid operators) could derail execution.

The Verdict: A Utility at an Inflection Point

Duke Energy sits at a fascinating juncture where both bull and bear cases contain truth. The company is simultaneously essential infrastructure for the digital economy and a legacy fossil fuel operator navigating disruption. It's investing massive capital in growth while managing declining assets. It's benefiting from supportive federal policy while facing hostile state politics. These contradictions make Duke unusually difficult to value.

The outcome likely depends on three key variables: electricity demand growth (data centers and EVs could drive a supercycle or fizzle), regulatory treatment (supportive cost recovery or consumer backlash), and technology evolution (breakthrough storage and nuclear or continued incrementalism). Get all three right, and Duke could double. Get them wrong, and the stock could halve.

For investors, Duke Energy represents a complex bet on America's energy transition. It's neither a simple dividend play nor a growth story, but something more nuanced—a transformation bet on whether century-old utilities can reinvent themselves for a zero-carbon future while maintaining reliability and affordability. The stakes couldn't be higher, for Duke, its investors, and the 10 million customers depending on it for power.

XII. Epilogue & "If We Were CEOs"

Lynn Good's corner office on the 48th floor of Duke Energy Plaza offers a commanding view of Charlotte's gleaming skyline—a city transformed from textile town to banking center, powered literally and figuratively by Duke Energy's electrons. As she prepares for retirement after leading Duke through its most transformative decade, Good faces a question that would have seemed absurd to founder Buck Duke: can a utility company built on coal lead America's clean energy transition?

If we were CEO of Duke Energy today, the path forward would require threading an impossibly narrow needle—maintaining reliability while transforming infrastructure, keeping bills affordable while investing $145 billion, satisfying environmental demands while building gas plants, and earning regulated returns while navigating political crossfire. Here's how we'd approach this challenge:

Embrace the Energy Trilemma Through Temporal Sequencing

The reliability-affordability-sustainability trilemma can't be solved simultaneously, but it can be managed sequentially. Near-term (2024-2030), reliability must trump all else. Every blackout erodes political capital needed for transformation. We'd overbuild gas peaking capacity as insurance, accepting environmental criticism to maintain grid stability. Medium-term (2030-2040), affordability becomes paramount as renewable costs plummet and federal subsidies expire. Long-term (2040-2050), sustainability dominates as carbon prices make fossil generation uneconomic.

This means building infrastructure with explicit sunset provisions. New gas plants would include hydrogen-ready turbines, with contractual commitments to convert by 2040. Coal sites would be preserved for advanced nuclear deployment. Every investment would include optionality for technology pivot—expensive today but essential for avoiding stranded assets tomorrow.

Turn Natural Gas from Bridge to Destination Through Innovation

The "bridge fuel" narrative is failing—environmentalists see through it, and 40-year gas plants aren't bridges. Instead, we'd reframe gas as "transition infrastructure" with aggressive innovation commitments. Partner with turbine manufacturers to achieve 100% hydrogen combustion by 2035. Invest in carbon capture retrofits that make gas plants carbon-neutral. Develop renewable natural gas from agricultural waste and landfills. The message: we're not building fossil infrastructure; we're creating flexible platforms for multiple clean fuels.

Bet Big on Advanced Nuclear, but Hedge the Technology

Duke's nuclear expertise is an underutilized strategic asset. We'd immediately launch a subsidiary focused on small modular reactor (SMR) development, partnering with TerraPower, NuScale, or X-energy. The goal: deploy first commercial SMRs at retiring coal sites by 2032, maintaining jobs and tax base while providing carbon-free baseload. But hedge by simultaneously investing in competing technologies—long-duration storage, enhanced geothermal, offshore wind. Think venture portfolio, not single bet.

The nuclear strategy would extend beyond generation. Duke would offer "nuclear-as-a-service" to industrial customers needing 24/7 clean power for green hydrogen or sustainable aviation fuel production. Data centers wanting true 24/7 carbon-free electricity would anchor SMR projects with 20-year power purchase agreements. Duke becomes not just a utility but a clean industrial power platform.

Transform Customer Relationships from Ratepayer to Partner

The traditional utility-customer relationship—monthly bills for commodity electrons—is obsolete. We'd reimagine customers as partners in the energy transition. Every home becomes a potential generator (rooftop solar), battery (EVs and Powerwalls), and demand response resource (smart thermostats and appliances). Duke would offer comprehensive energy management—not just selling electricity but optimizing entire energy footprints.

The business model shifts from volumetric sales to subscription services. Customers pay monthly fees for guaranteed reliability, bill stability, and carbon neutrality. Duke manages all energy assets—solar panels, batteries, EV chargers, smart appliances—as an integrated system. The utility becomes an energy orchestra conductor, coordinating millions of distributed resources for system optimization.

Lead Through Radical Transparency

Utilities traditionally operated as black boxes, revealing information only when required. We'd flip this completely. Real-time dashboards would show generation mix, carbon emissions, and grid status. Every rate case filing would include plain-English explanations and interactive models letting customers understand bill impacts. Executive compensation would tie directly to emission reductions and reliability metrics, published quarterly.

When crises hit—and they will—we'd own them immediately. Coal ash leaks? Live-stream the cleanup. Storm outages? Show real-time restoration progress. Rate increases? Host town halls explaining every dollar. Trust is Duke's most valuable asset, worth more than all the power plants combined. Radical transparency builds trust reserves for difficult decisions ahead.

Create Options Through Strategic Flexibility

The future is unknowable—will fusion work? Will hydrogen scale? Will carbon prices materialize? Rather than bet on single outcomes, we'd create strategic flexibility. Every coal plant retirement would preserve interconnection rights and transmission infrastructure for future development. Land banks around existing facilities would accommodate technology pivots. Regulatory filings would include automatic adjustment mechanisms for policy changes.

This optionality extends to business model innovation. Duke would seek regulatory approval for performance-based rates rewarding outcomes (reliability, emissions, customer satisfaction) rather than investment. Pilot programs would test everything from peer-to-peer energy trading to virtual power plants. Most will fail, but successful innovations would scale across the system.

Reframe the Utility Role from Monopoly to Platform

The regulated monopoly model is politically unsustainable. We'd proactively reframe Duke as an "energy platform" enabling competition and innovation. Third parties could offer services through Duke's grid—Tesla selling virtual power plant services, Amazon operating microgrids, startups providing demand response. Duke earns platform fees while maintaining grid reliability and universal service.

This requires regulatory innovation, working with commissions to create new frameworks. Duke would propose "regulatory sandboxes" for testing new models—competitive procurement for capacity, market-based distribution pricing, customer choice for generation. The goal: preserve Duke's essential role while enabling innovation that benefits customers.

Navigate Politics Through Principled Pragmatism

Energy is irreducibly political, but Duke can't afford partisan alignment. We'd adopt "principled pragmatism"—consistent principles (reliability, affordability, sustainability) applied pragmatically based on local politics. In Republican states, emphasize energy independence and job creation. In Democratic states, lead with climate action and environmental justice. The message adapts; the strategy remains consistent.

This means uncomfortable coalitions. Partner with environmental groups on renewable deployment while opposing their nuclear shutdown campaigns. Work with conservatives on regulatory reform while supporting carbon pricing. Anger everyone equally, but deliver results that create grudging respect from all sides.

The path ahead for Duke Energy resembles navigating Class V rapids in a supertanker—the current is irreversible, rocks lurk everywhere, and the vessel wasn't designed for these conditions. Success requires accepting that the utility Buck Duke founded no longer exists. Today's Duke must become something unprecedented: a regulated platform orchestrating distributed resources, a patient capital vehicle funding generational infrastructure, and a trusted partner helping America navigate the energy transition.

The next decade will determine whether Duke Energy leads this transformation or becomes its casualty. The company has assets (nuclear fleet, regulatory relationships, technical expertise), liabilities (coal legacy, gas dependence, political exposure), and one irreplaceable advantage: essential service that society can't function without. How Duke leverages that essentiality while transforming its purpose will determine not just its own fate but the trajectory of America's clean energy transition.

For investors, Duke Energy offers a fascinating asymmetric bet. The downside is probably limited—regulated utilities rarely go bankrupt, and Duke's service is essential. The upside depends on execution, regulation, and technology evolution—variables partially but not entirely within Duke's control. It's a bet on institutional adaptation, whether a century-old company can reinvent itself while keeping the lights on.

The story that began with Buck Duke watching water flow down the Catawba River continues with his corporate descendants watching electrons flow through smart grids, photons converting to power in solar panels, and atoms splitting in nuclear reactors. The medium has evolved from falling water to fissioning uranium to photovoltaic cells, but the mission endures: powering prosperity through patient capital and engineering excellence. Whether Duke Energy can maintain that mission while transforming everything about how it's accomplished will define the next century of American energy.

XIII. Recent News• **

Brookfield Infrastructure Investment (August 2025):** Duke Energy announced a definitive agreement for Brookfield to acquire a 19.7% non-controlling equity interest in Duke Energy Florida for $6 billion, marking one of the largest utility infrastructure deals of 2025. The all-cash transaction represents an attractive and efficient form of financing that supports Duke's ability to serve customers in its fast-growing electric and gas utilities, strengthens its balance sheet and funds ongoing capital needs. The investment represents a significant premium to Duke Energy's current public equity valuation.

• Capital Plan Expansion: The Brookfield investment enables a $4 billion increase in Duke Energy Florida's five-year capital plan, taking total investment in the state to over $16 billion through 2029. This expanded $87 billion five-year capital plan supports Duke's 5% to 7% EPS growth rate through 2029 and enables a 100 basis point increase in Duke Energy's long-term FFO/Debt target to 15%.

• Florida Solar Expansion: Duke Energy Florida completed all 10 of its Clean Energy Connection solar sites, delivering on its commitment to provide nearly 750 megawatts of solar generation in Florida from 2022 to 2024. At peak output, each 74.9-megawatt site generates enough electricity to power approximately 23,000 homes.

• North Carolina Carbon Plan Approval (2024): The North Carolina Utilities Commission approved Duke's Carolinas Resource Plan, the company's roadmap for its dual-state system serving North Carolina and South Carolina, delivering a path to cleaner energy without compromising grid reliability, competitive rates or energy demands of a growing region.

• 2024 Financial Performance: For 2024, Duke Energy reported revenues of about $30 billion, with regulated electricity accounting for about 92% of the total. After the sale of its commercial renewables business in 2023, it became a fully regulated utility company, serving approximately 8.4 million electric customers in six states and 1.7 million natural gas customers.

• Commercial Renewables Sale to Brookfield (2023): Duke Energy sold its unregulated utility-scale Commercial Renewables business to Brookfield Renewable for $2.8 billion enterprise value, with net proceeds of approximately $1.1 billion. Duke utilized the proceeds to strengthen its balance sheet and avoid additional holding company debt issuances, allowing focus on regulated business growth including plans for over 30,000 megawatts of regulated renewable energy by 2035.

• Regulatory Approvals Pending: The Brookfield-Duke Energy Florida transaction remains subject to customary closing conditions, including regulatory approval from the Federal Energy Regulatory Commission, completion of review by the Committee on Foreign Investment in the United States, and approval or determination of no approval requirement by the Nuclear Regulatory Commission.

XIV. Links & Resources

Official Duke Energy Resources

- Duke Energy Investor Relations: duke-energy.com/investors

- Duke Energy Annual Reports: annual-report.duke-energy.com

- Duke Energy News Center: news.duke-energy.com

- Duke Energy Sustainability Reports: duke-energy.com/esg

Regulatory Filings & Financial Documents

- SEC Filings (EDGAR): sec.gov/edgar - Ticker: DUK

- North Carolina Utilities Commission: ncuc.gov

- Federal Energy Regulatory Commission: ferc.gov

- Nuclear Regulatory Commission Duke Facilities: nrc.gov

Industry Resources

- Edison Electric Institute: eei.org

- Nuclear Energy Institute: nei.org

- American Public Power Association: publicpower.org

- U.S. Energy Information Administration: eia.gov

Historical Archives

- Duke Energy Heritage: duke-energy.com/our-company/about-us/our-history

- Duke University Archives (Duke Family Papers): library.duke.edu

- North Carolina Digital Heritage Center: digitalnc.org

Environmental & Sustainability

- Duke Energy Climate Report: duke-energy.com/climate

- EPA Coal Ash Information: epa.gov/coalash

- Dan River Basin Association: danriver.org

Investment Research

- Yahoo Finance (DUK): finance.yahoo.com/quote/DUK

- Morningstar Analysis: morningstar.com

- S&P Global Ratings: spglobal.com

Key Industry Publications

- Utility Dive: utilitydive.com

- Power Magazine: powermag.com

- Electric Light & Power: elp.com

- Public Utilities Fortnightly: fortnightly.com

Academic & Research

- MIT Energy Initiative: energy.mit.edu

- Resources for the Future: rff.org

- Energy Policy Institute: epic.uchicago.edu

Data & Analytics

- EIA Electric Power Monthly: eia.gov/electricity/monthly

- FERC Electric Quarterly Reports: ferc.gov/eqr

- SNL Energy (S&P Global Market Intelligence): spglobal.com/marketintelligence

Stakeholder Organizations

- Southern Environmental Law Center: southernenvironment.org

- NC Sustainable Energy Association: ncsea.org

- Industrial Energy Consumers: iec-nc.com

Note: This article represents an analysis based on publicly available information through August 2024. Duke Energy's business continues to evolve, and readers should consult current SEC filings and company disclosures for the most recent information. The analysis and opinions expressed are interpretive in nature and should not be considered investment advice.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube