Southern Company: America's Energy Infrastructure Giant

I. Introduction & Episode Roadmap

Picture this: It's July 2023, and in the red clay country of eastern Georgia, a nuclear reactor finally roars to life after seventeen years of construction, seven years behind schedule, and $21 billion over budget. This is Vogtle Unit 3, America's first new nuclear reactor in decades, and it belongs to Southern Company—a utility giant that simultaneously funds climate denial research while building the nation's only new nuclear plants. Welcome to the paradox that is Southern Company.

From its Atlanta headquarters, Southern Company commands an empire that would make any Gilded Age baron envious: 9 million customers across the Southeast, nearly 200,000 miles of transmission lines snaking through pine forests and coastal plains, 80,000 miles of gas pipelines buried beneath suburban lawns and city streets. It's America's second-largest utility by customer count, a $150 billion market cap behemoth that powers the data centers running your Netflix streams and the air conditioners keeping Miami habitable.

But here's the question that defines this episode: How did a collection of Depression-era Southern utilities, born from British capital and Alabama river dreams, evolve into America's most controversial clean energy paradox—a company that spent decades denying climate change while simultaneously making the biggest nuclear bet in the Western hemisphere?

This is a story about infrastructure as destiny. About how controlling electrons and molecules flowing through wires and pipes creates a different kind of monopoly power—one blessed by regulators, protected by politics, and paid for by captive customers. It's about big bets that go spectacularly wrong (hello, Vogtle), bigger bets that transform industries (the natural gas pivot), and the delicate dance between serving the public and enriching shareholders.

We'll trace Southern Company from James Mitchell's hydroelectric dreams in 1912 through coal-fired industrialization, nuclear ambitions, climate denial campaigns, and ultimately to today's awkward pivot toward clean energy. Along the way, we'll decode the regulatory capture playbook, dissect one of corporate America's most expensive construction disasters, and explore whether this century-old utility can navigate the energy transition without becoming a fossil itself.

What makes Southern Company fascinating isn't just its size or influence—it's how perfectly it embodies the contradictions of American capitalism. A regulated monopoly that acts like a free market player. A climate change denier that's building carbon-free nuclear plants. A Southern institution that powered the civil rights era's industrialization while maintaining the region's conservative politics. These tensions aren't bugs in Southern Company's system—they're features, carefully cultivated over a century of corporate evolution.

So buckle up. We're about to journey through boardrooms where billion-dollar bets get made on nuclear concrete, through Southern state houses where utility commissioners and executives blur into one entity, and into a future where artificial intelligence's insatiable power hunger might just save a company that many thought was destined for disruption. This is Southern Company—where the past and future of American energy collide.

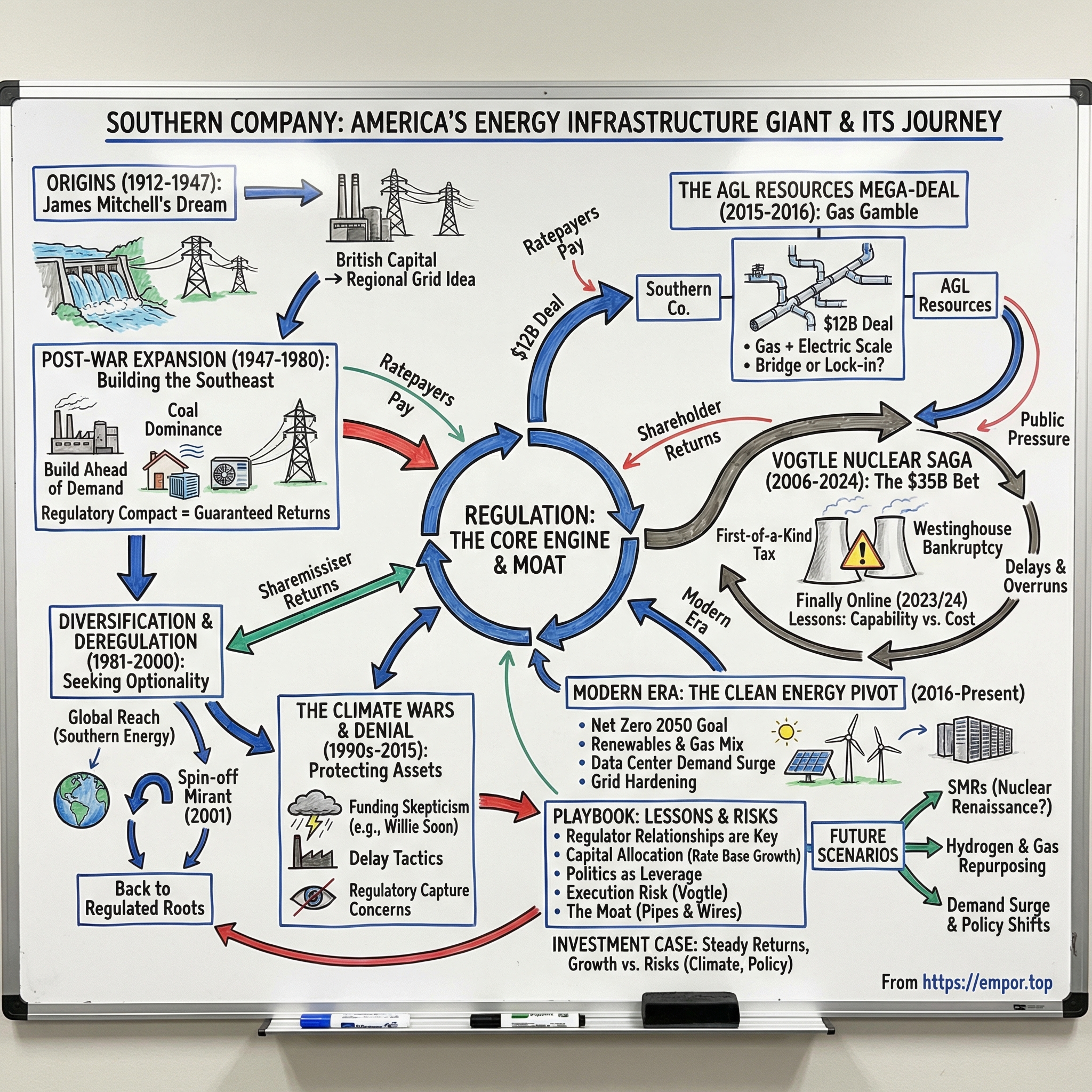

II. Origins: James Mitchell's Southern Dream (1912-1947)

The Coosa River tumbles down from the Appalachian foothills through Alabama like nature's own power plant, dropping hundreds of feet as it winds toward Mobile Bay. In 1906, a Canadian engineer named James Mitchell stood on its banks, watching the water rush past, and saw something nobody else did: the industrial future of the American South. Mitchell, who'd cut his teeth building power projects in Canada and Brazil, had been hired by a London syndicate to scout hydroelectric opportunities in the underdeveloped American Southeast. What he found in Alabama's rivers wasn't just water—it was liquid capital waiting to be harnessed.

Mitchell was the kind of engineer-entrepreneur who sketched dam sites on napkins and could calculate kilowatt potential in his head. British investors, flush with capital from their global empire and seeking returns in the former Confederacy, backed his vision with millions of pounds sterling. By 1912, Mitchell had cobbled together enough land rights, water permits, and foreign capital to incorporate Alabama Power Company. The marker at the company's first headquarters in Birmingham still reads: "Southern Company traces its roots to 1912," but that understates the audacity of Mitchell's original vision—he wasn't just building a power company, he was designing an entire regional grid from scratch.

The 1920s saw Mitchell's dream expand beyond Alabama. Alabama Power, Georgia Power, Gulf Power, and Mississippi Power—originally independent companies serving their feudal territories—began coordinating operations under a web of holding companies. This wasn't just about efficiency; it was about creating something unprecedented in the South: a unified electrical system that could power the region's transformation from agricultural backwater to industrial competitor. The utilities shared transmission lines like railroads shared tracks, moving power from where it was generated to where it was needed, creating the Southeast's first truly regional infrastructure network.

Enter Wendell Willkie, the Indiana lawyer who would become the face of Southern utilities during their most existential crisis. In 1933, Willkie took the helm of Commonwealth & Southern Corporation, the massive holding company that had absorbed Mitchell's creation and its sister utilities. Willkie was everything Mitchell wasn't—a smooth-talking lawyer who could charm Wall Street bankers and Washington politicians with equal ease. He needed every ounce of that charm when Franklin Roosevelt dropped a bomb on the private utility industry: the Tennessee Valley Authority.

The TVA represented everything Commonwealth & Southern feared: government-owned power generation, sold at prices no profit-seeking company could match, backed by the full faith and credit of the United States. When Congress created TVA in 1933, it drew its boundaries right through Commonwealth & Southern's territory. Willkie fought like a cornered wildcat, launching constitutional challenges, lobbying campaigns, and public relations blitzes against what he called "government socialism." But by 1939, after losing every legal battle, he was forced to sell Tennessee Electric Power Company to TVA for $78 million—a transaction that felt less like a business deal and more like a surrender at Appomattox.

The Public Utility Holding Company Act of 1935 delivered another body blow. Written in response to the pyramid schemes and financial engineering that had enriched utility financiers while impoverishing customers during the Depression, PUHCA essentially outlawed the complex holding company structures that controlled most of America's power companies. Commonwealth & Southern would have to be unwound, its components either sold off or reorganized into something simpler and more regulated.

The slow dissolution of Commonwealth & Southern became the painful birth of modern Southern Company. Lawyers and bankers spent over a decade untangling the corporate web, negotiating with the SEC, and restructuring debt. Finally, in 1946, Southern Company was incorporated as a simplified holding company for the four main operating utilities: Alabama Power, Georgia Power, Gulf Power, and Mississippi Power. The SEC blessed the structure in 1947, and Southern Company as we know it today was born—not with fanfare, but with relief that the existential threats of the 1930s had finally passed.

Yet even as Southern Company emerged from its bureaucratic chrysalis, the seeds of its future character were already planted. The fight against TVA had taught it that political power mattered as much as electrical power. The PUHCA restructuring had shown that regulatory relationships could make or break a utility's fortunes. And the post-war South, with its promise of air conditioning, suburban growth, and industrial development, offered opportunities that would have made James Mitchell's wildest dreams seem quaint. The company that entered the 1950s wasn't just a collection of utilities—it was an institution that had learned how to survive, and thrive, in the unique ecosystem of Southern politics and regulated capitalism.

III. Building the Southeast: Post-War Expansion (1947-1980)

The summer of 1951 in Atlanta hit different. For the first time, office buildings hummed with a new sound—the drone of central air conditioning units that made August in Georgia feel like October in Ohio. Rich's Department Store downtown had just installed a massive new cooling system, and suddenly shoppers lingered for hours in climate-controlled comfort instead of fleeing to porches and shade trees. This wasn't just a comfort revolution; it was Southern Company's ticket to geometric growth. Every air conditioner installed meant more kilowatts sold, more revenue guaranteed by regulators, and more capital to build more power plants to sell more kilowatts. The virtuous cycle of the regulated utility had begun.

From its Atlanta headquarters—strategically positioned in the South's emerging commercial capital rather than old-money Birmingham—Southern Company orchestrated one of the most aggressive infrastructure expansions in American corporate history. Between 1950 and 1970, the company built forty-two new power plants, mostly coal-fired behemoths that could generate more electricity in a day than Alabama had consumed in all of 1920. Plant Gaston in Alabama, Plant Bowen in Georgia, Plant Daniel in Mississippi—these weren't just power stations; they were industrial cathedrals, monuments to the New South's ambitions.

The economics were beautifully simple. State utility commissions guaranteed Southern Company a return on every dollar invested in power generation—typically 10-12% annually. The more the company built, the more profit it was legally entitled to earn. This "cost-plus" regulatory model turned conventional business logic on its head: efficiency and cost-cutting actually hurt profits, while gold-plating and overbuilding increased them. One Southern Company executive from this era later admitted, "We had zero incentive to control costs. If a plant was budgeted at $100 million and came in at $150 million, we just made more money."

The transmission grid became Southern Company's true competitive moat. While anyone could theoretically build a power plant, only Southern Company had the regulatory authority to string high-voltage lines across four states. By 1960, the company operated 15,000 miles of transmission lines, creating an electrical interstate highway system that connected rural Alabama to urban Atlanta, coastal Mississippi to inland Georgia. This grid didn't just move electricity; it moved the South into the modern economy.

Natural disasters became perverse opportunities for infrastructure investment. When Hurricane Camille devastated the Gulf Coast in 1969, destroying huge swaths of Mississippi Power's service territory, the rebuilding effort added hundreds of millions to the company's rate base. "Facing every conceivable impediment—natural and man-made disasters, hostile takeover attempts, financial challenges—Southern Company grew stronger and more resilient," the company's official history notes, though it fails to mention that each disaster meant higher rates for customers and higher returns for shareholders.

The nuclear age arrived in Georgia's Burke County in 1976, when Southern Company broke ground on Plant Vogtle. Named after Alvin Vogtle, a former company president who'd championed nuclear power as coal's inevitable successor, the project represented Southern Company's biggest bet yet. The original plan called for four reactors, each budgeted at under $1 billion, that would provide clean, abundant power for generations. Westinghouse would supply its newest pressurized water reactor design, Bechtel would manage construction, and Georgia Power would own the lion's share of the project.

What happened next would become a preview of nuclear power's American tragedy. Vogtle Units 1 and 2, those Westinghouse PWRs rated at 1,109 and 1,127 megawatts, were supposed to cost less than $1 billion each and come online by the early 1980s. Instead, they didn't begin operation until 1987 and 1989, with final costs skyrocketing to nearly $9 billion—almost a tenfold increase. Regulatory changes after Three Mile Island, construction delays, labor disputes, and what investigators called "systemic management failures" turned Vogtle into a financial black hole that consumed capital like a nuclear reaction consumes uranium.

Yet here's the perverse beauty of the regulated utility model: Southern Company's shareholders barely felt the pain. Georgia regulators simply approved rate increase after rate increase, passing the nuclear disaster's costs directly to customers. Between 1975 and 1990, Georgia Power's rates tripled, but its stock price steadily climbed. The company had discovered a fundamental truth about American capitalism: when you're a monopoly blessed by the state, failure can be as profitable as success.

The 1970s also saw Southern Company perfect its political influence machine. The company's executives didn't just lobby state regulators; they became them, in a revolving door that would make Washington blush. Former Southern Company lawyers routinely became public service commissioners. Retired commissioners joined Southern Company's board or its law firms. Campaign contributions flowed like electrons through copper wire—constant, powerful, and essentially invisible to the public.

By 1980, Southern Company had transformed the Southeast. The same region that had been America's poorest in 1945 now attracted Boeing factories, bank headquarters, and the early tech companies that would eventually make Atlanta the South's Silicon Valley. Air conditioning had made the South livable year-round, cheap electricity had made it profitable for manufacturing, and Southern Company had made itself indispensable to both. The company that James Mitchell had dreamed of in 1912 had become something he never could have imagined: a $10 billion enterprise that controlled the literal power switches of the New South. But success bred hubris, and hubris in the utility business has a way of becoming very expensive—as the next chapter in Southern Company's story would dramatically prove.

IV. Diversification & Deregulation Era (1981-2000)

The press release hit the wires on December 15, 1981, with all the understated drama of a Southern utilities announcement: "Southern Company Forms Unregulated Subsidiary." For students of American corporate history, this was like reading "Quaker Oats Enters Cocaine Business." For forty-six years, since the Public Utility Holding Company Act had dismantled the utility trusts, no electric holding company had dared venture beyond its regulated boundaries. But Southern Company's CEO at the time, Bill Reed, saw deregulation coming like a freight train and decided to jump on board rather than get run over.

Southern Energy, Inc. began operations in January 1982 with a simple premise that was revolutionary for a utility: compete in free markets, without guaranteed returns, using only Southern Company's expertise in building and operating power plants. Within five years, Southern Energy was developing projects in Pakistan, building plants in the Philippines, and negotiating deals in Argentina. The subsidiary grew like kudzu, eventually operating in ten countries across four continents, generating power for anyone who'd pay market rates rather than regulated tariffs.

The international expansion revealed something important about Southern Company's DNA: stripped of its regulatory protection, it was actually quite good at the power business. In Chile, Southern Energy built and operated plants that were more efficient than the state-owned competition. In the Philippines, it navigated corruption and political chaos to deliver reliable electricity to Manila's industrial zones. The company discovered it had exportable expertise—not just in engineering, but in the subtle art of managing large infrastructure projects in challenging political environments. After all, if you could work with Alabama regulators, Pakistani bureaucrats seemed almost straightforward.

Back home, Southern Company was building a different kind of empire. Southern Nuclear, formed in 1991, consolidated the operation of the company's nuclear plants under one specialized subsidiary—a prescient move given the complexity of running reactors in the post-Chernobyl era. Rather than having each state utility manage its own nuclear operations, Southern Nuclear created centers of excellence, standardized procedures, and most importantly, spread nuclear expertise across the entire system. This would matter enormously when the company decided to bet big on nuclear again two decades later.

The 1990s brought toys that utility executives had never imagined. In 1996, Southern Communications Services launched Southern LINC, a digital wireless network that piggybacked on the company's existing transmission infrastructure. Those high-voltage towers that carried electricity could also carry cell phone signals, and those right-of-ways that hosted power lines could also host fiber optic cables. Suddenly, Southern Company wasn't just in the electron business—it was in the bits and bytes business too.

But the real action was in wholesale power markets, where deregulation had created a casino for anyone who could generate and trade electricity. Southern Energy became one of the biggest players, building merchant power plants—facilities that sold electricity at market prices rather than regulated rates—across the United States. By 2000, Southern Energy operated more than 20,000 megawatts of generation capacity, making it one of America's largest independent power producers. The subsidiary was growing so fast that Wall Street analysts started valuing it separately from the sleepy regulated utilities, seeing it as Southern Company's growth engine for the new millennium.

The boom times created a cultural schism within Southern Company. The traditional utility executives in Atlanta, men who'd spent careers navigating public service commissions and managing coal plants, looked with suspicion at the cowboys running Southern Energy. These were MBAs who talked about "spark spreads" and "heat rate arbitrage," who flew to Buenos Aires for weekend negotiations and treated electricity like any other commodity. The tension was palpable at company meetings, where Southern Energy executives would present hockey-stick growth projections while utility veterans muttered about "Enron wannabes."

They weren't entirely wrong. By 2000, Southern Energy had transformed itself into something that looked suspiciously like Enron—a massive energy trading operation with a small side business in actually generating power. The subsidiary was making huge bets on natural gas prices, electricity demand, and weather patterns. When California's electricity crisis hit in 2000-2001, Southern Energy was right in the middle, selling power at astronomical prices to desperate California utilities. The profits were enormous, but so was the reputational risk.

The solution was surgical: spin off the problem child. On April 2, 2001, Southern Company distributed all shares of Southern Energy to its shareholders, creating an independent company called Mirant Corporation. The spinoff was marketed as "unlocking value," but everyone knew the real reason—Southern Company wanted to distance itself from the increasingly toxic world of energy trading before regulators and politicians came calling. It was prescient timing. Mirant would file for bankruptcy just two years later, caught in the same market collapse that destroyed Enron.

With Mirant gone, Southern Company created Southern Power in 2001, a wholesale generation subsidiary that would build and operate power plants for the competitive market—but without the trading desks and derivatives that had made Southern Energy so dangerous. Southern Power would be Southern Company's way of playing in deregulated markets while maintaining its boring utility reputation. It was a Goldilocks strategy: not too regulated, not too wild, just right for a company that had learned hard lessons about the dangers of straying too far from its roots.

The deregulation era had taught Southern Company a crucial lesson: it was good at building and operating infrastructure, decent at competing in free markets, but terrible at high-stakes financial engineering. The company that entered the 21st century had tried on different corporate identities—international conglomerate, energy trader, telecommunications provider—before settling back into what it knew best: being a regulated monopoly with just enough competitive operations to keep things interesting. But even as it retreated to safer ground, storm clouds were gathering. Climate change was becoming impossible to ignore, and Southern Company was about to find itself on the wrong side of history.

V. The Climate Wars & Denial Machine (1990s-2015)

The story begins with an email that shouldn't exist. February 2009: Willie Soon, an aerospace engineer masquerading as a climate scientist at the Harvard-Smithsonian Center for Astrophysics, writes to a Southern Company executive about his latest research product. "I am finishing a big, super-duper" report on how the sun affects climate, Soon gushes, like a contractor updating a client on kitchen renovations. What makes this email remarkable isn't Soon's enthusiasm—it's that he's describing peer-reviewed scientific research as a commercial deliverable, complete with corporate oversight and pre-publication review rights.

Between 1993 and 2004, Southern Company paid over $62 million to special interest groups and outside firms involved in campaigns against climate science and policies. To put that in perspective, Exxon paid over $33 million to such groups over a period of 18 years. Southern Company, the utility that powered air conditioners and strip malls across the Southeast, was outspending Big Oil in the climate denial business by nearly two-to-one.

This wasn't ignorance—it was betrayal. As early as 1980, a report circulated to Southern Company's research division warned that "fossil fuel combustion" was rapidly warming the atmosphere and could cause a "massive extinction of plant and animal species" along with a "5 to 6-meter rise in sea level." The company's own scientists participated in conferences throughout the 1980s where climate change was discussed as established fact. Southern acknowledged in a 2016 statement that it had "committed substantial financial and human resources" since the 1960s to the question of reducing carbon emissions.

Yet even as Southern Company's engineers studied climate science, its executives funded an elaborate denial machine. Southern Company funded five of Willie Soon's research projects for a total of $469,560 since 2005. The contracts included something extraordinary for academic research: clauses giving the company pre-publication review rights—"Smithsonian shall provide SCS an advance written copy of proposed publications regarding the deliverables for comment and input." Soon would later describe his papers to Southern Company as "deliverables" when writing journal articles or testimony before the U.S. Congress.

The Edison Electric Institute, the utility industry's main trade group, received nearly $20 million from Southern Company between 1993 and 2004. What did that money buy? EEI helped create one of the first media campaigns designed to "directly attack the proponents of global warming." Meanwhile, Southern Company worked with the Center for Energy and Economic Development, giving at least $200,000 to spread pro-coal messages to the public.

The campaign went beyond funding think tanks. In the mid-1990s, Southern Company and the Center for Energy and Economic Development targeted hundreds of teachers with workshops that promoted coal industry messages about the environment and climate change. Picture it: Southern Company executives standing before classrooms of science teachers, handing out materials that claimed carbon dioxide was plant food, not pollution. These weren't debates—they were indoctrination sessions, designed to plant seeds of doubt in the minds that would shape the next generation.

Southern Company's climate denial operation was both brazen and sophisticated. While Exxon tried to maintain plausible deniability by funding groups at arm's length, Southern Company executives directly managed their disinformation contractors. Willie Soon was emailing Southern Company his "deliverables"—or in other words, what Southern Company wanted Soon to publish. The relationship was so cozy that Soon and Harvard-Smithsonian pledged not to disclose Southern's role as a funder without permission.

The hypocrisy reached absurd heights. In 1985, a paper presented at a conference co-chaired by a Southern Company official concluded that "Control of emissions by the collection of gas from the stack is not a solution to the global build-up of carbon dioxide in the atmosphere." Southern Company knew carbon capture wouldn't work. Yet two decades later, they bet billions on the Kemper "clean coal" plant in Mississippi, complete with carbon capture technology that their own scientists had dismissed as ineffective.

CEO Tom Fanning became the face of Southern Company's climate denial in the 2010s. As late as 2017, Fanning claimed on CNBC that climate change has been "happening for millennia" and denied that CO2 was primarily responsible. This wasn't just any executive spouting nonsense—Fanning was the highest-paid utility executive in the country, receiving almost $28 million in 2019. When you're making that much money keeping the lights on, apparently the truth becomes negotiable.

The Willie Soon saga finally imploded in 2015 when documents obtained through Freedom of Information Act requests revealed the full extent of his corporate funding. From 2005 to 2015, Soon had received over $1.2 million from the fossil fuel industry, while failing to disclose that conflict of interest in most of his work. The revelations were so damaging that Southern Company announced it would no longer fund Soon's work, with spokesman Jack Bonnikson stating their agreement would expire with "no plans to renew it."

But the damage was done. As Dave Anderson of the Energy and Policy Institute observed: "A significant portion of our elected officials in Washington, and even of the US population, still thinks that climate change caused primarily by human activities isn't a real thing. And that's largely due to the seeds of doubt that were planted by Southern Company and others." Southern Company had helped create an alternate reality where climate science was controversial, where carbon dioxide was plant food, where the sun caused global warming—a reality that persists in certain corners of American politics to this day.

The climate denial machine Southern Company built wasn't just about protecting coal plants or gas pipelines. It was about protecting a business model where guaranteed returns on capital investment meant the more you built, the more profit you made—regardless of whether the planet could afford it. Every ton of CO2 emitted, every climate scientist discredited, every confused voter—it all served to extend the life of Southern Company's carbon-intensive assets and delay the reckoning that renewable energy would bring. In this twisted logic, funding climate denial wasn't a moral failure; it was fiduciary duty.

VI. The AGL Resources Mega-Deal (2015-2016)

The board meeting at Southern Company's Atlanta headquarters on August 24, 2015, had the gravity of a wartime cabinet session. Outside, natural gas prices had cratered to $2.60 per million BTU, down from $13 just seven years earlier. Fracking had unleashed a tsunami of cheap gas that was crushing coal plants across America—including Southern Company's own fleet. CEO Tom Fanning stood before his directors with a proposition that would have seemed insane a decade earlier: let's double down on the very commodity that's killing our legacy business. Let's buy AGL Resources, the second-largest natural gas utility in America, for $12 billion.

The numbers were staggering even for a company accustomed to billion-dollar bets. Southern Company would pay $8 billion in equity value plus assume $4 billion in AGL debt—the second-largest acquisition in the utility sector's history. Each AGL shareholder would receive $66 in cash per share, a 38% premium to the stock's trading price. For a company that had spent decades as a collection of sleepy regulated electric utilities, this was transformation by checkbook—instant metamorphosis from electron merchant to molecule mogul.

Fanning's pitch to the board was elegant in its simplicity: "We're not betting against our electric business; we're betting on America's energy future requiring both." The shale revolution had made natural gas abundant and cheap. Environmental regulations were making coal plants uneconomic. Gas turbines could ramp up and down to balance intermittent renewables. And most importantly, gas distribution was just as much a regulated monopoly as electric distribution—same guaranteed returns, same captive customers, just different pipes.

AGL Resources wasn't just any gas company. From its Atlanta headquarters (conveniently located just miles from Southern Company's own), it operated eleven gas distribution utilities across seven states, serving 4.5 million customers from Illinois to Virginia. Its crown jewel was Atlanta Gas Light, the largest natural gas distributor in the Southeast, plus Nicor Gas serving Chicago's suburbs, and Virginia Natural Gas serving the booming Hampton Roads region. AGL also owned pieces of gas pipelines, storage facilities, and even some retail energy marketing businesses—a fully integrated gas value chain.

The strategic logic was compelling, at least on PowerPoint. Post-merger, Southern Company would become America's premier energy infrastructure company, serving 9 million electric and gas customers across eleven states. The company would own nearly 200,000 miles of electric transmission and distribution lines plus 80,000 miles of gas pipelines—an energy delivery network so vast that it would touch one in eight American households. As Fanning told analysts, Southern Company was now "positioned to deliver even greater customer and shareholder value by playing offense in developing the infrastructure necessary to meet America's growing demand for natural gas."

But beneath the corporate speak lay a more existential calculation. Southern Company's traditional business model—building big coal and nuclear plants and earning guaranteed returns on them—was dying. The Vogtle nuclear disaster was already billions over budget. The Kemper "clean coal" catastrophe in Mississippi was heading toward abandonment. Coal plants were shutting down across the system. The company needed a new growth story, and natural gas distribution offered the same boring, predictable, regulated returns that had made Southern Company a dividend aristocrat for decades. It was diversification disguised as doubling down.

The deal's financing was a masterclass in utility financial engineering. Southern Company issued $5.6 billion in new debt and $2.4 billion in equity, carefully structured to maintain its investment-grade credit rating. The company promised $200 million in annual synergies by year five—mostly from the corporate euphemism of "optimizing shared services and eliminating redundancies," which everyone knew meant layoffs. The deal would be immediately accretive to earnings per share, that magical metric that makes Wall Street purr.

On July 1, 2016, the merger closed with surprisingly little drama. Regulators in multiple states had blessed the combination, viewing it as creating a stronger utility better able to invest in infrastructure. Environmental groups had lodged predictable protests about Southern Company's climate record, but couldn't stop a deal between two companies that already operated as regulated monopolies. At the closing ceremony in Atlanta, Fanning rang a ceremonial bell as AGL Resources officially became Southern Company Gas.

The integration, however, proved messier than the spreadsheets had suggested. AGL's gas utilities operated under different regulatory regimes than Southern Company's electric utilities. Illinois' regulatory environment was far more contentious than Georgia's cozy commission. Labor unions at Nicor Gas didn't appreciate Southern Company's more paternalistic management style. And coordinating gas and electric operations—supposedly a key synergy—turned out to be harder when the two systems had been built independently over a century with incompatible IT systems, different safety protocols, and distinct corporate cultures.

More fundamentally, Southern Company discovered that gas distribution, while steady, wasn't a growth business. Unlike electricity demand, which was starting to surge from data centers and EVs, residential gas demand was flat to declining as homes became more efficient and some cities began pushing electrification. The company found itself owning a massive gas infrastructure network just as the conversation was shifting to whether that network would become stranded assets in a decarbonizing economy.

Yet the AGL acquisition succeeded in one crucial way: it bought Southern Company time. Time to figure out its nuclear disaster at Vogtle. Time to shut down coal plants without cratering earnings. Time to build renewable projects through Southern Power. Time to navigate the energy transition while still paying that sacred dividend that had increased every year since 1948. The company that emerged from the AGL merger wasn't the Southern Company of James Mitchell's hydroelectric dreams or the coal-powered titan of the 20th century. It was something new: an energy infrastructure conglomerate trying to be everything to everyone—electric and gas, carbon and clean, past and future—all while collecting regulated returns on every pipe, wire, and meter in between.

VII. Vogtle Nuclear Saga: America's Last Big Nuclear Bet (2006-2024)

The PowerPoint slide that Southern Nuclear CEO Steve Kuczynski showed to the board in 2006 was beautiful in its simplicity. Two new Westinghouse AP1000 reactors at Plant Vogtle. Total cost: $14 billion. Online by 2016 and 2017. Clean, baseload power for Georgia for the next sixty years. The first new nuclear plants in America since the 1970s, proving that nuclear power could be economically built again. It was going to be Southern Company's crowning achievement, the project that would define its legacy in the 21st century. Eighteen years and $35 billion later, that slide would become Exhibit A in the largest construction disaster in utility history.

The story really begins in 2005, when Congress passed the Energy Policy Act with loan guarantees for new nuclear plants—essentially de-risking nuclear construction with federal backing. Southern Company, still haunted by the original Vogtle units that had cost nine times their original budget, saw an opportunity for redemption. The new AP1000 design from Westinghouse was supposed to be different: modular construction, passive safety systems, standardized components that could be built in factories and assembled on-site like Legos. Nuclear power's iPhone moment.

Southern Nuclear spent 2006 and 2007 developing the project with a consortium of partners: Georgia Power would own 45.7%, Oglethorpe Power 30%, MEAG Power 22.3%, and Dalton Utilities 1.6%. The partnership structure spread the risk but also created a hydra of decision-making that would prove problematic when things went wrong. Each partner had different risk tolerances, different regulatory oversight, different constituencies to answer to. But in 2006, with natural gas prices spiking and climate concerns growing, everyone wanted in on nuclear's renaissance.

The first red flag came before construction even began. In February 2012, when the Nuclear Regulatory Commission voted to approve Vogtle's construction license, Chairman Gregory Jaczko cast the lone dissenting vote. His reason? The NRC was approving the project without requiring Fukushima-inspired safety upgrades to be completed first. "I cannot support issuing this license as if Fukushima never happened," Jaczko said. The four other commissioners overruled him, and Southern Company got its license to build. The industry celebrated; Jaczko was later pushed out of the NRC.

Construction began with a ceremony in March 2013, where Georgia Governor Nathan Deal operated a bulldozer for the cameras. Southern Company CEO Tom Fanning promised the plant would showcase "American innovation and leadership." What it actually showcased was American industrial decline. The modular construction that was supposed to revolutionize nuclear building immediately ran into problems. Modules arrived on site with wrong dimensions. Welds failed inspections. Rebar was installed incorrectly and had to be jackhammered out.

The real catastrophe came in March 2017: Westinghouse, the project's primary contractor and designer of the AP1000 reactor, filed for Chapter 11 bankruptcy. The company had been hemorrhaging money on both Vogtle and the V.C. Summer project in South Carolina (which would ultimately be abandoned after $9 billion spent). Westinghouse's bankruptcy left Southern Company with a half-built nuclear plant, no contractor, and a technology that only Westinghouse fully understood. It was like being halfway through building a rocket to Mars when NASA suddenly disbanded.

Southern Nuclear made the fateful decision to take over construction itself, hiring Bechtel as the primary contractor. This was like a homeowner firing their general contractor mid-renovation and deciding to oversee the subcontractors directly—except the home was a nuclear power plant and the subcontractors numbered in the thousands. Bechtel, one of the few companies on Earth capable of managing such complexity, essentially wrote its own terms: cost-plus contracts with limited liability for delays.

Then came the documentation crisis that would define Vogtle's middle years. In 2018, Southern Nuclear discovered that inspection records for critical components were either incomplete or missing entirely. The backstory was tragicomic: various subcontractors had been doing inspections but not properly documenting them, assuming someone else was keeping records. Others had kept records but in incompatible systems that couldn't talk to each other. Some records were on paper in shipping containers; others were in Excel spreadsheets on personal laptops. The result was a backlog of more than 10,000 inspection records that needed to be reconstructed, verified, or redone.

The Nuclear Regulatory Commission was not amused. Work ground to a halt as Southern Nuclear brought in armies of consultants to recreate the paper trail that would prove the plant was being built safely. Components that had already been installed had to be re-inspected. Concrete that had been poured years earlier had to be X-rayed to verify rebar placement. The documentation crisis alone added two years and billions in costs.

By 2021, the Georgia Public Service Commission was holding emergency hearings every few months as costs spiraled and deadlines whooshed by. Commissioner Tim Echols, usually a reliable Southern Company ally, publicly questioned whether they should just abandon the project. The answer always came back the same: we're too far in to quit now. The sunk cost fallacy had become official regulatory policy. Besides, Southern Company argued, America needed this nuclear capacity for the coming wave of electric vehicles and data centers.

The human toll was enormous. Construction workers—at peak, over 9,000 of them—worked in brutal Georgia heat and bitter winter cold, putting in 60-hour weeks for years. Several died in construction accidents. Thousands of engineers spent their entire careers on this one project. Marriages collapsed under the strain of constant overtime. The town of Waynesboro, Georgia, nearest to the plant, went through boom and bust cycles as construction ramped up and down with various crises.

When Unit 3 finally achieved first criticality in March 2023—sending neutrons bouncing through uranium for the first time—it was almost anticlimactic. The control room operators, some of whom had been training on simulators for a decade waiting for this moment, later described feeling not triumph but relief. The reactor reached full commercial operation on July 31, 2023, seven years late. Unit 4 followed on April 29, 2024.

The final numbers were staggering: $35 billion total cost versus the original $14 billion estimate. Georgia Power's share alone ballooned from $6.1 billion to over $16 billion. Customer bills would rise by over $200 per year to pay for the plants. The cost per kilowatt of capacity was over $15,000—more than ten times the cost of solar or wind. By any financial metric, Vogtle was a disaster that would take decades for ratepayers to digest.

Yet Southern Company spun it as victory. These were the first new nuclear reactors in America in thirty years! They would generate carbon-free power for the next sixty to eighty years! They proved America could still build big things! Fanning called it "a testament to our commitment to a clean energy future." Critics called it the most expensive power plant ever built in the Western Hemisphere, a monument to sunk cost fallacy and regulatory capture.

The real tragedy of Vogtle wasn't just the money—it was the opportunity cost. $35 billion could have built enough solar and wind to power millions of homes, with enough left over for batteries to store it. It could have retrofitted hundreds of thousands of buildings for efficiency. It could have built a charging network for electric vehicles across the entire Southeast. Instead, it built two reactors that will generate power at costs far above market rates for their entire operational lives.

Vogtle's legacy extends beyond Southern Company. The V.C. Summer abandonment and Vogtle's catastrophic overruns essentially ended nuclear power's renaissance in America. No utility CEO looking at Vogtle's saga would propose a new nuclear plant to their board. The AP1000 design that was supposed to revolutionize the industry became its tombstone. Westinghouse, once the pride of American nuclear engineering, emerged from bankruptcy a shadow of itself. The nuclear construction workforce that had been painstakingly rebuilt was again scattered to the winds.

For Southern Company, Vogtle became a defining paradox: a massive strategic failure that the regulatory system transformed into a financial success. Because of Georgia's construction-work-in-progress rules, customers paid for the plant as it was being built, reducing financing costs. Because of regulatory guarantees, Southern Company would earn returns on every dollar spent, no matter how wastefully. The company that had funded climate denial for decades had built America's largest source of new carbon-free power—not out of environmental conviction, but because the regulatory math made even a catastrophically over-budget nuclear plant profitable. In the end, Vogtle proved that in the world of regulated utilities, there's no such thing as failure—only different levels of customer burden.

VIII. Modern Era: The Clean Energy Pivot (2016-Present)

Tom Fanning stepped up to the podium at Southern Company's 2018 investor day with the confidence of a man who'd just gotten away with murder. Vogtle was hemorrhaging billions, but the stock was near all-time highs. The company had spent decades denying climate science, but here was Fanning announcing a "transition to clean energy." The pivotal moment came when he unveiled the new target: net-zero greenhouse gas emissions by 2050. The audience of Wall Street analysts barely blinked. They'd seen this movie before—Big Tobacco becoming "health conscious," Big Oil going "Beyond Petroleum." Now it was Big Utility's turn to launder its reputation through carefully crafted promises about a distant future.

The transformation's urgency came from an unexpected source: data centers. By 2020, conversations with Amazon, Microsoft, and Google had shifted from polite inquiries to desperate pleas. These tech giants needed massive amounts of reliable power for their AI ambitions, and they needed it now. A single new data center campus could require 500 megawatts—enough to power a small city. Georgia, with its favorable tax treatment and Southern Company's reliable grid, became the Saudi Arabia of compute power. But there was a catch: these tech companies had their own climate commitments, and they wouldn't sign deals with a utility still burning coal like it was 1950.

Southern Company's response was swift and cynical: shut down the coal plants that were becoming uneconomic anyway, replace them with natural gas (which it now owned plenty of after the AGL acquisition), sprinkle in some solar farms for the press releases, and call it a clean energy transition. Between 2016 and 2024, the company announced the retirement of over half its coal fleet—21 units totaling 8,000 megawatts. Each closure was presented as climate leadership, though the reality was simpler: gas was cheaper, and the coal plants needed expensive upgrades to meet EPA standards.

The solar boom that followed was genuinely impressive, even if motivated by economics rather than environmentalism. Southern Power, the company's wholesale generation subsidiary, became one of America's largest solar developers, adding over 10,000 megawatts of renewable capacity to its portfolio. The installations were massive—thousand-acre solar farms in rural Georgia, Alabama, and Mississippi that looked like lakes of black glass from the air. The company learned to speak the language of environmental, social, and governance (ESG) investing, hiring sustainability officers and publishing glossy reports about its "commitment to communities."

But the real action was in natural gas. Post-AGL acquisition, Southern Company controlled gas from wellhead to burner tip. Southern Company Gas operated pipelines that brought gas from Texas and Louisiana. Southern Power built gas turbines that could ramp up when solar production dropped. Georgia Power sold that electricity to customers who also bought gas from Southern Company Gas for their furnaces and water heaters. It was vertical integration that would make Rockefeller jealous, all blessed by regulators who saw gas as the "bridge fuel" to a clean energy future.

The regulatory game had evolved but hadn't fundamentally changed. Southern Company mastered the new rules with its old playbook. When Georgia's Public Service Commission considered new renewable mandates, Southern Company lobbyists argued for "flexibility" and "reliability," code words for keeping gas plants running. When Alabama regulators examined solar policies, Alabama Power imposed punitive fees on rooftop solar customers, claiming they weren't paying their "fair share" for grid maintenance. The message was clear: we'll build clean energy, but on our terms and our timeline.

The grid itself became a profit center disguised as modernization. Southern Company launched massive "grid resilience" programs, replacing poles, upgrading substations, and installing smart meters. Each investment added to the rate base on which the company earned its guaranteed return. The smart meters were particularly clever—marketed as giving customers "control" over their energy use, they actually gave Southern Company granular data on consumption patterns and the ability to implement time-of-use pricing that shifted costs to captive customers.

Hurricane Michael in 2018 and Hurricane Sally in 2020 provided perfect cover for accelerated infrastructure spending. Climate change—which Southern Company had spent millions denying—now justified billions in grid hardening. The irony was lost on no one except apparently Southern Company's executives, who spoke earnestly about "preparing for extreme weather events" without acknowledging their role in creating them.

By 2023, Southern Company had achieved something remarkable: it had become a clean energy leader while remaining one of America's largest carbon emitters. The company ranked 163rd on the Fortune 500 with 31,300 employees and a market cap approaching $100 billion. Its stock had outperformed the S&P 500, its dividend had grown for 22 consecutive years, and ESG funds were buying shares despite the company's history. The transformation was complete—at least on paper.

The numbers told a different story. Despite all the solar farms and coal plant closures, Southern Company still generated over 50% of its electricity from natural gas. Its carbon emissions had declined but remained massive—over 100 million metric tons annually. The net-zero by 2050 pledge came with enough caveats and conditions to render it meaningless: it depended on technologies that didn't exist, regulations that hadn't been written, and economic conditions that couldn't be predicted.

CEO Chris Womack, who succeeded Fanning in 2021, brought a different style but the same substance. Where Fanning had been bombastic, Womack was technocratic. He spoke fluently about distributed energy resources, microgrids, and beneficial electrification. But the underlying strategy remained unchanged: maintain the regulated monopoly, maximize capital deployment, and manage the energy transition slowly enough to protect existing assets.

The modern Southern Company is a testament to institutional resilience. It has survived deregulation, climate science, distributed solar, and its own nuclear disaster. It has transformed from a coal-burning climate denier to a clean energy champion without fundamentally changing its business model. It continues to earn regulated returns on every dollar invested, whether in solar panels or gas pipelines, smart meters or nuclear concrete.

The next decade will test whether this resilience can continue. The Inflation Recovery Act has unleashed hundreds of billions in clean energy subsidies that could destabilize traditional utility economics. Distributed energy resources—rooftop solar, home batteries, electric vehicles—threaten the centralized grid model. Climate change keeps delivering hundred-year storms every few years, and each one costs billions to recover from. Most fundamentally, a new generation of customers and regulators might question whether regulated monopolies should exist at all in an age of abundant renewable energy and digital grid management. Southern Company's answer, as always, will be to adapt just enough to survive while changing as little as possible. It's worked for over a century. Whether it works for another remains to be seen.

IX. Playbook: Business & Regulatory Lessons

Every Thursday afternoon, the five commissioners of the Georgia Public Service Commission gather in a nondescript building in Atlanta to decide how much Georgians will pay for electricity. The meetings are public, technically, though they're scheduled at times when working people can't attend and filled with jargon that would stump most lawyers. The commissioners—elected in statewide races that draw less attention than county sheriff contests—wield more economic power than most legislators. They decide what Southern Company can charge, what it can build, and what returns it can earn. And for the past forty years, with rare exceptions, they've decided in Southern Company's favor.

This is the first lesson in Southern Company's playbook: regulatory capture isn't about corruption—it's about correlation. The commissioners don't need to be bribed when they already share Southern Company's worldview. They attend the same churches, send their kids to the same schools, belong to the same country clubs. When Southern Company proposes a new gas plant, the commissioners see jobs and economic development. When environmental groups propose renewable mandates, they see California-style blackouts and higher bills. The capture is cultural, not criminal.

Southern Company perfected this system through what it calls "constructive regulatory relationships"—a euphemism for a complex ecosystem of influence. The company employs more lobbyists in state capitals than most states have utility regulators. These aren't the cigar-chomping influence peddlers of Hollywood imagination; they're policy experts who draft legislation, former regulators who know where the bodies are buried, and lawyers who can make any rate increase sound reasonable. They don't win by fighting; they win by framing the debate.

Take the concept of "used and useful"—a regulatory principle that utilities should only earn returns on assets actually serving customers. Southern Company transformed this consumer protection into a profit center through something called Construction Work in Progress (CWIP). Under CWIP, customers pay for power plants while they're being built, reducing financing costs and transferring risk from shareholders to ratepayers. When Vogtle exploded from $14 billion to $35 billion, Georgia customers paid as they went, turning a construction disaster into a financial success. The genius wasn't getting CWIP approved—it was making it seem like common sense.

Capital allocation in the regulated utility world follows different rules than any MBA program teaches. In normal businesses, you want to minimize capital expenditure and maximize returns. In Southern Company's world, the opposite is true: the more capital you deploy, the more absolute dollars you earn. Spending $100 million to generate the same power as a $50 million plant literally doubles your profit. This perverse incentive explains why Southern Company's infrastructure projects consistently run over budget—there's no penalty for inefficiency when customers pay the bill.

The political influence strategy operates on multiple levels simultaneously. At the federal level, Southern Company plays both sides, contributing to Republicans who oppose renewable mandates and Democrats who support nuclear subsidies. At the state level, the company doesn't just lobby legislators—it helps elect them, contributing to campaigns through a maze of PACs and dark money groups. At the local level, Southern Company is often the largest employer and taxpayer, giving it effective veto power over any policy it opposes.

But the real mastery is in crisis management. When Vogtle's costs spiraled, Southern Company didn't deny or deflect—it embraced the sunk cost fallacy as strategy. Every quarterly update emphasized how much had already been spent, how close they were to completion, how stopping now would waste billions. They turned their failure into a hostage situation: finish the plant or lose everything. Regulators, faced with explaining billions in stranded costs to voters, chose the path of least resistance—keep building and pray.

The climate denial saga revealed another aspect of the playbook: when caught, pivot without apologizing. Southern Company never admitted wrongdoing for funding Willie Soon or climate denial campaigns. Instead, it simply started talking about clean energy and net-zero targets. No mea culpa, no reckoning, just a smooth transition from "climate change isn't real" to "we're leading on climate change." The media, focused on the next quarter's earnings, largely let them get away with it.

Managing mega-projects like Vogtle requires a particular kind of institutional psychopathy. You need thousands of people to keep working on something everyone knows is a disaster. Southern Company achieved this through compartmentalization—each team focused on their narrow piece, nobody empowered to see the whole picture except executives who were incentivized to keep going. When problems arose, they were treated as technical challenges rather than systemic failures. When whistleblowers spoke up, they were managed out. When regulators asked tough questions, they were buried in data.

The infrastructure monopoly moat is Southern Company's ultimate protection. You can compete with a product or service, but you can't compete with poles and wires, pipes and meters. Every solar panel needs grid connection. Every gas appliance needs pipeline delivery. Even if technology disrupts the generation side of the business, Southern Company still owns the delivery system—and earns regulated returns on every piece of it. It's the toll road model applied to electrons and molecules.

Balancing stakeholders—shareholders, ratepayers, regulators, politicians—requires careful choreography. Shareholders get steady dividends and predictable growth. Ratepayers get reliable service and gradual rate increases that seem reasonable in isolation. Regulators get compliance and respect for their authority. Politicians get jobs, tax revenue, and campaign contributions. Everyone gets something, and nobody gets everything. The system perpetuates itself because everyone has incentives to maintain it.

The most sophisticated element of Southern Company's playbook is its approach to innovation—adopt it just fast enough to claim leadership but slow enough to protect existing assets. The company builds solar farms while fighting rooftop solar. It promotes electric vehicles while maintaining gas infrastructure. It speaks the language of disruption while ensuring nothing actually gets disrupted. It's corporate jujitsu—using the energy of change to maintain stasis.

This playbook has worked for over a century, surviving technological disruption, regulatory reform, and social transformation. But its greatest vulnerability might be transparency. As information becomes more accessible and customers more engaged, the comfortable assumptions that underpin the regulated utility model—that monopolies are natural, that regulators are neutral, that costs are justified—face increasing scrutiny. Southern Company's playbook assumes a passive public and captured regulators. Whether those assumptions hold in an age of climate activism and distributed energy remains the billion-dollar question.

X. Analysis & Investment Case

Let's talk about money—specifically, the beautiful, boring predictability of Southern Company's financial model. The company generates about $25 billion in annual revenue with the excitement of watching grass grow, and that's exactly why certain investors love it. Return on equity hovers around 10-12%, right in the sweet spot that regulators allow. The dividend yield sits around 3.5-4%, and has increased every year since 2001. Free cash flow consistently covers the dividend with room to spare. For investors seeking utility exposure, Southern Company is the McDonald's of the sector—not exciting, not healthy, but absolutely reliable.

The rate base—that magical number on which Southern Company earns its regulated returns—is approaching $70 billion and growing at 6-7% annually. Every dollar spent on grid modernization, every smart meter installed, every gas pipeline upgraded adds to this number. Management guides for 5-6% earnings per share growth through 2027, which in utility-speak means "we'll hit this unless the world ends." The company's credit ratings (Baa2/BBB+/BBB+) are investment grade, allowing cheap debt financing that juices equity returns.

But here's where it gets interesting—or concerning, depending on your perspective. Southern Company trades at about 18-19x forward earnings, a premium to peers like Duke Energy (16x) or Dominion (17x) but a discount to NextEra Energy (24x), the renewable energy darling. The market is essentially saying Southern Company is better than traditional utilities but not as good as clean energy pure plays. This valuation limbo reflects the company's awkward position—too carbon-heavy for ESG funds, too renewable-friendly for value investors.

The bull case writes itself. America is about to experience an electricity demand super-cycle driven by data centers, AI, electric vehicles, and reshoring of manufacturing. Southern Company sits in the Southeast, the fastest-growing region in America, where tech companies are building massive data centers and auto manufacturers are constructing EV plants. Georgia alone has announced over $30 billion in new industrial investment since 2020. Every new factory, data center, and subdivision needs Southern Company's electrons and molecules.

The infrastructure angle is even more compelling. The U.S. grid is ancient, creaking, and wholly inadequate for a electrified economy. The Department of Energy estimates $2 trillion in grid investment needed by 2050. For Southern Company, this is pure rate base growth—guaranteed returns on essential spending that regulators can't deny. The Inflation Reduction Act has unleashed hundreds of billions in subsidies that Southern Company is uniquely positioned to capture, from nuclear production tax credits for Vogtle to renewable energy incentives for Southern Power.

The regulatory moat remains formidable. It would take literal acts of Congress to disrupt Southern Company's monopoly position, and even then, the company would likely be compensated for stranded assets. The political reality—Southern Company operates in red and purple states where free-market rhetoric paradoxically protects regulated monopolies—provides additional protection. No Georgia politician will seriously challenge the state's largest utility when it employs 31,000 people and powers the state's economic development.

But the bear case has teeth. Start with stranded asset risk. Southern Company still has $15 billion in net coal and gas plant assets that could become worthless if decarbonization accelerates. The company's net-zero pledge for 2050 is essentially an admission that its current infrastructure will eventually be abandoned. Who pays for these stranded assets—shareholders or ratepayers—will be the regulatory fight of the next decade.

Distributed energy presents an existential threat dressed as an opportunity. Every rooftop solar installation, every home battery, every vehicle-to-grid capable EV weakens the centralized utility model. Southern Company responds by imposing fees on solar customers and lobbying against net metering, but these are fingers in the dam. The technology curve is relentless—solar and battery costs keep falling while utility rates keep rising. At some point, grid defection becomes economically rational for large customers.

The climate transition creates massive execution risk. Southern Company needs to simultaneously shut down fossil plants, build renewables, upgrade the grid, and maintain reliability—all while keeping rates politically acceptable. One mistimed plant closure leading to blackouts could trigger regulatory backlash. One renewable project disaster could make Vogtle look cheap. The company is essentially rebuilding itself while flying, and the margin for error is thin.

ESG considerations are increasingly schizophrenic. Some funds exclude Southern Company for its carbon footprint and history of climate denial. Others include it as a transition play, betting the company can transform from brown to green. This uncertainty creates volatility—ESG fund flows have become a major driver of utility valuations, and Southern Company sits in the uncomfortable middle where it could be expelled or embraced depending on ever-changing ESG criteria.

Competition is evolving in unexpected ways. It's not just NextEra Energy building renewables anymore. Tech giants like Amazon and Google are becoming power developers, building their own renewable projects and negotiating directly with grid operators. Industrial customers are exploring microgrids and cogeneration. Even cities are considering municipalization, buying out investor-owned utilities to control their energy future. Southern Company's monopoly isn't under direct attack, but it's being nibbled at the edges.

The valuation math suggests Southern Company is priced for modest success but not transformation. At current multiples, the market expects the company to execute its capital plan, maintain its dividend growth, and navigate the energy transition without major disruption. Any deviation—a regulatory revolt, a stranded asset write-down, a dividend cut—would crater the stock. Conversely, successful transformation into a clean energy leader could drive multiple expansion toward NextEra's levels.

For fundamental investors, Southern Company presents a fascinating dilemma. It's a climate villain that's building America's only new nuclear plants. A regulated monopoly facing technological disruption. A dividend aristocrat with massive execution risk. A value stock trading at growth multiples. A Southeast infrastructure play with stranded asset exposure. The investment case ultimately depends on your view of American capitalism's ability to preserve incumbent advantages despite technological and social pressure for change. Southern Company is betting the house that regulated monopolies will endure, that the energy transition will be gradual, and that political influence can overcome economic forces. History suggests they might be right. Physics and economics suggest they might not. At 18x earnings, you're paying a premium to find out.

XI. Epilogue & Future Scenarios

The year is 2035, and Southern Company CEO Sarah Chen (the third CEO since Chris Womack) stands before the same Atlanta auditorium where Tom Fanning once promised a clean energy transition. Behind her, a holographic display shows Southern Company's latest triumph: the successful deployment of the Southeast's first commercial small modular reactor, built on time and on budget—a phrase that would have drawn bitter laughter just a decade earlier. The SMR revolution that Southern Company is now leading makes Vogtle look like a steam engine, but the path to this moment was anything but smooth.

Three scenarios could define Southern Company's next decade, each plausible, each with radically different implications for investors, customers, and the climate.

In the "Fortress Utility" scenario, Southern Company successfully defends its regulated monopoly against all threats. Distributed energy never reaches economic parity with grid power thanks to carefully crafted fees and regulations. Data center demand explodes even beyond current projections, requiring massive baseload capacity that only utilities can provide. Climate change drives demand for resilient, centralized infrastructure that only incumbent utilities can build. Southern Company's stock trades at 25x earnings as investors recognize the irreplaceable value of energy infrastructure monopolies. The company builds SMRs across the Southeast, earning regulated returns on hundreds of billions in new nuclear investment. The energy transition happens, but on Southern Company's timeline and terms.

The "Managed Decline" scenario sees Southern Company as the Kodak of utilities—still existing, still profitable, but fundamentally disrupted. Distributed solar-plus-storage reaches grid parity by 2028, and customers begin defecting en masse. Regulators, facing voter backlash over rising rates, cap returns and force accelerated coal and gas plant closures without full cost recovery. Tech companies build their own microgrids, bypassing utilities entirely. Southern Company's service territory shrinks to a rump of residential customers who can't afford their own generation. The stock trades at 10x earnings as investors flee to pure-play renewables companies. The dividend, that sacred cow, gets cut for the first time since World War II.

The "Green Phoenix" scenario represents transformation through crisis. A category 5 hurricane devastates Southern Company's coastal infrastructure in 2027, causing $20 billion in damage and month-long blackouts. The disaster triggers emergency federal intervention, with Congress passing legislation that effectively nationalizes grid modernization. Southern Company receives hundreds of billions in federal funding but must accept unprecedented federal oversight and mandates for renewable deployment. The company emerges as America's leading clean energy utility, but at the cost of its traditional autonomy. The stock initially crashes, then soars as investors realize the federal backstop has eliminated most risk while guaranteeing returns on the largest infrastructure build-out in history.

Each scenario contains elements already visible today. The SMR technology Southern Company is exploring with Westinghouse and Bill Gates' TerraPower could revolutionize nuclear power—or become Vogtle 2.0. The hydrogen economy Southern Company is positioning for could create massive new demand for electricity—or prove to be thermodynamically doomed. The grid modernization Southern Company is undertaking could cement its monopoly—or enable the very distributed resources that destroy it.

Climate resilience has become Southern Company's unexpected ace card. Every hurricane that knocks out power for a week makes the grid seem more valuable. Every wildfire in California makes Southern Company's reliability look better by comparison. The company has learned to monetize climate change itself, turning the crisis it helped create into a justification for endless infrastructure spending. It's disaster capitalism refined to its purest form—regulated returns on climate adaptation.

The distributed energy threat keeps evolving. Virtual power plants—aggregated home batteries and smart devices—are beginning to provide grid services that only utilities could offer before. Vehicle-to-grid technology could turn every EV into a mobile power plant. Blockchain-based peer-to-peer energy trading could eliminate the need for centralized utilities entirely. Southern Company's response has been to try to own the disruption, offering its own home battery programs and EV charging networks, but always in ways that preserve the centralized grid model.

The political landscape is shifting beneath Southern Company's feet. Young conservatives increasingly see rooftop solar as energy independence. Environmental justice activists are connecting utility rates to racial equity. Climate hawks are targeting utilities as the new Big Tobacco. The comfortable political consensus that protected Southern Company for a century is fracturing. The company's response—hiring more diverse executives, funding community programs, speaking the language of equity—feels cosmetic against these tectonic shifts.

The final wildcard is artificial intelligence—not just as a demand driver through data centers, but as a potential optimizer of energy systems. AI could enable a distributed grid that's more reliable than centralized generation. It could optimize demand response to eliminate the need for peaking plants. It could even automate regulatory proceedings, eliminating the information asymmetry that utilities have exploited for decades. Southern Company is investing in AI, but it's unclear whether it's embracing disruption or trying to control it.

Looking forward, Southern Company embodies the paradox of American infrastructure. It's simultaneously essential and obsolete, innovative and reactionary, public service and private profit. It's building the future while defending the past. It's a climate leader that was a climate denier. It's a regulated monopoly in an age that abhors monopolies. These contradictions aren't sustainable indefinitely—something will give.

The most likely outcome is that Southern Company muddles through, as it always has. It will build some SMRs, though they'll cost more than projected. It will deploy renewables, though slower than climate science demands. It will modernize the grid, though not enough to enable full distributed energy. It will maintain its monopoly, though with gradually eroding margins. It will pay its dividend, though growth will slow. It will survive, though transformed beyond what James Mitchell or any of his successors could have imagined.

The lesson of Southern Company's century-long story isn't about good or evil, progress or reaction. It's about institutional persistence—how organizations with sufficient political power and economic resources can survive almost anything. Southern Company has weathered technological disruption, regulatory upheaval, its own incompetence, and even exposure of its climate denial. It endures not because it's efficient or innovative or even necessary in its current form, but because it has mastered the art of making itself indispensable to the system it helped create.

That system—regulated monopoly capitalism—may be approaching its limits. Climate change, technological disruption, and social pressure are converging in ways that even Southern Company's legendary political influence might not be able to manage. The next decade will test whether a 20th-century utility can evolve into a 21st-century energy company, or whether it will become a fossil in more ways than one. For investors, customers, and the climate, the stakes couldn't be higher. Southern Company's future isn't just about one company—it's about whether America's entire model of infrastructure ownership and operation can survive the transformation ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube