Dollar Tree: The Art of the Dollar

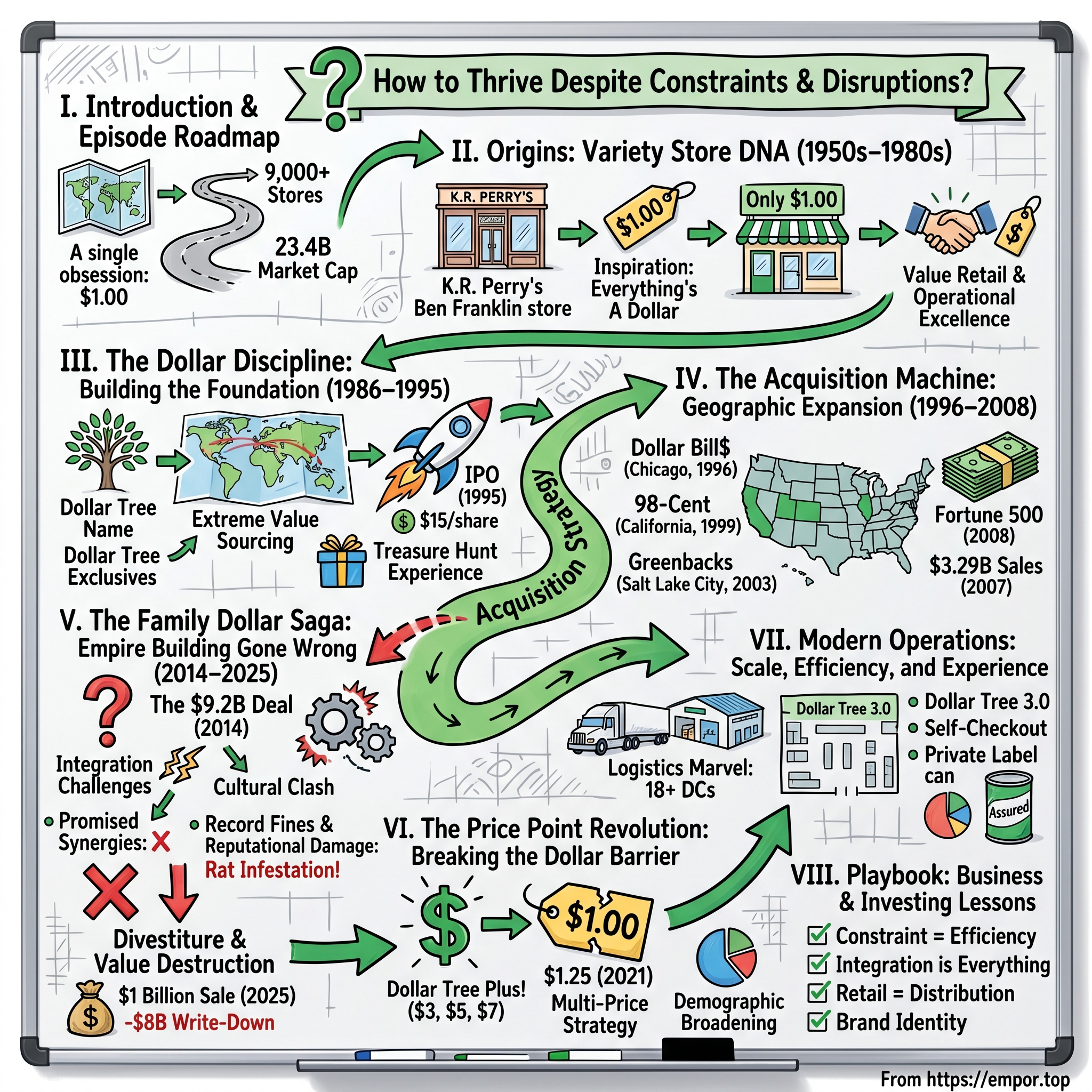

I. Introduction & Episode Roadmap

Picture this: It's 1986, and while America's retail landscape is dominated by sprawling department stores and emerging big-box chains, three men in Norfolk, Virginia are obsessing over a single number—one dollar. Not $0.99. Not $1.49. Exactly one dollar. That obsession would birth Dollar Tree, a retailer that today operates over 9,000 stores across North America with a market capitalization of $23.474 billion.

The story of Dollar Tree isn't just another retail success tale. It's a masterclass in constraint-driven innovation, where a rigid pricing model became the foundation for one of America's most resilient retail empires. While competitors zigged and zagged with pricing strategies, Dollar Tree held the line for 36 years—until inflation finally forced their hand in 2022.

This is the story of how a fixed-price concept evolved from a five-store experiment called "Only $1.00" into a retail phenomenon that redefined value shopping in America. It's about the discipline to say no to conventional wisdom, the audacity to acquire a competitor for $9.2 billion (and later sell it for $1 billion), and the operational excellence required to make money selling everything for a dollar.

We'll journey from K. R. Perry's variety store roots in the 1950s through the company's public offering in 1995, examine their acquisition machine that gobbled up regional chains from coast to coast, dissect the Family Dollar saga that became a cautionary tale in M&A, and explore how breaking the sacred dollar barrier in 2022 might have saved the company.

The core question we're tackling: In an era of Amazon dominance and Walmart's everyday low prices, how did a retailer built on the most rigid pricing constraint imaginable not just survive but thrive through multiple economic cycles, technological disruptions, and changing consumer behaviors?

What Dollar Tree built wasn't just a discount retail chain—it was a supply chain marvel, a real estate arbitrage machine, and a psychological phenomenon wrapped in the simplest possible value proposition. Let's unpack how they did it.

II. The Origins: Variety Store DNA

The roots of Dollar Tree trace back to 1953, when K. R. Perry opened a Ben Franklin variety store in Norfolk, Virginia. These weren't dollar stores—they were classic five-and-dimes, the kind where kids could buy candy for pennies and families could find household essentials without breaking the bank. Perry's store would eventually morph into K&K 5&10, laying the foundation for what would become a retail empire.

By 1970, K. R. Perry had brought his son Doug Perry and Macon Brock into the fold, launching K&K Toys. This wasn't just another toy store chain—it was a laboratory for understanding value retail. Over the next 16 years, the trio scaled K&K Toys to over 130 stores along the East Coast, learning crucial lessons about vendor negotiations, inventory turns, and the psychology of bargain hunting.

The 1980s retail environment was undergoing seismic shifts. Mall culture was peaking, discount chains like Walmart were expanding aggressively, and consumers were becoming increasingly price-conscious following the economic turbulence of the late 1970s. Traditional department stores were losing ground to specialty retailers and discounters. It was in this environment that Doug Perry, Macon Brock, and Ray Compton spotted an opportunity that seemed almost too simple.

The inspiration came from an unlikely source: Everything's A Dollar, a fixed-price retailer that would ironically go bankrupt in the 1990s. But where others saw a gimmick, the K&K team saw genius. The simplicity of the model was intoxicating—no price tags, no confusion, no comparison shopping. Every item, one dollar. They believed they could execute it better, with stronger vendor relationships and more disciplined operations.

In 1986, they launched "Only $1.00" with five stores. The name was literal, almost comically straightforward. But that straightforwardness was the point. In an era of complex pricing strategies and constant sales, they offered radical simplicity. The early days were brutal—convincing suppliers to provide quality merchandise at price points that allowed for profit at a dollar was like solving a three-dimensional puzzle blindfolded.

The challenge wasn't just economic; it was perceptual. How do you convince customers that a store where everything costs a dollar isn't selling junk? How do you convince vendors that you're a serious retailer when your entire business model sounds like a flea market concept? The answer lay in meticulous curation and operational excellence. Every product had to deliver obvious value at the dollar price point. Every store had to be clean, organized, and respectable.

What set Only $1.00 apart from Everything's A Dollar wasn't just better execution—it was the team's variety store DNA. They understood that value retail wasn't just about low prices; it was about the treasure hunt, the discovery, the satisfaction of finding something useful or delightful for almost nothing. This wasn't discount retail; it was entertainment retail at a price point that made it accessible to everyone.

By the late 1980s, it was clear they had something special. Customers were coming back, word was spreading, and the model was proving scalable. The stage was set for the next phase: building the foundation that would support thousands of stores. But first, they needed a better name.

III. The Dollar Discipline: Building the Foundation (1986–1995)

On April 27, 1989, at the Jessamine Mall in Sumter, South Carolina, the first store bearing the "Dollar Tree" name opened its doors. The rebrand from "Only $1.00" wasn't just cosmetic—it signaled ambition. A tree grows, spreads roots, reaches toward the sky. The metaphor was intentional.

The psychology behind fixed-price retail is deceptively complex. At a dollar, the friction of purchase decisions essentially disappears. Customers don't comparison shop within the store. They don't agonize over whether something is worth it. The mental math is binary: do I want this or not? This psychological simplicity drove basket sizes higher than traditional discount retailers. Customers would come in for one item and leave with ten because the incremental cost felt negligible.

But making money at a dollar required operational genius. The economics were brutal: if you're selling everything for a dollar, and you want healthy margins, you need to buy products for 50-60 cents or less. This meant developing direct relationships with manufacturers, often overseas, cutting out middlemen, and achieving massive scale to justify small margins per unit.

In 1991, Doug Perry and Macon Brock made a defining strategic decision: they sold K&K stores to KB Toys, owned by Melville Corporation, and all assets were used to expand dollar stores. This wasn't just divesting a side business—it was burning the boats. The message was clear: we're all-in on the dollar concept.

In 1993, the name Only $1.00 was changed to Dollar Tree Stores to address what could be a multi-price-point strategy in the future. The prescience of this decision wouldn't become apparent for another 26 years, but it showed strategic thinking beyond the immediate model.

The supply chain innovations during this period were nothing short of revolutionary. Dollar Tree pioneered what they called "extreme value sourcing"—working directly with factories in Asia to create products specifically for the dollar price point. This wasn't about finding leftover inventory or damaged goods; it was about engineering products from the ground up to be profitable at a dollar.

They developed relationships with vendors who would create "Dollar Tree exclusives"—products that looked like name brands but were manufactured specifically for their stores. A pack of batteries might have fewer units than the grocery store version. A bottle of shampoo might be 6 ounces instead of 8. The art was making these trade-offs invisible to the consumer while maintaining the perception of value.

In 1995, Dollar Tree went public on the NASDAQ exchange at $15 a share, with market cap calculated at $225 million. For a company selling everything for a dollar, this was validation that Wall Street understood the model. The IPO prospectus revealed impressive metrics: gross margins of 35%, same-store sales growth averaging 8% annually, and a store payback period of less than two years.

The operational discipline required to maintain profitability at the dollar price point created a culture of extreme efficiency. Store layouts were standardized to minimize labor costs. Products were pre-priced at distribution centers. Checkout was simplified—no price checks, no confusion. A new cashier could be productive within hours, not days.

But perhaps the most brilliant innovation was the treasure hunt mentality they cultivated. Unlike traditional retailers who prided themselves on consistency, Dollar Tree made inconsistency a feature. You never knew what you'd find. That uncertainty drove frequency—customers came back weekly to see what was new. The dollar price point removed the risk from impulse purchases, turning shopping into entertainment.

By 1995, Dollar Tree had proven that fixed-price retail wasn't just viable—it was scalable. They had 300 stores generating over $300 million in annual revenue. The foundation was set. Now it was time to grow—and grow they would, through one of the most aggressive acquisition strategies in retail history.

IV. The Acquisition Machine: Geographic Expansion (1996–2008)

In 1996, Dollar Tree acquired Dollar Bill$, Inc., a Chicago-based chain of 136 stores. This wasn't just Dollar Tree's first major acquisition—it was a masterclass in integration. Dollar Bill$ had been struggling, bleeding cash in the hyper-competitive Chicago market. Dollar Tree saw opportunity where others saw disaster. Within 18 months, they had converted all stores to the Dollar Tree banner, improved merchandise mix, and turned the portfolio profitable.

The acquisition playbook they developed with Dollar Bill$ would become their template: identify struggling regional dollar chains, acquire them at distressed valuations, convert them to Dollar Tree's superior operating model, and leverage the expanded footprint for better vendor negotiations. Rinse and repeat.

They broke ground on their first Distribution Center and new Store Support Center in Chesapeake, Virginia in 1997. This 500,000-square-foot facility wasn't just a warehouse—it was the nerve center of their Eastern operations, capable of supporting 500 stores with twice-weekly deliveries. The automation they implemented was cutting-edge for discount retail: conveyor systems that could sort 40,000 cases per day, RF scanning technology for inventory accuracy, and cross-docking capabilities that minimized handling costs.

At the tail end of the 1990s, Dollar Tree acquired the 98-Cent Clearance Centers in California and the Only $One Stores in New York. The California acquisition was particularly strategic—it gave them instant penetration in the nation's largest market and a beachhead for West Coast expansion. The 98-Cent Clearance Centers had prime real estate in strip malls throughout Southern California, locations that would have taken years to secure organically. In 2000, Dollar Tree acquired Dollar Express, a Philadelphia-based company. The deal gave them instant access to the Northeast corridor's dense population centers. In 2003, Greenbacks, Inc., a Salt Lake City company, brought them into the Mountain West. In 2006, they acquired 138 Deal$ stores from SUPERVALU INC., further consolidating their position in the Midwest.

The velocity of expansion was breathtaking. In 2004, Dollar Tree opened its first store in North Dakota which marked its operation of stores in all 48 contiguous states. Think about that—from a regional Virginia chain to nationwide coverage in less than two decades. In 2006, Dollar Tree celebrated its 20th year of retailing at a $1.00 price point, opened its 3,000th store.

The distribution network grew in lockstep with store expansion. By the end of the 2000s, Dollar Tree had opened or purchased seven Distribution Centers in California, Georgia, Pennsylvania, Oklahoma, Illinois, and Washington. Each facility was strategically positioned to serve 400-500 stores within a 400-mile radius, enabling the twice-weekly deliveries that kept stores fresh without excessive backroom inventory.

In 2007, we reached a market cap of $3.29 billion in sales. Finally, in 2008, our organization earned a place on the Fortune 500 list and had the number-one performing stock that year. Let that sink in—during the worst financial crisis since the Great Depression, when banks were collapsing and retailers were declaring bankruptcy, Dollar Tree's stock was the best performer in the entire Fortune 500.

The 2008 financial crisis actually accelerated Dollar Tree's growth. As consumers traded down, Dollar Tree was perfectly positioned to capture new customers who had never shopped dollar stores before. Middle-class families discovered that Dollar Tree wasn't just for the economically disadvantaged—it was for the economically savvy. The stigma of shopping at dollar stores evaporated almost overnight.

The acquisition machine wasn't just about buying stores; it was about buying market knowledge. Each regional chain they acquired brought vendor relationships, real estate expertise, and customer insights that would have taken years to develop organically. They learned what sold in Chicago versus Phoenix, how to negotiate mall leases in California, which distributors had the best closeout deals in the Northeast.

By 2008, Dollar Tree operated over 3,500 stores with sales exceeding $4 billion. They had transformed from a regional player to a national powerhouse, all while maintaining their sacred dollar price point. The foundation was complete, the model was proven, and the company seemed unstoppable. Which made what happened next all the more surprising.

V. The Family Dollar Saga: Empire Building Gone Wrong (2014–2025)

On July 28, 2014, Dollar Tree announced it was offering $9.2 billion for Family Dollar. The news sent shockwaves through retail. Dollar Tree, the disciplined operator that had never paid more than a few hundred million for an acquisition, was suddenly swinging for the fences with a deal that would nearly double its store count overnight.

Family Dollar was a different animal entirely. Founded in 1959, it operated on a multi-price-point model, serving primarily urban and low-income rural markets. Where Dollar Tree stores were clean, bright, and suburban, Family Dollar stores were often dated, cramped, and located in economically challenged neighborhoods. Where Dollar Tree sold discretionary items and seasonal goods, Family Dollar focused on consumables and everyday essentials.

The strategic rationale seemed compelling on paper: immediate scale to negotiate better vendor terms, complementary geographic footprints, and the ability to operate two distinct formats for different customer segments. Wall Street loved it initially—the combined company would be a discount retail juggernaut with over 13,000 stores.

Then Dollar General entered the fray. On August 18, 2014, they lodged a competing bid of $9.7 billion. What followed was one of the nastiest bidding wars in retail history. Dollar General ultimately raised its bid to $80.00 per share, significantly higher than Dollar Tree's $74.50. But there was a catch—antitrust concerns.

The FTC's position was clear: Dollar Tree's acquisition would require divestitures of approximately 300 stores, while a Dollar General deal would require 3,500-4,000 store closures. Family Dollar's board, led by Howard Levine, rejected Dollar General's higher bid, citing execution risk. The decision would prove fateful.

On July 6, Dollar Tree acquired Family Dollar, located in Charlotte, NC. The final price tag: $9.2 billion, creating a combined organization with more than 13,000 stores and sales exceeding $19 billion annually. Bob Sasser, Dollar Tree's CEO, promised investors the deal would be "transformational."

He was right, but not in the way he intended.

The integration challenges surfaced immediately. Family Dollar's IT systems were antiquated—some stores were still using DOS-based point-of-sale systems. Their distribution network was inefficient, with many stores receiving direct vendor deliveries rather than through centralized DCs. Most problematically, Family Dollar's corporate culture was completely different—hierarchical and slow-moving versus Dollar Tree's entrepreneurial and agile approach.

Dollar Tree tried to maintain both brands separately, but the overhead was crushing. They were essentially running two distinct supply chains, two merchandising teams, two real estate departments. The promised synergies of $300 million annually never materialized. Instead, costs ballooned as they tried to renovate Family Dollar stores while maintaining Dollar Tree's expansion.

The customer bases proved incompatible. Dollar Tree shoppers were treasure hunters looking for surprises; Family Dollar customers needed predictable access to milk, bread, and laundry detergent. Dollar Tree's merchants didn't understand Family Dollar's urban customers, leading to tone-deaf product selections. Family Dollar's old guard resented Dollar Tree's management, leading to an exodus of institutional knowledge. The numbers became increasingly dire. Family Dollar stores were hit with a record $41.6 million fine by the Justice Department in 2024 for violating product safety standards after selling items that were stocked in a rat-infested warehouse in West Memphis filled with live, dead and decaying rodents. The reputational damage was catastrophic.

By 2024, activist investors were circling. The company announced a strategic review of Family Dollar in June 2024. The writing was on the wall. On March 26, 2025, Dollar Tree announced the unthinkable: they would sell Family Dollar to Brigade Capital Management and Macellum Capital Management for $1 billion—a fraction of the $9 billion that Dollar Tree paid to acquire Family Dollar in 2015.

The sale completed on July 7, 2025. Net proceeds from the sale totaled approximately $800 million comprised of $665 million paid at closing and approximately $135 million as a result of the monetization of cash prior to closing through a reduction of net working capital. The Company expects the economic impact of tax benefits from losses on the sale to be approximately $375 million.

The Family Dollar saga represents one of the most spectacular value destructions in retail M&A history. An $8 billion write-down over a decade. But here's the paradox: it might have saved Dollar Tree. The distraction of trying to fix Family Dollar had caused them to neglect their core business. Store renovations were delayed. New initiatives were shelved. Management bandwidth was consumed by crisis management.

Now, freed from the Family Dollar albatross, Dollar Tree could return to what it did best: operating clean, efficient dollar stores with a treasure hunt mentality. The lessons were expensive but clear: culture matters more than synergies, operational excellence trumps financial engineering, and sometimes the best deal is the one you don't make.

VI. The Price Point Revolution: Breaking the Dollar Barrier

In May 2019, Dollar Tree launched Dollar Tree Plus!, a 100-store pilot that would fundamentally challenge the company's founding principle. For the first time in 33 years, they would sell items for more than a dollar—specifically, $3 and $5 price points in dedicated front-of-store bays. The purists were horrified. The pragmatists saw survival.

The psychology behind the move was complex. Dollar Tree's research showed that customers were frustrated when they couldn't find certain categories in the store—items that simply couldn't be profitably sold for a dollar anymore. Basic tools, larger home goods, premium seasonal decorations. By adding higher price points, they could expand their addressable market without abandoning their core promise.

The pilot results were encouraging. Same-store sales in Dollar Tree Plus! locations increased by 200-300 basis points compared to traditional stores. More importantly, the higher price points didn't cannibalize dollar sales—they were truly incremental. Customers understood the value proposition: most things for a dollar, some special items for a bit more.

But the real earthquake came in September 2021. CEO Michael Witynski announced what many thought impossible: Dollar Tree would raise its base price from $1.00 to $1.25. After 36 years, the sacred dollar was dead.

The decision wasn't made lightly. Inflation was running at multi-decade highs. Shipping costs had tripled during COVID. Labor costs were skyrocketing as retailers competed for workers. The math simply didn't work anymore at a dollar. Dollar Tree had two choices: raise prices or go out of business.

In 2022, Dollar Tree completed the rollout of its $1.25 price-point initiative to all Dollar Tree stores chainwide in the U.S. This was Dollar Tree's first price change in over 36 years, allowing them to continue offering all the items customers know and love, plus hundreds of new items, all at an incredible value.

Customer reaction was... surprisingly muted. There was grumbling on social media, some local news coverage about the "death of the dollar store," but foot traffic remained stable. Turns out, $1.25 was still an incredible value in an inflationary environment where a cup of coffee cost $5 and a fast-food meal approached $15.

The 25% price increase dropped almost entirely to the bottom line. Gross margins expanded by 400 basis points overnight. The additional capital allowed Dollar Tree to accelerate renovations, expand product assortments, and invest in technology. It was like removing ankle weights from a marathon runner.

The "thrill-of-the-hunt" shopping experience actually intensified with the new price points. At $1.25, Dollar Tree could offer name-brand products that were previously impossible. Real Tide detergent, not a knock-off. Branded snacks and beverages. Quality tools and hardware. The treasure hunt became more rewarding.

By 2024, Dollar Tree had expanded the multi-price strategy to over 6,000 stores. The Dollar Tree Plus! format offered items up to $7, carefully curated to maintain the value perception. A $5 LED flashlight that would cost $15 at Home Depot. A $3 picture frame that Michaels sold for $10. The deals were real, and customers noticed.

The price point revolution revealed a fundamental truth about Dollar Tree's business model: the exact price mattered less than the value perception and shopping experience. Customers didn't shop Dollar Tree because everything was a dollar; they shopped there because everything felt like a steal. As long as that feeling persisted, the model worked.

VII. Modern Operations: Scale, Efficiency, and Experience

Today's Dollar Tree operates at a scale that would have been unimaginable to its founders. With over 9,000 stores across the United States and Canada, they're within 5 miles of 75% of the American population. The company operates with a team of approximately 150,000 associates and 18 distribution centers across 48 contiguous states and five Canadian provinces under the brands Dollar Tree and Dollar Tree Canada.

The logistics network is a marvel of efficiency. Those 24 distribution centers aren't just warehouses—they're highly automated sorting facilities that can process millions of units weekly. Each DC serves approximately 400 stores within a carefully optimized delivery radius. Trucks leave on predetermined schedules, hitting multiple stores per route to maximize efficiency.

The product mix has evolved dramatically from the early days. Today's Dollar Tree carries over 7,000 SKUs across dozens of categories: health and beauty, food and snacks, party supplies, seasonal décor, housewares, toys, craft supplies, and more. Approximately 50% of products are consumables that drive repeat traffic, while the other 50% are variety goods that create the treasure hunt experience.

Private label has become a secret weapon. Brands like Sunny Acres (food), Assured (health), and Crafter's Square (crafts) deliver higher margins while maintaining quality standards. These aren't generic knock-offs—they're carefully developed products that often outperform national brands in blind tests. The Crafter's Square expansion to all U.S. stores in 2020 alone drove a 5% increase in craft category sales.

Technology investments, long delayed during the Family Dollar integration, are finally modernizing operations. Self-checkout systems are rolling out to high-volume stores. Inventory management systems now use predictive analytics to optimize product flow. Mobile apps allow customers to check product availability and find nearby stores.

The real estate strategy has shifted from pure expansion to optimization. Dollar Tree now focuses on "Dollar Tree 3.0" stores—larger formats (10,000-12,000 square feet versus the traditional 8,000) with wider aisles, better lighting, and enhanced seasonal sections. These stores generate 20-30% higher sales per square foot than older formats.

In 2020, Dollar Tree exceeded $25 billion in annual sales for the first time since the organization started—though this included Family Dollar. Post-divestiture, Dollar Tree's standalone revenue for 2024 was $17.57 billion, still representing one of the largest dollar store operations globally.

Store labor models have been refined to an art. A typical store operates with 3-5 employees per shift, with managers trained to flex labor based on delivery schedules and traffic patterns. The simplicity of the pricing model—even with multiple price points—means new associates can be productive within hours, not days or weeks.

The customer demographic has broadened significantly. While the core customer remains households earning under $50,000 annually, Dollar Tree increasingly attracts middle-income shoppers seeking specific value categories. Teachers buying classroom supplies. Party planners stocking up on decorations. Crafters finding project materials. Small business owners buying in bulk online.

Distribution efficiency remains the hidden competitive advantage. Dollar Tree's cost per carton moved through their DCs is approximately 40% lower than traditional retailers. This efficiency, combined with minimal store labor and simplified operations, allows them to maintain strong margins even at rock-bottom prices.

The modern Dollar Tree is a paradox: a massive, sophisticated retail operation built on the simplest possible value proposition. Every system, every process, every decision is optimized around a single question: how do we deliver maximum value at minimum price? That discipline, maintained over nearly four decades, has created one of America's most resilient retailers.

VIII. Playbook: Business & Investing Lessons

The Dollar Tree story offers a masterclass in constraint-driven innovation. For 36 years, they maintained price discipline at $1.00—not $0.99, not $1.49, exactly one dollar. This wasn't stubbornness; it was strategic brilliance. The constraint forced operational excellence that competitors couldn't match. When you can't raise prices, you must become ruthlessly efficient.

The power of this discipline becomes clear when you examine the unit economics. At a dollar price point with 35% gross margins, Dollar Tree had to land products at $0.65 or less. This meant direct sourcing from factories, eliminating middlemen, and achieving massive scale for negotiating power. Every penny mattered. A two-cent increase in product cost meant nearly 6% margin compression.

Building through acquisition can work, but integration is everything. Dollar Tree's pre-Family Dollar acquisition strategy was textbook perfect: buy struggling regional chains at distressed valuations, convert them to your superior operating model, leverage expanded scale for better terms. Small, digestible deals that could be integrated without disrupting the core business. The Dollar Bill$ acquisition in 1996—136 stores for a price that wasn't even material enough to disclose—became profitable within 18 months.

Contrast this with Family Dollar: a $9.2 billion bet that violated every principle of their successful acquisition playbook. Too big to integrate smoothly. Different customer base. Incompatible culture. Competing operating model. The lesson: when a deal requires you to fundamentally change who you are as a company, the price is probably too high regardless of the number.

Retail is ultimately a distribution business, not just merchandising. Dollar Tree understood this earlier than most. Their distribution centers aren't cost centers—they're profit enablers. By optimizing DC locations, automation levels, and delivery routes, they achieved distribution costs that were 40% lower than traditional retailers. This advantage compounds: lower distribution costs mean better margins, which means more capital for expansion, which means better scale for negotiation.

Managing vendor relationships at extreme price points requires a different playbook. Dollar Tree doesn't just negotiate with vendors; they partner with them to engineer products specifically for their price points. A vendor might create a 4-pack of batteries instead of 6, or a 6-ounce shampoo instead of 8. The key insight: customers care more about the price point than the unit count, as long as the value perception remains intact.

The Family Dollar failure offers perhaps the most important lesson: culture and operations matter more than financial engineering. Dollar Tree tried to run two distinct chains with different customer bases, different supply chains, and different cultures. The overhead was crushing. The complexity was paralyzing. Sometimes the highest ROI decision is admitting a mistake and moving on.

Capital allocation in retail requires balancing growth with renovation. Dollar Tree learned this the hard way during the Family Dollar years—while they were trying to fix Family Dollar stores, their core Dollar Tree locations aged. The new "Dollar Tree 3.0" format shows what happens when capital is properly deployed: 20-30% higher sales per square foot, better customer experience, and improved employee satisfaction.

The importance of brand identity cannot be overstated. Dollar Tree meant one thing for 36 years: everything for a dollar. When they finally broke that promise in 2022, they did it decisively—$1.25 across the board, no confusion. The lesson: if you must pivot your core value proposition, do it clearly and completely. Half-measures confuse customers and employees alike.

IX. Analysis & Bear vs. Bull Case

Bull Case:

Dollar Tree emerges from the Family Dollar divestiture as a focused, streamlined operator with a clear path to profitable growth. The $800 million in proceeds plus $375 million in tax benefits provides substantial capital for share buybacks and debt reduction. More importantly, management can now focus exclusively on the core Dollar Tree banner without the distraction of trying to fix a failing chain.

The business model has proven remarkably resilient through multiple economic cycles. During recessions, Dollar Tree benefits from trade-down as middle-income consumers seek value. During expansions, their low prices remain attractive for specific categories. The 2008 financial crisis saw Dollar Tree's stock as the best performer in the Fortune 500—a testament to the model's countercyclical strength.

Expanding price points unlock significant growth potential. The Dollar Tree Plus! format with items up to $7 allows the company to address product categories previously unavailable to them. Early results show 200-300 basis point same-store sales increases without cannibalizing core dollar (now $1.25) items. If rolled out to all 9,000 stores, this could add $1-2 billion in incremental revenue.

The company generates robust free cash flow—approximately $1 billion annually on a normalized basis. With minimal maintenance capex requirements (stores are simple boxes with basic fixtures) and high cash conversion, Dollar Tree can return substantial capital to shareholders while still investing in growth.

At a current market cap of $23.474 billion, Dollar Tree trades at compelling multiples relative to its growth potential. The company could easily support 12,000+ stores in North America based on population density analysis. International expansion remains completely untapped. The runway for growth extends for decades.

Bear Case:

The tariff exposure is existential. An estimated 40% of Dollar Tree's sales are reliant on imported goods, with the majority coming from China. A 25% tariff on Chinese goods would devastate margins unless passed through to consumers, which would break the value proposition that defines the brand. The company has limited ability to source domestically at their required price points.

Competition is intensifying from every angle. Walmart's expansion into smaller formats directly targets Dollar Tree's customer base. Amazon's growth in consumables and everyday essentials erodes the convenience advantage. Dollar General continues aggressive expansion with 575 new stores planned. The competitive moat is narrowing.

Inflation pressures make the fixed-price model increasingly difficult. While the move to $1.25 bought time, inflation continues to erode purchasing power. Another price increase risks customer defection, but maintaining current prices might mean accepting structurally lower margins. It's a no-win situation that will only worsen over time.

Store saturation in core markets limits organic growth potential. Dollar Tree already operates 9,000 stores in the U.S. and Canada. Most prime locations are taken. New store productivity is declining as the company is forced into secondary and tertiary markets. Same-store sales growth becomes harder to achieve as the store base matures.

Rising shrink (theft) and labor costs pressure profitability. Retail theft has become epidemic, particularly in the value retail sector where margins are already thin. Meanwhile, tight labor markets force wage increases that the simple pricing model struggles to absorb. These pressures are structural, not cyclical.

The bear case ultimately rests on a simple question: can a business model predicated on extreme value survive in an inflationary, high-cost, tariff-threatened environment? The answer might determine whether Dollar Tree thrives for another 40 years or becomes another casualty of retail's creative destruction.

X. Epilogue & "If We Were CEOs"

Post-Family Dollar, Dollar Tree faces its clearest strategic moment in decades. Freed from the albatross of a failing chain, management can focus on what made Dollar Tree great: operational excellence, treasure hunt merchandising, and value that seems almost impossible.

If we were running Dollar Tree, priority one would be accelerating the Dollar Tree Plus! rollout. The multi-price format isn't betraying the model—it's evolving it for modern retail realities. Every store should have $3, $5, and $7 sections within 18 months. The incrementality is proven, the customer acceptance is there, and the margin opportunity is substantial.

International expansion represents a massive untapped opportunity. Dollar Tree's model would translate beautifully to markets like Mexico, where proximity to existing supply chains and cultural appreciation for value retail create ideal conditions. Starting with 100 stores in northern Mexico would test the concept with minimal risk and maximum learning potential.

Private label needs aggressive expansion. Currently at 20% of sales, private label should reach 40% within five years. This isn't about cheapening the offering—it's about controlling the supply chain and capturing manufacturer margins. Every successful retailer from Costco to Trader Joe's has proven that private label, done right, enhances rather than diminishes brand value.

Technology investments should focus on operations, not flashy customer-facing features. RFID inventory tracking, automated distribution center systems, and predictive analytics for merchandising deliver real ROI. Self-checkout expansion makes sense in high-traffic stores. But Dollar Tree doesn't need an app with augmented reality—they need systems that make operations more efficient.

The supply chain needs geographic diversification urgently. With 40%+ of goods from China, tariff risk is existential. Vietnam, India, Bangladesh, and Mexico offer alternatives, but shifting supply chains takes years, not months. This work should have started five years ago. Starting now is critical for long-term survival.

Store format evolution should continue with Dollar Tree 3.0 as the template. Larger stores with better sight lines, improved lighting, and expanded seasonal sections drive higher sales and better customer experience. The incremental investment pays back in under two years. Every new store should be 3.0 format; renovations should accelerate.

The final strategic imperative: maintain price discipline, but with flexibility. The move from $1.00 to $1.25 was necessary and successful. But the next increase can't wait another 36 years. Building systematic price increase capabilities—IT systems, signage flexibility, employee training—prepares the company for inflation reality while maintaining the value perception that defines the brand.

Dollar Tree's next chapter will be written in a retail environment radically different from its founding era. E-commerce dominance, wage inflation, supply chain complexity, and changing consumer behaviors all challenge the traditional dollar store model. But Dollar Tree has survived and thrived through multiple retail apocalypses by maintaining focus on a simple truth: Americans love a bargain, especially when finding it feels like winning.

The company that emerges from the Family Dollar divestiture is leaner, more focused, and better positioned than it's been in a decade. With $23 billion in market cap, 9,000 stores, and a proven model, Dollar Tree has the resources and resilience to evolve while maintaining what made it special. The art of the dollar continues—even if that dollar is now $1.25.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube