Ross Stores: The Art of Off-Price Retail

I. Introduction & The Off-Price Paradox

Picture this: It's a Tuesday afternoon in suburban Sacramento, and the parking lot at Ross Dress for Less is packed. Inside, shoppers rifle through racks of Calvin Klein shirts priced at $12.99, Coach handbags marked down 70%, and Nike sneakers for under $30. Meanwhile, just two miles away, a Macy's sits half-empty, its carefully curated displays gathering dust as another department store prepares to shutter. This scene, replicated thousands of times across America every day, captures one of retail's most profound paradoxes: in an age of infinite online selection and same-day delivery, why are treasure-hunt discount stores absolutely crushing it?

The numbers tell a staggering story. While traditional retailers hemorrhage market share to Amazon, Ross Stores has quietly built a $21 billion empire that defies every supposed rule of modern retail. No e-commerce presence. No mobile app. No loyalty program. Just 1,795 stores across 43 states where the average item sells for $10, and customers happily dig through packed racks for designer goods at fraction of their original price. How did a chain that started as six modest California department stores become the nation's second-largest off-price retailer with a $49.3 billion market cap? The answer lies not in digital innovation or global expansion, but in mastering a counterintuitive retail strategy: making shopping harder, not easier. Ross deliberately creates friction—no online store, no inventory search, no buy-online-pickup-in-store. Customers must physically hunt through crowded racks, never knowing what they'll find. Yet this apparent inefficiency is precisely the magic.

As inflation-weary consumers increasingly embrace the thrill of the hunt, Ross has positioned itself at the intersection of two powerful trends: the permanent shift toward value consciousness across all income levels, and the surprising resilience of physical retail when it offers experiences that can't be replicated online. The average household income for Ross customers sits at $63,000 annually—significantly below Amazon's $85,000—yet these shoppers drive remarkable loyalty, returning week after week to see what new treasures have arrived.

The timing of this story couldn't be more relevant. While legacy department stores struggle with bloated inventories and massive real estate footprints, Ross turns their pain into profit. When brands overproduce or retailers cancel orders, Ross swoops in with cash, buying excess inventory at deep discounts and moving it through their stores at lightning speed. It's a business model that actually improves during economic uncertainty—a rare feat in retail.

This is the story of how Stuart Moldaw and Don Rowlett saw opportunity where others saw obsolescence, how they built a supply chain that thrives on chaos, and why, in an age of algorithmic recommendations and same-day delivery, millions of Americans still prefer to dig through racks at Ross every single week. It's a masterclass in contrarian thinking, operational excellence, and understanding that sometimes the best technology is no technology at all.

II. Origins: Morris Ross and the Original Vision (1950-1982)

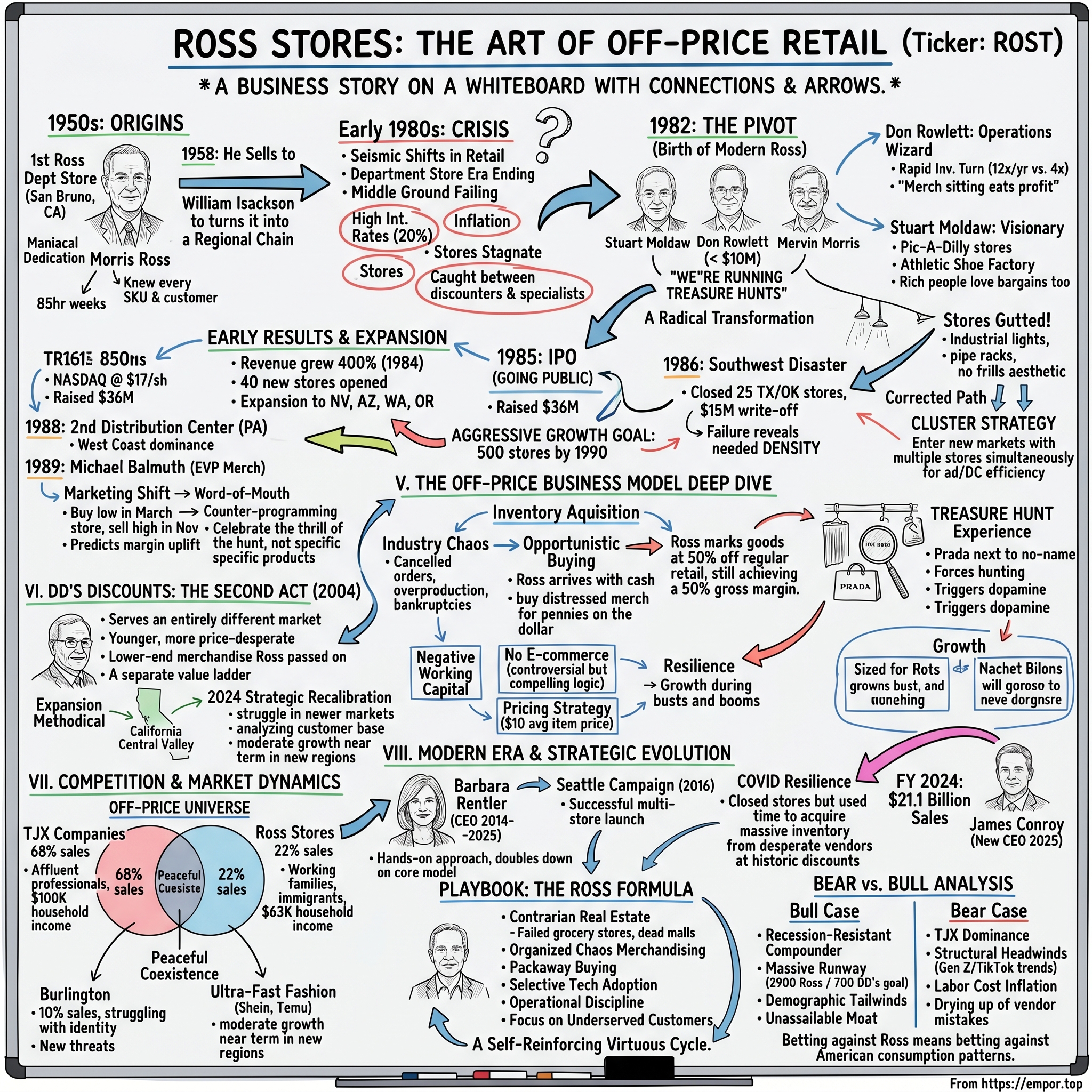

The year was 1950, and San Bruno, California, was transforming from sleepy farmland into bustling suburb. Just twelve miles south of San Francisco, the town sat at the epicenter of postwar American optimism—new highways, new homes, and most importantly for our story, new shopping habits. It was here that Morris "Morrie" Ross, a retail entrepreneur with boundless energy and an eye for opportunity, opened the first Ross Department Store.

Morrie Ross wasn't your typical merchant. While other retailers of the era focused on either high-end luxury or bottom-barrel discount, Ross carved out a different niche: respectable department store goods for the emerging middle class. His store at 711 El Camino Real wasn't fancy, but it was dignified. You could buy a decent suit, a reliable refrigerator, children's school clothes—the building blocks of suburban American life. What set Morrie apart was his maniacal dedication. Working 85 hours per week, he personally handled every aspect of the business—from selecting merchandise to balancing the books late into the night. Suppliers remembered him as the buyer who knew every SKU in his store, every customer's name, every vendor's cost structure.

But Morrie Ross had bigger dreams than retail. By 1958, after eight years of grinding retail work, he saw the California real estate boom beckoning. The same forces creating his customer base—suburban expansion, highway construction, population migration—were creating fortunes in land development. Ross made a calculated decision that would seem prescient in hindsight: he sold his store to William Isackson, pivoting entirely to become a residential and commercial real estate developer. The timing was impeccable. California real estate in the late 1950s was about to enter a golden age, and Morrie Ross would ride that wave to considerable wealth, leaving his namesake store behind.

William Isackson brought a different vision to Ross Department Store. Where Morrie had been content with one perfectly managed location, Isackson saw a chain. He understood that the Bay Area's explosive growth—fueled by aerospace, technology, and defense contractors—would create dozens of San Brunos. Each new suburb needed its own Ross.

The expansion began methodically. Pacifica came first, a foggy coastal town where young families sought affordable homes with ocean views. Then Novato in Marin County, capturing commuters heading north. Vacaville leveraged the agricultural Central Valley's urbanization. Redwood City served the Peninsula's growing middle class. Castro Valley anchored the East Bay expansion. By the late 1970s, Isackson had built Ross into a six-store regional chain, each location carefully chosen to serve distinct suburban communities.

But beneath this steady growth lay fundamental challenges. The retail landscape was shifting seismically. Discount chains like K-Mart and Target were revolutionizing how Americans shopped, using sophisticated logistics and massive scale to undercut traditional department stores. Specialty retailers were fragmenting the market from the other direction—The Gap for jeans, Footlocker for sneakers, Circuit City for electronics. The middle ground that Ross occupied was becoming a killing field.

Isackson's Ross stores, while profitable, were caught in this vice. They lacked the scale to compete with national discounters on price, yet couldn't match the specialization and brand power of focused retailers. Sales per square foot stagnated. Inventory turns slowed. The stores felt increasingly anachronistic—neither cheap enough to win on value nor special enough to command loyalty. By 1981, Isackson faced a stark choice: invest massive capital to modernize and expand, or sell to someone with a different vision.

The broader economic context made this decision even more pressing. Interest rates had soared to 20% under Federal Reserve Chairman Paul Volcker's inflation-fighting regime. Consumer spending was cratering. Traditional retail models were breaking down everywhere. Zayre was struggling. Woolworth's was in decline. The department store era that had defined American retail since the 1850s was ending. Ross, with its six locations and traditional approach, seemed destined to become another casualty.

Yet three men watching from the sidelines saw something different in those six struggling stores. Stuart Moldaw, Don Rowlett, and Mervin Morris weren't interested in Ross's current model—they saw it as raw material for something entirely new. They recognized that the very chaos destroying traditional retail could fuel a different kind of store. Where others saw the death of department stores, they saw the birth of off-price retail.

The seeds of transformation were already visible to those who knew where to look. In the Northeast, a company called Zayre had launched something called T.J. Maxx in 1976, buying excess inventory from struggling retailers and selling it cheap. In California, Moldaw himself had experimented with similar concepts through his Pic-A-Dilly stores. The idea was deceptively simple: as traditional retailers struggled with inventory management and merchandise planning became more complex, mistakes multiplied. Cancelled orders, overproduction, miscalculated trends—all created a river of quality merchandise looking for a home.

What Moldaw, Rowlett, and Morris understood—and what Isackson perhaps didn't—was that Ross's weakness could become its strength. Those six stores, freed from the obligation to carry specific merchandise or maintain traditional department store standards, could become something entirely different. They could become treasure-hunting destinations where the chaos of modern retail transformed into opportunity. But first, they had to buy the company, and then completely reimagine what a Ross store could be. The stage was set for one of retail history's most dramatic pivots.

III. The 1982 Pivot: Birth of Modern Ross

The meeting took place in a nondescript conference room in San Francisco's financial district in early 1982. Around the table sat an unlikely trio of retail veterans, each bringing a different piece of the puzzle that would transform Ross forever. Stuart Moldaw, 50 years old with prematurely silver hair and an intense gaze, had already built and sold multiple retail chains. Don Rowlett, a operations wizard known for his ability to squeeze profit from the tightest margins, sat with spreadsheets covered in handwritten calculations. And Mervin Morris—founder of the Mervyn's department store empire—brought not just capital but credibility. Together, they were about to execute one of retail's most audacious pivots.

The acquisition price was never publicly disclosed, but industry insiders estimated it at less than $10 million for the six stores—a bargain even by 1982 standards. What made the deal remarkable wasn't the price but the plan. Within minutes of signing the papers, Moldaw and Rowlett began implementing a transformation so radical that longtime Ross employees barely recognized their stores within weeks.

"We're not running department stores anymore," Moldaw announced at the first all-hands meeting. "We're running treasure hunts." The concept was revolutionary for 1982: Ross would abandon the traditional retail model entirely. No more ordered merchandise. No more seasonal planning. No more guaranteed inventory. Instead, Ross would become an opportunistic buyer of other retailers' mistakes, turning the industry's inefficiency into its own business model.

Stuart Moldaw's journey to this moment had been anything but linear. The son of a Chicago candy manufacturer, he'd started his retail career at Learned-Livingston, rising to president before striking out on his own. His Pic-A-Dilly stores in California had experimented with off-price apparel, teaching him that customers would trade convenience for value. The Athletic Shoe Factory had shown him how focused merchandising could drive traffic. Country Casuals had revealed the power of creating a treasure-hunt atmosphere. Each venture was a laboratory, and Ross would be the culmination of everything he'd learned.

Don Rowlett brought operational genius to the partnership. At J. Brannam, which he'd built for Woolworth, he'd pioneered systems for rapid inventory turnover that were revolutionary for their time. His philosophy was simple but powerful: "Every day merchandise sits in our store, it's eating profit." Under his system, Ross would aim to turn inventory 12 times per year—compared to 4 times at traditional department stores. This meant merchandise would move from truck to rack to customer in under 30 days.

The transformation began immediately. The first step was gutting the stores—literally. Out went the carpeting, the fitting rooms with doors, the organized department structure. In came industrial fluorescent lighting, simple pipe racks, and basic linoleum flooring. The aesthetic was deliberately bare-bones, signaling value before customers even saw a price tag. "We wanted people to walk in and immediately think 'bargains,'" Moldaw later explained. "Fancy stores make people expect fancy prices."

But the real revolution happened behind the scenes, in how Ross acquired merchandise. Moldaw and Rowlett assembled a team of buyers unlike anything in retail. These weren't traditional merchants planning seasons ahead—they were opportunists with cash, ready to pounce when manufacturers overproduced or retailers cancelled orders. The company established a war room in their Pacifica headquarters where buyers monitored the retail landscape like stock traders, waiting for opportunities.

The timing couldn't have been better. The 1982 recession was devastating traditional retail. Retailers were cancelling orders left and right. Manufacturers sitting on excess inventory were desperate for cash. Ross positioned itself as the solution—arriving with cash, buying entire lots, asking no questions. A typical deal might see Ross acquiring $1 million in Ralph Lauren shirts, originally destined for Macy's, at 20 cents on the dollar. Those shirts would hit Ross stores within days, priced at 50% off retail—still a 150% markup for Ross.

The early results were staggering. The Vacaville store, which had averaged $2 million in annual sales under the old model, hit $5 million in its first year post-transformation. Customer traffic doubled, then tripled. But not everything was smooth. The Redwood City location struggled initially—its affluent customer base resisted the no-frills approach. Moldaw's solution was brilliant: he brought in higher-end brands but maintained the bare-bones aesthetic. "Rich people love bargains too," he observed. "They just need to know they're getting quality."

By the end of 1983, the transformation was complete. Ross had expanded beyond California for the first time, opening a store in Reno, Nevada—chosen specifically to test whether the model could work outside its home market. The Reno store exceeded all projections, validating the concept's portability. Plans called for 20 new stores in 1984 across California, Arizona, Washington, and Oregon. By year's end, they'd opened 40.

The speed of expansion was breathtaking and occasionally chaotic. Store managers were hired sometimes just days before grand openings. Distribution systems were stretched to breaking points. The company's single distribution center in Newark, California, was processing volumes it was never designed to handle. Yet somehow, it worked. The very chaos that might have destroyed a traditional retailer fed Ross's model—customers never knew what they'd find, creating an addictive shopping experience.

The merchandising philosophy evolved rapidly during this period. Moldaw discovered that mixing high-end and moderate brands created a "halo effect"—finding a Versace dress next to a no-name blouse made both more desirable. The treasure-hunt mentality meant customers couldn't wait for sales—if you saw something you liked, you bought it immediately because it wouldn't be there next week. This urgency drove conversion rates far above industry norms.

Financial engineering was equally important. Ross operated on negative working capital—selling merchandise before paying suppliers. The company demanded terms that would make traditional retailers blanch: payment 60-90 days after delivery, no returns, no price adjustments. Yet suppliers agreed because Ross offered something precious: a way to monetize mistakes without destroying brand value. A shirt that didn't sell at Nordstrom didn't mean the brand failed—it just meant Ross customers got a bargain.

The cultural transformation within Ross was just as dramatic as the business model shift. Old-timers from the Isackson era found themselves in a completely different company. The measured pace of traditional retail was replaced by controlled chaos. Decisions that once took weeks now happened in hours. Moldaw and Rowlett were everywhere—visiting stores, talking to customers, adjusting strategies on the fly. They instituted "power hours" where entire teams would descend on a store to reset merchandise, creating fresh presentations daily.

Competition took notice quickly. TJ Maxx, which had pioneered the off-price model in the Northeast, began expanding westward. Marshalls accelerated its growth. New entrants like Nordstrom Rack appeared. But Ross had advantages: intimate knowledge of West Coast markets, relationships with suppliers built over decades, and most importantly, a willingness to go downmarket that others resisted. While TJ Maxx courted suburban sophisticates, Ross embraced working-class bargain hunters.

The transformation wasn't without casualties. Several longtime employees couldn't adapt to the new pace and left. Some vendors who'd supplied Ross for years found themselves cut off when they couldn't meet the new terms. The San Bruno community, which had taken pride in their local department store, watched it become something unrecognizable. But the numbers were undeniable: by the end of 1984, Ross's revenue had grown 400% from pre-acquisition levels.

Looking back, the 1982 pivot represents a masterclass in strategic transformation. Moldaw and Rowlett didn't try to fix Ross—they completely reimagined it. They recognized that the same forces destroying traditional retail could fuel a new model. They understood that in retail, as in life, one company's crisis is another's opportunity. Most remarkably, they executed this transformation not gradually but almost instantaneously, ripping off the band-aid in one decisive motion.

The foundation was now set. Ross had found its model, proven its concept, and demonstrated scalability. The next challenge would be even greater: taking this scrappy regional player public and competing on a national stage. But first, they'd need to convince Wall Street that a company built on chaos could deliver predictable returns.

IV. Going Public & Rapid Expansion (1985-1995)

August 8, 1985, dawned hot and humid in New York City, but inside the air-conditioned offices of Goldman Sachs, Stuart Moldaw was sweating for different reasons. In just two hours, Ross Stores would begin trading on the NASDAQ at $17 per share—a moment that would either validate three years of frantic transformation or expose the company as a regional oddity that couldn't scale. Moldaw had spent the previous week on a grueling roadshow, explaining to skeptical fund managers why a company that couldn't predict its inventory deserved public market valuation. "We're not selling predictability," he'd told them repeatedly. "We're selling a system that thrives on unpredictability."

The IPO raised $36 million, valuing Ross at roughly $175 million—a remarkable figure for a company that just three years earlier consisted of six struggling department stores. But Moldaw and Rowlett weren't celebrating. They saw the IPO not as a finish line but as rocket fuel for an expansion plan so aggressive it bordered on reckless. Their stated goal: 500 stores by 1990, spreading the Ross model from coast to coast.

The cash from the IPO immediately went to work. Within weeks, Ross announced the acquisition of 25 lease locations from the bankrupted Woolco chain, giving them instant presence in Arizona and Nevada. The company's real estate team, led by a former McDonald's executive who understood site selection like a science, had developed a proprietary model for identifying locations. They looked for sites traditional retailers ignored: former grocery stores in declining strip malls, abandoned department stores in working-class neighborhoods, spaces with ample parking but zero aesthetic appeal. "We wanted locations where the rent reflected the building's appearance, not its potential," the executive explained.

But 1986 brought Ross's first major crisis as a public company. In their enthusiasm to expand, they'd rushed into Texas and Oklahoma, opening 25 stores in less than six months. The Southwest expansion was a disaster. Texas customers, accustomed to Neiman Marcus and Sakowitz, rejected Ross's bare-bones aesthetic. Oklahoma stores sat virtually empty. Oil price collapses had devastated both states' economies. By October 1986, Moldaw made the painful decision to close all 25 stores, taking a $15 million write-off that sent the stock plummeting from $23 to $11.

The failure could have been fatal, but Moldaw's response revealed the resilience that would define Ross's culture. At the next earnings call, he was bracingly honest: "We screwed up. We didn't understand those markets, and we paid the price. But we learned something valuable: Ross needs density to work. We need multiple stores in a market to achieve advertising efficiency and customer awareness. Going forward, we'll expand in clusters, not scattered shots."

This cluster strategy became Ross's expansion bible. Instead of opening single stores in new cities, they'd enter markets with 5-10 stores simultaneously. Southern California became the proving ground. By the end of 1987, Ross had 50 stores in the Los Angeles metropolitan area alone, creating such density that advertising costs per store dropped 70%. Customers began to view Ross not as a single destination but as a network—if one store didn't have what you wanted, another might.

The distribution infrastructure had to evolve rapidly to support this growth. The Newark facility, designed for 30 stores, was now supporting 150. Lines of trucks stretched for blocks waiting to unload. Merchandise was literally falling off conveyor belts. In 1988, Ross opened a second distribution center in Carlisle, Pennsylvania, positioning them for East Coast expansion. But unlike traditional retailers who built massive automated facilities, Ross's DC operated like controlled chaos—merchandise flowed through so quickly that sophisticated sorting systems were unnecessary.

Leadership dynamics during this period were fascinating. Moldaw remained the visionary, constantly pushing for more stores, new markets, bigger bets. Rowlett was the operator, ensuring each store hit its numbers. But by 1988, tensions emerged. Rowlett wanted to slow expansion to improve same-store sales. Moldaw argued that in off-price retail, growth was the strategy—more stores meant more buying power, better deals, stronger competitive moats. The board sided with Moldaw, and Rowlett left to start his own retail venture, though he remained a major shareholder.

Michael Balmuth's arrival as Executive Vice President of Merchandising in 1989 marked a crucial evolution. Balmuth, poached from Bon Marché, brought sophisticated merchandising systems to Ross's chaotic buying model. He introduced "packaway"—buying merchandise at rock-bottom prices and storing it for optimal selling seasons. This was revolutionary: Ross could buy winter coats in March at 80% off, store them, and sell them in November at full margin. By 1990, packaway represented 40% of inventory, providing predictable margin uplift.

The competitive landscape was intensifying. TJ Maxx had grown to 400 stores and was pushing aggressively westward. Marshalls was expanding rapidly. New entrants like Tuesday Morning and Stein Mart were nibbling at the edges. But Ross had developed unique advantages. Their West Coast dominance gave them first access to Asian imports flooding through Los Angeles and San Francisco ports. Their relationship with Hollywood studios meant exclusive access to entertainment-related merchandise. Most importantly, their willingness to take bigger risks on bulk purchases meant better deals.

The early 1990s recession, which devastated traditional retail, became Ross's accelerant. As department stores closed and specialty retailers struggled, Ross was often the only buyer showing up with cash. The company acquired the entire inventory of bankrupted chains, sometimes buying goods still in transit from overseas factories. A legendary deal involved purchasing $50 million in merchandise from the collapsed Campeau retail empire for $8 million—merchandise that Ross sold through in just six weeks at 60% margins.

Store design evolved significantly during this period. While maintaining the no-frills approach, Ross discovered that certain investments paid dividends. Better lighting increased sales 15%. Wider aisles reduced theft. Strategic placement of mirrors near fitting rooms increased conversion rates. The company developed a cookie-cutter store model that could be replicated quickly: 25,000 square feet, 15 employees, $3 million in annual sales. A new store could go from lease signing to grand opening in 45 days.

The human element was crucial to this expansion. Ross developed a unique culture that blended entrepreneurial energy with operational discipline. Store managers were given unusual autonomy—they could adjust merchandise presentations, create local marketing initiatives, even negotiate with customers on bulk purchases. But they were held to strict financial metrics: inventory turns, shrinkage rates, sales per square foot. The best managers became mini-celebrities in their communities, known for special deals and insider information about incoming merchandise.

By 1993, Ross crossed a significant milestone: $1 billion in annual revenue, operating 215 stores across the Western United States. The stock had recovered from its 1986 lows to trade above $40, a 135% return from the IPO price. Wall Street analysts who'd been skeptical were now believers. One wrote: "Ross has cracked the code on making opportunistic buying systematic. They've turned chaos into a scalable business model."

The company's 1994 expansion into the Midwest marked another pivotal moment. Rather than repeat the Texas disaster, Ross spent six months studying markets like Chicago and Detroit. They discovered these rust-belt cities, hit hard by manufacturing declines, were perfect for Ross's value proposition. The initial 15 stores in Chicago exceeded projections by 40%. Detroit became one of Ross's strongest markets, with customers driving from suburbs to shop at inner-city locations.

Technology adoption during this period was deliberately minimal but strategic. While competitors invested millions in sophisticated inventory management systems, Ross maintained that their model required human judgment, not algorithms. However, they did implement point-of-sale systems that provided real-time sales data, allowing buyers to adjust strategies daily. The company's IT budget was 0.5% of revenue—compared to 2-3% at traditional retailers—with savings passed to customers.

Marketing strategy evolved significantly. Early Ross stores relied entirely on word-of-mouth. But as the chain grew, targeted advertising became necessary. The company's marketing genius was counter-programming: while department stores advertised specific products, Ross advertised the experience. "You never know what you'll find" became their unofficial motto. Television commercials showed real customers discovering designer goods at ridiculous prices, creating aspirational yet achievable narratives.

By the end of 1995, Ross operated 292 stores across 18 states, generating $1.4 billion in annual revenue. Same-store sales had grown for 33 consecutive quarters. The stock traded at $65, representing a 282% return from IPO. But more importantly, Ross had proven that off-price retail wasn't just a niche—it was the future. Department stores were closing by the dozens. Specialty retailers were struggling. But Ross was thriving, turning retail's disruption into their opportunity.

The foundation for national dominance was now complete. Ross had the scale, systems, and credibility to compete with anyone. But the next decade would bring new challenges: the rise of e-commerce, changing consumer behaviors, and the need to stay relevant to younger generations. The scrappy disruptor was becoming an institution, and with that came both opportunities and obligations they'd never anticipated.

V. The Off-Price Business Model Deep Dive

Inside Ross's buying offices in Dublin, California, at 7 AM on a typical Tuesday, controlled chaos reigns. Forty buyers sit at desks covered with fabric samples, spreadsheets, and constantly ringing phones. On the wall, a massive digital board tracks global retail bankruptcies, store closures, and inventory liquidations in real-time—what staffers call the "opportunity tracker." A buyer's phone rings: a manufacturer in Vietnam has 100,000 units of Nike athletic wear, a cancelled Foot Locker order, available at 18 cents on the dollar. The buyer has exactly 30 minutes to inspect samples, run margin calculations, and commit millions of dollars. This scene, replicated hundreds of times daily, represents the beating heart of Ross's business model—one that generates 20% operating margins while selling goods at 20-60% below traditional retail.

The economics of off-price retail seem paradoxical at first glance. How does a company achieve best-in-class margins while selling at the lowest prices? The answer lies in a fundamentally different approach to inventory acquisition and management. Traditional retailers operate on a "push" model—they predict what customers will want months in advance, place orders, and hope they're right. Ross operates on a "pull" model—they buy what's already been produced but didn't sell, acquiring proven merchandise at distressed prices. The math is compelling. A manufacturer produces 500,000 units expecting Macy's to buy them all. Macy's cancels half the order. The manufacturer now has 250,000 units sitting in a warehouse, eating storage costs, tying up capital. Ross arrives with a check for 25 cents on the dollar—far below cost but better than nothing. Ross marks those goods at 50% off regular retail, still achieving a 50% gross margin. The customer saves money. Ross makes money. The only loser is the traditional retailer who couldn't move the merchandise at full price.

"It's really about the value you're putting on the floor," CEO Barbara Rentler explains. "In a treasure hunt environment, 'If I don't buy it, it won't be there next week.'" This psychology is crucial. Traditional retailers train customers to wait for sales—everything eventually gets marked down. Ross trains customers for urgency—that Calvin Klein jacket won't be there tomorrow. This behavioral modification drives extraordinary metrics: inventory turns 12-13 times annually versus 4 times at department stores.

The buying operation itself is a marvel of organized chaos. Ross employs approximately 1,000 merchants and buyers who operate more like traders than traditional retail buyers. They're not planning assortments six months out or attending fashion shows in Milan. Instead, they're working phones, monitoring global production schedules, tracking retail bankruptcies. When opportunity strikes, they move with stunning speed. In fiscal year 2023, Ross purchased $13.5 billion worth of merchandise through opportunistic buying strategies, sourcing approximately 70% of inventory from manufacturers with excess inventory, canceled orders, or overproduced merchandise.

The packaway strategy, pioneered by Michael Balmuth in the late 1980s, adds another dimension. When winter coat manufacturers get stuck with inventory in March, prices crater. Ross buys millions of units at 10-20 cents on the dollar, stores them in warehouses, and releases them the following winter at full off-price margins. Packaway inventory accounted for 39% of total inventory as of August 3, 2024. This counter-seasonal buying provides predictable margin enhancement while giving Ross first shot at distressed inventory when manufacturers are most desperate.

Physical store design is deliberately austere—but strategically so. Fluorescent lighting, concrete floors, and pipe racks signal value before customers see a single price tag. Yet certain investments yield returns: wider aisles reduce shrinkage by improving sight lines, strategic mirror placement increases conversion rates, and better lighting can boost sales 15%. The company employs 105,000 associates across its retail network, with an average store size of 30,000 square feet carrying approximately 18,000-22,000 unique SKUs at any given time.

The treasure hunt experience is meticulously engineered randomness. New merchandise arrives multiple times weekly, but placement appears chaotic. A Prada handbag might sit next to a no-name purse. Nike shoes share space with unknown brands. This jumbling serves multiple purposes: it forces customers to hunt, increasing dwell time; it democratizes luxury, making high-end goods accessible; and it creates a casino-like variable reward schedule that triggers dopamine responses and drives addictive shopping behavior.

TJX and Ross cited pent-up demand from shoppers armed with stimulus dollars, but also a desire to look for deals. "We believe the appeal of our entertaining, treasure-hunt shopping experience gives consumers a compelling reason to shop us," TJX CEO Ernie Herrman said. This entertainment value is crucial—shopping at Ross isn't efficient, but it's engaging. Customers report the thrill of the find, the satisfaction of beating the system, the social currency of sharing deals with friends.

Distribution represents another counterintuitive advantage. Ross's distribution centers look primitive compared to Amazon's robotic warehouses. Merchandise flows through so quickly—often within 24-48 hours—that sophisticated sorting systems would slow things down. The company operates 17 distribution centers totaling 10.5 million square feet, but these function more as switching stations than storage facilities. Trucks arrive, merchandise gets sorted into store allocations, trucks depart. The entire system is optimized for velocity, not efficiency.

The lack of e-commerce is perhaps Ross's most controversial strategic decision. Ross doesn't have an e-commerce site. While analysts regularly question this choice, management's logic is compelling. The treasure hunt doesn't translate online—you can't replicate the serendipity of discovery through search filters. E-commerce would require predictable inventory, destroying the opportunistic buying model. Returns would skyrocket without try-on capability. Most importantly, online would cannibalize store traffic without adding incremental sales. By refusing to go digital, Ross forces customers into stores where impulse purchases flourish.

Vendor relationships in the off-price ecosystem are fascinatingly complex. Ross maintains relationships with approximately 12,000 vendors, from massive manufacturers to small importers. These aren't traditional supplier partnerships—they're more like a safety net for the industry's mistakes. Vendors know Ross will never be their primary channel, but when things go wrong, Ross provides liquidity without brand damage. A shirt that doesn't sell at Nordstrom doesn't mean the brand failed—it just means Ross customers get a bargain.

The financial model's elegance lies in its negative working capital structure. Ross typically sells merchandise before paying suppliers, using customer money to fund operations. Payment terms stretch 60-90 days while inventory turns in 30 days. This creates a virtuous cycle: more sales generate more cash, enabling bigger opportunistic purchases, driving more sales. It's a perpetual motion machine powered by retail industry inefficiency.

Pricing strategy walks a careful line. Ross offers brand-name apparel at 20-60% lower prices compared to department stores, maintaining an average gross margin of 27.3% in 2023. Items must be cheap enough to trigger value perception but expensive enough to maintain quality associations. The $10 average item price hits a psychological sweet spot—low enough for impulse purchases, high enough to feel substantial.

The model's resilience shows in any economic environment. During booms, overconfident retailers over-order, creating excess inventory for Ross to acquire. During busts, desperate manufacturers accept lower prices while consumers trade down to value retailers. The 2008 recession saw Ross's sales grow while department stores collapsed. The COVID pandemic created unprecedented inventory dislocations that Ross exploited masterfully. In 2024, Ross's revenue was $21.13 billion, an increase of 3.69%, with earnings of $2.09 billion, up 11.53%.

Yet the model has clear limitations. Ross can't guarantee specific products, making it impossible to build destination categories. They can't capture premium price points—true luxury brands won't sell to off-price. International expansion is virtually impossible without local buying expertise and vendor relationships. And the model requires density—stores need to cluster for advertising efficiency and customer awareness.

Competition for off-price inventory has intensified as the model's success attracts imitators. Amazon's overstock deals, Nordstrom Rack's expansion, and countless online liquidators all compete for the same distressed inventory. But Ross's scale provides decisive advantages: buying power to take entire production runs, distribution infrastructure to move merchandise quickly, and store density to reach customers efficiently.

The genius of Ross's model is that it gets stronger as retail gets more complex. Every new fashion trend that fails, every economic shock that disrupts planning, every e-commerce return that can't be resold—all create inventory that needs a home. Ross has positioned itself as retail's recycling system, turning industry waste into profit. In a world where predicting consumer demand becomes ever harder, betting against prediction might be the smartest prediction of all.

VI. DD's Discounts: The Second Act (2004-Present)

The fluorescent lights flickered on at 7 AM sharp on April 15, 2004, illuminating the first dd's DISCOUNTS store in Vallejo, California. Standing at the entrance, Stuart Moldaw, now 72 but still sharp as ever, watched as customers who'd been waiting since 5 AM rushed through the doors. These weren't typical Ross shoppers—they were younger, more diverse, more price-desperate. As Moldaw observed a grandmother filling her cart with $3 children's clothes while speaking rapid Spanish to her daughter, he knew they'd found an entirely different market. "Ross taught us that there's always someone looking for a better deal," he'd later tell investors. "DD's was about finding those someones."

The genesis of dd's DISCOUNTS reveals strategic brilliance hidden in plain sight. By 2003, Ross had become so successful that it was actually turning away merchandise—goods that were too low-end for the Ross brand but still represented massive opportunity. The company was literally leaving money on the table. Meanwhile, demographic shifts were creating a new consumer class: recent immigrants, young families, and urban communities where $50 could be a week's clothing budget. Ross executives realized they could serve this market without diluting their core brand—but they'd need to build something entirely different.

The name itself was carefully chosen. "DD's" supposedly stood for nothing specific, though insiders joked it meant "Deeper Discounts." The apostrophe-S construction subtly suggested possession—these were YOUR discounts. The logo's bright colors and playful font contrasted sharply with Ross's conservative branding. Everything signaled that this was a different animal: younger, louder, more aggressive on price. The DD's business model was radically different from Ross's carefully curated off-price approach. Where Ross maintained certain quality standards—never selling irregulars, maintaining brand integrity—DD's threw those rules out. Irregular merchandise? Fine. Private label goods mixed with brands? No problem. Last year's styles? Perfect. The average price point at DD's was 40% lower than Ross, with most items under $5. This wasn't just deeper discounting; it was a different universe of value retail.

The banner's offering focused on a moderately-priced assortment of first-quality, seasonal name-brand apparel, footwear and home fashion, though "moderately-priced" was relative—what counted as moderate at DD's would be rock-bottom elsewhere. The stores themselves were even more spartan than Ross. If Ross was no-frills, DD's was anti-frills. Concrete floors weren't just exposed; they were celebrated. Merchandise wasn't just packed; it was piled. The aesthetic screamed value so loudly that customers felt guilty not buying something.

The initial expansion was methodical and regional. California's Central Valley became the proving ground—Fresno, Modesto, Stockton—agricultural communities with large immigrant populations and household incomes below $40,000. These markets had been underserved by traditional retail and even by Ross. DD's filled a genuine void, offering new clothing at prices that competed with thrift stores.

Customer demographics told a fascinating story. While Ross's average customer household income was $63,000, DD's averaged under $40,000. These were people for whom a $3 shirt wasn't a bargain—it was a budget line item. Many were recent immigrants sending money home, young families living paycheck to paycheck, or seniors on fixed incomes. For them, DD's wasn't just shopping; it was survival retail.

The merchandise mix evolved through experimentation. DD's discovered that certain categories over-indexed dramatically with their customer base. Character-licensed children's clothing flew off racks. Work boots and uniforms disappeared instantly. Home textiles—sheets, towels, curtains—became traffic drivers. Beauty products, particularly hair care for diverse ethnicities, proved goldmines. These weren't categories Ross prioritized, but for DD's customers, they were essentials.

By 2010, DD's had expanded to 65 stores, generating roughly $400 million in revenue. The format was working, but growth was measured. Unlike Ross's explosive expansion in the 1980s, DD's grew deliberately, ensuring each market could support the ultra-low price points. The Great Recession actually accelerated growth as middle-class families traded down and discovered DD's for the first time.

The operational challenges were unique. Margins at DD's were razor-thin—often single digits on individual items. This required extraordinary discipline. Labor costs were minimized through self-service models. Store designs eliminated any unnecessary expense. Even shopping bags were optional—many customers brought their own or carried purchases out by hand. Every penny saved went to lower prices.

The relationship between Ross and DD's evolved into sophisticated portfolio management. When Ross buyers passed on merchandise as too downmarket, it went to DD's. When DD's customers "graduated" economically, they moved to Ross. The brands created a value ladder that captured customers at different life stages. A teenage mother might start at DD's, move to Ross as her career developed, but return to DD's for kids' clothes. This ecosystem approach maximized customer lifetime value across economic cycles.

The California-based company operated 2,127 Ross and DD's Discounts in 43 states, Washington, D.C. and Guam as of Monday. "As we look out over the long term, we remain confident that Ross can grow to 2,900 locations and DD's Discounts can become a chain of 700 stores given consumers' ongoing focus on value and convenience", McGillis stated in 2024.

But challenges emerged as DD's pushed beyond its core markets. Sales trends at DD's Discounts slightly trailed Ross' growth. "While DD's top-line results were respectable in fiscal 2023, we are disappointed with the performance in newer markets," CEO Barbara Rentler said. As a result, the company is "conducting an in-depth analysis of DD's" to gain a better understanding of the banner's customer base as it attempts to grow outside existing markets.

The struggle in newer markets revealed DD's limitations. In affluent suburbs, the brand was stigmatized. In rural areas, population density couldn't support the low margins. In diverse urban markets, established competitors like Rainbow and Citi Trends had strong footholds. DD's sweet spot—dense, working-class, ethnically diverse communities—wasn't uniformly distributed across America.

Competition intensified as dollar stores recognized the opportunity. Dollar General and Family Dollar expanded apparel offerings. Five Below pushed into the space. Online players like Wish.com offered similar price points with home delivery. DD's found itself squeezed between physical and digital competitors, all chasing the same price-sensitive consumer.

The strategic recalibration in 2024 was telling. Rentler said the company plans to moderate DD's growth near term in newer markets and focus on growing the banner in existing regions. This wasn't retreat but recognition that DD's couldn't be force-fit into every market. The focus shifted to deepening presence in proven geographies—California, Texas, Florida—where Hispanic populations and value-consciousness aligned perfectly with DD's proposition.

Technology adoption at DD's remained minimal but targeted. While e-commerce was still absent, the company invested in supply chain systems to move lower-margin goods even faster. RFID tags helped reduce shrinkage, crucial when profit margins were thin. Data analytics identified which categories resonated in specific communities, allowing micro-merchandising at scale.

The labor model at DD's became increasingly important as minimum wages rose. With average transaction values under $15, traditional staffing models didn't work. DD's pioneered ultra-lean operations: one manager, two associates could run an entire store during off-peak hours. Self-checkout systems, though initially resisted by the customer base, gradually gained acceptance. The goal was sub-10% labor costs as a percentage of sales—nearly impossible in traditional retail.

Marketing for DD's required cultural sensitivity and community connection. Traditional advertising didn't reach their customers effectively. Instead, DD's invested in community partnerships, sponsored local events, and built relationships with community organizations. Store managers became community figures, known by name, trusted for advice on stretching budgets. This grassroots approach created loyalty that transcended price.

The financial performance of DD's within Ross's portfolio remained somewhat opaque—the company didn't break out detailed segment reporting. But industry analysts estimated DD's generated roughly $2-2.5 billion in revenue by 2024, representing 10-12% of Ross's total sales. While margins were lower than Ross stores, the incremental revenue and market expansion justified continued investment.

Looking forward, DD's faces existential questions. Can ultra-low-price physical retail survive rising real estate and labor costs? Will second-generation immigrant families maintain the same value orientation as their parents? Can DD's expand beyond its core demographic without losing its identity? The answers will determine whether DD's becomes a 700-store chain or remains a profitable but limited niche player.

The DD's experiment proves something profound about American retail: there's always a lower price point that unlocks new demand. By serving customers that even Ross considered too price-sensitive, DD's created a $2 billion business from nothing. It's a reminder that in retail, as in physics, nature abhors a vacuum—and DD's filled one that nobody else wanted to touch.

VII. Competition & Market Dynamics

The conference room at TJX headquarters in Framingham, Massachusetts, could have been a war room. Covering the walls were heat maps of the United States, each dot representing a Ross or Burlington store, with TJX locations overlaid in different colors. It was 2015, and TJX CEO Ernie Herrman was explaining to his team why Ross, despite being a fraction of TJX's size, kept him up at night. "They're not competing with us for customers," he said, pointing to demographic data. "They're creating off-price converts we'll never see. That's the real threat—they're growing the pie in places we can't reach. "The numbers were stark: The highest off-price retail market share goes to The TJX Companies, which earned 68 percent of sales among the three major competitors in October 2022. Ross captured 22% while Burlington held just 10%. Yet these market share figures obscured a more nuanced reality. TJX and Ross weren't really competing for the same customers—they were expanding the off-price universe in parallel, each converting different segments of traditional retail shoppers.

TJX shoppers differed significantly from those at Ross or Burlington. With average household incomes approaching $100,000, TJX customers were affluent professionals who viewed off-price shopping as smart, not necessary. They cross-shopped at Nordstrom, Whole Foods, and Apple stores. The TJX experience reflected this demographic: better lighting, wider aisles, more sophisticated merchandising. HomeGoods, their home décor concept, felt more like a boutique than a discount store. "We saw (consolidated) comp store sales growth of three percent, and every division was entirely driven by customer transactions, which underscores the strength of our value proposition", CEO Ernie Herrman noted, highlighting how TJX was stealing bits of market share from traditional retail.

Ross occupied a different universe entirely. With customer household incomes averaging $63,000—well below Amazon's $85,000 average—Ross served working families, recent immigrants, and retirees. These customers didn't cross-shop at Nordstrom; they compared prices at Walmart and Target. For them, Ross wasn't about smart shopping but essential budgeting. This demographic difference created an unexpected dynamic: rather than fierce competition, TJX and Ross enjoyed peaceful coexistence, each dominating their income segment.

Burlington represented the wild card in off-price retail. Positioned between TJX and Ross on price but lacking either's clear identity, Burlington struggled to define its niche. Their "other stuff" strategy—selling everything from coats to baby furniture—created operational complexity without clear differentiation. Yet Burlington's challenges illuminated something important: success in off-price required more than just low prices. It demanded a coherent brand identity, operational excellence, and deep understanding of your specific customer.

The geographic strategies revealed further differentiation. TJX concentrated in affluent coastal markets and suburban power centers. Their stores anchored lifestyle centers next to Whole Foods and Lululemon. Ross dominated working-class suburbs and diverse urban neighborhoods, often taking over failed Kmart or Sears locations. Burlington scattered across secondary markets, trying to find pockets of opportunity both companies had missed.

The leader in share among the off-price segment is TJX, the parent company of T.J. Maxx, Marshalls and HomeGoods. TJX reported a 13% jump in sales during the holiday quarter, with net income growth of 34% from the year-ago period. Comp sales grew by 5%, outpacing the 4.6% forecast. But TJX's dominance came with limitations. Their upscale positioning meant they couldn't penetrate lower-income markets where Ross thrived. Their sophisticated systems and higher operating costs made ultra-low-price points impossible.

The vendor relationships told another story. TJX, with its massive scale and international presence, commanded first look at premium overstock. Luxury brands that would never sell to Ross happily worked with TJX, knowing their customers wouldn't damage brand equity. Ross, conversely, excelled at buying deeper into the supply chain—taking entire factory runs, importing directly from Asian manufacturers, buying goods other retailers wouldn't touch.

Marketing strategies diverged completely. TJX advertised in lifestyle magazines, sponsored fashion bloggers, and created Instagram-worthy store displays. Their message: "You're not shopping discount; you're shopping smart." Ross barely advertised at all, relying on word-of-mouth and community presence. When they did market, it was functional: "Designer brands, low prices, new arrivals daily." No lifestyle aspirations, just value propositions.

The COVID pandemic revealed each company's resilience and weaknesses. TJX, with some e-commerce capability through their HomeGoods site launched in September 2021, could capture some online demand. But their affluent customers also had more shopping options. Ross, with no online presence, suffered during lockdowns but exploded when stores reopened. Their customers, lacking alternatives, returned with pent-up demand. Burlington, caught in between, struggled most—neither essential enough to drive traffic nor upscale enough to command loyalty.

Post-pandemic expansion strategies diverged sharply. CEO Ernie Herrman told analysts he plans to expand TJX's store footprint by at least 1,300 stores "over the long term." "We continue to attract new Gen Z and millennial shoppers to our stores, which we believe bodes well for our future growth. It's really great when we see multiple generations shopping our stores together." TJX beat expectations in Q1, with sales growing 6% to $12.5 billion. Meanwhile, Ross focused on densification in existing markets rather than geographic expansion.

The department store apocalypse accelerated competitive dynamics. As Macy's, JCPenney, and others closed hundreds of locations, off-price retailers competed for their real estate and inventory. But even here, strategies differed. TJX cherry-picked premium locations, often subdividing massive department stores into multiple concepts. Ross took over entire stores in working-class malls, converting 100,000 square feet of Sears into Ross plus DD's combinations. Burlington bought distressed leases at bankruptcy auctions, gambling on locations others wouldn't touch.

Technology adoption revealed philosophical differences. TJX invested heavily in inventory management systems, using predictive analytics to optimize merchandise flow. They experimented with RFID, mobile apps, and even same-day delivery in select markets. Ross remained steadfastly analog, believing technology couldn't replicate human buyers' instincts. Burlington fell somewhere between, adopting enough technology to compete but not enough to differentiate.

The talent war in off-price retail was fierce but segmented. TJX recruited from traditional retailers and business schools, seeking polished executives who understood brand building. Ross promoted from within, valuing operational expertise over pedigree. Burlington struggled to define its talent needs, sometimes hiring TJX executives who couldn't adapt to Burlington's scrappier culture, other times promoting Ross-style operators who lacked strategic vision.

Supplier dynamics grew increasingly complex as off-price retail expanded. Manufacturers now planned for off-price channels, deliberately producing excess inventory knowing it would find homes. Some created specific lines for off-price, lower quality but carrying prestigious labels. This "planned overflow" threatened the off-price model's authenticity. TJX responded by emphasizing their buyers' expertise in identifying genuine overstock. Ross doubled down on opportunistic buying, refusing planned production. Burlington, lacking clear strategy, took whatever they could get.

The rise of ultra-fast fashion created new dynamics. Shein and Temu offered prices competitive with off-price but with trendy styles and home delivery. This particularly threatened Ross's younger customers, who might accept longer shipping times for lower prices. TJX's quality positioning insulated them somewhat—their customers wanted authentic brands, not knockoffs. But the long-term threat was clear: if consumers could buy new goods from China cheaper than American overstock, what happened to off-price retail?

International expansion revealed another divide. TJX operated successfully in Canada, Europe, and Australia, adapting their model to local markets. Ross remained steadfastly domestic, arguing their model required deep local knowledge impossible to replicate internationally. Burlington didn't even consider international expansion, struggling enough with domestic execution.

The financial metrics told the story of three different businesses. TJX generated the highest sales per square foot but also had the highest operating costs. Ross achieved the best margins through operational efficiency. Burlington lagged both, neither premium enough for high prices nor efficient enough for superior margins. Yet all three grew while department stores shrank, suggesting the off-price model's fundamental soundness.

Real estate strategies evolved with retail disruption. TJX increasingly took over entire lifestyle centers, creating TJX "campuses" with multiple concepts. Ross perfected the art of dead mall renovation, turning failed retail into thriving treasure hunts. Burlington became the ultimate bottom feeder, taking locations nobody else wanted and making them marginally profitable.

Looking ahead, the competitive dynamics seem set to intensify. The off price retail market is estimated to be valued at USD 372.46 Bn in 2025 and is expected to reach USD 668.30 Bn by 2032, exhibiting a compound annual growth rate (CAGR) of 8.7% from 2025 to 2032. This growth will attract new entrants, pressure margins, and force innovation. Yet the segmentation between TJX's upscale treasure hunt, Ross's working-class value proposition, and Burlington's "everything else" positioning will likely persist.

The lesson from off-price competition is that in retail, different can be better than better. TJX, Ross, and Burlington succeed not by beating each other but by serving distinct customer needs. In a world where Amazon theoretically sells everything to everyone, these retailers prove that specificity still matters, that physical retail still has a place, and that there's always room for a better deal.

VIII. Modern Era & Strategic Evolution (2010s-Today)

Barbara Rentler's first day as CEO of Ross Stores on June 1, 2014, began not in the executive suite but on the sales floor of the Oakland Coliseum store, one of Ross's highest-volume locations. Wearing jeans and a Ross-purchased blouse, she spent four hours working the floor, helping customers, observing traffic patterns, listening to complaints. A shopper, not recognizing her, complained that the fitting rooms were too crowded. Rentler grabbed a notebook and wrote it down. That evening, she called the real estate team: "We need bigger fitting rooms, and we need them now." This hands-on approach would define her tenure—the 25th female CEO of a Fortune 500 company who never forgot that retail is ultimately about the customer in the store.

The post-recession landscape that Rentler inherited was paradoxical. The economy was recovering, employment was rising, yet American shopping habits had fundamentally changed. The 2008 crisis hadn't just created temporary bargain hunters—it had permanently altered how middle-class Americans thought about value. Paying full price now seemed almost irresponsible. This psychological shift represented a massive opportunity for Ross, but also new challenges as every retailer suddenly claimed to offer "value."

By 2012, Ross reached $9.7 billion for the fiscal year with 1,091 stores in 33 states with an additional 108 for DD's Discounts in 8 states. The company's growth trajectory was impressive, but Rentler saw vulnerabilities. Same-store sales growth was slowing. New store productivity was declining. Most concerning, younger customers weren't discovering Ross at the same rate as previous generations. The treasure hunt that excited Boomers and Gen X felt dated to Millennials raised on Amazon's infinite selection and instant gratification.

Rentler's strategic response was subtle but profound: Ross wouldn't chase trends but would perfect its core model. "We're not trying to be Amazon or TJX," she told her leadership team. "We're Ross. Let's be the best Ross we can be." This meant doubling down on operational excellence, improving merchandise quality, and most importantly, deepening relationships with vendors to access better brands at better prices.

The merchandising evolution under Rentler was dramatic. Ross had always carried brands, but often older merchandise or less desirable styles. Rentler pushed buyers to be more aggressive, arriving first at liquidations, bidding higher for premium overstock, taking calculated risks on larger purchases. The result: fresher merchandise, better brands, shorter aging. A customer in 2015 might find current-season Nike, recent Calvin Klein, even occasional luxury brands that would never have appeared in Ross five years earlier.

The Pacific Northwest expansion showcased this evolved strategy. Seattle, Portland, and surrounding markets were affluent, educated, and historically resistant to off-price retail. But Rentler saw opportunity in tech workers making good money but carrying massive student debt, in Boeing engineers facing pension uncertainty, in Microsoft contractors lacking job security. These weren't traditional Ross customers, but economic anxiety made them receptive to value propositions.

The Seattle campaign was methodical. Rather than scattered stores, Ross opened 15 locations simultaneously in September 2016, creating instant density. Marketing emphasized quality, not just price: "The brands you love, prices you'll love more." Store designs were upgraded—still basic but cleaner, brighter, more organized. The gamble paid off spectacularly. Seattle became one of Ross's strongest markets, proving that even affluent consumers would embrace off-price if positioned correctly.

Technology adoption under Rentler remained minimalist but strategic. While competitors built mobile apps and experimented with augmented reality, Ross focused on invisible improvements. RFID tags reduced shrinkage. Advanced analytics optimized truck routes. Point-of-sale systems provided real-time data enabling dynamic merchandising decisions. The customer saw none of this, just better selection arriving faster.

The decision to remain offline became more controversial each year. Analysts constantly questioned the strategy. Rentler's response never wavered: "Our business model is incompatible with e-commerce. We buy opportunistically, sell immediately, and create urgency through scarcity. You can't replicate that online." But privately, Ross was studying digital carefully, not to launch e-commerce but to understand how online shopping changed offline behavior.

One discovery was profound: online research increased store traffic. Customers would see products online at full price, then visit Ross hoping to find them cheaper. This "reverse showrooming" became a vital traffic driver. Ross responded by ensuring stores near major malls received merchandise similar to what those malls' department stores had recently carried. Customers learned that if Nordstrom had it last month, Ross might have it this month at 70% off.

The vendor ecosystem evolved dramatically during this period. As traditional retail struggled, manufacturers needed Ross more than ever. But Rentler understood that desperate vendors made bad partners. Ross instituted vendor support programs, offering faster payment terms during crisis periods, providing volume guarantees to struggling manufacturers, even advancing capital in exchange for exclusive access to production runs. These partnerships created loyalty that transcended individual transactions.

Labor strategy became increasingly critical as unemployment fell and wages rose. Ross couldn't match tech industry salaries, but Rentler emphasized different benefits: predictable schedules, promotion from within, and most importantly, a culture that valued longevity. While Amazon warehouses suffered 150% annual turnover, Ross stores averaged 60%. Store managers often stayed decades, becoming community fixtures. This continuity reduced training costs and improved customer experience.

The 2020 pandemic initially devastated Ross. With no e-commerce capability and stores forced closed, revenue evaporated overnight. The company furloughed workers, suspended dividends, drew down credit lines. Survival mode. But Rentler saw opportunity in crisis. While stores were closed, Ross buyers were working phones, acquiring massive inventory from desperate vendors at historic discounts. The company's warehouses filled with merchandise bought at 10-15 cents on the dollar.

When stores reopened in May 2020, the results were extraordinary. Customers, desperate for retail therapy and armed with stimulus checks, flooded back. The inventory Ross had accumulated during closure was exactly what people wanted: comfortable clothes for working from home, athletic wear for newfound exercise routines, home goods for nest improvement. Sales exploded, exceeding 2019 levels within months.

The post-pandemic acceleration continued through 2024. For FY 2024, which ended Feb. 1, 2025, Ross generated $21.1 billion in sales, a 3.7% increase over the $20.4 billion in FY2023 sales. But beneath topline growth, fundamental changes were occurring. The customer base was diversifying—younger, more diverse, increasingly urban. Shopping patterns shifted from weekly trips to sporadic splurges. Basket sizes increased but frequency decreased.

Supply chain disruption created unprecedented opportunities. The bullwhip effect—where small demand changes create massive supply variations—generated enormous inventory dislocations. Retailers who over-ordered during shortage panics suddenly had massive excess. Manufacturers who ramped production found themselves with unsold goods. Ross was there for all of it, buying at prices not seen since the 2008 crisis.

But challenges mounted. Rising wages pressured margins. Real estate costs in desirable locations soared. New competitors emerged: Amazon's overstock deals, Walmart's fashion improvements, Chinese ultra-fast fashion. Most concerning, the generation raised on instant gratification struggled with Ross's treasure hunt model. Young customers wanted specific items immediately, not random discoveries eventually.

Rentler's response was measured evolution, not revolution. Stores were refreshed but not reimagined. Merchandise improved but strategies stayed consistent. Marketing increased but remained value-focused. The message was clear: Ross would adapt but not transform. The model that worked for 40 years would work for 40 more, even if the customers and products changed.

Leadership transition marked another evolution. On October 28, 2024, the company's board of directors appointed James Conroy as the new CEO, succeeding Barbara Rentler effective February 2, 2025. Conroy previously was CEO of Boot Barn. The choice of Conroy, an outsider with specialty retail experience, suggested Ross was preparing for its next chapter—one that might require fresh perspectives on attracting younger consumers while maintaining core value propositions.

The expansion strategy for the mid-2020s reflected confident conservatism. Ross remains confident that Ross can grow to 2,900 locations and dd's Discounts can become a chain of 700 stores given consumers' ongoing focus on value and convenience. This wasn't aggressive—roughly 90 stores annually—but it was steady, predictable, profitable. Each new store was profitable within months, requiring minimal capital investment, generating immediate cash flow.

Geographic expansion focused on densification rather than exploration. Instead of entering new states, Ross deepened penetration in existing markets. California went from 300 to 400 stores. Texas approached 300. Florida passed 200. This clustering strategy improved advertising efficiency, distribution economics, and brand awareness. Customers learned that Ross was everywhere, always convenient, always available.

The competitive landscape continued evolving. Department stores essentially surrendered, focusing on e-commerce and closing physical locations. TJX pushed upmarket, chasing affluent consumers with premium brands. Burlington struggled with identity, neither cheap enough nor nice enough. New entrants like Five Below nibbled at edges but lacked scale. Ross stood increasingly alone in its segment: serving working Americans with quality brands at genuinely low prices.

Financial performance validated the strategy. Operating margins exceeded 12% consistently. Return on equity approached 40%. Free cash flow generation enabled substantial shareholder returns while funding expansion. The balance sheet remained fortress-like: minimal debt, substantial cash, and massive untapped credit facilities. Ross could weather any storm, seize any opportunity.

Looking toward 2030, Ross faces existential questions. Can physical retail treasure hunts engage digital natives? Will climate change and social consciousness alter consumption patterns? How will artificial intelligence affect buying decisions and inventory management? Can the model survive rising labor costs and real estate prices? These challenges are real, but so is Ross's track record of adaptation without transformation.

The modern era proves Ross's resilience. Through recession and recovery, pandemic and reopening, the company has consistently delivered value to customers and shareholders. Not through innovation or disruption, but through relentless execution of a simple model: buy cheap, sell cheap, repeat. In a world of infinite complexity, Ross's simplicity might be its greatest strength.

IX. Playbook: The Ross Formula

The real estate committee meeting at Ross headquarters happens every Tuesday at 8 AM, and the decisions made in that room determine the company's future more than any merchandising strategy or marketing campaign. The scene is almost ritualistic: detailed demographic data, traffic patterns, competitor analyses, and most importantly, gut instinct from executives who've been choosing sites for decades. "You can have all the data in the world," says one veteran real estate executive, "but ultimately you need to stand in that parking lot at 2 PM on a Saturday and feel whether it's a Ross location."

The site selection criteria reads like a contrarian's manifesto. While traditional retailers chase prime real estate with perfect visibility and pristine surroundings, Ross hunts for diamonds in the rough. The ideal Ross location: a failed grocery store in a strip mall anchored by a discount grocer, a check-cashing store, and a McDonald's. Ample parking but cracked asphalt. Good traffic flow but not a destination. Rent that reflects the property's appearance, not its potential. These locations—ignored by Target, beneath Walmart—become gold mines for Ross.

The math is compelling. A typical Ross store requires 25,000-30,000 square feet, but not premium space. While Best Buy might pay $30 per square foot for a power center location, Ross pays $8-12 for secondary space. This rent differential—often $500,000 annually per store—flows directly to margins. Multiply across 1,800 locations, and you're talking nearly $1 billion in annual savings versus traditional retail real estate strategies.

But cheap rent is just the beginning. Ross has perfected the art of minimal build-out. Where traditional retailers spend $2-3 million preparing a location—custom fixtures, elaborate lighting, sophisticated HVAC—Ross spends $400,000. Concrete floors get basic sealant, not polishing. Lighting is functional fluorescent, not architectural LED. Fixtures are industrial pipe racks, not custom displays. The message to customers is clear before they see a single price tag: this is about value, not experience.

The merchandising philosophy represents organized chaos with method to the madness. Traditional retailers organize by brand, creating shop-in-shops and brand boutiques. Ross deliberately destroys brand coherence. Calvin Klein shirts hang next to no-name alternatives. Designer handbags mix with private label accessories. This jumbling serves multiple purposes: it democratizes luxury brands, forces treasure hunting, and prevents brand comparison shopping. You can't compare Ross's prices to Macy's because the presentation is incomparable.

The buying strategy operates on different timelines than traditional retail. While department stores plan seasons six months out, Ross buyers work on 30-60 day horizons. A typical Monday might see ten different opportunities: a manufacturer with cancelled orders needs immediate cash, a retailer's bankruptcy releases inventory, an importer has containers refused at port. Ross buyers have pre-approved capital allocations and can commit millions within hours. Speed is everything—hesitation means losing deals to TJX or Burlington.

But speed must balance with discipline. Ross has walked away from legendary deals because margins weren't sufficient. The company maintains strict hurdle rates: minimum 50% initial markup, maximum 45-day selling period, no special handling requirements. A buyer might pass on $10 million of Gucci handbags at 15 cents on the dollar because authentication costs would destroy margins. This discipline—saying no to good deals to wait for great ones—defines Ross's purchasing culture.

Vendor relationships in the Ross ecosystem resemble a complex dance of mutual dependence. Vendors need Ross as a release valve for excess inventory, but they fear brand dilution. Ross needs vendors for product but won't accept their terms. The result is a carefully choreographed partnership where both sides understand the rules. Vendors get cash quickly with no returns or chargebacks. Ross gets merchandise at prices that enable their model. Neither side loves the arrangement, but both profit from it.

The packaway strategy adds another dimension to buying sophistication. When winter coat manufacturers get stuck with inventory in March, prices crater to 10-20 cents on the dollar. Ross buys millions of units, stores them in warehouses, and releases them the following winter. This counter-seasonal buying requires massive capital commitment and storage costs, but the margin enhancement is extraordinary. Packaway can generate 70% gross margins versus 45% for regular purchases.

Distribution represents hidden operational excellence. Ross's distribution centers look primitive compared to Amazon's robotic marvels, but they're optimized for different objectives. Amazon optimizes for individual order fulfillment. Ross optimizes for bulk flow-through. Merchandise arrives in massive quantities, gets sorted into store allocations within 24-48 hours, and ships immediately. The entire system prioritizes velocity over efficiency—moving goods fast matters more than moving them perfectly.

Store operations follow rigid simplicity. A typical Ross store employs 15-20 people total, compared to 50+ at similar-sized department stores. The staffing model is deliberately lean: one manager, two assistant managers, four full-time associates, and 8-10 part-timers. Everyone does everything—cashiers stock shelves, managers run registers, nobody specializes. This cross-training reduces labor costs while improving flexibility. When trucks arrive, everyone unloads. When lines form, everyone cashiers.

The lack of customer service is strategic, not accidental. Ross associates don't help you find sizes, suggest alternatives, or provide styling advice. They stock shelves and run registers. This isn't poor service—it's appropriate service for the model. Customers who want hand-holding shop at Nordstrom. Ross customers want to be left alone to hunt for bargains. The money saved on service labor goes to lower prices.

Inventory management breaks conventional retail rules. Traditional retailers fear stockouts and maintain safety stock. Ross embraces stockouts as features, not bugs. When items sell out, they're gone forever, creating urgency for remaining merchandise. The company turns inventory 12-13 times annually versus 4 times for department stores. This velocity means less working capital, reduced markdowns, and fresher merchandise. Every item has a ticking clock—if it doesn't sell in 30 days, it gets marked down. At 45 days, it's gone.

Pricing strategy walks a tightrope between perception and reality. Items must be cheap enough to trigger value perception but expensive enough to signal quality. The $9.99 price point is sacred—high enough to feel substantial, low enough for impulse purchase. Ross discovered that $9.99 generates 40% more sales than $10.99, even though the difference is just 10%. These psychological price points get tested constantly, refined through millions of transactions.

Marketing remains minimal and functional. While competitors spend 3-4% of revenue on advertising, Ross spends less than 1%. The marketing that exists is purely tactical: announcing new store openings, promoting seasonal categories, reminding customers about value. No lifestyle advertising, no brand building, no emotional appeals. The product and price are the marketing. Every dollar not spent on advertising is a dollar available for lower prices.

The store refresh strategy maintains facilities without major investment. Every 7-10 years, stores get refreshed—new paint, carpet cleaning, fixture adjustment. But Ross never fully remodels. A store that opened in 1995 might have the same layout, same fixtures, same basic design in 2024. This consistency reduces costs while maintaining familiarity. Customers know exactly what to expect, where to find categories, how to navigate the treasure hunt.

Technology adoption remains deliberately selective. Ross uses technology where it clearly enhances operations—point-of-sale systems, inventory tracking, distribution optimization. But it avoids technology for technology's sake. No mobile apps, no augmented reality, no artificial intelligence stylists. The philosophy is simple: technology that helps buy or move merchandise cheaper gets adopted. Technology that enhances customer experience gets ignored.

The financial model's elegance lies in its simplicity. Ross operates on negative working capital—selling merchandise before paying suppliers. Standard payment terms are 60-90 days while inventory turns in 30 days. This creates a perpetual cash generation machine. More sales generate more cash, enabling bigger purchases, driving more sales. The model is self-reinforcing and requires minimal external capital.