Datadog: The DevOps Monitoring Unicorn That Said No to Cisco

I. Introduction & Episode Roadmap

Picture this: It's a crisp September morning in 2019. In a Manhattan boardroom overlooking the Hudson River, two French engineers are staring at an offer sheet that would make them instant billionaires. Cisco, the networking giant, has just put forward a takeover bid "significantly higher than $7 billion" for their nine-year-old monitoring software company. Most founders would pop champagne. Olivier Pomel and Alexis Lê-Quôc? They politely declined and filed for an IPO instead.

Three weeks later, on September 19, 2019, Datadog went public at a $8.7 billion valuation—already beating Cisco's offer. By late 2024, that same company would be worth over $100 billion, making the rejection one of the most lucrative "no thank you" responses in tech history. The story of Datadog is fundamentally a tale of two engineers who saw the future of software infrastructure before almost anyone else. Founded in 2010 by Olivier Pomel and Alexis Lê-Quôc, the company emerged just as the cloud revolution was beginning to reshape how companies build and run software. They weren't building for the world that existed—they were building for the world that was coming.

This is the anatomy of how a monitoring software company born in New York—not Silicon Valley—became the essential nervous system for modern cloud infrastructure. It's a story about timing markets perfectly, saying no to billions, and building a product so sticky that customers expand their spending year after year like clockwork. As of August 2025, Datadog has a market cap of approximately $44.8 billion, down from peaks above $100 billion but still representing one of the most successful enterprise software stories of the past decade.

What makes Datadog particularly fascinating for students of business strategy is how the founders repeatedly zigged when conventional wisdom said to zag. They built in New York when everyone said you needed to be in the Valley. They focused on self-service when enterprise software meant armies of consultants. They rejected a massive acquisition offer when most would have cashed out. And perhaps most importantly, they built for developers first in an era when "enterprise sales" meant schmoozing CIOs at golf courses.

The episode ahead traces this journey from a cramped New York office to becoming the default monitoring platform for companies running on AWS, Azure, and Google Cloud. We'll explore how two friends from engineering school in Paris built what is essentially the Bloomberg Terminal for DevOps engineers—a single pane of glass to understand what's happening across increasingly complex cloud architectures.

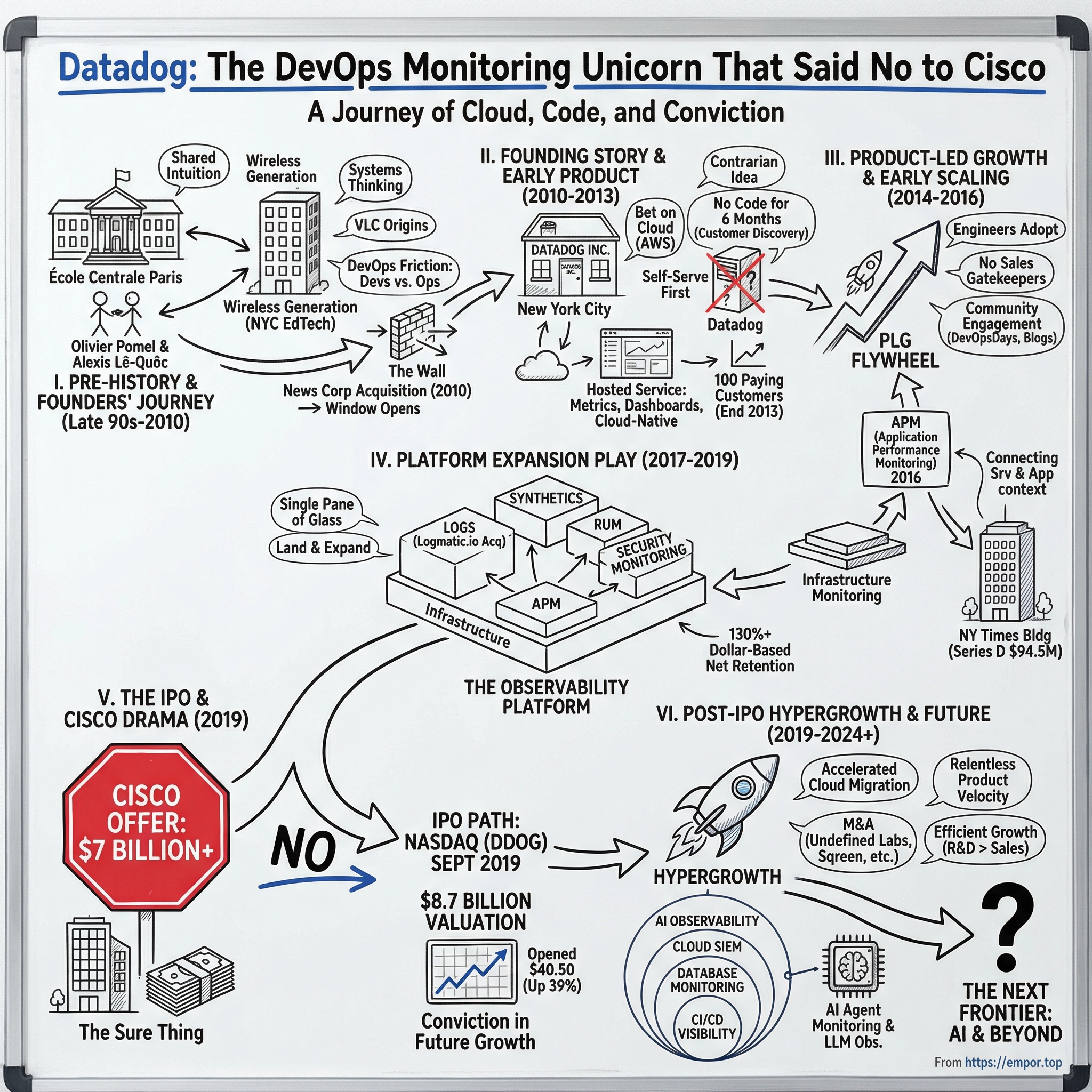

II. Pre-History: The Founders' Journey

The roots of Datadog trace back not to a Silicon Valley garage, but to the prestigious halls of École Centrale Paris in the late 1990s. There, two engineering students—Olivier Pomel and Alexis Lê-Quôc—first crossed paths. Pomel, the more reserved of the two, had already made his mark in the open-source world as the original author of VLC media player, a piece of software that would eventually be downloaded billions of times. Lê-Quôc, gregarious and technically brilliant, would later become one of the early voices in the DevOps movement that would reshape how software gets built and deployed. Their professional partnership truly began at Wireless Generation, an education technology company in New York that built assessment and data systems for K-12 teachers. At Wireless Generation, Pomel served as VP of Technology, growing the development team from a handful to close to 100 of the best engineers in New York, while Lê-Quôc served as Director of Operations, building the team and infrastructure that served more than four million students in 49 states. The scale was impressive—millions of students, thousands of schools, real-time data flowing constantly. But more importantly, it was here that the two experienced firsthand the fundamental disconnect that would inspire Datadog.

As they would later write in their S-1 filing: "In a previous life, we, Alexis and Olivier, stood on opposite sides of the dev and ops divide and witnessed how hard it was to get those two teams to understand their systems the same way and solve problems together". Pomel, on the development side, would build features and ship code. Lê-Quôc, on the operations side, would keep everything running. They spoke different languages, used different tools, and often worked at cross-purposes despite sharing the same goals.

The DevOps movement was just beginning to emerge—a philosophical shift arguing that developers and operations teams shouldn't be adversaries but collaborators. Lê-Quôc, as a member of the original "devops" movement, understood this deeply. The old model of throwing code "over the wall" from development to operations was breaking down as software ate the world and deployment cycles accelerated from months to minutes.

Then came 2010: News Corp acquired Wireless Generation. For many employees, this would be a lucrative exit and a chance to climb the corporate ladder within a media conglomerate. For Pomel and Lê-Quôc, it was the catalyst to finally pursue their own vision. They had spent nine years building someone else's dream. Now it was time to build their own.

The timing couldn't have been more perfect—or more terrifying. Amazon Web Services was just four years old. The term "cloud computing" still required explanation in most boardrooms. Most enterprises still ran their own data centers, lovingly maintained server farms with names like "prod-db-01" and "web-server-17." The idea that companies would willingly put their critical infrastructure in someone else's data center seemed absurd to many IT professionals.

But Pomel and Lê-Quôc saw what was coming. As they launched in 2010, they sensed the wind turning and understood that the cloud would become the reference technology for enterprise data management. They weren't building for the world that existed—they were building for the world that was emerging, where infrastructure would be ephemeral, where servers would spin up and down by the thousands, where the old monitoring tools built for static data centers would be hopelessly inadequate.

Their complementary skills made them an ideal founding team. Pomel brought deep technical credibility as an original author of VLC media player, a piece of open-source software that demonstrated his ability to build products used by millions. Lê-Quôc brought operational excellence and a deep understanding of what it meant to keep complex systems running at scale. Together, they had the technical chops, the operational experience, and crucially, the shared trauma of trying to manage modern infrastructure with stone-age tools.

As they prepared to leave the comfortable confines of a well-funded education technology company for the uncertainty of a startup, they made a critical decision: they would stay in New York. This might seem trivial now, but in 2010, the conventional wisdom was clear—serious tech companies needed to be in Silicon Valley. New York was for finance and media, not enterprise software. It would be the first of many contrarian bets that would define Datadog's journey.

III. Founding Story & Early Product (2010–2013)

The early days of Datadog began not with a product, but with a problem that kept both founders up at night. In the rapidly evolving landscape of 2010, companies were beginning to migrate from traditional on-premises infrastructure to the cloud, but the tools to monitor these new environments were stuck in the past. Imagine trying to watch a 4K movie through a 1990s television—that was the state of infrastructure monitoring as the cloud revolution began.

After Wireless Generation was acquired by NewsCorp, the two set out to create a product that would reduce the friction they experienced between developer and systems administration teams, who were often working at cross-purposes. They built Datadog to be a cloud infrastructure monitoring service, with dashboards, alerting, and visualizations of metrics.

The name itself—Datadog—was carefully chosen. Unlike the abstract, technical names favored by many enterprise software companies, Datadog was approachable, memorable, and captured the essence of what they were building: a loyal companion that would relentlessly track and fetch data across increasingly complex infrastructures. It suggested both reliability and friendliness, a combination that would prove central to their product philosophy. But raising money proved brutally difficult. As Olivier Pomel would later recall, "nous avons eu du mal à financer la société pendant plusieurs années" ("we had trouble financing the company for several years"). The problem wasn't just that they were in New York—it was that the problem they were solving seemed invisible to most investors. In 2010, most VCs still thought of infrastructure as servers in a data center, not ephemeral instances in the cloud. The idea that you'd need entirely new monitoring tools for this new world seemed premature at best, delusional at worst.

In 2010, Datadog launched with a seed round, with participation by NYC Seed, Contour Venture Partners, IA Ventures, Jerry Neumann and Alex Payne, among others. The company got its start at SeedStart, an incubator initiative of NYC Seed with additional backing by venture funds Contour, IA, RRE and Polaris, receiving its first $25,000 investment from the consortium. Co-founders Oliver Pomel and Alexis Lê-Quôc spent the summer of 2010 writing some of the initial code for Datadog at SeedStart's space at NYU.

The SeedStart program was one of the first institutional seed programs in New York, launched specifically to address the lack of seed capital for tech companies in the city. For Datadog, it meant not just the initial $20,000-25,000 in funding, but access to office space at NYU and mentorship from experienced entrepreneurs. It was validation that their vision wasn't crazy—at least a few people in New York believed in what they were building.

The early product was deceptively simple: a cloud infrastructure monitoring service with dashboards, alerting, and visualizations of metrics. But underneath this simplicity was a radical rethinking of how monitoring should work. Traditional monitoring tools like Nagios or Zabbix required extensive configuration, were built for static infrastructure, and treated developers and operations as separate tribes with different tools. Datadog was built from day one to be self-service, to auto-discover infrastructure, and to provide a unified view that both developers and operations teams could understand.

The technical architecture was equally forward-thinking. While competitors were building monolithic applications that customers would install on their own servers, Datadog was SaaS from the beginning. This wasn't just a deployment choice—it was fundamental to their vision. By running as a service, they could aggregate data across thousands of customers, identify patterns, and continuously improve the product without customers having to manage upgrades.

By 2012, they had gained enough traction to raise a proper Series A. In 2012, it raised a $6.2 million Series A round co-led by Index Ventures and RTP Ventures, with participation from existing investors IA Ventures, Amplify Partners, Contour Ventures and NYCSeed. Index Ventures, which had backed companies like Dropbox and Etsy, saw something special in the team and the market opportunity. The money would be used to expand development, sales, and marketing operations to serve a rapidly growing enterprise customer base.

The product philosophy during these early years was crystallized in a quote from CTO Alexis Lê-Quôc: "Our success is based on the simple premise that we built a tool practitioners want to use. It takes 5 minutes to set up, servers, clouds and apps appear automatically, and the product is as friendly as the best consumer sites." This wasn't just marketing speak—it represented a fundamental break from enterprise software orthodoxy. While competitors required weeks of professional services to deploy, Datadog could be up and running before your coffee got cold.

By the end of 2013, Datadog had surpassed 100 paying customers—a modest number by Silicon Valley standards, but each one represented validation of their core thesis. Companies were indeed moving to the cloud, infrastructure was becoming more complex and ephemeral, and the old tools simply weren't cutting it. The foundation was set for what would become one of the most impressive growth stories in enterprise software.

The rejection from investors, the struggle to explain the problem, the choice to build in New York—all of these early challenges would prove to be hidden advantages. They forced the company to be capital efficient, to focus obsessively on product-market fit, and to build deep relationships with early customers who became evangelists. As they entered 2014, the cloud revolution was about to shift into high gear, and Datadog was perfectly positioned to ride the wave.

IV. Product-Led Growth & Early Scaling (2014–2016)

The year 2014 marked an inflection point not just for Datadog, but for the entire cloud ecosystem. AWS revenue had grown to $4.6 billion, Microsoft had just appointed Satya Nadella as CEO with a mandate to embrace the cloud, and Google was pouring billions into its cloud platform. The "cloud-first" movement was no longer a fringe ideology—it was becoming enterprise orthodoxy. For Datadog, this meant their early bet was about to pay off spectacularly. The transformation began with a fundamental insight: Datadog wouldn't just be a monitoring tool, it would be a platform. In 2014, Datadog raised a $15 million Series B round led by OpenView Venture Partners. That same year, they began monitoring containers—a prescient move as Docker was just starting to gain mainstream adoption. The ability to monitor these ephemeral, lightweight compute units would prove crucial as the industry shifted from virtual machines to containerized applications.

But the real genius of Datadog's approach during this period was their go-to-market strategy. While competitors hired armies of enterprise salespeople to wine and dine CIOs, Datadog focused on developers and DevOps engineers—the practitioners who actually used the tools. They invested heavily in content marketing, hiring engineers who could write compelling technical content. Their blog became required reading for anyone dealing with cloud infrastructure, filled with practical guides on everything from monitoring Docker containers to optimizing AWS costs.

The self-service model was radical for enterprise software at the time. Customers could sign up and start seeing value in minutes without training or implementation. No six-figure professional services engagements, no months-long deployments. This wasn't just about reducing friction—it was about fundamentally reimagining how enterprise software gets adopted. Start with individual developers, prove value immediately, then expand organically as word spreads within the organization.

In 2015, the company crossed a critical milestone: surpassing 1,000 customers. They also opened a research and development office in Paris, tapping into the deep technical talent pool of their home country while maintaining their New York headquarters. This distributed model would become a competitive advantage, allowing them to hire the best engineers regardless of location—a philosophy that seems obvious post-COVID but was unconventional in 2015.

The Series C round in January 2015 brought in $31 million led by Index Ventures. By this point, Datadog had been adopted by thousands of companies, including Netflix, EA, Spotify, MercadoLibre and AdRoll. Datadog was monitoring more than 100,000 servers and drawing in over 25 billion data points a day. The scale was becoming astronomical, but more importantly, the customer list was a who's who of cloud-native companies—the very companies that other enterprises would look to as role models for digital transformation.

Then came 2016, a year that would prove transformative. The company moved its New York headquarters to a full floor of the New York Times Building, with the team doubling in size. But the real breakthrough was the beta release of Application Performance Monitoring (APM), marking Datadog's evolution from infrastructure monitoring to full-stack observability. This wasn't just adding another feature—it was a declaration of war against specialized APM vendors like New Relic and AppDynamics.

The timing was perfect. Companies were realizing that monitoring infrastructure without understanding application performance was like checking your car's oil without looking at the engine. APM allowed developers to trace requests through distributed systems, identify bottlenecks, and understand not just whether something was broken, but why. For existing Datadog customers, it meant they could consolidate vendors and get a unified view of their entire stack.

The market recognized the momentum. In January 2016, Datadog raised a massive $94.5 million Series D round led by ICONIQ Capital, one of the largest funding rounds for a New York City company that year. CEO Olivier Pomel reported the company had been tripling its revenue over the last four years and more than tripled it in 2015. Customers included Salesforce, Google, Zendesk, Airbnb, and Samsung—even HP, despite selling its own monitoring tools.

The cohort dynamics during this period told the real story. The 2014 cohort increased their ARR from $4.8M as of December 31, 2014 to $19.2M as of December 31, 2018, a multiple of 4.0x. This wasn't just customer retention—it was massive expansion within accounts. Companies would start monitoring a few servers, then expand to their entire infrastructure, then add APM, then logs. Each product made the others more valuable, creating a virtuous cycle of adoption.

By the end of 2016, Datadog had built something remarkable: a product-led growth engine that generated enterprise-scale revenues without enterprise-scale sales costs. They had proven that you could build a billion-dollar enterprise software company by focusing on developers first, by making products that were delightful to use, and by growing through expansion rather than endless new customer acquisition.

The foundation was now in place for the next phase: transforming from a monitoring company to a true observability platform. As 2017 dawned, the company had the capital, the customer base, and most importantly, the product velocity to take on much larger competitors. The startup phase was officially over—Datadog was ready to become an enterprise software powerhouse.

V. The Platform Expansion Play (2017–2019)

By early 2017, Datadog had reached an inflection point that separates good companies from great ones. With over 4,000 paying customers and north of $100 million in annual recurring revenue, they faced a critical strategic choice: remain a best-of-breed monitoring vendor or evolve into a comprehensive observability platform. The decision they made—and how they executed it—would determine whether Datadog would be a successful niche player or a generational software company. The acquisition strategy began in earnest with a September 2017 deal that would fundamentally alter Datadog's trajectory: the purchase of Logmatic.io, a Paris-based log management startup. This wasn't just about adding another feature—it was about completing what the industry would come to call the "three pillars of observability": metrics, traces, and logs. As Olivier Pomel explained at the time: "Integrating logs with the APM and Infrastructure monitoring we already provide is an important step in the evolution of the monitoring and analytics category".

The Logmatic acquisition was strategic on multiple levels. First, it brought critical technology—a platform for processing billions of log events daily with powerful visualization tools. Second, it accelerated Datadog's product roadmap by years. Building log management from scratch would have taken enormous resources and time. Third, and perhaps most importantly, it prevented competitors from acquiring the same capability. In the platform wars of enterprise software, denying assets to competitors is often as valuable as acquiring them yourself.

The integration was swift and elegant. By 2018, Datadog had fully launched its log management solution, making it one of the first companies to combine all three pillars of observability in a single platform. For customers, this meant they could finally correlate metrics showing a spike in latency with traces showing which service was affected and logs explaining exactly what went wrong. It was like giving engineers X-ray vision into their systems.

The numbers during this period tell a story of explosive growth. Revenue hit $198.1 million in 2018, up 97% year-over-year. By mid-2019, they had 8,846 customers across 100+ countries. The platform was monitoring more than 10 trillion events a day and millions of servers and containers. But the most impressive metric was customer expansion: dollar-based net retention rates hit 146% in the first half of 2019. This meant that for every dollar of revenue from existing customers a year ago, Datadog was now generating $1.46—purely from expansion within accounts. In February 2019, Datadog acquired Madumbo, a French AI-powered app-testing startup that had been incubated at Station F in Paris. This acquisition brought sophisticated AI capabilities for testing web applications without writing code—technology that would evolve into Datadog's Synthetic Monitoring product. The ability to simulate user interactions and proactively detect issues before real users encountered them was becoming table stakes for modern observability platforms.

The product velocity during this period was staggering. In 2019 alone, Datadog launched both Synthetics and Real User Monitoring (RUM), completing their frontend observability story. Synthetics allowed companies to proactively monitor application availability by simulating user traffic, while RUM provided visibility into actual user experiences. Together, they gave engineering teams both proactive and reactive insights into application performance.

The business model evolution was equally impressive. Datadog had perfected what would become the template for modern SaaS success: land with a small initial deployment, prove value quickly, then expand across products and usage. The 2014 cohort data revealed the power of this approach—customers who started with $4.8M in ARR in 2014 had expanded to $19.2M by 2018, a 4x increase. The top 25 customers showed even more dramatic expansion, with a median multiple of 33.9x from their first month as customers.

This wasn't just organic growth—it was systematic execution of a platform strategy. Each new product made existing products more valuable through correlation and context. Infrastructure metrics helped explain application traces. Logs provided the detailed context for metric anomalies. Synthetics tests could be correlated with real user monitoring to distinguish between potential and actual issues. The whole became exponentially more valuable than the sum of its parts.

By mid-2019, the company had grown to 1,212 employees across 24 countries, with 31% of full-time employees located outside the U.S., half of whom were in France. The distributed model that began as a necessity—two French founders in New York—had become a competitive advantage, allowing them to tap global talent pools and provide follow-the-sun support.

The financial metrics heading into the IPO were extraordinary. Revenue for 2018 came in at $198.1 million, up 97% year-over-year. The first half of 2019 showed $153.3 million in revenue, up 79% year-over-year. But perhaps most impressive was the efficiency: Datadog had built a nearly $200 million revenue business while raising less than $150 million in total funding. This capital efficiency would prove crucial when negotiating with potential acquirers.

As summer 2019 approached, Datadog faced a crossroads. The company had proven product-market fit, demonstrated a scalable go-to-market model, and built a comprehensive platform. They were the clear leader in cloud monitoring, but competition was intensifying. Established players like Splunk and New Relic were investing heavily in cloud capabilities. Cloud providers themselves were enhancing their native monitoring tools. The window to establish permanent market leadership was closing.

Behind closed doors, the board and management team were having intense discussions about the path forward. They could continue raising private capital—the market was frothy and they could easily command a multi-billion dollar valuation. They could pursue strategic partnerships with cloud providers. Or they could go public and use the currency of public stock to accelerate growth through acquisitions.

Then came the phone call that would test their resolve: Cisco wanted to buy the company. The networking giant, which had successfully acquired AppDynamics for $3.7 billion right before its IPO in 2017, saw Datadog as the missing piece in its enterprise software portfolio. The offer was compelling—north of $7 billion, representing a massive premium to their last private valuation. For the founders and early employees, it meant instant liquidity and the resources of a Fortune 500 company behind their products.

But Pomel and Lê-Quôc had built Datadog to be a generational company, not a product line within a larger corporation. They believed the cloud transformation was still in its early innings. They saw a future where every company would need comprehensive observability, where the complexity of cloud-native architectures would make their platform indispensable. Selling now would mean giving up that vision—and potentially billions in future value creation—for the certainty of a rich but capped outcome.

The stage was set for one of the most dramatic decisions in recent tech history: would they take the bird in hand, or bet on building something even bigger?

VI. The IPO & Cisco Drama (2019)

The summer of 2019 found Olivier Pomel pacing the conference room on the 45th floor of the New York Times Building. Through the floor-to-ceiling windows, Manhattan stretched out below—the city that had nurtured Datadog from a two-person startup to a company now valued in the billions. On the table before him lay two documents: a draft S-1 filing for an initial public offering, and a term sheet from Cisco Systems offering to acquire Datadog for what sources would later describe as "significantly higher than $7 billion. "The Cisco offer had arrived just weeks before the planned IPO. According to sources familiar with the matter who spoke to Bloomberg, Cisco offered "significantly higher than the $7 billion valuation" that Datadog was targeting in its initial filing. For context, this was the same Cisco that had successfully acquired AppDynamics for $3.7 billion in January 2017, literally days before that company's planned IPO. That acquisition had been considered a coup for Cisco—snatching a fast-growing application performance monitoring company at the last minute, preventing it from becoming a public competitor.

Now Cisco wanted to repeat the playbook with Datadog. The strategic rationale was compelling: combine AppDynamics' application monitoring with Datadog's infrastructure and log management capabilities to create an end-to-end observability powerhouse. For Cisco, struggling to transition from hardware to software, Datadog represented instant credibility in the cloud-native world. The price—rumored to be north of $7.5 billion and possibly as high as $8 billion—reflected Cisco's desperation to own the future of IT monitoring.

The board meetings during this period were intense. On one side were arguments for taking the deal: immediate liquidity for employees and investors, the resources of a Fortune 500 company, guaranteed outcome versus IPO uncertainty. The market conditions in September 2019 were volatile—WeWork had just pulled its IPO, Uber and Lyft were trading below their offering prices. Taking Cisco's money would eliminate execution risk.

But Pomel and Lê-Quôc had a different vision. Datadog rebuffed the advance to pursue a stock listing because it felt it could be worth more as a public company over time. They believed the cloud transformation was just beginning. AWS was growing at 35% annually and approaching a $40 billion run rate. Every company was becoming a software company. The complexity of cloud-native architectures was exploding. Datadog wasn't just riding a wave—they were selling surfboards in a world where the ocean was rising.

The decision to reject Cisco and proceed with the IPO was announced internally in early September. According to employees present, Pomel addressed the company with characteristic understatement: "We believe we're just getting started. Cisco's offer validates what we've built, but it doesn't reflect what we're going to build." The employees, many of whom held stock options, erupted in applause—they were betting their financial futures on the founders' vision.

The IPO roadshow that followed was a masterclass in narrative construction. The initial price range of $19-21 per share valued the company at roughly $5.5-6 billion. But demand was overwhelming. Institutional investors who had watched Datadog grow from the sidelines finally had their chance to buy in. The range was raised to $24-26, valuing the company at up to $7.5 billion. Even that proved conservative.

On the evening of September 18, 2019, the final pricing was set: $27 per share, above the already-raised range. Datadog went public via an IPO on the Nasdaq exchange on September 19, 2019, selling 24 million shares and raising $648 million, valuing the company at $8.7 billion. This was already higher than Cisco's reported offer, validating the founders' decision before the first trade.

September 19, 2019, 9:30 AM Eastern: The opening bell rang at the Nasdaq. Datadog's ticker symbol—DDOG—appeared on screens around the world. The first trade crossed at $40.12, a 48% pop from the IPO price. By the end of the day, shares closed at $37.55, up 39% from the offering price. The company's market cap had soared to nearly $11 billion.

The financial media had a field day with the story. Datadog Inc., a software company that bet it could do better as a public company than in a Cisco Systems Inc. buyout, jumped 39% after raising $648 million in its initial public offering. It was a David-and-Goliath narrative that resonated: two French engineers in New York had built a company that rejected one of tech's giants and were immediately proven right by the market.

For Cisco, the rejection was a significant blow. The company had been trying to transform itself into a software powerhouse, and Datadog would have accelerated that transition by years. The fact that Datadog immediately traded above Cisco's offer price added insult to injury. Some analysts speculated that Cisco should have bid higher, but others argued that Datadog was never really for sale—the IPO filing had been in motion for months, and the founders' commitment to independence was unwavering.

The contrast with AppDynamics was stark. That company's founder and CEO, Jyoti Bansal, had agreed to sell to Cisco just days before the IPO, later expressing some regret about not seeing the public market journey through. Datadog's founders had learned from that example. They understood that the real value creation in enterprise software comes post-IPO, when you have the currency of public stock for acquisitions, the visibility to attract talent, and the independence to execute your vision.

The IPO also marked a triumph for patient capital. Index Ventures, which had led the Series A in 2012 at a valuation of roughly $50 million, saw their stake worth billions. Individual employees who had joined in the early years became millionaires overnight. But perhaps most importantly, the successful IPO validated a new model for enterprise software: you could build a massive company by focusing on developers first, by being radically transparent with pricing, by building products that people actually wanted to use.

As the champagne flowed at Datadog's IPO party that evening at the Rainbow Room atop Rockefeller Center, Pomel and Lê-Quôc stood looking out over Manhattan. They had bet everything on their vision of the future—and won. But both understood this was just the beginning. Being public meant quarterly earnings calls, activist investors, and constant scrutiny. The real test wasn't whether they could reject $7 billion—it was whether they could build something worth $70 billion.

The market would soon provide its answer.

VII. Post-IPO Hypergrowth & Product Velocity (2019–2024)

The morning after Datadog's IPO party, as Manhattan's street cleaners swept away the previous night's celebration debris, Olivier Pomel sent a company-wide email with a simple message: "Day 1 starts now." While the public markets had validated their decision to reject Cisco, the real work of building a generational company was just beginning. What happened next would shock even the most bullish analysts on Wall Street. The numbers that followed were nothing short of extraordinary. Datadog annual revenue for 2020 was $603.47 million, a 66.34% increase from 2019—remarkable considering the global pandemic that crushed many enterprise software companies. While competitors struggled with delayed deals and frozen IT budgets, Datadog thrived. The reason was simple: as companies scrambled to enable remote work and accelerate cloud migrations, they needed visibility into their rapidly changing infrastructure more than ever.

Revenue growth continued to accelerate: 2021 saw $1.03 billion (70.48% growth), 2022 hit $1.675 billion (62.82% growth), 2023 reached $2.128 billion (27.06% growth), and 2024 achieved $2.684 billion (26.12% growth). In just five years as a public company, Datadog had grown revenue more than 13x from their IPO run rate. Wall Street analysts, who had projected $610 million in revenue for 2021, were off by more than 100%. The company had achieved something rare in enterprise software: sustained hypergrowth at scale. But growth was only part of the story. The real magic was happening in product development and strategic acquisitions. The post-IPO acquisition spree was surgical and strategic. In August 2020, Datadog acquired Undefined Labs, a testing and observability company for developer workflows, extending visibility into CI/CD pipelines. In February 2021, they announced dual acquisitions: Timber Technologies (developers of Vector, a high-performance observability data pipeline) and Sqreen (an application security platform), marking their serious entry into the security space.

November 2021 brought the acquisition of Ozcode, a live debugging solution that brings code-level visibility into production environments. The pattern was clear: each acquisition either added a new product category (security, CI/CD monitoring) or deepened existing capabilities (debugging, data pipelines). Unlike many acquirers who struggle with integration, Datadog had perfected the playbook: acquire, integrate rapidly into the platform, and cross-sell to the existing base.

The customer metrics told the real story of platform power. By December 31, 2024, Datadog had 462 customers with ARR of $1 million or more, up from 317 just five years earlier. More impressively, they had about 3,610 customers with ARR of $100,000 or more, up from 2,780. This wasn't just customer acquisition—it was systematic account expansion as customers adopted more products.

The product velocity during this period was breathtaking. As Olivier Pomel noted in the 2024 earnings call: "During 2024, we delivered hundreds of new features and capabilities to help our customers as they migrate to the cloud and adopt new technologies like next-gen AI." This wasn't hyperbole—the company was shipping major features weekly, minor updates daily. The platform now encompassed:

- Observability: Infrastructure monitoring, APM, log management, real user monitoring, synthetics, network performance monitoring

- Security: Cloud security posture management, cloud workload security, application security management

- Developer Tools: CI/CD visibility, incident management, service catalog

- Business Analytics: Cloud cost management, product analytics

The financial performance reflected this product expansion. Operating cash flow for 2024 hit $871 million, with free cash flow of $775 million—a remarkable 32% free cash flow margin. The company had achieved something rare in SaaS: rapid growth with significant profitability. They were no longer burning cash to grow; they were generating it.

Perhaps the most significant strategic development was the relationship with cloud providers. In 2019, Datadog signed an agreement with AWS to purchase at least $225 million of cloud services through April 2022. Rather than competing with cloud providers' native monitoring tools, Datadog positioned itself as complementary—the Switzerland of observability that could monitor across all clouds. This neutrality became a key selling point for enterprises pursuing multi-cloud strategies.

The market dynamics during this period were fascinating. Competitors were struggling to keep pace. New Relic, once the darling of APM, saw its growth stagnate and eventually went private in a $6.5 billion deal. Splunk, the log management giant, was acquired by Cisco for $28 billion—a massive price but one that reflected Cisco's desperation after missing out on Datadog. Meanwhile, cloud providers enhanced their native tools but couldn't match Datadog's breadth or ease of use.

The COVID-19 pandemic, which could have been a disaster for enterprise software spending, instead accelerated Datadog's growth. As companies rushed to enable remote work and accelerate digital transformation, the need for comprehensive monitoring became mission-critical. You couldn't manage what you couldn't see, and in a world of distributed teams and cloud infrastructure, Datadog provided the eyes.

By 2024, the company that Cisco had tried to buy for $7+ billion was generating nearly $2.7 billion in annual revenue with a market cap that had peaked above $100 billion. The decision to reject the acquisition and go public had been vindicated many times over. But more importantly, Datadog had achieved what few companies manage: they had become essential infrastructure for the modern internet.

The transformation was complete—or was it? As 2025 dawned, new challenges emerged. AI was reshaping software development. Observability data was exploding exponentially. Competition was intensifying from both established players and well-funded startups. The next chapter of Datadog's story would test whether they could maintain their innovation velocity while operating at massive scale.

VIII. Business Model & Unit Economics Deep Dive

Inside Datadog's New York headquarters, there's a dashboard that employees pass every day showing real-time metrics: new customers signed, expansion revenue, product adoption rates, and gross margins. It's a fitting metaphor for a company whose business model is essentially selling dashboards to monitor dashboards. But beneath this meta-irony lies one of the most elegant SaaS business models ever constructed—a machine that turns complexity into cash flow with remarkable efficiency. The foundation of Datadog's business model is consumption-based pricing—customers pay based on how much data they ingest and analyze, not just the number of seats or servers. This aligns perfectly with the cloud era's elastic infrastructure. When a customer's business grows and their infrastructure scales, Datadog's revenue scales automatically. When Netflix releases a hit show and traffic spikes, Datadog makes more money. It's a beautiful alignment of incentives.

The gross margins tell the story of operational excellence. In 2024, Datadog maintained gross margins in the 75-77% range—exceptional for a company processing trillions of data points daily. These margins reflect the leverage inherent in the SaaS model: the marginal cost of serving an additional customer or processing an additional gigabyte is minimal. The heavy lifting—building the ingestion pipelines, storage systems, and query engines—has already been done.

But the real magic happens in the unit economics of customer expansion. A typical Datadog customer journey looks like this: Start with infrastructure monitoring for a small team ($10K annual contract), add APM as you scale ($50K expansion), integrate log management when complexity grows ($100K expansion), layer in security and RUM ($250K+ total contract). The 2014 cohort data proved this wasn't theoretical—customers spending $4.8M in 2014 were spending $19.2M by 2018, a 4x expansion without any additional customer acquisition cost.

The sales efficiency metrics are where Datadog truly differentiates itself. While traditional enterprise software companies might spend $1.50 or more to generate $1 of new revenue, Datadog's product-led growth model inverts this. Sales and marketing expenses have declined from 45% of revenue in 2018 to just 29% in Q2 2024. Meanwhile, R&D expenses have increased from 27% to 43% of revenue over the same period. This is the opposite of most enterprise software companies—Datadog spends more on building products than selling them.

The free cash flow generation is perhaps the most impressive metric. For 2024, Datadog generated $871 million in operating cash flow and $775 million in free cash flow—a 29% free cash flow margin. This isn't a company burning cash to grow; it's a cash-generating machine. The company ended 2024 with $4.4 billion in cash and marketable securities, giving it enormous flexibility for acquisitions, R&D investment, or weathering economic downturns.

The network effects embedded in the model are subtle but powerful. As more companies adopt Datadog, the platform becomes smarter through pattern recognition across customers. An anomaly detection algorithm trained on millions of deployments can identify issues faster than any single company could. The 750+ integrations create switching costs—migrating from Datadog means reconfiguring hundreds of data pipelines and retraining teams on new tools.

The land-and-expand dynamics are best illustrated through customer segmentation. Datadog ended 2024 with: - 462 customers with ARR > $1 million (17% year-over-year growth) - 3,610 customers with ARR > $100K (13% growth) - 28,700+ total customers

The pyramid is healthy—plenty of small customers to grow into large ones, and large customers continuing to expand. The dollar-based net retention rate, consistently above 130%, means that even without adding new customers, revenue would grow 30% annually just from expansion.

The capital efficiency is remarkable. Unlike traditional software companies that require massive upfront investment in sales and marketing, Datadog's model generates leverage through product adoption. A developer finds Datadog through a Google search, signs up for a free trial, implements it in minutes, sees value immediately, and becomes an internal champion. The product sells itself, and sales teams focus on expansion and enterprise agreements rather than cold calling.

The pricing model deserves special attention. While competitors often have complex pricing with hidden costs, Datadog's pricing is transparent and predictable. You pay for what you use—hosts monitored, traces analyzed, logs ingested. This transparency builds trust and reduces friction in the sales process. CFOs can model costs accurately, and there are no surprise overages or licensing audits.

The strategic positioning as Switzerland in the cloud wars has proven invaluable. While AWS, Azure, and Google Cloud all offer native monitoring tools, Datadog provides unified visibility across all platforms. For enterprises pursuing multi-cloud strategies—which is essentially everyone—this neutrality is essential. Datadog isn't competing with cloud providers; it's complementing them.

The subscription revenue model provides incredible predictability. With most customers on annual contracts and high retention rates, Datadog can forecast revenue with remarkable accuracy. This predictability allows for aggressive R&D investment—you can hire engineers and commit to multi-year product roadmaps when you know the revenue will be there.

Looking at the lifetime value to customer acquisition cost (LTV/CAC) ratio, Datadog achieves metrics that make venture capitalists salivate. With net retention above 130% and gross margins of 75%+, the lifetime value of a customer is enormous. Meanwhile, the product-led acquisition model keeps CAC low. The result is unit economics that compound wealth over time rather than destroying it.

The model isn't without risks. The consumption-based pricing that provides upside during growth can work in reverse during recessions—if customers scale down infrastructure, Datadog's revenue declines automatically. Competition from cloud providers could intensify if they decide monitoring is strategic enough to subsidize. And the technical complexity of the product means there's always a risk of a major outage that could damage customer trust.

But perhaps the most impressive aspect of Datadog's business model is its simplicity. At its core, the company does one thing: it helps companies see what's happening in their infrastructure and applications. Everything else—the pricing model, the product expansion, the go-to-market strategy—flows from this central mission. In a world of increasing complexity, Datadog sells simplicity. And simplicity, it turns out, is worth about $45 billion in market cap.

IX. Competition & Market Dynamics

In the gleaming offices of Splunk's San Francisco headquarters, executives watched with growing alarm as Datadog's market cap surpassed theirs in 2021. Splunk had pioneered log management, essentially creating the market for searching and analyzing machine data. They had a two-decade head start, thousands of enterprise customers, and over $3 billion in annual revenue. Yet somehow, a company founded when Splunk was already public was now worth more. The story of how this happened reveals everything about the changing dynamics of enterprise software competition.

The competitive landscape in observability had undergone a seismic shift since 2019. Datadog has been recognized as a Leader in the 2024 Gartner® Magic Quadrant™ for Observability Platforms—for the fourth consecutive year, cementing its position as the gold standard against which all others were measured. But the market was no longer just about traditional monitoring vendors. It had become a three-way battle between established APM players, cloud provider native tools, and a new generation of AI-native observability startups.

The traditional competitors had each chosen different paths. Splunk, once the undisputed king of log management with over $3 billion in revenue, struggled to transition to cloud-native architectures. The company's on-premises heritage, which had been its strength, became an albatross in the cloud era. Cisco's acquisition of Splunk for $28 billion in 2024 was partly defensive—they needed to own something in observability after missing out on Datadog. But integrating Splunk with AppDynamics proved more challenging than anticipated, creating confusion rather than synergy.

New Relic's journey was perhaps the most dramatic. Once valued at over $5 billion as a public company, New Relic struggled with the transition from APM to full-stack observability. Their stock price languished as customers defected to more modern platforms. In 2023, they went private in a $6.5 billion deal with Francisco Partners and TPG, hoping that freedom from quarterly earnings pressure would allow them to rebuild. New Relic specializes in application performance monitoring (APM) and observability solutions, providing deep insights into application performance, infrastructure, and customer experience. Its real-time monitoring capabilities and extensive integration make it a strong competitor in the market.

Dynatrace offers AI-powered observability solutions for application performance monitoring, infrastructure monitoring, and digital experience management. With its automatic discovery and dependency mapping, Dynatrace provides automation and actionable insights for optimizing digital experiences. The company had pivoted hard into AI-powered observability, betting that automation would differentiate them. Their "Davis AI" could allegedly predict problems before they occurred, though customers remained skeptical about letting AI make production decisions.

The cloud providers represented a different kind of threat. AWS CloudWatch, Azure Monitor, and Google Cloud Operations had the ultimate distribution advantage—they were already there. Every customer using cloud infrastructure got basic monitoring for free. The question was whether "good enough" native tools would eventually subsume the need for specialized platforms. Other vendors offering obverservability monitoring platforms include IBM, Cisco, Microsoft, Sumo Logic, AWS, and LogicMonitor as examples.

But Datadog's real moat wasn't just technology—it was the network effects of their platform. With over 750 integrations, switching away meant reconfiguring hundreds of data pipelines. Their unified platform approach meant that metrics, traces, and logs were deeply interconnected. You couldn't just replace one piece without affecting the others. This created switching costs that grew exponentially with usage.

The market itself was exploding in size. The Observability Market is expected to reach USD 2.9 billion in 2025 and grow at a CAGR of 15.90% to reach USD 6.10 billion by 2030. Other estimates were even more bullish: The global observability tools and platforms market size was estimated at USD 2.71 billion in 2023 and is expected to grow at a CAGR of 10.7% from 2024 to 2030. The discrepancy in market size estimates reflected the difficulty in defining observability's boundaries—did it include traditional monitoring? Security? Business analytics?

After analyzing the data thoroughly, my analysis suggests that the observability market will be worth closer to $12 billion in 2024 and growing at approximately 20% annually. This more expansive view included not just pure-play observability vendors but also the observability components of broader platforms. The addressable market was even larger: Observability spend is often estimated at 15-20% of cloud infrastructure costs (source). The global cloud infrastructure market is projected to reach $261 billion in 2024. By that logic, the observability market could be $40-$50 billion.

The emergence of AI and large language models created both opportunity and threat. Generative-AI workloads demand monitoring of token usage, model drift, and bias, spurring vendors like Datadog to launch dedicated LLM observability modules. Datadog had quickly launched LLM Observability to help companies monitor their AI applications—tracking token usage, latency, and model performance. But AI also threatened to commoditize traditional observability by automating root cause analysis and anomaly detection.

The cost dynamics of observability were becoming a critical battleground. Not only are observability tools costly, costing about 30% of a company's outside vendor spending, but they also lack visibility and transparency in their pricing, making it nearly impossible to calculate how their pricing has been calculated. Companies were starting to push back on observability costs that could exceed their actual infrastructure spending. This created an opening for open-source alternatives and cost-optimized vendors.

As we can see from all of the above charts, Splunk and New Relic have nearly caught up to the offerings of Datadog on most fronts. Through their recent push towards observability, recent acquisitions, contributions to open-source projects, and partnerships. They also offer aggressive pricing, trying to undercut Datadog's premium positioning. But Datadog's response was elegant: they didn't compete on price but on value. Their platform's ability to reduce mean time to resolution (MTTR) by hours could justify almost any price tag.

The geographic expansion of the market favored Datadog's distributed model. By region, North America led with 36.9% revenue share in 2024, whereas Asia-Pacific is on course for a 20.1% CAGR, the fastest globally. Having engineering offices in Paris and New York positioned them well to capture both established and emerging markets.

The competitive dynamics were further complicated by the rise of specialized players. Companies like Monte Carlo focused exclusively on data observability. Honeycomb pioneered observability for microservices. Lightstep (acquired by ServiceNow) brought distributed tracing expertise. Each carved out a niche, but none achieved Datadog's platform breadth.

As one industry analyst noted: "The observability market isn't winner-take-all, but it's definitely winner-take-most. Datadog has established themselves as the default choice for cloud-native companies. Competitors are left fighting over specific use cases or price-sensitive customers." The question wasn't whether Datadog would maintain leadership, but whether the market was large enough for multiple winners.

X. Playbook: Business & Investing Lessons

If you were to distill Datadog's journey into a playbook for building a generational enterprise software company, it would read like a contrarian's guide to Silicon Valley wisdom. Nearly every major decision the founders made flew in the face of conventional advice, yet these choices became their greatest strengths. The lessons from their journey offer a masterclass in building enduring value in enterprise software.

Lesson 1: Product-Led Growth at Enterprise Scale Datadog proved that you could build a multi-billion dollar enterprise software company without an army of salespeople. Their self-service model, where developers could sign up and see value in minutes, revolutionized enterprise software distribution. The key insight: make the product so good that it sells itself, then use sales teams for expansion rather than initial adoption. This inverted the traditional enterprise sales model and dramatically improved unit economics.

Lesson 2: Timing Markets vs. Creating Them Pomel and Lê-Quôc didn't create the cloud computing market—they recognized it was inevitable and positioned themselves perfectly for when it arrived. They built for the world that was coming, not the world that existed. Starting in 2010, just as AWS was gaining traction but before cloud was mainstream, gave them time to build the product before demand exploded. The lesson: you don't need to create a market, but you need to time it perfectly.

Lesson 3: The Power of Saying No Rejecting Cisco's $7+ billion offer in 2019 seemed crazy at the time. The market was volatile, tech IPOs were struggling, and they had a guaranteed exit. But the founders understood their business's compounding potential. They believed the cloud transformation was in early innings and their platform would become more valuable over time. The discipline to reject a life-changing offer in pursuit of a bigger vision separates good companies from great ones.

Lesson 4: Platform Beats Point Solution While competitors focused on being best-of-breed in specific areas—Splunk in logs, New Relic in APM—Datadog systematically built a platform. Each product made the others more valuable through correlation and context. The lesson: in enterprise software, the platform eventually wins because IT buyers prefer fewer vendors and integrated solutions. But you must start with a wedge product that's genuinely superior.

Lesson 5: Technical Founders with Business Acumen Pomel and Lê-Quôc weren't just engineers—they understood business strategy. They priced transparently when competitors obscured costs. They focused on developers when others chased CIOs. They stayed independent when others sold. The combination of deep technical credibility with strategic business thinking is rare but powerful. Technical founders who can also think strategically about markets, pricing, and distribution have an enormous advantage.

Lesson 6: Capital Efficiency Enables Optionality By the time of IPO, Datadog had raised less than $150 million but built a $200 million revenue business. This capital efficiency gave them leverage in all negotiations—with investors, with Cisco, with the public markets. When you don't need money, you can make decisions based on long-term value rather than short-term necessity. The less capital you need, the more control you retain.

Lesson 7: Geographic Arbitrage in Talent Building in New York while maintaining R&D in Paris gave Datadog access to world-class talent at lower costs than Silicon Valley. They could hire the best engineers regardless of location, a philosophy that seemed radical in 2010 but prophetic post-COVID. The lesson: talent is globally distributed, and companies that can effectively manage distributed teams have a competitive advantage.

Lesson 8: Customer Success Through Product Excellence Datadog's net retention rates above 130% weren't achieved through account management heroics but through product excellence. Customers expanded usage because the product delivered value, not because salespeople convinced them. This organic expansion is the holy grail of SaaS—growth without incremental sales cost.

Lesson 9: The Compound Effect of Velocity Shipping hundreds of features annually might seem like feature bloat, but for Datadog it created competitive distance. Competitors couldn't match their pace of innovation. Each feature might be small, but collectively they created an insurmountable lead. Sustained velocity over time creates exponential competitive advantages.

Lesson 10: Building for Practitioners, Not Purchasers Traditional enterprise software focused on the economic buyer—the CIO or VP who signed the check. Datadog focused on the user—the developer or DevOps engineer who actually used the product. By delighting practitioners, they created bottom-up adoption that was harder to displace than top-down sales. The best enterprise software today is sold like consumer software—through viral adoption rather than golf course deals.

Lesson 11: Transparency as Competitive Advantage In a market where enterprise software pricing was intentionally opaque, Datadog published their prices online. This transparency built trust with developers and accelerated sales cycles. When customers can model costs accurately, they make decisions faster. Transparency that seems risky often becomes a competitive advantage.

Lesson 12: The New York Advantage Building in New York, away from Silicon Valley's echo chamber, gave Datadog a different perspective. They were closer to their customers—financial services, media companies, traditional enterprises going digital. This proximity to real enterprise needs, rather than Silicon Valley's latest fad, kept them grounded in solving actual problems.

The meta-lesson from Datadog's playbook is that conventional wisdom is often wrong. Building in New York was supposed to be a disadvantage. Rejecting acquisition offers was supposed to be greedy. Focusing on developers was supposed to limit enterprise sales. Yet each contrarian decision, executed well, became a competitive advantage.

For investors, Datadog offers lessons in identifying future winners. Look for companies with exceptional net retention rates—it's the clearest signal of product-market fit. Value capital efficiency over growth at all costs. Bet on technical founders who also understand business. And perhaps most importantly, recognize that the biggest returns come from companies that reject early exits to build something transformational.

XI. Analysis & Bear vs. Bull Case

Standing at a $45 billion market capitalization in August 2025, down from peaks above $100 billion but still representing a 5x return from its IPO price, Datadog presents one of the most fascinating risk-reward profiles in enterprise software. The company occupies a unique position: dominant in its category, generating significant cash flow, yet trading at valuations that assume continued hypergrowth. Understanding both the bull and bear cases is essential for anyone trying to evaluate Datadog's future.

The Bull Case: A Generational Compounding Machine

The optimistic view starts with the total addressable market expansion. If observability truly represents 15-20% of cloud infrastructure spend, and cloud infrastructure reaches $261 billion in 2024, we're looking at a $40-50 billion market opportunity. Even if Datadog captures just 20% of this market, that's $8-10 billion in revenue—3-4x their current run rate. The secular tailwinds of digital transformation, cloud migration, and increasing system complexity aren't slowing down.

The platform strategy is working exactly as designed. With 462 customers generating over $1 million in ARR and growing 17% year-over-year, Datadog has proven it can systematically expand within accounts. These aren't just any customers—they include the world's most sophisticated technology companies. When Netflix, Airbnb, and Spotify choose Datadog, it validates the platform's technical superiority.

AI represents a massive new growth vector. Every company experimenting with large language models needs to monitor token usage, latency, and model performance. Datadog's LLM Observability positions them to capture value from the AI revolution. As AI applications move to production, the need for specialized monitoring will explode. Datadog could become as essential to AI applications as they are to cloud infrastructure.

The financial profile is best-in-class. Growing at 26% with 32% free cash flow margins is almost unheard of at this scale. The company generated $775 million in free cash flow in 2024—they're not burning money to grow, they're printing it. With $4.4 billion in cash and no debt, they have enormous flexibility for acquisitions, buybacks, or weathering any economic storm.

The competitive moat is widening, not narrowing. Every new product launch, every new integration, every new customer makes the platform stickier. The switching costs are enormous—not just technical but organizational. Teams trained on Datadog, runbooks written for Datadog alerts, dashboards built in Datadog—all create lock-in that compounds over time.

International expansion remains early. While North America dominates revenue, the rest of the world is just beginning digital transformation. As European and Asian companies modernize their infrastructure, Datadog is perfectly positioned to capture this demand. The Paris R&D center gives them credibility and presence in European markets.

The Bear Case: Priced for Perfection in an Uncertain World

The pessimistic view starts with valuation. At 17x revenue and a P/E ratio over 300, Datadog is priced for perfection. Any stumble—a missed quarter, a delayed product launch, a major outage—could trigger a significant re-rating. The stock's 50% decline from its peaks shows how quickly sentiment can shift when growth stocks fall out of favor.

Competition is intensifying from every direction. Cloud providers are investing heavily in native monitoring tools. AWS CloudWatch, Azure Monitor, and Google Cloud Operations get better every year. While they may never match Datadog's functionality, they might become "good enough" for many use cases. When the CFO asks why you're paying for Datadog when AWS provides monitoring for free, it becomes a harder conversation.

The consumption-based model that drove growth could become a headwind. In a recession, as companies scale down infrastructure to cut costs, Datadog's revenue automatically declines. Unlike seat-based SaaS that's sticky during downturns, consumption-based pricing provides no floor. The 2022-2023 growth deceleration from 83% to 27% shows this sensitivity to macro conditions.

Market saturation is a real risk. Most large enterprises already use some observability solution. The greenfield opportunity is shrinking, and growth increasingly depends on taking share from competitors or expanding within existing accounts. At some point, even the best customers hit a ceiling on observability spend.

The innovator's dilemma looms large. Open-source alternatives like Prometheus and Grafana provide "good enough" observability for many use cases. A new generation of AI-native observability startups could disrupt Datadog the way they disrupted legacy monitoring vendors. Success in technology is often temporary—today's disruptor becomes tomorrow's incumbent.

Talent retention could become challenging. With the stock down 50% from highs, employee options are underwater. The best engineers have endless opportunities, and maintaining product velocity requires keeping top talent. Any brain drain could slow innovation and open the door for competitors.

The Balanced View: Navigating Uncertainty

The truth likely lies between these extremes. Datadog is neither a guaranteed compounder nor a bubble waiting to burst. It's a high-quality business with real competitive advantages operating in a large and growing market, but facing intensifying competition and macroeconomic uncertainty.

The key variables to watch are: - Net retention rates: Staying above 130% validates the platform strategy - New product adoption: Success in security and AI observability expands the TAM - Competitive dynamics: Market share versus cloud providers and other platforms - Macroeconomic conditions: Cloud spending growth and IT budget priorities - Innovation velocity: Ability to maintain product leadership while scaling

For long-term investors, Datadog represents a bet on the continued complexification of technology infrastructure. As systems become more distributed, more dynamic, and more critical to business operations, the need for comprehensive observability should grow. The question is whether Datadog can maintain its leadership position and capture enough of this value to justify its premium valuation.

For traders and short-term investors, Datadog is a high-beta play on cloud spending and growth stock sentiment. The stock will likely remain volatile, offering opportunities for those who can time entries and exits. But predicting short-term movements in a stock this sensitive to narrative shifts is treacherous.

The ultimate test will be whether Datadog can do what few technology companies achieve: successfully navigate the transition from hypergrowth to mature growth while maintaining competitive advantages. IBM did it in mainframes, Microsoft in personal computers, and Amazon in e-commerce. Whether Datadog joins this elite group or becomes another formerly high-flying software company that couldn't sustain its trajectory will define the next decade of its story.

XII. Epilogue & Looking Forward

As Olivier Pomel looked out from Datadog's New York headquarters in August 2025, the view had changed dramatically from that September day in 2019 when he rejected Cisco's billions. The Manhattan skyline was dotted with cranes—the city rebuilding, reimagining itself, much like the technology industry Datadog served. The company that had started in a cramped office with two engineers now employed over 5,200 people across the globe, monitored trillions of data points daily, and had become as essential to the internet's infrastructure as the cloud providers themselves.

The 2024 numbers told a story of sustained excellence in an industry where yesterday's winners quickly become tomorrow's has-beens. Revenue of $2.68 billion, growing 26% year-over-year, with free cash flow margins of 32%—metrics that would make any CFO envious. The company had delivered on its promise to shareholders, generating returns that dwarfed Cisco's offer. But Pomel knew the past was prologue. The next chapter would be written in an entirely different context.

The guidance for 2025—revenue of $3.175 to $3.195 billion—represented continued growth above 20%, remarkable for a company of Datadog's scale. But maintaining this trajectory required navigating multiple transformations simultaneously. The shift to AI-native applications wasn't just another technology trend—it was a fundamental reimagining of how software gets built and deployed. Large language models didn't just need monitoring; they needed entirely new observability paradigms for tracking token usage, model drift, and hallucination detection.

Datadog's response had been characteristically swift. The launch of LLM Observability provided visibility into AI applications, from prompt engineering to model performance. But this was just the beginning. As Pomel noted in the Q4 2024 earnings call, the company had "delivered hundreds of new features and capabilities" during the year. This relentless product velocity—shipping major features weekly, minor updates daily—had become Datadog's signature. It was exhausting for competitors to match and delightful for customers to experience.

The expansion into security represented another transformation. With the acquisitions of Sqreen and the launch of Cloud Security Posture Management, Datadog was blurring the lines between observability and security. In a world where every company was a software company and every software company was a target, the convergence of monitoring and security was inevitable. The question was whether Datadog could build security capabilities that matched their observability excellence.

The competitive landscape of 2025 looked nothing like 2019. Splunk, now part of Cisco, was trying to integrate with AppDynamics—creating either a formidable competitor or a Frankenstein's monster of incompatible technologies. New Relic had gone private, freed from public market pressure but also from public market capital. Dynatrace was betting everything on AI-powered automation. And the cloud providers continued their relentless march toward "good enough" native tools.

But perhaps the biggest change was in customer expectations. The COVID-19 pandemic had accelerated digital transformation by a decade. Every business now ran on software, every software ran in the cloud, and every cloud deployment needed observability. But customers were also becoming more sophisticated and cost-conscious. The days of unlimited observability budgets were ending. Companies wanted value, not just visibility.

Datadog's response was to become more than just a monitoring platform—to become an essential part of the software development lifecycle. From CI/CD visibility to incident management to cost optimization, they were expanding the definition of observability. The vision was ambitious: to be the single source of truth for everything happening in a company's technology stack.

The international opportunity remained massive. While North America generated the majority of revenue, the rest of the world was just beginning its cloud journey. The Paris R&D office, once a quirky decision by French founders, had become a strategic asset for European expansion. The Asian markets, particularly Japan and South Korea with their sophisticated technology sectors, represented the next frontier.

But success wasn't guaranteed. The history of enterprise software is littered with companies that dominated their categories only to be disrupted by the next wave of innovation. CA Technologies, BMC Software, Mercury Interactive—all were once high-flyers that failed to navigate technology transitions. Datadog's challenge was to avoid their fate, to remain paranoid and innovative even as they became the incumbent.

The organizational culture would be critical. As the company grew from 1,200 employees at IPO to over 5,200 in 2025, maintaining the startup mentality became harder. The founders' continued involvement—both Pomel and Lê-Quôc remained deeply engaged in product and strategy—provided continuity. But eventually, every company must navigate a founder transition. How Datadog handled this inevitable passage would determine whether it became a generational company or just another successful exit.

The financial position provided a cushion for experimentation. With $4.4 billion in cash and generating nearly $800 million in free cash flow annually, Datadog could afford to make bold bets. Whether through acquisitions, organic R&D, or entirely new ventures, they had the resources to shape their destiny rather than react to it.

Looking toward 2030, the observability market would be unrecognizable from today. Quantum computing might require entirely new monitoring paradigms. Edge computing would distribute infrastructure to millions of locations. Autonomous systems would need to monitor themselves. And AI would be embedded in every application, requiring observability tools that could understand not just performance but intent.

Datadog's bet was that complexity would only increase. As Pomel had said from the beginning, they were building for the world that was coming, not the world that existed. In a future where every company ran thousands of microservices, deployed continuously, across multiple clouds, with AI models making real-time decisions, the need for comprehensive observability would be existential, not optional.

The journey from a two-person startup to a $45 billion public company had been remarkable. But in technology, past success guarantees nothing. The only constant is change, and the only sustainable advantage is the ability to adapt faster than your competitors. As Datadog entered its second decade as a public company, the question wasn't whether they had won—it was whether they could keep winning.

The story of Datadog is far from over. It's a story still being written in code commits, customer deployments, and quarterly earnings. It's a story about the democratization of monitoring, the complexity of modern infrastructure, and the ambition of two French engineers who believed they could build something essential. Whether that story ends with Datadog as the Bloomberg of DevOps, an indispensable platform worth hundreds of billions, or as another formerly great software company disrupted by the next wave of innovation, remains to be seen.

But one thing is certain: in a world where software is eating everything, and everything is becoming more complex, the need for observability isn't going away. Someone will capture that value. The bet on Datadog is that their combination of technical excellence, customer obsession, and relentless execution makes them the most likely to succeed. Time, as always, will tell.

[This analysis represents a point-in-time examination of Datadog as of August 2025. The technology industry evolves rapidly, and readers should conduct their own research and consider their own risk tolerance before making any investment decisions. The authors do not hold positions in Datadog stock and this analysis should not be construed as investment advice.]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube