Zoom: The Story of Building the World's Video-First Communication Platform

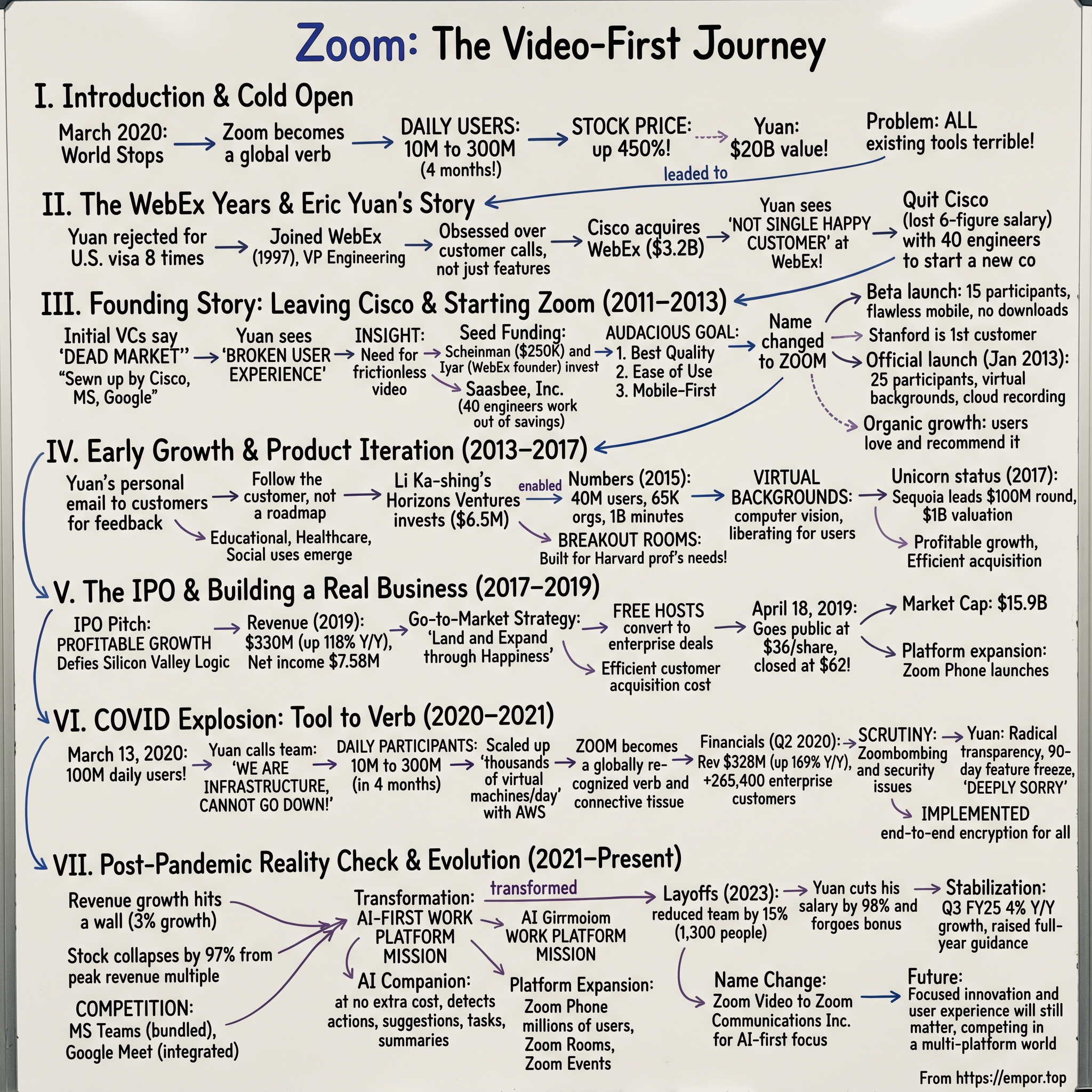

I. Introduction & Cold Open

March 2020. The world stops. Office towers empty. Schools shutter. And suddenly, a six-letter word becomes the most important verb in the global economy: Zoom.

In a matter of weeks, Zoom Video Communications transformed from a B2B software company known mainly to IT departments into the connective tissue of human civilization. Birthday parties, board meetings, weddings, funerals—if it involved human connection during the pandemic, it happened on Zoom. The company's daily meeting participants exploded from 10 million to 300 million in just four months. Its stock price rocketed up 450% in a single year. Eric Yuan, the soft-spoken founder who had been rejected for a U.S. visa eight times, was suddenly worth $20 billion.

But here's what makes this story remarkable: Zoom wasn't first. It wasn't even fifth. When Yuan founded the company in 2011, the videoconferencing market was considered dead money by Silicon Valley standards—dominated by established players like Cisco's WebEx (which Yuan himself had built), Microsoft's Skype, and Google's growing suite of communication tools. Investors literally laughed him out of the room. "Why would anyone need another video conferencing tool?" they asked.

The answer, as it turned out, was simple: because every existing tool was terrible.

This is the story of how a Chinese immigrant who couldn't speak English when he arrived in America built the defining product of remote work. It's a story about the power of obsessive customer focus, the importance of timing in technology, and what happens when a black swan event meets a perfectly positioned product. It's also a cautionary tale about hypergrowth, about going from hero to villain to somewhere in between, and about the challenge of building a second act when your first act was quite literally saving the world.

Today, Zoom trades at a fraction of its pandemic peak, facing intense competition from Microsoft Teams and Google Meet. The company that once commanded a revenue multiple of 109x now trades at just 3x. The question isn't whether Zoom was a pandemic phenomenon—it clearly was. The question is whether it can be something more.

II. The WebEx Years & Eric Yuan's Journey

The conference room at WebEx headquarters in Santa Clara was packed with engineers, but only one of them was crying. It was 1997, and Eric Yuan had just given his first product demo entirely in English—a language he'd been studying for less than three years. The demo went perfectly. The crying was from relief.

Yuan's journey to that conference room began in Shandong Province, China, where as a university student in 1987, he attended a speech by Bill Gates about the internet's promise. "I was mesmerized," Yuan would later recall. "I knew I had to be part of this revolution." But wanting to go to Silicon Valley and actually getting there were vastly different challenges. Between 1995 and 1997, Yuan applied for a U.S. visa eight times. Eight rejections. Each rejection meant months of waiting, thousands of dollars in fees, and explanations to family members who wondered why he kept trying.

The ninth attempt, in 1997, finally succeeded. Yuan arrived in Silicon Valley at age 27 with broken English but fluent C++. He joined WebEx as one of its first twenty engineers, hired by founder Subrah Iyar who saw something special in the determined young coder who had tried nine times to reach America.

But Yuan brought more than just coding skills to WebEx. He carried with him a deeply personal understanding of distance and connection. As a freshman at Shandong University of Science and Technology, Yuan regularly took ten-hour train rides to visit his girlfriend (now his wife) in another city. "I detested those rides," he remembered. "Ten hours each way, standing room only, terrible food. I would sit there imagining—what if I could just beam myself there? What if distance didn't matter?"

This wasn't just romantic daydreaming. Yuan understood viscerally what economists call the "distance penalty"—the human and economic cost of physical separation. And he believed technology could eliminate it.

At WebEx, Yuan quickly distinguished himself. While other engineers focused on features, Yuan obsessed over customer calls. He'd join support sessions, listen to complaints, watch usage patterns. By 2000, he was VP of Engineering. When Cisco acquired WebEx for $3.2 billion in 2007, Yuan had built one of the most successful enterprise software products of the decade. His compensation package at Cisco reached "very high six figures." He had, by any measure, made it in America.

Yet something gnawed at him. Despite WebEx's financial success, Yuan noticed a troubling pattern. "When I talked to customers about WebEx, I did not see a single happy customer," he observed. The product had grown bloated, complicated, expensive. Installation required IT support. Joining a meeting meant downloading plugins, entering access codes, waiting for the host. The very tool meant to save time was consuming it.

Yuan spent 2010 trying to convince Cisco's leadership to rebuild WebEx from scratch. "Make it mobile-first," he argued. "Make it so simple my parents can use it. Make it actually enjoyable." The response was always the same: "Eric, you are wrong. The future is our existing architecture. Video is about something else."

After a year of failed persuasion, Yuan made a decision that would seem insane to most people with a high-six-figure salary at Cisco: he quit. But he didn't quit alone. Forty WebEx engineers—many of whom Yuan had hired and mentored—decided to follow him. They didn't know what they were building yet. They only knew that Eric Yuan had never led them astray before.

"It wasn't logical," one of those engineers later reflected. "We were leaving Cisco to compete with Cisco. We were leaving stable jobs to build something in a market everyone said was dead. But Eric had this vision of what communication could be, should be. And honestly? We were all sick of using WebEx too."

III. The Founding Story: Leaving Cisco & Starting Zoom (2011–2013)

The rejection came quickly, professionally, and with a hint of condescension. "Eric, we love you, but video conferencing is a commodity business now," the Sand Hill Road venture capitalist explained, sliding Yuan's pitch deck back across the conference table. "Between Cisco, Microsoft, and Google, the market is sewn up. We're not interested."

It was June 2011, and Yuan had heard variations of this rejection from dozens of VCs. His company, temporarily named Saasbee, Inc. (a name so forgettable that even Yuan struggled to explain it), consisted of 40 engineers working out of a small office in Santa Clara, burning through their savings to build a videoconferencing product no investor wanted to fund.

The VC rejections stung, but they contained a kernel of truth: the market did appear saturated. Cisco WebEx dominated enterprise. Skype owned consumer. Google was giving away Hangouts for free. Microsoft had Lync. By conventional wisdom, starting a new videoconferencing company in 2011 was like starting a new search engine to compete with Google—technically possible but strategically foolish.

But Yuan had an insight these VCs missed. He didn't see videoconferencing as a market; he saw it as a broken user experience hiding inside successful businesses. "Every single one of these products was built for a different era," Yuan explained to anyone who would listen. "They were built when bandwidth was scarce, when computers were desktops, when IT departments controlled software. That world doesn't exist anymore."

Unable to convince traditional VCs, Yuan turned to his network. Dan Scheinman, Cisco's former Senior VP and General Counsel, had watched Yuan build WebEx from the inside. When Yuan approached him for funding, Scheinman didn't hesitate. "I wrote him a check for $250,000 on the spot," Scheinman recalled. "I'd seen Eric turn customer pain into product excellence for a decade. Betting against him would have been the mistake."

Subrah Iyar, WebEx's founder who had given Yuan his first American job, also invested. So did a collection of angel investors who had made fortunes in enterprise software and understood that markets dismissed as "saturated" were often ripe for disruption. By June 2011, Yuan had raised $3 million in seed funding—enough to keep his 40 engineers building for another year.

The technical challenge Yuan set for his team was audacious: build a videoconferencing system that worked perfectly on any device, with any bandwidth, without any downloads. "Three things," Yuan would repeat in every meeting. "Best video quality—that's number one. Extreme ease of use—no learning curve. And mobile-first—iPhone, iPad, Android, everything."

This meant throwing out the entire technical architecture that powered traditional videoconferencing. WebEx and its competitors used a hub-and-spoke model where all video streams went through central servers. This created latency, degraded quality, and made mobile participation nearly impossible. Yuan's team built a distributed mesh network that connected participants directly when possible, dynamically adjusting quality based on each participant's bandwidth.

The engineering effort was grueling. "We basically lived in the office for 18 months," remembered one early engineer. "Eric would be there at 6 AM and leave at midnight. Not micromanaging—just obsessing over every pixel, every millisecond of latency, every step in the user flow."

In May 2012, as the product neared beta, the company needed a new name. Saasbee was a non-starter for a consumer-friendly product. Yuan's children were reading Thacher Hurd's book "Zoom City" at the time, about a world where everything moves fast. The name clicked immediately: Zoom. It suggested speed, simplicity, forward movement. It was also, crucially, a verb—you could "Zoom" someone the way you could "Skype" them.

September 2012 marked the beta launch. The product supported up to 15 video participants, worked flawlessly on mobile devices, and required nothing more than clicking a link to join. No downloads. No plugins. No access codes. Just click and you're in.

Stanford University signed on as Zoom's first customer in November 2012, a crucial validation. If Stanford's tech-savvy community embraced Zoom, it would signal to the broader market that this wasn't just another videoconferencing tool.

The official launch came in January 2013, accompanied by a $6 million Series A round from Qualcomm Ventures, Yahoo founder Jerry Yang, and the same angels who had believed early. The funding valued the company at roughly $24 million—respectable but not spectacular. Version 1.0 supported 25 participants and included features that would become Zoom signatures: virtual backgrounds, screen sharing with annotation, and cloud recording.

The early metrics were promising but not explosive. First month: 400,000 users. By May 2013: 1 million users. These weren't WebEx numbers, but they represented something more important—organic growth. Zoom spent almost nothing on marketing. Users discovered the product, tried it, and actually liked it enough to recommend it. In the enterprise software world, where products spread through IT mandates and sales contracts, this was practically unheard of.

"We knew we had something when customers started sending us thank you notes," Yuan recalled. "Not support tickets—thank you notes. One customer wrote, 'I actually look forward to video meetings now.' When has anyone ever said that about enterprise software?"

IV. Early Growth & Product Iteration (2013–2017)

The email arrived at 11:47 PM on a Tuesday night in September 2013. "Eric, we need to talk about Breakout Rooms," the message from a Harvard Business School professor began. "My entire case study method depends on small group discussions. Without this feature, I can't use Zoom for my classes, and neither can thousands of other educators."

Yuan was still in the office, as usual. He immediately forwarded the email to his head of product with a note: "Priority #1. Whatever it takes."

This interaction captured the essence of Zoom's early growth strategy: obsessive responsiveness to customer needs, especially from use cases Yuan hadn't initially imagined. The company had built Zoom for business meetings, but users were pulling it in unexpected directions—education, healthcare, social gatherings. Rather than forcing users into a predetermined box, Yuan decided to follow them.

By June 2013, just six months after launch, Zoom had hosted 400,000 meetings across 2,500 cities. The geographic distribution was telling—this wasn't just Silicon Valley tech companies experimenting with a new tool. Insurance agents in Iowa were using it for client consultations. Doctors in India were conducting remote patient visits. Church groups in Alabama were holding Bible studies. The universality of the use cases suggested Zoom had tapped into something fundamental: the human need for face-to-face connection, regardless of distance.

The Series B funding round in September 2013, led by Li Ka-shing's Horizons Ventures, injected $6.5 million into the company. Li Ka-shing, Asia's richest person at the time, rarely invested in early-stage American software companies. His involvement sent a signal: Zoom wasn't just disrupting an American market, but solving a global problem.

The numbers by early 2015 validated this thesis: 40 million users, 65,000 organizations subscribed, 1 billion meeting minutes. For context, it had taken Skype nearly five years to reach 100 million users; Zoom was on pace to beat that significantly. The Series C round in February 2015 brought in $30 million from Emergence Capital, with additional participation from Qualcomm Ventures, Jerry Yang, and Dr. Patrick Soon-Shiong.

But growth revealed new challenges. As meeting sizes increased, the technical architecture needed constant refinement. The October 2015 release of version 2.5 pushed the participant limit to 50, then to 1,000 for business customers. This wasn't just a number change—it required fundamental rewrites of how Zoom handled video routing, bandwidth optimization, and screen layout.

The Breakout Rooms feature, launched in December 2015 after that late-night email from Harvard, exemplified Zoom's product philosophy. The feature allowed meeting hosts to split participants into smaller groups for discussions, then bring everyone back together—mimicking the physical world experience of stepping into side rooms during a conference. It was complex to build but simple to use, with drag-and-drop assignment and automatic timers.

"Most companies would have said, 'That's an education-specific feature, we'll put it on the roadmap for next year,'" observed an early product manager. "Eric's response was, 'If educators need it today, we build it today.' That urgency permeated everything."

Virtual backgrounds, introduced in July 2016, seemed almost frivolous compared to Breakout Rooms, but it revealed Yuan's understanding of a deeper truth: video calls were performative acts. People worried about their messy bedrooms, their barking dogs, their children wandering into frame. Virtual backgrounds weren't just fun—they were liberating. They gave users control over their professional presentation.

The technical achievement was remarkable. While competitors required green screens for background replacement, Zoom's implementation used advanced computer vision to work with any background. The feature consumed minimal CPU, maintaining video quality even on older devices. It was engineering excellence in service of a seemingly simple feature.

By January 2017, when Sequoia Capital led a $100 million Series D round at a $1 billion valuation, Zoom had achieved unicorn status. But more importantly, it had achieved something rarer: profitable growth. While most unicorns burned cash to acquire users, Zoom's efficient customer acquisition meant it was already cash-flow positive.

Carl Eschenbach, the Sequoia partner who led the investment, had seen hundreds of enterprise software companies as former president of VMware. His assessment was unequivocal: "Zoom has cracked the code for delivering effortless collaboration by providing the first product built from scratch with video in mind. This isn't iteration—it's innovation."

The numbers backed him up. Zoom's net promoter score—a measure of customer satisfaction—stood at 69, compared to the software industry average of 30. Customer retention exceeded 90%. The company was adding thousands of enterprise customers without a traditional enterprise sales force.

Yuan's approach to customer service during this period became legendary. He personally responded to customer complaints on social media. He gave out his personal email address at conferences. When a customer threatened to cancel their subscription, Yuan would often call them directly to understand why. "I'm not trying to save every customer," he explained. "I'm trying to understand every problem."

This obsessiveness extended to the company culture. Zoom's headquarters in San Jose featured a wall of customer testimonials—but also a "Wall of Shame" displaying the worst customer complaints each month. Engineers were required to spend time in customer support rotations. Product managers had to watch recordings of actual customer meetings to understand usage patterns.

The international expansion during this period happened almost accidentally. Zoom didn't have international offices or localized marketing. But the product's simplicity transcended language barriers. A Japanese company could schedule a Zoom meeting with Brazilian partners without either side needing instruction manuals. By 2017, over 20% of Zoom's revenue came from outside the United States, despite minimal international investment.

"We didn't expand internationally," Yuan reflected. "Our customers did it for us. They'd use Zoom with international partners, and those partners would become customers. It was the most efficient global expansion strategy possible: let the product sell itself."

V. The IPO & Building a Real Business (2017–2019)

The Morgan Stanley bankers sat in Zoom's conference room, their pitch decks untouched. Eric Yuan had just shown them something they'd never seen in decades of taking tech companies public: a profitable growth company that didn't need their money.

It was late 2018, and Zoom's S-1 filing would soon reveal numbers that defied Silicon Valley logic. Revenue had grown from $60 million in 2017 to $151 million in 2018, and was on track to hit $330 million in 2019. The company was projecting $540 million for the upcoming fiscal year. But here was the kicker: while revenue grew 118% year-over-year, Zoom had actually made money—$7.58 million in net income.

"You have to understand how unusual this was," explained a banker involved in the IPO process. "We were used to companies burning $100 million a quarter to grow half as fast. Zoom was printing cash while tripling revenue. It broke our models."

The efficiency came from Zoom's unique go-to-market strategy. While competitors like Microsoft and Cisco relied on expensive enterprise sales teams, Zoom had perfected what Yuan called "land and expand through happiness." The S-1 revealed a stunning statistic: 55% of Zoom's 344 customers contributing more than $100,000 annually had started with at least one free host before subscribing.

Think about that math. A free user tries Zoom for a team meeting. They like it. They get their team on it. The team likes it. IT gets inquiries about officially supporting it. Within months, a free user has transformed into a six-figure enterprise contract—without a single sales call.

The sales efficiency metrics were unprecedented. Zoom's sales and marketing spend as a percentage of revenue was just 33%, compared to 50-75% for typical SaaS companies. Customer acquisition cost payback period was under 12 months. The Rule of 40—a SaaS metric combining growth rate and profit margin—exceeded 100, nearly triple the benchmark for elite software companies.

On April 18, 2019, Zoom went public at $36 per share, valuing the company at $9.2 billion. Yuan had priced the IPO conservatively, wanting long-term investors rather than quick flips. The strategy backfired spectacularly—or succeeded beyond imagination, depending on your perspective.

The stock opened at $65, surged to a high of $66, and closed the first day at $62—a 72% gain. Zoom's market cap ended the day at $15.9 billion. Yuan, watching from the Nasdaq floor, seemed genuinely bewildered by the frenzy. "We just wanted to build a good product," he told reporters. "The rest is noise."

But the IPO revealed something deeper about Zoom's business model that public market investors immediately grasped: this was a rare combination of product-led growth, network effects, and gross margin expansion. The company's gross margins had improved from 79.8% to 81.2% as scale improved unit economics. Every additional customer made the service better and more profitable.

The customer concentration numbers told another story. No single customer represented more than 2% of revenue. The top 10 customers combined were less than 10%. This wasn't enterprise software dependent on a few large contracts; it was a distributed, resilient revenue base spanning from Fortune 500 companies to local flower shops.

The platform expansion strategy was already visible in the numbers. While video conferencing remained the core product, Zoom had quietly launched Zoom Phone in 2019, targeting the $50 billion unified communications market. Early adoption was promising—several thousand companies had already switched their entire phone systems to Zoom.

"The IPO wasn't about the money," Yuan emphasized in interviews. "We had money. It was about transparency, about showing the world our numbers, about being accountable to more than just ourselves." This transparency would soon prove both blessing and curse.

The international growth story embedded in the S-1 was remarkable. Without international offices, without localized sales teams, Zoom had achieved 20% international revenue mix. Companies in 180 countries were using the product. The viral coefficient—how many new users each existing user brought in—exceeded 2.5, meaning the product essentially marketed itself.

Wall Street analysts scrambled to find comparisons. The closest analog was perhaps Atlassian, another product-led growth story, but even Atlassian hadn't achieved profitability this early. Some compared it to Salesforce's early days, but Salesforce had required massive sales investment. Zoom had seemingly solved the enterprise software paradox: how to achieve enterprise scale with consumer simplicity.

The competitive moat, analysts realized, wasn't just technical. It was cultural. Zoom had made video conferencing feel different. Where WebEx felt corporate, Zoom felt human. Where Skype felt consumer-grade, Zoom felt professional. Where Google Hangouts felt like an afterthought, Zoom felt purposeful. The product had threaded an almost impossible needle.

Post-IPO, Zoom's stock continued climbing, reaching $100 by October 2019. The company was worth more than $25 billion, making Yuan one of America's richest immigrants. But Yuan seemed unchanged. He still answered customer emails personally. He still worked from 6 AM to midnight. He still insisted that every employee spend time in customer support.

The bear case from skeptics was straightforward: Microsoft and Google would eventually care enough to crush Zoom. The bull case was equally simple: Zoom had already won the user experience war, and in software, user experience compounds over time.

Nobody—not Yuan, not the analysts, not the competition—could have predicted what would happen next. In December 2019, a new virus was detected in Wuhan, China. Within months, it would transform Zoom from a successful software company into a critical piece of global infrastructure. The company that had prepared for everything would face the one thing nobody could prepare for: becoming essential overnight.

VI. The COVID Explosion: From Tool to Verb (2020–2021)

March 13, 2020, 3:47 AM Pacific Time. Eric Yuan's phone buzzed with an automated alert: Zoom's servers were approaching capacity. He checked the dashboard from his bedroom—daily meeting participants had just crossed 100 million, up from 10 million in December. His infrastructure team had modeled aggressive growth scenarios. None of them looked like this.

By 3:52 AM, Yuan was on a Zoom call with his engineering leads scattered across the world. The question wasn't whether they could handle the load—they had to. Schools were closing globally. Governments were issuing shelter-in-place orders. Entire economies were shifting online overnight. If Zoom failed now, it wouldn't just lose customers. It would fail humanity at its moment of greatest need.

"We are now infrastructure," Yuan told his team. "Like electricity. Like water. We cannot go down."

The numbers over the next four months defied comprehension. Daily meeting participants rocketed from 10 million in December 2019 to 200 million in March 2020, then to 300 million by April. For context, that's a 30x increase in four months—growth that should have taken a decade compressed into a season.

The infrastructure challenge was staggering. Zoom added more server capacity in the first two weeks of March than it had in all of 2019. Amazon Web Services, Zoom's primary cloud provider, later revealed that Zoom had scaled up "thousands of virtual machines per day" during peak pandemic growth—one of the fastest expansions in AWS history.

But the technical scaling, while impressive, wasn't the real story. The real story was cultural. Overnight, "Zoom" became a verb not just in English but in dozens of languages. Grandparents who had never used a computer were suddenly Zooming with grandchildren. Courts conducted trials over Zoom. Couples got married on Zoom. The British Parliament debated on Zoom. Saturday Night Live broadcast from cast members' homes via Zoom.

The second quarter 2020 earnings, announced in June, revealed the financial impact: revenue of $328 million, up 169% year-over-year. The company added 265,400 enterprise customers with more than 10 employees—a 354% increase. If you had invested $10,000 in Zoom stock on January 1, 2020, it was worth $55,000 by September—a 450% return during a global pandemic that crashed most stocks.

Yet with great scale came great scrutiny. The term "Zoombombing" entered the lexicon in March 2020, describing uninvited participants disrupting meetings with offensive content. The FBI issued warnings. School districts banned the platform. The New York Times ran a front-page story about Zoom's security flaws. The company that had been everyone's darling became, almost overnight, a privacy pariah.

Yuan's response defined the company's character. Rather than deflect or minimize, he owned every failure. On April 1, 2020, he published a blog post that began: "We recognize that we have fallen short of the community's—and our own—privacy and security expectations. For that, I am deeply sorry."

Zoom immediately announced a 90-day feature freeze, dedicating all engineering resources to security and privacy. They hired Alex Stamos, Facebook's former security chief. They acquired Keybase, an encryption company. They implemented end-to-end encryption for all users, not just paid ones—a decision that cost millions but restored trust.

"Most CEOs would have gone into bunker mode," observed a cybersecurity expert who worked with Zoom during the crisis. "Yuan went the opposite direction—radical transparency, immediate action, personal accountability. He turned a potential company-killer into a masterclass in crisis management."

The business model evolution during this period was fascinating. While consumer usage exploded, Zoom's revenue remained primarily enterprise-driven. Free users didn't directly generate revenue, but they created an unprecedented marketing funnel. Every happy free user was a potential enterprise buyer once offices reopened. The lifetime value calculations became almost absurd—acquire a user for free during the pandemic, convert them to a $100,000 enterprise contract post-pandemic.

The fiscal year ending January 31, 2021, showed pandemic impact in full force: revenue of $2.65 billion, up 326% from $623 million the previous year. The following year, even as pandemic restrictions eased, revenue grew another 55% to $4.10 billion. Zoom had gone from unicorn to decacorn to nearly hectocorn in 24 months.

The human stories from this period were profound. Italian hospitals used Zoom to let COVID patients say goodbye to families. Teachers conducted classes from their cars because their home internet couldn't handle the load. A wedding in India connected 500 guests across 20 countries. The platform designed for business meetings had become the connective tissue of human society.

Yuan himself became an unlikely celebrity. His net worth exceeded $20 billion by late 2020. TIME magazine named him Businessperson of the Year. But he seemed uncomfortable with the attention, repeatedly emphasizing that Zoom's success was "bittersweet"—born from global tragedy.

The engineering achievements during this period deserve their own chronicle. Zoom rebuilt its entire encryption infrastructure while usage was surging. They added capacity for 300 million concurrent users while maintaining 99.99% uptime. They shipped features like end-to-end encryption, improved waiting rooms, and enhanced authentication—all while supporting 30x growth.

"We were rebuilding the plane while flying it," recalled an engineering director. "While it was on fire. During a hurricane. With 300 million passengers aboard."

On November 9, 2020, Pfizer announced its COVID vaccine was 95% effective. Within hours, Zoom's stock price fell from $500 to $403—losing nearly $40 billion in market cap in a single day. The market's message was clear: Zoom's pandemic boom was temporary. The question now was whether the company could maintain relevance in a post-pandemic world.

Yuan, characteristically, was already thinking ahead. "The pandemic accelerated digital transformation by a decade," he said in a late 2020 interview. "We're not going back to 2019. The question isn't whether video communication remains important. It's how we evolve to serve the new hybrid world."

VII. Post-Pandemic Reality Check & Evolution (2021–Present)

The Zoom all-hands meeting in February 2023 had an ironic setting: Eric Yuan was delivering devastating news via the very platform his company had built. "We have made the tough but necessary decision to reduce our team by approximately 15%," he announced to employees worldwide. About 1,300 people would lose their jobs. The company that had defined remote work was now suffering from its normalization.

The numbers told a stark story. After growing 326% in fiscal 2021 and 55% in fiscal 2022, Zoom's revenue growth had hit a wall. Fiscal 2024 revenue of $4.53 billion represented just 3% growth—essentially flat when adjusted for inflation. The stock market's verdict was brutal: from a peak revenue multiple of 109x in 2020, Zoom now traded at just 3x revenue—a 97% collapse in valuation multiple.

But the competitive landscape had shifted even more dramatically than the numbers. Microsoft Teams, bundled free with Office 365, had grown to 280 million users. Google Meet, once an afterthought, was now deeply integrated into Google Workspace. Slack added video. Discord expanded beyond gaming. Facebook launched Messenger Rooms. Everyone wanted a piece of the video communication market that Zoom had validated.

"The bundling threat was existential," explained a former Zoom executive. "Imagine competing with Microsoft when they give away your core product free with software every enterprise already owns. It's like competing with Internet Explorer in the 1990s, except Microsoft learned from their antitrust mistakes. "Yuan's response was to transform Zoom from a videoconferencing company into what he called an "AI-first work platform." The company positioned AI as central to its strategy, with Yuan declaring Zoom's mission to be "delivering an AI-first platform for human connection." The centerpiece of this transformation was AI Companion, an AI personal assistant available at no additional cost with paid services.

The AI Companion rollout represented a fundamental rethinking of Zoom's value proposition. The assistant could automatically detect action items across meetings, chats, emails, and docs, provide suggestions for next steps, and execute tasks on users' behalf. Features included generating next steps from meeting summaries, summarizing unread messages in chat channels, and recapping email threads without reading every message.

"We're not competing on video quality anymore—everyone has good enough video now," explained a Zoom product manager. "We're competing on intelligence, on making meetings actually productive rather than just possible."

The platform expansion strategy accelerated. Zoom Phone, launched in 2019, had grown to millions of users by 2024. Zoom Rooms transformed conference rooms into smart collaboration spaces. Zoom Events targeted the virtual events market that had exploded during the pandemic. The goal was to make Zoom indispensable beyond just video calls—to own the entire communication stack.

But the market remained skeptical. Despite the AI innovations and platform expansion, revenue growth stayed anemic. The stock price, which had peaked at $588 in October 2020, traded below $70 by mid-2024—a destruction of over $150 billion in market value.

The cultural challenge was equally profound. Zoom had become synonymous with pandemic fatigue. "Zoom fatigue" was now a recognized psychological phenomenon. Companies proudly announced "No-Zoom Fridays." The very success that had made Zoom indispensable had also made it exhausting.

Yuan's vision for the future remained ambitious. "There are over 1 billion knowledge workers worldwide," he stated in a 2024 interview. "Our goal is to connect all those 1 billion knowledge workers with the Zoom platform." But achieving that goal meant competing not just with Microsoft and Google, but with the human desire to return to in-person interaction.

The February 2023 layoffs marked a painful acknowledgment of reality. After growing from 2,000 to 8,000 employees during the pandemic, Zoom had to right-size for a world where growth came in single digits, not triple digits. Yuan took responsibility, cutting his own salary by 98% and forgoing his bonus. The latest results tell a story of stabilization rather than recovery. Q3 fiscal 2025 showed revenue of $1.18 billion versus $1.16 billion expected, growing about 4% year over year. Net income reached $207.1 million, up from $141.2 million in the same quarter a year earlier. The company even raised its full-year guidance slightly. But 4% growth for a company that once grew 326% annually feels like treading water.

Perhaps most symbolically, the company announced it was changing its corporate name from Zoom Video Communications to Zoom Communications Inc., with Yuan explaining "This change reflects our evolution into an AI-first work platform for human connection and our vision for long-term growth". The name change represented both acknowledgment and aspiration—acknowledgment that video alone wasn't enough, aspiration that AI could provide a second act.

The transformation continues. The company announced AI Companion 2.0, the next generation of its AI personal assistant available at no additional cost, along with a custom add-on for organizations needing more personalized experiences. Features now include everything from automatic task detection to meeting agenda creation to real-time summaries during phone calls.

Yet the fundamental challenge remains: in a world where Microsoft bundles Teams with Office and Google gives Meet away free, how does an independent communication platform survive, let alone thrive? Yuan's bet is that focused innovation and superior user experience will continue to matter. History suggests he might be right—after all, Zoom shouldn't have succeeded the first time either.

VIII. Business Model & Competitive Advantages

The conference room at Sequoia Capital was silent as Eric Yuan finished explaining Zoom's unit economics to the partners. It was 2016, and Yuan had just revealed something that seemed impossible: Zoom acquired enterprise customers for less than $5,000 in sales and marketing spend, and those customers generated over $100,000 in lifetime value. The payback period was under 12 months. In enterprise software, this was like claiming you'd invented perpetual motion.

"Show us the math again," requested a partner, suspicious of the numbers. Yuan pulled up the spreadsheet. The secret wasn't complicated—it was just unprecedented. Zoom had cracked product-led growth in enterprise software, a category that had always required expensive sales teams and lengthy implementation cycles.

The mechanics were elegant. A free user hosts a meeting. Participants join without downloading software. The meeting works flawlessly. Participants become free users themselves. Some upgrade to paid plans. IT departments notice employees expensing Zoom subscriptions. Rather than fight it, they negotiate enterprise deals. The virus spreads from individual to team to department to company, all without a single cold call.

"Traditional enterprise software is sold top-down," Yuan explained to investors. "We grow bottom-up. By the time procurement gets involved, half the company is already using Zoom. We're not selling them software—we're just formalizing what's already happening."

The network effects compounded exponentially. Every Zoom meeting created between 5 and 100 potential new users. Each of those users averaged 2.5 additional users within their first month. The viral coefficient—the rate at which users brought in new users—exceeded anything seen in enterprise software. Consumer apps like Facebook had similar dynamics, but they monetized through ads at pennies per user. Zoom monetized at hundreds of dollars per user with 80% gross margins.

The engineering excellence underlying this growth was often overlooked but fundamental. Building reliable video conferencing is genuinely, technically hard. Audio and video must synchronize perfectly across multiple participants with varying bandwidth, devices, and network conditions. A 100-millisecond delay makes conversation feel unnatural. A 500-millisecond delay makes it unusable. Zoom consistently delivered sub-50-millisecond latency, even on congested networks.

The technical architecture was revolutionary. Traditional systems used centralized servers that became bottlenecks. Zoom built a distributed mesh network that connected participants peer-to-peer when possible, falling back to relay servers only when necessary. The system dynamically adjusted quality based on each participant's bandwidth—one person's poor connection didn't degrade everyone else's experience.

"We spent two years just on audio," recalled an early engineer. "Eric would make us test calls from coffee shops, airports, moving cars. If the audio wasn't perfect, we'd start over. He'd say, 'Nobody forgives bad audio. Nobody.'"

This obsession with quality created a powerful moat. Competitors could copy Zoom's features, but replicating the underlying infrastructure required years of engineering and billions of meeting minutes of real-world optimization. By the time competitors caught up to Zoom's 2013 quality, Zoom had moved far ahead.

The customer obsession culture amplified these advantages. Yuan's practice of personally calling unhappy customers wasn't just PR—it was intelligence gathering. Every complaint became a product improvement. Every churned customer became a learning opportunity. This created a feedback loop that accelerated product development beyond what traditional market research could achieve.

"Most companies do quarterly customer surveys," explained a former product manager. "We had real-time customer sentiment from thousands of daily conversations. We knew about problems before they became patterns."

The capital efficiency this enabled was extraordinary. While competitors burned hundreds of millions on sales and marketing, Zoom achieved similar growth spending a fraction of that amount. The company reached $1 billion in revenue while raising only $161 million in total funding. For comparison, Slack raised over $1 billion to reach similar revenue levels.

The freemium model was calibrated perfectly. Free meetings were limited to 40 minutes—long enough to be useful, short enough to encourage upgrades for serious use. The limitation felt natural rather than punitive. Users understood they were getting tremendous value for free and happily paid when they needed more.

But the real genius was making the product simultaneously consumer-simple and enterprise-capable. The same platform that grandmothers used for family calls also supported 10,000-person webinars with enterprise-grade security. This dual nature meant Zoom could enter organizations through any door—a sales team, an engineering squad, an HR department—and expand everywhere.

The platform strategy that emerged post-IPO built on these foundations. Zoom Phone wasn't just another product—it was a natural extension users requested. Zoom Rooms solved the conference room problem every Zoom user experienced. Each addition made the core product stickier while maintaining the simplicity that drove adoption.

"The mistake everyone makes is thinking Zoom succeeded because of the pandemic," observed a venture capitalist who passed on investing. "Zoom succeeded because it solved a universal problem with a product so good that users became evangelists. The pandemic just revealed what was already true."

The competitive advantages compound over time. Network effects grow stronger as more users join. The data advantage from billions of meeting minutes enables AI features competitors can't match. The brand has become verbified—people "Zoom" regardless of which platform they use. The engineering talent attracted by success enables faster innovation.

Yet vulnerabilities remain. Platform dependence on AWS creates risk. The freemium model that drove growth also limits monetization. Competition from bundled alternatives pressures pricing. The question isn't whether Zoom's advantages are real—they demonstrably are. The question is whether they're sufficient against competitors with infinite resources and distribution advantages.

IX. Playbook: Lessons for Founders & Investors

The Zoom board meeting in January 2020 was supposed to be routine—review Q4 results, approve budgets, discuss the upcoming IPO anniversary. Then Yuan's phone buzzed with a text from the engineering team: daily active users had just jumped 20% in 24 hours. The coronavirus was spreading in Asia, and businesses were sending employees home. "This is either our biggest opportunity or our biggest crisis," Yuan told the board. "Maybe both."

What happened next became a masterclass in navigating a black swan event, but the lessons from Zoom's journey extend far beyond pandemic management. They form a playbook for building transformational companies in competitive markets.

Lesson 1: Timing Isn't Everything, But It's Close

Yuan didn't time the market deliberately—he couldn't have predicted a pandemic. But he positioned Zoom at the intersection of three inevitable trends: cloud computing, mobile proliferation, and distributed work. When the forcing function arrived, Zoom was ready.

"The smartphone created a huge economy, the cloud created a huge economy," Yuan reflected. "If you start a company, timing is very important. But you can't time precisely—you can only position yourself where multiple trends converge."

The lesson for founders: Don't try to time the market perfectly. Instead, identify multiple secular trends and build at their intersection. If any single trend accelerates, you win. If multiple trends accelerate simultaneously, you win big.

Lesson 2: Product Quality Is the Ultimate Differentiator

In a world of growth hacks and viral loops, Zoom's success came from something unfashionable: making a product so good that marketing became optional. Every competitor had more resources, better distribution, bigger brands. Zoom had better video quality, easier usage, greater reliability.

"We could have grown faster with aggressive marketing," Yuan admitted. "But growing slower with a better product created a stronger foundation. When the moment came, we were ready to scale."

The engineering time invested in seemingly minor details—reducing latency by 10 milliseconds, improving audio compression by 5%—compounded into insurmountable advantages. Competitors could match features but couldn't match the accumulated optimization of billions of meeting minutes.

Lesson 3: The Power and Peril of Hypergrowth

Growing 30x in four months broke every assumption about scaling. Zoom had to add more servers in two weeks than in its entire history. Customer support went from handling thousands of tickets to millions. The company hired, onboarded, and trained hundreds of employees without ever meeting them in person.

The conventional wisdom says hypergrowth kills companies through cultural dilution, operational chaos, and quality degradation. Zoom survived because its culture and systems were built for a distributed world before that world existed. The company didn't have to adapt to remote work—it was born there.

But hypergrowth also created problems that persist today. Market expectations reset to pandemic levels. The talent hired during expansion didn't all fit post-pandemic reality. The stock compensation that seemed reasonable at $500 per share became problematic at $70.

Lesson 4: Building for Enterprise While Keeping Consumer Simplicity

The fundamental tension in enterprise software is between power and simplicity. Enterprise buyers want features, controls, integrations. Users want something that just works. Most companies choose one path. Zoom somehow traveled both simultaneously.

The key was radical prioritization. Every feature had to pass the "parents test"—could Yuan's parents use it without instruction? If not, it was either simplified or hidden in advanced settings. This discipline forced elegant solutions to complex problems.

"Enterprise features are table stakes," explained a product manager. "User experience is the differentiator. We won by making the complex appear simple."

Lesson 5: Managing Through a Black Swan Event

When "Zoombombing" threatened to destroy the company's reputation in April 2020, Yuan made a crucial decision: radical transparency. Instead of minimizing the problem, he owned it completely. The 90-day feature freeze to focus on security seemed insane during hypergrowth, but it saved the company.

The lesson transcends crisis management. When trust is your primary asset, protecting it supersedes everything else—growth, features, even revenue. Yuan understood that Zoom's permission to exist in people's lives depended on trust. Violate that trust, and no amount of features or marketing could recover it.

Lesson 6: When to Pivot vs. When to Persevere

Post-pandemic, Zoom faced an existential choice: accept being a video conferencing company in a shrinking market, or transform into something broader. The pivot to "AI-first work platform" wasn't just rebranding—it was a fundamental strategic shift requiring new capabilities, talent, and billions in investment.

The decision framework was clear: Is the core problem you're solving still valid? For Zoom, the answer was yes—human connection across distance remained essential. The solution needed evolution, not revolution. This clarity enabled focused transformation rather than desperate thrashing.

Lesson 7: Capital Allocation in Feast and Famine

Zoom's capital efficiency pre-pandemic—reaching $1 billion revenue on $161 million raised—became a liability post-pandemic. The company had too much cash, too high a stock price, too many acquisition options. The discipline that enabled efficient growth had to evolve into discipline preventing wasteful expansion.

The layoffs in 2023, while painful, demonstrated mature capital allocation. Rather than using pandemic windfalls to fund speculation, Zoom returned to its efficient roots. Yuan's 98% salary cut wasn't just symbolic—it signaled that pandemic economics were over and discipline had returned.

The meta-lesson is that capital efficiency isn't about being cheap—it's about resource allocation aligned with value creation. During hypergrowth, aggressive investment made sense. Post-pandemic, efficiency returned to focus. The key is matching capital deployment to market conditions, not following rigid rules.

X. Bear vs. Bull Case & Future Analysis

The PowerPoint slide on the Morgan Stanley trading floor showed two lines diverging like a wishbone. One projected Zoom reaching $10 billion in revenue by 2027. The other showed it shrinking to $3 billion. Both scenarios, the analyst argued, were entirely plausible. "I've never seen such divergent outcomes for a profitable, cash-flow positive company," she told clients. "Zoom is either massively undervalued or structurally impaired."

The Bear Case: Death by a Thousand Bundles

The bear thesis is straightforward and compelling: Zoom is a feature, not a company. Microsoft Teams comes free with Office 365, which 345 million people already use. Google Meet is bundled with Google Workspace. For IT departments managing costs, paying separately for Zoom makes increasingly little sense.

The numbers support the pessimists. Revenue growth has decelerated from 326% to 4%. The net dollar retention rate—a key SaaS metric—has declined from 130% to barely above 100%. Enterprise customer additions have slowed to a trickle. The stock trades at $70, down from $588 at its peak, destroying over $150 billion in market value.

"Zoom is the Netscape of video conferencing," argued a prominent short seller. "A pioneer that defined the category but lacks the structural advantages to survive against platform players. Microsoft doesn't need to make money on Teams—it's a loss leader for Office. Zoom needs every dollar."

The commoditization of video conferencing accelerates daily. What was once Zoom's differentiator—superior quality—has become table stakes. Microsoft Teams now matches Zoom's video quality. Google Meet works seamlessly across devices. The technical moat has evaporated.

Worse, the brand association with pandemic fatigue may be permanent. "Zoom fatigue" has entered the lexicon as a negative concept. Companies celebrating return-to-office explicitly position themselves as reducing Zoom usage. The product that saved work during the pandemic has become symbolic of what many want to leave behind.

The AI transformation, bears argue, is too little too late. Microsoft's Copilot integration across Office creates an AI advantage Zoom can't match. Google's Gemini provides similar capabilities. Zoom's AI Companion, while impressive, lacks the data and integration breadth of platform competitors.

International expansion faces headwinds. Chinese regulations make competing there impossible. European privacy requirements favor local alternatives. In emerging markets, WhatsApp and regional super-apps dominate. The global opportunity that seemed limitless in 2020 has narrowed considerably.

The Bull Case: The Focused Innovator's Advantage

The bull thesis rests on a different premise: in a world of bloated, complex platforms, focus wins. Zoom does one thing—human connection through video—better than anyone. While competitors add features, Zoom perfects the core experience that actually matters.

"Microsoft Teams is a Swiss Army knife—lots of tools, none excellent," observed a bull analyst. "Zoom is a scalpel—one tool, perfectly designed. For mission-critical communication, which do you choose?"

The numbers tell a more nuanced story than bears acknowledge. Yes, growth has slowed, but Zoom still generates $4.6 billion in revenue with 38% operating margins. The company has $7 billion in cash, no debt, and generates over $1.5 billion in free cash flow annually. This isn't a struggling company—it's a profitable one navigating a transition.

The AI opportunity, bulls argue, is underestimated. Zoom's mission is "delivering an AI-first platform for human connection," allowing "individuals and teams to focus on what they do best: engaging, connecting, and delivering creative and insightful work". Unlike competitors who bolt AI onto existing products, Zoom rebuilds around AI from the ground up.

Consider the market size. There are over 1 billion knowledge workers globally. Even capturing 10% at $100 annually—far below current enterprise prices—represents a $10 billion revenue opportunity. The enterprise communication market exceeds $50 billion and growing. Zoom's current 10% share could double with proper execution.

Hybrid work, bulls contend, is permanent. McKinsey research shows 58% of Americans work remotely at least one day weekly. That percentage approaches 80% for knowledge workers. The full return to office isn't happening. Companies need video communication infrastructure whether they admit it or not.

The platform expansion shows promise. Zoom Phone has grown to millions of users despite launching years after competitors. Zoom Events captures virtual event spending that didn't exist pre-pandemic. Zoom Rooms modernizes the conference room experience. Each addition increases account value and switching costs.

Customer loyalty remains strong despite competition. Enterprise customers grew to 192,400 in the latest quarter. Large customers spending over $100,000 annually increased 13.5% year-over-year. If Zoom were really being displaced by Teams, these numbers would be declining, not growing.

The Realistic Path Forward

The truth likely lies between extremes. Zoom isn't disappearing, but it's also unlikely to recapture pandemic valuations. The realistic scenario is evolution into a profitable, niche player serving customers who value best-in-class video communication over bundled convenience.

The strategic options are clear:

M&A Opportunities: With $7 billion in cash, Zoom could acquire complementary companies in adjacent spaces—workflow automation, customer service, industry-specific solutions. The risk is integration complexity and cultural dilution.

Geographic Expansion: International revenue remains under 20%. Focused expansion in markets where U.S. tech giants face regulatory challenges could drive growth. India, Southeast Asia, and Latin America offer significant opportunities.

Vertical Solutions: Building industry-specific versions—Zoom for Healthcare, Zoom for Education, Zoom for Financial Services—could command premium pricing and reduce commoditization risk.

AI Platform Play: Becoming the communication layer for AI agents and automation could position Zoom at the center of the autonomous work revolution. Imagine AI agents conducting meetings, with humans dropping in as needed.

The investment case depends on time horizon and risk tolerance. For value investors, Zoom trading at 15x earnings with $7 billion in cash looks compelling. For growth investors seeking the next doubling, better opportunities exist elsewhere. For long-term holders, the question is whether Yuan can execute a second act as successfully as the first.

XI. Epilogue: Defining the Future of Work

The museum exhibit opens in 2035. "Communication in the Digital Age," reads the placard at the entrance. Schoolchildren on a field trip wander through, wearing whatever neural interface or AR glasses have replaced smartphones by then. They stop at a display showing a reconstructed 2020-era home office: external webcam precariously balanced on a monitor, ring light, acoustic panels, the archaeological remains of remote work's awkward adolescence.

"People used to sit in front of cameras for eight hours a day," the guide explains. The children laugh. The idea seems as archaic as using a rotary phone.

But one child asks a prescient question: "Why did they do it that way?"

The answer, of course, is that Zoom and its competitors were solving for the wrong problem. They optimized for recreating in-person meetings digitally, when they should have been reimagining communication entirely. The future of work won't be better video calls—it will be the elimination of video calls as we know them.

Eric Yuan understands this, even if the market doesn't yet. In recent interviews, he's described a future where AI avatars attend meetings on our behalf, where language barriers disappear through real-time translation, where "presence" becomes untethered from physical or even visual representation. "The ultimate goal," he said, "is not to make meetings better. It's to make meetings unnecessary."

This vision explains Zoom's aggressive AI investments despite investor skepticism. The company that defined synchronous communication is betting its future on asynchronous intelligence. Your AI assistant attends the morning standup while you sleep. It negotiates contracts while you exercise. It synthesizes discussions across time zones and languages, presenting you with decisions rather than deliberations.

The cultural impact of Zoom transcends business metrics. A generation of children attended "Zoom school." Couples married over Zoom. Families said goodbye to dying relatives through Zoom. The platform became humanity's window during isolation, its lifeline during separation. No software company had ever been so intimately woven into the human experience.

Yet this intimacy created impossible expectations. Zoom was supposed to replace human connection, but it could only approximate it. The uncanny valley of digital interaction—the slight delay, the missing peripheral cues, the exhaustion of performed presence—reminded us that mediated communication, however sophisticated, remains mediation.

If Yuan and his team were running Zoom today, what would they do? The answer might surprise Wall Street: they'd probably destroy the core product.

Not literally, but conceptually. They'd recognize that competing with Microsoft and Google on their terms is a losing game. Instead, they'd use their $7 billion war chest to build what comes after video conferencing. Acquire the best AI companies. Hire researchers working on presence and embodiment. Partner with AR/VR platforms building spatial computing.

The Zoom of 2030 might not involve video at all. It might be an AI orchestration layer that manages human and artificial agents collaborating across modalities. Your "Zoom meeting" could be you talking to your smart glasses while walking, while your colleague participates through text, while an AI synthesizes both inputs for a third participant who reviews it later.

The surprising learning from Zoom's journey isn't about video conferencing or pandemic luck or even product excellence. It's about the power of solving universal human needs with radical simplicity. Every human since language evolved has wanted to communicate across distance. Zoom made it effortless. Whatever comes next must be even more effortless—perhaps invisible.

The key takeaway for entrepreneurs is that transformational companies don't just build better products—they collapse complexity. WebEx required IT support, access codes, downloads. Zoom required clicking a link. The next transformation will require nothing at all—communication will happen as naturally as thought.

For investors, Zoom represents a fascinating test case in platform transitions. Can a company that defined one paradigm successfully navigate to the next? History suggests it's nearly impossible—IBM didn't become Microsoft, Microsoft didn't become Google, Google didn't become Facebook. But Yuan has beaten conventional wisdom before.

The lasting legacy of Zoom might not be the product but the precedent: a company that made the impossible seem obvious. Before Zoom, nobody believed video conferencing could be consumer-simple. Before Zoom, nobody believed enterprise software could grow virally. Before Zoom, nobody believed a startup could compete with Microsoft, Google, and Cisco simultaneously.

Now we know better. The question isn't whether someone will build the next Zoom—something that makes current communication seem as archaic as smoke signals. The question is whether that someone will be Zoom itself.

As Yuan often says, borrowing from Wayne Gretzky: "Skate to where the puck is going, not where it has been." The puck is heading toward a world where physical and digital presence merge, where AI mediates most interaction, where communication happens continuously rather than in scheduled blocks.

Zoom's story isn't over. It's entering its second act, and second acts in technology are notoriously difficult. But if any company can transform from pandemic phenomenon to permanent infrastructure, it might be the one that transformed from nobody to necessity in less than a decade.

The exhibit in that 2035 museum will need updating. The question is whether Zoom will be displayed as a historical artifact—the way we show telegraphs and fax machines—or as the foundation for whatever comes next. Yuan is betting everything on the latter.

XII. Recent News

The drumbeat of news around Zoom in late 2024 tells a story of transformation amid stability. The Q3 fiscal 2025 earnings announced in November showed the company beating expectations with $1.38 adjusted earnings per share versus $1.31 expected, and revenue of $1.18 billion versus $1.16 billion expected. The 4% growth rate, while modest, has become predictable—a marked change from the volatility of the pandemic years.

Zoom raised its full-year fiscal 2025 guidance to $5.41-$5.43 in adjusted earnings per share with $4.656-$4.661 billion in revenue, with the middle of the range implying about 3% growth. Wall Street's reaction was muted—the stock fell 4% in after-hours trading despite the beat. The market seems to have settled into a steady-state view of Zoom: profitable but ex-growth, stable but unexciting.

The AI Companion updates announced at Zoomtopia 2024 represent the company's most aggressive push into artificial intelligence. AI Companion 2.0, available later in October 2024 at no additional cost for paid plans, works across Zoom Workplace and the web, connecting with Microsoft Outlook and Office, Gmail, Google Calendar, and Google Docs. The integration with competitors' products is notable—an acknowledgment that Zoom must play nicely in a multi-platform world.

The company reported 192,400 enterprise customers in Q3, up just 800 from the previous quarter. This deceleration in customer additions suggests that Zoom is focusing more on expanding within existing accounts rather than acquiring new logos—a mature company strategy rather than a growth company approach.

The competitive dynamics continue intensifying. Microsoft Teams pushes aggressive bundling with Office 365. Google Meet leverages Google Workspace integration. Newer entrants like Riverside.fm and Descript target content creators with advanced recording and editing features. The moat that seemed impregnable in 2020 faces erosion from multiple directions.

Yet Yuan remains optimistic, noting at Zoomtopia: "We announced major milestones such as AI Companion 2.0 and paid add-ons for AI Companion and industry-specific AI customization, further cementing our vision to deliver a differentiated AI-first work platform". The emphasis on customization and industry-specific solutions suggests a strategy of going deeper rather than broader.

Return-to-office trends present both challenge and opportunity. While some companies mandate full in-person work, hybrid arrangements dominate. Morgan Stanley research shows 58% of knowledge workers expect to work remotely at least one day per week permanently. This "permanent hybrid" state might be Zoom's sustainable market—not the pandemic explosion, but not a full return to 2019 either.

Stock performance reflects this ambiguity. Trading around $90 in late 2024, Zoom has recovered from its $60 lows but remains far below pandemic peaks. The company trades at approximately 15x forward earnings—reasonable for a profitable company but uninspiring for a former growth darling. Analyst sentiment has converged on "hold"—nobody expects collapse, but few see catalysts for significant appreciation.

The transformation from "Zoom Video Communications" to "Zoom Communications" symbolizes the strategic pivot. Video was the entry point, but the ambition extends to all workplace communication. Whether the market believes this transformation remains uncertain.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube