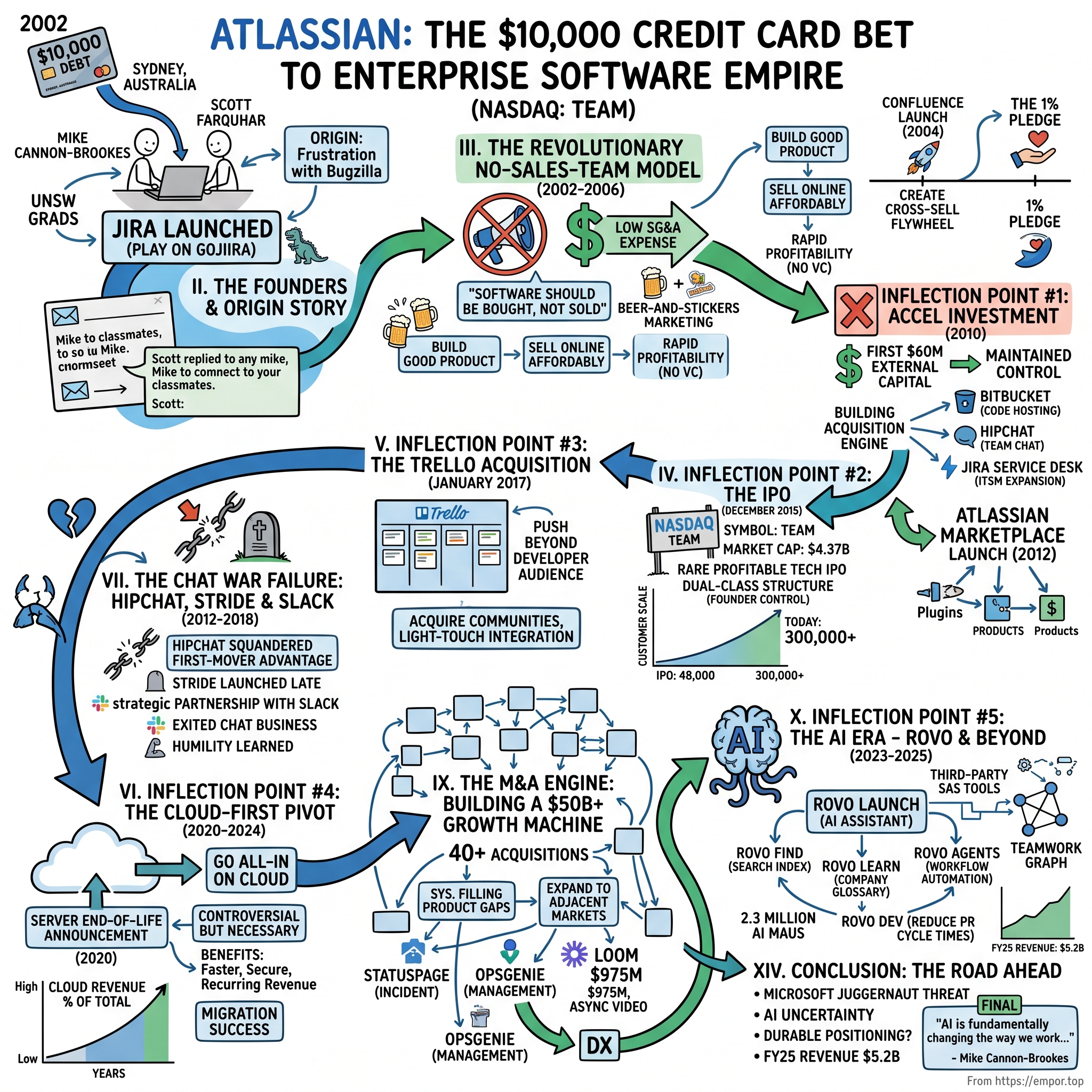

Atlassian: The $10,000 Credit Card Bet That Built An Enterprise Software Empire

I. Introduction & Episode Roadmap

In the annals of enterprise software history, few origin stories are as improbable—or as instructive—as Atlassian's. Here is a company that defied virtually every convention of the technology industry: bootstrapped in Australia when the continent had no meaningful tech ecosystem, built without venture capital when VC funding was considered essential, scaled without a traditional sales team when enterprise software demanded armies of quota-carrying reps, and made its founders billionaires while operating what The New York Times once called "a very boring software company."

Today, Atlassian generates $5.2 billion in revenue for fiscal year 2025, up 20% from $4.4 billion in fiscal year 2024. The company serves over 300,000 customers and employs nearly 14,000 people. It has reached 2.3 million AI monthly active users and generated over $1.4 billion in free cash flow for fiscal year 2025.

But the journey from two university students maxing out a credit card in 2002 to this point contains multitudes: revolutionary distribution strategies, painful strategic failures, audacious acquisitions, and one of the most consequential platform transitions in enterprise software history.

The central question that animated Atlassian's ascent remains relevant for every technology investor and entrepreneur: How did two Australians with no Silicon Valley connections, no venture backing, and no sales team build a global enterprise software giant that now challenges Microsoft, GitHub, and ServiceNow for dominance in developer tools and team collaboration?

The December 2015 IPO on NASDAQ put Atlassian's market capitalization at $4.37 billion and made founders Scott Farquhar and Mike Cannon-Brookes Australia's first tech startup billionaires. As of late November 2025, Atlassian's market cap stands at approximately $38 billion—representing roughly a 9x increase from its IPO valuation, though down significantly from its all-time high of over $100 billion during the 2021 tech bubble.

This story traverses bootstrapping discipline versus venture capital velocity, product-led growth before the term existed, strategic M&A that added billions in value, a chat product failure that taught humility, and a cloud transition that bet the entire company's future. Let's begin.

II. The Founders & Origin Story (2001-2002)

The Australian Tech Desert

Picture Sydney, Australia in 2002. The dot-com bubble had just finished its spectacular implosion. In Silicon Valley, shell-shocked entrepreneurs were retreating from the wreckage of Pets.com and Webvan, but at least they had a community of fellow travelers, angel investors willing to take flyers on the next thing, and a culture that normalized failure as a stepping stone.

In the aftermath of the dotcom crash in 2002, being an entrepreneur in Silicon Valley was tough, but being one in Sydney was tougher. The lack of a large tech community and local VCs was a huge stumbling block for tech startups in Australia.

Mike Cannon-Brookes would later describe it simply: there was no "IPO preschool" in Australia. No Y Combinator, no Sand Hill Road, no ecosystem of founders-turned-angels ready to write checks. If you wanted to build a technology company in Sydney, you were essentially starting from zero, with no playbook and no safety net.

The Email That Changed Everything

In 2001, Mike Cannon-Brookes sent an email to his University of New South Wales classmates asking if any of them were interested in helping him launch a tech startup after graduation. Scott Farquhar was the only one who responded, and together they founded Atlassian in 2002.

Consider the counterfactual: if one more classmate had responded, Atlassian might have become something entirely different. If no one had responded, it might not have existed at all. The company's entire trajectory hinged on this single reply.

Michael Cannon-Brookes was born on November 17, 1979, in Connecticut. The son of a global banking executive, he relocated to Taiwan when he was six months old, and to Hong Kong when he was three; he later attended boarding school in England. He attended Cranbrook School in Sydney and graduated from the University of New South Wales with a bachelor's degree in information systems.

Farquhar was born in December 1979 in Parramatta, Sydney. He attended Castle Hill Primary School and James Ruse Agricultural High School and graduated from the University of New South Wales with a Bachelor of Science in Business Information Technology. Farquhar developed an early interest in computers; his dad purchased an old computer for him to play games on, but it couldn't run Microsoft DOS, so Farquhar spent a year learning to make it work.

Farquhar often carries the epithet of "accidental billionaire" after he and his business partner Mike Cannon-Brookes founded Atlassian with the aim to replicate the $48,500 graduate starting salary typical at corporations without having to work for someone else.

After Farquhar rejected a job at PwC, they had only two simple goals: to not wear suits to work and earn more than the $50K salary that PwC had offered, by starting their own company.

The $10,000 Credit Card and Naming Atlas

They bootstrapped the company for several years, financing the startup with a $10,000 credit card debt. A lot has changed for Atlassian since founders Mike Cannon-Brookes and Scott Farquhar decided to max out the $10,000 limit on their credit card to launch what would become the world's leading agile project management software.

The name itself tells a story. The name was derived from the Greek mythological figure Atlas, inspired by his bronze statue in New York's Rockefeller Center. When they searched for a website domain, they discovered Atlas.com was already taken. So they transformed a noun into an adjective—Atlassian—creating a name that would become synonymous with developer tools.

From Customer Support to Building Jira

The company didn't start with grand ambitions to build a global software platform. Instead, it began with something far more mundane.

Together they launched Atlassian, a two-man tech support service that they managed from their bedrooms at all hours of the night. Unable to make money, Scott and Mike decided to pivot and sell some of the software they'd developed for themselves.

Initially, Cannon-Brookes and Farquhar were engaged in supporting other customer service teams, which required them to be available for calls at all hours. They were also unhappy with the bug-tracking software they were using at the time. To solve these issues, they developed Atlassian's flagship product, Jira, a project and issue tracking tool, and shifted their focus to selling this software.

Bugzilla, the software they used to track their work, couldn't meet their needs. Finally, they bootstrapped their own issue tracking and project management software, naming it Jira, a play on Gojira, the Japanese title of the 1954 film Godzilla. They soon realized they were better off selling Jira to the masses than providing support services.

There's something almost poetic about this origin: two young developers, frustrated by inadequate tools, built something better for themselves—and discovered that thousands of other developers shared their frustration. This customer-centric foundation would define Atlassian's approach for the next two decades.

III. The Revolutionary No-Sales-Team Model (2002-2006)

The Unconventional Distribution Bet

Here's where Atlassian's story diverges from virtually every enterprise software company that preceded it. Conventional wisdom in 2002 held that selling software to businesses required sales teams—expensive, quota-driven armies of account executives, solution architects, and customer success managers who could navigate complex procurement processes.

Mike and Scott recognized the US as their biggest target market, meaning they had to either invest in a traditional sales team or build a self-service purchase platform. They opted for the latter despite the risk. The co-founders knew it was the right decision when they awoke one morning to find a purchase order from American Airlines sitting in their fax machine.

That fax machine moment deserves emphasis. Here were two twenty-somethings in Sydney who had never visited American Airlines' headquarters, never made a sales call to a Fortune 500 company, never bought dinner for a procurement officer—and yet one of the world's largest airlines had found their product, evaluated it, and decided to buy it. All without any sales interaction whatsoever.

Atlassian operates under the principle that "software should be bought, not sold." Instead of running a traditional sales team, they opted to build a self-service purchase experience. This was considered risky in the early 2000s, but the strategy worked better than expected.

The Beer-and-Stickers Marketing Strategy

If they weren't spending on sales teams, where did they focus their marketing resources? The answer reveals much about Atlassian's culture and customer understanding.

They decided to forgo the expense of hiring salespeople, and instead spent their time and money on building a good product and selling it at a more affordable price via the Atlassian website. As of 2016, the company still did not have a traditional sales force, investing instead in research and development.

The original marketing strategy was remarkably grassroots: going to meetups for developers and buying them beers—with the Atlassian sticker on the bottle. It sounds almost quaint now, but it represented a profound understanding of their customer: developers talked to each other, they shared tools that made their lives easier, and they trusted peer recommendations over vendor pitches.

Atlassian benefits from significant economies of scale driven by its viral marketing and self-service sales model. This approach supports 81.82% gross profit margins, while sales, general, and administrative costs remain at just 46% of gross profit. In contrast, Salesforce spends approximately 74% of gross profit on SG&A.

The economic implications were staggering. By avoiding the massive sales and marketing overhead that burdened competitors, Atlassian could price products lower, invest more in R&D, and let the product itself drive adoption.

Rapid Profitability Without Venture Capital

Within three years after its founding, Atlassian was profitable without having taken any venture capital.

This single fact separates Atlassian from virtually every other enterprise software success story of the 2000s. While Salesforce, ServiceNow, and Workday were all building their businesses with substantial venture backing, Atlassian demonstrated that profitability could coexist with growth in enterprise software—if you architected your business model correctly.

In 2005, they opened an office in New York, where most of their clients were. Farquhar and Cannon-Brookes were recognized with the award of the 2006 Ernst & Young Entrepreneur of the Year Award.

Scott was the youngest person ever to be awarded the "Australian Entrepreneur of the Year" in 2006 by Ernst & Young alongside co-founder and co-CEO Mike Cannon-Brookes.

Early Product Expansion: Confluence (2004)

Then, in 2004, Atlassian launched its team collaboration platform named Confluence.

This wasn't just a product extension—it was a strategic masterstroke. Confluence's seamless integration with Jira, which was catching on fast in the developer community, was key to their success. "We had two rocket engines driving us along, not just one," Cannon-Brookes says.

With Jira capturing the issue tracking market and Confluence addressing team documentation and collaboration, Atlassian had created its first flywheel: customers who adopted one product had natural reasons to adopt the other. This cross-sell motion would become a defining characteristic of Atlassian's growth strategy.

The 1% Pledge & Company Culture

In 2006, only four years after launch—when the company was still small and scrappy—the founders made a decision that would define Atlassian's corporate identity for decades.

Atlassian believes every success is a group effort, so they are big believers in giving back. When Mike and Scott started the Atlassian Foundation, they pledged to donate one percent of profits, product, equity, and employee time to social impact organizations. At that time, Atlassian was still quite small, and making good on that pledge was painless. (One percent of almost nothing is nothing, right?) And because they baked that pledge into the operating model early on, it's never been treated as a sacrifice. Just a normal part of doing business.

Since 2006, the Atlassian Foundation has donated more than $54 million and 200,000 volunteer hours, supplying more than 133,000 nonprofits with free or deeply discounted product licenses.

This 1% pledge would later inspire a broader movement. In 2014, Farquhar co-founded Pledge 1%, a movement that encourages companies to dedicate 1% of equity, 1% of employee time, 1% of product, and 1% of profit to charity.

The investment implications of this early commitment to culture run deep. Companies with strong values tend to attract and retain better talent, which in enterprise software is perhaps the most important competitive advantage of all.

IV. Key Inflection Point #1: The Accel Investment & First $100M (2010-2012)

Taking the First Major External Capital

For eight years, Atlassian grew without a dollar of venture capital. By 2010, the founders had proven everything they needed to prove about their model—but they recognized that strategic capital could accelerate their ambitions.

In July 2010, Atlassian raised $60 million in secondaries venture capital from Accel Partners. By June of the next year, it announced that revenue had increased 35% in the previous year to $102 million.

The choice of Accel Partners wasn't arbitrary. The founders had received multiple investment inquiries from venture capitalists and were excited to take growth to the next level. It was just a matter of finding the right fit. They found it in Accel Partners. They shared Atlassian's values and the founders' point of view on how to lead a company, and wouldn't ask them to upend their model or their culture.

This is worth pausing on: Cannon-Brookes and Farquhar didn't need Accel's money to survive. They chose Accel because the firm wouldn't try to "fix" what was working. That negotiating leverage—coming from a position of profitability rather than desperation—allowed them to maintain control over the company's direction.

Building the Acquisition Engine

With capital in hand, Atlassian began systematically expanding its product portfolio through strategic acquisitions.

FishEye, Crucible, and Clover came into Atlassian's portfolio by acquiring another Australian software company, Cenqua, in 2007.

Their association with Accel led to the purchase of Bitbucket in September 2010.

In 2012, Atlassian acquired HipChat, an instant messenger for workplace environments.

The Bitbucket acquisition deserves particular attention. By acquiring a Git-based code hosting service, Atlassian positioned itself to compete directly with GitHub for developer mindshare. The thesis was elegant: if you're using Jira to track issues and Confluence to document your work, why wouldn't you host your code in Bitbucket and keep everything in one ecosystem?

The Atlassian Marketplace Launch (2012)

In May 2012, Atlassian Marketplace was introduced as a website where customers can download plug-ins for various Atlassian products.

The Marketplace represented Atlassian's platform play—a recognition that no single company could build every feature customers might need. By enabling third-party developers to build and sell add-ons, Atlassian created a ecosystem effect that made its products more valuable and created switching costs for customers.

The company operates Atlassian Marketplace, an online marketplace for selling third-party, as well as Atlassian-built, add-ons and extensions. From its inception in 2012 to September 30, 2015, the Atlassian Marketplace generated over $100 million in revenue, including over $80 million in revenue for these third-party vendors. As a result, Atlassian generated over $20 million in revenue from the Marketplace during this period.

Jira Service Desk & Market Expansion (2013)

The 2013 launch of Jira Service Desk marked a significant strategic expansion beyond Atlassian's traditional developer-focused customer base.

By extending Jira's capabilities into IT service management—a market traditionally dominated by ServiceNow and BMC—Atlassian demonstrated that its platform could serve broader enterprise needs. The logic was sound: IT teams already used Jira for development projects, so why not use it for help desk ticketing as well?

This expansion presaged Atlassian's longer-term strategy of moving beyond pure developer tools into broader team collaboration and enterprise service management.

V. Key Inflection Point #2: The IPO (December 2015)

Going Public on NASDAQ

Atlassian announced the pricing of its public offering of 22,000,000 Class A ordinary shares at a price of $21 per share.

On December 10, 2015, Atlassian made its initial public offering (IPO) on the NASDAQ stock exchange, under the symbol TEAM, putting the market capitalization of Atlassian at $4.37 billion.

After pricing its initial offering at $21 per share, well above its original range, shares of Atlassian opened even higher at $27.48. At the closing bell, Atlassian was up over 30% on the day.

The IPO pricing tells its own story: Atlassian initially expected to price between $16-$18, then raised the range to $19-$20, and ultimately priced at $21—which then popped 30% on opening day. The market was clearly hungry for Atlassian shares.

A Rare Profitable Tech IPO

Whether this success will continue in the long-term remains to be seen, but Atlassian came to market with a lot of advantages. For one, the company had been profitable for the last ten years, which is impressive considering that many tech companies remain in the red for years after their IPOs. Besides its profitability, Atlassian is unique in its approach to business. Unlike many other enterprise software companies, Atlassian does not have a traditional sales staff. Instead, it lists all of its product information, pricing, training material, and support requests directly on its website. This has saved the company a considerable amount of money throughout the years.

In an era when tech IPOs routinely featured companies burning through hundreds of millions of dollars annually, Atlassian's decade of profitability was remarkable. The company had demonstrated that high growth and profitability weren't mutually exclusive—a lesson that many technology companies have still not learned.

Founder Ownership & Dual-Class Structure

The company has two classes of ordinary shares, Class A ordinary shares and Class B ordinary shares. The rights of the holders of Class A ordinary shares and Class B ordinary shares are identical, except with respect to voting, conversion and transfer rights. Each Class A ordinary share is entitled to one vote. Each Class B ordinary share is entitled to ten votes and is convertible into one Class A ordinary share. The holders of outstanding Class B ordinary shares held approximately 96.7% of the voting power of the outstanding share capital following the offering.

This dual-class structure ensured that Farquhar and Cannon-Brookes maintained control over the company's strategic direction despite selling shares to the public. As of 2024, each founder owns approximately 20 percent of Atlassian, with super-voting shares that preserve their control over major corporate decisions.

Customer Scale at IPO

At the time of its IPO, Atlassian served about 48,000 customers and 5 million monthly active users (MAUs). Today, it serves more than 200,000 customers, including 83% of the Fortune 500, and 10 million MAUs.

The growth from 48,000 customers at IPO to over 300,000 today represents compound annual growth of roughly 20%—sustained over nearly a decade. This customer acquisition engine, powered by product-led growth and word-of-mouth, has been the foundation of Atlassian's revenue expansion.

VI. Key Inflection Point #3: The Trello Acquisition (January 2017)

The Biggest Deal Yet

In January 2017, Atlassian announced the purchase of Trello for $425 million.

The acquisition is valued at approximately $425 million, which is comprised of approximately $360 million in cash and the remainder in Atlassian restricted shares, restricted share units and options to acquire Atlassian shares, all subject to continued vesting provisions.

This marks Atlassian's 18th acquisition and, as Atlassian president Jay Simons noted, it is also the largest.

Why Trello Mattered

Atlassian entered into a definitive agreement to acquire Trello, a breakout collaboration service that has amassed more than 19 million registered users in just five years. Trello has pioneered an intuitive, visual system that solves the challenge of capturing and adding structure to fluid, fast-forming work for teams. The service has been rapidly adopted in more than 100 countries around the world.

The strategic logic was multi-layered. Trello represented Atlassian's push beyond its traditional developer audience into mainstream business collaboration. While Jira was powerful but complex—beloved by engineering teams but intimidating to marketing or HR departments—Trello was approachable, visual, and immediately intuitive.

The 2017 acquisition of Trello and similar tools gained escape velocity thanks to the consumer-grade experience, strong growth loops and freemium price point. But even back in 2023, Atlassian's flagship products Jira and Confluence were starting to gather some "enterprise dust." Each was good software and a profitable line of business, but as the company moved upmarket, it couldn't rely exclusively on product-led growth anymore.

More than 19 million users later, Trello is used by everyone from the family planning their next vacation to employees at the largest enterprises in the world. Companies like Google, National Geographic, and even the United Kingdom's government use Trello daily. Organizations like the United Nations and the Red Cross rely on Trello to accomplish their missions.

Integration Philosophy

The Trello acquisition also revealed something important about Atlassian's approach to M&A: they don't just acquire products, they acquire communities.

Just like with many of Atlassian's other acquisitions, the company plans to keep both the Trello service and brand alive and current users shouldn't see any immediate changes.

This light-touch integration approach—allowing acquired products to maintain their identity while gradually deepening platform connections—has become an Atlassian trademark. It reduces integration risk and preserves the user communities that made the products valuable in the first place.

VII. The Chat War Failure: HipChat, Stride & Slack (2012-2018)

The HipChat Acquisition & Missed Opportunity

Not every Atlassian strategic bet has paid off. The company's foray into enterprise chat—which seemed logical given its collaboration focus—ended in an expensive and humbling failure.

HipChat was launched in beta form back in 2009, long before Slack's debut in 2013. It mostly ruled its space in the time in between, leading Atlassian to acquire it in March of 2012. Slack quickly outgrew it in popularity though, for myriad reasons—be it a bigger suite of third-party integrations, a better reputation for uptime, or better marketing. By September of 2017, Atlassian overhauled its chat platform and rebranded it as "Stride," but it was never able to quite catch up with Slack's momentum.

The timing was particularly painful. Atlassian had acquired HipChat in 2012, before Slack even existed. They had first-mover advantage in the enterprise chat market—and squandered it.

The Painful Stride Shutdown

Atlassian announced that they are entering into a strategic partnership with Slack on July 26, 2018, and will no longer offer their own real-time communications products Hipchat Cloud, Hipchat Data Center, Hipchat Server, and Stride.

According to an FAQ about the change, Stride and HipChat's last day will be February 15th, 2019—or a bit shy of seven months from the date of the announcement.

Atlassian decided to exit the chat business because it just wasn't as successful as expected, and it wants to focus on project management software. In exchange for Hipchat Cloud and Stride's IP, the company will be getting a "small, but symbolically important" equity investment in Slack.

Atlassian VP of Product Management, Joff Redfern, confirmed the news in a blog post, calling it the "best way forward" for its existing customers. It's about as real of an example of "if you can't beat 'em, join 'em" as you can get; even Atlassian's own employees will be moved over to using Slack.

Lessons Learned

The HipChat/Stride debacle offers important lessons. Atlassian's leadership has been remarkably candid about what went wrong:

"I think it was just not a business that Atlassian wanted to be in," said analyst Alan Lepofsky of Constellation Research.

IT pros were skeptical of Atlassian Stride and judged it as too little and too late to compete with an entrenched ChatOps competitor.

The failure demonstrates that even great companies can misread markets. Atlassian tried to retrofit HipChat for enterprise customers while Slack was building a better product from the ground up with consumer-grade design sensibilities. By the time Stride launched in 2017, Slack had achieved escape velocity.

Atlassian co-CEO Mike Cannon-Brookes paid tribute to his staff: "Shout out to all of the Atlassians who worked their asses off building Stride + Hipchat," he tweeted. "We built a great product."

The silver lining: Atlassian's equity stake in Slack proved prescient when Salesforce acquired Slack for $27.7 billion in 2021, generating a meaningful return on what had been a strategic exit.

VIII. Key Inflection Point #4: The Cloud-First Pivot (2020-2024)

The Server End-of-Life Announcement

In October 2020, Atlassian made the most consequential strategic decision in its history: to end support for its server products and go all-in on cloud.

In 2020, driven by the mission to create a world-class Cloud experience, Atlassian made the strategic decision to discontinue support for server products. Starting February 15, 2024, Atlassian and Marketplace partners would no longer provide technical support, security updates, or bug fixes for vulnerabilities on server products or apps.

In order to focus on delivering a world-class cloud experience, Atlassian ended the sale and support of server licenses. On February 2, 2021, they stopped selling new licenses for server products and ceased new feature development in the server product line. For existing server license holders, they could continue to renew and receive maintenance and support until February 2, 2024.

First announced over three years ago, support for Atlassian's server products ended on February 15, 2024. This marks the end of a 20-year era! The first version of Jira Server was released in 2002 and the first Confluence Server version was released in 2004.

The Strategic Rationale

Cloud is faster, more secure, better for scaling, more cost effective, and more remote-friendly. And with the current roadmap, it's expected to meet the needs for all customers.

The decision was not without controversy. Many large enterprises, particularly those with strict data residency requirements or operating in regulated industries, relied on self-hosted server installations. Forcing them to migrate to cloud—or pay significantly more for Data Center licenses—created friction and, in some cases, pushed customers to competitors.

But Atlassian's leadership believed the long-term benefits outweighed the short-term risks. Cloud deployments are easier to maintain, update more frequently, provide better analytics, and—critically—generate more predictable recurring revenue.

Customer Impact & Migration Success

Atlassian's Deatsch told The Register migration rates have exceeded the vendor's forecasts. "We thought enterprises would be slow, but they were fast," he said. "Many got cloud mandates from their CIOs." His goal was to ensure that every remaining server customer "knows their options and understands incentives like migration tools, discounts, and extended trials."

Today, the Atlassian Cloud powers more than 290,000 customers like NASA, Reddit, Rivian, Domino's Pizza Enterprises Ltd, and PayPal. Customers now have more seats on the Atlassian Cloud than on Data Center and Server combined, and 94% of all customers have a Jira Software, Confluence, and/or a Jira Service Management presence on Cloud.

Atlassian has successfully completed its transition to a cloud-first model, with cloud revenue now constituting over 95% of total sales.

The cloud transition has fundamentally transformed Atlassian's business model. Cloud revenue, which consists of recurring subscription fees, provides much greater visibility and predictability than the one-time server license sales of the past. It also enables Atlassian to deliver features faster and collect usage data that informs product development.

IX. The M&A Engine: Building a $50B+ Growth Machine

Acquisition Strategy Overview

Atlassian's growth story cannot be told without understanding its prolific acquisition activity. The company has completed more than 40 acquisitions since its founding, systematically filling product gaps and expanding into adjacent markets.

A small startup called Dogwood Labs in Denver, Colorado, which had a product called StatusPage (that hosts pages updating customers during outages and maintenance), was acquired in July 2016.

On 12 October 2023, Atlassian agreed to buy video messaging company Loom for US$975 million, with the intention to integrate Loom's technology into its existing services.

Atlassian announced it has entered into a definitive agreement to acquire Loom, the video messaging platform that has amassed more than 25 million users and was named among the top 50 of Fast Company's World's Most Innovative companies in 2023. The global movement towards distributed work has fueled a need for new ways to help teams collaborate. Asynchronous (async) video has been at the forefront of this movement with Loom's business users recording almost 5 million videos per month.

Under the terms of the definitive agreement, Atlassian will acquire Loom for approximately $975 million, inclusive of Loom's cash balance, subject to customary adjustments.

Key Acquisitions Timeline

The pace and pattern of acquisitions reveals Atlassian's strategic thinking:

- 2007: Cenqua (FishEye, Crucible, Clover) - developer tools

- 2010: Bitbucket - code repository

- 2012: HipChat - team chat (later discontinued)

- 2015: Hall, Blue Jimp (Jitsi) - collaboration and video

- 2016: StatusPage - incident communication

- 2017: Trello ($425M) - visual project management

- 2018: OpsGenie ($295M) - incident management

- 2020: Halp, Mindville - service management tools

- 2021: Chartio - analytics

- 2023: Loom ($975M) - async video, AirTrack - asset management

- 2025: DX - developer intelligence

Atlassian's acquisition of The Browser Company (maker of Dia and Arc) raised questions in 2025. Atlassian has reached the scale where incremental moves won't generate the growth it needs. Its main strategy for years has been adding adjacencies to the Jira suite—Confluence for documentation, Trello for project management, Loom for video communication.

M&A Contribution to Revenue

The financial impact of Atlassian's acquisition strategy has been substantial. Acquired products often grow faster within the Atlassian ecosystem than they would have independently, benefiting from cross-selling opportunities, integration synergies, and Atlassian's distribution capabilities.

This M&A engine represents a sustainable competitive advantage. Atlassian's established customer relationships, technical infrastructure, and brand trust enable it to extract more value from acquired companies than standalone operators might achieve.

X. Key Inflection Point #5: The AI Era - Rovo & Beyond (2023-2025)

Atlassian Intelligence & Rovo Launch

During its Team '24 conference in Las Vegas, Atlassian launched Rovo, its new AI assistant. Rovo can take data from first- and third-party tools and make it easily accessible through a new AI-powered search tool and other integrations into Atlassian's products. The most interesting part, though, may be the new Rovo Agents, which can be used to automate workflows in tools like Jira and Confluence.

Atlassian's head of product for Atlassian Intelligence told TechCrunch: "We like to think of Rovo as a large knowledge model for organizations. It's a knowledge discovery product for every knowledge worker."

Powered by Atlassian Intelligence, a generative AI offering the company launched a year ago, Rovo helps companies find information lost amid multiple products, learn quickly, and act on behalf of employees like a "virtual teammate." "The first thing Rovo does is it brings together all those third-party SAS tools, as well as your custom-built in-house tools, and lets you put it all into one search index for all of your employees," Sherif Mansour, head of artificial intelligence at Atlassian, said.

Rovo's Architecture and Capabilities

All that knowledge has been poured into a proprietary common data model called "teamwork graph." This is the secret sauce that makes Rovo, and all other AI capabilities, so special. Teamwork graph pulls in data from Atlassian tools and other SaaS apps you choose to connect, unlocking a comprehensive view of your organization's goals, knowledge, teams, and work. With every new tool connection, team action, and project event, teamwork graph draws more connections and expands its knowledge.

Rovo has three parts, all of which can operate independently or, when combined, establish a workflow with the potential to improve discovery and decision-making. The first is Rovo Find, which indexes content from internal and third-party tools to put it in one place. The second is Rovo Learn, a tool to facilitate education, or a "tailored company glossary for your organization that updates in real-time." Lastly, there are Rovo Agents, specialized bots organizations can use in workflows to address time-consuming tasks.

At its Team '24 Europe event in Barcelona, the company announced the general availability of Rovo. Jamil Valliani, Atlassian's head of product for Atlassian Intelligence, said Search will support about 80 connectors in the coming months.

AI Adoption and Business Impact

Mike Cannon-Brookes stated: "We closed out FY25 delivering over $5.2 billion of revenue, generating over $1.4 billion in free cash flow, and reaching 2.3 million AI monthly active users. AI is fundamentally changing the way we work, and creating significant tailwinds for Atlassian in the process. With our world-class cloud platform underpinned by the breadth and depth of our Teamwork Graph, and Rovo's AI capabilities at the center, we are uniquely positioned to help every team unleash enterprise knowledge at scale."

In just the past six months, Rovo has been rolled out to every paying Atlassian Cloud customer—across Enterprise, Premium, and now Standard editions—as part of subscriptions at no extra cost. AI usage has already more than doubled across the customer base, with no signs of slowing.

In just six months, Rovo agents have already shown up in a whopping 2.4 million business workflows, creating a launch pad for the next wave of human-AI collaboration.

Mike Cannon-Brookes noted: "I am filled with immense pride as I reflect on Team '25 and our customers' and partners' reactions to our relentless focus on innovation. Our long-term investments in building a world-class Cloud platform have enabled us to advance the Atlassian System of Work and bring Rovo's powerful AI capabilities to the center."

Developer-Focused AI: Rovo Dev

Rovo Dev reduces friction across the entire software delivery lifecycle, available in terminal, IDE, and beyond. Break through blockers with AI that's more than just a vibe—helping deliver high-quality software, fast. Spend less time ramping up on requirements and codebases with clear code plans that surface knowledge from across the Atlassian platform. Get a head start with implementation that aligns to your code plans—refactoring, new tests and docs included. Let Rovo Dev analyze your code and suggest improvements, validating code changes against acceptance criteria in Jira. Run parallel tasks with AI working in the background to plan, generate, and review code at scale.

Customers report: "With Rovo Dev, we've cut PR cycle times by 45%—helping our developers deliver more value to our customers, faster."

The AI strategy represents Atlassian's next growth chapter. By embedding intelligence throughout its platform—from search to code generation to workflow automation—the company is positioning itself as essential infrastructure for the AI-enabled enterprise.

XI. Competitive Landscape & Strategic Positioning

The Microsoft Juggernaut

The company's most formidable rival is Microsoft, whose Azure DevOps platform and GitHub subsidiary, with its community of over 100 million developers, present significant competitive pressure.

Microsoft has emerged as one of Atlassian's most formidable competitors. Microsoft's Azure DevOps and GitHub target Atlassian's Jira in the product planning market, while Microsoft Teams is chasing Atlassian's Confluence in the cloud-based collaboration space.

Microsoft's competitive advantage is integration: companies already using Office 365, Azure, and Teams find Microsoft's development tools to be a natural extension of their existing stack. This "better together" story is compelling for enterprises looking to simplify their vendor relationships.

Integration with Development Tools: While not a direct competitor to Jira, Teams enhances its competitive edge through deep integration with Azure DevOps and GitHub, linking discussions directly with code repositories, builds, and deployments. Extensive Ecosystem: Teams is deeply integrated with the Microsoft Office suite and supports a broad ecosystem of third-party applications.

Point Solution Competitors

Beyond Microsoft, Atlassian faces competition from specialized players in each of its markets:

The company faces stiff competition from Microsoft, GitLab, IBM, ServiceNow, GitHub, Asana, Blueprint, and Broadcom.

Key competitors include Microsoft, GitLab, ServiceNow, Asana, Smartsheet, and Monday.com.

ServiceNow competes directly with Jira Service Management in IT service management. Asana, Monday.com, and Smartsheet challenge Trello and Jira in project management. GitLab offers a complete DevOps platform that competes with the combination of Jira, Bitbucket, and Confluence.

Market Position and Moat

Despite formidable competition, Atlassian maintains substantial competitive advantages:

Atlassian holds an estimated over 65% market share in the issue tracking and project management software segment for technical teams as of mid-2025. This commanding position in the DevOps tools market creates substantial barriers to entry for competitors seeking to challenge its dominance.

The company maintains exceptional financial health with gross margins nearing 85%, significantly outperforming SaaS industry averages. With a market capitalization around $55 billion, Atlassian demonstrates robust free cash flow generation and sustainable growth metrics.

Atlassian serves more than 300,000 customers in over 200 countries, including 92% of Fortune 500 companies. The company went public in December 2015 on NASDAQ under the ticker "TEAM" with an initial market capitalization of $4.37 billion.

XII. Financial Analysis & Investment Considerations

Current Financial Performance

Total revenue was $5.2 billion for fiscal year 2025, up 20% from $4.4 billion for fiscal year 2024. Net income was $975.9 million for fiscal year 2025, compared with net income of $762.4 million for fiscal year 2024. Net income per diluted share was $3.68 for fiscal year 2025, compared with net income per diluted share of $2.93 for fiscal year 2024. Free cash flow was $1,415.5 million for fiscal year 2025. Free cash flow margin for fiscal year 2025 was 27%.

CFO Joe Binz stated: "Strong execution by our sales teams and partners delivered a solid close to the fiscal year with Cloud revenue of $928 million, up 26% year over year in Q4."

Atlassian reported first-quarter FY26 results that easily topped guidance, with revenue up 21% year over year to $1.433 billion and non-GAAP operating margin of 22.6%, versus the high end of guidance at $1.403 billion and 20.5%, respectively.

Valuation Context

Atlassian market cap as of November 2025 is approximately $38.42B.

The latest closing stock price for Atlassian as of November 21, 2025 is $146.28. The all-time high Atlassian stock closing price was $458.13 on October 29, 2021.

The stock has fallen substantially from its 2021 peak, reflecting both broader tech sector compression and investor concerns about competition and growth deceleration. However, at current levels, the company trades at roughly 7x trailing revenue—a significant discount to its historical multiples.

Bull Case

The bull case for Atlassian rests on several pillars:

-

AI Monetization: With 2.3 million AI monthly active users and growing, Atlassian is positioned to benefit from enterprise AI adoption. CEO Cannon-Brookes noted: "AI is fundamentally changing the way we work, and creating significant tailwinds for Atlassian in the process."

-

Cloud Transition Complete: With over 95% of revenue now from cloud, Atlassian has successfully navigated a difficult platform transition that provides predictable recurring revenue.

-

Customer Expansion: Net revenue retention rates remain healthy, indicating customers continue to add users and adopt additional products.

-

Market Leadership: 65%+ market share in project management for technical teams creates significant switching costs and pricing power.

-

Free Cash Flow Generation: 27% free cash flow margins demonstrate operating leverage as the business scales.

Bear Case

The bear case focuses on:

-

Microsoft Competition: Microsoft's integrated offering and enterprise relationships pose an existential threat. GitHub's 100M+ developer community dwarfs Bitbucket's user base.

-

Growth Deceleration: 20% revenue growth, while healthy, represents significant deceleration from historical 30%+ rates.

-

AI Uncertainty: It remains unclear whether AI features will drive new revenue or become table stakes that customers expect for free.

-

Premium Valuation: Even after the selloff, ~7x revenue assumes continued strong growth that may not materialize.

-

Leadership Transition: Scott Farquhar resigned as joint CEO at the end of August 2024 to focus on family time, philanthropy, and furthering the global technology industry. He remains on the board and as a special adviser. Since September 2024, Cannon-Brookes is the sole CEO.

Porter's Five Forces Analysis

Threat of New Entrants: LOW High switching costs, network effects from the Marketplace ecosystem, and deep customer integrations create substantial barriers to entry.

Bargaining Power of Suppliers: LOW Atlassian's cloud infrastructure runs on major cloud providers (AWS, Google Cloud), who compete for the business. As a multi-billion dollar customer, Atlassian has meaningful leverage.

Bargaining Power of Buyers: MODERATE While individual customers have limited negotiating power, large enterprises increasingly demand competitive pricing. The presence of alternatives (Microsoft, GitLab) provides some buyer leverage.

Threat of Substitutes: MODERATE TO HIGH Microsoft's integrated stack, combined with best-of-breed point solutions, presents meaningful substitution risk. AI-native development tools could disrupt traditional project management approaches.

Competitive Rivalry: HIGH Microsoft, ServiceNow, GitLab, and numerous point-solution providers compete aggressively across Atlassian's markets.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Atlassian's self-service model creates significant scale advantages—revenue grows without proportional sales headcount additions.

Network Effects: The Atlassian Marketplace creates two-sided network effects between users (who want more plugins) and developers (who want larger user bases).

Counter-Positioning: Atlassian's no-sales-team model was initially counter-positioning against traditional enterprise software vendors. This advantage has eroded as competitors adopted similar approaches.

Switching Costs: Deep workflow integrations, custom configurations, and data accumulated in Jira/Confluence create meaningful switching costs.

Branding: Jira has become the default for software project management—a powerful form of brand power.

Cornered Resource: Not particularly applicable.

Process Power: Atlassian's product-led growth and viral distribution mechanics represent difficult-to-replicate operational advantages.

XIII. Key Performance Indicators to Watch

For long-term fundamental investors, three KPIs matter most for tracking Atlassian's ongoing performance:

1. Cloud Revenue Growth Rate

Cloud represents over 95% of revenue and is the primary driver of company value. Investors should monitor quarterly cloud revenue growth (currently ~26% YoY) as the key indicator of business health. Deceleration below 20% would be concerning; sustained growth above 25% would be bullish.

2. Net Revenue Retention (Dollar-Based)

This metric captures whether existing customers are expanding their Atlassian usage. A NRR above 120% indicates strong upselling and cross-selling; below 110% would signal weakening customer relationships. Atlassian does not publicly disclose this figure, but commentary on expansion dynamics in earnings calls provides proxy insights.

3. Free Cash Flow Margin

With a current FCF margin of 27%, Atlassian generates substantial cash from operations. Maintaining or expanding this margin while investing heavily in AI and R&D would demonstrate durable operating leverage. Compression below 20% would warrant scrutiny of expense discipline.

XIV. Conclusion: The Road Ahead

Atlassian's journey from a $10,000 credit card bet to a $40 billion enterprise software company encapsulates the best of what technology entrepreneurship can achieve. Cannon-Brookes and Farquhar built a globally significant business from Sydney when conventional wisdom said it couldn't be done, pioneered distribution models that became industry templates, navigated painful strategic failures with grace, and executed one of the most significant platform transitions in enterprise software history.

The company they built serves 92% of the Fortune 500 and has fundamentally shaped how software teams work. Jira has become virtually synonymous with project management for technical teams—the kind of category definition that creates enduring value.

Yet challenges remain. Microsoft's integrated juggernaut presents an existential competitive threat. Growth is decelerating as the company matures. The AI revolution creates both opportunity and risk—potential for new revenue streams but also the possibility that AI-native startups will disrupt traditional project management altogether.

As Cannon-Brookes concluded in the recent earnings call: "AI is fundamentally changing the way we work, and creating significant tailwinds for Atlassian in the process. With our world-class cloud platform underpinned by the breadth and depth of our Teamwork Graph, and Rovo's AI capabilities at the center, we are uniquely positioned to help every team unleash enterprise knowledge at scale."

Whether that positioning proves durable will depend on execution in an AI-transformed landscape. But if history is any guide, underestimating the two Australians who built an empire from their bedrooms has been an expensive mistake.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube