CubeSmart: How a Self-Storage REIT Quietly Built an Empire

I. Introduction & Episode Roadmap

Picture this: It's a sweltering August afternoon in the Bronx, and a young mother is pulling her minivan into the loading dock of a gleaming, multi-story building. She's not here for an apartment viewing or a doctor's appointment. She's here to store her grandmother's china, three boxes of her kids' baby clothes, and a set of vintage golf clubs that belonged to her late father. She'll pay about $300 a month for the privilege—roughly the price of a nice dinner for two in Manhattan, every single month, indefinitely.

This scene plays out tens of thousands of times per day across America, in facilities owned and operated by a company most investors have never heard of: CubeSmart.

According to the 2025 Self-Storage Almanac, CubeSmart is one of the top three owners and operators of self-storage properties in the United States. As of recent filings, CubeSmart maintains a portfolio of over 1,300 properties, generating total revenues of approximately $1.15 billion and consistently reporting strong occupancy rates often exceeding 91%.

But here's the thing about CubeSmart that makes it such a fascinating subject for a deep dive: this isn't a company that dominates headlines or commands cultish investor followings. It's not disrupting anything. There's no charismatic founder giving TED talks or posting cryptic tweets. Instead, CubeSmart is a self-administered and self-managed real estate investment trust, founded in 2004, headquartered in Malvern, Pennsylvania.

The big question we're going to answer today is this: How did a regional storage company founded in 2004 become a $10 billion+ REIT and cement its place among America's "Big Three" in self-storage?

The answer involves several intertwined themes: an extraordinarily fragmented industry ripe for consolidation, the structural advantages that public REIT capital provides, a series of brilliantly timed acquisitions that transformed the company's geographic footprint, and perhaps most importantly, a "boring" business model that quietly prints cash through economic cycles while most investors aren't paying attention.

We'll trace CubeSmart's journey from its origins as U-Store-It Trust—a family business taken public in Ohio—through multiple leadership transitions, a complete corporate rebrand, and transformative deals that gave it dominant positions in the most supply-constrained markets in America. Along the way, we'll explore why self-storage might be the most peculiar and underappreciated real estate category in existence.

II. The Self-Storage Industry: America's Uniquely "Stuff"-Obsessed Asset Class

Origins of Modern Self-Storage

Before we can understand CubeSmart, we need to understand the industry it operates in—and there's nothing quite like it anywhere else in the world.

Historians credit China as the original birthplace of self-storage. According to ancient records and legends, a man named Xiang Lau built huge storage vessels in underground pits to store personal items and turned them into a business. Ancient Egyptians stored possessions in tombs with chambers for the deceased, and Romans preserved food and artifacts in climate-controlled storehouses.

But modern self-storage as we know it—the rows of orange-doored units along American highways—is a distinctly American invention, born from a combination of consumerism, mobility, and geographic scale that exists nowhere else on Earth.

In 1964, Russ Williams and Bob Munn opened a facility called "A-1 U-Store-It U-Lock-It U-Carry-the-Key" in Odessa, Texas. Some say the men started the storage unit company to store their fishing gear. More likely, they were servicing the oil industry workers who needed secure places to store equipment. But either way, this unpretentious Texas facility represented the birth of an industry.

The big breakthrough came in 1972. The first Public Storage location opened in El Cajon, California with a fiesta complete with mariachis and bright orange doors to attract the attention of potential customers driving by on the nearby highway. The first customer was a distributor for STP Motor Oil. That customer needed somewhere to stash the cans of motor oil cluttering his driveway—his wife demanded they go. It's a perfect encapsulation of the industry's fundamental demand driver: life creates stuff, and stuff needs a place to go.

By the early 1970s, large national self-storage players like Public Storage, Shurgard, and Storage USA entered the market. The 1970s also saw a cultural shift, with factors like increased divorce rates, transitions between households, and consumer habits driving the demand for self-storage.

Why Self-Storage Works

The self-storage industry operates on what practitioners call the "4Ds of life." When discussing why a storage space is rented, industry experts often refer to "4Ds of life" (death, divorce, delimitation, and discombobulation). That last one—discombobulation—is industry jargon for the chaos of relocating, combining households, or simply feeling overwhelmed by accumulated possessions.

These demand drivers are remarkably persistent. People die in recessions. Couples divorce in booms. Students move to college in good times and bad. And Americans accumulate stuff relentlessly, regardless of economic conditions. Most self-storage facilities run around a 92% occupancy rate. It's estimated that nearly 10% of US households use some form of self-storage.

Perhaps most remarkably, the industry has proven to be genuinely resilient through economic downturns. There is a belief amongst investors that the self-storage industry is recession-proof. This belief is supported by the 5.1% total return the sector delivered to investors in 2008 during the Great Recession. While office buildings emptied and retail centers went dark, Americans kept paying their storage bills.

Unlike other sectors that are dependent on interest rates, job growth or income growth, self-storage is agnostic to the broader economy. Over the last 15 years, self-storage has outperformed industrial, multifamily, office and retail in net operating income, according to a recent Heitman report.

The Industry's Structural Dynamics

The self-storage industry has an unusual structural characteristic that creates enormous opportunity for sophisticated operators: extreme fragmentation.

The self-storage sector is highly fragmented, which is in contrast to other asset classes in the industry. 80% of self-storage facilities are owned by individuals or small investors.

Think about what that means: in an industry with over 50,000 facilities across America, the overwhelming majority are owned by mom-and-pop operators who may have built a single facility as a retirement investment or inherited one from a parent. These operators typically lack sophisticated revenue management systems, digital marketing capabilities, or access to capital for improvements.

Between 2000 and 2005, the self-storage industry saw rapid development, with over 3,000 new facilities built annually. Lifestyle changes drove consumer demand for contemporary storage units.

As of October 2024, the four public self storage REITs owned 30% of the entire U.S. self storage inventory, up from 17% in 2000. Institutional owners (including public REITs) own an estimated 45% of all self storage space in the U.S.

Public REITs now operate roughly 40% of national capacity, up from 20% five years earlier, confirming a progressive consolidation trend. The four largest brands—Public Storage, Extra Space Storage, CubeSmart, and National Storage Affiliates—jointly control near-20% of the United States self-storage market, leaving significant fragmentation among small operators.

This consolidation dynamic—still in its early innings despite decades of progress—is the fundamental investment thesis for CubeSmart. Every property acquired from a small operator can be upgraded with better technology, connected to a national marketing platform, and operated with institutional efficiency. The result is typically significant NOI improvement, creating value for shareholders while providing a reasonable exit for small operators who lack the capital or expertise to compete long-term.

III. Origins: The Amsdell Family & U-Store-It Trust (2004)

Formation Story

The CubeSmart story begins not in Malvern, Pennsylvania—its current headquarters—but in the industrial suburbs of Cleveland, Ohio, with a family whose roots in the self-storage business stretch back decades.

The Amsdell group of companies draws its roots from the family owned construction company founded in 1928. Today, it enjoys tremendous success as a premier full service, privately owned real estate company, specializing in the construction, development and management of self-storage facilities, business parks, and related commercial real estate.

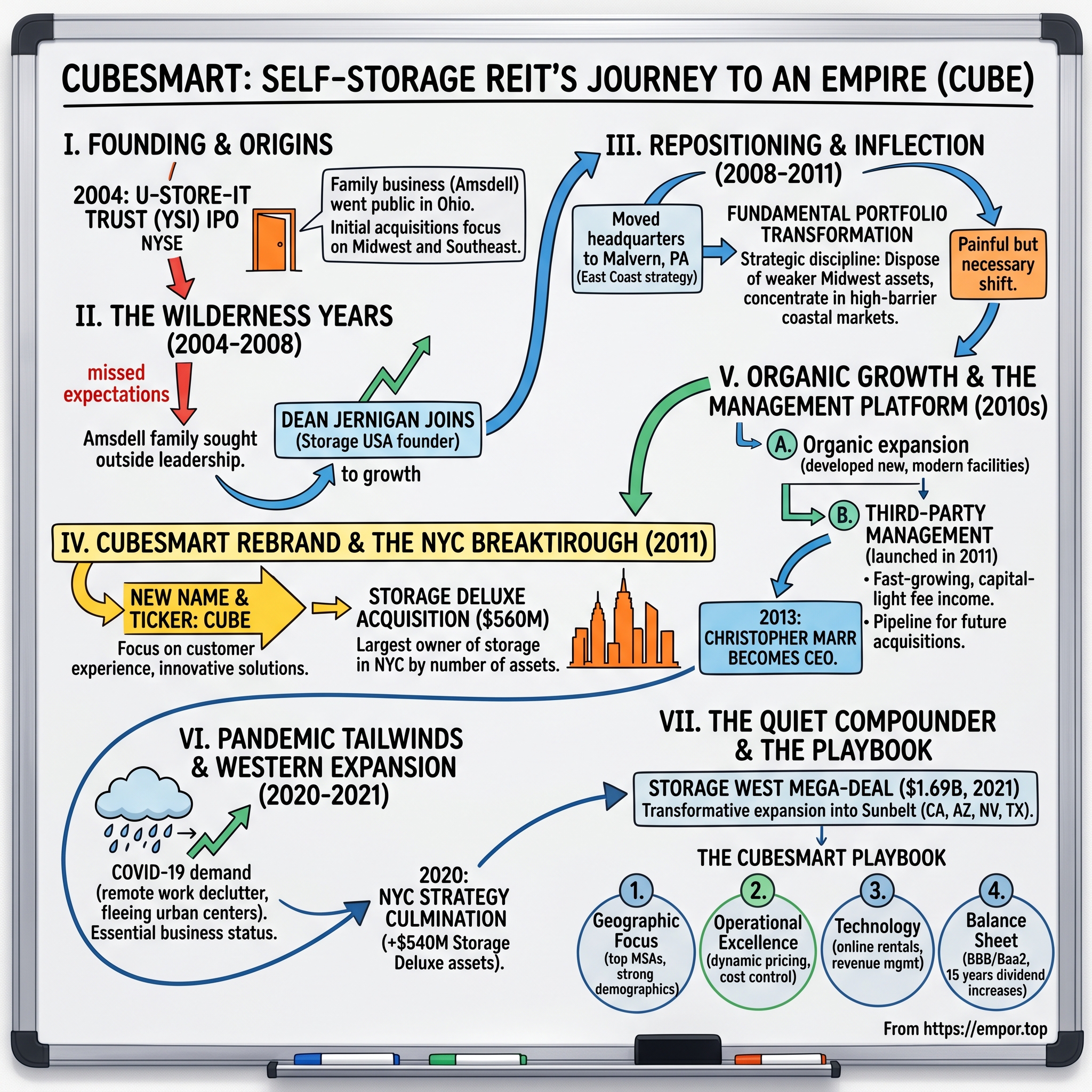

In 1976, the Amsdell family founded U-Store-It, a real estate company focused on the ownership, operation, acquisition and development of self-storage facilities. In 2004, U-Store-It became U-Store-It Trust (now CubeSmart Trust), a publicly traded REIT.

Two of the major self-storage real estate investment trusts (REITs) can trace their roots to the Amsdell Companies. The brothers were attracted to real estate because of the generous tax breaks that existed before the laws were changed with the Tax Reform Act of 1986. The financial landscape during the 1980s was littered with limited partnerships because they were touted as safe tax havens.

Previously, Barry Amsdell was the president of a construction company and Bob Amsdell was a lawyer. Amsdell discloses that his father and uncle believe they invented the modern self-storage industry when they bought a railway building in Pennsylvania in the early 1970s.

Whether or not the Amsdells truly "invented" self-storage is debatable—Russ Williams and Bob Munn in Odessa might dispute that claim. But what's undeniable is that the family built an impressive portfolio through the tax-advantaged limited partnership era, only to face a reckoning when tax law changes in 1986 altered the economics of their business model.

"Those changes facilitated the need for the next big change, which was to take the company public," says Amsdell. "As developers and construction company, it was not the best vehicle for us because it's difficult for public companies to build and develop, so Bob and Barry sold out their ownership in Sovran."

The IPO

On October 27, 2004, the Amsdell family took their self-storage business, U-Store-It, public. At that time, Robert Amsdell was named Chairman of the Board and Chief Executive Officer; Todd Amsdell, Robert's son, was named Chief Operating Officer; and Barry Amsdell was elected a Trustee of the Company. At the time of the Company's initial public offering, 19 of the self-storage properties owned by members of the Amsdell family were in development and not yet profitable.

The Company completed its initial public offering on October 27, 2004. The IPO listed on the New York Stock Exchange under the ticker symbol "YSI" and raised substantial capital that would fuel the company's early acquisition strategy.

U-Store-It Trust (NYSE: YSI), a self-administered and self-managed real estate investment trust focused primarily on self-storage facilities, announced that it completed the acquisition of the Metro Storage portfolio for $184.0 million. The portfolio consists of 42 self-storage facilities located in five states, Illinois, Indiana, Florida, Ohio and Wisconsin.

The Metro Storage acquisition, completed within days of the IPO closing, demonstrated the company's aggressive growth appetite. Becoming a publicly traded REIT unlocked access to significant capital, fueling the acquisition strategy that defined U-Store-It's early growth and established it as a major industry player.

IV. The Wilderness Years: 2004–2008

The period immediately following U-Store-It's IPO represented a time of ambitious expansion but also growing pains. The company went on a buying spree, snapping up portfolios across the Midwest and Southeast, rapidly scaling its property count.

The addition of Mr. Jernigan as CEO is an effort by U-Store-It to repair the damage on Wall Street following a series of missed earning estimates that the company blamed on its self-storage buying spree. But it's also a way for Mr. Amsdell, 65, to alter his role at the company and set up a long-term succession plan.

The challenges of operating in a highly fragmented market against entrenched competitors like Public Storage and Extra Space proved significant. U-Store-It's initial assets, concentrated primarily in the eastern and midwestern United States—including states such as Ohio, Florida, Illinois, Indiana, and Wisconsin—provided a stable base of revenue-generating properties. But the company struggled to translate portfolio growth into consistent earnings performance.

By 2006, the Amsdell family recognized they needed outside leadership to professionalize operations and restore Wall Street credibility.

A veteran public company executive and self-storage operator, Dean Jernigan, is the new president and CEO of U-Store-It Trust, the Middleburg Heights-based real estate investment trust announced today as U-Store-It co-founder Robert J. Amsdell announced plans to shift his focus from day-to-day operations. Mr. Jernigan succeeds Mr. Amsdell as CEO, though Mr. Amsdell remains executive chairman.

Dean Jernigan has more than 30 years of experience in the self storage industry. He entered the industry in 1984 when he founded Storage USA, a company he took public in 1994. He grew Storage USA from a single property to more than 570 properties at its peak. During its life as a public company and under his leadership as Chairman and CEO, the company returned a 17.5% compounded annual return to its investors.

The 60-year-old Mr. Jernigan was founder, chairman and CEO of Memphis, Tenn.-based Storage USA Inc. from 1985 until its $1 billion sale in 2002 to Security Capital Group, an international realty company.

Jernigan was, quite simply, the most accomplished executive in the self-storage industry. His track record at Storage USA was impeccable, and his relationships on Wall Street were deep. Bringing him in signaled serious intent to professionalize U-Store-It and compete at the highest level.

Mr. Jernigan said in an interview that he'd discovered he was too young to retire and wanted to return to work "after a few years traveling the world and playing all the golf and tennis I could handle." He said he used to describe his old job at Storage USA as "the best job in the world" and believes U-Store-It offers him the same opportunity to work again in the same industry and with Wall Street.

The arrival of Jernigan coincided with another critical hire that would prove even more consequential for CubeSmart's long-term trajectory.

V. Inflection Point #1: The Great Financial Crisis & Leadership Change (2008–2011)

Crisis as Catalyst

The Great Financial Crisis of 2008-2009 represented an existential moment for many real estate companies. Credit markets froze, property values plummeted, and leveraged operators found themselves unable to refinance maturing debt. U-Store-It, like all REITs, faced these headwinds directly.

But the crisis also created opportunity. In December 2008, the company transferred its headquarters to Malvern, Pennsylvania. This wasn't merely a change of scenery—it represented a strategic repositioning closer to the East Coast markets that would define the company's future growth trajectory.

More importantly, the financial crisis allowed U-Store-It's new leadership team to execute a fundamental portfolio transformation at distressed valuations.

Mr. Marr joined the Company in 2006, serving as Chief Financial Officer and Treasurer until November 2008. Prior to joining CubeSmart, Mr. Marr was Senior Vice President and Chief Financial Officer of Brandywine Realty Trust, a publicly-traded office REIT, from August 2002 to June 2006.

Prior to joining Brandywine Realty Trust, Mr. Marr served as Chief Financial Officer of Storage USA, Inc., a publicly-traded self-storage REIT, from 1998 to 2002.

Christopher Marr's background deserves special attention. He had served as CFO of Storage USA—the company Dean Jernigan founded—before moving to Brandywine Realty Trust and then to U-Store-It. This meant the two senior leaders at U-Store-It had worked together for nearly two decades and shared a deep understanding of both self-storage operations and public company management.

In June 2006, Marr was part of a new management team at CubeSmart trying to reorient their portfolio, focusing on quality properties in the top markets. They sold low-growth markets and reinvested in higher-growth cities in a process that Marr described as "painful."

"This transaction accelerates the portfolio transition that management began in 2008, further improving our demographics, margins and rent per square foot," said Christopher Marr. "Going forward, more than 60 percent of our portfolio net operating income will be derived from our core markets, a 43 percent improvement from January 2008."

Strategic Repositioning

The repositioning strategy was clear: dispose of weaker Midwest assets and concentrate capital in high-barrier, high-rent coastal markets. During the year ended December 31, 2011, the company sold 19 self-storage facilities located throughout Indiana, Ohio and Michigan for an aggregate sales price of approximately $45.2 million.

This willingness to shrink in order to improve quality—to take the painful step of selling familiar assets in home markets—demonstrated the strategic discipline that would characterize CubeSmart's growth for the next decade.

VI. Inflection Point #2: The CubeSmart Rebrand & Storage Deluxe Acquisition (2011)

The Rebrand

On September 14, 2011, the company announced and completed its rebranding from U-Store-It Trust to CubeSmart, with shares beginning to trade under the new ticker symbol "CUBE" on the New York Stock Exchange on September 19. The rebranding sought to modernize the company's image, emphasizing innovative customer solutions and broader market appeal in the self-storage industry.

The name change was more than cosmetic. Our old name put the service responsibility on the customer: YOU store it. YOU do it. YOU handle it. We made a brand promise with CubeSmart that is much broader, more positive, and more focused on the customer than was with U-Store-It.

In explaining the rebrand, CEO Dean Jernigan noted: "The answer kept coming back: customers know what business we're in, we don't have to tell them what the storage business is. In the 70s, it was worthwhile to say we're in the business of storage. That's no longer the case. People are very aware of what storage is and how it's to be used."

The rebranding costs were estimated to be approximately $8 million. The Company expected to change its corporate name to CubeSmart and to change its ticker symbol on the New York Stock Exchange from YSI to CUBE by the end of 2011.

The Transformative Storage Deluxe Deal

The rebrand announcement coincided with something far more significant: the most transformative acquisition in the company's history.

CubeSmart (NYSE: CUBE) announced that it has entered into an agreement to acquire a $560 million portfolio of high-quality self-storage facilities in the greater New York City area from Storage Deluxe. The Company has entered into a contract to acquire 22 Class A self-storage facilities from Storage Deluxe for total consideration of $560 million, including the assumption of $88 million of existing secured indebtedness. Following the closing of the transaction, the Company will be the largest owner, by number of assets, of self-storage facilities in New York City.

Storage Deluxe was founded in 1998 by its Chairman, Steven Guttman, formerly Chairman and CEO of Federal Realty Investment Trust. During the past 13 years, the company's portfolio grew to include 32 storage facilities with over 2 million rentable square feet, 30,000 storage units and over 150 employees—making it the largest owner of storage facilities in the NYC metro area.

The strategic logic was elegant. New York City has the most supply-constrained self-storage market in America. CubeSmart noted that New York City has the lowest square footage of self storage space per capita of the top 12 metro areas in the U.S., with supply per capita in Queens, Brooklyn and the Bronx less than half the national average. The supply constraints are expected to persist due to restrictions on development in Industrial Business Zones and the recent exclusion of self storage from eligibility for tax abatement under the Industrial & Commercial Abatement Program.

By proving they could close efficiently, paid a fair price and were "generally nice guys," CubeSmart eventually set up talks that resulted in the full acquisition of Storage Deluxe's portfolio. "It was an opportunity to control what we thought was the best self-storage market in the world," Marr said. "An opportunity to change the perception of our company. This was a third of the size of our company at the time."

The deal gives CubeSmart, which changed its name in September from U-Store-It, the opportunity to explode its presence in NYC. "The New York, Miami, Washington D.C., Chicago and Dallas metro areas will be our top five markets upon completion of this acquisition," said Christopher Marr.

Financing Innovation

Funding a $560 million acquisition required creative capital raising. During October 2011, CubeSmart completed a public offering of 23 million common shares at a public offering price of $9.20, receiving approximately $202.5 million in net proceeds. During November 2011, they completed a public offering of 3.1 million Series A preferred shares at a public offering price of $25.00 per share for gross proceeds of $77.5 million. The company used proceeds from both these offerings to pay a portion of the cash purchase price of the Storage Deluxe Acquisition.

The acquisition closed in phases, with 16 of the properties acquired on November 3, 2011 for approximately $357.3 million. The 16 properties purchased were located in New York, Connecticut and Pennsylvania.

This single transaction transformed CubeSmart from a regional Midwest operator into a nationally significant player with the dominant position in America's most valuable storage market.

VII. The 2010s Growth Machine: Organic Expansion & Third-Party Management

Organic Growth

During the 2010s, CubeSmart pursued organic growth by developing new facilities and converting existing properties, expanding its owned store count from 370 in 2011 to 543 by the end of 2020. This expansion included greenfield projects on undeveloped land and adaptive reuse of underutilized structures to meet rising demand in urban and suburban areas. Strategic initiatives in this period focused on enhancing facility quality, with a majority of properties featuring climate-controlled units by mid-2011 to protect stored items from environmental fluctuations.

The focus on climate-controlled units is worth highlighting. Traditional self-storage—the corrugated metal drive-up facility—faces limited pricing power. Climate-controlled units, by contrast, command significant premiums because they protect temperature-sensitive items: electronics, artwork, wine, documents. CubeSmart's shift toward these higher-value units reflected a deliberate strategy to improve revenue per square foot.

Third-Party Management Platform

Perhaps CubeSmart's most innovative strategic initiative during this period was the development of its third-party management platform.

CubeSmart's third-party management platform launched, and the company became the largest storage operator in NYC. CubeSmart Management's platform became the fastest growing in the U.S.

The third-party management platform has been, and continues to be, an important part of portfolio growth and strategy. The company continues to see significant and growing interest from private owners and developers who recognize the benefit of CubeSmart's brand, sophisticated operating platform, real-time reporting, and back-office support.

Importantly, the third-party management platform increases CubeSmart's scale and market penetration, adds a profitable revenue stream, and serves as an attractive pipeline for future acquisition opportunities. This platform, combined with deep industry relationships and disciplined investment process, provides a significant competitive advantage in pursuing external growth objectives.

The beauty of third-party management is its capital efficiency. Rather than deploying billions to acquire properties, CubeSmart can extend its brand and operational expertise to third-party owners for a management fee. This generates steady fee income, spreads technology investments across a larger base, and—critically—creates a warm pipeline for future acquisitions as third-party clients eventually decide to sell.

The REIT was formerly known as U-Store-It but rebranded to CubeSmart in 2011, along with a shift toward enhanced customer service. Today, 89% of owned-store net operating income (NOI) comes from the top 40 MSAs, while CubeSmart's third-party management program and joint ventures provide exposure to secondary and tertiary markets.

As of September 30, 2025, the Company's third-party management platform included 863 stores totaling 56.6 million rentable square feet. During the three and nine months ended September 30, 2025, the Company added 46 stores and 109 stores, respectively, to its third-party management platform.

CEO Transition

In 2013, CubeSmart announced another leadership transition. CubeSmart's Board of Trustees appointed Christopher P. Marr as successor to Dean Jernigan as Chief Executive Officer, effective upon Mr. Jernigan's previously announced retirement on December 31, 2013. Mr. Marr, a self-storage industry veteran, has more than 18 years of real estate investment trust (REIT) executive management experience. Mr. Marr currently served as CubeSmart's President, Chief Operating Officer, and Chief Investment Officer, in which capacity he has led the successful repositioning of the Company's property portfolio.

"My tenure as CEO has been exceedingly rewarding," added Dean Jernigan. "I am proud of our many accomplishments over the past seven years, as we have completely transformed this company's operational infrastructure, property portfolio, balance sheet, and culture. However, I am most proud of the extraordinary team of people that we have at CubeSmart. I have had the great fortune of working with Chris for nearly 20 years, and I cannot think of a more fully-prepared, capable, and deserving person to lead CubeSmart into its next phase of profitability and growth."

During Jernigan's tenure as CEO, the company's market capitalization more than doubled from approximately $2 billion to more than $4 billion.

VIII. Inflection Point #3: COVID-19 & The Storage West Mega-Deal (2020–2021)

Pandemic Tailwinds

The COVID-19 pandemic could have been catastrophic for self-storage—a business dependent on people moving, transitioning, and generally being mobile. Instead, it proved to be an unexpected tailwind.

The self-storage industry reported strong results during the COVID-19 pandemic. This is due to the fact that self-storage is considered to be an "essential business" in many jurisdictions so during a lockdown many facilities never closed and many people were reportedly panic buying storage units to keep valuables safe from contamination.

CubeSmart indicated that self storage fundamentals in New York City have held up well during the pandemic, with occupancy growing through the third quarter. An increase in moves has driven demand higher and the company expects an economic resurgence following the crisis.

The pandemic triggered several demand drivers simultaneously: remote workers needed home office space (prompting decluttering), urban residents fled to suburbs (requiring interim storage), and the housing market's subsequent boom created record transaction volumes.

The NYC Strategy Culmination (2020)

In October 2020, CubeSmart announced what it called the culmination of its decade-long New York City strategy.

CubeSmart described the deal as the culmination of a 10-year strategic plan to set up a market-leading presence in New York City, where the company made a splash in 2011 by purchasing 16 self storage assets as part of a 22-asset, $560 million acquisition from Storage Deluxe. The NYSE-listed real estate investment trust announced that it would purchase the assets totaling 780,425 rentable square feet in Queens, Brooklyn and the Bronx from Storage Deluxe. Following the closing of its latest transaction, the company expanded its portfolio by five properties in Queens, two properties in Brooklyn and one in the Bronx.

The $540 million acquisition brought CubeSmart's total investment in NYC to over $1 billion—an extraordinary concentration in America's most supply-constrained storage market.

Storage West: The Western Expansion

Then came the company's largest acquisition ever.

CubeSmart announced that it has entered into an agreement to acquire 100% of the outstanding partnership units of LAACO, Ltd. ("LAACO"), the owner of the Storage West platform for approximately $1.69 billion, which includes approximately $40.9 million of LAACO debt that will be repaid at, or shortly after, the closing. Storage West is the owner and operator of 59 self-storage assets in the highly desired western markets of Southern California (22), Phoenix (17), Las Vegas (13), and Houston (7).

December 9, 2021 – CubeSmart announced that it has closed on the previously announced acquisition of LAACO, LTD., the owner of the Storage West self-storage platform. With this acquisition, CubeSmart has added 59 high-quality assets to its portfolio in the desirable western markets of Southern California (22), Phoenix (17), Las Vegas (13), and Houston (7).

"We are excited to officially welcome the Storage West stores and the LAACO teammates to CubeSmart's national platform. This accretive transaction represented a unique opportunity to expand our footprint across these rapidly growing top-40 MSAs," commented Christopher P. Marr.

The acquisition was funded using the net proceeds from a combination of capital raising transactions, including the Company's recent offerings of 15,525,000 common shares, $550 million of unsecured senior notes due in 2028, and $500 million of unsecured senior notes due in 2032.

The Storage West deal represented exactly the kind of strategic expansion CubeSmart had been seeking. The western markets—Southern California, Phoenix, Las Vegas—had experienced explosive population growth and faced significant supply constraints. CubeSmart, previously concentrated in the Northeast and Midwest, suddenly had a diversified national footprint with significant exposure to Sunbelt growth markets.

The 59 properties in that portfolio are located in markets where CubeSmart was previously underrepresented—Southern California, Las Vegas, Phoenix, and Houston. The assets have not only enhanced CubeSmart's market share in attractive markets, says Marr, but were complimentary to the stores already owned and effectively helped lift their performance as well.

IX. The CubeSmart Playbook: How They Win

Geographic Focus

Marr, who joined CubeSmart in 2006 as CFO and treasurer and has been CEO since 2014, says the REIT focuses on stronger demographic markets with good existing population growth, high household incomes, and a solid percentage of renters versus owners. "People who rent move more often than people who own, so we have focused historically on the top 40 MSAs and will continue to spend most of our energy focused on those markets," he says.

This focus on demographics over raw growth is crucial. CubeSmart isn't simply chasing the fastest-growing markets—it's targeting markets where the underlying customer base has high incomes, high mobility, and limited alternatives for storage.

Operational Excellence

CubeSmart's operational model generates industry-leading margins. Property operating expenses account for approximately 30% of revenue, while general and administrative expenses represent roughly 6%. Gross margin is 72.30%, with operating and profit margins of 43.48% and 34.20%. This results in net operating income margins of around 70%—extraordinary for any real estate business.

This efficiency stems from several sources: technology investments that enable fewer on-site staff, centralized marketing and revenue management, and the scale to negotiate favorable vendor contracts.

Balance Sheet Strength

CubeSmart ended 2024 with leverage at 4.1x net debt/EBITDA, well below the target range for its current BBB/Baa2 investment grade credit rating. At the end of the year, its well-staggered debt maturity schedule had a weighted-average maturity of 4.4 years, ensuring stability well into the future.

As of Q3 2025, Timothy M. Martin stated, "Our leverage levels remain quite conservative with net debt to EBITDA at 4.7 times at quarter end," providing explicit clarity on balance sheet status.

For context, a net debt-to-EBITDA ratio below 5x is generally considered conservative for REITs. CubeSmart's sub-5x leverage provides significant capacity for opportunistic acquisitions while maintaining investment-grade credit ratings that ensure access to the debt markets.

CubeSmart has increased its dividends for 15 consecutive years. This is a positive sign of the company's financial stability and its ability to pay consistent dividends in the future.

Examining the past 5 years, CubeSmart has maintained an average Dividends Per Share Growth Rate of 8.87%.

Technology & Customer Experience

CubeSmart employs a dynamic pricing strategy that leverages market data to adjust rental rates in response to occupancy levels and seasonal demand fluctuations. This approach helps optimize revenue while maintaining competitive positioning.

A robust technology platform enhances customer experience and operational efficiency, driving online rentals and enabling sophisticated revenue management. The well-recognized brand aids customer acquisition and retention. Furthermore, the rapidly growing third-party management platform provides a capital-light expansion path, leveraging existing infrastructure and expertise to generate fee income.

X. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces

Threat of New Entrants: MODERATE

Self-storage development faces significant barriers in many markets. Supply constraints are expected to persist due to restrictions on development in Industrial Business Zones and the recent exclusion of self storage from eligibility for tax abatement under the Industrial & Commercial Abatement Program.

Municipalities increasingly block new storage construction, preferring retail or industrial developments with higher headcount and tax multipliers. More than 15 U.S. states have enacted moratoria since 2019. Existing operators see occupancy and pricing tailwinds, yet supply constraints hinder new entrants.

However, in less constrained markets, development remains possible for well-capitalized competitors, making this a moderate rather than low threat.

Bargaining Power of Suppliers: LOW

Self-storage facilities require basic construction materials and land. There's no specialized supplier dependency, and labor is not specialized. CubeSmart's scale provides negotiating leverage with vendors across construction, insurance, and maintenance services.

Bargaining Power of Buyers: LOW-MODERATE

Individual customers are fragmented and lack negotiating power. More importantly, once a customer has moved belongings into a unit, switching costs become substantial—the hassle of moving stored items to a competitor facility is typically greater than modest rent increases. This "stickiness" enables regular rent increases for existing customers.

Threat of Substitutes: LOW

Physical items require physical storage. While on-demand storage apps (like MakeSpace or Clutter) have emerged, they remain small relative to traditional self-storage and primarily serve different use cases. The fundamental need for secure space cannot be digitized away.

Competitive Rivalry: HIGH

The self storage market remains a highly fragmented industry, 13,300 owners sharing the national stock. Among them, almost 10,000 are small self storage providers managing less than 100,000 square feet. This diversity, combined with stabilized demand following the pandemic-driven peak and oversupply in some markets, creates a competitive environment.

While it might seem like REITs dominate the self-storage industry, the top six only own roughly 20% of the total square footage and provide third-party management services to another 5% of the market. The remaining properties are still in the hands of independent and regional owners as well as third-party management companies.

Competition isn't primarily between the Big Three REITs—it's between institutional operators and the vast universe of smaller operators. This creates opportunity for consolidation but also ensures ongoing price competition in most markets.

Hamilton's 7 Powers Analysis

Scale Economies: ✅ STRONG

CubeSmart spreads corporate costs across 1,300+ properties. Technology investments in revenue management, marketing platforms, and operational systems are amortized across this massive base. National advertising and vendor negotiations provide cost advantages impossible for single-facility operators to replicate.

Network Economies: ⚠️ MODERATE

Unlike true network businesses, CubeSmart's value doesn't increase exponentially with scale. However, brand recognition across markets enables more efficient customer acquisition, and the third-party management platform creates ecosystem effects where success attracts additional partners.

Counter-Positioning: ✅ STRONG

REITs have structural advantages that mom-and-pop operators cannot match: sophisticated technology, cheap capital, professional management, and national marketing. Smaller operators could theoretically adopt these practices, but doing so would fundamentally transform their business models and economics in ways that would cannibalize their existing operations.

Switching Costs: ✅ STRONG

Moving stored items is time-consuming and expensive. Tenants exhibit strong inertia—the hassle of renting a truck, loading belongings, transporting them to a new facility, and unloading exceeds the savings from modestly lower rent elsewhere. This enables regular rent increases for existing customers without proportionate churn.

Branding: ⚠️ MODERATE

CubeSmart's brand is recognized in key metros, but self-storage is not a high-brand-equity category. Price and location typically matter more than brand, though customer service focus differentiates CubeSmart from commodity storage operators.

Cornered Resource: ⚠️ MODERATE

CubeSmart owns prime real estate locations in supply-constrained markets, particularly the NYC outer boroughs where new development is effectively prohibited. CubeSmart noted that New York City has the lowest square footage of self storage space per capita of the top 12 metro areas in the U.S., with supply per capita in Queens, Brooklyn and the Bronx less than half the national average.

Process Power: ✅ STRONG

Mr. Marr joined the Company in 2006, serving as Chief Financial Officer and Treasurer until November 2008. Prior to joining CubeSmart, Mr. Marr was Senior Vice President and Chief Financial Officer of Brandywine Realty Trust from August 2002 to June 2006. Prior to joining Brandywine Realty Trust, Mr. Marr served as Chief Financial Officer of Storage USA, Inc., a publicly-traded self-storage REIT, from 1998 to 2002.

Leadership brings extensive experience from previous roles, with operational expertise in revenue management, dynamic pricing, and customer acquisition refined over more than two decades. This accumulated know-how is difficult for competitors to replicate quickly.

XI. Bear vs. Bull Case

Bull Case

Industry Consolidation Thesis Remains Intact

The publicly traded self-storage REITs are estimated to own roughly 15% of the storage assets in the United States. Given that the industry remains highly fragmented and there is continually more supply being added via development, there is plenty of consolidation left to be had for the storage REITs. REITs are also superior operators, which can achieve approximately 50-200 basis points of NOI upside out of assets that were previously run by smaller, less sophisticated operators. Thus, not only is there more opportunity to consolidate but there is ample operational upside to go along with it.

If the Big Three REITs can grow their combined market share from ~20% to ~50% over the next decade—a reasonable projection given current trends—the acquisition runway remains substantial.

Supply Constraints Tightening

Climate-controlled builds now require USD 35–70 per sq ft, squeezing project returns amid cap-rate expansion to 5.9% in 2024. Rising interest rates compound capital intensity, causing a 14% decline in construction starts late-2024. Smaller operators lacking procurement scale face margin compression, accelerating portfolio roll-ups by well-capitalized REITs.

Rising construction costs and municipal restrictions on new development protect existing operators from competitive supply additions—a significant tailwind for incumbent operators.

Dividend Yield Attractive

CubeSmart has an annual dividend of $2.08 per share, with a yield of 5.51%. The dividend is paid every three months.

At current prices, CubeSmart offers a compelling yield relative to alternatives, supported by a 15-year track record of consecutive dividend increases.

Operational Momentum Improving

As CEO Christopher Marr stated on Q3 2025 earnings call: "It was a very solid third quarter for CubeSmart, which resulted in guidance increases across our key same-store and earnings metrics. Across all markets, our existing customer KPIs remain strong with key credit and attrition metrics remaining consistent within historical normal ranges. We are continuing to feel diminishing headwinds from new supply as the stores placed in service over the last three years lease up and the forward pipeline continues shrinking."

Bear Case

Oversupply Risk in Select Markets

While supply constraints exist in many markets, certain Sunbelt metros have experienced significant new development. Regional Performance showed that Mid-Atlantic and Northeast urban markets continued to outperform, while the East Coast of Florida stabilized and several Sunbelt markets remained challenged by supply and demand uncertainties.

CubeSmart's Storage West acquisition concentrated exposure in precisely these Sunbelt markets, creating potential headwinds.

Interest Rate Sensitivity

Since 2022, REIT performance has generally moved inversely to changes in the 10-year Treasury yield. In the third quarter of 2024, REITs delivered strong total returns as the 10-year Treasury yield declined. However, since the end of the third quarter, a notable rise in the 10-year Treasury yield has caused REIT total returns to decline. If this inverse relationship continues, interest rates will remain a key factor in the valuation adjustment process.

Rising rates compress REIT valuations and increase the cost of acquisition financing, potentially slowing the consolidation story.

Competitive Intensity Among REITs

Extra Space Storage is the largest player in the U.S. self-storage sector after buying rival Life Storage in a $15 billion deal in 2023. In mid-2025, it had almost 4,180 properties in 43 states, with more than 321.5 million square feet of rentable space. It controlled 15% of the U.S. self-storage market, which was the largest share in the sector.

Extra Space's Life Storage acquisition created a significantly larger competitor with greater scale advantages. Public Storage, with its massive balance sheet and dominant brand, remains a formidable competitor. CubeSmart's smaller size relative to peers means new store additions could have more significant impact on overall performance, but also less margin for error.

Payout Ratio Concerns

CubeSmart's payout ratio is 132.52% which means that 132.52% of the company's earnings are paid out as dividends. A high payout ratio may indicate that the company is returning most of its earnings to shareholders.

For REITs, which are required to distribute most taxable income, payout ratios above 100% of GAAP earnings are common because non-cash depreciation reduces reported earnings below cash flow. However, sustained high payout ratios relative to FFO could constrain dividend growth or acquisitions if operating performance weakens.

XII. Critical KPIs for Investors to Track

For investors monitoring CubeSmart's ongoing performance, three key metrics stand out:

1. Same-Store Revenue Growth

This measures organic revenue growth from properties owned for comparable periods, excluding the impact of acquisitions. Same-store revenue growth reflects pricing power, occupancy trends, and the company's ability to raise rents on existing customers—the fundamental drivers of value creation. Same-store NOI declined 0.8%, with revenues decreasing 0.4% and operating expenses increasing 0.6% in Q1 2025. Watching this metric's trajectory reveals whether operational trends are improving or deteriorating.

2. Occupancy Rate

Physical occupancy measures the percentage of rentable square feet that is leased. The industry typically targets 90%+ occupancy; CubeSmart has historically operated in the 89-93% range. Occupancy below this range suggests either oversupply in key markets or competitive pressure from rival operators. The company's same-store occupancy slipped to 89.7% from 90.3% a year earlier.

3. Third-Party Managed Store Count

The growth of CubeSmart's third-party management platform serves as both a leading indicator of future acquisition opportunities and a measure of the company's competitive positioning. Healthy growth in managed stores suggests CubeSmart's platform is winning against competitors for third-party management contracts. CubeSmart added 46 sites to its third-party management platform during Q3 2025. The company now manages 863 facilities for other owners.

XIII. Conclusion: The Quiet Compounder

CubeSmart's journey from a Cleveland-based family business to a $10 billion national REIT encapsulates several lessons about value creation in real estate.

First, boring businesses can be excellent investments. Self-storage lacks the glamour of trophy office buildings or the growth narrative of data centers. But its persistent demand drivers, high operating margins, and capital efficiency have generated exceptional returns over time.

Second, professional management and patient capital can transform fragmented industries. The self-storage sector's extreme fragmentation created opportunity for institutional operators to acquire properties, improve operations, and generate value through consolidation—a playbook CubeSmart executed across two decades.

Third, strategic focus matters. CubeSmart's deliberate exit from weak Midwest markets and concentration in supply-constrained metros like New York City created a higher-quality portfolio that generates superior returns per square foot.

Fourth, conservative financial management provides optionality. CubeSmart's modest leverage and investment-grade credit rating ensure the company can pursue acquisitions when opportunities arise while maintaining dividend growth through economic cycles.

CubeSmart revenue for the twelve months ending September 30, 2025 was $1.108 billion, a 4.19% increase year-over-year. CubeSmart annual revenue for 2024 was $1.066 billion, a 1.51% increase from 2023. CubeSmart annual revenue for 2023 was $1.05 billion, a 4.03% increase from 2022.

The company now stands at an inflection point. Post-pandemic normalization has moderated the extraordinary growth rates of 2020-2022. Rising interest rates have compressed REIT valuations broadly. And competition among institutional operators—particularly following Extra Space's acquisition of Life Storage—has intensified.

But the fundamental consolidation thesis remains intact. One aspect of this huge transaction that everyone can agree on is the inevitability of more consolidation for the self-storage industry. "This has been ongoing since I've been in the business for 30 years, and will continue for the foreseeable future, as there is still significant fragmentation in our industry," says Ricky Jenkins. Consolidation is a primary avenue for the REITs to grow, particularly because they tend to focus on acquisitions and management contracts over ground-up projects.

For long-term investors, CubeSmart offers a compelling combination: exposure to an essential industry with persistent demand drivers, managed by an experienced leadership team with decades of track record, generating consistent dividend income while maintaining the balance sheet strength to pursue strategic growth.

It may never generate the headlines of a fast-growing technology company or the excitement of a turnaround story. But in a world of increasingly speculative investment narratives, there's something to be said for a business that simply stores people's stuff—and prints cash while doing it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube