ITT Inc.: From Telephone Empire to the Ultimate Conglomerate to Focused Industrial Champion

I. Introduction & Episode Roadmap

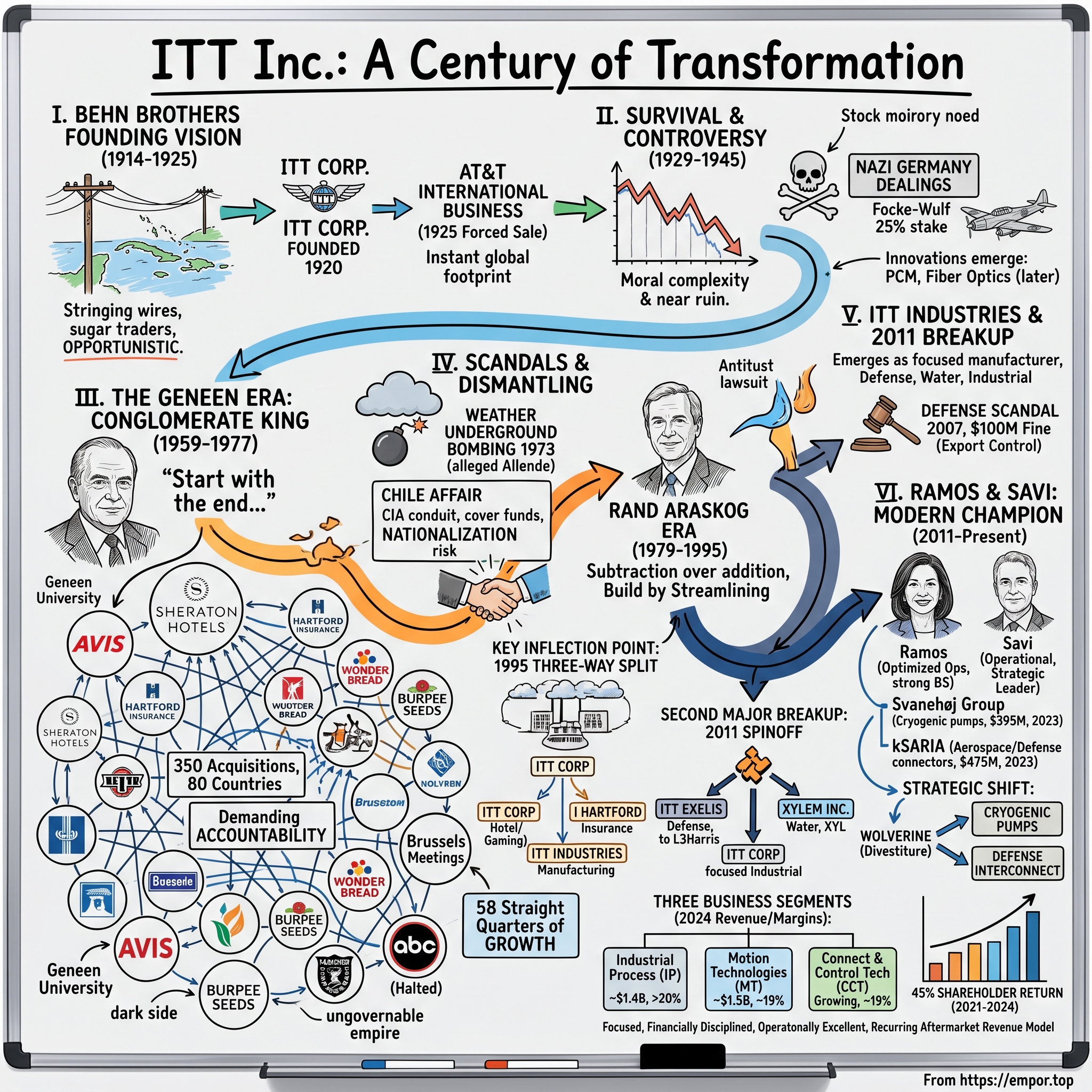

Picture this: A company founded in 1920 to string telephone wires across the Caribbean becomes, within five decades, the fourth-largest employer in the United States—owning everything from Sheraton hotels to Wonder Bread to a significant stake in a Nazi fighter plane manufacturer. Then, through a series of dramatic breakups and reinventions, it emerges in the 2020s as a sleek, $13+ billion market cap industrial powerhouse making brake pads, pumps, and aerospace connectors.

If business history were a novel, ITT would be its most improbable protagonist.

ITT Inc. was incorporated in 1920 and is headquartered in Stamford, Connecticut. What started as International Telephone & Telegraph—a name deliberately chosen to mimic the mighty AT&T—has lived through enough corporate drama to fill several seasons of a prestige television series: dealings with Adolf Hitler, CIA entanglements in Chile, one of the most aggressive acquisition sprees in American history, hostile takeover battles, and not one but two company-splitting spinoffs that scattered pieces of the original empire across the corporate landscape.

In 2024, ITT Inc.'s revenue was $3.63 billion, an increase of 10.59% compared to the previous year's $3.28 billion. Earnings were $518.30 million, an increase of 26.26%. The company that once owned Hartford Insurance, Sheraton Hotels, and Avis Rent-A-Car now makes its money from three focused segments: Industrial Process (pumps and valves), Motion Technologies (brake components and shock absorbers), and Connect & Control Technologies (aerospace and defense connectors).

ITT's differentiation—which has powered a total shareholder return of 45% from 2021-2024—is driven by execution, innovation and now, M&A. A combination of organic growth and margin expansion, along with an anticipated $500 to $700 million per year towards highly strategic acquisitions, are expected to drive the next chapter of value creation at ITT.

The thesis of this story is deceptively simple yet profoundly instructive: ITT's century-long journey represents a masterclass in conglomeration, de-conglomeration, and the power of strategic focus. Every business school case study about diversification, every debate about whether conglomerates create or destroy value, every lesson about the importance of management clarity—ITT has lived all of it, sometimes triumphantly, often painfully, always instructively.

What we're witnessing today is the third act of a company that has reinvented itself more dramatically than perhaps any other American corporation. And the current chapter, under CEO Luca Savi's leadership, may prove to be its most valuable yet.

II. The Behn Brothers & Founding Vision (1914-1925)

The story begins not in a corporate boardroom but in the sugarcane fields of the Caribbean. Sosthenes Behn was born in the island of St. Thomas, then part of the Danish West Indies. His ancestry was an improbable European cocktail—Danish on his paternal side, French on his maternal side—and his path to telecommunications pioneer was anything but direct.

Educated on the island of Corsica and in Paris, Behn began his career in 1901 with a New York City bank. In 1906, Behn and his brother Hernand took over a sugar business in Puerto Rico and snapped up a small and primitive local telephone company by closing in on a mortgage. Realizing the potential of the telephone, Behn began to buy up more companies in the Caribbean.

This was classic entrepreneurial opportunism. The Behn brothers weren't telecommunications visionaries who dreamed of connecting the world—they were sugar traders who saw a distressed asset and pounced. But Sosthenes Behn possessed something that would define ITT's first half-century: audacious international ambition. While American competitors focused on the domestic market, Behn looked at the underdeveloped telephone systems of Latin America and Europe and saw opportunity.

He became a United States citizen in 1913. In World War I, he was commissioned a Captain in the Signal Corps, later rising to the rank of Lieutenant Colonel. He served as chief of staff for General George Russell and also commanded the 232nd Field Signal Battalion, at Château Thierry, St. Mihiel, Argonne. His wartime service gave him two crucial assets: deep knowledge of military communications technology and, equally important, a Rolodex of contacts that would prove invaluable when navigating the corridors of power on both sides of the Atlantic.

In 1920, Behn's work in the field of cables enabled him and his brother to set up the International Telephone and Telegraph Corporation (ITT), with $6 million paid in capital. The name wasn't accidental—it was aspirational imitation. AT&T was the colossus of American telecommunications, and the Behn brothers wanted to signal that their company would be its international counterpart. The branding worked, conferring immediate credibility on what was still essentially a Caribbean phone operation with grand ambitions.

In 1924, the brothers expanded into Europe, gaining the right to operate the phone system in Spain. The next year, under pressure from the US government to abandon its overseas business, AT&T sold its European phone manufacturing business to ITT. This was a pivotal moment. The forced sale of AT&T's International Western Electric Company to ITT—subsequently renamed ITT Standard Electric Corporation—instantly made the Caribbean upstart a major telecommunications manufacturer across eleven countries.

The Behns soon became the chief telephone service provider in Britain, France, and Germany and expanded into Latin America. By the mid-1920s, a company founded on a foreclosed Puerto Rican phone system had become a genuinely international enterprise with operations spanning three continents.

The Behn brothers' strategy was built on a fundamental insight that would echo through ITT's history: governments were often the gatekeepers to telecommunications markets, and success required political sophistication as much as technical expertise. Sosthenes Behn cultivated relationships with political leaders, adapted his operations to local conditions, and showed remarkable flexibility in working with whatever regime held power—a trait that would later create enormous controversy.

When Behn retired, ITT employed, through 100 subsidiaries around the world, over 40,000 people and was doing an annual business in excess of $500 million. From sugar trading to global telecommunications giant in three decades—the Behn era established ITT as a company willing to go where opportunities led, regardless of borders, and to build through acquisition rather than solely through organic growth.

But this international presence would soon create complications that Sosthenes Behn could never have anticipated when he first glimpsed the potential in that bankrupt Puerto Rican phone company.

III. Surviving the Great Depression & World War II (1929-1945)

The 1930s tested ITT's international model in ways that nearly destroyed the company. The growth of the 1920s had been funded by high debt, and when the Great Depression hit, it threatened ITT's very existence. Foreign governments, desperate to conserve hard currency, blocked profits earned in their countries from returning to the United States. Suddenly, ITT had assets strewn across the globe but couldn't access their earnings.

The onset of the depression in 1931 brought financial difficulties, but Behn's skillful handling of the firm's indebtedness enabled ITT to survive and grow. Hernand died in 1933, leaving his brother in full control.

The company's survival during this period owed much to an uncomfortable reality: foreign operations were run by foreign nationals who had well-placed individuals on their boards with the clout to keep the company alive. This decentralized structure—which would later become central to Harold Geneen's management philosophy—originated as a survival mechanism during a period when American ownership of overseas assets was increasingly precarious.

Then came the most controversial chapter in ITT's history.

According to Anthony Sampson's book The Sovereign State of ITT, one of the first American businessmen Hitler received after taking power in 1933 was Sosthenes Behn, then the CEO of ITT, and his German representative, Henry Mann. ITT, through its subsidiary C. Lorenz AG of Berlin, owned 25% of Focke-Wulf, the German aircraft manufacturer, builder of some of the most successful Luftwaffe fighter aircraft.

Sosthenes Behn met with Hitler on August 3, 1933, and in 1936 there was a high-level meeting in Berlin. During the war, all of ITT's German holdings were put under Nazi control. These included a minority share in airplane manufacturer Focke-Wulf, which ITT had acquired through its contacts with German financier Kurt Baron von Schröder. After the end of the war, the US authorities returned these assets to their rightful US owner.

The moral complexity here is staggering. ITT's German subsidiaries produced equipment used by the Wehrmacht. Focke-Wulf built some of the Luftwaffe's most effective fighter aircraft. Yet Behn apparently maintained some connection to these operations even after America entered the war, working through Swiss intermediaries and German nationals on ITT's boards.

He was known to not only help the United States war cause during World War II, but also with his holdings in Axis countries, the opposing forces as well. Regardless of that fact, on February 16, 1946, Major General Harry C. Ingles, Chief Signal Officer of the United States Army, acting on behalf of President Harry S Truman, presented the Medal of Merit, at that time the nation's highest award to a civilian, to him. Ironically a few years later he received millions of dollars in compensation for war damage to his German plants in 1944.

In the 1960s, ITT won $27 million in compensation for damage inflicted on its share of the Focke-Wulf plant by Allied bombing during World War II. American planes had bombed factories owned by an American company that were producing planes that killed American pilots—and then American taxpayers compensated the American company for the damage. The absurdity was not lost on critics.

Amid this darkness, ITT also contributed genuinely important technological innovations. Alec Reeves, an ITT employee in France in the 1930s, developed pulse-code modulation (PCM) innovations, upon which future digital voice communication was based. Later, Charles K. Kao, working at ITT's subsidiary STC in the UK, pioneered the use of optical fiber from 1966—work for which he was awarded the 2009 Nobel Prize in Physics.

The near-ruin of the Depression years and the threat of nationalization in several countries convinced Behn to focus on domestic business after the war. This strategic pivot would set the stage for the company's most remarkable era—one led not by the founding family but by an accountant from Bournemouth, England, who would transform ITT into something the Behn brothers never imagined.

IV. Enter Harold Geneen: The Conglomerate King (1959-1977)

Harold Sydney Geneen arrived at ITT in 1959, and nothing about the company would ever be the same.

Harold "Hal" Sydney Geneen (January 22, 1910 – November 21, 1997), was an American businessman most famous for serving as president of the ITT Corporation. Geneen was born on January 22, 1910, in Bournemouth, Hampshire, England. His father was Russian-Jewish, and his mother was an Italian Roman Catholic. He migrated to the United States from England as an infant and later studied accounting at New York University.

Although he appeared in his ITT years as the completely self-confident leader who could not possibly fail, Geneen actually had a lonely childhood and years of painful struggle before he was able to seize the brass ring at ITT. Geneen even had to earn his college degree by attending night classes over an eight-year period. But his experience at a public accounting firm and several major companies finally brought him to the opportunity at ITT.

Between 1956 and 1959 he was senior vice president of Raytheon, developing his management structure, allowing a large degree of freedom for divisions while maintaining a high degree of financial and other accountability.

He grew the company from a medium-sized business with $765 million sales in 1961 into an international conglomerate with $17 billion sales in 1970. He extended its interests from manufacturing of telegraph equipment into insurance, hotels, real estate management, and other areas. Under Geneen's management, ITT became the archetypal modern multinational conglomerate.

The numbers are almost impossible to process. When Geneen took the helm of ITT, it had annual sales of about $700 million; by the time he left the company, he had turned it into the eleventh largest corporation in the United States, with sales of $17 billion. Profits soared from $29 million to $550 million. Along the way, ITT acquired some 250 companies in more than eighty countries.

ITT grew primarily through a series of approximately 350 acquisitions and mergers in 80 countries. Some of the largest of these were Hartford Fire Insurance Company (1970) and Sheraton Hotels.

The deals became legendary: Avis, the car rental company; Continental Baking, which made Wonder Bread; Burpee, which sold seeds to gardeners; and hundreds of others. In 1965, ITT attempted to purchase the ABC television network for $700 million. The deal was halted by federal antitrust regulators who feared ITT was growing too large. Undeterred, ITT moved to acquire companies outside the telecommunications industry to continue its growth without violating antitrust legislation.

What made Geneen's ITT remarkable wasn't just the pace of acquisitions—it was the management system he created to control his sprawling empire.

His accounting background gave him a strong faith in the power of numbers to provide an accurate picture of economic performance, and he devoted much of his time to meeting with various leaders in the company, attempting to discern what he called the "unshakable facts" regarding each division. Management meetings, held in Brussels, Belgium, on the last Monday of each month, ran for four days and took place in a room with the curtains drawn. Top managers representing ITT's various holdings around the world would present progress reports, and then would be subjected to a withering series of questions by the CEO.

The Brussels meetings became the stuff of corporate legend. Managers would fly in from around the world, knowing that Geneen had read their reports with terrifying thoroughness. The pressure was relentless. Geneen believed that managers should never be surprised by events—strikes, shortages, economic shifts—that they hadn't anticipated in their planning. The cardinal sin at ITT was being caught off guard.

Hard work, efficient planning, close attention to certain details and unwavering pursuit of specific business goals were the elements of his great success. There was no way that Geneen himself could have fully grasped the products and operations of the 250 profit centers in the ITT tent, but he managed to control this empire by demanding careful planning from his managers and holding them accountable for hitting growth and profit targets. The cardinal sin for an ITT manager was to be surprised by events such as strikes and shortages which he had not anticipated in his previous planning. Geneen, a financial executive in his earlier years, devotes a complete chapter to the importance of "The Numbers" in managing a business.

He managed to produce fifty-eight straight quarters of earnings growth, an impressive record by any standard. That's nearly fifteen years of unbroken quarterly earnings increases—a feat that required not just good management but also, inevitably, some creative accounting and deal-making.

ITT had over 250 profit centres and employed half a million people in 4 continents. ITT also became known as the Geneen University for his consistent delivery of positive commercial results.

Geneen's philosophy was elegantly summarized in his own words: "You read a book from beginning to end. You run a business the opposite way. You start with the end, and then you do everything you must to reach it."

But there was a darker side to the Geneen era. The result was a corporation that in 1979 had 370,000 employees in more than 100 countries. Among its multitude of ventures, ITT was manufacturing radar in Los Angeles, television sets in West Germany, shock absorbers in The Netherlands and radios in Zimbabwe, and helping Egypt to rebuild Cairo's water-treatment system.

The empire had grown so large, so diverse, and so debt-laden that it was becoming ungovernable by anyone other than Geneen himself. And Geneen, for all his brilliance, was not immortal.

V. Controversy & Political Scandals (1970s)

The 1970s marked the moment when ITT's international reach became a geopolitical liability. The same flexibility that allowed the company to operate across dozens of countries—adapting to local political conditions, working with whatever regime held power—now drew it into scandals that would define the era's debates about corporate power.

In 1970, the U.S. manufacturing company ITT Corporation owned 70 percent of Chitelco, the Chilean Telephone Company, and funded El Mercurio, a Chilean right-wing newspaper. The CIA used ITT as a conduit to financially aid opponents of Allende's government.

ITT had some $200 million-worth of investments in Chile. Under Geneen's leadership, ITT funneled $350,000 to Allende's opponent, Jorge Alessandri.

The situation escalated dramatically after Salvador Allende won the Chilean presidential election. Almost immediately after the election, Henry Kissinger, then national security adviser to President Richard M. Nixon, developed a program at the CIA to prevent Allende from coming to power. At the September 9, 1970, board of directors meeting of ITT, Harold Geneen, ITT's chief executive officer, informed the board that Chiltelco, a telephone company in Chile in which ITT had a substantial stake, was in danger of being nationalized if Allende were elected.

At the very least, it is now definitively established that ITT officials covertly funneled some $350,000 in corporate funds to right wing opponents of the late Dr. Allende in the fall of 1970, a fruitless operation carried out with the advice of the CIA.

When Allende was overthrown and died in the September 11, 1973 military coup led by General Augusto Pinochet, ITT's involvement became a subject of intense scrutiny. On 28 September 1973, ITT's headquarters in New York City were bombed by the Weather Underground for the alleged involvement of the company in the overthrow of Allende.

When Harold Geneen, the former chairman and CEO of ITT, died, the obituaries invariably singled out the same large aspects of his public life: his unprecedented capacity for work, his relentless campaign to increase the size of ITT through acquisitions, his prominence as an advocate and practitioner of the corporate conglomerate, his overreaching in attempts to influence the Antitrust Division of the Department of Justice, and his offers of money to the CIA to overthrow the election of Salvador Allende as president of Chile.

The Chile affair wasn't ITT's only brush with political scandal. The company became involved in controversy related to the 1972 Republican National Convention. In May 1971, ITT president Geneen pledged $400,000 to support a proposal to hold the convention in San Diego; only $100,000 of the contribution was publicly disclosed. When newspaper columnist Jack Anderson disclosed an interoffice memo from ITT lobbyist Dita Beard that appeared to draw a connection between ITT's contribution and a favorable settlement of an antitrust lawsuit, the resulting scandal threatened to engulf the Nixon administration.

In the 1970s, however, Geneen became tagged as "controversial" by an often hostile press. Critics gleefully pounced on the company's political contributions and alleged involvement in the overthrow of Chile's Allende government to discredit both Geneen and ITT. In this tumultuous period, Geneen was usually too busy running his company to explain himself to the public.

ITT under Geneen was a prototype for the international conglomerate at a time when such an entity had yet to be comprehended by the leadership of even the largest corporations. As such, it possessed both the strengths and the shortcomings embodied in the phrase "multinational corporation." In the 1960s and early 1970s the company was a powerful player on the national and international stages; but, as symbols of international capitalist influence, Geneen and ITT were targets of scorn among left-wing political activists of the era.

The scandals didn't bring down ITT—the company was too large, too diversified, too deeply embedded in too many economies to fail. But they tarnished its reputation and, more importantly, they signaled that the freewheeling era of conglomerate expansion was coming to an end. Regulators, politicians, and the public were beginning to question whether corporations like ITT had grown too powerful, too opaque, and too willing to interfere in the affairs of sovereign nations.

When Geneen finally stepped down, the bill for his empire-building would come due.

VI. The Araskog Era: Dismantling the Empire (1979-1995)

Rand Vincent Araskog (October 31, 1931 – August 9, 2021) was an American manufacturing executive, investor, and writer who was the CEO of ITT Corporation. During his time as the CEO between 1979 and 1998 he was known for divesting the conglomerate of multiple businesses including hotels, rental cars, and insurance to retain its focus on its core telecom businesses.

Rand Vincent Araskog was born on October 30, 1931, in Fergus Falls, Minnesota in a family of Swedish descent. His father was a tax collector and a dairy farmer in the town. He was elected as a valedictorian in his school and went on to the United States Military Academy at West Point where he graduated in 1953, majoring in Soviet studies. He graduated from Harvard University majoring in Russian studies and spent a year in West Germany serving at a US Army intelligence post. Araskog started his career working for the Defense Department at the Pentagon and the National Security Agency.

The contrast with Geneen could not have been starker. Where Geneen was a night-school accountant who clawed his way up through corporate America, Araskog was a West Point man with intelligence credentials. Where Geneen built through relentless acquisition, Araskog would build by subtraction.

When Rand Araskog took over as head of ITT in 1979, revenues had been climbing throughout the decade, but the debt was $4 billion.

When Araskog took over in 1979, he found the company burdened with debt. So he went on a huge divestiture program and has now shed more than 250 operations, including Continental, Avis and Rayonier.

The decision to streamline ITT was a long time coming, partly because Geneen was a long time going. He turned 65 in 1975 but was reluctant to retire. Staying on as chairman, he installed an heir apparent, Lyman Hamilton, as chief executive officer in 1978. But after Hamilton started planning a big reorganization, Geneen sacked him. When Geneen finally turned over the chairmanship to Araskog in 1980, he kept a seat on the board of directors.

Some Wall Streeters believe it was not until Geneen left the board in May 1983 that Araskog, a West Point graduate who grew up on a Minnesota farm, could assume full command. The clearest signal that he was committed to major divestitures came last August, when ITT sold Continental Baking, which makes Wonder bread and Twinkies, to Ralston Purina for $475 million.

One reason for the poor performance was that the company's $8 billion debt, largely a legacy of the Geneen years, generated an annual interest bill of more than $600 million.

His early years were spent building the group's telecom business, including developing the ITT System 12, an early stage digital telephone exchange, before selling the business to French state-owned company Generale d'Electricite in 1986.

The divestiture of the core telecommunications business in 1986 was symbolic. The company that had been founded to build a global telephone network was now getting out of telephones entirely. ITT had become a holding company for a collection of businesses that shared nothing but common ownership.

ITT's proposed breakup also climaxes a 16-year effort by Rand V. Araskog, ITT's chairman, to disassemble the far-flung empire built by Harold S. Geneen, who as chairman turned a little overseas telephone company called International Telephone & Telegraph Corp. into a titan of American business. (ITT adopted its current name in 1983.)

He continued to spend the remainder of his time as the CEO in divesting the vast conglomerate as investors were vying for focus on its core businesses. He saw off a hostile takeover bid by Hilton Hotels corporation but agreed to sell the group's hotel businesses under the Sheraton brand to Starwood Hotel & Resorts Worldwide, Inc. in 1997. He retired from the company in 1998.

The culminating moment came in 1995, when Araskog orchestrated a three-way split of ITT into separate public companies. The spinoff continues a trend among conglomerates to divest some businesses or narrow their focus. Sears, Roebuck & Co., for instance, spun off Allstate Corp., and Stamford-based Xerox Corp. sold its Crum and Forster insurance business.

A 32-year veteran of ITT, Mr. Araskog was the catalyst in the 1995 separation of ITT into three individual publicly traded companies.

The three new companies were: - ITT Corporation: focused on hotel and gaming businesses (Sheraton, Caesars) - ITT Hartford: stand-alone insurance operation - ITT Industries: collection of manufacturing companies including defense electronics, pumps, and connectors

When the announcement finally came, investors cheered the move and boosted ITT's stock price $6.25 a share, to $115.50, in New York Stock Exchange composite trading. "This is going to make three much stronger entities," said an analyst at Fitch Investors Service.

The market's reaction validated what Araskog had spent sixteen years arguing: Geneen's empire was worth more in pieces than as a whole. The conglomerate discount—the persistent undervaluation of diversified companies whose various businesses obscured each other's value—had become ITT's albatross.

In 1997, ITT Corp. completed a merger with Starwood, which wanted to acquire Sheraton Hotels and Resorts. By 1999, ITT Corp. had dropped the ITT name entirely in favor of Starwood. The Hartford changed its name. Only ITT Industries retained the historic ITT brand—and would continue the company's transformation toward its modern form.

VII. ITT Industries Emerges (1996-2010)

From the ashes of the Geneen conglomerate, ITT Industries emerged as a focused manufacturer with an identity crisis. The company had inherited an eclectic collection of businesses—defense electronics, pumps, connectors, shock absorbers—that shared engineering excellence but not much else. The challenge was to forge these disparate operations into a coherent whole.

In 1996, the current company was founded as a spinoff of ITT as ITT Industries, Inc. It later changed its name back to ITT Corporation in 2006, reclaiming the historic brand after Starwood had abandoned it.

A decade after the 1995 breakup, the landscape had shifted dramatically. ITT Hartford had changed its name to The Hartford Financial Services Group. The hospitality-focused ITT Corporation had been absorbed into Starwood. Only ITT Industries continued its transformation, playing an important role in several vital markets: water treatment and fluids management, global defense and security, and motion and flow control.

But the defense business would become both ITT's largest segment and its most troublesome.

In March 2007, ITT Corporation became the first major defense contractor to be convicted for criminal violations of the U.S. Arms Export Control Act. The fines resulted from ITT's outsourcing program, in which they transferred night vision goggles and classified information about countermeasures against laser weapons to engineers in Singapore, the People's Republic of China, and the United Kingdom.

The company was fined $100 million although they were also given the option of spending half of that sum on research and development of new night vision technology, with the U.S. government assuming rights to the resulting intellectual property. The investigation found that the corporation had gone to significant lengths to circumvent export rules, including setting up a front company.

The conviction highlighted a fundamental tension within ITT. The defense business was profitable and growing, but it operated in a heavily regulated environment where the company's entrepreneurial instincts—its willingness to push boundaries, to move fast, to find workarounds—could lead to catastrophic legal exposure.

By 2010, ITT was generating approximately $11 billion in annual revenue across three segments: Defense & Information Solutions (the largest, at roughly $6 billion), Fluid & Motion Control (the original industrial heritage), and Water Technology (a growing market with sustainability tailwinds).

But the very structure that had emerged from the Araskog breakup was now creating problems. The low-growth defense business—which generated more than half of the company's revenues and operating income—was weighing down the valuation of the higher-growth water and industrial engineering businesses. Investors looking for water infrastructure plays didn't want defense exposure. Defense investors didn't want industrial cyclicality. Everyone agreed the pieces were valuable; no one could agree on how to value the whole.

The stage was set for another transformation.

VIII. Key Inflection Point: The 2011 Spinoff – Birth of Modern ITT

On January 11, 2011, ITT Corporation's board of directors made a decision that would reshape the company more fundamentally than anything since Geneen's acquisition spree: they voted unanimously to split the company into three distinct, publicly traded entities.

On January 11, 2011, the Board of Directors of ITT Corporation approved a plan to separate ITT into three independent, publicly traded companies. Under the plan, ITT would execute tax-free spin-offs of its Defense and Information Solutions business, Exelis Inc., and its water-related businesses, Xylem Inc. Following completion of the transaction, ITT will continue to trade on the New York Stock Exchange as a highly engineered industrial products company that supplies solutions in the aerospace, transportation and energy markets. Immediately following the completion of the spin-offs, ITT shareholders will own all of the outstanding shares of common stock of Exelis and Xylem. We believe that this separation is in the best interest of our company and its constituents, as these three businesses are well-positioned to create significant value for shareholders as standalone companies.

Upon completion of the spinoffs, the future water company will be named Xylem and the future defense company will be named ITT Exelis. ITT's core industrial business will continue under the ITT Corporation name.

Upon completion of the planned separation, the future water company will be named Xylem ('zi-lem) and will consist of the Water & Wastewater, Residential & Commercial Water and Flow Control businesses. The name Xylem, derived from classical Greek, is the tissue that transports water in plants. It signifies the company's unique position in the marketplace as a leading equipment and service provider of a broad product line that addresses the full cycle of water.

Following completion of the planned separation, the future defense company will be named ITT Exelis and will be a leader in Command, Control, Communications, Computers, Intelligence, Surveillance and Reconnaissance (C4ISR) related products and systems. ITT Exelis is an energetic name that is derived from the word "excel," which is rooted in "ex," meaning "out in front" or "beyond."

The new ITT would have pro forma sales of approximately $2.1 billion, while the defense company (Exelis) would have sales of about $5.8 billion and the water technology business (Xylem) would generate roughly $3.6 billion. ITT's stock climbed 17 percent on the announcement—the market clearly believed the pieces were worth more than the whole.

Each ITT shareholder of record as of the close of business on October 17, 2011, the record date for the distribution, will receive on the distribution date one share of ITT Exelis common stock and one share of Xylem common stock for each share of ITT common stock held as of the record date.

Following the spinoffs, all three companies will be listed on the New York Stock Exchange. ITT shares will continue to trade on the NYSE under the ticker symbol "ITT." ITT Exelis shares will trade under the symbol "XLS," while Xylem shares will trade under the symbol "XYL."

The financial engineering behind the split was sophisticated. The new ITT emerged debt-free, shifting all of its debt to the other two spin-offs. Xylem took on $1.2 billion of debt and Exelis $890 million. The new ITT also transferred a majority of the company's pension obligations onto Exelis, which had pension liabilities estimated at $1.7 billion underfunded. The one liability retained by the new ITT was asbestos liability, estimated at $707 million—a legacy of decades of industrial manufacturing.

On October 31, 2011, ITT Corporation spun off its defense and water technology businesses to form three separate, publicly traded companies: Exelis Inc., a global aerospace, defense, information and services company headquartered in Tysons Corner...

Exelis was acquired by the Harris Corporation for $4.75 billion in 2015. Harris later merged with L3 Technologies to form L3Harris Technologies. Xylem (NYSE: XYL) thrived as an independent water technology company and is now a $30+ billion market cap enterprise.

And ITT? The $2 billion industrial rump that retained the historic name? It would embark on a remarkable journey of its own.

Denise L. Ramos, who will become ITT's chief executive officer and president effective upon the completion of the spinoffs and who is currently ITT's chief financial officer.

The appointment of Denise Ramos as CEO signaled the kind of company ITT intended to become: focused, financially disciplined, and operationally excellent. Ramos, a CFO by background with experience at KFC, Yum! Brands, and Furniture Brands International, would bring the same financial rigor to the CEO role that she had applied to ITT's balance sheet.

The 2011 spinoff was ITT's second major breakup in sixteen years. But where the 1995 split had been about escaping the conglomerate discount, the 2011 separation was about enabling strategic focus. Each of the three new companies could now pursue strategies appropriate to their markets, attract investors who understood their businesses, and create compensation structures that aligned management with performance.

For the new ITT, that meant becoming the best possible version of a focused industrial manufacturer.

IX. The Ramos & Savi Era: Building the Modern Champion (2011-Present)

Frank MacInnis, Chairman of ITT's Board of Directors, said: "Denise's leadership over the past seven years has been outstanding as she has successfully driven the creation of a company distinguished by its strong performance, attractive portfolio of businesses, robust balance sheet and intense commitment to building a vibrant culture.

Under her tenure as CEO, market capitalization for the company increased nearly three times to more than $5 billion.

Ms. Denise L. Ramos has been the Chief Executive Officer and President at ITT Corporation since 2011. She served as the Chief Financial Officer and Senior Vice President of ITT Corporation since July 1, 2007. She was responsible for all aspects of financial management and reporting for the global multi-industry company.

Ramos inherited a company that had been stripped of its defense and water businesses but retained a strong foundation in industrial manufacturing. Her approach was methodical: optimize operations, strengthen the balance sheet, and position the company for eventual growth through M&A. It was classic CFO-turned-CEO strategy—get the house in order before expanding.

After five years of success under this approach, ITT reorganized in 2016, creating a new parent company, ITT Inc., a global, multi-industrial manufacturer of highly engineered critical components and customized technology solutions for transportation, industrial, and energy markets.

"It has been an honor to lead ITT over the past seven years, and I am very proud of the performance and success that our talented team has achieved together," said Ramos in August 2018, announcing her decision to retire.

As part of the company's long-term succession planning process, Luca Savi has been named to the newly created role of President and Chief Operating Officer, and he will become Chief Executive Officer and President on Jan. 1, 2019. For the remainder of 2018, Savi will continue to report to Ramos as they work together to ensure a seamless transition.

Luca Savi has been instrumental in guiding ITT since joining the Motion Technologies business in 2011, ascending to CEO in 2019.

Luca Savi is chief executive officer and president at ITT Inc. Luca previously served as ITT's president and chief operating officer. He joined ITT in 2011 as president of the company's Motion Technologies business. Previously Luca held several key leadership roles in Italy, China and the United States for Comau, a subsidiary of the Fiat Group. He also formerly held senior roles at Honeywell International. He began his career as an engineer with Royal Dutch Shell and Ferruzzi-Montedison Group. He has a degree in chemical engineering from the Politechnic of Milan in Italy and an M.B.A. from London Business School.

Savi also served as president of the company's Motion Technologies segment, where he led the development of strong operational capabilities, revenue growth of 55%, global expansion and customer-centric innovation such as the ITT Smart Pad.

Savi's background—chemical engineering, global operations experience at Fiat and Honeywell, deep knowledge of ITT's manufacturing base—made him ideally suited to lead the next phase of ITT's evolution. Where Ramos had been the financial architect of the post-spinoff company, Savi would be its operational and strategic leader.

Under Savi, ITT has pursued a more aggressive M&A strategy while maintaining operational discipline:

ITT announced it has signed an agreement to acquire privately held Svanehøj Group A/S (Svanehøj) for approximately $395 million in November 2023. The transaction closed in the first quarter of 2024. Svanehøj became part of ITT's Industrial Process (IP) segment, a global leader in flow focused on highly engineered pumps, valves and aftermarket services. Headquartered in Svenstrup, Denmark, Svanehøj is a supplier of pumps and related aftermarket services with leading positions in cryogenic applications for the marine sector. Its product portfolio primarily consists of deepwell gas cargo pumps, fuel and energy pumps and tank control systems.

ITT Inc. has reported a 9% revenue growth for the second quarter of 2024, largely driven by increased volumes and strategic acquisitions. The company's acquisitions included Svanehoj and kSARIA, a leader in fiber cable applications for defense contractors, which was purchased for $475 million.

This quarter we have also taken a significant step in reshaping the ITT portfolio, shifting towards attractive defense and aerospace interconnect markets while reducing our automotive exposure. Today we announced both the acquisition of kSARIA and the divestiture of Wolverine. This follows three previous acquisitions to expand our flow and connector portfolios and the sale of two non-core product lines. In total, over the past two years, we have committed over $1 billion towards acquisitions.

In 2024, we deployed more than $860 million to acquire Svanehøj and kSARIA. This portfolio shift to higher growth and higher margin businesses is already creating value for our shareholders. Svanehoj orders grew 26% for the full year in 2024 as it is a leader in the transition towards cleaner fuels. And kSARIA, after just three months as part of ITT in 2024, is already contributing meaningfully and continues to gain share on highly coveted defense platforms including the Columbia Class submarine.

"In 2024, our teams delivered on our commitments once again. We grew revenues 11% in total, 7% organically, with strength across all segments. Our businesses drove strong margin expansion and eclipsed our long-term margin target two years ahead of plan. We deployed over $860 million of capital through the acquisitions of cryogenic pump manufacturer, Svanehøj, and defense interconnect specialist, kSARIA. These acquisitions, coupled with the divestiture of our automotive component business, significantly enhanced ITT's opportunities in higher growth and higher margin flow and connectors businesses whilst strategically shifting our portfolio. On top of this, we invested over $100 million in growth and productivity to further our differentiation, paid down over $500 million of debt related to M&A, and returned over $200 million of capital to shareholders."

The most recent strategic expansion occurred in 2025. ITT announced a $25 million expansion of its Industrial Process manufacturing facility in Dammam, Saudi Arabia, doubling the company's capacity and bolstering its position as a preferred supplier to Middle Eastern customers. In 2024, the site secured $160 million in orders, and, with the new expansion, ITT is targeting over $300 million in annual orders by 2030.

In Q1 2025, ITT launched VIDAR, a game-changing industrial motor, enabling us to enter a $6 billion addressable market for industrial motors. VIDAR delivers variable-speed technology for industrial applications that drastically reduces costs and improves energy efficiency for our customers. And, it is the only industrial motor of its kind on the market.

X. The Business Model Today

ITT's current business model is elegantly simple: manufacture highly engineered critical components for harsh environments, then capture long-term recurring revenue from aftermarket parts and services.

ITT operates through three segments: Industrial Process (IP), Motion Technologies (MT), and Connect and Control Technologies (CCT). The IP segment provides engineered fluid process equipment and aftermarket services for the chemical, energy, mining, and other industrial sectors. The MT segment manufactures brake components, shock absorbers, and damping technologies for the automotive and rail transportation markets. The CCT segment designs and manufactures connectors, critical energy absorption systems, and flow control components for the aerospace, defense, and industrial markets.

The Industrial Process segment sells its products under the Goulds Pumps, Bornemann, Engineered Valves, Hamworthy Pumps, PRO Services, C'treat, i-ALERT, Svanehøj, Rheinhütte Pumpen, and Habonim brand names. The Connect & Control Technologies segment offers engineered connectors and specialized products for critical applications supporting various markets, including aerospace and defence, industrial, transportation, medical, and energy under the Cannon, VEAM, BIW Connector Systems, Aerospace Controls, Enidine, Compact Automation, Neo-Dyn Process Controls, Conoflow, kSARIA, and Micro-Mode brand names.

The aftermarket opportunity is the economic heart of the business model. ITT's aftermarket solutions, which represented approximately 45% of IP's revenue in 2023, provide customers with replacement parts, services and plant optimization solutions that reduce total cost of ownership of pumps and rotating equipment. In addition to providing standard repairs, IP also develops engineered solutions for specific customer process issues. Examples include innovative technologies like PumpSmart® Control & Protection Technology and i-ALERT® Equipment Health Monitoring Devices, which remotely control and monitor pumps and other rotating equipment.

ITT's operational model is centered on a high-mix, low-volume manufacturing approach for critical applications, which means they focus on precision over mass production. This framework drives value by ensuring their components are essential and difficult to replace, which allows for strong pricing power and recurring aftermarket revenue. Here's the quick math: high-performance parts wear out, so the original equipment sale leads to a long-tail of high-margin replacement parts and service revenue.

The Motion Technologies segment's revenue, representing approximately 34% of ITT's total in recent years, has been driven by OE volume growth in friction products and strength in rail damping solutions, with key customers like Continental accounting for 17% of MT sales in 2024.

ITT Inc. is a global leader in technology, manufacturing, and engineering, committed to solving critical needs across key industries. The company's continuous improvement mindset and strong global presence, with over 100 facilities in 35 countries, ensure it remains at the cutting edge of industrial solutions.

The company's IP business specializes in flow technology for the chemical, energy, mining, marine, and industrial markets, with approximately $1.4 billion in revenue in 2024.

Segment Performance (2024): - Industrial Process: ~$1.4B revenue, 20%+ operating margins - Motion Technologies: ~$1.5B revenue, approaching 19% margins - Connect & Control Technologies: Growing rapidly post-kSARIA acquisition, approaching 19% margins

The company achieved significant margin expansion, with its Industrial Process (IP) segment surpassing the long-term target margin of 20% and its Motion Technologies (MT) and Connect & Control Technologies (CCT) segments nearing 19%.

XI. Strategic Outlook & Investment Framework

The Bull Case

ITT's transformation from a sprawling conglomerate to a focused industrial champion represents one of the more successful corporate reinventions in American business history. The current strategy—focused on highly engineered components for harsh environments with strong aftermarket dynamics—creates several attractive characteristics:

-

Recurring Revenue Model: The aftermarket business, representing 45% of Industrial Process revenue, provides predictable, high-margin cash flows that support investment in growth initiatives.

-

Positioning for Secular Trends: The Svanehøj acquisition positions ITT to benefit from the energy transition, particularly growth in LNG and alternative fuel vessels. Svanehøj is well positioned to benefit from growth related to decarbonization, the energy transition, and emissions reduction regulations for marine vessels.

-

Defense & Aerospace Exposure: The kSARIA acquisition brings exposure to multi-decade defense programs. With a significant presence in the North American defense market, valued at nearly $7 billion and expected to grow steadily through 2028, kSARIA holds a competitive edge with 70% of its positions as sole or primary source suppliers.

-

Financial Discipline: ITT's debt-to-equity ratio is below the industry average at 0.34, reflecting a lower dependency on debt financing and a more conservative financial approach.

-

Management Execution Track Record: In 2024, once again our value creation from organic growth and margin expansion continued, highlighted by double-digit growth in orders and revenue, 80 basis points of adjusted margin expansion to 17.7% and 12% adjusted EPS growth after more than 17% growth in 2023.

The Bear Case

However, significant risks and challenges remain:

-

Automotive Cyclicality: Despite the Wolverine divestiture reducing automotive exposure, the Motion Technologies segment remains tied to global auto production. European production weakness and the uncertain EV transition timeline create near-term headwinds.

-

Acquisition Integration Risk: With the acquisitions of cryogenic pump manufacturer Svanehoj and defense interconnect specialist kSARIA to bolster our position in higher growth, higher margin businesses whilst divesting the Wolverine automotive business—ITT has committed over $1 billion to acquisitions that must deliver on their strategic and financial promises.

-

Geographic and Currency Exposure: ITT operates in over 35 countries with sales in approximately 125 countries, allowing them to serve local markets and mitigate regional economic risk—but this also creates foreign currency exposure and geopolitical risks.

-

Defense Regulatory Environment: Given ITT's past conviction for Arms Export Control Act violations, any regulatory missteps in the expanded defense portfolio would carry heightened reputational and financial consequences.

-

Valuation: The company has a market cap of $13.94 billion, a PE ratio of 29.70—trading at a premium that leaves limited margin of safety if execution falters.

Competitive Positioning (Porter's Five Forces Analysis)

Threat of New Entrants: LOW ITT's products require specialized engineering capabilities, established customer relationships (often decades-long), and regulatory certifications that create meaningful barriers to entry. The aerospace and defense connectors business, in particular, requires years of qualification processes.

Bargaining Power of Suppliers: MODERATE ITT sources specialty materials including steel, copper, and aluminum that can experience price volatility. However, the company's scale and multi-supplier relationships provide some leverage.

Bargaining Power of Buyers: MODERATE-LOW ITT's products are often specified into customer designs, creating switching costs. The aftermarket dynamic—where customers need replacement parts for installed equipment—further limits buyer power.

Threat of Substitutes: LOW Highly engineered components for harsh environments (cryogenic pumps, aerospace connectors, high-performance brake pads) have few viable substitutes. When equipment failure can result in safety incidents or production shutdowns, customers prioritize reliability over cost.

Competitive Rivalry: MODERATE ITT competes with both large diversified industrials (Parker Hannifin, Flowserve, Amphenol) and niche specialists. Competition is intense on technology and service but less price-focused given the critical nature of applications.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Moderate. ITT benefits from manufacturing scale but competes against larger players in some segments.

Network Economies: Weak. ITT's products don't exhibit network effects.

Counter-Positioning: Strong. ITT's focus on harsh-environment applications and aftermarket services creates a business model that larger, more diversified competitors have difficulty replicating.

Switching Costs: Strong. Once ITT products are specified into customer designs and installed, switching requires significant engineering and qualification work.

Branding: Moderate. Goulds Pumps, KONI, and Cannon connectors have strong brand recognition within their markets.

Cornered Resource: Moderate. ITT's engineering talent and customer relationships represent difficult-to-replicate assets.

Process Power: Strong. ITT's operational excellence—particularly the near-perfect on-time delivery at facilities like Saudi Arabia (96% since 2019)—creates sustainable competitive advantage.

Key Performance Indicators to Track

For long-term investors monitoring ITT's ongoing performance, three KPIs deserve particular attention:

-

Aftermarket Revenue as % of Total Revenue: This metric captures the quality of ITT's revenue mix. Higher aftermarket contribution indicates stronger recurring revenue streams with superior margins and less cyclicality. Target: 45%+ of Industrial Process revenue, growing.

-

Organic Order Growth: Orders are the leading indicator of future revenue. ITT's backlog and book-to-bill ratio signal whether the company is winning new business and maintaining pricing power. Book-to-Bill Ratio: 1.08 year-to-date indicates healthy demand.

-

Adjusted Operating Margin Expansion: ITT's stated goal is continued margin improvement through operational excellence and portfolio mix shift toward higher-margin businesses. Progress toward and beyond the 18%+ adjusted operating margin target demonstrates management execution.

XII. Conclusion: Lessons from a Century of Reinvention

ITT's story is, in many ways, the story of American business itself across the twentieth and into the twenty-first century.

It began with immigrant entrepreneurs who saw opportunity where others saw only undeveloped markets. Sosthenes and Hernand Behn's insight—that international telecommunications markets were underserved and that an American company with local knowledge could serve them—created the foundation for everything that followed.

It survived near-death during the Depression and made morally compromised choices during World War II that continue to trouble historians. The company's dealings with Nazi Germany illustrate the darkest possibilities of international capitalism—the willingness to do business with anyone, anywhere, under any regime.

It became, under Harold Geneen, the prototype for the modern conglomerate—a business model that seemed to defy traditional management logic by combining unrelated businesses under common ownership and intense centralized control. Geneen's fifty-eight quarters of consecutive earnings growth represented a remarkable achievement; his political scandals and the eventual unraveling of his empire represented its limits.

It was methodically dismantled under Rand Araskog, who spent nearly two decades undoing what Geneen had built—selling off more than 250 operations to pay down debt and restore focus. The 1995 breakup into three companies (ITT, Hartford, ITT Industries) was the first formal acknowledgment that the Geneen model had failed.

It split again in 2011, shedding defense and water businesses to create the focused industrial company that exists today. Each separation validated the same lesson: conglomerate structures destroy value, and focused businesses create it.

And now, under Luca Savi, ITT is writing a new chapter—one focused on operational excellence, disciplined M&A, and positioning for secular growth trends in energy transition, aerospace, and defense.

Ten equities research analysts have rated the stock with a Buy rating and one has given a Hold rating to the company's stock. According to MarketBeat.com, the stock presently has a consensus rating of "Moderate Buy" and an average target price of $201.25.

The company that once owned everything from Wonder Bread to Sheraton Hotels now makes its money from brake pads, pumps, and aerospace connectors. It's a smaller company than it was in the Geneen era—much smaller. But it's a better company: more focused, more profitable, more aligned with where value is actually created.

For investors, the ITT story offers a cautionary tale about conglomeration and an encouraging example of corporate reinvention. It demonstrates that companies can recover from strategic mistakes—even decades-long strategic mistakes—if they're willing to make painful but necessary changes.

The question now is whether the current strategy can deliver sustained value creation in an uncertain economic environment. ITT has the operational excellence, the balance sheet strength, and the market positioning to succeed. Whether it does will depend on execution, acquisition integration, and—as it always has for ITT—the ability to adapt to a changing world.

One hundred five years after two brothers in the Caribbean decided to get into the telephone business, their company continues to evolve. That, perhaps, is the most remarkable fact of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube