Applied Industrial Technologies: The Quiet Compounder of Industrial America

I. Introduction & Episode Roadmap

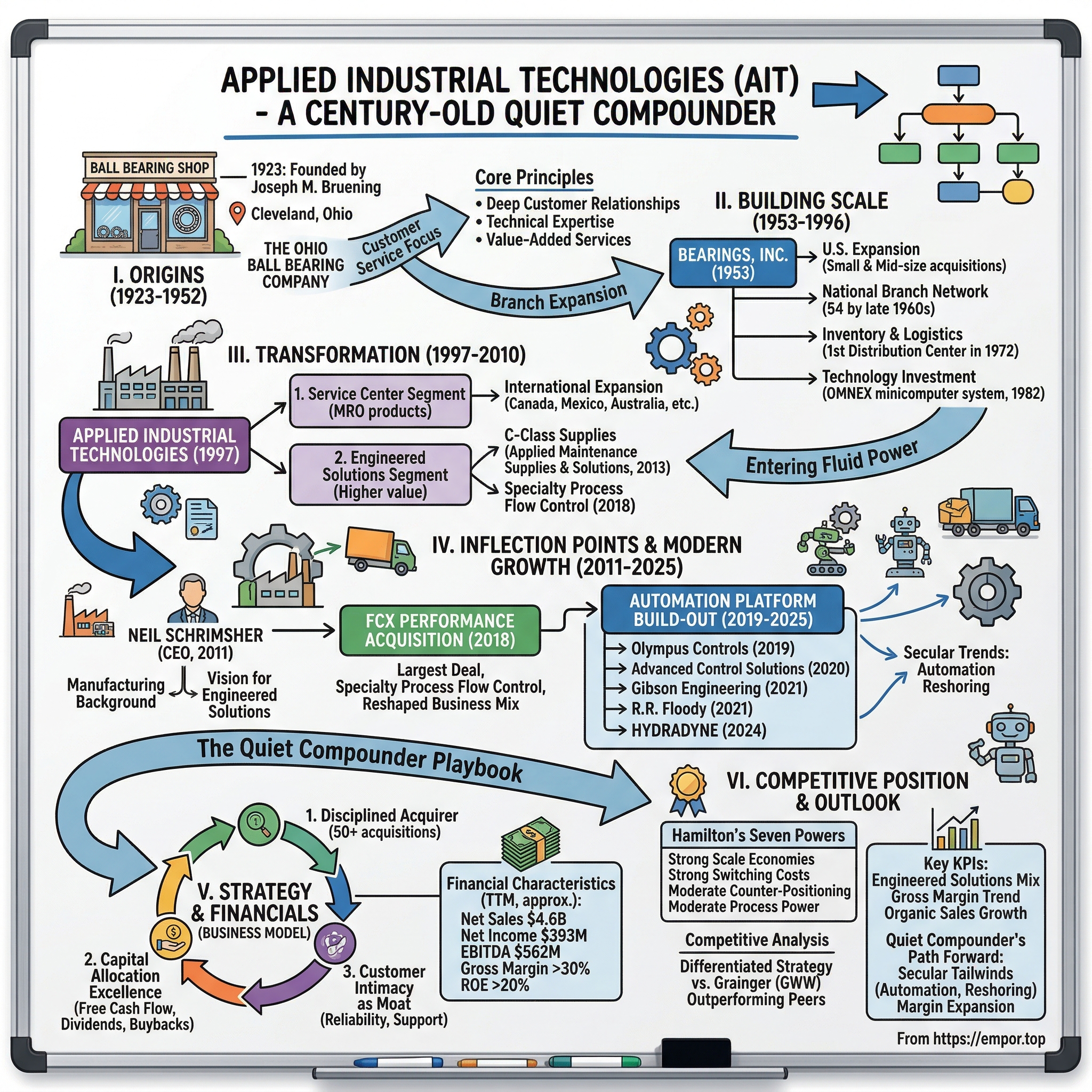

Picture the skyline of Cleveland, Ohio on a January evening in 2023, as the iconic Terminal Tower blazed purple and teal—the corporate colors of Applied Industrial Technologies, celebrating its centennial anniversary. This wasn't a Silicon Valley unicorn or a Wall Street darling demanding attention; it was something far rarer: a century-old industrial distributor that had quietly compounded its way from a single ball bearing shop to a $10 billion Fortune 1000 company.

On this day in 1923, Joseph M. Bruening founded the business that is now one of the largest value-added distributors and solution providers of industrial motion, power, control, and automation technologies in the world. What began as a modest enterprise selling replacement bearings to Cleveland's industrial base has transformed into something far more sophisticated—a leading value-added distributor and technical solutions provider of industrial products and services, specializing in motion control, fluid power, flow control, automation technologies, bearings, power transmission components, and engineered systems.

The core question that animates this story: How does a ball bearing distributor in the industrial Midwest survive—let alone thrive—for over one hundred years? The answer lies not in glamorous technology pivots or celebrity CEOs, but in the disciplined execution of an unglamorous playbook: deep customer relationships, technical expertise, strategic acquisitions, and the relentless pursuit of value-added services.

Applied has experienced consistent growth for ten decades to become a Fortune 1000 company with record sales of $3.8 billion in fiscal year 2022. But the trajectory since then tells an even more compelling story. For the twelve months ended June 30, 2025, sales of $4.6 billion increased 1.9% compared with the prior year. Net income was $393.0 million, or $10.12 per share, and EBITDA was $562.1 million.

Over the past five years, AIT has demonstrated a 14% compound annual growth rate (CAGR) in EBITDA and a 22% CAGR in EPS, reflecting its ability to enhance profitability through operational discipline and strategic acquisitions. This isn't just growth—it's margin expansion at scale, the hallmark of a company transitioning from commodity distribution to value-added solutions.

Several themes will guide our exploration: the art of industrial distribution and why it matters more than Wall Street often recognizes; M&A as a growth flywheel and how disciplined acquisition strategy can transform a regional player into an industry leader; the critical transition from commoditized products to engineered solutions; and the underappreciated power of "boring" businesses that compound wealth over generations.

Applied Industrial Technologies has a market cap or net worth of $10.25 billion as of August 5, 2025. Its market cap has increased by 27.90% in one year. That performance—outpacing the broader market—reflects investor recognition that Applied is no longer simply a parts distributor, but increasingly a technical partner embedded in its customers' most critical operations.

II. Origins: The Ohio Ball Bearing Company (1923-1952)

Cleveland in the early 1920s was the Silicon Valley of industrial America. The city that had birthed Standard Oil and would become home to General Electric's lighting division pulsed with manufacturing ambition. Steel mills lined the Cuyahoga River, machine shops hummed with precision work, and a young generation of entrepreneurs saw opportunity in the complex supply chains that kept American industry moving.

Joseph Bruening was a classic American success story. Prior to launching the company that evolved into Applied Industrial more than a half-century later, he was a customer service troubleshooter for an axle maker in Detroit. In 1922, Bruening resigned to manage Detroit Bearing Company, a maker of replacement bearings for cars and trucks. The owner gave him a mandate to turn around the fortunes of the company's Cleveland-based office in 90 days. Bruening did just that and then offered to buy the local business.

This origin story reveals something essential about Bruening's character—and about the DNA that would define Applied for the next century. He wasn't a manufacturer who built products; he was a customer service expert who understood how to solve problems. The distinction matters enormously. In an era when manufacturers focused on production efficiency and scale, Bruening recognized that the real opportunity lay in the space between factories: the fragmented, complex world of industrial supply chains.

Joseph M. Bruening founded Applied Industrial Technologies, then called The Ohio Ball Bearing Company, in 1923. The name itself tells a story of strategic positioning. Ball bearings were the lifeblood of industrial machinery—small components that enabled rotation, reduced friction, and kept production lines moving. When a bearing failed, entire factories ground to a halt. The cost of downtime far exceeded the cost of the bearing itself, creating an economic dynamic that would prove central to Applied's business model for the next century.

"He articulated the responsibility each of us had to leave the business better than when we walked in," current CEO Neil Schrimsher says of the founder. This philosophy—"Taking Care of the Customer"—became the company's guiding principle. In practical terms, it meant building technical expertise that could help customers select the right bearing for their application, maintaining inventory that could prevent costly downtime, and establishing relationships that transcended transactional purchasing.

Over the next few decades, new branches opened and sales rose steadily. The expansion pattern followed Cleveland's industrial geography—first to Youngstown in 1927, then to Cincinnati, Akron, and Columbus. By 1937, the company established its first out-of-state branch in Indianapolis, signaling ambitions that extended beyond Ohio's borders.

The strategic brilliance of Bruening's approach becomes clear when you understand the economics of industrial distribution in this era. Manufacturers couldn't afford to maintain the inventory needed to serve every customer application. Industrial plants couldn't afford the expertise to specify every bearing correctly. The distributor occupied a critical position in the value chain—aggregating inventory, providing technical knowledge, and offering the local service that manufacturers couldn't economically replicate.

Company operations totaled six stores and 50 employees by 1940. The numbers seem modest by today's standards, but they represented something significant: a proven business model that could be replicated across geographies. Each branch served as a node in a growing network, combining local customer relationships with centralized purchasing power.

In 1952, prior to the rebranding, The Ohio Ball Bearing Company merged with Pennsylvania Bearings, Inc., Indiana Bearings, Inc., and West Virginia Bearings, Inc., forming Bearings Specialists, Inc., which facilitated broader geographic coverage across the Midwest and Appalachia. This wasn't simply growth—it was the emergence of a regional consolidation strategy that would define the company's expansion for decades. The industrial heartland of America was fragmented among thousands of local distributors. Bruening and his successors recognized that combining these businesses could create scale advantages in purchasing, inventory management, and technical capabilities.

The timing proved prescient. Post-war America was entering its greatest industrial expansion, and the companies that could serve this growth most efficiently would prosper. As the Ohio Ball Bearing Company transformed into Bearings Specialists, it positioned itself as a regional consolidator just as American manufacturing was hitting its stride.

III. Building Scale: Bearings, Inc. Era (1953-1996)

The year 1953 marked a watershed moment in the company's history. The company's name was changed from The Ohio Ball Bearing Company to Bearings, Inc. in 1953 and was first publicly traded on the American Stock Exchange that same year. The dual transformation—rebranding and going public—signaled ambitions that extended far beyond Cleveland's immediate orbit.

The name change itself carried strategic significance. "Ohio Ball Bearing Company" suggested a regional player focused on a single product category. "Bearings, Inc." implied broader geographic reach and positioned the company for expansion into power transmission and other adjacent product categories. The IPO provided capital for acquisitions and established the governance structures needed to professionalize operations.

From the 1950s through the early 1990s, Applied® targeted U.S. expansion with small and mid-size acquisitions. This deliberate, patient approach to M&A would prove to be the company's most enduring competitive advantage. Rather than pursuing transformative deals that might strain integration capabilities, management focused on tuck-in acquisitions that expanded geographic reach while maintaining the local customer relationships that drove the business.

By 1957, further acquisitions of Dixie Bearings, Inc., Southern Bearings Co., and Bearings Service Co. extended operations into the Southeast, including Florida. The southern expansion brought new challenges and opportunities. The region's economy was diversifying beyond agriculture toward manufacturing and energy, creating demand for the technical expertise that Bearings, Inc. had honed in the industrial Midwest.

Organic branch openings added momentum, with the network growing to 28 locations by 1956 and reaching 54 branches across multiple states by the end of the 1960s. The branch model combined the advantages of national scale with local execution. Each location maintained relationships with nearby industrial customers, while the corporate network provided purchasing power, inventory optimization, and technical resources that no local competitor could match.

The 1970s marked accelerated scaling, as expansion efforts brought the total to 113 locations in 24 states by 1970, supported by additional mergers such as the acquisition of Neiman Bearings Co. in 1960 and five Pacific Northwest distributors in the late 1960s and early 1970s. The Pacific Northwest push was particularly significant, bringing the company to the West Coast and establishing truly national coverage.

Understanding the economics of MRO (Maintenance, Repair, and Operations) distribution illuminates why this scale mattered. Industrial customers don't buy bearings and power transmission components on a regular schedule—they buy them when equipment fails or when preventive maintenance programs identify components nearing end of life. This unpredictable demand pattern creates inventory challenges. A single location serving a small geography can't economically stock the full range of products that customers might need. But a network of 113 locations can pool inventory risk, maintain deeper stock in regional distribution centers, and transfer products between locations to meet emergency needs.

The tension between national scale and local technical expertise defined the company's strategic challenges during this period. Large customers increasingly demanded national contracts and centralized procurement, while the value proposition still rested on local expertise and rapid response. Bearings, Inc. navigated this tension by maintaining local autonomy for customer relationships while centralizing functions where scale created genuine advantage: purchasing, inventory management, and technical training.

By 1972, the company opened its first distribution center in Cleveland with sales exceeding $100 million for the first time. The distribution center model represented an evolution in the company's logistics strategy—creating a hub that could serve regional branches with broader inventory selection than any single location could economically maintain.

The investment in technology paralleled the physical expansion. The company developed a minicomputer inventory control system to automate manual functions of a stocking center in 1977 and established OMNEX, a fully operational online information and processing tool that linked all locations, in 1982. For a company in an unglamorous industry, these investments in information technology proved prescient. Inventory optimization—knowing what to stock where—would become increasingly central to competitive advantage as the industry consolidated.

In the mid-1990s, we increased the overall pace of acquisitions, expanding our fluid power operations in particular. The fluid power expansion marked an important strategic evolution. Fluid power systems—hydraulic and pneumatic components that transmit force and motion—represented a natural adjacency to the bearings and power transmission products that had been the company's foundation. More importantly, fluid power systems often required engineering and integration services, positioning the company to move up the value chain from simple product distribution to technical solutions.

By the mid-1990s, Bearings, Inc. had established itself as one of America's leading industrial distributors. But the company's name and identity still reflected its origins in a single product category. A more fundamental transformation was coming.

IV. Transformation: Applied Industrial Technologies Emerges (1997-2010)

In 1997, the Company changed its name to Applied Industrial Technologies to more accurately reflect its diversified product lines, and is currently traded on the New York Stock Exchange with the symbol AIT. The rebranding represented far more than corporate identity; it signaled a strategic vision that would guide the company for the next quarter century.

The name "Applied Industrial Technologies" communicated several important messages. "Applied" suggested a focus on customer applications rather than product categories. "Industrial" positioned the company squarely in the B2B space. "Technologies" pointed toward increasingly sophisticated engineered solutions rather than commodity distribution. The move from AMEX to NYSE reflected the company's increased scale and ambition to compete for institutional capital.

Applied Industrial Technologies, Inc. distributes industrial motion, power, control, and automation technology solutions in the United States, Canada, Mexico, Australia, New Zealand, Singapore, and Costa Rica. It operates in two segments, Service Center and Engineered Solutions. The Service Center segment distributes industrial bearings, power transmission, fluid power components and systems, specialty flow control, and advanced factory automation solutions, as well as general maintenance products.

Since 2000, Applied has also grown internationally with locations in Canada, Mexico, Australia, New Zealand and Singapore. The international expansion reflected both opportunity and strategic necessity. Many of Applied's largest customers operated globally and demanded consistent service across geographies. Meanwhile, emerging markets in Asia Pacific offered growth opportunities as manufacturing shifted eastward.

The two-segment structure that emerged during this period reveals the company's strategic direction. The Service Center segment represented the traditional distribution business—maintaining inventory, filling orders, and providing technical support for routine MRO needs. The Engineered Solutions segment focused on higher-value applications: designing and integrating fluid power systems, flow control solutions, and increasingly sophisticated automation technologies.

The economics of these segments differ significantly. Service Center operations generate relatively predictable revenue with modest margins, driven by the sheer volume of industrial MRO activity. Engineered Solutions involves longer sales cycles, deeper customer relationships, higher technical content, and meaningfully better margins. Management's strategic objective was clear: leverage the Service Center network to identify Engineered Solutions opportunities while progressively shifting the business mix toward higher-value activities.

In 2013, we formed Applied Maintenance Supplies & Solutions® making us a leading national distributor of C-Class maintenance, repair, operating and production (MROP) supplies. The year 2018 brought expansion into specialty process flow control products and solutions, followed by automation technologies in 2019.

The C-Class initiative deserves particular attention. "C-Class" supplies are the small, consumable items that industrial facilities need in vast quantities—fasteners, abrasives, lubricants, safety equipment. Individually, these items generate thin margins. But collectively, they represent enormous purchasing volume and frequent customer touchpoints. Applied Maintenance Supplies & Solutions positioned the company to capture a share of this business, deepening customer relationships while cross-selling higher-margin products and services.

As the new millennium dawned, Applied Industrial commenced a major international expansion plan, culminating with locations in Canada, Mexico, Australia, New Zealand and Singapore. The international footprint reflected the globalization of Applied's customer base. Major manufacturers maintained operations across multiple continents and increasingly demanded consistent service from their supply chain partners.

By 2010, Applied had evolved from a regional ball bearing distributor to a national industrial distributor with international operations and an increasingly sophisticated product portfolio. But the most transformative phase of the company's evolution was about to begin—ushered in by new leadership with ambitious plans for accelerating growth.

V. Inflection Point #1: The Neil Schrimsher Era Begins (2011)

Every enduring company faces moments when leadership transitions either reinforce institutional momentum or redirect strategic trajectory. For Applied Industrial Technologies, October 2011 proved to be a pivotal inflection point.

Neil A. Schrimsher joined Applied® as Chief Executive Officer in 2011. In 2013 his title was expanded to President & CEO. What made this appointment unusual was Schrimsher's background: he came not from distribution, but from manufacturing. This outside perspective would prove transformative.

Mr. Schrimsher, age 47, was most recently Executive Vice President of Cooper Industries, a $5.1 billion (2010 revenues) global electrical products manufacturer, where he lead multiple businesses in Cooper's Electrical Products Group and headed numerous domestic and international growth initiatives. Prior to joining Applied, he served as Executive Vice President of Cooper Industries where he led multiple businesses in Cooper's Electrical Products Group and headed numerous domestic and international growth initiatives. Before joining Cooper in 2006 as President of Cooper Lighting, Schrimsher worked in Atlanta for Siemens Energy & Automation.

The board's rationale for bringing in a manufacturing executive to lead a distribution company reflected sophisticated thinking about the industry's evolution. "Neil Schrimsher is an outstanding, seasoned leader with extensive experience and an exceptional track record of driving profitable growth at GE, Siemens and Cooper Industries," said Applied's presiding non-management director, Peter C. Wallace. "Throughout his career, he has been highly active with end users and selling through distribution, so he has an excellent understanding of industrial distribution business from a manufacturer's viewpoint and a customer's perspective."

Neil received a bachelor's degree from University of Tennessee and a master's degree from John Carroll University. His educational path—engineering undergraduate work followed by business studies—reflected the dual competencies that would shape his leadership: technical credibility with Applied's engineering staff and customer base, combined with strategic and financial sophistication.

"In leading global businesses at Cooper and Siemens, he built and executed strategies, drove operational improvements and generated growth -- both organically and through acquisitions." This track record—combining organic growth with disciplined M&A—would prove central to Applied's strategy under Schrimsher's leadership.

For the past 12 years, Applied Industrial Technologies CEO Neil Schrimsher has looked backwards at the work of his five predecessors to inform strategic opportunities for the future. After taking the helm in 2011, Schrimsher continued to grow the company, adding specialty process flow control products and solutions in 2018, then automation technologies in 2019. As legacy industrial infrastructure converged with emerging technologies, he bolstered Applied Industrial's digital, technical and application capabilities to become a leading distributor and solutions provider across advanced machine vision, as well as collaborative and mobile robotic technologies.

The strategic vision that Schrimsher articulated represented an evolution rather than a revolution. The foundational elements remained: customer relationships, technical expertise, geographic coverage, inventory capabilities. But the emphasis shifted decisively toward value-added solutions and engineered systems. Rather than simply distributing components, Applied would increasingly design, integrate, and service sophisticated industrial systems.

The large-scale acquisition of FCX Performance in 2018, followed by subsequent targeted acquisitions through 2024, marked a definitive shift towards higher-value engineered solutions and automation. This strategy aimed to differentiate AIT from traditional distributors by offering technical expertise and customized systems, driving margin improvement and deeper customer relationships.

The transformation under Schrimsher's leadership is evident in the financial results. When he took the helm, Applied was a solid but slow-growing distributor with modest margins. Over the past five years, AIT has demonstrated a 14% compound annual growth rate (CAGR) in EBITDA and a 22% CAGR in EPS, reflecting its ability to enhance profitability through operational discipline and strategic acquisitions.

"We achieved new records for sales, EBITDA and EPS. Full year EPS growth of 4% exceeded the high end of our initial guidance. Gross margins expanded nearly 50 basis points and surpassed 30% for the first time in our history." The milestone of 30% gross margins deserves emphasis. For a distribution business, gross margin expansion of this magnitude reflects fundamental changes in business mix and competitive positioning. Applied was no longer competing primarily on price and availability; it was selling technical expertise and engineered solutions.

VI. Inflection Point #2: The FCX Performance Acquisition (2018)

If Schrimsher's appointment marked a leadership inflection point, the acquisition of FCX Performance in 2018 represented a strategic one. This was Applied's largest deal in company history—a transformative transaction that would reshape the business mix and accelerate the shift toward engineered solutions.

Applied Industrial Technologies (NYSE:AIT) today announced it has reached a definitive agreement to acquire FCX Performance, Inc. (FCX), a leading distributor of specialty process flow control products and services based in Columbus, Ohio, for total consideration of approximately $768 million, subject to customary adjustments.

The total purchase price of the acquisition after contractual working capital adjustments was approximately $784 million, and was financed with a new credit facility comprised of a $780 million Term Loan A and a $250 million revolver.

The scale of this transaction demands context. Applied's fiscal 2017 revenue was approximately $2.59 billion. A $784 million acquisition represented nearly a year's worth of EBITDA—a bold bet that required significant leverage to finance. Management's willingness to take on debt for the right strategic opportunity signaled confidence in both integration capabilities and the deal's value-creation potential.

FCX is the premier distributor of highly engineered valves, instruments, pumps, and lifecycle services to MRO and OEM customers across diverse industrial and process end markets. The company's comprehensive value-added solutions help customers improve cost productivity, reduce downtime, increase efficiency and effectively meet increasing regulatory compliance standards.

The strategic rationale extended beyond simple revenue addition. Based in Columbus, Ohio, FCX operates 68 locations with more than 1,000 team members. FCX brought not just revenue, but technical capabilities in flow control that complemented Applied's existing strengths in fluid power. The combination positioned Applied as the clear industry leader in engineered fluid power and flow control solutions.

Applied had 2017 full year sales of $2.59 billion, while FCX had 2016 sales of $346 million. The addition will move Applied further into the upper echelon of industrial distributors based on market share, forming a company that has about $3 billion in combined revenue.

The acquisition is anticipated to contribute approximately $550 million in sales and $68 million in EBITDA in the first 12 months of Applied ownership. The implied EBITDA margin of approximately 12% for FCX exceeded Applied's historical margins, indicating the value-added nature of flow control distribution compared to traditional MRO products.

For the full year 2018, Applied's total sales of $3.073 billion increased 18.5 percent from 2017, with the FCX acquisition responsible for 10.2 percentage points of that growth. The remaining 8.3% organic growth reflected favorable industrial conditions, but the acquisition clearly transformed Applied's scale and market position.

"Fiscal 2018 proved to be an exciting and successful year, including record fiscal-year financial performance and continued progress in enhancing our differentiation as a value-added industrial distributor."

The integration lessons from FCX would prove valuable for subsequent acquisitions. Applied preserved FCX's customer relationships and technical capabilities while progressively integrating back-office functions where scale created genuine advantage. The approach—preserving local expertise while capturing centralized synergies—reflected decades of M&A experience.

Why flow control was a natural adjacency to Applied's existing businesses becomes clear when you understand the customer relationship. Industrial facilities that need fluid power systems (hydraulics and pneumatics for motion control) often also need flow control systems (valves and instruments for process control). Serving both needs from a single relationship deepened customer engagement and created cross-selling opportunities.

VII. Inflection Point #3: The Automation Platform Build-Out (2019-2025)

The FCX acquisition established Applied as the leader in fluid power and flow control distribution. But management recognized that the industrial landscape was shifting toward a new frontier: automation. Beginning in 2019, Applied embarked on a systematic effort to build an automation platform through a series of targeted acquisitions.

Aug. 14, 2019 - Applied Industrial Technologies (NYSE: AIT) today announced it has signed a definitive agreement to acquire Olympus Controls Corp. ("Olympus"), an automation solutions provider – including design, assembly, integration, and distribution – of motion control, machine vision, and robotic technologies. The transaction is expected to close before the end of August 2019.

The Olympus acquisition marked Applied's entry into the automation space. Founded in 1998, Olympus and its team of 80+ employees serve customers throughout the Pacific Northwest, West Coast and Lower Central States from five locations.

Applied's automation acquisitions include Olympus Controls Corp. in August 2019; Advanced Control Solutions in October 2020; R.R. Floody in August 2021; and Gibson Engineering Company in January 2021.

"We are pleased to announce the addition of Gibson Engineering and the continued expansion of our next generation automation offering and footprint. Gibson is a leading provider of emerging automation technologies across the U.S. Northeast and Mid-Atlantic markets. They bring established customer and supplier relationships, along with an experienced team highly regarded for their technical and engineering expertise that aligns with our growth strategy, market focus, and value proposition."

"Today's announcement represents another key step in the continued expansion of our next generation automation offering. Automation, Inc. is a leading provider of emerging automation technologies across the U.S. Upper Midwest with advanced capabilities in machine vision, pneumatic automation, and value-added assembly services and engineered solutions."

The automation strategy aligned with powerful secular trends in industrial markets. "Secular demand tailwinds are building as customers manage through structural labor constraints and evolving production considerations to support long-term growth and supply chain initiatives. We are well positioned to capitalize on this opportunity given our application and engineering expertise, as well as accelerated adoption of advanced technologies aligned with our product focus including collaborative and mobile robots, machine vision, and digital solutions."

The reshoring phenomenon amplified automation demand. The Reshoring Initiative 2024 Annual Report shows that 244,000 U.S. manufacturing jobs were announced in 2024 via reshoring and foreign direct investment (FDI), continuing the nation's push to rebuild domestic production capacity. The industrial automation market size stood at USD 221.64 billion in 2025 and is set to reach USD 325.51 billion by 2030, reflecting a 7.99% CAGR. Smart-factory programs, government reshoring incentives, and energy-efficiency mandates have been the main accelerants.

Companies bringing manufacturing back to North America faced a fundamental challenge: labor costs and availability. The success or failure of training millions of workers could skew the outcome of the U.S. reindustrialization momentum in either direction. Even without a surge in reshoring, 2.1 million manufacturing jobs are forecast to go unfilled by 2030, with an estimated loss to GDP of $1T. Automation offered the solution—enabling domestic production at competitive costs despite higher labor rates.

In late 2024, Applied announced its most significant acquisition since FCX. Applied Industrial Technologies has announced a definitive agreement to acquire Hydradyne, LLC for $272 million, marking a strategic expansion of its Engineered Solutions segment.

Based in Dallas, Texas, Hydradyne is one of the largest U.S. distributors focused on fluid power and motion control systems with advanced service capabilities and product offerings in hydraulics, pneumatics, electromechanical, instrumentation, filtration, and fluid conveyance. The company's team of nearly 500 associates operate out of 33 locations across the Southeastern U.S. with specialization in fluid power system design, fabrication, assembly, installation, repair and component support. Hydradyne's products and solutions are integral to powering and controlling critical stationary and mobile equipment.

Applied said that it expects Hydradyne to add some $260 million in sales and $30 million in EBITDA — before anticipated synergies — within 12 months, prior to transaction-related expenses and accounting adjustments. The deal is also expected to be accretive to the company's earnings per share over that span.

Applied Industrial Technologies (NYSE: AIT) today announced it completed the acquisition of Hydradyne, LLC on December 31, 2024. "This transaction will enhance our leading fluid power distribution position in the U.S. by leveraging complementary technical capabilities and innovative engineered solutions across legacy and emerging end markets."

The Southeast focus of the Hydradyne acquisition aligned with reshoring geography. The southern U.S. remains the most competitive region. Favorable costs, infrastructure, an established ecosystem for hot products, incentives and right-to-work make the Southeast the leading region for manufacturing investment.

VIII. The Business Model Deep-Dive

To understand Applied's competitive position and value creation potential, we must examine the mechanics of its business model with precision.

What makes Applied Industrial Technologies, Inc. a critical player in the industrial distribution landscape, especially after achieving net sales of $1.1 billion in just its second quarter of fiscal 2024? This company isn't just selling parts; it delivers essential maintenance, repair, and operational (MRO) products alongside specialized engineering services across North America, Australia, New Zealand, and Singapore.

With over 100 years of experience, as of June 2025 AIT maintains a vast inventory exceeding 9.2 million stock-keeping units (SKUs) and employs more than 6,800 associates across its global network of service centers and operations.

The inventory breadth deserves emphasis. 9.2 million SKUs represents an extraordinary range of products—from commodity fasteners to highly specialized flow control valves. No single customer could economically maintain this inventory depth. Applied's scale enables it to aggregate demand across thousands of customers, optimizing inventory investment while ensuring product availability.

Two Segments, Distinct Economics

It operates in two segments, Service Center and Engineered Solutions. The Service Center segment distributes industrial bearings, power transmission, fluid power components and systems, specialty flow control, and advanced factory automation solutions, as well as general maintenance products; and motors, belting, drives, couplings, pumps, linear motion, hydraulic and pneumatic components, filtration supplies, hoses, and other related supplies.

The Service Center segment represents the traditional distribution business. Customers call when they need components—often urgently when equipment fails. Success depends on having the right inventory, responding quickly, and providing technical guidance on product selection. Gross margins in this segment typically range from the mid-20s to low-30s percent, constrained by competitive pressure on commodity products.

The Engineered Solutions segment operates differently. Here, Applied's engineers work with customers to design and integrate systems—fluid power configurations, flow control assemblies, automation cells. Sales cycles are longer, but customer relationships are deeper. The Engineered Solutions segment saw total sales increase by 20.7% over the prior year quarter in Q4 FY25, demonstrating growth momentum in this higher-value business.

Value-Added Services as Differentiator

The company's core offerings include not only the distribution of high-quality components from leading manufacturers but also value-added services such as custom system design, assembly, repair, predictive maintenance, and automation integration to optimize industrial operations and reduce downtime.

These services transform the customer relationship from transactional to consultative. A customer buying a bearing is price-sensitive and can easily switch suppliers. A customer whose fluid power system was designed and installed by Applied's engineers—and whose preventive maintenance program is managed through Applied's services—is far less likely to switch for modest price savings.

Unlike Grainger, Applied Industrial Technologies has a more specialized product focus, with a strong emphasis on fluid power products, bearings, industrial rubber products, and power transmission components. The company distinguishes itself by offering ancillary services like application engineering, inventory management solutions, maintenance services, and customized training programs.

Financial Characteristics

EBITDA (TTM) 585.632M · ROE (TTM) 22.10% Revenue (TTM) 4.664B · Gross Margin (TTM) 30.44% Net Margin (TTM) 8.61% Debt To Equity (MRQ) 30.38%

Return on equity exceeding 20% demonstrates efficient capital utilization. The balance sheet strength—net leverage ratio of just 0.27x as of September 30, 2025—provides substantial capacity for M&A and shareholder returns.

Applied Industrial Technologies Inc (NYSE:AIT) achieved new records for sales, EBITDA, and EPS in fiscal 2025, with full-year EPS growth of 4% exceeding the high end of initial guidance. Gross margins expanded nearly 50 basis points, surpassing 30% for the first time in the company's history.

The gross margin milestone reflects the strategic shift toward higher-value activities. Traditional MRO distribution generates gross margins in the mid-to-high 20s. Achieving 30%+ indicates meaningful progress in the Engineered Solutions mix shift.

IX. Playbook: Strategy & Business Lessons

Applied's century-long journey offers valuable lessons for investors seeking to understand what makes industrial compounders succeed over generations.

The Disciplined Acquirer Playbook

Applied has completed over 50 acquisitions in the past four decades. The pattern reveals consistent principles:

- Geographic expansion through regional distributors that bring customer relationships and market knowledge

- Capability adjacencies like fluid power, flow control, and automation that complement existing strengths

- Cultural fit ensuring acquired companies share Applied's customer-service orientation

- Integration discipline preserving local expertise while capturing centralized synergies

Applied continued its investment in the automation industry with its fourth acquisition in that market since 2019. The systematic platform build-out demonstrates how patient capital allocation can create new growth vectors.

Capital Allocation Excellence

The company's approach to capital deployment reflects sophisticated prioritization:

The company generated over $465 million of free cash, up 34% to a new record, enabling significant capital deployment including share buybacks and dividend increases.

Quarterly Dividend Increased 24% to $0.46 Per Share in early 2025. The dividend increase demonstrated confidence in the business's cash generation while maintaining flexibility for opportunistic M&A.

The company maintains a conservative financial position with a net leverage ratio of just 0.27x as of September 30, 2025. This balance sheet strength represents dry powder for acquisitions while providing resilience against economic downturns.

Customer Intimacy as Competitive Moat

"Taking Care of the Customer has remained the guiding principle at Applied® throughout our 100-year history," said Neil A. Schrimsher. "As a critical business partner across virtually all industrial markets, we have played a significant role in maximizing our customers' productivity and returns across their core operational assets."

The emphasis on customer relationships—rather than product features or price competition—reflects the fundamental economics of MRO distribution. Customers prioritize reliability, technical support, and response time over marginal price differences. A bearing that arrives an hour late can cost thousands in lost production; saving a few dollars per unit provides little consolation.

X. Competitive Analysis: Porter's Five Forces & Hamilton's Seven Powers

Porter's Five Forces Analysis

| Force | Rating | Analysis |

|---|---|---|

| Threat of New Entrants | LOW | High barriers due to: (1) 100+ years of supplier relationships and preferred distributor status, (2) Technical expertise that takes decades to build, (3) Scale advantages in inventory and logistics, (4) Established customer relationships in mission-critical applications |

| Bargaining Power of Suppliers | MODERATE | Applied distributes for major manufacturers like SKF, but its scale as one of the largest distributors gives it leverage. Some supplier dependency in key categories creates moderate risk |

| Bargaining Power of Buyers | MODERATE-LOW | Industrial customers are fragmented across manufacturing, energy, mining, and agriculture. Technical expertise and downtime avoidance costs limit buyer power |

| Threat of Substitutes | LOW | Industrial bearings, fluid power systems, and automation components are essential with few substitutes. Value-added services further reduce substitutability |

| Competitive Rivalry | MODERATE-HIGH | Competitors include WESCO, MSC Industrial, W.W. Grainger, and DXP Enterprises. However, Applied's engineered solutions focus creates differentiation |

The company provides a range of products, from power transmission components and industrial rubber products to general maintenance and repair supplies. It primarily serves manufacturing, mining, oil and gas, food processing, and transportation industries. The company operates about 600 facilities across the world.

Applied Industrial Technologies excels with its focus on fluid power products, bearings, industrial rubber products, and power transmission components. The company's targeted approach gives it deeper category expertise than Grainger's broader catalog.

Hamilton's Seven Powers Analysis

| Power | Present? | Evidence |

|---|---|---|

| Scale Economies | ✓ STRONG | 9.2 million SKUs, 6,800+ employees, and 600+ locations provide purchasing power, inventory efficiency, and logistics advantages unmatched by smaller competitors |

| Network Effects | ✗ WEAK | Limited direct network effects in B2B distribution. Some benefits from customer density enabling faster service |

| Counter-Positioning | ✓ MODERATE | The shift to engineered solutions and automation creates a position that commodity distributors would cannibalize their existing business to match |

| Switching Costs | ✓ STRONG | Technical expertise embedded in customer relationships, custom system designs, and equipment familiarity create high switching costs. Downtime risk far exceeds any price savings |

| Branding | ✓ MODERATE | The Company has been a recipient of numerous awards and recognition from customers, suppliers and organizations, including being named to the Forbes list of World's Best Employers |

| Cornered Resource | ✗ WEAK | No unique access to products or technologies. Competitive advantage comes from expertise and execution rather than exclusive resources |

| Process Power | ✓ MODERATE | Decades of M&A integration experience, inventory optimization systems, and technical training programs create operational advantages difficult to replicate |

Competitive Positioning vs. Industry Peers

Grainger's revenue reached $17.2 billion in 2024, while its competitors tried to match its successful two-segment business model. W.W. Grainger operates at roughly 4x Applied's revenue scale, but with a broader product focus rather than Applied's specialized technical depth.

W.W. Grainger's competitor, Applied Industrial Technologies, Inc. (AIT), has outperformed GWW. AIT has gained 62.6% over the past 52 weeks and 56.7% in 2024.

The outperformance reflects market recognition of Applied's differentiated strategy. While Grainger competes broadly across the MRO landscape, Applied has carved a defensible position in technical distribution where expertise matters more than catalog breadth.

XI. Key Performance Indicators for Investors

For long-term investors monitoring Applied's ongoing performance, three KPIs deserve particular attention:

1. Engineered Solutions Segment Revenue Mix

Currently approximately 30% of total revenue, this segment represents Applied's strategic future. Tracking the percentage of revenue from Engineered Solutions provides insight into the company's progress toward higher-value activities. Management's actions—including the automation platform build-out and Hydradyne acquisition—indicate intention to grow this segment faster than Service Center operations.

2. Gross Margin Trend

Gross margins expanded nearly 50 basis points, surpassing 30% for the first time in the company's history. Gross margin reflects business mix and competitive positioning. Continued expansion would indicate successful execution of the value-added strategy. Margin compression might signal pricing pressure or unfavorable mix shifts.

3. Organic Sales Growth (Daily Basis)

The company's organic sales growth has returned to positive territory after several quarters of decline, marking the strongest organic growth in two years. Organic growth isolates underlying business momentum from acquisition contributions. For fiscal 2026, management guides to up 1% to 4% on an organic basis.

XII. Bull and Bear Case Analysis

The Bull Case

Secular Tailwinds Provide Multi-Year Runway

The convergence of reshoring, automation adoption, and aging industrial infrastructure creates favorable demand conditions for Applied's offerings. Both reshoring and foreign direct investment have grown, from generating 11,000 new U.S.-based jobs per year in 2010 to more than 300,000 in 2022. Each new domestic manufacturing facility requires the fluid power, flow control, and automation systems that Applied distributes and integrates.

Margin Expansion Potential Remains

The shift toward Engineered Solutions continues. As this higher-margin segment grows as a percentage of revenue, overall profitability should improve. EBITDA margins of 12.2% to 12.5% guidance suggests management sees further expansion potential.

M&A Optionality with Strong Balance Sheet

Net leverage ratio of just 0.27x provides substantial capacity for strategic acquisitions. The industrial distribution landscape remains fragmented, offering opportunities for disciplined consolidators.

Dividend Track Record Signals Management Confidence

The company has maintained dividend payments for multiple consecutive decades, with 15+ years of consecutive increases. This track record demonstrates both cash generation capability and management's confidence in business sustainability.

The Bear Case

Cyclical Exposure to Industrial Economy

Applied's revenue correlates with industrial production and capital investment. Economic recession or manufacturing downturn would pressure both volumes and pricing power. The muted organic growth environment in recent quarters demonstrates this sensitivity.

Acquisition Integration Risk

The Hydradyne acquisition—the largest since FCX—requires successful integration to deliver expected synergies. M&A execution risk is inherent in the growth strategy.

Competitive Pressure from Larger Players

Grainger's revenue reached $17.2 billion in 2024—roughly 4x Applied's scale. Large competitors with greater resources could intensify competition in Applied's core markets.

Valuation Reflects High Expectations

At the time, AIT's stock traded well above the firm's previous price target of $250, with a forward EBITDA multiple of 18x. This valuation implies the market is pricing in perpetual organic sales growth of 4-5%, aligning with management's long-term targets. The stock's premium valuation leaves limited margin of safety if growth disappoints.

XIII. Myth vs. Reality

| Consensus Narrative | Reality Check |

|---|---|

| "Distributors are boring commodity businesses" | Applied generates 22% ROE and has delivered 14% EBITDA CAGR over five years—outperforming many "exciting" growth companies |

| "E-commerce will disintermediate industrial distributors" | Technical sales require application expertise that pure e-commerce cannot replicate. Amazon Business has made limited inroads in specialized MRO |

| "Manufacturing is leaving America" | 244,000 U.S. manufacturing jobs were announced in 2024 via reshoring and FDI—creating demand for Applied's products and services |

| "Industrial distribution is mature with no growth" | Automation, flow control, and engineered solutions represent expanding addressable markets as manufacturing becomes more sophisticated |

XIV. Regulatory and Accounting Considerations

Material Legal/Regulatory Overhangs: No significant regulatory issues currently affect the company. Applied operates in a relatively low-regulation industry compared to healthcare or financial services.

Accounting Judgments to Monitor:

-

LIFO inventory accounting: Applied uses last-in, first-out (LIFO) inventory valuation, which can create earnings volatility. On a pre-tax basis, full-year results include $7.7 million ($0.16 after tax per share) of LIFO expense compared to $13.0 million ($0.25 after tax per share) of LIFO expense in the prior-year period.

-

Goodwill from acquisitions: Significant acquisition activity has accumulated goodwill on the balance sheet, which requires impairment testing annually.

-

Revenue recognition on long-term projects: Some Engineered Solutions contracts span multiple periods, requiring judgment on percentage-of-completion recognition.

XV. Conclusion: The Quiet Compounder's Path Forward

Applied Industrial Technologies represents a particular species of American business: the quiet compounder. Unlike companies that capture headlines with bold pivots or charismatic leaders, Applied has built value through patient execution, disciplined capital allocation, and relentless focus on customer needs.

"Looking ahead, we are excited to build on this history through our multi-faceted strategy of enhancing and leveraging our core Service Center operations, while expanding across higher-engineered solutions tied to advanced automation, industrial power, and process technologies."

The company's century-long journey—from a Cleveland ball bearing shop to a $10 billion industrial technology distributor—illustrates the power of compounding in unglamorous industries. Joseph Bruening's 1923 insight that customer service mattered more than product features remains central to Applied's competitive advantage today.

"A strong focus on cost accountability, continuous improvement and how we expanded the business to increase relevancy to the customers we serve in today's industrial economy, all played a role," says Schrimsher. "We look backwards and take great pride in how we've grown and evolved over 100 years, but we also look forward with excitement about the potential ahead."

For investors seeking exposure to North American industrial activity with margin expansion potential and disciplined capital allocation, Applied Industrial Technologies merits serious consideration. The story isn't flashy, but the fundamentals are sound—and sometimes boring businesses make the best investments.

The Terminal Tower glowing purple and teal on that January evening in 2023 celebrated not just a centennial anniversary, but something rarer: a business model that has endured through two World Wars, multiple recessions, the rise and fall of Cleveland's industrial prominence, and the complete transformation of American manufacturing. The next century will bring its own challenges—but Applied's track record suggests it will adapt, as it always has, by taking care of the customer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube