CTS Corporation: The 129-Year Journey from Telephones to Sensing the Future

I. Introduction: A Masterclass in Corporate Reinvention

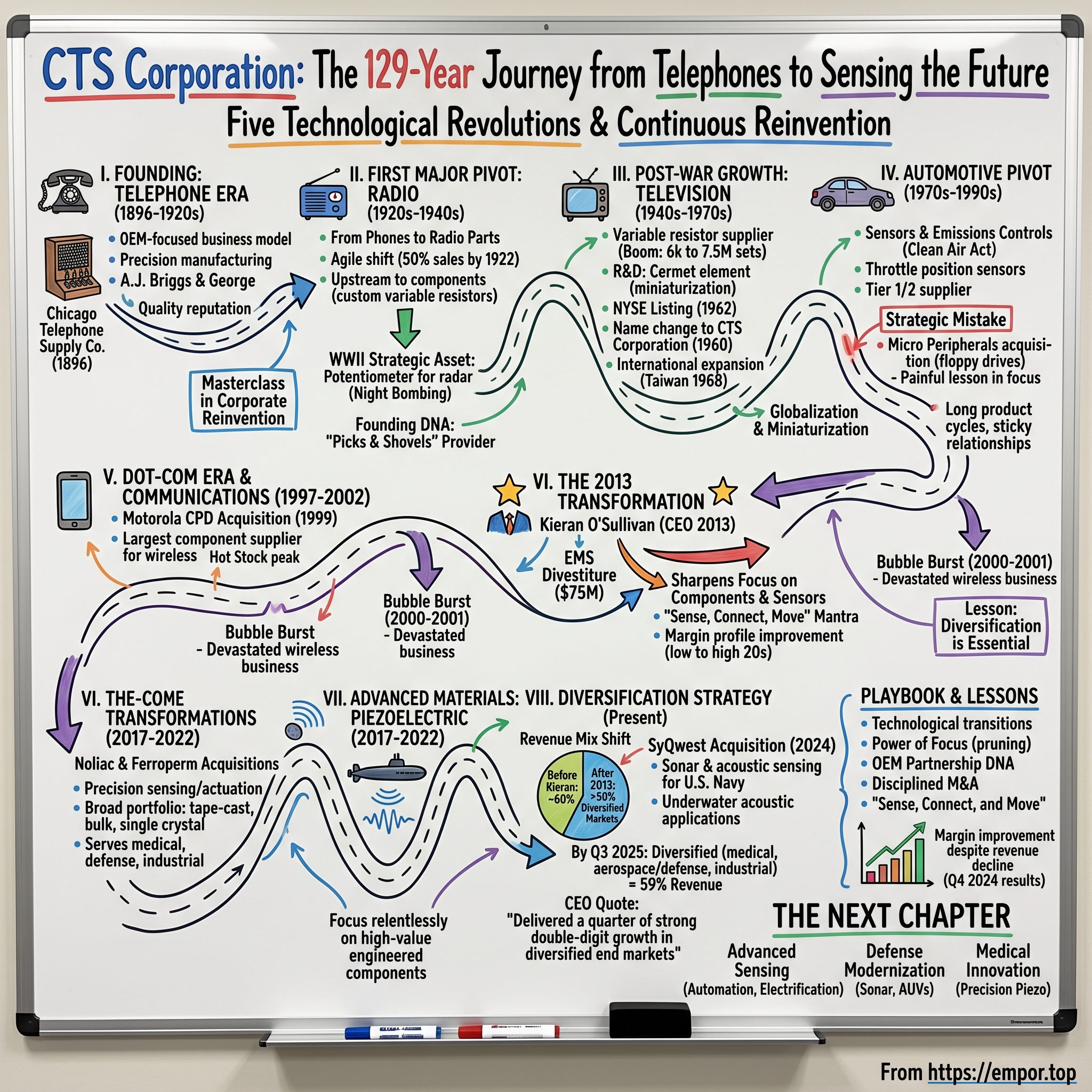

Picture Chicago in 1896: William McKinley campaigns for president promising "a full dinner pail," the Dow Jones Industrial Average hovers around 40 points, and the telephone remains a revolutionary technology that most Americans have never used. Into this world stepped A.J. Briggs and his son George, two entrepreneurs who founded the Chicago Telephone Supply Company to manufacture magneto-driven telephones and switchboards.

The company now known as CTS Corporation was founded in Chicago in 1896 by A.J. Briggs and his son, George, as Chicago Telephone Supply Company. It was established to make magneto-driven telephones and switchboards, which were sold either to telephone companies or to end consumers.

Fast forward 129 years, and that modest telephone manufacturer has transformed into something its founders could never have imagined. CTS Corporation is a leading designer and manufacturer of sensors, actuators, and electronic components primarily serving the transportation, industrial, medical, aerospace and defense, and communications markets. Headquartered in Lisle, Illinois, CTS employs approximately 3,549 people worldwide with a market capitalization of $1.223B.

The journey from telephone switchboards to submarine sonar systems spans five distinct technological epochs: the telephone era, the radio revolution, the television explosion, the automotive electronics transformation, and now the age of electrification and advanced sensing. Few industrial companies can claim such radical reinvention while maintaining an unbroken thread of core competency—precision engineering and OEM relationships that stretch back to the administration of the 25th President.

The central question this analysis explores is deceptively simple: How did a telephone company navigate through the Great Depression, two World Wars, the dot-com bubble, and the 2008 financial crisis to emerge as a critical supplier to Tesla's competitors and the U.S. Navy's submarine fleet? The answer lies in understanding CTS's unique DNA—a willingness to pivot aggressively while staying true to a narrow set of manufacturing competencies.

For long-term investors, CTS presents a fascinating case study in the tension between focus and diversification. Under CEO Kieran O'Sullivan's leadership since 2013, the company has systematically transformed its revenue mix, reducing dependence on the cyclical automotive sector while building positions in medical devices, aerospace, and defense. CTS Corporation today announced that its diversified business "with solid progress in the medical, industrial, and aerospace and defense markets, which now represent more than 50% of our revenue. We also delivered solid profitability improvements and strong cash flow in a challenging operating environment," said Kieran O'Sullivan, CEO of CTS Corporation.

II. Founding & Early History: The Telephone Era (1896–1920s)

The late 1890s witnessed a telecommunications arms race as hundreds of independent telephone companies competed against the Bell monopoly. The Briggs family spotted an opportunity: these independents needed reliable equipment suppliers who weren't captive to Bell interests.

The company quickly built a reputation for quality and product reliability by issuing certificates guaranteeing trouble-free service for the telephone equipment it manufactured. Needing larger facilities for its work force of 250 employees, the company moved 100 miles east to Elkhart, Indiana, in 1902. That city gave CTS a new building on a railroad spur in exchange for promised jobs and wages. For the next 18 years CTS would manufacture some 175,000 telephones and hundreds of switchboards.

The move to Elkhart represented more than a real estate decision—it established a pattern that would repeat throughout CTS's history. Rather than building expensive facilities in major urban centers, the company sought locations offering manufacturing advantages and community support. This Midwestern practicality would characterize CTS's approach for the next century.

By 1910, the company was producing a wide variety of telephone models, as well as 20 different types of switchboards ranging from apartment building size units up to express switchboards that could accommodate up to 300 telephone connections.

What set CTS apart during this period wasn't technological brilliance—the company manufactured commodity equipment. Rather, it was the establishment of an OEM-focused business model that persists today. From its earliest days, CTS sold to other businesses, not consumers. This created longer sales cycles but stickier customer relationships—a trade-off the company would embrace across every subsequent technology transition.

The DNA established in these formative years—precision manufacturing, OEM partnerships, geographic pragmatism, and quality-focused differentiation—would prove remarkably durable. When radio emerged as the next great communications platform, CTS possessed the organizational capabilities to pivot, even though the technology itself was entirely different from telephony.

For investors analyzing CTS today, this early history matters because it reveals the company's fundamental playbook: find an emerging technology wave, develop precision manufacturing capabilities for critical components, build deep OEM relationships, and ride the wave until the next transition arrives. The telephones were never the point—the manufacturing excellence and customer relationships were.

III. The First Major Pivot: From Phones to Radio Parts (1920s–1940s)

The roaring twenties brought America's first electronic consumer revolution. In 1920, KDKA in Pittsburgh became the first commercial radio station. By 1922, over 500 stations operated nationwide, and Americans scrambled to acquire receivers. CTS management recognized that their telephone business faced inevitable commoditization as Bell consolidated its monopoly, while radio represented virgin territory.

In the 1920s CTS redirected its efforts from telephones to radios. The radio communications market was emerging in the early 1920s, and by 1922 half of CTS's sales came from radio parts, including jacks, plugs, headphones, antenna switches, and rheostats.

The speed of this pivot is remarkable: within two years of radio's commercialization, CTS had already diversified half its revenue away from its founding product line. This agility stemmed from recognizing that the underlying skills—precision electrical component manufacturing—transferred directly to the new medium.

The 1930s marked an even more profound transformation. Rather than simply following customers into radio, CTS evolved its fundamental identity from a manufacturer of finished products to a component supplier.

During the 1930s CTS evolved from a manufacturer of finished products to a manufacturer of components. During the Great Depression CTS developed a more cost effective, stable carbon composition resistor that helped lower the cost of radios. CTS's custom variable resistor controls became the cornerstone of its business for the next 50 years.

This strategic shift—moving "upstream" to components—proved decisive for CTS's long-term survival. Finished product manufacturers faced brutal price competition and rapid obsolescence. Component suppliers, especially those with proprietary technology like CTS's carbon composition resistors, enjoyed higher margins and longer product cycles. The Depression, counterintuitively, forced CTS into a more defensible competitive position.

The last commercial telephone produced by the company was manufactured in 1940. By 1941 CTS was the largest producer of variable resistor products in the world.

World War II transformed CTS from a successful industrial supplier into a strategic asset for the United States military. During World War II the company developed a special precision potentiometer for radar units that gave the Allies their first capability to perform night bombing missions, thereby shortening the war.

The RLB potentiometer—enabling night bombing that historians credit with accelerating Allied victory—established CTS in the defense sector that would remain a growth engine eight decades later. The company's piezoelectric and sensing technologies today trace their lineage directly to this wartime work.

The investor lesson here is crucial: CTS's first successful reinvention validated a repeatable playbook. When a new technology emerges, CTS doesn't try to become a systems integrator or consumer products company. Instead, it identifies the precision components required by systems builders and develops proprietary manufacturing capabilities. This focus on being "the picks and shovels" provider across multiple gold rushes has proven far more durable than betting on any single technology.

IV. Post-War Growth & Going Public (1945–1970s)

America emerged from World War II with unprecedented manufacturing capacity and consumer demand. The television represented the quintessential post-war product: sophisticated technology that had matured during wartime, now ready for mass consumption.

CTS continued to develop the technology and products required by the radio market and the emerging television market in the 1940s and 1950s. Between 1946 and 1950 the number of television sets manufactured in the United States went from 6,000 to 7.5 million. Each set required from six to ten variable resistor components, and CTS supplied many of them.

The television boom represented CTS's third consecutive technology ride—telephone, radio, television—executed using the same playbook: precision component manufacturing for OEM customers. By the mid-1950s, CTS had successfully navigated fifty years of electronics evolution without changing its fundamental strategy.

The company's commitment to technological leadership intensified through internal R&D. In 1958 CTS engineers developed Cermet, a more stable resistance element that met the demand of miniaturized applications for military use. In 1960 the company officially changed its name to CTS Corporation, formally adopting the name by which it was generally known by the public. In 1962 CTS began trading its stock on the New York Stock Exchange.

The NYSE listing represented CTS's graduation from regional manufacturer to national public company. More importantly, the Cermet technology positioned CTS at the forefront of electronics miniaturization—the trend that would define the next half-century of technology development.

The next year CTS entered the data processing market by adapting Cermet technology to produce thick film fixed resistor networks, which became common components of computers during the 1960s. CTS met the demand for miniaturization of consumer electronic products by manufacturing hybrid microcircuits. In 1968 CTS established a manufacturing operation in Taiwan to serve the offshore production facilities of North American-based OEMs.

The Taiwan facility marked CTS's first significant international expansion and foreshadowed the globalization of electronics manufacturing. CTS leadership recognized that following customers offshore was essential for maintaining OEM relationships, even at the cost of operational complexity.

By 1970, CTS had evolved from a telephone manufacturer to a diversified electronic components supplier serving television, computer, military, and early consumer electronics markets. The pattern of riding technology waves while maintaining component-level focus had produced consistent growth across seven decades.

V. The Automotive Pivot: Sensors & Emissions Controls (1970s–1990s)

The 1970s introduced a new force into American industry: environmental regulation. The Clean Air Act of 1970 and subsequent automotive emissions standards created a massive market for sensors capable of monitoring and controlling engine performance. CTS, with its precision components expertise, spotted an opportunity that would reshape the company for the next fifty years.

When the U.S. government mandated emissions control standards for automobiles in the 1970s, CTS developed throttle position sensors and other sensor products for automobiles.

The automotive pivot represented CTS's most significant strategic bet since the radio transition. Unlike consumer electronics, which featured short product cycles and intense competition, automotive components required extensive qualification processes, multi-year contracts, and deep engineering partnerships with OEMs. Once CTS won a position on a vehicle platform, it could count on years of production revenue.

In the automotive market CTS's core product was its resistive contacting throttle position sensing device, which used the company's proprietary position-sensing technology. Other products developed for the automotive market included exhaust emission gas recirculating sensors, pintle position sensors, fuel pedal sensors, actuators for electronic throttle controls, and suspension shock height sensors.

The focused push into the automotive sensor market during the 1980s and 1990s proved highly successful. This strategic decision leveraged CTS's expertise in electronic components and positioned the company as a critical supplier to a global industry undergoing significant technological change, driving substantial revenue growth for decades.

The automotive expansion also brought CTS's most significant strategic mistake. In June 1983 CTS acquired California-based Micro Peripherals, Inc., a leading manufacturer of floppy disk drives for computers. By 1984 CTS had sustained significant losses in its floppy disk drive business and decided to divest Micro Peripherals. In January 1985, 15 months after acquiring Micro Peripherals, CTS found a buyer for the subsidiary.

The Micro Peripherals debacle taught CTS a painful lesson about staying in its lane. Floppy disk drives were finished products requiring consumer marketing and retail distribution—capabilities utterly foreign to CTS's OEM component model. The company had violated its seventy-year-old playbook and paid the price. Future management would cite this acquisition as justification for maintaining laser focus on components and sensors.

By the 1990s, CTS had established itself as a Tier 1 and Tier 2 supplier to major global automakers. CTS's Automotive Products division accounted for about 30 percent of the company's 1998 revenue. Once CTS completed its acquisition of Motorola's CPD unit, wireless communications products would account for about 40 percent of CTS's annual revenue.

The automotive foundation CTS built during this period remains central to the company today, though management has spent the past decade deliberately reducing its dominance in the revenue mix.

VI. The Dot-Com Era: Motorola Acquisition & Communications Boom (1997–2002)

The late 1990s wireless boom created what appeared to be a transformational opportunity for CTS. Mobile phones were experiencing exponential growth, base station infrastructure was deploying globally, and CTS possessed the precision RF component capabilities needed by wireless OEMs.

In 1997, CTS acquired Dynamics Corporation of America (DCA), adding frequency control products and thermal management capabilities. But the defining transaction came in 1999 with the acquisition of Motorola's Component Products Division (CPD).

As a result of its acquisition of Motorola's CPD unit, CTS enjoyed an 83 percent increase in revenue, from $370 million in 1998 to $677 million in 1999. The acquisition transformed CTS and positioned it as the largest manufacturer of electronic components for wireless applications in North America. The company was now a global leader for supplying components to the fast-growing mobile wireless industry and would pursue a strategy of globalization to enhance that position.

After the acquisition was completed in early 1999, CPD became CTS Wireless Components Inc. and the parent gained a portfolio of some 300 high technology patents globally as well as manufacturing facilities in China, Taiwan, and the United States.

Electronic Buyers' News named CTS as the best-managed company in the passive electronic components industry in its October 18, 1999, issue. The company's stock was also picked by Bloomberg's Personal Finance Magazine as one of the top 100 hot stocks for 1999.

At the peak of the dot-com bubble, CTS appeared positioned perfectly for the wireless future. Communications products represented nearly half of company revenue, and the growth trajectory seemed unlimited. Then came the crash.

The telecommunications bubble burst in 2000-2001 devastated CTS's wireless business. Suddenly, the company's greatest strength—concentration in communications—became its primary vulnerability. The painful lesson reinforced what Micro Peripherals had taught a generation earlier: diversification across end markets provides essential resilience.

The early 2000s represented a period of retrenchment and strategic soul-searching for CTS. Revenue declined from 2000's highs, and management faced difficult decisions about portfolio rationalization. The seeds of the 2013 transformation were planted during this challenging period, as leadership recognized that the company needed structural change to reduce volatility.

For investors, the dot-com era serves as a cautionary tale about concentration risk—a lesson that continues to inform CTS's current diversification strategy. The company's recent push to reduce transportation dependence below 50% of revenue reflects institutional memory of what happens when a dominant end market collapses.

VII. The 2013 Transformation: Kieran O'Sullivan & The EMS Divestiture

January 2013 marked the beginning of CTS's most significant strategic transformation since the 1920s radio pivot. Mr. O'Sullivan joined CTS in January 2013 as President and Chief Executive Officer and was appointed Chairman of the Board in May 2014. From 2006 until 2012, Mr. O'Sullivan served in several executive-level roles with Continental A.G., a global business focused on technology solutions and products for the transportation and mobility industries.

O'Sullivan brought precisely the perspective CTS needed: deep automotive industry experience combined with an outsider's willingness to question established practices. His prior role at Continental, one of the world's largest automotive suppliers, provided insight into what OEM customers truly valued—and what they didn't.

The new CEO wasted no time. Within months of his arrival, O'Sullivan orchestrated the most significant divestiture in CTS history.

CTS Corporation today announced that it has entered into a definitive agreement with Benchmark Electronics, Inc. under which Benchmark has acquired CTS' Electronics Manufacturing Solutions (EMS) business for $75 million in cash. Included are five manufacturing facilities located in Moorpark, CA, Londonderry, NH, Bangkok, Thailand, Matamoros, Mexico, and San Jose, CA and approximately 1,000 employees. The transaction sharpens CTS' focus on its Components and Sensors business.

The EMS divestiture embodied a counterintuitive strategic logic: CTS would become more valuable by becoming smaller. Among the biggest changes that CTS has implemented in recent years has been the divestiture of roughly 40 percent of the business to simplify its operations, focus on core areas and drive profitable growth. In 2013, the company sold off its Electronics Manufacturing Solutions business to Benchmark Electronics for $75 million. By selling that part of the business, CTS became better positioned to focus on the sensors, actuators and electronic components business.

The financial impact was immediate and dramatic. This past year has been a year of transition for CTS as we divested our EMS business, changed our margin profile from the low 20s to the high 20s and delivered improved financial results in each quarter.

O'Sullivan stated: "As an organization we have a very clear and deep strategy aligned with our board and investors, focused on products that Sense, Connect and Move. This is where we are focusing." The reorganization has created a smaller, more profitable company. It is leaner, more nimble and competitive globally. In addition to reducing the number of physical locations, the company reduced its corporate structure by 20 percent to improve cost efficiency.

The "Sense, Connect, and Move" mantra distilled CTS's value proposition into three words—an elegant simplification that guided subsequent acquisitions and organic investments. Products that didn't fit this framework became candidates for divestiture or deprioritization.

The 2013 transformation established the strategic playbook that guides CTS today: focus relentlessly on high-value engineered components, maintain OEM relationships but reduce customer concentration, improve margins through mix rather than volume, and deploy capital toward diversification rather than scale in any single market.

VIII. Building Piezoelectric Capabilities: The Noliac & Ferroperm Acquisitions

With the EMS divestiture complete and margins improving, O'Sullivan pivoted to acquisition-led growth focused on advanced materials capabilities. Piezoelectric technology—materials that generate electrical charges in response to mechanical stress, or conversely, deform when electrical voltage is applied—represented an ideal target. The technology enables precision sensing and actuation across medical, defense, and industrial applications, perfectly aligned with CTS's "Sense, Connect, and Move" strategy.

Noliac A/S was acquired by CTS Corporation in May 2017.

CTS Corporation has announced the acquisition of Noliac A/S; a designer and manufacturer of tape cast and bulk piezoelectric components, sensors and transducers. Headquartered in Denmark with manufacturing facilities in Denmark and the Czech Republic, Noliac serves OEMs in the aerospace & defense, test & measurement, medical and industrial markets. Founded in 1997, Noliac leverages twenty years of experience in piezoelectric multi-layer tape cast manufacturing to produce stacked actuators and other components.

The Noliac acquisition served multiple strategic objectives. First, it expanded CTS's European manufacturing and engineering presence, providing local support for European OEM customers. Second, it added tape-cast piezoelectric manufacturing—a distinct process capability complementing CTS's existing bulk piezoelectric production. Third, it brought diversified end-market exposure in medical and defense applications.

The piezoelectric buildout continued in 2022 with an even more significant acquisition. CTS Corporation completed the previously announced acquisition of Ferroperm Piezoceramics from Meggitt PLC for 525 million Danish Krone in cash.

Ferroperm joined the CTS Corporation family as Ferroperm Piezoceramics. In May, 2024, Ferroperm Piezoceramics merged with CTS Ceramics Denmark (formerly 'Noliac') under our current name 'CTS Denmark A/S'.

The Ferroperm acquisition—approximately $70 million at exchange rates at the time—brought CTS into the premium end of the piezoceramic market. More recently, a series of strategic acquisitions, particularly in piezoelectric technologies (Noliac, Ferroperm) and temperature sensing (TEWA), represent another transformation.

The strategic logic of combining Noliac and Ferroperm is compelling. Engineering expertise in areas like sensor technology, piezoelectric materials, and thermal management allows for highly customized, application-specific solutions that command value.

With three distinct piezoceramic technology platforms—tape-cast, bulk, and single crystal—CTS now possesses one of the broadest piezoelectric portfolios in the industry. This matters because different applications require different material characteristics. Medical ultrasound transducers, industrial flow sensors, aerospace actuators, and defense sonar systems each demand specific piezoelectric properties that CTS can now address from a unified technical platform.

The piezoelectric buildout positioned CTS for its most significant recent acquisition: entry into the naval defense market through underwater acoustic sensing.

IX. The Diversification Strategy: Reducing Transportation Dependence

For decades, CTS derived the majority of its revenue from transportation—primarily automotive, with growing commercial vehicle exposure. While this concentration provided stable, long-term platform contracts, it also subjected CTS to the brutal cyclicality of global vehicle production. The COVID-19 pandemic, semiconductor shortages, and EV transition uncertainty amplified these concerns.

O'Sullivan's response has been a sustained diversification campaign, executed through both organic investment and strategic acquisition. On Thursday, March 20, 2025, CTS Corp presented its strategic plans at the Sidoti Small-Cap Virtual Conference. CEO Kieran O'Sullivan outlined the company's focus on diversification and electrification, while addressing both growth targets and market challenges. CTS Corp aims for a 10% revenue growth, balancing organic expansion and acquisitions. CTS Corp targets a 10% revenue growth, with 5% from organic growth and 5% from acquisitions. The company is reducing its reliance on transportation, now 49% of revenue, to grow in medical, industrial, aerospace, and defense.

The 2024 acquisition of SyQwest represented the most dramatic diversification move to date. CTS completed the acquisition of SyQwest, LLC on July 29, 2024 for $125 million, net of cash and debt, and contingent consideration. SyQwest is a leading designer and manufacturer of a broad set of sonar and acoustic sensing solutions primarily for naval applications. "SyQwest adds strong technical capabilities and enhances our scale in underwater acoustic applications in the defense end market, further advancing our diversification strategy."

Headquartered in Cranston, RI, SyQwest is a leading designer and manufacturer of a broad set of sonar and acoustic sensing solutions primarily for the U.S. naval defense market. The Company's solutions aid in navigation, guidance, and situational awareness for destroyers, submarines, torpedoes, and autonomous underwater vehicles ("AUVs"). Supporting the Navy's modernization efforts and combat readiness, SyQwest is a critical link and trusted technology partner in the value chain for both government customers and prime contractors responsible for system integration. Founded in 2003, SyQwest specializes in the design, engineering and manufacturing of advanced underwater sensors and systems.

The SyQwest acquisition connects CTS's piezoelectric capabilities with high-value defense applications. This acquisition strengthens our strategy and scale in the defense end market, further advances our diversification strategy and brings an addressable market of approximately $500 million.

By Q3 2025, the diversification strategy showed clear results. The company reported 8% year-over-year revenue growth to $143 million. Diversified end markets, comprising medical, aerospace & defense, and industrial segments, grew revenue by 22% year-over-year and now account for 59% of total revenue.

CEO O'Sullivan stated: "We delivered a quarter of strong double-digit growth in our diversified end markets, with sales up 22% versus the prior year period. Diversified sales for the quarter were 59% of overall company revenue."

The numbers tell a clear story: CTS has successfully crossed the halfway point in its diversification journey. Transportation, which once represented over 60% of revenue, now accounts for approximately 41% as of Q3 2025. The strategic transformation that began with the 2013 EMS divestiture has fundamentally reshaped CTS's revenue composition and risk profile.

X. Current Business Model & Financial Profile

CTS Corporation is a leading designer and manufacturer of products that Sense, Connect and Move. CTS manufactures sensors, actuators and electronic components in North America, Europe and Asia, and provides engineered products to customers in the aerospace/defense, industrial, medical and transportation markets.

The 2024 financial results reflect both the challenges of automotive cyclicality and the benefits of diversification strategy. Net sales were $515,771 for the year ended December 31, 2024, a decrease of $34,651, or 6.3%, from 2023. The decline in net sales was primarily driven by a decreased volume of transportation products, which were down $51,077, or 16.9%. Net sales to the diversified end markets increased $16,425, or 6.6%. The SyQwest acquisition added net sales of $14,448 in 2024.

Net income was $58 million, or 11% of sales, compared to $61 million, or 11% of sales in 2023. Earnings per diluted share were $1.89, compared to $1.92 in 2023. Adjusted earnings per diluted share were $2.17, down from $2.22 in 2023. Adjusted EBITDA margin was 23%, up from 22% in 2023. Operating cash flow was $99 million, up from $89 million in 2023.

The margin improvement despite revenue decline demonstrates the quality-over-quantity strategic thesis: by shifting revenue mix toward higher-margin diversified end markets, CTS can improve profitability even when total revenue contracts. This is the core financial logic behind the diversification strategy.

CTS expects full-year 2025 sales to be in the range of $520-$550 million and adjusted diluted EPS to be in the range of $2.20-$2.35.

The balance sheet remains conservative. CTS maintained a strong financial position with $110 million in cash and $91 million in borrowed debt as of September 30, 2025. The company generated $73 million in operating cash flow year-to-date, consistent with the prior year, and $60 million in free cash flow after $13 million in capital expenditures.

CTS's capital allocation priorities reflect the strategic transformation. Our focus remains on strong cash generation and appropriate capital allocation and we continue to support organic growth, strategic acquisitions and returning cash to shareholders.

CTS returned $44 million to shareholders through dividends and share buybacks in the first three quarters of 2025.

The company's approach to M&A has been consistently disciplined. CTS has acquired 15 companies, including 5 in the last 5 years. It has also divested 1 asset. These bolt-on acquisitions—typically in the $50-$150 million range—extend capabilities or geographic reach without bet-the-company risk.

XI. Playbook: Business & Investing Lessons from 129 Years

1. Mastering Technological Transitions

CTS's longevity stems from a single consistent pattern: ride technology waves while maintaining core manufacturing competencies. From telephones to radios to TVs to military electronics to automotive sensors to EVs and submarine sonar, CTS has successfully navigated at least six major technology transitions by staying focused on precision components rather than finished products.

That ability to adapt to changes in technology and create new products has helped the company to survive in an industry where many others have not. Continued innovation at CTS led to a diversified base of products, which include hundreds of electronic components, sensors and switches.

2. The Power of Focus

The 2013 EMS divestiture exemplifies counterintuitive value creation: CTS became more valuable by becoming smaller. Selling 40% of revenue improved margins from the low 20s to high 20s by eliminating lower-margin contract manufacturing. The lesson applies broadly: portfolio pruning can create more value than acquisition-led growth.

3. OEM Partnership DNA

Since 1896, CTS has sold to other businesses, not consumers. This B2B focus creates longer sales cycles but stickier relationships. Major automotive platforms can run for 5-10 years, providing revenue visibility that consumer electronics companies can only dream about. The qualification barriers that frustrate new entrants protect incumbent suppliers.

4. M&A Discipline

CTS has avoided transformational acquisitions in favor of strategic bolt-ons. The Noliac, Ferroperm, and SyQwest acquisitions each added specific capabilities—tape-cast piezoceramics, premium piezoelectric materials, and underwater acoustics respectively—while remaining digestible for CTS's integration capabilities.

5. Geographic Diversification

Global manufacturing scale enables cost-effective production, regional customer support, and supply chain flexibility, a crucial factor demonstrated throughout 2024.

CTS's manufacturing footprint across North America, Europe, and Asia provides both cost optimization and customer proximity. As OEM customers globalized, CTS followed, maintaining local engineering and manufacturing support that competitors cannot easily replicate.

6. Product Philosophy: "Sense, Connect, and Move"

This three-word framework provides strategic clarity that guides portfolio decisions. Products that fit the framework receive investment; those that don't become divestiture candidates. Simple frameworks enable fast decision-making in complex organizations.

XII. Porter's Five Forces & Competitive Analysis

Threat of New Entrants: MODERATE-LOW

Engineering expertise in areas like sensor technology, piezoelectric materials, and thermal management allows for highly customized, application-specific solutions that command value.

The barriers to entering CTS's markets are substantial. Automotive qualification cycles run 12-24 months, requiring entrants to invest years before earning revenue. Medical and defense applications demand even more rigorous certification. CTS's proprietary manufacturing processes—particularly in piezoceramics—require accumulated know-how that cannot be easily replicated.

Bargaining Power of Buyers: MODERATE-HIGH

CTS serves large OEMs—automotive manufacturers, medical device companies, defense primes—that possess significant purchasing leverage. Customer concentration remains a concern: the largest customers likely account for meaningful revenue shares, though specific percentages are not disclosed. The strategic diversification effort partly addresses this risk by broadening the customer base across end markets.

Bargaining Power of Suppliers: MODERATE

Raw materials for sensors and electronic components—ceramics, rare earths, specialty metals—generally have multiple suppliers. However, some specialized piezoelectric materials may have limited sources, creating potential supply chain vulnerabilities that require active management.

Threat of Substitutes: LOW-MODERATE

Many CTS products serve regulatory-mandated applications (emissions sensors, safety systems) where substitution options are limited. Piezoelectric sensing remains difficult to replace in applications requiring its unique combination of precision, durability, and size. However, advancing semiconductor-based sensing technologies could eventually address some applications currently served by electromechanical sensors.

Competitive Rivalry: HIGH

CTS Corporation operates in several highly competitive electronic component markets, with different sets of competitors across its various business segments. In the transportation electronics segment, which represents CTS's largest revenue source, the company competes with larger automotive suppliers such as Continental AG, Bosch, and Sensata Technologies. These competitors offer broader automotive product portfolios, while CTS focuses on specialized sensors and actuators where it maintains strong market positions in specific applications. In the industrial and medical electronics segments, CTS faces competition from companies like TE Connectivity, Amphenol, and Honeywell.

While CTS lacks the scale of some larger competitors, its focused strategy on high-value engineered components for specific applications has enabled it to maintain strong positions in its target markets.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Limited. CTS operates at subscale relative to giants like TE Connectivity ($15B+ revenue) or Amphenol ($12B+ revenue). This size disadvantage is partially offset by focus on niches where scale matters less.

Network Effects: Not applicable. CTS's products are physical components without network characteristics.

Counter-Positioning: Partially applicable. CTS's component-only focus positions it differently than vertically integrated automotive suppliers. OEM customers may prefer CTS's independence from systems-level competition.

Switching Costs: Moderate-High. Automotive qualification processes create meaningful switching costs. Medical and defense applications require even more extensive re-qualification, making customer relationships sticky.

Branding: Limited. Industrial components sell on specifications and relationships, not consumer brand awareness.

Cornered Resources: Modest. CTS's piezoelectric technology portfolio—combining tape-cast, bulk, and single crystal capabilities—represents accumulated know-how that competitors cannot easily replicate.

Process Power: Moderate. CTS's 129-year history of precision manufacturing has developed process capabilities and institutional knowledge that create meaningful competitive advantages in quality and consistency.

XIII. Investment Framework: Key KPIs to Monitor

For investors tracking CTS's ongoing performance, three metrics matter most:

1. Diversified End-Market Revenue Percentage

This single metric captures the strategic transformation's progress. The journey from ~40% diversified revenue in 2013 to ~59% in Q3 2025 demonstrates execution against the stated strategy. Investors should track whether this percentage continues trending toward management's implicit target of 65-70%+.

Management has stated that diversified markets (medical, aerospace/defense, industrial) earn better margins than transportation. Therefore, each percentage point shift in revenue mix improves blended profitability—a leverage effect that compounds over time.

2. Adjusted EBITDA Margin

CTS targets ongoing margin improvement through mix shift and operational efficiency. The progression from low 20s (pre-2013) to 23%+ today reflects strategic execution. Sustainable margins above 23-24% would validate the diversification thesis; margin compression would suggest either execution challenges or competitive pressure.

3. Book-to-Bill Ratio by End Market

Forward indicators matter for cyclical businesses. The book-to-bill ratio—new orders divided by billed revenue—provides visibility into demand trends. CTS reports bookings data by end market, enabling investors to track whether diversification gains are sustainable. Strong bookings in medical, aerospace, and defense combined with stable-to-improving transportation bookings would support the investment thesis.

XIV. Risk Factors & Regulatory Considerations

Transportation Cyclicality: Despite diversification progress, transportation still represents ~41% of revenue. Global automotive production remains volatile, subject to economic cycles, semiconductor availability, and EV transition timing. A severe automotive downturn would materially impact CTS despite diversification efforts.

Customer Concentration: While CTS has broadened its customer base, specific concentration data is not disclosed. Material exposure to individual automotive OEMs or defense primes creates event risk that investors cannot precisely quantify.

Tariff & Trade Policy: CTS operates manufacturing facilities in Mexico, Asia, and Europe, creating exposure to trade policy changes. Tariffs, especially in Mexico, pose a challenge, but CTS plans to pass costs to customers. The ability to pass through tariff costs depends on customer relationships and competitive dynamics.

Defense Budget Exposure: The SyQwest acquisition increases CTS's exposure to U.S. defense spending patterns. The first full year of revenue from our SyQwest acquisition will introduce some seasonality where the timing of revenue may be influenced by approval of funding by the U.S. government.

Technology Risk: CTS's piezoelectric and electromechanical sensing technologies could face long-term substitution pressure from advanced semiconductor-based sensors. While current applications favor traditional sensing approaches, technology evolution requires ongoing R&D investment.

Environmental Liabilities: CTS has disclosed EPA-related costs. Q3 2025 included a $4.2 million charge related to the previously disclosed EPA past cost recovery claim. Historical manufacturing operations may create ongoing environmental remediation obligations.

XV. Bull and Bear Cases

Bull Case

-

Diversification Momentum Accelerates: If diversified end markets continue growing 20%+ annually while transportation stabilizes, CTS could achieve 70%+ diversified revenue by 2027-2028. This mix shift would drive margin expansion and reduce earnings volatility.

-

Defense Tailwinds: Growing U.S. and allied defense spending, particularly on submarine modernization and autonomous underwater vehicles, positions SyQwest for multi-year growth. CTS's combined piezoelectric and acoustic sensing capabilities could win platform positions across multiple Navy programs.

-

Medical Expansion: Piezoelectric technology enables therapeutic applications (ultrasound surgery, drug delivery) beyond traditional diagnostic ultrasound. CTS's premium Ferroperm materials position the company for high-margin medical growth.

-

EV Transition Creates Opportunity: While EV transition disrupts traditional powertrain sensors, CTS emphasizes "powertrain agnostic" products—pedal modules, position sensors, current sensors—that apply across ICE, hybrid, and battery-electric vehicles.

-

M&A Optionality: With leverage below 1x and strong cash generation, CTS retains capacity for additional bolt-on acquisitions that could accelerate diversification.

Bear Case

-

Automotive Cyclical Collapse: A severe global recession triggering 20-30% automotive production declines would overwhelm diversification benefits. Transportation revenue would collapse while fixed costs remain.

-

Defense Budget Cuts: Political priorities could shift defense spending away from naval platforms toward other priorities, limiting SyQwest's growth potential.

-

Competitive Pressure: Larger competitors like Sensata, TE Connectivity, and Amphenol possess greater scale, broader portfolios, and deeper customer relationships. Price pressure in commoditizing applications could compress margins.

-

Technology Disruption: Advancing MEMS (micro-electromechanical systems) and semiconductor-based sensing could eventually substitute for traditional electromechanical sensors in some applications.

-

Integration Risk: While CTS has successfully integrated small acquisitions, execution challenges with SyQwest or future acquisitions could destroy value.

-

Key Person Risk: CEO Kieran O'Sullivan has led CTS's transformation since 2013. Leadership transition—he is 62—creates uncertainty about strategic continuity.

XVI. Closing Thoughts: The Next Chapter

CTS Corporation's 129-year journey illuminates a fundamental business truth: survival requires reinvention, but sustainable reinvention requires strategic discipline. The company's success stems not from prescient technology bets—CTS has never been first to any technology wave—but from recognizing which waves to ride and maintaining the manufacturing excellence to serve OEM customers across multiple transitions.

The current strategic transformation, now entering its thirteenth year under O'Sullivan's leadership, represents CTS's most deliberate reinvention attempt. Rather than waiting for market forces to compel change, management has proactively reshaped the revenue mix, invested in advanced materials capabilities, and entered new end markets while the legacy automotive business remained profitable.

Whether this strategy succeeds depends on execution across multiple dimensions: continued organic growth in diversified markets, successful integration of acquisitions like SyQwest, maintenance of automotive market positions during the EV transition, and disciplined capital allocation as opportunities emerge. The early results are encouraging—diversified revenue crossing 50% of total, margins improving despite volume headwinds, balance sheet remaining conservative—but the transformation is incomplete.

For long-term investors, CTS offers exposure to several compelling themes: advanced sensing technologies enabling automation and electrification, defense modernization driving underwater acoustic demand, medical device innovation requiring precision piezoelectric components. The company's subscale position relative to larger competitors creates both risk (competitive disadvantage in commoditizing markets) and opportunity (acquisition target potential, niche dominance in specialized applications).

The fundamental question investors must answer is whether CTS's strategic clarity and execution capabilities can overcome its size disadvantages in a consolidating electronic components industry. The 129-year track record suggests the company possesses institutional DNA for adaptation. Whether that DNA produces superior returns in the coming decade depends on how skillfully management continues navigating the tension between focus and diversification that has defined CTS since the telephone era.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube