Solaris Energy Infrastructure: From Frac Sand Silos to AI Data Center Power

I. Introduction: The Fastest Pivot in Energy History

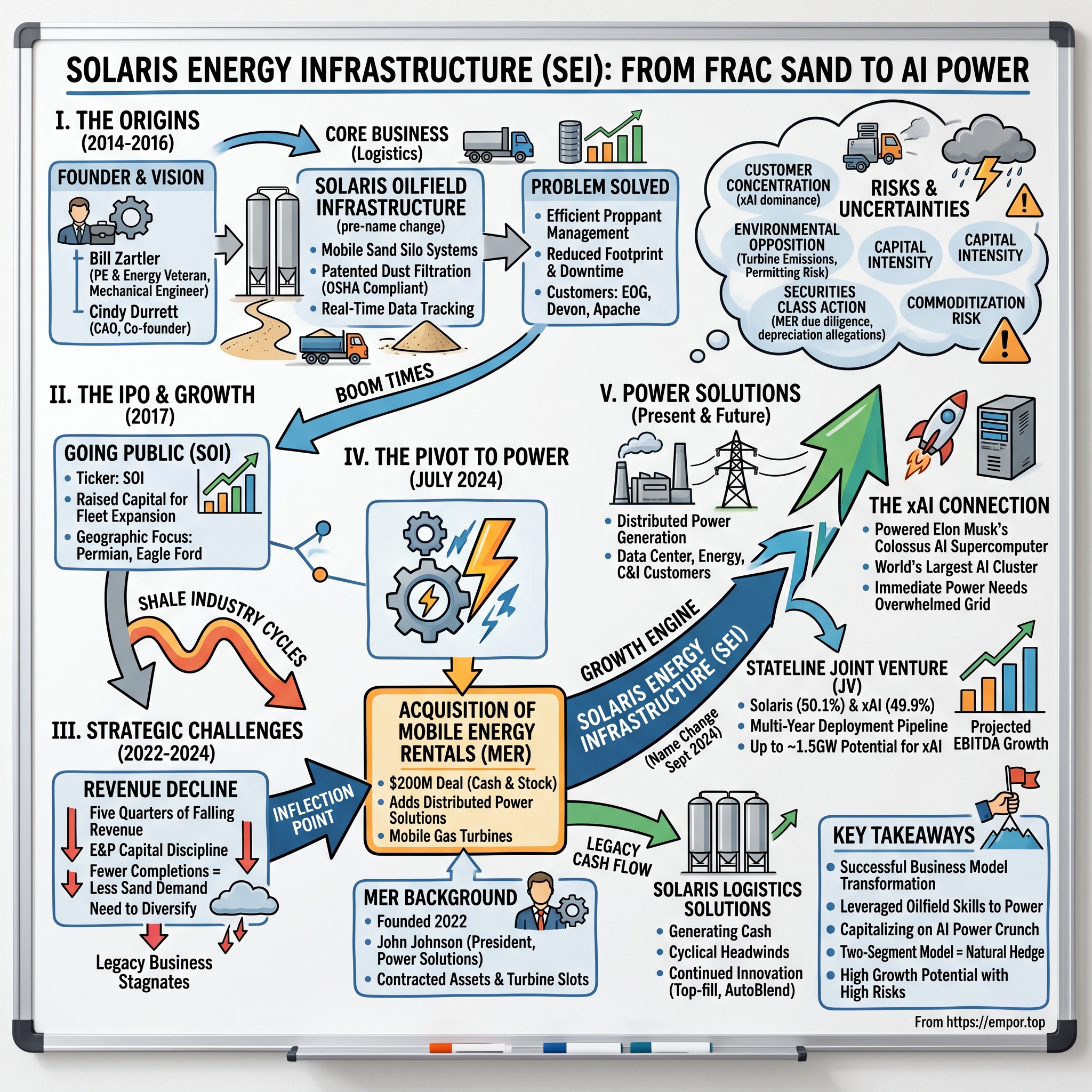

In the sweltering summer of 2024, something remarkable happened in the energy world. A company formerly known as Solaris Oilfield Infrastructure, Inc. changed its name to Solaris Energy Infrastructure, Inc. in September 2024. What had been a modest provider of sand silos to fracking operations suddenly found itself at the center of the most consequential technology buildout of our era: powering Elon Musk's AI supercomputers.

The numbers tell a striking transformation story. With trailing twelve-month revenue of $538.8 million and an enterprise value exceeding $3.1 billion, Solaris has undergone the kind of corporate reinvention that rarely succeeds in capital-intensive industries. In 2024, SEI's revenue was $313.09 million, an increase of 6.88% compared to the previous year's $292.95 million.

But this article isn't simply about a stock that has surged on AI enthusiasm. The central question is more fundamental: How did an oilfield sand logistics company—one that experienced five consecutive quarters of declining revenues—become a mission-critical supplier to what may be the world's largest AI training cluster?

The answer lies in understanding three converging forces: the shale revolution that created Solaris's original business, the punishing cyclicality that nearly destroyed it, and the unprecedented power crunch that provided a lifeline. Today, Solaris provides mobile and scalable equipment-based solutions for use in distributed power generation and management of raw materials used in the completion of oil and natural gas wells. The company operates in two segments: Solaris Power Solutions and Solaris Logistics Solutions.

This is a story about reinvention at an inflection point—about a founder who saw around corners, an acquisition that changed everything, and the largest bet any company has made on the proposition that AI's hunger for electricity will reshape the energy landscape. Whether Solaris's gambit succeeds or fails will tell us much about the future of distributed power and the sustainability of the AI boom itself.

II. The Founder & The Origin Story (2014-2016)

Bill Zartler: The Private Equity Energy Veteran

Every compelling business story begins with a protagonist whose biography explains the vision. Bill Zartler's background is unusually well-suited for the company he would build.

Prior to founding the Solaris Companies in 2014, Bill was a Founder and Managing Partner of Denham Capital Management, a global energy and commodities private equity firm. He led Denham's global investing activity in the midstream and oilfield services sectors and served on the investment and executive committees.

This wasn't merely a former banker dabbling in operations. Zartler had done the tours that mattered. Denham Capital managed over $7 billion in assets. While at Denham, Bill served on the boards of numerous portfolio companies, including NGL Energy Partners (NYSE:NGL), Gulf Atlantic Operations, Kitimat LNG, Freebird Gas Storage, Cadre Proppants, MS Energy Services and Greene's Energy Group.

The Cadre Proppants board seat is particularly revealing. Proppants—the specialized sand pumped into hydraulic fractures to hold them open—were becoming critical to the shale revolution. Zartler watched this market from the boardroom and understood both its promise and its pain points.

Previously, Bill held the role of Senior Vice President and General Manager at Dynegy Inc., building and managing the natural gas liquids business. Prior to that he held the roles of Feedstock Trading Manager and Business Analyst at Dow Hydrocarbons and Resources.

The Dynegy experience gave Zartler operational credibility in physical energy markets—the messy business of moving molecules from point A to point B. The Dow years taught him about feedstock logistics and the chemical industry's voracious appetite for reliable supply chains.

Bill received the Ernst and Young Entrepreneur of the Year award for the Gulf Coast Region in 2018. He earned a Bachelor of Science in Mechanical Engineering from The University of Texas at Austin and a Master of Business Administration from Texas A&M University.

The mechanical engineering degree matters. Solaris would be built on patented equipment, and Zartler could speak the language of design engineers, not just financial spreadsheets.

The Founding Vision

By 2014, Zartler had witnessed the shale revolution transform American energy. Horizontal drilling and hydraulic fracturing had unlocked previously inaccessible oil and gas reserves. But he'd also seen the operational chaos at wellsites—the logistics nightmare of moving millions of pounds of sand to remote locations on unpredictable schedules.

Headquartered in Houston, Solaris Oilfield Infrastructure was formed in 2014 to provide innovative and cost-effective oilfield products, services and infrastructure to enhance drilling, completions, efficiency and safety in North American shale plays. Solaris is the sole manufacturer and distributor of the Solaris Mobile Sand Silo System and the Mobile Transload System. All of Solaris' mobile storage and delivery systems feature patented dust filtration technology designed to reduce free-floating silica dust during operation.

The founding insight was elegant: vertical silos could store far more sand in a smaller footprint than horizontal storage containers, and mobile systems could be deployed to any wellsite rather than building permanent infrastructure. Since commencing operations in April 2014, we have grown our fleet from two systems to 33 systems. We currently have more demand for our systems than we can satisfy with our existing fleet.

Zartler didn't build Solaris alone. Cindy Durrett oversees the company's information technology, human resources, risk management and administrative functions. Prior to being named Chief Administrative Officer, Cindy was Vice President of Business Operations and was one of the founding leaders of Solaris in 2014. She brings over 30 years of midstream and oilfield services experience to Solaris. Prior to Solaris, she was the Director of Business Planning and Capital Projects for Cadre Proppants and was responsible for developing and leading several growth projects. Prior to Cadre, she served as Managing Director of Dynegy Midstream Services.

The Cadre Proppants and Dynegy connections weren't coincidental—Zartler was recruiting people who'd seen the same problems he had and shared his conviction that better engineering could solve them.

Investor Insight: Founder-market fit matters enormously in capital-intensive industries. Zartler's board experience at proppant and oilfield services companies gave him visibility into precisely the operational pain points Solaris would address. His private equity background meant he understood capital markets and could navigate an eventual IPO. This combination of operational insight and financial sophistication is rare and valuable.

III. The Core Business: Proppant Management Systems (2014-2017)

The Problem Being Solved

To understand Solaris's original business, you must first understand the scale of hydraulic fracturing operations. Hydraulic fracturing is used to stimulate hydrocarbon production. The process involves the injection of water, proppants, and chemical additives into the formation to fracture the surrounding rock, increase permeability and stimulate production. According to Solaris's estimates, current horizontal well completion designs require between 400 and 1,000 truckloads of proppant delivered to the well site per well.

Consider that math: a single well might need 1,000 truckloads of sand. A drilling rig completing multiple wells on a pad could require continuous sand delivery for weeks. Any interruption—truck traffic delays, weather, equipment failures—meant expensive downtime for the entire completion operation.

The traditional approach used horizontal storage containers called "sand boxes" that took up enormous footprints at the wellsite. Trucks would arrive, dump sand into these containers, and the sand would be conveyed to the blender and ultimately pumped downhole. The system worked, but inefficiently.

This new 12-silo system recently was used to successfully complete a "zipper" frac of two wells on a pad in the Permian Basin. The system delivered sand at an average rate of nearly 23,000 pounds per minute into two blenders simultaneously. The Solaris system was used to complete 34 frac stages and deliver 30 million pounds of sand during the four-day completion of both wells. During a single 24-hour period, the system delivered nearly 9 million pounds of sand to the wells.

The Technology Advantage

Solaris's innovation centered on vertical storage—50-foot-tall silos that could store the same amount of sand in a fraction of the footprint. As of June 30, 2018, Solaris had 131 systems in the fleet, all of which were deployed to customers. Storage-wise, Solaris' standard Mobile Proppant Management System has 2.5 million pounds of vertical proppant storage capacity. This is considerably smaller than traditional or competing well site proppant storage equipment.

But the real value proposition went beyond footprint reduction. The system samples more than 1,400 data points, aggregating and trending proppant inventory levels and consumption rates in real time. The Solaris Sand Controls System provides superior control of sand flow by indicating real-time sand storage levels and broadcasting a live feed of comprehensive data to a durable touch screen located outdoors at the frac site, to laptops inside the data van and to remote mobile devices.

The 12-pack system provides 5 million pounds of proppant storage, allowing 25 hours of inventory buffer and can deliver sand at an average rate of over 35,000 pounds per minute. The systems are designed to be OSHA compliant throughout the entire proppant path at the wellsite, so operators can safely operate within all silica dust regulations. From silo filtration cabinets and tarps to local exhaust ventilation units on top of silos and fully automated sand delivery, the technologies reduce the amount of silica dust, prevent spillage and remove personnel from high-exposure areas.

The OSHA compliance feature would prove increasingly valuable. Regulatory scrutiny of silica dust exposure at wellsites intensified through the mid-2010s, and Solaris's patented dust control technology provided customers with both safety and regulatory benefits.

Customer Base and Geography

The systems reduce customers' cost and time to complete wells by improving the efficiency of proppant logistics, in addition to enhancing well site safety. Customers include oil and natural gas exploration and production companies, such as EOG Resources, Inc., Devon Energy and Apache Corporation, as well as oilfield service companies, such as ProPetro Services, Inc.

The customer list was impressive—EOG, Devon, and Apache were among the most sophisticated operators in North American shale. Winning their business validated Solaris's technology proposition.

Systems are deployed in many of the most active oil and natural gas basins in the U.S., including the Permian Basin, the Eagle Ford Shale and the SCOOP/STACK formation.

The geographic concentration in the Permian Basin, America's most prolific oil-producing region, positioned Solaris in the industry's center of gravity. This wasn't an accident—Zartler understood that being close to the most active basins meant shorter mobilization times and more efficient fleet utilization.

The Competitive Moat

The manufacturing strategy reinforced the technology advantage. Building equipment in-house rather than sourcing from third parties gave Solaris control over quality and rapid response to customer needs. The patented designs created barriers to direct copying, though competitors would eventually develop alternative vertical storage solutions.

Investor Insight: Solaris's original business demonstrated classic characteristics of a quality oilfield services company: patented technology, blue-chip customer relationships, and operational leverage from fleet expansion. However, the fundamental challenge remained: demand was entirely dependent on the cyclical oil and gas industry, creating inherent earnings volatility that the company couldn't control.

IV. The IPO: Going Public in the Shale Boom (2017)

IPO Dynamics

By early 2017, Solaris was ready for the public markets. The shale industry was recovering from the 2014-2016 oil price collapse, completion activity was accelerating, and demand for Solaris's systems exceeded supply.

Solaris was incorporated as a Delaware corporation in February 2017. Following this offering and the related transactions, we will be a holding company whose sole material asset will consist of membership interests in Solaris LLC. Solaris LLC owns all of the outstanding equity interest in the subsidiaries through which we operate our assets. After the consummation of the transactions contemplated by this prospectus, we will be the sole managing member of Solaris LLC.

The Up-C structure—a holding company atop an LLC—was designed for tax efficiency, allowing existing owners to retain their partnership interests while new public shareholders acquired Class A stock. This structure would become relevant later when the company used Class B shares to acquire Mobile Energy Rentals.

Solaris Oilfield Infrastructure aimed to sell 10.6 million Class A common shares at a midpoint price of $16.50 per share for gross proceeds of $175 million in its IPO. Solaris rents mobile fracking services equipment to the oilfield services industry. While the company is profitable and cash flow positive, management was proposing to sell shares at a post-IPO market cap of $722 million on $18 million in revenues for a nearly 40x Price/Sales multiple.

Skepticism and Valuation

The proposed valuation raised eyebrows. Direct competitor National Oilwell Varco (NOV) has a Price/Sales multiple of 1.88x, so analysts failed to see compelling justification for Solaris's sky-high valuation expectations.

The skepticism was understandable. A 40x sales multiple for a company selling into the notoriously cyclical oilfield services market seemed aggressive. With 2016 revenues of $18.2 million, management was proposing investors pay an astronomically high 39.7x Price/Sales multiple.

Solaris has only one major outside investor, private equity firm Yorktown Energy Partners, which will own 46.4% of Class B stock post-IPO.

We have a valuable relationship with Yorktown Partners LLC, a private investment firm investing exclusively in the energy industry with an emphasis on North American oil and gas production and midstream and oilfield service businesses. Yorktown Partners LLC has raised 11 private equity funds with aggregate partner commitments totaling over $8 billion. Yorktown Partners LLC's investors include university endowments, foundations, families, insurance companies, and other institutional investors.

Yorktown's backing provided credibility—they were experienced energy investors who had been involved with Solaris since the early days.

The Public Debut

The IPO priced at $12 per share on May 11, 2017—below the marketed range of $15-$18, suggesting institutional investors demanded a discount to the proposed valuation. The stock traded on the New York Stock Exchange under the ticker symbol "SOI." Credit Suisse and Goldman Sachs served as the lead underwriters.

Despite the pricing discount, the offering succeeded. Solaris raised the capital needed to expand its fleet, and the public currency would later prove valuable for acquisitions and employee retention.

The rapid fleet expansion validated the growth thesis. The company grew from 33 systems at founding to a fleet that would eventually exceed 130 systems, generating scale economies and demonstrating that demand for its technology was real.

Investor Insight: The IPO skepticism proved partially warranted—the stock would trade below its IPO price for extended periods during the 2022-2024 downturn. However, the Up-C structure and public currency would prove essential for the transformative MER acquisition in 2024. Sometimes corporate structures designed for one purpose (tax efficiency) create optionality for entirely different strategic moves years later.

V. The Shale Industry Cycles: Boom, Bust, and Recovery (2017-2022)

Riding the Shale Wave

The years following Solaris's IPO brought both vindication and volatility. The company expanded its offerings beyond simple sand storage, developing integrated solutions for the entire proppant supply chain.

The transloading business represented a natural adjacency. Sand mined in Wisconsin or Texas had to reach well sites in the Permian or other basins, often via rail. Transload facilities—where sand was transferred from rail cars to trucks—were critical choke points.

Solaris' patented equipment and systems are deployed in many of the most active oil and natural gas basins in the United States, including the Permian Basin, the Eagle Ford Shale, and the STACK/SCOOP. Solaris' high-capacity transload facility, being built in Kingfisher, Oklahoma, will serve customers with operations in the STACK/SCOOP.

Software solutions expanded the value proposition further. Real-time inventory tracking, consumption analytics, and logistics optimization tools transformed Solaris from an equipment rental company into an integrated supply chain manager.

Industry Cyclicality Challenges

The oilfield services industry is defined by its cyclicality. When oil prices rise, drilling activity accelerates, completion crews work overtime, and equipment providers like Solaris see surging demand. When prices fall, the opposite occurs with brutal speed.

The 2020 COVID-19 crash demonstrated this vividly. Oil prices briefly went negative, and completion activity collapsed. Even well-capitalized operators slashed spending, idling equipment and deferring well completions.

Solaris reported net loss of $1.3 million, or $(0.04) per diluted Class A share, for full year 2021, compared to full year 2020 net loss of $51.1 million, or $(1.03) per diluted Class A share. Adjusted pro forma net loss for full year 2021 was $2.6 million, or $(0.06) per fully diluted share, compared to full year 2020 adjusted pro forma net loss of $6.6 million, or $(0.15) per fully diluted share.

The 2020 loss of $51 million represented a severe stress test. Yet Solaris survived where weaker competitors didn't.

Shareholder Returns Focus

What distinguished Solaris during this period was its commitment to shareholder returns even through the downturn. "Solaris has a strong record of returning cash to shareholders. We have returned approximately $112 million since 2018 through dividends and share repurchases and were one of the few companies in our industry that maintained its dividend through all points of the cycle," Solaris' Chairman and Chief Executive Officer Bill Zartler commented. "Our recent investments in new technology have increased, and we expect will continue to increase, Solaris' cash flow. We plan to return at least 50% of free cash flow to shareholders through dividends and share repurchases."

Since initiating the dividend in December 2018, the Company has paid 18 consecutive quarterly dividends and repurchased approximately 9% of total outstanding shares. Cumulatively, the Company has returned approximately $131 million in cash to shareholders through dividends and share repurchases since December 2018.

Maintaining the dividend through the cycle was unusual in oilfield services, where most competitors suspended or eliminated dividends during downturns. This discipline signaled management's confidence in the business model and their respect for shareholder capital.

By late 2024, that cumulative return figure would grow significantly. Approximately $15 million remains under the current share repurchase authorization. Pro forma for the announced fourth quarter 2024 dividend, Solaris has returned approximately $190 million to shareholders through dividends and share repurchases.

Investor Insight: Solaris's dividend discipline through the cycle demonstrated management's capital allocation priorities. However, the fundamental challenge remained unsolved: the business was hostage to oil and gas prices and completion activity levels, neither of which management could control. No amount of operational excellence could change that structural vulnerability.

VI. Inflection Point #1: The Revenue Decline (2022-2024)

The Legacy Business Crumbles

By late 2022, the warning signs were unmistakable. Despite robust oil prices, completion activity began declining as E&P companies prioritized capital discipline and shareholder returns over production growth.

The market dynamics had shifted fundamentally. Where shale operators once drilled aggressively to build production, they now maintained flat production while returning cash to investors. Fewer wells meant less demand for proppant, which meant less demand for Solaris's equipment.

The revenue decline accelerated through 2023. Quarter after quarter, the numbers moved in the wrong direction. By January 2024, the situation had reached crisis proportions. The share price tumbled to a multi-year low, trading dramatically below the original IPO price.

For a company that had maintained its dividend through COVID-19 and the oil price collapse, this was existential. The legacy business model—providing proppant management systems to an increasingly disciplined oil and gas industry—was structurally impaired.

SEI has enjoyed rapid growth as it transitions from oilfield services to distributed power. In FY 2024 the company reported Q4 revenue of $96 million, net income $14 million and adjusted EBITDA $37 million. FY 2024 revenue growth reflected strong demand for its mobile power fleet and increased adoption of its last-mile logistics solutions.

The shift in completion activity created a strategic imperative: Solaris needed to diversify away from its dependence on the cyclical oil and gas industry. But pivoting a capital-intensive equipment business is easier said than done.

The completion efficiency gains that benefited E&P companies hurt Solaris. As operators learned to complete wells faster with fewer stages, proppant intensity per well actually declined in some basins. Technology improvements that helped customers directly hurt Solaris's utilization rates.

"The Solaris Logistics Solutions segment has demonstrated a strong rebound in activity early in 2025 relative to the seasonal softness experienced in the fourth quarter."

Management's response demonstrated both realism and creativity. They acknowledged the cyclical headwinds while emphasizing the company's technology advantages and customer relationships. But internal discussions were surely more urgent: without diversification, Solaris faced a long, slow decline tied to an industry that had fundamentally changed.

Investor Insight: The 2022-2024 revenue decline illustrated a harsh reality about oilfield services: structural changes in customer behavior can devastate even well-run equipment providers. Solaris's technology remained excellent, customer relationships remained strong, but the addressable market was shrinking. This created both pressure to act and an opening for bold strategic moves.

VII. Inflection Point #2: The MER Acquisition & Pivot to Power (July 2024)

The Transformative Deal

July 9, 2024 marked the inflection point that would define Solaris's future. Solaris' Chairman and Chief Executive Officer Bill Zartler commented, "We are excited to welcome the MER team to Solaris and expand our mobile infrastructure solutions offering. MER's solutions complement our all-electric offering and provide access to new end-market opportunities, including oil and gas production, midstream and downstream activities as well as various C&I applications. As we evaluate the 'electrification of everything' and computing power growth needs, we believe reliable power access will become a growing challenge that larger scale, distributed power generation assets are well-positioned to address."

Solaris Energy Infrastructure Inc. has completed its acquisition of Mobile Energy Rentals LLC (MER). The $200 million deal, first announced in July, adds critical distributed power infrastructure solutions and multiple end markets, including oil and gas production and midstream and downstream activities to Solaris' portfolio. The deal creates a pro forma business mix with more than 50% distributed power infrastructure.

The deal structure was clever. Consideration for the transaction included $60 million in cash and 16.5 million shares of Solaris Class B common stock to MER's founders and management team. To grow MER's distributed power fleet, Solaris also entered into a $325 million senior secured term loan and is finalizing a $75 million revolving credit facility.

The MER Story: From Tiny Startup to Acquisition Target

The origins of Mobile Energy Rentals reveal how quickly opportunities can emerge in rapidly changing markets. MER was founded in 2022 and, like Solaris, is based in Houston, Texas.

Founded in 2022 and based in Houston, Texas, MER provides configurable sets of primarily natural-gas powered mobile turbines and ancillary equipment to energy, data center and other C&I end-markets. MER's solutions provide reliable and cost-effective power where grid infrastructure may not be available or is unreliable.

John Johnson serves as President for Power Solutions, and brings more than thirty years of energy generation, transmission, and distribution experience to Solaris. John was the founder and a co-owner of Mobile Energy Rentals, LLC ("MER"), and prior to founding MER, he founded J-Turbines, Inc.

Johnson's background in turbine equipment gave MER technical credibility. John A. Johnson, MER founder and co-owner said, "We recognize significant value in Solaris' existing offering, including a complementary field service team that is skilled in mobilizing and commissioning electric equipment, as well as engineering and manufacturing capabilities that can provide synergies for our business".

The strategic logic was compelling: MER had contracted customers and turbine delivery slots; Solaris had capital, public company infrastructure, and field service capabilities. Together, they could scale faster than either could alone.

At closing, MER's fleet totaled 153 MW of mobile turbines, with orders placed to expand capacity to 478 MW by Q3 2025. MER generated ~$50M in run-rate EBITDA, implying Solaris paid only ~4x EBITDA, well below infrastructure peer multiples. By combining MER's contracted growth with Solaris' engineering, manufacturing, and field service capabilities, SEI positioned itself to scale quickly.

The xAI Connection: Elon Musk's AI Power Needs

The timing of the MER acquisition coincided with one of the most audacious construction projects in technology history. Colossus is a supercomputer developed by xAI. Construction began in 2024 in Memphis, Tennessee, and operation started in July 2024. It is currently believed to be the world's largest AI supercomputer. Its primary purpose is to train the company's chatbot, Grok.

Colossus was launched in September 2024 at a former Electrolux site in South Memphis to train the AI language model Grok. Reportedly, within 19 days of the project's conception, xAI was ready to begin construction. In comparison, other data centers have taken an average of four years to finalize the plans for a project, ship the equipment, and have it installed. The site was chosen because the abandoned Electrolux building could be repurposed to expedite construction.

It was originally powered by 100,000 Nvidia graphics processing units (GPUs) and was constructed in 122 days. Three months after the first 100,000 GPUs were deployed, xAI announced that they had increased the system to 200,000 GPUs and that they intended to continue increasing the computer's processing power to 1 million GPUs.

The power requirements were staggering. At the site of Colossus in South Memphis, the grid connection was only 8 MW, so xAI applied to temporarily set up more than a dozen gas turbines which would steadily burn methane gas from a 16-inch natural gas main.

According to advocacy groups, aerial imagery in April 2025 showed 35 gas turbines had been set up at a combined 422 MW.

Why Mobile Gas Turbines for Data Centers?

The power challenge facing AI data centers is unlike anything the tech industry has encountered. Traditional data centers connect to the electrical grid and scale gradually. AI training clusters require enormous power immediately—often in locations where grid infrastructure cannot deliver sufficient capacity for years.

To deploy faster than peers, xAI relies on rental turbine companies. NYSE-listed Solaris Energy Infrastructure owns a fleet of 600MW of gas turbines, of which ~400MW currently serve xAI.

Mobile gas turbines offered a solution: deploy generators at the site, connect them to natural gas pipelines, and deliver power within weeks rather than years. The turbines are technically "portable," which initially allowed them to sidestep some permitting requirements.

According to specifications from Solaris Energy Infrastructure (SEI), the Houston-based company installing the turbines, the machines emit pollutants including nitrogen oxides and formaldehyde—substances linked to increased respiratory illness and long-term health risks. Solaris markets itself as a rapid-deployment energy firm for data centers and industrial operations with large, immediate power needs.

For Solaris, the xAI relationship validated the entire strategic pivot. A customer willing to pay premium prices for immediate power delivery represented exactly the market opportunity Zartler had identified.

Investor Insight: The MER acquisition represented a calculated bet on the proposition that AI's hunger for electricity would create sustained demand for distributed power solutions. The 4x EBITDA purchase multiple was attractive, but the real value lay in the contracted turbine deliveries and customer relationships. Whether this was brilliant timing or lucky coincidence, the result was transformational.

VIII. The New Two-Segment Business Model (2024-Present)

Segment 1: Solaris Logistics Solutions (Legacy Business)

The Solaris Logistics Solutions segment designs and manufactures specialized equipment; and offers field technician support, last mile, and mobilization logistics services, as well as provides software solutions to oil and natural gas operators and their suppliers.

The legacy business hasn't disappeared—it continues generating cash flow while facing cyclical headwinds. The technology advantages remain: patented silo systems, real-time monitoring software, and dust control solutions that competitors struggle to match.

System activity in the logistics segment saw a 25% sequential increase, driven by seasonal rebound, new customer wins, and the adoption of the top-fill system. The company's silo systems are capable of handling increased throughput, contributing to the success of the top-fill system, which was effectively sold out in Q1 2025. Approximately 75% of logistics locations are now equipped with both legacy SAN silo and top-fill systems, doubling earnings potential at the well-site level.

New product introductions like the top-fill system demonstrate continued innovation. The AutoBlend integrated e-blender technology represents the electrification trend even within the traditional oilfield business—customers increasingly want all-electric completion equipment to reduce emissions and operating costs.

Segment 2: Solaris Power Solutions (Growth Engine)

The Solaris Power Solutions segment offers configurable all-electric natural gas-powered mobile turbines and ancillary equipment to data center, energy, exploration and production, oilfield services, and other commercial and industrial sector customers.

The Power Solutions segment has become the dominant growth driver. By Q4 2024, the segment's revenue had grown to $34 million, with Adjusted EBITDA hitting $24 million. These figures are projected to rise sharply as operational capacity expands: from 260 MW in Q4 2024 to an estimated 420 MW by Q2 2025.

The financial trajectory has been extraordinary. Q3 2025 revenue was $167M, net income $25M and EBITDA $68M. EBITDA outlook is $65–$70M; $0.12 dividend December 18, record December 8; issued approximately $748M 0.25% notes due 2031.

The centerpiece of SEI's presentation was its ambitious growth strategy, targeting expansion from the current 760 MW average capacity to 2,200 MW by early 2028. This expansion is expected to more than double the company's Adjusted EBITDA potential.

The xAI Joint Venture

The relationship with xAI evolved beyond simple equipment rental into a structural partnership. Musk's firm weighs 67% of SEI's 1,700MW orderbook, i.e. 1,140MW. There are ~240MW on the Memphis Colossus 1 site, while the remaining 900MW will be owned by a Joint Venture owned at 50.1% by Solaris and 49.9% by xAI.

Solaris and a major data center client entered into a joint venture, Stateline Power, LLC (the "JV").

The JV has executed a term sheet and is finalizing definitive documentation for up to $550 million in the form of a senior secured term loan facility which is expected to support a majority of the capital needs of the JV. The Company's first quarter expenditures included its cash equity investment in the JV and the partner will contribute its pro rata share of cash equity in the second quarter of 2025. Ownership Structure – No change to previously announced structure of 50.1% Solaris-owned and 49.9% customer-owned.

Solaris expects to have over 1.1GW of fully operating turbines for xAI by Q2 2027. There remains ~425MW available for contracting, and analysts think xAI will likely pull the trigger to get to over 1.5GW of total gross power.

The joint venture structure aligns incentives between Solaris and xAI while sharing the capital burden of the massive expansion. For Solaris, it provides visibility into a multi-year deployment pipeline. For xAI, it ensures dedicated capacity for its computing ambitions.

Investor Insight: The two-segment structure creates natural hedging. When oil and gas activity is weak, the Power Solutions segment provides growth. When (eventually) AI data center demand stabilizes, the logistics business may benefit from a completion activity recovery. However, the customer concentration risk is undeniable—a change in xAI's strategy or financial position could significantly impact Solaris.

IX. The AI Data Center Power Opportunity

The Colossus Supercomputer and AI Arms Race

To understand Solaris's opportunity, you must understand the scale of what xAI and other AI companies are building. As of June 2025, the supercomputer consists of 150,000 H100 GPUs, 50,000 H200 GPUs and 30,000 GB200 GPUs. Another 110,000 GB200 GPUs are to be brought online at a second data center also in the Memphis area. The expansion of this supercomputer has already been discussed and will be the second phase of the project. It is stated that it will add 320 new jobs. Not only that, but in its expansion, xAI also plans to increase Colossus to 1 million graphics processing units.

This marks the second major data center xAI has launched in Memphis. The first — a 300 MW facility built in just 122 days by retrofitting a shuttered Electrolux plant — is currently the world's largest operational AI training cluster.

The broader industry context is crucial. "Global electricity demand from data centres is set to more than double over the next five years, consuming as much electricity by 2030 as the whole of Japan does today. The effects will be particularly strong in some countries."

The IEA's Base Case finds that global electricity consumption for data centres is projected to double to reach around 945 TWh by 2030, representing just under 3% of total global electricity consumption in 2030. From 2024 to 2030, data centre electricity consumption grows by around 15% per year, more than four times faster than the growth of total electricity consumption from all other sectors. Electricity consumption in accelerated servers, which is mainly driven by AI adoption, is projected to grow by 30% annually in the Base Case.

The Grid Can't Keep Up

The fundamental problem facing AI companies is time. Grid infrastructure takes years to build; AI training clusters need power in months.

"It used to be the case a 50 megawatt data center was pretty big. Now, it's very common to have data centers that are 20 times that size — that are a gigawatt." Grid Strategies, a power sector consulting firm, estimates 120 gigawatts of additional electricity demand by 2030. This includes 60 gigawatts from data centers based on forecasts from the utilities. To put that in perspective, 60 gigawatts is roughly equivalent to the 2024 peak hourly power demand of Italy, the world's eighth-largest economy.

The explosion in interest in generative artificial intelligence has resulted in an arms race to develop the technology, which will require many high-density data centers as well as much more electricity to power them. Goldman Sachs Research forecasts global power demand from data centers will increase 50% by 2027 and by as much as 165% by the end of the decade (compared with 2023).

To meet AI systems' growing demand for computational resources, AI data centers could need 68 gigawatts of power capacity by 2027—close to the current total power capacity of the state of California. Larger training runs and widespread deployment of future artificial intelligence (AI) systems may demand a rapid scale-up of computational resources (compute) that require unprecedented amounts of power.

This gap between AI ambition and grid capacity creates Solaris's market opportunity. Companies that can deliver power quickly—regardless of grid availability—fill a critical need.

Expansion Beyond xAI

While xAI represents Solaris's anchor customer, management has emphasized diversification efforts. In the final four months of 2024, a single hyperscale data center contract accounted for 96% of Power Solutions revenue. By mid-2025, SEI had expanded to six customers, but xAI still dominated the order book.

Kyle Ramachandran noted that the 70 megawatts went to an existing high-quality midstream operator. While the duration is shorter than data center contracts, the pricing is more attractive. Solaris is balancing holding capacity for larger data center contracts with deploying capacity to meet immediate demand.

The diversification into midstream and industrial customers reduces concentration risk while maintaining the distributed power growth thesis. These customers need reliable power in remote locations—exactly the proposition that mobile turbines deliver.

Investor Insight: The AI power opportunity is enormous but faces significant uncertainties. Questions about AI adoption pace, efficiency improvements, and competitive dynamics remain unresolved. Solaris has positioned itself as an early mover, but the distributed power market could become commoditized if demand growth slows or competitors scale rapidly.

X. Risks, Controversies, and Legal Matters

Environmental Opposition

The xAI turbine deployment has generated significant controversy in Memphis. Elon Musk's artificial intelligence startup, xAI, has secured a permit to operate natural gas-burning turbines at its controversial supercomputer facility in Memphis, Tennessee, despite mounting public opposition and legal pressure. The permit, issued by the Shelby County Health Department on July 2, allows the company to power its Colossus datacenter using 15 gas turbines, which have become the focus of heated environmental and health concerns from residents and advocacy groups. The approval comes after months of protests and public hearings during which local residents criticized the project's effect on air quality in the surrounding neighborhood. Many said the operation of the turbines had already resulted in air pollution so severe that they could no longer open their windows or exercise outside without experiencing strong odors and discomfort.

In a letter to the Shelby County Health Department, the Southern Environmental Law Center stated the emissions from the turbines make the facility "...likely the largest industrial emitter of NOx in Memphis..."

The environmental scrutiny creates regulatory risk. If permits are revoked or more stringent requirements imposed, the economics of mobile turbine operations could change significantly.

Securities Class Action

The most significant legal development came in March 2025. On July 9, 2024, Solaris announced that it has entered into an agreement to acquire Mobile Energy Rentals LLC ("MER"). Solaris completed the MER acquisition on September 11, 2024. On March 17, 2025, Morpheus Research published an investigative report alleging, among other things, that MER had been "a ~$2.5 million revenue equipment leasing business based out of a condo with zero employees, no turbines, and no track record in the mobile turbine rental industry." The report revealed that one of MER's co-owners, John Tuma, was in fact, a "convicted felon" for "environmental crimes and lying to the court 'on multiple occasions under oath'" and was involved in a "$800 million gas turbine scandal."

The complaint alleges that during the class period, Defendants issued materially false and/or misleading statements and/or failed to disclose that: (1) MER, Mobile Energy Rentals LLC, had little to no corporate history in the mobile turbine leasing space; (2) MER did not have a diversified earnings stream; (3) MER's co-owner was a convicted felon associated with multiple allegations of turbine-related fraud; (4) as a result, Solaris overstated the commercial prospects posed by the Acquisition; (5) Solaris inflated profitability metrics by failing to properly depreciate its turbines; and (6) that, as a result of the foregoing, defendants' positive statements about the Company's business, operations, and prospects were materially misleading and/or lacked a reasonable basis.

The report revealed that one of MER's co-owners was a convicted felon who was involved in an "$800 million gas turbine scandal… that included allegations of bid rigging [and] corruption." On this news, Solaris' stock price fell $4.15, or nearly 17%, to close at $20.46 per share on March 17, 2025.

The company has not disclosed its response to these allegations in detail. Securities class actions of this type are common following significant stock price declines, and the ultimate outcome will depend on the merits of the underlying claims.

The Company believes that the claims asserted in the Lawsuit are without merit and will vigorously defend against them. At this time, we are unable to predict the ultimate outcome of this case or estimate the range of possible loss, if any.

Customer Concentration Risk

Extreme customer concentration is a risk for any business, especially when that customer is a known slow payer who has reportedly received multiple cut-off notices for failing to pay electricity bills. Beyond the concentration risk, however, our research uncovered several issues that could threaten the contracts' profitability and long-term viability.

The dependence on xAI creates vulnerability. Any change in xAI's financial position, strategic direction, or relationship with Solaris could significantly impact results.

Investor Insight: The legal and regulatory challenges are material considerations. The securities class action adds uncertainty about disclosure practices and the MER acquisition process. Environmental opposition could increase permitting costs or create operational disruptions. Customer concentration remains the most fundamental risk—the thesis depends heavily on xAI's continued expansion and willingness to pay.

XI. Bull Case vs. Bear Case: A Framework for Analysis

The Bull Case

Hamilton Helmer's 7 Powers Framework Analysis:

-

Scale Economies: Solaris's growing turbine fleet creates operating leverage—fixed costs spread across more megawatts. The manufacturing capability in Early, Texas provides cost advantages for system maintenance and modification.

-

Network Effects: Limited applicability. Each turbine deployment is largely independent.

-

Counter-Positioning: Strong. Incumbent utilities face regulatory constraints and long planning cycles that prevent them from addressing near-term power gaps. Mobile turbines occupy a niche that grid-based solutions cannot fill quickly.

-

Switching Costs: Moderate. Once turbines are deployed and integrated into a customer's operations, switching providers involves mobilization costs and operational disruption. Long-term contracts reinforce this.

-

Branding: Limited. This is a B2B business where technical capabilities matter more than brand perception.

-

Cornered Resource: The turbine delivery slots represent a form of cornered resource. With OEMs facing capacity constraints, companies with turbines on order have advantage over those starting procurement processes today.

-

Process Power: Emerging. Solaris's field service capabilities and experience deploying mobile power systems create operational know-how that competitors must develop over time.

Porter's Five Forces:

- Threat of New Entrants: Moderate. Capital requirements are substantial but not prohibitive. The real barrier is turbine availability—OEMs have delivery backlogs extending years.

- Supplier Power: High. Turbine manufacturers (Solar Turbines, GE, etc.) have significant pricing power given demand exceeds supply.

- Buyer Power: Concentrated among few large customers (xAI dominant), creating negotiating leverage. However, buyers' alternatives are limited by grid constraints.

- Threat of Substitutes: Low near-term, high long-term. Grid upgrades and permanent power plants will eventually address the capacity gap, but this takes years.

- Industry Rivalry: Increasing. Competitors are entering the mobile power space, attracted by high returns.

The bull case emphasizes the structural tailwind. In the United States, power consumption by data centres is on course to account for almost half of the growth in electricity demand between now and 2030. Driven by AI use, the US economy is set to consume more electricity in 2030 for processing data than for manufacturing all energy-intensive goods combined, including aluminium, steel, cement and chemicals. In advanced economies more broadly, data centres are projected to drive more than 20% of the growth in electricity demand between now and 2030.

The Bear Case

The bear thesis centers on several concerns:

-

Customer Concentration: With xAI representing ~67% of the orderbook, any change in that relationship would be devastating.

-

Commoditization Risk: Mobile gas turbines are not proprietary technology. As the market develops, competitors with lower cost structures or better OEM relationships could undercut pricing.

-

Temporary Demand: If grid infrastructure catches up to AI demand, the market for "bridge power" solutions shrinks. The mobile turbine business may peak within a few years.

-

Environmental/Regulatory Risk: Increasing scrutiny of turbine emissions could lead to more stringent permitting, operational constraints, or outright restrictions.

-

Capital Intensity: Scaling requires massive capital expenditure. The plan shows consolidated capex of $798 million in 2025, $595 million in 2026, and $295 million in 2027, with a portion funded through joint venture partnerships. Dilution or increased leverage is inevitable.

-

Depreciation Questions: The lawsuit allegations about depreciation practices, if substantiated, could impact reported profitability and investor confidence.

Key Metrics to Watch

For investors following Solaris, three KPIs matter most:

-

Megawatts Earning Revenue: This metric tracks actual deployed capacity generating cash flow. The progression from 260 MW (Q4 2024) to 760 MW (Q3 2025) tells the growth story. Watch for acceleration or deceleration against management guidance.

-

EBITDA per Megawatt: This measures unit economics and can reveal pricing pressure or operational efficiency changes. Declining EBITDA per MW could signal commoditization.

-

Customer Diversification: Track the percentage of Power Solutions revenue from non-xAI customers. Movement from 4% (end 2024) toward higher diversification reduces concentration risk.

XII. Conclusion: A New Chapter in Energy Infrastructure

Solaris Energy Infrastructure represents one of the most dramatic corporate pivots in recent memory. From frac sand silos serving the Permian Basin to gas turbines powering Elon Musk's AI supercomputers, the transformation has been swift and consequential.

"We have also recently taken numerous measures to position Solaris for the next phase of growth in our Power Generation business. These actions include ordering additional generation capacity to support our accelerating commercial pipeline, enhancing balance sheet flexibility and adding liquidity to fund future growth, closing on the acquisition of HVMVLV, and bringing in Amanda Brock as Co-Chief Executive Officer and Director to help lead Solaris during this period of significant growth."

The addition of Amanda Brock as Co-CEO signals management's recognition that scaling a distributed power business requires different skills than running an oilfield services company.

At full fleet deployment (approximately 1,700 MW operated), potential for $575 million to $600 million in annual run rate Adjusted EBITDA (consolidated). Net to Solaris (approximately 1,250 MW owned), projected annual run rate Adjusted EBITDA of $440 million to $465 million, assuming 3-4 year paybacks on uncontracted equipment.

The bull case for Solaris rests on the proposition that AI's hunger for electricity will create sustained, multi-year demand for distributed power solutions that grid infrastructure cannot satisfy. The bear case warns that customer concentration, commoditization risk, and temporary demand dynamics could make the current opportunity ephemeral.

What's undeniable is that Bill Zartler and his team saw an inflection point and acted decisively. Whether the MER acquisition proves to be brilliant timing or an example of reaching for growth at the wrong price will become clear over the coming years.

For students of business strategy, Solaris offers lessons in several dimensions: the importance of founder-market fit, the power of corporate optionality (the Up-C structure enabled the MER equity deal), and the risks and rewards of concentrated customer relationships.

The company's original thesis—that better equipment could improve oilfield logistics—proved correct but ultimately limited by industry cyclicality. The new thesis—that mobile power can fill the gap between AI ambition and grid capacity—is bolder and potentially more valuable, but carries greater execution risk.

SEI has an annual dividend of $0.48 per share, with a yield of 1.01%. The dividend is paid every three months and the next ex-dividend date is December 8, 2025.

The maintained dividend through the transformation signals management's confidence in the underlying cash generation. Whether that confidence proves justified will depend on execution, customer diversification, and the durability of the AI power opportunity.

In the energy infrastructure landscape, few companies have attempted such a dramatic pivot—and even fewer have succeeded. Solaris's journey from frac sand silos to AI data center power is still being written, but the chapter headings already contain lessons for investors, operators, and strategists watching the intersection of energy and technology reshape our economy.

Material Regulatory and Legal Considerations: - Securities class action lawsuit pending (Class Period: July 9, 2024 - March 17, 2025) - Environmental permit challenges related to xAI turbine operations in Memphis - Patent litigation pending regarding proppant management technology (IPR proceeding expected conclusion January 2026)

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube