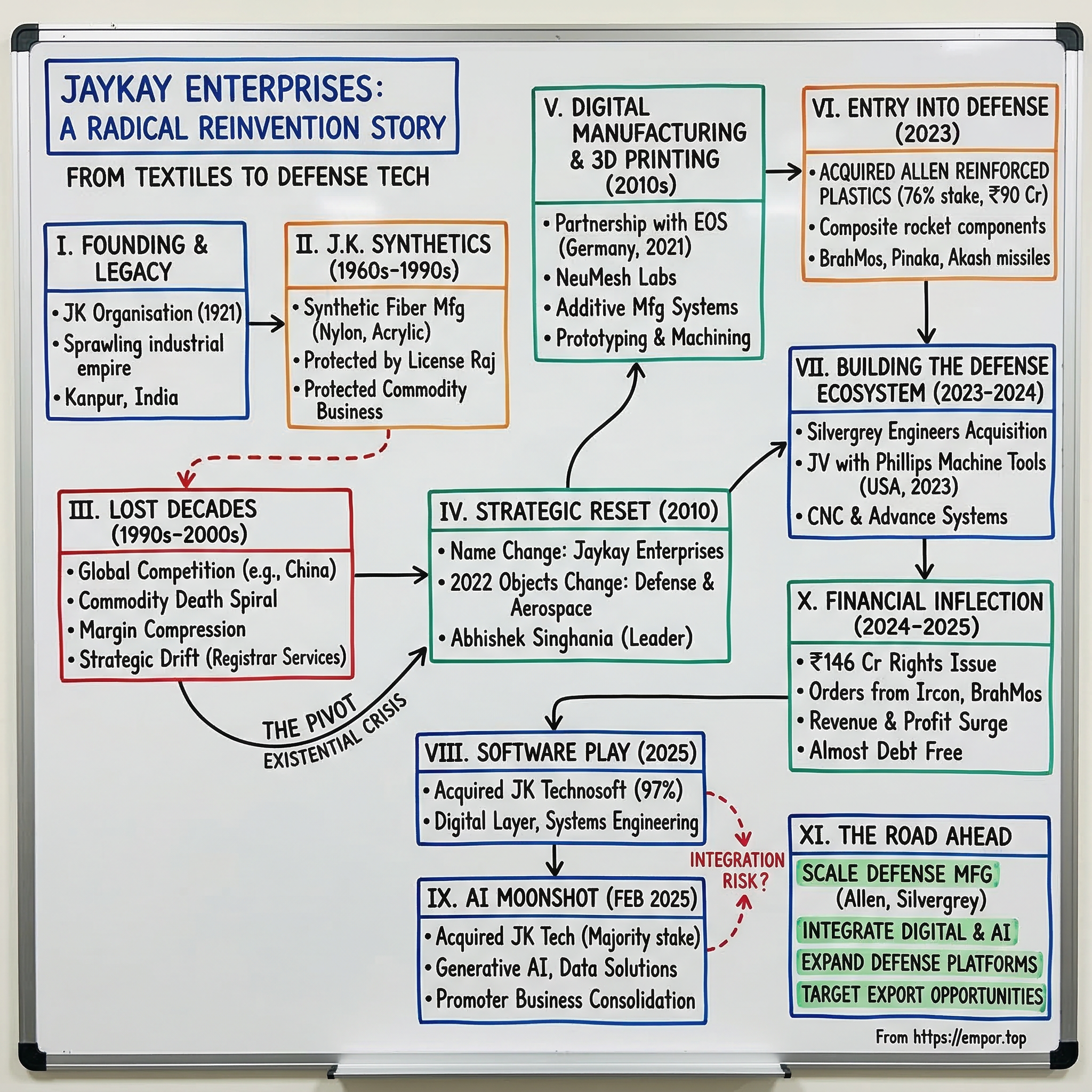

Jaykay Enterprises: From Textiles to Defense Tech — India's Radical Reinvention Story

I. Introduction & Episode Roadmap

Picture this: A textile company churning out nylon and acrylic fibers in Kanpur—the kind of commodity business where margins evaporate faster than monsoon puddles on hot asphalt. Now fast-forward to 2025, and that same company manufactures composite rocket components for BrahMos missiles, operates metal 3D printing facilities for aerospace applications, and deploys AI-powered software platforms across global enterprises.

Incorporated in 1961, Jaykay Enterprises Ltd is in the business of additive manufacturing, prototyping, 3D printing, but that prosaic description masks one of the most dramatic corporate transformations in Indian business history. The central question driving this story: How did a synthetic fiber company trapped in a commodity death spiral reinvent itself as a defense and aerospace technology player—and do it profitably?

The company currently commands a market capitalization of ₹3,012 crore, trades at a stock P/E of 136, and sits almost debt free—metrics that tell you the market believes something interesting is happening here. But it's the journey, not the destination, that makes this story remarkable.

This episode will unfold across five acts: We'll trace the JK Organisation legacy and how Jaykay Enterprises emerged from that sprawling industrial empire. We'll examine the "lost decades" of synthetic fibers and why that business model collapsed. Then comes the pivot—the 2010 name change that signaled existential crisis and strategic reset. The dramatic acceleration follows: the 2023 entry into defense through the Allen Reinforced Plastics acquisition, the 2025 software plays with JK Technosoft and JK Tech, and the infrastructure built through partnerships with German 3D printing leader EOS and American CNC manufacturer Phillips Corporation.

Why does this matter beyond one company's survival story? Jaykay Enterprises represents a masterclass in corporate reinvention within India's broader defense indigenization push—the "Atmanirbhar Bharat" initiative that's reshaping the country's strategic industries. For every investor who's held a zombie company hoping for resurrection, for every founder contemplating radical pivots, for every strategist wondering whether legacy businesses can truly transform—this story offers both inspiration and instruction.

The stakes are clear: either become relevant in high-tech manufacturing or fade into irrelevance as a commodity producer. Jaykay Enterprises chose the former, and the breakneck execution from 2023 to 2025 makes this one of the most interesting small-cap transformation stories in India today.

II. The JK Organisation Legacy & Founding Context

To understand Jaykay Enterprises, you must first understand the Singhania family tree—and the sprawling JK Organisation that spawned it. Lala Juggilal Singhania (1857-1922) was the founder of JK Organisation along with his son Lala Kamlapat Singhania, establishing what would become one of India's industrial dynasties.

The origin story reads like classic Indian entrepreneurial lore: Vinodi Das Singhania left his home in Singhana—a little town in the Jhunjhunu district of Rajasthan—in 1775. He resettled in Farrukhabad, a small business town near Kanpur. He started off as a Banker and diversified into trading. Four generations of accumulation, relationship-building, and opportunism followed.

But the real inflection point came in 1921. Lala Juggilal and his son Lala Kamlapat Singhania started with Juggilal Kamlapat Cotton Spinning & Weaving Mills in 1921—the cornerstone of what would become the JK business empire. Along with his father's contribution he established Juggilal Kamlapat Cotton Spinning & Weaving Mills in 1921, riding the wave of India's nascent industrialization and the Swadeshi movement's patriotic fervor.

Kamlapat proved to be a serial entrepreneur before the term existed. He went on to set up several mills—Kamla Ice Factory in 1921, JK Oil Mills in 1924, JK Hosiery Factory in 1929, JK Jute Mills in 1931, MP Sugar Mills in 1932, JK Cotton Manufacturers Ltd in 1933 and JK Iron & Steel Co Ltd in 1934. This wasn't diversification as modern portfolio theory teaches it—this was empire-building through vertical and horizontal integration, capturing value across the industrial value chain of pre-independence India.

The family structure created a decentralized federation. Kamlapat married Rampyari Devi and they had three daughters and three sons: Padampat, Kailashpat and Lakshmipat Singhania. The brothers decided to share responsibilities by allotting region-wise responsibilities, with Sir Padampat looking after the northern zone, Kailashpat looking after the western zone and Lakshmipat looking after the eastern zone. With that, the three brothers parted ways. Kailashpat headed for Bombay and Lakshmipat resettled in Calcutta. The overall control of the business, however, lay with Sir Padampat, who was looked up to as the family head.

Today, the family owns majority stakes in several publicly listed companies such as JK Tyre, JK Cement, JK Lakshmi Cement, JK Paper, Jaykay Enterprises, JK Agri Genetics (JK Seeds) and JK Dairy (Umang Dairies). The JK Organisation touches multiple industries—from tires to cement to paper—representing the kind of industrial diversity that characterized India's first generation of large family-owned conglomerates.

Within this empire, Jaykay Enterprises emerged as part of the Kanpur branch, under the control of Abhishek, Son of Govind Hari Singhania. Companies include JK Technosoft—involved in software supply—and Jaykay Enterprises Ltd (formerly JK Synthetics Ltd.), which was involved in manufacturing of nylon and acrylic fibres.

This genealogy matters because it explains both the resources Jaykay could tap (financial muscle, reputation, business acumen) and the constraints it faced (family dynamics, legacy business models, the weight of tradition). The JK name opened doors—but it also meant operating in the shadow of more successful siblings like JK Tyre and JK Cement, which maintained clearer strategic identities.

The founding ethos—nation-building through manufacturing, vertical integration, patient capital—would resurface decades later when Jaykay faced its existential crisis. Sometimes the old playbook still works; you just need to apply it to new industries.

III. Early Years: Investment Trust to Synthetics (1943-2000s)

The Company was incorporated under the name J.K. Investment Trust Limited and functioned primarily as an investment Company. It ceased to be recognized as investment trust Company in 1959—already a sign of strategic drift. The company spent its first sixteen years as a capital allocator before management decided that wasn't the business they wanted to be in.

In 1960 the Company changed its name to J. K. Synthetics Limited, pivoting into manufacturing. The Company initially engaged in the business of manufacturing nylon and acrylic fibers—riding the post-independence wave of synthetic textiles that promised to clothe India's growing middle class affordably.

For several decades, this looked like a sensible play. India's License Raj protected domestic manufacturers from foreign competition. The Singhania family knew textiles intimately—it was the business that built the JK empire. Synthetic fibers represented modernity, technology, progress. And for a while, it worked.

But commoditization is a cruel master. By the 1990s and 2000s, several forces converged to destroy the economics of synthetic fiber manufacturing in India:

Global competition: Chinese manufacturers achieved scale that Indian producers couldn't match. Lower labor costs, better infrastructure, and aggressive government support created an unlevel playing field.

Commodity trap: Nylon and acrylic fibers became undifferentiated products where price was the only variable that mattered. No brand loyalty, no switching costs, no moat.

Margin compression: As raw material costs (petroleum-based inputs) fluctuated and selling prices collapsed under competitive pressure, margins evaporated. The business generated revenue but destroyed value.

Technological stasis: Unlike industries where continuous innovation creates new profit pools (semiconductors, pharmaceuticals), synthetic fibers offered limited opportunities for differentiation through R&D.

Somewhere along the way, the Company was primarily involved in registrar and transfer agent services—yet another strategic detour that suggested management was searching for a sustainable business model. Running share registries is steady, low-margin work that requires different capabilities than manufacturing. This wasn't diversification; it was desperation dressed as strategy.

By the mid-2000s, Jaykay Enterprises looked like what private equity professionals call a "melting ice cube"—generating cash today but with no clear path to sustainable value creation. The synthetic fiber business was in structural decline. The registrar business was a side hustle that couldn't support the company's ambitions. And unlike its JK Organisation siblings who had found durable competitive positions, Jaykay Enterprises was drifting.

The "wandering years" had begun—that dangerous period when a company has lost its identity but hasn't yet found a new one. Revenue was reported, dividends were skipped, and the stock price reflected the market's verdict: this business had no future. For investors who bought and held, hoping the JK name would somehow create value, this was the decade of regret. For the Singhania family members running the business, it must have been both humbling and clarifying: either reinvent radically or accept irrelevance.

The stage was set for transformation, but transformation requires both vision and crisis. The vision would come from Abhishek Singhania, the next generation leader. The crisis was already here—the business model was broken and everyone knew it.

IV. The Existential Crisis & Name Change (2010)

In 1960 the Company changed its name to J. K. Synthetics Limited subsequently the name was changed to Jaykay Enterprises Limited in October, 2010. Corporate name changes usually signal one of two things: rebranding success or masking failure. This was clearly the latter—an acknowledgment that "Synthetics" no longer described the business anyone wanted to build.

The name "Jaykay Enterprises" was deliberately vague—"Enterprises" is what you call a company when you don't yet know what it will become. It's the corporate equivalent of "consulting"—broad enough to encompass almost anything, specific enough to suggest you're in business. This wasn't confident repositioning; this was strategic flexibility born of necessity.

But the real inflection point came twelve years later. In May 2022, the company changed its objects by a resolution passed at the Extraordinary General Meeting to incorporate activities related to the defense and aerospace sector in order to diversify the company's activities, along with collaboration or technical know-how in the fields of defense, aerospace and space technologies.

This wasn't tinkering at the edges—this was fundamental strategic redirection. Defense and aerospace? For a company that made acrylic fibers? The gap between stated aspiration and current capabilities was enormous. Investors had every reason to be skeptical. After all, companies announce "strategic pivots" all the time; executing them is another matter entirely.

The leadership context matters here. Mr. Abhishek Singhania is the Promoter, Chairman & Managing Director of Jaykay Enterprises Limited and scion of one of the best known business families of India. Mr. Singhania spearhead in Carving new business opportunities and managing strategic investments in Defence & Aerospace, Digital Manufacturing (3D & Processing), Digital Transformation.

Abhishek represented the fifth generation of Singhania entrepreneurs—educated, globally aware, and confronting a business that his great-great-grandfather's generation would barely recognize. He is the cofounder & has served as Managing Director of JK Technosoft Ltd and leads the company's global operations. He has invaluable experience within JK Organisation companies, handling various aspects of J K businesses. He has rich experience in the manufacturing & IT services industry and multi-dimensional expertise in basic & core sector industries such as textiles, synthetic fibres, cement and chemical processing. Mr. Singhania has deep insights in Software Development Life Cycle (SDLC), Project Management, Strategic Planning, Business Development, Thought Leadership.

This unusual combination—deep operational experience in legacy industries plus software/IT expertise—positioned him uniquely to understand both what the company was leaving behind and where it needed to go. He wasn't a parachuted-in professional manager with no skin in the game. He wasn't a third-generation heir content to clip coupons. He was a builder confronting ruins.

The strategic question facing Abhishek and his team was stark: Buy, build, or die?

Build meant organic development of defense and aerospace capabilities—hiring engineers, establishing manufacturing facilities, developing products, pursuing certifications, courting customers. Timeline: 7-10 years minimum. Probability of success without domain expertise: low.

Die meant accepting managed decline—milking remaining cash flows from legacy businesses, perhaps selling assets piecemeal, eventually dissolving the company or merging it into a stronger sibling. This preserved family wealth but destroyed legacy.

Buy meant aggressive inorganic growth—identifying targets with defense/aerospace capabilities, acquiring them, integrating operations, leveraging existing relationships and certifications to accelerate entry. Timeline: 2-3 years. Risk: execution complexity and acquisition integration.

The choice to buy—and buy aggressively—would define everything that followed. But first, Jaykay needed to build some foundational capabilities that would make it a credible acquirer. That meant entering digital manufacturing and 3D printing, establishing technical credibility, and creating a platform that defense companies could plug into.

The 2010 name change was symbolic. The 2022 object clause change was strategic commitment. But the real transformation would happen between 2023 and 2025, when Abhishek Singhania executed one of the most aggressive acquisition strategies in Indian small-cap history.

V. The Great Pivot: Digital Manufacturing & 3D Printing (2010s)

While the world watched India's defense sector consolidate around massive players like Tata, Larsen & Toubro, and Reliance, Jaykay Enterprises quietly positioned itself at the intersection of two megatrends: additive manufacturing and defense indigenization.

The company specializes in Additive Manufacturing Systems, Prototyping, Powder Metallurgy, Large Scale Digital Manufacturing, Reverse Engineering, and Plant Modelling. In the Defense and Aerospace sectors, it provides engineering products, software design and development, and manufactures parts and accessories. Its work includes composite applications, underwater mines, and aerospace machining.

The 3D printing strategy was both pragmatic and visionary. Pragmatic because it represented a natural adjacency from manufacturing—applying new production technologies to complex components. Visionary because additive manufacturing was fundamentally changing how aerospace and defense companies approached prototyping and low-volume production.

In January 2021, Jaykay Enterprises entered into a joint venture partnership with Germany's EOS, a global leader in 3D metal design and printing market, to address the need of 3D metal printing in India. The joint venture would operate through a new subsidiary called NeuMesh Labs Pvt Ltd, headquartered at Bengaluru, with EOS providing technical knowledge.

This partnership was crucial for several reasons. First, it gave Jaykay instant credibility—EOS is to industrial 3D printing what Intel is to semiconductors, a recognized technology leader. Second, it provided access to cutting-edge equipment and processes that would take years to develop independently. Third, it signaled to potential defense customers that Jaykay was serious about advanced manufacturing.

The JV would support Indian companies to adapt metal 3D printing by offering 'EOS Additive Minds' consulting topics in the area of Design For Additive Manufacturing (DFAM), part screening and selection, topology optimisation and to generate business cases. This wasn't just selling equipment—it was providing the full stack of design, optimization, and manufacturing services that defense contractors needed.

Why did 3D printing matter for defense? Several reasons converged:

Complex geometries: Aircraft and missile components often require shapes that are difficult or impossible to produce through traditional subtractive manufacturing (machining) or forming processes. Additive manufacturing excels at complexity.

Low-volume production: Defense projects typically require dozens or hundreds of parts, not millions. Traditional tooling economics don't work at that scale. 3D printing eliminates tooling costs.

Rapid prototyping: Development cycles accelerate dramatically when you can iterate designs in weeks rather than months.

Supply chain resilience: Being able to manufacture complex parts locally reduces dependence on foreign suppliers and long lead times.

Lightweighting: Additive manufacturing enables topology optimization—creating parts with material only where stress analysis shows it's needed. This matters enormously in aerospace where every gram of weight reduction cascades through the system.

But the early days were challenging. Jaykay Enterprises along with its eco system partners indigenously developed a polymer printer JK Print 300 and JKPM3 series, a Powder Management System which was unveiled in IMTEX 23 Fair in Bengaluru. The initial customer response has been encouraging. The JK Print 300 Printer is suitable for usage in prototyping, consumer goods, Automobile, and architecture for low volume production. The machine is ideal for usage in low volume production and training of students and technicians.

Revenue was modest, margins were uncertain, and the market had no idea how to value this emerging capability. But Jaykay was accumulating something more valuable than revenue: technical credibility, customer relationships, and proof points that it could execute in advanced manufacturing.

The company acquired 99% stake in Bangalore based partnership firm M/s. Silvergrey Engineers (SGE) engaged in manufacturing and supply of parts and accessories to defence equipment manufacturing industry, catering to Customers including HAL, BEL, ISRO, Gas Turbine Research Establishment, Aeronautical Development Agency, Tata Advance Systems amongst others. This 2023 acquisition gave Jaykay a direct foothold with defense PSUs and a manufacturing facility in Bangalore, India's aerospace hub.

By 2023, Jaykay had built a credible platform: 3D printing capabilities through the EOS partnership, precision machining through Silvergrey Engineers, design and engineering services, and growing relationships with defense customers. The foundation was laid. Now it was time to scale dramatically through the acquisition that would change everything: Allen Reinforced Plastics.

VI. Entry into Defense & Aerospace: The Game-Changer (2023)

If you had to pinpoint the single transaction that transformed Jaykay Enterprises from a struggling pivot story into a legitimate defense player, it was this: Jaykay Enterprises through its wholly owned subsidiary i.e. JK Defence & Aerospace Limited ("JK Defence") acquired the 76.41% equity stake in Allen Reinforced Plastics Private Limited (Allen). Accordingly, Allen Reinforced Plastics Private Limited became a subsidiary of JK Defence and a step-down subsidiary of the Company with effect from July 09, 2023.

It paid ₹90 crores in cash for acquiring the stake—not a trivial sum for a company with Jaykay's market capitalization at the time, but transformative if executed well.

First, understand what Allen brought to the table. Allen Reinforced Plastics (P) Ltd was incorporated in December 1987 by the founders, Mr. P.V.Rao, Mr. K.Chandrasekhar and Mr. N.V.Rao. The Company is involved in the design, development, manufacture and testing of composite and allied engineering products for the purpose of Defence, Aerospace and Engineering products like Missile & Rockets components, Underwater Applications, Marine and submarine, Gun and accessories.

This wasn't a startup with promising technology and no customers. This wasn't a turnaround situation requiring operational fixes. Allen Reinforced Plastics reported a turnover of ₹86.1 million in FY21, ₹289.9 million in FY22 and ₹252.1 million in FY23—a profitable, operating business with established relationships.

The company had a presence with its head office and two manufacturing plants in Hyderabad—real physical assets and production capacity that could be leveraged immediately.

But the real value wasn't the plants or even the revenue. It was the intangibles: government approvals, security clearances, established vendor status with India's defense establishment, engineering expertise in composite materials, and battle-tested processes for quality control and testing. These are the barriers to entry that take years to build and can't be shortcuts through capital investment alone.

Allen indigenously develops and supplies critical components to key defence projects in the country, such as BrahMos, Pinaka, SMILE, Akash missiles to defence undertakings such as DRDO, ISRO, OFB, BHEL, BDL among others. Read that list again: BrahMos (the supersonic cruise missile that represents the crown jewel of Indo-Russian defense cooperation), Pinaka (multi-barrel rocket launcher), Akash (surface-to-air missile system), plus relationships with DRDO (Defense Research and Development Organisation) and ISRO (Indian Space Research Organisation). This was instant legitimacy.

The timing was perfect—or rather, deliberately chosen. India's defense indigenization push was accelerating under the "Atmanirbhar Bharat" (Self-Reliant India) initiative. The government had committed to massive increases in domestic procurement. Defense PSUs and private companies were scrambling to build or acquire indigenous supply chains. Allen Reinforced Plastics was exactly what everyone needed: a proven manufacturer of critical composite components with established relationships and certifications.

The board approved raising up to ~Rs 150 crore through rights issue of equity shares to fund the acquisition & expand its operations in various subsidiaries. In 2024, the issue size of Jaykay Enterprises Rights Issue was 5,84,57,688 equity shares at ₹25 per share aggregating up to ₹146.14 Crores—putting equity capital to work immediately to consolidate the defense platform.

On Completion of full payment of the Rights Shares, JK Defence & Aerospace Limited's shareholding in Allen Reinforced Plastics Private Limited would increase to 92.92% from 76.41%, demonstrating management's commitment to full control rather than passive financial investment.

Why did composite materials matter so much in defense? The physics are straightforward but the implications are profound:

Strength-to-weight ratio: Composites (typically fiberglass or carbon fiber reinforced plastics) offer exceptional strength while weighing far less than metals. For missiles and aircraft, weight reduction directly translates to range, payload capacity, and fuel efficiency.

Radar signatures: Certain composite materials are radar-transparent or have low radar cross-sections—crucial for stealth applications.

Corrosion resistance: Naval and submarine applications require materials that can withstand seawater exposure. Composites excel here.

Complex shapes: Like 3D printing, composite layup processes enable geometries difficult to achieve with metal fabrication.

Cost at volume: While tooling costs can be high, unit costs at production volumes become very attractive.

The Allen acquisition represented vertical integration in the best sense—adding capabilities that complemented Jaykay's 3D printing and machining operations while opening access to an entirely new customer base. Suddenly, Jaykay could offer defense contractors a full suite of manufacturing services: metal 3D printing through the EOS partnership, precision machining through Silvergrey Engineers, and composite manufacturing through Allen Reinforced Plastics.

The market noticed. Jaykay's stock jumped on the announcement, but more importantly, the strategic narrative changed. No longer was this a textile company trying to pivot. It was a defense manufacturer with growing capabilities and validated customer relationships.

And the validation kept coming. In September 2025, Allen Reinforced Plastics Ltd, secured a major order worth ₹94.45 crore from BrahMos Aerospace Private Limited, a government-owned entity—proof that the acquisition wasn't just buying past relationships but enabling future growth.

From 76.41% ownership to 92.92% stake, from one acquisition to an integrated defense platform, from ₹90 crores invested to order flows exceeding that amount—the Allen acquisition was the strategic masterstroke that made everything else possible. It provided proof of concept that Jaykay could execute in defense, gave it instant credibility with government customers, and created the foundation for further expansion.

But Abhishek Singhania and his team weren't done building. The defense platform needed more capabilities, particularly in CNC machining and digital transformation. The acquisition spree was just getting started.

VII. Building the Defense Ecosystem (2023-2024)

With Allen Reinforced Plastics providing the composite manufacturing anchor, Jaykay moved aggressively to build out complementary capabilities. The strategy was clear: create a full-stack defense manufacturing platform that could serve as a one-stop shop for complex components.

The customer list tells the story better than any pitch deck could. Silvergrey Engineers catered to Customers including HAL, BEL, ISRO, Gas Turbine Research Establishment, Aeronautical Development Agency, Tata Advance Systems amongst others—a who's who of India's defense and aerospace establishment.

This wasn't luck or legacy relationships inherited from the JK Organisation. This was systematic capability building: identify what defense contractors need, acquire or build those capabilities, execute flawlessly on initial orders, win repeat business, and expand the relationship. The flywheel was starting to spin.

In December 2023, JKE entered into an Agreement with Phillips Machine Tools India Private Limited, a subsidiary of Phillips Corporation, USA, to form and constitute a Limited Liability Partnership under the name and style of JK-Phillips LLP. The Company made a capital contribution of Rs 1,00,000/- (Rupees One Lakhs Only) in the LLP and holds 50% of the right to share profit in the LLP.

This LLP was formed to carry out the business of trading and distribution of Advance systems which includes CNC machines, lathes, hydraulic press, 3D printers, moulding machines and accessories originally produced by Phillips and other manufacturing/ trading activities including after-sales services.

The Phillips partnership represented a different strategic angle—not acquiring manufacturing capabilities but gaining access to advanced manufacturing equipment and establishing a distribution channel. It also created optionality: as India invested in MSME (Micro, Small, and Medium Enterprises) capacity building, there would be demand for training facilities equipped with modern CNC machines and digital manufacturing tools.

That optionality paid off quickly. In September 2025, J K Phillips LLP secured a Letter of Acceptance (LOA) worth ₹139.48 crore (including GST) from Ircon International Ltd, a Government of India Navratna company. The project had a completion period of 240 days from the LOA date.

The order involved the design, supply, installation, commissioning, and training of a wide range of conventional machines for MSME training centres across India, on a turnkey basis—exactly the kind of large-scale infrastructure project that India's defense indigenization push was generating. The government recognized that building a domestic defense industrial base required training thousands of technicians in modern manufacturing techniques. Jaykay, through its JV with Phillips, positioned itself to supply that infrastructure.

The financial impact was immediate. Jaykay Enterprises Ltd's net profit jumped 343.42% since last year same period to ₹20.22Cr in the Q1 2025-2026. On a quarterly growth basis, Jaykay Enterprises Ltd generated 632.11% jump in its net profits since last 3-months. The company's revenue jumped 228.65% since last year same period to ₹77.43Cr in the Q1 2025-2026. On a quarterly growth basis, Jaykay Enterprises Ltd generated 365.05% jump in its revenue since last 3-months.

These weren't marginal improvements or accounting games—this was genuine top-line and bottom-line growth driven by order execution. The market rewarded it: Jaykay Enterprises Ltd share price moved up by 599.47% on BSE over last 3 years.

The manufacturing footprint now spanned critical hubs: Bangalore (Silvergrey Engineers and Neumesh Labs for 3D printing), Hyderabad (Allen Reinforced Plastics for composites), and the emerging capability-building network through the Phillips partnership. Geographic diversity reduced concentration risk while positioning Jaykay close to major aerospace and defense clusters.

But manufacturing capabilities alone don't create competitive moats in defense. You need software, systems integration, and digital transformation capabilities—the ability to model complex systems, simulate performance, and optimize designs before physical prototyping. This realization would drive Jaykay's next major acquisition: JK Technosoft.

VIII. The Software Play: JK Technosoft Acquisition (2025)

If the Allen acquisition represented vertical integration into physical manufacturing, the JK Technosoft acquisition represented vertical integration into the digital layer—the software, simulation, and systems engineering capabilities that increasingly define modern defense development.

Jaykay Enterprises Limited agreed to acquire 97.48% stake in Jk Technosoft Limited for approximately INR 888 million on February 11, 2025. The timing, just months after consolidating the physical manufacturing base, signaled ambitious horizontal expansion—Jaykay wasn't content to be a contract manufacturer; it wanted to move up the value chain into design and engineering services.

The strategic logic was compelling: defense contractors increasingly needed integrated capabilities—not just someone to manufacture components to specifications, but partners who could collaborate on design, simulate performance, optimize manufacturability, and then execute production. This "design-for-manufacturability" approach reduces development time, eliminates costly design iterations, and creates stickier customer relationships.

JK Technosoft brought software development, IT services, and digital transformation capabilities. While specific revenue and customer details aren't extensively disclosed, the acquisition size (nearly ₹89 crores) suggested a substantial business—not a startup bet but an established operation with recurring revenue streams.

The company made investment by way of secondary acquisition of 1,24,07,276 Partly paid-up Equity Shares of face value of Rs. 10/- (Paid up Rs. 2.50/-) each of JK Technosoft Limited, for an aggregate consideration not exceeding Rs. 1,12,45,95,496.64/- at an adjusted acquisition price of Rs. 90.64/-, payable by way of Swap of 1,24,07,276 partly paid-up Equity Shares of JKTL against issuance of fully paid-up Equity Shares of the Company—structured as a share swap rather than cash acquisition, conserving balance sheet liquidity for operational expansion.

The potential applications in defense were numerous:

Digital twin technology: Creating virtual replicas of physical systems to simulate performance under various conditions—crucial for testing missile trajectories, aircraft stress analysis, and system integration without expensive physical prototyping.

Plant modeling and simulation: Optimizing manufacturing layouts, workflow, and capacity utilization before physical implementation.

PLM (Product Lifecycle Management) systems: Managing the complex documentation, version control, and regulatory compliance requirements that defense projects demand.

Industry 4.0 integration: Connecting manufacturing equipment, sensors, and control systems to enable predictive maintenance, quality monitoring, and efficiency optimization.

The acquisition also created interesting cross-selling opportunities. A defense contractor working with Allen Reinforced Plastics on composite components might also need software services for design optimization or manufacturing simulation. Similarly, a customer buying CNC equipment through the Phillips partnership might require training, simulation software, and integration services.

But there was another dimension to the JK Technosoft acquisition that wouldn't become clear until the next deal: consolidating the promoter's business interests under the Jaykay Enterprises umbrella. Mr. Abhishek Singhania is the Promoter, Chairman & Managing Director of Jaykay Enterprises Limited and scion of one of the best known business families of India. He is the cofounder & has served as Managing Director of JK Technosoft Ltd.

This created both opportunity and potential conflicts. On one hand, bringing multiple businesses under common ownership could unlock synergies and simplify governance. On the other hand, related-party transactions always carry the risk (or perception) of value transfer rather than value creation. Minority shareholders would be watching closely to ensure acquisitions were done at fair valuations and genuinely strategic, not just empire-building or family consolidation.

The JK Technosoft acquisition demonstrated that Jaykay's transformation wasn't just about manufacturing—it was about building an integrated technology platform spanning physical production, digital design, and systems integration. But the most controversial and ambitious acquisition was still to come: JK Tech, the AI and software services company that would push Jaykay far beyond its manufacturing comfort zone.

IX. The AI Moonshot: JK Tech Acquisition (February 2025)

If investors thought the JK Technosoft acquisition represented the outer boundary of Jaykay's diversification, they were about to be surprised. In February 2025, Jay Kay Enterprises (JKE), a leader in high-precision manufacturing for the Defence and Aerospace sector, acquired a majority stake in JK Tech, a global provider of Generative AI and data-driven solutions.

Wait—a defense manufacturing company acquiring a global AI services firm? The strategic logic wasn't immediately obvious, and the market's reaction reflected that confusion. This wasn't vertical integration into adjacent capabilities. This was horizontal diversification into an entirely different business model: software services, global delivery, enterprise AI applications.

JK Tech is a global leader in Generative AI and data-driven solutions, specializing in transforming enterprises in Retail, CPG, and Insurance. Its flagship JIVA platform enables businesses to unlock the full potential of their data through AI-powered automation, data discovery, and intelligent decision-making. JK Tech's commitment to measurable outcomes and rapid ROI ensures sustainable growth for its clients.

Retail? CPG? Insurance? These were about as far from rocket components and composite manufacturing as you could get. And unlike the Allen or JK Technosoft acquisitions, which had clear industrial applications, the JK Tech acquisition seemed to serve a different purpose.

Mr. Partho Kar, Joint Managing Director, JKE stated: "The acquisition marks a significant step toward consolidating the promoters' businesses under the JKE umbrella. By combining the expertise and strengths of both organizations, we are well-positioned to push the boundaries of AI innovation and deliver next-generation solutions to our customers. This will add value to JKE in its quest to get into industrial engineering and EPC contracting, thus unlocking new growth opportunities".

There it was, explicitly stated: "consolidating the promoters' businesses under the JKE umbrella." This wasn't primarily a strategic acquisition to serve defense customers better—it was corporate restructuring to bring family-controlled businesses under one listed entity.

The question for minority shareholders: Was this value-accretive or value-extractive? Several perspectives emerged:

The Bull Case for AI Integration: - Manufacturing is increasingly software-defined. AI enables predictive maintenance, quality control, design optimization, and production scheduling. - Defense applications of AI are exploding: autonomous systems, target recognition, cyber security, logistics optimization. - JK Tech's JIVA platform could be adapted for industrial applications, creating differentiation in manufacturing services. - As a listed entity, JK Tech would have better access to capital markets for expansion. - Cross-selling opportunities exist: defense contractors need both hardware (Jaykay's core) and software (JK Tech's expertise).

The Bear Case for Diversification: - Software services and manufacturing are fundamentally different businesses requiring different management capabilities, talent pools, and go-to-market strategies. - Integration risk is enormous—companies often fail to realize synergies from unrelated acquisitions. - JK Tech serves Retail, CPG, and Insurance—customer bases with zero overlap with defense manufacturing. - Management attention gets diluted across too many initiatives. - This looks more like empire-building or family consolidation than strategic focus. - Valuation opacity: Was the acquisition done at market prices or sweetheart terms for promoters?

JKE, led by Abhishek Singhania, has long been at the forefront of cutting-edge manufacturing, where AI and Gen AI are playing a crucial role in transforming operations. With this investment, JK Tech will leverage the strength of the JKE group to enhance its AI capabilities, expand its reach, and drive transformation at an unprecedented pace.

The attempted justification—that AI is transforming manufacturing—is true but doesn't necessarily justify acquiring a services company focused on completely different industries. A partnership or licensing arrangement could potentially achieve the same technology access without the integration complexity.

JK Tech will continue to operate under its current leadership while leveraging JKE's resources and market expertise—suggesting limited integration, which reduces both risk and potential synergy capture.

The financial impact would take time to assess. Unlike the Allen acquisition, which immediately contributed defense revenue and order flow, or the Phillips partnership, which generated equipment sales contracts, JK Tech's contribution to Jaykay's defense transformation story was indirect at best.

For long-term fundamental investors, the JK Tech acquisition represented a crossroads: either trust that management saw connections others didn't and would execute a complex integration, or worry that strategic focus was being sacrificed for family business consolidation. The coming quarters would reveal which narrative was correct.

What's indisputable: Jaykay Enterprises in early 2025 looked nothing like Jaykay Enterprises in 2020. From synthetic fibers to composite manufacturing to CNC distribution to software services to AI platforms—the transformation was complete, perhaps too complete. Sometimes the best strategy is saying no to attractive opportunities that don't fit. Whether Jaykay had maintained sufficient focus would be tested by execution.

X. Financial Transformation & Operating Leverage (2024-2025)

Strategy is meaningless without execution, and execution shows up in financial statements. For Jaykay Enterprises, the numbers told a story of dramatic inflection—not smooth, linear growth, but the kind of explosive expansion that happens when multiple acquisitions integrate successfully and order pipelines convert to revenue.

Net profit of Jaykay Enterprises rose 343.42% to Rs 20.22 crore in the quarter ended June 2025 as against Rs 4.56 crore during the previous quarter ended June 2024. Sales rose 223.51% to Rs 55.45 crore in the quarter ended June 2025 as against Rs 17.14 crore during the previous quarter ended June 2024.

Those aren't rounding errors—those are step-function changes in business scale. Revenue more than tripled year-over-year. Net profit increased 4.4 times. Quarterly comparison showed even more dramatic growth: 632.11% jump in net profits since last 3-months.

This kind of growth trajectory creates both excitement and skepticism. Excitement because it validates the acquisition strategy—the pieces are clearly generating revenue and profitability. Skepticism because high-percentage growth from a small base can be deceiving, and sustainability is always the question.

Let's examine the underlying drivers:

Allen Reinforced Plastics order execution: The BrahMos contract and ongoing defense projects converted from order book to recognized revenue. Allen reported a total turnover of ₹22.07 crore in FY 2024, ₹25.21 crore in FY 2023 and ₹28.99 crore in FY 2022—a relatively stable base that Jaykay could now cross-sell to other defense customers and expand through capital investment.

Phillips JV contracts: The ₹139.48 crore Ircon order represented a near-term revenue visibility that most small-cap companies dream of—government-backed, multi-quarter execution, turnkey deliverables.

Operating leverage: Fixed costs (facilities, equipment, core personnel) were largely in place from acquisitions. Incremental revenue dropped much more dramatically to the bottom line than the initial revenue did, creating margin expansion.

Other income: Earnings include an other income of Rs.34.0 Cr—a significant portion of overall profitability. This line item always deserves scrutiny. Is it one-time gains, investment income, or recurring business income? The sustainability of profitability depends heavily on whether this other income persists or was a one-time event.

The capital structure evolution is equally important. Company is almost debt free—a remarkable achievement for a company executing aggressive M&A. How did Jaykay fund multiple acquisitions without levering the balance sheet?

Rights issue: The ₹146.14 crore rights issue in 2024 provided equity capital specifically earmarked for acquisition funding and capacity expansion. The Company intended to utilize the Net Proceeds for Investment in the Wholly Owned Subsidiary JK Defence & Aerospace Limited to establish the manufacturing facility of defence-related products and repayment of loan taken by JK Defence, and Investment in JK Digital & Advance Systems Private Limited for the purchase of 3-D Printing machinery and establishment of a Center of Excellence in 3-D Printing.

Share swaps: The JK Technosoft acquisition used equity rather than cash, preserving liquidity.

Promoter conviction: Promoter holding has increased by 2.30% over last quarter, demonstrating that the controlling shareholders weren't just extracting value but increasing their stake—typically a positive signal about management's confidence in future prospects.

But not everything in the financial picture was rosy. Company has high debtors of 529 days—meaning the average time to collect payment from customers exceeded 17 months. This is common in defense contracts, where government payment cycles are notoriously slow, but it creates working capital strain. Even profitable contracts consume cash if customers don't pay promptly.

Company has a low return on equity of 0.21% over last 3 years—a backward-looking metric that reflects the "lost years" before the transformation gained momentum. Three-year ROE includes 2022 and 2023, when the company was still primarily legacy businesses. The relevant question isn't historical ROE but forward ROE: can the current mix of businesses generate attractive returns on the enlarged equity base?

The stock market's response provided partial validation. Jaykay Enterprises achieved an all-time high of Rs. 237 on September 30, 2025, highlighting its strong performance in the Aerospace & Defense sector. The stock has gained momentum, with significant returns over various periods, showcasing impressive growth and a solid market position amid industry competition.

The company currently commands a market cap of ₹3,012 Cr with a Stock P/E of 136—that multiple implies the market is pricing in substantial future growth. A P/E of 136 means investors are paying ₹136 for every ₹1 of current earnings, betting that earnings will expand dramatically. If they're right, the stock is reasonably valued. If execution stumbles or growth slows, that multiple will compress painfully.

The financial transformation was real, dramatic, and ongoing. From losses to profitability, from single-digit crores to approaching ₹100 crore quarterly revenue, from debt-laden to nearly debt-free—these weren't cosmetic changes but fundamental business transformation. The question was sustainability: could this growth continue, or had the easy gains from initial integration already been harvested?

XI. Playbook: Business & Investing Lessons

Zooming out from the tactical details of each acquisition and quarterly result, what broader lessons does the Jaykay Enterprises transformation offer?

Lesson 1 — Corporate Reinvention is Possible, But Requires Radical Commitment

Most "turnaround" stories involve operational improvements—cutting costs, improving margins, rationalizing SKUs, optimizing working capital. Jaykay's transformation wasn't operational; it was existential. The company didn't fix the synthetic fiber business; it exited it entirely and rebuilt around completely different capabilities. That requires courage, capital, and conviction that most management teams lack.

For investors holding struggling businesses, the question becomes: Is management capable of this level of strategic reinvention, or are they incrementally improving a fundamentally broken model? Look for concrete evidence of willingness to abandon legacy businesses, not just promises to "explore new opportunities."

Lesson 2 — Ride Macro Waves, Don't Fight Them

India's defense indigenization push—crystallized in the Atmanirbhar Bharat initiative—created a once-in-a-generation opportunity. As of 2023-24, around 75% of India's capital procurement budget was allocated to domestic sources, a significant increase from 68% in 2022-23. This boost aligns with India's broader "Atmanirbhar Bharat" (self-reliant India) initiative and highlights the growing role of local defence manufacturers.

That shift—from majority foreign procurement to majority domestic—represented hundreds of billions of rupees flowing to Indian companies. Jaykay positioned itself in the path of that capital flood. Contrast this with companies fighting against macro trends (e.g., traditional retail fighting e-commerce) where even brilliant execution struggles to overcome structural headwinds.

India's defence exports witnessed a remarkable surge, with the 2022-23 fiscal year recording ₹16,000 crore (USD 1.93 billion), more than doubling from ₹8,434 crore in 2021-22. This growth is largely attributed to government policies aimed at promoting indigenization and facilitating exports, as well as the development of indigenous platforms like the Light Combat Aircraft (LCA) Tejas, advanced UAVs, helicopters, and naval ships.

For investors, the lesson: identify macro structural shifts early (government policy changes, demographic trends, technological disruption) and find companies with credible strategies to capitalize on them. The wind at your back matters enormously.

Lesson 3 — Acquire Capabilities, Don't Build From Scratch

Jaykay could have tried to organically develop defense manufacturing capabilities—hiring engineers, establishing plants, pursuing certifications, courting customers. Timeline: 7-10 years, success probability: low. Instead, Allen Reinforced Plastics was incorporated in December 1987 and was involved in design, development, manufacture and testing of composite products for defence, aerospace including missile & rocket components, underwater applications, marine and submarine—instant credibility and capabilities that would have taken a decade to build.

The same logic applied to the EOS partnership for 3D printing technology, the Phillips partnership for CNC distribution, and the software acquisitions. Build what differentiates you, buy what doesn't.

For founders contemplating buildversus-buy decisions: if the capability isn't central to your competitive advantage and someone else has already figured it out, acquisition or partnership often beats organic development. But only if you can integrate and leverage effectively—which brings us to the next lesson.

Lesson 4 — Vertical Integration Creates Moats When Done Right

Jaykay built a capability stack that few competitors could match: 3D printing for complex geometries, precision machining for tight-tolerance components, composite manufacturing for lightweight structures, software for design optimization, and CNC equipment distribution for capacity building. Each capability alone is commoditized; together, they create switching costs and cross-selling opportunities.

A defense contractor working with Allen on composite rocket components might also need precision-machined metal parts, 3D-printed prototypes, and software for design verification. If Jaykay can deliver all of that from one integrated supplier with security clearances already in place, why would the customer fragment across multiple vendors?

But vertical integration carries risks: complexity, capital intensity, and the temptation to diversify into areas without competitive advantage. The JK Tech acquisition tested the boundaries of productive integration.

Lesson 5 — Family Business Agility Can Beat PSU Bureaucracy

India's defense manufacturing is dominated by PSUs (Public Sector Undertakings) like HAL, BEL, and the Ordnance Factory Board—massive organizations with deep technical capabilities but also legendary bureaucracy. Jaykay's small size and family control created decision-making speed that larger competitors couldn't match. Acquisitions that would require months of board approvals and government clearances at PSUs could be executed in weeks at Jaykay.

Mr. Abhishek Singhania is the Promoter, Chairman & Managing Director of Jaykay Enterprises Limited—meaning strategic decisions flow through one person who has both the authority and personal capital at stake. That structure enables rapid pivots but also creates key-person risk.

Lesson 6 — Promoter Skin in the Game Matters

Promoter holding has increased by 2.30% over last quarter—the Singhania family was putting more capital at risk, not extracting it. When insiders are buying, especially during a transformation where outcomes are uncertain, it signals conviction. Contrast this with companies where promoters sell into rallies or dilute aggressively—those actions speak louder than any earnings call optimism.

Lesson 7 — Timing is Everything

Would the Jaykay transformation have worked in 2010? Unlikely. The defense indigenization push hadn't begun in earnest. 3D printing was still early-stage and expensive. The political will to reshape defense procurement didn't exist.

By 2023, all the pieces had aligned: government policy favoring domestic procurement, proven technologies reducing execution risk, a competitive landscape fragmented enough to allow new entrants, and capital markets willing to fund equity raises. Strategic patience meant waiting for the right moment rather than forcing transformation prematurely.

Capital Allocation Philosophy: Growth Over Dividends

Though the company is reporting repeated profits, it is not paying out dividend—a choice that signals management's belief that reinvesting in growth creates more value than returning cash to shareholders. In transformation situations with high-return opportunities, this is exactly right. Once the platform is built and growth slows to mature-market rates, dividend policy should shift. But during the land-grab phase, retaining cash makes sense.

These lessons aren't universal—every company's situation is unique. But they represent transferable principles: identify macro tailwinds, acquire rather than build when possible, move faster than incumbents, maintain strategic focus while building capabilities, and ensure management has skin in the game. Execute those principles well, and transformations like Jaykay's become possible, if not probable.

XII. Analysis & Bear vs. Bull Case

Investors analyzing Jaykay Enterprises in November 2025 face a binary question: Is this a company in the early innings of a multi-year growth story, or one that's pulled forward gains through aggressive acquisitions and now faces execution headwinds? The truth likely lies somewhere between, but the extremes help frame the analysis.

Bull Case: The Transformation is Real and Accelerating

India is expected to experience a significant increase in yearly defence production over the next four years, with estimates reaching a substantial US$ 35.9 billion (Rs. 3 lakh crore). This growth further shows that the government is dedicated to making the nation's defence stronger by relying on itself. Within that massive expansion, Jaykay is positioned at the critical chokepoint: complex component manufacturing with composite materials, additive manufacturing, and precision machining.

Early mover advantage matters. Allen indigenously develops and supplies critical components to key defence projects in the country, such as BrahMos, Pinaka, SMILE, Akash missiles to defence undertakings such as DRDO, ISRO, OFB, BHEL, BDL—these aren't marginal programs but the crown jewels of India's defense modernization. Winning supplier status on these platforms creates multi-year revenue visibility and switching costs that protect margins.

Government relationships are in place and validated. The Ircon contract, the BrahMos orders, the ongoing relationships with HAL, BEL, ISRO—these aren't promises of future opportunity but current, executing contracts. Net profit jumped 343.42% since last year same period to ₹20.22Cr in Q1 2025-2026, with a 632.11% jump in net profits since last 3-months—proving the order book is converting to revenue and profitability.

Margin expansion is only beginning. As utilization rates increase across acquired facilities, fixed cost leverage amplifies profitability. Manufacturing businesses with high fixed costs and relatively low variable costs (once equipment and facilities are in place) show exponential profit growth as revenue scales—the "operating leverage" that investors prize.

The AI integration, while seemingly tangential, could create unique differentiation. If JK Tech's capabilities can be adapted for defense applications—AI-powered design optimization, predictive maintenance, cyber security—Jaykay offers something competitors don't: integrated physical-digital solutions. Defense systems are increasingly software-defined; hardware manufacturers who ignore software risk commoditization.

Company is almost debt free—providing financial flexibility to pursue additional acquisitions, invest in capacity expansion, or weather industry cyclicality without financial distress. Compare this to competitors levered to fund growth; Jaykay's clean balance sheet is a strategic asset.

Stock price moved up by 599.47% over last 3 years on BSE—the market is recognizing the transformation, and momentum often begets momentum. Improved analyst coverage, institutional interest, and liquidity could drive further re-rating.

Export potential remains untapped. If Jaykay can establish quality and reliability credentials domestically, Middle Eastern and Southeast Asian defense markets offer growth opportunities beyond India's borders. The composites and 3D printing capabilities are globally relevant, not India-specific.

Bear Case: Execution Risk is Enormous and Valuation Leaves No Room for Error

Stock P/E of 136 implies perfection—flawless execution, sustained high growth, margin expansion, and no competitive threats. History suggests that companies trading at triple-digit multiples rarely live up to expectations. Mean reversion is powerful.

Company has a low return on equity of 0.21% over last 3 years—while backward-looking, it reminds us this is a business that destroyed value for decades. Management's track record is short; one good year doesn't make a durable franchise.

Integration risk multiplies with each acquisition. Jaykay acquired Allen (composites), Silvergrey Engineers (machining), Neumesh Labs (3D printing), JK Technosoft (software), and JK Tech (AI services) in just over two years. Even experienced acquirers struggle to integrate one company well; simultaneously integrating five across different geographies and business models is extraordinarily difficult.

The JK Tech acquisition particularly raises red flags. The acquisition marks a significant step toward consolidating the promoters' businesses under the JKE umbrella—explicit acknowledgment this was family consolidation rather than purely strategic. Were minority shareholders diluted to benefit promoters? The optics are problematic.

Defense contracts are lumpy and unpredictable. A ₹94 crore BrahMos order is wonderful, but what if it's not renewed? What if the program faces delays or budget cuts? Defense procurement timelines stretch years, payment terms are terrible (hence the 529-day debtor cycle), and government budget constraints can derail the best-laid plans.

Company has high debtors of 529 days—nearly 18 months to collect cash. This creates perpetual working capital strain. Even profitable contracts consume cash if payments lag significantly. One bad debt or disputed contract could crater liquidity despite reported profits.

Competition is intensifying. Tata Advanced Systems, Larsen & Toubro, Bharat Forge, and dozens of other better-capitalized competitors are pursuing the same defense indigenization opportunity. Jaykay's current advantages (early mover status, existing relationships) erode as others invest in similar capabilities.

The manufacturing capacity constraint hasn't hit yet but will. Current facilities can support current revenue, but scaling to ₹500 crore or ₹1,000 crore revenue requires massive capex. That means either dilutive equity raises, debt (destroying the clean balance sheet), or growth constraints.

Promoter conflicts of interest persist. Mr. Abhishek Singhania is the Promoter, Chairman & Managing Director of Jaykay Enterprises Limited and cofounder of JK Technosoft Ltd—wearing multiple hats creates unavoidable conflicts. Will related-party transactions be priced fairly? Will resources be allocated to maximize Jaykay's value or to benefit other family entities?

Key person risk is acute. This transformation bears Abhishek Singhania's fingerprints entirely. If something happens to him, does the strategy survive? Is there a credible succession plan or management bench?

The "other income" question looms. Earnings include an other income of Rs.34.0 Cr—a huge portion of overall profitability. If this is one-time gains from asset sales or investment marks, rather than recurring business income, the sustainable earnings power is much lower than headline numbers suggest.

The Reality: Somewhere in Between

Most great investments are neither obvious nor hopeless—they're situations where reasonable people can disagree based on how they weight uncertainties. Jaykay Enterprises fits that profile perfectly.

The transformation is real. The defense indigenization tailwind is real. The acquired capabilities are valuable. Management has executed impressively on an aggressive timeline.

But the valuation is full, the risks are numerous, and the track record is short. This isn't a "sleep well at night" investment; it's a calculated bet on management execution, favorable industry dynamics, and continued government support for defense indigenization.

For value investors seeking margin of safety, the current valuation offers little. For growth investors willing to pay for potential and comfortable with volatility, the setup is intriguing. For most investors, the right answer is probably: watch closely, wait for a pullback or more evidence of sustained execution, and size appropriately for the risk level.

XIII. The Road Ahead & What Success Looks Like

Standing in November 2025, what does the next five years hold for Jaykay Enterprises? The strategic roadmap isn't fully disclosed, but the pieces point toward several clear priorities:

Execute on the Current Order Book

The most important work is unglamorous: deliver the Ircon contract on time and on budget, maintain quality on BrahMos components, win repeat orders from existing defense customers, and prove that acquired businesses can operate efficiently under Jaykay's ownership. Flawless execution on current commitments builds reputation and reference-ability for future opportunities.

Scale Allen Reinforced Plastics

Allen generated a total turnover of ₹22.07 crore in FY 2024—respectable but modest relative to the opportunity. Investing in additional capacity, expanding the product line, and leveraging Allen's relationships to win larger contracts should drive material revenue growth. The BrahMos order represented nearly ₹95 crores—multiple years of Allen's historical revenue in a single contract. Can Jaykay replicate that success across other defense platforms?

Integrate Software Capabilities or Admit the Mistake

The JK Technosoft and JK Tech acquisitions need to either demonstrate clear value creation through integration into the defense manufacturing platform, or management should consider divesting them to refocus on core capabilities. There's no shame in pivoting away from a strategic experiment that isn't working. The shame comes from persisting with suboptimal strategies out of ego or sunk cost fallacy.

If AI integration works—enabling design-for-manufacturability services, predictive maintenance offerings, or digital twin capabilities that differentiate Jaykay's manufacturing services—that creates a durable competitive advantage. If it doesn't, divesting the software businesses returns capital and management attention to where it's most productive.

Expand into Adjacent Defense Platforms

Currently, Allen supplies components for missile systems primarily. But India is modernizing across all defense domains: fighter aircraft, helicopters, naval vessels, submarines, armored vehicles, radar systems, and space applications. Each represents a potential market for composite components, 3D-printed parts, or precision machined assemblies. Systematic expansion across platforms diversifies customer concentration risk while leveraging existing capabilities.

Build a World-Class Engineering Brand

India's defense procurement is relationship-driven, and reputation matters enormously. Government and PSU customers need confidence that suppliers will deliver—on time, to specification, with proper security protocols. Jaykay should invest heavily in thought leadership, technical publications, defense expo presence, and case studies documenting successful programs. The goal: when defense contractors think "advanced composites" or "3D printing for aerospace," Jaykay is top-of-mind.

Consider Export Opportunities Selectively

Middle Eastern nations are diversifying defense supply chains. Southeast Asian countries are modernizing militaries. These markets value quality, reliability, and technologies that local manufacturers can't yet provide. But export defense sales require government-to-government relationships, export licenses, and patient capital. This shouldn't be the primary strategy, but selective opportunities could accelerate growth and diversify geography-specific risk.

If I Were CEO: Four Priorities

If we ran Jaykay Enterprises, four priorities would dominate the agenda:

1. Execution Discipline Over Growth Ambition The temptation to chase every opportunity is understandable—defense indigenization is the opportunity of a generation. But trying to be everything to everyone usually produces mediocrity everywhere. Focus on aerospace composites, 3D printing for prototyping, and precision machining. Say no to adjacent opportunities unless they clearly leverage existing capabilities and customer relationships.

2. Transparency with Minority Shareholders Address the related-party transaction concerns head-on. Publish detailed valuation methodologies for acquisitions. Establish independent board committees to review transactions. Earn investor trust through disclosure and fair dealing, not opacity and "trust us" communication.

3. Talent Investment as Core Strategy Manufacturing excellence and engineering services businesses are ultimately people businesses. Recruit aggressively from defense PSUs, aerospace programs, and top engineering colleges. Create career paths that retain talent. Build an engineering culture that attracts the best technical minds. Compensation matters, but so does mission, pride in work, and opportunity to solve hard problems.

4. Build Institutional Credibility Engage with research analysts, host facility tours for institutional investors, present at defense industry conferences, and publish technical papers. The goal: transform Jaykay from "that small-cap defense stock" to "the leading independent defense component manufacturer in India." Perception drives valuation, which drives capital availability, which drives growth—a virtuous cycle worth cultivating.

Can Abhishek Singhania Build the Indian Northrop Grumman?

That's probably the wrong benchmark—Northrop Grumman is a $70 billion market cap prime contractor building complete systems (aircraft, ships, satellites, missiles). Jaykay is a component manufacturer and services provider, a tier-2 or tier-3 supplier in defense industry parlance.

A better comparison might be Hexcel (American advanced composites manufacturer), Spirit AeroSystems (tier-1 aerostructures manufacturer), or smaller defense-focused component suppliers that achieve $1-3 billion revenue by being excellent at a specific capability rather than trying to do everything.

Could Jaykay reach ₹2,000-3,000 crore revenue with 15-20% EBITDA margins in five years? That's plausible with successful execution—it requires roughly 4x revenue growth from current run-rates, which is aggressive but not absurd given the industry backdrop. That would justify a ₹5,000-8,000 crore market cap (roughly 2x current levels), generating attractive returns for investors who buy at today's prices if execution delivers.

But that's a big "if." Defense is littered with companies that had great technology, strong customer relationships, and capable management—yet still failed due to program delays, budget cuts, execution missteps, or competitive dynamics. The road ahead is opportunity-rich but execution-dependent.

XIV. Final Reflections

Step back from the financial minutiae, the acquisition details, and the bull/bear debate. What makes the Jaykay Enterprises story fascinating?

Proof That Corporate Resurrection is Possible

Business cemeteries are filled with companies that couldn't adapt—Kodak, Blockbuster, Nokia, Yahoo, and countless others that dominated industries until they didn't. The usual narrative is that incumbents can't transform; disruption happens through creative destruction, not adaptive change.

Jaykay Enterprises offers a counter-narrative: a 60-year-old company trapped in a dying business, from a family business structure often maligned as sclerotic, operating in a country where "License Raj" mentality still lingers—yet successfully pivoting to cutting-edge manufacturing in a strategically critical industry. If Jaykay can do it, other "zombie" companies might too. That's inspiring for founders, management teams, and investors who believe businesses can change.

The India Story in Microcosm

India's transformation from services-led economy to deep-tech manufacturing hub is one of the defining economic narratives of the 2020s. India's defence ecosystem has transformed considerably across key areas in recent years. Notably, institutional and policy changes have driven defence indigenisation, domestic capital procurement and defence exports.

Jaykay's journey parallels the national one: from commodity production (synthetic fibers mirror India's legacy textile focus), through a crisis of strategic direction (the post-liberalization identity search), to technology-driven manufacturing (defense indigenization and high-tech capabilities). Micro-level company transformations and macro-level national transformations often move together—recognizing that parallel helps identify investment opportunities.

What We Got Wrong About Family Businesses

Professional investors often view family-controlled businesses with skepticism: concentrated ownership enables value extraction, related-party transactions favor insiders, nepotism trumps merit, and strategic vision gets sacrificed for family harmony.

Jaykay demonstrates family ownership's potential advantages: decision-making speed (no lengthy board processes or shareholder votes), long-term orientation (Abhishek Singhania is building for generations, not quarterly earnings), risk tolerance (willingness to execute bold transformations that career-risk-averse managers avoid), and network effects (leveraging JK Organisation relationships and reputation).

Family ownership is neither inherently good nor bad—it amplifies management quality. Great families build generational businesses; weak families destroy them. The Singhania family, at least in Jaykay's case, seems to be demonstrating the former.

The "Acquired" Framework Applied: Did They Acquire Well?

In classic Acquired podcast style, the ultimate question is: Did the acquisitions create durable value? Did Jaykay "acquire" its way to competitive advantage, or just buy revenue growth that competitors will eventually commoditize?

The verdict: Mostly yes, with one questionable decision.

Allen Reinforced Plastics (July 2023): Unambiguously successful. ₹90 crores paid for instant defense credibility, established customer relationships, scarce composite manufacturing expertise, and multi-decade institutional knowledge. This acquisition unlocked everything else. Grade: A

Phillips Partnership (December 2023): Clever asset-light approach to CNC equipment distribution. The Ircon contract validated the strategy. Creates optionality for capacity-building contracts as India invests in MSME training. Low capital commitment, high potential return. Grade: A-

JK Technosoft (February 2025): Strategically coherent—software, simulation, and digital services complement manufacturing. But limited public information makes assessment difficult. If integrated well, creates differentiation. If not, a distraction. Judgment reserved. Grade: B+ (provisional)

JK Tech (February 2025): Questionable strategic fit. Acquiring a global AI services company focused on Retail/CPG/Insurance when you're building a defense manufacturing platform seems like overreach. Explicitly described as "consolidating the promoters' businesses," suggesting non-strategic motivations. High integration risk, uncertain synergy capture. Grade: C+

Overall acquisition strategy: B+ — Three out of four decisions strengthened the defense platform; one looks like empire-building.

Biggest Surprise: The Speed of Transformation

From the Allen acquisition in July 2023 to a ₹94 crore BrahMos order in September 2025—that's just 26 months. From synthetic fiber commodity business to aerospace component supplier with ₹200+ crore order book—in two years.

Corporate transformations usually take 5-10 years to fully manifest. Jaykay compressed the timeline dramatically, enabled by aggressive M&A, favorable industry tailwinds, and decisive leadership. That speed created risks (integration complexity, execution pressure, valuation getting ahead of results) but also advantages (seizing first-mover opportunities before competition intensified).

For Founders: Sometimes Complete Reinvention is the Answer

Most business advice counsels incremental improvement: optimize margins, improve customer satisfaction, enhance products, expand markets. But sometimes the right answer is scorching the earth and starting over on the same land.

Jaykay didn't try to make better acrylic fibers or find new markets for synthetic textiles. It exited entirely and built something new. That takes courage, but also clear-eyed assessment that incremental improvements in a declining business still produce decline—just slower decline.

If you're running a business with broken unit economics in a structurally declining industry, the playbook is: maximize cash extraction from legacy operations while aggressively building/acquiring capabilities in growth industries. Don't sentimentally preserve dying businesses out of nostalgia or fear.

For Investors: Inflection Points Beat Trends

Trend-following works in markets: buy high-growth companies in expanding industries, ride the wave until momentum breaks. But the highest-return opportunities often come from inflection points—companies or industries transitioning from decline to growth, chaos to order, or mediocrity to excellence.

Jaykay in 2022 (before the Allen acquisition, before defense orders, while still associated with synthetic fibers) was an inflection point opportunity. The price was low, expectations were zero, and strategic direction was uncertain. By 2025, the stock had re-rated 6x, the transformation was proven, and expectations were high.

The best time to invest was when the story was ambiguous but the pieces were falling into place. By the time transformation is obvious and validated, much of the return has been captured. This requires conviction to invest when facts are incomplete—uncomfortable but potentially lucrative.

Final Thought: Jaykay Might Be the Most Interesting Defense Stock Nobody's Talking About

Open a discussion about Indian defense stocks, and the usual names dominate: HAL (Hindustan Aeronautics Limited), Bharat Dynamics, Mazagon Dock, Bharat Electronics, or private giants like Tata's defense arm and L&T's defense segment. These are large, liquid, institutionally-owned, and widely covered.

Jaykay Enterprises? A ₹3,000 crore market cap small-cap with spotty analyst coverage, limited institutional ownership, and a confusing recent history. But that obscurity creates opportunity—if the transformation delivers, Jaykay offers asymmetric upside as the market gradually recognizes what's been built.

The risk, of course, is that obscurity reflects reality: the market understands something bulls don't, and the valuation gap is justified. Only time and execution will reveal which narrative is correct.

For now, Jaykay Enterprises stands as one of the most dramatic corporate transformations in recent Indian business history—from textile commodity producer to defense technology provider in less than five years. Whether that transformation creates sustainable value or proves to be an ephemeral bubble of acquisition-driven growth will define whether this story ends as inspiration or cautionary tale.

The next 24 months will tell.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube