BorgWarner: From the Indianapolis 500 to the Electric Future

I. Introduction & Episode Roadmap

Picture the scene: May 1936, Indianapolis Motor Speedway. The roar of engines subsides as Louis Meyer climbs out of his winning car after claiming his third Indianapolis 500 victory. As photographers jostle for position, something gleams in the Indiana sunshine behind him—a towering five-foot-four-inch sterling silver trophy, weighing over 110 pounds, Art Deco wings flanking its sides like the speed of flight itself. Meyer, parched and triumphant, asks for a cold bottle of buttermilk. Two American traditions were born that day: the milk celebration and the Borg-Warner Trophy.

That trophy, now valued at over $3.5 million and permanently housed at the Indianapolis Motor Speedway Museum, tells the story of American automotive innovation better than any corporate history ever could. But the company that commissioned it—BorgWarner—has a story even more remarkable than the racing legends whose faces are permanently affixed to that sterling silver.

BorgWarner Inc. is an American automotive and e-mobility supplier headquartered in Auburn Hills, Michigan. As of 2023, the company maintains production facilities and sites at 92 locations in 24 countries, generates revenues of US$14.2 billion, and employs around 39,900 people. The company is one of the 25 largest automotive suppliers in the world.

But these statistics tell only a fraction of the story. The central question this analysis grapples with is both simple and profound: How did a collection of early 20th-century auto parts makers survive hostile takeovers, leveraged buyouts, multiple spin-offs, and now attempt to reinvent itself for the electric vehicle era?

Foundational products—the combustion vehicle business—contributes more than 80% to group revenue while BorgWarner transitions to becoming an electric vehicle-centric parts supplier. In 2024, 23% of the company's revenue was sourced from Volkswagen and Ford. Revenue is well diversified geographically, with approximately a third each generated in North America, Europe, and Asia.

The themes that emerge from BorgWarner's nearly century-long journey read like a masterclass in corporate strategy: consolidation as survival strategy, the art of the spin-off, navigating industry disruption, and perhaps most audaciously—the courage to cannibalize your own business before someone else does.

Under the "Charging Forward" strategy unveiled in 2021, the company has set an ambitious target: BorgWarner stands to benefit from the industry's electrification trend, with potential content per vehicle rising from $548 for combustion vehicles to $2,569 for battery electric vehicles. This represents a nearly 5x increase in potential revenue per vehicle, providing a clear growth path as EV adoption increases.

That's the opportunity. The question is whether a 97-year-old company with its DNA forged in synchronizers, transfer cases, and turbochargers can execute one of the most dramatic pivots in automotive history.

II. Origins: The 1928 Merger & Early Automotive Industry

The Founding Companies

BorgWarner's history is as complex and interesting as one of its powertrain assemblies: a cluster of components (in this case, small, specialized auto parts manufacturers) harmoniously working to power a highly successful industrial giant.

To understand what BorgWarner became, you must first understand what America's automobile industry looked like in the 1920s. Picture Chicago in that era—not just the gangsters and jazz, but the industrial muscle that was transforming the Midwest into the arsenal of the automotive revolution. Ford's moving assembly line had democratized the automobile, and suddenly, millions of Americans needed parts, components, and systems that no single company could possibly manufacture.

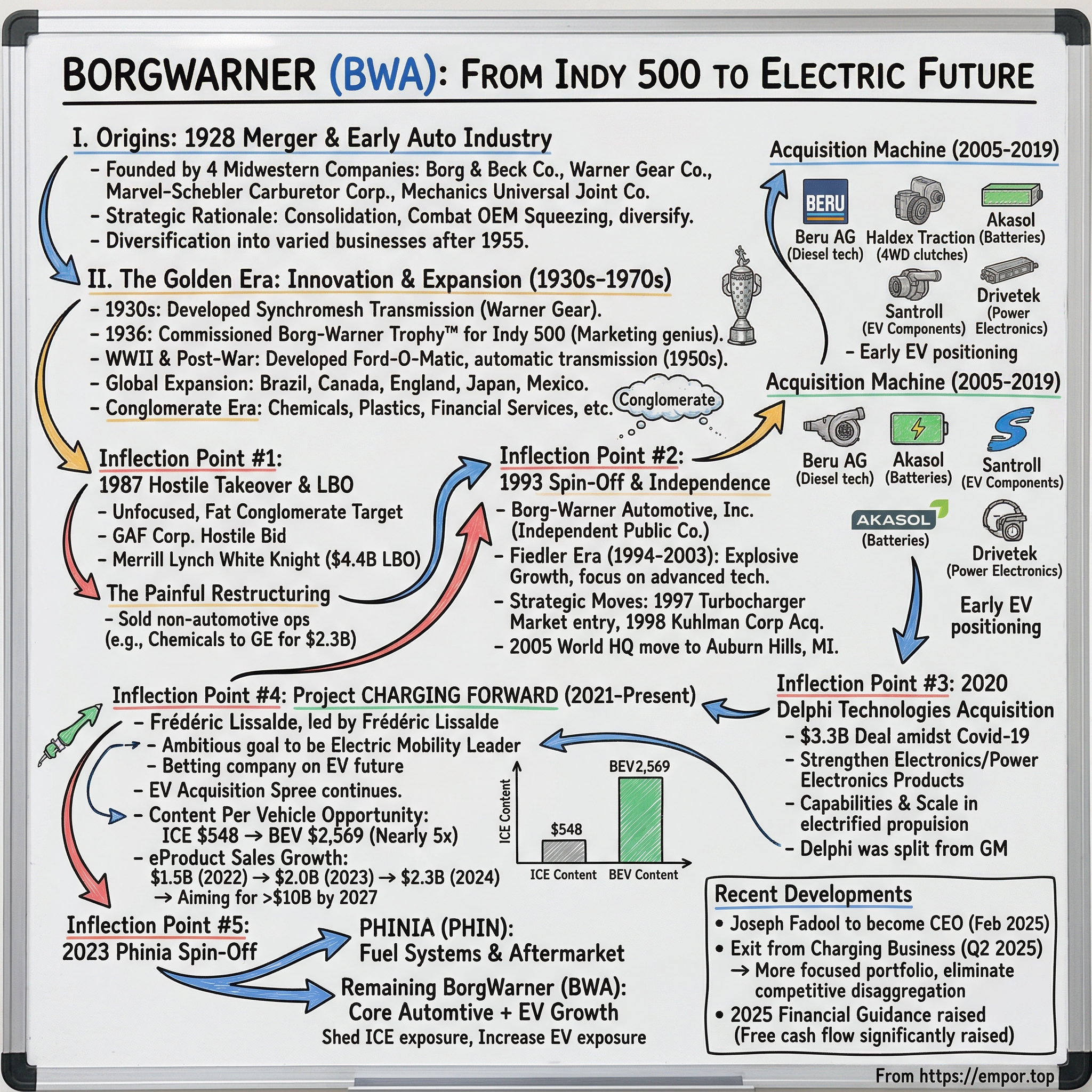

Borg-Warner Corporation was created in 1928 by the merger of four midwestern manufacturing companies: Borg & Beck Company, Warner Gear Company, Marvel-Schebler Carburetor Corporation, and Mechanics Universal Joint Company. These four companies had prospered during the early 20th century by supplying innovative parts to U.S. car manufacturers.

Each of these founding companies brought something essential to the new entity. Warner Gear, founded by Thomas Warner in Muncie, Indiana in 1901, had established itself as a pioneer in manual transmission technology. Borg & Beck, established by Charles Borg and Marshall Beck in 1903, specialized in clutches—the critical interface between engine and transmission. Marvel-Schebler, operating from Flint, Michigan, had mastered the arcane art of carburetion. And Mechanics Universal Joint provided the critical components that allowed power to transfer through changing angles as vehicles bounced down America's largely unpaved roads.

The Strategic Rationale for Consolidation

Why merge in 1928? The logic was both defensive and offensive. The explosive growth of Ford, General Motors, and Chrysler created a peculiar dynamic in the supplier industry. These automotive giants wielded enormous purchasing power, and fragmented suppliers found themselves squeezed on pricing while facing the constant threat that their customers might integrate backward and produce components themselves.

By consolidating, Borg-Warner achieved something remarkable: it became too important to ignore and too diversified to replace. When you supplied transmissions AND clutches AND carburetors AND universal joints, an automaker couldn't easily walk away without disrupting multiple vehicle programs simultaneously. This wasn't accidental—it was strategic genius disguised as industrial consolidation.

Borg-Warner continued to be heavily dependent upon this business. Nevertheless, diversification, especially after 1955, eventually brought BWC to appliances, heating and air conditioning, chemicals, financial services, and protective services. These new operations enabled Borg-Warner to weather the trend toward integration among U.S. carmakers.

Chicago served as the headquarters, placing the company at the crossroads of American industry—equidistant from the Big Three in Detroit and the nation's agricultural heartland that was rapidly mechanizing and demanding its own automotive solutions.

The 1928 merger established a pattern that would define BorgWarner for nearly a century: when faced with market fragmentation or competitive pressure, consolidate; when faced with technological change, acquire or develop; and always, always maintain optionality.

III. The Golden Era: Innovation & Expansion (1930s–1970s)

Technological Breakthroughs

The 1930s tested the young corporation severely. The Great Depression decimated automobile sales, yet Borg-Warner emerged not just intact but stronger, having used the downturn to consolidate market position and invest in technologies that would prove transformative.

In the next decade, Warner Gear was one of the first automotive suppliers to develop its own synchromesh transmission—the 'synchronizer'—a device that made a manual transmission's gear teeth mesh together with ease for smooth shifting, making synchromesh transmissions broadly available; Morse Chain brought out its first roller chain; and BorgWarner's self-contained overdrive transmission was introduced, with Chrysler and 11 other automakers purchasing the transmissions. BorgWarner Automotive Service Parts Division was also founded in the 1930s, and in 1936, the company commissioned a sterling silver trophy for the Indianapolis 500 (the Borg-Warner Trophy).

The synchronizer deserves special attention because it illustrates BorgWarner's approach to innovation. Before synchromesh transmissions, shifting gears required a skill called "double-clutching"—releasing the clutch, moving to neutral, matching engine speed manually, then engaging the new gear. Get it wrong, and you'd produce the horrifying grinding sound that still haunts drivers of older vehicles. The synchronizer automated this process mechanically, democratizing the ability to drive a manual transmission. Suddenly, millions more Americans could competently operate automobiles.

The Indianapolis 500 Connection

BorgWarner is closely associated with the Indianapolis 500, one of the world's greatest racing events. Since 1936, the Borg-Warner Trophy™ has been synonymous with top performance, speed and leading-edge automotive technology, the same qualities that continue to characterize us today.

Why would an auto parts company commission such an extravagant trophy? The answer reveals sophisticated marketing thinking decades ahead of its time. Commissioned in 1935, it was designed by Robert J. Hill and Spaulding-Gorham, Inc. of Chicago. The trophy was unveiled at a dinner hosted by then-Indianapolis Motor Speedway (IMS) owner Eddie Rickenbacker in 1936. At that dinner, the trophy was officially declared the annual prize for Indianapolis 500 winners. Designed in the Art Deco style that was popular in the 1930's, the trophy is made of sterling silver and is just over 5 feet 4 inches tall and weighs approximately 110 pounds, of which roughly 80 pounds is sterling silver.

Every year, when the winning driver hoists that trophy (or more accurately, poses with it—the trophy isn't actually given to winners), millions of Americans see the Borg-Warner name. The faces of racing legends from Ray Harroun in 1911 to Josef Newgarden in 2024 are permanently affixed to its surface—The bas-relief, sterling silver image of Newgarden is the 111th face to be affixed to the iconic trophy, awarded annually to the winner of the Indianapolis 500 since 1936.

It was—and remains—one of the most brilliant sustained brand-building exercises in industrial history.

World War II & Post-War Growth

The company's trajectory accelerated after World War II. In 1950, it developed its first lock-up torque converter, a three-speed automatic transmission (the 'Ford-O-Matic'), along with Holley brand Borg & Beck Carburetors. Studebaker and Ford initiated long-term cooperations in regard to the newly developed technologies. The company's automotive sales reached over $200 million at the time.

The Ford-O-Matic transmission represented a bet on where America was heading: toward comfort, convenience, and the suburbs. As highways spread and commutes lengthened, drivers increasingly preferred the effortlessness of automatic transmissions. BorgWarner positioned itself perfectly to ride this wave.

Global Expansion

As the 1950s continued, BorgWarner expanded its operations, establishing Borg & Beck do Brasil South America and setting up new facilities in Simcoe, Ontario, and Letchworth (England). The English facility was soon producing Warner Gear's overdrive units and the Model D.G. automatic transmission. Marvel-Schebler was developing fuel injection systems, while BorgWarner developed a line of paper-related wet friction components. Later on, BorgWarner acquired Coote & Jurgenson, an Australian transmission producer for cars and tractors in 1957.

The expansion into Japan proved particularly prescient. In 1962, BorgWarner expanded into Mexico, and into Asia with two Japanese joint ventures (NSK-Warner and Tsubakimoto-Morse). In 1969, Aisin-Warner was formed as another joint venture in Japan to build automatic transmissions.

These Japanese partnerships would prove invaluable decades later, as Japanese automakers rose to global prominence and BorgWarner found itself already embedded in their supply chains.

The Conglomerate Era & Seeds of Future Problems

BorgWarner also diversified into several other industries, while its automotive division remained contributing upwards of 50 percent of BorgWarner's total revenue.

By the 1970s, BorgWarner had become a true conglomerate—chemicals, plastics, financial services, and security services all operated under the corporate umbrella. This diversification strategy was fashionable at the time, supposedly reducing risk through portfolio diversification. In reality, it created a company that was neither focused nor particularly good at any one thing. The automotive division, which had built the company's reputation, was now just another business unit competing for capital and attention.

When Borg-Warner celebrated its 50th anniversary in 1978, its automotive profits had reached $98 million. The next year, overall sales topped $2.7 billion as the company headed into the tumultuous 1980s.

What the executives gathered at that anniversary celebration couldn't know was that the corporate raider era was about to begin—and their diversified conglomerate would prove an irresistible target.

IV. Inflection Point #1: The 1987 Hostile Takeover & LBO

The Corporate Raiders Arrive

The 1980s brought a new breed of financial predator to corporate America. Names like Carl Icahn, Ronald Perelman, and Irwin Jacobs became synonymous with hostile takeovers, leveraged buyouts, and the dismemberment of conglomerates that had grown fat and unfocused.

Borg-Warner's chemicals and plastics business had become profitable enough to attract unwanted attention.

Borg-Warner's growth, however, was halted in 1987 when it became the object of a hostile takeover attempt by GAF Corporation, a chemical company based in Wayne, New Jersey. Samuel J. Heyman, the chairman of GAF, was searching for acquisitions to expand his company's chemical business, and Borg-Warner's profitable chemical operations had attracted his attention.

Yet for all of Borg-Warner Automotive's success, there was a steep price—the interest of corporate raiders Irwin Jacobs and Samuel Heyman in the fast-and-loose leveraged buyout (LBO) haven of the 1980s. After spending $680 million, Jacobs and Heyman each possessed ten percent of the company, to the shock and dismay of Borg-Warner's board.

The board faced an impossible choice. Let the raiders accumulate more shares and eventually force a breakup? Or find a way to take the company private and restructure on their own terms?

Determined to squelch not only Jacobs' and Heyman's takeover attempt but any future opportunists as well, Borg-Warner's brass decided to take the company private. Turning to Merrill Lynch Capital Partners, an LBO fund, Borg-Warner's board was supposed to offer stockholders $43 per share. Instead, the directors decided to wait, hoping Jacobs and Heyman would lose interest. However, in March 1987 Heyman bought Jacobs' holdings and offered stockholders $46 a share in a hostile takeover bid.

The Merrill Lynch White Knight

Borg-Warner's independence was finally preserved by the sudden appearance of a $4.2 billion leveraged buyout offer from Merrill Lynch Capital Partners. Although Merrill Lynch promised to respect the wishes of Borg-Warner executives, the $2.75 billion in debts contracted during the buyout forced drastic action.

Borg-Warner Corp. announced major changes Thursday in its top management hours after a $4.4 billion takeover by an investor group led by a Merrill Lynch & Co. subsidiary was completed.

The Painful Restructuring

At Merrill Lynch's insistence Bere was brought back as chief executive in June 1987. This was swiftly followed by wholesale changes in top management, including the departure of Johnson. Bere, one of eight managing partners and a 2.5% shareholder in the now-private firm, arranged the sale of all Borg-Warner operations except the automotive group and the guard and courier businesses. The largest sale involved the chemicals group, which was bought in September 1988 by General Electric for $2.3 billion.

The irony was staggering. The very diversification strategy that was supposed to protect Borg-Warner had made it a target. Heyman didn't want the automotive business—he wanted the chemicals. By stripping the company down to its automotive core, the LBO restructuring inadvertently accomplished exactly what would be needed for the company's future success.

The steady if unspectacular growth experienced by Borg-Warner was interrupted in 1986 when the company went private through a leveraged buyout. Faced with a large debt load, the corporation sold most of its diversified operations and returned to its core business of automotive parts manufacturing.

Sometimes the best thing that can happen to a company is being forced to rediscover what made it great in the first place. The corporate raiders, in their relentless pursuit of short-term profits, inadvertently positioned BorgWarner for its next century of success by stripping away decades of unfocused diversification.

V. Inflection Point #2: The 1993 Spin-Off & Independence

A New Beginning

1987: Company is taken private through a $4.4 billion leveraged buyout. 1993: Borg-Warner Automotive, Inc. is spun off from Borg-Warner Security Corporation.

The six years between the LBO and the spin-off were spent restructuring, reducing debt, and preparing the automotive division for independence. When Borg-Warner Automotive finally emerged as an independent public company in 1993, it did so carrying the scars of its ordeal—but also a newly sharpened focus.

The company closed its first year of independence with $985.4 million in sales (and a net loss of $97.1 million due to spinoff accounting charges), up from 1992's $926 million.

The Fiedler Era & Explosive Growth

In July 1994, John Fiedler was named president and CEO of Borg-Warner Automotive after serving Goodyear's North American Tire division for 30 years. The company, poised for a renaissance as the automotive industry boomed, was now comprised of four subsidiaries: Automatic Transmission Systems, Control Systems, Morse TEC (Chain Systems), and Powertrain Systems. The latter unit, propelled by transfer cases—the darling of the sport utility vehicle and light truck industry—grew by over 12 percent to account for 40 percent ($550.7 million) of 1994's total $1.2 billion in revenues. When Fiedler came on board, one of his first pronouncements was his intention to double BWA's revenues by the end of the 1990s, implement a slew of cost reductions, improve productivity, increase foreign investments, and form more joint ventures both in and out of North America.

Fiedler, an Akron native who had spent three decades in the tire industry at Goodyear, brought an outsider's perspective and a tire executive's discipline to the automotive components business. Born in Akron in 1938, John Fiedler was raised in Cuyahoga Falls, graduated from "old" St. Mary's High School and earned his bachelor's degree in chemistry from Kent State University. As a Sloan Fellow, he received his master's degree in business from the Massachusetts Institute of Technology in 1979. He has spent the past 30 years in the chemical and tire industry.

Fiedler also hinted that he and BWA's directors were in an acquisitive mood: "We're in an excellent position to grow and we're going to raise some eyebrows," he told Barron's in August 1994, after posting an impressive 25 percent sales gain for the first half of the year, way over the industry's 11 percent overall increase. The company finished 1994 with sales of $1.22 billion and a net profit of $64.4 million.

Fiedler retired in 2003, having shepherded a booming nine-year span in which revenues surged from $800 million to $2.73 billion. His tenure was noteworthy for the focus on advanced technology products, the big move into engine components, and a lessening in the company's dependence on the U.S. Big Three automakers. To the last point, by 2002 the Big Three comprised only 63 percent of BorgWarner's sales.

Strategic Moves (1990s-2000s)

1997: Borg-Warner enters turbocharger market through purchase of majority interest in German firm. 1998: Turbocharger maker Kuhlman Corporation is acquired.

The turbocharger entry proved transformative. At the time, turbochargers were primarily associated with high-performance European diesels. Few predicted that emissions regulations and fuel efficiency standards would make turbocharging nearly universal across the global automotive industry within two decades. BorgWarner's early bet would eventually make it one of the world's largest turbocharger manufacturers.

The company is also notable for co-developing a variable-geometry turbocharger with Porsche, the Variable Turbine Geometry (VTG) system, used in the 2007 911 Turbo.

In 2005, BorgWarner's world headquarters moved from Chicago to Auburn Hills, Michigan—heart of America's automotive industry. The move symbolized the company's complete transformation from diversified conglomerate to focused automotive technology leader.

VI. The Acquisition Machine: Building Scale (2005-2019)

Strategic M&A Activity

The post-Fiedler era saw BorgWarner shift into aggressive acquisition mode. This included German-based battery manufacturer Akasol in the same year and in 2022, Santroll Automotive Components and Rhombus Energy Solutions. In December 2022, BorgWarner had acquired the Swiss-based company Drivetek AG, a manufacturer of engineering and products for inverters, electric components, and power electronics.

The company made a particularly strategic acquisition in 2005, taking a majority stake in Beru AG, a German supplier specializing in diesel cold-start technology, sensors, electronics, and ignition technology. This positioned BorgWarner perfectly for the European diesel boom that followed.

In 2010, BorgWarner acquired Swedish-based Haldex Traction Systems, known for the Haldex clutch—a multi-plate wet clutch used in four-wheel-drive passenger cars. The Haldex clutch had become standard equipment in countless crossover vehicles, and the acquisition brought this critical technology in-house.

Early EV Positioning

In 2016, BorgWarner presents its first integrated electric drive module (iDM) for the electric vehicle market and launches the 48-volt eBooster® electrically driven compressor in Daimler's 3.0-liter gasoline engine. Complementing its power electronics and electrified propulsion solutions, BorgWarner acquires Sevcon, Inc. in 2017.

To stay ahead of emerging technology trends, the company partners with Plug and Play and Franklin Venture Partners in 2018. In 2019, BorgWarner acquires propulsion inverters and controls businesses for HEVs and EVs in the specialty and commercial vehicle sectors.

Customer Diversification

One of the most important metrics in the automotive supply business is customer concentration. Over-dependence on a single automaker creates existential risk—as countless suppliers discovered during the Big Three's near-collapse in 2008-2009.

By 2002 the Big Three comprised only 63 percent of BorgWarner's sales.

Today, Volkswagen Group serves as BorgWarner's largest customer by sales volume. The German automotive manufacturer has used BorgWarner K-Series turbochargers exclusively since 1999 for their 1.8T engines.

The transformation was remarkable. From a company once entirely dependent on Detroit's Big Three, BorgWarner had evolved into a globally diversified supplier with relationships spanning virtually every major automaker in the world.

VII. Inflection Point #3: The Delphi Technologies Acquisition (2020)

The Transformative Deal

BorgWarner Inc. and Delphi Technologies PLC announced that they have entered into a definitive transaction agreement under which BorgWarner will acquire Delphi Technologies in an all-stock transaction that values Delphi Technologies' enterprise value at approximately $3.3 billion.

The timing could hardly have been worse—or better, depending on your perspective. The deal was announced in January 2020, just as the COVID-19 pandemic was beginning its global spread. By spring, automotive production had collapsed, and deals of this magnitude seemed absurdly risky.

BorgWarner Inc. today announced it has completed its acquisition of Delphi Technologies. The combination of BorgWarner and Delphi Technologies is expected to strengthen BorgWarner's electronics and power electronics products, capabilities...

On 30 September 2020 the European Commission unconditionally approved BorgWarner's acquisition of Delphi Technologies. The transaction had previously been cleared in several other jurisdictions worldwide including China, South Korea, Mexico, Russia and Turkey.

Why Delphi Was Critical

Strengthen BorgWarner's electronics and power electronics products, capabilities and scale, creating a leader in electrified propulsion systems that BorgWarner believes is well-positioned to take advantage of future propulsion migration. Delphi Technologies brings industry leading power electronics technology and talent, with an established production, supply and customer base.

The combined company will be able to offer standalone and integrated solutions to its power electronics customers.

The acquisition addressed a critical gap in BorgWarner's capabilities. While the company had mastered mechanical systems—transmissions, turbochargers, transfer cases—the future belonged to electronics. Electric vehicles don't need turbochargers, but they absolutely need sophisticated power electronics, inverters, and control systems. Delphi Technologies brought exactly these capabilities.

Delphi itself emerged from the supplier business of General Motors in 1999. In 2017, the company will be split up; the Delphi Technologies division will concentrate on drive technologies, while the spin-off company Aptiv will focus on vehicle electronics, networking and autonomous driving.

The irony was rich: BorgWarner was acquiring a company that had been spun out of GM, just as BorgWarner itself had once been restructured through spin-offs. The circle of automotive industry consolidation and reconsolidation continued.

VIII. Inflection Point #4: Project CHARGING FORWARD (2021-Present)

The Grand Strategy

In 2021, Frédéric Lissalde (born July 17, 1967) is the president and chief executive officer (CEO) of BorgWarner Inc. Lissalde was appointed to this role on Aug. 1, 2018, taking over for retiring president and CEO, James Verrier.

Prior to joining BorgWarner, Lissalde held positions at Valeo and ZF Friedrichshafen AG in program management, engineering, operations and sales roles throughout the U.K., Japan and France. Lissalde attended Ecole Nationale Supérieure d'Arts et Métiers (ENSAM), where he earned a Master of Engineering degree. He has a Master's of Business Administration from HEC Paris (ISA) and is also a graduate of executive courses at INSEAD, Harvard University and Massachusetts Institute of Technology.

Under Lissalde's leadership, BorgWarner unveiled its most ambitious strategic initiative ever: "Charging Forward."

BorgWarner approached us at a very exciting time for the company. They had a clear and transformative business strategy—Charging Forward—that laid out clear goals to become an electric mobility leader.

The strategy set aggressive targets: grow revenue from electric vehicles to approximately 45% of total revenue by 2030 from less than 3% at the time. For a company that had built its reputation—and its iconic trophy—on combustion engine technology, this was nothing short of betting the company on an electric future.

EV Acquisition Spree (2021-2022)

The strategy wasn't just words on PowerPoint slides. BorgWarner backed it with aggressive acquisitions:

- 2021: Akasol (German battery manufacturer)

- 2022: Santroll Automotive Components

- 2022: Rhombus Energy Solutions

- 2022: Drivetek AG (Swiss inverter manufacturer)

Each acquisition addressed a specific gap in BorgWarner's electrification portfolio. Akasol brought battery pack manufacturing expertise. Rhombus added EV charging infrastructure. Drivetek contributed power electronics capabilities.

The Content Per Vehicle Opportunity

BorgWarner stands to benefit from the industry's electrification trend, with potential content per vehicle rising from $548 for combustion vehicles to $2,569 for battery electric vehicles. This represents a nearly 5x increase in potential revenue per vehicle, providing a clear growth path as EV adoption increases.

This single statistic explains why management was willing to bet so aggressively on electrification. If a traditional internal combustion engine vehicle contained roughly $550 of BorgWarner content, and a battery electric vehicle could contain nearly five times that amount, the growth opportunity was transformational—even if EV adoption took longer than optimists predicted.

eProduct Growth

The company's eProduct sales have shown consistent growth despite market volatility: eProduct sales grew from $1.5 billion in 2022 to $2.0 billion in 2023 and reached $2.3 billion in 2024.

As part of Charging Forward 2027, the company established 2027 targets of achieving more than $10 billion in eProduct revenue, delivering approximately 7% adjusted operating margin on its eProduct portfolio, and sustaining its strong foundational operating margins.

IX. Inflection Point #5: The Phinia Spin-Off (2023)

The Logic of Separation

BorgWarner Inc. today announced the successful completion of the spin-off of its Fuel Systems and Aftermarket segments into a separate, publicly-traded company named PHINIA (NYSE: PHIN).

Frédéric Lissalde, President and Chief Executive Officer, said: "A tremendous amount of work has gone into bringing us to where we are today." Two years ago, BorgWarner announced Charging Forward, the company's strategy to accelerate its transition to electrification. That strategy included the disposition of $3B to $4B in combustion-related revenue by 2025. The completion of the spin-off of PHINIA combined with the 2022 sale of the North American controls business represents the completion of this key pillar of the Charging Forward strategy.

PHINIA common stock will be traded on the New York Stock Exchange under the ticker symbol PHIN. The first day of trading is expected to be Wednesday, July 5, 2023.

BWA will spin-off 100% of PHIN. Shareholders will receive 1 share of PHIN for every 5 shares of BWA.

The spin-off logic was elegant: PHINIA would focus on fuel systems and aftermarket distribution—businesses with stable cash flows but limited growth potential in an electrifying world. BorgWarner would retain the higher-growth (if higher-risk) electrification businesses alongside its traditional turbocharger and drivetrain operations.

In 2022, the SpinCo businesses generated $3.6BN in revenue (21% of total revenue) and have an adjusted operating profit of 14.5% (vs. 13.7% for RemainCo).

To put it simply, the rationale for the spin-off is to shed exposure to internal combustion engines and increase exposure to electric vehicles. Borgwarner is on track to meet or exceed its goal of 25% of revenue from EV by 2025.

X. Recent Developments: CEO Transition & Strategic Refinement

Leadership Succession

Joseph Fadool, EVP and COO, to Become President and CEO effective close of business on February 6, 2025. BorgWarner Inc. today announced that its Board of Directors approved a leadership succession plan whereby Joseph Fadool, BorgWarner's Executive Vice President and Chief Operating Officer, has been appointed President and Chief Executive Officer and a member of BorgWarner's Board of Directors effective at the close of business on February 6, 2025.

At that time, Frédéric Lissalde will retire from his role as President and CEO and step down from the Board of Directors. To support a seamless transition, Mr. Lissalde will serve in an advisory role until August 30, 2025. Alexis P. Michas, Non-Executive Chairman of the Board of Directors, said, "As CEO, Fred has reshaped our product portfolio and set BorgWarner on a path to lead the world's energy transition to electrified vehicles."

Joseph Fadool joined BorgWarner in 2010 and has held a number of top positions across the Company, including Chief Operating Officer and President and General Manager of Emissions, Thermal and Turbo Systems, Morse Systems and TorqTransfer Systems, the precursor to PowerDrive Systems. Prior to joining BorgWarner, Mr. Fadool worked at Continental Automotive Systems as Vice President for North American Electronic Operations and at Ford Motor Company.

Exit from Charging Business

In May 2025, under new CEO Fadool, BorgWarner made a significant strategic pivot:

The Company announced a number of portfolio actions that are intended to drive focus and enhance its future long-term profitable growth including: Exiting its Charging business during the second quarter of 2025. This action is expected to create a more focused portfolio and eliminate approximately...

"We made the difficult decision to exit our charging business. Ultimately we did not see this business creating shareholder value within our planning horizon," he told investors during his first earnings call since taking over as CEO from Frédéric Lissalde in February.

"Unfortunately the charging market is not growing as anticipated in both North America and Europe," Fadool told investors. "The market also remains highly competitive and disaggregated."

2025 Financial Performance

BorgWarner Inc. today reported third quarter results and increased 2025 guidance. BorgWarner's U.S. GAAP net sales increased approximately 4.1%, while organic sales increased approximately 2.1%, year-over-year compared with third quarter 2024. The Company achieved a U.S. GAAP operating margin of 6.9% during the third quarter of 2025, which equated to an adjusted operating margin of 10.7% or an increase of 60 basis points compared with third quarter 2024. The Company's solid conversion on higher sales and focus on cost controls allowed it to deliver strong performance despite a 60 basis point net headwind from tariffs.

The revised outlook projects adjusted operating margin between 10.3% and 10.5%, up from the previous guidance of 10.1% to 10.3%. Similarly, the adjusted diluted EPS forecast has been increased to $4.60-$4.75, compared to the earlier projection of $4.45-$4.65. Free cash flow guidance has been significantly raised to $850-$950 million from the previous $700-$800 million range.

XI. Bull and Bear Cases: Strategic Analysis

Bull Case: The Propulsion Agnostic Supplier

BorgWarner's strategic positioning offers compelling logic. The company maintains what it calls a "propulsion agnostic" portfolio—meaning it can profit whether the future belongs to combustion, hybrid, or battery electric vehicles.

The content per vehicle opportunity in EVs remains the most powerful argument for the bull case. BorgWarner stands to benefit from the industry's electrification trend, with potential content per vehicle rising from $548 for combustion vehicles to $2,569 for battery electric vehicles. This represents a nearly 5x increase in potential revenue per vehicle, providing a clear growth path as EV adoption increases.

The Company's outgrowth of approximately 3.7% was primarily driven by strong light vehicle eProduct sales, which increased 47% year over year.

Porter's Five Forces Analysis

Supplier Power: Moderate. BorgWarner sources from diverse suppliers globally, though specialized semiconductor and rare earth dependencies create pockets of supplier leverage.

Buyer Power: High. The concentration of the auto industry—where a handful of OEMs drive most global production—gives automakers significant negotiating leverage. BorgWarner mitigates this through technological leadership and switching costs.

Threat of New Entrants: Low to Moderate. Capital requirements and engineering expertise create barriers, but Chinese suppliers increasingly threaten traditional Western dominance.

Threat of Substitutes: High and Existential. This is the fundamental challenge: BorgWarner's traditional products (turbochargers, transmissions) face technological obsolescence as EVs proliferate.

Competitive Rivalry: Intense. BorgWarner's top 17 competitors are Bosch, DENSO, Hitachi, Magna, Valeo, Vitesco Technologies, Schaeffler, Continental, TRAD North America, Rheinmetall Automotive, Eberspaecher Group, Tsubakimoto Chain, USUI, JTEKT , Safran, GE and 3M.

Hamilton Helmer's 7 Powers Framework

Scale Economies: BorgWarner benefits from significant manufacturing scale, particularly in turbochargers and transfer cases where it holds leading global positions.

Network Effects: Limited. This is not a platform business.

Counter-Positioning: The "Charging Forward" strategy attempts to counter-position against legacy competitors hesitant to cannibalize combustion businesses.

Switching Costs: Significant. Automotive components are designed into vehicle platforms years before production. Once specified, switching costs are substantial.

Branding: The Borg-Warner Trophy provides unique brand equity among automotive enthusiasts, but B2B supplier relationships are ultimately won on performance and price.

Cornered Resource: Limited. While BorgWarner holds significant intellectual property, competitors can generally develop alternative solutions.

Process Power: Strong. Decades of manufacturing excellence, particularly in precision mechanical components, create process advantages difficult to replicate quickly.

Bear Case: Caught Between Two Worlds

The bear case centers on execution risk during an unprecedented industry transition. BorgWarner must simultaneously:

- Extract maximum cash flow from declining combustion businesses

- Invest heavily in unproven EV technologies

- Compete against both traditional competitors and Chinese insurgents

- Navigate regulatory uncertainty that could accelerate or decelerate the EV transition

Non-comparable items include $646 million of goodwill and fixed asset impairment charges recorded during the fourth quarter in our PowerDrive Systems and Battery and Charging Systems business units.

The $646 million impairment charge recorded in Q4 2024 illustrates the risks inherent in the EV transition. Investments made based on aggressive EV adoption forecasts may prove premature if adoption slows.

The exit from the charging business under new CEO Fadool suggests that the original "Charging Forward" strategy may have been too aggressive in some areas. As a result, management felt it would not be able to scale the business in a timely enough fashion that would enable that business to reach its minimum 15% target for ROIC.

XII. Key Metrics for Investors

Critical KPIs to Monitor

1. eProduct Sales Growth Rate

This is the single most important metric for tracking BorgWarner's transition. The company has demonstrated consistent growth:

- 2022: $1.5 billion

- 2023: $2.0 billion

- 2024: $2.3 billion

The target remains ambitious: achieving more than $10 billion in eProduct revenue by 2027. Quarter-by-quarter progress against this target reveals whether the electrification bet is paying off.

2. Market Outgrowth

BorgWarner consistently emphasizes its ability to "outgrow" underlying vehicle production volumes. BorgWarner's U.S. GAAP net sales increased approximately 4.1%, while organic sales increased approximately 2.1%, year-over-year compared with third quarter 2024.

Market outgrowth measures whether BorgWarner is winning share through new platform wins and content expansion. A company that consistently outgrows its end markets by 100-300 basis points is executing well; sustained underperformance signals competitive weakness.

3. Adjusted Operating Margin

Excluding the impact of non-comparable items and the add back of intangible asset amortization expense, adjusted operating margin is expected to be in the range of 10.3% to 10.5%. The increase compared to the Company's previous adjusted operating margin range of 10.1% to 10.3% is due to strong year-to-date results and on-going cost performance measures.

Margin performance reveals whether BorgWarner can grow its EV business profitably. The company has targeted approximately 7% adjusted operating margin on its eProduct portfolio—below the foundational business margins but still healthy. Tracking segment margins shows whether EV investments are creating or destroying value.

XIII. Conclusion: The Next Chapter

BorgWarner's nearly century-long journey encapsulates the broader American industrial story: innovation, consolidation, near-death through financial engineering, resurrection through focus, and now—perhaps the most challenging transformation of all—the pivot from combustion to electrification.

Since February 2025, Joseph F. Fadool has been CEO of BorgWarner Inc.

Under Fadool's leadership, the company appears to be taking a more disciplined approach to the EV transition. The exit from the charging business, while representing a retreat from the most aggressive version of "Charging Forward," demonstrates willingness to reallocate capital from underperforming investments.

The fundamental investment case rests on whether BorgWarner can successfully navigate what may be the automotive industry's most significant technological transition since the Model T. The company has survived hostile takeovers, LBOs, multiple spin-offs, and repeated industry downturns. It has reinvented itself from conglomerate to focused supplier, from purely domestic to globally diversified, from mechanical systems to electronics.

Whether it can make the leap from internal combustion to electrification—while maintaining profitability and market position—remains the defining question for the company's next century.

That sterling silver trophy at Indianapolis Motor Speedway continues to grow, face by face, year by year. Somewhere in Auburn Hills, Michigan, BorgWarner's engineers are working to ensure that the company's story continues to evolve just as impressively—even if the vehicles that carry its components no longer need turbochargers to cross the finish line first.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube