Carpenter Technology: The 136-Year-Old Specialty Metals Pioneer Powering Modern Aerospace

I. Introduction & Episode Roadmap

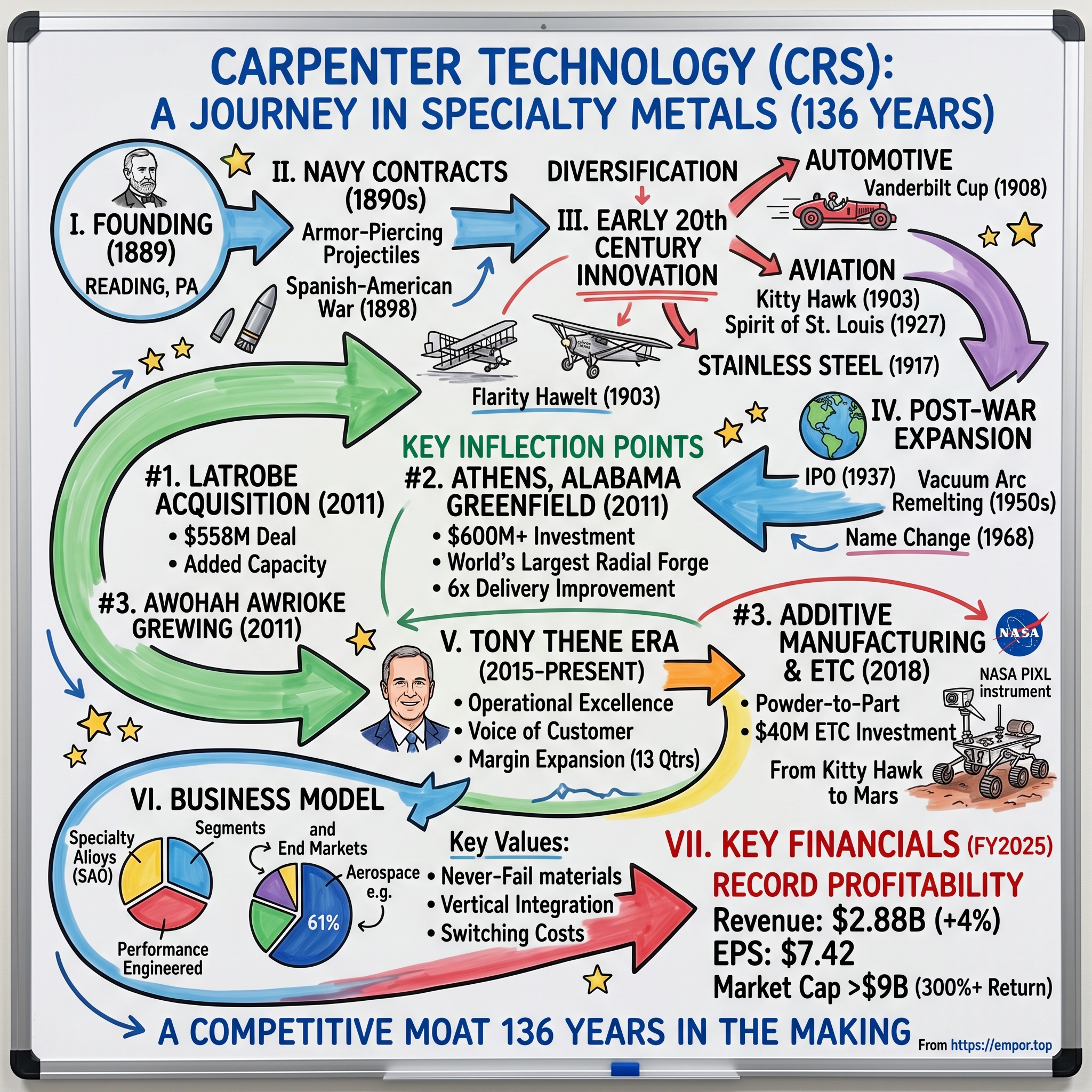

In December 1903, on the wind-swept dunes of Kitty Hawk, North Carolina, Orville Wright lay prone on the lower wing of a fragile wooden contraption. The 12-horsepower engine sputtered to life, and for 12 seconds that changed human history, the Wright Flyer achieved powered flight. What almost nobody remembers: the engine that made it all possible contained specialty steels forged by a small Pennsylvania company called Carpenter Steel.

Fast forward 120 years, and Carpenter Technology's materials are still at the heart of aerospace innovation—only now they're traveling 292.5 million miles to Mars, not 120 feet across the sand. The titanium parts that Carpenter Additive 3D-printed for the PIXL instrument on NASA's Perseverance rover have three or four times less mass than if they'd been produced conventionally. As PIXL's lead mechanical engineer Michael Schein put it: "In a very real sense, 3D printing made this instrument possible."

Carpenter Technology Corporation engages in the manufacture, fabrication, and distribution of specialty metals in the United States, Europe, the Asia Pacific, Mexico, Canada, and internationally. It operates in two segments: Specialty Alloys Operations and Performance Engineered Products.

The numbers tell a story of transformation. Over the past two years, Carpenter has generated total return to shareholders over 300% and increased market capitalization from $2.2 billion to over $9 billion. The latest closing stock price for Carpenter Technology as of November 20, 2025 is $305.39. The all-time high Carpenter Technology stock closing price was $332.15 on November 17, 2025.

How does a 136-year-old Pennsylvania steelmaker become irreplaceable to the aerospace industry? The answer lies in a combination of deep metallurgical expertise accumulated over more than a century, strategic capital allocation, and a relentless focus on what the industry calls "never-fail" materials—specialty alloys that cannot be allowed to fail because the consequences are catastrophic.

This is the story of Carpenter Technology: from Civil War veteran James Henry Carpenter's armor-piercing projectiles to Mars rovers, from Reading foundries to the world's largest radial forge in Alabama, and from a traditional metals company to a cutting-edge additive manufacturing powerhouse.

II. Founding Story & The Carpenter Legacy (1889–1900s)

The Boy Sailor Who Built an Empire

James Henry Carpenter (September 14, 1846 – March 6, 1898) was a 19th-century American engineer and industrialist who founded the Carpenter Steel Company. Born in Brooklyn, New York, he joined the Union Navy as a "cabin boy" at age 15 during the American Civil War, during which he was wounded in action. He was promoted to master's mate in the United States Navy for meritorious conduct and was appointed to the United States Naval Academy at age 16.

Picture a 15-year-old boy in May 1861, as the first shots of the Civil War still echoed across the nation, enlisting to serve on the USS Santee, a 44-gun wooden frigate. At the end of December 1861, Santee captured the CSN schooner Garonne. Shortly after, Carpenter was made acting master's mate of Santee. On February 11, 1862, Carpenter was appointed a master's mate and ordered to the flagship, USS Niagara. After evaluation he was appointed as master's mate to the steamer USS R. R. Cuyler and took part in the capture of several enemy vessels.

This early exposure to naval warfare and shipbuilding would shape Carpenter's entire career. He resigned from the US Navy in 1865, aged 19, and studied engineering in New Jersey. On June 7, 1889, he founded the Carpenter Steel Company of Reading, Pennsylvania, becoming its general manager.

Reading, Pennsylvania: The Birthplace of Specialty Steel

Why Reading? A New Yorker, Carpenter was encouraged to found a steel-making enterprise in Reading, Pennsylvania, by a visionary city councilman who, realizing that the region's bustling iron industry would naturally support such a venture, foresaw a boon to the city's economy.

The region offered everything a steel entrepreneur needed: abundant coal, established iron foundries, skilled workers, and river access for shipping. Incorporated in New Jersey on June 7, 1889, Carpenter Steel Company leased a rail-making plant in Reading and soon received its first order for 3,000 tons of steel. Within five months, the fledgling company had outgrown the rail-making plant and acquired a facility known as Union Foundry, which over 100 years later still functioned as company headquarters and a specialty steel mill.

The Navy Contract That Changed Everything

Carpenter's transformation from a generic steelmaker to a specialty metals pioneer began with a single contract. Carpenter's branching into specialty steel operations began with a May 1890 contract with the U.S. Secretary of the Navy. Having found Carpenter's tool steels to be of superior quality, the Navy was betting, correctly as it turned out, that the company could develop armor-piercing projectiles. The fulfillment of the Navy contract was enabled by a patent granted to James Carpenter for an "air-hardening steel" manufacturing process.

In November 1896, the United States Secretary of the Navy referred to the company's armor-piercing projectiles as "the first made that would pierce improved armor plate." This wasn't marketing hyperbole—it was Congressional testimony that would make Carpenter's reputation.

In the Spanish-American War of 1898, the routing of the Spanish fleet at Manila Bay was credited in part to Carpenter projectiles. Unfortunately, the preeminence Carpenter achieved through its wartime armaments proved to be a curse when the Spanish-American War, and the contracts it fostered, ended.

Tragedy and Resurrection

Complicating the decline in business was the death, in March 1898, of founder James Carpenter. The founder had died just as his company's military contracts evaporated. The enterprise encountered early financial challenges, culminating in receivership by 1903, followed by reorganization under Robert E. Jennings, who assumed the presidency in 1904 and steered the company toward stability through diversification into specialty steels.

However, the court-appointed receiver, Robert E. Jennings, was a former vice-president of a rival steel company and would soon oversee a dramatic resurgence at Carpenter. Elected president of a reorganized Carpenter Steel Company the following year, Jennings's expertise was in marketing; for the remainder of the decade he presided over innovations resulting in a variety of steel grades broad enough for almost every extant tooling application.

The near-death experience of receivership taught Carpenter a lesson that would define its strategy for the next century: never become dependent on a single customer or market. Diversification into specialty steels—products where metallurgical expertise and quality mattered more than volume—became the company's north star.

III. The Innovation Engine: Early 20th Century (1900–1945)

Powering the Automotive Revolution

With Jennings at the helm, Carpenter pivoted from military contracts to the emerging automobile industry. In 1905, the company developed a prime grade chrome-nickel steel; by 1908 it had created ten other steels that were used to make automobile chassis. Most of the "runabout" vehicles of the day ran on Carpenter steel, and "Old 16," the racer that won the Vanderbilt Cup in 1908, comprised front and rear axles, crankshaft, gears, and other parts fabricated from Carpenter steel.

The Vanderbilt Cup was the premier automobile race in America—the Indianapolis 500 of its era. Having your steel power the winning car was the equivalent of a semiconductor company's chips being in both the winning Formula 1 car and the leading smartphone. It demonstrated both performance excellence and reliability.

Affinity with automobile manufacturers gave rise to a hallmark of Carpenter's distribution system: maintaining service centers where its customers were based. The beginnings of its modern regional service center system began with the opening of branch warehouses in Cleveland and Hartford, then the centers of automobile production, in 1907 and 1909.

The Birth of Stainless Steel and Aviation

In 1917, the company manufactured its first high-strength, chemical-resistant stainless steel, which was immediately used in airplane engine components, cutlery, and spark plugs. Stainless steel was revolutionary—a material that could resist corrosion while maintaining strength, opening applications from aircraft to kitchens.

From Kitty Hawk to Paris: The Spirit of St. Louis

Another historical milestone that demonstrated Carpenter's preeminence was Charles Lindbergh's pioneering nonstop flight from New York to Paris in May 1927. The gears, shafts, and fasteners of the engine of the "Spirit of St. Louis," Lindbergh's legendary plane, were all made from Carpenter steel.

An identical engine had powered Richard Byrd's flight to the North Pole the previous year. Even the Wright Brothers' maiden flight in 1903 had been achieved with Carpenter steel-based engine components. This wasn't coincidence—it was the result of Carpenter's emerging reputation as the go-to supplier when failure was not an option.

Product Innovation Never Stopped

In 1928, the company introduced the first free machining steel. It was 0.15% sulfur to make it easier to machine. The introduction of stainless steel strip in the mid-1920s reestablished Carpenter as an important supplier to the automobile industry.

Going Public Amid Depression and War

In June 1937, the company conducted an initial public offering, transitioning from private ownership to a publicly traded entity listed on major exchanges, which broadened its capital access and shareholder composition. This IPO represented a pivotal shift, aligning the firm with public market dynamics amid the Great Depression's aftermath and impending wartime demands.

During World War II, the company's stainless steel was used in engine parts, steel fasteners, and cockpit instruments for fighter planes and bombers; components of Sherman tanks and submarines; radio masts for PT boats and radio equipment for battle fronts; and medical supplies such as hypodermic needles and surgical implements.

The breadth of wartime applications—from combat vehicles to medical supplies—demonstrated Carpenter's diversification strategy in action. When the war ended, the company wouldn't face the same boom-and-bust cycle that had nearly destroyed it in 1898.

IV. Post-War Expansion & Corporate Evolution (1945–1990s)

The Space Age Demands Purity

After the war, Carpenter returned to stable, profitable operations. The 1950s brought significant technological advances in melting, particularly with the process of vacuum arc remelting in a consumable-electrode furnace, which allowed unprecedented high purity in steel alloys—and none too soon, since applications in the embryonic aerospace field required immaculate degrees of purity.

Jet engines and rockets operated at temperatures and stresses that would have been unthinkable to James Henry Carpenter. During the same decade, Carpenter introduced "Stainless 20," an alloy which by virtue of rare earth element additives could withstand harsh, corrosive chemicals.

Name Change Signals Strategic Shift

In 1968, the company changed its name to Carpenter Technology Corporation to reflect its research and development initiatives. The word "Technology" was deliberate—signaling that this was no longer merely a steel company, but an advanced materials enterprise.

Building Through Acquisition

The company began assembling capabilities through strategic acquisitions:

In May 1983, the company acquired Eagle Precision Metals of Fryeburg, Maine, a precision drilling facility that produced high quality hollow steel bars. In 1984, the company acquired a wire-finishing plant, capable of redrawing steel wire to extremely fine sizes from AMAX Specialty Metals of Orangeburg, South Carolina.

The 1990s brought larger, more strategic deals:

In January 1997, Carpenter acquired Dynamet, a titanium alloy producer based in Washington, Pennsylvania, for $161 million. In September 1997, the company acquired Talley Industries for $185 million.

The Dynamet acquisition was particularly significant. Titanium alloys would become increasingly critical for aerospace applications—lighter than steel, strong, and corrosion-resistant. In October 1998, the company announced a $113.6 million investment to expand its Reading, Pennsylvania melt shop.

These moves positioned Carpenter for the aerospace supercycle that was still decades away. Management was building capabilities that customers didn't fully need yet—a bet that would pay off spectacularly in the 2020s.

V. Key Inflection Point #1: The Latrobe Acquisition (2011)

Combining Two Century-Old Legacies

By 2011, Carpenter faced a strategic challenge: strong customer demand for premium alloys was outstripping its production capacity. The solution came in the form of another specialty metals company with roots stretching back to 1913.

Jones Day advised Latrobe Specialty Metals, Inc. in its acquisition by Carpenter Technology Corporation for $558 million. In the transaction, 8.1 million shares of Carpenter stock representing a current equity value of approximately $388 million will be issued to the current owners, including Hicks Equity Partners and The Watermill Group. Carpenter will also use up to $170 million in cash at closing to eliminate Latrobe debt and reimburse certain transaction costs.

Acquired by Hicks Equity Partners and The Watermill Group in December 2006, Latrobe manufactures and distributes high-performance materials for aerospace, defense, energy, and other significant applications with manufacturing operations in Pennsylvania, Ohio, Texas, and the United Kingdom and seven distribution centers located throughout the United States. Annual revenues and EBITDA for the twelve months ending March 31, 2011 were $379 million and $58 million respectively.

Strategic Rationale

William A. Wulfsohn, then President and CEO of Carpenter, articulated the strategic logic: "Our strategy is to grow through a combination of organic growth initiatives and acquisitions - with a focus on markets that value the technical sophistication of our products. The Latrobe acquisition will provide needed capacity to meet strong customer demand for our premium products, improves our position in attractive segments like aerospace and energy."

The company expected synergies to be substantial: "By combining the two companies we will improve product mix, lower cost, and reduce required capital investments for future growth. We expect the acquisition to be accretive in year one, even including the one-time costs associated with the merger, and highly accretive in future years. Annual net synergies are anticipated to be in excess of $25 million."

Regulatory Scrutiny and Resolution

The acquisition drew regulatory attention from the FTC. The FTC required specialty metals manufacturer Carpenter Technology Corporation to sell assets involved in producing two metal alloys used in the aerospace industry, under a settlement resolving charges that Carpenter's proposed $410 million acquisition of Latrobe Specialty Metals, Inc. would harm competition in the U.S. markets for these alloys.

In February 2012, Carpenter Technology Corporation announced that they had completed the acquisition of Latrobe Specialty Metals, Inc. following approval by the U.S. Federal Trade Commission (FTC). Former owners of Latrobe, including Hicks Equity Partners and The Watermill Group, received 8.1 million shares of Carpenter stock as a part of the transaction. Pursuant to the terms of the merger agreement, Carpenter also paid approximately $168 million in cash at closing to pay off Latrobe debt and reimburse certain transaction costs.

The Latrobe acquisition gave Carpenter critical manufacturing capacity just as aerospace demand was beginning its long ascent. But management was already planning an even bolder move.

VI. Key Inflection Point #2: The Athens, Alabama Greenfield Investment (2011–2019)

The Bold Bet

In 2011, the same year Carpenter announced the Latrobe acquisition, the company made an even more audacious decision: building its first greenfield manufacturing facility outside Pennsylvania in 122 years of history.

Carpenter Technology undertook a huge initiative to build a new 200-acre facility in Athens, Alabama, to increase production capacity and subsequently provide faster customer response time. To achieve their goals, they collaborated with Turner Construction and Barge Design Solutions on a fast-track design-build initiative for the Athens Operations Program, a $500+ million investment focused on specialty alloy steel products for high-performance products such as jet engines, turbines, and medical devices.

Why Alabama?

"This was a very big step for Carpenter, emotionally, just looking outside of our roots in Reading," says Dave Strobel, senior vice president of global operations. "We have a big and capable facility up here, but with the growth we saw in key markets of aerospace and energy and others, we had to figure out how do we grow and where do we grow."

Tax incentives, including $95 million over 20 years, were a factor in the whole equation, but Strobel says it was not his main focus. "My primary consideration was not tax incentives, but where I can put a plant and grow it over time and feel good that we can pull in the right work force to run it."

Limestone County's proximity to Huntsville's aerospace cluster was critical. Huntsville—home to NASA's Marshall Space Flight Center and a growing ecosystem of aerospace contractors—meant customers were nearby. "It was also the support of the community down there," Strobel says. "Spending time at the robotics center and the local tech schools really and truly sold us on Alabama."

World-Class Capabilities

The project's initial phase centered on developing essential site infrastructure and the installation of the world's largest radial forge. Phase I included the installation of the world's largest radial forge and the site development and infrastructure. Our team designed a total of 10 buildings ranging in size from 20,000 to 500,000 square feet.

The largest radial press in the world is at the heart of the plant's operations. It is responsible for pressing, shaping and changing the network of steel at temperatures hotter than 2,000 degrees Fahrenheit. Getting the massive press to the plant was a challenge. It was moved to the plant in three pieces, each weighing 160 tons. It took eight hours to move each part from the marina in Decatur about five miles to the plant site.

Operational Excellence by Design

Plant General Manager Ernie Jones says the plant was designed with modern technology and optimum product flow to meet customer requirements for reduced lead times. Once it's operating at full capacity, the Athens Operations will be capable of producing approximately 27,000 tons per year. Right now, the average delivery time is four to six weeks after an order is placed. The same order could take up to 30 weeks at another plant.

Think about that: a six-fold improvement in delivery times. In aerospace, where production schedules are measured in years and delays cascade through supply chains, this capability was transformational.

Governor Robert Bentley joined Carpenter Technology officials on January 27, 2014 to mark the startup of the company's $518 million Limestone County plant. The 500,000-square-foot plant will remelt, forge, finish and test steel alloys. The plant plans to produce 8,000 to 10,000 tons of material in the facility through 2014, before ramping up to its 27,000-ton-per-year capacity.

The company has invested over $600 million in its Alabama operations.

VII. Key Inflection Point #3: The Tony Thene Era & Strategic Transformation (2015–Present)

A Finance Mind at the Helm

On June 2, 2015, Carpenter Technology Corporation announced that its Board of Directors has appointed Tony R. Thene as Carpenter's President, Chief Executive Officer (CEO) and member of the Board of Directors, effective July 1, 2015.

Tony R. Thene was appointed President & CEO of Carpenter Technology Corporation in July 2015, and is also a member of the company's Board of Directors. Before being named top executive of Carpenter's $2.2 billion global manufacturing operation, which serves the aerospace, energy, transportation, medical, and industrial markets, Thene joined the company in January 2013 as Senior Vice President & Chief Financial Officer.

Prior to joining Carpenter Technology, Thene served as Vice President of Alcoa, Inc. and the Chief Financial Officer of the Engineered Products and Solutions Group, and was a member of Alcoa's Executive Council. Previously, he served as Vice President, Controller and Chief Accounting Officer for Alcoa. Tony also held the positions of Director, Investor Relations; Chief Financial Officer for the Flat Rolled Products Group; Chief Financial Officer for Alcoa World Alumina and Chemicals; and manufacturing manager for the Alumina Chemicals business among other roles during his 23 years with Alcoa.

Thene brought an unusual combination: deep manufacturing experience from Alcoa (one of the world's largest aluminum producers), financial discipline from his CFO background, and investor relations sophistication from his time in that role.

The Four Pillars of Transformation

Thene has focused his efforts on providing customers with innovative material solutions for complex problems. His "voice of the customer" approach to business was the driving force behind the development of Carpenter's strategy, which focuses on Technology Development, Operational Excellence, Strategic Marketing, and Talent Engagement.

In addition, he embedded the "Carpenter Operating Model" into Carpenter's culture, emphasizing safety and lean manufacturing principles to drive distinctive product and process capabilities, and also developed the organization's values and vision, rounding out a clear direction and identity for the company.

The Results Speak for Themselves

Carpenter Technology's Board of Directors has unanimously elected Tony R. Thene, current President and Chief Executive Officer, to assume the additional duties of Chairman of the Board, effective October 7, 2025. For the last 10 years, Mr. Thene has served as President and Chief Executive Officer of Carpenter Technology and has been instrumental in leading significant growth. Under Mr. Thene's leadership, the Company has transformed into a leading preferred solutions provider in specialty materials serving key growth markets, with a focus on safety, quality, technology development and continuous improvement across operations.

In addition, Brian Malloy, currently Senior Vice President and Chief Operating Officer, has been promoted to President and Chief Operating Officer effective October 7, 2025. Mr. Malloy joined Carpenter Technology in August 2015 and has served in various Commercial and Operations leadership roles. Since joining Carpenter Technology, Mr. Malloy has leveraged his deep industry, marketing, operations and technical background to drive significant growth and improvement across areas including strategic marketing, technology innovation and operational excellence. He was most recently appointed Senior Vice President and Chief Operating Officer in December 2023.

The succession planning is notable—Malloy has been groomed for nearly a decade, ensuring continuity of the strategy that has driven Carpenter's transformation.

VIII. Key Inflection Point #4: Additive Manufacturing & The Emerging Technology Center (2018–2024)

The AM Bet

While many traditional metals companies viewed 3D printing as either a threat or a fad, Thene saw an opportunity.

Building upon Carpenter's reputation as an established and respected powdered metals supplier, Thene recently expanded Carpenter's additive manufacturing (AM) capabilities with the formation of Carpenter Additive, providing complete "powder-to-part" solutions and further establishing Carpenter as an influential industry leader.

Emerging Technology Center

On December 4, 2019, Carpenter Technology Corporation announced the grand opening of its Emerging Technology Center (ETC) in Athens, Alabama. Carpenter Technology's 500,000-square-foot ETC is North America's newest additive manufacturing (AM) facility containing true end-to-end capabilities. The ETC provides the capability to atomize a range of specialty alloys into metal powder and manufacture the powder into finished parts using AM technology (3D metal printing). Its downstream equipment includes the latest, state-of-the-art quick cooling Hot Isostatic Press (HIP) system in the United States, as well as vacuum heat treating to optimize the material properties of high-value specialty alloy components. Parts manufactured in the ETC can then be qualified for use in a range of cross-industry applications, from aerospace and transportation to oil and gas and energy.

"We have chosen to further invest in North Alabama and continue to grow and develop here because it offers three important advantages — a high-quality, tech-oriented workforce, a clear connection with the aerospace industry, and a close working partnership with state and local government officials," Carpenter Technology President and CEO Tony Thene said. "The state of Alabama continues to be an ideal partner for us." Carpenter Technology has invested approximately $40 million to date in the ETC and is expected to create approximately 60 jobs over the next five years.

NASA Partnership: From Kitty Hawk to Mars

The most dramatic demonstration of Carpenter's additive manufacturing capabilities came from an unlikely source: NASA's Jet Propulsion Laboratory.

The Planetary Instrument for X-ray Lithochemistry (PIXL) carries a highly sensitive X-ray spectrometer for precision chemical analysis and experiments. NASA's Jet Propulsion Laboratory reached out to the experts at Carpenter Additive to 3D print the housing for this equipment for the journey. "Touching down on Mars can best be described as a highly engineered, controlled crash landing, and these parts have to withstand that force and then carry out precision experiments" stated Carpenter Additive's Director of Additive Technology and project lead.

PIXL shares space with other tools in the 88-pound rotating turret at the end of the rover's 7-foot-long robotic arm. To make the instrument as light as possible, the JPL team designed PIXL's two-piece titanium shell, a mounting frame, and two support struts that secure the shell to the end of the arm to be hollow and extremely thin. In fact, the parts, which were 3D printed by a vendor called Carpenter Additive, have three or four times less mass than if they'd been produced conventionally. "In a very real sense, 3D printing made this instrument possible," said Michael Schein, PIXL's lead mechanical engineer at JPL. "These techniques allowed us to achieve a low mass and high-precision pointing that could not be made with conventional fabrication."

From the Wright Brothers' engine to the Mars Perseverance rover—Carpenter's materials have been at humanity's frontier of exploration for over 120 years.

IX. The Business Model Deep-Dive

Two Operating Segments

Carpenter Technology Corporation operates in two segments: Specialty Alloys Operations (SAO) and Performance Engineered Products (PEP). The SAO segment comprises its premium alloy and stainless-steel manufacturing operations. This includes operations performed at mills primarily in Reading and Latrobe, Pennsylvania and surrounding areas, as well as South Carolina and Alabama. The PEP segment comprises its differentiated operations. This segment includes the Dynamet titanium business, the Carpenter Additive business and the Latrobe and Mexico distribution businesses. It provides specialty alloy-based materials and process solutions for critical applications in the aerospace, defense, medical, transportation, energy, industrial and consumer markets.

Revenue Mix and End Markets

In fiscal year 2018, the company's revenues were derived from the aerospace and defense industry (55%), the industrial and consumer industry (17%), the medical industry (8%), the transportation industry (7%), the energy industry (7%), and the distribution industry (6%).

The upgrade reflects expectations that Carpenter's operating performance, free cash flow, and credit metrics will continue to strengthen over the next 12 to 18 months, supported by robust demand in the aerospace and defense sector, which accounted for about 61% of the company's net sales.

The shift from 55% aerospace in 2018 to over 61% in 2025 reflects both market dynamics (aerospace supercycle) and Carpenter's strategic focus on its highest-value applications.

The "Never-Fail" Positioning

The company's products are used in landing gear, shaft collars, safety wires, electricity generation products, intervertebral disc arthroplasty, and engine valves and weldings.

Consider what these applications have in common: catastrophic consequences for failure. A landing gear that cracks on landing. An artificial spine component that breaks inside a patient's body. A jet engine valve that fails at 40,000 feet. These are applications where price is secondary to absolute reliability—the definition of "never-fail" materials.

Vertical Integration Advantage

The company maintains in-house, start-to-finish production that gives Carpenter a secure environment and precise control over the chemistry and performance of alloys. This vertical integration spans from initial melting through forming, finishing, and testing.

Global Footprint

Carpenter makes and distributes specialty metals, including billet, bar, rod, wire, strip and metal powders. The company has more than 200 patents in melting technology, powder metallurgy, stainless steels, high-strength alloys, corrosion-resistant alloys and other specialty metals.

Carpenter's main manufacturing plants are in Reading, Orwigsburg, Washington, Bridgeville, Latrobe and Franklin; Hartsville and Orangeburg, S.C.; Clearwater, Fla.; Elyria and Wauseon, Ohio; Woonsocket, R.I.; Tyler, Texas; and Limestone County, Ala. (a 400,000 square-foot facility that opened in 2014 and makes products for aerospace, defense and energy industries).

X. Current Financial Performance & Recent Results

Record-Breaking Performance

In 2025, Carpenter Technology's revenue was $2.88 billion, an increase of 4.25% compared to the previous year's $2.76 billion. Earnings were $375.80 million, an increase of 101.83%.

Delivered Record Quarterly Operating Income in Fourth Quarter; Generated Record Adjusted Free Cash Flow in Fourth Quarter; Completed Most Profitable Year in Company History; Fiscal Year 2026 Outlook 26% to 33% Higher Than Record Fiscal Year 2025.

For fiscal year 2025: Net sales were $2,877.1 million. Operating income was $521.8 million. Adjusted operating income excluding special items was $525.4 million. Net income was $376.0 million. Earnings per diluted share was $7.42.

Carpenter's adjusted EBITDA reached a record high of $683 million in fiscal 2025 (ended June 2025), compared to $508 million in fiscal 2024.

Margin Expansion Story

Carpenter Technology reported record financial results for Q3 FY2025, with operating income of $137.8 million and earnings per diluted share of $1.88. The company's Specialty Alloys Operations (SAO) segment achieved an adjusted operating margin of 29.1%, up from 21.4% year-over-year, marking thirteen consecutive quarters of margin growth. Net sales reached $727.0 million, a 6% increase from Q3 FY2024, despite a 7% decrease in shipment volume.

Thirteen consecutive quarters of margin improvement is remarkable. The company has systematically shifted its product mix toward higher-value, more complex alloys while implementing operational improvements.

Stock Performance and Market Recognition

Carpenter Technology Corporation (CRS) up 213% since 2024 thanks to Big Money outlier buys.

According to 5 analysts, the average rating for CRS stock is "Strong Buy." The 12-month stock price target is $374.6, which is an increase of 24.08% from the latest price.

Expansion Investment

Carpenter Technology announced a $400 million investment in a brownfield expansion of its facilities in Athens, Alabama. Additional remelt capacity will also be added in Athens. The added capacity should bring additional work to CarTech's complementary finishing assets across its system, primarily in Reading. The company will be able to produce a range of specialized alloys for use in high value markets. According to Malloy, Carpenter is targeting early fiscal year 2028 for commissioning.

The project is expected to accelerate earnings growth but will not materially impact the current supply/demand imbalance. It will be funded through internal cash generation and provide a return on capital over 20%.

Capital Returns

Carpenter will return cash to shareholders through the $400 million stock buy-back program.

In July 2024, Carpenter Technology's Board of Directors authorized a share repurchase program up to $400.0 million of its outstanding common stock.

XI. Competitive Analysis & Porter's Five Forces

Key Competitors

Carpenter Technology operates in a competitive landscape with several key players in the specialty metals and alloys industry. Some of the primary competitors include: Ametek is a global manufacturer of electronic instruments and electromechanical devices. The company has a strong presence in the aerospace and defense sectors. ATI specializes in the production of specialty materials and advanced manufacturing capabilities. The company competes directly with Carpenter Technology in high-performance alloys and is known for its extensive product range. Haynes International focuses on high-performance alloys, particularly for the aerospace and industrial markets. Its expertise in nickel and cobalt-based superalloys positions it as a formidable competitor. TimkenSteel produces high-quality steel products and specialty alloys.

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

Building a competitive specialty metals facility requires capital investment exceeding $500 million, as Carpenter's Athens facility demonstrated. Beyond capital, new entrants face:

- Decades-long customer qualification processes: Aerospace customers spend years qualifying new suppliers, conducting extensive testing before allowing materials into flight-critical applications.

- Deep metallurgical expertise: Carpenter's team includes nearly 200 metallurgists and application engineers. This expertise is accumulated over decades, not hired overnight.

- Regulatory certifications: ISO and AS9100 certifications require documented quality systems and track records.

The vertical integration that Carpenter maintains—controlling the entire process from melting to finishing—creates additional barriers, as it would require a new entrant to invest across the entire value chain.

2. Bargaining Power of Suppliers: MODERATE

Raw material inputs (nickel, cobalt, titanium) trade on commodity markets, limiting supplier pricing power. However, Carpenter's scale provides purchasing leverage. The company's expansion into powder production through additive manufacturing has further reduced dependency on external suppliers for certain inputs.

3. Bargaining Power of Buyers: MODERATE-TO-LOW

This is where Carpenter's "never-fail" positioning becomes a competitive moat. When your product goes into jet engine components, landing gear, or surgical implants, switching costs are enormous:

- Customers must re-qualify materials, a process taking months to years

- Supply chain disruption risk is unacceptable for mission-critical applications

- Premium pricing is accepted when the cost of failure is catastrophic

This robust backlog not only offers revenue visibility but also allows for more effective production planning and resource allocation. While current trends in the aerospace sector are favorable, Carpenter Technology's heavy reliance on this industry could pose risks in the event of a market downturn.

4. Threat of Substitutes: LOW

For extreme aerospace and defense applications, there are simply no viable substitutes for specialty alloys. Composites have made inroads in some aerospace structures, but engine hot sections, landing gear, and other high-stress applications still require advanced metal alloys. Furthermore, Carpenter is the innovator developing new materials, not threatened by them—witness the Mars rover components.

5. Competitive Rivalry: MODERATE

Direct competitors in the specialty metals market, such as Allegheny Technologies Incorporated (NYSE: ATI) or Haynes International (NASDAQ: HAYN), might experience some pressure from Carpenter's strong performance.

The specialty metals industry is concentrated among a handful of qualified suppliers. While competition exists, the market is not commoditized—customers value quality, technical support, and reliability over pure price competition.

Hamilton Helmer's 7 Powers Framework

Scale Economies: The Athens facility with the world's largest radial forge demonstrates scale advantages. Fixed costs are spread over larger volumes, and lead times of 4-6 weeks vs. 30 weeks at competitors create meaningful operational advantages.

Network Economics: Limited application in this B2B manufacturing context.

Counter-Positioning: Carpenter's early and aggressive investment in additive manufacturing represents counter-positioning—incumbents focused on traditional manufacturing may struggle to replicate Carpenter's "powder-to-part" capabilities.

Switching Costs: Extremely high. Re-qualifying aerospace materials is costly and time-consuming. This creates customer lock-in once relationships are established.

Branding: While Carpenter has strong brand recognition in its niche, branding power is less relevant in technical B2B markets than consumer goods.

Cornered Resource: Carpenter's metallurgical expertise accumulated over 136 years represents human capital that competitors cannot easily replicate. The institutional knowledge of how to develop and produce specialty alloys for specific applications is a cornered resource.

Process Power: The Carpenter Operating Model, lean manufacturing principles, and operational excellence initiatives represent process power that has driven margin expansion for 13 consecutive quarters.

Bull and Bear Case Analysis

Bull Case

The Aerospace Supercycle Has Years to Run: The worldwide commercial backlog reached a historic high of more than 17,000 aircraft in 2024, significantly higher than the 2010 to 2019 backlog of around 13,000 aircraft per year. Airlines need more planes than manufacturers can deliver. Engine makers need more materials than Carpenter can supply. This supply-demand imbalance supports pricing power and utilization.

Pricing Power in Action: Revenue grew 6% on 7% lower volume in Q3 FY2025. The company is selling higher-value products at better prices—the hallmark of a business with competitive advantages.

Capacity Expansion Timing: The $400 million Athens brownfield expansion will come online in FY2028, perfectly positioned for continued aerospace demand while generating returns above 20%.

Additive Manufacturing Optionality: The Emerging Technology Center positions Carpenter for the next wave of aerospace manufacturing—3D printed engine components that reduce weight and improve performance.

Strong Cash Generation: The company expects to generate approximately $1 billion in free cash flow from FY2025 through FY2027, reaching a 90% conversion rate excluding brownfield investment. This strong cash generation will support both long-term growth investments and shareholder returns.

Bear Case

Aerospace Concentration Risk: Carpenter Technology's heavy reliance on this industry could pose risks in the event of a market downturn. A potential slowdown in passenger travel growth or delays in aircraft production programs could negatively impact demand for CRS's products.

Customer Concentration: Dependence on major aerospace OEMs and engine manufacturers creates concentration risk.

Operational Execution Risk: Carpenter Technology has made significant progress in improving its operational efficiency, but maintaining these gains could prove challenging. Factors such as labor market pressures, raw material cost fluctuations, or supply chain disruptions could potentially erode the company's recent efficiency improvements.

Cyclicality: Specialty metals have historically been cyclical. While current conditions are favorable, aerospace downturns—triggered by recessions, safety incidents, or other factors—could impact demand.

Valuation: After a 300%+ return in two years, the stock is priced for continued execution and growth.

Key Performance Indicators to Watch

For long-term fundamental investors, three KPIs are critical for monitoring Carpenter Technology's ongoing performance:

1. Specialty Alloys Operations (SAO) Segment Operating Margin

The SAO segment represents the core of Carpenter's business and has delivered 13 consecutive quarters of margin improvement. Management has demonstrated an ability to shift product mix toward higher-value, more complex alloys while implementing operational improvements. Track whether this margin expansion continues or plateaus—it signals whether the pricing power and operational excellence are sustainable.

2. Order Backlog

Carpenter's substantial backlog provides visibility into future demand and allows production planning optimization. The backlog reflects customer commitments for premium materials and serves as a leading indicator of revenue and utilization. A declining backlog would signal softening demand well before it hits the income statement.

3. Aerospace & Defense Revenue Mix

With aerospace and defense now representing over 60% of sales, the concentration in this sector is a double-edged sword—providing exposure to a strong secular trend while creating vulnerability to aerospace-specific downturns. Monitor whether the company is diversifying into adjacent markets (medical, energy, power generation) or becoming more concentrated.

Conclusion: A Competitive Moat 136 Years in the Making

Carpenter Technology's story spans the entire history of American aerospace—from the Wright Brothers to Mars rovers. But the company's current position reflects more than historical legacy. Under Tony Thene's leadership, Carpenter has been systematically transformed:

- The Latrobe acquisition added critical capacity and capabilities

- The Athens greenfield investment created world-class manufacturing with industry-leading lead times

- The Emerging Technology Center positioned the company for additive manufacturing growth

- The Carpenter Operating Model drove operational excellence across the enterprise

"In the fourth quarter of fiscal year 2024 we exceeded our previous guidance, generating $125.2 million of adjusted operating income," said Tony R. Thene, President and CEO of Carpenter Technology. "The record fourth quarter performance completed the most profitable year in Carpenter Technology's history, achieving $354.1 million in adjusted operating income in fiscal year 2024."

Completed most profitable year on record, with $525.4 million of adjusted operating income in fiscal year 2025, up 48 percent over fiscal year 2024. Generated $287.5 million of adjusted free cash flow for fiscal year 2025. Increased Aerospace and Defense share of revenue to greater than 60 percent. "Looking over the long term, the same dynamics that are driving our current performance are expected to only get stronger into the future. The markets that we serve, in particular Aerospace and Defense, Medical and Power Generation, have a strong, multi-year outlook. Further, our customers rely on our diverse portfolio of advanced material solutions and world class capabilities."

The company that James Henry Carpenter founded in a Reading foundry in 1889 has become, in management's words, "an essential partner in the manufacture of mission critical never-fail products." That positioning—built on metallurgical expertise, manufacturing excellence, and deep customer relationships—represents a competitive moat that has taken 136 years to construct.

Whether providing steel for Lindbergh's transatlantic crossing, alloys for jet fighter landing gear, or 3D-printed titanium components for Mars exploration, Carpenter Technology has consistently positioned itself at the frontier of human achievement. The company's current financial performance suggests that positioning is being rewarded as never before.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube