RBC Bearings: The Precision Engineering Compounder

I. Introduction & Episode Roadmap

Picture a world without bearings. Every wheel would grind to a halt. Every jet engine would seize. Every submarine's torpedo tube would jam. These unassuming metal rings, often smaller than a coffee cup, are the connective tissue of the industrial world—and one company has spent over a century mastering the art of making them.

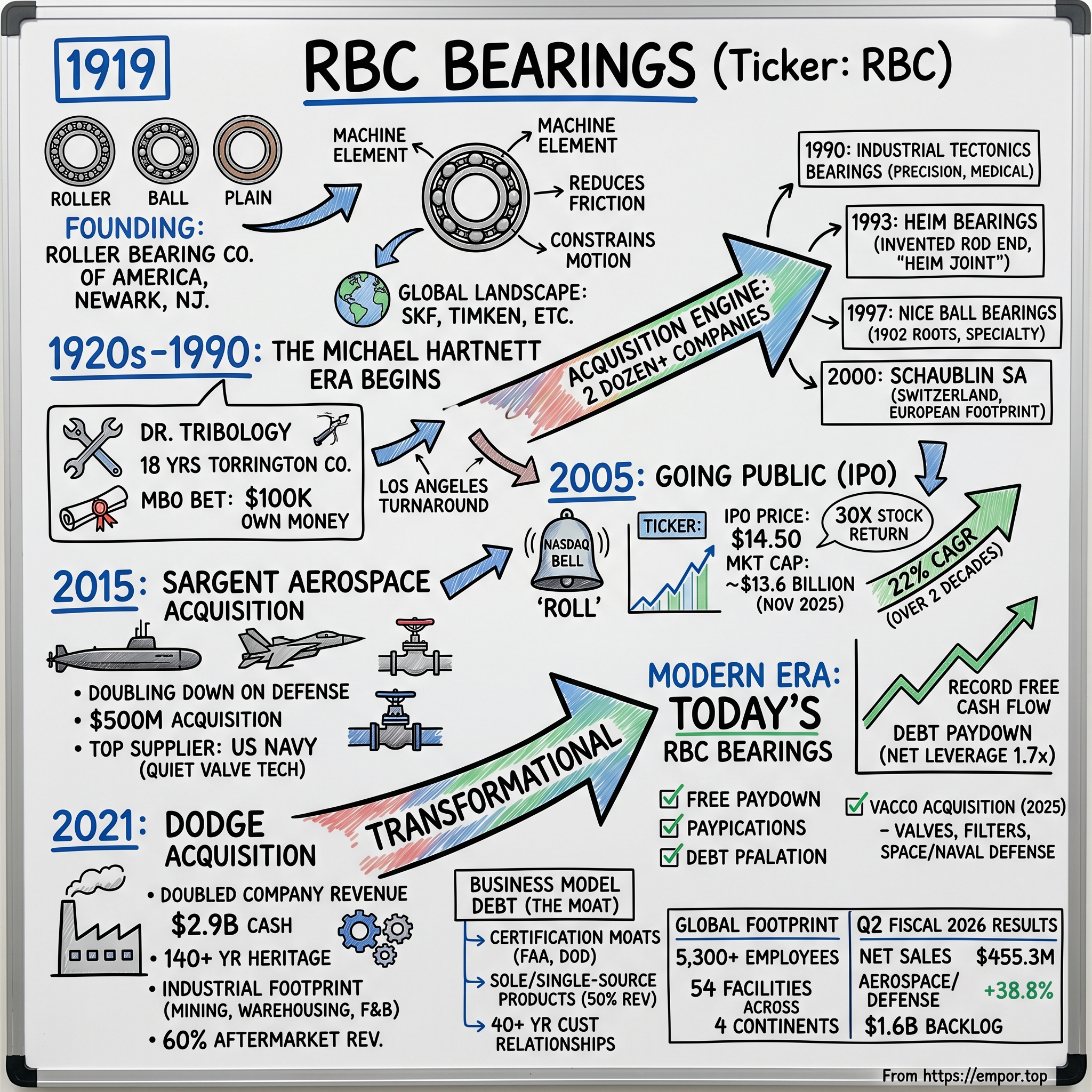

RBC Bearings Incorporated is an international manufacturer and marketer of highly engineered precision bearings and components. Founded in 1919, the Company is primarily focused on producing highly technical or regulated bearing products and components requiring sophisticated design, testing and manufacturing capabilities for the diversified industrial, aerospace and defense markets.

The numbers tell a stunning story of compounding value. When CEO Michael Hartnett joined RBC, revenue was $35 million. For the fiscal year ending March 2015, net revenue stood at $445.3 million. RBC went public in August 2005 at $14.50 per share. Today, in November 2025, the stock trades around $430 per share—a nearly 30x return from the IPO price over two decades. The company now commands a market capitalization approaching $13.6 billion.

This is the story of how a "boring" bearings company became anything but boring. It's a masterclass in several interlocking strategies: the power of an engineer-CEO who understands every nuance of his products; a relentless acquisition engine that has absorbed more than two dozen companies; an aerospace and defense moat built on FAA certifications, DOD approvals, and decades-long customer relationships; and the careful transition from private equity backing to public markets.

The company's trajectory accelerated dramatically in recent years. Net sales for the second quarter of fiscal 2026 were $455.3 million, an increase of 14.4% from $397.9 million in the second quarter of fiscal 2025. $24.7 of net sales this quarter came from VACCO, which was acquired on July 18, 2025. Net sales for the Industrial segment increased 0.7%, while net sales for the Aerospace/Defense segment increased 38.8%.

What we'll explore is not just a company history, but a blueprint for building durable competitive advantage in markets that most investors overlook. RBC Bearings proves that there's enormous value creation possible in the unglamorous corners of industrial manufacturing—if you have the right leader, the right strategy, and the patience to compound over decades.

II. Founding & Early History: The Roller Bearing Company of America (1919–1990)

Newark, New Jersey, 1919. The First World War had just ended, and American industry was awakening to a new era of mechanization. Against this backdrop of rapid industrialization, the Roller Bearing Company of America opened its doors, beginning a journey that would span more than a century.

RBC Bearings was founded in 1919 and is headquartered in Oxford, Connecticut. The Company is primarily focused on producing highly technical or regulated bearing products and components requiring sophisticated design, testing and manufacturing capabilities for the diversified industrial, aerospace and defense markets.

To understand RBC's story, one must first understand what bearings actually are—and why they matter so profoundly to modern civilization.

What Is a Bearing?

At its core, a bearing is a machine element that constrains relative motion and reduces friction between moving parts. Bearings are integral to the manufacture and operation of most machines, aircraft and mechanical systems, to reduce wear to moving parts, facilitate proper power transmission, reduce damage and energy loss caused by friction, and control pressure and flow.

Imagine trying to spin a wheel without a bearing—metal grinding against metal, generating heat, wearing down components, wasting energy. Bearings solve this fundamental engineering problem by providing a smooth interface between rotating and stationary parts. They come in several major categories: ball bearings (which use spherical rolling elements), roller bearings (using cylindrical or tapered rolling elements), and plain bearings (which rely on sliding surfaces, often self-lubricating).

The precision required in bearing manufacturing is extraordinary. Tolerances are measured in thousandths of an inch. Surface finishes must be mirror-smooth. Heat treatment processes must be precisely controlled to achieve the right metallurgical properties. This complexity creates natural barriers to entry and rewards companies with deep engineering expertise.

The Competitive Landscape

The global bearings industry has long been dominated by a handful of major players. Leading companies in the global bearings market include SKF, Schaeffler Group, NTN Corporation, NSK Ltd, THE TIMKEN COMPANY, and JTEKT Corporation. These companies dominate the market due to their large-scale production capabilities, strong R&D focus, global presence, and established relationships with OEMs and end-users.

SKF was founded in 1907 in Gothenburg, Sweden. Timken was founded in 1899 by Henry Timken, the inventor of the tapered roller bearing. The company revolutionized the bearing industry with the introduction of the self-aligning bearing in 1902. Timken is recognized as the world's largest manufacturer of tapered roller bearings.

Connecticut, where RBC is now headquartered, has deep roots in bearing manufacturing. The state was a heartland of the bearings industry in the mid-1900s with big players, such as TRW and SKF. "There were half a dozen plants in Torrington alone," Hartnett noted. "We have employees who worked for every one of those companies."

For most of its early decades, RBC remained a relatively small player in this competitive landscape, manufacturing specialized bearing products for industrial clients. The company changed hands multiple times, struggled through various economic cycles, and remained largely unknown outside its niche markets.

What would transform RBC from a struggling regional player into a publicly-traded industry leader was the arrival, in 1990, of a mechanical engineer with a doctorate in tribology—the science of friction—and a vision for what the company could become.

III. The Michael Hartnett Era Begins: The 1992 Management Buyout

The story of modern RBC Bearings is inseparable from the story of Dr. Michael J. Hartnett. Born on July 12, 1945, Hartnett's path to becoming a manufacturing entrepreneur was forged in the tool-and-die shops of Waterbury, Connecticut.

Growing up in Waterbury, Michael Hartnett apprenticed at his dad's tool-and-die factory, building a work ethic and a love of engineering that forms the DNA of his brand of entrepreneurship.

This wasn't the typical background of a Fortune 500 CEO. Hartnett didn't grow up in corporate boardrooms or elite business schools. He grew up learning to run lathes and mills, to feel the difference between a properly machined surface and a substandard one, to understand viscerally how metal behaves under stress. This hands-on foundation would prove invaluable.

The Torrington Years

After his formative years in his father's shop, Hartnett pursued engineering with singular focus. Dr. Hartnett holds an undergraduate degree from the University of New Haven, a Master's degree from Worcester Polytechnic Institute and a Doctoral degree in Applied Mechanics from the University of Connecticut.

His doctoral work focused on tribology—the study of friction, lubrication, and wear between surfaces in relative motion. This might sound arcane, but it's precisely the science that underlies bearing design. Understanding tribology at a deep theoretical level gave Hartnett an edge that few executives in the industry could match.

Hartnett served as President and General Manager of Industrial Tectonics Bearings Corporation, or ITB, subsidiary from 1990, following 18 years at The Torrington Company, one of the three largest bearings manufacturers in the U.S. While at The Torrington Company, Dr. Hartnett held the position of Vice President and General Manager of the Aerospace Business Unit and was, prior to that, Vice President of the Research and Development Division.

Eighteen years at Torrington gave Hartnett a comprehensive education in the bearing business. He ran R&D, developing new products and manufacturing processes. He ran the aerospace business unit, learning the demanding requirements of aircraft manufacturers. He saw how a large bearing company operated at scale.

But by 1990, Hartnett was ready for something different. As he later explained, he needed "that next step" in his career and didn't see it at Ingersoll-Rand (which had acquired Torrington). A friend who owned RBC, then based in Trenton, New Jersey, approached him with an opportunity: manage a newly acquired, struggling operation in Los Angeles.

The Los Angeles Turnaround

RBC itself was struggling, and its New York-based investors "had become disenchanted." This was hardly an attractive proposition on paper—a small, troubled division of a small, troubled company. But Hartnett saw opportunity where others saw problems.

Oxford-headquartered RBC Bearings tells the story of how Dr. Michael J. Hartnett, President and CEO, used to help out at the age of 12 at his dad's tool and die plant in Waterbury. He later bought a failing bearings company in New Jersey, moved it to Connecticut, and turned it into one of the leading suppliers in the aerospace industry in North America.

Within months, Hartnett had made the Los Angeles operation profitable. His approach was fundamentally old-fashioned: strengthen balance sheet fundamentals, re-engineer each production method and process around a budget. No elaborate turnaround strategy or management consultant playbook—just rigorous operational discipline applied by someone who truly understood the manufacturing processes.

The Buyout

Two years later in 1992, at 43, he bought the company, forking out $100,000 of his own money. The rest was put in by Aurora Capital Group, a private equity firm in Los Angeles, which exited in 1997.

This buyout represented a pivotal moment. Hartnett was betting his savings and his career on his ability to build RBC into something significant. Aurora Capital, which had co-founded in 1991, provided the capital and governance structure. Richard Crowell, who has been a director since 2002, is a Managing Partner of Vance Street Capital LLC, a private equity investment firm he founded in 2007. Previously he was the President of Aurora Capital Group, a private equity investment firm he co-founded in 1991.

The private equity backing was crucial. It gave Hartnett the financial flexibility to pursue acquisitions and invest in manufacturing capabilities. But Aurora's exit in 1997 meant that Hartnett and his team were increasingly in control of the company's destiny.

Dr. Hartnett has been the Company's President and Chief Executive Officer since 1992 and Chairman of the Board since 1993. Dr. Hartnett provides the Board with significant leadership and executive experience.

One of Hartnett's first strategic moves was relocating the company. Hartnett moved RBC – originally the Roller Bearing Co. of America when it was founded in 1919 — to Connecticut because of the state's reputation for a skilled workforce. This wasn't just about finding cheaper real estate. Connecticut's manufacturing heritage meant a deep pool of experienced machinists and engineers—exactly the talent needed for precision bearing production.

Dr. Hartnett has developed numerous patents, authored more than two dozen technical papers and is well known for his contributions to the field of tribology, the study of friction. The patents and technical papers weren't mere credentials—they represented genuinely differentiated engineering capability that would become central to RBC's competitive advantage.

What differentiated Hartnett's leadership was the unusual combination of deep technical knowledge, operational discipline, and strategic vision. He wasn't just a manager overseeing engineers—he was himself an engineer who could dive into product design discussions, challenge manufacturing processes, and identify acquisition targets that others might overlook. This engineer-CEO model would prove exceptionally well-suited to building a specialized manufacturing company.

IV. The Acquisition Engine: Building Through M&A (1990s–2000s)

If Michael Hartnett's technical expertise was the engine of RBC's success, acquisitions were the fuel. The majority of that growth was driven by acquisitions – more than two dozen to date. Understanding RBC's M&A playbook reveals a disciplined, patient approach to building a portfolio of complementary businesses.

The Acquisition Philosophy

RBC's acquisition strategy has never been about pursuing scale for its own sake. Instead, each deal followed a consistent logic: acquire complementary businesses that bring new product lines, new customer relationships, or new manufacturing capabilities—then integrate operations while preserving engineering excellence.

The targets shared common characteristics: highly engineered products, established customer relationships (often spanning decades), technical certifications or approvals that create barriers to entry, and typically some operational improvement opportunity that RBC's management could exploit.

Industrial Tectonics Bearings (1990)

The acquisition of Industrial Tectonics Bearings in 1990 was pivotal. ITB specialized in thin section ball bearings crucial for medical equipment and automation—high-precision products where RBC's engineering capabilities could shine. This was also how Hartnett initially came to RBC, serving as President and General Manager of the ITB subsidiary before the buyout.

Heim Bearings (1993)

The first integral rod end was invented by an RBC Bearings division named Heim Bearings. The rod end is also referred to as the Heim Joint named after the inventor Lewis Heim who founded the Heim Bearing Company. While spherical plain bearings offer misalignment capability in a fixed housing position; rod ends offer ease in mounting and adjustment of position in installations such as mechanisms, linkages, and control rods. Rod ends also provide a compact, lightweight, economical design alternative to a conventional housing installation.

Heim Bearings, located in Fairfield, Connecticut, joined the RBC family in 1993. Louis Heim had founded the company in 1942 with an ingenious invention: the integral rod end bearing, specifically the Unibal spherical bearing rod end. This bearing was originally designed to solve aircraft delivery delays due to critical shortages in rod ends and self-aligning bearings during the war effort. Today, rod ends are so universally referred to as "Heim Joints"—even by competitors—that the brand name has become nearly synonymous with the product category.

Nice Ball Bearings (1997)

In 1902, William Nice, Jr. founded the Pressed Steel Manufacturing Company, which produced and sold ball bearings made from sheet steel on a sub-contract basis. In 1914, the first true manufacturing operations commenced, and the company's name was changed to The Nice Ball Bearing Company. Following WWI, the first company factory was built on a 187-acre section of North Philadelphia originally given to the Nice family by William Penn "for services rendered." Nice was purchased in 1997 by RBC Bearings, Inc., where it remains today an integral part of RBC's broad portfolio of bearings companies.

Nice Ball Bearings brought nearly a century of heritage to RBC. The company traced its roots to 1902, when William Nice founded one of the first "anti-friction" bearing manufacturing plants. Nice specialized in precision ground and semi-ground specialty ball bearings, most of which were custom-engineered. The acquisition gave RBC deeper capabilities in industrial applications.

Schaublin SA (2000)

In 2000, RBC expanded internationally by acquiring Schaublin SA, based in Delémont, Switzerland. This acquisition added metric rod ends and metric spherical bearings to the product portfolio and established a base from which to service the European market. It marked RBC's first significant international footprint and demonstrated the company's ambition beyond North America.

The Cumulative Effect

By the early 2000s, RBC had assembled a portfolio of bearing companies, each with distinct technical specialties and customer relationships. The company had evolved from a struggling single-site operation into a multi-division enterprise serving aerospace, defense, and industrial markets across multiple continents.

Founded in 1919, the Company is primarily focused on producing highly technical or regulated bearing products requiring sophisticated design, testing, and manufacturing capabilities for the diversified industrial, aerospace and defense markets. Headquartered in Oxford, Connecticut, RBC Bearings currently employs approximately 1,700 people in 18 facilities located throughout North America and Europe.

The pattern that emerged—buy specialized manufacturers, integrate operations, preserve engineering excellence—would scale dramatically in the years ahead as RBC gained access to public market capital.

V. Going Public: The 2005 IPO

By 2005, RBC Bearings had built a track record worthy of Wall Street's attention. The company had grown steadily through organic expansion and acquisitions, developed a reputation for engineering excellence, and assembled a management team capable of executing on a growth strategy.

RBC Bearings Incorporated will begin trading its common stock on the Nasdaq National Market today under the ticker symbol "ROLL." The initial public offering of 9,288,000 shares of common stock was priced at $14.50 per share. Of the shares offered, 6,273,000 shares were sold by the Company and 3,015,000 shares were sold by selling stockholders.

The IPO, effective on August 9, 2005 and closing on August 15, 2005, marked RBC's transition from a private equity-backed company to a publicly traded enterprise. The offering was made through an underwriting syndicate led by Merrill Lynch & Co. as the sole book-running manager and Keybanc Capital Markets and Jefferies & Company as co-managers.

The ticker symbol "ROLL"—a playful nod to roller bearings—was itself an indication of the company's culture. This was a precision manufacturer with serious engineering credentials, but one that didn't take itself too seriously.

The Follow-On Offering

RBC Bearings completed a follow-on offering in April 2006. The offering totaled 8,989,550 shares at $20.50 per share. The company sold a total number of 2,994,021 shares in the offering and selling stockholders sold a total of 5,995,529 shares. RBC Bearings realized net proceeds from the offering of approximately $57.2 million and used the net proceeds to prepay outstanding indebtedness.

The follow-on offering accomplished two objectives: it provided liquidity for early investors (including Aurora Capital's remaining stake) and strengthened the company's balance sheet for future acquisitions. Using proceeds to pay down debt rather than fund operating losses signaled a company focused on financial discipline.

Stock Performance

Since August 10, 2005, RBC Bearings's market cap has increased from $236.10M to $12.62B, an increase of 5,245.59%. That is a compound annual growth rate of 21.95%.

Few industrial companies have delivered returns like this. A 22% compound annual growth rate over two decades is extraordinary, especially for a manufacturer in a mature industry. The performance reflected both organic growth and the value creation from acquisitions—and validated Hartnett's strategy of building a focused, highly-engineered manufacturing business.

Being public provided access to capital markets for larger acquisitions, but it also brought new constraints—quarterly earnings pressure, analyst scrutiny, Sarbanes-Oxley compliance. RBC's management navigated these tensions by maintaining a long-term focus while delivering consistent results that satisfied short-term-oriented investors.

VI. The Sargent Aerospace Acquisition: Doubling Down on Defense (2015)

By 2015, RBC Bearings was ready for a transformational acquisition. The company had completed numerous smaller deals, developed integration expertise, and built relationships with aerospace and defense customers. Now it was time to think bigger.

RBC Bearings Incorporated, a leading international manufacturer of highly-engineered precision plain, roller and ball bearings for the industrial, defense and aerospace industries, announced that it has entered into a definitive agreement to acquire the Sargent Aerospace & Defense business ("Sargent") of Dover Corporation for $500 million, to be financed through a combination of cash on hand and senior debt.

Connecticut-based RBC Bearings Inc. closed out a $500 million cash and senior debt acquisition of Sargent Aerospace & Defense from Dover Corp., the growing company's 24th acquisition and the first since 2013.

Understanding Sargent

With headquarters in Tucson, Arizona, Sargent is a leader in precision-engineered products, solutions and repairs for aircraft airframes and engines, rotorcraft, submarines and land vehicles. The company manufactures, sells, and services hydraulic valves and actuators, specialty bearings, specialty fasteners, seal rings & alignment joints, and precision components under leading brands including KAHR Bearing, Airtomic, Sonic Industries, Sargent Controls, and Sargent Aerospace & Defense.

Annual sales were approximately $195.0 million and the company had over 750 employees in six facilities in three countries.

Sargent's history was particularly compelling. In 1952, Sargent delivered a unique line of marine valves and actuators for nuclear-powered U.S. Navy submarines. The company's innovation and engineering capabilities persuaded the Navy to accept lightweight aluminum components to replace traditional steel components. At the time, the government was concerned about Navy submarines emitting a sonic signature when being hunted and it turned to Sargent and other manufacturers to make the quietest possible marine valves.

Sargent Aerospace and Defense has been a top supplier of complex hydraulic components for use on nuclear submarines for over 70 years. Sargent's valves and manifolds have been used on platforms ranging from Seawolf, Los Angeles, Ohio, Virginia, and Columbia class nuclear submarines.

This was exactly the kind of business RBC sought: highly engineered products with demanding technical requirements, long-standing customer relationships (70+ years with the Navy!), and significant barriers to entry. The "quiet valve" technology for submarines exemplified the specialized engineering that competitors couldn't easily replicate.

Strategic Rationale

Marine Hydraulics- Designs, manufactures, assembles, and tests hydraulic valves for the U.S. Navy Nuclear Submarine force. Sargent has been supporting the US Navy since the 1950s and has designs on a number of nuclear submarines including the Ohio Class (SSBN) and Virginia Class (SSN). Kahr Bearing- Designs and manufactures specialty bearings for various markets, including commercial and military rotorcraft and fixed-wing aircraft, marine, space, and industrial. Kahr Bearing's specialty products are based on industry-leading liner systems that routinely outperform competing products in longevity and weight.

The Sargent acquisition substantially strengthened RBC's aerospace and defense franchise. It brought hydraulic valves and actuators—a new product category—plus specialty bearings, fasteners, and precision components. The customer overlap was significant: both companies served Boeing, major defense contractors, and the U.S. military.

The acquisition was designed to expand and strengthen RBC's aerospace and defense business and portfolio. It fit well with RBC's philosophy of providing high quality products and solutions to its customer base, broadened and strengthened product offering enhancing customer solutions and experience, diversified product offering within aerospace and defense markets, and extended Sargent product offering to RBC's international reach.

Integration Challenges

The integration wasn't without challenges. As Hartnett noted at the time, when Dover was working on selling Sargent, the operation had fallen behind on orders. RBC's management had to work through a backlog while simultaneously integrating the business. The second quarter adjusted gross profit margin of 37.9 percent following the acquisition was strong, though revenue and operating profit initially came in below analyst expectations due to these capacity constraints.

But RBC's patient approach to integration—focusing on operational excellence rather than aggressive cost-cutting—eventually paid off. Sargent became a cornerstone of RBC's aerospace and defense segment.

VII. The Transformational DODGE Acquisition: Doubling the Company (2021)

If Sargent was RBC's largest acquisition to date, DODGE was transformational at an entirely different scale. The deal, announced in July 2021, represented the biggest bet in RBC's history.

ABB announced it has signed a definitive agreement to divest its Mechanical Power Transmission division (Dodge) to RBC Bearings Incorporated (Nasdaq: ROLL), for $2.9 billion in cash.

The DODGE Heritage

For more than 140 years, the Dodge business has been a leader in the design, production, and marketing of mounted bearings, enclosed gearing, and power transmission components. It offers one of the broadest portfolios of mechanical power transmission products in the market, selling to industries such as surface mining, aggregates & cement, warehousing and food & beverage.

The Dodge brand has stood for innovation for over 140 years, building upon the legacy of its founder, Wallace Dodge, by providing advanced product solutions and technologies and best-in-class services that help manufacturers improve output, decrease downtime, and enhance system value.

With headquarters in Greenville, South Carolina, DODGE is a leading manufacturer of mounted bearings and mechanical products with market-leading brand recognition. DODGE manufactures a complete line of mounted bearings, enclosed gearing and power transmission components across a diverse set of industrial end markets. DODGE primarily operates across the construction and mining aftermarket, food & beverage, warehousing and general machinery verticals, with sales predominately in the Americas. DODGE generated revenue of approximately $617 million and adjusted EBITDA of approximately $174 million, representing an adjusted EBITDA margin of 28%, for the 12 months ended June 30, 2021.

Deal Economics

RBC Bearings announced that it has entered into a definitive agreement to acquire the DODGE mechanical power transmission division of Asea Brown Boveri Ltd ("ABB") for $2.9 billion in cash. The purchase price represents 16.7x DODGE's adjusted EBITDA for the 12 months ended June 30, 2021, or 10.6x to 11.9x adjusted EBITDA when including estimated run-rate synergies.

At nearly $3 billion, the acquisition represented a bold expansion of RBC's industrial footprint. The company was paying a premium multiple, but one justified by DODGE's brand strength, market position, and synergy potential.

The acquisition was anticipated to be immediately accretive to RBC Bearings' cash EPS by approximately 40% to 60% in the first full fiscal year after close. The company expected cash EPS to be in the range of $7.00 to $8.00 per share in the first full fiscal year. The acquisition was expected to generate annual pre-tax run-rate synergies of approximately $70 million to $100 million by fiscal year 2026.

Financing the Deal

RBC Bearings was in active negotiations with certain lenders to enter into a new credit agreement providing for a term loan facility in an aggregate amount of $1.3 billion and a revolving facility in an aggregate amount of $500 million. The new term loan and revolving facility have been allocated and the new credit agreement was expected to close concurrently with the closing of the Dodge acquisition. RBC Bearings intended to use the net proceeds from these financings to fund a portion of the cash purchase price for the pending acquisition of Dodge, to pay acquisition-related fees and expenses, and for other general corporate purposes.

The financing structure—combining debt, equity, and preferred stock—demonstrated RBC's financial sophistication and its lenders' confidence in the combined company.

Strategic Transformation

The acquisition doubled revenue. It brought attractive profitability with DODGE's $174 million EBITDA representing a 28% margin. It maintained low capital intensity with Capex at approximately 3% of revenue. And it added stable recurring revenue base with approximately 60% of DODGE revenue from aftermarket.

The strategic logic was compelling. RBC Bearings had historically been weighted toward aerospace and defense, which provided stability but also concentration risk. DODGE brought diversification into industrial markets—construction, mining, food and beverage, warehousing—where replacement cycles provided recurring revenue streams.

RBC Bearings announced on November 1, 2021 that it has completed its previously announced acquisition of the DODGE mechanical power transmission division. CEO Michael J. Hartnett said "We are excited to welcome our DODGE teammates to the RBC Bearings' family. The closing of this transaction is the first step to realizing the great benefits of this combination."

The integration philosophy remained consistent: preserve what makes each business successful while finding operational synergies.

VIII. The Modern Era: Today's RBC Bearings (2022–Present)

The years since the DODGE acquisition have validated the strategic logic. RBC Bearings has successfully integrated the business while continuing to grow both organically and through additional acquisitions.

Fiscal 2025 Results

Fiscal 2025 net sales of $1,636.3 million increased 4.9% over last year, Aerospace/Defense up 14.1% and Industrial up 0.2%. Gross margin of 44.4% for fiscal 2025 compared to 43.0% last year.

Dr. Michael J. Hartnett stated: "I am proud of our team's outstanding performance in Fiscal 2025. We executed flawlessly in an aerospace production environment that included multiple disruptions, and our intense focus on organic growth as a cornerstone of the RBC Ops Management System enabled us to significantly outgrow Industrial markets that mostly contracted throughout the year. In true RBC fashion, we delivered a stronger than expected operating performance, translating revenue growth of roughly five percent to Adjusted EBITDA growth of 7.8 percent, and Adjusted EPS growth of 16.1 percent. That translated into another record year for free cash flow generation, which we used to pay down an additional $275 million of debt, taking trailing net leverage to a post-Dodge low of 1.7x."

The debt paydown is particularly significant. RBC took on substantial leverage to acquire DODGE, but the company has steadily de-leveraged through strong free cash flow generation. The 1.7x net leverage ratio positions RBC for future acquisitions.

Most Recent Results: Q2 Fiscal 2026

Net sales for the second quarter of fiscal 2026 were $455.3 million, an increase of 14.4% from $397.9 million in the second quarter of fiscal 2025. $24.7 of net sales this quarter came from VACCO, which was acquired on July 18, 2025. Net sales for the Industrial segment increased 0.7%, while net sales for the Aerospace/Defense segment increased 38.8%. Gross margin for the second quarter of fiscal 2026 was $200.6 million compared to $173.8 million for the same period last year.

The company reports a segment revenue mix of 56% Industrial and 44% A&D, with A&D projected to reach parity next year. RBC Bearings delivered double-digit top-line growth and significant margin expansion for fiscal Q2 2026, propelled by exceptional Aerospace and Defense performance, and disciplined expense management. Operations are capacity-constrained in core aerospace plants, prompting ongoing investments to expand output in response to record demand and a sharply increased backlog. Management's near-term focus remains on expanding manufacturing, integrating new assets, extracting operational efficiencies, and promptly realizing margin benefits from recently renegotiated aerospace contracts. Management confirmed an expectation to approach $2 billion in backlog by year-end.

The VACCO Acquisition

RBC Bearings Inc. announced that it has closed on its previously announced acquisition of Southern California valves and filters maker VACCO Industries. RBC bought the business from ESCO Technologies Inc. for $275 million in cash. VACCO was integrated into RBC's aerospace and defense unit.

VACCO Industries, headquartered in South El Monte, California, is a key player in the manufacturing of sophisticated valves, manifolds, regulators, filters, and precision components and subsystems tailored for the space and naval defense markets.

"VACCO has a tremendous amount of design, engineering and manufacturing capabilities," said Dr. Michael J. Hartnett. "Combining VACCO's expertise in highly engineered valves, regulators and manifolds with RBC's broader portfolio will enable us to better serve the evolving needs of customers in the secularly growing space and naval submarine channels."

The VACCO acquisition continues RBC's pattern: highly engineered products, defense and aerospace exposure, specialized manufacturing capabilities. The space channel, in particular, represents a growing market as commercial space activities accelerate.

Global Footprint

RBC employs 5,302 people worldwide. Of that, 3,738 are employed at 35 U.S. facilities and 1,564 are employed at 19 international facilities located in Canada, Mexico, France, Switzerland, Germany, Poland, India, Australia, China and England.

RBC Bearings has 5334 employees. The company's manufacturing footprint spans four continents, allowing it to serve customers globally while maintaining proximity to key markets.

IX. Business Model Deep Dive: Understanding the Moat

What makes RBC Bearings special? Why has this company outperformed peers so dramatically over two decades? The answers lie in a set of interlocking competitive advantages.

Certification Moats

RBC produces highly technical or regulated bearing products and components requiring sophisticated design, testing and manufacturing capabilities. While manufacturing products in all major categories, the company focuses primarily on highly technical or regulated bearing products and engineered products for specialized markets that require sophisticated design, testing and manufacturing capabilities.

For aerospace and defense products, the certification process creates formidable barriers. Obtaining FAA approval or DOD certification can take years and requires substantial investment in testing, documentation, and quality systems. Once a company achieves certification, it has a significant advantage over potential competitors who would need to invest similar time and resources.

In many instances, RBC is the only approved supplier of a given bearing or engineered component. Currently, a half of RBC's revenue is from proprietary designed bearings for which no other supplier is approved. "In the other 50 percent of our business, we compete on service levels," Hartnett has explained.

Customer Relationships

Employing more than 3,500 people, RBC Bearings is a well-known and respected supplier, with clients that include Boeing, Airbus, NASA, and the U.S. Department of Defense.

These aren't transactional relationships. RBC's engineers work directly with customers on application design, often developing custom bearings for specific programs. Once a bearing is designed into an aircraft or submarine, the switching costs are enormous—any change requires re-certification, re-testing, and carries risk that buyers are unwilling to accept.

Market position reflects strong customer relationships, long-term contracts (approximately 65% of revenues), highly specialized products, with approximately 60% of revenue from sole/single-source products, and 40+ year relationships on average with top customers.

Technical Depth

The company's technical capabilities run deep. RBC offers:

- Plain bearings with self-lubricating or metal-to-metal designs

- Roller bearings including tapered, needle roller, and cam followers

- Ball bearings for high precision aerospace and industrial applications

- Engineered products including collets, precision components, and hydraulic systems

RBC Bearings manufactures and markets engineered precision bearings, components, and systems in the United States and internationally. It operates through two segments, Aerospace/Defense and Industrial. The company produces plain bearings with self-lubricating or metal-to-metal designs, including rod end bearings, spherical plain bearings, and journal bearings; roller bearings, such as tapered roller bearings, needle roller bearings, and needle bearing track rollers and cam followers.

The Aftermarket Advantage

A crucial element of RBC's model is aftermarket revenue. Bearings wear out and must be replaced. Once RBC bearings are installed in an aircraft, submarine, or industrial machine, the company has a recurring revenue stream from replacement sales.

DODGE brought particularly strong aftermarket characteristics, with approximately 60% of revenue from replacement sales. This creates a "like-for-like" replacement cycle where installed hardware generates ongoing demand.

End Market Diversification

The company's products include precision mechanical components used in various general industrial applications and machine tool collets used for holding circular or rod-like pieces. It serves commercial and defense aerospace, construction, mining, forestry, energy, agricultural, food and beverage, metals and mining material handling, chemicals, oil and gas production, warehousing and logistics, semiconductor equipment, waste and water management, and rail and transportation applications through its direct sales force, and a network of industrial and aerospace distributors.

This diversification provides resilience. When one end market weakens, others often compensate. Commercial aerospace cycles differently than defense spending, which cycles differently than mining equipment demand.

X. Porter's Five Forces Analysis & Investment Framework

Threat of New Entrants: LOW

The bearing industry, particularly the specialized segments where RBC competes, presents formidable barriers to entry:

- Certification requirements: FAA certifications, DOD approvals, and OEM qualifications take years to obtain. In many instances RBC is the only approved supplier of a given bearing or engineered component.

- Capital intensity: Precision manufacturing equipment requires substantial investment.

- Technical expertise: Dr. Hartnett has developed numerous patents, authored more than two dozen technical papers and is well known for his contributions to the field of tribology. This depth of expertise is developed over decades, not years.

- Customer relationships: 40+ year relationships with major customers create institutional knowledge and trust that new entrants cannot replicate.

Bargaining Power of Suppliers: LOW-MODERATE

Raw materials for bearings—specialty steels and alloys—are generally available from multiple sources. RBC's scale provides purchasing leverage, and the company has reduced supplier dependency through vertical integration via acquisitions.

Bargaining Power of Buyers: LOW-MODERATE

Sole and single source products are items for which RBC is the only (sole) or one of very few (single) approved suppliers under long-term agreements. When RBC is the only approved supplier, buyer bargaining power is minimal. Even in more competitive segments, the high switching costs (re-certification, risk of failure) give RBC pricing power.

The concentration risk cuts both ways—losing a major customer like Boeing would be painful. But the long-term nature of aerospace programs provides visibility and stability.

Threat of Substitutes: LOW

Bearings are fundamental to mechanical systems. While bearing designs evolve, the basic function—reducing friction between moving parts—has no practical substitute. Electric motors still need bearings. Self-driving vehicles still need bearings. The technology evolution in bearings is incremental refinement, not wholesale replacement.

Competitive Rivalry: MODERATE

The global bearing market is highly competitive and consolidated, with leading companies including SKF, Schaeffler Group, NTN Corporation, NSK Ltd, THE TIMKEN COMPANY, and JTEKT Corporation dominating due to their large-scale production capabilities, strong R&D focus, global presence, and established relationships with OEMs and end-users.

RBC competes against much larger companies, but has carved out defensible niches in specialized, high-margin segments. The company doesn't compete on volume in commodity bearings—it competes on engineering capability in precision applications.

Hamilton Helmer's 7 Powers Framework

Evaluating RBC through the lens of competitive moats:

-

Scale Economies: Moderate. RBC isn't the largest bearing manufacturer, but scale in specialized segments matters.

-

Network Effects: Weak. Bearings don't have network effects.

-

Counter-Positioning: Strong. RBC's focus on specialized, highly-engineered products allows it to operate differently than high-volume manufacturers.

-

Switching Costs: Very Strong. Certification requirements, designed-in products, and risk aversion create powerful switching costs.

-

Branding: Moderate. Brands like DODGE and Heim have recognition in their markets.

-

Cornered Resource: Strong. The combination of certifications, customer relationships, and engineering expertise represents proprietary capability.

-

Process Power: Strong. RBC's manufacturing processes have been refined over decades, creating quality and efficiency advantages.

Key Performance Indicators to Track

For investors following RBC Bearings, three metrics deserve close attention:

-

Gross Margin: Currently at 44%+, gross margin reflects the company's ability to maintain pricing power and manufacturing efficiency. Expanding margins indicate successful integration and mix shift toward higher-value products.

-

Aerospace/Defense Segment Growth: This segment provides visibility into RBC's core competitive advantages. The Aerospace/Defense segment increased 38.8% in Q2 FY2026—exceptional growth driven by Boeing and Airbus production increases plus defense spending.

-

Backlog: The company's backlog as of September 27, 2025, was $1.6 billion, up from $1.0 billion as of June 28, 2025, and $0.9 billion as of September 28, 2024. Backlog growth provides forward visibility and indicates demand strength.

XI. Bull and Bear Cases

Bull Case

Aerospace Supercycle: Boeing and Airbus are ramping production to unprecedented levels after years of subdued output. As Boeing and Airbus and Embraer continue increasing build rates to unprecedented levels, production of RBC's products must follow. The company has substantial contracts in these airframes and engines, supplying precision and line bearings as well as integrated structural components. Building rates of submarines and aircraft are at levels not seen in over a generation, since the early 1980s for submarines. The company is currently booking some orders for deliveries into the 2030s. RBC is positioned with a considerable number of proprietary sole and single source products governed by multiyear contracts in the majority of cases.

Defense Spending: Naval submarine programs represent particularly compelling growth drivers. The Virginia-class and Columbia-class submarine programs require specialized hydraulic components where RBC (through Sargent) has decades of heritage and sole-source positions.

Margin Expansion: As RBC achieves run-rate synergies from DODGE and VACCO while renegotiating aerospace contracts, margins have room to expand further.

Continued M&A: With leverage at 1.7x—the lowest since DODGE—and management signaling a "more selective approach to mergers and acquisitions," the company has firepower for additional deals.

Management Track Record: Under Hartnett's leadership, the company's sales have grown from $35 million to nearly $700 million—and that was before DODGE. The team has demonstrated an ability to create value through organic growth and acquisitions over more than three decades.

Bear Case

Valuation: At a PE ratio of 52.38, the stock prices in substantial growth and execution. Any disappointment could trigger multiple compression.

Aerospace Concentration Risk: The dependence on Boeing and Airbus means that production disruptions at these customers (labor strikes, quality issues, supply chain problems) directly impact RBC. The recent Boeing strike demonstrated this vulnerability.

Succession Risk: Dr. Hartnett, born in 1945, has led the company since 1992. While the management team is capable, the eventual leadership transition represents uncertainty.

Industrial Weakness: The Industrial segment increased only 0.7%—essentially flat. If aerospace growth moderates while industrial markets remain sluggish, overall growth could disappoint.

Acquisition Integration: Each acquisition carries integration risk. VACCO, while smaller, requires management attention. Future deals, if larger, could prove more challenging.

Rising Interest Rates Impact: While RBC has paid down debt aggressively, higher rates increase financing costs for both the company and potential acquisition targets.

XII. Conclusion: The Compounding Machine

RBC Bearings represents a particular kind of business story—one that unfolds over decades rather than quarters, built through patient accumulation of competitive advantages rather than dramatic pivots. It's the story of an engineer who understood his products, his customers, and his industry, and who methodically built a company that could compound value over the very long term.

The company today looks dramatically different than it did when Hartnett led the 1992 buyout with $100,000 of his own money. From a struggling regional manufacturer to a $13+ billion enterprise serving global aerospace, defense, and industrial markets. From 18 facilities to 54. From dozens of employees to over 5,300.

Yet the core philosophy has remained consistent: focus on highly-engineered products where technical expertise creates barriers to entry; build and maintain long-term customer relationships; acquire complementary businesses and integrate them carefully; generate strong free cash flow and use it wisely.

"We fully expect to approach $2 billion in backlog by year's end," Dr. Hartnett stated. The company plans to pay off its term loan by November 2026.

For investors, RBC Bearings offers a case study in industrial compounding. The valuation isn't cheap, but then again, truly great businesses rarely are. The question isn't whether RBC is expensive relative to the market—it's whether the company can continue executing the playbook that has worked for over three decades.

In a world obsessed with disruption and transformation, RBC Bearings stands as a reminder that there's another path to creating value: master something difficult, do it better than anyone else, and keep doing it year after year. The bearings might be invisible to most people, but the results are not.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube