Shin-Etsu Chemical: The Invisible Empire Behind Every Chip

I. Introduction & Episode Roadmap

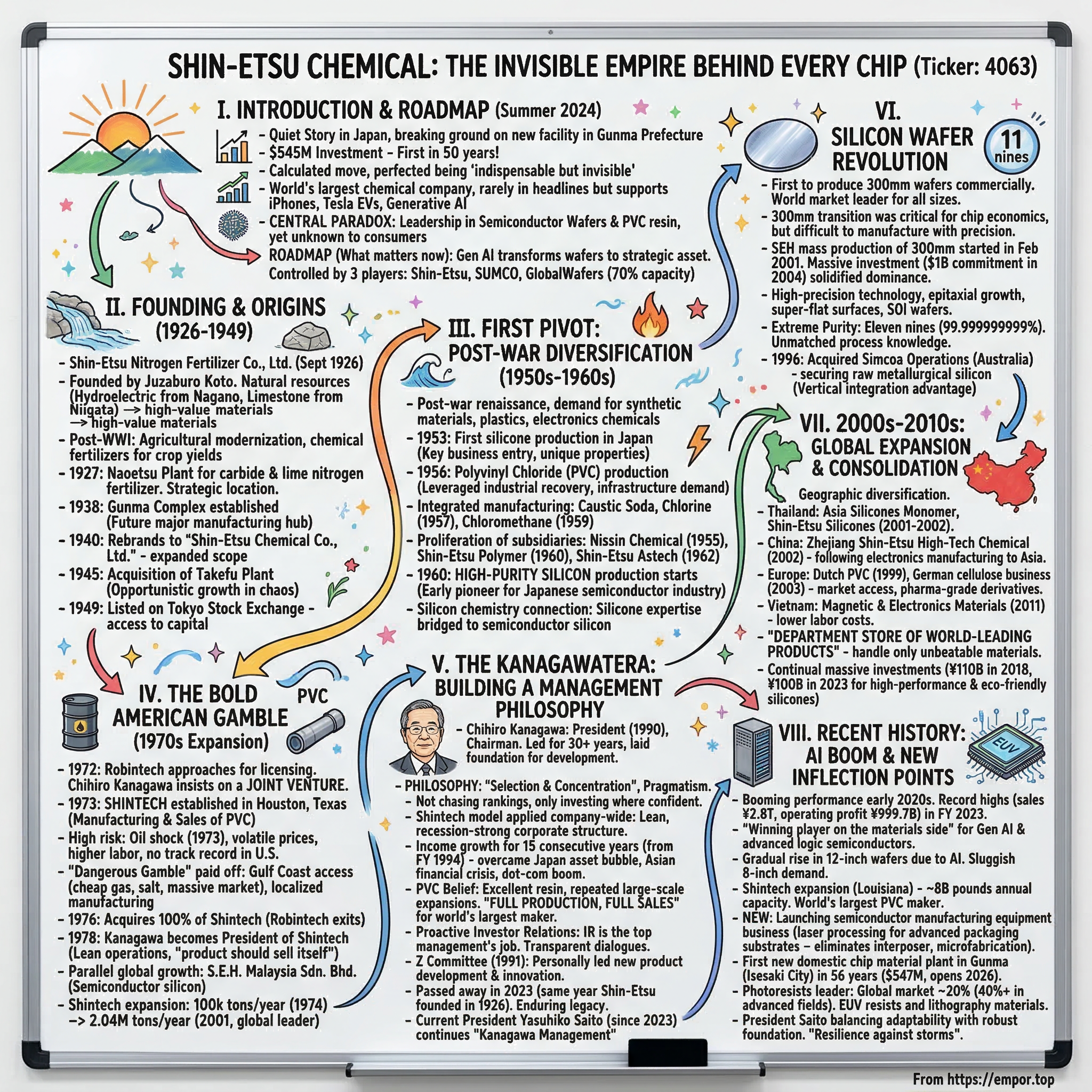

In the summer of 2024, as the world watched Nvidia's market capitalization soar past $3 trillion on the back of AI fever, a quieter story was unfolding in the industrial heartlands of Japan. In a modest factory complex in Gunma Prefecture, workers began breaking ground on what would become the first new manufacturing facility built by Shin-Etsu Chemical in Japan in over half a century. The $545 million investment was no vanity project—it was a calculated move by a company that has spent nearly a century perfecting the art of being indispensable while remaining invisible.

Shin-Etsu Chemical Co., Ltd. is the largest chemical company in Japan. The company holds the largest global market share for polyvinyl chloride, semiconductor silicon, and photomask substrates. Yet outside the rarified circles of materials science and semiconductor manufacturing, few consumers would recognize the name. This is by design. Shin-Etsu has never chased consumer brands or retail visibility. Instead, it has methodically positioned itself at the foundational layer of modern technology—the place where raw materials become the building blocks of civilization.

The central paradox of Shin-Etsu is this: the company holds the global leadership position in semiconductor silicon wafers and polyvinyl chloride (PVC) resin, yet it rarely appears in headlines. Though rarely visible to consumers, it is truly the unsung hero supporting Apple's iPhones and Tesla's EVs behind the scenes. Every advanced chip powering generative AI, every PVC pipe carrying water to homes across America, every silicone sealant in a new construction project—Shin-Etsu's materials are there, invisible but essential.

Why does this matter now? Shin-Etsu Chemical, the world's top producer of silicon wafers, controls about 30% of the wafer market. The company is also the world's second-largest producer of photoresists and advanced photomask blanks used for forming circuit patterns. In an era when generative AI has transformed semiconductor wafers from a commodity into a strategic asset, Shin-Etsu finds itself at the center of one of the most important supply chains on Earth. Three incumbent suppliers—Shin-Etsu Chemical, SUMCO, and GlobalWafers—command roughly 70% of worldwide capacity.

The company's story is one of patient capital, methodical expansion, and a management philosophy that prioritizes decades over quarters. It is a story of how a fertilizer company founded in the mountains of central Japan became an indispensable supplier to the world's most advanced technology manufacturers. And it is a story that illuminates something essential about the nature of competitive advantage in materials science—an industry where moats are built not through software or network effects, but through process knowledge, vertical integration, and the relentless pursuit of purity measured in parts per trillion.

II. Founding & Origins: From Fertilizer to Fortune

The origin of Shin-Etsu Chemical is literally written into its name. Nagano Prefecture's plentiful water gave birth to electric power and the limestone that came from Niigata Prefecture was a key raw material, which was called "Oyashirazu's great earth." Because of the presence of these two gifts of nature, Shin-Etsu Nitrogen Fertilizer Co., Ltd. was founded in September 1926 to manufacture chemical fertilizer and limestone nitrogen. The company's "Shin" comes from Shinano and "Etsu" is taken from Echigo.

The founder, Juzaburo Koto, understood something fundamental about industrial chemistry: it is, at its core, the business of transforming abundant natural resources into scarce, high-value materials. Nagano Prefecture offered hydroelectric power—cheap, reliable electricity that could drive the energy-intensive processes required for chemical manufacturing. Niigata Prefecture offered limestone, the essential raw material for nitrogen fertilizers. Koto's vision was to bring these two gifts of nature together.

The timing was significant. Post-World War I Japan was pushing aggressively for agricultural modernization and self-sufficiency. The government understood that a nation dependent on imported food was a nation vulnerable to external pressure. Chemical fertilizers offered the promise of dramatically increased crop yields, and companies that could manufacture them domestically would find ready markets and government support.

Shin-Etsu Nitrogen Fertilizer Co., Ltd. was founded in 1926 and in 1927 the Naoetsu plant was constructed for the production of carbide and lime nitrogen fertilizer. The Naoetsu Plant began production of carbide and lime nitrogen fertilizer in 1927, establishing the company's first manufacturing base. The choice of location was strategic: close to the limestone deposits of Niigata, with access to hydroelectric power, and connected to distribution networks that could reach agricultural markets throughout Japan.

In 1938 the first facility of the Gunma Complex was established. The Gunma Complex would eventually grow to become one of Shin-Etsu's most important manufacturing hubs, producing silicon wafers, silicones, and other advanced materials. But in 1938, the facility represented a geographical diversification—a hedge against the risks of concentrating all production in a single location.

The company changed its name to Shin-Etsu Chemical Co., Ltd. in 1940. The name change reflected a broader strategic vision. Shin-Etsu was no longer simply a nitrogen fertilizer company; it was becoming a diversified chemical manufacturer. The new name kept the geographical roots—the connection to the Shin'etsu region—while signaling an expanded scope of ambitions.

The war years and immediate postwar period tested the company's resilience. Like all Japanese industrial firms, Shin-Etsu faced disruption, destruction, and reconstruction. In 1945, the company expanded with the acquisition of the Takefu plant. This acquisition, made in the chaotic final months of World War II, demonstrated an opportunistic approach to growth that would characterize Shin-Etsu's strategy for decades to come.

In 1949, the company shares were listed on the Tokyo Stock Exchange. The public listing marked a turning point. It brought access to capital markets, greater visibility, and the discipline of public company reporting. It also coincided with Japan's early postwar recovery, as American occupation authorities worked to rebuild Japanese industry along more competitive, less monopolistic lines.

The foundation laid in these early years—the focus on chemical processing, the connection to natural resources, the willingness to expand through acquisition, and the patient accumulation of process knowledge—would prove essential to everything that followed.

III. The First Pivot: Post-War Diversification (1950s-1960s)

Japan's postwar industrial renaissance created enormous opportunities for chemical companies willing to move beyond traditional products. As the economy rebuilt and urbanized, demand surged for synthetic materials, plastics, and the specialized chemicals required for electronics manufacturing. Shin-Etsu positioned itself to capitalize on these trends through a series of strategic pivots that would define its future.

The first silicone production facilities were set up in 1953. This entry into silicones represented Shin-Etsu's first venture into what would become one of its core businesses. In 1953, Shin-Etsu Chemical became the first firm in Japan to enter the silicones business. In the decades since, Shin-Etsu has created a diverse line of products designed to exploit the many useful properties of silicones.

The silicone breakthrough was significant for several reasons. Silicones—polymers containing silicon, oxygen, and organic groups—offered properties that no other materials could match: heat resistance, electrical insulation, water repellency, and chemical stability. These properties made silicones essential for applications ranging from construction sealants to medical devices to electronics manufacturing. By becoming Japan's first silicone producer, Shin-Etsu secured an early-mover advantage in a high-growth market.

In the mid-1950s, Shin-Etsu Chemical began diversifying beyond its early focus on fertilizers by entering the organic chemicals sector, with the initiation of polyvinyl chloride (PVC) production in 1956. This move marked a pivotal shift toward synthetic resins, leveraging Japan's post-war industrial recovery and growing demand for durable plastics in construction and consumer goods. By integrating chlorine-based processes, the company established a foundation for integrated chemical manufacturing, which included subsequent starts in caustic soda and chlorine production in 1957 and chloromethane in 1959.

The PVC business would eventually become one of Shin-Etsu's largest profit centers, but in the 1950s it represented a calculated bet on Japan's urbanization. PVC's durability, cost-effectiveness, and versatility made it ideal for pipes, window frames, flooring, and countless other construction applications. As Japan rebuilt its cities and infrastructure, demand for PVC would grow exponentially.

Shin-Etsu established Nissin Chemical Industry Co., Ltd. in 1955, which was followed by the establishment of Shin-Etsu Polymer Co., Ltd. in 1960 and two years later the Shin-Etsu Astech Co., Ltd. This proliferation of subsidiaries reflected Shin-Etsu's approach to growth: rather than expanding a single corporate entity, the company created specialized affiliates focused on specific products and markets. This structure allowed for targeted investments, clear accountability, and the flexibility to enter and exit businesses as conditions changed.

The 1960s saw further expansion into electronics materials, driven by the global rise of semiconductors. In 1960, Shin-Etsu commenced high-purity silicon production, a critical input for silicon wafers used in integrated circuits, positioning the company as an early pioneer in Japan's nascent semiconductor industry. That same year, it established Shin-Etsu Polymer Co., Ltd. as a wholly owned subsidiary to develop and manufacture polymer-based products, including PVC compounds and silicone-derived components. These initiatives capitalized on the company's expertise in silicon chemistry, enabling vertical integration from raw silicon metal to advanced electronic applications.

The entry into high-purity silicon in 1960 was perhaps the most consequential decision of this era. At the time, the semiconductor industry was still in its infancy. Texas Instruments and Fairchild Semiconductor were pioneering integrated circuits in the United States, but the global market for semiconductor materials was tiny. Shin-Etsu's decision to invest in silicon purification technology reflected a long-term view of the industry's potential—a willingness to accept years of modest returns in exchange for building capabilities that would prove invaluable decades later.

The key theme of this era was the silicon chemistry connection. Shin-Etsu's expertise in silicones provided a natural bridge to semiconductor silicon. Both businesses required deep understanding of silicon's chemical properties, both demanded extreme purity in manufacturing, and both benefited from vertical integration in raw material supply. By mastering silicon chemistry, Shin-Etsu created a platform that could support multiple product lines across different end markets.

Silicone is a highly functional material that has both organic and inorganic characteristics and has many superior distinguishing features. The Shin-Etsu Group currently provides more than 5,000 silicone products to a wide range of industries. This breadth—from construction sealants to semiconductor encapsulants—would become one of Shin-Etsu's defining competitive advantages.

IV. The Bold American Gamble: Shintech & The 1970s Expansion

In 1972, a sales inquiry arrived at Shin-Etsu's headquarters that would change the company's trajectory forever. In the fall of 1972, Robintech Inc., which was a large manufacturer of PVC pipes used for water pipes, approached Shin-Etsu Chemical asking for licensing of their manufacturing technologies. At that time, Chihiro Kanagawa strongly believed that they should not sell the technologies which were the lifeline of their business, but rather establish a joint venture. Therefore in 1973 they established Shintech in Houston, Texas for the manufacturing and sales of PVC.

The decision to establish Shintech rather than simply license technology was characteristic of the aggressive, ownership-oriented approach that would define Shin-Etsu's international strategy. Both Shin-Etsu Chemical and Robintech invested $2.5 million. Due to the first oil shock in 1973, the price of PVC soared, but then by 1974 the price sharply dropped as a reaction to it. When Shintech started its production in October 1974 under this severe situation, they produced 100,000 tons per year. Their market share in North America was only 3% and ranked at the 13th position.

The timing could not have been worse. The oil shock of 1973 sent energy prices soaring, disrupting petrochemical economics worldwide. PVC prices were volatile, and many observers questioned whether a Japanese company could successfully compete in the American market against established domestic producers.

The company boldly undertook the construction of a large-scale PVC plant in the United States during the 1970s, a move that was considered a "dangerous gamble" at the time. Industry analysts and competitors viewed the venture with skepticism. American labor costs were higher, logistics were unfamiliar, and Shin-Etsu had no track record in the U.S. market.

But Shin-Etsu saw what others missed. The U.S. Gulf Coast offered access to cheap natural gas, the primary feedstock for ethylene production. It offered abundant salt deposits for chlorine production. And it offered proximity to the massive construction and infrastructure markets that consumed the majority of PVC output. By manufacturing locally, Shin-Etsu could avoid import tariffs, reduce shipping costs, and respond more quickly to customer needs.

At that time the CEO of Robintech, which was Shintech's joint venture partner, was Mr. Brad Corbett. He was a flamboyant businessman and bought the Texas Rangers, a baseball team, in 1974. After that, Robintech's business worsened, and in 1976 the company requested Shin-Etsu Chemical to purchase their share of Shintech stocks. As a result, Shin-Etsu Chemical acquired 100% ownership of Shintech.

The departure of Robintech created both opportunity and challenge. Shin-Etsu now had full control, but also full responsibility. The company needed leadership on the ground who understood both American business culture and Shin-Etsu's manufacturing philosophy.

Kanagawa became Chairman and recruited a president, who used to be a business manager of a large U.S. company. However, he soon found that his management policies and his were quite different. For instance, he claimed that they should have as many as forty sales people, whereas Kanagawa believed that two people should have been enough. So in March 1978, Kanagawa ended up becoming the president of Shintech.

This anecdote reveals something essential about the "Kanagawa Management" philosophy that would define Shin-Etsu for decades. Kanagawa believed in lean operations, minimal overhead, and empowering workers to take responsibility for their areas. The idea that a PVC manufacturer needed forty salespeople struck him as absurd—the product should sell itself through quality and competitive pricing, not through an army of sales representatives.

In 1973, Shin-etsu established its first U.S.-based company named Shintech, Inc., and its first Malaysia-based company, S.E.H. Malaysia Sdn. Bhd. The parallel establishment of Malaysian operations signaled the beginning of Shin-Etsu's semiconductor silicon business internationally. While Shintech would focus on PVC, the Malaysian subsidiary would produce silicon wafers for the burgeoning semiconductor industry.

Production at the Shintech Freeport plant began in 1976, and that same year the PVC & Polymer Materials Research Center and the Silicone Electronics Materials Research Center were established. The simultaneous investment in research centers and production facilities reflected Shin-Etsu's integrated approach: manufacturing excellence required continuous innovation, and innovation required close connection to manufacturing realities.

Shintech started the production of polyvinyl chloride (PVC) at Freeport, Texas in October 1974. The annual production capacity was 100,000 tons, and Shintech embarked on the road to operation as the 13th largest manufacturer in the U.S. Dr. Kanagawa, who managed the company, aggressively penetrated both the U.S. and world markets, and expanded its production capacity to 450,000 tons in ten years, and by 1990, the production capacity reached 900,000 tons. In 2001, the company became the global leader with an annual production capacity of 2,040,000 tons.

This growth trajectory—from 100,000 tons to over 2 million tons in less than three decades—was remarkable. Shintech didn't just enter the American market; it came to dominate it.

V. The Kanagawa Era: Building a Management Philosophy

At Shin-Etsu Chemical, in 1990 Chihiro Kanagawa was appointed President after serving as General Manager of the International Division, Senior Managing Director, General Manager of the PVC Division, and Executive Vice President. Kanagawa's appointment marked the beginning of one of the most transformative leadership eras in Japanese corporate history.

The current President and Representative Director is Mr. Yasuhiko Saito (appointed in 2023). Former Chairman Mr. Chihiro Kanagawa (deceased in 2023) is known for leading the company for over 30 years and laying the foundation for its development.

Kanagawa's management philosophy can be summed up as "selection and concentration" and "pragmatism." In interviews during his lifetime, Kanagawa stated he would not make forced investments just to chase rankings. He explicitly stated he wouldn't engage in businesses where he lacked confidence.

This philosophy stood in stark contrast to the empire-building mentality that characterized many Japanese conglomerates. While other companies diversified into unrelated businesses, acquired competitors for the sake of scale, and pursued growth for its own sake, Kanagawa focused relentlessly on businesses where Shin-Etsu could achieve and maintain world leadership.

His approach to Shintech became the template for the broader company. In the harsh business environment after the bursting of the bubble economy in Japan, he introduced the rational management practiced in the management of Shintech into the Company, and built a corporate structure that is strong against recession. At the same time, he worked to develop new businesses such as photoresists. Overcoming the severe external environment, including the bursting of the IT bubble, he achieved income growth for 15 consecutive years from the fiscal year ended March 1994.

Fifteen consecutive years of income growth—through the bursting of Japan's asset bubble, through the Asian financial crisis, through the collapse of the dot-com boom—was an extraordinary achievement. It reflected not luck but systematic management: conservative financial policies, continuous operational improvement, and strategic investments in growth areas offset by restraint in declining ones.

Based on the conviction that "PVC is an excellent resin that contributes to society and the environment, and the demand continues to grow," he repeatedly carried out large-scale PVC plant expansions with Shintech's own funds and continued "full production, full sales." Shintech grew into the world's largest PVC manufacturer.

Kanagawa's belief in PVC was unwavering. While environmental activists criticized the material and competitors hedged their bets, Kanagawa doubled down. He understood that PVC's durability, cost-effectiveness, and recyclability made it irreplaceable for infrastructure applications. Water pipes, window frames, medical tubing, electrical insulation—these applications weren't going away, and PVC remained the best material for most of them.

The "full production, full sales" philosophy was central to Shintech's success. Rather than adjusting production to match short-term demand fluctuations, Kanagawa kept plants running at maximum capacity, using scale advantages to undercut competitors on price while maintaining profitability through operational efficiency. This approach worked because Shin-Etsu's manufacturing processes were genuinely more efficient than competitors'—a gap that widened with every capacity expansion.

In the latter half of the 1990s, he affirmed that IR is the job to be done by the top management. He held numerous dialogues with investors and sell-side analysts and continued to explain management and businesses in his own words.

This commitment to investor relations was unusual for Japanese companies of that era. Many Japanese executives viewed investor communication as a distraction from the real work of running the business. Kanagawa saw it differently: transparent communication with investors built trust, reduced the cost of capital, and created a constituency of long-term shareholders who understood and supported management's strategy.

Chihiro Kanagawa, who passed away on January 1 this year, served as President of Shin-Etsu Chemicals from August 1990 and oversaw an impressive expansion of the business, bringing substantial increases to its sales, profits, and market value. While maintaining the core task of consolidating and further growing existing business areas, Kanagawa believed that developing new areas of business was essential for the sustained growth of the organization. To that end, he set up in 1991 the Z Committee, a body for new product development, with himself as the chair. Considerable resources were channeled through this body to the research of new business areas.

The Z Committee exemplified Kanagawa's approach to innovation. Rather than delegating new business development to middle managers, he personally led the effort. This ensured that new initiatives received adequate resources and attention, and that promising ideas weren't killed by organizational resistance to change.

It is with great sadness that Shin-Etsu Chemical announced the passing of Chihiro Kanagawa, Chairman of the Company. Mr. Kanagawa passed away on January 1, 2023 because of pneumonia. He was 96 years old, having been born in March 1926—the same year Shin-Etsu was founded.

President Yasuhiko Saitoh stated: "Mr. Kanagawa propelled Shin-Etsu Chemical to growth and developed it into a global chemical company during his tenure as president. During that time, he also went out of his way to instill the company with his management method, 'Kanagawa Management.' I myself have been fortunate enough to work under him for many years. The experience and way of thinking I gained in those years form the backbone of my work. Without his management, Shin-Etsu Chemical would not have been what it is today."

VI. The Silicon Wafer Revolution: From Commodity to Dominance

Shin-Etsu was first in the world to produce 300mm wafers commercially and is the world market leader in wafers of all sizes. Shin-Etsu Chemical has become the manufacturer holding the world's top market share in a number of key fields.

This simple statement—first in the world to produce 300mm wafers commercially—represents one of the most consequential bets in semiconductor history. With the arrival of the era of full-scale mass production of 300mm wafers, customers' expectations of silicon wafers are increasingly high. As a pioneer in the world silicon market, Shin-Etsu Handotai (SEH) took the head start of the mass production of 300mm and has established a system ensuring a stable supply to the market. They have responded to the growing market demand in a timely manner with their capacity expansions since the starting of the mass production in February 2001.

To understand why 300mm wafers mattered, one must understand the economics of semiconductor manufacturing. Silicon wafers are the substrate on which chips are fabricated. A larger wafer means more chips per batch, spreading the enormous fixed costs of fab operation across more units. The transition from 200mm to 300mm wafers effectively doubled the usable area per wafer, offering dramatic cost reductions for manufacturers who could make the transition.

But the transition was not simple. Larger wafers are harder to manufacture with the extreme precision required for advanced semiconductors. They're harder to handle without introducing defects. They require new equipment, new processes, and new quality control systems. Many wafer manufacturers hesitated, unsure whether the industry would actually make the transition.

SEH began commercially producing 300mm silicon wafers in February 2001 and had increased capacity to 200,000 wafers per month by March of this year. Between March and December, capacity was further increased to 300,000 wafers per month.

Shin-Etsu Handotai was the first company in the world to begin mass production of 300mm silicon wafers back in February 2001. Shin-Etsu Chemical continuously implemented further facility investment, expanding its production capacity to 300,000 monthly in 2004 and 400,000 monthly in 2005.

The scale of investment was staggering. By expanding production capacity through subsequent investments, including a $1 billion commitment announced in 2004, Shin-Etsu solidified its dominance in the silicon wafer market. This willingness to invest heavily during uncertain market conditions—when competitors were hesitating—cemented Shin-Etsu's leadership position.

As the world's leading company providing silicon wafers for integrated circuits, the Shin-Etsu Group continues be in the technological forefront with regard to cutting-edge large-diameter and super-flat wafers. They have succeeded ahead of others in the mass production of 300mm wafers and silicon-on-insulator (SOI) wafers that realize high speed and low power consumption, and are stably supplying these superior products. In addition to the company's high-precision single-crystal technology and high-level processing technology, their high-quality epitaxial growth technology for cutting-edge image sensor devices and their systems for product quality control and evaluation analysis are highly valued by customers around the world.

The technology behind semiconductor-grade silicon wafers is extraordinarily demanding. High purity silica rocks, which can be found only in select mines around the world, are reduced to silicon metal in a special furnace. From this silicon metal, polycrystalline silicon of 99.999999999% purity is created, and this is the raw material used by Shin-Etsu to fabricate semiconductor grade single-crystal silicon wafers. Special crystal growing methods are used to melt polycrystalline silicon and then convert to a large single-crystal round ingot, having perfect atomic structure. These crystals can be 300mm in diameter and longer than one meter. A silicon wafer is produced by slicing these ingots, followed by shaping and polishing processes. The final silicon wafer, which has extremely low levels of contamination and defects and surface particles is the "substrate" used to create many types of semiconductor devices.

That level of purity—eleven nines, meaning 99.999999999%—is almost incomprehensible. It means that for every trillion atoms in the silicon, only one can be an impurity. Achieving and maintaining such purity requires not just advanced equipment but deep process knowledge accumulated over decades.

In 1996, Shin-Etsu Chemical acquired Simcoa Operations Pty. Ltd. (Australia). This acquisition bolstered silicon raw material supply by securing a dedicated metallurgical silicon facility, ensuring stable inputs for high-purity products. Vertical integration—controlling the supply chain from raw metallurgical silicon to finished wafers—became a key competitive advantage.

By diameter, 300mm substrates commanded 63.1% of the semiconductor silicon wafer market share in 2024, while the market for logic devices is expected to advance at a 4.9% CAGR to 2030.

VII. The 2000s-2010s: Global Expansion & Consolidation

The new millennium brought continued geographic diversification as Shin-Etsu expanded its global manufacturing footprint.

Construction of the first phase of the Shintech Addis plant was completed in 2000, and the second in 2002. The company set up Asia Silicones Monomer Ltd. and Shin-Etsu Silicones Ltd. in Thailand during 2001 and in 2002, Shin-Etsu Chemical established Zhejiang Shin-Etsu High-Tech Chemical Co., Ltd in the Zhejiang Province of China for the production of silicon products.

The Thai and Chinese investments reflected a strategic response to shifting global manufacturing patterns. As electronics production migrated to Asia, Shin-Etsu followed, establishing silicone manufacturing close to where its customers were building products.

In 1999, a Dutch PVC business was purchased and Shin-Etsu PVC B.V. was established. In 2003, a Germany cellulose business was purchased. That year, Shin-Etsu Silicone International Trading (Shanghai) Co., Ltd. and SE Tylose GmbH & Co., KG were also established.

The European expansion served multiple purposes. The Dutch PVC acquisition gave Shin-Etsu a manufacturing base within the European Union, avoiding tariffs and positioning the company closer to European construction markets. The German cellulose acquisition added pharmaceutical-grade cellulose derivatives to Shin-Etsu's portfolio—a specialty chemical business with high margins and strong growth prospects.

In 2011, Shin-Etsu Magnetic Materials Vietnam Co., Ltd. and Shin-Etsu Electronics Materials Vietnam Co., Ltd. were established. Vietnam offered lower labor costs than established manufacturing centers, making it attractive for labor-intensive assembly and processing operations.

Since the 1960s, Shin-Etsu has expanded its business domains under the strategy of "only handling materials that cannot be surpassed by competitors worldwide," becoming what is often described today as a department store of world-leading products.

This "department store of world-leading products" strategy was the logical extension of Kanagawa's "selection and concentration" philosophy. Rather than being good at many things, Shin-Etsu aimed to be the best in the world at a carefully selected set of materials. The company would enter a market only if it believed it could achieve global leadership, and would exit if leadership proved unattainable.

As a result, Shin-Etsu has grown to become the No.1 silicone manufacturer in Japan and one of the leading firms worldwide.

In September 2018, Shin-Etsu Chemical announced plans to make ¥110 billion in facility investment in its silicones business. In July 2023, Shin-Etsu announced plans to enhance its high-performance silicones products and expand its line-up of eco-friendly products, making a large-scale investment of ¥100 billion.

These sustained investments—totaling hundreds of billions of yen over multiple years—reflect Shin-Etsu's continued commitment to the silicones business even as semiconductor silicon grabbed headlines. The company understood that its competitive advantage depended on being the scale leader in multiple product categories, not just one.

VIII. Recent History: The AI Boom & New Inflection Points

Riding the wave of global semiconductor demand expansion and the booming U.S. housing market in the early 2020s, Shin-Etsu Chemical's performance grew significantly. For the fiscal year ending March 2023, sales reached approximately ¥2.8 trillion and operating profit hit ¥999.7 billion, both record highs, with the operating profit margin approaching approximately 35%. Particularly, the PVC business achieved record profit contributions from 2022 to 2023 due to increased demand and soaring prices in the U.S., resulting in an exceptionally high segment operating profit margin that temporarily exceeded 40%. The semiconductor wafer business also progressed with stable shipments and price increases against a backdrop of supply shortages. However, entering 2024, a global semiconductor market adjustment and a reversal in PVC prices led to stagnation in some segments.

Shin-Etsu experienced a substantial growth in net sales over the period from 2005 to 2024, with an increase from approximately nine billion U.S. dollars in 2005 to approximately 15.99 billion U.S. dollars in 2024.

This revenue trajectory—nearly doubling over two decades—reflects both market growth and market share gains. In 2005, the net income of chemical company Shin-Etsu amounted to approximately 1.09 billion U.S. dollars. By 2024, the net income increased to roughly 3.5 billion U.S. dollars.

Some analysts point out that Shin-Etsu Chemical has become a target for overseas investors as a "winning player on the materials side," driven by increased demand for advanced logic semiconductors fueled by the AI boom. Indeed, as global investment in data centers for generative AI, including ChatGPT, expands, expectations are rising that demand for silicon wafers, a key semiconductor material supporting this growth, will regain momentum.

Driven by increasing demand for artificial intelligence (AI) technologies, Shin-Etsu Chemical expects a gradual rise in shipments of 12-inch silicon wafers. In contrast, demand for 8-inch wafers is expected to remain sluggish.

The divergence between 12-inch (300mm) and 8-inch (200mm) wafer demand reflects the structure of the semiconductor industry. Leading-edge AI chips—the GPUs and TPUs powering large language models—are fabricated on 300mm wafers using the most advanced process nodes. Older 200mm wafers serve legacy applications and mature-node chips. Shin-Etsu's early bet on 300mm technology positioned it perfectly for the AI boom.

With the expansion in Plaquemine, Shintech now has about 8 billion pounds of annual PVC capacity at plants in Texas and Louisiana. Demand growth led Shintech Inc. to add more than 900 million pounds of annual PVC resin capacity in Plaquemine, La. Shintech is the world's largest PVC maker. The firm is a unit of Shin-Etsu Chemical Co. Ltd. of Tokyo. Shintech entered U.S. PVC production in 1974 in Freeport.

Shin-Etsu holds a leading global market position in PVC as the No.1 producer, with the world's largest production capacity of approximately 4.44 million tons annually across facilities in Japan, the United States, and Europe. A new PVC facility in the US adding 400,000 tons/year started operations in fall 2024.

Shin-Etsu Chemical, the world's top producer of silicon wafers, plans to launch a semiconductor manufacturing equipment business, as the Japanese company expands its core electronics material segment.

This move into semiconductor equipment represents a significant strategic expansion. For decades, Shin-Etsu has been a materials supplier to chipmakers. Now it aims to become an equipment supplier as well.

Shin-Etsu Chemical has developed equipment to manufacture semiconductor package substrates with a new manufacturing method subsequently to manufacturing micro-LED manufacturing system. The equipment is a high-performance processing equipment using excimer laser in which a dual damascene method, as is also used in the front end of semiconductor manufacturing process, is applied to package substrate manufacturing process (back end process). As a result, an interposer's functions are directly formed into a package substrate. This not only eliminates the need of an interposer, but also enables further microfabrication, where conventional manufacturing methods could not realize. It also reduces costs and capital investment as it does not require the photoresist process in package substrate manufacturing process.

At the time when Japan is strengthening the construction of its semiconductor supply chain, Japanese photoresist giant Shin-Etsu Chemical is building a chip material plant in Gunma Prefecture, Japan, which marks its first new domestic manufacturing base in Japan over the past 56 years. Shin-Etsu Chemical plans to invest approximately JPY 83 billion (USD 547 million) in Isesaki City, northern Tokyo, Gunma Prefecture, Japan to construct a factory covering an area of around 150,000 square meters, which is scheduled to be completed in 2026.

Shin-Etsu launched its photoresists business in 1997 and started production of the then-most cutting-edge KrF photoresists at its Naoetsu Plant in Niigata Prefecture, Japan. Since then, the company has successfully developed and commercialized a succession of semiconductor lithography materials such as photomask blanks, ArF photoresists, multilayer materials, extreme ultraviolet (EUV) resists and others. It established the second production base in Fukui Prefecture in 2016 and the third production base in Yunlin County in the western part of Taiwan in 2019. Demand for semiconductor lithography materials is growing as they are indispensable materials for the manufacture of cutting-edge semiconductors.

Public data shows that Shin-Etsu Chemical holds about 20% of the global photoresist market, especially in advanced product fields, where it aims to capture at least 40% market share.

Kanagawa's right-hand man overseeing finance and international operations has made the core principles of his leadership the continuation of the Kanagawa philosophy and agile adaptation to changing times. Mr. Saito himself stated, "Agile adaptation to societal changes is crucial. However, without a robust core foundation established in normal times, one risks merely running around without purpose." He advocates balancing adaptability with strengthening the business foundation. He also states, "A company needs resilience and strength to withstand fierce storms."

IX. Business Model Deep Dive: The "Department Store of World-Leading Products"

Shin-Etsu Chemical manufactures numerous products that command large shares of their respective global markets, including PVC, silicones, semiconductor silicon, synthetic quartz and cellulose derivatives. It is the company's policy to avoid over dependence on any one product line and to strengthen diversified, individual lines of business. This portfolio approach continues to be one of the company's strengths.

Shin-Etsu Chemical Co., Ltd. is a chemical group organized around 3 product families: chemical products (52.8% of net sales) including polyvinyl chloride, silicones, methanol, methane chloride, cellulose derivatives, caustic soda, silicon, etc.; materials for electronic products (40.7%) including encapsulation materials made with silicone, resins, adhesives, etc. for semiconductors, LED products, etc.; and other (6.5%). Net sales break down geographically as follows: Japan (26.1%), Asia (34.2%), the United States (22.9%), Europe (10.2%) and other (6.6%).

This revenue breakdown reveals several important characteristics. First, Shin-Etsu is genuinely diversified—neither the infrastructure materials business (led by PVC) nor the electronics materials business (led by silicon wafers) dominates to the point of creating dangerous concentration. Second, the company is genuinely global—with less than a third of sales in Japan and significant presence in Asia, America, and Europe. Third, the "other" segment at 6.5% suggests disciplined portfolio management; the company isn't chasing marginal businesses.

The three largest subsidiaries in terms of total sales are Shin-Etsu Handotai Co., Ltd., making semiconductor silicon wafers, Shintech Inc., the largest PVC producer in the world, and Shin-Etsu Polymer Co., Ltd., producing silicone rubber and PVC products.

Shin-Etsu Chemical's overwhelming strength lies in its world-class technological capabilities and vertically integrated manufacturing system, which competitors find difficult to match across various fields.

The vertical integration is key. In PVC, Shin-Etsu controls everything from raw salt and ethylene procurement to finished resin production. In silicon wafers, the company controls from metallurgical silicon refining to polished wafer finishing. This integration provides cost advantages (no intermediary margins), supply security (less dependence on external suppliers), and quality control (end-to-end process visibility).

Shin-Etsu Chemical produces its own supply of metallurgical silicon, the primary raw material of silicones.

Shin-Etsu Silicone is totally committed to meeting the needs of customers. Customers have the choice of around 5,000 different kinds of high-performance silicone products to meet their needs, as they are suited to be used in various fields such as electrical, electronics, automotive, machines, chemical, textile, food, and construction.

Five thousand products is an extraordinary breadth. It reflects decades of application engineering—working with customers to develop specialized silicone formulations for specific uses. Each custom formulation creates switching costs: once a customer has qualified a Shin-Etsu silicone for their production process, switching to a competitor requires requalification, testing, and potential production disruption.

X. Competitive Positioning: Porter's Five Forces & Strategic Moats

Industry Structure Analysis

The semiconductor materials industry exhibits characteristics that favor incumbent suppliers with scale, technology, and customer relationships.

Barriers to Entry: Extremely high. Building a semiconductor-grade silicon wafer facility requires billions of dollars in capital, years of process development, and customer qualification cycles that can extend for 12-24 months. New entrants face not just capital barriers but knowledge barriers—the tacit process expertise accumulated over decades.

Supplier Power: Moderate. Raw material inputs (metallurgical silicon, specialty chemicals) come from multiple sources, and Shin-Etsu's vertical integration into metallurgical silicon production reduces supplier dependence.

Customer Power: Moderate to high. Shin-Etsu's customers include the world's most sophisticated semiconductor manufacturers—TSMC, Intel, Samsung—who possess significant purchasing power and technical expertise. However, switching costs are substantial, and qualification requirements create stickiness.

Threat of Substitutes: Low for silicon wafers in most applications. While compound semiconductors (gallium arsenide, silicon carbide, gallium nitride) serve specialized applications, silicon remains the workhorse material for digital logic and memory. Shin-Etsu's QST substrates are currently being evaluated by many Japanese and international customers for applications such as power devices, high-frequency devices, and LED devices. They are currently in the development phase for practical applications to address the recently increasing interest in AI data center power supplies.

Competitive Rivalry: Concentrated but intense. Three incumbent suppliers—Shin-Etsu Chemical, SUMCO, and GlobalWafers—command roughly 70% of worldwide capacity. This oligopolistic structure limits destructive price competition, but competitors invest aggressively in capacity and technology.

Hamilton Helmer's 7 Powers Analysis

Shin-Etsu's competitive position can be analyzed through the lens of Hamilton Helmer's framework:

Scale Economies: Strong. Wafer manufacturing exhibits significant fixed costs (cleanroom facilities, crystal-growing equipment) spread across variable production. Shin-Etsu's market-leading scale provides cost advantages that smaller competitors cannot match.

Network Effects: Weak. Materials businesses typically don't exhibit network effects—a wafer's value doesn't increase because other customers use the same wafers.

Counter-Positioning: Moderate. Shin-Etsu's integrated manufacturing model differs from competitors who rely more heavily on outsourcing. New entrants would find it difficult to replicate this integration without cannibalizing existing supplier relationships.

Switching Costs: Strong. Semiconductor manufacturers face significant qualification costs when changing wafer suppliers. Each supplier's wafers have subtly different characteristics; switching requires revalidation of manufacturing processes.

Branding: Weak in the traditional sense, but strong in the B2B context. Shin-Etsu's reputation for quality and reliability functions as a form of brand equity among semiconductor manufacturers.

Cornered Resource: Moderate. Process knowledge accumulated over decades constitutes a cornered resource that cannot be easily acquired or replicated. Additionally, Shin-Etsu's ownership of metallurgical silicon production (including Australian assets) provides raw material security.

Process Power: Very strong. The core moat. Shin-Etsu's ability to produce silicon wafers with extreme purity and consistency reflects embedded process knowledge that took decades to develop. This knowledge is tacit, distributed across the organization, and difficult for competitors to replicate.

Myth vs. Reality

Myth: Semiconductor materials are a commodity business with thin margins. Reality: Shin-Etsu's operating margins approaching 35% in peak years demonstrate that materials excellence commands premium pricing. The "commodity" label applies only to low-quality, undifferentiated producers.

Myth: AI will reduce demand for silicon as computing moves to specialized accelerators. Reality: AI accelerators are fabricated on silicon wafers. The AI boom has increased demand for advanced 300mm wafers suitable for leading-edge process nodes.

Myth: Geographic diversification in semiconductor manufacturing will hurt Japanese suppliers. Reality: Shin-Etsu's global footprint—with significant operations in the U.S., Europe, and Asia—positions it to serve semiconductor fabs regardless of their location.

XI. Key Risks, Regulatory Considerations & ESG Factors

Regulatory and Environmental Considerations

Shin-Etsu is responsible for placing at least five persistent chemicals on the US/EU market, including several PFAS substances. The risks linked to these "forever chemicals" are becoming increasingly clear, not only for human health and the environment, but also for companies and their shareholders. The regulatory tightening, high-profile lawsuits, and rising consumer awareness make business models based on persistent chemicals increasingly risky.

PFAS (per- and polyfluoroalkyl substances) regulation represents a potential headwind. These "forever chemicals" are used in various industrial applications, and increasing regulatory scrutiny could require reformulation of some products or increased compliance costs.

The European Union's 2024 revision to Regulation (EU) 2024/573 schedules a phase-down of hydrofluorocarbon usage by 90% before 2045. Many EUV photoresists now employ perfluorinated photoacid generators and solvents, which are subject to registration, evaluation, and authorization. Compliance requires analytical verification of impurity levels below 1 ppb, which drives up quality-control costs and forces formulators to test alternative chemistries that may risk lower performance.

Geopolitical Risks

Japanese suppliers JSR, Tokyo Ohka Kogyo, and Shin-Etsu Chemical together supply more than 70% of advanced EUV-grade resists. U.S. export-control updates in 2025 extended licensing to specialized photo-acid generators critical for sub-10 nm patterning, constraining Chinese foundries. Although China funds domestic producers, such as Beijing Kehua New Chemical, the technology gap remains five years or more.

Shin-Etsu's concentration in Japan for advanced photoresist production creates both opportunity and risk. On one hand, the company benefits from Japanese export controls that limit Chinese access to cutting-edge materials. On the other hand, geopolitical tensions could disrupt supply chains or invite retaliation.

Currency Exposure

With over 70% of sales outside Japan, Shin-Etsu faces significant currency translation effects. Yen weakness has been a tailwind in recent years, flattering dollar-denominated revenue growth. Yen strength would have the opposite effect.

Cyclicality

Both PVC and semiconductor silicon are cyclical businesses. PVC demand tracks construction activity, which correlates with housing starts and infrastructure spending. Semiconductor silicon demand tracks the semiconductor cycle, which has historically exhibited boom-bust patterns. Shin-Etsu's diversification across both businesses provides some offsetting, but neither is immune to broader economic downturns.

XII. Investment Considerations & Key Metrics to Watch

Key Performance Indicators

For investors tracking Shin-Etsu's ongoing performance, three metrics stand out as most important:

-

Silicon Wafer Capacity Utilization & Pricing: The semiconductor silicon business accounts for a significant portion of profits. Tracking capacity utilization at Shin-Etsu Handotai and comparing wafer pricing trends (available through industry reports from SEMI) provides leading indicators of segment performance. Semiconductor silicon is expected to experience persistent chronic supply shortages due to increased semiconductor demand driven by the expansion of AI, autonomous driving, and IoT. Wafer manufacturers like Shin-Etsu Chemical and SUMCO are planning production expansion investments worth hundreds of billions of yen beyond 2024.

-

Shintech PVC Volume & Margins: Shintech's performance drives the infrastructure materials segment. U.S. housing starts, PVC pricing indices, and ethylene feedstock costs provide context for Shintech's likely profitability. The "full production, full sales" philosophy means volume should remain high, but margin expansion depends on pricing relative to feedstock costs.

-

Photoresist Revenue Growth: As the company's stated goal is to capture 40% of the advanced photoresist market, tracking revenue growth in this segment indicates progress toward that objective. Growth above the industry average would signal market share gains.

Bull Case

The bull case for Shin-Etsu rests on structural tailwinds in semiconductor demand and continued execution of the proven playbook:

- AI-driven semiconductor demand accelerates, tightening the silicon wafer market and supporting pricing power

- The new Gunma photoresist facility comes online in 2026, expanding capacity just as EUV adoption accelerates

- Shintech maintains cost leadership in PVC, gaining share as marginal competitors exit

- The semiconductor equipment business achieves commercial traction, opening a new growth vector

- Capital allocation remains disciplined, with buybacks and dividends returning cash to shareholders

While the stock price temporarily adjusted in 2023 due to concerns over a global economic slowdown, it resumed an upward trend from 2024 onward. This was largely supported not only by a rebound in semiconductor-related stocks overall but also by Shin-Etsu Chemical's own share buyback program and its decision to increase dividends.

Bear Case

The bear case focuses on cyclical and structural risks:

- Semiconductor inventory correction extends longer than expected, pressuring wafer volumes and pricing

- U.S. housing market weakens significantly, reducing PVC demand and Shintech profitability

- Chinese wafer manufacturers achieve technology parity faster than expected, intensifying competition

- PFAS regulation forces costly reformulation or product exits in the silicones and photoresist businesses

- Yen strengthens significantly, reversing currency tailwinds

Valuation Context

Shin-Etsu trades at a premium to Japanese chemical peers, reflecting its superior profitability and market positions. The premium appears justified given the company's track record, but leaves less room for multiple expansion. Future returns will likely depend more on earnings growth than on valuation re-rating.

XIII. Conclusion: The Quiet Empire

Nearly a century after Juzaburo Koto brought together Nagano's water and Niigata's limestone, Shin-Etsu Chemical stands as one of the world's most important companies that most people have never heard of. Its materials enable the technologies that define modern life—the chips in our phones, the pipes that carry our water, the silicones in our cosmetics and medical devices.

The company's success reflects a distinctive approach to business: patient capital, methodical expansion, relentless focus on operational excellence, and the discipline to pursue only businesses where world leadership is achievable. Chihiro Kanagawa's management philosophy—selection and concentration, pragmatism over rankings, lean operations, and transparent communication—created a culture that survived his passing and continues to guide the company today.

As AI reshapes the semiconductor industry and creates new demands for ever-more-advanced materials, Shin-Etsu is positioned at the foundation layer. The company that mastered silicon chemistry seventy years ago now supplies the wafers on which the world's most advanced AI chips are built. The photoresists that pattern those chips, the silicones that protect them, the PVC pipes that provide infrastructure—all flow from the same source.

For investors, Shin-Etsu offers exposure to structural growth themes (AI, semiconductor demand, global infrastructure) through a company with proven management, strong competitive positions, and disciplined capital allocation. The risks are real—cyclicality, currency, regulation—but the track record of navigating such challenges spans decades.

The invisible empire continues to grow, one wafer, one pipe, one silicone formulation at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube