Costco: The $400 Billion Warehouse Revolution

I. Introduction & Cold Open

Picture this: It's a sweltering July afternoon in 2018, and Craig Jelinek, Costco's CEO, is sitting across from his CFO in the company's modest Issaquah headquarters. The CFO slides a spreadsheet across the table showing projected margins if they raise the price of their famous hot dog combo from $1.50 to $1.75. It's been the same price since 1985—thirty-three years without a single penny increase. Jelinek doesn't even look at the numbers. "If you raise the price of the fucking hot dog, I will kill you," he says, echoing the exact words his predecessor Jim Sinegal once told him. The CFO laughs nervously, then realizes his boss isn't joking. The price stays at $1.50.

This moment encapsulates everything about Costco: a $268 billion revenue giant that operates by principles so counter-intuitive they sound like business school satire. They charge customers money just to walk through their doors. They deliberately limit their profit margins. They sell $200 million diamond rings next to $4.99 rotisserie chickens. And somehow, this bizarre formula has created the world's third-largest retailer, with a market cap north of $400 billion.

How did a company that breaks every retail rule become one of the most successful businesses in history? The answer lies not in Silicon Valley disruption or Wall Street financial engineering, but in the radical ideas of a lawyer-turned-retailer named Sol Price and his protégé Jim Sinegal, who understood something fundamental: if you align the interests of customers, employees, and shareholders—truly align them, not just say it in annual reports—you create something nearly indestructible.

This is the story of how two men built a retail empire on the revolutionary idea that making less money could actually make you more valuable. It's about treasure hunts in warehouses, billion-dollar private labels, and why 129 million people worldwide pay for the privilege of buying toilet paper in bulk. Most importantly, it's about how culture, not strategy, became the ultimate competitive moat in American business.

II. The Sol Price Genesis: Inventing the Warehouse Club (1954-1976)

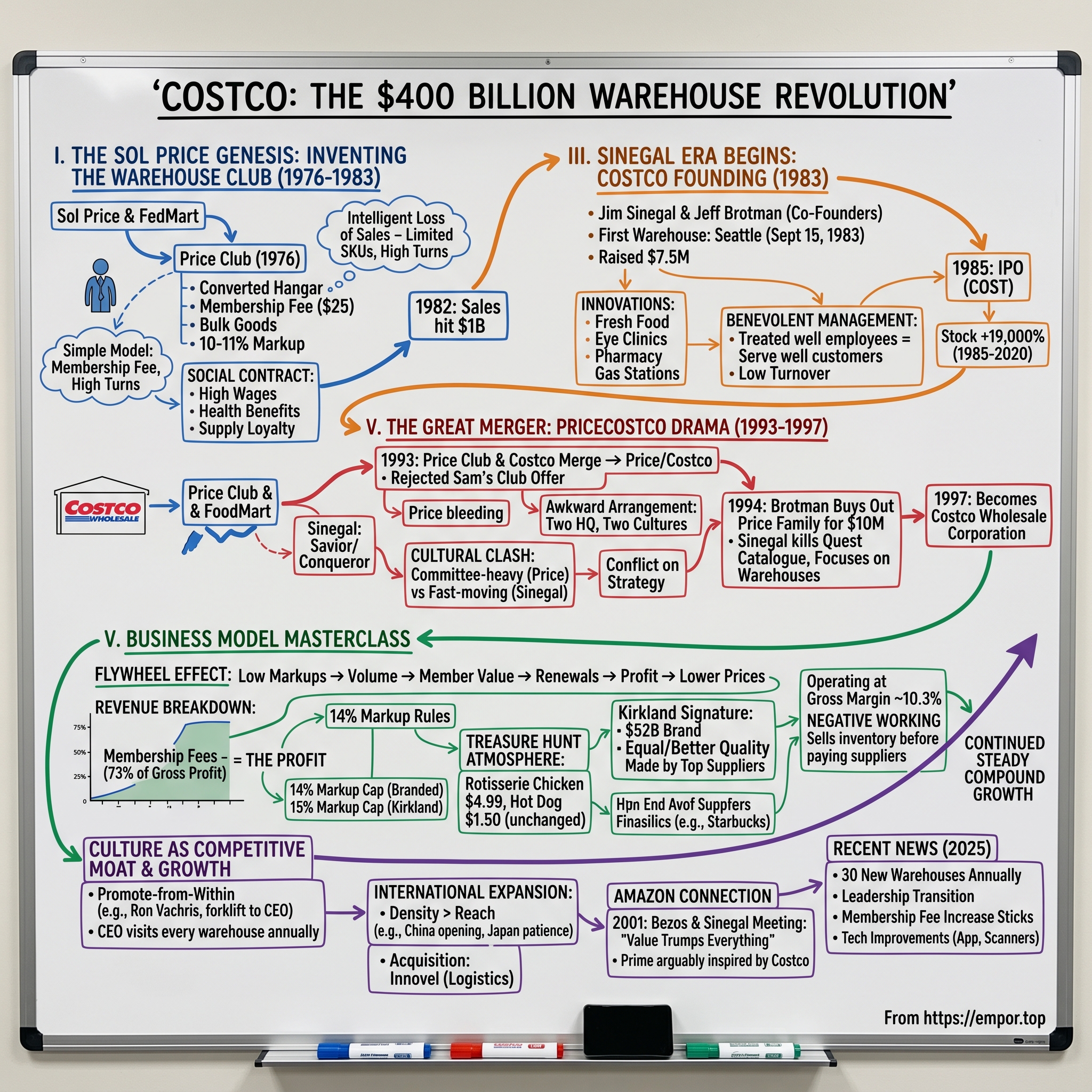

Sol Price didn't set out to revolutionize retail. In 1954, he was just a San Diego lawyer who'd inherited a small jewelry store from his client's estate and had no idea what to do with it. Standing in the empty store, Price had what would become his first counter-intuitive insight: instead of selling to everyone, what if he sold only to government employees? He could verify their employment, offer them special prices, and build loyalty through exclusivity. He called it FedMart, and within a decade, it would grow to a $350 million business.

But FedMart was just the laboratory. The real revolution began in 1976, in a converted airplane hangar in San Diego's industrial Morena Boulevard district. Price, now 60 and fresh off being unceremoniously ousted from FedMart by its German acquirer Hugo Mann, was angry and determined. He gathered his former lieutenants—including a young warehouse manager named Jim Sinegal who'd started as a bagger earning $1.25 an hour—and pitched them something audacious: Price Club.

The concept was so radical that Price's own son Lawrence thought his father had lost his mind. "Dad, you want people to pay money before they can spend money?" The model was simple but unprecedented: charge an annual membership fee (initially $25 for businesses, later $10 for individuals), operate out of no-frills warehouses, sell in bulk quantities, and mark up products by only 10-11%. Traditional retailers marked up 25-50%. Department stores went even higher.

Price's genius wasn't just the membership fee—it was understanding the psychology it created. When customers paid to shop, they felt invested. They shopped more frequently to justify the fee. They brought friends, creating viral growth before anyone used that term. And most brilliantly, the membership fees meant Price Club could sell products at near-cost and still be profitable. The fees were pure margin.

Jim Sinegal, who would later say "I learned everything from Sol Price," watched his mentor obsess over details that seemed insignificant. Price would spend hours debating the optimal height for merchandise pallets (low enough for customers to reach, high enough to hold volume). He instituted the "intelligent loss of sales" principle—deliberately stocking limited SKUs to increase inventory turns and reduce complexity. Where a supermarket might stock 50 types of ketchup, Price Club would stock one or two.

The early days were brutal. The first Price Club lost money for three years. Suppliers refused to sell to them, seeing the model as a threat to traditional retail. Procter & Gamble wouldn't even return their calls. Price had to buy merchandise from intermediaries at higher prices, eroding already thin margins. Local retailers filed lawsuits claiming unfair competition. The City of San Diego tried to zone them out of existence.

But Price had something more powerful than deep pockets: an almost religious belief in what he called "the intelligent loss of sales." By saying no to complexity, no to extensive product lines, no to fancy stores, Price Club could say yes to value. And slowly, customers began to understand. By 1980, Price Club had four locations and was profitable. By 1982, sales hit $1 billion.

The warehouse club wasn't just a new retail format—it was a new social contract. Price believed businesses had obligations beyond shareholders. He paid wages 50% above retail norms, offered health benefits when few retailers did, and promoted almost exclusively from within. "If you pay people well and treat them with respect," Price would say, "they'll move mountains for you." This wasn't feel-good management speak. It was cold, hard business logic: lower turnover meant lower training costs, experienced employees meant better operations, and committed workers meant better customer service.

Price's philosophy extended to suppliers too. While other retailers squeezed vendors for every penny, Price Club paid promptly and fairly. They might drive hard bargains, but they honored their commitments. When a small supplier faced bankruptcy, Price would sometimes prepay orders to keep them afloat. This created fierce loyalty—suppliers would offer Price Club exclusive products and first access to deals.

Perhaps most remarkably, Sol Price understood something about American consumers that others missed: they didn't just want low prices, they wanted to feel smart about shopping. The membership fee wasn't a barrier—it was a badge of intelligence. Shopping at Price Club meant you were savvy enough to pay upfront for long-term savings. The treasure hunt atmosphere, where premium products appeared randomly at shocking prices, made shopping feel like winning.

By 1983, when Sinegal left to start Costco, Price Club had become a phenomenon. But Sol Price's greatest contribution wasn't the company he built—it was the blueprint he created and the disciples he trained. Sinegal would later say, "Sol taught me that this wasn't about being a retailer. It was about being a fiduciary for our members." That distinction would drive everything that came next.

III. The Sinegal Era Begins: Costco's Founding (1976-1983)

Jim Sinegal stood in a half-empty Seattle warehouse on September 15, 1983, watching forklifts arrange pallets of toilet paper and canned goods. At 47, he'd spent three decades learning retail from Sol Price, rising from a $1.25-an-hour bagger to executive vice president. Now, with his new partner Jeff Brotman—a Seattle lawyer-turned-entrepreneur who'd made his first fortune selling women's jeans—Sinegal was launching his own version of the warehouse club dream. Together with Seattle retailer Jeff Brotman, he co-founded Costco, opening the first Costco warehouse in Seattle on September 15, 1983.

The partnership itself was unlikely. The idea to start Costco came after a trip to France, where Brotman saw a hypermarket that combined a discount grocery store with a department store. At the time, his father encouraged him to look at Price Club in California. With those ideas in mind, Brotman sought out Jim Sinegal, who already had a reputation in the wholesale club business, to join him. When they met in 1982, the chemistry was instant. "We hit it off immediately," says Sinegal. Brotman brought Seattle connections, real estate expertise, and crucially, access to capital. Sinegal brought three decades of warehouse retail experience and Sol Price's playbook burned into his DNA.

Their division of labor was clean: Sinegal would handle operations and merchandising—the guts of the business. Brotman would manage real estate, expansion strategy, and investor relations. They first financed the new operation with their own money. Then Brotman made the rounds of friends and acquaintances with a three-ring binder full of pictures and details, raising $7.5 million to open the first three stores. That was in 1983.

But Costco wasn't just a Price Club clone. From day one, Sinegal implemented innovations that would distinguish it from his mentor's creation. Sinegal's innovations made Costco the first "warehouse club" to include fresh food, eye-care clinics, pharmacies, and gas stations in its mix of goods and services. While Price Club focused primarily on small businesses, Sinegal saw opportunity in a broader market—families who would buy bulk if the value proposition was compelling enough.

The fresh food decision was particularly radical. Conventional wisdom said perishables and warehouse clubs didn't mix—too much spoilage, too complex to manage. But Sinegal understood that fresh food drove frequency. If members came weekly for milk and produce instead of monthly for paper goods, the entire business model strengthened. It required massive investment in refrigeration and more sophisticated logistics, but it would become one of Costco's defining advantages.

Sinegal is known for a benevolent style of management rooted in the belief that employees who are treated well will in turn treat and serve customers well. Sinegal, through Costco, provided his employees — at every level of the company, including the stores — compensation and benefits that are much higher than retail industry norms. For example, over 90% of Costco employees qualify for employer-sponsored health insurance; the US retail industry average is just under 60%. As a result, Costco has one of the lowest employee turnover rates in retail.

This wasn't altruism—it was arithmetic. Sinegal would pull out a napkin and demonstrate the math to anyone who'd listen: if you pay $20 an hour instead of $12, but your turnover drops from 50% to 10%, you save more in training costs than you spend in wages. Add in the productivity gains from experienced workers, the customer service improvements, and the reduced shrinkage, and generous compensation became a competitive weapon.

The early months were brutal. Seattle in 1983 was Boeing country, not retail innovation territory. The first Costco lost money daily. Suppliers remained skeptical—why would Procter & Gamble care about three warehouses in the Pacific Northwest when they already had relationships with Price Club? Local grocers viewed them as an existential threat and lobbied for zoning restrictions. The Seattle Times ran skeptical articles about whether consumers really wanted to buy mayonnaise by the gallon.

But Sinegal had learned patience from Price. He knew the model needed time to prove itself. By early 1984, something shifted. Word-of-mouth kicked in. Small business owners discovered they could buy office supplies at 30% less than traditional suppliers. Families realized that despite the membership fee, they saved hundreds of dollars annually. The treasure hunt mentality—where premium products appeared randomly at shocking discounts—created an almost addictive shopping experience.

Mr. Brotman and Sinegal opened the first Costco warehouse in Seattle in 1983. "On occasion, you will see a store run a loss-leader, where it reflects the same price as ours. But day after day, you can't find cheaper prices than here," Mr. Brotman said in a 1983 Seattle Times story about the then-new warehouse store and its strategy.

By December 1983, they'd opened locations in Portland and Spokane. The expansion was strategic—stay regional, perfect the model, build density before going national. This contrasted with other warehouse clubs that expanded rapidly and thinly. Sinegal wanted every new warehouse within trucking distance of existing ones, creating logistics efficiencies and marketing synergies.

The philosophical differences with Sol Price began to emerge. Price believed in pure efficiency—minimal service, basic products, strictly business customers. Sinegal saw opportunity in selective complexity. Adding pharmacies meant dealing with insurance companies and regulations, but it drove member loyalty. Gas stations required massive capital investment, but they guaranteed weekly visits. Each addition was carefully calculated: would it strengthen the member relationship more than it complicated operations?

In an interview published in the Houston Chronicle on July 17, 2005, he told Steven Greenhouse that he did not care about Wall Street analysts who had criticized him for putting good treatment of employees and customers ahead of pleasing shareholders. Investors might want higher earnings, but Sinegal stated, "We want to build a company that will still be here 50 and 60 years from now".

This long-term thinking manifested in countless daily decisions. When a buyer found an incredible deal on Calvin Klein jeans—enough to sell them at $19.99 versus $50 retail—the traditional retail response would be to price at $39.99 and pocket the margin. Sinegal's response: price at $19.99, sell them in a week, and earn the member's trust forever. Short-term profit sacrificed for long-term loyalty.

The Kirkland Signature private label, launched in these early years, exemplified this philosophy. Named after Costco's new headquarters city, it wasn't positioned as a cheaper alternative but as equal or better quality at a better price. Sinegal would personally taste-test Kirkland wines against premium brands, refusing to launch until they won blind comparisons. This obsessive focus on quality would eventually make Kirkland a $52 billion brand—larger than Coca-Cola or Nike.

By 1985, just two years after founding, Costco was ready for the public markets. From 1985, when Costco went public, to 2020, the company's stock value increased 19,000%. But going public meant Wall Street scrutiny, quarterly earnings pressure, and analysts who couldn't understand why Costco wouldn't just raise prices or cut wages to boost margins. This tension between Wall Street's short-term demands and Sinegal's long-term vision would define the next chapter of Costco's story.

IV. The Great Merger: PriceCostco Drama (1993-1997)

The boardroom at Price Club's San Diego headquarters hummed with tension on a humid June morning in 1993. Robert E. Price, chairman and chief executive officer of San Diego-based Price, and Jim Sinegal, president and CEO of Kirkland, Wash.-based Costco, said the merger will create greater operating efficiencies, leading to lower prices for members. But behind the corporate speak lay a more complex reality: Price Club was bleeding. Same-store sales had dropped 6.4% in the previous quarter. Earnings were down 40%. The warehouse club industry Price's father Sol had invented was now eating his company alive.

The irony was exquisite. Sol Price had created the warehouse club concept in 1976. Now, seventeen years later, his greatest student—Jim Sinegal—sat across the table as both savior and conqueror. In 1993, Costco and Price Club agreed to merge operations after Price declined an offer from Walmart to merge Price Club with their warehouse store chain, Sam's Club. The decision to reject Sam Walton's overtures would prove fateful.

Price Co. and Costco Wholesale Corp. announced Friday they have merged into a new company called Price/Costco, with 206 membership warehouses in four countries and annual sales of more than $15 billion. Shares of the new company, the nation's largest membership-warehouse chain with 18 million members and 43,000 employees, started trading Friday on Nasdaq under the symbol PCCW at $19.50 a share.

The structure revealed the delicate power dynamics at play. The deal gave 48 percent ownership of the new company to Price shareholders and 52 percent to Costco shareholders. On paper, it looked like equals joining forces. Price Co. chief Robert E. Price, who becomes chairman of the merged company and Costco chief James D. Sinegal, who is the new president and chief executive officer. But everyone in the industry knew the truth: Costco had won.

Called a partial merger, the two companies would continue to operate their respective headquarters, with the bulk of domestic responsibility going to Costco and international business to be headed by Price. This awkward arrangement—two headquarters, two cultures, two visions—was a recipe for conflict. Robert Price, Sol's son, wanted to pursue real estate ventures and technology experiments like the Quest Electronic Catalogue. Sinegal wanted pure warehouse expansion, nothing fancy, just more locations executing the proven model.

The cultural clash was immediate and visceral. Price Club executives, accustomed to Sol Price's more deliberate, analytical approach, found themselves steamrolled by Costco's aggressive expansion mentality. Costco people, trained in Sinegal's fast-moving, instinct-driven culture, chafed at Price Club's committee-heavy decision-making. Meetings that should have taken hours stretched into days. Simple decisions became political negotiations.

By early 1994, the marriage was already fracturing. However, hopes that the merger would halt sales declines did not materialize, and by 1994 sales for stores open more than a year had fallen by 3 percent, with a corresponding drop in earnings. Despite the initial optimism that had greeted the merger, the two management sides had never reached agreement on many crucial issues. Board meetings devolved into shouting matches. Robert Price pushed for diversification; Sinegal demanded focus. The company operated with two headquarters, two strategies, and increasingly, two hostile camps.

The breaking point came in late 1994. Barely a year into PriceCostco's operations, Costco co-founder Jeffrey Brotman bought out his counterparts from the Price family—Sol and Robert Price—for $10 million. The amount was almost insulting—$10 million for the founders of the entire warehouse club industry. But the Prices were exhausted. Sol and Robert Price left just a year later in 1994 to launch a separate chain called Price Enterprises in Latin America and the Caribbean.

Apart from its commercial real estate, Price Enterprises took with it four warehouse locations; a 51 percent interest in the Quest catalogue; 51 percent of PriceCostco's Mexican partnership, which by then included nine stores; and 51 percent ownership of PriceCostco's international development projects in Central America, Australia, and New Zealand. Together, these assets represented less than 10 percent of PriceCostco's earnings.

With the Prices gone, Sinegal moved swiftly. Sinegal remained as president and CEO of PriceCostco, while his long-time partner, Jeffrey Brotman, took over as chairman. The pretense of equality vanished. This was now Costco's company in everything but name. Sinegal immediately killed the Quest catalogue system, consolidated operations to Kirkland, and refocused entirely on warehouse expansion.

The transformation was ruthless in its efficiency. Price Club locations were converted to Costco branding. Price Club's more experimental initiatives were shuttered. The real estate ventures were sold off. Within months, every trace of Price Club's independent identity began to disappear. It ditched the PriceCostco name, becoming Costco Wholesale Corporation in 1997.

Yet Sinegal never forgot what Sol Price had taught him. In private moments, he would acknowledge the tragedy of it all—the master pushed aside by his student, the inventor of an industry forced to watch someone else perfect it. When Sol Price died in 2009, Sinegal delivered a eulogy that brought the warehouse club industry to tears: "Sol Price was the smartest man I ever met. He taught me everything. The tragedy is that I had to use what he taught me to compete against him."

The numbers validated Sinegal's approach. Since absorbing Price Club back in 1993, Costco has grown store count +300% and sales dollars over +1000% in under 30 years. Just this past year, Costco continued opening new warehouses at a rapid pace while also crossing $200 billion in annual sales for the first time. What had been a merger of equals became Costco's launching pad for global dominance.

The PriceCostco drama offers a masterclass in merger dynamics. Two companies with identical business models but fundamentally different cultures attempted to unite. One was the innovative pioneer, now struggling with succession and strategy. The other was the aggressive imitator, hungry and focused. When they collided, only one could survive intact. The lesson was clear: in business, as in nature, the student eventually surpasses the master. But unlike nature, in business, the master has to watch it happen.

V. The Business Model Masterclass

Here's the simple math that Wall Street analysts can't wrap their heads around: Costco has to be lean because Brotman and Sinegal long ago established a rule that no branded item could be marked up more than 14% and no Kirkland Signature item may be marked up more than 15% over cost. According to the company's 2018 annual report, the average item in the store is only marked up 11%, compared to the 25%-50% often seen in retail. This isn't generosity—it's genius.

The mathematics are brutally elegant. For the three months ending May 7, 2023, Costco reported sales of $52.6 billion, revenue from membership fees of $1.04 billion, and operating expenses of $52 billion. Essentially, Costco earned a gross margin of 10.3%, meaning that 62% of its operating income was derived from membership fees, while the rest came from product sales. Put another way: Costco essentially breaks even on the products it sells. The membership fees are the profit.

This creates what venture capitalists would call a flywheel effect, though Sol Price was doing it before anyone coined the term. Low markups drive volume. Volume drives membership value. Membership value drives renewals. Renewals provide predictable profit. That profit funds even lower prices. The wheel spins faster.

Consider the psychology: when you pay $60 or $120 annually just to shop somewhere, you're pre-committed. You've already spent money, so you need to extract value. This isn't a customer relationship—it's a partnership. Members become evangelists because their economic interests align with Costco's success. The more they shop, the more they save, the more valuable their membership becomes.

The company runs very lean, with overhead costs at about 10% of revenue and profit margins at 2%. For example, Costco has no public relations department and buys no outside advertising. Why would they? Their 129 million members are their marketing department, each one a walking testimonial to the value proposition.

The treasure hunt atmosphere deserves its own Harvard Business School case study. In a 2017 speech in San Diego, Sinegal said "we have created a treasure-hunt atmosphere". By rotating inventory constantly and limiting selection to 3,700-4,000 SKUs (versus 140,000 at a typical Walmart Supercenter), Costco creates urgency. That $2,000 television might not be there next week. That designer handbag definitely won't be. This isn't just retail—it's gamification of shopping.

The 14% markup rule functions as a trust mechanism. When members know that Costco is contractually prevented from gouging them, even when they could, it builds institutional loyalty that transcends price. During COVID-19, when hand sanitizer was selling for $50 a bottle on Amazon, Costco kept their prices flat. They could have made billions in windfall profits. They chose trust instead.

But the crown jewel of this model is Kirkland Signature, now an $86 billion brand that ranks among the largest consumer brands globally. In 1995, Costco cofounder and former CEO Jim Sinegal, inspired by a Forbes article on branding, decided to create a single, unifying brand called Kirkland Signature, named for the Seattle suburb where Costco's original headquarters were located.

The Kirkland strategy is deceptively simple: take premium products, have them manufactured by top-tier suppliers, and sell them at 20% less than national brands. But it is known that Starbucks makes some Kirkland coffee, while Duracell, Huggies' parent Kimberly-Clark, and Ocean Spray also reportedly produce Kirkland items incognito. These aren't knockoffs—they're the same products in different packaging.

73% of Costco's gross profit comes from its membership fees. Membership fees make up 2% of revenue, yet contribute 73% of gross profit. This ratio is the key to understanding Costco's entire business model. They're not really a retailer—they're a membership club that happens to sell things.

The discipline required to maintain this model is extraordinary. Every buyer at Costco knows the markup rules are inviolate. When suppliers offer special deals, the savings go to members, not Costco's bottom line. When costs rise, Costco eats the margin compression rather than breaking the 14% ceiling. This isn't corporate policy—it's corporate religion.

Wall Street has never understood this. Analysts regularly publish notes suggesting Costco could "unlock value" by raising markups just 1-2%. A 1% increase in price would translate into a 50% increase in Costco's net profits. But this misses the entire point. The moment Costco breaks the covenant, the magic dies. Trust, once broken, never fully returns.

The membership model also provides Costco with something invaluable: predictable cash flow. More than half of Costco memberships are at the highest executive tier, which is $130 a year membership fee, versus the standard tier, which is $65 a year. With renewal rates hovering around 90% in the U.S. and even higher for Executive members, Costco can predict its profit stream years in advance.

This predictability allows for long-term thinking that public companies rarely achieve. Costco can invest in infrastructure, technology, and employee development without worrying about quarterly earnings volatility. They can maintain prices on loss leaders like the $1.50 hot dog or the $4.99 rotisserie chicken because the membership fees provide the cushion.

The inventory turnover metrics reveal another layer of sophistication. So it takes them 27 days to sell a month's worth of procurement. And their suppliers are on net 30 payment terms. So Costco doesn't have to up front necessarily put up the money for the inventory that it's procuring. By the time it comes time to pay suppliers, they've already moved all of that inventory and product. Costco essentially operates on negative working capital—they sell products before they pay for them.

This model has proven so powerful that it's spawned imitators worldwide, from Sam's Club to BJ's Wholesale to China's Metro. But none have replicated Costco's cultural commitment to the model. Others raise markups when they can. Others cut employee benefits when times get tough. Others compromise on quality to boost margins. Costco never does.

The ultimate proof of the model's power? Investors who bought $10,000 of Costco stock in 1992 found it worth $43,564 just 10 years later — a return of 354% (15.855%, annually). From 1985, when Costco went public, to 2020, the company's stock value increased 19,000%. Those returns didn't come from financial engineering or aggressive accounting. They came from relentlessly executing a model that puts members first, employees second, and shareholders third—and paradoxically creates more value for shareholders than any "shareholder-first" retailer ever has.

VI. Culture as Competitive Moat

Ron Vachris became president and CEO Jan. 1, 2024 after starting as a forklift driver in 1982, taking a seasonal position with Price Club while on holiday break from studying business at Glendale Community College outside Phoenix. "I'm learning more here in real life than I am at school about business, so I just pursued this opportunity that I have with Price Club at the time," Vachris reflected. Forty-two years later, he runs a $268 billion company. This isn't a feel-good story—it's Costco's competitive weapon.

The promote-from-within philosophy isn't corporate propaganda; it's mathematical reality. "I'm not the exception; I really am not," Vachris emphasized. "Throughout the company, there's many like me; there's just only one CEO position, so I just happened to be in that one". Walk into any Costco warehouse and you'll find managers who started stocking shelves, buyers who began on cash registers, regional VPs who once drove forklifts. This creates institutional knowledge that money can't buy.

Jim Sinegal set the cultural template with an almost monastic devotion to the warehouses. As CEO, Sinegal was well known for traveling to each Costco location every year to inspect it personally. Not quarterly reviews with regional managers. Not video conferences. Physical presence in every single warehouse, every single year. He'd arrive unannounced, walk the floor, taste the samples, check the bathrooms, talk to hourly employees by name.

This wasn't theater. Sinegal could spot a pricing error from fifty feet away. He'd notice if the rotisserie chickens were slightly overcooked. He'd question why a particular SKU was placed at eye level versus knee level. After decades in warehouses, his pattern recognition was so refined that he could diagnose operational problems through subtle cues—the way merchandise was stacked, the flow of customer traffic, the energy level of employees.

Craig Jelinek, who succeeded Sinegal and served as CEO from 2012 to 2024, maintained this hands-on tradition. "Costco has a very strong culture and a deep bench of management talent," Jelinek said in a statement on Wednesday. "I have total confidence in Ron and feel that we are fortunate as a Company to have an executive of his caliber to succeed me". Under Jelinek's leadership, the company's warehouse count soaring from 617 to 861 and revenues more than doubling from $99 billion in 2012 to a staggering $242.3 billion in the recent fiscal year.

The cultural transmission mechanism works through apprenticeship, not MBA programs. Young managers are paired with veterans who've spent decades perfecting the Costco way. They learn that merchandise should be stacked to exact specifications—not for aesthetics, but because it affects picking efficiency. They discover that sample stations should be positioned to create traffic flow, not random placement. They understand why certain products are loss leaders and others are profit centers.

The employee compensation philosophy extends far beyond wages. Costco's health benefits kick in after 90 days for part-time workers—unheard of in retail. The company contributes to 401(k)s whether employees do or not. Dental and vision are included. Dependent coverage is affordable. These aren't perks—they're retention tools. When you invest thousands of dollars training someone to Costco standards, letting them leave over a few dollars an hour is economically irrational.

The numbers prove the model works. Over 90% of Costco employees qualify for employer-sponsored health insurance; the US retail industry average is just under 60%. As a result, Costco has one of the lowest employee turnover rates in retail. In 2006, Costco's turnover rate was 17% overall and 6% after one year of employment. Compare that to retail industry averages of 60-100% annually. Each percentage point of reduced turnover saves millions in training costs and productivity losses.

But the deeper cultural moat comes from shared mythology. Every Costco employee knows the story of the $1.50 hot dog. They know Sol Price paid employees well during recessions when competitors were cutting wages. They know Sinegal told Wall Street analysts to go to hell when they suggested cutting benefits. These stories aren't just history—they're behavioral scripts that guide decisions when nobody's watching.

The cultural immune system rejects foreign bodies immediately. When Costco has hired senior executives from other retailers, bringing "best practices" from traditional retail, they rarely last. The Costco way seems inefficient to outsiders—why have buyers personally inspect every shipment? Why maintain relationships with small suppliers who can barely fill one warehouse's needs? Why keep unprofitable items just because long-time members expect them?

The answer lies in compound trust. Every decision that prioritizes long-term relationships over short-term profit builds cultural capital. Suppliers know Costco won't squeeze them during tough times. Employees know their jobs are safe during recessions. Members know prices won't mysteriously increase before sales. This predictability creates efficiency that spreadsheets can't capture.

Wall Street has never understood this. "In an interview published in the Houston Chronicle on July 17, 2005, he told Steven Greenhouse that he did not care about Wall Street analysts who had criticized him for putting good treatment of employees and customers ahead of pleasing shareholders. Investors might want higher earnings, but Sinegal stated, 'We want to build a company that will still be here 50 and 60 years from now'".

The succession planning embodies this long-term thinking. In 2016, then-CEO Craig Jelinek asked Vachris to try something new again, overseeing buying for Costco, becoming executive vice president of merchandising and chief operating officer. Then in January 2022, he became president and COO, signaling the company's succession plans. He became president and CEO Jan. 1 after Jelinek's retirement. This wasn't a sudden decision—it was a six-year grooming process, ensuring cultural continuity.

The physical spaces reinforce cultural values. Costco's corporate headquarters in Issaquah, Washington, sits next to a working warehouse. Executives shop where members shop. They wait in the same lines. They eat the same $1.50 hot dogs. The CEO's office is famously modest—no marble lobbies, no executive dining rooms, no corporate jets. When you're selling value, you have to live it.

Even the famous sample stations serve a cultural purpose beyond sales. They're staffed by third-party vendors, but Costco treats them as family. Sample staff often work the same locations for years, knowing customers by name. They're brand ambassadors who happen to be serving teriyaki chicken. When COVID hit, Costco found ways to keep them employed even when samples were suspended. That's not charity—it's cultural preservation.

The "treasure hunt" atmosphere isn't just merchandising—it's cultural programming. Employees take pride in creating discoveries for members. Buyers compete to find the most amazing deals. Warehouse managers brag about their unique finds. This gamification makes routine retail work feel like a mission. You're not stocking shelves; you're creating joy.

Perhaps most remarkably, this culture scales. From Seoul to San Diego, from 17 warehouses to 861, the Costco way remains consistent. This isn't achieved through manuals or training videos, but through human transmission—each generation teaching the next, stories becoming legends, practices becoming rituals.

Like Costco's concrete and steel warehouses, there's nothing pretentious about Vachris; it's all about getting the job done — doing right by employees, members, suppliers, and shareholders as the company follows its simply stated mission: "To continually provide our members with quality goods and services at the lowest possible prices". This simplicity is deceptive. Any company can write a mission statement. Only Costco has built a culture that makes it mathematically impossible to violate that mission and remain employed.

The ultimate test of culture is crisis. During the 2008 financial crisis, when competitors were slashing jobs and benefits, Costco gave raises. During COVID, when price gouging could have generated billions in profit, Costco held prices flat. During supply chain chaos, when vendors couldn't deliver, Costco worked with them rather than finding replacements. Each crisis strengthened the culture rather than breaking it.

This is why Costco's culture is its ultimate moat. Competitors can copy the warehouse format. They can match the membership fees. They can attempt low markups. But they can't replicate forty years of compound cultural capital. They can't manufacture the trust that comes from never violating your principles. They can't create true believers through corporate mandate. Culture, unlike strategy, can't be reversed engineered.

VII. Scaling the Unscalable: Growth & International Expansion

When Costco rang the opening bell on NASDAQ on December 5, 1985, Jim Sinegal watched from Seattle as his company's stock opened at $10 per share. On December 5, 1985, Costco went public, opening on NASDAQ at a price of $10 per share; at the time, the company had 17 warehouses nationally and 1,950 employees. What happened next defied every rule of retail physics: Costco became the first company ever to grow from zero to $3 billion in sales in less than six years from its founding.

This wasn't just rapid growth—it was unprecedented velocity in an industry where established players like Sears and Kmart had taken decades to reach similar milestones. The secret wasn't technology or innovation in the traditional sense. It was the ruthless application of a simple formula: membership fees fund low prices, low prices drive volume, volume enables buying power, buying power lowers costs, lower costs enable lower prices. The flywheel, once spinning, became self-accelerating.

The early expansion followed a counterintuitive pattern. While competitors rushed to blanket the country with stores, Costco built density. After Seattle came Portland, then Spokane—creating a Pacific Northwest fortress before venturing beyond. This clustering strategy, learned from Sol Price, created operational leverage. One distribution center could serve multiple warehouses. Regional managers could visit all locations weekly. Marketing dollars went further when concentrated in a single media market.

International expansion began almost accidentally. Costco opens it's first Canadian warehouse in Burnaby, British Columbia in 1986, just three years after founding. The Canadian market proved perfect for the Costco model—affluent, suburban, and underserved by existing retailers. But instead of racing across Canada, Costco again chose density over reach, saturating British Columbia before moving east.

The real test came with Asia. The first Asia Costco opens in Seoul, Korea in 1994, followed by The first Taiwan Costco opens in Kaohsiung in 1997 and The first Japan warehouse opens in Hisayama in 1999. Each market required adaptation without abandoning core principles. In Japan, where customers expected immaculate presentation, Costco had to elevate its visual standards while maintaining the warehouse aesthetic. In Korea, where gift-giving culture dominated, Costco created elaborate gift sets that looked premium but maintained value pricing.

The Japan expansion nearly failed. Early stores struggled as Japanese consumers, accustomed to daily shopping for fresh items in small quantities, couldn't understand buying 48 rolls of toilet paper at once. Costco's response was patient education rather than radical change. They hosted warehouse tours explaining the economics. They provided freezer bags so customers could divide bulk purchases. They added more refrigerated sections for smaller apartment dwellers. Slowly, Japanese consumers began to understand that Costco wasn't asking them to change their lifestyle—just their shopping frequency.

By the numbers, the international expansion looked modest. Based in Issaquah, Washington, the company should end 2025 with 914 stores worldwide, with approximately 629 stores in the U.S. and Puerto Rico, 110 stores in Canada, 41 in Mexico, 29 in the United Kingdom, 37 in Japan, 14 in Taiwan, 19 in Korea, 15 in Australia, five in Spain, one in Iceland, one in New Zealand, and two in Sweden, two in France, and seven in China. But this geographic diversity provided crucial learnings that strengthened the entire system.

The China entry, beginning in 2014, represented the ultimate test of Costco's model. When the first Shanghai location opened in 2019, the response was so overwhelming that police had to shut it down on opening day. Videos of thousands of shoppers flooding the warehouse went viral globally. Costco had to implement appointment systems and traffic management that would have horrified Sol Price. But they held firm on the fundamental model: membership fees, low markups, quality products.

25 warehouses exceed annual sales of $200 million, with one warehouse that exceeded $300 million. These aren't stores—they're economic engines. The average Costco warehouse generates more revenue per square foot than almost any other retailer. This productivity enables the company to pay higher wages, invest in better infrastructure, and still maintain lower prices than competitors.

The technological evolution happened quietly. While Amazon was garnering headlines, Costco was building one of retail's most sophisticated supply chain systems. The company invested billions in distribution centers that could process millions of SKUs daily with minimal human intervention. They pioneered cross-docking systems that moved products from suppliers to stores without intermediate storage. They built proprietary inventory management systems that could predict demand patterns down to individual warehouse levels.

In November 1998, the company launched Costco Online, its online shopping site. But unlike other retailers who saw e-commerce as the future, Costco viewed it as complementary to the warehouse experience. Online sales were deliberately limited to items that made sense for shipping—no competing with the in-store treasure hunt. This restraint, mocked by digital evangelists, proved prescient. While pure e-commerce players struggle with profitability, Costco's hybrid model generates consistent returns.

The 2020 pandemic provided unexpected validation. Due to the COVID-19 pandemic, Costco's online sales increased dramatically, with more online sales growth in 2020 than the previous five years combined. But the real story was the warehouses. As restaurants closed and families ate at home, Costco's bulk model suddenly made perfect sense. Members who previously visited monthly came weekly. The average transaction size exploded. Costco had accidentally built the perfect pandemic retailer—a place to stock up efficiently and safely.

In March 2020, Costco announced the acquisition of Innovel, a logistics company, for one billion dollars. This wasn't just about delivery capability—it was about controlling the last mile for big and bulky items, the products that e-commerce struggles to deliver profitably. By owning the logistics, Costco could maintain its margin discipline while expanding into furniture, appliances, and other large-ticket items.

The financial returns have been staggering. Over the nearly 35-year time frame, Costco stock returned a compound annual growth rate (CAGR) of approximately 16.7%, excluding dividends. Over that same stretch, the S&P 500 generated annual returns of only about 8.3%. A $1,000 investment in Costco's IPO would be worth almost $223,000 today. These returns came not from financial engineering or aggressive accounting, but from relentlessly executing the same model year after year.

The international expansion strategy reveals Costco's true genius: they scale the unscalable by not trying to scale it. Each warehouse is essentially the same—same products, same layout, same hot dog price. But each market requires years of patient cultivation, relationship building with local suppliers, and subtle adaptations to local preferences. This combination of global standardization and local patience creates a moat that pure e-commerce can never replicate.

VIII. The Amazon Connection & Modern Competition

The scene at the Starbucks inside the Barnes & Noble near Amazon's Bellevue headquarters in 2001 was unremarkable—two middle-aged men in khakis talking over coffee. What made it extraordinary was the context: Jeff Bezos's company was dying. Back in 2001, its very survival was in doubt after the dot-com bubble burst and Amazon's stock dipped by 90 percent. Critics were writing obituaries. Wall Street had given up. And here was Bezos, learning from his competitor how to survive.

That year, Bezos met Sinegal for coffee at a Starbucks inside a Barnes & Noble near Amazon's offices in Bellevue, Washington, according to the 2013 book "The Everything Store," by journalist Brad Stone. Bezos wanted to talk about using Costco as a wholesale supplier for some products, but the meeting's key takeaway ended up involving pricing strategies.

What Sinegal explained wasn't revolutionary—it was fundamental. "The membership fee is a one-time pain, but it's reinforced every time customers walk in and see forty-seven-inch televisions that are two hundred dollars less than anyplace else," Sinegal told Bezos, according to Stone. "It reinforces the value of the concept. Customers know they will find really cheap stuff at Costco".

Costco's approach was that "value trumps everything," and it would always work hard to ensure it delivered enough value to keep customers happy, Sinegal emphasized. This wasn't just retail philosophy—it was a fundamental shift in how to think about customer relationships. Instead of extracting maximum value from each transaction, you could build a business on delivering maximum value in each transaction.

Bezos has never publicly credited the meeting with Sinegal for inspiring any of Amazon's pricing strategies, but Stone wrote that Bezos called a meeting at Amazon just a few days after sitting down with Sinegal. The Monday after that meeting, Bezos met with his senior managers and announced that Amazon.com would immediately be cutting prices of books, music, and videos by 20 to 30 percent. Later during a quarterly conference call with analysts, he observed, "There are two kinds of retailers: there are those folks who work to figure how to charge more, and there are companies that work to figure out how to charge less, and we are going to be the second, full-stop".

The transformation was immediate and brutal. Amazon slashed margins to the bone. They invested every penny of potential profit into lower prices and better service. Wall Street howled. But something remarkable happened: customers noticed. Sales began to accelerate. The flywheel that would power Amazon for the next two decades started spinning.

A few years later, in 2005, Amazon rolled out its own membership program, Amazon Prime, offering discounted prices and free shipping on orders for members who pay an upfront fee. The parallels to Costco were unmistakable. In a 2016 letter to Amazon's shareholders, Bezos described the idea behind Prime using language reminiscent of Sinegal and Costco: "We want Prime to be such a good value, you'd be irresponsible not to be a member".

Today, Prime has over 200 million members worldwide, generating more than $35 billion annually. But Prime isn't just a Costco clone—it's an evolution. Where Costco uses physical warehouses to create value through bulk purchasing, Amazon uses digital infrastructure to create value through convenience and selection. Where Costco limits SKUs to increase turns, Amazon offers infinite selection through marketplace sellers. Where Costco builds trust through consistent pricing, Amazon builds it through consistent delivery.

According to Sinegal, Bezos allegedly does the same thing with Costco. He even speculated that Amazon Prime may have been inspired by his company's membership model. The student had become a rival, but the respect remained mutual. In 2008, Costco founder Jim Sinegal bought a Kindle from Amazon with a defective screen. He was so impressed when the company immediately replaced it that he wrote to Amazon CEO Jeff Bezos to comment on the seamless customer service. He got a message in return from the man himself.

The irony is delicious. Sinegal taught Bezos the membership model that would help Amazon survive and thrive. But Costco's moat—its physical warehouses, its treasure hunt experience, its culture of restraint—proved unassailable. Amazon became a $2 trillion company. Costco continued growing at its steady, relentless pace. Both won by focusing on customer value over extraction.

The competitive dynamics reveal something profound about moats in the modern economy. Amazon couldn't replicate Costco's physical experience, culture, or economics. Costco couldn't match Amazon's convenience, selection, or technological infrastructure. Sam's Club, despite Walmart's resources, remains a distant second to Costco. BJ's Wholesale Club operates in the shadows. The warehouse club model, perfected by Sol Price and scaled by Jim Sinegal, resists disruption because it's not really about warehouses—it's about trust.

But he said that Costco has Amazon beat when it comes to across-the-board low prices, and sooner or later, Amazon shareholders are going to force a change. This prediction, made years ago, reveals Sinegal's understanding of the fundamental tension. Amazon must eventually choose between growth and profitability. Costco made that choice decades ago—profitability through membership fees, growth through value delivery.

The Sinegal-Bezos connection extended beyond direct competition. He led Starbucks through a turnaround during the 2008 financial crisis — relying on advice he now "vividly" remembers from Costco co-founder and former CEO Jim Sinegal, he wrote. "Howard, the cost of losing your core customers and trying to get them back during a down economy will be much greater than the cost of acquiring new customers," Sinegal said, according to Schultz. "[Sinegal's] sage gift became a core principle for us during that time of crisis, helping us emerge stronger as the headwinds died down," Schultz wrote.

This wisdom—that customer retention through value delivery beats customer acquisition through marketing—has become Silicon Valley orthodoxy. But Sinegal was practicing it when Bezos was still at D.E. Shaw and Schultz was selling coffee makers door-to-door. The principle predates the metrics, the software, the entire digital economy.

The modern competitive landscape validates both models. Costco operates 897 stores and generates $254 billion in revenue. Amazon generates over $500 billion. Both have market caps exceeding $400 billion. Both have transformed how Americans shop. Both have created enormous consumer surplus—the economic term for value delivered above price paid.

Yet the differences are telling. Amazon's margins have crept up over time as shareholder pressure mounts. AWS, not retail, drives most of Amazon's profits. Prime membership costs have more than doubled since launch. The company that committed to being the low-price leader increasingly relies on convenience and selection rather than price.

Costco, meanwhile, hasn't budged. The 14% markup rule remains inviolate. The hot dog still costs $1.50. Executive compensation remains modest by tech standards. The company still doesn't advertise. The membership fee increases come once per decade, not annually. The discipline that Sinegal instilled—that value delivery is the strategy, not a tactic—remains unchanged.

The ultimate lesson from the Sinegal-Bezos coffee isn't that one model is superior. It's that sustainable competitive advantages come from alignment, not tactics. Costco aligns every stakeholder—employees, members, suppliers, shareholders—around value delivery. Amazon aligns everything around customer convenience and selection. Both models work because they're internally consistent and rigorously executed.

But there's a deeper truth here. In teaching Bezos about value, Sinegal may have saved his biggest competitor. Without Amazon pushing the boundaries of convenience and selection, Costco might have grown complacent. Without Costco demonstrating the power of value and restraint, Amazon might have become extractive. The competition made both stronger.

Today's retail landscape would be unrecognizable without that 2001 coffee meeting. Prime exists because of Costco's membership model. Whole Foods 365 exists because of Kirkland Signature. Amazon's minimum wage increase followed Costco's example. The entire e-commerce industry learned that membership programs create stickiness and enable investment in customer value.

The paradox is perfect: Costco's greatest contribution to retail might be the competitor it helped create. And Amazon's greatest teacher might be the competitor it can never quite beat. In the end, customers won. Which, if you ask Jim Sinegal, was the point all along.

IX. Financial Analysis & Unit Economics

The numbers tell a story that Wall Street consistently misunderstands. For the 52-week fiscal year, the Company reported net sales of $249.6 billion, an increase of 5.0 percent from $237.7 billion reported in the 53-week fiscal year 2023. Add membership fees and total revenue hits $254 billion. But here's what matters: In its fiscal 2024, Costco had total operating income of $9.3 billion. Depending on how one looks at things, its membership fee revenue provided over half of this profit.

Let's dissect this mathematical miracle. Costco's membership fee revenue was $1.24 billion in Q3 2025, increasing from $1.123 billion in the same quarter last year. These fees have virtually zero marginal cost—no inventory to buy, no trucks to fuel, no warehouses to cool. It's nearly pure profit flowing straight to the bottom line. When you understand this, you realize Costco isn't really a retailer. It's a membership business that happens to sell things at cost.

The unit economics are breathtaking in their simplicity. The company had 137 million cardholders at the end of Q4, which was a 7% year-over-year increase. With membership fees now at $65 for basic and $130 for Executive (after the September 2024 increase), and renewal rates at 92.9% in the U.S. and Canada, Costco has essentially created an annuity stream worth approximately $5 billion annually.

Now consider the leverage. When combined with the operating efficiencies achieved by volume purchasing, efficient distribution and reduced handling of merchandise in no-frills, self-service warehouse facilities, these volumes and turnover enable us to operate profitably at significantly lower gross margins. The company operates at gross margins of roughly 10-11%, while competitors like Walmart operate at 24%. This isn't inefficiency—it's strategy.

The inventory turnover metrics reveal the operational excellence underneath. With approximately 12 inventory turns per year (versus 8-9 for Walmart), Costco sells its entire inventory every month. Combined with payment terms that allow them to pay suppliers after selling the goods, Costco operates with negative working capital. They're using supplier money to fund operations while generating returns on member fees.

In the fiscal fourth quarter of 2024, Costco reported a net income of $2.35 billion, or $5.29 per share, representing a 7% year-over-year increase. This figure surpassed analyst expectations, which had projected earnings per share (EPS) of $5.08. But focusing on quarterly earnings misses the point. Costco's real financial genius lies in its predictability.

The membership model creates remarkable earnings visibility. With over 50% being Executive members who pay $130 annually and get 2% cash back, these members are essentially pre-committing to spending thousands at Costco to justify the higher fee. The math is elegant: to earn back the extra $65 fee differential, Executive members need to spend $3,250 annually. Most spend far more, creating a virtuous cycle of loyalty and volume.

The recent membership fee increase—the first in seven years—demonstrates pricing power that most retailers can only dream of. Costco raised its membership fees for the first time in seven years, effective September 1, 2024. The annual fee for U.S. and Canada Gold Star individual members, Business members, and Business add-on members increased by $5 to $65, while Executive Memberships saw a $10 increase to $130. This change affects approximately 52 million memberships.

The market's reaction reveals its misunderstanding. Following the earnings report, Costco shares declined about 1% to $892.55 in extended trading. Analysts worried about revenue missing estimates by 0.3%. But this obsession with quarterly revenue variance ignores the structural advantages that matter. In its fiscal fourth quarter of 2024, its membership renewal rate for the U.S. and Canada was 92.9%. That's really high and virtually unchanged despite the fee increase.

The stock performance over time tells the real story. Costco's stock price closed at $901.79, reflecting a 6.09% increase over the last three months and a significant 63.66% rise over the past year. From IPO in 1985 to today, the stock has increased approximately 42,700%, crushing the S&P 500's 2,350% return over the same period. This isn't momentum—it's compound value creation.

E-commerce metrics reveal Costco's disciplined approach to digital. E-commerce sales grew 18.4% in the quarter compared with the year earlier, reaching approximately 15-16% growth annually. But unlike pure e-commerce players burning cash for growth, Costco's online business is profitable because it's integrated with the warehouse model. Buy online, pick up at warehouse. Order bulk items for delivery. The physical and digital reinforce rather than cannibalize each other.

The capital efficiency is remarkable. Costco operates 905 warehouses across 13 countries, including 624 in the United States and Puerto Rico. Each warehouse generates average annual sales exceeding $200 million, with some surpassing $300 million. The return on invested capital consistently exceeds 20%, a level most retailers never achieve even temporarily.

Total equity as of September 1, 2024, was $23.622 billion, down from $25.058 billion the previous year, primarily due to share buybacks and dividends. This isn't weakness—it's capital discipline. Why hold excess equity when the business generates such strong cash flows? Costco returns capital to shareholders while still funding 25-30 new warehouses annually.

The margin structure deserves deeper analysis. About 40% of sales are sundries (including candy, alcohol and tobacco); 14% fresh food; 26% non-food including hard-lines (such as electronics and appliances) and soft-lines (including apparel and jewelry); and 20% other ancillary businesses, including gas stations, pharmacy, optical, hearing aids and printing. Each category serves a different purpose—sundries drive frequency, fresh food creates habit, non-food provides margin, ancillary services deepen member value.

Gas stations exemplify the model's brilliance. Costco sells gas at razor-thin margins, sometimes at a loss. But gas drives weekly visits, increases membership value perception, and creates switching costs. Members factor in gas savings when evaluating the membership fee. It's a loss leader that strengthens the entire ecosystem.

The Kirkland Signature economics are even more impressive. With the brand generating $74-86 billion in revenue (depending on inclusion of gas), and typical private label margins 5-7% higher than national brands, Kirkland contributes disproportionately to Costco's profitability while still offering members 20% savings. It's value creation, not value extraction.

Same-store sales growth of 5.3% might seem modest, but in retail, consistent comp growth is extraordinarily difficult. Most retailers see comp sales decline after the initial honeymoon period. Costco warehouses keep growing because the model creates habit, not just transactions. Members change their behavior—buying in bulk, shopping less frequently but spending more per trip.

The international performance reveals untapped potential. Other International comparable sales grew 5.7% for the fourth quarter and 8.1% for the year. With only 281 international locations versus 624 in the U.S., international expansion could drive decades of growth. Each new country requires patient cultivation, but once established, the model proves remarkably consistent across cultures.

Analysts have raised Costco's price target to $950 per share, up from $875, reflecting confidence in continued growth driven by membership fee increases, store expansions, and strong operational fundamentals. But these targets still undervalue the business. At roughly 50x earnings, Costco seems expensive. But when you understand that membership fees are essentially a subscription software business hiding inside a retailer, the multiple makes sense.

The financial model's resilience shows in downturns. During recessions, Costco typically gains market share as consumers seek value. The membership fee becomes more valuable, not less, when budgets tighten. This counter-cyclical dynamic provides portfolio ballast that pure growth stocks lack.

Looking forward, the financial trajectory seems almost boringly predictable—which is the point. Add 25 warehouses annually, grow membership 5-7%, raise fees every 5-7 years, maintain discipline on markups, let inflation flow through to nominal growth. No moonshots, no pivots, no "transformation initiatives." Just relentless execution of a model perfected over four decades.

The ultimate financial insight is this: Costco has solved retail's fundamental challenge—how to grow profitably while delivering increasing value to customers. By making membership fees the profit center and product sales the value delivery mechanism, they've aligned interests in a way that creates compound value for all stakeholders. The numbers aren't just good—they're inevitable.

X. Playbook: Lessons for Founders & Investors

The Costco story offers a masterclass in contrarian thinking that actually works. While every MBA program teaches differentiation and premium pricing, Costco built a $400 billion company by doing the opposite. The lessons aren't just for retailers—they're universal principles for building enduring businesses in any industry.

Counter-intuitive business models that actually work

The greatest businesses often sound terrible when first described. Charge customers money before they can shop? Cap your profit margins permanently? Sell forty-pound bags of rice to suburban families? Refuse to advertise? On paper, Costco violates every rule of retail. In practice, these violations become moats.

The lesson for founders: if your business model doesn't confuse smart people at first, it's probably not revolutionary enough. True innovation often lies in combining elements that seem contradictory. Costco combined wholesale with retail, membership fees with low prices, premium quality with warehouse presentation. The contradiction is the innovation.

Consider the psychological inversion Costco achieved. Traditional retail thinking says customers hate fees. But by charging a membership fee, Costco transformed shopping from a transaction into an investment. Members don't compare Costco prices to Walmart—they calculate how much they're saving to justify their membership. The fee doesn't repel customers; it recruits evangelists.

The power of aligned incentives

Most businesses face inherent conflicts between stakeholders. Shareholders want higher margins, customers want lower prices. Employees want higher wages, shareholders want lower costs. Suppliers want higher prices, retailers want lower costs. These conflicts create friction that destroys value.

Costco's genius was designing a system where everyone wins simultaneously. Members get lower prices which justifies membership fees which provides profit for shareholders which funds employee benefits which reduces turnover which improves service which attracts more members. It's not a zero-sum game—it's a positive-sum ecosystem.

For founders, the lesson is profound: spend less time optimizing individual metrics and more time aligning systemic incentives. When incentives align, execution becomes easier because everyone rows in the same direction. When they conflict, even perfect execution fails because stakeholders work at cross purposes.

Long-term thinking in a short-term world

"We want to build a company that will still be here 50 and 60 years from now," Sinegal told investors who questioned his generous employee benefits. This wasn't rhetoric—it was capital allocation philosophy. Every decision was evaluated not on quarterly impact but generational implications.

This long-term orientation enabled decisions that seemed irrational short-term. Keeping the hot dog at $1.50 for forty years destroyed millions in potential profit. But it built billions in brand value. Paying employees 50% above market rates increased costs. But it decreased turnover, improved service, and created institutional knowledge worth far more.

For investors, Costco teaches patience. The stock has rarely been "cheap" by traditional metrics. It's always traded at premium multiples because the market eventually recognized that predictable compound growth is worth more than volatile higher growth. The best investments often look expensive on current metrics but cheap on future fundamentals.

Culture as the ultimate competitive advantage

Strategy can be copied. Technology can be purchased. Talent can be poached. But culture—real culture, not mission statements—takes decades to build and is nearly impossible to replicate. Costco's culture isn't what they say; it's what they do when nobody's watching.

When COVID hit and Costco could have price-gouged on essential items, they held prices flat. When e-commerce threatened their model, they didn't panic-pivot to digital. When activists pushed for margin expansion, management told them to sell the stock. These decisions weren't strategy—they were culture manifested.

For founders building cultures: it starts with founder behavior, not company policies. Sinegal visiting every warehouse annually wasn't a management technique—it was cultural transmission. Promoting from within wasn't an HR policy—it was values preservation. The hot dog price wasn't about food service—it was about promise-keeping.

When to ignore Wall Street

Every earnings call, analysts asked the same questions: When will you raise markups? When will you cut employee benefits? When will you monetize data? Why don't you advertise? The answer was always the same: that's not our model. The stock would dip, then recover as results proved the model worked.

The lesson isn't to always ignore Wall Street—it's to know when your understanding exceeds theirs. If you've built something genuinely different, conventional metrics won't capture the value. Costco's P/E ratio has looked "too high" for forty years. Amazon didn't show profits for decades. The best businesses often look bad on spreadsheets before they look great in reality.

The membership/subscription model blueprint

Costco pioneered the physical membership model that became the subscription economy. Netflix, Amazon Prime, Spotify—they're all variations on Sol Price's original insight: recurring revenue changes everything. It provides predictability, creates switching costs, and aligns provider-customer incentives.

But Costco's version remains superior because it combines digital economics with physical moats. Anyone can cancel Netflix with a click. Canceling Costco means changing shopping habits, finding new suppliers, and losing social proof ("Where'd you get that?" "Costco."). Digital subscriptions have convenience; physical memberships have commitment.

For founders considering subscription models: the key isn't the recurring revenue—it's the value delivery that justifies it. Costco members save multiples of their membership fee. Netflix viewers consume multiples of the monthly cost in content. The subscription is just the business model; value delivery is the business.

Building trust through consistency

In an era of dynamic pricing, algorithmic optimization, and growth hacking, Costco's consistency seems antiquated. Same markup rules for forty years. Same hot dog price. Same employee philosophy. Same warehouse layout. This consistency isn't stubbornness—it's trust building.

Trust compounds like interest. Every time Costco keeps a promise—fair prices, quality products, ethical treatment—trust deepens. This accumulated trust becomes a strategic asset worth more than any brand campaign. Members don't price-compare at Costco because they trust the value proposition. That trust took decades to build and would take minutes to destroy.

The playbook lesson: identify your core promises and never violate them. Not for quarterly earnings. Not for strategic pivots. Not for competitive responses. Your core promises become your identity. Violating them isn't just a tactical error—it's an existential threat.

The paradox of constraint

Costco's self-imposed constraints—14% markup maximum, 4,000 SKU limit, no advertising—seem like competitive disadvantages. In reality, they're strategic advantages. Constraints force innovation, prevent mission drift, and create identity.

The markup constraint forces operational efficiency. The SKU constraint forces curation excellence. The advertising constraint forces product quality. By removing options, Costco channels energy into execution. It's not about what you can do—it's about what you choose not to do.

For founders, the lesson is to embrace strategic constraints. Unlimited options lead to unfocused execution. Clear constraints create clear identity. The companies that try to be everything to everyone become nothing to no one. The companies that accept limits often transcend them.

Scale and soul

The conventional wisdom says companies lose their soul as they scale. Culture dilutes, values compromise, founders leave. Costco proves this isn't inevitable. At 900 warehouses and $250 billion in revenue, they still operate by Sol Price's principles. The hot dog still costs $1.50.

The secret is that Costco didn't scale its culture—it scaled its cultural transmission mechanisms. New employees learn from veterans, not manuals. Executives visit warehouses, not spreadsheets. Promotions come from within, not without. The culture doesn't scale; the system that perpetuates culture scales.

The ultimate lesson

Costco's playbook isn't about retail—it's about building businesses that create value rather than extract it. In a world of optimization, arbitrage, and financial engineering, Costco proves that simple models, executed consistently, with aligned incentives, over long timeframes, create extraordinary outcomes.

The paradox is perfect: by leaving money on the table every day—through low markups, high wages, and membership value—Costco has created more shareholder value than almost any company that tried to maximize it. By focusing on customers and employees first, shareholders won biggest.

For founders and investors, Costco offers a different path: build businesses that make all stakeholders better off. It's harder than extraction. It takes longer than disruption. It requires more discipline than pivoting. But it creates something extraction never can: a company that customers love, employees cherish, suppliers respect, and investors treasure. That's not just a business model—it's a blueprint for capitalism that actually works.

XI. Bear vs Bull Case & Future Outlook

Bull Case: The Fortress Retailer

The optimistic view of Costco rests on a simple observation: the company has solved retail. Not temporarily, not partially, but fundamentally and permanently. In an industry littered with fallen giants—Sears, Kmart, JCPenney—Costco hasn't just survived; it's thrived through every disruption imaginable.

The membership model creates incredible stickiness that only strengthens over time. With renewal rates approaching 93% and membership fees providing the majority of operating income, Costco has essentially created a subscription to savings. Unlike digital subscriptions that can be canceled with a click, Costco membership is woven into members' lifestyles. They've bought freezers to store bulk purchases. They've planned monthly shopping trips. They've integrated Costco into their routines. This behavioral lock-in transcends mere switching costs—it's habit formation at scale.

International expansion provides a multi-decade runway that's barely been tapped. With only 281 locations outside North America versus 624 in the U.S., the growth potential is staggering. China alone, where the Shanghai opening caused near-riots of enthusiasm, could eventually support hundreds of locations. India, Southeast Asia, and Latin America remain virtually untouched. Each new country requires patient cultivation, but once established, the model has proven remarkably consistent across cultures.

Inflation paradoxically makes bulk buying more attractive, not less. When consumer prices rise, the savings from buying in bulk become more meaningful. The membership fee becomes easier to justify when a single shopping trip saves multiples of the annual cost. Costco's scale allows them to negotiate better than smaller competitors during supply crunches, ensuring product availability when others have empty shelves. Economic uncertainty drives consumers toward value, and no one delivers value more consistently than Costco.

The cultural moat is nearly impossible to replicate. Forty years of promoting from within, treating employees well, and maintaining price discipline has created institutional knowledge that money can't buy. Competitors can copy the warehouse format, match the membership fees, even attempt similar pricing. But they can't replicate decades of accumulated trust, employee expertise, and supplier relationships. Culture isn't a strategy that can be implemented—it's an evolution that must be lived.

Demographics favor the model surprisingly well. Millennials and Gen Z, despite stereotypes about wanting everything delivered, are embracing Costco enthusiastically. About half of Costco's new members are younger than 40 years old. These younger members appreciate value, authenticity, and sustainability—all Costco strengths. The treasure hunt atmosphere appeals to social media culture. The Kirkland brand has become ironically cool. Costco has accidentally become trendy by steadfastly refusing to try.

The financial fortress provides enormous resilience. With minimal debt, strong cash generation, and the ability to fund growth from operations, Costco can weather any storm. The membership fee model provides predictable revenue regardless of economic conditions. The low-margin approach means there's little room for competitors to undercut on price. The company has survived recessions, pandemics, and disruptions while gaining market share through each crisis.

Bear Case: The Disruption Scenarios

The pessimistic view sees several threats that could crack Costco's seemingly impregnable fortress.

E-commerce disruption risk remains the most obvious threat. While Costco has built a successful online business, the fundamental model relies on physical warehouses. Amazon and others continue to improve delivery speed and reduce costs. Same-day delivery of bulk items, once impossible, is becoming routine in major markets. If convenience ultimately trumps cost savings, Costco's model could face existential pressure.

Demographic shifts in shopping behavior pose long-term challenges. Urbanization continues globally, and city dwellers have less space for bulk storage. Smaller households mean less need for forty-roll toilet paper packages. Work-from-home reduces commutes past Costco locations. Car ownership declining among younger urbanites limits access to warehouses. These aren't immediate threats, but generational shifts that could erode the model's relevance.

The limited SKU model shows vulnerability to infinite selection online. While Costco's curation provides value, younger consumers accustomed to infinite choice might find 4,000 SKUs constraining. Amazon offers millions of products; Costco offers thousands. For staples, limitation works. For discovery and variety, it's a weakness. The treasure hunt that delights current members might frustrate digital natives.

Succession and culture preservation challenges loom larger than acknowledged. The company has successfully transitioned from Sol Price to Jim Sinegal to Craig Jelinek to Ron Vachris. But each transition risks cultural dilution. The promote-from-within philosophy maintains continuity but potentially limits fresh thinking. As founding-era employees retire, will their replacements maintain the same discipline? Can you teach culture, or must it be absorbed through experience?

Market saturation in core geographies limits domestic growth. The U.S. and Canada are approaching warehouse density limits in many markets. Same-store sales growth, while positive, is decelerating. New warehouse productivity is declining as prime locations are exhausted. International expansion, while promising, requires enormous investment and patience with uncertain returns.

Technology disruption beyond e-commerce poses unknowns. Autonomous delivery could eliminate Costco's bulk-buying advantage. Virtual reality shopping could replicate the treasure hunt digitally. AI-powered price optimization could match Costco's value proposition without membership fees. Drone delivery could make warehouse trips obsolete. These seem far-fetched today, but so did e-commerce in 1995.

The Realistic Outlook

The truth likely lies between extremes. Costco isn't invulnerable, but it's remarkably resilient. The bear cases are real but manageable. The bull cases are compelling but not guaranteed.