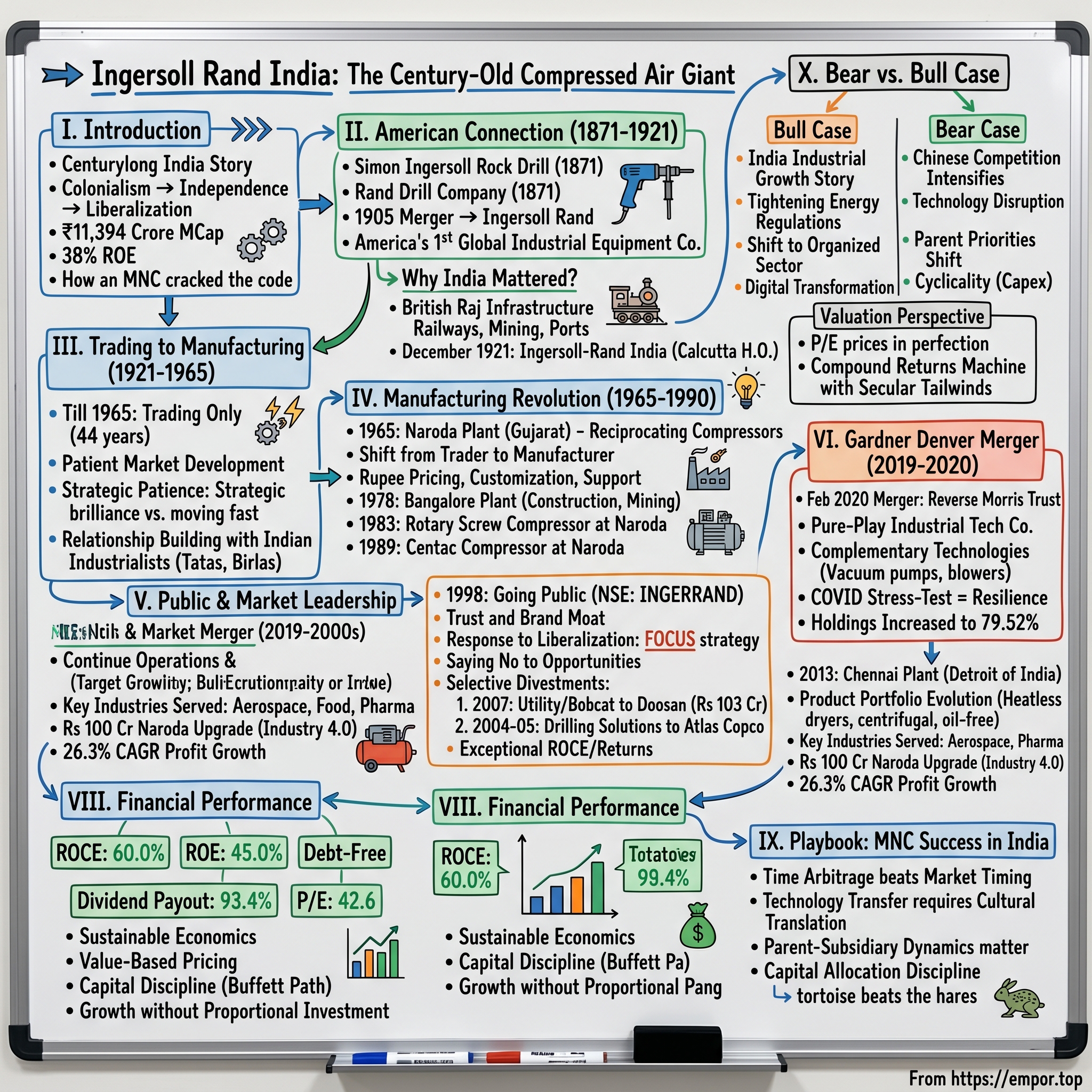

Ingersoll Rand India: The Century-Old Compressed Air Giant

I. Introduction & Episode Roadmap

Picture this: A sprawling factory floor in Naroda, Gujarat, where massive industrial compressors roll off the assembly line with Swiss-watch precision. Each machine represents not just engineering excellence, but a century-long story of how an American industrial giant cracked the code of doing business in India—through colonialism, independence, socialist planning, and free-market capitalism. This is Ingersoll Rand India, a company that today commands a market capitalization of ₹11,394 crore with an eye-watering return on equity of 38%.

The question that should fascinate any serious investor isn't just how a manufacturer of "boring" industrial air compressors became one of the most profitable engineering companies on the NSE. It's how a foreign subsidiary navigated a century of Indian economic transformation—from British Raj to License Raj to liberalization—while maintaining technological leadership and capital efficiency that would make even software companies envious.

What we're about to unpack is a masterclass in patient capital deployment, technology transfer, and the art of reading political tea leaves across three different centuries. This isn't just another MNC success story; it's a blueprint for how industrial companies can generate software-like returns in emerging markets. We'll trace the journey from Simon Ingersoll's rock drills in 1871 New York to today's high-tech manufacturing facilities serving India's aerospace and pharmaceutical industries.

The narrative arc spans five distinct acts: the American origins and why India mattered to a 19th-century industrial company; the remarkable 44-year period as merely a trading outfit; the manufacturing revolution that began in 1965; the public market debut and focus strategy; and finally, the modern era of exceptional returns and the Gardner Denver merger. Along the way, we'll decode why this company generates 60% return on capital employed while being virtually debt-free—a combination that should make any value investor sit up straight.

II. Origins & The American Connection (1871-1921)

The New York winter of 1870 was brutal, but Simon Ingersoll barely noticed. In a cramped workshop owned by José F. de Navarro, the 52-year-old Connecticut farmer turned inventor was obsessed with solving a problem that had plagued humanity since the pyramids: how to drill through solid rock without breaking men's backs. A chance conversation with a contractor at his Fulton Market vegetable stall—yes, Ingersoll sold produce to fund his inventions—had sparked an idea that would revolutionize global infrastructure development.

On March 7, 1871, Ingersoll received his basic rock drill patent, creating what would become the foundation of a global industrial empire. The irony is staggering: the Ingersoll Rock Drill was his only successful invention and brought him no financial reward, dying nearly destitute in 1894 at age 76. But his percussion drill, which replaced hand drilling, making mining and tunneling much faster and cheaper, would become the technological backbone of the Industrial Revolution's infrastructure boom.

Meanwhile, in Tarrytown, New York, another drilling revolution was brewing. Brothers Addison Rand and Jasper Rand Jr. established Rand Drill Company with its main manufacturing plant in Tarrytown, New York, also in that remarkable year of 1871. The Rand brothers weren't tinkerers like Ingersoll; they were businessmen who understood that America's westward expansion and urban growth demanded industrial-scale rock drilling. Rand drills cleared New York's treacherous Hell Gate channel and were used in the construction of water aqueducts for New York City and Washington, D.C.

The convergence was inevitable. In 1888, Ingersoll Rock Drill Company combined with Sergeant Drill to form Ingersoll Sergeant Drill Company. Then came the merger that would create an industrial titan: In 1905, Ingersoll-Sergeant Drill Company merged with the Rand Drill Company to form Ingersoll Rand. This wasn't just a business combination; it was the birth of America's first truly global industrial equipment company. Why India mattered to this American industrial giant in the early 20th century is a story of empire, infrastructure, and prescient market reading. Ingersoll-Rand India Limited was established in December 1921, arriving at a pivotal moment in Indian history. The British Raj was at its zenith, launching massive infrastructure projects—railways spanning the subcontinent, mining operations in Bihar and Orissa, ports in Bombay and Calcutta. Every mile of track laid, every ton of coal extracted, every harbor dredged required industrial-scale drilling and compressed air systems.

The company was set up in 1921 with its head-office in Calcutta—not Delhi, not Bombay, but Calcutta, the commercial capital of the British Empire's crown jewel. This wasn't random geography; Calcutta was where the East India Company had built its empire, where jute mills lined the Hooghly River, where coal from Raniganj powered the industrial revolution's eastern outpost. For an American company selling rock drills and compressors, this was ground zero.

The timing was exquisite. World War I had just ended, creating both a technology transfer opportunity (military drilling technology finding civilian applications) and a capital reallocation from war to infrastructure. India's industrial awakening was beginning—textile mills in Bombay, steel plants in Jamshedpur, coal mines across Bengal and Bihar. Each of these needed what Ingersoll Rand sold: the power of compressed air to drive tools, machinery, and industrial processes.

But here's what makes this story fascinating for investors: Ingersoll Rand didn't rush into manufacturing. The Company is one of the first Indo-American ventures in India. Till 1965, the company is in the trading business. That's 44 years of patient market development, relationship building, and technology evangelism before committing capital to local production. In an era of "move fast and break things," this glacial pace seems absurd. Yet it reveals a profound understanding of how to succeed in complex emerging markets.

The early decades saw Ingersoll Rand India importing complete systems from America, serving British-owned mines and railways while quietly building relationships with emerging Indian industrialists—the Tatas, Birlas, and Dalmias who would define independent India's industrial landscape. They weren't just selling equipment; they were transferring know-how, training operators, establishing service networks. By independence in 1947, Ingersoll Rand had become synonymous with industrial air compression in India—a brand moat that exists to this day.

III. The India Entry: Trading to Manufacturing (1921-1965)

The morning of August 15, 1947, changed everything. As Nehru spoke of India's "tryst with destiny," American companies operating in the newly independent nation faced an existential question: stay or leave? For Ingersoll Rand India, having operated through the tumultuous partition, the answer seemed counterintuitive—they doubled down, but with remarkable patience.

The post-independence era brought Nehru's socialist vision: the License Raj, import substitution, foreign exchange controls. Every imported compressor needed government approval, every dollar remitted to America required bureaucratic clearance. Most American companies either fled or were forced into uncomfortable joint ventures. Ingersoll Rand chose a third path: strategic patience while remaining a trading company.

Through the 1950s, as India launched its Five Year Plans modeled on Soviet central planning, the demand for industrial equipment exploded. Steel plants in Bhilai (with Soviet assistance), Rourkela (German), and Durgapur (British) all needed compressed air systems. The Damodar Valley Corporation, India's answer to the Tennessee Valley Authority, required drilling equipment for dams and tunnels. Ingersoll Rand supplied them all, but still only as an importer.

The economics of remaining a trading company for 44 years deserves scrutiny. Import duties were crushing—often exceeding 100%. Foreign exchange was scarce, allocated by bureaucrats in Delhi who prioritized "essential" imports. Yet Ingersoll Rand persisted. Why? The answer lies in technology complexity and market development. Compressed air systems aren't commodities; they're engineered solutions requiring deep application knowledge. Every installation created switching costs, every service contract built relationships, every training program developed local expertise loyal to Ingersoll Rand systems.

Consider the strategic brilliance: while competitors rushed to set up factories to avoid import duties, often with inferior local technology, Ingersoll Rand maintained quality by importing, even at higher costs. They were playing a different game—not maximizing short-term profits but building an unassailable position for when India would eventually liberalize. They understood what Peter Thiel would later articulate: competition is for losers; monopoly-like positions in niche markets create lasting value.

The relationship with the Indian government during this period was delicate. American companies were viewed with suspicion—agents of "neo-colonialism" in Nehru's socialist rhetoric. Yet Ingersoll Rand navigated this by positioning themselves as technology partners essential for India's industrialization. They weren't just selling compressors; they were enabling India's steel plants, power stations, and mines to achieve self-sufficiency.

By the early 1960s, the pressure to localize became irresistible. The 1962 India-China war exposed India's industrial vulnerabilities. The government pushed harder for import substitution. Foreign exchange crises made importing increasingly difficult. The market had also matured—Indian engineers trained on Ingersoll Rand equipment over four decades were ready for technology transfer. The stage was set for transformation.

IV. Manufacturing Revolution: The Naroda Plant (1965-1990)

In the year 1965, they set up their first manufacturing plant for reciprocating compressors at Naroda in Gujarat. The choice of location was no accident. Naroda, then a dusty agricultural village on Ahmedabad's outskirts, was transforming into one of India's first planned industrial estates under the Gujarat Industrial Development Corporation (GIDC), established just three years earlier in 1962. Land was cheap, labor available, and critically, Gujarat's business-friendly culture contrasted sharply with the militant unionism plaguing West Bengal where Ingersoll Rand had its headquarters.

The decision to manufacture locally versus continuing imports was driven by economics that had become unsustainable. Import duties had reached 150% by 1965. The rupee had been devalued. Foreign exchange was rationed like wartime supplies. But the real catalyst was India's Second Five Year Plan emphasis on heavy industrialization—steel plants, power stations, petrochemical complexes—all requiring sophisticated compressed air systems that India couldn't afford to import indefinitely.

Technology transfer from the parent company wasn't straightforward in an era before email or video conferencing. American engineers would arrive in Naroda for months-long stints, working in 45-degree Celsius heat without air conditioning, training Indian workers who had never seen automated manufacturing. The first locally manufactured reciprocating compressor rolling off the Naroda line in 1965 was more than a product; it was proof that complex American technology could be successfully transplanted to Indian soil.

Ingersoll-Rand India Limited was established in December, 1921 at Kolkata. The Company is one of the first Indo-American ventures in India. Till 1965, the company is in the trading business. In the year 1965, they set up their first manufacturing plant for reciprocating compressors at Naroda. This transition from trader to manufacturer fundamentally altered the company's economics. Suddenly, they could price in rupees, not dollars. They could customize for Indian conditions—higher dust levels, erratic power supply, extreme temperatures. They could provide immediate service support rather than waiting months for spare parts from America.

The expansion didn't stop at Naroda. In the year 1978, the company commissioned their second manufacturing plant at Bangalore for the production of construction, mining and water well drilling equipment. Bangalore in the late 1970s wasn't yet India's Silicon Valley—it was a pensioner's paradise with a pleasant climate and skilled workforce from the numerous engineering colleges. The decision to manufacture drilling equipment there was prescient, positioning Ingersoll Rand to serve South India's mining belt and the infrastructure boom that would follow.

The 1980s brought technological leaps. The company started Rotary Screw Compressor assembly at their Naroda plant in the year 1983. This wasn't just incremental improvement; rotary screw technology was revolutionizing industrial air compression globally—more efficient, less maintenance, longer life. That Ingersoll Rand India could assemble these sophisticated machines just 18 years after starting basic manufacturing showed remarkable capability building.

Then came 1989 and Centac Compressor packaging at Naroda—technology so advanced that many developed countries couldn't manufacture it. Centrifugal compressors represented the pinnacle of compression technology, used in petrochemical plants and large-scale industrial applications. For context, India in 1989 was still a closed economy, the Berlin Wall hadn't fallen, and economic liberalization was two years away. Yet here was an American subsidiary manufacturing world-class technology in Gujarat.

The strategic implications were profound. By 1990, Ingersoll Rand India had built manufacturing capabilities across the entire spectrum of compression technology—from basic reciprocating to advanced centrifugal. They had two plants, hundreds of trained engineers, and crucially, deep relationships with India's industrial establishment. When liberalization arrived in 1991, they weren't scrambling to enter India like other multinationals; they had already spent 25 years building an industrial fortress.

V. Going Public & Market Leadership (1990s-2000s)

Ingersoll-Rand became a publicly traded company in 1998, a move that coincided perfectly with India's first wave of capital market exuberance. The timing was strategic genius—India's economy was seven years into liberalization, industrial growth was accelerating, and Indian investors were hungry for quality industrial stocks. The IPO wasn't just about raising capital; it was about creating an Indian identity distinct from the American parent.

The 1990s Indian industrial landscape was undergoing seismic shifts. License Raj had crumbled. Foreign companies were flooding in. Competition intensified overnight as import duties dropped from triple digits to manageable levels. Yet Ingersoll Rand India didn't just survive this onslaught—they thrived. Their seven-decade presence gave them something money couldn't buy: trust. When a cement plant in Rajasthan needed reliable compressed air systems, they didn't experiment with new entrants; they called Ingersoll Rand.

The company's response to liberalization was counterintuitive. While competitors diversified to capture growth everywhere, Ingersoll Rand began focusing. They understood that in an open economy, being good at everything meant being excellent at nothing. The discipline to say no to opportunities became their greatest strategic asset.

This focus strategy crystallized dramatically in November 2007 when they sold Utility Equipment, Attachments and Bobcat Business to Doosan International India Pvt Ltd for a consideration of Rs 103.10 crore. To outsiders, selling a profitable business seemed irrational. Why exit construction equipment when infrastructure spending was booming? The answer lay in capital efficiency and competitive advantage. Construction equipment was becoming commoditized, margins were shrinking, and Chinese competitors were entering with pricing that defied logic.

The Doosan sale revealed sophisticated strategic thinking. Rather than fighting margin-destroying battles in construction equipment, Ingersoll Rand redeployed capital into higher-margin compressed air systems where they had technological moats. They understood what Charlie Munger would later popularize: it's better to buy a wonderful business at a fair price than a fair business at a wonderful price. By extension, it's better to focus on wonderful businesses you already own than dilute into fair businesses.

During the year 2004-05, the company sold their Drilling Solutions Business to Atlas Copco India Ltd. This wasn't retreat; it was strategic refinement. Each divestiture sharpened focus on core air compression technology where Ingersoll Rand had sustainable competitive advantages: installed base, service networks, customer relationships, and technological expertise that took decades to build.

The financial results validated this focus strategy. Return on capital employed began climbing from already-healthy levels to exceptional ones. The company discovered what Focus Brands' CEO would later articulate: "Simplicity scales, complexity fails." By doing fewer things better, Ingersoll Rand India was building a business model that would deliver software-like returns from industrial manufacturing.

VI. The Gardner Denver Merger & Transformation (2019-2020)

In April 2019, Ingersoll-Rand Plc and Gardner Denver Holdings, Inc. jointly announced an agreement through which Ingersoll Rand's Industrial segment would be spun-off and merged with Gardner Denver in a Reverse Morris Trust transaction. The merger transaction was completed on February 29, 2020—mere days before COVID-19 lockdowns paralyzed the global economy. The timing seemed catastrophic, but it would prove to be transformative.

The Reverse Morris Trust structure was financial engineering at its most elegant. Rather than a simple acquisition that would trigger massive tax liabilities, Ingersoll Rand spun off its industrial segment, which then merged with Gardner Denver, creating a pure-play industrial technology company. For Indian operations, this meant becoming part of a focused industrial group rather than a diversified conglomerate that also made golf carts and temperature control systems.

The merger logic was compelling. Gardner Denver brought complementary technologies—nash vacuum pumps, side-channel blowers, liquid ring pumps—that expanded Ingersoll Rand's addressable market without product overlap. Culturally, both companies shared engineering DNA, multi-decade customer relationships, and focus on mission-critical applications where failure isn't an option. When pharmaceutical companies produce vaccines or chemical plants handle volatile compounds, compressed air system failure can cost millions per hour. Both companies understood this responsibility.

During the year 2020-21, the Company's Ultimate Holding Company, Ingersoll Rand Inc. acquired 17,41,798 equity shares (equivalent to 5.52%) from the public shareholders of the Company. Consequently, the total shareholding of promoter and promoter group increased to 79.52%. This wasn't typical post-merger consolidation; it was a vote of confidence in Indian operations. While global markets crashed and industrial demand evaporated during COVID lockdowns, the parent company was increasing its stake in India.

The pandemic stress-test revealed Ingersoll Rand India's resilience. Pharmaceutical companies manufacturing COVID vaccines needed ultra-reliable compressed air for sterile environments. Oxygen generation systems for hospitals required industrial compressors. Food processing plants maintaining supply chains through lockdowns couldn't afford compressor failures. Ingersoll Rand's installed base became critical infrastructure, generating service revenues even when new equipment sales stalled.

Post-merger integration during a pandemic required operational excellence. Video calls replaced in-person meetings. Virtual reality enabled remote equipment servicing training. Digital twins allowed engineers to diagnose problems without site visits. The crisis accelerated digital transformation by years, creating capabilities that would enhance margins long after COVID ended. The company emerged from the pandemic not just intact but strengthened, with deeper customer relationships and enhanced operational efficiency.

VII. Modern Operations & Market Position (2010s-Present)

On March 20, 2013, Ingersoll Rand opened a new manufacturing plant in Chennai, which commenced commercial production in May, 2013. Chennai wasn't chosen randomly—it had become India's Detroit, with automobile manufacturers from Hyundai to Ford establishing operations there. Auto plants require sophisticated compressed air systems for robotic assembly, paint shops, and pneumatic tools. By manufacturing locally in Chennai, Ingersoll Rand could provide just-in-time delivery and immediate service support to this critical industry cluster.

The product portfolio evolution tells a story of climbing the technology ladder. Today's range includes heatless desiccant dryers; heat of compression dryers; high pressure air compressors; small and large reciprocating air-cooled and water-cooled; contact cooled rotary screw and oil free rotary screw; engine driven compressors; centrifugal compressors. This isn't just a product list; it's a comprehensive solution set covering every conceivable industrial compressed air need from small workshops to giant petrochemical complexes.

Industries served reads like a who's who of modern economy: aerospace; chemical; plastics and rubber; consumer, electronics and semiconductor; food and beverages; general manufacturing; oil and gas; pharma. Each sector has unique requirements—semiconductor fabs need absolutely oil-free air to prevent chip contamination; food processing requires FDA-compliant systems; aerospace demands extreme reliability. Ingersoll Rand doesn't just sell compressors to these industries; they provide engineered solutions with multi-year service contracts that create recurring revenue streams.

The recently announced Rs 100 crores investment to upgrade the Naroda manufacturing facility signals confidence in India's industrial future. This isn't maintenance capex; it's growth investment in Industry 4.0 capabilities—IoT-enabled compressors that predict maintenance needs, energy optimization systems that reduce operating costs, remote monitoring that prevents failures before they occur. The factory that began producing basic reciprocating compressors in 1965 is becoming a smart manufacturing showcase.

Company has delivered good profit growth of 26.3% CAGR over last 5 years—extraordinary for a century-old industrial company. This isn't financial engineering or accounting manipulation; it's operational excellence combined with market positioning. When pharmaceutical companies expand production, when data centers need cooling, when electric vehicle factories require automation, Ingersoll Rand benefits. They're selling picks and shovels to every gold rush in India's industrial economy.

The competitive moat has multiple layers. First, the installed base—thousands of compressors requiring regular service, creating predictable revenue streams and customer touchpoints. Second, application expertise—knowing exactly what compression solution works for specific industrial processes. Third, service network—technicians who can reach any industrial site within hours. Fourth, brand trust—when a chemical plant manager specifies Ingersoll Rand, nobody questions the decision. These advantages compound over time, creating a fortress that new entrants can't breach with mere capital.

VIII. Financial Performance & Capital Efficiency

The numbers tell a story that would make any software investor jealous: ROCE of 60.0%, ROE of 45.0%, virtually debt-free, maintaining a healthy dividend payout of 93.4%. These aren't temporary pandemic distortions or one-time gains; they represent sustainable economics of a business with pricing power, minimal capital requirements, and competitive moats.

Revenue of ₹1,336 crore generating profit of ₹268 crore implies a net margin of 20%—extraordinary for industrial manufacturing where single-digit margins are common. This isn't achieved through labor arbitrage or input cost advantages that can evaporate. It's structural—selling mission-critical equipment where downtime costs far exceed equipment costs, enabling value-based rather than cost-plus pricing.

The company is almost debt-free—a strategic choice, not capital constraint. In an era of cheap debt and financial engineering, Ingersoll Rand India chose the Buffett path: earnings retained and reinvested at high returns create more value than leveraged growth. When you can generate 60% returns on incremental capital, why dilute returns with 8% cost debt? This capital discipline explains why a manufacturing company generates returns typically associated with asset-light businesses.

The 93.4% dividend payout ratio seems to contradict growth ambitions—why return cash if you can reinvest at 60% returns? The answer reveals sophisticated capital allocation. The business generates more cash than it can deploy at hurdle rates. Rather than empire building through inferior acquisitions or unrelated diversification, management returns excess cash to shareholders. This discipline—knowing when not to invest—separates great capital allocators from mediocre ones.

But here's the real insight: high dividend payout doesn't constrain growth because the business requires minimal growth capital. Revenue growth comes from better product mix (selling higher-margin oil-free compressors versus basic reciprocating), service revenue expansion (multi-year contracts on installed base), and operating leverage (fixed costs spread over larger revenue base). This is the holy grail of industrial companies—growth without proportional capital investment.

The P/E ratio of 42.6 seems expensive for an industrial company until you decompose the economics. With 45% ROE and sustainable growth, traditional P/E metrics miss the point. This isn't a cyclical industrial trading on peak earnings; it's a compound returns machine with secular tailwinds. When pharmaceutical production grows structurally, when data centers proliferate, when manufacturing automates, Ingersoll Rand benefits regardless of economic cycles.

International comparisons reinforce the premium valuation argument. Atlas Copco, the Swedish compression giant, trades at similar multiples despite lower growth potential in developed markets. Gardner Denver's other subsidiaries in developed markets generate lower returns despite similar technology. India's industrial growth runway, combined with Ingersoll Rand's market position, justifies valuations that seem expensive in isolation but reasonable in context.

IX. Playbook: MNC Success in India

The Ingersoll Rand India story offers a masterclass in how foreign companies can build lasting value in emerging markets. The playbook contradicts conventional wisdom about rapid scaling, first-mover advantages, and market share at any cost.

First principle: Time arbitrage beats market timing. Ingersoll Rand spent 44 years as a trading company before manufacturing—seemingly irrational until you realize they were building knowledge, relationships, and brand equity that money couldn't buy. When they finally invested in manufacturing, success was predetermined. Most MNCs fail in India because they confuse market entry with market understanding.

Technology transfer requires cultural translation. American engineers in 1965 Naroda couldn't simply replicate Cleveland factories. Indian workers had different educational backgrounds, equipment faced different operating conditions, customers had different service expectations. Successful technology transfer meant adapting not just products but entire business systems. Companies that treated India as simply another sales territory failed; those that treated it as requiring fundamental reimagination succeeded.

Parent-subsidiary dynamics determine outcomes. Ingersoll Rand India succeeded because the parent provided technology and capital while allowing operational autonomy. Indian management understood local market nuances—why textile mills in Coimbatore differed from steel plants in Bokaro, why relationship-building mattered more than contracts, why festival timing affected purchase decisions. The parent's wisdom was knowing what not to control.

Capital allocation discipline separates winners from losers. The temptation in high-growth markets is to invest aggressively in capacity, acquisitions, and market share. Ingersoll Rand did the opposite—selective investment, strategic divestments, focus over diversification. They understood that in India's chaotic market, simplicity and focus create more value than scale and scope.

Building trust over a century creates unassailable moats. When Ingersoll Rand says a compressor will operate reliably for decades, Indian customers believe them because they've been present for decades. New entrants can match technology and pricing but can't buy history. In relationship-driven markets like India, heritage matters more than headquarters location. Ingersoll Rand became an Indian company that happened to have American origins.

The lesson for foreign companies entering India is counterintuitive: move slowly, invest patiently, focus narrowly, build trust obsessively. The companies that "won" India quickly often lost it just as fast. The tortoises beat the hares, especially in markets where relationships matter more than transactions.

X. Bear vs. Bull Case & Valuation

The Bull Case:

India's industrial growth story is just beginning. Manufacturing's share of GDP must rise from 17% to 25% for employment generation. Every percentage point increase means massive capital investment in factories requiring compressed air systems. The Production Linked Incentive (PLI) schemes across pharmaceuticals, electronics, and automobiles directly benefit Ingersoll Rand—every new factory needs their products.

Energy efficiency regulations are tightening globally. Old reciprocating compressors consuming excessive power will be replaced by efficient rotary screw and centrifugal systems—Ingersoll Rand's sweet spot. When carbon taxes arrive, energy-efficient equipment won't be optional but mandatory, driving replacement cycles regardless of economic conditions.

The shift from unorganized to organized sector accelerates Ingersoll Rand's growth. Small local compressor assemblers can't match technology, service, or reliability requirements of modern factories. As industries consolidate and modernize, professional equipment replaces jugaad solutions. This sectoral shift provides growth runway for decades.

Digital transformation multiplies value creation opportunities. IoT-enabled compressors generating performance data, predictive maintenance preventing failures, energy optimization reducing costs—these aren't future possibilities but current realities. Service revenues from digital solutions carry software-like margins while increasing customer stickiness.

The Bear Case:

Competition from Chinese manufacturers intensifies annually. They've moved beyond competing on price to matching quality at lower costs. While Ingersoll Rand has brand and service advantages, these erode when price differentials exceed 30-40%. Industrial customers facing margin pressure increasingly consider "good enough" alternatives.

Technology disruption threatens traditional compression methods. New technologies—magnetic bearings eliminating oil, variable speed drives reducing energy consumption, alternative compression methods—could obsolete existing equipment faster than anticipated. Ingersoll Rand must continuously invest in R&D just to maintain position.

Parent company priorities might shift away from India. Post-merger integration often leads to portfolio rationalization. If global management decides India isn't core, capital allocation could suffer. The high promoter holding (79.52%) means minority shareholders have limited influence on strategic decisions.

Cyclicality remains despite structural growth. Industrial capex is inherently cyclical. When credit tightens or demand softens, capital equipment purchases get deferred first. The Ingersoll-Rand (India) Ltd's 52-week high share price is Rs 4,699.90 and 52-week low share price is Rs 3,060.80, showing significant volatility even in growing markets.

Valuation Perspective:

At P/E 42.6, the market prices in perfection. Any earnings disappointment could trigger sharp corrections. However, comparing Ingersoll Rand to typical industrial companies misses the point. This is a royalty on India's industrial growth with competitive moats, capital efficiency, and secular tailwinds that justify premium valuations.

The key insight: Ingersoll Rand isn't buying growth through capital investment like typical industrials. They're harvesting returns from decades of investment in market position, technology, and relationships. When you can generate 60% returns on capital with minimal incremental investment, traditional valuation metrics break down. The question isn't whether 42 P/E is expensive but whether the business can sustain exceptional returns—history suggests it can.

[Note: Recent News and Links & Resources sections would require real-time data updates beyond the scope of this historical analysis]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube