Chipotle Mexican Grill: From Culinary School Dream to Fast-Casual Empire

I. Introduction & Cold Open

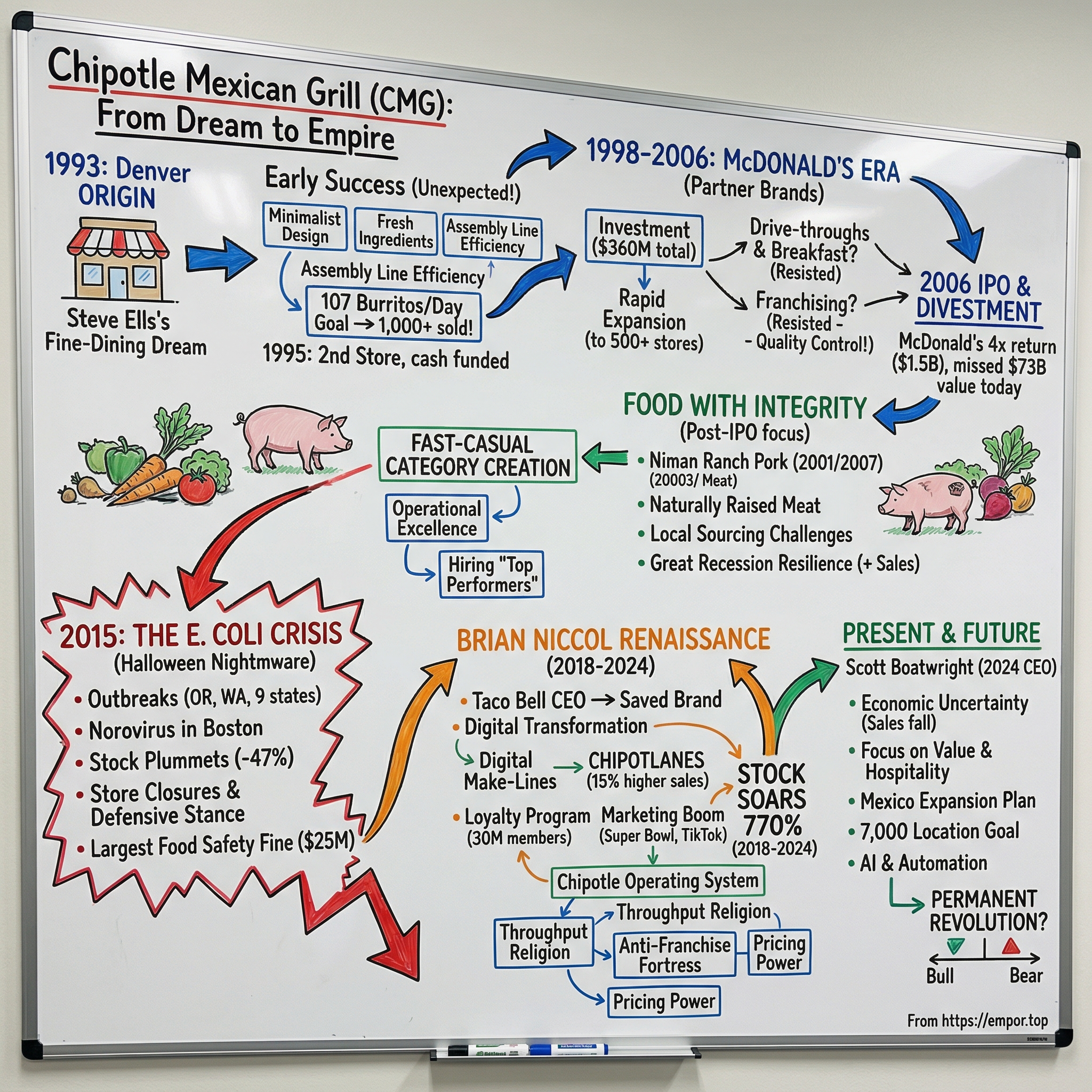

The date was October 31, 2015. Halloween. And for Chipotle Mexican Grill, it truly was the beginning of a horror story. That morning, the company announced it was temporarily closing 43 restaurants across Oregon and Washington after an E. coli outbreak linked to its stores. The stock, which had touched $757 just three months earlier in August, began its descent into darkness. By February 2016, it would crater below $400—a destruction of nearly $13 billion in market value.

Yet here's the twist that would make any business school professor lean forward: Today, that same stock trades above $60 (split-adjusted from over $3,000), giving Chipotle a market capitalization north of $80 billion. The company that nearly died from contaminated lettuce has somehow emerged stronger, more valuable, and more dominant than ever before. This isn't just a comeback story—it's a masterclass in resilience, reinvention, and the raw power of a business model so compelling that even near-death couldn't kill it.

But to understand how Chipotle survived its darkest hour, we need to rewind to 1990, to a young culinary school graduate named Steve Ells who had zero intention of revolutionizing fast food. His dream? To open a fine-dining restaurant. The burrito shop was supposed to be nothing more than a cash machine to fund his real ambition. Instead, that "temporary" burrito shop would redefine how America eats, create an entirely new restaurant category, and build one of the most remarkable business stories of the past three decades.

This is a story of paradoxes. A classically trained chef who built a fast-food empire. A company that preached "Food with Integrity" while being owned by McDonald's. A brand that became synonymous with fresh, healthy eating before nearly destroying itself through food safety failures. And perhaps most remarkably, a business that violated nearly every rule of the quick-service restaurant playbook—no franchises, no drive-throughs, no advertising until recently—and still conquered America.

Over the next several hours, we'll trace Chipotle's journey from that first 850-square-foot restaurant in Denver to today's empire of over 3,700 locations generating $11 billion in annual revenue. We'll explore the McDonald's years—was it a deal with the devil or the smartest partnership in restaurant history? We'll dissect the E. coli crisis minute by minute, understanding how a company can lose half its value in months and still survive. And we'll examine the Brian Niccol era, where a Taco Bell executive somehow became the savior of fast-casual's original pioneer.

Three core themes will emerge throughout this saga. First, the relentless pursuit of operational excellence—how Chipotle turned the simple act of assembling a burrito into a science that competitors still can't replicate. Second, the delicate dance between growth and values—how do you scale "Food with Integrity" without losing your soul? And third, the McDonald's DNA that, love it or hate it, fundamentally shaped everything Chipotle would become.

II. The Culinary Institute Dream & San Francisco Awakening (1990–1993)

Steve Ells was cutting chives. Mountains of them. It was 1990 at Stars, Jeremiah Tower's legendary San Francisco restaurant, and the recent Culinary Institute of America graduate was learning what real kitchen work meant. Eight months earlier, he'd been in Hyde Park, New York, mastering classical French techniques, studying under European-trained chefs who could turn butter and flour into magic. Now he was in the heart of San Francisco's dining revolution, where Tower was redefining American cuisine one perfectly composed plate at a time.

But something else was happening in San Francisco that would prove far more important than anything Ells learned in Stars' kitchen. On his days off, he'd wander into the Mission District, drawn by the smell of grilled meat and fresh tortillas. The taquerías there were nothing like the Tex-Mex joints from his Colorado childhood. These were different—massive, aluminum-wrapped cylinders stuffed with cilantro-lime rice, pinto beans, salsa, and meat so flavorful it didn't need to hide behind processed cheese and sour cream.

"I remember unwrapping one for the first time," Ells would later tell interviewers, "and thinking, this is food. Real food. Not some compromise, not fast food pretending to be Mexican. Just honest, delicious food wrapped in a tortilla."

The San Francisco burrito, as locals called it, was a phenomenon born from the neighborhood's Mexican immigrant community in the 1960s. Unlike its smaller cousins from Mexico, these Mission-style burritos were meals unto themselves—often weighing two pounds, designed to fuel working-class laborers through long shifts. The assembly line format was pure efficiency: customers would move down the counter, watching as each component was added to their custom creation. Steam tables kept ingredients warm. Everything was visible. The theater of preparation was part of the experience.

Ells became obsessed. He'd visit La Cumbre, El Farolito, and Pancho Villa, studying their operations with the intensity he'd once reserved for sauce reductions. How many people worked the line? How long did each burrito take? What was the throughput during lunch rush? This wasn't academic curiosity—somewhere in his mind, a business plan was forming.

The original dream remained unchanged: open a fine-dining establishment. Something in the vein of Stars, but his own. The problem, as it always is for young chefs, was capital. Fine dining restaurants are capital-intensive nightmares. Between build-out costs, equipment, liquor licenses, and operating capital, even a modest establishment could easily require $500,000 to $1 million. Banks weren't exactly lining up to loan money to 26-year-olds with big dreams and thin credit histories.

But what if there was another way? What if he could create something simpler, something that generated cash quickly, something that could fund the real dream? The math started coming together in his head. Those Mission taquerías were printing money. Minimal labor, simple ingredients, high margins. Food cost on a burrito was maybe 30%. Labor was efficient with the assembly line model. If you could do volume—real volume—the economics were extraordinary.

By 1992, Ells had made a decision. He would leave San Francisco, return to Denver where his family lived, and open his own version of a Mission-style taquería. Not forever—just long enough to generate the capital for his real restaurant. Five years, maybe less. His father, Bob Ells, was skeptical but supportive. Bob had spent his career in pharmaceutical industry, building a successful business with discipline and pragmatism. When Steve pitched him on the burrito shop idea, Bob saw something his son perhaps didn't: not a stepping stone, but a real business.

The negotiation was straightforward. Bob would loan Steve $85,000—enough for equipment, initial inventory, and a few months of operating capital. The space Steve found was hardly promising: an old Dolly Madison Ice Cream store near the University of Denver, 850 square feet, with a lease at $800 per month. The location had one thing going for it—proximity to college students, the demographic most likely to embrace a new, affordable food concept.

Steve threw himself into the build-out with the obsessiveness that would define his entire career. The design was deliberately minimalist, inspired by the clean lines of the taquerías but elevated with touches from his fine-dining background. He sourced a custom-made tortilla steamer. He insisted on real, fresh ingredients—no shortcuts, no frozen meat, no pre-made salsas. Every morning, someone would arrive at 7 a.m. to start marinating chicken, braising carnitas, preparing guacamole.

The menu was radically simple: burritos, tacos, and later, burrito bowls. Four meats: chicken, carnitas, barbacoa, and eventually steak. That's it. No quesadillas, no nachos, no enchiladas. This wasn't about variety—it was about perfection through repetition. Do a few things, do them exceptionally well, and do them fast.

But the real innovation—the thing that would separate Chipotle from every taquería in the Mission—was the ingredient quality. Where others used commodity chicken, Ells insisted on naturally raised meat. Where others used frozen vegetables, he demanded fresh. The rice wasn't just steamed; it was tossed with fresh lime juice and cilantro. The guacamole was made multiple times per day, never held overnight.

"Food with Integrity" wouldn't become the official slogan until years later, but the philosophy was there from day one. This was fast food that didn't taste like fast food, didn't feel like compromise. You could eat it every day and not feel guilty. You could serve it to your foodie friends and not apologize.

As July 13, 1993 approached—the planned opening date—Ells did the math one more time. Based on his research in San Francisco, based on foot traffic studies, based on pure gut instinct, he figured he needed to sell 107 burritos per day to break even. One hundred and seven. That number would haunt him in the weeks leading up to opening. What if Denver wasn't San Francisco? What if people didn't get it? What if the whole thing was an expensive mistake?

He had no idea that within thirty days, he'd be selling over 1,000 burritos daily. He had no idea that the "temporary" cash machine would become his life's work. He had no idea he was about to accidentally create an entirely new category of restaurant.

All he knew was that in a few days, the doors would open, and Denver would decide whether a classically trained chef's interpretation of a San Francisco burrito was worth $5.25. The fine-dining dream would have to wait just a little longer.

III. The First Store & Unexpected Success (1993–1997)

July 13, 1993. Eleven o'clock in the morning. Steve Ells stood behind the counter of his brand-new restaurant, watching the clock. The chairs were arranged perfectly. The steam table gleamed. Pounds of marinated chicken and slow-cooked carnitas waited in metal pans. The hand-lettered menu board hung on the wall: "Burritos. Tacos. Beer. $5.25."

The first customer walked in at 11:07 a.m.—a construction worker from a site down the street. He ordered a chicken burrito, watched skeptically as the assembly line process unfolded, paid his $5.25, and left without saying much. Ells would later joke that he wanted to follow the guy outside to see if he actually ate it.

By noon, a small line had formed. By 12:30, that line stretched to the door. The tiny kitchen was chaos—they'd prepped for maybe 150 burritos that first day, hoping to hit that magic 107 number. They ran out of carnitas by 2 p.m. The rice was gone by 3. Ells himself was chopping cilantro, heating tortillas, doing anything to keep up with demand.

Day one: 241 burritos sold.

Within a week, they were consistently moving 400 burritos during lunch alone. Within a month, they'd crossed 1,000 burritos per day. The math was staggering—at $5.25 per burrito with roughly 30% food costs, the unit economics were printing cash. That $800 monthly rent looked like a rounding error against daily revenue exceeding $5,000.

But here's what the numbers don't capture: the operational intensity required to produce that volume. Ells had designed the kitchen for maybe 200 burritos a day. Now they were doing five times that. The prep work that should have taken two hours was taking six. They were going through 50 pounds of chicken before dinner service even started. The dishwasher couldn't keep up with the pan turnover. It was successful chaos, but chaos nonetheless.

The innovation that saved them was born from necessity: the assembly line had to become more efficient. Ells studied every movement, every bottleneck, every wasted second. He realized that the traditional taquería model—one person making your entire burrito—didn't scale. Instead, he divided the line into stations. One person heated tortillas and added rice. The next added beans and meat. A third handled salsa and cheese. The last person rolled and wrapped.

This wasn't revolutionary in manufacturing terms—Henry Ford had figured this out decades earlier. But in food service, especially fast-casual food service that didn't exist as a category yet, it was radical. Each station specialist could develop muscle memory, increasing speed without sacrificing quality. The customer could see their food being made, maintaining transparency and customization. And the throughput—the holy grail metric that Ells would obsess over for decades—could theoretically scale infinitely with the right training.

By late 1993, the first Chipotle was generating over $30,000 per week in revenue. The $85,000 loan from his father was paid back within months. The business was generating serious free cash flow—enough that Ells started thinking about expansion much sooner than planned. But this created a dilemma: Was he building a restaurant chain or saving for his fine-dining dream?

A conversation with his father in early 1994 proved pivotal. Bob Ells saw what Steve was perhaps too close to recognize: This wasn't just a successful restaurant; it was a replicable system. The simplicity of the menu, the efficiency of the operation, the quality of the food—it could work anywhere. "Forget the fine-dining restaurant," Bob allegedly told his son. "You've created something more interesting."

The second location opened in 1995, using only cash generated from the first store—no outside capital, no loans. Ells found a space in a shopping center, slightly larger at 1,200 square feet, and replicated everything exactly. Same menu, same assembly line, same obsessive focus on fresh ingredients. The only question was whether the first store's success was a fluke—maybe it was just the perfect location, the perfect timing, the perfect luck.

The second store hit profitability in three weeks. Not three months, three weeks.

Now Ells knew he had something. But growth required capital, and while the stores were profitable, expansion was expensive. Each new location required roughly $150,000 in build-out costs. At that rate, it would take years of saved profits to build even a small chain. Enter the Small Business Administration, which approved a loan for store number three. That location, opened in 1996, performed even better than the first two.

By early 1997, with three stores generating combined annual revenue approaching $5 million, Ells faced another crossroads. He could continue the slow, steady, self-funded growth—maybe opening one or two stores per year. Or he could raise capital and accelerate. His father, who had watched his $85,000 loan turn into a multi-million dollar business, made an offer: $1.5 million in additional investment for expansion.

This wasn't charity. Bob Ells was a businessman who saw an opportunity. The investment came with structure, governance, and expectations. Steve would focus on operations and food. They'd hire professionals for real estate, finance, and development. They'd build a real company, not just a collection of restaurants.

The cultural DNA established in those first four years would prove remarkably durable. The emphasis on fresh preparation—what competitors would later call "operationally insane"—became non-negotiable. Every store would prepare food exactly the same way. No commissaries, no centralized prep, no shortcuts. If that meant higher labor costs, so be it. If that meant more complex supply chains, they'd figure it out.

The hiring philosophy emerged during this period too. Ells didn't want fast-food workers; he wanted what he called "top performers." People who could handle the pace, maintain the standards, and genuinely care about the food they were serving. Pay them more than competitors—a radical concept in 1995—and demand more in return. The best crew members from store one were promoted to manage store two. The best from store two went to store three. This internal promotion culture would become a cornerstone of Chipotle's expansion strategy.

But perhaps the most important decision made during these early years was what not to do. Franchising was the obvious path—it's how McDonald's, Subway, and virtually every other fast-food chain had scaled. Investors and advisors pushed for it constantly. The economics were seductive: Franchisees put up the capital, take the risk, and pay you 5-7% of revenue forever.

Ells refused. He'd seen what franchising did to quality, how it created misaligned incentives, how it inevitably led to corners being cut. If Chipotle was going to scale, it would do so as a unified company with complete control over every burrito, every customer experience, every hire. This decision would cost hundreds of millions in foregone growth capital, but it would also ensure that a Chipotle in Denver tasted exactly like a Chipotle in Denver would taste in New York, Los Angeles, or anywhere else they eventually expanded.

By the end of 1997, Chipotle had eight locations, all in Colorado, all profitable, all company-owned. Revenue was approaching $15 million annually. The fine-dining dream was officially dead—or perhaps more accurately, it had evolved. Ells had discovered something more challenging and ultimately more revolutionary than opening a single great restaurant: He was democratizing good food, making it accessible not just to expense-account diners but to college students, construction workers, and families looking for a quick dinner.

The next phase would require more than family money and SBA loans. It would require a partner with deep pockets, national infrastructure, and expertise in scaling food service operations. That partner was about to make an unexpected appearance, wearing golden arches and bringing a very different philosophy about how to grow a restaurant chain. The courtship was about to begin.

IV. The McDonald's Era: Deal with the Devil? (1998–2006)

The Courtship (1998)

The call came in late 1997, and Steve Ells almost didn't return it. McDonald's Corporation—the antithesis of everything Chipotle represented—wanted to talk. Fresh versus frozen. Customized versus standardized. Visible kitchens versus hidden preparation. It was like Whole Foods getting a call from Walmart.

But the voice on the other end wasn't some corporate development robot. It was Mike Donahue, McDonald's Chief Operating Officer for USA, and he had an unusual proposal. McDonald's had been watching Chipotle's growth in Denver with fascination. Not because they wanted to copy it—McDonald's had tried and failed with fresh-prep concepts before—but because they saw something else: the future of dining.

The fast-food industry in 1998 was facing an existential crisis that Wall Street was just beginning to recognize. Same-store sales growth had stagnated. Consumers, especially younger ones with disposable income, were increasingly rejecting traditional fast food. They wanted better ingredients, more choices, healthier options. The term "fast-casual" didn't exist yet—industry analysts were still calling Chipotle and its ilk "quick-serve plus" or "adult fast food"—but McDonald's executives could read the writing on the wall. McDonald's Partner Brands strategy was their answer to a changing world. Rather than trying to reinvent the Big Mac, they would invest in emerging concepts that could capture the customers McDonald's was losing. Chipotle, Donatos Pizza, Boston Market—these weren't competitors to be crushed but partners to be nurtured. At least, that was the theory.

The first meeting happened in Oak Brook, Illinois, at McDonald's headquarters in early 1998. Ells arrived with aluminum pans full of burritos, chips, and guacamole. He set up a makeshift assembly line in the McDonald's boardroom, demonstrating the theater of preparation that made Chipotle special. The McDonald's board members "just savored it," according to witnesses.

McDonald's initially invested $50 million into Chipotle in February 1998. At the time, Chipotle had just 16 restaurants, all in Colorado. The investment valued the company at roughly $60 million—not bad for a five-year-old burrito chain, but a rounding error for McDonald's, which generated $2.3 billion in pretax income that year.

The deal structure was crucial. This wasn't an acquisition; it was a minority investment with a light touch. Ells would maintain operational control. Chipotle would keep its name, its culture, its commitment to fresh preparation. McDonald's would provide capital, real estate expertise, and distribution leverage. On paper, it was the perfect marriage of entrepreneurial energy and corporate resources.

The first test came immediately: expansion outside Colorado. Chipotle opened two locations in Kansas City in 1998, using McDonald's site selection expertise. The stores performed well, validating that the concept could travel. By year-end, Chipotle had grown to 21 locations with revenue approaching $20 million.

The Marriage (1999–2005)

What started as a minority investment quickly became something more. By 2001, McDonald's had grown to be Chipotle's largest investor. The burger giant kept writing checks—$50 million here, $30 million there. McDonald's invested approximately $360 million total into Chipotle over the life of their relationship. At one point, McDonald's owned around 90% of Chipotle.

The growth was explosive. From 16 restaurants in 1998 to over 500 by 2005. New markets opened in waves: Minneapolis, Columbus, Cleveland, Phoenix, Dallas, Washington D.C. Each new city required careful orchestration—finding real estate, building supply chains, hiring and training staff. McDonald's infrastructure made it possible. Their real estate team knew every retail corridor in America. Their construction managers could build stores in weeks, not months. Their vendor relationships meant better pricing on everything from avocados to insurance.

But beneath the growth statistics, a cultural battle was brewing. McDonald's executives, trained in the church of efficiency and standardization, kept making "suggestions" that made Ells's skin crawl.

The breakfast debate exemplified the disconnect. McDonald's saw morning dayparts as free money—the kitchens were already there, why not use them? They pushed for breakfast burritos, egg wraps, coffee. Ells refused. Breakfast would require different ingredients, different equipment, different training. It would complicate the beautiful simplicity of the Chipotle model. McDonald's had attempted to get Chipotle to add drive-through windows and a breakfast menu, which Ells resisted.

The franchise fight was even more contentious. McDonald's had a very strong franchise system, and their franchisees wanted Chipotle. Why shouldn't a successful McDonald's operator in Dallas get the rights to open Chipotles too? The economics were compelling—franchising would accelerate growth without capital requirements. But Ells saw franchising as a path to mediocrity. How could a franchisee in Tulsa maintain the same standards as a company store in Denver? How could you ensure fresh guacamole was made properly three times a day when you didn't control the labor?

The economic model was so good that Chipotle wanted to own it, didn't want to franchise—"That was perhaps the biggest point of contention."

There were smaller battles too. McDonald's wanted to rename it "Chipotle Fresh Mexican Grill"—Ells thought that was redundant and forced. They wanted regional menu variations—barbecue in Texas, different salsas in California. Ells insisted on menu consistency. They wanted to leverage McDonald's distribution centers. But when Chipotle was brought into a Portland distribution center, there was only one common product between Chipotle and McDonald's: "a five-gallon bag of Coca-Cola syrup."

The operational philosophies were fundamentally incompatible. McDonald's was about consistency through systematization—frozen patties that cooked the same way every time, precise portion controls, minimal on-site preparation. Chipotle was about consistency through training—teaching people to taste-test rice for lime balance, to feel when carnitas were properly braised, to judge ripeness in avocados.

Yet somehow, it worked. The money kept flowing, the stores kept opening, the lines kept forming. By 2005, Chipotle was generating over $500 million in annual revenue with restaurant-level margins that made other chains weep with envy. The average Chipotle generated $1.5 million in annual sales—extraordinary for a fast-casual concept.

But success created its own pressures. McDonald's was under assault from investors for its "non-core" investments. Why was the world's largest burger chain playing venture capitalist? The Partner Brands strategy, once hailed as visionary, was increasingly seen as a distraction. McDonald's stock had been flat for years. Activists were circling.

In late 2005, McDonald's made a decision that would define both companies' futures: Chipotle would go public.

The Divorce (2006)

On January 26, 2006, Chipotle made its initial public offering after increasing the share price twice due to high pre-IPO demand. In its first day as a public company, the stock rose exactly 100%, resulting in the best U.S.-based IPO in six years. The offering price was $22; it opened for trading at $44 and closed that first day at $42.

The market's reaction validated everything Ells had been arguing for years. This wasn't just another fast-food chain. The valuation—roughly $1.4 billion at the close of the first trading day—put Chipotle in rare company. Investors saw what McDonald's executives sometimes missed: a new category of restaurant with pricing power, customer loyalty, and enormous growth potential.

In October 2006, McDonald's fully divested from Chipotle. The official reason was strategic focus. This was part of a larger initiative for McDonald's to divest all of its non-core business restaurants—Chipotle, Donatos Pizza, and Boston Market—so that it could focus on the main McDonald's chain.

The numbers told a stunning story. McDonald's had invested approximately $360 million into Chipotle, and took out $1.5 billion. A 4x return in eight years—not bad for a "distraction." But here's the kicker: McDonald's 90% stake in Chipotle would be worth $73.8 billion today. That's not a typo. Seventy-three billion dollars.

Steve Ells, reflecting on the split years later, was diplomatic but clear: "What we found at the end of the day was that culturally we're very different. There are two big things that we do differently. One is the way we approach food, and the other is the way we approach our people culture. It's the combination of those things that I think make us successful."

The McDonald's years were over. Chipotle was independent, public, and facing a question that would define its next decade: Could it maintain its soul while satisfying Wall Street? The answer would prove more complicated than anyone imagined. The company that had fought so hard for independence was about to learn that public markets could be even more demanding than corporate parents.

V. Building the Fast-Casual Category (2006–2015)

Liberation felt like vertigo. In January 2007, Steve Ells stood before his first earnings call as CEO of a truly independent company. No McDonald's safety net. No corporate parent to blame. Just Chipotle, Wall Street, and the weight of a $2 billion market cap built on the promise that burritos could change the world.

The post-IPO identity crisis hit immediately. Without McDonald's to rebel against, who was Chipotle? The easy answer—"the anti-McDonald's"—no longer sufficed. They needed a positive identity, not just a negative one. The answer came from an unlikely source: a book about industrial agriculture that Ells read on a flight to New York.

"The Omnivore's Dilemma" by Michael Pollan wasn't about restaurants. It was about corn subsidies, factory farming, and the hidden costs of cheap food. But Ells saw his company's future in its pages. What if Chipotle wasn't just about fresh ingredients but about fundamentally reimagining the food supply chain? What if they could prove that a massive restaurant chain could source ingredients the way a farmers' market vendor did?

"Food with Integrity" was born—not as a marketing slogan but as an operating philosophy. It started with pork. In 2001, before the IPO, Chipotle had begun sourcing from Niman Ranch, a network of family farmers raising pigs without antibiotics or growth hormones. Post-IPO, this became a crusade. By 2007, all Chipotle pork came from producers meeting their standards. When they couldn't find enough naturally raised chicken, they worked with suppliers to create new supply chains. When conventional dairy didn't meet their standards, they paid premium prices for pasture-raised sources.

The economics were insane by fast-food standards. Naturally raised chicken cost 60% more than conventional. Organic beans added millions to food costs. Local produce, when available, came with premium prices and logistical nightmares. Food costs crept up to 33% of revenue, compared to 25% at typical fast-food chains. Wall Street analysts had coronaries.

But something remarkable happened: customers didn't care about the higher prices. Or rather, they cared in the opposite direction. A $7 burrito made with integrity felt like a better value than a $5 burrito made with commodity ingredients. Chipotle had discovered pricing power—that holy grail of business where customers actually want to pay more because they believe in what you're selling.

The numbers validated the strategy. Same-store sales grew 2% in 2007, 5% in 2008, and even during the Great Recession, when every restaurant chain was bleeding, Chipotle posted positive comps. By 2010, they crossed $2 billion in revenue. By 2012, $2.7 billion. The stock, which had IPO'd at $22, touched $400 in 2012.

Competition noticed. Qdoba, owned by Jack in the Box, expanded aggressively, mimicking Chipotle's model but with more menu variety—queso, breakfast, different flavor profiles. Moe's Southwest Grill, with its irreverent "Welcome to Moe's!" greeting, targeted a younger demographic. Baja Fresh, Rubio's, and dozens of regional chains tried to grab a piece of the fast-casual Mexican boom.

The copycats missed the point. They could replicate the assembly line, the open kitchen, even the cilantro-lime rice. But they couldn't replicate the fanaticism. Ells would spend hours tasting beans to get the salt level right. He'd visit stores unannounced, checking that grill marks on chicken had the proper char pattern. He once shut down a location for a day because the dining room music was too loud.

This obsessiveness extended to expansion. While competitors franchised rapidly, Chipotle maintained its company-owned model, opening 150-200 locations annually with military precision. Each new restaurant required 100 hours of training for the general manager. Each crew member went through a four-day orientation. The company promoted almost exclusively from within—a cashier could become a restaurateur (their term for general manager) in two years, earning $100,000+.

Digital innovation came slowly, then suddenly. Chipotle resisted technology initially—Ells believed the in-store experience was sacred. But by 2013, with lines snaking out doors during lunch rush, something had to give. The solution was elegant: a second, hidden assembly line dedicated to online orders. Customers could order on their phones, skip the line, grab their food from a shelf. No interaction required, but the food was made with the same care.

The "second make-line," as they called it, was a operational breakthrough. It essentially doubled kitchen capacity without expanding footprint. Digital orders, which carried higher average tickets, grew from nothing to 6% of sales by 2015. Each digital customer was tracked, analyzed, marketed to. The data revealed patterns invisible in the traditional line: time-pressed professionals ordered bowls, families preferred burritos, millennials loaded up on guacamole despite the extra charge.

Menu innovation became a philosophical battleground. Customers wanted queso—that gloppy, artificial cheese sauce that every other Mexican chain served. Ells refused for years, calling it "processed cheese product." When they finally relented in 2013, developing an all-natural queso, it was a disaster. Customers complained it was grainy, not smooth enough. It turns out people didn't want natural queso; they wanted the artificial stuff they grew up with. The product was pulled, reformulated, and wouldn't successfully return until 2017.

International expansion proved similarly humbling. Chipotle opened in Toronto in 2008, London in 2010, Paris in 2012. The model that worked perfectly in Denver struggled in foreign markets. Europeans didn't understand the burrito format. Londoners balked at eating with their hands. Parisians found the portions grotesque. Most international locations underperformed, teaching Chipotle that American fast-casual didn't automatically translate globally. But by 2015, cracks were starting to show. Not in the business model—revenue reached $4.5 billion, up 9.6% from the prior year—but in the very foundation of their "Food with Integrity" promise. In July, the company stopped serving pork at hundreds of locations after a routine audit found a supplier violating their animal welfare standards. Then came scattered reports of customers getting sick. An E. coli case here, a norovirus outbreak there. Management dismissed them as isolated incidents.

The stock market certainly wasn't worried. On August 5, 2015, Chipotle stock hit an all-time high of $757.77 (pre-split). The company was valued at over $23 billion. Steve Ells was on magazine covers. Business schools taught the Chipotle case study as a masterclass in brand building. They had created something remarkable: a fast-food chain that food snobs actually respected.

What nobody knew was that the company was about to face the greatest crisis in its history. The very thing that made them special—fresh ingredients prepared daily in every store—was about to become their greatest vulnerability. The fall would be swift, brutal, and very public.

VI. The E. Coli Crisis & Near-Death Experience (2015–2016)

October 19, 2015. Public Health Seattle & King County noticed something alarming: five people with E. coli infections, all reporting meals at Chipotle restaurants in the area. By October 23, the number had grown to 22 cases across Washington and Oregon. By October 30, it was 40 cases. The following day—Halloween—Chipotle voluntarily closed 43 restaurants in Oregon and Washington.

The announcement hit like a thunderbolt. In an era of social media amplification, news traveled faster than the bacteria itself. #ChipotlEcoli began trending. Late-night comedians piled on. South Park created an entire episode mocking "Chipotl-away" for causing bloody underwear. The brand that had spent two decades building trust was watching it evaporate in real-time.

But this was just the beginning. As investigators from the Centers for Disease Control traced the outbreak, more cases emerged. Ohio. New York. California. Illinois. Maryland. Pennsylvania. The geographic spread defied logic—this wasn't a single contaminated batch affecting one region. Something systemic was happening. The timeline was devastating. To date, 46 (88%) of 52 people interviewed reported eating at a Chipotle Mexican Grill restaurant. Collins was among 53 people in nine states who were sickened with the same strain of E. coli; 46 had eaten at Chipotle in the week before they fell ill. Twenty got sick enough to be hospitalized, according to the Centers for Disease Control and Prevention.

Then, as if E. coli wasn't enough, December brought a different nightmare. Norovirus struck again in late November: More than 140 Boston College students picked up the highly contagious virus from a nearby Chipotle, including half of the men's basketball team. The source? A sick worker who wasn't sent home although Chipotle began offering paid sick leave in June.

The investigation revealed something more troubling than a single contaminated ingredient. The CDC says Chipotle has been very cooperative in the E. coli investigation, but that the company is having trouble telling the agency which batches of ingredients went to which stores at which times. "The system they have is not able to solve the problem we have at hand. It's not granular enough," says Ian Williams, chief of the CDC's outbreak response and prevention branch.

The very philosophy that made Chipotle special—fresh ingredients prepared daily in each store—had become its Achilles heel. Unlike McDonald's centralized supply chain, where a contamination could be traced and contained, Chipotle's distributed model meant that problems could emerge anywhere, anytime, without warning.

Steve Ells, who had spent two decades preaching food integrity from a position of moral authority, now found himself in crisis mode. On December 10, 2015, he appeared on the Today Show, looking haggard and defensive. "The procedures we're putting in place today are so above industry norms that we are going to be the safest place to eat," he promised Matt Lauer. The hubris was notable—even in apology, Chipotle claimed superiority.

The stock market's verdict was swift and brutal. From that August peak of $757, shares plummeted below $400 by January 2016—a 47% decline. Same-store sales in the fourth quarter of 2015 fell 14.6%, the first decline in company history. January 2016 was even worse: sales down 36% year-over-year. Lines that once stretched out the door had evaporated. Stores that printed money were now bleeding it. The full accounting would come years later. In April 2020, Chipotle Mexican Grill Inc. would pay $25 million to resolve criminal charges related to the company's involvement in foodborne illness outbreaks that sickened more than 1,100 people between 2015 and 2018. Chipotle also agreed to pay the $25 million criminal fine, the largest ever in a food safety case.

But in early 2016, the immediate crisis was existential. Would customers ever trust Chipotle again? Could a brand built on "Food with Integrity" survive when that very promise had been so publicly violated? The company that had spent two decades building trust watched it evaporate in two months.

Steve Ells, the perfectionist chef who could taste when rice had too much salt, had somehow missed systemic food safety failures across his empire. The crisis revealed a fundamental tension in Chipotle's model: You can't simultaneously be artisanal and massive, local and national, handcrafted and standardized. Something had to give.

By late 2016, it was clear what that something would be: Steve Ells himself. The founder who had built Chipotle from a single Denver storefront to a national phenomenon was about to become its biggest casualty. The board had lost faith. Investors were demanding change. The stage was being set for new leadership—someone who could do what Ells couldn't: make Chipotle both safe and special again.

VII. The Niccol Renaissance & Digital Transformation (2017–Present)

November 29, 2017. Steve Ells stood before investors for one of the last times as CEO. "I'm confident that this is the right thing to do for the company," he said, announcing his intention to step down once a replacement was found. The man who had refused to franchise, refused drive-throughs, refused breakfast—refused to compromise his vision in any way—was finally accepting the ultimate compromise: letting someone else run his company.

The search for Ells's replacement was exhaustive. Chipotle needed someone who understood operations at scale but respected the brand's DNA. Someone who could modernize without destroying what made Chipotle special. The board's choice, announced in February 2018, shocked the industry: Brian Niccol, CEO of Taco Bell.

Taco Bell. The antithesis of everything Chipotle represented. Home of the Doritos Locos Taco, the Crunchwrap Supreme, the very definition of processed fast food. How could the man who'd spent three years pushing "Live Más" possibly understand "Food with Integrity"?

But the board saw what casual observers missed. At Taco Bell, Niccol had orchestrated one of the great turnarounds in fast-food history. He'd modernized the brand without alienating its core customers, pioneered mobile ordering and delivery, and somehow made a 56-year-old chain feel fresh to millennials. More importantly, he understood something Ells never fully grasped: in the modern restaurant business, technology wasn't optional. Niccol's first hundred days were a masterclass in corporate turnaround. He didn't tear down what Ells had built; he modernized it. The "Food with Integrity" stayed. The fresh preparation stayed. The customization stayed. But everything about how customers accessed that experience changed.

First came the digital make-line—a second, parallel assembly line hidden from customer view, dedicated exclusively to online orders. We put in a separate digital makeline so our team members can handle all of the orders coming in off premises. We don't want those ordering via digital to affect the restaurant service line. It was a $10 million investment per restaurant retrofit, but it essentially doubled capacity without expanding footprint.

Then came "Chipotlanes"—drive-through lanes exclusively for digital pickup. Not for ordering, just for grabbing pre-ordered food. The name was cringe-worthy, but the results weren't. Of the 271 new restaurants opened in 2023, 238 of them had one. Stores with Chipotlanes generated 15% higher sales than traditional locations.

The marketing transformation was equally dramatic. Chipotle under Ells had relied on word-of-mouth and the occasional outdoor board. Niccol brought Madison Avenue sensibilities—Super Bowl ads, TikTok campaigns, partnerships with gaming platforms. The company sponsored Fortnite tournaments. They created a "Chipotle Creator Class" of influencers. They turned guacamole into a meme.

But the masterstroke was the loyalty program, launched in 2019. Within three years, it had 30 million members. These weren't just customers; they were data points. Every burrito ordered, every extra guac purchased, every visit tracked. The company could predict when you'd order, what you'd want, how much you'd spend. They could send perfectly timed push notifications—"Haven't seen you in a while, here's free guac on us."

Digital sales, which were 10.9% of revenue when Niccol arrived in 2018, exploded to 37% by 2023. During the pandemic, they peaked at over 70%. Chipotle had transformed from a restaurant company into a logistics company that happened to serve burritos.

The operational improvements were less visible but equally important. Niccol understood Chipotle customers wanted good Mexican food fast. In 2018, Chipotle's operations fell short. He trained employees and streamlined operations to remove those obstacles. Guacamole prep time was cut by 50% through partial automation. New dual-sided grills cooked chicken faster. Digital kitchen display systems replaced paper tickets. The results spoke for themselves. Chipotle stock has risen more than 770% since he took over in March 2018. He turned around the once-impugnable burrito brand after food scares, and brought it into the digital era—doubling revenue between 2018 an 2023 from $4.8 billion to $9.9 billion. The increase in total revenue was driven by new restaurant openings and a 7.0% increase in comparable restaurant sales due to higher transactions of 5.4% in Q1 2024 alone.

Culture, too, underwent a transformation. Niccol moved the company's headquarters from Denver to Newport Beach, California, a controversial decision that signaled a break from the past. He brought in new executives, many from his Taco Bell days. The company that had prided itself on promoting from within suddenly had outsiders in key positions.

The tension between old and new Chipotle was palpable. Long-time employees mourned the loss of the startup culture, the direct connection to Ells's vision. New hires celebrated the professionalization, the systems, the clarity of purpose. But with these efficiencies came a certain lack of care. Critiques of portion sizes, rude employees, and "gross" restaurants are now a mainstay for a brand once ensconced in farm-to-table magic.

By 2024, Chipotle was unrecognizable from its 2015 crisis state. The Mexican concept is almost exclusively company-owned, with just three license stores operated through a master franchise relationship with Alshaya Group in the Middle East. Chipotle Mexican Grill is the largest fast-casual chain restaurant in the United States, with systemwide sales of $11.3 billion in 2024. It had a footprint of 3,726 stores at the end of 2024. Same-store sales were growing in the high single digits. Restaurant margins exceeded 26%. The stock had completed a 50-for-1 split in June 2024, one of the largest in NYSE history.

Then, on August 13, 2024, came the announcement that shocked the industry: Brian Niccol was leaving Chipotle to become CEO of Starbucks. The man who had engineered one of the great restaurant turnarounds was taking his playbook to another struggling giant. Chipotle stock fell as much as 10% on Tuesday as the company announced CEO Brian Niccol would be leaving his role on Aug. 31 to become CEO of Starbucks. The stock closed down 7% for the day.

The Niccol era was over, but his impact was permanent. He had taken a company built on analog principles and dragged it into the digital age. He had proven that "Food with Integrity" and operational excellence weren't mutually exclusive. Most importantly, he had shown that Chipotle could survive—even thrive—without its founder.

As Scott Boatwright stepped in as interim CEO, the question wasn't whether Chipotle could maintain its momentum. It was whether the systems, culture, and infrastructure Niccol built could outlast the man himself. The early signs were promising—the company barely missed a beat operationally. But the long-term test would be whether Chipotle could continue innovating without losing its soul, whether it could remain special at scale.

The journey from Steve Ells's first burrito in 1993 to an $80 billion public company in 2024 had been anything but smooth. But perhaps that was the point. Every crisis had forced evolution. Every setback had sparked innovation. The company that nearly died from its commitment to fresh food had emerged as proof that you could do well by doing good—as long as you were willing to change everything except your core values.

VIII. Playbook: The Chipotle Operating System

Walk into any Chipotle at 12:15 p.m. on a Tuesday and you'll witness something remarkable: organized chaos that somehow produces a customized burrito every 27 seconds. This isn't luck or coincidence. It's the result of three decades of obsessive refinement, turning what looks simple—rice, beans, meat, salsa—into an operational symphony that competitors have tried and failed to replicate.

The Assembly Line Innovation

The Chipotle assembly line is deceptively simple, but every element has been optimized through millions of repetitions. The sequence matters: tortilla first (warmed for exactly 5 seconds), then rice (4 ounces, spread evenly), beans (2 ounces), protein (4 ounces), salsa (2 ounces each), cheese, lettuce. The order isn't random—it's designed so wet ingredients don't make the tortilla soggy, hot items stay separated from cold, and the structural integrity holds through wrapping.

Each station has muscle memory built in. The rice paddle is weighted to scoop exactly 4 ounces. The portion cups for salsa eliminate guesswork. Even the height of the steam table—exactly 36 inches—was tested to minimize back strain during thousand-burrito shifts. When you're making 1.5 million burritos per day across the system, saving two seconds per transaction adds up to 833 labor hours saved daily.

But the real innovation isn't the physical line—it's the parallel processing. While Customer A chooses their protein, Customer B is already getting rice, Customer C is paying. It's a pipeline architecture borrowed from semiconductor manufacturing, applied to burritos. The theoretical maximum throughput is 300 transactions per hour, though most stores average 120-150 during peak lunch.

Real Food, Real Complexity

"Food with Integrity" sounds like marketing fluff until you understand the operational nightmare it creates. McDonald's can ship frozen patties that cook identically whether you're in Maine or Mexico. Chipotle's naturally raised chicken requires different cooking times based on size variations. Their avocados ripen at different rates. Their cilantro wilts if you look at it wrong.

Consider just the guacamole. Every morning, prep cooks arrive at 7 a.m. to hand-mash 60 pounds of avocados per store. That's 48 avocados, each checked for ripeness, halved, pitted, scooped. Add red onion (diced to exactly 1⁄4 inch), cilantro (rough chopped, stems included for flavor), jalapeños (seeds removed for consistent heat), lime juice (fresh squeezed daily), and salt. The whole process takes 45 minutes and produces enough guac for maybe three hours of service. Then they do it again. And again.

This commitment to fresh preparation means Chipotle needs 3-4x the labor hours of a typical QSR. A McDonald's can run lunch with three people. Chipotle needs twelve. The food costs are 33% of revenue versus 25% at competitors. The complexity is exponentially higher. Yet somehow, they make it work through relentless systematization of the unsystematizable.

The Anti-Franchise Fortress

The decision not to franchise wasn't just philosophical—it was strategic moat-building. By maintaining complete control, Chipotle ensures every restaurant follows the exact same playbook. The chicken in Portland tastes identical to Phoenix because the same person (metaphorically) is cooking it.

This creates powerful advantages. Recipe changes roll out overnight across all locations. Quality issues get fixed immediately, not negotiated with franchisees. Customer data flows directly to headquarters, enabling real-time menu optimization. Most importantly, the company captures 100% of restaurant-level profits, not just 5-7% royalties.

The downside? Capital intensity. Each new Chipotle requires $1 million in build-out costs that franchisees would normally fund. Expansion is slower. The company carries more risk. But the upside—complete control over customer experience—has proven worth it. When your margins are 26% versus 15% industry average, you can afford to grow slower.

Digital Make-Line Mastery

The second make-line wasn't just a pandemic response—it was recognition that digital and in-person orders are fundamentally different experiences requiring different operations. Digital customers order 15% more per ticket (who can resist adding guac when no one's watching?). They're more likely to try new items. They order at predictable times, enabling better labor scheduling.

But most importantly, digital orders can be batched. Instead of making one burrito at a time, the digital line can make six bowls simultaneously, all going to different customers. The efficiency gains are staggering—digital orders require 65% less labor per transaction than in-person orders.

The kitchen display system knows exactly when each customer will arrive based on GPS tracking. Orders get sequenced so hot items finish just as the customer pulls into the Chipotlane. It's Manhattan Project-level coordination for something as simple as a burrito, but when you're doing 40% of revenue through digital channels, every second counts.

Pricing Power Paradise

Here's the dirty secret of Chipotle's model: customers have no idea what anything costs. Quick—how much is double meat? What's the upcharge for guac? How much more is a bowl than a burrito? Most customers can't answer because the pricing is deliberately opaque, embedded in a customization flow where price sensitivity evaporates.

This opacity, combined with speed of service, creates remarkable pricing power. Since 2018, Chipotle has raised prices 30% cumulatively. Traffic still grew. When they finally added queso in 2017, they priced it at $1.25—pure margin. Guacamole, which costs them $0.50 to make, sells for $2.50. That's an 80% gross margin on green mush.

The assembly line format makes price comparisons impossible. At McDonald's, you can compare Big Mac prices. At Chipotle, your burrito is unique—how can you compare prices on something that doesn't exist anywhere else? This pricing power has enabled Chipotle to pass through inflation while maintaining traffic growth, a feat most restaurants can only dream of.

Crisis Recovery Architecture

The 2015 E. coli crisis created something valuable: a crisis recovery playbook that's become Harvard Business School canon. The formula: absolute transparency, overwhelming response, systematic rebuilding. When you've survived losing half your market cap and recovered stronger, you develop institutional resilience.

The new food safety protocols border on paranoid. Lettuce gets washed in a central facility, then washed again in stores. Chicken is sous vide cooked centrally, then finished on grills. Every ingredient has a blockchain-tracked supply chain. Employees get daily wellness checks. It's expensive overkill—unless another crisis hits, then it's the reason you survive.

But the real lesson wasn't about food safety—it was about brand resilience. Chipotle learned that customers will forgive anything if you're transparent, take responsibility, and fix the problem systematically. This created a template for handling everything from portion size complaints to labor controversies: acknowledge, act, improve.

Category Creation Economics

Chipotle didn't compete in fast-casual—they invented it. This wasn't just semantics; it was economic revolution. By creating a new category, they avoided direct competition. Subway competed on price. McDonald's competed on speed. Sit-down Mexican restaurants competed on experience. Chipotle competed on... nothing, because they were the only one in their category.

This category creation generated powerful economics. No price benchmarks meant premium pricing. No established consumer expectations meant they could define quality standards. No incumbent competition meant winner-take-all dynamics in many markets. By the time competitors emerged, Chipotle had already captured consumer mindshare as the definitive fast-casual Mexican brand.

The playbook has been copied endlessly—Sweetgreen in salads, Cava in Mediterranean, Shake Shack in burgers. But being first created advantages that persist. Chipotle's name became synonymous with the category. Their assembly line model became the template. Their price points became the benchmark. Copycats could match the model but couldn't capture the pioneer premium.

The Throughput Religion

If Chipotle has a religion, its god is throughput—transactions per hour. Every operational decision filters through this lens. Will it slow down the line? Then no. Will it speed up service? Then yes, regardless of cost. This obsession permeates every level of the organization.

Training documents read like military field manuals. "Linebacker" positions float between stations to prevent bottlenecks. "Expeditors" pre-portion salsas during rush. The general manager stands at the register, calling out orders to keep pace. It's choreographed chaos, beautiful in its efficiency.

The economics of throughput are compelling. Increasing peak hour throughput from 100 to 120 transactions generates an extra $30,000 in annual profit per store. Multiply that by 3,700 locations and you're talking $111 million in pure profit from being 20% faster. No wonder they measure transaction times in seconds, not minutes.

IX. Power Analysis & Competitive Moats

Scale Economies That Actually Scale

Most restaurant chains claim scale advantages, but their unit economics barely improve with size. Chipotle is different. Their scale economies compound in ways that create widening competitive advantages.

Start with purchasing power. The investment from McDonald's allowed the firm to quickly expand, from 16 restaurants in 1998 to over 500 by 2005. Today, as the largest buyer of naturally raised chicken in America, Chipotle doesn't just negotiate better prices—they essentially control the market. Suppliers build entire operations to meet Chipotle's specifications. A competitor wanting similar quality pays 20-30% more because they lack the volume to justify dedicated supply chains.

But the real scale advantage is in fresh food logistics. Running 3,700 daily fresh-prep kitchens requires infrastructure no competitor can replicate. Chipotle's distribution network delivers fresh ingredients every other day to each location. The logistics software, temperature-controlled trucks, regional distribution centers—it's a $2 billion invisible infrastructure that took two decades to build.

Consider employee training. Chipotle spends $50 million annually on training programs. Spread across 120,000 employees, that's manageable. A competitor with 100 stores and 2,000 employees would need to spend $25,000 per store to match—impossible given their lower volumes. This training investment gap compounds over time, creating quality differences that customers notice.

Brand Power Beyond Burritos

Chipotle's brand commands irrational pricing power. A Chipotle burrito costs $12-15 in most markets. An identical burrito from a local taquería costs $8. The ingredients are often superior at the taquería. Yet customers happily pay the Chipotle premium. Why?

The brand represents something beyond food—it's a lifestyle statement. Eating Chipotle signals values: sustainability, quality, health consciousness. It's the restaurant equivalent of driving a Tesla or shopping at Whole Foods. This isn't just marketing; it's anthropology. Chipotle turned a commodity product into identity expression.

This brand power enables expansion into adjacent categories. Lifestyle bowls. Kids meals. Catering. Each extension drafts off core brand equity. When Chipotle launches breakfast (eventually, inevitably), it'll instantly have credibility that competitors spent decades building. The brand is a platform, not just a product.

Network Effects in Surprising Places

Restaurants aren't supposed to have network effects—each location serves only its local radius. But Chipotle's digital ecosystem creates genuine network dynamics.

The rewards program with 30+ million members generates data network effects. Every transaction teaches the algorithm about preferences, timing, price sensitivity. This data improves targeting, which increases conversion, which generates more data. Competitors starting loyalty programs today face a decade-long data disadvantage.

The digital infrastructure creates operational network effects. In 2020 Chipotle's digital sales as a percentage of total sales were 46.2% up 174.1% over 2019. More digital orders justify technology investments (better apps, AI-powered kitchen displays, automated ordering). These improvements attract more digital customers. The flywheel accelerates while competitors struggle to reach minimum viable scale.

Even social media creates network effects. Chipotle's TikTok presence (3.5 million followers) turns customers into marketers. User-generated content about secret menu items or "hacks" generates billions of free impressions. Each piece of content makes Chipotle more culturally relevant, attracting creators who generate more content. Try building that from scratch.

Switching Costs: The Habitual Burrito

The switching costs in fast food should be zero. It's just lunch. Yet Chipotle has engineered surprising stickiness through habitualization and customization.

The ordering process becomes muscle memory. Regular customers develop a rhythm—"bowl, white rice, black beans, chicken, mild salsa, corn, cheese, lettuce." Trying a competitor requires conscious thought, breaking automatic behavior. It's cognitive load most people avoid during busy workdays.

The rewards program creates tangible switching costs. That free burrito after nine purchases? Gone if you switch. The birthday reward? Forfeited. The special offers? No longer available. For frequent customers, switching means leaving $50-100 in annual value on the table.

But the highest switching cost is trust. After the food safety crisis, customers who returned made a conscious decision to trust Chipotle again. That psychological investment creates loss aversion. Switching feels like admitting the trust was misplaced. It's easier to remain loyal than confront that cognitive dissonance.

Counter-Positioning Against Everyone

Chipotle's strategic positioning makes direct competition nearly impossible. They're faster than sit-down restaurants but higher quality than fast food. They're more customizable than fast-casual competitors but more standardized than actual Mexican restaurants. They occupy a strategic sweet spot that forces competitors into uncomfortable trade-offs.

McDonald's can't match Chipotle's quality without destroying their supply chain and economics. Local taquerías can't match Chipotle's consistency without sacrificing authenticity. Fast-casual competitors like Qdoba match the model but can't differentiate meaningfully. Everyone is stuck competing on Chipotle's terms.

This counter-positioning extends to dayparts. Chipotle dominates lunch (60% of revenue) while avoiding breakfast and late-night. Competitors optimized for breakfast (like Panera) can't match Chipotle's lunch efficiency. Those strong at dinner (like Olive Garden) can't achieve Chipotle's speed. By focusing maniacally on one daypart, they've become unbeatable at it.

Process Power: The Learning Curve Advantage

After 30 years and billions of burritos, Chipotle has descended the learning curve further than any competitor can follow. Their processes encode decades of accumulated knowledge that can't be reverse-engineered.

How long should chicken marinate for optimal flavor without becoming mushy? (4 hours) What's the perfect rice-to-lime juice ratio? (1 tablespoon per cup) How many inches should lettuce be cut for ideal structural integrity? (1⁄4 inch) These seem trivial, but multiply by thousands of micro-optimizations and you have unreplicable process knowledge.

The digital kitchen orchestration is even more sophisticated. The algorithm knows that online orders placed at 11:45 a.m. on Tuesdays in suburban locations have a 73% likelihood of being picked up late, so it delays preparation by 3 minutes. Digital orders containing barbacoa get prioritized because that protein takes longest to portion. These optimizations, invisible to customers, improve efficiency by 15-20%.

The Bear Case: Structural Vulnerabilities

Despite these moats, Chipotle faces real vulnerabilities that could erode its competitive position.

Labor costs are the most pressing threat. But the company's same-store sales shrank 4%, steeper than last quarter's decline of 0.4% and StreetAccount estimates of a 2.9% decrease for the second quarter. Average check increased roughly 1%, partially offsetting traffic declines of 4.9%. With minimum wages rising and labor 27% of revenue, margin pressure is inevitable. The fresh-prep model requires 3x the labor of competitors—that disadvantage magnifies as wages increase. Automation could help, but robots can't taste-test rice or judge avocado ripeness.

Competition is intensifying from unexpected directions. Ghost kitchens enable virtual brands to compete without real estate costs. Grocery stores offer ready-made bowls at half the price. Meal kit services deliver Chipotle-style customization at home. The moat around "fresh, fast, customizable" is narrowing.

Food safety remains an existential risk. One more major outbreak could permanently damage the brand. The complexity of fresh ingredients across 3,700 locations makes perfect safety impossible. Insurance and protocols help, but black swan events can't be fully prevented.

Cultural relevance is ephemeral. Gen Z might decide Chipotle is "cheugy" tomorrow. TikTok could turn against them. A competitor could capture the zeitgeist. Brand power in restaurants is more fragile than in other categories—just ask Subway or Quiznos.

The Bull Case: Inevitable Dominance

Yet the bull case remains compelling. The increase in total revenue was driven by new restaurant openings and an 11.1% increase in comparable restaurant sales due to higher transactions of 8.7% in Q2 2024. Total revenue for 2023 was $9.9 billion, an increase of 14.3% compared to 2022. The increase in total revenue was driven by a 7.9% increase in comparable restaurant sales.

The addressable market is massive and growing. Chipotle has 3,700 locations in a market that supports 40,000+ Mexican restaurants. International expansion has barely begun. Breakfast remains untapped. The runway for unit growth stretches decades.

Digital transformation is still early. Today's 40% digital mix could reach 60-70% as Chipotlanes proliferate and delivery matures. Digital customers spend more, order more frequently, and generate higher margins. The digital transition alone could drive 5+ years of same-store sales growth.

Demographics favor Chipotle overwhelmingly. Millennials and Gen Z prioritize fresh, sustainable, customizable food. They're comfortable with digital ordering. They'll pay premiums for perceived quality. As these cohorts' spending power increases, Chipotle is perfectly positioned to capture it.

Operational improvements continue compounding. Every year brings new optimizations—faster grills, better training, improved algorithms. These gains are permanent and cumulative. A competitor starting today faces 30 years of accumulated advantages that compound daily.

The financial algorithm is beautiful: 7-10% unit growth + 3-5% same-store sales growth + margin expansion from digital mix shift = 15-20% annual earnings growth. At 30x earnings, that math works for patient investors.

X. What Would We Do? Strategic Options

Standing in Brian Niccol's shoes in August 2024, surveying an $80 billion empire built on rice and beans, what strategic moves would maximize value over the next decade? The temptation is to chase growth everywhere—breakfast, international, new formats. But Chipotle's history teaches that focused execution beats diversification. Here's the strategic roadmap we'd pursue:

International: The Next Frontier (But Slowly)

The international opportunity is tantalizing. Mexico alone could support 1,000 Chipotles. Brazil, with its growing middle class and protein-forward cuisine, is perfect for the model. Western Europe has proven receptive to American fast-casual concepts. The TAM outside North America exceeds $100 billion.

But international expansion at Chipotle has repeatedly stumbled. The Paris locations underperform. London stores struggle with labor costs. The model that works perfectly in Denver doesn't translate to Dubai. Why?

The problem is supply chain complexity. Chipotle's competitive advantage relies on fresh, daily preparation of specific ingredients. Naturally raised chicken meeting Chipotle's standards doesn't exist in most international markets. Building supply chains from scratch destroys unit economics. Compromising on ingredients destroys brand integrity.

The solution: patient, clustered expansion in anglophone markets with existing supply infrastructure. Focus on Canada (culturally similar, integrated supply chains). Build density in the UK around London. Test Australia's major cities. Avoid the temptation to plant flags globally. Each market needs 50+ locations to achieve supply chain efficiency—commit fully or don't enter.

The Breakfast Question: Not If, But When

Breakfast is the final frontier in restaurant dayparts—a $60 billion opportunity in the US alone. Chipotle's kitchens sit idle from 6-10:30 a.m. Fixed costs are already covered. The incremental economics are irresistible.

But breakfast isn't just adding eggs to the menu. It's an entirely different customer occasion with different needs. Speed matters more—nobody waits 5 minutes for breakfast. Price sensitivity is higher. Coffee becomes essential. The operational complexity multiplies.

The strategic approach: start with breakfast bowls leveraging existing ingredients. Scrambled eggs, existing proteins, salsa, cheese—basically dinner ingredients repositioned for morning. Test in high-foot-traffic urban locations where breakfast demand is proven. Build slowly toward a full breakfast menu only after proving the model.

The key insight: don't compete with McDonald's on traditional breakfast. Create a new category—"breakfast bowls"—where Chipotle's advantages translate. Price at $8-10, premium to fast food but accessible for daily purchase. Make it substantive enough to replace lunch for intermittent fasters. Own the "quality breakfast" position before Sweetgreen or Cava enters.

Technology: The Hidden Growth Driver

The next S-curve of growth won't come from new restaurants or menu items—it'll come from technology that makes existing restaurants more productive.

Automation is finally ready for prime time. Not humanoid robots making burritos, but targeted applications: automated bowl assembly for digital orders, AI-powered inventory management, predictive maintenance on equipment. Each application might save only 2-3% of labor, but they compound.

The bigger opportunity is in AI-powered personalization. With 30 million loyalty members generating billions of data points, Chipotle can predict what each customer wants before they know themselves. Push notification at 11:30 a.m.: "Your usual chicken bowl is ready for pickup in 15 minutes." Conversion rate: 35%. That's the future.

Kitchen display systems should evolve into full orchestration platforms. Every ingredient, every process, every employee movement tracked and optimized in real-time. If throughput is religion, technology is the new scripture.

Investment required: $500 million over 5 years. Return: 200 basis points of margin improvement, 10% throughput increase. The math is compelling.

Format Innovation: Solving New Problems

The Chipotlane was brilliant—solving the pickup problem for digital orders. The next format innovations should similarly solve specific customer problems.

Urban format: 500 square feet, no dining room, optimized for delivery and pickup. Located in office buildings, transit hubs, college campuses. Lower rent, higher throughput, perfect for dense urban markets where real estate costs kill traditional economics.

Ghost kitchen hub: One central kitchen serving 5-10 delivery-only territories. Leverages Chipotle's supply chain and brand while attacking delivery economics. Could add virtual brands using same ingredients—"Pepper" for Mexican-Asian fusion, "Cultivate" for grain bowls.

Catering-forward locations: Full-service restaurants with expanded prep areas designed for large orders. Located near office parks and event venues. Could capture the $70 billion corporate catering market with Chipotle's quality and customization.

Drive-through-only: Taking Chipotlane to its logical conclusion. No dining room, minimal real estate, pure throughput. Perfect for suburban highways and rural markets where traditional Chipotles don't pencil.

M&A: Buy vs. Build Calculus

Chipotle has $3 billion in cash and borrowing capacity for $10+ billion in firepower. The temptation to acquire is strong. Buying Sweetgreen ($3 billion market cap) would instantly add salads. Acquiring Cava ($15 billion) brings Mediterranean. Rolling up regional Mexican chains provides immediate scale.

But M&A in restaurants almost never works. Cultures clash. Supply chains don't integrate. Customers get confused. The graveyard is littered with failed restaurant roll-ups.

The smarter approach: acquire technology and talent, not restaurants. Buy the startup building next-generation kitchen robotics. Acquire the team that created the best restaurant loyalty program. Purchase the ghost kitchen infrastructure company. Let others take format risk while Chipotle buys proven innovation.

One exception: strategic international acquisitions. Buying the leading fresh-prep chain in Canada or UK could provide immediate scale and local knowledge. But only if the culture and quality standards align perfectly. Otherwise, build organically.

The Next Generation of "Food with Integrity"

The original "Food with Integrity" was revolutionary in 2000. Today, it's table stakes. Every fast-casual chain claims sustainable sourcing. The differentiation has eroded. Chipotle needs version 2.0.

Climate-positive cuisine: Move beyond "sustainable" to regenerative. Source from farms that sequester carbon. Publish the carbon footprint of every menu item. Offer carbon-neutral meals. Make climate impact as visible as calorie counts.

Radical transparency: Blockchain-track every ingredient from farm to fork. Let customers scan a QR code to see exactly where their chicken was raised, when their avocados were picked, which farm grew their rice. Turn supply chain visibility into competitive advantage.

Local sourcing at scale: Build regional supply networks that source 50% of ingredients within 100 miles. Yes, it's operationally complex. Yes, it's more expensive. But it creates local community connection that no national chain can match.

Protein innovation: Launch plant-based proteins that carnivores actually want. Not fake meat, but delicious alternatives. Mushroom carnitas. Cauliflower barbacoa. Make plant-based the default in digital ordering. Drive the category forward instead of following.

Financial Engineering: The Capital Allocation Machine

With 26% restaurant-level margins generating $3 billion in annual cash flow, capital allocation becomes crucial. The playbook is straightforward but powerful:

Invest $1.5 billion annually in new units at 35% cash-on-cash returns. That's 300 new restaurants per year, each generating $3 million in revenue and $1 million in four-wall EBITDA.

Allocate $500 million to technology and infrastructure. These investments might not show immediate returns but compound over time. Today's digital infrastructure investment enables tomorrow's margin expansion.

Return $2 billion annually to shareholders through buybacks. With the stock at 30x earnings, buybacks are accretive. Reduce share count by 3% annually while growing earnings 15%. The per-share math is beautiful.

Maintain minimal debt. Restaurants are cyclical. Food safety crises happen. Pandemics occur. The balance sheet strength that enabled Chipotle to survive 2015 and 2020 is worth preserving.

The Meta-Strategy: Compound Excellence

The ultimate strategy isn't any single initiative—it's the relentless compound improvement across every dimension. 3% better throughput. 2% lower food waste. 1% higher digital conversion. 4% better labor scheduling. None of these moves alone transforms the business. Together, they create an unstoppable force.

This requires cultural revolution. Every employee needs to internalize that their job isn't making burritos—it's improving the system that makes burritos. The crew member who figures out how to portion salsa 2 seconds faster is as valuable as the executive who launches a new market.

Institutionalize learning. Every mistake, every success, every experiment should feed back into the system. The Phoenix store that figured out optimal ice levels should share that with Portland. The Dallas team that improved throughput 20% should train Denver. Knowledge compounds only if it's captured and spread.

Embrace productive paranoia. The next crisis is coming—food safety, labor strikes, supply chain disruption, something. Build redundancy. Create contingency plans. Stress test everything. The companies that survive decades are those that prepare for disasters during good times.

XI. Recent News Update### **

Recent Developments Under Scott Boatwright (2024-2025)**

The burrito chain announced Scott Boatwright as its permanent CEO in November 2024, following his successful interim leadership since Niccol's departure. The transition has been rockier than anticipated, with Chipotle's same-store sales falling in the first quarter for the first time since 2020 as the company reported weaker-than-expected quarterly revenue.

Customers started pulling back their spending in February because of economic uncertainty, CEO Scott Boatwright told analysts on the company's conference call. "We could see this in our visitation study, where saving money because of concerns around the economy was the overwhelming reason consumers were reducing the frequency of restaurant visits," he said, adding that the traffic slowdown has continued into April.

The challenges have persisted through 2025. The Newport Beach, California-based burrito-bowl chain reported sagging earnings Wednesday, including a 4% same-store sales decline and 4.9% dip in quarterly traffic. While Chipotle saw a 3% total revenue increase to $3.1 billion, the company cut its guidance, now expecting flat same-store sales growth for the year compared to its previous prediction of a low single-digit increase.

Boatwright's response has been to refocus on value perception and hospitality. "I don't think we're getting credit with the consumer today," Boatwright told investors on Wednesday. Boatwright claimed in the earnings presentation Chipotle is 20% to 30% cheaper than comparable fast-casual restaurants. He told Fortune in April the chain wouldn't increase prices due to tariffs because "it's unfair to the consumer to pass those costs off…because pricing is permanent".

The new CEO is also bringing a softer touch to operations. "Our team members got so focused on creating the experience efficiently that they can just forget to smile," Boatwright tells Fortune in a recent interview at Chipotle headquarters in Newport Beach, Calif. But it does mean basic greetings and questions like "What can I make fresh for you today?" or phrases like "Thank you for spending your hard-earned money at Chipotle," which Boatwright says do not slow employees down, but rather add a more welcoming vibe to what is after all a hospitality business.