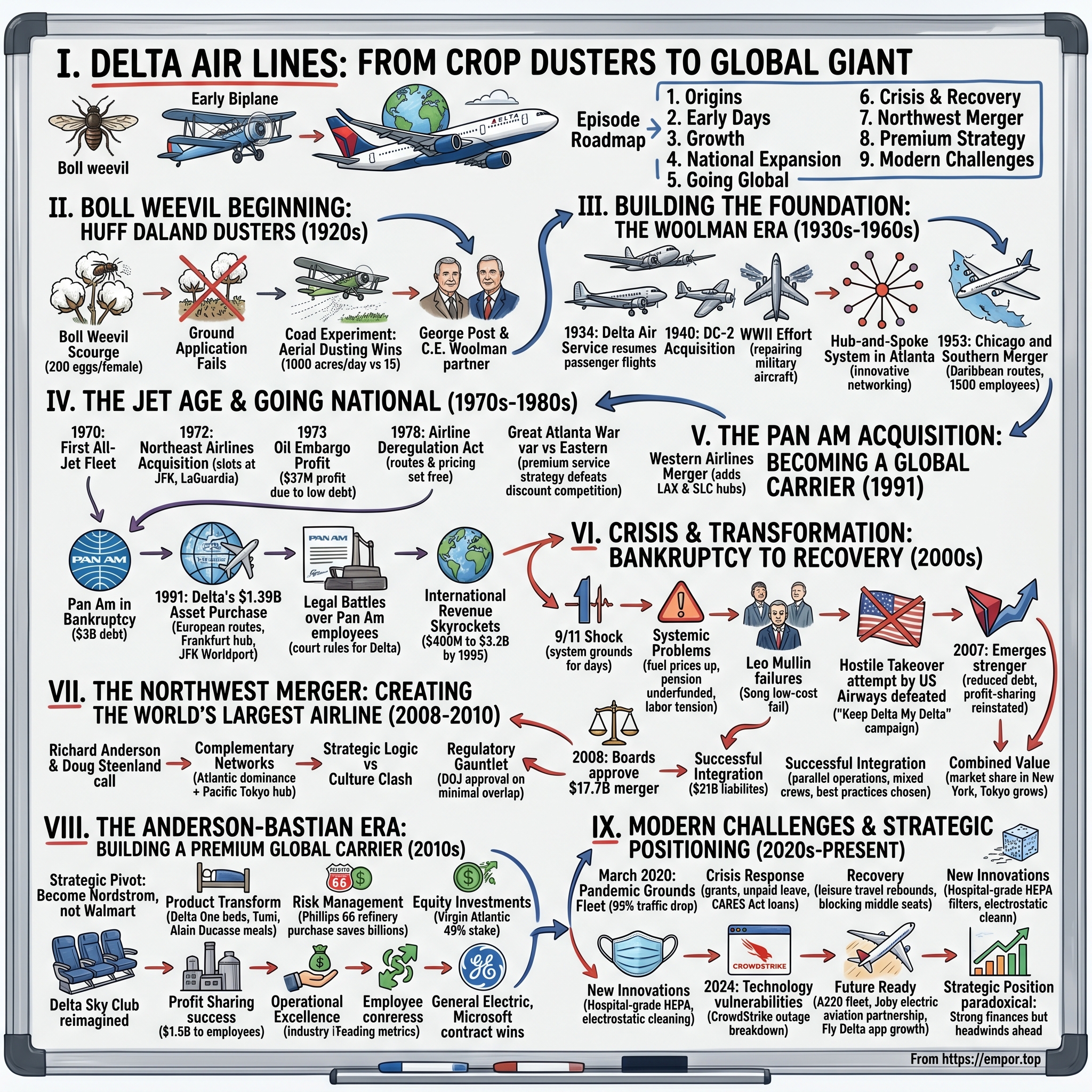

Delta Air Lines: From Crop Dusters to Global Giant

I. Introduction & Episode Roadmap

Picture this: A swarm of insects smaller than a fingernail brings the American South to its knees. Cotton fields from Texas to the Carolinas wither as the boll weevil—that "little black devil" as farmers called it—devours $200 million worth of crops annually by the 1920s. The U.S. Department of Agriculture declares it the worst agricultural disaster in American history. In response, a ragtag group of World War I pilots, agricultural scientists, and Louisiana businessmen launch the world's first aerial crop-dusting company. Their weapon? Modified biplanes loaded with calcium arsenate powder, diving low over cotton fields in death-defying runs.

This is where Delta Air Lines begins—not in some gleaming corporate boardroom or with venture capital backing, but in the muddy fields of Monroe, Louisiana, fighting bugs.

Today, Delta generates over $50 billion in annual revenue, flies nearly 200 million passengers yearly, and commands the highest brand value among global airlines. It operates from the world's busiest airport in Atlanta, maintains the industry's best operational metrics, and distributes billions in profit-sharing to employees. The transformation from crop duster to global aviation powerhouse represents one of American business's most improbable success stories.

How does a company make this leap? How does fighting agricultural pests in rural Louisiana evolve into competing with century-old European flag carriers for premium transatlantic business? The answer lies in a unique combination of Southern culture meeting global ambition, an obsession with operational excellence that borders on the religious, and a mastery of strategic acquisitions that would make any private equity firm envious.

This is the story of Delta—a company that shouldn't exist in its current form, built through bankruptcies, hostile takeovers, and industry consolidation wars, yet somehow emerged as the gold standard of American aviation. It's a tale of how culture beats strategy, how premium beats cheap, and how sometimes the best business model is simply refusing to be as terrible as your competitors.

II. The Boll Weevil Beginning: Huff Daland Dusters (1920s)

The boll weevil crossed the Rio Grande from Mexico in 1892, and by 1922 had infested nearly all U.S. cotton-growing areas. Each female beetle could lay 200 eggs, creating exponential destruction. Cotton production in infested areas dropped by 50%. The South's entire economy—still recovering from the Civil War—faced existential threat.

Enter B.R. Coad, a USDA entomologist stationed in Tallulah, Louisiana. Coad had been experimenting with calcium arsenate dust to kill the weevils, but ground-based application was slow and ineffective. In 1922, he convinced the Army Air Service to loan him a Curtiss JN-4 "Jenny" biplane and a pilot. The results were revolutionary: aerial dusting could cover 1,000 acres per day versus 15 acres by mule-drawn equipment.

George Post, a New York engineer, saw opportunity. He partnered with Ogden Phipps, heir to a steel fortune, to organize aerial crop dusting as a commercial enterprise. They recruited C.E. Woolman, an agricultural extension agent with Louisiana State University who understood both farming and the emerging aviation industry. Woolman would become Delta's founding genius—a man who spoke the language of Southern farmers while envisioning transcontinental aviation networks.

On March 2, 1925, Huff Daland Dusters incorporated in Macon, Georgia, becoming the world's first aerial crop-dusting company. The company operated eighteen DH.4B biplanes modified with hoppers and dust-spreading equipment. Pilots flew at treetop level—often below 10 feet—in open cockpits, breathing calcium arsenate dust that would later be banned as a deadly poison. They called themselves "dustermen" and developed a cowboy culture of risk-taking that would permeate Delta's DNA.

The business model was elegant: charge farmers $4-7 per acre for dusting, covering 500-1,000 acres daily per plane. With cotton selling at 20 cents per pound and dusting increasing yields by 100-200 pounds per acre, the economics worked. By 1925's end, Huff Daland had dusted 60,000 acres and saved millions in cotton crops.

But the company faced a geographic problem. Crop dusting was seasonal—active only during summer growing months. Planes and pilots sat idle for half the year, burning capital. The Peru venture in 1927—establishing operations in South America where seasons were reversed—proved disastrous due to political instability and payment collection issues.

C.E. Woolman saw a different future. While company executives in New York focused on international expansion, Woolman noticed something happening in the American South: cities were growing, businesses needed to move people and mail quickly, and no adequate transportation infrastructure existed. The same planes dusting cotton could carry passengers and mail year-round.

In 1928, Woolman organized local Monroe investors to purchase Huff Daland's assets. On December 3, 1928, they incorporated Delta Air Service, named after the Mississippi Delta region they served. The investors weren't Wall Street financiers but local merchants, planters, and professionals who understood the South's transportation needs. Travis Oliver, a Monroe businessman, became president, with Woolman as vice president and general manager.

Delta started passenger service on June 17, 1929, with a single-route from Dallas to Jackson, Mississippi, via Shreveport and Monroe. The first passenger was S.H. Lynch, a traveling salesman who paid $65 for the Dallas-Jackson journey—equivalent to about $1,100 today. The five-passenger Travel Air S-6000-B aircraft featured innovations considered luxurious: enclosed cabins, leather seats, and windows passengers could actually see through.

The timing seemed perfect. Commercial aviation was booming nationally, with passenger traffic doubling annually. Delta expanded rapidly, adding routes to Birmingham and Atlanta. By late 1929, the airline operated multiple daily flights and carried mail under federal contract—a crucial revenue source that provided steady cash flow.

Then October 29, 1929 arrived. The stock market crashed, beginning the Great Depression. Within months, passenger traffic evaporated. Business travelers—Delta's primary customers—stopped flying. The airmail contracts that provided financial stability were cancelled in the 1930 "Spoils Conference" scandal, where Postmaster General Walter Brown redistributed routes to favored carriers. Delta, lacking political connections, lost everything.

By 1930, Delta ceased passenger operations entirely, reverting to crop dusting to survive. Most aviation companies of this era disappeared. Of the 44 airlines operating in 1929, only a handful would survive the Depression. But Woolman refused to liquidate. He maintained the corporate structure, kept key personnel on partial pay, and waited. This patience—this refusal to panic during crisis—would become a defining Delta characteristic.

The company learned crucial lessons during these dark years. First, diversification mattered: crop dusting revenue, though modest, provided survival cash flow when passenger service disappeared. Second, local ownership created patient capital: Monroe investors, unlike Wall Street speculators, didn't demand immediate returns. Third, operational excellence meant survival: Delta's perfect safety record and reliable service built reputation capital that would matter when passenger service resumed.

Woolman also used the hiatus to study the industry's evolution. He observed how airlines like United and American were consolidating, building transcontinental routes, and leveraging mail contracts for growth. He studied their hub-and-spoke systems, their fleet strategies, their labor relations. When Delta returned to passenger service, it would apply these lessons with Southern efficiency.

The boll weevil had created Delta, but the Depression forged its character: conservative financially, operationally obsessed, comfortable with crisis, and patient in pursuit of opportunity. These traits—born in Louisiana cotton fields and hardened by economic catastrophe—would define Delta for the next century.

III. Building the Foundation: The Woolman Era (1930s–1960s)

The summer of 1934 brought redemption. The Air Mail Act of 1934, following the disastrous "Air Mail Scandal" where Army pilots died trying to fly mail routes, reopened bidding to private carriers. Woolman had prepared meticulously, maintaining Delta's certifications and keeping skeleton crews trained. When Route 24 (Charleston-Dallas via Atlanta) came available, Delta won with a low bid of 23.93 cents per mile. On July 4, 1934, passenger service resumed with a single Stinson-A trimotor aircraft.

This time, Woolman built differently. Instead of rapid expansion, he focused on profitable routes and operational reliability. Delta's on-time performance exceeded 95% when industry average was below 75%. The airline developed a reputation: "Delta gets you there." By 1935, passenger revenue exceeded mail revenue—unusual in an industry still dependent on government contracts.

The DC-2 acquisition in 1940 marked Delta's technological coming-of-age. Douglas Aircraft's revolutionary all-metal monoplane could carry 14 passengers at 170 mph—50% faster than Delta's existing fleet. Woolman negotiated personally with Donald Douglas, securing favorable financing terms by guaranteeing purchase of multiple aircraft. The DC-3 followed in 1941, becoming the workhorse that would define commercial aviation for a generation.

December 1941 changed everything. Within days of Pearl Harbor, the military requisitioned half of Delta's fleet and most experienced pilots. The airline could have suspended operations like many competitors. Instead, Woolman volunteered Delta's facilities for the war effort. The Atlanta hangar became a modification center for military aircraft. Delta mechanics installed gun turrets on B-29 bombers. The company trained 7,000 military pilots and mechanics. Revenue from military contracts exceeded peacetime passenger revenue, but more importantly, Delta gained expertise in large-scale operations and complex logistics.

The 1941 headquarters move to Atlanta proved visionary. Woolman chose Atlanta not for its current size—it ranked 30th among U.S. cities—but for its potential. No mountains complicated flight paths. Weather was generally favorable. Most importantly, Atlanta sat at the geographic center of the Southeast, equidistant from major Southern cities. While competitors fought over New York and Chicago, Delta quietly built a Southern empire.

Post-war expansion came methodically. On May 1, 1945, the company officially became Delta Air Lines, Inc., signaling national ambitions. Routes expanded to Cincinnati, Miami, and New Orleans. But the real innovation was operational. In 1947, Delta introduced the "hub-and-spoke" system in Atlanta, though they didn't call it that. Instead of point-to-point routes, flights were scheduled to arrive in Atlanta within minutes of each other, allowing passengers to connect quickly to outbound flights. The noon "push"—with 20 flights arriving and departing within an hour—created the world's busiest air transfer point.

The economics were transformative. A route from Savannah to Memphis might not support direct service, but connecting through Atlanta made both legs profitable. Network effects multiplied: each new spoke made every other spoke more valuable. Competitors initially mocked the system as inefficient. Why fly through Atlanta when you could fly direct? They missed the point: most city pairs couldn't support direct service. Delta's hub system made hundreds of previously impossible routes economically viable.

The 1953 Chicago and Southern Air Lines merger brought international credibility. C&S operated routes to the Caribbean and Caracas—Delta's first international services. More importantly, C&S brought experienced international operations staff and government relationships. The $32 million stock swap was Delta's largest transaction to date, adding 1,500 employees and doubling route miles. Integration went smoothly because Woolman insisted on cultural fit: C&S shared Delta's Southern roots and operational focus.

Technology adoption accelerated under Woolman's leadership. Delta was first to fly the Douglas DC-8 jet in 1959, beating Eastern and National on competitive Florida routes. First with the Convair 880 in 1960, offering speeds approaching 600 mph. First to operate the McDonnell Douglas DC-9 in 1965, perfect for shorter spoke routes. Each aircraft introduction followed Woolman's pattern: negotiate aggressively on price, train exhaustively on operations, market relentlessly on passenger benefits.

The cultural foundation Woolman built proved more important than any aircraft purchase. He knew every employee's name—all 6,000 by 1960. He ate in the employee cafeteria, not executive dining rooms. During the 1955 pilot strike threat, Woolman met personally with pilot representatives, listening for twelve hours straight to grievances. The strike never materialized. Delta pilots wouldn't organize a union until 2008—decades after every other major carrier.

"The Delta Family" wasn't corporate propaganda but lived reality. Profit-sharing began in 1953, revolutionary for the era. Employee Christmas parties included everyone from baggage handlers to board members. When financial pressures mounted, executives took pay cuts before any frontline employee was laid off. This created fanatical loyalty. Delta employees routinely worked off-the-clock to ensure on-time departures. Gate agents personally ran to find connecting passengers. The culture produced industry-leading operational metrics that no amount of consulting could replicate.

Woolman's health declined through 1966. Diabetes and heart disease—the costs of decades of eighteen-hour days and constant travel—took their toll. On September 11, 1966, he died at Emory Hospital in Atlanta. Twenty thousand people attended his funeral. Pilots wore black armbands for a month. The New York Times obituary called him "the most beloved airline executive in history."

Charles H. Dolson, Delta's financial architect since 1945, became CEO. But Woolman's imprint was indelible. He had transformed crop dusters into a major airline through patient capital allocation, operational excellence, and most importantly, treating employees as partners rather than costs. Revenue had grown from $243,000 in 1934 to $256 million in 1966. The airline that started with a single three-passenger plane now operated 119 jets.

Yet Woolman's greatest achievement wasn't growth but institutionalized culture. The "Delta Difference"—exceptional service delivered by motivated employees—became self-perpetuating. New hires were selected for cultural fit over credentials. Senior employees mentored juniors in "the Delta way." Stories of exceptional service became organizational mythology, setting expectations for each generation.

This cultural foundation would be tested in coming decades by deregulation, consolidation, and crisis. But it would endure, providing competitive advantage no balance sheet could capture. As Woolman often said, "Running an airline is like having a baby: fun to conceive, hell to deliver, but once you have it, you wouldn't take a million dollars for it."

IV. The Jet Age & Going National (1970s–1980s)

On January 15, 1970, Delta retired its last propeller aircraft, a Convair 440 operating the Atlanta-Columbus, Georgia route. The ceremony at Hartsfield Airport attracted thousands of employees and aviation enthusiasts. Captain Tom Brooks, who had flown props since 1942, took the controls for the final flight. Upon landing, he handed the keys to CEO Charles Dolson and said, "We're a jet airline now." Delta became the world's first all-jet carrier—beating United by six months and American by nearly a year.

The achievement required massive capital investment. Converting to jets meant spending $1.2 billion on aircraft between 1965-1970—more than Delta's total revenue in 1969. But the economics were compelling: jets flew twice as fast, carried three times more passengers, and required 40% less maintenance per seat-mile. The DC-9 could complete five Atlanta-Birmingham round trips daily versus three for a prop. Revenue per aircraft doubled while operating costs increased only 30%.

The Northeast Airlines acquisition in August 1972 transformed Delta from regional carrier to national powerhouse. Northeast, teetering on bankruptcy, operated lucrative Boston-New York-Florida routes but suffered from aging aircraft and toxic labor relations. Delta paid $38.5 million—mostly assumed debt—for assets worth $200 million. The real prize: gates and slots at Logan and LaGuardia, nearly impossible to obtain otherwise.

Integration proved challenging. Northeast's unionized culture clashed with Delta's family atmosphere. Boston mechanics, accustomed to strict work rules, were baffled when Atlanta colleagues helped load bags during delays. Some Northeast pilots refused to wear Delta's required ties, viewing it as corporate oppression. Tom Beebe, who succeeded Dolson as CEO in 1971, spent months in Boston personally meeting with former Northeast employees, explaining Delta culture not as rules but as shared pride.

The merger's success hinged on small gestures. Delta honored all Northeast pension obligations, unusual in airline acquisitions. Seniority lists were merged fairly, with no Delta preference. Within eighteen months, operational metrics at Boston matched Atlanta standards. Former Northeast employees, initially skeptical, became Delta evangelists. The transformation proved cultural integration could overcome operational differences.

Then came 1973's oil embargo. Fuel prices quadrupled overnight. Airlines globally hemorrhaged cash—Braniff lost $50 million, Eastern $80 million. Delta? Posted a $37 million profit. The difference was Woolman's conservative legacy: Delta maintained the industry's lowest debt levels, owned rather than leased most aircraft, and kept six months of cash reserves. When competitors desperately sold aircraft at fire-sale prices, Delta bought, acquiring nearly-new 727s at 40% discounts.

International expansion accelerated under CEO David Garrett, who succeeded Beebe in 1978. The first transatlantic flight—Atlanta to London on April 30, 1978—marked Delta's evolution into a global carrier. The L-1011 TriStar wide-body aircraft, configured with unprecedented legroom and Delta's first business class, challenged Pan Am and TWA on premium routes. Load factors exceeded 85% within six months, validating demand for Southern-originated international service.

But 1978 brought seismic disruption: the Airline Deregulation Act. Overnight, four decades of regulated routes and pricing ended. Any carrier could fly anywhere, charge anything. New entrants like People Express offered $29 transcontinental fares. Industry experts predicted only three or four carriers would survive the carnage.

Frank Borman, Eastern's CEO and former astronaut, declared, "Deregulation will destroy Delta. They've been protected in Atlanta like a hothouse flower. Real competition will kill them." He launched an all-out assault on Delta's hub, adding fifty daily Atlanta flights. The "Great Atlanta War" of 1979-1980 saw Eastern, Braniff, and newcomer PeoplExpress slash fares below cost, attempting to break Delta's fortress.

Delta's response surprised everyone: they didn't match the lowest fares. Instead, Garrett articulated what became Delta's enduring strategy: "We're not in the transportation business. We're in the customer service business that happens to use airplanes." Delta maintained higher fares but guaranteed on-time performance, no overbooking, and free bag checking. Business travelers, valuing reliability over price, remained loyal. By 1981, Eastern retreated from Atlanta, Braniff entered bankruptcy, and People Express never gained foothold.

The Western Airlines merger in 1987 demonstrated Delta's acquisition mastery. Western, the oldest U.S. carrier, dominated Los Angeles and Salt Lake City but struggled financially. The $860 million purchase price seemed high—Western lost money five of the previous seven years. But Delta saw hidden value: Western's Salt Lake hub perfectly positioned for Asia-Pacific expansion, their Los Angeles presence countered American's fortress hub, and the fleet of efficient 737s and DC-10s fit Delta's needs.

Ronald Allen, who became CEO in 1987, personally managed integration. He established "merger committees" pairing Delta and Western employees in every department. Rather than impose Atlanta methods, committees identified best practices from either airline. Western's superior Pacific cargo operations were adopted system-wide. Delta's customer service training became standard. Within a year, the combined airline achieved the industry's best on-time performance and lowest complaint ratio.

The smoking ban decision in 1987 epitomized Delta's willingness to lead. When other carriers worried about losing passengers, Delta unilaterally banned smoking on all flights—first among U.S. carriers. The decision cost an estimated $50 million in lost bookings initially. But health-conscious business travelers shifted to Delta, more than offsetting losses. Within two years, federal law mandated smoking bans, but Delta had already captured market share and reputation benefit.

Throughout the 1980s, Atlanta's hub grew to staggering proportions. By 1989, Delta operated 650 daily departures from Hartsfield—more than LaGuardia's total operations. The hub generated network effects competitors couldn't replicate: a Birmingham business traveler could reach 142 cities with one stop, versus 31 on any other carrier. Delta's 75% market share in Atlanta created pricing power that funded expansion elsewhere.

The decade closed with Delta as America's third-largest airline by revenue, fourth by passengers, but first in profitability. Stock price increased 400% from 1980-1989, outperforming every major competitor. The airline had successfully navigated deregulation, executed two major mergers, and built sustainable competitive advantages in operational excellence and network strength.

Yet challenges loomed. International expansion remained limited compared to Pan Am or TWA. Labor relations, while positive, grew strained as pay lagged competitors. New low-cost carriers like Southwest challenged the hub economics. The 1990s would test whether Delta's culture and strategy could sustain success in an increasingly global, competitive market.

V. The Pan Am Acquisition: Becoming a Global Carrier (1991)

Juan Trippe built Pan American World Airways as America's unofficial flag carrier—the "blue chip" of aviation that pioneered transpacific routes, introduced the 747, and flew the Beatles to America. By 1991, Pan Am was dying. The Lockerbie bombing, Gulf War, and decades of mismanagement left the icon with $3 billion in debt, losing $3 million daily. On July 8, 1991, Pan Am's board gathered at the airline's Park Avenue headquarters for what everyone knew was the end.

Russell Ray, Delta's CFO, had been secretly negotiating with Pan Am for months. The initial ask was staggering: $1.5 billion for the entire airline. Delta's internal analysis valued Pan Am at negative $500 million—liabilities exceeded assets. But Ray saw opportunity in pieces: the European routes generated $2 billion annually, the Frankfurt hub connected to 35 cities, and the Pan Am Worldport at JFK handled 10 million passengers yearly. Most valuable were the "slots"—government-granted takeoff and landing rights at congested airports, impossible to obtain except through acquisition.

Carl Icahn's TWA bid first, offering $1.2 billion for everything. United and American countered with a joint $1.3 billion bid, planning to split assets. The Justice Department would never approve competitors collaborating, but Pan Am's desperation made any deal attractive. Stephen Wolf, United's CEO, privately told analysts, "We'll own international aviation. Delta will be stuck flying Birmingham to Baton Rouge forever."

On August 12, 1991, Ronald Allen convened Delta's board for an emergency session. The presentation was stark: matching competing bids meant betting 40% of Delta's market capitalization on a failed airline's assets. Board member Eugene Callaway, former U.S. Ambassador to the UN, asked the crucial question: "Can Delta remain competitive without international expansion?" Allen's answer: "We'll become a regional carrier within a decade. The industry is consolidating globally. This is our only chance."

Delta offered $1.39 billion but with a twist—they wanted only profitable assets: European routes, the Frankfurt mini-hub, Northeast Shuttle operations, 45 aircraft, and JFK facilities. The remaining airline—Pacific routes, Latin American operations, the Pan Am building—would continue operating independently. Pan Am's board, facing imminent bankruptcy, accepted on August 12. The announcement shocked the industry. Delta, the conservative Southern airline, had just made the largest route acquisition in aviation history.

Thomas Plaskett, Pan Am's CEO, promised employees Delta would provide additional financing to keep Pan Am alive. Allen made no such commitment. The purchase agreement explicitly stated Delta had no obligation beyond the asset purchase. This distinction would prove catastrophic for Pan Am's 7,500 remaining employees.

Integration began immediately. Delta teams descended on Pan Am facilities worldwide, evaluating everything from landing slots to coffee suppliers. The Frankfurt hub alone required 2,000 Delta employees to relocate. Language barriers, cultural differences, and operational complexity dwarfed previous mergers. Pan Am operated differently—international flights required multilingual crews, complex customs procedures, and diplomatic protocols Delta had never encountered.

The most valuable assets were intangible. Pan Am's route authorities to London, Paris, and Frankfurt had taken decades to negotiate. Delta inherited grandfather rights dating to the 1940s—permissions no amount of money could buy today. The Heathrow slots alone analysts valued at $500 million. Delta overnight became the largest U.S. transatlantic carrier, operating 80 daily flights to 30 European cities.

But Pan Am's collapse accelerated. Without European revenue, losses reached $10 million daily. Plaskett begged Allen for emergency funding. Allen refused, stating Delta had fulfilled all contractual obligations. On December 4, 1991, Pan Am ceased operations. The final flight, PA 436 from Barbados to Miami, landed at 2:45 AM. Captain Mark Pyle announced to passengers: "This is the end of 64 years of Pan American Airways." Many crew members wept openly.

The aftermath was ugly. Pan Am creditors, owed $2.5 billion, sued Delta for "fraudulent conveyance," claiming Delta deliberately structured the deal to force Pan Am's liquidation. Internal Pan Am documents revealed Plaskett believed Delta had made verbal commitments to provide additional funding. Edwin Russell, representing creditors, called it "corporate murder—Delta killed Pan Am to eliminate competition."

The legal battle consumed four years. Delta argued they saved what could be saved—without the acquisition, all Pan Am assets would have been liquidated. In 1994, bankruptcy judge Cornelius Blackshear ruled for Delta, finding no evidence of verbal commitments or fraudulent intent. The decision established precedent: buyers of distressed assets have no obligation to save selling companies.

Operationally, the Pan Am integration exceeded expectations. Frankfurt became Delta's European hub, feeding traffic from 35 cities to Atlanta. The Shuttle, rebranded Delta Shuttle, dominated Boston-New York-Washington traffic with 60% market share. JFK's Worldport, though aging, provided critical New York international presence. Within eighteen months, former Pan Am routes generated $500 million in operating profit.

Cultural integration proved harder. Pan Am employees—pilots who had flown presidents, flight attendants who spoke six languages—bristled at Delta's "Southern hospitality" training. They viewed themselves as sophisticated internationalists, not regional service workers. David Duvel, a former Pan Am captain, recalled: "We flew Sinatra to Rome, Kennedy to Berlin. Now they wanted us to serve peanuts with a drawl?"

Ronald Allen addressed the tension directly. At a Frankfurt employee meeting, he acknowledged Pan Am's legacy but insisted on Delta standards: "Pan Am was about glamour. Delta is about reliability. Our passengers don't need champagne and caviar. They need to arrive on time with their luggage." Some Pan Am veterans left for competitors. Those who stayed gradually absorbed Delta culture, creating a hybrid—internationally sophisticated but operationally disciplined.

The financial returns validated the acquisition. International revenue grew from $400 million in 1990 to $3.2 billion by 1995. The Frankfurt hub's connections to Eastern Europe, opened after communism's fall, generated enormous traffic. London-Atlanta became Delta's most profitable route, with business class yields exceeding $4,000 per passenger. The purchase price was recovered within four years through operating profits alone.

Yet the human cost haunted Delta's reputation. Twenty thousand Pan Am employees lost jobs without severance. Delta hired only 5,000, cherry-picking the best talent. The airline industry learned a harsh lesson: in distressed acquisitions, buyers hold all power. Critics called Delta ruthless, abandoning its family values for Wall Street returns.

Allen defended the decision until his death: "Business isn't charity. We saved what made economic sense. If we had tried to save all of Pan Am, both airlines would have failed. Five thousand jobs and continued service to millions of passengers is better than nothing." The logic was sound, but Delta's carefully cultivated image as the caring airline suffered permanent damage.

The Pan Am acquisition transformed Delta into a truly global carrier, but at a price beyond dollars. The conservative, employee-focused culture collided with harsh financial reality. Future acquisitions would require balancing growth ambitions with human consequences—a lesson learned through Pan Am's employees' suffering.

VI. Crisis & Transformation: Bankruptcy to Recovery (2000s)

September 11, 2001, 8:46 AM: American Airlines Flight 11 struck the North Tower. Within hours, U.S. airspace closed for the first time in history. Delta had 623 aircraft airborne, forced to land immediately wherever possible. Flight 15 from Frankfurt landed in Newfoundland, where passengers spent five days sleeping in schools. The industry lost $10 billion in September alone. Delta's daily cash burn reached $20 million.

Leo Mullin, CEO since 1997, faced impossible choices. A Harvard MBA and former investment banker, Mullin understood finance but struggled with airline operations. His response to 9/11 mixed necessary cuts with strategic blunders. Delta eliminated 13,000 jobs—20% of workforce—while maintaining executive bonuses. The symbolism was devastating. Mechanics who had worked thirty years received two weeks' severance while Mullin collected $10 million in compensation.

The operational decisions proved worse. To cut costs, Mullin outsourced heavy maintenance to contractors in Mexico and El Salvador. Quality plummeted. Delta's on-time performance fell from first to worst among major carriers. In 2003, a Delta MD-88 lost cabin pressure due to improper maintenance, forcing an emergency landing. Nobody died, but the FAA investigation revealed systemic maintenance failures. The fine—$9.5 million—was then the largest in aviation history.

Mullin's growth strategy—launching low-cost carrier Song to compete with JetBlue—became a legendary failure. Song burned through $500 million trying to be hip, with flight attendants in Kate Spade uniforms serving organic food. But Delta's cost structure made competing on price impossible. Song's cost per seat mile was 11 cents versus JetBlue's 6 cents. As one analyst noted: "It's like Tiffany trying to compete with Walmart by painting their store blue."

Meanwhile, fuel prices exploded from $25 per barrel in 2001 to $70 by 2005. Every dollar increase cost Delta $60 million annually. The airline's pension obligations—$5.6 billion underfunded—consumed cash needed for operations. Labor relations deteriorated as pilots, who had accepted 32% pay cuts post-9/11, watched executives receive retention bonuses. In 2004, pilots refused voluntary overtime, causing hundreds of Christmas flight cancellations.

The board fired Mullin in December 2003, bringing back Gerald Grinstein, who had served as CEO of Western Airlines before its Delta merger. Grinstein, then 71, took the job for $500,000 annually—symbolic pay demonstrating shared sacrifice. His first all-employee broadcast was blunt: "We're months from bankruptcy. We either transform everything or cease to exist."

Grinstein implemented "Operation Clockwork"—a back-to-basics focus on operational excellence. Decisions were pushed down to frontline employees. Gate agents could authorize compensation for delays without supervisor approval. Maintenance shifted back in-house with aggressive hiring of experienced mechanics. Within six months, on-time performance improved from 65% to 78%.

But financial mathematics remained brutal. Despite $2.8 billion in labor concessions, Delta lost $5.2 billion in 2004. Credit markets, burned by United and US Airways bankruptcies, refused additional financing. On September 14, 2005, Delta filed Chapter 11 bankruptcy, listing $21 billion in liabilities against $17 billion in assets.

The bankruptcy filing was precisely orchestrated. Unlike Eastern or Pan Am's chaotic collapses, Delta maintained full operations. Grinstein personally called major corporate clients, guaranteeing continued service. The airline had arranged $2.8 billion in DIP (debtor-in-possession) financing, ensuring liquidity during restructuring. Passengers barely noticed—flights operated normally, frequent flyer miles remained valid, and service quality actually improved as employees rallied.

Then came the hostile takeover attempt. Doug Parker, CEO of US Airways, announced an $8.7 billion bid for Delta on November 15, 2006. Parker promised $1.65 billion in synergies, mainly from eliminating Atlanta-Charlotte hub overlap. The creditors' committee, owed $15 billion, initially supported the deal—cash today beats promises tomorrow.

Grinstein mobilized resistance. Delta employees organized "Keep Delta My Delta" rallies. Twenty thousand employees protested at Atlanta's airport. Politicians from Georgia to New York opposed losing hometown airline headquarters. Richard Anderson, former Northwest CEO working as a healthcare executive, was recruited to lead Delta post-bankruptcy. His credibility with creditors—having successfully restructured Northwest—shifted sentiment.

The decisive moment came at the creditors' hearing on December 19, 2006. Anderson presented Delta's standalone plan: emerging from bankruptcy debt-free, with $2.5 billion in exit financing arranged, projecting $3 billion operating profit by 2010. When asked why creditors should reject US Airways' cash offer, Anderson responded: "Because Delta's network, culture, and Atlanta hub are worth more than any competitor will pay. We're not just an airline—we're an economic engine for the entire Southeast."

On January 31, 2007, creditors rejected US Airways' bid. Delta emerged from bankruptcy on April 30, 2007—the first major carrier to successfully restructure without merger or liquidation. The transformation was remarkable: debt reduced from $17 billion to $7 billion, labor costs cut 30%, fleet rationalized from eleven aircraft types to six. Most importantly, employee profit-sharing was reinstated, aligning interests after years of adversarial relations.

Anderson became CEO on September 1, 2007. His first executive meeting set the tone: "Bankruptcy is over. Excuses are over. We're going to become the world's premier airline or die trying." The strategy had three pillars: operational excellence (return to Woolman's basics), network expansion (particularly international), and brand transformation (from discount to premium).

Early results vindicated the standalone strategy. In 2007's fourth quarter—traditionally weak—Delta posted $220 million profit while US Airways lost $79 million. The Atlanta hub, which Parker planned to shrink, was expanded to 1,000 daily flights. International expansion accelerated with new routes to Africa, India, and China. The stock, issued at $20 upon bankruptcy exit, reached $40 within eighteen months.

The bankruptcy experience fundamentally changed Delta's DNA. The near-death experience eliminated complacency. Employees who had fought to save their airline developed fierce loyalty. Management learned that financial engineering without operational excellence leads to failure. Most importantly, the crisis proved Delta's culture—though strained—could survive even bankruptcy.

Grinstein retired in 2007, declining any retirement package beyond his pension. At his farewell, he told employees: "You saved Delta. Not me, not the board, not the creditors. You did it by remembering what made this airline special—taking care of customers and each other." The bankruptcy that should have killed Delta instead catalyzed its transformation into the industry's strongest carrier.

VII. The Northwest Merger: Creating the World's Largest Airline (2008–2010)

Richard Anderson's phone rang at 5:47 AM on January 17, 2008. Doug Steenland, Northwest's CEO and Anderson's former colleague, had a proposition: "Richard, let's build something historic. Northwest and Delta together." Anderson had been expecting this call. Oil had reached $100 per barrel. Industry consolidation was inevitable. The only questions were who would merge with whom, and who would lead.

The strategic logic was compelling. Delta dominated the Atlantic with its European network inherited from Pan Am. Northwest ruled the Pacific through its Tokyo Narita hub—the only U.S. carrier with beyond-rights to fly from Japan to other Asian cities, a privilege from post-World War II occupation. Delta was strong in the South and East Coast. Northwest owned the upper Midwest through Minneapolis and Detroit hubs. Fleet overlap was minimal: Delta flew Boeing 767s and 777s internationally while Northwest operated 747s and A330s. Combined, they would operate 786 aircraft to 390 destinations—the world's largest airline.

But logic doesn't address culture, and culturally, these airlines were from different planets. Delta employees called Northwest "Northworst" for its notorious service. Northwest called Delta "Southern comfort" for perceived operational softness. Delta flight attendants served with genuine warmth. Northwest flight attendants, battle-hardened from decades of labor strife, viewed passengers as potential combatants. A Northwest pilot joke: "What's the difference between Northwest and Delta? Delta employees smile when they screw you."

Anderson understood cultural integration would determine success. He recruited Ed Bastian, Delta's former CFO who had returned as President, to lead merger planning. Bastian assembled "clean teams"—employees from both airlines who could share information without violating antitrust laws. The first clean team meeting in February 2008 was awkward. Northwest representatives arrived in dark suits with briefcases. Delta representatives wore polo shirts and brought doughnuts. The culture clash was immediate and obvious.

The financial negotiations were brutal. Northwest wanted a merger of equals—50/50 ownership, co-headquarters in Atlanta and Minneapolis, alternating board chairs. Anderson's counter was harsh: Delta's market capitalization exceeded Northwest's by $1.7 billion. Delta emerged from bankruptcy stronger while Northwest still struggled. The final structure reflected reality: Delta shareholders owned 67%, Northwest 33%. Headquarters would be Atlanta. Anderson would be CEO.

On April 14, 2008, boards approved the $17.7 billion merger. The announcement shocked the industry. United and Continental, American and US Airways scrambled to respond. Within weeks, the entire industry was discussing consolidation. But Delta-Northwest had first-mover advantage, beginning integration planning while competitors remained in negotiation.

The regulatory gauntlet began immediately. The justice department worried about reduced competition, particularly on Detroit-Amsterdam and Minneapolis-Paris routes where both carriers operated. Labor unions opposed potential job losses. Politicians from Minnesota and Michigan fought to protect hometown hubs. Consumer advocates predicted higher fares and worse service.

Anderson and Steenland testified before Congress on May 14, 2008. Congressman James Oberstar of Minnesota, whose district included Northwest's headquarters, was hostile: "This merger will devastate Minnesota's economy and eliminate thousands of jobs." Anderson's response was carefully prepared: "Congressman, we commit to maintaining all hubs for at least two years and no frontline employee layoffs. This merger is about growth, not shrinkage."

The DOJ review took six months. Delta's legal team, led by General Counsel Ben Hirst, submitted 4 million documents demonstrating minimal route overlap. The key argument: Delta and Northwest were complementary, not competing networks. Of 1,200 combined routes, only 12 had both carriers—less than 1% overlap. On October 29, 2008, DOJ approved the merger without conditions—unprecedented for a transaction this size.

Meanwhile, Lehman Brothers had collapsed on September 15, triggering global financial crisis. Airline bookings evaporated. Credit markets froze. Oil prices swung wildly from $147 to $35 per barrel. Many analysts predicted Delta would abandon the merger. A Merrill Lynch report stated: "In this environment, integration risk is suicidal. Delta should walk away."

Anderson saw opportunity in crisis. With airline valuations crushed, the stock-for-stock exchange ratio now favored Delta. Integration could happen with less passenger disruption as overall traffic was down. Most importantly, competitors were too weakened to respond aggressively. On September 26, shareholders approved the merger—78% of Delta shares and 89% of Northwest shares voted yes.

The integration itself was methodically planned. Rather than immediate combination, Anderson implemented "parallel operations"—running two airlines with increasing coordination. Reservation systems remained separate for six months to avoid technical meltdowns that plagued previous mergers. Frequent flyer programs merged gradually with no member losing status. Route networks were optimized slowly—unprofitable routes eliminated, new connections added.

Labor integration proved most challenging. Northwest pilots, among the industry's highest paid, feared pay cuts. Delta pilots worried about seniority integration with a more senior Northwest group. The solution was expensive but necessary: no pilot would lose pay, and seniority lists would be merged by date of hire regardless of airline. The combined pilot group would receive industry-leading wages. Cost: $1 billion annually, but it bought labor peace.

The cultural transformation required deliberate intervention. Anderson created "7,000 ambassadors"—employees from each airline who spent weeks at the other's facilities. Delta employees learned Northwest's analytical rigor and cost discipline. Northwest employees absorbed Delta's customer service ethos. Mixed crews were deliberately scheduled—Delta captains with Northwest first officers, creating thousands of cultural exchanges at 35,000 feet.

Ed Bastian's integration leadership proved masterful. He established "rules of engagement": every meeting must have equal representation, all ideas would be evaluated on merit regardless of source, and "not invented here" syndrome was explicitly banned. When selecting operational procedures, teams chose best practices regardless of origin. Northwest's superior Pacific cargo operations became standard. Delta's customer service training was mandated system-wide.

December 31, 2009, marked legal completion when operating certificates merged. Northwest Airlines ceased to exist after 83 years. The final Northwest flight, NW 2470 from Los Angeles to Las Vegas, received water cannon salute. Captain Gary Peterson's final announcement: "Northwest airlines thanks you for your loyalty. Delta Air Lines looks forward to serving you." Many Northwest employees wore red dresses or ties—Northwest's signature color—as memorial.

The financial results exceeded all projections. Synergies reached $2 billion annually by 2010, double the initial estimate. The combined network generated revenue premiums: a Minneapolis-Amsterdam passenger paid 15% more for single-carrier service versus connections through other hubs. The Pacific network, enhanced by Delta's domestic feed, grew 40% within two years. Market share in key business markets like New York-Tokyo reached 35%.

More importantly, the merger triggered industry transformation. United merged with Continental in 2010. American merged with US Airways in 2013. Southwest acquired AirTran in 2011. Within five years, the U.S. airline industry consolidated from nine major carriers to four. The Delta-Northwest merger started the dominos falling.

By 2010, the cultural integration was largely complete. Former Northwest employees stopped identifying as "red tails" (Northwest's aircraft livery). Employee satisfaction scores equalized between legacy groups. Operational metrics—on-time performance, baggage handling, customer satisfaction—reached historic highs. The "Minnesota nice" service culture merged with "Southern hospitality" creating something unique: analytical rigor with human warmth.

Anderson reflected later: "We didn't just merge two airlines. We created a new model—the discipline of Northwest with the heart of Delta. That's why we succeeded where others failed." The numbers supported his claim. While United-Continental struggled with integration for years and American-US Airways faced labor strife, Delta posted record profits and industry-leading margins.

The Northwest merger wasn't just the largest in airline history—it was the most successful. It proved that with careful planning, cultural sensitivity, and employee engagement, even massive corporate combinations could create value rather than destroy it. The new Delta was more than the sum of its parts: a global network carrier with operational excellence that competitors couldn't match.

VIII. The Anderson-Bastian Era: Building a Premium Global Carrier (2010s)

Richard Anderson stood before 45,000 employees via satellite broadcast on January 3, 2011, delivering a message that would have seemed insane five years earlier: "We're going to become the world's most premium airline. Not the biggest, not the cheapest—the best." The industry laughed. Delta? The airline that had just exited bankruptcy? That served peanuts in coach? Premium?

Anderson's strategy reflected brutal math. Low-cost carriers like Spirit could operate at 6 cents per seat mile. Delta's cost was 14 cents. No amount of efficiency could close that gap—union contracts, hub infrastructure, and international operations created structural costs. The only solution: charge more by delivering more. "We can't out-Walmart Walmart," Anderson told his board. "But we can be Nordstrom."

The transformation started with product. Delta One—the new international business class introduced in 2011—featured fully flat beds, Tumi amenity kits, and Alain Ducasse-designed meals. The $2 billion cabin retrofit program upgraded every aircraft interior. Economy seats got additional legroom. In-flight entertainment systems offered 3,000 hours of content. Wi-Fi was installed fleet-wide—Delta was first to offer satellite-based internet on international flights.

But Anderson understood premium meant more than seats. In 2012, Delta shocked the industry by purchasing a Phillips 66 oil refinery in Trainer, Pennsylvania for $150 million. Analysts called it insane—what did an airline know about refining? The logic was risk management: jet fuel represented 35% of operating costs. The refinery could produce 185,000 barrels daily, covering 80% of Delta's domestic fuel needs. More importantly, it captured the "crack spread"—the profit margin between crude oil and refined jet fuel.

The refinery struggled initially, losing $63 million in 2012. Critics demanded Anderson admit failure. Instead, he hired refinery experts from ExxonMobil, invested another $100 million in upgrades, and shifted production entirely to jet fuel and diesel. By 2014, the refinery was profitable. During 2015's oil price collapse, when competitors hedged incorrectly and lost billions, Delta's refinery provided natural hedge. Total savings: $3.5 billion over the decade.

International expansion accelerated through strategic equity investments. The 2013 purchase of 49% of Virgin Atlantic for $360 million secured Heathrow access—the world's most valuable airport for business travel. Unlike arms-length alliances, equity investment aligned incentives. Delta and Virgin coordinated schedules, shared lounges, and jointly marketed to corporate clients. Revenue synergies exceeded $500 million annually.

The Sky Club transformation epitomized the premium strategy. Delta's lounges had been industry jokes—overcrowded rooms with stale pretzels and warm beer. Anderson hired Marriott executives to reimagine the experience. New clubs featured local cuisine, craft cocktails, shower suites, and workspace designed by Gensler. The $5 billion investment seemed excessive for airport lounges. But premium passengers spent 60% of travel time in airports. Superior lounges drove corporate contract wins.

May 2, 2016, marked transition when Ed Bastian became CEO after Anderson's promotion to Executive Chairman. Bastian, who had risen from internal auditor to President, understood Delta's operations intimately. His first memo to employees was revealing: "Richard taught us to think big. Now we execute flawlessly." Where Anderson was visionary, Bastian was operational. Where Anderson charmed Wall Street, Bastian focused on employees.

Bastian's signature initiative was industry-leading profit sharing. In 2016, Delta distributed $1.5 billion to employees—15% of annual wages. The February 14 "Valentine's Day" payment became cultural touchstone. Baggage handlers received $5,000 checks. Pilots got $30,000. The program cost more than competitors' entire profits, but Bastian defended it vigorously: "Employees who share in success deliver success."

The operational metrics validated the strategy. By 2017, Delta achieved:

- 85.7% on-time arrivals (industry average: 79.6%)

- 99.3% completion factor (industry average: 97.8%)

- 1.91 mishandled bags per 1,000 (industry average: 3.52)

- Lowest customer complaint ratio among major carriers

These weren't random achievements but systematic excellence. Delta pioneered predictive maintenance using sensors on every engine component. The Operations Control Center in Atlanta—a 40,000-square-foot facility monitoring every flight globally—could predict weather disruptions 72 hours in advance. When storms approached, Delta pre-cancelled flights and rebooked passengers before competitors recognized threats.

Corporate sales demonstrated premium strategy success. In 2018, Delta won General Electric's $150 million annual contract from United. GE's procurement head explained: "Delta's on-time performance meant our executives made meetings. That reliability was worth the 8% price premium." Similar wins with Microsoft, Coca-Cola, and McKinsey followed. Corporate revenue grew from $3.8 billion in 2010 to $7.2 billion by 2019.

The brand transformation was measurable. Net Promoter Score—likelihood customers recommend Delta—increased from 19 in 2010 to 44 in 2019, highest among U.S. carriers. J.D. Power ranked Delta first in customer satisfaction among premium airlines six consecutive years. Fortune named Delta the World's Most Admired Airline from 2014-2019. These weren't participation trophies but validation that premium positioning worked.

Yet challenges persisted. Basic Economy—introduced in 2012 to compete with ultra-low-cost carriers—contradicted premium positioning. Customers buying cheapest fares encountered restrictive policies: no seat selection, no changes, no overhead bin access. The product segmentation was necessary for revenue management but created brand confusion. How could Delta be premium while selling commodity products?

Labor relations grew tense despite profit sharing. Pilots, seeing record profits, demanded industry-leading wages beyond profit sharing. The 2016 contract negotiations nearly triggered strikes before agreement on 30% raises over four years. Flight attendants, still non-union, complained about scheduling practices and rest requirements. The family culture Woolman created was straining under institutional investor pressure for returns.

Technology investments had mixed results. The $75 million Fly Delta app became industry's best, enabling everything from seat upgrades to bag tracking. But the 2016 system outage—caused by a single piece of failed equipment—grounded 2,000 flights and cost $150 million. The 2024 CrowdStrike incident would prove even more damaging, demonstrating technology dependencies.

Anderson retired fully on October 11, 2016, leaving Bastian to navigate alone. His farewell letter to employees was characteristically direct: "We proved airlines don't have to be terrible. We showed that treating employees and customers well generates superior returns. Don't let anyone convince you otherwise."

Under Bastian's solo leadership, the premium strategy accelerated. American Express partnership expanded, offering exclusive lounges for Centurion cardholders. Partnerships with Wheels Up (private aviation) and Lyft (ground transportation) created door-to-door premium experiences. The 2019 launch of Delta Premium Select—a new cabin between economy and business—captured price-sensitive premium demand.

By decade's end, the transformation was complete. Revenue per available seat mile reached 17.5 cents, 40% premium to low-cost carriers. Operating margin hit 15.3% in 2019, the highest among network carriers globally. Market capitalization exceeded $40 billion, recovering the entire bankruptcy loss and more. The stock price increased 500% from 2010-2019, outperforming the S&P 500 by 300%.

The Anderson-Bastian era proved a fundamental business truth: in commoditized industries, differentiation through service and reliability creates sustainable competitive advantage. While competitors raced to bottom on price, Delta raced to top on experience. The strategy required massive investment, cultural transformation, and operational excellence. But it worked, generating $20 billion in profits from 2010-2019 while paying employees $10 billion in profit sharing.

As Bastian told investors in 2019: "We're not really an airline anymore. We're a premium service company that happens to fly planes. Once you understand that distinction, everything else makes sense."

IX. Modern Challenges & Strategic Positioning (2020s–Present)

March 12, 2020, 2:30 PM: Ed Bastian gathered his leadership team in Delta's Atlanta boardroom. The WHO had just declared COVID-19 a pandemic. That morning, Delta's booking system had reversed—cancellations exceeded new reservations for the first time in history. "Gentlemen and ladies," Bastian began, "we're about to face something worse than 9/11, worse than 2008, maybe worse than anything in aviation history."

Within two weeks, passenger traffic fell 95%. Delta parked 650 aircraft—70% of the fleet—in Arizona deserts and rural airports. The sight of hundreds of jets lined up at Victorville, California became dystopian symbol of aviation's collapse. Daily cash burn reached $100 million. At that rate, Delta's $16 billion liquidity would last 160 days.

The initial response mixed desperation with innovation. Delta retrofitted passenger cabins for cargo, removing seats to carry medical supplies. The airline operated "ghost flights"—empty planes flying to maintain pilot certifications and airport slots. Employees volunteered for unpaid leave in extraordinary numbers—35,000 within a month. The culture Woolman built—employees sacrificing for company survival—manifested again.

Government intervention through the CARES Act provided lifeline. Delta received $5.4 billion in grants and loans, conditional on maintaining employment through September 2020. Bastian's negotiation with Treasury was masterful—while competitors gave government equity stakes, Delta structured most support as loans, avoiding dilution. The decision would save shareholders billions when airlines recovered.

But survival required more than government money. Delta retired entire fleets overnight—the MD-88, MD-90, 777, and older 767s vanished. The 30% capacity reduction was permanent; these planes would never fly again. Maintenance facilities closed. Training centers shuttered. The Minneapolis hub—Northwest's former fortress—saw 40% service reduction. Detroit lost 35% of flights.

The human cost was devastating. Despite CARES Act protections, Delta implemented voluntary severance for 17,000 employees—20% of workforce. Pilots earning $300,000 annually took early retirement with partial pensions. Veterans with 40 years service departed quietly. The "Delta family" was fracturing under economic necessity.

Yet crisis sparked innovation. Delta created "parallel pandemic products." Middle seats were blocked through April 2021—longer than any competitor—sacrificing revenue for passenger confidence. HEPA filtration systems were upgraded to hospital-grade standards. Electrostatic cleaning protocols using quaternary ammonium compounds became standard. The "Delta CareStandard" certification required 300 safety measures, from masked gate agents to contactless boarding.

Recovery began tentatively in March 2021 as vaccines rolled out. But the traffic pattern had transformed. Business travel—formerly 50% of revenue but 70% of profit—remained depressed. Zoom replaced flights for routine meetings. Corporate travel policies restricted international trips. McKinsey estimated business travel would permanently remain 20% below 2019 levels.

Leisure travel, however, exploded. "Revenge travel"—consumers making up for lost time—drove unprecedented demand to beach and mountain destinations. Delta's summer 2021 load factors exceeded 90% on Florida routes. But leisure passengers paid less, expected less, and complained more. The premium strategy faced existential challenge: what if premium demand never returned?

Bastian doubled down on premium positioning. In 2023, Delta announced free Wi-Fi on all flights—a $1 billion annual investment. The logic: business travelers value connectivity above everything. If Delta offered superior internet, corporate contracts would follow. Early results were promising—T-Mobile signed a $500 million contract citing Wi-Fi as deciding factor.

The February 14, 2024, profit-sharing payment shattered records: $1.4 billion distributed to 100,000 employees. The average payment exceeded $14,000—two months' salary for many workers. Critics called it excessive when Delta could have reported higher earnings. Bastian's response was pointed: "Our employees saved this airline during COVID. They deserve every penny."

But operational challenges mounted. The July 2024 CrowdStrike incident exposed technological vulnerabilities. A faulty software update crashed Windows systems globally, but Delta suffered disproportionately. While other airlines recovered within days, Delta cancelled 5,000 flights over five days, stranding 500,000 passengers. The meltdown cost $500 million and triggered DOT investigation for passenger rights violations.

The root cause was technical debt. Delta's crew scheduling system—inherited from Northwest and running on 1990s code—couldn't handle massive disruption. When crews timed out or were displaced, manual intervention was required. But the staff trained on legacy systems had retired during COVID. Young employees couldn't operate antiquated interfaces. The same technology that enabled operational excellence became Achilles' heel during crisis.

Competition intensified from unexpected directions. United, under CEO Scott Kirby, aggressively pursued premium travelers with Polaris business class and expanded international network. American strengthened its Charlotte and Dallas hubs while building partnership with JetBlue for Northeast feed. Southwest abandoned its point-to-point model for quasi-hub system, competing directly in Atlanta. Even ultra-low-cost carriers like Frontier added premium seats, blurring market segmentation.

Labor relations reached inflection point in 2024. Pilots, seeing record profits, demanded 40% raises over four years. Flight attendants, still non-union at Delta alone among major carriers, threatened organization drives. Ground workers compared their wages to Amazon warehouse workers earning similar amounts with less stress. The profit-sharing that once bought loyalty now seemed insufficient against inflation and cost-of-living increases.

Sustainability pressures mounted. Corporate clients demanded net-zero commitments. European regulations threatened taxes on carbon emissions. Delta's 2050 net-zero pledge required $1 billion annual investment in sustainable aviation fuel, electric ground equipment, and carbon offsets. But sustainable fuel cost triple conventional jet fuel. Electric aircraft remained decades from commercial viability. The math didn't work without massive ticket price increases.

Fleet modernization accelerated despite challenges. Delta operated the world's largest fleet of Airbus A220s—efficient narrow-bodies perfect for thin routes. The airline ordered 100 Boeing 737 MAX 10s, ending decade-long exclusive Airbus narrow-body relationship. Wide-body replacement remained contentious—the Airbus A350 offered efficiency while Boeing's 787 provided commonality. Split orders increased training costs but reduced manufacturer dependency.

The network strategy evolved toward "coastal gateways." While Atlanta remained the mega-hub, Delta built Los Angeles into a Pacific gateway, New York for transatlantic, and Boston for Europe/Africa. Seattle became focus city for Asia despite Alaska Airlines' hometown advantage. The multi-hub strategy provided resilience—weather or disruption at one hub didn't cripple the network.

Partnership expansion continued through equity investments. The 2024 announcement of 20% stake in LATAM for $1.9 billion secured South American dominance. Joint ventures with Air France-KLM, Virgin Atlantic, and Korean Air created metal-neutral partnerships—sharing revenue regardless of operating carrier. These deep partnerships provided network breadth no single airline could achieve.

Digital transformation accelerated under Bastian's leadership. The Fly Delta app processed 3 billion API calls monthly—more than most tech companies. Predictive rebooking using machine learning moved disrupted passengers before they knew problems existed. Baggage tracking with RFID tags achieved 99.9% accuracy. Digital channels generated 65% of revenue, reducing distribution costs.

As 2024 ended, Delta's position seemed paradoxical. Financial metrics were stellar—operating margins exceeded 12%, revenue reached $60 billion, and the stock hit all-time highs. But structural challenges loomed: business travel's incomplete recovery, labor cost pressures, technology infrastructure needs, and sustainability requirements.

Bastian framed the challenge in stark terms at the 2024 investor day: "The easy growth is over. Population growth is slowing. Business travel has structurally changed. Climate regulations will increase costs. We're entering an era where excellence isn't enough—we need to reimagine what an airline can be."

That reimagination was beginning. Delta Tech Hub in Atlanta employed 2,000 software engineers. The airline was developing autonomous baggage systems, biometric boarding, and predictive maintenance AI. Partnerships with Joby Aviation for electric vertical takeoff aircraft suggested future where Delta operated door-to-door transportation, not just airport-to-airport flights.

The modern challenges facing Delta were unlike any in its century-long history. Not financial crisis or competition, but fundamental questions about aviation's role in a climate-conscious, digitally connected world. The crop duster that became a global carrier now had to become something else—perhaps a mobility company, perhaps a hospitality brand, perhaps something not yet imagined.

X. Playbook: Business & Investing Lessons

The transformation from crop-dusting operation to $60 billion global carrier offers timeless lessons about building enduring businesses. Delta's century-long journey demonstrates that sustainable competitive advantage comes not from any single factor but from compounding advantages that reinforce each other over decades.

The Power of Culture as Strategy

C.E. Woolman's greatest insight wasn't about airplanes or routes—it was that culture precedes strategy. The "Delta family" concept, born in 1920s Louisiana, created competitive advantage no spreadsheet could capture. When Northwest employees joined Delta in 2008, they were stunned that gate agents would stay late voluntarily to ensure on-time departure. This wasn't policy but culture—thousands of micro-decisions daily that compounded into operational excellence.

Culture manifests in metrics. Delta's employee turnover runs 5% annually versus 10-15% at competitors. Lower turnover means experienced employees who handle disruptions better. Experience means fewer mistakes, faster problem resolution, and institutional knowledge that can't be replaced. The math is compelling: reducing turnover from 15% to 5% saves approximately $400 million annually in training costs alone.

But culture requires constant investment. The $1.4 billion profit-sharing distribution in 2024 seemed excessive to Wall Street. Yet it generated loyalty that prevented unionization of flight attendants—saving billions in work rule restrictions. It motivated employees to achieve 85% on-time performance when industry average was 78%. That 7-point difference drove corporate contract wins worth $2 billion annually. The ROI on culture investment exceeds any aircraft purchase.

Hub Economics and Network Effects at Scale

Atlanta's dominance demonstrates network effects in physical form. With 1,000 daily departures, Delta can offer nonstop service to 200 destinations. A passenger from Birmingham can reach 150 cities with one stop. No competitor can match this connectivity from Birmingham. This creates pricing power—Birmingham passengers pay 20% premiums for Delta's superior network.

The mathematics of hub economics are counterintuitive. Adding the 1,000th daily flight from Atlanta costs marginally little—gates, staff, and facilities already exist. But that flight might connect ten spoke cities to ten others, creating 100 new city pairs. Each new connection makes every existing route more valuable. This is why dismantling hubs rarely works—remove 10% of flights and connectivity drops 30%.

Delta learned this lesson repeatedly. When they reduced Cincinnati hub post-bankruptcy, connecting traffic evaporated faster than capacity reduction. The hub generated $200 million in annual profits at peak but lost money immediately when downsized. The lesson: hubs exhibit step-function economics. They're either large enough to generate network effects or they're worthless.

Acquisition Integration Excellence

Delta executed seven major mergers, absorbing different cultures, fleets, and systems while maintaining operations. The playbook evolved but core principles remained:

First, protect revenue during integration. Every past airline merger saw customers defect during chaos. Delta maintained separate reservation systems until integration was flawless. Customer-facing changes happened last, not first. Revenue protection justified slower integration timelines.

Second, achieve labor peace regardless of cost. The Northwest pilot integration cost $1 billion in higher wages but prevented strikes that killed Eastern Airlines. Labor disruption during merger integration is fatal—customers never return. Overpaying for labor peace generates positive returns through retained revenue.

Third, cherry-pick best practices regardless of source. Delta adopted Northwest's analytical rigor in revenue management while Northwest absorbed Delta's customer service standards. Ego-driven "conqueror" mentality destroys value. The combined entity must be superior to either predecessor.

Fourth, move decisively on facilities and fleets. Maintaining duplicate facilities bleeds cash. Delta closed Northwest's Memphis hub within two years, eliminating $300 million in annual costs. The 777 fleet retirement was executed overnight. Gradual optimization extends losses.

The Premium Pivot: Moving Upmarket While Competitors Race to Bottom

Anderson's 2011 decision to pursue premium positioning seemed irrational. Low-cost carriers were growing rapidly. Consumers appeared increasingly price-sensitive. Yet Anderson understood a fundamental truth: in commodity markets, someone must be premium provider, and premium providers capture disproportionate profits.

The math is instructive. Spirit Airlines fills 85% of seats at $80 average fare, generating $68 per seat. Delta fills 82% of seats at $180 average fare, generating $148 per seat. The 3-point load factor sacrifice generates 118% revenue premium. But the real advantage is cost structure. Premium passengers check bags (high-margin ancillary revenue), buy food and drinks (60% margins), and generate loyalty program revenue (pure profit).

Premium positioning requires systematic commitment. Every touchpoint must reinforce positioning—lounges, seats, food, service, reliability. Delta spent $12 billion on product improvements from 2010-2020. Competitors who tried selective premium investments failed. American's Flagship product competed with Delta One but poor operational reliability undermined premium pricing. You cannot be selectively premium.

Operational Excellence as Competitive Advantage

Operational metrics seem boring but drive everything. Delta's 85.7% on-time performance versus industry average of 79.6% appears marginal. But that 6-point difference means:

- Corporate travelers make meetings, driving contract renewals

- Crews remain in position, preventing cascade disruptions

- Aircraft utilization increases, improving capital efficiency

- Customer satisfaction scores rise, reducing complaint handling costs

- Employee morale improves, reducing turnover

Operational excellence compounds. On-time departure enables on-time arrival enables quick turn enables next on-time departure. One delayed flight can cascade into dozens of disruptions. Conversely, consistent operations create virtuous cycles where everything runs smoothly.

Delta's Operations Control Center investment—$45 million for 40,000 square feet of monitoring capabilities—seemed excessive. But preventing single day's disruption saves $20 million. The facility pays for itself by avoiding two meltdowns annually. This is why operational investment generates returns that financial engineering cannot match.

Capital Allocation: When to Buy Distressed Assets

Delta's acquisition history reveals pattern recognition in distressed asset purchases: - Pan Am (1991): Paid $1.39 billion for routes worth $3 billion to replacement cost - Northwest (2008): Acquired during financial crisis when valuations were crushed - LATAM stake (2019): Bought during Latin American recession

The pattern: acquire strategic assets during sector distress when sellers lack alternatives and financing is scarce. But distressed acquisitions require operational capability to fix broken assets. Delta could integrate Pan Am's routes because they had Atlanta hub infrastructure. They could merge with Northwest because they had just completed bankruptcy restructuring.

The counter-pattern is equally instructive. Delta avoided acquiring assets during boom times. They passed on Virgin America when Alaska paid premium valuation. They avoided bidding wars for American during its bankruptcy. Patient capital allocation—waiting for distressed opportunities—generates superior returns to empire building.

Managing Through Crisis: Multiple Bankruptcies, Emerging Stronger

Delta survived industry crises that killed competitors: 1930s Depression, 1970s oil crisis, 2001 terrorism, 2005 bankruptcy, 2008 financial crisis, 2020 pandemic. The survival playbook remains consistent:

Preserve cash immediately. Delta grounded aircraft within days of COVID outbreak, before government mandates. They negotiated payment deferrals with suppliers before liquidity crisis. Moving first preserved options.

Communicate transparently with stakeholders. During bankruptcy, Grinstein held weekly calls with creditors. During COVID, Bastian sent daily videos to employees. Uncertainty breeds panic. Information creates confidence.

Restructure permanently, not temporarily. Delta retired entire fleets during COVID rather than parking temporarily. They eliminated structural costs rather than implementing hiring freezes. Permanent restructuring prevents zombie recovery where costs return faster than revenue.

Align stakeholder interests through shared sacrifice and reward. Executives took pay cuts before frontline employees. But they also shared recovery through profit-sharing. This alignment prevented adversarial dynamics that destroy companies during crisis.

Most importantly, use crisis to accelerate strategic changes. Bankruptcy enabled Delta to reject unfavorable aircraft leases. COVID justified retiring old fleets. Crisis creates burning platform for changes impossible during normal times.

The Compound Effect of Continuous Improvement

Delta's story isn't about single transformative decisions but thousands of incremental improvements compounding over decades. Reducing turn time by 5 minutes enables additional daily flight. Improving bag handling by 0.5% reduces complaint costs. Increasing load factor by 1 point generates $500 million annually. These improvements seem marginal individually but compound into insurmountable advantages.

This requires cultural commitment to excellence that transcends leadership changes. Woolman established the standard. Every subsequent CEO—through different strategies and crises—maintained operational obsession. This consistency allowed improvements to compound rather than reset with each leadership transition.

The investor lesson is profound: sustainable competitive advantage doesn't come from brilliant strategy but from executing basics better than competitors consistently over time. Delta flies the same planes to the same places as competitors. But they do it on time, with intact luggage, and pleasant service. That operational edge, compounded over decades, created $40 billion in market value.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Structural Advantages Compound

Delta's operational supremacy creates a self-reinforcing cycle that competitors cannot break. The airline achieves 85.7% on-time performance, 7 points above industry average. This reliability attracts corporate contracts that pay 15-20% fare premiums. Premium revenue funds operational investments that further improve reliability. The cycle accelerates with each iteration.

The Atlanta fortress hub is essentially unassailable. Delta controls 75% of gates through long-term leases extending to 2057. Building competing hub would require $5 billion in infrastructure investment. Even if a competitor made that investment, they would face Delta's 1,000 daily flights providing superior connectivity. No rational competitor would attempt frontal assault on Atlanta. This monopolistic position generates $3 billion in annual profits that fund competition elsewhere.

The balance sheet strength provides strategic flexibility competitors lack. With $18 billion in liquidity and investment-grade credit rating (unique among U.S. airlines), Delta can weather downturns without distressed asset sales. During the next crisis, Delta will be buyer, not seller. This patient capital allocation creates option value—the ability to make strategic moves when opportunities arise.

Network effects from successful merger integration cannot be replicated. The Northwest merger created Pacific network that would take decades to build organically. Tokyo hub rights from post-WWII occupation cannot be obtained at any price. The Virgin Atlantic stake provides Heathrow access that's literally priceless—slots haven't traded in decade. These structural advantages compound daily as network connectivity drives revenue premiums.

The brand transformation to premium positioning is nearly complete. Net Promoter Scores exceed 40, highest among U.S. carriers. Corporate travel managers explicitly prefer Delta for C-suite travel. This brand equity took decade to build and would take decade to destroy. Even if Delta's service temporarily declined, brand persistence would maintain premium pricing for years.

Employee culture, though strained, remains superior. The 5% turnover rate versus 10-15% at competitors means Delta's workforce is more experienced. Experience drives operational excellence—senior mechanics diagnose problems faster, veteran gate agents handle disruptions better. This human capital advantage is unquantifiable but real.

Technology infrastructure investments are bearing fruit. The Fly Delta app processes more transactions than most e-commerce platforms. Predictive maintenance reduces mechanical delays 30%. Baggage tracking achieves 99.9% accuracy. These capabilities took decade and billions to build. Competitors starting now are permanently behind.

Bear Case: The Structural Headwinds Accumulate